Dynamically optimal treatment allocation using Reinforcement Learning

Abstract.

Dynamic decisions are pivotal to economic policy making. We show how existing evidence from randomized control trials can be utilized to guide personalized decisions in challenging dynamic environments with constraints such as limited budget or queues. Recent developments in reinforcement learning make it possible to solve many realistically complex settings for the first time. We allow for restricted policy functions and prove that their regret decays at rate , the same as in the static case. We illustrate our methods with an application to job training. The approach scales to a wide range of important problems faced by policy makers.

Keywords. Policy learning, Reinforcement learning, Program evaluation

We would like to thank Facundo Albornoz, Tim Armstrong, Debopam Bhattacharya, Xiaohong Chen, Denis Chetverikov, Wouter Den Haan, Frank Diebold, John Ham, Stephen Hansen, Toru Kitagawa, Anders Bredahl Kock, Damian Kozbur, Franck Portier, Marcia Schafgans, Frank Schorfheide, Aleksey Tetenov, Brendan Tracey, Alwyn Young and seminar participants at Brown, University of Pennsylvania, Vanderbilt, Yale, Greater NY area Econometrics conference, Bristol Econometrics study group, the HSG causal machine learning workshop, AEA-ESEM meetings, and the CEMMAP/UCL workshop on Personalized Treatment for helpful comments.

All relevant code for this paper can be downloaded from:

https://github.com/friedrichgeiecke/dynamic_treatment.

Supplementary material for this paper (not intended for publication) can be accessed here.

⋆Department of Economics, University of Pennsylvania; akarun@sas.upenn.edu

†Department of Methodology, London School of Economics; f.c.geiecke@lse.ac.uk

‡Department of Economics, University of Zurich; claudio.schilter@econ.uzh.ch

1. Introduction

Many important and challenging policy problems involve dynamic decision making. A healthcare system may need to manage queues in emergency situations or prioritize specific treatments under capacity constraints, an aid agency may want to distribute funds over time while facing borrowing constraints, a policy maker may need to assign job-training under limited budget to people who become unemployed sequentially. These settings are dynamic programming problems. A policy maker needs to make sequential decisions to maximize welfare, and her decisions affect future states (e.g. deplete a budget or increase queue length). If allocations in these problems could be improved, welfare gains for societies would be substantial. Yet, in real world applications, the number of potential state variables is often very large. A lot of information is available for individualizing decisions and should be taken into account. For instance, it is clearly beneficial for a medical administrator to induce different waiting times for patients with numerous different characteristics, symptoms, and medical histories.

This paper provides a framework for obtaining individualized treatment rules in dynamic settings. We describe both theoretical and computational tools for attacking these problems. Recent advances in reinforcement learning (RL) allow us to solve many realistically complicated decision problems for the first time. Like other methods, RL is a tool to obtain policy functions for dynamic programming problems. Yet, it can find policy functions for state spaces otherwise entirely out of reach (e.g., the policy function in Degrave et al (2022) has around 150 continuous state variables). As a result, RL has been the driving force behind many very prominent recent advances in artificial intelligence, e.g. mastering Go and Chess at previously unseen levels and without human knowledge, or controlling plasma in a nuclear fusion reactor (Silver et al, 2017; Silver et al, 2018; Degrave et al, 2022).

The contribution of the paper is twofold: (1) It is the first to show that it is possible to combine RL with RCT data to characterize optimal decisions in many highly relevant and challenging dynamic problems faced by economic policy makers. This has the potential to be a powerful aid. In addition, the combination of RL and causal inference developed in this paper is a deep necessity for the applications we consider. An important reason why RL breakthroughs so far have been seen in games, physical systems, or theoretical models is that in these environments the effects of a policy’s actions are known (e.g. through a physical model). We are able to expand the use of this technology into other real world domains only because tools from causal inference allow us to estimate the causal effect of the policy’s actions on its environment. In other words, we can only build our simulation to train an RL policy based on empirical data, because the RCT allows us to estimate the causal effect of the policy’s actions.111This could also open the door to use the approach in other domains beyond the scope of this paper. Common trainings grounds for building and benchmarking different RL algorithms e.g. require the policy to learn controlling simulated pendulums, spaceships, or humanoid figures (see e.g. Brockman et al, 2016). With RCTs and causal inference it is possible to build different types of training grounds. (2) We provide the necessary theoretical support that our policy rule approaches the optimal welfare as the sample size of the RCT data grows (and approaches it relatively fast, which is important in practice). To obtain this, we study a suitable limiting version of the dynamic programming problem by following recent literature and taking the rate of arrivals to infinity (Wager and Xu, 2021; Fan and Glynn, 2021; Adusumilli, 2022), resulting in a continuous time approximation of the problem. Exploiting Partial Differential Equation (PDE) methods in a novel manner, we are able to prove that regret222Regret is defined as the difference in welfare from using the estimated policy rule, relative to the optimal policy within a candidate class of policy rules. decays at a rate, where is the sample size of the RCT. This is the same rate as in the setting without dynamics though it is not obvious a priori that the rate should continue to apply, since, under dynamics there is a great deal of dependence - the covariates of any individual affect the actions for all subsequently arriving individuals (e.g., by depleting the budget).333Our primary interest in this paper is on estimation error and we do not present results on the effect of computational errors on regret. Theoretical results on the accuracy of A3C under realistic assumptions is still an active area of research. Also, all computational errors could in principle be reduced to 0 with enough computational time.

Our methodology is based on offline learning of the policy function (i.e., training the algorithm on existing data rather than experimenting live/online). There is a large and important literature on bandit algorithms for online learning, see e.g., Agarwal et al (2014), Russo and van Roy (2016), and Lattimore and Szepesvari (2021). This literature aims to learn the (heterogenous) treatment effects sequentially. However, our setup is different in that resource constraints evolve dynamically, e.g., the budget is depleted as more individuals are treated. These constraints do not affect the outcomes but constrain future actions, and standard bandit algorithms do not account for such variables. The focus of this paper is on devising algorithms that are dynamically optimal under resource constraints. To make headway on this problem we start with offline learning, though many of our insights extend to online learning as well (see Appendix E.2).

There are also good reasons why it is important to study offline learning in its own right. First, a large literature in RL has argued that sample efficient algorithms need to involve aspects of both online and offline learning, see e.g., Sutton and Barto (2018, Chapter 8), Yu et al, (2020) and Kidambi et al (2020). Online learning by itself is not welfare efficient; it would require prohibitively many rounds of experimentation to visit all states (e.g., all possible budgets) and it would not even be welfare optimal to do so. In our setting, the law of motion for state variables (i.e., how the budget changes) is known beforehand, so we can combine this with offline data to simulate dynamic environments. In fact, some of the best performing RL algorithms use techniques such as experience replay (Mnih et al, 2015), which is a form of offline learning. Second, online learning is not feasible if the outcomes are only known after a long gap (in our empirical example it is 3 years). Third, government agencies often need to be transparent about the rules being used and dynamically updating them in view of new data in real time might not be a realistic possibility. Finally, if subsequent online learning is desired to fine-tune the policy with newer data, our algorithm can be modified for this purpose as well. Still, a key feature of the approach is its ability to utilize large amounts of readily existing RCT data. If such RCT data already exists, at least initialising the training of policy parameters with it can reduce welfare costs of new experimentation.

With dynamic constraints being common across governmental and non-governmental settings, the following examples illustrate the generality of our approach:

Example 1.1.

(Finite budget) A social planner has received a one-off outlay of funds for providing treatment to individuals. Since the planner’s actions influence future states, in this case budget, this is a dynamic programming problem. The planner faces a trade-off in terms of using some of the funds to treat an individual immediately, or holding off until a more deserving individual arrives in the future. The future individuals’ utility is discounted. The planner would like a policy rule for treating individuals as a function of the individual covariates and current budget.

Two aspects of this example are worth highlighting: First, existing methods cannot be applied here even if the planner restricts consideration to stationary policy rules that are only a function of individual’s characteristics (by contrast, we call a policy non-stationary if it changes with budget or time). Techniques such as Empirical Welfare Maximization (EWM, Kitagawa and Tetenov, 2018), solve a simultaneous allocation problem where the policy rule is meant to be applied simultaneously on the population. Here, budget or capacity constraints are modeled as a constraint on the fraction of the population that can be treated. But in the present example, there is no set number to the population as individuals arrive sequentially, and hence no notion of a population fraction. Even more importantly, these methods cannot take into account the effect of discounting (see, Section 2.1 for a formal discussion). If the discount factor is small, it is optimal to wait for the people having the highest expected outcomes (based on their covariates) to turn up. If the discount factor is high, it would be optimal to treat anyone who is expected to benefit from the treatment. Discounting is an inherently dynamic consideration that has no counterpart in a fixed sample.

Second, stationary rules are inferior in terms of welfare to non-stationary rules that change with budget. When the budget is low, it is optimal to be more selective in treatment as opposed to when budget is high. A policy rule that changes continuously with budget can therefore deliver higher welfare. In an empirical illustration of this example in Section 6, we find that a non-stationary rule can deliver a welfare gain as high as 24% over a stationary one. Administratively, stationary rules are easier to communicate, so policy makers might favor stationary policies if the welfare loss is relatively small. Our method allows us to compute both and assess whether the additional welfare gain is worth having to justify the use of non-stationary rules which imply different policies at different points in time.

Example 1.2.

(Borrowing constraints) A social planner receives a steady flow of revenue, with individuals arriving at a constant rate. The planner is subject to a borrowing constraint. The optimal stationary policy maximizes welfare subject to the constraint that expected costs equal expected revenue. Under such a stationary policy, the budget would set off on a random walk, since the individuals are i.i.d. draws from a distribution, and the expected change to budget is 0 only on average. This implies the budget may accumulate to high levels, or hit the borrowing constraints over extended periods, both of which are sub-optimal. In fact, it is easy to verify that to achieve optimal welfare, the budget process needs to be controlled so it always takes on a constant value that is close to the borrowing constraint. Our methods enable us to solve for such a policy rule.

Example 1.3.

(Finite horizon) A planner receives an operating budget for each period, e.g. a year. Any unused funds will be sent back at the end of the year (this could be an approximation for how some governmental programs are run, with a budget outlay legislated at the beginning of each fiscal year). The planner would like to know the optimal policy rule for allocating treatments.

Example 1.4.

(Queues) Suppose the amount of time needed to treat an individual is longer than the average waiting time between the arrivals of two individuals. For instance, the treatment could be a medical procedure that takes time, or an unemployment service that requires the individual to meet with a caseworker. The social planner thus places the individuals selected for treatment in a queue. It is then useful to turn people away from treatment if the length of the queue is too long. Given some known or estimable cost of waiting, the planner would like to determine the optimal rule for whether or not to place an individual in a queue, as a function of the individual characteristics and the current waiting times. Generalizing the above, the planner may also want to allow for multiple queues, with the shorter queues reserved for individuals deemed more at risk.

In all these examples, we show how one can leverage RCT data to estimate the policy function that maximizes expected welfare. Beyond the issues highlighted above, our methods also allow for time varying rates of arrivals, time varying distributions of covariates, and uncertainty in arrival rates.

We discuss algorithms to minimize regret within a pre-specified policy class. As explained by Kitagawa and Tetenov (2018), one may wish to do this for ethical or legal reasons. Another reason is incentive compatibility - the planner may prefer a stationary policy (that depends only on covariates) to prevent manipulation of arrival times. For non-stationary policies, we assume the policy does not affect the arrival rates and the covariate distribution of individuals. This is reasonable in settings like unemployment, arrivals to emergency rooms etc., where the time of arrival is determined by factors exogenous to the provision of treatment.

In simple settings - see, e.g., Section 6 - the optimal policies can be estimated exactly (i.e., without numerical error) using PDE methods. But even with a moderate number of state variables, this quickly becomes infeasible. Hence, for computation, we utilise RL, namely an Actor-Critic (AC) algorithm (e.g., Sutton et al, 2000) with a parallel implementation - known as A3C (Mnih et al, 2016) - that can solve for the optimal policy within a pre-specified policy class. Our implementation of the algorithm is informed by our PDE theory, which enables us to achieve dimension reduction in the value function.

We illustrate the feasibility of our methodology using data from the Job Training Partnership Act (hereafter JTPA). We incorporate dynamic considerations into this setting in two ways: (1) a finite budget constraint as in Example 1.1; and (2) a finite budget and time constraint as in Example 1.3.

1.1. Literature review

If the dynamic aspect can be ignored, there exist a number of methods for estimating an optimal policy function that maximizes social welfare, starting from the seminal contribution of Manski (2004), and extended by Hirano and Porter (2009), Stoye (2009, 2012), Chamberlain (2011), Bhattacharya and Dupas (2012), and Tetenov (2012), among others. More recently, Kitagawa and Tetenov (2018), and Athey and Wager (2018) proposed and extended Empirical Welfare Maximization in this context.

Bandits with knapsacks (Slivkins, 2019; Chapter 10) are a variant of standard bandits with resource constraints. Example 1.1 falls into this category. Compared to knapsack algorithms, our methodology amounts to solving the full dynamic programming problem; Section 6 shows that this can be solved efficiently using PDE techniques. For this reason, we expect our techniques to deliver higher welfare, though a formal comparison is difficult as knapsack algorithms are devised for online learning. Other advantages of our approach include a more natural handling of continuous covariates, and the ability to optimize within a constrained policy class.

Dynamic Treatment Regimes (DTRs) are another related literature, see e.g., Laber et al (2014) for an overview. DTRs consist of a sequence of individualized treatment decisions. The data in these studies is a sequence of dynamic paths for each individual. By contrast, the dynamics in our setting are faced by the social planner, not the individual.444Another difference is that the number of decision points in DTRs is quite small (often in the single digits), whereas, in our setting, this corresponds to the number of arrivals, which is very high.

There is a vast literature on the computation of optimal policy functions. Previous work in economics has often used Monte-Carlo methods or non-stochastic grid-based methods such as generalized policy iteration (e.g., Benitez-Silva et al, 2000). The AC approach is conceptually related to Monte Carlo methods. However, it incorporates additional ingredients such as ‘bootstrapping’, stochastic gradients and parallelization, which translates to substantial computational gains. We also prefer AC methods over other RL algorithms such as Q-learning, as they are known to be more stable, and, importantly for us, can also solve for the optimal policy within a chosen functional class. AC has been one of the default methods of choice for RL applications in recent years. In our application, we use 12 continuous terms (five continuous covariates with various interactions) in the policy function. The dimensionality can be challenging with grid based approaches, but the RL algorithm reaches a solution with relative ease.

In making use of the knowledge of dynamics, our methods fall under the banner of model-based RL. Recent studies (Yu et al, 2020; Kidambi et al, 2020) have argued that model based methods greatly expand the sample efficiency and applicability of RL. Compared to these works, our methods are narrowly tailored to the specific setup studied here, but for this same reason are more efficient. For instance, in Example 1.1, our algorithm does not need to visit all budget values to learn the optimal policy. But generic model-based RL methods behave conservatively when not all the states are reached, and typically minimize only a lower bound to regret.

2. Setup

Consider a social planner who is faced with making treatment decisions for a sequence of individuals under different institutional constraints. The state variables are denoted by where denotes the vector of individual covariates, is the institutional variable (e.g., current budget), and is time. For convenience, we take to be scalar for the rest of this paper.

The arrivals are determined by an inhomogeneous Poisson point process with parameter . Here, is a scale parameter that determines the rate at which individuals arrive, while itself is normalized via . Thus is the relative frequency of arrivals at time compared to that at time . Following recent literature (Wager and Xu, 2021; Fan and Glynn, 2021; Adusumilli, 2022) we take to end up with a PDE for characterizing welfare. Any approach to determine policy rules must use one or more forecasts (or estimates) of the arrival function and use this as optimally as possible. Therefore, for the most part of this paper, we take as given (density forecasts are also possible, and discussed in the appendix).

Based on the state , the planner makes a decision on whether to provide a treatment ( or not ). The decision is governed by the policy rule, , that specifies the probability of choosing action given state :

The set of all policy classes under consideration is denoted by . The policies are indexed by some (possibly infinite dimensional) parameter . We discuss policy classes in Section 2.3.

Once an action, , has been chosen, the planner receives a felicity/instantaneous utility of that is equivalent to the potential outcome of the individual under action and state .555So there is a continuum of potential outcomes, each corresponding to the planner’s felicity in a state where the individual happened to arrive at and the planner took action . The felicities are divided by to rescale them to a ‘per-person’ quantity, which will be convenient when we take . The definition of allows, e.g., the cost of treatment to vary with . The covariates and the set of potential outcomes for each individual are assumed to be drawn from a joint distribution that is independent of (see, however, Appendix E.1 for extensions to time-varying ).

We focus on utilitarian social welfare criteria: the welfare from administering actions , when a sequence of individuals with potential outcomes arrives at times into the future, is given by . Note that we always define welfare relative to not treating anyone. This is a convenient normalization that ensures the welfare is if the budget is .

Define , where the expectation is taken under the distribution , as the (unscaled) ‘reward’, i.e., the expected felicity, for the social planner from choosing action for an individual when the state variable is . Given our relative welfare criterion, it will be convenient to normalize , and set .

Conditional on , the evolution of to is governed by the ‘law of motion’:

where is a known function. For instance, in Example 1.1, if the cost the cost of treatment were , we would have

| (2.1) |

We can interpret as the flow rate of , when the flow is defined with respect to the number of arrivals .666To see why, note that (2.1) implies is the change in budget for a unit increase in the number of arrivals, when the arrivals are scaled by . As , the scaled number of arrivals before any state converges to . This implies is the flow rate of over time. For instance, if the planner receives interest income at the rate , where is the saving/borrowing rate and is current endowment, then .

Let denote the value function at some state under policy , defined as the expected social welfare from implementing this policy when the initial state is . In the fixed setting, we can characterize this recursively as

| (2.2) |

where denotes the state variable for the next arrival immediately following , and is the expectation jointly over (i) the new covariate , (ii) the waiting time , and (iii) the randomized policy , which influences the value of via . Unfortunately, the dependence of on makes it hard to characterize its properties (for one, does not have a stable limit as ). Furthermore, the iid nature of arrivals implies is independent of , so it would be convenient to integrate this out and achieve a dimension reduction for the value function. This motivates the integrated value function .

In the limit as , converges to the solution of the PDE:

| (2.3) |

where

and is the domain of the PDE (more on this below). In particular, under some assumptions noted in Section 5 , we show that

| (2.4) |

for some . Equation (2.4) is a direct consequence of Theorem 1, proved in a more general setting in Section 5.

PDE (2.3), and relatedly (2.4), is a key contribution of this paper. The terms, and , are the average rewards and average change to under when the state variable is . Now, can be interpreted as expected flow reward, while can be interpreted as the total rate of change of with respect to time. PDE (2.3) then equates the flow value of welfare, , to the sum of the flow rewards and rate of change of . Thus the PDE has an asset pricing interpretation if we think of as the natural interest rate.

Remarkably, PDE (2.3) characterizes in terms of only the the expected (given ) rate of change, of , so e.g., the variance of does not matter for welfare. Now, it is only in the limit as that the second and higher moments of are not relevant. For fixed , it can seen from (2.2) that the entire distribution of matters as is generally nonlinear in . This highlights the usefulness of the continuous time limit. Another convenient aspect of the PDE is that it depends only on the current state , which enables us to abstract away from the time series dependence of (which in turn makes the rewards dependent). This property is useful for deriving regret bounds.

2.0.1. Large approximation

can be interpreted as the expected number of individuals arriving in a unit time period. In our empirical application, where arrivals consist of people who just became unemployed, we measure in years. Then, corresponds to the number of unemployed individuals per year, which is a large number. Hence, we expect PDE (2.3) to provide a very good approximation in this setting.

2.0.2. General arrival processes

While it is natural to model arrivals as an exponential process, this is not necessary. In fact, the randomness of the arrivals becomes irrelevant for the properties of as . Let denote the waiting time between arrivals when the last arrival was at time . We require and at each (note that these are satisfied by the exponential distribution with parameter ). Any arrival process that satisfies these conditions will lead to PDE 2.3.

2.0.3. Batching

In practice, the planner may want group arrivals into small batches and apply the same policy rule on each batch. Our methods can easily accommodate batching. Let denote the batch size. Then, PDE (2.3) continues to apply as long as , so applying our proposed policy rules with such small batches delivers the same welfare as not using batching. We can also account for larger batch sizes, , by using piece-wise constant policy rules. These are policy rules that only change at specific time intervals; see Section 6.1 for an example.

2.1. Informal derivation of PDE (2.3) in a simplified setting

Because of the importance of PDE (2.3), we provide an intuitive derivation of it in a simplified version of Example 1.1 (with a budget constraint) where is constant for all , is independent of and the budget evolves as . In this setting, is no longer a state variable. We can represent in recursive form as

In deriving the above, we used , where , and replaced with to simplify notation. Define and . Then, taking expectations with respect to on both sides of the recursion for gives

| (2.5) | ||||

Now subtract from both sides, take a second order Taylor expansion of , and multiply the entire expression by (the derivation is only for intuition, in reality, need not be twice differentiable). Then, in the limit as , we end up with the following Ordinary Differential Equation (ODE) for the evolution of :777Sufficient conditions for a unique solution to (2.6) are provided in Appendix D.1.

| (2.6) |

This is just a special case of PDE (2.3).

Suppose we restrict attention to stationary policies that do not change with . Then, and we can obtain an explicit solution to (2.6) as The optimal policy solves , where is the initial budget. On the other hand, the EWM rule with budget constraints corresponds to the population problem: for some given . Clearly the two optimization problems are not equivalent. One can of course solve the EWM problem for each and choose the one that results in the best value for , but this requires knowledge of provided in this paper (and this derivation is only applicable to stationary policies).

2.2. Boundary conditions

To complete the dynamic model, we need to specify a boundary condition for (2.3). As illustrated by the examples in section 1, our approach can be applied to various situations. Different situations require different boundary conditions. We consider the following possibilities, which arguably cover the majority of relevant applications:

Dirichlet boundary condition.

This includes boundary conditions of the form (e.g., a budget constraint as in a simple version of Example 1.1), or (e.g., a finite time constraint), or both (as in Example 1.3). Here, and are known constants. Formally, , and the boundary condition is specified as ( or is allowed)888We depart from the convention of taking to be an open set. We could have alternatively specified , but as the solution will be continuous, we can extend it to , and a short argument will show that (2.3) also holds at (see, e.g., Crandall et al, 1984, Lemma 4.1).

| (2.7) |

We emphasize that the above does not impose any restrictions on .

In general, .

In fact, it might even be optimal to allow

to treat as many individuals as possible before the constraints are

hit. Formally, the domain of is only

the interior . As the program terminates when the boundary

is reached, there may be an effective discontinuity in the planners’

actions before and after the boundary. However, this has no bearing

on the continuity of .

Periodic boundary condition.

When the program continues indefinitely, is a relevant state variable only as it relates to some periodic quantity, e.g., seasonality. So, in this setting (as in a version of Example 1.1 where seasonality is also important), , and we impose the periodic boundary condition:

| (2.8) |

Here, denotes the period length. This boundary condition can only be valid if are periodic in with period length . This implies that should also be periodic.

Neumann boundary condition.

Consider a no-borrowing constraint (as in Example 1.2) at . Assume that the planner receives a flow of funds at the rate with respect to time, and the rate of interest is . Then, at , the flow rate of change of is and flow rewards are 0 (since no individual can be treated). Hence, the evolution of at is governed by

| (2.9) |

Intuitively, one can imagine that the coefficients of PDE (2.3) are discontinuous at and this discontinuity is formulated as the boundary condition (2.9). Thus, boundary conditions of this form allow the dynamics at the boundary to be different from those in the interior. This can also be useful in examples with queues or capacity constraints (e.g., when the queue length is , or the capacity is full). The following generalization of (2.9) accommodates all these examples: set and the boundary condition to be

| (2.10) | ||||

Here, and are known functions. We require for all , to ensure cannot decrease after hitting the boundary.

2.3. Policy classes and optimal policies

For the theory, we consider a class of policies indexed by some (possibly infinite dimensional) parameter .

For computation using RL methods, however, we require to be differentiable in . This still allows for rich spaces of policy functions. The class of soft-max functions is convenient and also commonly used in RL (see Sutton and Barto, 2018). Let denote a vector of functions of dimension . The soft-max function takes the form

| (2.11) |

As currently written, would need to be normalized, e.g., by setting one of the coefficients to . The term is a ‘temperature’ parameter that is either determined beforehand, or computed along with , in which case we could subsume it into and drop the normalization. For a fixed , we define the soft-max policy class as , where each element, , of is suitably normalized. As , this becomes equivalent to the class of Generalized Eligibility Scores (Kitagawa and Tetenov, 2018), which are of the form . More generally, the class can approximate any deterministic policy, including the first best policy rule (i.e., the one that maximizes over all possible ), arbitrarily well, given a large enough dimension . For even more expressive policies, this can be generalized, e.g., to multi-layer neural networks.

In using RL methods, we cannot directly work with deterministic rules, as they are not differentiable in . In practice, however, we just let the algorithm choose both , i.e., we drop and let the algorithm optimize over . This will eventually lead us to a deterministic policy if that is indeed optimal.

Note that (2.3) defines a class of PDEs indexed by , the solution to each is the integrated value function from following . The social planner’s objective is to choose that maximizes the forecast welfare at the initial values, , of :

| (2.12) |

3. Sample version of the planner’s problem

The unknown parameters in the social planner’s problem are and . We suppose that the social planner can leverage observational data to obtain estimates and of and . For the most part, we consider the setting where i.e., the rewards do not depend on . In such cases, we suppose that the planner has access to an observational study consisting of a random sample of size denoting observed outcomes , treatments , and covariates . This sample is drawn from some joint population distribution over , assumed to satisfy ignorability, i.e., . We further assume that the joint distribution of is given by , introduced in the previous section, and for simplicity we denote the entire population distribution of by as well. The empirical distribution, , of these observations is thus a good proxy for . Let denote the conditional expectations for , and , the propensity score. We recommend a doubly robust method to estimate over , e.g.,

| (3.1) |

where and are non-parametric estimates of and respectively.

We can then plug-in the above quantities to obtain

Based on the above we can construct the sample version of PDE (2.3) as

| (3.2) |

together with the corresponding sample versions of the boundary conditions (2.7), (2.8) or (2.10). In fact, for technical reasons, the existence of a unique solution to PDE (3.2) is not guaranteed without additional assumptions. For this reason, it is useful to think of PDE (3.2) as a heuristic device. In practice, we would always work with a discretized version of (3.2), described below, which does not suffer from existence issues.

We discretize the arrivals so that the law of motion for is given by (the ‘prime’ notation denotes one-step ahead quantities following the current one)

| (3.3) |

for some approximation factor . Additionally, in the approximation scheme, the difference between arrival times is specified as

| (3.4) |

with the censoring at used as a device to impose a finite horizon boundary condition. To simplify the notation, we allow and to be potentially discontinuous at in case of the Neumann boundary condition, and thus avoid the need for the quantities and .999However, we need them for the theory of viscosity solutions since it it requires continuous PDEs. The rest of environment is the same as before. For this discretized setup, define as the integrated value function at the state when an individual happens to arrive at that state. This can be obtained as the fixed point to the following dynamic programming problem:

| (3.5) | where |

for any function , and denotes the right censored exponential distribution with parameter and censoring at .

The usual contraction mapping argument ensures that always exists as long as or . We can therefore use as the feasible sample counterpart of , and solve the sample version of the social planner’s problem:

| (3.6) |

4. The actor-critic algorithm

This section discusses a RL algorithm to efficiently compute in (3.5). We focus on the Dirichlet boundary condition.101010Extensions to the other boundary conditions are discussed in the supplementary material.

We use an Actor-Critic (AC) algorithm for our context, for a more extensive discussion of its baseline version see Sutton and Barto (2018). The algorithm runs multiple episodes, each of which are simulations of the ‘sample’ dynamic environment. At each state , the algorithm chooses an action , where is the current policy parameter. This results in a reward of , and an update to the new state , where , and are obtained as in (3.3) and (3.4). Based on and , the policy parameter is updated to a new value . This process repeats until reaches the boundary of . Following this, the algorithm starts a new episode with the starting values , and continues in this fashion indefinitely.

In detail, the AC algorithm employs gradient descent along the direction :

where is the learning rate. Denote by the action-value function

| (4.1) |

where and has been defined in (3.5). The Policy-Gradient theorem (Sutton et al, 2000) provides an expression for as

| (4.2) |

for a ‘baseline’, , that can be any function of . Let denote some functional approximation for . We use as the baseline. In addition, we also employ this to approximate by replacing with in equation (4.1):

The above enables us to obtain an approximation for as

| (4.3) |

where is the Temporal-Difference (TD) error, defined as

We now describe the functional approximation for . Let denote a vector of basis functions of dimension over the space of . We approximate as , where the value weights, , are updated using Temporal-Difference learning (Sutton and Barto, 2018):

| (4.4) |

for some value learning rate .

Using equations (4.3) and (4.4), we can construct Stochastic Gradient Descent (SGD) updates for as

| (4.5) | ||||

| (4.6) |

by getting rid of the expectations in (4.3) and (4.4). These updates are applied at every decision point or in batches, using those values of that come up as the algorithm chooses actions according to . Importantly, the updates (4.5) and (4.6) can be applied simultaneously - instead of waiting for the value parameters to converge - by choosing the learning rates so that the speed of learning for is much faster than that for . This is an example of two-timescale SGD.

The pseudo-code for the resulting procedure is presented in Algorithm 1 in the appendix. The algorithm can be shown to converge under suitable choices of learning rates, see, e.g., Bhatnagar et al, 2009, and Appendix C.1 (even if, admittedly, these theoretical rates are seldom used).

4.1. Parallel and batch updates

In practice, SGD updates are volatile and may take a long time to converge. We use two techniques for stabilizing SGD: Asynchronous parallel updates, resulting in the A3C algorithm (see, Mnih et al, 2016), and batch updates. Asynchronous updating involves running multiple versions of the dynamic environment in parallel processes, each of which independently and asynchronously updates the shared global parameters and . Since at any given point in time, the parallel threads are at a different point in the dynamic environment, successive updates are decorrelated. Additionally, the algorithm is faster by dint of being run in parallel. In batch updating, the researcher chooses a batch size such that the parameter updates occur only after averaging over observations. This reduces the variance of the updates at the cost of slightly higher memory requirements. The pseudocode for the AC algorithm with both these modifications is provided in Appendix C.1.

4.2. Tuning parameters

We need to specify the basis functions for the value approximation and the learning rates. The choice of the dimension, , of the basis functions is based on computational feasibility. From a statistical point of view the optimal choice of is infinity, since we would like to compute exactly. For the basis functions, it will be efficient to incorporate prior knowledge about the environment. For instance, if the boundary condition is of the form , the basis functions could be chosen so that they are also when .

For the value learning rate, a common rule of thumb is (see, e.g., Sutton and Barto, 2018).111111The learning rates are typically taken to be constant, rather than decaying over time. In practice, as long as they are set small enough, this just means the parameters will oscillate slightly around their optimal values. The value of , however, requires experimentation, although we found learning to be stable across a relatively large range of in our empirical example.

5. Statistical and numerical properties

We start by discussing the existence and uniqueness of PDE (2.3).

5.1. Existence and uniqueness of viscosity solutions

For semi-linear PDEs of the form (2.3), it is well known that a classical solution (i.e., a solution that is continuously differentiable) does not exist. We instead employ the weak solution concept of a viscosity solution (Crandall and Lions, 1983). This is a common solution concept for equations of the HJB form; see Crandall et al (1992) for a user’s guide, and Achdou et al (2017) for a useful discussion. The following ensures existence of a unique, continuous viscosity solution to (2.3):

Assumption 1.

(i) , are Lipschitz continuous uniformly over .

(ii) is bounded, Lipschitz continuous, and bounded away from .

(iii) There exists such that for all .

(iv) are bounded and Lipschitz continuous in uniformly over . Furthermore, there exists such that for all .

The sole role of Assumption 1(i) is to ensure exists and is uniformly Lipschitz continuous. In so far as the latter goes, Assumption 1(i) can be relaxed in specific settings. For instance, depending on the boundary condition, we can allow to be discontinuous in one of the arguments, see Appendix D.1. For ODE (2.6), just integrability of is sufficient. We do not address the question of minimal sufficient conditions, but make do with Assumption 1(i) for simplicity. Appendix D.1 provides primitive conditions for verifying Assumption 1(i) under the soft-max policy class (2.11). Briefly, we require either be bounded away from , or at least one of the covariates be continuous. With purely discrete covariates and , and will typically be discontinuous, unless the policies depend only on .

Note that is discontinuous in . But this does not affect the continuity of since and enter separately in the definition of .

Assumption 1(ii) implies the arrival rates vary smoothly with and are bounded away from 0. Assumption 1(iii) is a mild requirement ensuring the expected rewards and changes to are bounded. Assumption 1(iv) provides regularity conditions for the Neumann boundary condition.

5.2. Assumptions for regret bounds

In addition to Assumption 1, we impose:

Assumption 2.

(i) There exists such that .

(ii) In the Dirichlet setting with , there exists s.t .

(iii) (Complexity of the policy function space) The collection of functions121212Except for the Neumann boundary conditions, the domain of in the definitions of and can be taken to be instead of . For the Neumann boundary conditions, we require and to be defined by continuously extending the ‘interior’ values of and to the boundary, even though the actual policy and law of motion at the boundary may be quite different.

indexed by and , is a VC-subgraph class with finite VC index . Furthermore, for each , the collection of functions

is also a VC-subgraph class with finite VC index . Let .

Assumption 2(i) is a boundedness assumption, imposed mainly for ease of deriving the theoretical results (see, e.g., Kitagawa and Tetenov, 2018). In practice, it is virtually guaranteed that the changes to budget are smaller than some finite number.

Assumption 2(ii) is required only in the Dirichlet setting, and even here, only where the boundary condition is determined partly by . In these settings, plays the role of time, so we need the coefficient, , multiplying in PDE (2.3) to be non-singular. Typically, we already have in such settings (e.g., the budget can only be depleted), so Assumption 2(ii) additionally requires to be strictly bounded away from . This is a mild restriction: if there exist some people that benefit from treatment and , it is a dominant strategy to always treat some fraction of the population.

The term in Assumption 2(iii) is a measure of the complexity of the policy class. Since the policy class is chosen by the policy maker, this only puts some mild restrictions on that choice. Often, is independent of , as in equation (2.1), in which case . In calculating the VC dimension, we treat as an index to the functions , similarly to . This is intuitive, since how rapidly the policy rules change with budget is also a measure of their complexity.

The next set of assumptions relate to the properties of the observational data from which we estimate , see Section 3 for the terminology. For now, we focus on the situation where do not affect the potential outcomes, see Appendix D.3 for extensions.

Assumption 3.

(i) .

(ii) are an iid draw from the distribution .

(iii) (Selection on observables) .

(iv) There exists such that for all .

Assumption 3(ii) assumes the observed data is representative of the population. Assumption 3(iii) requires the observational data to satisfy ignorability. Assumption 3(iv) ensures the propensity scores are bounded away from 0 and 1. All three are trivially satisfied for RCT data.

Under Assumptions 2 and 3, there exist many different estimates of the rewards, , that are consistent for . In this paper, we use the doubly robust estimates given in (3.1). We assume that the estimates of are obtained through cross-fitting (see, Chernozhukov et al, 2018, or Athey and Wager, 2018 for a description). We choose some non-parametric procedures, for estimating , and apply cross-fitting to weaken the assumptions required and reduce bias. We impose the following high-level conditions on :

Assumption 4.

(i) (Sup convergence) There exists such that, for ,

(ii) ( convergence) There exists some such that

Assumption 4 is taken from Athey and Wager (2018). The requirements imposed are weak and satisfied by almost all non-parametric procedures.

5.3. Regret bounds

Our main result is a probabilistic bound on the regret, , from employing as the policy rule. This is obtained by bounding the maximal difference between the integrated value functions, i.e., . The latter suffices since (see, e.g., Kitagawa and Tetenov, 2018)

As computing requires choosing a ‘approximation’ factor , we characterize the numerical error resulting from any sequence .

Theorem 1.

Suppose that Assumptions 1-4 hold and . Then, with probability approaching one, there exists independent of such that

under the Dirichlet boundary condition (2.7). Furthermore, there exists that depends only on the upper bounds for and such that the above also holds under the periodic boundary condition (2.8) as long as .

The term in Theorem 1 corresponds to the approximation error. Setting ensures this is of the same order as the statistical regret. Unfortunately, the theorem does not account for the computational error arising from the use of RL algorithms (but PDE methods, useful in simple cases, do provide exact solutions). In fact, we are not aware of any theoretical results on the rates of convergence of AC algorithms. Nevertheless, Theorem 1 remains useful for comparing policies. If the empirical welfare of the estimated policy, , is higher that that of some other policy, , we see that the regret from using over cannot be higher than a factor of .

The theorem requires to be sufficiently large in the periodic setting. This is a standard requirement under infinite horizons, see e.g., Crandall and Lions (1983).

5.3.1. Regret bounds with empirical PDE solutions

We conjecture Theorem 1 holds for the Neumann boundary condition as well, but were unable to prove this with our current techniques. The case of is also not covered by the theorem. For these remaining cases, we offer alternative results bounding the regret from using , obtained as

| (5.1) |

where is the solution to the empirical PDE (3.2). While estimation of is not always feasible (though PDE methods can be employed in some simple cases), the bounds we obtain are useful as a baseline for the regret when there is no numerical error.

Existence of does not follow from Lemma 1. We need a comparison theorem (Crandall et al 1992), which will guarantee existence and uniqueness. A sufficient condition for this is: are uniformly continuous in for each . We will therefore assume this below. While certainly onerous - it precludes deterministic policies that vary with in the soft-max class (though any is fine) - we believe more powerful comparison theorems can be devised that eliminate this requirement and leave this as an avenue for future research.

Theorem 2.

The theorem allows to be arbitrary, even negative, under Dirichlet and Neumann boundary conditions. The intuition behind Theorem 2 is that by Kitagawa and Tetenov (2018) and Athey and Wager (2018), the coefficients of the PDEs (2.3) and (3.2), i.e., the quantities and , are uniformly close. This implies the solutions are uniformly close as well, which we verify using the theory of viscosity solutions. The rate for the regret cannot be improved, since Kitagawa and Tetenov (2018) show that this rate is optimal in the static case.

6. Empirical application

Consider a policy maker who is charged with assigning job training to a stream of individuals arriving sequentially when they become unemployed. The policy maker would like to obtain a policy rule that maximizes expected social welfare under budget and/or time constraints. We use the popular dataset on randomized training provided under the JTPA to illustrate how RL algorithms allow us to obtain personalized policy rules for such dynamic decision problems when there are many state variables. This dataset was also previously used by Kitagawa and Tetenov (2018). During 18 months, applicants who contacted job centers after becoming unemployed were randomized to receive job training131313In fact, local centers could choose to supply one of the following forms of support: training, job-search assistance, or other support. Following Kitagawa and Tetenov (2018), we consolidate all forms of support and term this ‘job training’. or not. We follow the sample selection strategy of Kitagawa and Tetenov (2018), resulting in 9223 observations. The data contains baseline information about the participants as well as their subsequent earnings for 30 months, with the latter being the outcome of interest. We illustrate our methods in two settings:

The first setting corresponds to Example 1.1, where budget is finite but there is no time constraint. As argued in the introduction and Section 2.1, static methods, i.e., methods devised for simultaneous allocation, are not applicable here; this is so even if we restrict attention to stationary policies. In fact, depending on the parameter values, non-stationary policies can substantially outperform stationary ones in terms of welfare. Admittedly, stationary policies are easier to implement for a policy maker; our results provide useful information on when this tradeoff could be worth-while. The setting is also simple enough that it is possible to solve the optimization problem exactly, using differential-equation techniques.

The second setting corresponds to Example 1.3, i.e., there is a constraint on both budget and time. As in the first example, static methods are not directly applicable - the optimization problem they solve does not correspond to maximizing the sample analogue of welfare in this setting, as the latter can only be characterized as the solution of a dynamic programming problem (because actions now affect future states via changes to budget). Nevertheless, one may wonder how different these objectives are in specific instances. We therefore compare the policy rules obtained from our approach with a budget-constrained EWM benchmark that (necessarily) ignores dynamics. Even when employing stationary policies within the same policy class (so a like-to-like comparison is possible), using our methods results in a 25% gain in welfare.141414We do not provide a detailed comparison to existing, static, methods in the first example as it is not clear what the relevant benchmark could be. Suppose the planner starts with enough budget to treat 25% of expected yearly arrivals. We could artificially convert it to a constraint of treating 25% of the population in the budget-constrained EWM problem, even if this is not particularly meaningful as the policy could run for multiple years, and the ‘population’ is not well defined in the open ended setting. With this benchmark, and under a yearly discount factor of , our proposed stationary policy delivers a 43% welfare gain. This highlights the importance of treating the problem as a dynamic programming one, as opposed to approximating it with a simultaneous allocation problem, see Section 6.2.2 for a further explanation. Interestingly, we find in this setting that non-stationary policies do not provide any discernible welfare gain over stationary ones (atleast under our chosen parameter values). Again, this would not have been known a priori, so our methods can help the policy maker in deciding which to implement. The setting is also computationally more demanding and we use it to introduce our RL approach.

6.1. Budget constraints

The planner is endowed with an initial budget , measured as the fraction of expected arrivals per year that can be treated. For each individual who arrives, the planner has to decide whether to offer job training or not. The decision may be based on remaining budget, and individual characteristics. For the latter, we use education, previous earnings, and age. Job training is free to the individual, but costly to the planner who must spend for the training from her budget.

To simplify matters, we assume that arrival rates are constant (our next setting relaxes this). We consider two policy classes: (A) a stationary one of the form , and (B) a non-stationary one , where the functions are allowed to vary unrestrictedly with budget, . A stationary policy is potentially more attractive as the policy rule does not change with budget, so there is no incentive for individuals to manipulate arrival times and it is also arguably easier to implement.

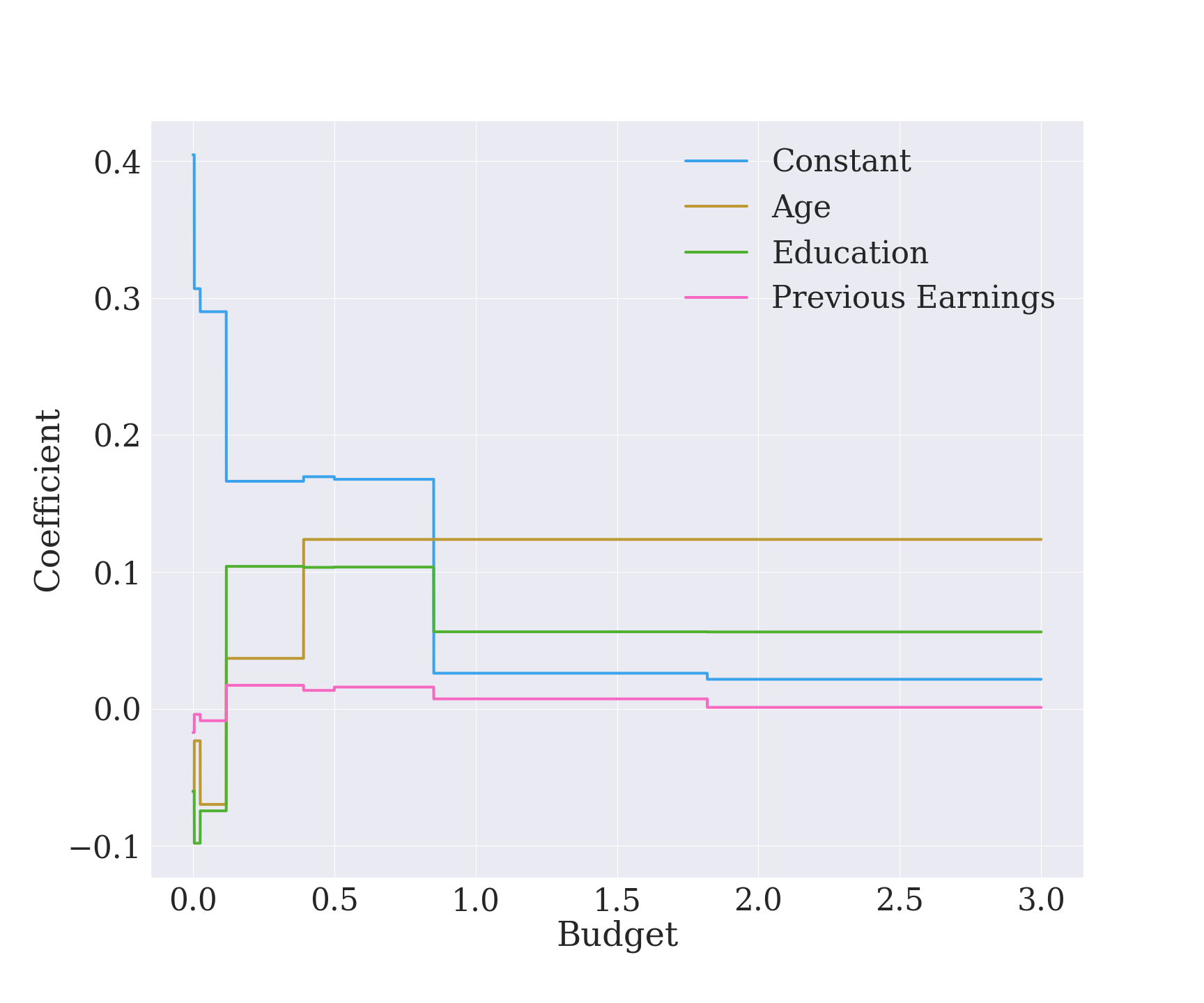

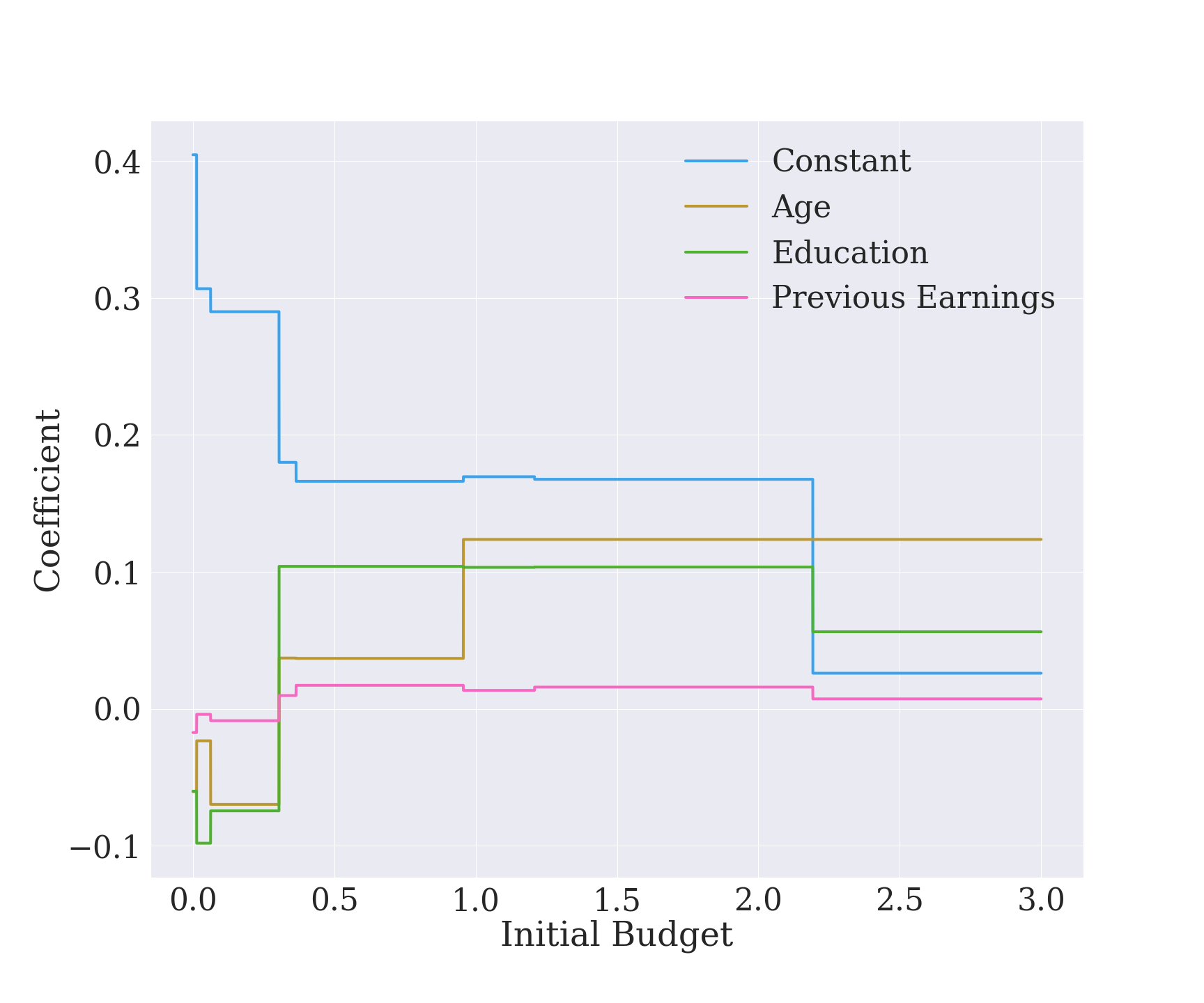

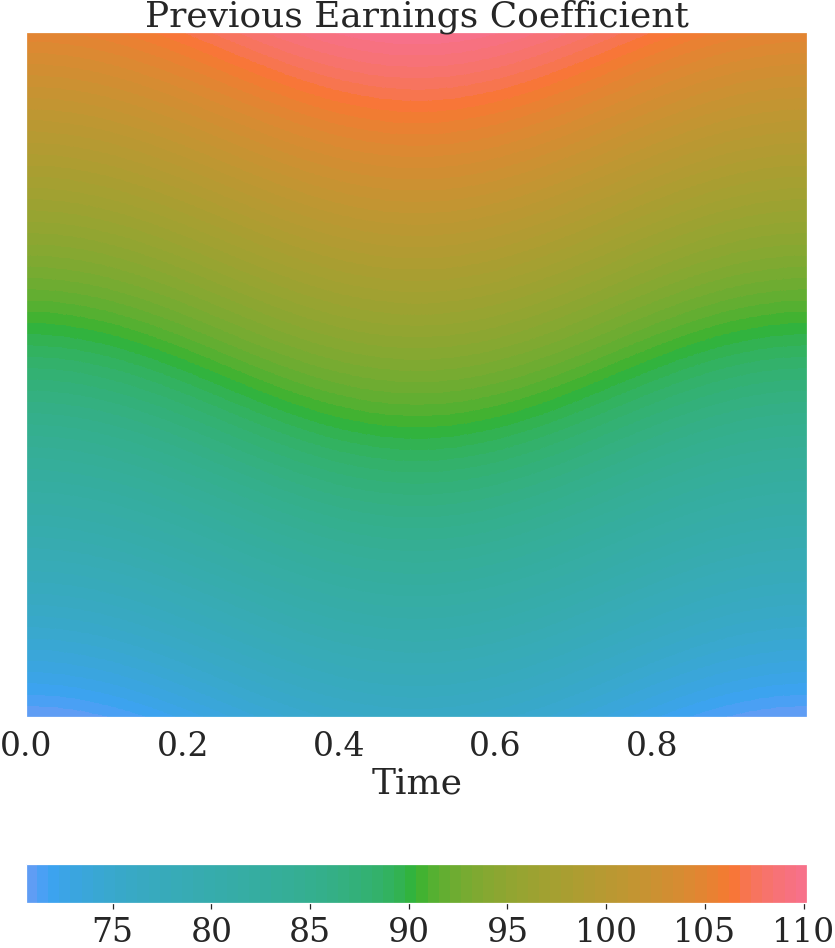

We obtain the reward estimates from a cross-fitted doubly robust procedure as in (3.1), where we use simple OLS to estimate the conditional means, , and the propensity score is , as set by the RCT.151515In the supplementary material, we discuss the results under the alternative estimates for the rewards, where the conditional means are again estimated using simple OLS. The optimal stationary policy is then computed analytically using the procedure described in Section 2.1. The optimal non-stationary policy is computed by solving ODE (2.6) using the technique of ‘piece-wise constant policy approximations’, see Krylov (1999). This involves approximating and with piece-wise constant functions that stay constant within a set of grid points for budget. The values of and within each grid can then be computed recursively by starting from and iteratively employing the technique described in Section 2.1 (the value function at the end of each step becomes the initial condition of ODE (2.6) for the next iteration). We can thus approximate the optimal arbitrarily well by letting . We take (because some covariates are discrete, the resulting approximation error is essentially ). In fact, fixing to a specific value (even though we do not do this here) would make this a batched policy. The use of ODE techniques is possible due to the presence of a single state variable, , in . With additional state variables, the methodology quickly becomes infeasible and we have to resort to RL algorithms.

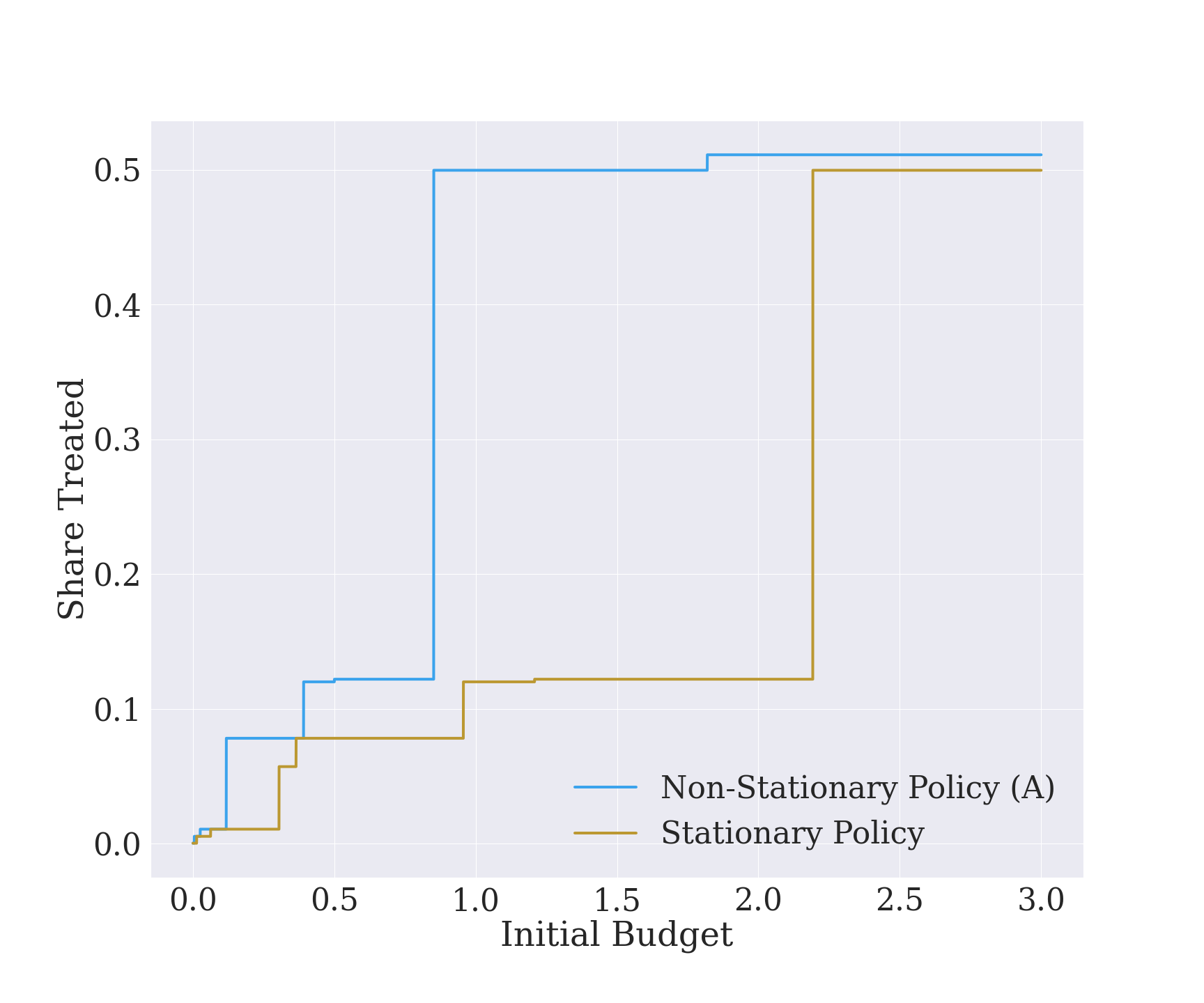

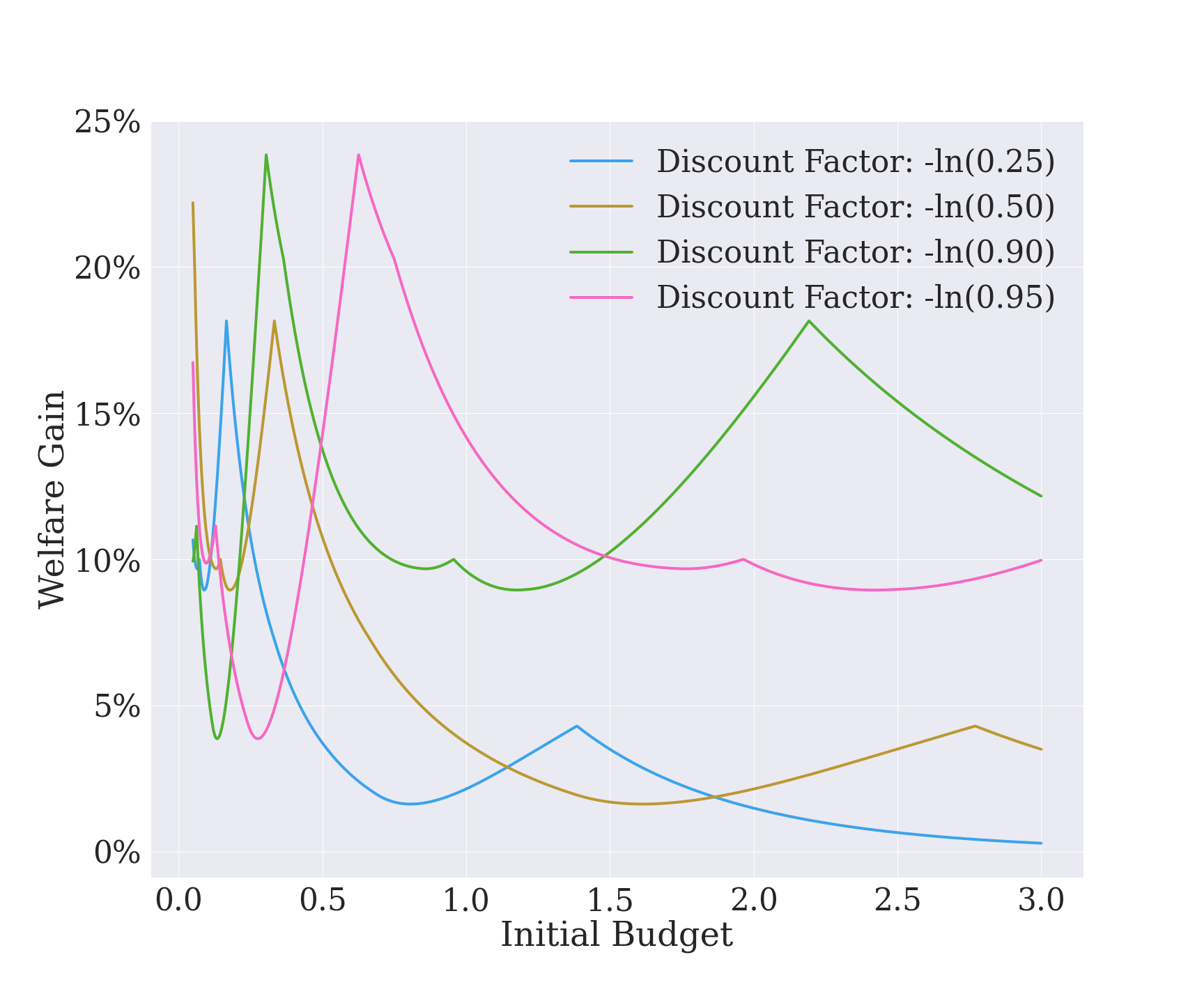

Figures 6.1 and 6.2 illustrate how the optimal policy functions’ coefficients change with different amounts of available budget, and what this implies for the probability of treatment after averaging across the covariates. We use a discount factor of for the figures (i.e., rewards accruing after 1 year are multiplied by . Due to the discrete nature of some covariates, the coefficients are constant over some intervals of the budget. The optimal stationary policy varies under different initial endowments , but always treats a smaller share of arrivals at any given budget value as compared to the non-stationary policy. It is inferior as it must remain constant even as the budget is used up over time. As figure 6.2 shows, the welfare gain from the non-stationary policy can be as high as 24%. For some budgets and discount factors, the difference is only moderate though. A policy maker with a desire for stationary rules might be willing to bear this welfare cost.

| A: Non-Stationary Policy | B: Stationary Policy |

Note: A budget of 1 corresponds to the expected cost of treating all arrivals of one year. The stationary policy is only affected by initial budget. The non-stationary policy responds to the remaining budget both at the initial value and over the course of its use.

Note: A budget of 1 corresponds to the expected cost of treating all arrivals of one year. The share treated remains constant between an initial budget of 3 and 10. If not indicated otherwise, we use a discount factor of .

6.2. Budget and time constraints

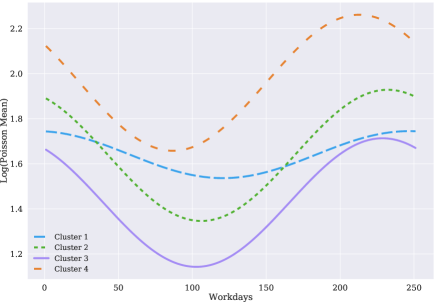

We now consider a setting where the policy duration is year, and the planner is assumed to be endowed with a budget that can treat 25% of the expected number of arrivals per year. The program terminates when either all budget is used up or the year ends. The discount factor is . We also allow the distribution of the arrivals to vary throughout the year. As the dataset contains information regarding when participants arrived, we can approximate the arrival process using cluster-specific inhomogeneous Poisson processes. We partition the data into four clusters using k-median clustering on the covariates, and estimate the arrival rates using Poisson regression. The procedure is described in Appendix F.

To apply our methods, we rescale time and budget so that corresponds to a year and set the initial budget, , to 1. The cost of treatment is , where is the expected number of people arriving in a year, given our Poisson rates. The reward estimates, , are constructed in the same manner as in the previous example. We consider three policy classes: (A) a non-stationary policy: , (B) a second non-stationary policy: where are dummies for quarter of the year; and (C) a stationary one: , where . The rationale for using the term was to account for the seasonal nature of arrivals. Policy classes A and B give almost identical outcomes (the difference in welfare is less than 0.5%). For brevity, we only display the outcomes from policy class A.

6.2.1. Tuning parameter choice

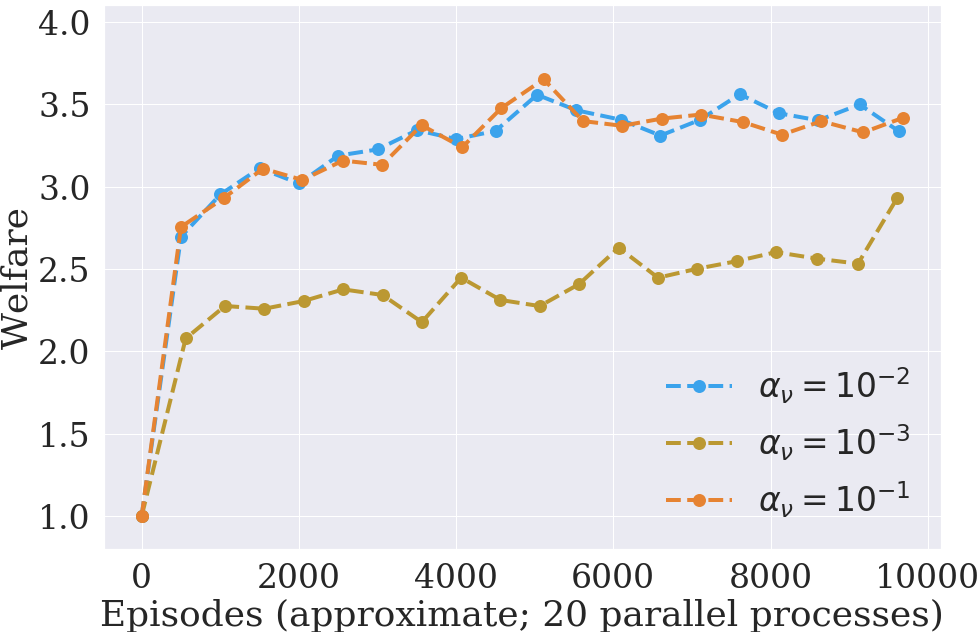

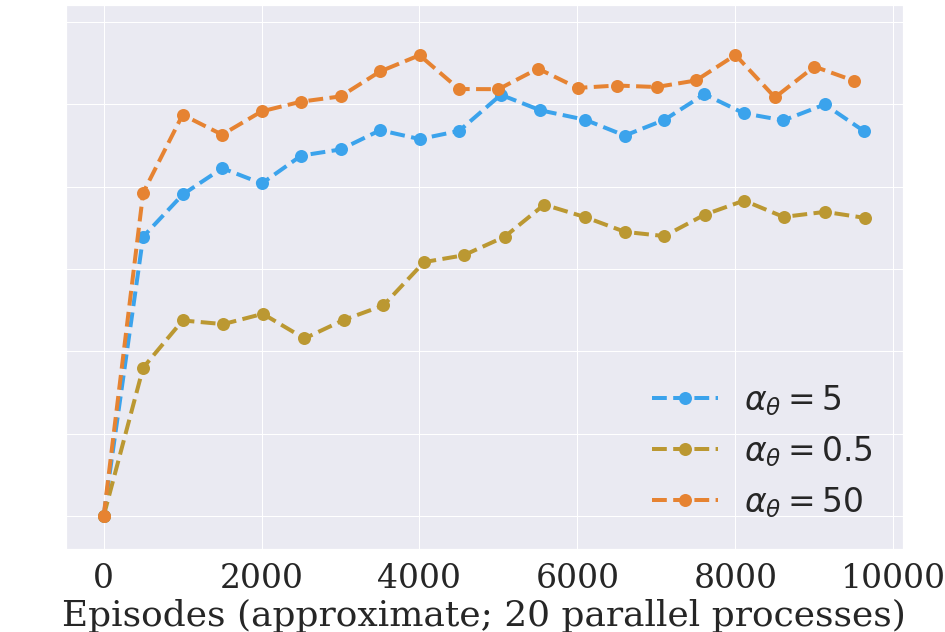

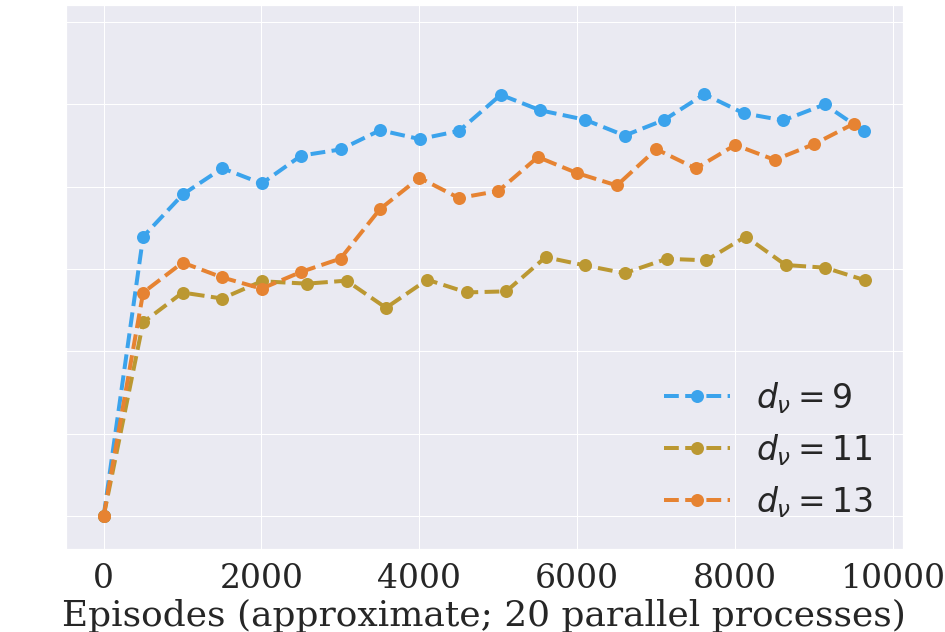

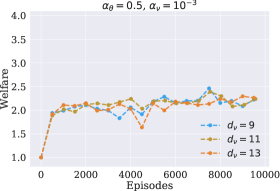

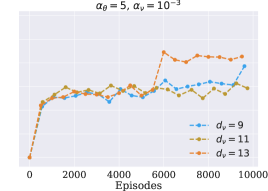

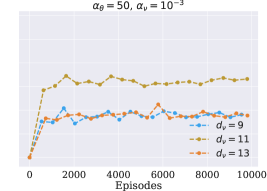

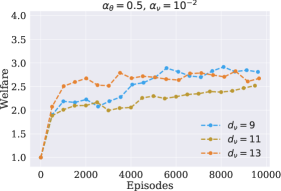

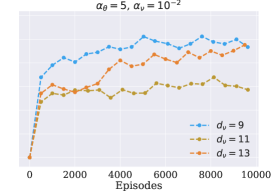

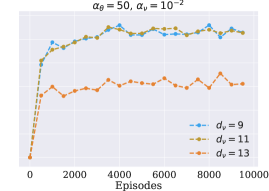

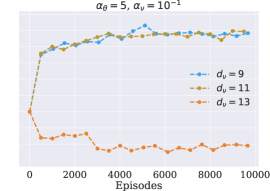

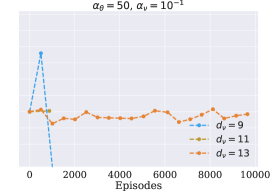

We solve for the optimal policies within each policy class using the A3C algorithm with clusters (see Appendix C.1). For the tuning parameters, we conducted a grid search with three different values for each of , , and , where is the dimension of basis functions for the value approximation (see Appendix F for further details). Our implementation further has RL agents training in parallel (higher is better, this is only restricted by hardware constraints), with the batch size set to (higher is better, but it appears there is little gain beyond a certain level). From the grid search we found that setting , and achieves reasonably quick and stable convergence (this is consistent with the rule of thumb choice for the value learning rate, which is in this application).161616Each episode takes about 6-12 seconds to run depending on the CPU clock rate and memory. Figure 6.3 illustrates the variability in learning with respect to deviations from this baseline. Learning is reliable for two orders of magnitudes of and , but can be substantially worse or unstable outside this range.

Note: Training was performed in 20 parallel processes. Each point is an average over 500 evaluation episodes. A welfare of corresponds to a random policy (50% treatment probability). The main specification uses .

6.2.2. Results

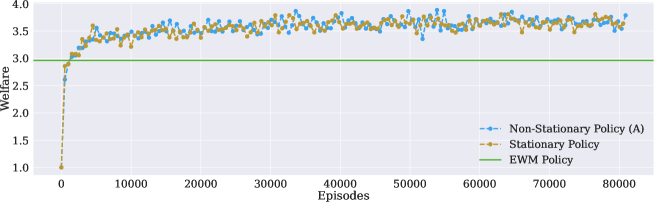

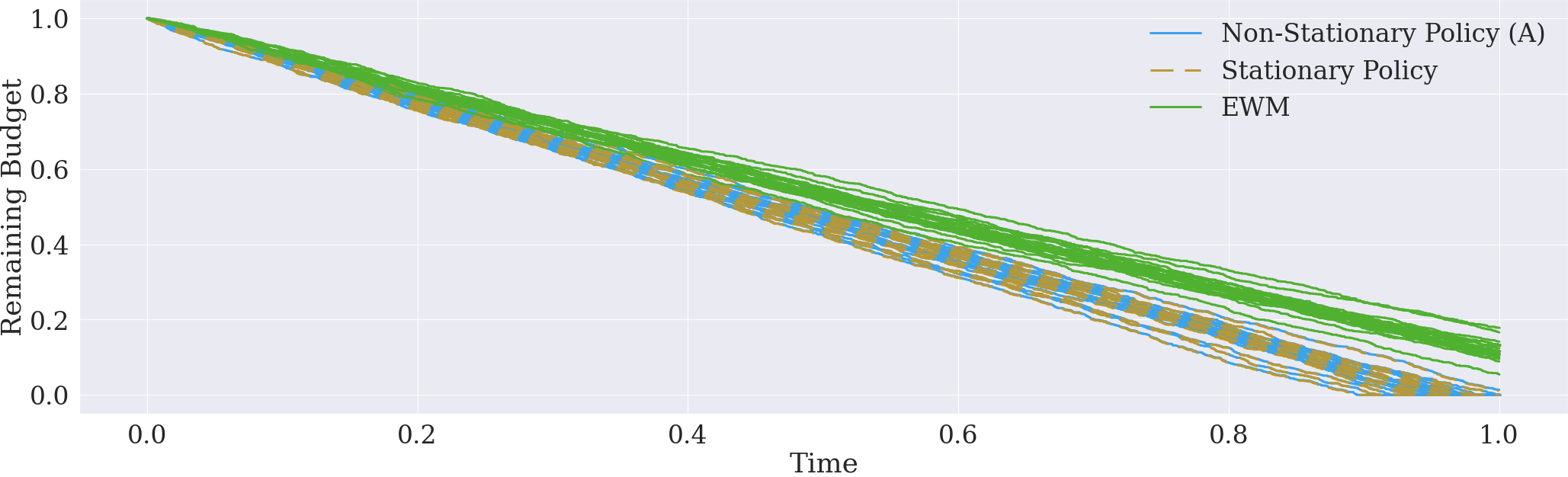

Figure 6.4 shows the result from running our baseline implementation for our policy classes. We also compare our policies, which are both solutions to a dynamic programming problem, to that obtained from the EWM method of Kitagawa and Tetenov (2018) under a budget constraint of . We use the same rewards and apply their methods on the policy class - which is just a deterministic version of our soft-max class. As noted earlier, the objective function in EWM maximizes in-sample welfare, and is meant to be simultaneously applied on the population. The use of discounting, and the fact that the distribution of arrivals varies within the year require the optimal policy to be derived using dynamic programming methods. These are important aspects of the optimization problem. Dropping them has severe consequences: we see a 25% higher welfare on average under both our proposed policies.171717See Appendix F.4 for more details.181818Kitagawa and Tetenov (2018) only use two covariates (education and previous earnings, but not age). The percentage gain in welfare is even larger when age is dropped as a covariate. At the same time, there is not much gain from employing non-stationary policies in this example, the increase in welfare being less than . In this specific example, the stationary policy turns out to be very attractive for a policy maker.

Note: The stationary policy does not include budget or time but is computed by the RL algorithm as a solution to a dynamic programming problem (with a value function that still contains budget and time). The EWM policy assumes the problem to be static. Training was performed in 20 parallel processes. Each point is an average over 500 evaluation episodes. A welfare of corresponds to a random policy (50% treatment probability).

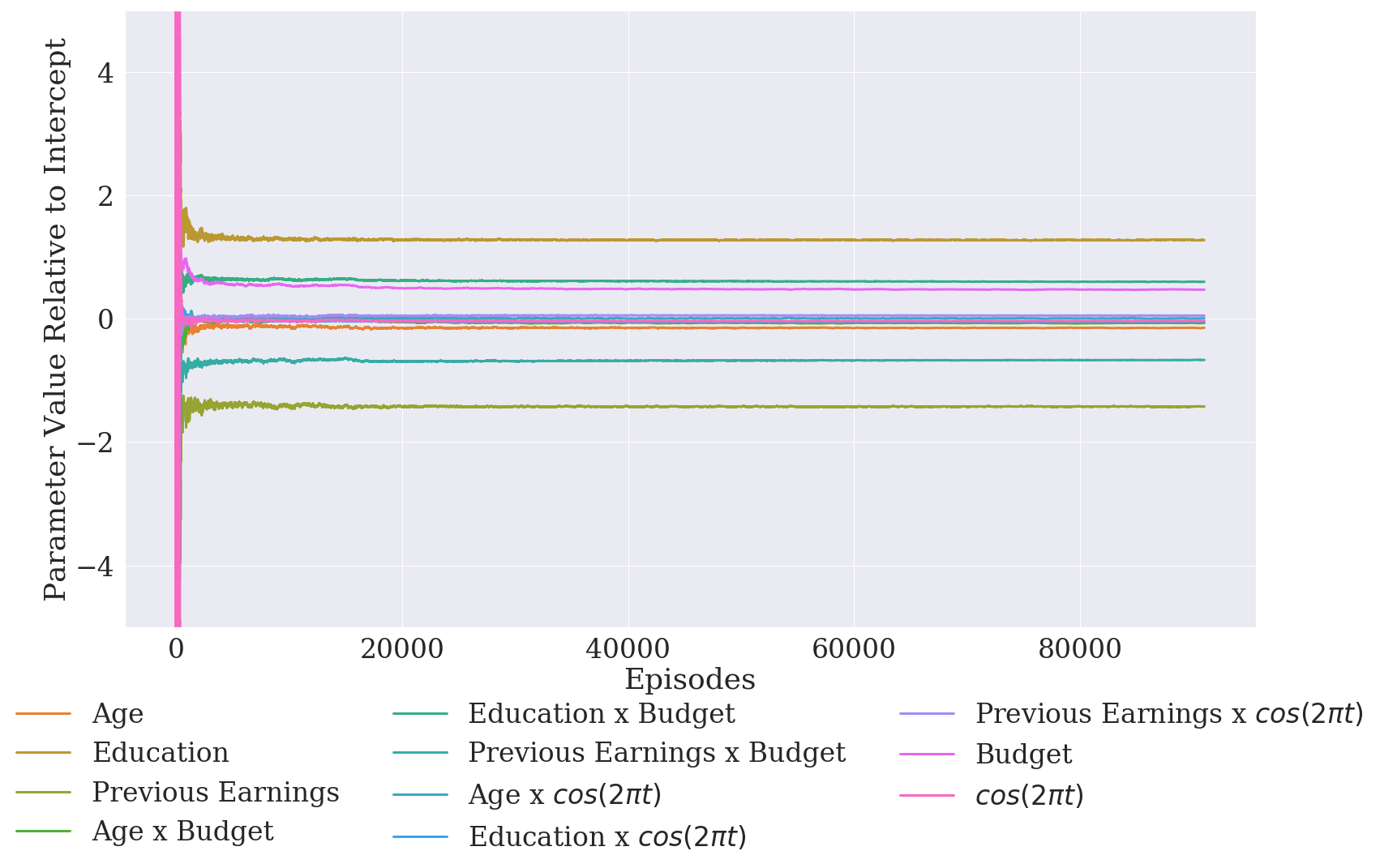

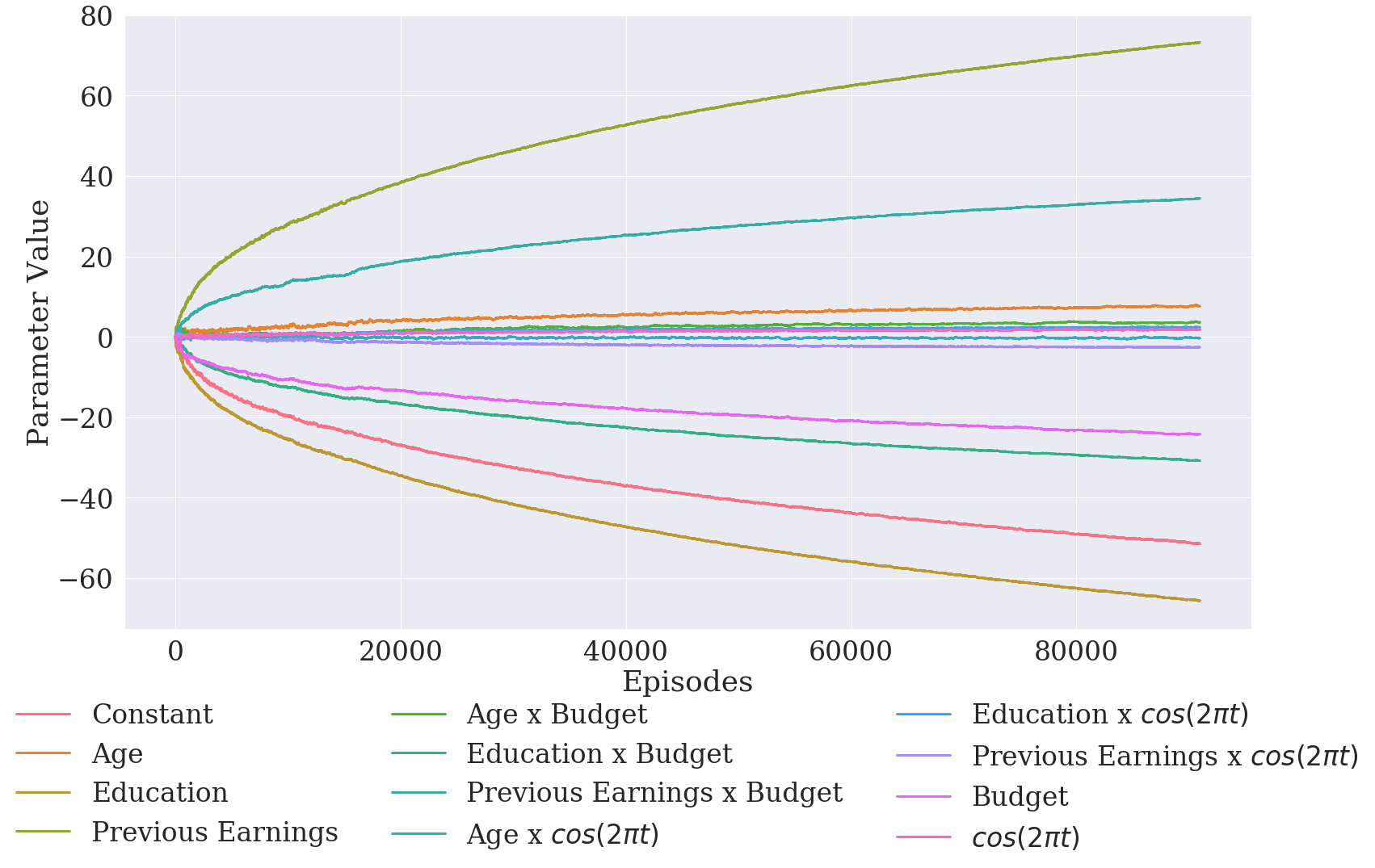

Figure 6.5 displays the convergence of the policy coefficients for the non-stationary policy class A. The relative values of the coefficients (in the figure this is relative to the intercept) converge rather fast. The coefficients, however, keep increasing slowly in absolute value, which makes the policy more deterministic (i.e. the action probabilities closer to either 0 or 1). In practice, we can thus truncate the training episodes early and convert the soft-max policy rule to a deterministic one (i.e., treat if treatment probability is larger than 50%). With this deterministic version of our policy, we achieve 28% higher welfare compared to EWM.

| A: Relative Coefficients over the Course of Training | B: Coefficients over the Course of Training |

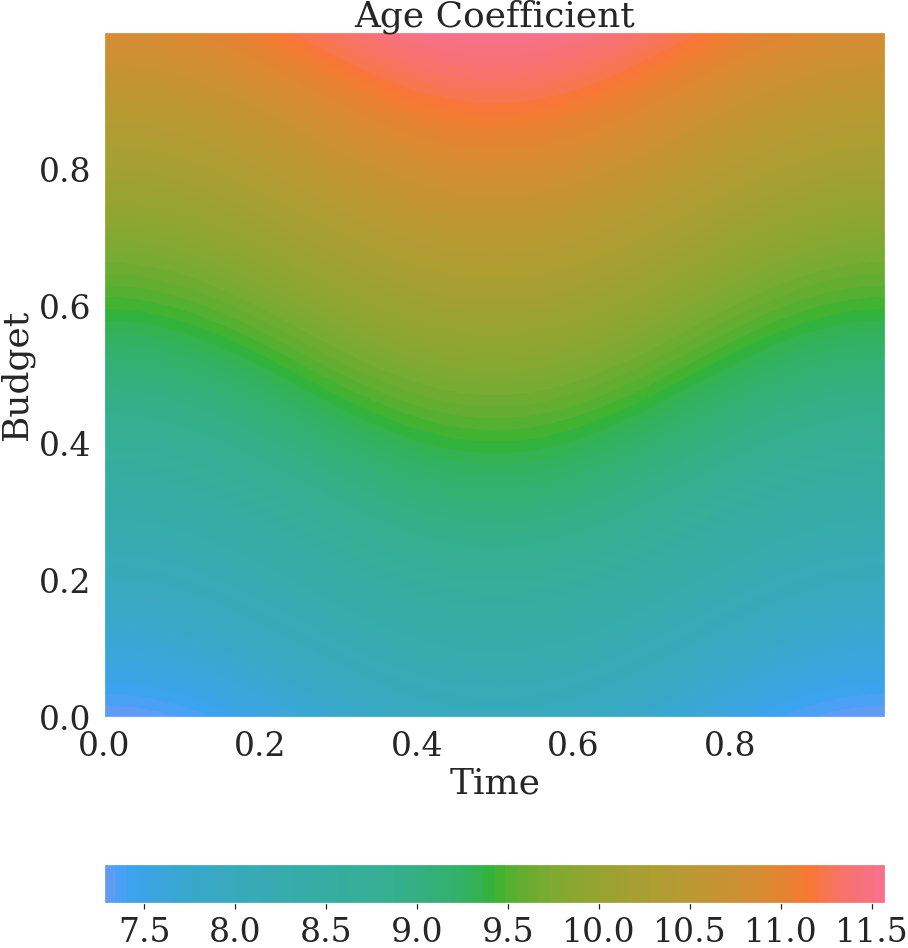

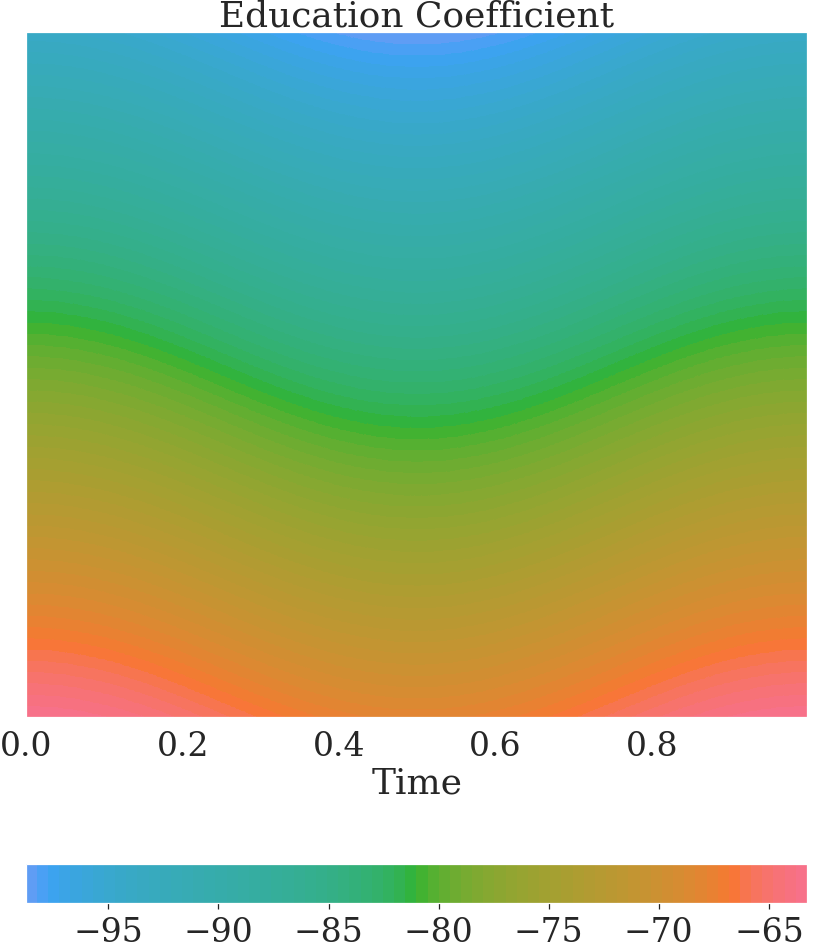

In the non-stationary policy class A, time and budget influence how the covariates affect the treatment decision. Figure 6.6 indicates how large the coefficient value corresponding to each covariate is, after including interactions with time and budget. Specifically, if we write in the form , then age affects the treatment decision with the coefficient , which we plot. Based on the heatmaps we find, e.g., that older individuals are more likely to be treated at the beginning of the year. Similar comments apply to policy class B (results not shown).

In summary, the example shows that RL algorithms can increase welfare in the challenging dynamic decision settings faced by economic policy makers. While the use of the JTPA data allows us to compare our approach to recent work, the dynamic environment we use to illustrate the potential of RL solutions is already of considerable complexity. Indeed, our policy function (with interactions) contains 12 coefficients.

7. Conclusion

In this paper, we have shown how RL can be combined with data from RCTs to obtain dynamic assignment rules under constraints. Our framework is general and incorporates a range of settings of practical importance (for an extension to non-compliance, see the supplementary material). Furthermore, it can utilize large amounts of existing RCT data. As A3C algorithms scale to problems with much higher dimensional state spaces (see e.g. Mnih et al, 2016), the approach is very flexible and applicable to an array of datasets and real world decision problems which policy makers face. The ability of RL methods to take into account large amounts of state variables when personalizing treatments could also give incentives to run targeted studies with many recorded covariates.

At the same time, the work raises a number of avenues for future research. One interesting avenue would be to study how existing RCT data can be used not only to train a policy function as in our examples, but also to employ further online learning to fine-tune the initialized policy to current data. We have also assumed that individuals do not respond strategically to non-stationary policies. However, if they do and the response is known or estimable, this could be directly included in our setup. Furthermore, our methodology requires the social-planner to pre-select a class of policy rules, but it is silent on how this class is to be chosen. In reality, the planner must balance various welfare and ethical tradeoffs in choosing the policy class, e.g., in choosing which covariates to include. The planner may note that more covariates may lead to higher welfare, but also more possibilities for statistical discrimination. In future work, it would be particularly interesting to study how “ethical constraints” can be added to the RL environment and reward structure, such as changing the welfare criterion so that rewards are higher if certain target allocations are met. This would help develop algorithms that aid economic policy making while directly taking wider ethical considerations into account.

References

- Achdou et al., (2017) Achdou, Y., Han, J., Lasry, J.-M., Lions, P.-L., and Moll, B. (2017). Income and wealth distribution in macroeconomics: A continuous-time approach. Technical report, National Bureau of Economic Research.

- Adusumilli, (2021) Adusumilli, K. (2021). Risk and optimal policies in bandit experiments. arXiv preprint arXiv:2112.06363.

- Anderberg, (1973) Anderberg, M. R. (1973). Cluster Analysis for Applications. Academic Press, New York.

- Athey and Wager, (2018) Athey, S. and Wager, S. (2018). Efficient Policy Learning. arXiv:1702.02896.

- Barles and Chasseigne, (2014) Barles, G. and Chasseigne, E. (2014). (almost) everything you always wanted to know about deterministic control problems in stratified domains. arXiv preprint arXiv:1412.7556.

- Barles and Lions, (1991) Barles, G. and Lions, P.-L. (1991). Fully nonlinear neumann type boundary conditions for first-order hamilton–jacobi equations. Nonlinear Analysis: Theory, Methods & Applications, 16(2):143–153.

- Benitez-Silva et al., (2000) Benitez-Silva, H., Hall, G., Hitsch, G. J., Pauletto, G., and Rust, J. (2000). A comparison of discrete and parametric approximation methods for continuous-state dynamic programming problems. manuscript, Yale University.

- Bhatnagar et al., (2009) Bhatnagar, S., Sutton, R. S., Ghavamzadeh, M., and Lee, M. (2009). Natural Actor-Critic Algorithms. Automatica, 45(11):2471–2482.

- Bhattacharya and Dupas, (2012) Bhattacharya, D. and Dupas, P. (2012). Inferring Welfare Maximizing Treatment Assignment under Budget Constraints. Journal of Econometrics, 167:168–196.

- Bostan and Namah, (2007) Bostan, M. and Namah, G. (2007). Time periodic viscosity solutions of hamilton-jacobi equations. In Applied Analysis And Differential Equations, pages 21–30. World Scientific.

- Brockman et al., (2016) Brockman, G., Cheung, V., Pettersson, L., Schneider, J., Schulman, J., Tang, J., and Zaremba, W. (2016). Openai gym. arXiv preprint arXiv:1606.01540.

- Chamberlain, (2011) Chamberlain, G. (2011). Bayesian Aspects of Treatment Choice. In Geweke, J., Koop, G., and Van Dijk, H., editors, The Oxford Handbook of Bayesian Econometrics, pages 11–39. Oxford University Press.

- Chernozhukov et al., (2018) Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68.

- Crandall, (1997) Crandall, M. G. (1997). Viscosity solutions: a primer. In Viscosity solutions and applications, pages 1–43. Springer.

- Crandall et al., (1984) Crandall, M. G., Evans, L. C., and Lions, P.-L. (1984). Some properties of viscosity solutions of hamilton-jacobi equations. Transactions of the American Mathematical Society, 282(2):487–502.

- Crandall et al., (1992) Crandall, M. G., Ishii, H., and Lions, P.-L. (1992). User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American mathematical society, 27(1):1–67.

- Crandall and Lions, (1983) Crandall, M. G. and Lions, P.-L. (1983). Viscosity solutions of hamilton-jacobi equations. Transactions of the American mathematical society, 277(1):1–42.

- Crandall and Lions, (1986) Crandall, M. G. and Lions, P.-L. (1986). On existence and uniqueness of solutions of hamilton-jacobi equations. Nonlinear Analysis: Theory, Methods & Applications, 10(4):353–370.

- Degrave et al., (2022) Degrave, J., Felici, F., Buchli, J., Neunert, M., Tracey, B., Carpanese, F., Ewalds, T., Hafner, R., Abdolmaleki, A., de Las Casas, D., et al. (2022). Magnetic control of tokamak plasmas through deep reinforcement learning. Nature, 602(7897):414–419.

- Fan and Glynn, (2021) Fan, L. and Glynn, P. W. (2021). Diffusion approximations for thompson sampling. arXiv preprint arXiv:2105.09232.

- Hirano and Porter, (2009) Hirano, K. and Porter, J. R. (2009). Asymptotics for Statistical Treatment Rules. Econometrica, 77(5):1683–1701.

- Ishii, (1985) Ishii, H. (1985). Hamilton-jacobi equations with discontinuous hamiltonians on arbitrary open sets. Bull. Fac. Sci. Eng. Chuo Univ, 28(28):1985.

- Kidambi et al., (2020) Kidambi, R., Rajeswaran, A., Netrapalli, P., and Joachims, T. (2020). Morel: Model-based offline reinforcement learning. arXiv preprint arXiv:2005.05951.

- Kitagawa and Tetenov, (2018) Kitagawa, T. and Tetenov, A. (2018). Who Should Be Treated? Empirical Welfare Maximization Methods for Treatment Choice. Econometrica, 86(2):591–616.

- Kock et al., (2018) Kock, A. B., Preinerstorfer, D., and Veliyev, B. (2018). Functional sequential treatment allocation. arXiv preprint arXiv:1812.09408.

- Laber et al., (2014) Laber, E. B., Lizotte, D. J., Qian, M., Pelham, W. E., and Murphy, S. A. (2014). Dynamic treatment regimes: Technical challenges and applications. Electronic journal of statistics, 8(1):1225.

- Mandt et al., (2017) Mandt, S., Hoffman, M. D., and Blei, D. M. (2017). Stochastic gradient descent as approximate bayesian inference. The Journal of Machine Learning Research, 18(1):4873–4907.

- Manski, (2004) Manski, C. F. (2004). Statistical Treatment Rules for Heterogeneous Populations. Econometrica, 72(4):1221–1246.

- Mnih et al., (2016) Mnih, V., Badia, A. P., Mirza, M., Graves, A., Lillicrap, T., Harley, T., Silver, D., and Kavukcuoglu, K. (2016). Asynchronous methods for deep reinforcement learning. In International conference on machine learning, pages 1928–1937.

- Mnih et al., (2015) Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., Graves, A., Riedmiller, M., Fidjeland, A. K., Ostrovski, G., Petersen, S., Beattie, C., Sadik, A., Antonoglou, I., King, H., Kumaran, D., Wierstra, D., Legg, S., and Hassabis, D. (2015). Human-Level Control through Deep Reinforcement Learning. Nature, 518(7540):529–533.

- Silver et al., (2018) Silver, D., Hubert, T., Schrittwieser, J., Antonoglou, I., Lai, M., Guez, A., Lanctot, M., Sifre, L., Kumaran, D., Graepel, T., Lillicrap, T., Simonyan, K., and Hassabis, D. (2018). A general reinforcement learning algorithm that masters chess, shogi, and go through self-play. Science, 362(6419):1140–1144.

- Silver et al., (2017) Silver, D., Schrittwieser, J., Simonyan, K., Antonoglou, I., Huang, A., Guez, A., Hubert, T., Baker, L., Lai, M., Bolton, A., et al. (2017). Mastering the game of go without human knowledge. Nature, 550(7676):354.

- Slivkins, (2019) Slivkins, A. (2019). Introduction to multi-armed bandits. arXiv preprint arXiv:1904.07272.

- Souganidis, (1985) Souganidis, P. E. (1985). Existence of viscosity solutions of hamilton-jacobi equations. Journal of Differential Equations, 56(3):345–390.

- Souganidis, (2009) Souganidis, P. E. (2009). Rates of convergence for monotone approximations of viscosity solutions of fully nonlinear uniformly elliptic pde (viscosity solutions of differential equations and related topics).

- Stoye, (2009) Stoye, J. (2009). Minimax Regret Treatment Choice with Finite Samples. Journal of Econometrics, 151(1):70–81.

- Sutton and Barto, (2018) Sutton, R. S. and Barto, A. G. (2018). Reinforcement learning: An introduction. MIT press.

- Sutton et al., (2000) Sutton, R. S., McAllester, D. A., Singh, S. P., and Mansour, Y. (2000). Policy gradient methods for reinforcement learning with function approximation. In Advances in neural information processing systems, pages 1057–1063.

- Tetenov, (2012) Tetenov, A. (2012). Statistical treatment choice based on asymmetric minimax regret criteria. Journal of Econometrics, 166(1):157–165.

- Tsitsiklis and Van Roy, (1997) Tsitsiklis, J. and Van Roy, B. (1997). An analysis of temporal-difference learning with function approximation. IEEE Transactions on Automatic Control, 42(5):674–690.

- Wager and Xu, (2021) Wager, S. and Xu, K. (2021). Diffusion asymptotics for sequential experiments. arXiv preprint arXiv:2101.09855.

- Yu et al., (2020) Yu, T., Thomas, G., Yu, L., Ermon, S., Zou, J., Levine, S., Finn, C., and Ma, T. (2020). Mopo: Model-based offline policy optimization. arXiv preprint arXiv:2005.13239.

For Online Publication

Appendix to:

DYNAMICALLY OPTIMAL TREATMENT ALLOCATION USING REINFORCEMENT LEARNING

Karun Adusumilli⋆, Friedrich Geiecke† & Claudio Schilter‡

⋆Department of Economics, University of Pennsylvania;

akarun@sas.upenn.edu

†Department of Methodology, London School of Economics;

f.c.geiecke@lse.ac.uk

‡Department of Economics, University of Zurich; claudio.schilter@econ.uzh.ch

Supplementary material for this paper (not intended for publication) can be accessed here.

Appendix A Proofs of main results

We start by recalling the definition of a viscosity solution. We focus here on the Dirichlet boundary condition. The other boundary conditions are discussed in Appendix B.

Consider the Dirichlet problem

| (A.1) |

where denotes the derivative with respect to , is the domain of the PDE, and is the set on which the boundary condition is specified. In what follows, let . Also, denotes the space of all twice continuously differentiable functions on .

Definition 1.

A bounded continuous is a viscosity sub-solution to (A.1) if:

(i) on , and

(ii) for each , if has a local maximum at , then

Similarly, a bounded continuous is a viscosity super-solution to (A.1) if:

(i) on , and

(ii) for each , if has a local minimum at , then

Finally, is a viscosity solution to (A.1) if it is both a sub- and a super-solution.

We say that is a viscosity sub-solution to (A.1) on if only condition (ii) holds, i.e., it need not be the case that on . Similarly, is a viscosity super-solution to (A.1) on if only condition (ii) holds. Henceforth, whenever we refer to a viscosity super- or sub-solution, we will implicitly assume that it is bounded and continuous.

We say that a PDE is in Hamiltonian form if

for some Hamiltonian . Suppose that the PDE (A.1) can be written in Hamiltonian form. Then there exists a unique viscosity solutions to (A.1) if the following regularity conditions are satisfied (see, e.g., Crandall et al, 1992):

-

(R1)

is uniformly continuous in all its arguments.

-

(R2)

There exists a modulus of continuity such that ,

-

(R3)

-

(R4)

There exist some viscosity sub- and super-solutions to PDE (A.1).

A.1. Proof of Lemma 1

We prove the lemma for the Dirichlet boundary condition. The other boundary conditions are discussed in Appendix B. Consider the PDE

| (A.2) | ||||

where is defined as

| (A.3) |

Let denote a viscosity solution to (A.2). By Lemma G.1 in Appendix G and the subsequent discussion, there is a one-to-one transformation between and any solution, , for PDE (2.3) under the Dirichlet boundary condition (2.7); this transformation is given by . Hence, exists and is unique if and only if also exists and is unique.111The utility of this transformation is that we can now handle any .

It thus suffices to show existence of a unique solution for (A.2). It is straightforward to verify that the function satisfies the regularity conditions (R1)-(R3) under Assumption 1. Furthermore, the set satisfies the uniform exterior sphere condition.222A set is said to satisfy the uniform exterior sphere condition if there exists such that every point is on the boundary of a ball of radius that otherwise does not intersect . When these properties are satisfied, Crandall (1997, Section 9) shows that a unique viscosity solution exists for (A.2), as long as (R4) is satisfied, i.e., we are able to exhibit continuous sub- and super-solutions to (A.2). Under Assumption 1, it can be verified that one such set is and , where is chosen to satisfy .

A.2. Proof of Theorem 1

The following proof is based on an argument first sketched by Souganidis (2009). We focus here on the Dirichlet boundary condition with (but could be ). The argument for the setting with is similar, so we omit it. We also omit the proof for the periodic boundary condition since it follows by the same reasoning (and is in fact simpler since we do not need to consider separate cases for regions close to the boundary).