Convergence Analyses of Online ADAM Algorithm in Convex Setting and Two-Layer ReLU Neural Network

Abstract

Nowadays, online learning is an appealing learning paradigm, which is of great interest in practice due to the recent emergence of large scale applications such as online advertising placement and online web ranking. Standard online learning assumes a finite number of samples while in practice data is streamed infinitely. In such a setting gradient descent with a diminishing learning rate does not work. We first introduce regret with rolling window, a performance metric for online streaming learning, which measures the performance of an algorithm on every fixed number of contiguous samples. At the same time, we propose a family of algorithms based on gradient descent with a constant or adaptive learning rate and provide very technical analyses establishing regret bound properties of the algorithms. We cover the convex setting showing the regret of the order of the square root of the size of the window in the constant and dynamic learning rate scenarios. Our proof is applicable also to the standard online setting where we provide analyses of the same regret order (the previous proofs have flaws). We also study a two layer neural network setting with reLU activation. In this case we establish that if initial weights are close to a stationary point, the same square root regret bound is attainable. We conduct computational experiments demonstrating a superior performance of the proposed algorithms.

1 Introduction

Online learning is the process of dynamically incorporating knowledge of the geometry of the data observed in earlier iterations to perform more informative learning in later iterations, as opposed to standard machine learning techniques which provide an optimal predictor after training over the entire dataset. Online learning is a preferred paradigm in situations where the algorithm has to dynamically adapt to new patterns in the dataset, or when the dataset itself is generated as a function of time, i.e. stock price prediction. Online learning is also used when the dataset itself is computationally infeasible to be trained over the entire dataset.

In standard online learning it is assumed that a finite number of samples is encountered however in real world streaming setting an infinite number of samples is observed (e.g., Twitter is streaming since inception and will continue to do so for foreseeable future). The performance of an online learning algorithm on early examples is negligible when measuring the performance or making predictions and decisions on the later portion of a dataset (the performance of an algorithm on tweets from ten years ago has very little bearing on its performance on recent tweets). The problem can be tackled by restarting, however, it is challenging to determine when to restart. For this reason we propose a metric which forgets about samples encountered a long time ago. Consequently, we introduce a performance metric, regret with rolling window, which measures the performance of an online learning algorithm over a possible infinite size dataset. This metric also requires an adaptation of prior algorithms, because, for example, a diminishing learning rate has poor performance on an infinite data stream.

Stochastic gradient descent (Sgd) [27] is a widely used approach in areas of online machine learning, where the weights are updated each time a new sample is received. Furthermore, it requires a diminishing learning rate in order to achieve a high-quality performance. It has been empirically observed that, in order to reduce the impact of the choice of the learning rate and conduct stochastic optimization more efficiently, the adaptive moment estimation algorithm (Adam) [16] and its extensions ([20],[22]) are another type of popular methods, which store an exponentially decaying average of past gradients and squared gradients and applies adaptive learning rate. (In standard gradient descent algorithms we use the term learning rate, while in adaptive learning rate algorithms we call stepsize the hyperparameter that governs the scale between the weights and the adjusted gradient.) In spite of this, no contribution has been made to the case where the regret is computed in a rolling window. Moreover, applying a diminishing learning rate or stepsize to regret with rolling window is not a good strategy, otherwise, the performance is heavily dependent on the learning rate or stepsize and the rank of a sample. Namely, regret with rolling window requires a constant learning rate or stepsize.

Standard online setting has been studied in the convex setting. With improvements in computational power resulting from GPUs, deep neural networks have been very popular in a variety of AI problems recently. A core application of online learning is online web search and recommender systems [28] where deep learning solutions have recently emerged. At the same time, online learning based on deep neural networks has become an integral role in many stages in finance, from portfolio management, algorithmic trading, to fraud detection, to loan and insurance underwriting. To this end we focus not only on convex loss functions, but also on deep neural networks.

In this work, we propose a new family of efficient online subgradient methods for both general convex functions and a two-layer ReLU neural network based on regret with rolling window metric. More precisely, we first present an algorithm, namely convergent Adam (convgAdam), designed for general strictly convex functions based on gradient descent using adaptive learning rate and inspired by the work of [22]. convgAdam is a more general algorithm that can dynamically adapt to an arbitrary sequence of strictly convex functions. In the meanwhile, we experimentally show that convgAdam outperforms state-of-the-art, yet non-adaptive, online gradient descent (OGD) [27]. Then, we propose an algorithm, called deep neural network gradient descent (dnnGd), for a two-layer ReLU neural network. dnnGd takes standard gradient first, then it rescales the weights upon receiving each new sample. Lastly, we introduce a new algorithm, deep neural network Adam (dnnAdam), which uses an adaptive learning rate for the two-layer ReLU neural network. dnnAdam is first endowed with long-term memory by using gradient updates scaled by square roots of exponential decaying moving averages of squared past gradients and then it rescales weights with every new sample.

In this paper, we not only propose a new family of gradient-based online learning algorithms for both convex and non-convex loss functions, but also present a complete technical proof of regret with rolling window for each of them. For strongly convex functions, given a constant learning rate, we show that convgAdam attains regret with rolling window which is proportional to the square root of the size of the rolling window, compared to the true regret of AMSGrad [22]. Besides, we not only point out but also fix the problem in the proof of regret for AMSGrad later in this paper. Table 1 in Appendix A.2 summarizes all regret bounds in various settings, including the previous flawed analyses. Furthermore, we prove that both dnnGd and dnnAdam attain the same regret with rolling window under reasonable assumptions for the two-layer ReLU neural network. The strongest assumption requires that the angle between the current sample and weight error is bounded away from . Although dnnGd and dnnAdam require some assumptions, these two algorithms have a higher probability to converge than other flavors of Adam due to the convergence analyses provided in Section 5. In summary, we make the following five contributions.

-

•

We introduce regret with rolling window that is applicable in data streaming, i.e., infinite stream of data.

-

•

We provide a proof of regret with rolling window which is proportional to the square root of the size of the rolling window when applying OGD to an arbitrary sequence of convex loss functions.

-

•

We provide a convergent first-order gradient-based algorithm, i.e. convgAdam, employing adaptive learning rate to dynamically adapt to the new patterns in the dataset. Furthermore, given strictly convex functions and a constant stepsize, we provide a complete technical proof of regret with rolling window. Besides, we point out a problem with the proof of convergence of AMSGrad [22], which eventually leads to regret in the standard online setting, and we provide a different analysis for AMSGrad which obtains regret in standard online setting by using our proof technique.

-

•

We propose a first-order gradient-based algorithm, called dnnGd, for the two-layer ReLU neural network. Moreover, we show that dnnGd shares the same regret with rolling window with OGD when employing a constant learning rate.

-

•

We further develop an algorithm, i.e. dnnAdam, based on adaptive estimation of lower-order moments for the two-layer ReLU neural network. At the same time, we argue that dnnAdam shares the same regret with rolling window with convgAdam when employing a constant stepsize.

-

•

We present numerical results showing that convgAdam outperforms state-of-art, yet not adaptive, OGD.

The paper is organized as follow. In the next section, we review several works related to Adam, analyses of two-layer neural networks and regret in online convex learning. In Section 3, we state the formal optimization problem in streaming, i.e., we introduce regret with rolling window. In the subsequent section we propose the two algorithms in presence of convex loss functions and we provide the underlying regret analyses. In Section 5 we study the case of deep neural networks as the loss function. In Section 6 we present experimental results comparing convgAdam with OGD.

2 Related Work

Adam and its variants: Adam [16] is one of the most popular stochastic optimization methods that has been applied to convex loss functions and deep networks which is based on using gradient updates scaled by square roots of exponential moving averages of squared past gradients. In many applications, e.g. learning with large output spaces, it has been empirically observed that it fails to converge to an optimal solution or a critical point in nonconvex settings. A cause for such failures is the exponential moving average, which leads Adam to forget about the influence of large and informative gradients quickly [4]. To tackle this issue, AMSGrad [22] is introduced which has long-term memory of past gradients. AdaBound [20] is another extension of Adam, which employs dynamic bounds on learning rates to achieve a gradual and smooth transition from adaptive methods to stochastic gradient. Though both AMSGrad [22] and AdaBound [20] provide theoretical proofs of convergence in a convex case, very limited further research related to Adam has be done in a non-convex case while Adam in particular has become the default algorithm leveraged across many deep learning frameworks due to its rapid training loss progress. Unfortunately, there are flaws in the proof of AMSGrad, which is explained in a later section and articulated in Appendix A.

Two-layer neural network: Deep learning achieves state-of-art performance on a wide variety of problems in machine learning and AI. Despite its empirical success, there is little theoretical evidence to support it. Inspired by the idea that gradient descent converges to minimizers and avoids any poor local minima or saddle points ([18], [17], [2], [12], [15]), Luo & Wu [24] prove that there is no spurious local minima in a two-hidden-unit ReLU network. However, Luo & Wu make an assumption that the 2nd layer is fixed, which does not hold in applications. Li & Yuan [19] also make progress on understanding algorithms by providing a convergence analysis for Sgd on special two-layer feedforward networks with ReLU activations, yet, they specify the 1st layer as begin offset by “identity mapping” (mimicking residual connections) and the 2nd layer as the -norm function. Additionally, based on their work [10], Du et al [9] give the 2nd layer more freedom in the problem of learning a two-layer neural network with a non-overlapping convolutional layer and ReLU activation. They prove that although there is a spurious local minimizer, gradient descent with weight normalization can still recover the true parameters with constant probability when given Gaussian inputs. Nevertheless, the convergence is guaranteed when the 1st layer is a convolutional layer.

Online convex learning: Many successful algorithms and associated proofs have been studied and provided over the past few years to minimize regret in online learning setting. Zinkevich [27] shows that the online gradient descent algorithm achieves regret , for an arbitrary sequence of convex loss functions (of bounded gradients) and given a diminishing learning rate. Then, Hazan et al [13] improve regret to when given strictly convex functions and a diminishing learning rate. The idea of adapting first order optimization methods is by no means new and is also popular in online convex learning. Duchi, Hazan & Singer [11] present AdaGrad, which employs very low learning rates for frequently occurring features and high learning rates for infrequent features, and obtain a comparable bound by assuming 1-strongly convex proximal functions. In a similar framework, Zhu & Xu [26] extend the celebrated online gradient descent algorithm to Hilbert spaces (function spaces) and analyzed the convergence guarantee of the algorithm. The online functional gradient algorithm they propose also achieves regret when given convex loss functions. In all these algorithms, the loss function is required to be convex or strongly convex and the learning rate or step size must diminish. However, no work about regret analyses of online learning applied on deep neural networks (non-convex loss functions) has been done.

Adaptive regret: Recently, adaptive regret has been studied in the setting of prediction with expert advice (PEA) in online learning. Adaptive regret measures the maximum difference of the performances of an online algorithm and the offline optimum for any consecutive samples in total rounds, while our regret measures the maximum difference of the performances in the whole history. Existing online algorithms are closely related in the sense that adaptive algorithms designed are usually built upon the PEA algorithms. The concept of adaptive regret is formally introduced by Hazan and Seshadhri [14]. They also propose a new algorithm named follow the leading history (FLH), which contains an expert-algorithm, a set of intervals and a meta-algorithm. Then Daniely in [7] extends this idea by introducing strongly adaptive algorithms, which provide a regret bound where s is the end point of the rolling window and is the size of the window. Later on, Zhang in [25] applies the concept of the adaptive learning rate to adaptive regret and proposes adaptive algorithms for convex and smooth functions, and finally obtains a regret bound , where is the loss function for the sample given any in the corresponding domain, and and are the starting and ending data points of the interested sequence. Notice that in conjunction with infinite streaming, blows up and eventually dominates the regret bound. Although the concept of the adaptive regret is similar to our regret with rolling window, adaptive regret relies on other existing online algorithms which not only use diminishing learning rate but also bring extra error. In regret with rolling window, we consider these two aspects together (infinite time stream and the issue of learning rates) and propose a new family of online algorithms which use a constant learning rate and achieve a more robust regret. Specifically, our regret bound is , which does not depend of the position of the window.

3 Regret with Rolling Window

We consider the problem of optimizing regret with rolling window, inspired by the standard regret ([27], [1], [21]). The problem with the traditional regret is that it captures the performance of an algorithm only over a fixed number of samples or loss functions. In most applications data is continuously streamed with an infinite number of future loss functions. The performance over any finite number of consecutive loss functions is of interest. The concept of regret is to compare the optimal offline algorithm with access to contiguous loss functions with the performance of the underlying online algorithm. Regret with rolling window is to find the maximum of all differences between the online loss and the loss of the offline algorithm for any contiguous samples. More precisely, for an infinite sequence , where each feature vector is associated with the corresponding label , given fixed and any , we first define , which corresponds to the optimal solution of the offline algorithm. In general, , e.g. if the linear regression model is applied and the mean square error is used. Then, we consider

| (1) |

with , where is a function of sample . The regret with rolling window metric captures regret over every consecutive loss functions and it is aiming to assess the worst possible regret over every such sequence. Note that if we have only loss functions corresponding only to , then this is the standard regret definition in online learning. The goal is to develop algorithms with low regret with rolling window. We prove that regret with rolling window can be bounded by . In other words, the average regret with rolling window approaches zero.

4 Convex Setting

In the convex setting, we propose two algorithms with a different learning rate or stepsize strategy and analyze them with respect to (1) in the streaming setting.

4.1 Algorithms

Algorithms in standard online setting are almost all based on gradient descent where the parameters are updated after each new loss function is received based on the gradient of the current loss function. A challenge is the strategy to select an appropriate learning rate. In order to guarantee good regret the learning rate is usually decaying. In the streaming setting, we point out that a decaying learning rate is improper since far away samples (very large ) would get a very small learning rate implying low consideration to such samples. In conclusion, the learning rate has to be a constant or it should follow a dynamically adaptive learning algorithm, i.e. ADAM. The algorithms we provide for solving (1) in the streaming setting are based on gradient descent and one of the just mentioned learning rate strategies.

In order to present our algorithms, we first need to specify notation and parameters. In each algorithm, we denote by and the learning rate or stepsize and a subgradient of loss function associated with sample , respectively. Additionally, we employ to represent the element-wise multiplication between two vectors or matrices (Hadamard product). However, for other operations we do not introduce new notation, e.g., for element-wise division () and square root (), since these two operations are written differently when representing standard matrix or vector operations.

We start with OGD which mimics gradient descent in online setting and achieves regret with rolling window when given constant learning rate. Algorithm 1 is a twist on Zinkevich’s Online Gradient Descent [27]. OGD updates its weight when a new sample is received in step 4. In addition, OGD uses constant learning rate in the streaming setting so as to efficiently and dynamically learn the geometry of the dataset. Otherwise, if a diminishing learning rate is applied, OGD misses informative samples which arrive late due to the extremely small learning rate and leads to regret with rolling window (this is trivial to observe if the loss functions are bounded). Regret of is achieved in the streaming setting if learning rate .

Constant learning rates have a drawback by treating all features equally. Consequently, we adapt ADAM to online setting and further extend it to streaming. Algorithm 2, inspired by ADAM [16] and AMSGrad [22], has regret with rolling window also of the order given constant stepsize as shown in the next section. The key difference of convgADAM with AMSGrad is that it maintains the same ratio of the past gradients and the current gradient instead of putting more and more weight on the current gradient and losing the memory of the past gradients fast. In Algorithm 2, convgAdam records exponential moving average of gradients and moments in step 5 and 6. Step 7 guarantees that is the maximum of all until the present time step. Then, step 8 gives the adaptive update rule by using the maximum value of to normalize the running average of the gradient at time . Besides, constant stepsize is crucial to make convgAdam well-performed due to the aforementioned reason with a potential decaying learning rate or stepsize.

In step 8, we observe that for a feature implies , therefore, we retain the foregoing weight as the succeeding weight . In other words, in this case we define .

4.2 Analyses

In this section, we provide regret analyses of OGD and convgAdam showing that both of them attain regret with rolling window which is proportional to the square root of the size of the rolling window given a constant learning rate or stepsize in the streaming setting. For inner (scalar) products, given the fact that for two vectors and , in the rest of the paper, for short expressions we use , but for longer we use .

We require the following standard assumptions.

Assumption 1:

-

1.

There exists a constant , such that , for any .

-

2.

The loss gradients are bounded, i.e., for all such that , we have .

-

3.

Functions are convex and differentiable with respect to for every .

-

4.

Functions are strongly convex with parameter , i.e., for all and , and for , it holds .

The first condition in Assumption 1 assumes that are bounded. This assumption can be removed by further complicating certain aspects of the upcoming proofs. This extension is discussed in Appendix A.1 for the sake of clarity of the algorithm. In 2 from Assumption 1, the gradient of the loss function is requested to be upper bounded. Notice that each loss function is enforced to be differentiable and convex in 3, whereas is required to be strictly convex with parameter in 4. All these are standard assumptions.

We first provide the regret analysis of OGD.

Theorem 1.

The proof is provided in Appendix B. Under the assumptions in Assumption 1, by finding a relationship for the sequence of the weight error and employing the property of convexity from condition 3 from Assumption 1, we prove that OGD obtains the regret with rolling window which is proportional to the square root of the size of the rolling window when given the constant learning rate. This is consistent with the regret of OGD in the standard online setting.

The analysis of OGD is not totally new but still has some important differences. Also, when using a diminishing learning rate, given strongly convex , it has been proven in [13] by Hazan that OGD obtains logarithmic regret. However, this is not possible even given strongly convex when using a constant learning rate, which should be clear after reading our regret analysis of OGD and comparing it with the regret analysis in [13].

If OGD is an analogue to the Gradient Descent optimization method for the online setting, then convgAdam is an online analogue of Adam, which dynamically incorporates knowledge of the characteristics of the dataset received in earlier iterations to perform more informative gradient-based learning. Next, we show that convgAdam achieves the same regret with rolling window given a constant stepsize.

Theorem 2.

If Assumption 1 holds, and and are two constants between 0 and 1 such that and , then for for any positive constant , the sequence generated by convgAdam achieves .

The proof is provided in Appendix C. The very technical proof follows the following steps. Based on the updating procedure in steps 4-8, we establish a relationship for the sequence of the weight error . Meanwhile, considering condition 4 in Assumption 1, we obtain another relationship between the loss function error and . Assembling these two relationships provide a relationship between the weight error and the loss function error . By deriving upper bounds for all of the remaining terms based on conditions from Assumption 1, we are able to argue the same regret with rolling window of .

In the regret analysis of AMSGrad [22], the authors forget that the stepsize is and take the hyperparameter to be exponentially decaying for granted without assumptions which eventually leads to regret in standard online setting. Our analysis is flexible enough to extend to AMSGrad and a slight change to our proof yields the regret for AMSGrad. The changes in our proof to accommodate standard online setting and AMSGrad are stated in Appendix A.2. Moreover, the proof of convergence of AMSGrad in [22] uses a diminishing stepsize while our proof is valid for both constant and diminishing stepsizes. Likewise, for AdaBound [20], the right scale of the stepsize is also missed and the regret should be , which is discussed in more detail in Appendix A.2. In this section we also discuss how to amend our proof to provide the regret bound in standard online setting for AdaBound.

Theorem 2 guarantees that convgAdam achieves the same regret with rolling window as OGD for convex loss functions. On the other hand, very limited work has been done about regret for nonconvex loss functions, e.g. the loss function of a two-layer ReLU neural network. In the following section, we argue that both dnnGD and dnnAdam attain the same regret with rolling window if the initial starting point is close to an optimal offline solution and by using a constant learning rate or stepsize. In addition to a favorable starting point, further assumptions are needed.

5 Two-Layer ReLU Neural Network

In this section we consider a two layer neural network with the first hidden layer having an arbitrary number of neurons and the second hidden layer has a single neuron. The underlying activation function is a probabilistic version of ReLU and minimum square error is considered as the loss function. First of all, the optimization problem of such a two-layer ReLU neural network is neither convex nor convex (and clearly non linear), therefore, it is very hard to find a global minimizer. Instead, we show that our algorithms achieve regret with rolling window when the initial point is close enough to an optimal solution.

Neural networks as classifiers have a lot of success in practice, whereas a formal theoretical understanding of the mechanism of why they work is largely missing. Studying a general neural network is challenging, therefore, we focus on the proposed two-layer ReLU neural network. For a dataset , the standard loss function of the two-layer neural network is , where represents the ReLU activation function applied element-wise, is the parameter vector, and is the parameter matrix. It turns out that ReLU is challenging to analyze since nesting them yields many combinations of the various values being below zeros. One way to get around this is to consider a probabilistic version of ReLU and capturing expected loss, Luo & Wu [24].

To this end we treat ReLU as a random Bernoulli variable in the sense that Pr, Pr. Luo & Wu [24] in the standard offline setting analyze for the probabilistic version of ReLU. For our online analyses we need to slightly alter the setting by introducing two independent identically distributed random variables and and the loss function as follows

| (2) |

There is a crucial property of which is positive-homogeneity. That is, for any , . This property allows the network to be rescaled without changing the function computed by the network.

For two-layer ReLU neural network, given , we consider regret with rolling window as

| (3) |

Next, we propose two algorithms with different learning rates or stepsizes for the two-layer neural network and analyze them with respect to (3).

5.1 Algorithms

In order to present the algorithms, let us first introduce notation and parameters. For any matrix and vector , let and denote the element in the row and column of matrix and coordinate of vector , respectively. Similarly, we use () to represent the column ( row) of matrix . Next, in order to be consistent, we also denote and as the learning rate or stepsize and a subgradient of loss function associated with sample , respectively. Let and be constants. Lastly, in order to be consistent with the notation in the convex setting, we employ to represent the element-wise multiplication between vectors or matrices while using standard division and square root notation for the corresponding operations element-wise in vectors and matrices.

We start with dnnGd which is the algorithm with a fixed learning rate, Algorithm 3. We show later that its regret with rolling window is . dnnGD is an analogue of the gradient descent optimization method for the online setting with the two-layer ReLU neural network, and at the same time it is an extension of OGD. Different from OGD, dnnGD not only modifies weights at a given iteration by following the gradient direction, but it also rescales weights based on the domain constraint in step 6, i.e. has a fixed norm. Then, is rescaled at the same time to impose positive-homogeneity in step 7.

Taking the drawbacks of a constant learning rate into consideration, we propose Algorithm 4, which is an extension of convgAdam for the two-layer ReLU neural network and likewise attains regret with rolling window. In dnnAdam, the stochastic gradients computed in steps 4 and 5 are different than those in dnnGD. This is due to challenges in establishing the regret bound. Nevertheless, the stochastic gradients are unbiased estimators of gradients of the loss function. An alternative is to have four samples, two per gradient group. This would also enable the regret analysis, however we only employ two of them so as to reduce the variance of the algorithm. dnnAdam records exponential moving average of gradients and moments in steps 6 - 9. Step 10 modifies to be a matrix with same value in the same column. This is a divergence from standard ADAM which does not have this requirement. The modification is required for the regret analysis. Then, steps 11 and 12 guarantee that and are nondecreasing sequences element-wise. Lastly, we update weights and also perform the rescaling modification to dnnAdam in steps 13 and 14. Additionally, we apply the same strategy as we mention in convgAdam when or . More precisely, if (), it implies () for all , which in turn yields (). Thus, we define and . Therefore, we maintain the weights from the last iteration.

5.2 Analyses

In this section, we discuss regret with rolling window bounds of dnnGd and dnnAdam showing that both of them attain regret with rolling window proportional to the square root of the size of the rolling window. Before establishing the regret bounds, we first require the following assumptions.

Assumption 2:

-

1.

Activations are independent Bernoulli random variables with the same probability of success, i.e. Pr, Pr.

-

2.

There exists and such that for all .

-

3.

Quantities , and are all bounded for any . In particular, let and for any .

-

4.

There exists such that for all when .

-

5.

There exits a positive constant such that .

As Kawaguchi assumed in [15] and other works ([8], [5], [6]), we also assume that ’s are Bernoulli random variables with the same probability of success and are independent from input ’s and weights ’s in 1 from Assumption 2. 111In general, the distribution of the Bernoulli random variable representing the ReLU activation function is not required to be stationary for all . Since all loss functions are considered separately, we only need to assume that for every , there is a corresponding such that , then, later in the proof, those ’s are absorbed into . Therefore, the algorithms can dynamically adapt to the new patterns in the dataset. In the proof, we simplify this process by using a constant . Then, given are i.i.d, . At the same time, the new loss function is . Therefore, minimizing our new loss function is the same as minimizing the original loss given that is a positive constant. Condition in 2 from Assumption 2 states that the optimal expected loss is zero. This is also assumed in other prior work in offline, e.g. [24], [9]. The 3rd condition in Assumption 2 is an extension of 1 in Assumption 1. Likewise, the constraints on and can be removed by further introducing technique discussed in Appendix A.1, and consequently, and are bounded due to steps 4 and 5. The next to the last condition in Assumption 2 requires that a new coming sample has to be beneficial to improve current weights. More precisely, we interpret the difference between the current weights and optimal weights as an error that needs to be corrected. Then, a new sample which is not relevant to the error vector is not allowed. In other words, we assume that the algorithm does not receive any uninformative samples. Condition 5 from Assumption 2 assumes that any nonzero is lower bounded by a constant for all and . It is a weak constraint since for any and . In practice, we can modify it by only memorizing the first nonzero value in each coordinate and finding the smallest among these values. Otherwise, if all of , then we can set by default.

The regret statement for dnnGd is as follows.

Theorem 3.

The proof is in Appendix D. Based on the fact that the loss function is nonconvex, i.e., we no longer have a direct relationship between the loss function error and , any technique that relies on the property of convexity is inappropriate. The main challenges are coming from building a bridge between the loss function error and the weight error . To address this problem, we explore the difference between and in detail.

The steps to study the regret with rolling window are as follows. Based on steps 4 - 7, we expand to establish a relationship for the sequence of the weight error . In association with explicit formulas of gradients and condition 4 in Assumption 2, we obtain the loss function error . Meanwhile, all of the remaining terms are bounded due to condition 3 from Assumption 2. Combined with the fact that has a constant norm, the regret with rolling window bound of dnnGd is achieved by applying the law of iterated expectation.

At the same time, our proof is flexible enough to extend to standard online setting. For a constant learning rate, Appendix D provides the necessary details for the standard case. In summary, regret of is achieved. We note that such a result has only been known for the diminishing learning rate and thus we extend the prior knowledge by covering the constant learning rate case.

The adaptive learning setting algorithm dnnAdam has the same regret bound as stated in the following theorem.

Theorem 4.

If Assumption 2 holds, for any positive constant , are constants between and such that and , and with , and , then, the sequence and generated by dnnAdam for the 2-layer ReLU neural network achieves .

The proof is in Appendix E. Similar to the difficulty faced in the proof of Theorem 3, we do not possess a relationship between the loss function error and . Even worse, the variance of the algorithm caused by merging all previous information and normalizing the stepsize makes the relationship between the loss function error and the weight error more ambiguous. The way we deal with this is by treating together as the gradient first and then extracting the effective gradient out from it and bounding the remaining terms.

The structure of the technical proof is similar to that of Theorem 3. We first establish a relationship for the sequence of the weight error by multiplying . Then, using the definitions of ’s, ’s and ’s, we bound all the terms without the stepsize by constants except those which potentially can contribute to the loss function. To this end, we obtain a relationship between the weight error and the loss function. Finally, combined with step12 and the law of iterated expectation, we are able to argue regret with rolling window for dnnAdam.

6 Numerical Study

In this section, we compare the convgAdam method with OGD [27] for solving problem (1) with a long sequence of data points (mimicking streaming). We conduct experiments on the MNIST8M dataset and two other different-size real datasets from the Yahoo! Research Alliance Webscope program. For all of these datasets, we train multi-class hinge loss support vector machines (SVM) [23] and we assume that the samples are streamed one by one based on a certain random order. For all the figures provided in this section, the horizontal axis is in scale. Moreover, we set and in convgAdam. We mostly capture the log of the loss function value which is defined as .

6.1 Multiclass SVM with Yahoo! Targeting User Modeling Dataset

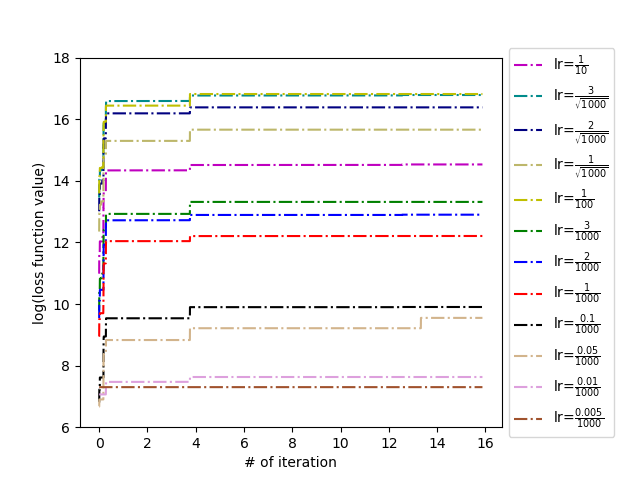

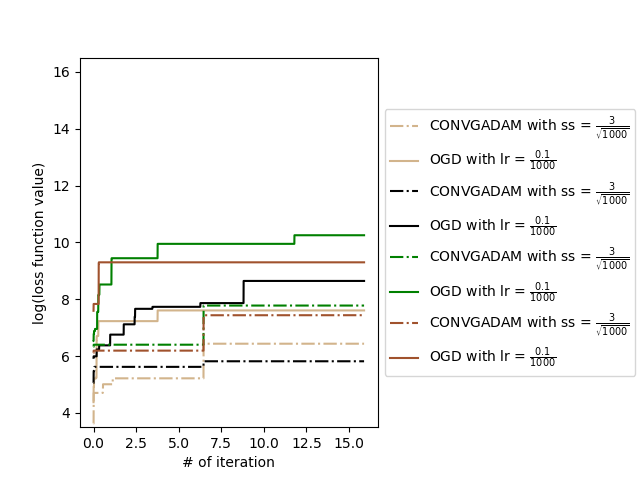

We first compare convgAdam with OGD using the Yahoo! user targeting and interest prediction dataset consisting of Yahoo user profiles222https://webscope.sandbox.yahoo.com/catalog.php?datatype=a. It contains 1,589,113 samples (i.e., user profiles), represented by a total of 13,346 features and 380 different classification problems (called labels in the supporting documentation) each one with 3 classes.

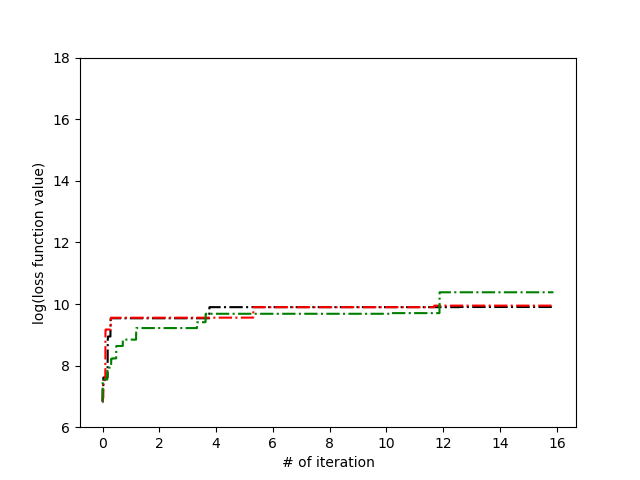

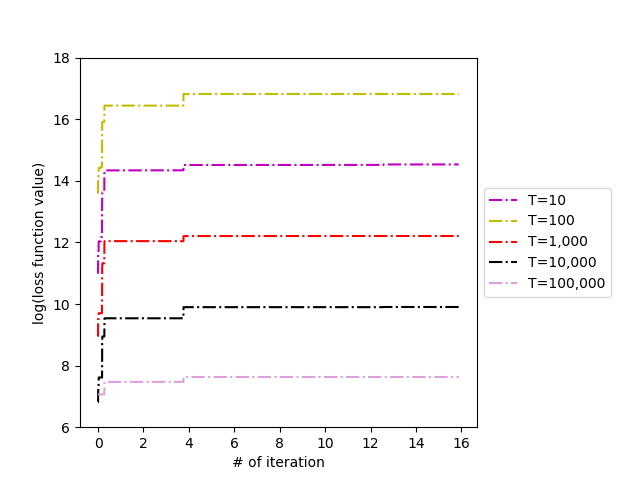

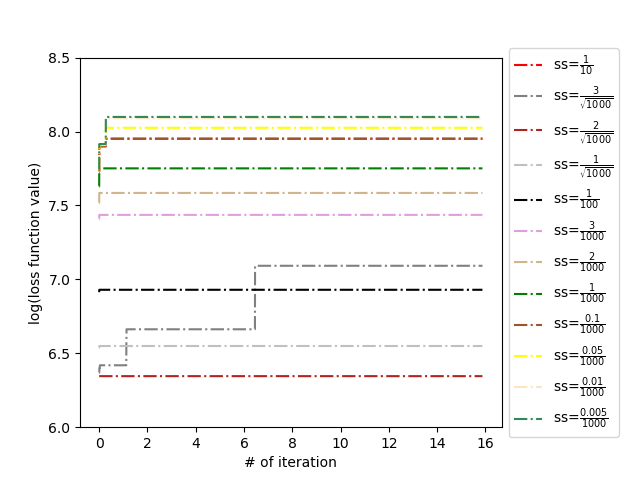

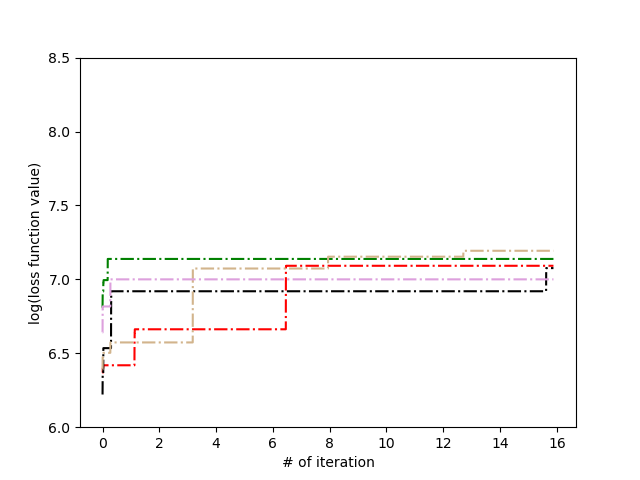

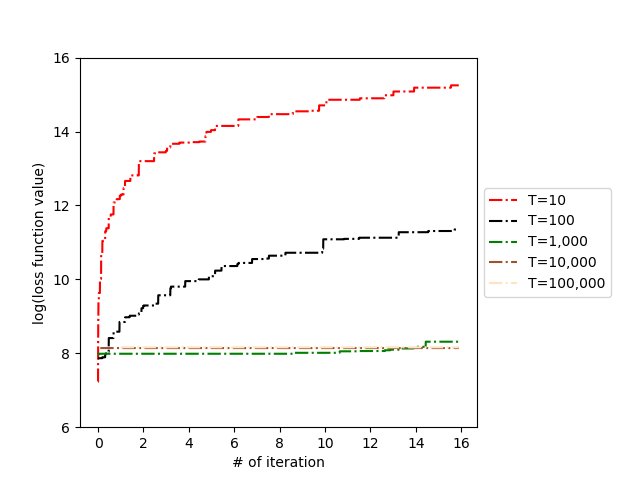

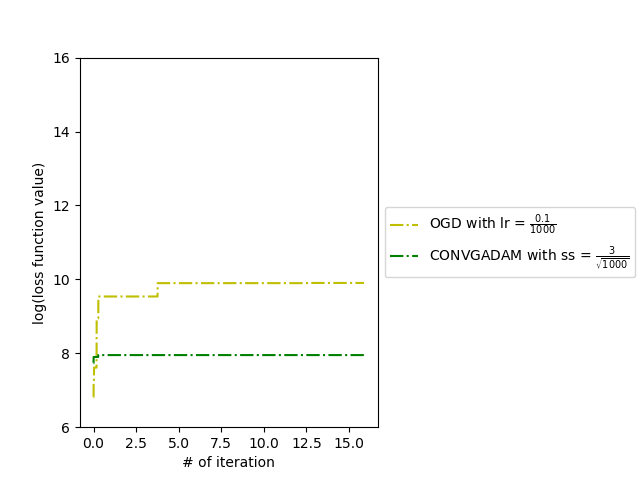

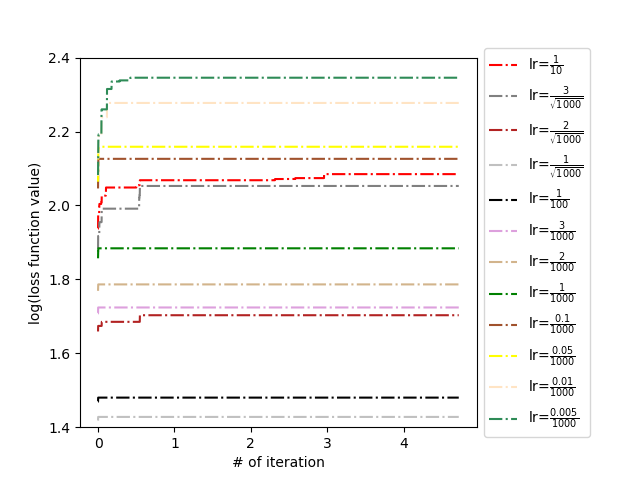

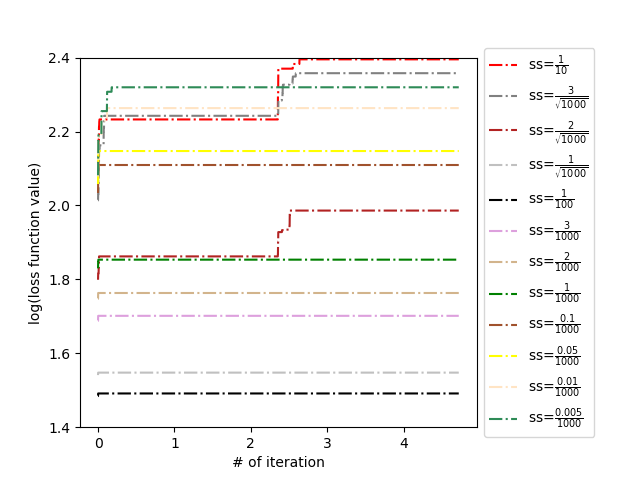

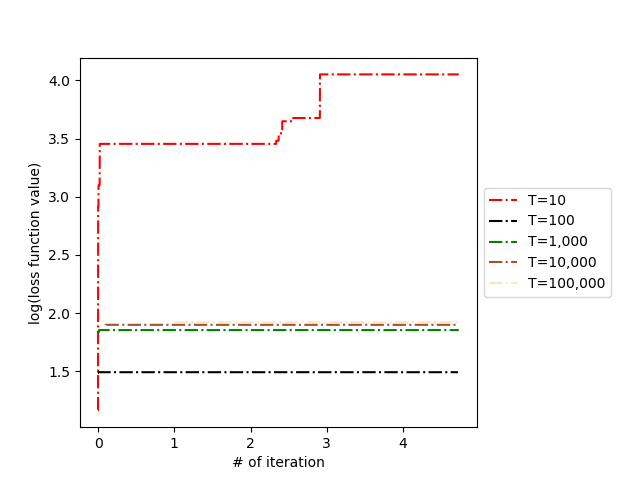

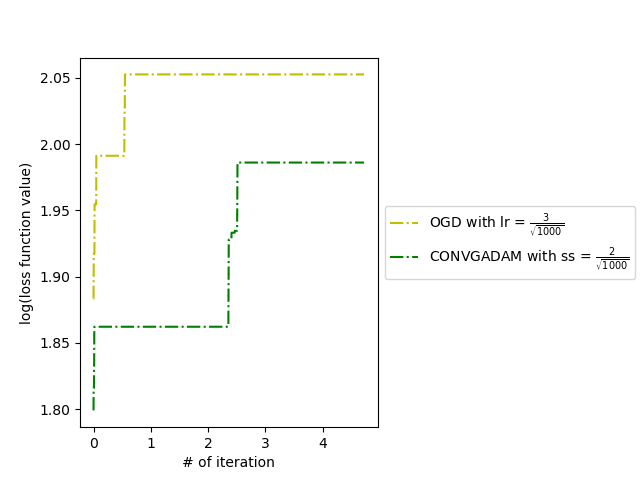

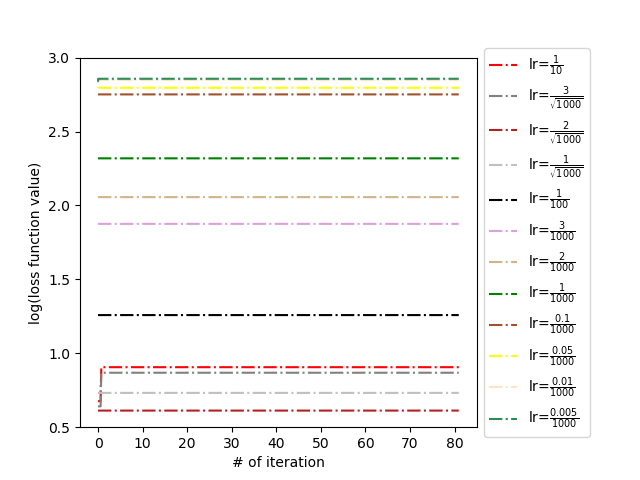

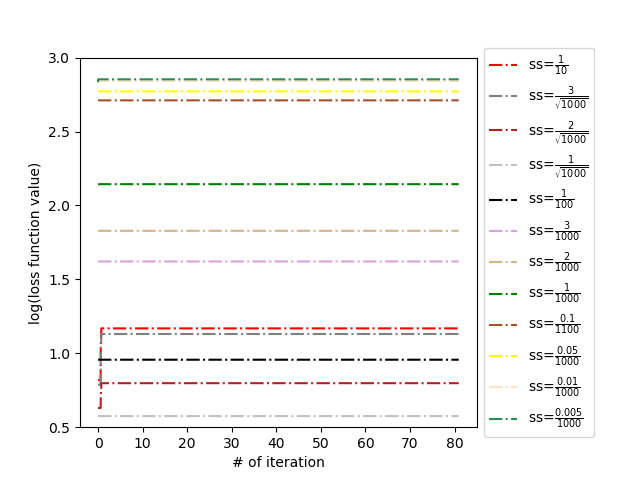

First, we pick the first label out and conduct a sequence of experiments with respect to this label. The most important results are presented in Figure 1 for OGD and Figure 2 for convgAdam. In Figures 1(a) and 2(a), we consider the cases when the learning rate or step size varies from to while keeping the order and fixed at 1,000. Figures 1(b) and 2(b) provide the influence of the order of the sequence. Figures 1(c) and 2(c) represent the case where varies from to with a fixed learning rate or step size. Lastly, in Figure 2(d), we compare the performance of convgAdam and OGD with certain learning rates and step sizes.

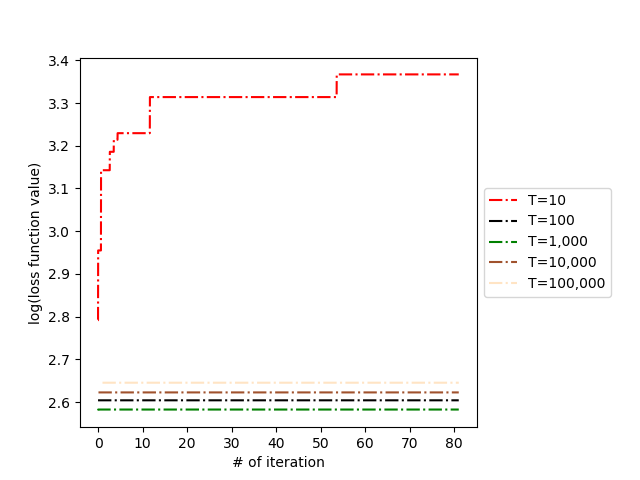

In these plots, we observe that convgAdam outperforms OGD for most of the learning rates and step sizes, and definitely for promissing choices. More precisely, in Figure 1(a) and 2(a), we discover that 0.1/1000 and 3/ are two high-quality learning rate and stepsize values which have relatively low error and are learning for OGD and convgAdam, respectively. Therefore, we apply those two learning rates for the remaining experiments on this dataset. In Figures 1(b) and 2(b), we observe that the perturbation caused by the change of the order is negligible especially when compared to the loss value, which is a positive characteristic. Thus, in the remaining experiments, we no longer need to consider the impact of the order of the sequence. From Figure 1(c) and Figure 1(d), we discover that the loss and have a significantly positive correlation as we expect. Notice that changing but fixing the learning rate or stepsize essentially means containing more samples in the regret, in other words, the regret for is roughly times the regret for . Since the pattern in the figures is preserved for the different values for OGD and convgAdam, in the remaining experiments we fix . In Figure 2(c), we discover that too big or too small causes poor performance and therefore, for the remaining experiments, we set whenever is fixed. From Figure 2(d), we observe that convgAdam outperforms OGD.

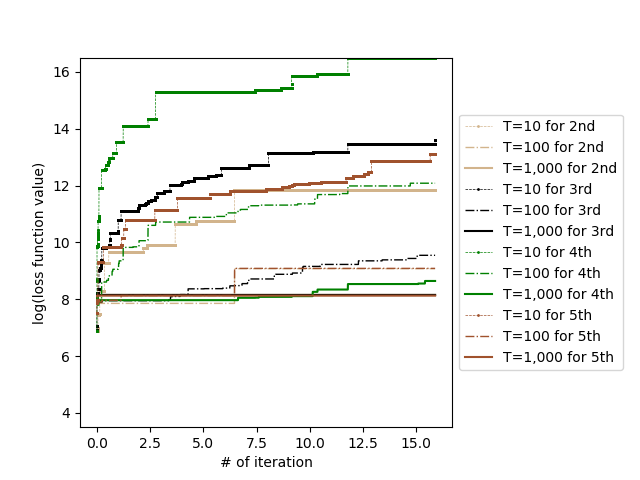

After studying the algorithms on the first label, we test them on the next four labels. In Figure 3, we compare the performance of convgAdam for different and the difference with OGD on the four labels. In these plots, we observe that provides a more stable and better performance than the other two values. Moreover, convgAdam outperforms OGD for all considered learning rates and step sizes.

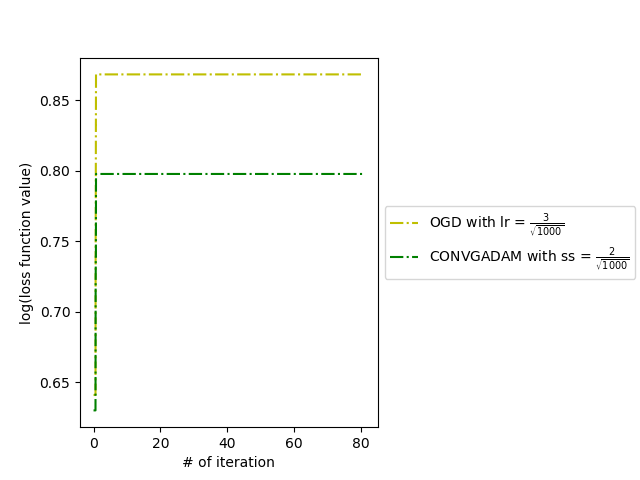

6.2 Multiclass SVM with Yahoo! Learn to Rank Challenge Dataset

In this set of experiments, we study the performances of convgAdam and OGD on Yahoo! Learn to Rank Challenge Dataset333https://webscope.sandbox.yahoo.com/catalog.php?datatype=c. The dataset contains 473,134 samples, represented by a total of 700 features and 5 classes.

Figures 4(a) and 4(b) show the performances of OGD and convgAdam for different learning rates and stepsizes. Figure 4(c) provides the performance of convgAdam for different . Lastly, Figure 4(d) compares the performance of convgAdam and OGD for a set of good learning rates but same .

From Figures 4(a) and 4(b), we select the learning rate and stepsize 3/ and 2/ for convgAdam and OGD, respectively. From Figure 4(d), we discover the superior behavior of convgAdam over OGD as we expect.

6.3 Multiclass SVM with MNIST8M Dataset

In this set of experiments, we study the performances of convgAdam and OGD on MNIST8M Dataset444https://www.csie.ntu.edu.tw/ cjlin/libsvmtools/datasets/. The dataset is generated on the fly by performing careful elastic deformation of the original MNIST training set. The dataset contains 8,100,000 samples, represented by a total of 784 features and 10 classes.

In Figures 5(a) and 5(b), we compare the performances of OGD and convgAdam for different learning rates and stepsizes. Figure 5(c) shows that performance of convgAdam for different . Lastly, Figure 5(d) depicts the comparison of convgAdam and OGD. From Figures 5(a) and 5(b), we select the stepsize 2/ and the learning rate of 1/. As we observe, convgAdam always exhibits a better performance than OGD.

References

- Abernethy et al. [2012] Abernethy, J. D., Hazan, E., and Rakhlin, A. (2012). Interior-point methods for full-information and bandit online learning. IEEE Transactions on Information Theory, 58(7):4164–4175.

- Baldi and Hornik [1989] Baldi, P. and Hornik, K. (1989). Neural networks and principal component analysis: Learning from examples without local minima. Neural Networks, 2(1):53–58.

- Blum [1998] Blum, A. (1998). On-line algorithms in machine learning. In Online algorithms, pages 306–325. Springer.

- Chen et al. [2019] Chen, X., Liu, S., Sun, R., and Hong, M. (2019). On the convergence of a class of ADAM-type algorithms for non-convex optimization. In International Conference on Learning Representations.

- Choromanska et al. [2015a] Choromanska, A., Henaff, M., Mathieu, M., Arous, G. B., and LeCun, Y. (2015a). The loss surfaces of multilayer networks. In Artificial Intelligence and Statistics, pages 192–204.

- Choromanska et al. [2015b] Choromanska, A., LeCun, Y., and Arous, G. B. (2015b). Open problem: The landscape of the loss surfaces of multilayer networks. In Conference on Learning Theory, pages 1756–1760.

- Daniely et al. [2015] Daniely, A., Gonen, A., and Shalev-Shwartz, S. (2015). Strongly adaptive online learning. In International Conference on Machine Learning, pages 1405–1411.

- Dauphin et al. [2014] Dauphin, Y. N., Pascanu, R., Gulcehre, C., Cho, K., Ganguli, S., and Bengio, Y. (2014). Identifying and attacking the saddle point problem in high-dimensional non-convex optimization. In Advances in Neural Information Processing Systems, pages 2933–2941.

- Du et al. [2018a] Du, S., Lee, J., Tian, Y., Singh, A., and Poczos, B. (2018a). Gradient descent learns one-hidden-layer CNN: Don’t be afraid of spurious local minima. In Dy, J. and Krause, A., editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 1339–1348, Stockholmsmässan, Stockholm Sweden. PMLR.

- Du et al. [2018b] Du, S. S., Lee, J. D., and Tian, Y. (2018b). When is a convolutional filter easy to learn? In International Conference on Learning Representations.

- Duchi et al. [2011] Duchi, J., Hazan, E., and Singer, Y. (2011). Adaptive subgradient methods for online learning and stochastic optimization. Journal of Machine Learning Research, 12(Jul):2121–2159.

- Goodfellow et al. [2016] Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep Learning. MIT Press.

- Hazan et al. [2007] Hazan, E., Agarwal, A., and Kale, S. (2007). Logarithmic regret algorithms for online convex optimization. Mach. Learn., 69(2-3):169–192.

- Hazan and Seshadhri [2007] Hazan, E. and Seshadhri, C. (2007). Adaptive algorithms for online decision problems. In Electronic colloquium on computational complexity (ECCC), volume 14.

- Kawaguchi [2016] Kawaguchi, K. (2016). Deep learning without poor local minima. In Advances in Neural Information Processing Systems, pages 586–594.

- Kingma and Ba [2015] Kingma, D. P. and Ba, J. (2015). ADAM: A method for stochastic optimization. CoRR, abs/1412.6980.

- Lee et al. [2017] Lee, J. D., Panageas, I., Piliouras, G., Simchowitz, M., Jordan, M. I., and Recht, B. (2017). First-order methods almost always avoid saddle points. CoRR, abs/1710.07406.

- Lee et al. [2016] Lee, J. D., Simchowitz, M., Jordan, M. I., and Recht, B. (2016). Gradient descent only converges to minimizers. In Conference on Learning Theory, pages 1246–1257.

- Li and Yuan [2017] Li, Y. and Yuan, Y. (2017). Convergence analysis of two-layer neural networks with ReLU activation. In Advances in Neural Information Processing Systems, pages 597–607.

- Luo et al. [2019] Luo, L., Xiong, Y., and Liu, Y. (2019). Adaptive gradient methods with dynamic bound of learning rate. In International Conference on Learning Representations.

- Rakhlin and Tewari [2009] Rakhlin, A. and Tewari, A. (2009). Lecture notes on online learning. Draft, April.

- Reddi et al. [2018] Reddi, S. J., Kale, S., and Kumar, S. (2018). On the convergence of ADAM and beyond. In International Conference on Learning Representations.

- Shalev-Shwartz and Ben-David [2014] Shalev-Shwartz, S. and Ben-David, S. (2014). Understanding machine learning: From theory to algorithms. Cambridge University Press.

- Wu et al. [2018] Wu, C., Luo, J., and Lee, J. D. (2018). No spurious local minima in a two hidden unit ReLU network.

- Zhang et al. [2019] Zhang, L., Liu, T.-Y., and Zhou, Z.-H. (2019). Adaptive regret of convex and smooth functions. In Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 7414–7423, Long Beach, California, USA. PMLR.

- Zhu and Xu [2015] Zhu, C. and Xu, H. (2015). Online gradient descent in function space. CoRR, abs/1512.02394.

- Zinkevich [2003] Zinkevich, M. (2003). Online convex programming and generalized infinitesimal gradient ascent. In Proceedings of the 20th International Conference on Machine Learning (ICML-03), pages 928–936.

- Zoghi et al. [2017] Zoghi, M., Tunys, T., Ghavamzadeh, M., Kveton, B., Szepesvari, C., and Wen, Z. (2017). Online learning to rank in stochastic click models. In Proceedings of the 34th International Conference on Machine Learning - Volume 70, ICML’17, pages 4199–4208. JMLR.

7 Appendix

A Extensions

We first introduce techniques to guarantee boundedness of the weight , i.e. how to remove condition 1 in Assumption 1. We then point out problems in the proofs of AMSGrad [22] and AdaBound [20] and provide a different proof for AMSGrad.

A.1 Unbounded Case

Projection is a popular technique to guarantee that a weight does not exceed a certain bound ([3], [13], [11], [20]). For unbounded weight , we introduce the following notation. Given convex sets , , vectors and matrix , we define projections

Projection is the standard projection which maps vector into set . If an optimal weight is such that , then we have

which could be directly applied in the proofs of Theorem 1 and 2.

For and , we could regard them as a combination of two standard projections. Note that, for the outer projection, we require that it does not affect the product of , which could be done by projection methods for linear equality constraints. In this way, we have

which could also be directly applied in the proofs of Theorem 3 and 4.

A.2 Standard setting of Adam

First, let us point out the problem in AMSGrad [22]. At the bottom of Page 18 in [22], the authors obtain an upper bound for the regret which has a term containing . Without assuming that is exponentially decaying, it is questionable to establish given since . Although this questionable term can be bounded by assumptions on , the last term in Theorem 4 is since is the concatenation of the gradients from 0 to current time in the coordinate. Moreover, the authors argue that decaying is crucial to guarantee the convergence, however, our proof shows regret for AMSGrad with constant and both constant and diminishing stepsizes, which is more practically relevant. For a diminishing stepsize, the slight change we need to make in the proof is that needs to be considered together with in (7) and the rest of proof of Theorem 2. Applying the fact that and yields regret in standard online setting.

Table 1 summarizes the various regret bounds in different convex settings.

B Regret with Rolling Window Analysis of OGD

Proof of Theorem 1

Proof.

For any and fixed , from step 4 in Algorithm 1, for any , we obtain

which in turn yields

| (4) |

Applying convexity of yields

| (5) |

By summing up all differences, we obtain

| (6) |

The second inequality holds due to 2 in Assumption 1 and the last inequality uses 4 in Assumption 1 and the definition of . Since (7) holds for any and , setting for each yields the statement in Theorem 1. ∎

C Regret with Rolling Window Analyses of convgAdam

Lemma 1.

Under the conditions assumed in Theorem 2, we have

Proof of Lemma 1.

By the definition of , for any , we obtain

| (7) |

The second equality follows from the updating rule of Algorithm 2. The second inequality follows from the Cauchy-Schwarz inequality, while the third inequality follows from the inequality . Using (7) for all time steps yields

| (8) |

We first bound the first term in (7) for each as follows,

| (9) |

The first inequality follows from the fact that and the last inequality is due to 2 in Assumption 1. Using a similar argument, we further bound the second term in (7) as follows,

| (10) |

Inserting (9) and (10) into (7) implies

This completes the proof of the lemma. ∎

In order to establish the regret analysis of Algorithm 2, we further need the following intermediate result.

Lemma 2.

Under the conditions in Theorem 2, we have

Proof of Lemma 2.

Proof of Theorem 2

Proof.

Based on the update step 8 in Algorithm 2 and given any , we obtain

| (11) |

The first inequality uses the same argument as those used in Theorem 1. Rearranging (11) gives

| (12) |

From the strong convexity property of in 4 in Assumption 1, we obtain

Using (7) in the above inequality and summing up over all time steps yields

| (13) |

We proceed by separating (13) into 3 parts and find upper bounds for each one of them. Considering the first part in (13), we have

| (14) |

Since is maximum of all for each until the current time step, i.e. , by using 1 in Assumption 1, (7) can be further bounded as follows,

By the definition of in step 6 in Algorithm 2, for any and , we have

which in turn yields

| (15) |

The last equality is due to the setting of the stepsize, i.e. . For the second term in (13), from the relationship between and , we obtain

which in turn yields

| (16) |

Thus, (16) guarantees negativity of the second term in (13). For the third term in (13), by using Lemmas 1 and 2, we assert

| (17) |

The desired result follows directly from (13), (15), (16) and (17). ∎

D Regret with Rolling Window Analysis of dnnOGD for Two-Layer ReLU Neural Network

For a two-layer ReLU neural network, we first introduce that records all previous iterates up until .

Proof of Lemma 3.

Lemma 4.

Under the conditions assumed in Theorem 3, we have

| (19) | ||||

| (20) |

Proof of Theorem 3

Proof.

First, based on the update step 6 and 7 in Algorithm 3, we obtain

| (21) |

By Lemma 4 we conclude that and are bounded due to 3 in Assumption 2, which in turn yields

| (22) |

where is a fixed positive number. The first inequality comes from the Cauchy-Schwarz inequality and the second inequality is due to the boundedness of , , , , , and . Inserting (22) into (21) gives

| (23) |

Using (19) yields

| (24) |

The last equality follows from (18) in Lemma 3. Then, we have

| (25) |

Note that by 3 in Assumption 2. If , then the inequality holds trivially. Using (23), (24) and (25) we obtain

| (26) |

From update step 6 we notice that , thus, (26) could be further simplified as

Applying the law of iterated expectation implies

By summing up all differences, we obtain

| (27) |

The last equality uses 3 from Assumption 2 and the definition of . The desired result in Theorem 3 follows directly from (27) since it holds for any .

∎

E Regret with Rolling Window Analyses of dnnAdam for Two-Layer ReLU Neural Network

Lemma 5.

In Algorithm 4, given and , there exists a bounded matrix such that

| (28) |

where is an element-wise multiplication operation.

Proof of Lemma 5.

From step 10 in Algorithm 4, is a matrix with same value in the same column, which in turn yields

where is a diagonal matrix with , and is the 1st row of matrix . Applying the same argument for yields (28). Next, let us show that is bounded. It is sufficient to show that is bounded. From steps 12 and 9, we conclude that

Therefore, it is sufficient to show that is bounded for all . For each entry in the matrix, since , we obtain

| (29) |

By combining with the fact that is bounded due to step 5 and the boundedness of and from condition 3 in Assumption 2, Lemma 5 follows. ∎

Lemma 6.

In Algorithm 4, given and for any , and and are constants between and such that and , then

| (30) | |||

| (31) | |||

| (32) | |||

| (33) |

Proof of Lemma 6.

Based on steps 6 - 12 in Algorithm 4, we obtain

| (34) | |||

| (35) | |||

| (36) | |||

| (37) |

Then, combining (34) and (36) yields

The first inequality follows from the definition of , which is maximum of all until the current time step. The third inequality follows from the Cauchy-Schwarz inequality and the forth inequality uses the fact that for any . Applying the same argument to implies (32). Then, applying the fact that yields

where the last inequality follows from (31). Lastly, implies . By combining (35) and (37), we get

∎

Proof of Theorem 4

Proof.

Now, let us multiply by , then take expectation given all records until time . Then, from steps 6 - 14, we obtain

| (38) | ||||

| (39) | ||||

| (40) | ||||

| (41) | ||||

| (42) |

Let us first consider the expectations in (41) and (42). From (29), we conclude that is bounded. Similarly, given and with , for each entry, we attain

Since , and are bounded from Lemma 6 and are also bounded from Assumption 2 and Lemma 5, applying Lemma 6 and Cauchy-Schwarz inequality yields

| (43) |

where is a fixed constant. Now, let us proceed to show an upper bound for the term in (39). Applying Lemma 5 to (39) yields

| (44) | ||||

| (45) |

Since and are all bounded, for the term in (44), there exists a constant such that

| (46) |

Next, let us bound the term in (45). Based on Lemma 6, we have

Now, let us focus on the product in the expectation. Since is a diagonal matrix, let us denote the element on diagonal as . Then,

where such that . Then, we obtain

Based on (29) and condition 5 from Assumption 2, we discover

| (47) |

which in turn yields

| (48) |

Note that in (47), we assume that is nonzero on the coordinate. On the other hand, if is zero on the coordinate, then it implies for on the coordinate, which in turn yields . Thus, (48) directly follows. Then, based on step 4 in Algorithm 4, we obtain

| (49) |

The last inequality follows by applying conditions 3 and 4 in Assumption 2. Next, Let us deal with the term in (40). Based on step 7 in Algorithm 4, we observe

| (50) | ||||

| (51) |

The last equality holds true due to (20) in Lemma 4. By using the fact that and are all bounded, for the term in (50), there exists a constant such that

| (52) |

At the same time, by inserting (18) from Lemma 3 into (51) we get

| (53) |

By inserting (43),(46),(49), (52), and (53), into (38) we obtain

Since , which in turn yields

Therefore, by recalling the law of iterated expectations and summing up all loss functions for , we get

| (54) |

Applying the definition of and implies

| (55) |

Since , we notice that . Applying Lemma 5 yields

| (56) |

where represents the element on diagonal in matrix and represents the coordinate in vector . Since and are all bounded for any , e.g. and due to the fact that , (56) can be further simplified as

| (57) |

Substituting (55) and (57) in (54) gives

| (58) |

The last equality uses the definition of . The desired result in Theorem 3 follows directly from (58) since it holds for any . ∎