Pricing and hedging of VIX options for Barndorff-Nielsen and Shephard models

Abstract

The VIX call options for the Barndorff-Nielsen and Shephard models will be discussed. Derivatives written on the VIX, which is the most popular volatility measurement, have been traded actively very much. In this paper, we give representations of the VIX call option price for the Barndorff-Nielsen and Shephard models: non-Gaussian Ornstein–Uhlenbeck type stochastic volatility models. Moreover, we provide representations of the locally risk-minimizing strategy constructed by a combination of the underlying riskless and risky assets. Remark that the representations obtained in this paper are efficient to develop a numerical method using the fast Fourier transform. Thus, numerical experiments will be implemented in the last section of this paper.

Keywords: VIX, VIX options, Stochastic volatility models, Barndorff-Nielsen and Shephard models, Local risk-minimization, Fast Fourier transform.

1 Introduction

Our main objectives are to provide numerically efficient representations of the prices and the locally risk-minimizing (LRM) strategies for the VIX call options for the Barndorff-Nielsen and Shephard (BNS) models, and implement numerical experiments using the fast Fourier transform (FFT).

The BNS models are non-Gaussian Ornstein–Uhlenbeck (OU)-type stochastic volatility models undertaken by Barndorff–Nielsen and Shephard [7], [8]. More precisely, we consider throughout a financial market model composed of one riskless asset with interest rate and one risky asset whose price at time , denoted by , is expressed as

| (1.1) |

where , , and . Here, is a -dimensional Brownian motion, and is a subordinator without drift. The squared volatility process is given by an OU process driven by , that is, the solution to the following equation:

with . In this paper, we take so that the discounted asset price process , denoted by , becomes a martingale. Thus, for any option matured at time , its price at time is given by , where is a filtration. On the other hand, since our underlying market is incomplete, there is no perfect hedge in general. Instead, we consider an alternative hedging strategy, which is not perfect, but optimal in some sense. Actually, many such hedging strategies for incomplete market models have been suggested. Among them, we focus on the LRM strategy, which is a very well-known quadratic hedging method. In particular, its theoretical aspects have been well developed, but little is known about its explicit representations. Meanwhile, Arai et al. [2] gave a representation of the LRM strategies for call options for BNS models using Malliavin calculus for Lévy processes, and illustrated an FFT-based numerical method.

Now, the VIX is the most popular volatility measurement launched by the Chicago Board Options Exchange (CBOE) [11]. More precisely, it is defined as the square root of the expected value of integrated variance of the S&P 500 index over the next 30 business days. In this paper, the VIX at time , denoted by , is defined as the integrated variance over the time interval , where is the fixed observation period. As seen in Section 2, the mathematical definition of the square of is naturally given as

| (1.2) |

In addition, the right-hand side of (1.2) is rewritten as

| (1.3) |

Remark that the second term is due to the jump component of (1.1). It is well-known that changes of the VIX are negatively correlated to changes in asset prices, but it is not directly investable. Thus, trades of derivatives written on the VIX are inevitable in order to reduce risks caused by changes of volatility. Actually, such derivatives have been traded actively very much, and there are much literature on this topic. In this paper, we focus on the European-type call options written on the VIX, of which payoff is described as , where is maturity and is strike price; and provide representations of their prices and LRM strategies for the BNS models by extending results in [2], where the LRM strategies discussed in this paper are given by a combination of the underlying riskless and risky assets. In particular, our representations obtained in this paper are efficient to develop an FFT-based numerical method.

Pricing and hedging problems of derivatives on the VIX or volatilities for jump type models have already been studied by a number of researchers ([6], [13], [14], [17], [19], [26], [27], [30] and so forth). Among them, Lian and Zhu [20] derived a pricing formula of the VIX call options for the so-called SVJJ models, in which the asset price process is given as the solution to the following stochastic differential equation (SDE):

| (1.4) |

where , is a -dimensional Brownian motion, is a compound Poisson process. Note that their formula was obtained as a correction of [21]. In addition, [10] also pointed out errors of [21]. Here, in (1.4) is a volatility process given from the solution to the following SDE:

where , and are constants satisfying the Feller condition

is a -dimensional Brownian motion correlated to , and is a compound Poisson process generated by the same Poisson process as , that is, jumps of and happen simultaneously. Remark that this model framework does not include the BNS models.

As another literature, Barletta and Nicolato [5] also considered the same model framework as [20], and derived a closed-form pricing formula using approximations via orthogonal expansions. Kallsen et al. [18] studied pricing of options written on the quadratic variation of a given asset price process for affine stochastic volatility models with jumps. In particular, they illustrated numerical experiments for BNS models. Benth et al. [9] obtained a valuation formula for conditional expectations of powers of the realized volatility

for the BNS models without jumps, that is, the case where . Note that the realized volatility used in [9] is different from the VIX defined in (1.3). Moreover, Habtemicael and SenGupta [15] and Issaka and SenGupta [16] studied the variance swap and the volatility swap for the BNS models with jumps, where is delivery price. In particular, [16] derived a partial integro-differential equation describing the price dynamics of the variance swaps, and a Večeř-type formula. To our best knowledge, any representations of the prices and the LRM strategies of the VIX call options for the BNS models have not been provided. In particular, no one has discussed the LRM strategies for the VIX options for jump-type stochastic volatility models.

The rest of the paper is organized as follows: In Section 2, we give model description, and discuss the VIX. Our main results, that is, representations of the prices and the LRM strategies of the VIX call options are given in Sections 3 and 4, respectively. Section 5 is devoted to numerical results.

2 Preliminaries

2.1 Model description

We consider, throughout this paper, a financial market being composed of one riskless asset with interest rate and one risky asset whose price dynamics is described by (1.1). Note that the risky asset price process is also given as the solution to the following SDE:

| (2.1) |

Here denotes the Poisson random measure of the subordinator , that is,

holds for , is the Lévy measure of ; and is the compensated version of , which is represented as

Remark that the last term in (1.1) accounts for the leverage effect, which is a stylized fact such that the asset price declines at the moment when volatility increases. In this paper, we treat only the case where the discounted asset price process () becomes a martingale. In other words, is assumed to be given as . Thus, (2.1) implies that the dynamics of is given by

Remark 2.1

We shall use Malliavin calculus based on the canonical Lévy space, undertaken by Solé et al. [28]. Thus, the underlying probability space is supposed to be given as the product space , where and are a one-dimensional Wiener space and the canonical Lévy space for the pure jump Lévy process , respectively. A filtration denotes the canonical filtration completed for . Although the results obtained in this paper are basically not depending on the structure of the underlying probability space, we choose the canonical Lévy space framework in order to simplify mathematical description and discussion. For example, it is possible to use results on the canonical Lévy space introduced in Arai and Suzuki [3], Delong and Imkeller [12] and Suzuki [29].

As seen in Introduction, the volatility process in (2.1) is a square root of an OU process driven by the subordinator . Now, we introduce two important examples of the squared volatility process appeared in BNS models. For more details on this topic, see also Schoutens [23] and Nicolato and Venardos [22].

-

1.

The first one is the case where follows an IG-OU process. The corresponding Lévy measure is given by

where and . Note that this is a representative example of BNS models with infinite active jumps, that is, . In this case, the invariant distribution of follows an inverse-Gaussian distribution with parameters and .

-

2.

The second example is the gamma-OU case. In this case, is described as

and the invariant distribution of is given by a gamma distribution with parameters and .

2.2 VIX

In this subsection, we discuss the reason why the VIX is defined as in (1.2), and show that (1.3) holds for the BNS models. To this end, we firstly consider a continuous-type stochastic volatility model in which the discounted asset price process is given as

Note that we do not need to specify the volatility process . The square of the VIX for this model, denoted by , is naturally defined as

for , where is the observation period. By simple calculation, we have

| (2.2) |

On the other hand, due to the jump component, the integrated variance over for the BNS models is different from . Thus, taking account of (2.2), we define the square of the VIX for the BNS models as in (1.2). In order to treat the VIX on the time interval , the processes and should be defined on the extended time interval , where is the maturity of the option to be priced and hedged.

3 Pricing

The aim of this section is to provide two representations of the prices of the VIX call options for the BNS models. Note that our representations are efficient to develop an FFT-based numerical scheme. Firstly, we give an integral expression under an integrable condition on the characteristic function of . Note that this condition is satisfied in the IG-OU case, but not in the gamma-OU case. Thus, we suggest alternatively an approximate method in order to treat the gamma-OU case.

Consider the VIX call option matured at time with strike price . Then, its payoff is described as ; and its price at time , denoted by , is given as follows:

In addition, we define the Fourier transform of the payoff function of the VIX call option as

for and . Note that, since is positive, is defined as an integration on instead of ; and it is enough to treat only the case where . A concrete expression of is given as follows:

Lemma 3.1

For any , and , we have

where

In order to give an expression of , we need to define the conditional characteristic function of given as

for . Lemma 2.1 of [22] implies that, denoting

we have

| (3.1) |

for any with , where

Now, has the following integration expression:

Proposition 3.2 (Proposition 2 of Tankov [31])

Suppose that and

| (3.2) |

for any and . We have then

| (3.3) |

for any , and . Note that the right-hand side of (3.3) is independent of the choice of .

Remark 3.3

Remark 3.4

As another important derivative written on the VIX, the VIX futures has been traded actively. Its value at time is denoted by

which is corresponding to the price of the VIX call option with strike price when the interest rate is also . Thus, (3.3) implies that

holds under all the conditions of Proposition 3.2.

We show that the IG-OU case introduced in Subsection 2.1 satisfies all the conditions of Proposition 3.2, that is, the VIX option prices for the IG-OU case are described as (3.3).

Example 3.5

Firstly, (2.8) of [22] implies that

for , which means . Next, we show that the condition (3.2) is satisfied for any , . To this end, we calculate for with as follows:

| (3.4) | ||||

where and . Taking and , we substitute for to estimate the real part of the integrand of (3.4). We then can find a constant such that

for any and any with sufficient large . Consequently, the IG-OU case always satisfies (3.2) from the view of (3).

For the gamma-OU case, which is another typical framework of the BNS models, the condition (3.2) is not satisfied as seen in Example 3.8 below, that is, the right-hand side of (3.3) is not well-defined. To overcome this difficulty, we develop an approximate method by replacing with , denoted by , for sufficient small . To this end, we need to consider the VIX of , instead of . Since might take negative values, we rewrite the payoff of the VIX call options as

and define

for . We have then

which means that computing for sufficient small gives the value of approximately. Now, we show that has the same type integral representation as (3.3).

Proposition 3.6

Suppose that , and, for any and , there exists a constant such that

| (3.5) |

for any . We have then

| (3.6) |

for , and . Note that the right-hand side of (3.6) is independent of the choice of .

Proof. Denoting

| (3.7) |

for , and , we have

which implies that

holds for any , and by the condition (3.5). As a result, we obtain (3.6) using Proposition 3.2.

Remark 3.7

Considering

for instead of , we expect that it gives a good approximation for by computing for sufficient large , since integrations on are computed numerically by truncating the integration interval. However, never converges to as tends to for the gamma-OU cases.

We see that the gamma-OU case satisfies all the conditions of Proposition 3.6. As a result, we can compute the values of numerically using the integral expression (3.6), which approximates the values of when is small enough.

Example 3.8

Recall that the Lévy measure in the gamma-OU case is described as

for , . By (2.10) of [22],

holds for , and , which is positive. For with , we have

| (3.8) | ||||

where , , and

Thus, we have

| (3.9) |

As a result, for and , substituting for in (3.9), we obtain

which is bounded on . Hence, (3) implies that the gamma-OU case does not satisfy (3.2), but does (3.5) for any , .

4 LRM strategies

In this section, representations of the LRM strategies for the VIX call options are discussed. A definition of the LRM strategies is given in Appendix A.2. Note that hedging strategies discussed in this paper are constructed by the underlying riskless and risky assets. For any , we denote by the value of the LRM strategy at time for the VIX call option matured at time with strike price . In other words, an investor hedging the VIX call option in the LRM approach should hold units of the risky asset at time . On the other had, once is given, we can compute the amount of units of the riskless asset at time through (A.2). Thus, we give representations of alone.

Under the condition (3.2), a representation of is given as follows:

Theorem 4.1

Proof. This theorem is shown by Theorem A.1 of [2] (see also Theorem 3.7 of [3]). Thus, we confirm if all the conditions of Theorem A.1 of [2] are satisfied in our setting. Firstly, AS1 and AS2 are automatically satisfied, since is a martingale, and and by Lemma 4.4 below, where and are the Sobolev space and the Malliavin derivative operator respectively, defined in Appendix A.1. As for AS3, (4.5) below implies that

for any . Since holds, we have

which implies the condition AS3. In addition, we need to notice that Theorem A.1 of [2] holds under their Assumption 2.2, which is satisfied in our setting under the condition (4.1). Remark that we can omit Item 2 of Assumption 2.2 of [2], since is a martingale. Moreover, we do not need the finiteness of , since it has been used to show AS2 in [2]. Consequently, Theorem A.1 of [2] is available.

Theorem A.1 of [2] implies that exists, and

| (4.3) |

holds, since by Lemma 4.4. Denoting

for and , and using Lemma 4.4 and (2.4), we can rewrite (4.3) as

| (4.4) |

Remark that

Thus, from the view of Proposition 3.2, denoting , we can rewrite (4) as

for . This completes the proof of Theorem 4.1.

Remark 4.2

Remark 4.3

Lemma 4.4

For any and , we have and

| (4.5) |

where . Note that the definitions of the space and the operator are given in Appendix A.1.

Proof. First of all, we show ; and calculate for and . Now, we define for , that is, . Note that we can extend to a -function on with bounded derivative . Thus, since and by Lemma A.2 of [2], Proposition 2.6 of [29] implies that ,

and

for . Hence, Theorem 4.1 of [3] implies that

from which we obtain (4.5).

Next, we provide an approximate representation of under the condition (3.5) instead of (3.2). This representation enables us to compute approximately for the gamma-OU case.

Theorem 4.5

5 Numerical experiments

Our aim of this section is to compute the prices and the LRM strategies by using the FFT. First of all, we introduce its basic idea by taking given in (3.3) as an example. Defining a function as

for , we have

In addition, defining the Fourier transform of as

we can rewrite (3.3) as

Thus, we can compute with the FFT.

Remark 5.1

Considering the vanilla option written on the underlying asset , its price is given as

by Example 2 of [31], where is the conditional characteristic function of . This is computable with a Fourier transform on . Hence, for computation on the VIX options, the FFT is used in a different way from the case of other options.

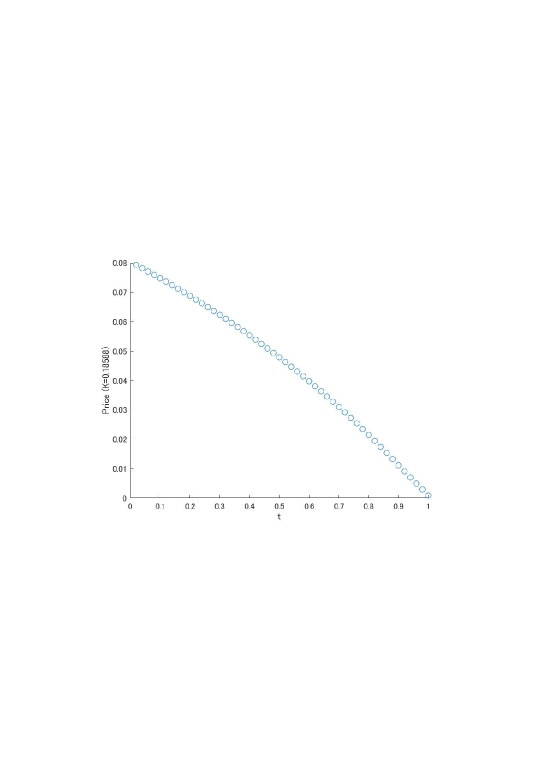

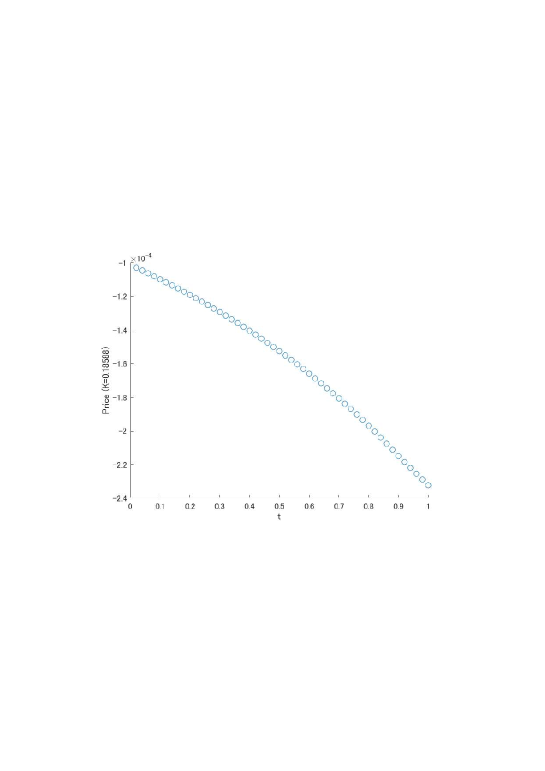

Next, we implement numerical experiments on the prices and the LRM strategies for the gamma-OU case by computing the right-hand sides of (3.6) and (4.5) respectively with sufficient small . We use the parameter set estimated in [23], that is, we set , , , . Moreover, we fix , . This parameter set satisfies the condition (4.7). Moreover, is set to 1.75, and the observation period appeared in the definition of the VIX is fixed to , which is approximately one month. In our numerical experiments, the asset price and the squared volatility at time are fixed to and respectively, even if time may change. Note that the values of the VIX at time is 0.18588. We compute the right-hand sides of (3.6) and (4.5) with to obtain the values of and approximately.

The following two types of experiments are implemented: First, we compute the values of and for times when the option is at the money, that is, is fixed to 0.18588. See Figures 4 and 4. Second, is fixed to 0.5, and we instead vary from 0.12 to 0.3 at steps of 0.02, and compute and . See Figures 4 and 4. As seen in Figures 4 and 4, the values of the LRM strategies are negative, since the VIX and the underlying risky asset have a negative correlation.

Appendix A Appendix

A.1 Malliavin calculus

We introduce Malliavin calculus for Lévy processes briefly. As stated in Remark 2.1, we consider Malliavin calculus based on the canonical Lévy space, undertaken by [28]. For more details on this topic, see [12], [28] and [29].

To begin with, we define two measures and on as

and

where and is the Dirac measure at . For , we denote by the set of product measurable, deterministic functions satisfying

For and , we define

Formally, we denote and for . Under this setting, any square integrable -measurable random variable has the unique representation

with functions that are symmetric in the pairs , and we have

We define the Sobolev space and Malliavin derivative operator as follows:

Definition A.1

-

1.

Let denote the set of -measurable random variables with satisfying

-

2.

For any , the Malliavin derivative is defined as

for -a.e. , -a.s.

A.2 Definition of the LRM strategy

Before providing a definition of the LRM strategy, we prepare some terminologies.

Definition A.2

-

1.

A strategy is defined as a pair , where is a predictable process, and is an adapted process. Note that and represent the amount of units of the risky and the riskless assets respectively which an investor holds at time . The discounted value of the strategy at time is defined as

In particular, gives the initial cost of .

-

2.

A strategy is said to be self-financing, if it satisfies

for any , where denotes the discounted gain process induced by , that is,

for . If a strategy is self-financing, then is automatically determined by and the initial cost .

-

3.

For a strategy , a process defined by

for is called the discounted cost process of . When is self-financing, its discounted cost process is a constant.

-

4.

Let be a square integrable random variable representing the payoff of a contingent claim at the maturity . A strategy is said to replicate the claim , if it satisfies , where the discounted value of .

Finally, we give a definition of the LRM strategy . Roughly speaking, a strategy , which is not necessarily self-financing, is called the LRM strategy for the claim , if it is the replicating strategy minimizing a risk caused by in the -sense among all replicating strategies. The following definition is a simplified version based on Theorem 1.6 of Schweizer [25] under the assumption that is a martingale, since the original one introduced by Schweizer [24] and [25] is rather complicated. Note that [25] treated the problem under the assumption that . For the case where , see, e.g. Biagini and Cretarola [4].

Definition A.3

-

1.

A strategy is said to be an -strategy, if is a predictable process satisfying

(A.1) and is an adapted process such that is a right continuous process with for every .

-

2.

An -strategy is called the LRM strategy for the claim , if , and is a uniformly integrable martingale.

-

3.

admits a Föllmer-Schweizer decomposition, if it can be described by

where , is a predictable process satisfying (A.1) and is a square-integrable martingale orthogonal to with .

Then, Proposition 5.2 of [25] or Proposition 3.7 of [4], together with Remark 2.3 of [2], provides that, under the condition (4.1), the LRM strategy for exists if and only if () admits a Föllmer-Schweizer decomposition

and its relationship is given by

| (A.2) |

As a result, it suffices to obtain a representation of in order to get . Thus, we identify with in this paper.

Acknowledgments

The author gratefully acknowledges the financial support of the MEXT Grant in Aid for Scientific Research (C) No.15K04936 and No.18K03422.

References

- [1] Arai, T., Imai, Y., & Suzuki, R. (2016). Numerical analysis on local risk-minimization for exponential Lévy models. International Journal of Theoretical and Applied Finance, 19(02), 1650008.

- [2] Arai, T., Imai, Y., & Suzuki, R. (2017). Local risk-minimization for Barndorff-Nielsen and Shephard models. Finance and Stochastics, 21(2), 551-592.

- [3] Arai, T., & Suzuki, R. (2015). Local risk-minimization for Lévy markets. International Journal of Financial Engineering, 2(02), 1550015.

- [4] Biagini, F., & Cretarola, A. (2012). Local risk-minimization for defaultable claims with recovery process. Applied Mathematics & Optimization, 65(3), 293-314.

- [5] Barletta, A., & Nicolato, E. (2018). Orthogonal expansions for VIX options under affine jump diffusions. Quantitative Finance, 18(6), 951-967.

- [6] Barletta, A., Nicolato, E. & Pagliarani, S. (2018) The short-time behavior of VIX-implied volatilities in a multifactor stochastic volatility framework. to appear in Mathematical Finance.

- [7] Barndorff-Nielsen, O. E., & Shephard, N. (2001). Modelling by Lévy processess for financial econometrics. In Lévy processes (pp. 283-318). Birkhäuser, Boston, MA.

- [8] Barndorff-Nielsen, O. E., & Shephard, N. (2001). Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63(2), 167-241.

- [9] Benth, F. E., Groth, M., & Kufakunesu, R. (2007). Valuing Volatility and Variance Swaps for a Non-Gaussian Ornstein-Uhlenbeck Stochastic Volatility Model. Applied Mathematical Finance, 14(4), 347-363.

- [10] Cheng, J., Ibraimi, M., Leippold, M., & Zhang, J. E. (2012). A remark on Lin and Chang’s paper ‘Consistent modeling of S&P 500 and VIX derivatives’. Journal of Economic Dynamics and Control, 36(5), 708-715.

- [11] Chicago Board Options Exchange (2009). The CBOE volatility index-VIX. White Paper (available at www.cboe.com/micro/vixS)

- [12] Delong, Ł., & Imkeller, P. (2010). On Malliavin’s differentiability of BSDEs with time delayed generators driven by Brownian motions and Poisson random measures. Stochastic Processes and their Applications, 120(9), 1748-1775.

- [13] Detemple, J., & Kitapbayev, Y. (2018). On American VIX options under the generalized 3/2 and 1/2 models. Mathematical Finance, 28(2), 550-581.

- [14] Goard, J., & Mazur, M. (2013). Stochastic volatility models and the pricing of VIX options. Mathematical Finance, 23(3), 439-458.

- [15] Habtemicael, S., & SenGupta, I. (2016). Pricing variance and volatility swaps for Barndorff-Nielsen and Shephard process driven financial markets. International Journal of Financial Engineering, 3(04), 1650027.

- [16] Issaka, A., & SenGupta, I. (2017). Analysis of variance based instruments for Ornstein-Uhlenbeck type models: swap and price index. Annals of Finance, 13(4), 401-434.

- [17] Jacquier, A., Martini, C., & Muguruza, A. (2018). On VIX futures in the rough Bergomi model. Quantitative Finance, 18(1), 45-61.

- [18] Kallsen, J., Muhle-Karbe, J., & Voß, M. (2011). Pricing options on variance in affine stochastic volatility models. Mathematical Finance, 21(4), 627-641.

- [19] Li, J., Li, L., & Zhang, G. (2017). Pure jump models for pricing and hedging VIX derivatives. Journal of Economic Dynamics and Control, 74, 28-55.

- [20] Lian, G. H., & Zhu, S. P. (2013). Pricing VIX options with stochastic volatility and random jumps. Decisions in Economics and Finance, 36(1), 71-88.

- [21] Lin, Y. N., & Chang, C. H. (2010). Consistent modeling of S&P 500 and VIX derivatives. Journal of Economic Dynamics and Control, 34(11), 2302-2319.

- [22] Nicolato, E., & Venardos, E. (2003). Option pricing in stochastic volatility models of the Ornstein-Uhlenbeck type. Mathematical Finance, 13(4), 445-466.

- [23] Schoutens, W. (2003). Lévy processes in finance: pricing financial derivatives. John Wiley & Sons, Hoboken.

- [24] Schweizer, M. (2001). A guided tour through quadratic hedging approaches, In Option pricing, interest rates and risk management (E. Jouini, J. Cvitanic, and M. Musiela, eds.) (pp. 538–574). Cambridge University Press, Cambridge.

- [25] Schweizer, M. (2008). Local risk-minimization for multidimensional assets and payment streams. Banach Cent. Publ, 83, 213-229.

- [26] Sepp, A. (2008). VIX option pricing in a jump-diffusion model. Risk Magazine, Risk Magazine, April 2008, 84-89.

- [27] Sepp, A. (2012). Pricing options on realized variance in the heston model with jumps in returns and volatility-part ii: An approximate distribution of discrete variance. Journal of Computational Finance, 16(2), 3-32.

- [28] Solé, J. L., Utzet, F., & Vives, J. (2007). Canonical Lévy process and Malliavin calculus. Stochastic processes and their Applications, 117(2), 165-187.

- [29] Suzuki, R. (2013). A Clark-Ocone type formula under change of measure for Lévy processes with -Lévy measure. Communications on Stochastic Analysis, 7(3), 383–407.

- [30] Swishchuk, A. V., & Wang, Z. (2017). Variance and Volatility Swaps and Futures Pricing for Stochastic Volatility Models. Available at SSRN 3084186.

- [31] Tankov, P. (2011). Pricing and hedging in exponential Lévy models: review of recent results. In Paris-Princeton Lectures on Mathematical Finance 2010 (pp. 319-359). Springer, Berlin, Heidelberg.