Relative Bound and Asymptotic Comparison of Expectile with Respect to Expected Shortfall

Samuel Drapeau

School of Mathematical Sciences & Shanghai Advanced Institute for Finance (CAFR)

Shanghai Jiao Tong University, Shanghai, China

sdrapeau@saif.sjtu.edu.cnhttp://www.samuel-drapeau.info and Mekonnen Tadese

School of Mathematical Sciences

Shanghai Jiao Tong University, Shanghai, China

mekonnenta@sjtu.edu.cn

(Date: March 7, 2024)

Abstract.

Expectile bears some interesting properties in comparison to the industry wide expected shortfall in terms of assessment of tail risk.

We study the relationship between expectile and expected shortfall using duality results and the link to optimized certainty equivalent.

Lower and upper bounds of expectile are derived in terms of expected shortfall as well as a characterization of expectile in terms of expected shortfall.

Further, we study the asymptotic behavior of expectile with respect to expected shortfall as the confidence level goes to in terms of extreme value distributions.

We use concentration inequalities to illustrate that the estimation of value at risk requires larger sample size than expected shortfall and expectile for heavy tail distributions when is close to .

Illustrating the formulation of expectile in terms of expected shortfall, we also provide explicit or semi-explicit expressions of expectile and some simulation results for some classical distributions.

Keywords: Expectile; Expected Shortfall; Value at Risk; Extreme Value; Risk Measure.

National Science Foundation of China, Grants Numbers: 11971310 and 11671257; Grant “Assessment of Risk and Uncertainty in Finance” number AF0710020 from Shanghai Jiao Tong University; are gratefully acknowledged.

Both authors thanks Stéphane Crépey and Hans Föllmer for fruitful discussions.

1. Introduction

The expectile is a generalization of quantile introduced by Newey and Powell [34].

It is defined as the argmin of a quadratic loss

For , the expectile is a coherent risk measure that corresponds to Föllmer and Schied [17]’s shortfall risk with loss function .

Widely used in insurance and statistics, it has recently gained some interest in finance as it bears some interesting features for the assessment of tail risk in comparison to the industry wide expected shortfall risk measure introduced by Artzner et al. [3].

From its definition, expectile is elicitable, which is a useful property in terms of backtesting, see Gneiting [21], Bellini and Bignozzi [6], Emmer et al. [16], Ziegel [41], and Chen [11] for a discussion about the financial relevance.

In the seminal paper Weber [40], and later Bellini and Bignozzi [6], Ziegel [41], Delbaen et al. [15], it actually turns out that expectile is the only elicitable risk measure within the class of coherent and law invariant risk measures.

Expectile is also invariant under randomization, while expected shortfall is not, see Weber [40] and Guo and Xu [22].

The property of invariance under randomization is closely related to the convexity of the acceptance set and rejection set of a risk measure, when risk is defined on the space of distributions.

That is, for expectile if both and are acceptable, then the randomized position with probability and with probability with in is also acceptable, see [40] for the detail.

Finally, multivariate shortfall risk – expectile being an example of which – seems to be suitable in terms of systemic risk management and risk allocation, see Armenti et al. [2].

Due to these appealing properties, several authors suggest expectile as an alternative to expected shortfall and value at risk, see [16, 8, 7, 6, 11] for instance.

The goal of this paper is to study the relationship between expectile and expected shortfall.

More specifically, the objective is to provide lower and upper bounds of expectile in terms of expected shortfall, formulate explicitly expectile and its Euler allocation as a function of expected shortfall, and compare the asymptotic behavior of expectile and its Euler allocation with respect to expected shortfall as the confidence level goes to .

As for the bounds, our approach is based on duality results and the link between expectile and expected shortfall through optimized certainty equivalent.

For loss profile with zero mean, our first result mainly focus on the bounds

(1.1)

As shown in Proposition 3.2, the optimal lower bound is in fact an equality

where .

For continuous distribution, the expression of is mentioned in Taylor [39, Equation 7] based on results by Newey and Powell [34].

We generalized this result to any distribution using optimized certainty equivalent.

As an application of this relation we can easily derive explicit or semi-explicit formulations of expectile for wide classes of distributions.

Let be loss profiles such that .

Under some smoothness assumptions, in the same sprits of the optimal lower bound, the Euler allocations of expectile can also be formulated as a function of the Euler allocation of expected shortfall given by

As for the upper bound, Delbaen [14] and Ziegel [41] provide a comonotone least upper bound of expectile in terms of concave distortion risk measure.

Using this result, we show that the upper bound given by Relation (1.1) is the smallest within the class of expected shortfalls dominating expectile.

According to these bounds, expected shortfall is more conservative than expectile.

We therefore, address their comparative asymptotic behavior as the confidence level goes to .

In actuarial literature, asymptotic analysis is a subject of intensive research as it helps risk managers to model large losses with small amounts of data and to establish asymptotic relationships between risk measures, see Hua and Joe [24].

While Hua and Joe [24], Tang and Yang [36] and Mao and Hu [30] establish asymptotic relationship between expected shortfall and value at risk, Bellini and Di Bernardino [7] and Mao et al. [32] provides asymptotic analysis of expectile in terms of value at risk when the loss profile belongs to the maximum domain of attraction of extreme value distributions.

There is in particular an asymptotic relationship between value at risk and expectile excerpting the tail index of the distribution belonging to the Frechet type for instance.

It is therefore possible to estimate the tail index of a distribution by comparing the empirical value of value at risk and expectile for large .

However, from an asymptotic point of view the estimation of value at risk may need large sample size as compared to expected shortfall and expectile for heavy tailed distributions.

From recent concentration inequality results from Fournier and Guillin [19] using Wasserstein distance, we provide estimations of the error for the empirical expected shortfall and empirical expectile as a function of the confidence level and their corresponding required sample size and .

For instance, in the case where the distribution has some moment , we obtain

for any where the constant and are independent of , and .

In particular, as showed in Proposition 4.2, for Fréchet type distributions with a moment , both and are of the order which are infinitesimal with respect to the corresponding for the quantile as goes to one.

Note that estimation for the empirical estimation of the expected shortfall and expectiles and more general risk measures has been the subject of recent studies, see Gao and Shaochen [20], Holzmann and Klar [23], Kolla et al. [27], and Bartl and Tangpi [5] for instance.

We use here the bounds in [19] to get the explicit dependence in terms of the confidence level which is new to our knowledge.

Using related results, when the loss profile belongs to the domain of attraction of either Weibull type , Gumbel type or Fréchet type , we establish asymptotic relationship between expectile and expected shortfall by providing both the first-order and second-order asymptotic expansion.

For a Fréchet type tail distribution with , asymptotically the ratio of expectile to expected shortfall become strictly less than .

In this case, it actually hold

This result also show that the upper bound provided by Relation (1.1) is not asymptotically equivalent to in general.

It also allows an estimation of tail index based on empirical data.

We also consider the asymptotic behavior of the parameter .

For loss profiles whose distribution belongs to Fréchet type with , Bellini et al. [8] provide the asymptotic behavior of in terms of .

For Weibull type and Gumbel type , we show that .

For Fréchet case, we also provide a second-order asymptotic expansion for .

The paper is organized as follows.

In Section 2, aside definitions and notations, we revisit the link between expectile and expected shortfall through optimized certainty equivalent.

In Section 3, we address the lower and upper bounds of expectile in terms of expected shortfall as well as characterize expectile and its Euler allocations in terms of expected shortfall.

Section 4 focuses on asymptotic behavior of expectile in terms of expected shortfall according to the maximum domain of attractions of extreme value distributions to which the loss profile belongs.

Section 5 illustrate the results of Section 3 in terms of explicit or semi-explicit expression of expectile for commonly known distributions.

It also provide an illustrations for some of the asymptotic results of Section 4.

2. Expectile Versus Expected Shortfall through Optimized Certainty Equivalent

Let be a probability space and be the set of integrable random variables identified in the almost sure sense.

For and with , denote by

Throughout, elements of are generically denoted by and considered as a loss profile.

Given such an in , we denote by and its cumulative distribution and left-quantile function, respectively, that is

We also denote the right-quantile function of by , that is .

A function is called a risk measure if it is

(I)

quasi-convex: for every .

(II)

monotone: whenever almost surely.

A risk measure is further called monetary if it is additionally

(III)

cash-invariant: for every in .

Finally, a monetary risk measure is called coherent if it is additionally

(IV)

sub-additive: .

It is known that monetary risk measures are automatically convex, and, coherent monetary risk measures are positive-homogeneous111 for every ..

For in , we define

Value at Risk: for ,

Expected Shortfall: for ,

Expectile: for , the -expectile of is defined as a unique number solving

The value at risk is cash invariant, monotone and positive-homogeneous, it is however not sub-additive, see [3, 37].

The expected shortfall is a special case of an optimized certainty equivalent, while the expectile corresponds to the shortfall risk with loss function in the standard definition, [40, 41, 17].

Indeed, is increasing, convex whenever and such that whenever .

Hence, the expectile can be seen as a scaled version of an optimized certainty equivalent, see [9].

In the literature, see for instance [8, 34], expectile is also defined as

for in .

However, due to the first order condition this coincides with the present definition.

Let us recall the following known properties of expectile and expected shortfall.

Proposition 2.1.

The expectile and expected shortfall are law invariant monetary risk measures and it holds

with optimal density

where is a constant such that and

(2.1)

(2.2)

(2.3)

with optimal density

where is a parameterized family of distribution on .

These results can be found or derived from [9, 17, 3, 8].

Interestingly though, they are strongly connected through the optimized certainty equivalent from Ben-Tal and Teboulle [9].

For the sake of readability and further computation we expose briefly this connection.

Proposition 2.2.

For a loss function where and , the optimized certainty equivalent defined as

(2.4)

is a law invariant coherent risk measure such that

(2.5)

(2.6)

(2.7)

(2.8)

where .

Furthermore, for it holds

(2.9)

Proof.

Following [9], the optimal in definition (2.4) satisfies

Rearranging, we get showing that .

Plugging the optimizer into (2.4) yields (2.5).

From (2.5) to (2.6) comes from the fact that .

As for (2.7)

The Relation (2.6) implies that the optimized certainty equivalent is a law invariant and coherent risk measure.

The Relation (2.8) follows from the general robust representation of optimized certainty equivalent in terms of divergences, that is

see [9, Theorem 4.2], since the convex conjugate222 . if and otherwise.

As for the last Relation (2.9), it comes from the general relation between optimized certainty equivalent and shortfall risk [9, Section 5.2] where

The relations for the expected shortfall follows directly from Proposition 2.2 by noticing that for and .

As for the relations for the expectile, they follow from (2.9) as for and which fulfills the conditions of Proposition 2.2 as .

As for the optimal density for expected shortfall, see Föllmer and Schied [18], McNeil et al. [33] and for expectile it is given in [8, Proposition 8].

∎

Remark 2.3.

Relations (2.1)–(2.3) provide the link between expectile and expected shortfall.

One sees in particular, that while expected shortfall is comonotone, the expectile is not.

Indeed, Relation (2.2) is the Kusuoka representation which can not fulfill the assumptions of [18, Theorem 4.93, p. 260].

On the other hand, as showed in [40] while expectile is invariant under randomization, the expected shortfall is not.

3. Expectile as a Function of Expected Shortfall

Based on Relation (2.1) we provide bounds for the expectile in terms of expected shortfall in the spirit of [8, Proposition 9].

The upper bound is to our knowledge new, while the larger upper bound is given in [14].

The present proof uses the relation between optimized certainty equivalent and expectile.

Proposition 3.1.

Let be in with zero mean333

Due to translation invariance, in the case where , we get

.

Then for each , it holds

Proof.

Let be given.

On the one hand, from the proof of Propositions 2.1 and 2.2, for and .

It implies that and therefore from (2.7) it follows that for every .

Solving for yields the left hand inequality.

On the other hand, we have , showing together with that .

Since and , as a result of (2.7) the right hand side inequalities also hold.

∎

If we set , the lower bound corresponds to the one stated in [8, Proposition 9], that is

(3.1)

As for the lower bound, from (2.1), it is immediate that there exists satisfying the equality in the above proposition.

When is continuous, from [39, Equation ] we get an optimal .

We generalized this result for any distribution and formulate expectile as a convex combination of expected shortfalls.

Proposition 3.2.

Let be in not identically constant,444If is identically constant, then is any number in . it holds that

where .

Proof.

First, let us show that if is not identically constant, then every in is strictly between and .

Since and , it hold that .

If , then and hence .

The first order condition can be written as

(3.2)

It follows that which contradict the fact that .

Hence, must be in .

By the definition of , it holds that is in .

As a result of [1, Proposition 4.2], it holds that

From the proof of Proposition 3.2, it is easy to see that the inequality (3.1) become equality, that is, the optimal if and only if is the -quantile.

When is strictly increasing and continuous, it holds that .

Hence, in this special case if and only if the expectile is a value at risk at confidence level .

This is the case for instance when , see Koenker [26].

Remark 3.3.

If is strictly increasing and continuous, then uniquely solves

(3.3)

Let be in such that .

For any risk measure , the Euler risk contribution of position to the risk capital is defined as

(3.4)

provided that the limit exist for each .

It is well known, see for instance [25, 38], that if , then

provided that the limit defined in (3.4) exists.

Similarly, for the case where such that the limit defined in (3.4) exist, according to [16] we also get

Hence, in the same sprit of Proposition 3.2, the Euler risk contributions of position to the expectile risk capital can also be formulated as a function of its Euler risk contribution to the expected shortfall risk capital.

Proposition 3.4.

Let be in such that the limit defined in (3.4) exist for both and , where .

Then the Euler risk contribution of position to the risk capital is given by

We now turn to the question of the upper bound.

If is non-atomic, from [14] and [41], we get an other upper bound of expectile

which is a distortion function corresponding to the concave distortion function , given by .

Furthermore, is the least one from the class of law-invariant coherent and comonotonic risk measure dominating .

It also holds that for each .

Since the upper bound given in Proposition 3.1 is also coherent and comonotone, it follows in particular that

However, the upper bound is the least one within the class of expected shortfall in the sense stated in the following proposition.

Proposition 3.5.

Suppose be non-atomic. Then

is the smallest risk measure of the form with , and uniformly dominating for in .

Proof.

Note that

for the concave distortion function

which is continuous and strictly increasing with and .

For , and , we have

On the one hand, let for some in .

Since is non-atomic, there exist such that .

Following [18] and [35], we get and therefore can not dominate .

Hence, for every , and , we have dominate only if .

On the other hand, for every , and such that , it holds

In this case, .

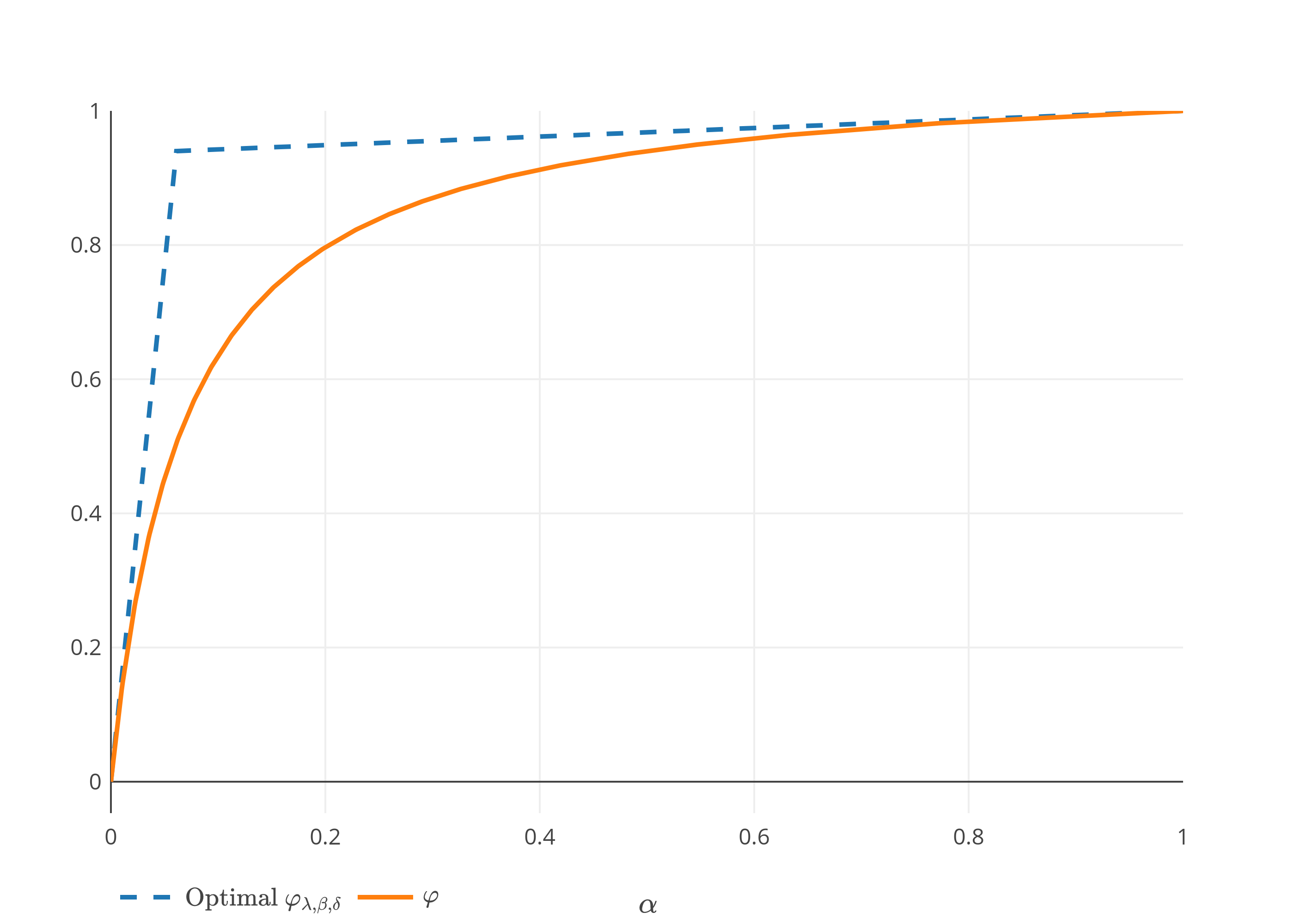

Indeed, since is tangent to at the point and , and is strictly concave, for some in implies there exist in such that for some in , see Figure 1.

By a similar argument, it follows that can not dominate .

Therefore, is the better one when , and .

∎

Figure 1. Graph of and optimal for .

Remark 3.6.

If contains atoms, Proposition 3.5 may not be true in general.

For instance, when with , , and , we get ,

Every in is of the form for some and in .

Without loss of generality, assume , a simple computation yields

and .

This implies that dominates , but it is dominated by .

Hence, is not the least one.

4. Expectile Versus Expected Shortfall: Asymptotic Comparison

Throughout this section, we consider a loss profile with zero mean and for ease of notation its cumulative distribution is denoted by .

For ease of notations, we also use

Given , independent copies of , we denote by the empirical cumulative distribution function of the empirical measure .

Correspondingly, we use the notations , and for the value at risk, expected shortfall and expectile of the empirical measure, respectively.

We also use the standard notation and as goes to which means that and , respectively.

For we may equivalently write .

For a given risk level , expectile and value at risk are less conservative than expected shortfall, that is, and .

Expectile can be less or more conservative than value at risk depending on the considered loss profile, see [7].

When is in the maximum domain of attraction of an extreme value distribution function, [7] and [32] give asymptotic comparison between value at risk and expectile.

For Fréchet type with , from [7] we have the relation

(4.1)

Using this asymptotic result, [12] introduces the extreme expectile estimator

where is the Hill estimator of .

Relation (4.1) also allows for instance to provide estimation of tail index using the ratio of empirical expectile to empirical value at risk for large values of .

However, when looking at the tails, extreme quantile estimation may needs extremely very large sample size compared to expected shortfall and expectile in the case of heavy tail distributions as close to .

This fact is explained in Proposition 4.1 and 4.2 below and this motivates the study of asymptotic comparison of expectile with respect to expected shortfall instead of value at risk.

Therefore, in this section we are comparing the number of sample size required for the estimation of extreme quantile with respect to expected shortfall and expectile when the sample is taken from distribution that belongs to a Fréchet type .

We also consider the asymptotic behavior of expectile with respect to expected shortfall and the optimal when belongs to extreme value distributions as the confidence level goes to .

These propositions are based on concentration inequalities using Wasserstein distance.

Such an approach has recently been adopted by Bartl and Tangpi [5] to provide error bounds for classes of empirical risk measures.

In our context we focus however on the sensitivity with respect to the confidence level and make an approach which is slightly different using the results in Fournier and Guillin [19].

The asymptotic comparison uses techniques from extreme value theory.

We say is in the maximum domain of attraction of an extreme value distribution function , denoted by , if

for some constants and .

It is well known that extreme value distribution belongs to either one of the following three categories:

Weibull555 for . (), Gumbel 666 for . () or Fréchet777 for . (), where , see [33, 36, 30, 7] for more discussion in the present context.

Let for .

The condition that belongs to the maximum domain of attraction can be equivalently given by the extended regular variation of .

Recall that a measurable function is said to be of extended regular variation with parameter , denoted by , if there exist a function such that for each ,

It is known that is in the maximum domain of attractions of Fréchet type , with if and only if .

is in the maximum domain of attractions of Weibull type , with if and only if .

Finally, is in the maximum domain of attraction of Gumbel type if and only if , see [13, Theorem 1.1.6] for instance.

The Wasserstein distance between the probability measures with cumulative distributions and is defined as

We consider the following assumptions on :

(4.2)

(4.3)

(4.4)

where and .

A simple application of concentration results by Fournier and Guillin [19] yields the following concentration inequalities for expected shortfall and expectile.

Proposition 4.1.

Let be a random sample from such that either assumption (4.2), (4.3) or (4.4) holds.

If , for all and , it holds

and

where

where and are positive constant that depends only on , , , , and depending on the set of assumptions.

It follows that the sample sizes required for expected shortfall and expectile with a given precision and confidence is given by

respectively, where

Proof.

According to [19, Theorem ], for all and it holds888For the third case, it is possible to have . However the case where is not the best choice in terms of bounds.

(4.5)

Note that the constants and are positive and depends only on , , and for the case (4.2), on , and for the case (4.3) and on and for the case (4.4), see [19].

Let us treat the cases separately.

The Relations (4.6) -(4.8) yields the required concentration inequalities.

As for the sample size fix a confidence level such that for expected shortfall and for the expectile and solving for yields the required result.

∎

According to Proposition 4.1, for a given precision and confidence , it follows that and tends to .

Furthermore, under either of the assumptions (4.2), (4.3) or (4.4), it holds

However, this is not the case in general for value at risk versus expected shortfall and value at risk versus expectile.

For instance, suppose has a strictly positive and continuous density function on the interval for some .

According to [20, Corollary ] for every and in , it holds

where

It implies that sample size for a given precision in and confidence is given by

(4.9)

Hence, depends on the relative behavior of as goes to .

Assuming that the density become non-increasing for large enough values, we get .

When belongs to the Fréchet type , it holds that is in .

From [13, Proposition B.1.9], we get and this implies that

(4.10)

Hence, asymptotically for heavy tailed distributions, we may have and tends to faster than and as shown in the following proposition.

Proposition 4.2.

Suppose that belongs to a Fréchet type with and some moment .

Suppose further that the density function of is strictly positive and decreasing for large enough values.

Then, for every , and confidence level , as goes to it holds

Proof.

Since goes to as goes to , by assumption, is strictly positive and continuous on the interval .

A simple application of Proposition 4.1 and Relation (4.9) yields

for some constant .

As a result of Relation (4.10), goes to as goes to .

Likewise, as goes to .

∎

We now turn to the asymptotic behavior of the optimal and expectile with respect to expected shortfall.

A direct application of [8, 7, 30] yields

Proposition 4.3.

For in the maximum domain of attraction of Fréchet type with , as the confidence level goes to , we have that

Proof.

The relation between and is given in [8], and from [30] we have

Together with Relation (4.1) this yields the required result.

∎

Beyond this first order expansion, a second order one is useful to determine the rate of convergence.

In order to do so, we impose a second-order regular variation condition on .

A measurable function is said to be of regular variation with parameter , denoted by , if , for each .

A regularly varying function which is eventually positive is said to be of second-order regular variation with first-order parameter and second-order parameter , denoted by , if and there exists a measurable function which does not change sign eventually and converges to as goes to such that, for each

see, [13, 28] for further properties of regular variations.

The function is in , see [13, Theorem 2.3.3], and is called the auxiliary function for .

Proposition 4.4.

For in the maximum domain of attraction of Fréchet type such that with , and auxiliary function , as the confidence level goes to , it holds

where

Furthermore,

Proof.

Let be in with , and auxiliary function .

According to [31, Theorem 3.1], we get

where

The condition with auxiliary function is equivalent to is in with auxiliary function , see [13, Theorem 2.3.9].

Hence, by [30, Theorem 4.5], we get

It follows that

which gives the required result for .

As for the ratio of , from [31, Proof of Theorem 3.1], we have

From Relation (4.1), we have .

Since , a straightforward application of [13, Proposition B.1.10] yields showing that

The first order condition given by Relation (3.2) can also be written as

Combining the last two equations gives the required result for .

∎

Remark 4.5.

When , for , following [31], we get that is in with auxiliary function , where is the cumulative distribution of .

For a given confidence level , expectile is always less conservative than expected shortfall, that is, .

Proposition 4.3 implies that this inequality is more pronounced for Fréchet type when is close to .

For , it holds that .

For heavy tail index sufficiently close to 1, and are asymptotically equivalent.

According to [10] and [23], for a random sample from having a finite mean the empirical estimators and converges almost surely to and , respectively.

If is further a Fréchet type with , then almost surely

For the comparison of the empirical ratio with the theoretical ratio , we provide a simulation study for Pareto and Student distributions with different regularity tail index and sample size , see Example 5.3 and 5.4 for more discussion.

In the same sprit of Proposition 4.3, the Euler allocations of expectile can also be formulated as a function of expected shortfall in the sense of the following proposition.

Proposition 4.6.

Let be a non-negative loss profiles in with continuous distribution such that .

If the cumulative distribution of belongs to a Fréchet type with such that

Under the given assumption, [4] showed that is Fréchet type , as goes to and for some as goes to.

Together with Proposition 4.3, this yields

∎

We now turn to the asymptotic comparison between expectile and expected shortfall for in the domain of attraction of Weibull and Gumbel type.

For that belongs to Weibull type , it is known that .

A direct application of [30, 32] yields

Proposition 4.7.

Let .

For in the maximum domain of attraction of Weibull type , as goes to , it holds

Proof.

The first order condition given by Relation (3.2) can also be re-written as

Since asymptotically the first order condition becomes

which implies .

From [30, Theorem 3.4] and [32, Proposition 3.3] we have

which yields the desired asymptotic relationship between and .

∎

Since the Weibull type distributions have a finite right end point , both and converges to as goes to .

Proposition 4.7 implies that converges to very fast as compared to .

Under additional assumption on the distribution of , we also provide a second order expansion.

Proposition 4.8.

For in the maximum domain of attraction of Weibull type such that and with , and auxiliary function , as the confidence level goes to , it holds

where

Furthermore,

Proof.

Let be in with , and auxiliary function .

According to [30, Proposition 2.4], as goes to we have for some .

Hence, by [32, Proposition 3.3], it holds

(4.11)

In particular, for the same reason as in the proof of Proposition 4.4, it follows that

(4.12)

The regularity condition on implies that with auxiliary function asymptotically equivalent to as goes to , see [28].

Hence, using Relation (4.12), and [36, Theorem 4.5] gives

(4.13)

Using Relation (4.12) and [32, Relation 3.14 and 3.17], we also get that

(4.14)

Substituting the left hand side of Equation (4.14) with (4.11) and solving for gives

(4.15)

Computations using Relations (4.12)-(4.13) and (4.15) yields the required expression of .

As for , using the fact that goes to as goes to , [31, Relation 3.13] and the first order condition given by Relation (3.2) implies that

Combining these Relations together with Relation (4.11) yields the result.

∎

Remark 4.9.

When , the proof of Proposition 4.8 allow to derive the expression

where

A direct combination of results by [36, 30] and [7] yields

Proposition 4.10.

For in the domain of attraction of Gumbel type , as the confidence level goes to , it holds .

If further with and , then

Moreover, if

(4.16)

for some constant , then

Proof.

From [32, Proposition 3.6], we have .

For in , it is known that , see [36] for instance.

Therefore, .

As for the relationship between expectile and expected shortfall it is a direct consequence of [36, 30] and [7, Proposition 2.4].

∎

As an application of the asymptotic results, we compare and the upper bound

when belongs to the domain of attractions of extreme value distributions.

In general, this bound is asymptotically equivalent to .

For in the domain of attraction of Fréchet type with , it holds that as goes to .

In this particular case, the bound is not asymptotically equivalent to .

Every distribution in the Weibull type has finite end point .

This implies that both and converges to .

Hence, the bound become asymptotically equivalent to provided that .

For in the Gumbel type with finite end point or satisfying condition (4.16), the bound also becomes asymptotically equivalent to .

5. Examples and Simulations

For many common distributions explicit or semi-explicit expressions for both the quantile and expected shortfall are known.

Taking this advantage, in this section we illustrate the explicit or semi-explicit computations of expectile using the optimal and illustrating some of the results of Section 4 for Beta, exponential, Pareto and Student distributions.

While Beta distribution is a Weibull type , the exponential is Gumbel type .

The Pareto and Student distributions are Fréchet type with and , respectively.

We also include a simulation study for Pareto and Student distributions to compare the sample size required for empirical ratio and to converge the theoretical ratio and , respectively.

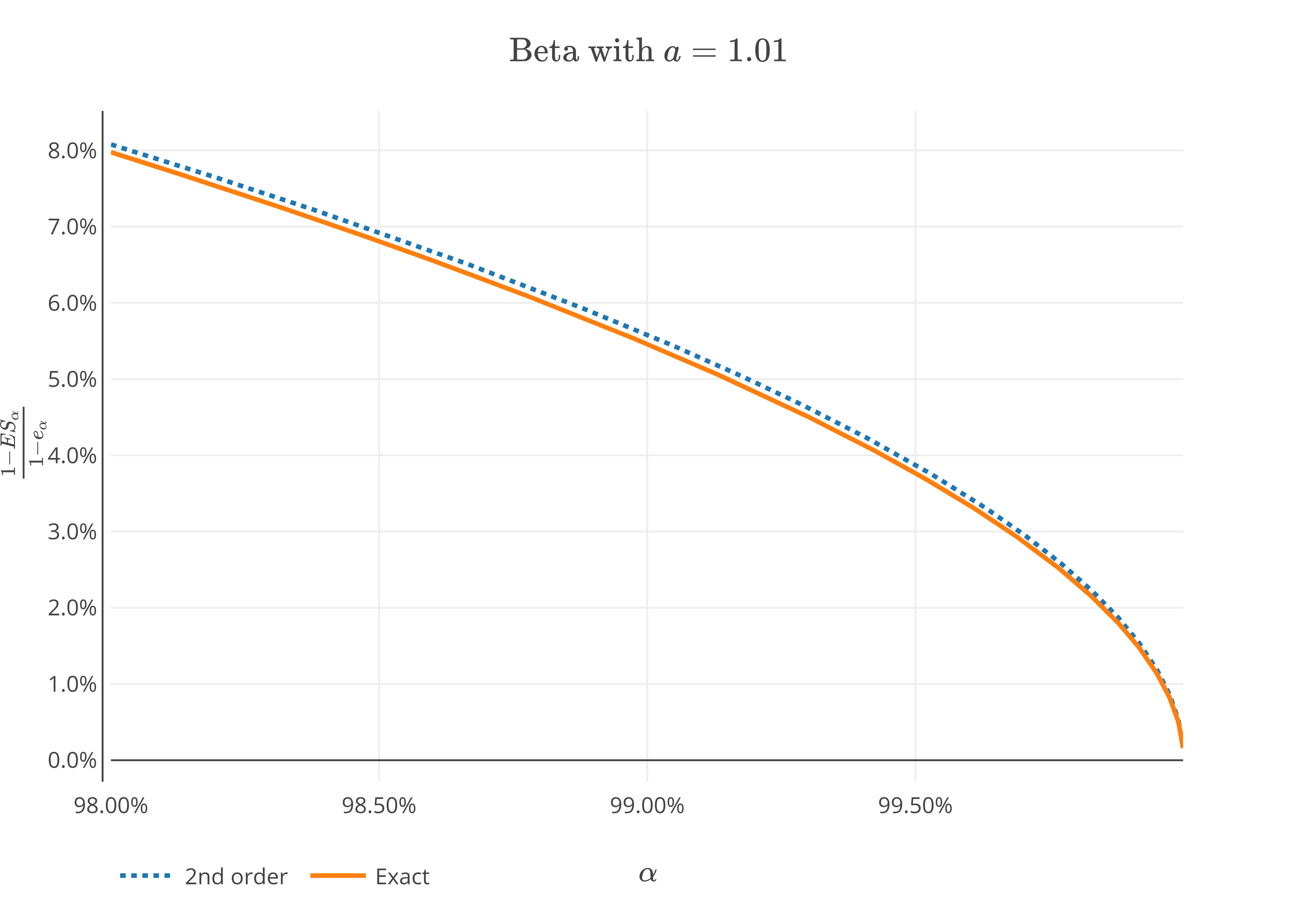

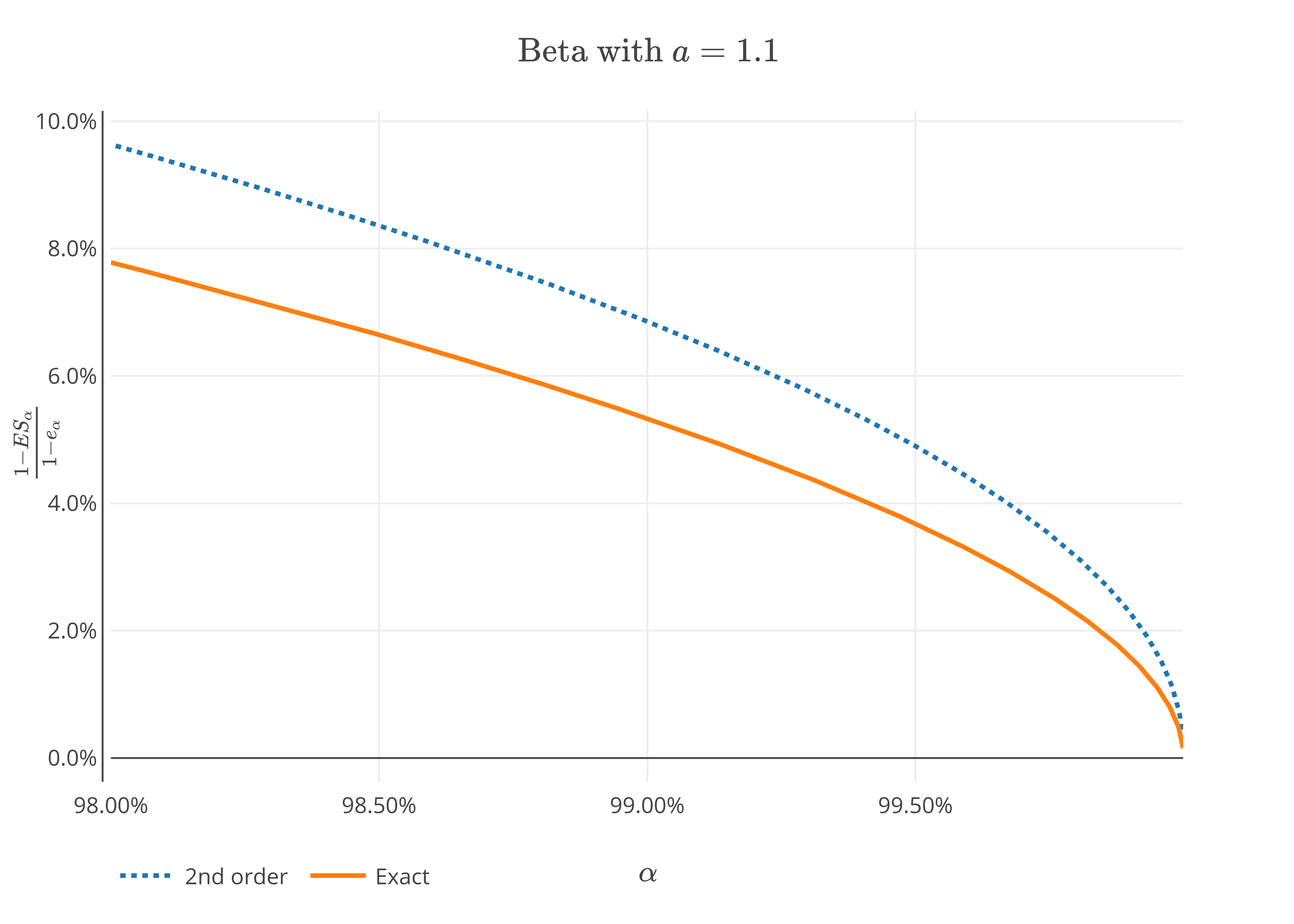

For , the Beta distribution coincides with the standard uniform distribution and it holds that

If , then with auxiliary function , see [30, 32] for instance.

By Remark 4.9, we have

Figure 2. Graph of the ratio for Beta distribution with and .

As goes to , the ratio goes to .

As shown in figure 2, the accuracy of the second order expansion for depends on the parameter .

As close to , the second order expansion become more accurate.

Example 5.2(Exponential).

Let for .

Then and .

The Relation (3.3) becomes .

For , it holds .

Thus, and

where, is Lambert function999 is a function such that if and only if ..

Therefore,

A similar expression for can also be found in [7].

It is also known that belongs to Gumbel type and satisfy condition (4.16).

Hence, .

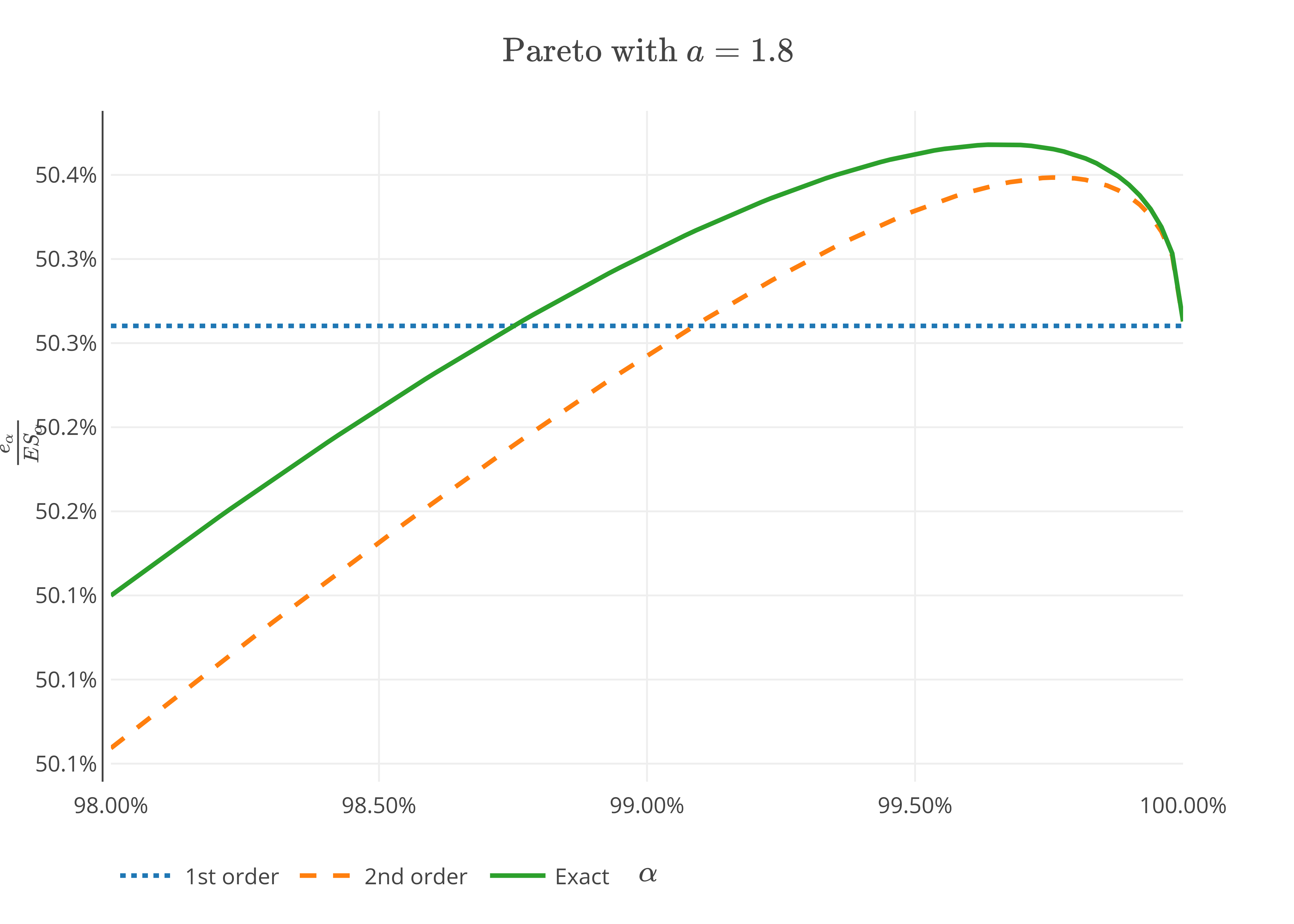

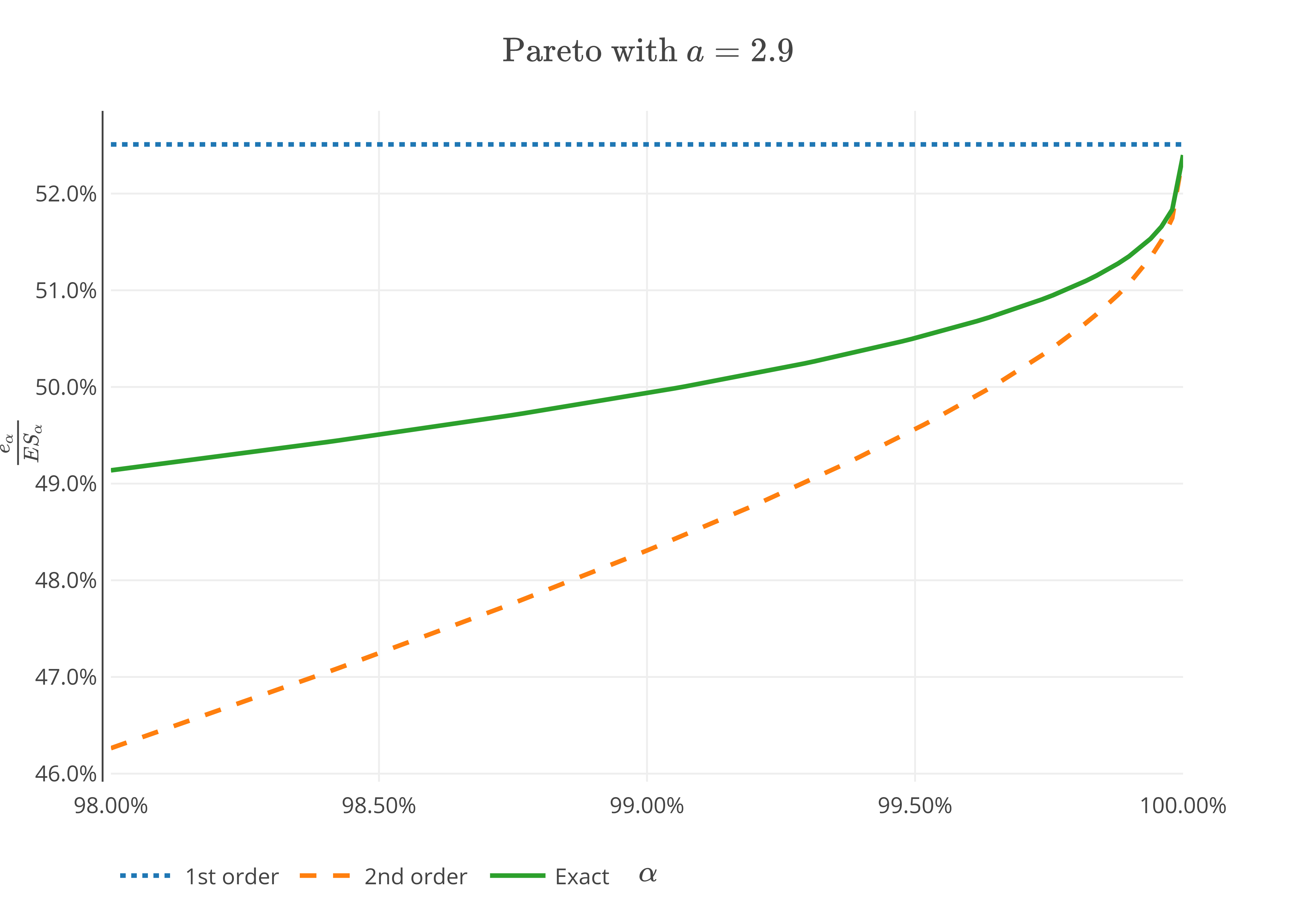

Example 5.3(Pareto).

For and , let .

It follows that , and .

Relation (3.3) gives the optimal solving

Hence,

In particular, for ,

It also holds that with auxiliary function , see [24, 32].

By Remark 4.5, for it follows that with auxiliary function .

Hence, by Proposition 4.4, it holds that

The cash-invariant property gives

Figure 3. Graph of for Pareto distribution for and .

The second order expansion is more accurate than the first order one.

The accuracy seems better when the tail become more heavier, see Figure 3.

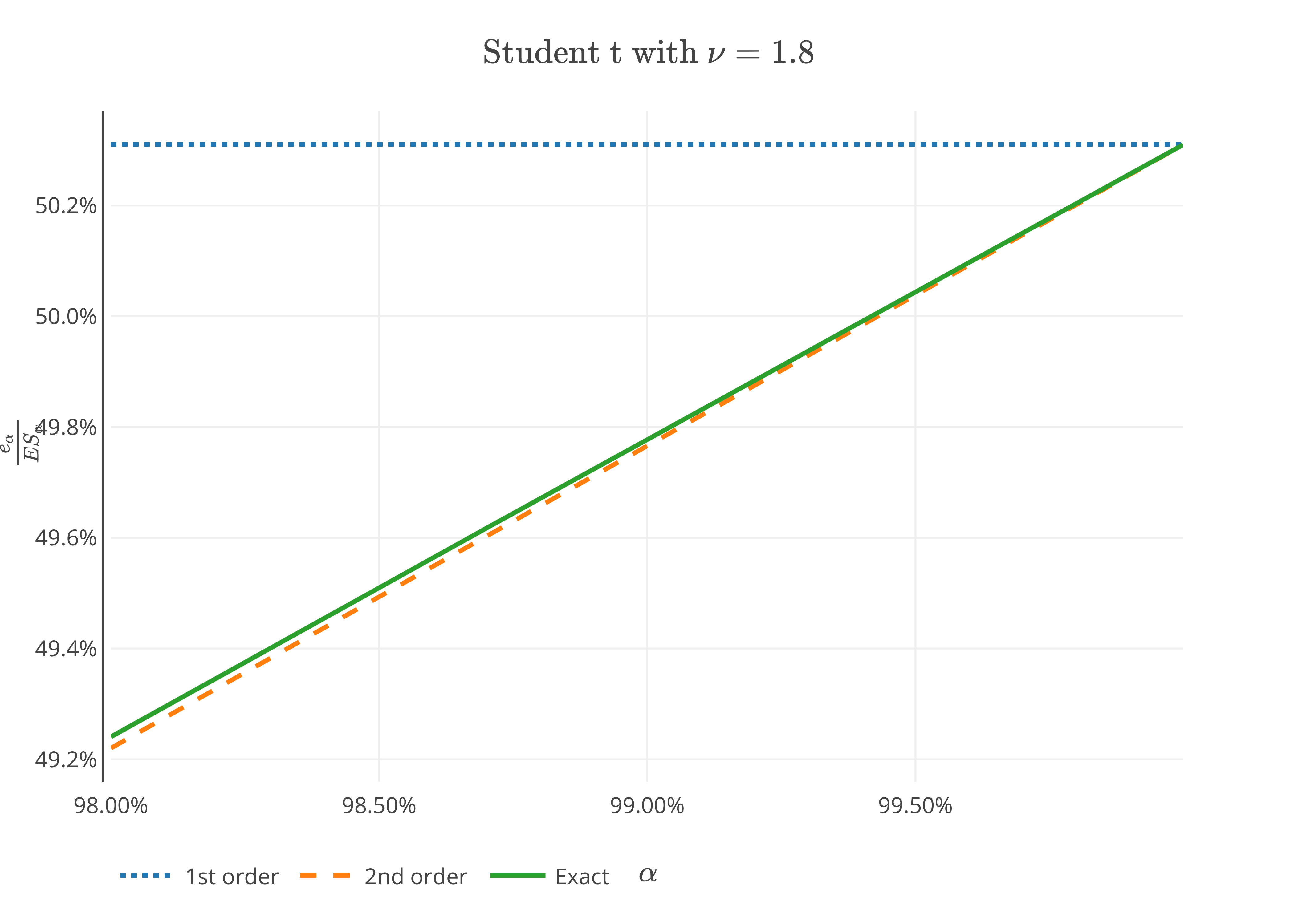

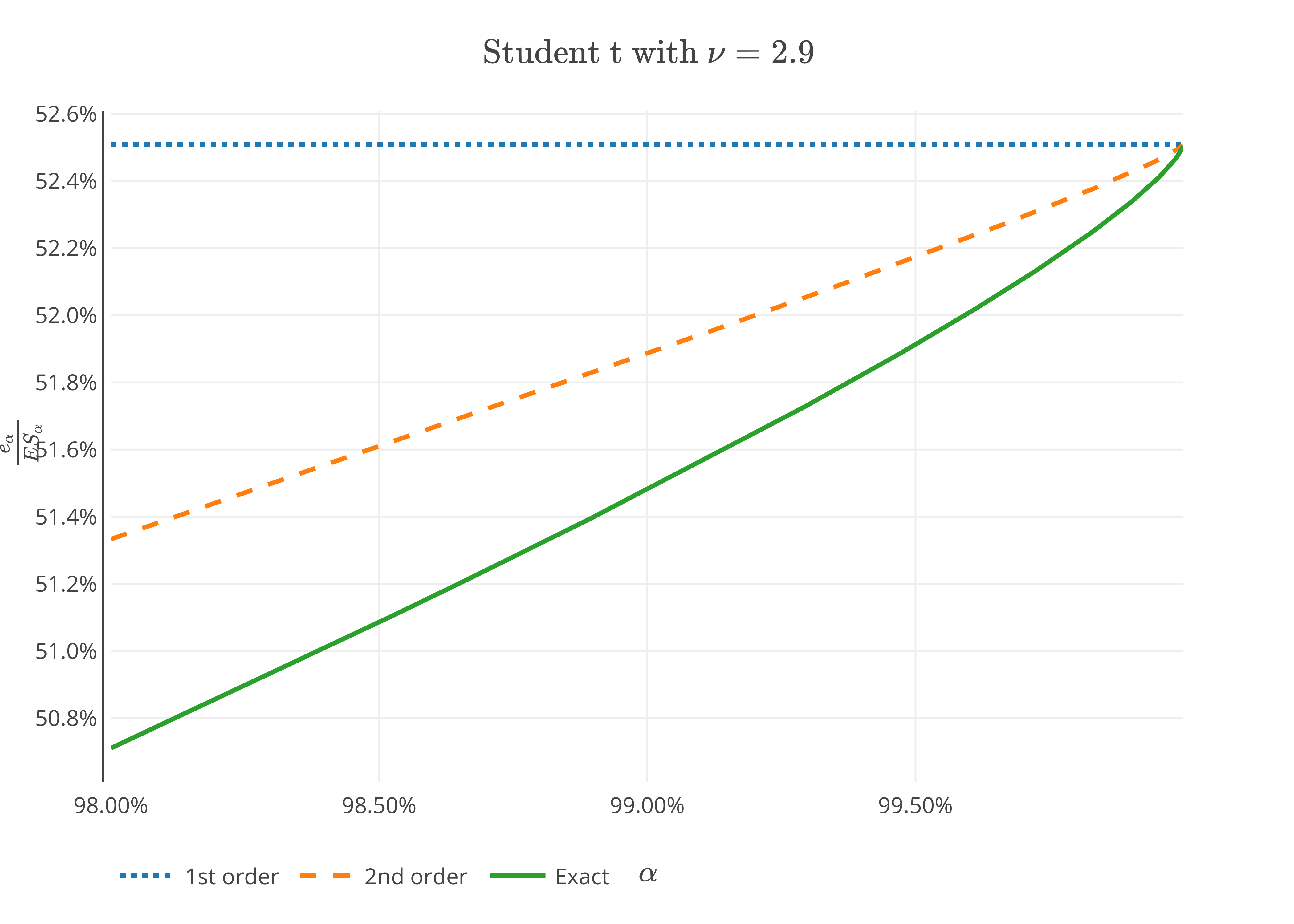

Example 5.4(Standard Student t).

Let be a standard Student with degree of freedom .

From [33], we get

where and are the cumulative distribution and probability density function of the standard Student distribution with degree of freedom, respectively.

Relation (3.3), yields the optimal solving

Hence,

It also holds that such that with auxiliary function , see [24, 32].

By Proposition 4.4, it holds that

Figure 4 shows that the second order expansion is more accurate than the first order one.

The simulation results suggests that the accuracy of the second order expansion is better when the distribution become more heavier.

Figure 4. Graph of for standard Student distribution for and .

As shown in Section 4, in order to have the same bound for the probability of an estimation error bigger than a fixed threshold , value at risk needs more observations than expected shortfall and expectile as goes to , when the data is sampled from a heavy tailed distribution.

As a result of this fact, the same argument can be applied for the ratio of expectile to quantile versus the ratio of expectile to expected shortfall.

To illustrate this fact, we compare the empirical ratios and with the theoretical ratio and , respectively by generating a random sample from Pareto and Standard Student distributions with tail index and .

We denote by the absolute relative percentage error

of the empirical ratio to the theoretical ratio for quantile and expected shortfall, respectively.

Table 1–4 compares the relative percentage error of the empirical ratios and with the theoretical ratio and , respectively.

Indeed, both tables suggest that for Pareto and Student distributions the ratio converges to faster than the ratio of expectile to value at risk.

Theo. Ratio

Emp. Ratio

Emp. Ratio

Emp. Ratio

Expectile vs

Value at Risk

Expectile vs

ES

Table 1. The ratio , , , and relative percentage error of Pareto distribution with .

Theo. Ratio

Emp. Ratio

Emp. Ratio

Emp. Ratio

Expectile vs

Value at Risk

Expectile vs

ES

Table 2. The ratio , , , and relative percentage error for standard Student distribution with .

The simulation result also suggest that with for Student distribution more observations may be needed for than to converge to the theoretical ratio as compared to Pareto distribution with , see Table 1 and 2.

Theo. Ratio

Emp. Ratio

Emp. Ratio

Emp. Ratio

Expectile vs

Value at Risk

Expectile vs

ES

Table 3. The Ratio , , and relative percentage error for Pareto distribution with .

Theo. Ratio

Emp. Ratio

Emp. Ratio

Emp. Ratio

Expectile vs

Value at Risk

Expectile vs

ES

Table 4. The ratio , , , and relative percentage error for standard Student distribution with .

References

Acerbi and Tasche [2002]

C. Acerbi and D. Tasche.

On the coherence of expected shortfall.

Journal of Banking & Finance, 26(7):1487–1503, 2002.

Armenti et al. [2018]

Y. Armenti, S. Crépey, S. Drapeau, and A. Papapantoleon.

Multivariate shortfall risk allocation and systemic risk.

SIAM Journal on Financial Mathematics, 9(1):90–126, 2018.

Artzner et al. [1999]

P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath.

Coherent measures of risk.

Mathematical Finance, 9(3):203–228, 1999.

Asimit et al. [2011]

A. V. Asimit, E. Furman, Q. Tang, and R. Vernic.

Asymptotics for risk capital allocations based on conditional tail

expectation.

Insurance: Mathematics and Economics, 49(3):310–324, 2011.

Bartl and Tangpi [2020]

D. Bartl and L. Tangpi.

Non-asymptotic rates for the estimation of risk measures.

ArXiV, 2020.

Bellini and Bignozzi [2015]

F. Bellini and V. Bignozzi.

On elicitable risk measures.

Quantitative Finance, 15(5):725–733,

2015.

Bellini and Di Bernardino [2017]

F. Bellini and E. Di Bernardino.

Risk management with expectiles.

The European Journal of Finance, 23(6):487–506, 2017.

Bellini et al. [2014]

F. Bellini, B. Klar, A. Müller, and E. Rosazza Gianin.

Generalized quantiles as risk measures.

Insurance: Mathematics and Economics, 54:41–48,

2014.

Ben-Tal and Teboulle [2007]

A. Ben-Tal and M. Teboulle.

An old-new concept of convex risk measures: The optimized certainity

equivalent.

Mathematical Finance, 17(3):449–476,

2007.

Brazauskas et al. [2008]

V. Brazauskas, B. L. Jones, M. L. Puri, and R. Zitikis.

Estimating conditional tail expectation with actuarial applications

in view.

Journal of Statistical Planning and Inference, 138(11):3590–3604, 2008.

Chen [2018]

J. M. Chen.

On exactitude in financial regulation: Value-at-risk, expected

shortfall, and expectiles.

Risks, 6(2):61, 2018.

Daouia et al. [2018]

A. Daouia, S. Girard, and G. Stupfler.

Estimation of tail risk based on extreme expectiles.

Journal of the Royal Statistical Society: Series B (Statistical

Methodology), 80(2):263–292, 2018.

de Haan and Ferreira [2006]

L. de Haan and A. Ferreira.

Extreme Value Theory: An Introduction.

Springer, 2006.

Delbaen [2013]

F. Delbaen.

A remark on the structure of expectiles.

Preprint ArXiV, 2013.

Delbaen et al. [2016]

F. Delbaen, F. Bellini, V. Bignozzi, and J. F. Ziegel.

Risk measures with the CxLS property.

Finance and Stochastics, 20(2):433–453,

2016.

Emmer et al. [2015]

S. Emmer, M. Kratz, and D. Tasche.

What is the best risk measure in practice? A comparison of standard

measures.

Journal of Risk, 18(2):31–60, 2015.

Föllmer and Schied [2002]

H. Föllmer and A. Schied.

Convex measures of risk and trading constraints.

Finance and Stochastics, 6(4):429–447,

2002.

Föllmer and Schied [2016]

H. Föllmer and A. Schied.

Stochastic Finance.

De Gruyter, Berlin, Boston, 4 edition, 2016.

Fournier and Guillin [2015]

N. Fournier and A. Guillin.

On the rate of convergence in Wasserstein distance of the empirical

measure.

Probability Theory and Related Fields, 162(3):707–738, 2015.

Gao and Shaochen [2011]

F. Gao and W. Shaochen.

Asymptotic behavior of the empirical conditional value-at-risk.

Insurance: Mathematics and Economics, 49(3):345–352, 2011.

Gneiting [2011]

T. Gneiting.

Making and evaluating point forecasts.

Journal of the American Statistical Association, 106(494):746–762, 2011.

Guo and Xu [2019]

S. Guo and H. Xu.

Distributionally robust shortfall risk optimization model and its

approximation.

Mathematical Programming, 174(1):473–498,

2019.

Holzmann and Klar [2016]

H. Holzmann and B. Klar.

Expectile asymptotics.

Electronic Journal of Statistics, 10(2):2355–2371, 2016.

Hua and Joe [2011]

L. Hua and H. Joe.

Second order regular variation and conditional tail expectation of

multiple risks.

Insurance: Mathematics and Economics, 49(3):537–546, 2011.

Kalkbrener [2005]

M. Kalkbrener.

An axiomatic approach to capital allocation.

Mathematical Finance, 15(3):425–437,

2005.

Koenker [1993]

R. Koenker.

When are expectiles percentiles?

Econometric Theory, 9(3):526–527, 1993.

Kolla et al. [2019]

R. K. Kolla, P. L.A., , S. P. Bhat, and K. Jagannathan.

Concentration bounds for empirical conditional value-at-risk: The

unbounded case.

Operations Research Letters, 17(1):16–20,

2019.

Lv et al. [2012]

W. Lv, T. Mao, and T. Hu.

Properties of second-order regular variation and expansions for risk

concentration.

Probability in the Engineering and Informational Sciences,

26(4):535–559, 2012.

Major [1978]

P. Major.

On the invariance principle for sums of independent identically

distributed random variables.

Journal of Multivariate Analysis, 8(4):487–517, 1978.

Mao and Hu [2012]

T. Mao and T. Hu.

Second-order properties of the Haezendonck–Goovaerts

risk measure for extreme risks.

Insurance: Mathematics and Economics, 51(2):333–343, 2012.

Mao and Yang [2015]

T. Mao and F. Yang.

Risk concentration based on expectiles for extreme risks under FGM

copula.

Insurance: Mathematics and Economics, 64:429–439,

2015.

Mao et al. [2015]

T. Mao, K. W. Ng, and T. Hu.

Asymptotic expansions of generalized quantiles and expectiles for

extreme risks.

Probability in the Engineering and Informational Sciences,

29(3):309–327, 2015.

McNeil et al. [2015]

A. J. McNeil, R. Frey, and P. Embrechts.

Quantitative risk management: Concepts, techniques and tools:

Revised edition.

Princeton University Press, 2015.

Newey and Powell [1987]

W. K. Newey and J. L. Powell.

Asymmetric least squares estimation and testing.

Econometrica, 55(4):819–847, 1987.

Shapiro [2013]

A. Shapiro.

On Kusuoka representation of law invariant risk measures.

Mathematics of Operations Research, 38(1):142–152, 2013.

Tang and Yang [2012]

Q. Tang and F. Yang.

On the Haezendonck–Goovaerts risk measure for extreme

risks.

Insurance: Mathematics and Economics, 50(1):217–227, 2012.

Tasche [2002]

D. Tasche.

Expected shortfall and beyond.

Journal of Banking & Finance, 26(7):1519–1533, 2002.

Tasche [2008]

D. Tasche.

Capital allocation to business units and sub-portfolios: the Euler

principle.

Preprint ArXiV, 2008.

Taylor [2008]

J. W. Taylor.

Estimating value at risk and expected shortfall using expectiles.

Journal of Financial Econometrics, 6(2):231–252, 2008.

Weber [2006]

S. Weber.

Distribution-invariant risk measures, information, and dynamic

consistency.

Mathematical Finance, 16(2):419–441,

2006.

Ziegel [2016]

J. F. Ziegel.

Coherence and elicitability.

Mathematical Finance, 26(4):901–918,

2016.