Machine Learning for Pricing American Options in High-Dimensional Markovian and non-Markovian models

Abstract

In this paper we propose two efficient techniques which allow one to compute the price of American basket options. In particular, we consider a basket of assets that follow a multi-dimensional Black-Scholes dynamics. The proposed techniques, called GPR Tree (GRP-Tree) and GPR Exact Integration (GPR-EI), are both based on Machine Learning, exploited together with binomial trees or with a closed formula for integration. Moreover, these two methods solve the backward dynamic programming problem considering a Bermudan approximation of the American option. On the exercise dates, the value of the option is first computed as the maximum between the exercise value and the continuation value and then approximated by means of Gaussian Process Regression. The two methods mainly differ in the approach used to compute the continuation value: a single step of binomial tree or integration according to the probability density of the process. Numerical results show that these two methods are accurate and reliable in handling American options on very large baskets of assets. Moreover we also consider the rough Bergomi model, which provides stochastic volatility with memory. Despite this model is only bidimensional, the whole history of the process impacts on the price, and handling all this information is not obvious at all. To this aim, we present how to adapt the GPR-Tree and GPR-EI methods and we focus on pricing American options in this non-Markovian framework.

Keywords: Machine Learning, American Options, Multi-dimensional Black-Scholes Model, Rough Bergomi Model, Binomial Tree Method, Exact Integration.

1 Introduction

Pricing American options is clearly a crucial question of finance but also a challenging one since computing the optimal exercise strategy is not an evident task. This issue is even more exacting when the underling of the option is a multi-dimensional process, such as a baskets of assets, since in this case the direct application of standard numerical schemes, such as finite difference or tree methods, is not possible because of the exponential growth of the calculation time and the required working memory.

Common approaches in this field can be divided in four groups: techniques which rely on recombinant trees to discretize the underlyings (see [4], [11] and [24]), techniques which employ regression on a truncated basis of in order to compute the conditional expectations (see [28] and [32]), techniques which exploit Malliavin calculus to obtain representation formulas for the conditional expectation (see [1], [3], [9], and [27]) and techniques which make use of duality-based approaches for Bermudan option pricing (see [21], [26] and [31]).

Recently, Machine Learning algorithms (Rasmussen and Williams [33]) and Deep Learning techniques (Nielsen [30]) have found great application in this sector of option pricing.

Neural networks are used by Kohler et al. [25] to price American options based on several underlyings. Deep Learning techniques are nowadays widely used in solving large differential equations, which is intimately related to option pricing. In particular, Han et al. [20] introduce a Deep Learning-based approach that can handle general high-dimensional parabolic PDEs. E et al. [14] propose an algorithm for solving parabolic partial differential equations and backward stochastic differential equations in high dimension. Beck et al. [7] introduce a method for solving high-dimensional fully nonlinear second-order PDEs. As far as American options in high dimension are concerned, Becker et al. [8] develop a Deep Learning method for optimal stopping problems which directly learns the optimal stopping rule from Monte Carlo samples.

Also Machine Learning techniques have made their contribution. For example, Dixon and Crépey present a multi-Gaussian process regression for estimating portfolio risk, and in particular the associated CVA. De Spiegeleer et al. [13] propose to apply Gaussian Process Regression (GPR) to predict the price of the derivatives from a training set made of observed prices for particular combinations of model parameters. Ludkovski [29] proposes to use GPR meta-models for fitting the continuation values of Bermudan options. Similarly, GoudenÚge et al. [18] propose the GPR-MC, which is a backward induction algorithm that employs Monte Carlo simulations and GPR to compute the price of American options in very high dimension (up to 100). In the insurance context, Gan [16] studies the pricing of a large portfolio of Variable Annuities in the Black-Scholes model by using clustering and GPR. Moreover, Gan and Lin [17] propose a novel approach that combines clustering technique and GPR to efficiently evaluate policies considering nested simulations.

In this paper we present two numerical techniques which upgrade the GPR-MC approach by replacing the Monte Carlo based computation of the continuation value respectively with a tree step and with an exact integration step. In particular, the algorithms we propose proceed backward over time and compute the price function only on a set of predetermined points. At each time step, a binomial tree step or a closed formula for integration are used together with GPR to approximate the continuation value at these points. The option price is then obtained as the maximum between the continuation value and the intrinsic value of the option and the algorithms proceed backward. For the sake of simplicity, we name these new approaches Gaussian Process Regression - Tree (GPR-Tree) and Gaussian Process Regression - Exact Integration (GPR-EI). We observe that the use of the GPR method to extrapolate the option value is particularly efficient in terms of computing time with respect to other techniques such as Neural Networks, especially because a small dataset is considered here. Moreover, Le Gratiet et Garnier [19] developed recent convergence results about GPR, extending the outcomes of Rasmussen and Williams [33], and founding the convergence rate when different kernels are employed.

In order to demonstrate the wide applicability of the GPR methods, we also consider the rough Bergomi model, which is a non-Markovian model with stochastic volatility. Such a model, introduced by Bayer et al. [5] stood out for explaining implied volatility smiles and other phenomena in the pricing of European options. The non-Markovian property of the model makes it difficult to implement a methodologically correct approach to address the valuation of American options. The literature in this framework is really poor. Horvat et al. [23] propose an approach based on Donsker’s approximation for fractional Brownian motion and on a tree with exponential complexity. More recently, Bayer et al. [6] introduce a method based on Monte Carlo simulation and exercise Rate Optimization.

Numerical results show that both the GPR-Tree and the GPR-EI methods are accurate and reliable in the multi-dimensional Black-Scholes model. Moreover the computational times with respect to the GPR-MC method are improved. The GPR-Tree and the GPR-EI methods prove its accuracy also when applied to the rough Bergomi model.

The reminder of the paper is organized as follows. Section 2 presents American options in the multi-dimensional Black-Scholes model. Section 3 and Section 4 introduce the GPR-Tree and the GPR-EI methods for the multi-dimensional Black-Scholes model respectively. Section 5 presents the American options in the rough Bergomi model. Section 6 and Section 7 introduce the GPR-Tree and the GPR-EI methods for the rough Bergomi model. Section 8 reports some numerical results. Section 9 draws some conclusions.

2 American options in the multi-dimensional Black-Scholes model

An American option with maturity is a derivative instrument whose holder can exercise the intrinsic optionality at any moment before maturity. Let denote the -dimensional underlying process, which is supposed to randomly evolve according to the multi-dimensional Black-Scholes model: under the risk neutral probability, such a model is given by the following equation

| (2.1) |

with the spot price, the (constant) interest rate, the vector of volatilities, a -dimensional correlated Brownian motion and the instantaneous correlation coefficient between and Moreover, let denote the cash-flow associated with the option at maturity . Thus, the price at time of an American option having maturity and payoff function is then

| (2.2) |

where stands for the set of all the stopping times taking values on and represents the expectation given all the information at time and in particular assuming .

For simulation purposes, the dimensional Black-Scholes model can be written alternatively using the Cholesky decomposition. Specifically, for we can write

| (2.3) |

where is a -dimensional uncorrelated Brownian motion and is the -th row of the matrix defined as a square root of the correlation matrix , given by

| (2.4) |

3 The GPR-Tree method in the multi-dimensional Black-Scholes model

The GPR-Tree method is similar to the GPR-MC method but the diffusion of the underlyings is performed through a step of a binomial tree. In particular, the algorithm proceeds backward over time, approximating the price of the American option with the price of a Bermudan option on the same basket. At each time step, the price function is evaluated only on a set of predetermined points, through a binomial tree step together with GPR to approximate the continuation value. Finally, the optionality is exploited by computing the option value as the maximum between the continuation value and the exercise value.

Let denote the number of time steps, be the time increment and represent the discrete exercise dates for . At any exercise date , the value of the option is determined by the vector of the underlying prices as follows:

| (3.1) |

where denotes the continuation value of the option and it is given by the following relation:

| (3.2) |

We observe that, if the function is known, then it is possible to compute by approximating the expectation in (3.2). In order to obtain such an approximation, we consider a set of points whose elements represent certain possible values for the underlyings :

| (3.3) |

where . Such a set is determined as done by GoudenÚge et al. [18], that is the elements of are obtained through a quasi-random simulation of based on the Halton sequence (see [18] for more details).

The GPR-Tree method assesses for each through one step of the binomial tree proposed by Ekval [15]. In particular, for each , we consider a set of possible values for

| (3.4) |

which are computed as follows:

| (3.5) |

being the -th point of the space . In particular, if is the vector whose components are the digits of the binary representation of , then . It is worth noticing that, as pointed out in [15], the elements of are equally likely and this simplifies the evaluation of the expected value to the computation of the arithmetic mean of the future values. Using the tree step, the price function may be approximated by

| (3.6) |

The computation in (3.6) can be performed only if the quantities are known for all the future points . If we proceed backward, the function is known at maturity since it is given by the payoff function and so (3.6) can be computed at and for all the points of . In order to compute for all , and thus going on up to , we have to evaluate the function for all the points in , but we only know at . To overcome this issue, we employ the GPR method to approximate the function at any point of and in particular at the elements of . Specifically, let denote the GPR prediction of , obtained by considering the predictor set and the response given by

| (3.7) |

The GPR-Tree approximation of the value function at time can be computed as follows:

| (3.8) |

Following the same steps, the dynamic programming problem can be solved. Specifically, let and let denote the GPR prediction of obtained from predictor set and the response given by

| (3.9) |

Then, the function can be obtained as

| (3.10) |

4 The GPR-EI method in the multi-dimensional Black-Scholes model

The GPR-EI method differs from both the GPR-MC and GPR-Tree methods for two reasons. First of all, the predictors employed in the GPR step are related to the logarithms of the predictors used in the GPR-Tree method. Secondly, the continuation value at these points is computed through a closed formula which comes from an exact integration.

Let be the same set as in (3.3) and define as the vector obtained by applying the natural logarithm to all the components of , that is . Moreover, let us define the set

| (4.1) |

In this case, we do not work directly with the function , but we rather consider the function defined as

| (4.2) |

In a nutshell, the main idea is to approximate the function at by using the GPR method on the fixed grid . In particular, we employ the Squared Exponential Kernel , which is given by

| (4.3) |

where the identity matrix, is the characteristic length scale and is the signal standard deviation. These two parameters are obtained by means of a maximum likelihood estimation. The GPR approach allows one to approximate the function at time by

| (4.4) |

where are weights that are computed by solving a linear system. The continuation value can be computed by integrating the function against a -dimensional probability density. This calculation can be done easily by means of a closed formula.

Specifically, the GPR-EI method relies on the following Proposition.

Proposition 1.

Let and suppose the function at time to be known at . The GPR-EI approximation of the option value at time at is given by

| (4.5) |

, , and are certain constants determined by the GPR approximation of the function for , considering as the predictor set, and is the covariance matrix of the log-increments defined by .

The proof of Proposition 1 is reported in the Appendix A. Equation (4.5) allows one to compute the option price at time by proceeding backward. In fact, the function is known at time throught (4.2) since the price function is equal to the payoff function . Moreover, if an approximation of is available, then one can approximate at by means of relation (4.5). Finally, the option price at time is approximated by .

5 American options in the rough Bergomi model

The rough Bergomi model, introduced by Bayer et al. [5], shapes the underlying process and its volatility through the following relations:

| (5.1) | ||||

| (5.2) |

with the (constant) interest rate, a positive parameter and the Hurst parameter. The deterministic function represents the forward variance curve and following Bayer et al. [5] we consider it as constant. The process is a Brownian motion, whereas is a Riemann-Liouville fractional Brownian motion that can be expressed as a stochastic integral:

| (5.3) |

with a Brownian motion and the instantaneous correlation coefficient between and .

The rough Bergomi model stood out for its ability to explain implied volatility and other phenomena related to European options. Moreover, it is particularly interesting from a computational point of view as it is a non-Markovian model and therefore it is not possible to apply standard techniques for American options.

In this framework, the price at time of an American option having maturity and payoff function is then

| (5.4) |

where is the natural filtration generated by the couple for . We point out that, as opposed to the multi-dimensional Brownian motion, in this case, the stopping time does not only depend from the actual values of and but, since these are non-Markovian processes, it depends on the whole filtration, that is from the whole observed history of the processes.

6 The GPR-Tree method in the rough Bergomi model

The GPR-Tree method can be adapted to price American options in the rough Bergomi model. Despite the dimension of the model is only two, it is a non-Markovian model which obliges one to take into account the past history when evaluating the price of an option. So, the price of an option at a certain moment depends on all the filtration at that moment. Clearly, evaluating an option by considering the whole history of the process (a continuous process) is not possible. To overcome such an issue, we simulate the process on a finite number of dates and we consider the sub-filtration induced by these observations. First of all, we consider a finite number of time steps that determines the time increment , and we employ the scheme presented in Bayer et. al [5] to generate a set of simulations of the couple at for . In particular, if we set , then the -dimensional random vector , given by

| (6.1) |

follows a zero-mean Gaussian distribution. Moreover, using the relations stated in Appendix B, one can calculate the covariance matrix of and its lower triangular square root by using the Cholesky factorization. The vector can be simulated by computing , where is a vector of independent standard Gaussian random variables. Finally, a simulation for can be obtained from by considering the initial values

| (6.2) |

and the Euler–Maruyama scheme given by

| (6.3) | ||||

| (6.4) |

First of all, the GPR-Tree method simulates different samples for the vector , namely for , and it computes the corresponding paths according to (6.2), (6.3) and (6.4). To summarize the values assumed by and , let us define the vector

| (6.5) |

for and . Moreover, we also define

| (6.6) |

where stands for the natural logarithm.

Then, the GPR-Tree method computes the option value for each of these trajectories, proceeding backward in time and considering the past history coded into the filtration. Since we consider only a finite number of steps, we approximate the filtration with the natural filtration generated by the variables . Moreover, is equal to the filtration generated by because there exists a deterministic bijective function that allows one to obtain from and vice versa. Therefore, when we calculate the option value conditioned by filtration , it is enough to conditioning with respect to the knowledge of the variables .

The GPR-Tree method proceeds backward in time, using a tree method and the GPR to calculate the option price with respect to the initially simulated trajectories. As opposed to the multi-dimensional Black-Scholes model, here we perform more than one single tree step, so as to reduce the number of GPR regressions and thus increasing the computational efficiency. In particular, we consider with and natural numbers that represent how many times the tree method is used and the number of time steps employed, respectively.

After simulating the random paths , we compute the tree approximation of the option value at time for each path as follows:

| (6.7) |

with stands for the the approximation of the continuation value function at time obtained by means of a tree approach, which discretizes each component of the Gaussian vector that generates the process. As opposed to the multi-dimensional Black-Scholes model, the approximation of the independent Gaussian components of through the equiprobable couple is not suitable since the convergence to the right price is too slow. So, we propose to use the same discrete approximation employed by Alfonsi in [2], which is stated in the following Lemma.

Lemma 2.

The discrete variable defined by and fits the first seven moments of a standard Gaussian random variable.

So, for each path , we consider a quadrinomial tree with time steps, and we use it to compute the continuation value. In particular, we consider the discrete time process defined through

| (6.8) |

| (6.9) | ||||

| (6.10) |

where is the -th rows of the matrix and the -th row. Moreover, for and the other components, that is for , are sampled by using the random variable of Lemma 2.

An option value is assigned to each node of the tree: at maturity, that is for it is equal to the payoff , and for it can be obtained as the maximum between the exercise value and the discounted mean value at the future nodes, weighted according to the transition probabilities determined by the probability distribution of .

This approach allows us to compute the function for . We point out that, since the quadrinomial tree is not recombinant, the number of nodes grows exponentially with the number of time steps . Therefore, must be small. A similar problem arises with the tree approach proposed by Horvat et al. [23]. In order to overcome such an issue, we apply the GPR method to approximate the function . Specifically, consider a natural number and define . We train the GPR method considering the predictor set given by

| (6.11) |

and the response given by

| (6.12) |

We term the function obtained by the aforementioned regression, which depends on . We stress out that if we consider (or greater), then the function would consider all the observed values of and as predictors. Anyway, numerical tests show that it is enough to consider smaller values of , which reduces the dimension of the regression and thus improves the numerical efficiency. A similar approach is taken by Bayer et al. [6].

Once we have obtained , we can approximate the option value at time by means of the tree approach again. The only difference in this case is that the value attributed to the terminal nodes is not determined by the payoff function, but through the function . We term the function obtained after this backward tree step. If we train the GPR method considering the predictor set given by

| (6.13) |

and the response given by

| (6.14) |

then we obtain the function , which can be employed to repeat the tree step and the GPR step, proceeding backward up to obtaining the initial option price by backward induction.

7 The GPR-EI method in the rough Bergomi model

The GPR-EI method can be adapted to price American options in the rough Bergomi model. Just like the GPR-Tree approach, the GPR-EI method starts by simulating different paths for the processes and , and it goes on by solving a backward induction problem, through the use of the GPR method and a closed formula for integration.

As opposed to the multi-dimensional Black-Scholes model, in the rough Bergomi case the use of the squared exponential kernel is not suitable because it is a isotropic kernel and the predictors employed have different nature (prices and volatilities at different times) and thus changes in each predictor impact differently on the price. So, we employ the Automatic Relevance Determination (ARD) Squared Exponential Kernel, that has separate length scale for each predictor and it is given by

| (7.1) |

with the number of the considered predictors. Specifically, the GPR-EI method relies on the following Propositions.

Proposition 3.

The GPR-EI approximation of the option value at time at is given by:

| (7.2) |

where , , and are certain constants determined by the GPR approximation of the function . Moreover,

| (7.3) |

and

| (7.4) |

The proof of Proposition 3 is reported in the Appendix C. Therefore, we can compute the value of the option at time for each simulated path by using (7.2).

Proposition 4.

Let and suppose the option price function at time to be known for all the simulated paths . Define

| (7.5) |

where is the -th row of the matrix and , and

| (7.6) |

where stands for the element of in position . Moreover, consider a natural number and set Then, the GPR-EI approximation of the option value at time at is given by

| (7.7) |

where , , and are certain constants determined by the GPR approximation of the function considering as the predictor set. Moreover, and are two factors given by

| (7.8) |

and

| (7.9) |

where if is even and if is odd, for .

8 Numerical results

In this Section we present some numerical results about the effectiveness of the proposed algorithms. The first section is devoted to the numerical tests about the multi-dimensional Black-Scholes model, while the second is devoted to the rough Bergomi model. The algorithms have been implemented in MATLAB and computations have been preformed on a server which employs a GHz Intel® Xenon® processor (Gold 6148, Skylake) and 20 GB of RAM.

8.1 Multi-dimensional Black-Scholes model

Following GoudenÚge et al. [18], we consider an Arithmetic basket Put, a Geometric basket Put and a Call on the Maximum of -assets.

In particular, we use the following parameters , , , , constant volatilities , constant correlations and exercise dates. Moreover, we consider or points. As opposed to the other input parameters, we vary the dimension , considering and .

We present now the numerical results obtained with the GPR-Tree and the GPR-EI methods for the three payoff examples.

8.1.1 Geometric basket Put option

Geometric basket Put is a particularly interesting option since it is possible to reduce the problem of pricing it in the -dimensional model to a one dimensional American Put option in the Black-Scholes model which can be priced straightforwardly, for example using the CRR algorithm with steps (see Cox et al. [12]). Therefore, in this case, we have a reliable benchmark to test the proposed methods. Moreover, when is smaller than we can also compute the price by means of a multi-dimensional binomial tree (see Ekvall [15]). In particular, the number of steps employed for the multi-dimensional binomial tree is equal to when and to when . For values of larger than , prices cannot be approximated via such a tree, because the memory required for the calculations would be too large. Furthermore, we also report the prices obtained with the GPR-MC method, employing points and Monte Carlo simulations, for comparison purposes. As far as the GPR-Tree is concerned, we compute the prices only for the values of smaller than since for higher values of the tree step becomes over time demanding. In fact, the computation of the continuation value with the tree step grows exponentially with the dimension and for it requires the evaluation of the GPR approximation at points for every times step and for every point of .

Results are reported in Table 1. We observe that the two proposed methods provide accurate and stable results and the computational time is generally very small, except for the GPR-Tree method at . Moreover, the computer processing time of the GRP-EI method increases little with the size of the problem and this makes the method particularly effective when the dimension of the problem is high. This is because the computation of the expected value and the training of the GPR model are minimally affected by the dimension of the problem.

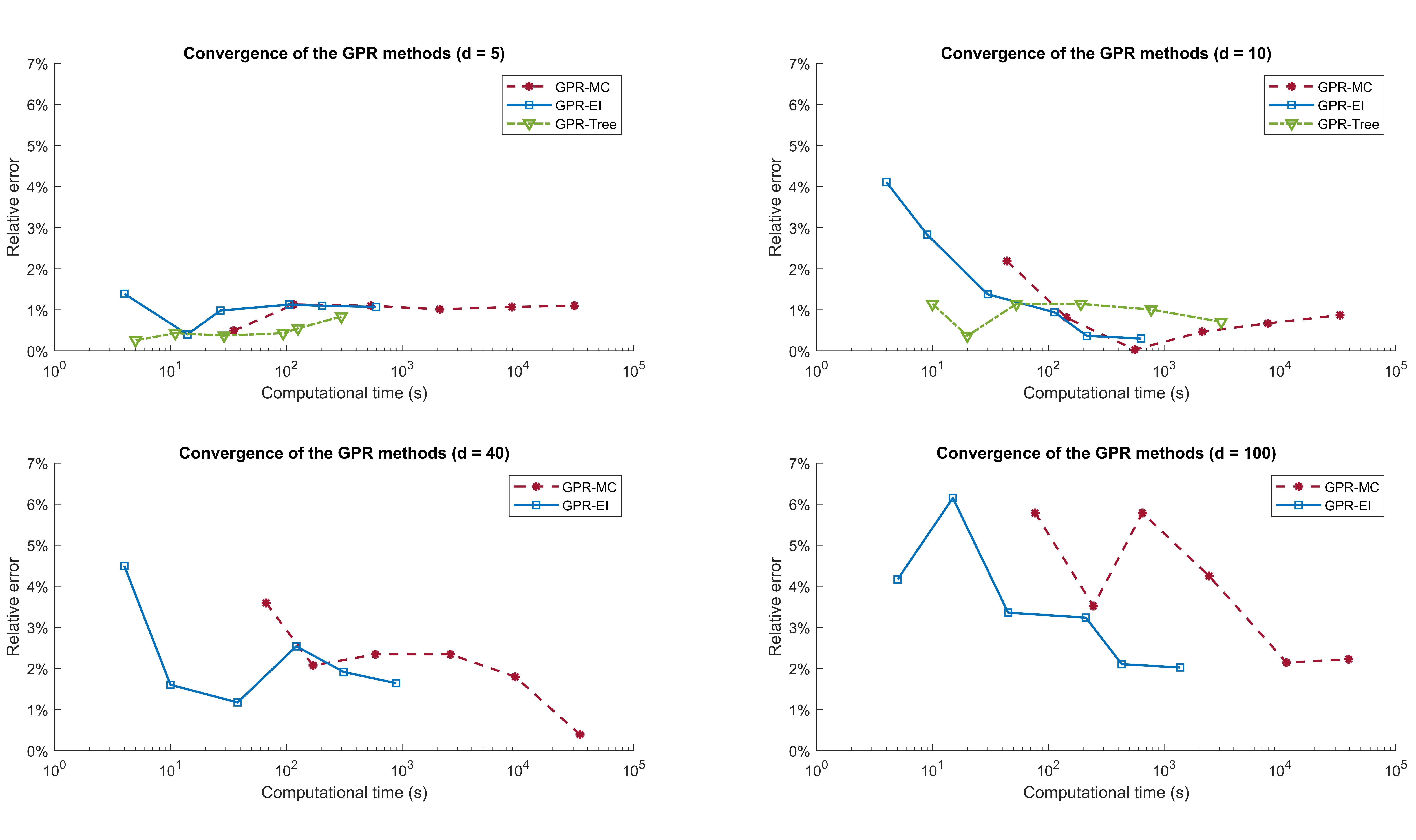

Figure 8.1 investigates the convergence of the GPR methods changing the dimension . As we can see, the relative error is small with all the considered methods, but the computational time required by the GPR-Tree method and the GPR-EI method is generally smaller with respect to the GPR-MC method.

| GPR-Tree | GPR-EI | GPR-MC | Ekvall | Benchmark | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 | |||||||||||||

| 5 | |||||||||||||

| 10 | |||||||||||||

| 20 | |||||||||||||

| 40 | |||||||||||||

| 100 | |||||||||||||

8.1.2 Arithmetic basket Put option

As opposed to the Geometric basket Put option, in this case we have no method to obtain a fully reliable benchmark. Therefore we only consider the prices obtained by means of the GPR-MC method, employed with points and Monte Carlo simulations. Moreover, for small values of , a benchmark can be obtained by means of a multi-dimensional tree method (see Boyle et al. [10]), just as shown for the Geometric case. Results are reported in Table 2. Similarly to the Geometric basket Put, the prices obtained are reliable and they do not change much with respect to the number of points. As opposed to the GPR-Tree method, which can not be applied for high values of , the GPR-EI method requires a small computational time for all the values concerned of .

| GPR-Tree | GPR-EI | GPR-MC | Ekvall | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 | |||||||||||||

| 5 | |||||||||||||

| 10 | |||||||||||||

| 20 | |||||||||||||

| 40 | |||||||||||||

| 100 | |||||||||||||

8.1.3 Call on the Maximum

As for the Arithmetic basket Put, in this case we have no numerical methods to obtain a fully reliable benchmark. However, for small values of , we can approximate the price obtained by means of a multi-dimensional tree method. Moreover, we also consider the price obtained with the GPR-MC method. Results, which are shown in Table 3, have an accuracy comparable to the one obtained for the Arithmetic basket Put option.

| GPR-Tree | GPR-EI | GPR-MC | Ekvall | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 | |||||||||||||

| 5 | |||||||||||||

| 10 | |||||||||||||

| 20 | |||||||||||||

| 40 | |||||||||||||

| 100 | |||||||||||||

8.2 Rough Bergomi model

Following Bayer et al. [6], we consider an American Put option and we use the same parameters: , , , , , , and strike or . As far as the GPR-Tree is concerned, we employ or time steps with , or random paths, and or past values. As far as the GPR-EI is concerned, we employ or time steps, or random paths, and or past values. Similar to what observed by Bayer et al. [6], the difference changing the value of does not impact significantly on the price, which indicates that considering the non-Markovian nature of the processes in the formulation of the exercise strategies is not particularly relevant. Conversely, using a large number of predictors significantly increases computational time. Numerical results are reported in Tables 4 and 5, together with the results reported by Bayer et al. in [6]. Prices are very close to the benchmark, except for the case : in this case with both the two GPR methods we obtain a price which is close to while Bayer et al. obtain . Anyway, it is worth noticing that the relative gap between these two results is less than .

| GPR-Tree | Bayer et al. | |||||||||||||

| 1.88 | ||||||||||||||

| 3.22 | ||||||||||||||

| 5.31 | ||||||||||||||

| 8.50 | ||||||||||||||

| 13.23 | ||||||||||||||

| 20.00 | ||||||||||||||

| Always | Always | 30.00 | ||||||||||||

| Always | Always | 40.00 | ||||||||||||

| GPR-EI | Bayer et al. | ||||||||||||

| 1.88 | |||||||||||||

| 3.22 | |||||||||||||

| 5.31 | |||||||||||||

| 8.50 | |||||||||||||

| 13.23 | |||||||||||||

| 20.00 | |||||||||||||

| Always | Always | 30.00 | |||||||||||

| Always | Always | 40.00 | |||||||||||

9 Conclusions

In this paper we have presented two numerical methods to compute the price of American options on a basket of underlyings following the Black-Scholes dynamics. These two methods are based on the GPR-Monte Carlo method and improve its results in terms of accuracy and computational time. The GPR-Tree method can be applied for dimensions up to and it proves to be very efficient when . The GPR-Exact Integration method proves to be particularly flexible and stands out for the small computational cost which allows one to obtain excellent estimates in a very short time. The two methods also turns out to be an effective tool to address non-Markovian problems such as the pricing of American options in the rough Bergomi model. These two methods are thus a step forward in overcoming the curse of dimensionality.

References

- [1] L. Abbas-Turki and B. Lapeyre. American options by Malliavin calculus and nonparametric variance and bias reduction methods. SIAM Journal on Financial Mathematics, 3(1):479–510, 2012.

- [2] A. Alfonsi. High order discretization schemes for the CIR process: application to affine term structure and Heston models. Mathematics of Computation, 79(269):209–237, 2010.

- [3] V. Bally, L. Caramellino, and A. Zanette. Pricing and hedging American options by Monte Carlo methods using a Malliavin calculus approach. Monte Carlo Methods and Application, 11(2):97–133, 2005.

- [4] V. Bally, G. Pagès, and J. Printems. First-order schemes in the numerical quantization method. Mathematical Finance, 13(1):1–16, 2003.

- [5] C. Bayer, P. Friz, and J. Gatheral. Pricing under rough volatility. Quantitative Finance, 16(6):887–904, 2016.

- [6] C. Bayer, R. Tempone, and S. Wolfers. Pricing American options by exercise rate optimization. arXiv: 1809.07300, 2018.

- [7] C. Beck, W. E, and A. Jentzen. Machine Learning approximation algorithms for high-dimensional fully nonlinear partial differential equations and second-order backward stochastic differential equations. Journal of Nonlinear Science, pages 1–57, 2017.

- [8] S. Becker, P. Cheridito, and A. Jentzen. Deep optimal stopping. Journal of Machine Learning Research, 20(74):1–25, 2019.

- [9] B. Bouchard and N. Touzi. Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. Stochastic Processes and their applications, 111(2):175–206, 2004.

- [10] P. P. Boyle, J. Evnine, and S. Gibbs. Numerical evaluation of multivariate contingent claims. The Review of Financial Studies, 2(2):241–250, 1989.

- [11] M. Broadie and P. Glasserman. Pricing American-style securities using simulation. Journal of Economic Dynamics and Control, 21(8-9):1323–1352, 1997.

- [12] J. C. Cox, S. A. Ross, and M. Rubinstein. Option pricing: A simplified approach. Journal of Financial Economics, 7(3):229–263, 1979.

- [13] J. De Spiegeleer, D. B. Madan, S. Reyners, and W. Schoutens. Machine Learning for quantitative finance: fast derivative pricing, hedging and fitting. Quantitative Finance, 18(10):1635–1643, 2018.

- [14] W. E, J. Han, and A. Jentzen. Deep Learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5(4):349–380, 2017.

- [15] N. Ekvall. A lattice approach for pricing of multivariate contingent claims. European Journal of Operational Research, 91(2):214–228, 1996.

- [16] G. Gan. Application of Data Clustering and Machine Learning in Variable Annuity valuation. Insurance: Mathematics and Economics, 53(3):795–801, 2013.

- [17] G. Gan and X. S. Lin. Valuation of large variable annuity portfolios under nested simulation: A functional data approach. Insurance: Mathematics and Economics, 62:138 – 150, 2015.

- [18] L. Goudenège, A. Molent, and A. Zanette. Machine Learning for pricing American options in high dimension. arXiv: 1903.11275, 2019.

- [19] L. L. Gratiet and J. Garnier. Regularity dependence of the rate of convergence of the learning curve for Gaussian process regression. arXiv: 1210.2879, 2012.

- [20] J. Han, A. Jentzen, and W. E. Solving high-dimensional partial differential equations using Deep Learning. Proceedings of the National Academy of Sciences, 115(34):8505–8510, 2018.

- [21] M. B. Haugh and L. Kogan. Pricing American options: a duality approach. Operations Research, 52(2):258–270, 2004.

- [22] R. V. Hogg, J. McKean, and A. T. Craig. Introduction to Mathematical Statistics. Pearson Education, 2005.

- [23] B. Horvath, A. Jacquier, and A. Muguruza. Functional central limit theorems for rough volatility. arXiv: 1711.03078, 2017.

- [24] S. Jain and C. W. Oosterlee. Pricing high-dimensional Bermudan options using the stochastic grid method. International Journal of Computer Mathematics, 89(9):1186–1211, 2012.

- [25] M. Kohler, A. Krzyżak, and N. Todorovic. Pricing of high-dimensional American options by neural networks. Mathematical Finance, 20(3):383–410, 2010.

- [26] J. Lelong. Dual pricing of American options by Wiener chaos expansion. SIAM Journal on Financial Mathematics, 9(2):493–519, 2018.

- [27] P. Lions and H. Regnier. Calcul du prix et des sensibilités d’une option américaine par une méthode de Monte Carlo. preprint, 2, 2001.

- [28] F. A. Longstaff and E. S. Schwartz. Valuing American options by simulation: a simple least-squares approach. The Review of Financial Studies, 14(1):113–147, 2001.

- [29] M. Ludkovski. Kriging metamodels and experimental design for Bermudan option pricing. Journal of Computational Finance, 22(1), 2018.

- [30] M. A. Nielsen. Neural Networks and Deep Learning, volume 25. Determination press San Francisco, CA, USA, 2015.

- [31] L. C. Rogers. Monte Carlo valuation of American options. Mathematical Finance, 12(3):271–286, 2002.

- [32] J. N. Tsitsiklis and B. Van Roy. Optimal stopping of Markov processes: Hilbert space theory, approximation algorithms, and an application to pricing high-dimensional financial derivatives. IEEE Transactions on Automatic Control, 44(10):1840–1851, 1999.

- [33] C. K. Williams and C. E. Rasmussen. Gaussian Processes for Machine Learning, volume 2. MIT Press Cambridge, MA, 2006.

Appendix A Proof of Proposition 1

Let and suppose the function at time to be known at . Let us define the quantity

| (A.1) |

for . The function at time at follows

| (A.2) | ||||

| (A.3) |

where

| (A.4) |

We can also write

| (A.5) | ||||

| (A.6) |

where is the random variable defined as

| (A.7) |

Let us define as the covariance matrix of the log-increments, that is . Moreover, let be a square root of and as a vector that follows a standard Gaussian law. Then, we observe that has the following conditional law

| (A.8) |

In fact, simple Algebra leads to

| (A.9) |

Moreover, relation (A.8) can also be stated as

| (A.10) |

Let denote the density function of given . Specifically,

| (A.11) |

Then, according to (A.6),we can write

| (A.12) |

Now, let us consider GPR approximation of the function , obtained by assuming as the predictor set and by employing the Squared Exponential Kernel , which is given by

| (A.13) |

In particular, with reference to (A.13), the additional parameters and are called hyperparameters and are obtained by means of a maximum likelihood estimation. So let

| (A.14) |

be the GPR approximation of the function , where in (A.14) is a vector of weights that can be computed by solving a linear system (see Rasmussen and Williams [33]). The GPR-EI approximation of the continuation value is then given by

| (A.15) | ||||

| (A.16) |

To compute each integral in (A.16), we observe that

| (A.17) |

where is the convolution product and is the density function of a Gaussian random vector which has law given by . Moreover, the convolution product of the densities of two independent random variables is equal to the density of their sum (see Hogg et al. [22]) and we can obtain the following relation which allows one to exactly compute the integrals in (A.16):

| (A.18) |

Therefore, the GPR-EI approximation at reads

| (A.19) |

and the GPR-EI approximation of the option value at time and at is given by

| (A.20) |

Appendix B Covariance of the vector in (6.1)

Let us report the formulas for the covariance of the components of the vector in (6.1). For all , and , the following relations hold:

| (B.1) |

| (B.2) |

| (B.3) |

| (B.4) |

| (B.5) |

| (B.6) |

| (B.7) |

Appendix C Proof of Proposition 3

Let us denote the random vector for and with . We observe that the option value at time is given by the payoff function , which only depends by the final value of the underlying. The option value at time about the -th path is given by

| (C.1) |

where stands for the continuation value and it is equal to

| (C.2) |

We approximate the continuation value in (C.2) by means of the GPR approximation of . In particular, let be the approximation of the function by using the GPR method employing the Squared Exponential Kernel and considering the log-underlying values at maturity as predictors. Specifically, the predictor set is

| (C.3) |

and the response is given by

| (C.4) |

In particular, we can write

| (C.5) |

where is the Squared Exponential kernel, is the characteristic length scale, is the signal standard deviation and are weights.

So we approximate the continuation value with the expression:

| (C.6) |

We observe that the law of given is normal

| (C.7) |

where

| (C.8) |

and

| (C.9) |

Therefore, the GPR-EI approximation for the continuation value at time is as follows:

| (C.10) |

Taking advantage of the properties of the convolution between density functions, we obtain

| (C.11) |

Appendix D Proof of Proposition 4

In order to proceed backward, from up to we consider an integer positive value and train the GPR method considering the last observed values of the couple as predictors, and the option price as response. Specifically, the predictor set is

| (D.1) |

where and the response is given by

| (D.2) |

We term the obtained function. In particular, and

| (D.3) |

approximates .

Since the predictors have different nature (log-prices and log-volatilities at different times), we use the Automatic Relevance Determination (ARD) Squared Exponential Kernel to perform the GPR regression. In particular, if is the dimension of the space containing the predictors, it holds

| (D.4) |

As opposed to the Squared Exponential kernel, the ARD Squared Exponential kernel considers a different length scale for each predictor that allows the regression to better learn the impact of each predictor on the response.

We present now how to perform the backward induction. So, let us consider and suppose the GPR approximation to be known. In particular, and for each it holds

| (D.5) |

where if is even and if is odd, for . This means that is the observed log-price at time of the -th path if is even, and it is the observed log-volatility at time of the -th path if is odd.

We explain now how to compute the GPR approximation of the price function at time . First of all, we observe that the vector is not -measurable whereas is -measurable. The law of given is normal:

| (D.6) |

In particular

| (D.7) |

where is the -th row of the matrix and . Moreover, the covariance matrix is given by

| (D.8) |

where stands for the element of in position . Using a similar reasoning as done for the continuation value at time , one can obtain the following GPR-EI approximation for the continuation value at time :

| (D.9) |

where and are two factors given by

| (D.10) |

and

| (D.11) |

In particular, measures the impact of the past observed values on the price, whereas integrates the changes due to the diffusion of the underlying and its volatility.

Therefore, we obtain

Finally, we observe that, in order to compute , we train the GPR method considering the predictor set given by

| (D.12) |

and the response is given by

| (D.13) |

By induction we can compute the option price value for .

To conclude, we observe that the continuation value at time can be computed by using (D.9) and considering for since in this case, there are no past values to consider.