-Divergence loss for the kernel density estimation with bias reduced

Abstract

Allthough nonparametric kernel density estimation with bias reduce is nowadays a standard technique in explorative data-analysis, there is still a big dispute on how to assess the quality of the estimate and which choice of bandwidth is optimal. This article examines the most important bandwidth selection methods for kernel density estimation with bias reduce, in particular, normal reference, least squares cross-validation, biased crossvalidation and -Divergence loss. Methods are described and expressions are presented. We will compare these various bandwidth selector on simulated data. As an example of real data, we will use econometric data sets CO2 per capita in example 1 and the second data set consists of 107 eruption lengths in minutes for the Old Faithful geyser in Yellowstone National Park, USA.

keywords:

-Divergence; Kernel Density Estimation; bandwidth.1 Introduction

Selecting an appropriate bandwidth for a kernel density estimator is of crucial importance, and the purpose of the estimation may be an influential factor in the selection method. In many situations, it is sufficient to subjectively choose the smoothing parameter by looking at the density estimates produced by a range of bandwidths. A good overview on kernel density estimators is supplied by Silverman [18]; Scott [17]; Mugdadi and Ahmad [14].

Throughout this article, we use the following notation. Let , of size from a density where the Parzen [15] kernel estimator is defined by

In general, is the kernel function (e.g. normal density function) and is the bandwidth. A large body of research is devoted to choosing , essentially the amount of smoothing to apply. Usually, smoothing parameters can be chosen via cross validation or by minimizing a measure of error.

An important recent paper in this area is Xie and Wu [21]. Xie and Wu studied an estimator which reduces the bias, the performance of which in both theory and simulations proved to be clearly superior to other methods currently popular in the literature. Xie and Wu [21] presented an estimator which reduces the bias, defined by:

| (1) | |||||

| (2) |

the bandwidth is the most dominant parameter in the kernel density estimator. This parameter controls the amount of smoothing, and is analogous to the bandwidth in a histogram.

Even though the kernel estimator depends on the kernel and the bandwidth in a rather complicated way, a graphical representation clearly illustrates the difference in importance between these two parameters, see figure 2.3 and 2.6a in Wand and Jones [20]. To explore the most relevant bandwidth selection methods in density estimation for complete data see the reviews of Turlach [19], Cao et al. [3], Jones et al. [8] or Heidenreich et al. (2013), Mammen et al. ([11] and [12]), and the recent work on -Divergence for Bandwidth Selection by Dhaker and al. [5].

Our aim in this paper is to propose and compare several bandwidth selection procedures for the kernel density estimators introduced by Xie and Wu [21]. The procedures we study are bandwidth selector based on the criterion of -divergence with different beta values. A simulation study is then carried out to assess the finite sample behavior of these bandwidth selectors.

The remainder of the paper is organised as follows. In Section 2, we state our main results: presents the method proposed for bandwidth selector based . Section 3 estimation of the optimal bandwidth

Section 4 is devoted to our simulation results. Section 5 applies the methods to real data. We conclude the paper in Section 6,

2 Bandwidth selection based -divergence

The -divergence [Cichocki [4], Basu [1] and Eguchi [6]] is a general framework of similarity measures induced from various statistical models, such as Poisson, Gamma, Gaussian, Inverse Gaussian and compound Poisson distribution. For the connection between the -divergence and the various statistical distributions, see Jorgensen [9]. Beta divergence was proposed in Basu [1] and Minami and Eguchi [13] and is defined as dissimilarity between the density function and its estimator

In the case ,

The following theorem allows us to give the analytical value of bandwidth which minimizes the mean .

Theorem 1

Let the following conditions on be satisfied:

-

(F1)

is compactly supported on .

-

(F2)

is four times continuously differentiable on .

-

(F3)

.

the bandwidth that minimizes the mean -divergence between a kernel estimator and density is:

| (3) |

Proposition 1

Under we have

| (4) |

and

| (5) |

where

Corollary 1

and

3 The choice of the bandwidth

In this section, we describe bandwidth selection methods for the density estimator defined in (1). These methods consist of adaptations of common automatic selectors for kernel density estimation. We propose two selection methods a Normal reference and the cross-validation method. The Normal reference bandwidth is based on estimating the infeasible optimal expression (6), in which the unknown element is .

3.1 Rule-of-thumb for bandwidth selection

This method is based on the rule-of-thumb, Silverman [18], for complete data.The idea is to assume that the underlying distribution is normal, , and in this situation

so

and

In that case the asymptotically optimal bandwidth in Equation (3) becomes the normal reference bandwidth.

with being the standard deviation of .

For the Gaussian kernel, and so that

| (8) |

for

| (9) |

The standard deviation can be estimated by the sample standard deviation or by the standardized interquartile range for robustness against outliers , but a better rule of thumb is (e.g., Silverman, 1986, pp. 45–47; Härdle, 1991, p. 91).

| (10) |

with

3.2 Cross-validation

The method previously defined is based on minimising estimations of the , more precisely of the . This procedure relies on the minimisation of the (integrated squared error), the methodology is the same as in Rudemo [16] and Bowman [2] applied to (1).

Let write:

Note that dz does not depend on , so the minimisation of the ISE is equivalent to minimise the following function:

The principle of the least squares cross-validation method is to find an estimate of from the data and minimize it over . Consider the estimator

with

4 Simulation

In this section we evaluate the performance of the bandwidth selection procedures presented in Section 2. To this goal we have carried out a simulation study including rule-of-thumb (), cross-validation bandwidth () and for minimizing criterion -divergence (with ).

We consider various sets of experiments in which data are generated from the mixture of a Normal and Normal distributions. Hence, the DGP (Data Generating Process) is generated from with the density

| (11) |

where and . One thousand Monte Carlo samples of size n are generated from the normal mixture model in Equation (11) for each combination of .

The results of our different sets of experiments are presented in Tables 1-3.

Table 1 give the exhibits simulated relative efficiency of the kernel estimator, using bandwidths , and , it is lower than 1, because the optimal bandwidth minimize . Each bandwidth, mean and mean relation error are obtained, these values are given by respectively,

Tables 2 and 3.

-

1-

For all situations, each relative efficiency because the optimal bandwidth minimizes the .

-

2-

The normal reference bandwidth hNR performswell if the true density is not very far from normal, such as the cases of , and . Otherwise, it usually has the smallest and largest , tending to oversmooth its kernel density estimate the most.

-

2-

We have to remark that in table 1, the LSCV bandwidth hlscv needs a large sample size in order to be competitive. Note also that in Table 2, it is seen that is close to the optimal , but the corresponding is large, which means that the bias of is small but its variation is large in Table 3.

-

3-

The bandwidth seems to be the best existing bandwidth selectors. In most situations, it is indeed one of the best bandwidth selectors, However, it behaves very poorly for small (the true density curve is sharp).

| 50 | 0.934 | 0.953 | 0.853 | 0.723 | 0.703 |

|---|---|---|---|---|---|

| 200 | 0.945 | 0.925 | 0.955 | 0.931 | 0.903 |

| 700 | 0.990 | 0.945 | 0.982 | 0.987 | 0.952 |

| 50 | 0.870 | 0.837 | 0.867 | 0.890 | 0.905 |

| 200 | 0.937 | 0.880 | 0.897 | 0.954 | 0.932 |

| 700 | 0.964 | 0.930 | 0.929 | 0.842 | 0.858 |

| 50 | 0.584 | 0.767 | 0.634 | 0.631 | 0.623 |

| 200 | 0.553 | 0.892 | 0.625 | 0.879 | 0.721 |

| 700 | 0.529 | 0.946 | 0.612 | 0.877 | 0.813 |

| 50 | 0.864 | 0.899 | 0.904 | 0.853 | 0.876 |

| 200 | 0.938 | 0.928 | 0.914 | 0.962 | 0.987 |

| 700 | 0.973 | 0.952 | 0.974 | 0.927 | 0.932 |

| 50 | 0.882 | 0.852 | 0.823 | 0.734 | 0.872 |

| 200 | 0.963 | 0.880 | 0.780 | 0.925 | 0.967 |

| 700 | 0.836 | 0.925 | 0.743 | 0.943 | 0.780 |

| 50 | 0.230 | 0.770 | 0.611 | 0.587 | 0.554 |

| 200 | 0.101 | 0.912 | 0.686 | 0.769 | 0.687 |

| 700 | 0.051 | 0.949 | 0.727 | 0.880 | 0.721 |

| 50 | 0.400 | 0.810 | 0.723 | 0.889 | 0.457 |

| 200 | 0.285 | 0.945 | 0.852 | 0.934 | 0.579 |

| 700 | 0.222 | 0.963 | 0.967 | 0.978 | 0.789 |

| 50 | 0.2390 | 0.852 | 0.712 | 0.845 | 0.831 |

| 200 | 0.1390 | 0.926 | 0.897 | 0.915 | 0.805 |

| 700 | 0.0817 | 0.956 | 0.945 | 0.921 | 0.878 |

| 50 | 0.1360 | 0.588 | 0.702 | 0.645 | 0.613 |

| 200 | 0.0523 | 0.458 | 0.764 | 0.758 | 0.802 |

| 700 | 0.0205 | 0.341 | 0.861 | 0.655 | 0.841 |

| 50 | 0.464 | 0.528 | 0.530 | 0.520 | 0.323 | 0.347 |

|---|---|---|---|---|---|---|

| 200 | 0.362 | 0.393 | 0.399 | 0.383 | 0.321 | 0.328 |

| 700 | 0.287 | 0.302 | 0.310 | 0.293 | 0.308 | 0.309 |

| 50 | 0.330 | 0.397 | 0.425 | 0.343 | 0.223 | 0.286 |

| 200 | 0.248 | 0.267 | 0.312 | 0.248 | 0.193 | 0.280 |

| 700 | 0.196 | 0.197 | 0.242 | 0.200 | 0.186 | 0.244 |

| 50 | 0.134 | 0.104 | 0.358 | 0.098 | 0.510 | 0.041 |

| 200 | 0.087 | 0.060 | 0.027 | 0.087 | 0.485 | 0.038 |

| 700 | 0.068 | 0.043 | 0.219 | 0.057 | 0.421 | 0.0370 |

| 50 | 0.520 | 0.590 | 0.592 | 0.588 | 0.429 | 0.426 |

| 200 | 0.404 | 0.437 | 0.444 | 0.434 | 0.395 | 0.423 |

| 700 | 0.316 | 0.336 | 0.344 | 0.333 | 0.354 | 0.345 |

| 50 | 0.401 | 0.430 | 0.479 | 0.373 | 0.326 | 0.342 |

| 200 | 0.320 | 0.298 | 0.373 | 0.265 | 0.280 | 0.282 |

| 700 | 0.254 | 0.214 | 0.287 | 0.212 | 0.233 | 0.239 |

| 50 | 0.366 | 0.103 | 0.464 | 0.203 | 0.0422 | 0.0451 |

| 200 | 0.276 | 0.061 | 0.342 | 0.053 | 0.0380 | 0.0380 |

| 700 | 0.221 | 0.0428 | 0.267 | 0.0426 | 0.0343 | 0.0314 |

| 50 | 1.290 | 0.770 | 1.400 | 0.608 | 0.420 | 0.475 |

| 200 | 0.989 | 0.477 | 0.1.070 | 0.441 | 0.330 | 0.470 |

| 700 | 0.768 | 0.353 | 0.829 | 0.336 | 0.442 | 0.272 |

| 50 | 1.270 | 0.468 | 1.370 | 0.369 | 0.310 | 0.295 |

| 200 | 0.961 | 0.297 | 1.040 | 0.262 | 0.210 | 0.286 |

| 700 | 0.750 | 0.208 | 0.810 | 0.197 | 0.209 | 0.270 |

| 50 | 1.270 | 0.0982 | 1.370 | 0.0745 | 0.045 | 0.0415 |

| 200 | 0.955 | 0.061 | 1.030 | 0.053 | 0.040 | 0.0385 |

| 700 | 0.745 | 0.0424 | 0.804 | 0.040 | 0.039 | 0.0339 |

| 50 | 0.124 | 0.072 | 0.077 | 0.0874 | 0.379 |

|---|---|---|---|---|---|

| 200 | 0.0785 | 0.0829 | 0.1050 | 0.0578 | 0.1620 |

| 700 | 0.0396 | 0.0717 | 0.0572 | 0.0436 | 0.0509 |

| 50 | 0.1370 | 0.1510 | 0.1670 | 0.1510 | 0.4560 |

| 200 | 0.0655 | 0.1360 | 0.0882 | 0.1010 | 0.2490 |

| 700 | 0.0559 | 0.0729 | 0.0537 | 0.0818 | 0.0104 |

| 50 | 0.772 | 0.2530 | 0.3000 | 0.3990 | 0.4410 |

| 200 | 0.674 | 0.1210 | 0.1250 | 0.1520 | 0.2070 |

| 700 | 0.679 | 0.0772 | 0.0506 | 0.0726 | 0.185 |

| 50 | 0.1430 | 0.1040 | 0.1630 | 0.0748 | 0.398 |

| 200 | 0.0774 | 0.0800 | 0.0931 | 0.0501 | 0.184 |

| 700 | 0.0483 | 0.0626 | 0.0600 | 0.0361 | 0.037 |

| 50 | 0.172 | 0.1930 | 0.1400 | 0.2260 | 0.4560 |

| 200 | 0.236 | 0.1530 | 0.0899 | 0.1460 | 0.121 |

| 700 | 0.285 | 0.0989 | 0.0506 | 0.0794 | 0.119 |

| 50 | 3.67 | 0.2620 | 1.380 | 0.3980 | |

| 200 | 4.29 | 0.1250 | 0.986 | 0.1720 | 0.353 |

| 700 | 4.58 | 0.0838 | 0.652 | 0.0878 | 0.137 |

| 50 | 1.14 | 0.1450 | 0.2390 | 0.2430 | 0.4580 |

| 200 | 1.23 | 0.0815 | 0.1210 | 0.0899 | 0.2530 |

| 700 | 1.29 | 0.0686 | 0.0745 | 0.0540 | 0.0203 |

| 50 | 2.40 | 0.1860 | 0.600 | 0.2510 | 0.4340 |

| 200 | 2.68 | 0.1180 | 0.444 | 0.1440 | 0.2020 |

| 700 | 2.80 | 0.0743 | 0.296 | 0.0804 | 0.0597 |

| 50 | 15.7 | 0.884 | 5.95 | 0.3980 | 0.4810 |

| 200 | 17.1 | 1.021 | 4.51 | 0.1570 | 0.2630 |

| 700 | 17.7 | 1.104 | 3.34 | 0.0656 | 0.0178 |

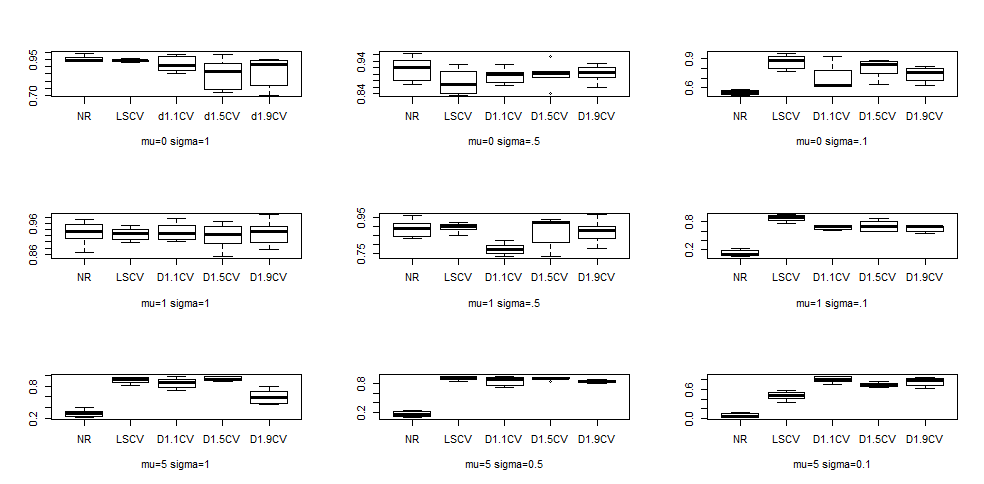

Figure 1 compare, for densities with and , the results of the five bandwidth selection , and (discussed in Section 3), relatively to the results obtained by using the optimal bandwidth (). These figures present boxplots of the ratio for each bandwidths , and (with and ). We see the and (with ) methods gave overall the bests ratios across all simulations, and that this ratio was rather large in general.

5 Illustration with real data

Two examples are provided to demonstrate the performance of kernel density estimation with different bandwidths, where the Gaussian kernel is used. All of them are classical examples of unimodal and bimodal distributions, respectively.

Example 1

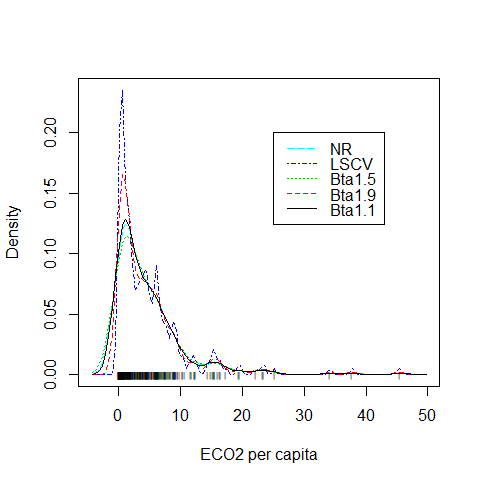

The first data set comprises the CO2 per capita in the year of 2014. The data set can be downloaded from the world bank website.

Figure 2 shows the estimated density of CO2 per capita in the year of 2008, , we using bandwidths , , , and

The data set that the estimated density that was computed with the and bandwidths captures the peak that characterizes the mode, while the estimated density with the bandwidths that , and smoothes out this peak.

This happens because the outliers at the tail of the distribution contribute to , and be larger than the than other bandwidths..

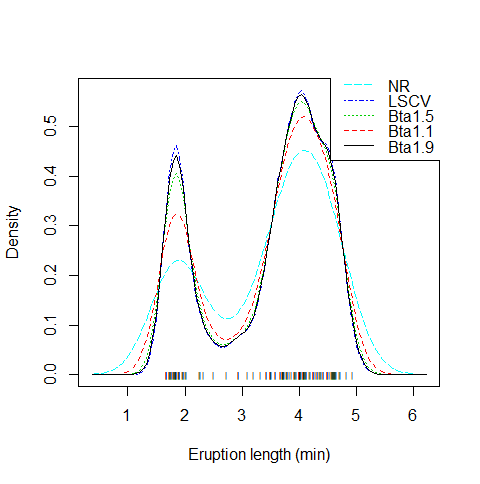

Example 2

we use the time between eruptions set for the Old Faithful geyser in Yellowstone National Park, Wyoming, USA (107 sample data, source: Silvermanl [21]).

Figure 3 plot the data points and the kernel density

estimates for old faithful geyser data, we using bandwidths

, , , and .

An important point to note that the density curve for eruption length is similar to bimodal normal density (normal mixture). From our example 2 we see that the is always larger than the others bandwidths, he heavily oversmoothes its kernel density curve, underestimating the two peaks of the curve but overestimating the valley between them. About , and seems to undersmooth the curve too much, overestimating the two peaks but underestimating for the valley.

However is proper bandwidth for their density estimate to be able to capture the feature of the true density curve.

6 Conclusions

This paper proposed the method for bandwidth selection of bias reduction kernel density estimator, given in (2). A various bandwidth selection strategies have been proposed such as normal reference , least squares cross-validation and for minimizing criterion -divergence (with and ).

The normal reference bandwidth method is a simple and quick selector, but limited the practical use ., since they are restricted to situations where a pre-specified family of densities is correctly selected.

The do not provide a smooth density estimation, although asymptotically optimal, the finite sample behavior of is disappointing for its variability and undersmoothing.

We have attempted to evaluate choice the optimal bandwidth

and , using -divergence. Compared to traditional bandwidth selection methods designed for kernel density estimation, our proposed bandwidth selection method is always one of the best for having large and small .

Simulation studies showed that our proposed optimal bandwidth method designed for kernel density estimation adapts to different situations, and out-performs other bandwidths.

we conclude that the choice of the bandwidth based on the real data is consistent with the one based on simulations which is the and ) method gives us a smoother density estimation.

References

- [1] Basu, A., Harris,I. R., Hjort N. L. and Jones M. C. (1998). Robust and efficient estimation by minimising a density power divergence, Biometrika 85(3) , 549-559.

- [2] Bowman A. W., (1984). An alternative method of cross-validation for the smoothing of density estimates, Biometrika 71(2), 353-360.

- [3] Cao, R., Cuevas, A., and Gonalez-Manteiga, W. (1994), A comparative study of several smoothing methods in density estimation?, Computational Statistics and Data Analysis, 17, 153?176.

- [4] Cichocki, A.; Zdunek, R.; Amari, S. (2006) Csiszar?s divergences for nonnegative matrix factorization: Family of new algorithms. In Lecture Notes in Computer Science; Springer: Charleston, SC, USA, 3889, 32?39.

- [5] Dhaker H., Ngom P., Deme Elhadji and Mbodj M. New approach for bandwidth selection in the kernel density estimation based on -divergence, Journal of Mathematical Sciences: Advances and Applications. 51, 2018, 57-83

- [6] Eguchi S. and Kano Y. (2001) Robustifying maximum likelihood estimation. Technical report, Institute of Statistical Mathematics, June.

- [7] Eugene F. S, (1969), Estimation of a probability density function and its derivatives, The annals of Mathematical Statistics, 40(4), 1187-1195.

- [8] Jones, M.C., Marron, J.S., and Sheather, S.J. (1996), A brief survey of bandwidth selection for density estimation, Journal of the American Statistical Association, 91, 401–407.

- [9] Jorgensen B. (1997) The Theory of Dispersion Models. Chapman Hall/CRC Monographs on Statistics and Applied Probability.

- [10] Kanazawa Y. (1993) Hellinger distance and Kullback-Leibler loss for the kernel density estimator, Statistics and Probability Letters 18(4), 315-321.

- [11] Mammen, E., Martinez-Miranda, M.D., Nielsen, J.P., and Sperlich, S. (2011), Do-validation for kernel density estimatio?, Journal of the American Statistical Association, 106, 651-660.

- [12] Mammen, E., Martinez-Miranda, M.D., Nielsen, J.P., and Sperlich, S. (2014), Further theoretical and practical insight to the do-validated bandwidth selector, Journal of the Korean Statistical Society, 43, 355-365.

- [13] Minami, M.; Eguchi, S. (2002) Robust blind source separation by Beta-divergence. Neural Comput. 14, 1859-1886.

- [14] Mugdadi, A. R. and Ibrahim A. A. (2004), A bandwidth selection for kernel density estimation of functions of random variables, Computational Statistics and Data Analysis, 47(1), 49-62

- [15] Parzen, E. (1962), On estimation of a probability density function and mode, Annals of Mathematical Statistics 33, 1065-1076.

- [16] Rudemo M. (1982) Empirical choice of histograms and kernel density estimators, Scandinavia Journal of Statistics 9(2), 65-78.

- [17] Scott, W. D (1992), Multivariate density estimation theory, practice, and visualization, Wiley, New York.

- [18] Silverman, B. W. (1986), Density estimation for statistics and data analysis, Chapman and Hall, London.

- [19] Turlach, B.A. (1993), Bandwidth selection in kernel density estimation: A review, Technical report, Universite catholique de Louvain.

- [20] Wand, M. P. and M. C. Jones (1995), Kernel Smoothing, Chapman and Hall, London, UK.

- [21] Xie X. and Wu J. (2014), Some Improvement on Convergence Rates of Kernel Density Estimator, Applied Mathematics, 2014, 5, 1684-1696.