A CLT for second difference estimators

with an application to volatility and intensity

Abstract.

In this paper we introduce a general method for estimating the quadratic covariation of one or more spot parameters processes associated with continuous time semimartingales. This estimator is applicable to a wide range of spot parameter processes, and may also be used to estimate the leverage effect of stochastic volatility models. The estimator we introduce is based on sums of squared increments of second differences of the observed process, and the intervals over which the differences are computed are rolling and overlapping. This latter feature lets us take full advantage of the data, and, by sufficiency considerations, ought to outperform estimators that are only based on one partition of the observational window. The main result of the paper is a central limit theorem for such triangular array rolling quadratic variations. We highlight the wide applicability of this theorem by showcasing how it might be applied to a novel leverage effect estimator. The principal motivation for the present study, however, is that the discrete times at which a continuous time semimartingale is observed might depend on features of the observable process other than its level, such as its (non-observable) spot-volatility process. As the main application of our estimator, we therefore show how it may be used to estimate the quadratic covariation between the spot-volatility process and the intensity process of the observation times, when both of these are taken to be semimartingales. The finite sample properties of this estimator are studied by way of a simulation experiment, and we also apply this estimator in an empirical analysis of the Apple stock. Our analysis of the Apple stock indicates a rather strong correlation between the spot volatility process of the log-prices process and the times at which this stock is traded (hence observed).

Key words and phrases:

Asynchronous times; central limit theorem, consistency; convergence rates; counting processes; endogenous observation times; high-frequency; intensity; irregular times; microstructure; observed asymptotic variance; overlapping intervals; rolling intervals; sufficiency; two-scales estimation.1. Introduction

With an increasing availability of high frequency data, the ambition level as to what can be estimated with reasonable precision has, naturally, also been raised. This paper concerns the estimation of the quadratic covariation of various spot parameter processes associated with continuous time semimartingales, which are observed at discrete times over a finite interval of time. The main result of the paper is a central limit theorem that applies to a class of such estimators. Estimation of the quadratic covariation associated with spot parameter processes is, for example, important for learning about the (hyper-) parameters governing the spot parameter processes, e.g. volatility-of-volatility; or for learning about possible dependencies between concurrently observed semimartingale processes; or for estimating the possible dependency between the observation times and various spot parameter processes associated with the observable process. The motivation for the present paper is an example of the latter, namely the estimation of the quadratic covariation between the volatility of a continuous semimartingale process, and the intensity processes governing the observation times of this process.

To fix ideas, consider a typical analysis of high frequency data: Based on discrete time observations of a continuous semimartingale process one seeks to estimate an integrated parameter ,

where is a spot parameter process such as volatility, leverage effect, an instantaneous regression coefficient, or the like. The canonical example is the case where is the spot-volatility process associated with an Itô process of the form , where is a standard Wiener process, and the problem is to estimate the integrated volatility over one or consecutive intervals of time. This example goes back to the research on realised volatility by Andersen et al. (2001), Barndorff-Nielsen and Shephard (2002), Jacod and Protter (1998), Zhang et al. (2005), and others. The econometric interest in investigating nonparametric estimates of this type grew out of the study of volatility clustering by Engle (1982) and Bollerslev (1986). For further references, see Jacod and Protter (2011), Mykland and Zhang (2012), and Aït-Sahalia and Jacod (2014).

The general setup and results of this paper take the following form. Let and be spot parameter processes (potentially the same) associated with one or more semimartingale processes observed at discrete times over a finite interval of time . In Mykland and Zhang (2017a, b) an estimator of the quadratic covariation was introduced, and it was shown that this estimator is consistent. In the present paper we further derive the convergence rates for such estimators, and prove a general central limit theorem that, under some regularity conditions, applies to a wide range of estimators based on the second differencing of estimators of integrated spot processes. As mentioned, our main example of the use of this estimator is the problem of estimating the quadratic covariation between the volatility of a semimartingale process, and the intensity of the observation times of this process. This type of endogenous time problem exists in real applications but is often overlooked. We also sketch how our estimation methods and the central limit theorem can be applied to a novel estimator of the leverage effect.

The paper proceeds as follows. In Section 2 we first describe the model and state our most important assumptions, subsequently we provide a heuristic derivation of the stochastic quantities that are important for the theory that follows. Section 2.2 contains the consistency results and introduces the “two-scale” estimator of . These consistency results generalise the findings in Mykland and Zhang (2017a). In Section 3 we present the main theoretical novelty of the paper, namely a central limit theorem for triangular array rolling quadratic variations based on second differencing of estimators of integrated spot processes. The proof of this theorem is deferred to Appendix F. Section 2.2 also contains an important corollary to the effect that the ‘Observed asymptotic variance’ developed in Mykland and Zhang (2017a) yields consistent estimates of the asymptotic variance of the two-scales estimator we introduce. In Section 4 we specialise the theory developed in the preceding sections to the problem of estimating the quadratic covariation between the spot parameter process of a continuous time semimartingale, and the intensity process of its observation times. This is the volatility-intensity problem. In Section 4.2 we investigate the finite samples properties of our estimator by way of a simulation study, while Section 4.3 contains an empirical analysis of the Apple stock observed over trading days in January . Most technical matters as well as long proofs can be found in the appendices. Appendix B also contains a stable central limit theorem for càdlàg martingales, as well as a corollary with some alternative conditions that might be easier to check in applications.

2. The general setup and problem

In this section we first present the setting for our estimation procedures, define some key quantities, provide a heuristic overview of some important results, and explain what type of estimators our central limit theorem applies to. Subsequently, in Section 2.2, we provide a more formal presentation, and state the main consistency results of the paper.

2.1. Setup and basic insights

We suppose that one or more semimartingale processes are observed at high frequency over a finite interval of time . The semimartingales are typically contaminated by microstructure noise, so what we observe is , for time points, where is microstructure noise. Based on these data we form estimators and , which are consistent for and , respectively, where the spot parameter processes and are also assumed to be semimartingales. Our results continue to hold when and are replaced by the sequences and of semimartingale processes, but to ease the notation we drop the superscript for the time being. The spot parameter processes may be the spot volatility of the continuous part of the process , with a standard Wiener process, that is ; it may be the instantaneous leverage effect, ; or the instantaneous volatility of volatility, ; or the stochastic intensity process governing the frequency of the observation times, etc.

To be clear, the notation refers to the continuous time quadratic covariation of two semimartingales and from time zero to (Jacod and Shiryaev, 2003, pp. 51–52). Semimartingales are defined in, for example, Jacod and Shiryaev (2003, Definition I.4.21, p. 43).

Definition 2.1.

We assume that all our semimartingales are càdlàg (right continuous with left limits), and that all data generating and latent processes live on the same filtered probability space with , and that this filtered space satisfies the ‘usual conditions’ (Jacod and Shiryaev, 2003, Definitions I.1.2–I.1.3, p. 2). When necessary, we will also invoke sequences of filtrations on , that is for all .

For the proof of the main central limit theorem of the paper, Theorem 3.2, we will need a few additional technical conditions on the structure of the filtered probability space.

We now turn to the construction of our estimator. Divide the time interval into blocks , of equal length, with and . Set , and for convenience, assume that for . Since we shall permit rolling and overlapping intervals, let be an integer no greater than . From now on we drop the index from the , and when it does not cause confusion. For any real functions and , define

| (2.1) |

where , and write . For , the notation means that

with an increasing sequence of integers. The basic building block for all the estimators we present is the rolling quadratic covariation

where and are consistent estimators of the integrated spot processes and , respectively. It is important to keep in mind that and are defined on the discrete grid , as opposed to the continuous time quadratic covariation .

To see how is used to estimate , we here present a heuristic analysis, to be made precise in the subsequent section. Under the assumption that can be expressed as a sum of , an error martingale, and terms associated with the edge effects, we can write,

where the ‘estimation error’ might contain terms that are not asymptotically negligible, and must be dealt with by so-called two-scale constructions (Zhang et al., 2005; Mykland et al., 2019). We return to this issue shortly. From Mykland and Zhang (2017a, Theorem 1, p.203), we have the ‘Integral-to-Spot Device’, that is

as , and and . The key ingredient for proving this theorem is an application of Lemma 2 in Mykland and Zhang (2017a, p. 206), from which we obtain that

| (2.2) |

where for are the functions

| (2.3) |

The central limit theorem we present in Section 3 concerns quantities of the type

| (2.4) |

as and . In (2.4) the functions and are bounded and deterministic, while and are sequences of semimartingale processes. We see that the right hand side of (2.2) is a special case of (2.4), and so are the non-negligible terms contained in the ‘estimation error’ referred to above.

2.2. Consistency

Suppose that and are two integrated spot-processes, and that and are sequences of semimartingales adapted to (or in the case that or for all ), and that both sequences satisfy Condition 3 below. If and depend on , we assume that the pair converges in probability to limiting semimartingales and , and that converges in probability to .

The two spot-processes might be associated with the same underlying semimartingale (in which case we can have for all ), or with two different semimartingales concurrently observed. In the latter case, the sampling times can be asynchronous, and the total number of observations may differ. To not overburden the notation, however, we assume that the number of observations are the same for both processes, and equals . We are given the estimators and of and , respectively. Both and are consistent and admit representations of the type , in terms of a semimartingale and edge effects and associated with phasing in and phasing out the estimator, respectively. For we write . This means that for the estimators can be represented as

| (2.5) |

The assumption, implicit in (2.5), that the edge effect of phasing in an estimator at is the same as the edge effect associated with phasing out an estimator at . This is exact in the (usual) case of additive estimators (Mykland and Zhang, 2017a, Section 5.1, p. 215). The results that follow extend with little effort to situations where the edge effects in the two ends of the interval behave differently.

Definition 2.2.

(Stable convergence). We say that a sequence of martingales converges stably in law to with respect to if (i) is measurable with respect to belonging to an extension of ; and (ii) for every measurable (real-valued) random variable , the sequence converges in law to . We then write stably.

Condition 1.

Remark 2.3.

The requirements of Condition 1 are likely to be satisfied in applications, but they are stronger than what we need for the present purposes. For the consistency results of this section we only need the weaker Condition 5 of Mykland and Zhang (2017b, p. 7), which is implied by Condition 1. A sequence of semimartingales fulfills this condition if it is tight and P-UT (see Jacod and Shiryaev (2003, p. 377) for the definition of the P-UT property).

Theorem 2.4.

Proof.

In Appendix D we also provide the conclusion of the above theorem with slightly more stringent restrictions on the edge effects. Corresponding results for all combinations of assumptions on the edge effects can be deduced from the results in Appendix D.

We now turn to estimation of the quadratic covariation . As will become clear, how one ought to estimate depends on the convergence rates of the error martingales and , that is the and required for and to satisfy Condition 1. From the conclusion of Theorem 2.4 we see that, provided is of order , then

By Condition 1 the quadratic covariation of the error martingales is , consequently,

which tends to zero in probability as provided . We summarise this in a lemma.

Lemma 2.5.

Assume that Condition 1 holds. Suppose that , that and such that is of order as , then

| (2.6) |

Proof.

By Condition 1 this is direct from the two displays above. ∎

Notice that the conclusion of Lemma 2.5 continues to hold when provided and are asymptotically orthogonal (see Jacod and Shiryaev (2003, Proposition I.4.15, p. 41) for the notion of local martingales being orthogonal). Also note that when one might choose such that , at the cost of a slower rate of convergence.

The estimation problem is harder when is not asymptotically negligible. This occurs, for example, when one seeks to estimate , such that the convergence rates and of Condition 1 are equal. As an estimator of the quadratic covariation in such situations we propose the Two Scales Quadratic Covariation (TSQC) estimator. It is given by

| (2.7) |

where are user specified sequences of integers (tuning parameters) tending to infinity. Since and must be of the same order, a natural choice is for some integer , with fixed and independent of . We first present a consistency result, and then return to the central limit theory for this estimator at the end of Section 3.

Corollary 2.6.

(Consistency of the TSQC-estimator) Assume that the conditions of Theorem 2.4 are in force, and that . Let , for some fixed integer , be positive integers tending to infinity such that . Then,

as .

Proof.

Remark 2.7.

The conclusion of Corollary 2.6 is still valid when provided . But if the convergence rates are known and different one would, as already mentioned, rather use the estimator in (2.6). There might be situations, however, where the convergence rates and are not known exactly, but known to lie in some interval, say . In that case, one sets , and the conclusion of Corollary 2.6 holds.

3. Central limit theory

The consistency results of the previous section are extensions of theory developed in Mykland and Zhang (2017a, b). That paper, however, did not establish limiting normality for the estimators presented, and it is to this topic we now turn.

In a first part we present a theorem on the convergence rate of triangular array rolling quadratic covariations as approximations to quadratic covariations of spot processes. We then present the central limit theorem for such approximations. Both these results supplement the consistency result of Mykland and Zhang (2017b, Theorem 7, p. 1). The proofs of both these theorems are deferred to the appendix. As an example of the use of this theorem, and to show its versatility, we show how it can be applied to a novel estimator of the leverage effect. In Section 3.2 we present theory for the TSQC-estimator. In particular, we show that the observed asymptotic variance of Mykland and Zhang (2017a) can be applied to estimate the asymptotic variance of this estimator. This is important because analytical expressions for the TSQC are hard to derive (see the discussion in Mykland and Zhang (2017a, pp. 198–200)).

3.1. Convergence rate and CLT for rolling quadratic variations

Introduce the processes

| (3.1) |

where and are sequences of semimartingales, and and are deterministic càdlàg functions bounded by (there is nothing special about here, and it suffices that they are bounded by a constant). We denote by a countable collection , of such functions, such as from (2.3), but more generally to be defined in each case, and similarly belongs to the collection (see Appendix A for further details). In Mykland and Zhang (2017b, Theorem 7, p. 1) it was shown that

| (3.2) |

In this section we study the rate of convergence and present a central limit theorem for the approximation in (3.2). Such statements will help with the assessment of the accuracy and with optimal calibration of the TSQC-estimators, as well as other rolling intervals estimators that depend on approximations such as the one in (3.2).

Theorem 3.1.

Proof.

See Appendix E. ∎

Let the error term in the approximation in (3.2) be

| (3.3) |

Notice that is interpolated into a continuous time martingale. The errors are only defined at discrete times, but the interpolation error is asymptotically negligible, and consequently we only need to prove the central limit theorem for the interpolated process, which will be done by applying the general central limit theorem, Theorem B.1, that is contained in Appendix B.

For the notion of an -conditional Gaussian martingale, see Jacod and Shiryaev (2003, Definition II.7.4, p. 129), or Jacod (1997, p. 233). Define

We write for the compensator of the jump process associated with a sequence (in ) of semimartingale process (see Jacod and Shiryaev (2003, Ch. II.1)). We can now state the main result of the paper.

Theorem 3.2.

(CLT for triangular array rolling quadratic variations). Suppose that Conditions 3–6 in Appendix A hold; that , , and are locally continuous in mean square; and that for all , the Lindeberg conditon

| (3.4) |

as is satisfied for both processes. Set

and assume that there is a -measurable process for which

Then converges stably in law to an -conditional Gaussian martingale with quadratic variation

Proof.

See Appendix F. ∎

The notation “” means that we sum over two terms, the one given and the corresponding one where, in , and have changed place. As an example, . The meaning of the notation will be clear from the context. The notion of being locally continuous in mean square is defined in Definition A.3 in Appendix 3. Before we proceed to Section 4, and the application that motivated the present study, we showcase the applicability of Theorem 3.2 by considering the problem of leverage effect estimation.

Example 3.3.

(Leverage effect estimation). Estimators of the leverage effect have been studied previously by Wang and Mykland (2014), Kalnina and Xiu (2017), Aït-Sahalia et al. (2017), to mention some. In this example we introduce a rolling intervals estimator of the leverage effect, and show how Theorem 3.2 can be used to derive the limit distribution of this estimator. We limit ourselves to the following simple model. Assume that the process is observed at the discrete and equidistant times , and that there is no microstructure noise; a one dimensional Wiener process, and is a locally bounded Itô process which may or may not be correlated with . The leverage effect is the spot process . A natural estimator of is the realised volatility (see the references in the Introduction),

and define via . It can then be shown that converges stably in law to a normal distribution with (random) variance (Mykland and Zhang, 2012, Corollary 2.30, p. 154), hence satisfies Condition 1. In analogy with (2.1), consider

| (3.5) |

where, due to the equidistant sampling times, we take . It then follows from Lemma 2.5 that

To sketch the application of the central limit theorem of this paper, note that we may write . Let be as defined in (2.3), and introduce

| (3.6) |

for . Let , and define the two continuous time martingales

and

Then is asymptotically equivalent to . The predictable quadratic variation of is

Provided that the processes involved satisfy the assumptions of Theorem 3.2, we see how the development so far leads to a central limit theorem for the leverage effect estimator of (3.5). In particular, converges stably in law to a Gaussian martingale with (random) asymptotic variance of the form . How this leverage effect estimator generalises to more complicated data structures, i.e. non-equidistant sampling times, microstructure noise, and edge effects, is a topic we plan to explore in a subsequent paper.

3.2. Uncertainty of the TSQC

To compute the uncertainty associated with the TSQC estimator we use the observed asymptotic variance of Mykland and Zhang (2017a), which allows us to circumvent the derivation of an explicit expression for the asymptotic variance of the TSQC estimator. The applicability of the observed asymptotic variance is contingent on the sequences of semimartingales in question satisfying Condition 1 in Section 2.2, or the weaker Condition 5 in Mykland and Zhang (2017b, p. 7). According to this latter condition the sequence of error martingales associated with the estimator whose uncertainty one wants to compute needs to be tight and P-UT. Consider

| (3.7) |

This is the sequence for which we are going to use the observed asymptotic variance to compute its uncertainty. For and , define the interpolated processes

for general semimartingales and , and families of functions and belonging to the classes and , respectively (see Definition A.2). Define also . Now, let the functions and be as defined in (2.3) and (3.6), respectively. Writing , and imposing the assumptions of Theorem 2.4, we can write

| (3.8) |

From this expression we see that when and is of order , then all four terms in this sum will contribute the asymptotic variance of the sequence in (3.7).

Corollary 3.4.

Proof.

Since and are of the same order, it follows from Theorem 3.2 that all the error martingales for in (3.8) are tight and P-UT. Since is of the same order as , the factors outside the last three terms in (3.8) are either or will tend to one. By assumption, the quadratic variations of the eight have continuous limits (or tend to zero). Combined with the Lindeberg-condition of Theorem 3.2 this entails that the are -tight (see the proof of Theorem B). Sums of -tight sequences are -tight (Jacod and Shiryaev, 2003, Corollary VI.3.33, p. 353), and sums of sequences that are P-UT are P-UT (Jacod and Shiryaev, 2003, VI.6.4, p. 377). ∎

Remark 3.5.

Inspection of the proof of Theorem 3.2 reveals that it is fully possible to derive a central limit theorem for the TSQC-estimator. The key to such a proof is to show that quadratic covariations of the form (assuming that we are dealing with martingales)

converge in probability to a continuous limit when , and . That such convergence in probability occurs under the assumptions of Theorem 3.2 can be shown by the same techniques used to prove said theorem, albeit at the cost of a somewhat heavier notational burden. For the present purposes, all we want is to show that the observed asymptotic variance can be applied to the TSQC-estimator, and for that tightness and P-UT is sufficient.

4. Volatility and intensity

In this section we turn to the application that motivated the current paper, namely the estimation of the quadratic covariation between the volatility process of a continuous time semimartingale, and the intensity process of the observation times. When estimating parameters associated with a continuous time process that is only observed at discrete times, simplifying assumptions are often imposed on the relation between the observation times and the underlying process. The observation times are typically either taken as fixed and equidistant, or they are governed by a stochastic process postulated to be independent of the observable process (see e.g., Aït-Sahalia and Jacod (2014, Ch. 9) for a discussion). We refer to both cases as ‘exogenous times’. In many settings the assumption of exogenous times is violated, the case of high-frequency financial data being, at least in some cases, a pertinent example. Decisions to buy or sell a given security may, in part, be determined by features of that security, and since it is only at the times at which transactions are conducted that we get a glimpse of the continuous processes ticking in the background (modulo microstructure noise), one would expect that the observation times may be correlated with transaction-igniting features of the underlying process.

In recent years, much progress has been made when the assumption of exogenous times is relaxed. In Li et al. (2013, 2014) the realised volatility estimator is studied in the presence of endogenous observation times, and it is shown that a ‘bias’ term appears in the limiting distribution of this estimator. This ‘bias’ term is of the same order of magnitude as the process tending (stably) to a normal limit, and is thus not a bias term in the traditional sense. The reasons for caring about it have to do with efficiency considerations, and not with the estimation being off-the-target in an expected value sense. Jacod et al. (2019) construct an estimator of the integrated volatility in the presence of microstructure noise, jumps, and endogenous times. Other papers have dealt with consistency and central limit theorems under irregular and random times (Renault and Werker, 2011; Hayashi et al., 2011; Fukasawa and Rosenbaum, 2012; Potiron and Mykland, 2017). Common for all the above papers is that the endogeneity of the observation times comes about because the times depend on the efficient price process itself, as opposed to latent spot parameter processes governing the evolution of the efficient price process. The tools developed in Section 2 allow us to statistically study situations where the observation times might depend on underlying non-observable features of the efficient price process, such as its spot-volatility process, the associated volatility-of-volatility, the leverage effect, and so on. To assess the direction and magnitude of such correlations, we can use the TSQC-estimator of (2.7), and also a correlation estimator based on the TSQC. In this section we first present some theory specific to the volatility-intensity covariance estimation, then, in Section 4.2 we perform a simulation study to assess the finite sample behaviour of our estimators, while Section 4.3 contains an empirical study of the Apple stock over trading days in January .

4.1. A model for volatility-intensity covariance estimation

For a given frequency of observations, indexed by , the succesive observations occur at times , where is a sequence of finite stopping times. Define the sequence of counting processes . We are going to assume (in Condition 2) that, for observation frequency , the inter-observational lags are of the same order of magnitude as , and moreover, that has a possibly random probability limit when goes to infinity (see Li et al. (2014) and Jacod et al. (2017, 2019) for similar constructions). Based on the observations of , we form an estimator of , where the spot parameter process is itself assumed to be a semimartingale, and assume that is consistent for . In the following we think of as the spot-volatility process , and as the integrated volatility . The counting process can be decomposed as , in terms of a martingale and an increasing and predictable process . We assume that the latter process is absolutely continuous, so that , and that , called the intensity process, is itself a semimartingale. The process we seek to estimate is then over one or consecutive observation windows.

Since is followed over the finite interval , where is fixed, our arguments are based on asymptotics as the observation frequency gets higher, that is , so-called infill asymptotics. To let the number of observations tend to infinity, and at the same time get a finite expression for the limiting intensity of the observation times, we impose the following condition.

Condition 2.

There is a non-negative semimartingale such that , for all .

One may think of as proportional to the expected distance between two observation times, or as being proportional to the expected number of observations per period. The point is that Condition 2 allows us to develop asymptotic theory in terms of for the estimators we construct. This construction is similar to that previously employed by Li et al. (2013); and by Jacod et al. (2019, Assumption (O-, ), p. 82).

Suppose that the estimator satisfies the decomposition in (2.5), and that its error process martingale obeys Condition 1. We return to the assumptions on the edge effects in due time. Define . The counting process simply counts the transactions and is hence observable, whereas is a non-observable abstraction introduced so that the asymptotic theory developed in the two preceding sections generalises to volatility-intensity estimation. This means that is a rescaling of an estimator. For the (finite sample) empirical applications of our estimator, the index will turn out to be immaterial.

Remark 4.1.

We emphasize that does not need to be observed for the developments in this section to be valid. We need to exist in the sense of Condition 2, but otherwise is a notational convenience that permits us to state results more simply, and is in this sense always only a scaling. For example, can be restated as , where .

Notice that there are no edge effects associated with , so (2.5) becomes , where is a martingale sequence. Moreover, as ,

| (4.1) |

by Condition 2. The convergence in (4.1) combined with the fact that is increasing and continuous, yield

where is a Wiener process defined on an extension of the original probability space (see Theorem B.1 in Appendix B). Set , and we have the first part of Condition 1. For Theorem 2.4 to be applicable, the sequence of martingales must also be P-UT.

Lemma 4.2.

Assume Condition 2. Then is P-UT.

Proof.

In the absence of edge effects on the part of , can be decomposed as (cf. the decomposition in (D.1) of Appendix D),

| (4.2) |

by the Cauchy–Schwarz inequality, where

and .

Corollary 4.3.

Proof.

We have that , which via (4.2) shows how differing restrictions on the edge effects associated with the integrated volatility estimator give differing conclusions about (see the discussion in Appendix D). If we assume that the edge effects associated with are , which is not unrealistic when working with two-scales estimators and pre-averaged observations (see Zhang et al. (2005) and Mykland et al. (2019)), then the conclusion of Corollary 4.3 is

Since , Corollary 2.6 entails that is consistent. With the definitions in Remark 4.1, is also consistent. Also, consider the process , given by

Notice that for all due to the Kunita–Watanabe inequality (Protter, 2004, Theorem II.25, p. 69). For each we see that by the continuous mapping theorem, which means that the coefficient can be consistently estimated using the estimators and , the latter simply defined as . In particular, define

and note that , from which consistency of this estimator follows. When and have different convergence rates, as in Lemma 2.5, another consistent estimator for is . Since the speed at which converges is governed by the inferior convergence rate, there is, however, not that much to be gained in using this latter estimator, potentially apart from some less fine tuning of the and parameters. These two estimators of have a similar flavour to them, but are different from, the first-order correlation estimator introduced in Barndorff-Nielsen and Shephard (2004, Sections 3.1-3.2, pp. 899–903).

In Section 4.2 we study the performance of on simulated data, and investigate its sensitivity to the choice of tuning parameters and . Before proceeding to the simulations and the empirical application, we provide an example of a simple model satisfying the above assumptions.

Example 4.4.

(A volatility-intensity model). Suppose that we observe samples from the process , where the spot volatility and the intensity follow CIR-processes (Cox et al., 1985) given by,

| (4.3) |

where and are Wiener processes such that , and is a Wiener process that may or may not be correlated with , thus allowing for a leverage effect, or . The parameters and as well as and are positive and we assume that the Feller condition (Feller, 1951) holds for both the volatility and the intensity, that is , and for all . In this model, the dependency between and is introduced by the correlation between and . Suppose that , and that as . Then, for each , we have that , and that

| (4.4) |

as . See Appendix C for details.

In the next section the model of Example 4.4 is used as the basis for a simulation study.

4.2. Simulations

The data were simulated from the model presented in Example 4.4. The initial observations for the volatility and intensity processes were sampled from a Gamma distribution with parameters and a Gamma distribution with parameters distribution, respectively. The parameter values were (volatility model), , with . The microstructure noise was taken as additive on the efficient price and independent of the three underlying Brownian motions, that is, we observe

where the were independent mean zero normals with standard deviation , independent of and . These three process were all Brownian motions, was independent of and , while and were jointly Brownian with correlation . The data were simulated to mimic features of the actual Apple stock data that we analyse in Section 4.3. With one trading day ( hours) the intensity function is such that we have about observations of per day. This is a common number of daily trades of a liquid stock such as that of Apple. As our estimator of the integrated volatility we used the Two-Scales Realised Volatility (TSRV) of Zhang et al. (2005), while was used to estimate the cumulative intensity of the observation times. The TSRV we used is given by

| (4.5) |

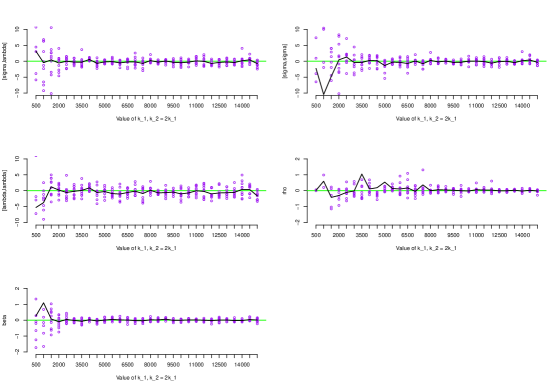

where are pre-averaged observations, and , where are the number of ‘observations’ of , and is a tuning parameter chosen by the user (Mykland et al. (2019, Eq. (17), p. 106) for this construction). Recall that the rescaling by is an abstraction that does not affect consistency, cf. Remark 4.1. For each simulation we estimated the quadratic covariation , the coefficient and , the latter defined as . All the quadratic (co-)variations were estimated using the TSQC-estimator. Note, however, that the quadratic covariation could have been estimated directly using , this is because the TSRV of (4.5) has convergence rate to (depending on the degree of preaveraging), while converges at the rate (see Zhang et al. (2005, Theorem 4, p. 1402) and Lemma 2.5). In Figure 1 we have plotted the deviance of the estimates from the (random) estimands for various values of , with throughout.

4.3. An empirical application

In the empirical study we analyse features of the Apple stock as traded over a period of trading days in January 2018. All transactions registered in the U.S. National Market System conducted between 9:45 am - 3:45 pm Eastern Standard Time are included. The reason for choosing this window is to avoid abnormal trading activity during the opening and closing of the New York Stock Exchange, and to avoid those pre- and post-market hours during which the trading frequency is low (Wang and Mykland, 2014, p. 205). The Apple stock data is recorded down to the nanosecond ( seconds), and for the period under study the mean number of transactions over a trading day during the time window we use was , which is about nine transactions per second. After some data cleaning, the data was pre-averaged and the TSRV estimator of Zhang et al. (2005) was used to estimate the integrated volatility. The cumulative intensity of the observation times was estimated by , where counts the number of transactions conducted from 9:45 am to 9:45 am plus . Besides making the plots more aesthetically pleasing, the number plays no role.

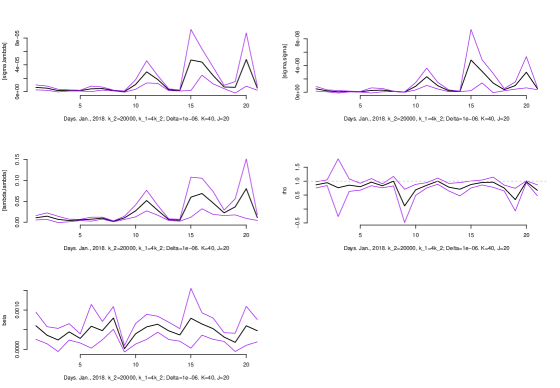

We used the TSQC-estimator for daily estimation of the volatility-intensity covariance matrix and the two transformations thereof, and . The estimates of are time-varying and lie between and for most of the days under study, indicating that the two processes are indeed correlated. To estimate the (pointwise) confidence bands of our TSQC-estimators we employed the Observed asymptotic variance of Mykland and Zhang (2017a). This estimator of the asymptotic variance is akin to the observed information in likelihood theory, and by using it, we avoid the difficulty of finding an explicit expression for the asymptotic variance. The applicability of the observed asymptotic variance is ensured by Corollary 3.4.

4.4. Using the volatility-intensity relationship to gain efficiency

We have seen above that

where, in the latter equation, there is no normalization by , hence the two equations are equivalent, and, once again, one can calculate as if were known. This is an ANOVA decomposition along the lines of Mykland and Zhang (2006), but in this case, and are unobserved. The process is estimated as above in this paper. The quantities and can be estimated as spot (instantaneous) quantities, as in Mykland and Zhang (2008).

When microstructure is present in prices, but not in the observation times (as is the usual understanding), then has a faster rate of convergence than , and hence this is also true for and . The construction in Mykland and Zhang (2008) uses , and similarly for , where and are chosen to be (at least rate-) optimal, by the use of a variance-variance tradeoff. This leads to the rates for and to be and , respectively (when a rate optimal estimator of volatility is used, such as the S-TSRV which is used in this paper, or the multi-scale estimator of Zhang (2006), see also Bibinger and Mykland (2016) for the multivariate case and the connection to realised kernels, as well as the references therein. Finally, Lemma 2.5 and Theorem 3.1 provide for to have a rate of convergence of , thus

| (4.6) |

If, as in our data, the residual (or ) is small, the question naturally occurs whether to prefer , with a low rate of convergence, or with a much better rate of convergence, but with a bias of (or ). The conventional asymptotics-based answer to this question is that a slow convergence rate of is preferable to a much better convergence rate to a limit with an bias. In other words, pick , even if is small.

This answer is uncomfortable, and has already caused some degree of argument in connection with volatility estimation, where there is an argument over whether intra-day estimators are always preferable, or whether to draw on longer time periods. Assumptions of stationarity will not help, and longer time periods are usually introduced by drawing on more highly specified models, such as ARCH and GARCH type models, going back to the seminal papers of Engle (1982) and Bollerslev (1986). There is a huge literature in this area, see, for example the survey by Engle (1995).

Another path is to express “ is small” by a triangular array asymptotic regime whereby as . Triangular array asymptotic regimes are often used close to a singularity, see, e.g., Chan and Wei (1987) and Phillips (1987) in the context of time series close to the unit root. In this context, it is often referred to as ‘local to unity asymptotics’. Under this regime, one can augment the estimate of by adding an estimate of , giving rise to an estimate of the form

| (4.7) |

The tuning parameter should then be chosen to minimise the (random) mean squared error in , and in any case, , thus improving the rate of convergence. A proper analysis of (4.7) would require an assessment of the mean squared error of , which would presumably involve the estimation of , which brings us back to the ANOVA problem of Mykland and Zhang (2006), but now with latent variables everywhere. This is beyond the scope of the present paper.

If a reasonable solution can be found, similar methods may apply to a number of estimators that involve the estimation of spot volatility, such as leverage effect (Example 3.3), volatility-of-volatility (in this paper, and also Vetter (2015) and Mykland and Zhang (2017a)), as well as regression, and ANOVA (Mykland and Zhang (2009, Section 4.2, pp. 1424–1426), Zhang (2012, Section 4, pp. 268–273), Reiß et al. (2015), and the references therein).

5. Conclusion

This paper introduces a consistent estimator of the quadratic covariation between two non-observable spot-process semimartingales, derives the convergence rates of this estimator, and presents a central limit theorem for such estimators. The main theoretical contribution of the paper is this central limit theorem, a theorem that is applicable to a wide range of estimators based on triangular arrays of rolling quadratic covariations and second differencing of estimators of integrated spot processes.

As recognised in much recent literature on estimation in high-frequency data, the assumption of exogenous observation times is often untenable, and one typically allows for dependency between the observation times and the price process. In this paper we have considered possible dependencies between the observation times and non-observable spot-processes associated with the price process, of which the spot volatility is a prime example. A simulation study shows that the estimators perform well with decent amounts of data. The empirical study of the Apple stock indicates that the observation times and the volatility process of this stock are positively correlated.

Appendix A Notation and conditions

We start by recalling some definitions from Mykland and Zhang (2017a).

Definition A.1.

(Orders in Probability) For a sequence of semimartingales, we say that if the sequence is tight, with respect to convergence in law relative to the Skorokhod topology on (Jacod and Shiryaev, 2003, Theorem VI.3.21, p. 350). For scalar random quantities, and are defined as usual, see, e.g., (Pollard, 1984, Appendix A).

Condition 3.

Let and be sequences (in ) of semimartingales. Each of these sequences are (separately) assumed to be .

Definition A.2.

(Notation). The symbol will refer to a collection of nonrandom functions càdlàg on , with , and , satisfying

Similarly, will refer to a collection with the same size and properties.

Given and , set

For a random variable the norm is . If and are defined on and for all , for a fixed constant , we write .

Condition 4.

(Conditions for Rate-of-Convergence Statements and CLT) The sequence of semimartingales , possibly defined on a sequence of filtrations , is said to satisfy this condition if it can be written as , where for each , is a square integrable martingale with predictable quadratic variation that is absolutely continuous, and and are locally bounded uniformly in .

A single semimartingale is said to satisfy Condition 4 if the above is satisfied for the constant sequence . Note also that Condition 4 implies that each is an Itô-semimartingale (see Jacod and Protter (2012, Eq. (4.4.1), p. 114)).

Definition A.3.

A processes is locally continuous in mean square if

provided , where is a stopping time such that as .

For the proof of Theorem 3.2 contained in Appendix F we need to be more specific about the construction of the probability space on which the sequence of processes , , as well as potentially stochastic spot-processes related to these two, are defined. Since the result of Theorem 3.2 is a stable convergence result, we need everything (except, possibly, microstructure noise) to be defined on the same probability space. Let , with be a filtered probability space on which the processes are defined, and for each let be a filtration on .

Condition 5.

A filtration on is said to satisfy the current condition if it is generated by where is a Poisson random measure with deterministic compensator that is absolutely continuous as a function of time, and are independent one-dimensional Wiener processes.

Condition 6.

For any finite family of -adapted bounded martingales there is a sequence of -adapted martingales such that .

By Cohen and Elliott (2015, Theorem 14.5.7, p. 360) Condition 5 is sufficient to represent the local martingales encountered in Theorem 3.2. Importantly, any martingale (resp. ) adapted to (resp. ) has a predictable quadratic variation process (resp. ) that is absolutely continuous with respect to Lebesgue measure.

Appendix B A stable central limit theorem for càdlàg martingales

We find the following theorem and its corollaries to be convenient in applications. It is a generalisation of Theorem 2.28 in Mykland and Zhang (2012, p. 152) (originally stated in Zhang (2001)), and is a special case of a theorem found in Jacod and Shiryaev (2003, ch. IV.7), but with a different and perhaps more accessible statement and proof. The proof of the present theorem employs techniques from the proofs of both these earlier theorems. The formulation of our theorem also gives rise to Corollary B.2. This corollary provides alternative Lindeberg type conditions that are easier to check.

We have a filtered probability space , where . For each , we have a filtration and a -adapted square integrable martingale . This is the martingale that we wish to show that converges stably in distribution.

We assume that is countably generated, that is, for a countable sequence in . There is then a sequence of random variables that is dense in (Kolmogorov and Fomin, 1970, Theorem 3, p. 382). Set , which is then a bounded martingale on . Here are two results that can be found in Jacod (1979, pp. 114–115), and also stated in Jacod (1997).

-

(a)

Every bounded martingale is the limit in , uniformly in time, of a sequence of stochastic integrals with respect to a finite number of .

-

(b)

If is the smallest filtration with respect to which is adapted, then up to -null sets.

The countably many -adapted bounded martingales play a role similar to the Wiener processes appearing in Condition 2.26 in Mykland and Zhang (2012, p. 151).

Theorem B.1.

Assume Condition 6. Let be a sequence of locally square integrable martingales on , adapted to for each . Suppose that there is an -adapted process such that

-

(i)

for all ;

-

(ii)

for all ;

-

(iii)

for all and all bounded martingales on .

Then converges stably in distribution to , where is a Wiener process defined on an extension of the original probability space.

Proof.

Convergence in probability implies convergence in distribution, so (i) implies that in the sense of finite dimensional distributions. Combining this with the facts that is a non-decreasing process and has a non-decreasing and continuous limit, Theorem VI.3.37 in Jacod and Shiryaev (2003, p. 354) yields process convergence of to . The sample paths are continuous, so is -tight (Jacod and Shiryaev, 2003, Def. 3.25, p. 351), implying that is tight (Jacod and Shiryaev, 2003, Theorem VI.4.12, p. 358). Condition (ii) implies that , combined with the tightness of this implies that is -tight (Jacod and Shiryaev, 2003, Lemma VI.4.22, p. 360, and Theorem VI.3.26(iii), p. 351). Recall that , and denote . By Condition 6 there is a sequence , such that . Since is -tight and is tight by Condition 6, Corollary 3.33 in Jacod and Shiryaev (2003, p. 353) gives that is tight. By Prokhorov’s theorem (see e.g. van der Vaart (1998, Theorem 2.5(ii), p. 8)), this tightness entails that we can for any subsequence find a further subsequence such that

| (B.1) |

For each , write

| (B.2) |

in terms of the measure associated with the jumps of , and its compensator , and where is a local martingale with bounded jumps. For the decomposition in (B.2), see e.g., Jacod and Protter (2012, Eq. (2.1.10), p. 29) and use that , their , is a martingale; or see Proposition II.2.29 in Jacod and Shiryaev (2003, p. 82), and the fact that their in the martingale case. Since is the predictable compensator of , it follows from Lenglart’s inequality (Jacod and Shiryaev, 2003, Lemma 3.30(a), p. 35) and Condition (ii) that for all , thus

| (B.3) |

But (B.3) must also hold for any subsequence, so (B.1) and the Cramér–Slutsky rules entail that converges in law to . Since has bounded jumps , Theorem IX.1.17 in Jacod and Shiryaev (2003, p. 526) gives that is a local martingale with respect to the filtration generated by (hence the importance of fact (b), and where we use that Theorem IX.1.17 extends from the finite to the countable case, see Jacod and Shiryaev (2003, p. 586)).

We now want to show that is P-UT, because that will ensure joint convergence of . Let , where as well as the elementary stochastic integral are as defined in Jacod and Shiryaev (2003, p. 377). Then . So by Lenglart’s inequality Jacod and Shiryaev (2003, Lemma I.3.30(a), p. 35), for every , and for any , and for any ,

But since is tight, this shows that is P-UT. Since is P-UT, Theorem VI.6.26 in Jacod and Shiryaev (2003, p. 384) gives that converges in law to ; from continuity of we get that (Jacod and Shiryaev, 2003, Theorem I.4.52, p. 55); and by Condition (i), .

Assume without loss of generality that (see Mykland and Zhang (2012, p. 152)), and set . Then and by Condition (iii) for any bounded martingale . Lévy’s theorem (Jacod and Shiryaev, 2003, p. 102) then gives that is a Wiener process. Since is independent of by Condition (iii), we can realise on the extension , , , , where is the space of all continuous functions on , and for fixed, is the Wiener measure. Then is a Wiener process for each , and is a continuous process on the extension, orthogonal to all bounded martingales on , and is -measurable by Condition (i). Thus, is an -conditional Gaussian martingale on the extension. This proves the theorem for a subsequence , but since the subsequence was arbitrary, the claim of the theorem follows (see corollary on p. 337 in Billingsley (1995), or Billingsley (1999, Theorem 2.6, p. 20)). ∎

Corollary B.2.

Proof.

For (ii)′: By Proposition II.1.28 (p. 72) and Theorem I.3.17 (p. 32) in Jacod and Shiryaev (2003), we have that

which proves that (ii)′(ii). For (ii)′′: We must show that (ii)′′ implies (B.3). Using the the triangle inequality and the fact that is a (non-negative) measure

| (B.4) |

Since is tight, is P-UT, and we have that for all (Jacod and Shiryaev, 2003, Theorem VI.6.16, p. 380), so the first term on the right in (B.4) tends to zero in probability by the Cramér–Slutsky rules. For the second term on the right, since is the predicable compensator of the adapted process , Lenglart’s inequality (Jacod and Shiryaev, 2003, Lemma I.3.30(b), p. 35) gives that for all ,

As we saw above . For all , by Hölder’s inequality

as . Since were arbitrary, converges in probability to zero for all . ∎

Remark B.3.

In the proof of Theorem B.1 we use that if is a sequence of local square integrable martingales, that for all as , and that is continuous, then is P-UT. This is a useful implication that, perhaps because it is deemed obvious, is not spelled out explicitly in Jacod and Shiryaev (2003, ch. VI.6). Using this implication, an immediate corollary to Proposition 6 in Mykland and Zhang (2017b, p. 12) is: If converges in law to , and , with being continuous, then converges -stably in law, where . For several other results associated with the P-UT property, see Mykland and Zhang (2017b, Appendix D).

Appendix C Proof of the claims in Example 4.4

Assume that , and that as . Then, for each ,

| (C.1) |

as . We now prove (C.1): The expectation of the intensity is , and

| (C.2) |

Note that

and from (C.2), , from which it follows that for each , . By Chebyshev’s inequality we get that for each the sequence of random variables are uniformly integrable (see Eq. (25.13) in Billingsley (1995, p. 338)). Moreover, from the above we see that for all and , and the right hand side is trivially integrable on . Hence, the sequence of stochastic processes satisfies the conditions of Andersen et al. (1993, Proposition II.5.2, p. 85), and the first part of (C.1) follows. For the second part we have that

which by three applications of Hölder’s inequality and the Itô isometry is seen to be bounded by a constant, hence , and uniform integrability of the random variables follows. Since for all and , and a constant is integrable on , so the second part of (C.1) follows by the same argument as above.

Appendix D Notes on Theorem 2.4

The proof follows with trivial adjustments from Mykland and Zhang (2017a, Theorem 3, p. 208). Note that the convergence rates change due to our Theorem 3.1. Recall the setup in (2.5), that is and . Mykland and Zhang (2017a, Theorem 3, p. 208) and the convergence rates from Theorem 3.1 give

| (D.1) |

where and

while is given by

We now consider two different sets of restrictions on the edge effect. All other cases can be deduced from (D.1). For all on a given grid,

Under Case (1) we have that (D.1) is

While under Case (2) we find that (D.1) is

It thus appears that the more stringent conditions on the edge effects in Case (2) are needed for the convergence rates of Theorem 3.1 to ‘enter’ Theorem 2.4. Do note, however, that this may be an artefact of the Cauchy–Schwarz inequality used in deriving (D.1).

Appendix E Proof of Theorem 3.1

Recall that

| (E.1) |

It is enough to show the result when the sequences and are local square-integrable martingales. Let

and set . Let the stopping time and the positive constants and be such that, for , and . In particular, , by the Kunita–Watanabe inequality (see e.g., (Protter, 2004, Theorem II.25, p. 69)). By Itô’s lemma we have that

From which

| (E.2) |

Changing the order of summation and integration we have that,

and similarly for the second term on the right in (E.2). For the third and fourth terms on the right in (E.2) we use that for , and Hölder’s inequality,

and similarly for the fourth term. Now, all the action takes place in expressions of the form

| (E.3) |

Since and for all , , and , we have that

| (E.4) |

For , define

and notice that

Substituting the bound in (E.4) and the three similar ones into , then

where the proportionality constant left out is . Let

By Condition 4, as . Let and choose and sufficiently large, so that , and let . Then

provided . This shows that is tight, so

By Lenglart’s inequality (Andersen et al., 1993, p. 86), for any and

With the same and the same as above, , from which we conclude that

Appendix F Proof of Theorem 3.2

For this theorem we are assuming that the sequences and are square-integrable local martingales, both equal to zero at time . For , we define

| (F.1) |

and set

so that is the martingale in (3.3). We will verify that the sequence satisfies Conditions (i)–(iii) of Theorem B.1, and the claim will follow.

Recall that by Condition 4 we assume there are processes, say , , and , such that

and that these are locally bounded uniformly in , that is, there is a sequence of stopping times such that for we have finite constants , and such that , , and , and as . Moreover, we assume that , and are locally continuous in mean square, see Definition A.3.

The quadratic variation of is

Here

| (F.2) |

by which we define for . Start by concentrating on , which is given by

| (F.3) |

Write

where the indices on the right hand side are such that , and let be the set of these time points, i.e. . With this notation we have, e.g. that

The time defined in (E.1) is now simply . Attach the number to if it is not already there, and suppose, without loss of generality, that for all , and that . We can then write

| (F.4) |

We now want to show that (F.4) is

| (F.5) |

The key is to show equalities of the type

and that the ‘negligible terms’ are of the appropriate order. Recall that , thus by Itô’s formula

This means that

We now turn to the two last terms on the right hand side of this expression, and look at

| (F.6) |

Consider the two terms on the right in (F.6) separately, starting with the first term. Define the functions

and note that since for all , the functions are Lipschitz with constant , that is,

An application of Itô’s formula yields

Integrating from to ,

Since is deterministic it is predictable, so the right hand side of this expression is a martingale. Then, for ,

Since the martingale increments are uncorrelated, this gives

By Chebyshev’s inequality we have that for any ,

which shows that is as . We now turn to the second term in (F.6). For ,

From this we get that for ,

from which

By Markov’s inequality

By Assumption A.3, i.e. mean square continuity of , we get

This completes the proof of (F.5), and obviously, the same holds for .

We must now show that similar results apply to and . It suffices to look at . In analogy with (F.4), we can write

and we will have to deal with error terms of the form

Define the functions , and note that for all . Then for ,

Analogous to above, this gives that

Looking back at the derivations above, we also see that

By the same localisation techniques used previously, this establishes that (cf. (F.2)),

Hence,

By assumption, there is a -measurable process such that for all as tends to infinity, so this shows that satisfies Condition (i) of Theorem B.1.

We now turn to Condition (ii), that is the Lindeberg condition, of said theorem. To verify that this condition holds, we appeal to Condition (ii)′′ of Corollary B.2. We must verify that the sequence is P-UT, that as , and that for all . We have seen that converges in probability, hence also in distribution, to the continuous and increasing process . By Jacod and Shiryaev (2003, Theorem VI.3.37, p. 354) this yields process convergence of to , which means that in the sense of Definition A.1. To see that is P-UT, let be any predictable process with , and let be the elementary stochastic integral (see Jacod and Shiryaev (2003, p. 377) for both definitions). Now, , so by Lenglart’s inequality, for any ,

and that is P-UT follows from the definition (Jacod and Shiryaev, 2003, Definition VI.6.1, p. 377), because is tight.

The jumps of are

Using (F.1) we see that

| (F.7) |

For any , where , we have that by the Itô isometry,

which show that is -dominated (Jacod and Shiryaev, 2003, Definition I.3.29, p. 35) by the predictable process , and that the latter is . Therefore, by Condition 4,

which shows that both and are as . But for any ,

as by the Lindeberg condition in (3.4), combined with Lenglart’s inequality. But since was arbitrary, , and we conclude that . For the last condition, by Jacod and Shiryaev (2003, Theorem I.4.47(c), p. 52), the triangle inequality, and using that is an increasing process, we have that for any ,

but in Appendix E we saw that . Thus for all , and we conclude that Condition (ii)′′ of Corollary B.2 is satisfied, and therefore also the Lindeberg condition of Theorem B.1.

It remains to check Condition (iii) of Theorem B.1, namely that for each , where is a sequence of bounded martingales. It is enough to check this condition for a sequence of processes that is either a sequence of Wiener processes, or a sequence of Poisson processes (this is a consequence of the representation theorem in Cohen and Elliott (2015, Theorem 14.5.7, p. 360). This means that the the sequence has predictable quadratic variation or for some deterministic function . For simplicity of notation we assume that is a sequence of Wiener processes. By the Kunita–Watanabe inequality, for and ,

Thus, , where

denotes the positive plus the negative part of the function. For a fixed and (here , , etc.)

where for the third inequality we have used Hölder’s inequality. Then, for ,

hence for each , and the third requirement of Theorem B.1 follows from Condition 4.

We have now shown that the martingale sequence converges stably in law to a -conditional Gaussian martingale with variance process . This proves the theorem.

References

- Aït-Sahalia et al. (2017) Aït-Sahalia, Y., J. Fan, R. J. Laeven, C. D. Wang, and X. Yang (2017): “Estimation of the continuous and discontinuous leverage effects,” Journal of the American Statistical Association, 112, 1744–1758.

- Aït-Sahalia and Jacod (2014) Aït-Sahalia, Y. and J. Jacod (2014): High-Frequency Financial Econometrics, Princeton University Press.

- Andersen et al. (1993) Andersen, P. K., Ø. Borgan, R. D. Gill, and N. Keiding (1993): Statistical Models Based on Counting Processes, Berlin: Springer.

- Andersen et al. (2001) Andersen, T. G., T. Bollerslev, F. X. Diebold, and P. Labys (2001): “The Distribution of Realized Exchange Rate Volatility,” Journal of the American Statistical Association, 96, 42–55.

- Barndorff-Nielsen and Shephard (2002) Barndorff-Nielsen, O. E. and N. Shephard (2002): “Econometric Analysis of Realized Volatility and Its Use in Estimating Stochastic Volatility Models,” Journal of the Royal Statistical Society, B, 64, 253–280.

- Barndorff-Nielsen and Shephard (2004) ——— (2004): “Econometric analysis of realized covariation: High frequency based covariance, regression, and correlation in financial economics,” Econometrica, 72, 885–925.

- Bibinger and Mykland (2016) Bibinger, M. and P. A. Mykland (2016): “Inference for Multi-dimensional High-frequency Data with an Application to Conditional Independence Testing,” Scandinavian Journal of Statistics, 43, 1078–1102.

- Billingsley (1995) Billingsley, P. (1995): Probability and Measure. Third Edition, Wiley.

- Billingsley (1999) ——— (1999): Convergence of Probability Measures. Second Edition, Wiley.

- Bollerslev (1986) Bollerslev, T. (1986): “Generalized Autorgeressive Conditional Heteroskedasticity,” Journal of Econometrics, 31, 307–327.

- Chan and Wei (1987) Chan, N. H. and C. Z. Wei (1987): “Asymptotic inference for nearly nonstationary AR(1) processes,” Annals of Statistics, 15, 1050–1063.

- Cohen and Elliott (2015) Cohen, S. N. and R. J. Elliott (2015): Stochastic Calculus and Applications. Second Edition, New York: Birkhäuser, Springer.

- Cox et al. (1985) Cox, J. C., J. E. Ingersoll Jr, and S. A. Ross (1985): “A theory of the term structure of interest rates,” Econometrica, 53, 385–408.

- Engle (1982) Engle, R. F. (1982): “Autogregressive Conditional Heteroskedasticity with Estimates of the Variance of U.K. Inflation,” Econometrica, 50, 987–1008.

- Engle (1995) ——— (1995): ARCH: Selected Readings, New York, NY: Oxford University Press.

- Feller (1951) Feller, W. (1951): “Two singular diffusion problems,” Annals of Mathematics, 54, 173–182.

- Fukasawa and Rosenbaum (2012) Fukasawa, M. and M. Rosenbaum (2012): “Central limit theorems for realized volatility under hitting times of an irregular grid,” Stochastic processes and their applications, 122, 3901–3920.

- Hayashi et al. (2011) Hayashi, T., J. Jacod, and N. Yoshida (2011): “Irregular sampling and central limit theorems for power variations: The continuous case,” Annales de l’Institut Henri Poincaré – Probabilités et Statistiques, 47, 1197–1218.

- Jacod (1979) Jacod, J. (1979): Calcul stochastique et problèmes de martingales, Springer.

- Jacod (1997) ——— (1997): “On continuous conditional Gaussian martingales and stable convergence in law,” in Séminaire de Probabilités XXXI, Springer, vol. 31, 232–246.

- Jacod et al. (2017) Jacod, J., Y. Li, and X. Zheng (2017): “Statistical properties of microstructure noise,” Econometrica, 85, 1133–1174.

- Jacod et al. (2019) ——— (2019): “Estimating the integrated volatility with tick observations,” Journal of Econometrics, 208, 80–100.

- Jacod and Protter (1998) Jacod, J. and P. Protter (1998): “Asymptotic Error Distributions for the Euler Method for Stochastic Differential Equations,” Annals of Probability, 26, 267–307.

- Jacod and Protter (2011) ——— (2011): Discretization of Processes, Springer.

- Jacod and Protter (2012) ——— (2012): Discretization of Processes, New York: Springer.

- Jacod and Shiryaev (2003) Jacod, J. and A. N. Shiryaev (2003): Limit Theorems for Stochastic Processes. Second Edition, Berlin: Springer.

- Kalnina and Xiu (2017) Kalnina, I. and D. Xiu (2017): “Nonparametric estimation of the leverage effect: A trade-off between robustness and efficiency,” Journal of the American Statistical Association, 112, 384–396.

- Kolmogorov and Fomin (1970) Kolmogorov, A. and S. Fomin (1970): Introductory Real Analysis, New York: Dover Publications, Inc.

- Li et al. (2014) Li, Y., P. A. Mykland, E. Renault, L. Zhang, and X. Zheng (2014): “Realized volatility when sampling times are possibly endogenous,” Econometric Theory, 30, 580–605.

- Li et al. (2013) Li, Y., Z. Zhang, and X. Zheng (2013): “Volatility inference in the presence of both endogenous time and microstructure noise,” Stochastic Processes and their Applications, 123, 2696–2727.

- Mykland and Zhang (2006) Mykland, P. A. and L. Zhang (2006): “ANOVA for Diffusions and Itô Processes,” The Annals of Statistics, 34, 1931–1963.

- Mykland and Zhang (2008) ——— (2008): “Inference for Volatility-Type Objects and Implications for Hedging,” Statistics and its Interface, 1, 255–278.

- Mykland and Zhang (2009) ——— (2009): “Inference for continuous semimartingales observed at high frequency,” Econometrica, 77, 1403–1445.

- Mykland and Zhang (2012) ——— (2012): “The Econometrics of High Frequency Data,” in Statistical Methods for Stochastic Differential Equations, ed. by M. Kessler, A. Lindner, and M. Sørensen, CRC Press, 109–190.

- Mykland and Zhang (2017a) ——— (2017a): “Assessment of uncertainty in high frequency data: the observed asymptotic variance,” Econometrica, 85, 197–231.

- Mykland and Zhang (2017b) ——— (2017b): “Supplement to ‘Assessment of uncertainty in high frequency data: the observed asymptotic variance’,” Econometrica Supplementary Material, 85, available at: https://onlinelibrary.wiley.com/doi/abs/10.3982/ECTA12501.

- Mykland et al. (2019) Mykland, P. A., L. Zhang, and D. Chen (2019): “The algebra of two scales estimation, and the S-TSRV: High frequency estimation that is robust to sampling times,” Journal of Econometrics, 208, 101–119.

- Phillips (1987) Phillips, P. C. (1987): “Towards a unified asymptotic theory for autoregression,” Biometrika, 74, 535–547.

- Pollard (1984) Pollard, D. (1984): Convergence of Stochastic Processes, Berlin: Springer.

- Potiron and Mykland (2017) Potiron, Y. and P. A. Mykland (2017): “Estimation of integrated quadratic covariation with endogenous sampling times,” Journal of Econometrics, 197, 20–41.

- Protter (2004) Protter, P. (2004): Stochastic Integration and Stochastic Differential Equations (Second Edition), New York: Springer.

- Reiß et al. (2015) Reiß, M., V. Todorov, and G. Tauchen (2015): “Nonparametric test for a constant beta between Itô semi-martingales based on high-frequency data,” Stochastic Processes and their Applications, 125, 2955–2988.

- Renault and Werker (2011) Renault, E. and B. J. Werker (2011): “Causality effects in return volatility measures with random times,” Journal of Econometrics, 160, 272–279.

- van der Vaart (1998) van der Vaart, A. W. (1998): Asymptotic Statistics, Cambridge: Cambridge University Press.

- Vetter (2015) Vetter, M. (2015): “Estimation of Integrated Volatility of Volatility with Applications to Goodness-of-fit Testing,” Bernoulli, 21, 2393–2418.

- Wang and Mykland (2014) Wang, C. D. and P. A. Mykland (2014): “The estimation of leverage effect with high-frequency data,” Journal of the American Statistical Association, 109, 197–215.

- Zhang (2001) Zhang, L. (2001): “From martingales to ANOVA: Implied and realized volatility,” Ph.D. thesis, Department of Statistics, The University of Chicago.

- Zhang (2006) ——— (2006): “Efficient Estimation of Stochastic Volatility Using Noisy Observations: A Multi-Scale Approach,” Bernoulli, 12, 1019–1043.

- Zhang (2012) ——— (2012): “Implied and realized volatility: Empirical model selection,” Annals of Finance, 8, 259–275.

- Zhang et al. (2005) Zhang, L., P. A. Mykland, and Y. Aït-Sahalia (2005): “A tale of two time scales: Determining integrated volatility with noisy high-frequency data,” Journal of the American Statistical Association, 100, 1394–1411.