Resolving New Keynesian Anomalies

with Wealth in the Utility Function

At the zero lower bound, the New Keynesian model predicts that output and inflation collapse to implausibly low levels, and that government spending and forward guidance have implausibly large effects. To resolve these anomalies, we introduce wealth into the utility function; the justification is that wealth is a marker of social status, and people value status. Since people partly save to accrue social status, the Euler equation is modified. As a result, when the marginal utility of wealth is sufficiently large, the dynamical system representing the zero-lower-bound equilibrium transforms from a saddle to a source—which resolves all the anomalies.

Introduction

A current issue in monetary economics is that the New Keynesian model makes several anomalous predictions when the zero lower bound on nominal interest rates (ZLB) is binding: implausibly large collapse of output and inflation (Eggertsson and Woodford 2004; Eggertsson 2011; Werning 2011); implausibly large effect of forward guidance (Del Negro, Giannoni, and Patterson 2015; Carlstrom, Fuerst, and Paustian 2015; Cochrane 2017); and implausibly large effect of government spending (Christiano, Eichenbaum, and Rebelo 2011; Woodford 2011; Cochrane 2017).

Several papers have developed variants of the New Keynesian model that behave well at the ZLB (Gabaix 2016; Diba and Loisel 2019; Cochrane 2018; Bilbiie 2019; Acharya and Dogra 2019); but these variants are more complex than the standard model. In some cases the derivations are complicated by bounded rationality or heterogeneity. In other cases the dynamical system representing the equilibrium—normally composed of an Euler equation and a Phillips curve—includes additional differential equations that describe bank-reserve dynamics, price-level dynamics, or the evolution of the wealth distribution. Moreover, a good chunk of the analysis is conducted by numerical simulations. Hence, it is sometimes difficult to grasp the nature of the anomalies and their resolutions.

It may therefore be valuable to strip the logic to the bone. We do so using a New Keynesian model in which relative wealth enters the utility function. The justification for the assumption is that relative wealth is a marker of social status, and people value high social status. We deviate from the standard model only minimally: the derivations are the same; the equilibrium is described by a dynamical system composed of an Euler equation and a Phillips curve; the only difference is an extra term in the Euler equation. We also veer away from numerical simulations and establish our results with phase diagrams describing the dynamics of output and inflation given by the Euler-Phillips system. The model’s simplicity and the phase diagrams allow us to gain new insights into the anomalies and their resolutions.111Our approach relates to the work of Michaillat and Saez (2014), Ono and Yamada (2018), and Michau (2018). By assuming wealth in the utility function, they obtain non-New-Keynesian models that behave well at the ZLB. But their results are not portable to the New Keynesian framework because they require strong forms of wage or price rigidity (exogenous wages, fixed inflation, or downward nominal wage rigidity). Our approach also relates to the work of Fisher (2015) and Campbell et al. (2017), who build New Keynesian models with government bonds in the utility function. The bonds-in-the-utility assumption captures special features of government bonds relative to other assets, such as safety and liquidity (for example, Krishnamurthy and Vissing-Jorgensen 2012). While their assumption and ours are conceptually different, they affect equilibrium conditions in a similar way. These papers use their assumption to generate risk-premium shocks (Fisher) and to alleviate the forward-guidance puzzle (Campbell et al.).

Using the phase diagrams, we begin by depicting the anomalies in the standard New Keynesian model. First, we find that output and inflation collapse to unboundedly low levels when the ZLB episode is arbitrarily long-lasting. Second, we find that there is a duration of forward guidance above which any ZLB episode, irrespective of its duration, is transformed into a boom. Such boom is unbounded when the ZLB episode is arbitrarily long-lasting. Third, we find that there is an amount of government spending at which the government-spending multiplier becomes infinite when the ZLB episode is arbitrarily long-lasting. Furthermore, when government spending exceeds this amount, an arbitrarily long ZLB episode prompts an unbounded boom.

The phase diagrams also pinpoint the origin of the anomalies: they arise because the Euler-Phillips system is a saddle at the ZLB. In normal times, by contrast, the Euler-Phillips system is source, so there are no anomalies. In economic terms, the anomalies arise because household consumption (given by the Euler equation) responds too strongly to the real interest rate. Indeed, since the only motive for saving is future consumption, households are very forward-looking, and their response to interest rates is strong.

Once wealth enters the utility function, however, the Euler equation is “discounted”—in the sense of McKay, Nakamura, and Steinsson (2017)—which alters the properties of the Euler-Phillips system. People now save partly because they enjoy holding wealth; this is a present consideration, which does not require them to look into the future. As people are less forward-looking, their consumption responds less to interest rates; this creates discounting.

With enough marginal utility of wealth, the discounting is strong enough to transform the Euler-Phillips system from a saddle to a source at the ZLB and thus eliminate all the anomalies. First, output and inflation never collapse at the ZLB: they are bounded below by the ZLB steady state. Second, when the ZLB episode is long enough, the economy necessarily experiences a slump, irrespective of the duration of forward guidance. Third, government-spending multipliers are always finite, irrespective of the duration of the ZLB episode.

Apart from its anomalies, the standard New Keynesian model has several other intriguing properties at the ZLB—some labeled “paradoxes” because they defy usual economic logic (Eggertsson 2010; Werning 2011; Eggertsson and Krugman 2012). Our model shares these properties. First, the paradox of thrift holds: when households desire to save more than their neighbors, the economy contracts and they end up saving the same amount as the neighbors. The paradox of toil also holds: when households desire to work more, the economy contracts and they end up working less. The paradox of flexibility is present too: the economy contracts when prices become more flexible. Last, the government-spending multiplier is above one, so government spending stimulates private consumption.

Justification for Wealth in the Utility Function

Before delving into the model, we justify our assumption of wealth in the utility function.

The standard model assumes that people save to smooth consumption over time, but it has long been recognized that people seem to enjoy accumulating wealth irrespective of future consumption. Describing the European upper class of the early 20th century, Keynes (1919, chap. 2) noted that “The duty of saving became nine-tenths of virtue and the growth of the cake the object of true religion…. Saving was for old age or for your children; but this was only in theory—the virtue of the cake was that it was never to be consumed, neither by you nor by your children after you.” Irving Fisher added that “A man may include in the benefits of his wealth …the social standing he thinks it gives him, or political power and influence, or the mere miserly sense of possession, or the satisfaction in the mere process of further accumulation” (Fisher 1930, p. 17). Fisher’s perspective is interesting since he developed the theory of saving based on consumption smoothing.

Neuroscientific evidence confirms that wealth itself provides utility, independently of the consumption it can buy. Camerer, Loewenstein, and Prelec (2005, p. 32) note that “brain-scans conducted while people win or lose money suggest that money activates similar reward areas as do other ‘primary reinforcers’ like food and drugs, which implies that money confers direct utility, rather than simply being valued only for what it can buy.”

Among all the reasons why people may value wealth, we focus on social status: we postulate that people enjoy wealth because it provides social status. We therefore introduce relative (not absolute) wealth into the utility function.222Cole, Mailath, and Postlewaite (1992, 1995) develop models in which relative wealth does not directly confer utility but has other attributes such that people behave as if wealth entered their utility function. In one such model, wealthier individuals have higher social rankings, which allows them to marry wealthier partners and enjoy higher utility. The assumption is convenient: in equilibrium everybody is the same, so relative wealth is zero. And the assumption seems plausible. Adam Smith, Ricardo, John Rae, J.S. Mill, Marshall, Veblen, and Frank Knight all believed that people accumulate wealth to attain high social status (Steedman 1981). More recently, a broad literature has documented that people seek to achieve high social status, and that accumulating wealth is a prevalent pathway to do so (Weiss and Fershtman 1998; Heffetz and Frank 2011; Fiske 2010; Anderson, Hildreth, and Howland 2015; Cheng and Tracy 2013; Ridgeway 2014; Mattan, Kubota, and Cloutier 2017).333The wealth-in-the-utility assumption has been found useful in models of long-run growth (Kurz 1968; Konrad 1992; Zou 1994; Corneo and Jeanne 1997; Futagami and Shibata 1998), risk attitudes (Robson 1992; Clemens 2004), asset pricing (Bakshi and Chen 1996; Gong and Zou 2002; Kamihigashi 2008; Michau, Ono, and Schlegl 2018), life-cycle consumption (Zou 1995; Carroll 2000; Francis 2009; Straub 2019), social stratification (Long and Shimomura 2004), international macroeconomics (Fisher 2005; Fisher and Hof 2005), financial crises (Kumhof, Ranciere, and Winant 2015), and optimal taxation (Saez and Stantcheva 2018). Such usefulness lends further support to the assumption.

New Keynesian Model with Wealth in the Utility Function

We extend the New Keynesian model by assuming that households derive utility not only from consumption and leisure but also from relative wealth. To simplify derivations and be able to represent the equilibrium with phase diagrams, we use an alternative formulation of the New Keynesian model, inspired by Benhabib, Schmitt-Grohe, and Uribe (2001) and Werning (2011). Our formulation features continuous time instead of discrete time; self-employed households instead of firms and households; and Rotemberg (1982) pricing instead of Calvo (1983) pricing.

Assumptions

The economy is composed of a measure 1 of self-employed households. Each household produces units of a good at time , sold to other households at a price . The household’s production function is , where represents the level of technology, and is hours of work. Working causes a disutility , where is the marginal disutility of labor.

The goods produced by households are imperfect substitutes for one another, so each household exercises some monopoly power. Moreover, households face a quadratic cost when they change their price: changing a price at a rate causes a disutility . The parameter governs the cost to change prices and thus price rigidity.

Each household consumes goods produced by other households. Household buys quantities of the goods . These quantities are aggregated into a consumption index

where is the elasticity of substitution between goods. The consumption index yields utility . Given the consumption index, the relevant price index is

When households optimally allocate their consumption expenditure across goods, is the price of one unit of consumption index. The inflation rate is defined as .

Households save using government bonds. Since we postulate that people derive utility from their relative real wealth, and since bonds are the only store of wealth, holding bonds directly provides utility. Formally, holding a nominal quantity of bonds yields utility

The function is increasing and concave, is average nominal wealth, and is household ’s relative real wealth.

Bonds earn a nominal interest rate , where is the nominal interest rate set by the central bank, and is a spread between the monetary-policy rate () and the rate used by households for savings decisions (). The spread captures the efficiency of financial intermediation (Woodford 2011); the spread is large when financial intermediation is severely disrupted, as during the Great Depression and Great Recession. The law of motion of household bond holdings is

The term is interest income; is labor income; is consumption expenditure; and is a lump-sum tax (used among other things to service government debt).

Lastly, the problem of household is to choose time paths for , , , , for all , and to maximize the discounted sum of instantaneous utilities

where is the time discount rate. The household faces four constraints: production function; law of motion of good ’s price, ; law of motion of bond holdings; and demand for good coming from other households’ maximization,

where is aggregate consumption. The household also faces a borrowing constraint preventing Ponzi schemes. The household takes as given aggregate variables, initial wealth , and initial price . All households face the same initial conditions, so they will behave the same.

Euler Equation and Phillips Curve

The equilibrium is described by a system of two differential equations: an Euler equation and a Phillips curve. The Euler-Phillips system governs the dynamics of output and inflation . Here we present the system; formal and heuristic derivations are in appendices A and B; a discrete-time version is in appendix C.

The Phillips curve arises from households’ optimal pricing decisions:

| (1) |

where

| (2) |

The Phillips curve is not modified by wealth in the utility function.

The steady-state Phillips curve, obtained by setting in (1), describes inflation as a linearly increasing function of output:

| (3) |

We see that is the natural level of output: the level at which producers keep their prices constant.

The Euler equation arises from households’ optimal consumption-savings decisions:

| (4) |

where is the real monetary-policy rate and

| (5) |

The marginal utility of wealth, , enters the Euler equation, so unlike the Phillips curve, the Euler equation is modified by the wealth-in-the-utility assumption. To understand why consumption-savings choices are affected by the assumption, we rewrite the Euler equation as

| (6) |

where is the real interest rate on bonds. In the standard equation, consumption-savings choices are governed by the financial returns on wealth, given by , and the cost of delaying consumption, given by . Here, people also enjoy holding wealth, so a new term appears to capture the hedonic returns on wealth: the marginal rate of substitution between wealth and consumption, . In the marginal rate of substitution, the marginal utility of wealth is because in equilibrium all households hold the same wealth so relative wealth is zero; the marginal utility of consumption is because consumption utility is log. Thus the wealth-in-the-utility assumption operates by transforming the rate of return on wealth from to .

Because consumption-savings choices depend not only on interest rates but also on the marginal rate of substitution between wealth and consumption, future interest rates have less impact on today’s consumption than in the standard model: the Euler equation is discounted. In fact, the discrete-time version of Euler equation (4) features discounting exactly as in McKay, Nakamura, and Steinsson (2017) (see appendix C).

The steady-state Euler equation is obtained by setting in (4):

| (7) |

The equation describes output as a linearly decreasing function of the real monetary-policy rate—as in the old-fashioned, Keynesian IS curve. We see that is the natural rate of interest: the real monetary-policy rate at which households consume a quantity .

The steady-state Euler equation is deeply affected by the wealth-in-the-utility assumption. To understand why, we rewrite (7) as

| (8) |

The standard steady-state Euler equation boils down to . It imposes that the financial rate of return on wealth equals the time discount rate—otherwise households would not keep their consumption constant. With wealth in the utility function, the returns on wealth are not only financial but also hedonic. The total rate of return becomes , where the hedonic returns are measured by . The steady-state Euler equation imposes that the total rate of return on wealth equals the time discount rate, so it now involves output . When the real interest rate is higher, people have a financial incentive to save more and postpone consumption. They keep consumption constant only if the hedonic returns on wealth fall enough to offset the increase in financial returns: this requires output to decline. As a result, with wealth in the utility function, the steady-state Euler equation describes output as a decreasing function of the real interest rate—as in the traditional IS curve, but through a different mechanism.

The wealth-in-the-utility assumption adds one parameter to the equilibrium conditions: . Accordingly, we compare two submodels:

Definition 1.

The New Keynesian (NK) model has zero marginal utility of wealth: . The wealth-in-the-utility New Keynesian (WUNK) model has sufficient marginal utility of wealth:

| (9) |

The NK model is the standard model; the WUNK model is the extension proposed in this paper. When prices are fixed (), condition (9) becomes ; when prices are perfectly flexible (), condition (9) becomes . Hence, at the fixed-price limit, the WUNK model only requires an infinitesimal marginal utility of wealth; at the flexible-price limit, the WUNK model is not well-defined. In the WUNK model we also impose in order to accommodate positive natural rates of interest.444Indeed, using (2) and (9), we see that in the WUNK model This implies that the natural rate of interest, , is bounded above: For the WUNK model to accommodate positive natural rates of interest, the upper bound on the natural rate must be positive, which requires .

Natural Rate of Interest and Monetary Policy

The central bank aims to maintain the economy at the natural steady state, where inflation is at zero and output at its natural level.

In normal times, the natural rate of interest is positive, and the central bank is able to maintain the economy at the natural steady state using the simple policy rule . The corresponding real policy rate is . The parameter governs the response of interest rates to inflation: monetary policy is active when and passive when .

When the natural rate of interest is negative, however, the natural steady state cannot be achieved—because this would require the central bank to set a negative nominal policy rate, which would violate the ZLB. In that case, the central bank moves to the ZLB: , so .

What could cause the natural rate of interest to be negative? A first possibility is a banking crisis, which disrupts financial intermediation and raises the interest-rate spread (Woodford 2011; Eggertsson 2011). The natural rate of interest turns negative when the spread is large enough: . Another possibility in the WUNK model is drop in consumer sentiment, which leads households to favor saving over consumption, and can be parameterized by an increase in the marginal utility of wealth. The natural rate of interest turns negative when the marginal utility is large enough: .

Properties of the Euler-Phillips System

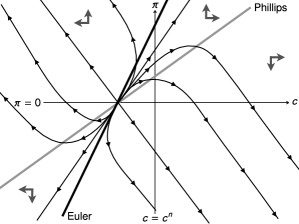

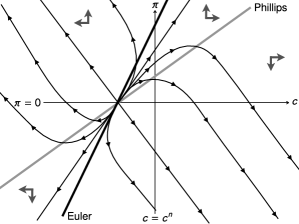

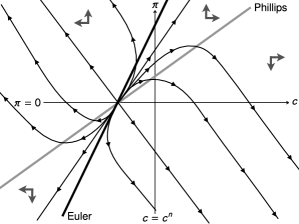

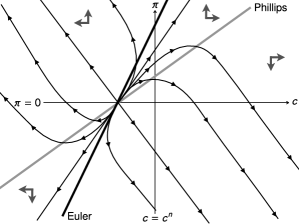

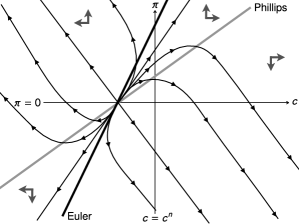

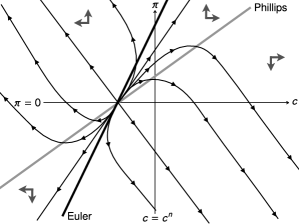

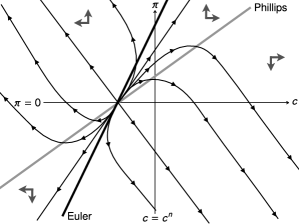

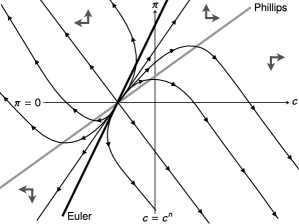

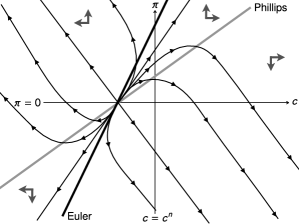

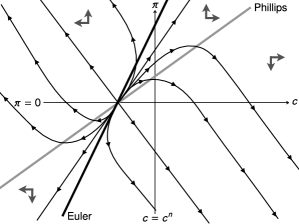

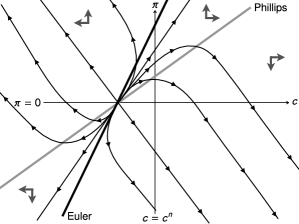

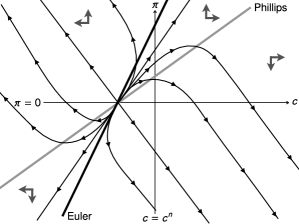

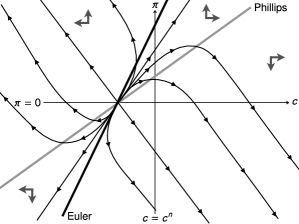

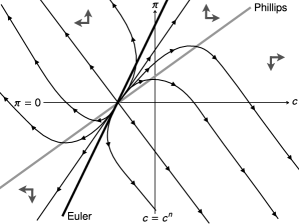

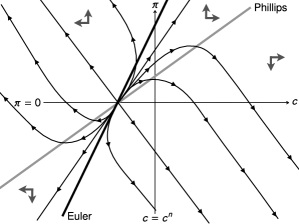

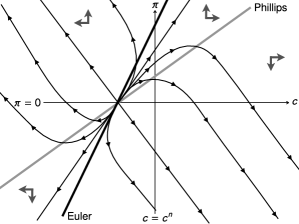

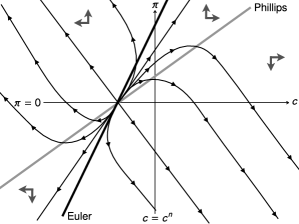

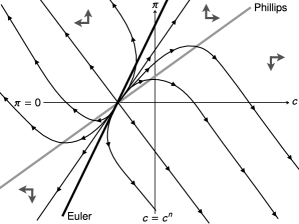

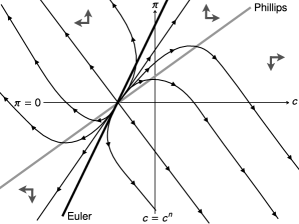

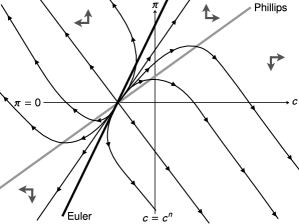

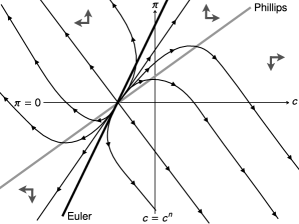

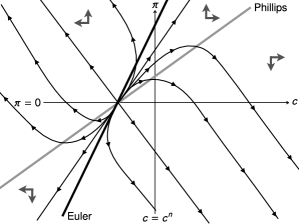

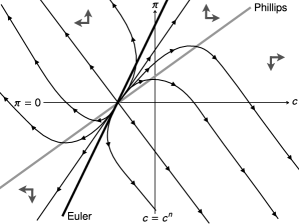

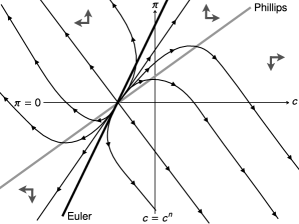

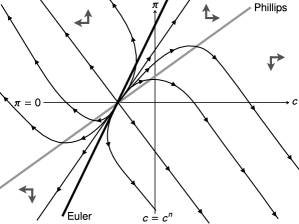

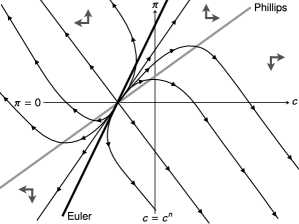

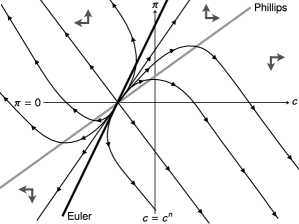

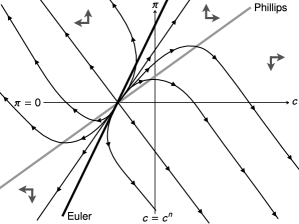

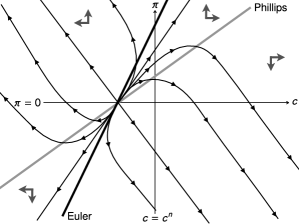

We now establish the properties of the Euler-Phillips systems in the NK and WUNK models by constructing their phase diagrams.555The properties are rederived using an algebraic approach in appendix D. The diagrams are displayed in figure 1.

The figure displays phase diagrams for the dynamical system generated by the Euler equation (4) and Phillips curve (1): is output; is inflation; is the natural level of output; the Euler line is the locus ; the Phillips line is the locus ; the trajectories are solutions to the Euler-Phillips system linearized around its steady state, plotted for going from to . The four panels contrast various cases. The NK model is the standard New Keynesian model. The WUNK model is the same model, except that the marginal utility of wealth is not zero but is sufficiently large to satisfy (9). In normal times, the natural rate of interest is positive, and the monetary-policy rate is given by ; when monetary policy is active, . At the ZLB, the natural rate of interest is negative, and the monetary-policy rate is zero. The figure shows that in the NK model, the Euler-Phillips system is a source in normal times with active monetary policy (panel A); but the system is a saddle at the ZLB (panel C). In the WUNK model, by contrast, the Euler-Phillips system is a source both in normal times and at the ZLB (panels B and D). (Panels A and B display a nodal source, but the system could also be a spiral source, depending on the value of ; in panel D the system is always a nodal source.)

We begin with the Phillips curve, which gives . First, we plot the locus , which we label “Phillips.” The locus is given by the steady-state Phillips curve (3): it is linear, upward sloping, and goes through the point . Second, we plot the arrows giving the directions of the trajectories solving the Euler-Phillips system. The sign of is given by the Phillips curve (1): any point above the Phillips line (where ) has , and any point below the line has . So inflation is rising above the Phillips line and falling below it.

We next turn to the Euler equation, which gives . Whereas the Phillips curve is the same in the NK and WUNK models, and in normal times and at the ZLB, the Euler equation is different in each case. We therefore proceed case by case.

We start with the NK model in normal times and with active monetary policy (panel A). The Euler equation (4) becomes

with . The locus , labeled “Euler,” is simply the horizontal line . Since the Phillips and Euler lines only intersect at the point , we conclude that the Euler-Phillips system admits a unique steady state with zero inflation and natural output. Next we examine the sign of . As , any point above the Euler line has , and any point below the line has . Since all the trajectories solving the Euler-Phillips system move away from the steady state in the four quadrants delimited by the Phillips and Euler lines, we conclude that the Euler-Phillips system is a source.

We then consider the WUNK model in normal times with active monetary policy (panel B). The Euler equation (4) becomes

with . We first use the Euler equation to compute the Euler line (locus ):

The Euler line is linear, downward sloping (as ), and goes through the point . Since the Phillips and Euler lines only intersect at the point , we conclude that the Euler-Phillips system admits a unique steady state, with zero inflation and output at its natural level. Next we use the Euler equation to determine the sign of . As , any point above the Euler line has , and any point below it has . Hence, the solution trajectories move away from the steady state in all four quadrants of the phase diagram; we conclude that the Euler-Phillips system is a source. In normal times with active monetary policy, the Euler-Phillips system therefore behaves similarly in the NK and WUNK models.

We next turn to the NK model at the ZLB (panel C). The Euler equation (4) becomes

Thus the Euler line (locus ) shifts up from in normal times to at the ZLB. We infer that the Euler-Phillips system admits a unique steady state, where inflation is positive and output is above its natural level. Furthermore, any point above the Euler line has , and any point below it has . As a result, the solution trajectories move toward the steady state in the southwest and northeast quadrants of the phase diagram, whereas they move away from it in the southeast and northwest quadrants. We infer that the Euler-Phillips system is a saddle.

We finally move to the WUNK model at the ZLB (panel D). The Euler equation (4) becomes

First, this differential equation implies that the Euler line (locus ) is given by

| (10) |

So the Euler line is linear, upward sloping, and goes through the point . The Euler line has become upward sloping because the real monetary-policy rate, which was increasing with inflation when monetary policy was active, has become decreasing with inflation at the ZLB (). Since , the Euler line has shifted inward of the point , explaining why the central bank is unable to achieve the natural steady state at the ZLB. And since the slope of the Euler line is while that of the Phillips line is , the WUNK condition (9) ensures that the Euler line is steeper than the Phillips line at the ZLB. From the Euler and Phillips lines, we infer that the Euler-Phillips system admits a unique steady state, in which inflation is negative and output is below its natural level.666We also check that the intersection of the Euler and Phillips lines has positive output (appendix D).

Second, the differential equation shows that any point above the Euler line has , and any point below it has . Hence, in all four quadrants of the phase diagram, the trajectories move away from the steady state. We conclude that the Euler-Phillips system is a source. At the ZLB, the Euler-Phillips system therefore behaves very differently in the NK and WUNK models.

With passive monetary policy in normal times, the phase diagrams of the Euler-Phillips system would be similar to the ZLB phase diagrams—except that the Euler and Phillips lines would intersect at . In particular, the Euler-Phillips system would be a saddle in the NK model and a source in the WUNK model.

For completeness, we also plot sample solutions to the Euler-Phillips system. The trajectories are obtained by linearizing the Euler-Phillips system at its steady state.777Technically the trajectories only approximate the exact solutions; but the approximation is accurate in the neighborhood of the steady state. When the system is a source, there are two unstable lines (trajectories that move away from the steady state in a straight line). At , all other trajectories are in the vicinity of the steady state and move away tangentially to one of the unstable lines. At , the trajectories move to infinity parallel to the other unstable line. When the system is a saddle, there is one unstable line and one stable line (trajectory that goes to the steady state in a straight line). All other trajectories come from infinity parallel to the stable line when , and move to infinity parallel to the unstable line when .

The next propositions summarize the results:

Proposition 1.

Consider the Euler-Phillips system in normal times. The system admits a unique steady state, where output is at its natural level, inflation is zero, and the ZLB is not binding. In the NK model, the system is a source when monetary policy is active but a saddle when monetary policy is passive. In the WUNK model, the system is a source whether monetary policy is active or passive.

Proposition 2.

Consider the Euler-Phillips system at the ZLB. In the NK model, the system admits a unique steady state, where output is above its natural level and inflation is positive; furthermore, the system is a saddle. In the WUNK model, the system admits a unique steady state, where output is below its natural level and inflation is negative; furthermore, the system is a source.

The propositions give the key difference between the NK and WUNK models: at the ZLB, the Euler-Phillips system remains a source in the WUNK model, whereas it becomes a saddle in the NK model. This difference will explain why the WUNK model does not suffer from the anomalies plaguing the NK model at the ZLB. The phase diagrams also illustrate the origin of the WUNK condition (9). In the WUNK model, the Euler-Phillips system remains a source at the ZLB as long as the Euler line is steeper than the Phillips line (figure 1, panel D). The Euler line’s slope at the ZLB is the marginal utility of wealth, so that marginal utility is required to be above a certain level—which is given by (9).

The propositions have implications for equilibrium determinacy. When the Euler-Phillips system is a source, the equilibrium is determinate: the only equilibrium trajectory in the vicinity of the steady state is to jump to the steady state and stay there; if the economy jumped somewhere else, output or inflation would diverge following a trajectory similar to those plotted in panels A, B, and D of figure 1. When the system is a saddle, the equilibrium is indeterminate: any trajectory jumping somewhere on the saddle path and converging to the steady state is an equilibrium (figure 1, panel C). Hence, in the NK model, the equilibrium is determinate when monetary policy is active but indeterminate when monetary policy is passive and at the ZLB. In the WUNK model, the equilibrium is always determinate, even when monetary policy is passive and at the ZLB.

Accordingly, in the NK model, the Taylor principle holds: the central bank must adhere to an active monetary policy to avoid indeterminacy. From now on, we therefore assume that the central bank in the NK model follows an active policy whenever it can ( whenever ). In the WUNK model, by contrast, indeterminacy is never a risk, so the central bank does not need to worry about how strongly its policy rate responds to inflation. The central bank could even follow an interest-rate peg without creating indeterminacy.

The results that pertain to the NK model in propositions 1 and 2 are well-known (for example, Woodford 2001). The results that pertain to the WUNK model are close to those obtained by Gabaix (2016, proposition 3.1), although he does not use our phase-diagram representation. Gabaix finds that when bounded rationality is strong enough, the Euler-Phillips system is a source even at the ZLB. He also finds that when prices are more flexible, more bounded rationality is required to maintain the source property. The same is true here: when the marginal utility of wealth is high enough, such that (9) holds, the Euler-Phillips system is a source even at the ZLB; and when the price-adjustment cost is lower, (9) imposes a higher threshold on the marginal utility of wealth. Our phase diagrams illustrate the logic behind these results. The Euler-Phillips system remains a source at the ZLB as long as the Euler line is steeper than the Phillips line (figure 1, panel D). As the slope of the Euler line is determined by bounded rationality in the Gabaix model and by marginal utility of wealth in our model, these need to be large enough. When prices are more flexible, the Phillips line steepens, so the Euler line’s required steepness increases: bounded rationality or marginal utility of wealth need to be larger.

Description and Resolution of the New Keynesian Anomalies

We now describe the anomalous predictions of the NK model at the ZLB: implausibly large drop in output and inflation; and implausibly strong effects of forward guidance and government spending. We then show that these anomalies are absent from the WUNK model.

| Timeline | Natural rate | Monetary | Government | |

| of interest | policy | spending | ||

| A. ZLB episode | ||||

| ZLB: | – | |||

| Normal times: | – | |||

| B. ZLB episode with forward guidance | ||||

| ZLB: | – | |||

| Forward guidance: | – | |||

| Normal times: | – | |||

| C. ZLB episode with government spending | ||||

| ZLB: | ||||

| Normal times: | ||||

This table describes the three scenarios analyzed in section 4: the ZLB episode, in section 4.1; the ZLB episode with forward guidance, in section 4.2; and the ZLB episode with government spending, in section 4.3. The parameter gives the duration of the ZLB episode; the parameter gives the duration of forward guidance. We assume that monetary policy is active () in normal times in the NK model; this assumption is required to ensure equilibrium determinacy (Taylor principle). In the WUNK model, monetary policy can be active or passive in normal times.

Drop in Output and Inflation

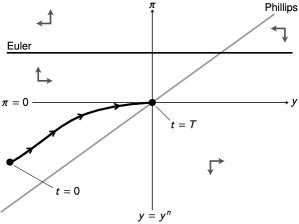

We consider a temporary ZLB episode, as in Werning (2011). Between times and , the natural rate of interest is negative. In response, the central bank maintains its policy rate at zero. After time , the natural rate is positive again, and monetary policy returns to normal. This scenario is summarized in table 1, panel A. We analyze the ZLB episode using the phase diagrams in figure 2.

We start with the NK model. We analyze the ZLB episode by going backward in time. After time , monetary policy maintains the economy at the natural steady state. Since equilibrium trajectories are continuous, the economy also is at the natural steady state at the end of the ZLB, when .888The trajectories are continuous in output and inflation because households have concave preferences over the two arguments. If consumption had an expected discrete jump, for example, households would be able to increase their utility by reducing the size of the discontinuity.

We then move back to the ZLB episode, when . At time , the economy jumps to the unique position leading to at time . Hence, inflation and output initially jump down to and , and then recover following the unique trajectory leading to . The ZLB therefore creates a slump, with below-natural output and deflation (panel A).

Critically, the economy is always on the same trajectory during the ZLB, irrespective of the ZLB duration . A longer ZLB only forces output and inflation to start from a lower position on the trajectory at time . Thus, as the ZLB lasts longer, initial output and inflation collapse to unboundedly low levels (panel C).

The figure describes various ZLB episodes. The timeline of a ZLB episode is presented in table 1, panel A. Panel A displays the phase diagram of the NK model’s Euler-Phillips system at the ZLB; it comes from figure 1, panel C. Panel B displays the phase diagram of the WUNK model’s Euler-Phillips system at the ZLB; it comes from figure 1, panel D. Panels C and D are the same as panels A and B, but with a longer-lasting ZLB (larger ). The equilibrium trajectories are the unique trajectories reaching the natural steady state (where and ) at time . The figure shows that the economy slumps during the ZLB: inflation is negative and output is below its natural level (panels A and B). In the NK model, the initial slump becomes unboundedly severe as the ZLB lasts longer (panel C). In the WUNK model, there is no such collapse: output and inflation are bounded below by the ZLB steady state (panel D).

Now let us examine the WUNK model. Output and inflation never collapse during the ZLB. Initially inflation and output jump down toward the ZLB steady state, denoted , so and . They then recover following the trajectory going through . Consequently the ZLB episode creates a slump (panel B), which is deeper when the ZLB lasts longer (panel D). But unlike in the NK model, the slump is bounded below by the ZLB steady state: irrespective of the duration of the ZLB, output and inflation remain above and , respectively, so they never collapse. Moreover, if the natural rate of interest is negative but close to zero, such that is close to zero and to , output and inflation will barely deviate from the natural steady state during the ZLB—even if the ZLB lasts a very long time.

The following proposition records these results:999The result that in the NK model output becomes infinitely negative when the ZLB becomes infinitely long should not be interpreted literally. It is obtained because we omitted the constraint that output must remain positive. The proper interpretation is that output falls much, much below its natural level—in fact it converges to zero.

Proposition 3.

Consider a ZLB episode between times and . The economy enters a slump: and for all . In the NK model, the slump becomes infinitely severe as the ZLB duration approaches infinity: . In the WUNK model, in contrast, the slump is bounded below by the ZLB steady state : and for all . In fact, the slump approaches the ZLB steady state as the ZLB duration approaches infinity: and .

In the NK model, output and inflation collapse when the ZLB is long-lasting, which is well-known (Eggertsson and Woodford 2004, fig. 1; Eggertsson 2011, fig. 1; Werning 2011, proposition 1). This collapse is difficult to reconcile with real-world observations. The ZLB episode that started in 1995 in Japan lasted for more than twenty years without sustained deflation. The ZLB episode that started in 2009 in the euro area lasted for more than 10 years; it did not yield sustained deflation either. The same is true of the ZLB episode that occurred in the United States between 2008 and 2015.

In the WUNK model, in contrast, inflation and output never collapse. Instead, as the duration of the ZLB increases, the economy converges to the ZLB steady state. That ZLB steady state may not be far from the natural steady state: if the natural rate of interest is only slightly negative, inflation is only slightly below zero and output only slightly below its natural level. Gabaix (2016, proposition 3.2) obtains a closely related result: in his model output and inflation also converge to the ZLB steady state when the ZLB is arbitrarily long.

Forward Guidance

We turn to the effects of forward guidance at the ZLB. We consider a three-stage scenario, as in Cochrane (2017). Between times and , there is a ZLB episode. To alleviate the situation, the central bank makes a forward-guidance promise at time : that it will maintain the policy rate at zero for a duration once the ZLB is over. After time , the natural rate of interest is positive again. Between times and , the central bank fulfills its forward-guidance promise and keeps the policy rate at zero. After time , monetary policy returns to normal. This scenario is summarized in table 1, panel B.

We analyze the ZLB episode with forward guidance using the phase diagrams in figures 3 and 4. The forward-guidance diagrams are based on the ZLB diagrams in figure 1. In the NK model (figure 3, panel A), the diagram is the same as in panel C of figure 1, except that the Euler line is lower because instead of . In the WUNK model (figure 4, panel A), the diagram is the same as in panel D of figure 1, except that the Euler line (10) is shifted outward because instead of .

The figure describes various ZLB episodes with forward guidance in the NK model. The timeline of such episode is presented in table 1, panel B. Panel A displays the phase diagram of the NK model’s Euler-Phillips system during forward guidance; it is similar to the diagram in figure 1, panel C but with . The equilibrium trajectory during forward guidance is the unique trajectory reaching the natural steady state at time . Panels B, C, and D display the phase diagram of the NK model’s Euler-Phillips system at the ZLB; they comes from figure 1, panel C. The equilibrium trajectory at the ZLB is the unique trajectory reaching the point determined by forward guidance at time . Panels B, C, and D differ in the underlying duration of forward guidance (): short in panel B, medium in panel C, and long in panel D. The figure shows that the NK model suffers from an anomaly: when forward guidance lasts sufficiently to bring above the unstable line, any ZLB episode—however long—triggers a boom (panel D). On the other hand, if forward guidance is short enough to keep below the unstable line, long-enough ZLB episodes are slumps (panel B). In the knife-edge case where falls just on the unstable line, arbitrarily long ZLB episodes converge to the ZLB steady state (panel C).

We begin with the NK model (figure 3). We go backward in time. After time , monetary policy maintains the economy at the natural steady state. Between times and , the economy is in forward guidance (panel A). Following the logic of figure 2, we find that at time , inflation is positive and output above its natural level. They subsequently decrease over time, following the unique trajectory leading to the natural steady state at time . Accordingly, the economy booms during forward guidance. Furthermore, as forward guidance lengthens, inflation and output at time become higher.

We look next at the ZLB episode, between times and . Since equilibrium trajectories are continuous, the economy is at the same point at the end of the ZLB and at the beginning of forward guidance. The boom engineered during forward guidance therefore improves the situation at the ZLB. Instead of reaching the natural steady state at time , the economy reaches a point with positive inflation and above-natural output, so at any time before , inflation and output tend to be higher than without forward guidance (panel B).

Forward guidance can actually have tremendously strong effects in the NK model. For small durations of forward guidance, the position at time is below the ZLB unstable line. It is therefore connected to trajectories coming from the southwest quadrant of the phase diagram (panel B). As the ZLB lasts longer, initial output and inflation collapse. When the duration of forward guidance is such that the position at time is exactly on the unstable line, the position at time is on the unstable line as well (panel C). As the ZLB lasts longer, the initial position inches closer to the ZLB steady state. For even longer forward guidance, the position at time is above the unstable line, so it is connected to trajectories coming from the northeast quadrant (panel D). Then, as the ZLB lasts longer, initial output and inflation become higher and higher. As a result, if the duration of forward guidance is long enough, a deep slump can be transformed into a roaring boom. Moreover, the forward-guidance duration threshold is independent of the ZLB duration.

The figure describes various ZLB episodes with forward guidance in the WUNK model. The timeline of such episode is presented in table 1, panel B. Panel A displays the phase diagram of the WUNK model’s Euler-Phillips system during forward guidance; it is similar to the diagram in figure 1, panel D but with . The equilibrium trajectory during forward guidance is the unique trajectory reaching the natural steady state at time . Panel B displays the phase diagram of the WUNK model’s Euler-Phillips system at the ZLB; it comes from figure 1, panel D. The equilibrium trajectory at the ZLB is the unique trajectory reaching the point determined by forward guidance at time . Panel C is the same as panel B, but with a longer-lasting ZLB (larger ). Panel D is a generic version of panels A, B, and C, describing any duration of ZLB and forward guidance. The figure shows that the NK model’s anomaly disappears in the WUNK model: a long-enough ZLB episode prompts a slump irrespective of the duration of forward guidance (panel C).

In comparison, the power of forward guidance is subdued in the WUNK model (figure 4). Between times and , forward guidance operates (panel A). Inflation is positive and output is above its natural level at time . They then decrease over time, following the trajectory leading to the natural steady state at time . The economy booms during forward guidance; but unlike in the NK model, output and inflation are bounded above by the forward-guidance steady state.

Before forward guidance comes the ZLB episode (panels B and C). Thanks to the boom engineered by forward guidance, the situation is improved at the ZLB: inflation and output tend to be higher than without forward guidance. Yet, unlike in the NK model, output during the ZLB episode is always below its level at time , so forward guidance cannot generate unbounded booms (panel D). The ZLB cannot generate unbounded slumps either, since output and inflation are bounded below by the ZLB steady state (panel D). Actually, for any forward-guidance duration, as the ZLB lasts longer, the economy converges to the ZLB steady state at time . The implication is that forward guidance can never prevent a slump when the ZLB lasts long enough.

Based on these dynamics, we identify an anomaly in the NK model, which is resolved in the WUNK model (proof details in appendix D):

Proposition 4.

Consider a ZLB episode during followed by forward guidance during .

-

•

In the NK model, there exists a threshold such that a forward guidance longer than transforms a ZLB episode of any duration into a boom: let ; for any and for all , and . In addition, when forward guidance is longer than , a long-enough forward guidance or ZLB episode generates an arbitrarily large boom: for any , ; and for any , .

-

•

In the WUNK model, in contrast, there exists a threshold such that a ZLB episode longer than prompts a slump, irrespective of the duration of forward guidance: let ; for any , and . Furthermore, the slump approaches the ZLB steady state as the ZLB duration approaches infinity: for any , and . In addition, the economy is bounded above by the forward-guidance steady state : for any and , and for all , and .

The anomaly identified in the proposition corresponds to the forward-guidance puzzle described by Carlstrom, Fuerst, and Paustian (2015, fig. 1) and Cochrane (2017, fig. 6).101010In the literature the forward-guidance puzzle takes several forms. The common element is that future monetary policy has an implausibly strong effect on current output and inflation. These papers also find that a long-enough forward guidance transforms a ZLB slump into a boom.

In the WUNK model, this anomalous pattern vanishes. In the New Keynesian models by Gabaix (2016), Diba and Loisel (2019), Acharya and Dogra (2019), and Bilbiie (2019), forward guidance also has more subdued effects than in the standard model. Besides, New Keynesian models have been developed with the sole goal of solving the forward-guidance puzzle. Among these, ours belongs to the group that uses discounted Euler equations.111111Other approaches to solve the forward-guidance puzzle include modifying the Phillips curve (Carlstrom, Fuerst, and Paustian 2015), combining reflective expectations and temporary equilibrium (Garcia-Schmidt and Woodford 2019), combining bounded rationality and incomplete markets (Farhi and Werning 2019), and introducing an endogenous liquidity premium (Bredemeier, Kaufmann, and Schabert 2018). For example, Del Negro, Giannoni, and Patterson (2015) generate discounting from overlapping generations; McKay, Nakamura, and Steinsson (2016) from heterogeneous agents facing borrowing constraints and cyclical income risk; Angeletos and Lian (2018) from incomplete information; and Campbell et al. (2017) from government bonds in the utility function (which is closely related to our approach).

Government Spending

Last we consider the effects of government spending at the ZLB. We first extend the model by assuming that the government purchases goods from all households, which are aggregated into public consumption . To ensure that government spending affects inflation and private consumption, we also assume that the disutility of labor is convex: household incurs disutility from working, where is the inverse of the Frisch elasticity. Complete extended model, derivations, and results are presented in appendix E.

In this model, the Euler equation is unchanged, but the Phillips curve is modified because the marginal disutility of labor is not constant, and because households produce goods for the government. The modification of the Phillips curve alters the analysis in three ways.

First, the steady-state Phillips curve becomes nonlinear, which may introduce additional steady states. We handle this issue as in the literature: we linearize the Euler-Phillips system around the natural steady state without government spending, and concentrate on the dynamics of the linearized system. These dynamics are described by phase diagrams similar to those in the basic model.

Second, the slope of the steady-state Phillips curve is modified, so the WUNK assumption needs to be adjusted. Instead of (3), the linearized steady-state Phillips curve is

| (11) |

The WUNK assumption guarantees that at the ZLB, the steady-state Euler equation (with slope ) is steeper than the steady-state Phillips curve (now given by (11)). Hence, we need to replace assumption (9) by

| (12) |

Naturally, for , this assumption reduces to (9).

Third, public consumption enters the Phillips curve, so government spending operates through that curve. Indeed, since in (11), government spending shifts the steady-state Phillips curve upward. Intuitively, given private consumption, an increase in government spending raises production and thus marginal costs. Facing higher marginal costs, producers augment inflation.

The figure describes various ZLB episodes with government spending in the NK model. The timeline of such episode is presented in table 1, panel C. The panels display the phase diagrams of the linearized Euler-Phillips system for the NK model with government spending and convex disutility of labor at the ZLB: is private consumption; is inflation; is the natural level of private consumption; the Euler line is the locus ; the Phillips line is the locus . The phase diagrams have the same properties as that in figure 1, panel C, except that the Phillips line shifts upward when government spending increases (see equation (11)). The equilibrium trajectory at the ZLB is the unique trajectory reaching the natural steady state at time . The four panels feature an increasing amount of government spending (), starting from in panel A. The figure shows that the NK model suffers from an anomaly: when government spending brings down the unstable line from above to below the natural steady state, an arbitrarily long ZLB episode sees an arbitrarily large increase in output, which triggers an unboundedly large boom (from panel B to panel D). On the other hand, if government spending is low enough to keep the unstable line above the natural steady state, long-enough ZLB episodes are slumps (panel B). In the knife-edge case where the natural steady state falls just on the unstable line, arbitrarily long ZLB episodes converge to the ZLB steady state (panel C).

We now study a ZLB episode during which the government increases spending in an effort to stimulate the economy, as in Cochrane (2017). Between times and , there is a ZLB episode. To alleviate the situation, the government provides an amount of public consumption. After time , the natural rate of interest is positive again, government spending stops, and monetary policy returns to normal. This scenario is summarized in table 1, panel C.

We start with the NK model (figure 5).121212There is a small difference with the phase diagrams of the basic model: private consumption is on the horizontal axis instead of output . But in the basic model (government spending is zero), so the phase diagrams with private consumption on the horizontal axis would be the same as those with output. We construct the equilibrium path by going backward in time. At time , monetary policy brings the economy to the natural steady state. At the ZLB, government spending helps, but through a different mechanism than forward guidance. Forward guidance improves the situation at the end of the ZLB, which pulls up the economy during the entire ZLB. Government spending leaves the end of the ZLB unchanged: the economy reaches the natural steady state. Instead, government spending shifts the Phillips line upward, and with it, the field of trajectories. As a result, the natural steady state is connected to trajectories with higher consumption and inflation, which improves the situation during the entire ZLB (panel A versus panel B).

Just like forward guidance, government spending can have very strong effects in the NK model. When spending is low, the natural steady state is below the ZLB unstable line (panel B). It is therefore connected to trajectories coming from the southwest quadrant of the phase diagram—just as without government spending (panel A). Then, if the ZLB lasts longer, initial consumption and inflation fall lower. When spending is high enough that the unstable line crosses the natural steady state, the economy is also on the unstable line at time (panel C). Finally, when spending is even higher, the natural steady state moves above the unstable line, so it is connected to trajectories coming from the northeast quadrant (panel D). As a result, initial output and inflation are higher than previously. And as the ZLB lasts longer, initial output and inflation become even higher, without bound.

The figure describes various ZLB episodes with government spending in the WUNK model. The timeline of such episode is presented in table 1, panel C. The panels display the phase diagrams of the linearized Euler-Phillips system for the WUNK model with government spending and convex disutility of labor at the ZLB: is private consumption; is inflation; is the natural level of private consumption; the Euler line is the locus ; the Phillips line is the locus . The phase diagrams have the same properties as that in figure 1, panel D, except that the Phillips line shifts upward when government spending increases (see equation (11)). The equilibrium trajectory at the ZLB is the unique trajectory reaching the natural steady state at time . The four panels feature an increasing amount of government spending (), starting from in panel A. The figure shows that the NK model’s anomaly disappears in the WUNK model: the government-spending multiplier is finite when the ZLB becomes arbitrarily long-lasting; and equilibrium trajectories are bounded irrespective of the duration of the ZLB.

The power of government spending at the ZLB is much weaker in the WUNK model (figure 6). Government spending does improves the situation at the ZLB, as inflation and consumption tend to be higher than without spending. But as the ZLB lasts longer, the position at the beginning of the ZLB converges to the ZLB steady state—unlike in the NK model, it does not go to infinity. So equilibrium trajectories are bounded, and government spending cannot generate unbounded booms.

Based on these dynamics, we isolate another anomaly in the NK model, which is resolved in the WUNK model (proof details in appendix F):

Proposition 5.

Consider a ZLB episode during , accompanied by government spending . Let and be private consumption and output at time ; let be some incremental government spending; and let

be the government-spending multiplier.

-

•

In the NK model, there exists a government spending such that the government-spending multiplier becomes infinitely large when the ZLB duration approaches infinity: for any , . In addition, when government spending is above , a long-enough ZLB episode generates an arbitrarily large boom: for any , .

-

•

In the WUNK model, in contrast, the multiplier has a finite limit when the ZLB duration approaches infinity: for any and , when , converges to

(13) Moreover, the economy is bounded above for any ZLB duration: let be private consumption in the ZLB steady state with government spending ; for any and for all , .

The anomaly that a finite amount of government spending may generate an infinitely large boom as the ZLB becomes arbitrarily long-lasting is reminiscent of the findings by Christiano, Eichenbaum, and Rebelo (2011, fig. 2), Woodford (2011, fig. 2), and Cochrane (2017, fig. 5). They find that in the NK model government spending is exceedingly powerful when the ZLB is long-lasting.

In the WUNK model, this anomaly vanishes. Diba and Loisel (2019) and Acharya and Dogra (2019) also obtain more realistic effects of government spending at the ZLB. In addition, Bredemeier, Juessen, and Schabert (2018) obtain moderate multipliers at the ZLB by introducing an endogenous liquidity premium in the New Keynesian model.

Other New Keynesian Properties at the ZLB

Beside the anomalous properties described in section 4, the New Keynesian model has several other intriguing properties at the ZLB: the paradoxes of thrift, toil, and flexibility; and a government-spending multiplier greater than one. We now show that the WUNK model shares these properties.

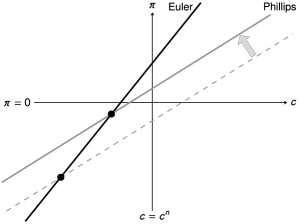

In the NK model these properties are studied in the context of a temporary ZLB episode. An advantage of the WUNK model is that we can simply work with a permanent ZLB episode. We assume that the natural rate of interest is permanently negative, and the central bank keeps the policy rate at zero forever. The only equilibrium is at the ZLB steady state, where the economy is in a slump: inflation is negative and output is below its natural level. The ZLB equilibrium is represented in figure 7: it is the intersection of a Phillips line, describing the steady-state Phillips curve, and an Euler line, describing the steady-state Euler equation. When an unexpected and permanent shock occurs, the economy jumps to a new ZLB steady state; we use the graphs to study such jumps.

Paradox of Thrift

We first study an increase in the marginal utility of wealth (). The steady-state Phillips curve is unaffected, but the steady-state Euler equation changes. Using (5), we rewrite the steady-state Euler equation (10):

Increasing the marginal utility of wealth steepens the Euler line, which moves the economy inward along the Phillips line. Output and inflation therefore decrease (figure 7, panel A). The following proposition gives the results:

Proposition 6.

At the ZLB in the WUNK model, the paradox of thrift holds: an unexpected and permanent increase in the marginal utility of wealth reduces output and inflation but does not affect relative wealth.

The paradox of thrift was first discussed by Keynes, but it also appears in the New Keynesian model (Eggertsson 2010, p. 16; Eggertsson and Krugman 2012, p. 1486). When the marginal utility of wealth is higher, people want to increase their wealth holdings relative to their peers, so they favor saving over consumption. But in equilibrium, relative wealth is fixed at zero because everybody is the same; the only way to increase saving relative to consumption is to reduce consumption. In normal times, the central bank would offset this drop in aggregate demand by reducing nominal interest rates. This is not an option at the ZLB, so output falls.

The figure describes four comparative statics of the WUNK model at the ZLB. In panels A, B, and C, the Euler and Phillips lines are the same as in figure 1, panel D. In panel D, the Euler and Phillips lines are the same as in figure 6. The ZLB equilibrium is at the intersection of the Euler and Phillips lines: output/consumption is below its natural level and inflation is negative. Panel A illustrates the paradox of thrift: increasing the marginal utility of wealth steepens the Euler line, which depresses output and inflation without changing relative wealth. Panel B illustrates the paradox of toil: reducing the disutility of labor moves the Phillips line outward, which depresses output, inflation, and hours worked. Panel C illustrates the paradox of flexibility: decreasing the price-adjustment cost rotates the Phillips line counterclockwise around the natural steady state, which depresses output and inflation. Panel D shows that the government-spending multiplier is above one: increasing government spending shifts the Phillips line upward, which raises private consumption and therefore increases output more than one-for-one.

Paradox of Toil

Next we consider a reduction in the disutility of labor (). In this case, the steady-state Phillips curve changes while the steady-state Euler equation does not. Using (2), we rewrite the steady-state Phillips curve (3):

Reducing the disutility of labor flattens the Phillips line, which moves the economy inward along the Euler line. Thus, both output and inflation decrease (figure 7, panel B). Since hours worked and output are related by , hours fall as well. The following proposition states the results:

Proposition 7.

At the ZLB in the WUNK model, the paradox of toil holds: an unexpected and permanent reduction in the disutility of labor reduces output, inflation, and hours worked.

The paradox of toil was discovered by Eggertsson (2010, p. 15) and Eggertsson and Krugman (2012, p. 1487). It operates as follows. With lower disutility of labor, real marginal costs are lower, and the natural level of output is higher: producers would like to sell more. To increase sales, they reduce their prices by reducing inflation. At the ZLB, nominal interest rates are fixed, so the decrease in inflation raises real interest rates—which renders households more prone to save. In equilibrium, this lowers output and hours worked.131313An increase in technology () would have the same effect as a reduction in the disutility of labor: it would lower output, inflation, and hours.

Paradox of Flexibility

We then examine a decrease in the price-adjustment cost (). The steady-state Euler equation is not affected, but the steady-state Phillips curve is. Equation (3) shows that decreasing the price-adjustment cost leads to a counterclockwise rotation of the Phillips line around the natural steady state. This moves the economy downward along the Euler line, so output and inflation decrease (figure 7, panel C). The following proposition records the results:

Proposition 8.

At the ZLB in the WUNK model, the paradox of flexibility holds: an unexpected and permanent decrease in price-adjustment cost reduces output and inflation.

The paradox of flexibility was discovered by Werning (2011, pp. 13–14) and Eggertsson and Krugman (2012, pp. 1487–1488). Intuitively, with a lower price-adjustment cost, producers are keener to adjust their prices to bring production closer to the natural level of output. Since production is below the natural level at the ZLB, producers are keener to reduce their prices to stimulate sales. This accentuates the existing deflation, which translates into higher real interest rates. As a result, households are more prone to save, which in equilibrium depresses output.

Above-One Government-Spending Multiplier

We finally look at an increase in government spending (), using the model with government spending introduced in section 4.3. From (11) we see that increasing government spending shifts the Phillips line upward, which moves the economy upward along the Euler line: both private consumption and inflation increase (figure 7, panel D). Since private consumption increases when public consumption does, the government-spending multiplier is greater than one. The ensuing proposition gives the results (proof details in appendix F):

Proposition 9.

At the ZLB in the WUNK model, an unexpected and permanent increase in government spending raises private consumption and inflation. Hence the government-spending multiplier is above one; its value is given by (13).

Christiano, Eichenbaum, and Rebelo (2011), Eggertsson (2011), and Woodford (2011) also show that at the ZLB in the New Keynesian model, the government-spending multiplier is above one. The intuition is the following. With higher government spending, real marginal costs are higher for a given level of sales to households. Producers pass the cost increase through into prices, which raises inflation. At the ZLB, the increase in inflation lowers real interest rates—as nominal interest rates are fixed—which deters households from saving. In equilibrium, this leads to higher private consumption and a multiplier above one.

Empirical Assessment of the WUNK Assumption

In the WUNK model, the marginal utility of wealth is assumed to be high enough that the steady-state Euler equation is steeper than the steady-state Phillips curve at the ZLB. We assess this assumption using US evidence.

As a first step, we re-express the WUNK assumption in terms of estimable statistics. We obtain the following condition (derivations in appendix G):

| (14) |

where is the time discount rate, is the average natural rate of interest, and is the coefficient on output gap in a New Keynesian Phillips curve. The term measures the marginal rate of substitution between wealth and consumption, . It indicates how high the marginal utility of wealth is and thus how steep the steady-state Euler equation is at the ZLB. The term indicates how steep the steady-state Phillips curve is. The comes from the denominator of the slopes of the Phillips curves (3) and (11); the measures the rest of the slope coefficients. Condition (14) is expressed in terms of sufficient statistics, so it applies both when the disutility of labor is linear (in which case it is equivalent to (9)) and when the disutility of labor is convex (in which case it is equivalent to (12)). We now survey the literature to obtain estimates of , , and .

Natural Rate of Interest

A large number of macroeconometric studies have estimated the natural rate of interest, using different statistical models, methodologies, and data. Recent studies obtain comparable estimates of the natural rate for the United States: around per annum on average between 1985 and 2015 (Williams 2017, fig. 1). Accordingly, we use as our estimate.

Output-Gap Coefficient in the New Keynesian Phillips Curve

Many studies have estimated New Keynesian Phillips curves. Mavroeidis, Plagborg-Moller, and Stock (2014, sec. 5) offer a synthesis for the United States. They generate estimates of the New Keynesian Phillips curve using an array of US data, methods, and specifications found in the literature. They find significant uncertainty around the estimates, but in many cases the output-gap coefficient is positive and very small. Overall, their median estimate of the output-gap coefficient is (table 5, row 1), which we use as our estimate.

Time Discount Rate

Since the 1970s, many studies have estimated time discount rates using field and laboratory experiments and real-world behavior. Frederick, Loewenstein, and O’Donoghue (2002, table 1) survey 43 such studies. The estimates are quite dispersed, but the majority of them points to high discount rates, much higher than prevailing market interest rates. We compute the mean estimate in each of the studies covered by the survey, and then compute the median value of these means. We obtain an annual discount rate of .

There is one immediate limitation with the studies discussed by Frederick, Loewenstein, and O’Donoghue: they use a single rate to exponentially discount future utility. But exponential discounting does not describe reality well because people seem to choose more impatiently for the present than for the future—they exhibit present-focused preferences (Ericson and Laibson 2019). Recent studies have moved away from exponential discounting and allowed for present-focused preferences, including quasi-hyperbolic (-) discounting. Andersen et al. (2014, table 3) survey 16 such studies, concentrating on experimental studies with real incentives. We compute the mean estimate in each study and then the median value of these means; we obtain an annual discount rate of . Accordingly, even after accounting for present-focus, time discounting remains high. We use as our estimate.141414There are two potential issues with the experiments discussed in Andersen et al. (2014). First, many are run with university students instead of subjects representative of the general population. There does not seem to be systematic differences in discounting between student and non-student subjects, however (Cohen et al. 2019, sec. 6A). Hence, using students is unlikely to bias the estimates reported by Andersen et al.. Second, all the experiments elicit discount rates using financial flows, not consumption flows. As the goal is to elicit the discount rate on consumption, this could be problematic (Cohen et al. 2019, sec. 4B); the problems could be exacerbated if subjects derive utility from wealth. To assess this potential issue, suppose first (as in most of the literature) that monetary payments are consumed at the time of receipt, and that the utility function is locally linear. Then the experiments deliver estimates of the relevant discount rate (Cohen et al. 2019, sec. 4B). If these conditions do not hold, the experimental findings are more difficult to interpret. For instance, if subjects optimally smooth their consumption over time by borrowing and saving, then the experiments only elicit the interest rate faced by subjects, and reveal nothing about their discount rate (Cohen et al. 2019, sec. 4B). In that case, we should rely on experiments using time-dated consumption rewards instead of monetary rewards. Such experiments directly deliver estimates of the discount rate. Many such experiments have been conducted; a robust finding is that discount rates are systematically higher for consumption rewards than for monetary rewards (Cohen et al. 2019, sec. 3A). Hence, the estimates presented in Andersen et al. are, if anything, lower bounds on actual discount rates.

Assessment

We now combine our estimates of , , and to assess the WUNK assumption. Since is estimated using quarters as units of time, we re-express and as quarterly rates: per quarter, and per quarter. We conclude that (14) comfortably holds: , which is much larger than . Hence the WUNK assumption holds in US data.

The discount rate used here (43% per annum) is much higher than discount rates used in macroeconomic models (typically less than 5% per annum). This is because our discount rate is calibrated from microevidence, while the discount rate in macroeconomic models is calibrated to match observed real interest rates.

This discrepancy occasions two remarks. First, the wealth-in-the-utility assumption is advantageous because it accords with the fact that people exhibit double-digit time discount rates and yet are willing to save at single-digit interest rates. In the standard model, by contrast, the discount rate necessarily equals the real interest rate in steady state, so the model cannot have .

Second, the WUNK assumption would also hold with discount rates below 43%. Indeed, (14) holds for discount rates as low as 27% because is greater than . An annual discount rate of 27% is at the low end of available microestimates: in 11 of the 16 studies in Andersen et al. (2014, table 3), the bottom of the estimate range is above 27%; and in 13 of the 16 studies, the mean estimate is above 27%.

Finally, while our model omits firms and assumes that households are both producers and consumers, in reality firms and households are often separate entities that could have different discount rates. With different discount rates, (14) would become

where is households’ discount rate and is firms’ discount rate. Clearly, if firms have a low discount rate, the WUNK assumption is less likely to be satisfied. If we use , , and , we find that the WUNK condition holds as long as firms have an annual discount rate above 16% because is greater than . A discount rate of 16% is only slightly above that reported by large US firms: in a survey of 228 CEOs, Poterba and Summers (1995) find an average annual real discount rate of 12.2%; and in a survey of 86 CFOs, Jagannathan et al. (2016, p. 447) find an average annual real discount rate of 12.7%.

Conclusion

This paper proposes an extension of the New Keynesian model that is immune to the anomalies that plague the standard model at the ZLB. The extended model deviates only minimally from the standard model: relative wealth enters the utility function, which only adds an extra term in the Euler equation. Yet, when the marginal utility of wealth is sufficiently high, the model behaves well at the ZLB: even when the ZLB is long-lasting, there is no collapse of inflation and output, and both forward guidance and government spending have limited, plausible effects. The extended model also retains other properties of the standard model at the ZLB: the paradoxes of thrift, toil, and flexibility; and a government-spending multiplier greater than one.

Our analysis would apply more generally to any New Keynesian model representable by a discounted Euler equation and a Phillips curve (for example, Del Negro, Giannoni, and Patterson 2015; Gabaix 2016; McKay, Nakamura, and Steinsson 2017; Campbell et al. 2017; Beaudry and Portier 2018; Angeletos and Lian 2018). Wealth in the utility function is a simple way to generate discounting; but any model with discounting would have similar phase diagrams and properties. Hence, for such models to behave well at the ZLB, there is only one requirement: that discounting is strong enough to make the steady-state Euler equation steeper than the steady-state Phillips curve at the ZLB; the source of discounting is unimportant. In the real world, several discounting mechanisms might operate at the same time and reinforce each other. A model blending these mechanisms would be even more likely to behave well at the ZLB.

References

- (1)

- Acemoglu (2009) Acemoglu, Daron. 2009. Introduction to Modern Economic Growth. Princeton, NJ: Princeton University Press.

- Acharya and Dogra (2019) Acharya, Sushant, and Keshav Dogra. 2019. “Understanding HANK: Insights from a PRANK.” https://perma.cc/E5JY-HL55.

- Andersen et al. (2014) Andersen, Steffen, Glenn W. Harrison, Morten I. Lau, and E. Elisabet Rutstrom. 2014. “Discounting Behavior: A Reconsideration.” European Economic Review 71: 15–33.

- Anderson, Hildreth, and Howland (2015) Anderson, Cameron, John A.D. Hildreth, and Laura Howland. 2015. “Is the Desire for Status a Fundamental Human Motive? A Review of the Empirical Literature.” Psychological Bulletin 141 (3): 574–601.

- Angeletos and Lian (2018) Angeletos, George-Marios, and Chen Lian. 2018. “Forward Guidance without Common Knowledge.” American Economic Review 108 (9): 2477–2512.

- Bakshi and Chen (1996) Bakshi, Gurdip S., and Zhiwu Chen. 1996. “The Spirit of Capitalism and Stock-Market Prices.” American Economic Review 86 (1): 133–157.

- Beaudry and Portier (2018) Beaudry, Paul, and Franck Portier. 2018. “Real Keynesian Models and Sticky Prices.” NBER Working Paper 24223.

- Benhabib, Schmitt-Grohe, and Uribe (2001) Benhabib, Jess, Stephanie Schmitt-Grohe, and Martin Uribe. 2001. “The Perils of Taylor Rules.” Journal of Economic Theory 96 (1-2): 40–69.

- Bilbiie (2019) Bilbiie, Florin O. 2019. “Heterogeneity and Determinacy: An Analytical Framework.” CEPR Discussion Paper 12601.

- Blanchard and Fischer (1989) Blanchard, Olivier J., and Stanley Fischer. 1989. Lectures on Macroeconomics. Cambridge, MA: MIT Press.

- Bredemeier, Juessen, and Schabert (2018) Bredemeier, Christian, Falko Juessen, and Andreas Schabert. 2018. “Fiscal Multipliers and Monetary Policy: Reconciling Theory and Evidence.” https://perma.cc/6ZER-P2UD.

- Bredemeier, Kaufmann, and Schabert (2018) Bredemeier, Christian, Christoph Kaufmann, and Andreas Schabert. 2018. “Interest Rate Spreads and Forward Guidance.” ECB Working Paper 2186.

- Calvo (1983) Calvo, Guillermo A. 1983. “Staggered Prices in a Utility-Maximizing Framework.” Journal of Monetary Economics 12 (3): 383–398.

- Camerer, Loewenstein, and Prelec (2005) Camerer, Colin, George Loewenstein, and Drazen Prelec. 2005. “Neuroeconomics: How Neuroscience Can Inform Economics.” Journal of Economic Literature 43 (1): 9–64.

- Campbell et al. (2017) Campbell, Jeffrey R., Jonas D.M. Fisher, Alejandro Justiniano, and Leonardo Melosi. 2017. “Forward Guidance and Macroeconomic Outcomes Since the Financial Crisis.” In NBER Macroeconomics Annual 2016, edited by Martin Eichenbaum and Jonathan A. Parker, chap. 4. Chicago: University of Chicago Press.

- Carlstrom, Fuerst, and Paustian (2015) Carlstrom, Charles T., Timothy S. Fuerst, and Matthias Paustian. 2015. “Inflation and Output in New Keynesian Models with a Transient Interest Rate Peg.” Journal of Monetary Economics 76: 230–243.

- Carroll (2000) Carroll, Christopher D. 2000. “Why Do the Rich Save So Much?” In Does Atlas Shrug? The Economic Consequences of Taxing the Rich, edited by Joel B. Slemrod. Cambridge, MA: Harvard University Press.

- Cheng and Tracy (2013) Cheng, Joey T., and Jessica L. Tracy. 2013. “The Impact of Wealth on Prestige and Dominance Rank Relationships.” Psychological Inquiry 24 (2): 102–108.

- Christiano, Eichenbaum, and Rebelo (2011) Christiano, Lawrence, Martin Eichenbaum, and Sergio Rebelo. 2011. “When Is the Government Spending Multiplier Large?.” Journal of Political Economy 119 (1): 78–121.

- Clemens (2004) Clemens, Christiane. 2004. “Status, Risk-Taking and Intertemporal Substitution in an Endogenous Growth Model.” Journal of Economics 83 (2): 103–123.

- Cochrane (2017) Cochrane, John H. 2017. “The New-Keynesian Liquidity Trap.” Journal of Monetary Economics 92: 47–63.

- Cochrane (2018) Cochrane, John H. 2018. “Michelson-Morley, Fisher, and Occam: The Radical Implications of Stable Quiet Inflation at the Zero Bound.” In NBER Macroeconomics Annual 2017, edited by Martin Eichenbaum and Jonathan A. Parker, chap. 2. Chicago: University of Chicago Press.

- Cohen et al. (2019) Cohen, Jonathan D., Keith M. Ericson, David Laibson, and John M. White. 2019. “Measuring Time Preferences.” Journal of Economic Perspectives forthcoming.

- Cole, Mailath, and Postlewaite (1992) Cole, Harold L., George J. Mailath, and Andrew Postlewaite. 1992. “Social Norms, Savings Behavior, and Growth.” Journal of Political Economy 100 (6): 1092–1125.

- Cole, Mailath, and Postlewaite (1995) Cole, Harold L., George J. Mailath, and Andrew Postlewaite. 1995. “Incorporating Concern for Relative Wealth Into Economic Models.” Quarterly Review 19 (3): 12–21.

- Corneo and Jeanne (1997) Corneo, Giacomo, and Olivier Jeanne. 1997. “On Relative Wealth Effects and the Optimality of Growth.” Economics Letters 54 (1): 87–92.

- Del Negro, Giannoni, and Patterson (2015) Del Negro, Marco, Marc P. Giannoni, and Christina Patterson. 2015. “The Forward Guidance Puzzle.” Federal Reserve Bank of New York Staff Report 574.

- Diba and Loisel (2019) Diba, Behzad, and Olivier Loisel. 2019. “Pegging the Interest Rate on Bank Reserves: A Resolution of New Keynesian Puzzles and Paradoxes.” https://perma.cc/U6RL-7PDM.