Discrete Choice under Risk with Limited Consideration††thanks: We are grateful to Liran Einav, three anonymous referees, Abi Adams, Jose Apesteguia, Miguel Ballester, Arthur Lewbel, Chuck Manski, and Jack Porter for useful comments and constructive criticism. For comments and suggestions we thank the participants to the 2017 Barcelona GSE Summer Forum on Stochastic Choice, the 2018 Cornell Conference “Identification and Inference in Limited Attention Models”, the 2018 Penn State-Cornell Conference on Econometrics and IO, the 2018 GNYMA Conference, the 2019 ASSA meetings, the IFS 2019 “Consumer Behaviour: New Models, New Methods” Conference, and to seminars at Stanford, Berkeley, UCL, Wisconsin, Bocconi, and Duke. Part of this research was carried out while Barseghyan and Molinari were on sabbatical leave at the Department of Economics at Duke University, whose hospitality is gratefully acknowledged. We gratefully acknowledge support from National Science Foundation grant SES-1824448 and from the Institute for Social Sciences at Cornell University.

This paper is concerned with learning decision makers’

preferences using data on observed choices from a finite set of risky alternatives. We propose a discrete choice model with unobserved heterogeneity in consideration sets and

in standard risk aversion. We obtain sufficient conditions for the model’s semi-nonparametric point identification,

including in cases where consideration depends on preferences and on some of the exogenous variables. Our method yields an estimator that is easy to compute and is applicable in markets with large choice sets. We illustrate its properties using a dataset on property insurance purchases.

Keywords: discrete choice, limited consideration, semi-nonparametric identification

1 Introduction

This paper is concerned with learning decision makers’ (DMs) preferences using data on observed choices from a finite set of risky alternatives with monetary outcomes. The prevailing empirical approach to study this problem merges expected utility theory (EUT) models with econometric methods for discrete choice analysis. Standard EUT assumes that the DM evaluates all available alternatives and chooses the one yielding the highest expected utility. The DM’s risk aversion is determined by the concavity of her Bernoulli utility function. The set of all alternatives – the choice set – is assumed to be observable by the researcher.

We depart from this standard approach by proposing a discrete choice model with unobserved heterogeneity in preferences and unobserved heterogeneity in consideration sets. Specifically, preferences satisfy the classic Single Crossing Property (SCP) of \@BBOPcitet\@BAP\@BBNMirrlees (1971)\@BBCP and \@BBOPcitet\@BAP\@BBNSpence (1974)\@BBCP, central to important studies of decision making under risk.111E.g., \@BBOPcite\@BAP\@BBNApesteguia et al. (2017); Chiappori et al. (2019)\@BBCP. While our focus is on decision making under risk, the SCP property is satisfied in many contexts, ranging from single agent models with goods that can be unambiguously ordered based on quality, to multiple agents models (e.g., \@BBOPcite\@BAP\@BBNAthey (2001)\@BBCP). That is, the preference order of any two alternatives switches only at one value of the preference parameter.222The EUT framework satisfies the SCP, which requires that if a DM with a certain degree of risk aversion prefers a safer lottery to a riskier one, then all DMs with higher risk aversion also prefer the safer lottery. Given her unobserved preference parameter, each DM evaluates only the alternatives in her unobserved consideration set, which is a subset of the choice set.

Our first contribution is to provide a general framework for point identification of these models. Our analysis relies on two types of observed data variation. In the first case, we assume that the data include a single (common) excluded regressor affecting the utility of each alternative. In the second case, we assume that each alternative has its own excluded regressor. In both cases, the excluded regressor(s) is independent of unobserved preference heterogeneity. When the excluded regressor(s) also has large support it becomes a “special regressor” \@BBOPcitep\@BAP\@BBN(Lewbel, 2000, 2014)\@BBCP. For reasons we explain, the case of the single common excluded regressor is the most demanding from an identification standpoint. Nonetheless, under classic conditions for identification of full-consideration discrete choice models \@BBOPcitep\@BAP\@BBN(see, e.g., Lewbel, 2000; Matzkin, 2007)\@BBCP and the SCP, we obtain semi-nonparametric identification of the preference distribution given basically any consideration set formation mechanism (henceforth, consideration mechanism).333The identification results are semi-nonparametric because we specify the utility function up to a DM-specific preference parameter. We establish nonparametric identification of the distribution of the latter. We also prove identification of the consideration mechanism for the widely used Alternative-specific Random Consideration (ARC) model of \@BBOPcite\@BAP\@BBNManski (1977)\@BBCP and \@BBOPcite\@BAP\@BBNManzini & Mariotti (2014)\@BBCP. The identification argument is constructive and applicable beyond the ARC model. We establish identification results for preferences that do not require large support of the excluded regressor(s). We also show that identification of both preferences and the consideration mechanism is attainable when consideration depends on preferences. In particular, we introduce (i) binary consideration types, and (ii) proportionally shifting consideration, both of which can capture the notion that the DM’s attention probabilistically shifts from riskier to safer alternatives as her risk aversion increases. In these cases, identification requires that the distribution of the preference parameter admits a continuous density function.

We can significantly expand our results with alternative-specific excluded regressors. First, we can allow for essentially unrestricted dependence of consideration on preferences without assuming that the excluded regressors have large support. Second, we show that consideration can depend both on preferences and on some excluded regressors. We show this for two cases. In the first case, there is one alternative (the default) that is always considered. The probability of considering other alternatives can depend on the default-specific excluded regressor. This is a generalization of the models in \@BBOPcitet\@BAP\@BBNHeiss et al. (2016); Ho et al. (2017); Abaluck & Adams (2018)\@BBCP, where the consideration mechanism only allows for the possibility that either the default or the entire choice set is considered. We, however, allow for each subset of the choice set containing the default to have its own probability of being drawn and this probability can vary with the DM’s preferences. In the second case, we allow the consideration of each alternative to depend on its own excluded regressor, but not on the regressors of other alternatives \@BBOPcitep\@BAP\@BBN(Goeree, 2008; Abaluck & Adams, 2018; Kawaguchi et al., 2020)\@BBCP. In addition, consideration may depend on preferences – a feature unique to our paper.

Our second contribution is to provide a simple method to compute our likelihood-based estimator. Its computational complexity grows polynomially in the number of parameters governing the consideration mechanism. Because the SCP generates a natural ordering of alternatives akin to vertical product differentiation, our method does not require enumerating all possible subsets of the choice set. If it did, the computational complexity would grow exponentially with the size of the choice set. Moreover, we compute the utility of each alternative only once for a given value of the preference parameter, gaining enormous computational advantage similar to that of importance-sampling methods.

Our third contribution is to elucidate the applicability and the advantages of our framework over the standard application of full consideration random utility models (RUMs) with additively separable unobserved heterogeneity (e.g., Mixed Logit). First, our model can generate zero shares for non-dominated alternatives. Second, the model has no difficulty explaining relatively large shares of dominated alternatives. Third, in markets with many choice domains, our model can match not only the marginal but also the joint distribution of choices across domains. Forth, our framework is immune to an important criticism by \@BBOPcite\@BAP\@BBNApesteguia & Ballester (2018)\@BBCP against using standard RUMs to study decision making under risk. As these authors note, combining standard EUT with additive noise results in non-monotonicity of choice probabilities in the risk preferences, a clearly undesirable feature.

Random preference models like the ones we consider are random utility models as envisioned by \@BBOPcite\@BAP\@BBNMcFadden (1974)\@BBCP \@BBOPcitep\@BAP\@BBN(for a textbook treatment see Manski, 2009)\@BBCP. We show that our random preference models can be written as RUMs with unobserved heterogeneity in risk aversion and with an additive error that has a discrete distribution with support . Then, it is natural to draw parallels with the Mixed (random coefficient) Logit model \@BBOPcitep\@BAP\@BBN(e.g., McFadden & Train, 2000)\@BBCP. In our setting, the Mixed Logit boils down to assuming that, given the DM’s risk aversion, her evaluation of an alternative equals its expected utility summed with an unobserved heterogeneity term capturing the DM’s idiosyncratic taste for unobserved characteristics of that alternative. However, in some markets it is hard to envision such characteristics.444Many insurance contracts are identical in all aspects except for the coverage level and price, e.g., employer provided health insurance, auto, or home insurance offered by a single company. In other contexts, unobservable characteristics may affect choice mostly via consideration – as we model – rather than via “additive noise”. E.g., a DM may only consider those supplemental prescription drug plans that cover specific medications. We show that limited consideration models and the Mixed Logit generate several contrasting implications. First, the Mixed Logit generally implies that each alternative has a positive probability of being chosen, while a limited consideration model can generate zero shares by setting the consideration probability of a given alternative to zero. Second, the Mixed Logit satisfies a Generalized Dominance Property that we derive: if for any degree of risk aversion alternative has lower expected utility than either alternative or , then the probability of choosing must be no larger than the probability of choosing or . Limited consideration models do not necessarily abide Generalized Dominance. Third, in limited consideration models choice probabilities depend on the ordinal expected utility rankings of the alternatives, while in the Mixed Logit it depends on the cardinal ranking. This difference implies that choice probabilities may be monotone in risk preferences in the limited consideration models we propose, while in the Mixed Logit they are not \@BBOPcitep\@BAP\@BBN(Apesteguia & Ballester, 2018)\@BBCP.

We illustrate our method in a study of households’ deductible choices across three lines of insurance: auto collision, auto comprehensive, and home (all perils). We aim to estimate the distribution of risk preferences and the consideration parameters and to assess the resulting fit of the models. We find that the ARC model does a remarkable job at matching the distribution of observed choices, and because of its aforementioned properties, outperforms the Mixed Logit. Under the ARC model, we find that although households are on average strongly risk averse, they consider lower coverages more often than higher coverages. We also find support for proportionally shifting consideration. In particular, risk-neutral DMs consider each of the safer alternatives () less often than do extremely risk averse DMs (DMs with median risk aversion).

The rest of the paper is organized as follows. We describe the model of DMs’ preferences in Section 2, and study identification in Section 3. In Section 4 we describe the computational advantages of our approach. Section 5 compares our model to the Mixed Logit. Section 6 presents our empirical application. Section 7 contextualizes our contribution relative to the extant literature and offers concluding remarks.

2 Preferences

2.1 Decision Making under Risk in a Market Setting: An Example

Consider as an example the following insurance market, which mimics the setting of our empirical application. There is an underlying risk of a loss that occurs with probability that may vary across DMs. A finite number of alternatives are available to insure against this loss. Conditional on risk type, i.e., given , each alternative is fully characterized by the pair . The first element is the insurance deductible, which is the DM’s out of pocket expense in the case a loss occurs. Deductibles are decreasing with index , and all deductibles are less than the lowest realization of the loss. The second element is the price (insurance premium), which also varies across DMs. For each DM there is a baseline price that determines prices for all alternatives faced by the DM according to the multiplication rule . Lower deductibles provide more coverage and cost more, so is increasing with . Both and are invariant across DMs. The lotteries that DMs face are , where . DMs are expected utility maximizers. Given initial wealth , the expected utility of deductible lottery is

where is a Bernoulli utility function defined over final wealth states. We assume that belongs to a family of utility functions that are fully characterized by a scalar (e.g. Constant Absolute Risk Aversion (CARA), Constant Relative Risk Aversion (CRRA), or Negligible Third Derivative (NTD)), which varies across DMs.555Under CRRA, it is implied that DMs’ initial wealth is known to the researcher. NTD utility is defined in \@BBOPcite\@BAP\@BBNCohen & Einav (2007)\@BBCP and in \@BBOPcite\@BAP\@BBNBarseghyan et al. (2013)\@BBCP.

Given the risk type, the relationship between risk aversion and prices is standard. At sufficiently high , less coverage is always preferred to more coverage for all on the support: . At sufficiently low , we have the opposite ordering for all on the support: . At moderate prices, for each pair of deductible lotteries there is a cutoff value in the interior of ’s support, found by solving for . On the left of this cutoff the higher deductible is preferred and on the right the lower deductible is preferred. In other words, is the unique coefficient of risk aversion that makes the DM indifferent between and , known to the researcher at any given . Those with lower choose the riskier alternative , while those with higher choose the safer alternative . Provided is smooth in , is smooth in . In fact, under CARA, CRRA, or NTD, is a continuously differentiable monotone function. The prices are such that, under CARA, CRRA, or NTD, whenever it is also the case that .666We analytically verify this claim for our application in Appendix B, but it can also be checked numerically for any given dataset. As we show below, this can be stated as . That is, if the DM’s risk aversion is so low that she prefers the riskiest lottery to a safer one, then she also prefers it to an even safer one. Finally, there are no three-way ties. That is, for a given there are no alternatives such that .777It is straightforward to very this condition, and we do so in our application.

2.2 Preferences with Single Crossing Property

There is a continuum of DMs. Each of them faces a choice among a finite number of alternatives, i.e., a choice set, which is denoted . The number of alternatives is invariant across DMs. Alternatives vary by their utility-relevant characteristics and are distinguished by (at least) one characteristic, , which is DM invariant. This characteristic reflects the quality of alternative (e.g., insurance deductible). When it is unambiguous, we may write instead of “alternative ”. Other characteristics may vary across DMs or across alternatives. Our analysis rests on the excluded regressor(s) . To keep the notation as lean as possible, we state our assumptions and results implicitly conditioning on all remaining characteristics. Hence, alternative is fully characterized by . We consider two cases. In one case, all ’s are perfectly correlated with a single (common) excluded regressor, (e.g., in our insurance example). In the other case, each has its own variation conditional on all other (e.g., each alternative on the market exhibits locally independent price variation).

Assumption T0.

The random variable (or vector) has a strictly positive density on a set .

Each DM’s valuation of the alternatives is defined by a utility function , which depends on a DM-specific index distributed according to over a bounded support.888We assume that while has bounded support, the utility function is well defined for any real valued .

Assumption T1.

The density of , denoted , is continuous and strictly positive on and zero everywhere else.

The DMs’ draws of are not observed by the researcher. We require that DMs’ preferences satisfy the Single Crossing Property (SCP).

Assumption T2 (Single Crossing Property).

For any two alternatives, and , there exists a continuously differentiable function such that

where or . We refer to as the cutoff between and .

The SCP implies that the DM’s ranking of alternatives is monotone in . In the context of risk preferences, if a DM with a certain level of risk aversion prefers a safer asset to a riskier one, then all DMs with higher risk aversion also prefer the safer asset. Since the cutoffs may be infinite, the SCP does not exclude dominated alternatives.

Definition 1 (Dominated Alternatives).

Given , alternative is dominated if there exists an alternative such that , .

We now establish some useful facts that follow from Assumption Assumption T2. First, the index in indicates the alternative that is preferred on the left of the cutoff. It is without loss of generality to assume and because of the following fact:

Fact 1 (Natural Ordering of Alternatives).

Suppose Assumption Assumption T2 holds. Then alternatives can be enumerated such that as , for all at which no alternative is dominated.

We assume that alternatives are enumerated according to the Natural Ordering of Alternatives.999Under this enumeration, will be ordered in either ascending or descending order. In our example from the previous section, since refers to the deductible and is the risk aversion coefficient, the natural ordering implies As the next fact shows, for high values of the preference over the Natural Ordering of Alternatives is reversed.

Fact 2 (Rank Switch).

Suppose Assumption Assumption T2 holds. Consider any such that no alternative is dominated. As ,

The SCP also has implications for the relative position of the cutoffs. For readability, we state them for alternatives , but they hold for any , .

Fact 3 (Simple Relative Order of Cutoffs).

Suppose Assumption Assumption T2 holds. Given , if , then or both and dominate ().

The next fact concerns the relative order of cutoffs for non-dominated alternatives. Before stating it, it is convenient to define Never-the-First-Best Alternatives.

Definition 2 (Never-the-First-Best).

Given , alternative is Never-the-First-Best in if for every there exists another alternative in such that .

Fact 4 (Cutoff Relative Order).

Suppose that Assumption Assumption T2 holds. If, given , alternatives , , and are not dominated, then one and only one of the following cases holds:

-

(i)

and is the first best in , ;

-

(ii)

and is Never-the-First-Best in ;

-

(iii)

and is strictly worse than either or for all except for where there is a three-way tie among these alternatives.

Fact 4 is a convenient way to distill and exploit the SCP. In particular, for any , the complete preference order of the alternatives is known for all DMs as well as the identity (of the preference parameter) of the DM indifferent between any two alternatives and .

3 Identification

The classic identification argument for discrete choice under full consideration rests on the following four canonical assumptions.

Assumption I0.

The random variable (or vector) is independent of preferences.

Assumption I1.

s.t. covers the support of : .

Assumption I2.

Consideration is independent of preferences.

Assumption I3.

Consideration is independent of .

The last two conditions are vacuous in the standard full consideration model, while the first two are typically stated as data requirements.

We first discuss how to obtain identification and the role of Assumptions Assumption I0-Assumption I3 in the simplest case of two alternatives (Section 3.1). We then consider the general model with alternatives. Table 1 organizes our results by assumptions imposed, the consideration mechanism assumed, data availability, and the theorems’ conclusions. Theorems 1-3 in Section 3.2 demonstrate that the preference distribution and some features of the consideration mechanism are identified with a single excluded regressor. Next, we show that alternative-specific variation allows for identification of both the preference distribution and the consideration mechanism when consideration depends on preferences and one of the excluded regressors (Theorem 4 and Corollary 1 in Section 3.3). We discuss testing for limited consideration in Section 3.4. We then turn to the ARC model in Section 3.5. We show that the full model is identified with a single excluded regressor (Theorem 5). Moreover, identification attains for a particular case where consideration depends on preferences (Theorem 6). Finally, Theorem 7 shows that with alternative-specific variation, identification attains when consideration of each alternative depends both on preferences and its own regressor, without requiring full support.

| Assumptions | Consideration Mechanism | Excluded Regressor | Identification Result | ||||||||

| Generic | Loosely | ARC | Single | Alternative Specific | Preferences | Consideration | |||||

| I0 | I1 | I2 | I3 | Ordered | |||||||

| Theorem 1 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| Theorem 2 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||

| Theorem 3 | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| Theorem 4 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||

| Corollary 1 | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| Theorem 5 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Theorem 6 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| Theorem 7 | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

3.1 The Role of the Canonical Assumptions

Let the choice set be binary and suppose that the DM considers both alternatives. In addition, let be a scalar so that there is a single excluded regressor. Under Assumptions Assumption T0-Assumption T2 and Assumption I0-Assumption I3, any realization of is associated with a single conditional moment in the data:

because the DM chooses if and only if her preference parameter is less than . The distribution is non-parametrically identified, since for any on the support there is an such that .

We emphasize two points. First, given a family of utility functions, for any the value of the cutoff can be solved for. Hence, the function (and its derivatives) can be treated as data. Second, Assumption Assumption I1 requires that the cutoff reaches both ends of the support: there exist and such that and .

Turning to limited consideration, suppose that is considered with probability , and whenever it is considered so is .101010With two alternatives this implies that is always considered. Then, is chosen when it is considered and it is preferred to , yielding:

| (1) |

At first glance, it appears that the distribution of preferences is identified up to a constant. Yet, at the boundary of the support , so that is identified. Once is known, the distribution is identified by varying over the support of , similar to the full consideration case. We now explore what happens to identification if Assumptions Assumption I0–Assumption I3 are not satisfied.

Assumption Assumption I0 fails: the variation in is not independent of preferences. Then is not non-parametrically identified under either full or limited consideration.

Assumption Assumption I1 fails: the variation in is such that only covers an interval . Then the data provide no information about preferences outside of the interval . Inside the interval, the conditional distribution is identified under both limited and full consideration. The consideration probability (and hence the scale of ) is partially identified and satisfies the bounds , where is such that . Point identification can be attained if an additional assumption is maintained to pin down the scale of . For example, one can simply assume full consideration and set .

Assumption Assumption I2 fails: depends on preferences and this dependence is arbitrary. Then identification breaks down completely as there is one data moment to identify two unknown objects. However, since we assume – as it is common in the econometrics literature – that the density function of is continuous and strictly positive, identification is possible for some types of dependence between consideration and preferences. Suppose there are two consideration types:

where is an unobserved breakpoint. We show that , , and are identified. First, the product is identified under Assumptions Assumption I0, Assumption I1, and Assumption I3, since

| (2) |

at . The product is discontinuous only at the point . Thus, the breakpoint is identified by continuously varying across Next, the ratio is identified by the ratio of the right and left derivatives of at the breakpoint (). The quantity is identified by the ratio:

Hence, and are identified. Identification of on the entire support follows from Assumption Assumption I1. The same argument above applies if the probability of considering an alternative discretely jumps in (i.e., Assumption Assumption I3 fails). Concretely, suppose there is a breakpoint in at and let . The breakpoint is identified by the point of discontinuity in Equation (2), and the rest follows.

To summarize the case of the binary choice set, the only seemingly real difference in identification is that without large support the scale of the preference distribution is partially identified under limited consideration, while it is assumed to be known under full consideration. The key to identification is a one-to-one mapping from a data moment, , and the preference distribution at a single point on the support, . As we will show next, even with just a single excluded regressor, Assumptions Assumption I0-Assumption I3 allow for such a mapping to be constructed for a generic consideration mechanism and a choice set of arbitrary size.

3.2 Single Common Excluded Regressor

We start by introducing general notation for consideration probabilities.

Definition 3.

Let be the probability that, given , the DM with preference parameter draws consideration set conditional on .

Let be the probability that, given , every alternative in set is in the consideration set and every alternative in set is not for the DM with preference parameter :

The subscript is suppressed when consideration does not depend on preferences, and the superscript is suppressed when it does not depend on the excluded regressor(s).

To ease exposition, we build our discussion around a choice set with three alternatives, , such that for all . That is, by Fact 3, if then for all . Suppose consideration is independent of preferences and of the excluded regressor. Then the choice frequencies of and are

Consider the expression for . Its RHS has three terms. The first term captures the case when is considered along with , which happens with probability Given the relative position of the cutoffs, whether is considered or not is irrelevant. The DM will choose over if and only if her preference parameter is below . The second term captures the case when is considered along with , but is not considered, which happens with probability . Then the relevant cutoff for choosing is . Third, when is the only alternative considered, it is chosen regardless of the DM’s risk aversion. This event occurs with probability .

Since there are two cutoffs, and , that enter the moment , there is not, without additional assumptions, a one-to-one mapping between the moment and the preference distribution at one point on the support, as it was the case in Section 3.1. That is, as changes, the observed choice frequency of may change because of two types of marginal DMs: those indifferent between and , and those indifferent between and . This is apparent in the following derivative:

| (3) |

The corresponding equation for does not immediately help, as it brings about evaluated at yet another cutoff, :

| (4) |

3.2.1 Identification with Large Support

When Assumption Assumption I1 holds, we can construct a one-to-one mapping sequentially. The algorithm for doing so consists of four steps. First, we rewrite Equation (3) as

| (5) |

where and . Second, for ’s near the far end of the support, we can find and such that and . For any such pair, , and, hence, by Equations (3) and (4):

The first equation identifies , while the ratio of the two equations identifies . Third, whenever is known, is uniquely pinned down by Equation (5). Because , , we can learn sequentially:

-

1.

Take an such that is already known, learn ;

-

2.

Take such that , learn ;

-

3.

Let . Repeat Step 2 until the entire support has been covered, i.e., .

For this approach to work, cannot “catch up” to (i.e., as assumed, whenever is on the support). This requires that DMs with preference coefficients on the support are never indifferent between and two other alternatives – i.e. there are no three way ties involving . Fourth, integration of over the entire support recovers the scale and the true density. Indeed,

pins down , and hence is identified. A generalization of this strategy yields our first formal result.

Theorem 1.

Suppose Assumptions Assumption I0, Assumption I2, Assumption I3, Assumption T0-Assumption T2 hold, and

-

1.

The consideration mechanism is s.t. with positive probability and are considered together;

-

2.

Assumption Assumption I1 holds for s.t.

Then is identified and so are and . For , if for some , then is identified.

The first assumption of the theorem ensures that a generalized version of Equation (5) is informative. The second assumption implies that the cutoffs for alternative are ordered: . While Theorem 1 requires large support for the excluded regressor, it does not generally require it to exhibit variation that forces alternative to go from being the first best to the least preferred. Rather, the theorem requires that at one extreme of the support alternative dominates all others. However, at the other extreme we only require that is preferred to for all DMs. Identification is attained for any consideration mechanism that allows and to be considered together with positive probability. Moreover, if the probability of being considered together is zero for and , but positive for and , the theorem still holds as long as the assumptions of the theorem hold for instead of . Theorem 1 identifies some features of the consideration mechanism. These features may be sufficient for identifying the entire mechanism. In particular, as shown in Section 3.5, Theorem 1 yields identification of the ARC model, including the consideration mechanism.

Dependence between consideration and preferences. We next generalize the example in Section 3.1 by allowing for high/low consideration types.

Assumption I2.BCT (Binary Consideration Types).

For some unknown :

where, and , and .

Theorem 2.

Suppose Assumptions Assumption I0, Assumption I2.BCT, Assumption I3, Assumption T0-Assumption T2, and Condition 2 of Theorem 1 hold. Suppose Condition 1 of Theorem 1 holds for all . Then is identified and so is . Suppose is discontinuous. Then is identified. If, in addition, for some and , then is also identified.

A discontinuity in may occur when a cutoff crosses . In some cases it may not happen despite binary consideration. For example, the probability of considering and may jump but in a way that remains constant. In such a case, is identified but not necessarily the breakpoint .

The theorem holds if Assumption Assumption I2.BCT is replaced with

for some unknown . In sum, preferences can be identified even when there are threshold effects affecting consideration. Assumption Assumption I2.BCT is one instance where Assumption Assumption I2 does not hold but identification attains. Another instance, which we establish for the ARC model in Section 3.5.1, is proportionately shifting consideration.

3.2.2 Identification without large support

Returning to our example with three alternatives, it is immediate to see that if whenever is considered so is , i.e. , the one-to-one mapping is restored. Indeed, the second term on the RHS of Equation (3) disappears and we are back to Equation (1).

Proposition 1.

Suppose Assumptions Assumption I0, Assumption I2, Assumption I3, Assumption T0-Assumption T2 hold, and

-

1.

The consideration mechanism is such that is considered with positive probability and whenever it is considered so is ;

-

2.

There exists such that , , covers and

Then is identified.

The proposition above uses (the derivative of) to create the one-to-one mapping from data to the preference density function. Depending on the consideration mechanism, the same can be achieved using the derivative of .

Definition 4 (Loosely Ordered Consideration).

The consideration mechanism is loosely ordered around , , if whenever alternatives and , , are both considered, so are and . In addition, and have a positive probability of being considered together.

Theorem 3.

Suppose Assumptions Assumption I0, Assumption I2, Assumption I3, Assumption T0-Assumption T2 hold, and

-

1.

The consideration mechanism is loosely ordered around .

-

2.

There exists such that , , covers and

Then is identified.

Condition 1 in Theorem 3 – a loosely ordered consideration mechanism – splits the choice set into “low quality” and “high quality” sets. Any subset of the low quality set can form the consideration set and so can any subset of the high quality set. However, if a consideration set contains both high and low quality alternatives, then it must also contain the “bridging” alternatives . The following mechanisms can generate loosely ordered consideration:

-

I.

Bottom-Up consideration: Alternative is considered only if is considered;

-

II.

Top-Down consideration: Alternative is considered only if is considered;

-

III.

Center-to-edges consideration: Alternative , , is always considered. Alternative , , is considered only if is considered. Alternative , , is considered only if is considered;

-

IV.

Trimmed-from-the-edges consideration: Only consideration sets of the form can occur with positive probability.

The identification result in Theorem 3 extends to mixtures of these mechanisms. They cover a wide array of models including versions of threshold models \@BBOPcitep\@BAP\@BBN(Kimya, 2018)\@BBCP, (partial) elimination-by-aspects \@BBOPcitep\@BAP\@BBN(Tversky, 1972)\@BBCP, extremeness aversion \@BBOPcitep\@BAP\@BBN(Simonson & Tversky, 1992)\@BBCP, and edge aversion \@BBOPcitep\@BAP\@BBN(Teigen, 1983; Christenfeld, 1995; Rubinstein et al., 1997; Attali & Bar-Hillel, 2003)\@BBCP, as well as models that embed budget or liquidity constraints.

Condition 2 in Theorem 3 requires that whenever a DM prefers to , she also prefers to all high quality alternatives; and whenever a DM prefers to , she also prefers to all low quality alternatives. This condition can be tested in any given dataset and is automatically satisfied if no alternative is never-the-first-best.

3.3 Alternative-specific Excluded Regressors

With alternative-specific excluded regressors we can allow for consideration to depend on preferences. To illustrate, we continue to assume that the choice set is . However, now each alternative has its own regressor that only affects the utility of alternative : . In addition, these regressors vary independently of one another and each consideration set contains at least two alternatives.

Identification is built on the following insight. Consider the change in the choice frequency of alternative in response to an incremental change in (e.g., a price increase for alternative ). The DMs who may switch to are those indifferent between and and consider them both. If these DMs prefer and to , whether is considered is irrelevant; otherwise, for the response to occur, should not be considered. These two cases translate to the following statements: (i) ; and (ii) and is not considered. No other ordering of cutoffs can occur by Fact 4. With alternative specific variation we can construct two vectors of regressors, and , such that and .111111 First, we can construct an such that . To do so, we fix the price of the first alternative, , and find a price for the second alternative that makes the DM with preference parameter indifferent between and . Since does not affect the utility of nor , we can find an so that the DM is indifferent between and , and hence she is indifferent between all three alternatives. The two cases are then constructed by taking a small perturbation of . Taken in a direction that reduces generates Case (i); and in the opposite direction Case (ii). The derivative of the choice frequency of with respect to for these cases are, respectively:

It follows that and are identified. In a similar fashion, and are identified. Hence, the consideration probability of each non-singleton set is identified up to the same scale. The scale, however, is identified because consideration probabilities must sum to one: . Hence, is also identified for each . The following theorem generalizes this idea.

Definition 5 (Alternative-Specific Variation).

We say that there is alternative-specific variation if depends only on : .

Theorem 4.

Suppose Assumptions Assumption I0, Assumption I3, Assumption T0-Assumption T2 hold, there is alternative-specific variation, and the choice set contains at least three alternatives. Suppose

-

1.

Each consideration set contains at least two alternatives and is measurable;

-

2.

For a given value of , there exists an with an open neighborhood around it in s.t.

Then is identified and so are , .

The assumptions of the theorem above rule out singleton (and empty) consideration sets: identification is impossible with singleton consideration sets and arbitrary dependence on preferences, because any empirical choice frequency can be explained by such consideration sets. An alternative approach is to have one alternative – the “default” – that is always considered as the following corollary demonstrates. The identification argument exploits the response of to changes in , but not the response of to changes in . Hence, excluded regressors are sufficient for identification, allowing for arbitrary dependence of consideration on one (the default’s) excluded regressor.

Corollary 1.

Suppose Assumptions Assumption I0, Assumption T0-Assumption T2 hold, there is alternative-specific variation, the choice set contains at least three alternatives, all consideration sets contain , and

-

1.

Consideration is independent of : , and are measurable functions, continuous in ;

-

2.

The consideration of is independent of : , ;

-

3.

For a given value of and each value of , there exists an and an open neighborhood around in s.t.

Then is identified and so are , , for all on the support.

Corollary 1 generalizes the model of \@BBOPcitet\@BAP\@BBNHeiss et al. (2016); Ho et al. (2017)\@BBCP in two dimensions. First, here each subset of the choice set containing the default has its own probability of being drawn. Second, this probability can vary with the DM’s preferences as well as with the excluded regressor of the default alternative.

3.4 Testing for limited consideration

Since full consideration is a special case of limited consideration, it follows from the identification results above that under the SCP one can test for full consideration. The theorem below states one way of doing so without: (1) relying on large support; (2) specifying a consideration mechanism; or (3) invoking the independence assumptions Assumption I2 and Assumption I3.

Proposition 2.

Suppose Assumptions Assumption I0, Assumption T0-Assumption T2 hold. Suppose there exist , and sets s.t. for some

-

1.

, , and ,

-

2.

, , and ,

If , then there is limited consideration.

Condition 1 of the theorem requires that, given , the first-best alternative belongs to for all DMs with and to for all DMs with . Condition 2 is the identical requirement, but given and stated for . Under these conditions and full consideration, the probability of choosing an alternative in or, respectively, should be in both cases. Thus, if , then there is a limited consideration mechanism pushing DMs’ choices away from and at different rates.

3.5 The ARC Model

We now introduce a specific consideration mechanism, while maintaining the preference structure, including the SCP, from Section 2.2. We refer to this model as the Alternative-specific Random Consideration (ARC) model \@BBOPcitep\@BAP\@BBN(Manski, 1977; Manzini & Mariotti, 2014)\@BBCP. Each alternative appears in the consideration set with probability independently of other alternatives. For now, we assume that these probabilities do not depend on DMs’ preferences or the excluded regressor. Once the consideration set is drawn, the DM chooses the best alternative according to her preferences. To avoid empty consideration sets, following \@BBOPcite\@BAP\@BBNManski (1977)\@BBCP, we assume that at least one alternative whose identity is unknown to the researcher is always considered.121212In the previous version of this paper \@BBOPcitep\@BAP\@BBN(Barseghyan, Molinari, & Thirkettle, 2019)\@BBCP this completion rule is called Preferred Option(s). There we also provide identification results for other completion rules, including Coin Toss (if the empty consideration set is drawn, the DM randomly uniformly picks one alternative from the choice set, i.e. each alternative has probability of being chosen), Default Option (there is a preset alternative that is chosen if the empty set is drawn), and Outside Option (the DM exits the market if the empty set is drawn).

Assumption ARC (The Basic ARC Model).

The probability that the consideration set takes realization is

where , and s.t. .

By assuming , we omit never-considered alternatives from the choice problem. Since a never-considered alternative is never compared to any other alternative, whether it is in the choice set or not does not affect the DM’s problem. Hence, never-considered alternatives have no impact on what we can learn about preferences.

Under the assumptions of Theorem 1, identification attains. Notably, each consideration parameter is identified (as long as is chosen with positive probability at some ).

Theorem 5.

Suppose Assumptions Assumption I0, Assumption I2-Assumption I3, Assumption T0-Assumption T2, Assumption ARC hold, and Assumption Assumption I1 holds for s.t.

Then is identified and so are and . In addition, if for some , then is identified.

3.5.1 Preference-Dependent Consideration

Returning to our example with three alternatives, recall that we have an additional moment . The information it provides allows us to identify some forms of dependence between consideration and preferences, i.e., to relax Assumption Assumption I2. To see how, suppose is always considered. Then, with preference dependence, the choice frequencies become:

The ratio of the derivatives of these two moments yields . More assumptions are required to obtain point identification of the ’s. In Section 3.2 we provided identification results for Binary Consideration Types. Here, leveraging the additional structure provided by the ARC model, we can allow for more flexible dependence between consideration and preferences. We do so through a proportionally shifting consideration mechanism, formally defined below. This mechanism may arise when there is a cost to evaluate each alternative. In such a case, the DMs may consider alternatives that they ex-ante deem more aligned with their preferences (e.g., the DM’s consideration shifts away from riskier to safer alternatives as her risk aversion increases).

Assumption ARC.P (ARC with Proportional Consideration).

The consideration mechanism follows the ARC model with or , and

s.t. is differentiable a.e., a.e., , , .

In the case with three alternatives, . From this, is identified when and are chosen such that . Once is identified, is known for all ; hence, can be solved for. Identification of follows from substituting into the expression for . The theorem below generalizes this argument.

Definition 6.

(No Three Way Ties) For a given , there are no-three way ties if and s.t. .

Theorem 6.

Suppose Assumptions Assumption I0, Assumption I3, Assumption T0-Assumption T2, Assumption ARC.P hold, and Assumption Assumption I1 holds for s.t. there are no three-way ties and

and s.t. .

Then and are identified.

The conditions of the theorem are stronger than in Theorem 5, as they impose relative order of the cutoffs not only for alternative but also for . In many cases, the relative order of ’s alone is sufficient, for example when is always considered.

3.5.2 Identification with Alternative-specific Excluded Regressors

By leveraging features of the ARC model, the identification results in Section 3.3 can be extended to the case where the consideration of is a function both of and preferences. This differs from Corollary 1, which restricted the consideration of alternative to depend only on the default alternative’s excluded regressor. We continue to assume that the choice set is and that is always considered. Let the consideration of be a measurable function of and , continuous in its first argument: . Similar to the example in Section 3.3, we construct two vectors, and , such that: (i) ; and (ii) . The derivative of the choice frequency of with respect to for these cases are, respectively:

| (6) | ||||

The ratio of the expressions in Equation (6) identifies . Using a similar logic, we can identify . Plugging these consideration probabilities into Equation (6) identifies . In sum, alternative-specific variation yields identification without large support and without the independence Assumptions Assumption I2 and Assumption I3. It is also possible to allow consideration of (and ) to depend on , , as well as . The key exclusion restriction in this case is that the consideration of is independent of all components of . Our last identification result generalizes this example.

Assumption ARC.AS.

The consideration mechanism follows the ARC model. The consideration probability of each alternative is a measurable function of and preferences: , continuous in the first argument. Default alternative is s.t. for all and for all .

Theorem 7.

Suppose Assumptions Assumption I0, Assumption T0-Assumption T2, Assumption ARC.AS hold. Suppose there is alternative-specific variation and the choice sets contain at least three alternatives. Suppose for a given value of there exists an , and an open neighborhood around it in , s.t.

Then and are identified.

Existing identification results that rely on alternate-specific variation \@BBOPcitep\@BAP\@BBN(Goeree, 2008; Abaluck & Adams, 2018; Kawaguchi et al., 2020)\@BBCP allow for consideration dependence on its own regressor, but not preferences. Theorem 7 states identification for a general version of the ARC model where the alternative-specific consideration probability can depend on both its own regressor and DMs’ preferences.

4 Likelihood and Tractability

We now turn to the computational aspects of limited consideration models under the SCP and, in particular, of their likelihood function. Consider a generic consideration mechanism.

A computationally appealing way to write the likelihood function is to determine the probability that a DM with preference parameter chooses alternative conditional on . Alternative is chosen if and only if is in the consideration set and every alternative that is preferred to is not. Denote the set of alternatives that are preferred to by

Then,

| (7) |

The object on the RHS does not require evaluating the utility of each alternative within each possible consideration set. In fact, needs to be computed only once for each , , and to create , which does not vary with the consideration set. Hence the computational complexity lies in the mapping from to the parameters governing the consideration mechanism. This, however, may not even require enumerating all possible consideration sets. To demonstrate this with a concrete example, we proceed with the basic ARC model. In this case, the RHS of Equation (7) is:

| (8) |

Given , the integrand is piecewise constant in with at most breakpoints, corresponding to indifference points between alternatives and , i.e., , that are computed only once for each observed . There are at least two methods to compute this integral. First, for every and , we can directly compute the breakpoints and hence write as a weighted sum:

where ’s are the sequentially ordered breakpoints augmented by the integration endpoints: and . This expression is trivial to evaluate given and breakpoints . More importantly, since the breakpoints are invariant with respect to the consideration probabilities, they are computed only once for each . This simplifies the likelihood maximization routine by orders of magnitude, as each evaluation of the objective function involves a summation over products with at most terms. A second approach is to compute using Riemann approximation:

where is the number of intervals in the approximating sum, is the intervals’ length, ’s are the intervals’ midpoints, and is the density of . Again, one does not need to evaluate the utility from different alternatives in the likelihood maximization. Instead, one a priori computes the utility rankings for each , . These rankings determine . The likelihood maximization is now a standard search routine over and . Our theory restricts to the class of continuous and strictly positive functions. In practice, the search is over a class of non-parametric estimators for .131313One could use a mixture of Beta distributions \@BBOPcitep\@BAP\@BBN(Ghosal, 2001)\@BBCP, as we do in Section 6. If the density is parameterized, i.e., , then the maximization is over and . Finally, the interval midpoints are the same across all DMs as they do not depend on , further reducing computational burden.141414Depending on the class of , it may be more accurate to compute by substituting with , where and are the endpoints of the corresponding interval.

Allowing consideration to depend on preferences (or on ) introduces only minimal adjustments to the likelihood function. For example, let each consideration function be parameterized by : . Then, at each , we can substitute with the corresponding , and the likelihood maximization is now over and . Given the desired level of parameterization – i.e., the dimensionality of the parameter vectors and – the computational complexity of the problem grows polynomially in .

As a final remark, if alternative is never chosen, then one can conduct estimation as if were not in the choice set. Indeed, per Equation (8), contributes positively to the likelihood if and only if alternative is chosen. When it is never chosen, it may only enter via the term ; hence, the likelihood will be maximized by setting . Therefore, setting for all zero-share alternatives, regardless of why they were not chosen, has no impact on estimation. This too may speed up estimation.

5 Limited Consideration and RUM: A Comparison

We focus on a standard application of the RUM with full consideration in the context of our example in Section 2.1. The final evaluation of the utility that the DM derives from alternative now includes a separately additive error term:

| (9) |

where, as before, captures unobserved heterogeneity in preferences, and is assumed independent of the random coefficients (in this application, ).

Typical implementations of this model further specify that is i.i.d. across alternatives (and DMs) with a Type 1 Extreme Value distribution, following the seminal work of \@BBOPcite\@BAP\@BBNMcFadden (1974)\@BBCP. This yields a Mixed Logit that is distinct from the commonly used one in \@BBOPcite\@BAP\@BBNMcFadden & Train (2000)\@BBCP. In their model, random coefficient(s) enter the utility function linearly, while in the context of expected utility they enter nonlinearly. We now discuss two properties of the Mixed Logit that hinder its applicability in our context.

5.1 Monotonicity

Coupling utility functions in the hyperbolic absolute risk aversion (HARA) family, for example CARA or CRRA, with a Type 1 Extreme Value distributed additive error yields:

Proposition 3.

\@BBOPcitep\@BAP\@BBN(Non-monotonicity in RUM, Apesteguia & Ballester, 2018; Wilcox, 2008)\@BBCP In Model (9) with HARA preferences and i.i.d. Type 1 Extreme Value, as the DM’s risk aversion increases, the probability that she chooses a riskier alternative declines at first but eventually starts to increase.

To see why, consider two non-dominated alternatives and such that is riskier than . A risk neutral DM prefers to , and hence will choose the former with higher probability. As risk aversion increases, the DM eventually becomes indifferent between and and chooses either of these alternatives with equal probability. As risk aversion increases further, she prefers to and chooses the latter with lower probability. However, as risk aversion gets even larger, the expected utility under HARA of any lottery with finite stakes converges to zero. Consequently, the choice probabilities of all alternatives, regardless of their riskiness, converge to a common value.151515Recall that in the Mixed Logit the magnitude of the utility differences is tied to differences in (log) choice probabilities, , so that as the choice probabilities are predicted to be all equal. Hence, at some point the probability of choosing is increasing in risk aversion.

To the contrary, our model with a limited consideration mechanism that is independent of preferences yields choice probabilities that are monotone in the preference parameter.

Property 1 (Generalized Preference Monotonicity).

A model satisfies generalized preference monotonicity if for any and :

In the context of risk preferences, Property 1 states that the probability of choosing one of the riskiest alternatives declines as increases. Since Property 1 is satisfied for any choice set under the SCP and full consideration, it is also satisfied under limited consideration:

Proposition 4.

A model that satisfies the SCP (i.e., Assumption Assumption T2) and Assumption Assumption I2 satisfies Generalized Preference Monotonicity.

5.2 Generalized Dominance

Next, we establish the relation between utility differences across two alternatives and their respective choice probabilities. Because our random expected utility model features unobserved preference heterogeneity, we work with an analog of the rank order property in \@BBOPcite\@BAP\@BBNManski (1975)\@BBCP that is conditional on :

Definition 7.

(Conditional Rank Order of Choice Probabilities) The model yields conditional rank order of the choice probabilities if for given and alternatives ,

We show that the conditional rank order property implies the following upper bound on the probability that suboptimal alternatives are chosen.

Property 2.

(Generalized Dominance) A model satisfies Generalized Dominance if for any , , and set s.t. alternative is never-the-first-best in

Generalized Dominance holds in the Mixed Logit model and, more broadly, in models that satisfy the conditional rank order property. However, it may not hold in some limited consideration models. For example, Generalized Dominance is violated if is never-the-first best among , is almost always considered, and alternatives and are rarely considered.

5.3 Limited Consideration as Ordinal RUM

In the Mixed Logit, the cardinality of the differences in the (random) expected utility of alternatives plays a crucial role in the determination of choice probabilities, as it interacts with the realization of the additive error. In contrast, in models that satisfy the SCP, the DMs’ choices are determined by the ordinal expected utility ranking of the alternatives. Hence, limited consideration models can be recast as Ordinal Random Utility models (ORUM), where the key departure from standard RUMs is the distribution of the additive error term.

Proposition 5.

(Limited Consideration as ORUM) A Limited Consideration Model is equivalent to an additive error random utility model with unobserved preference heterogeneity where all alternatives are considered, the DM’s utility of each alternative is given by

and is distributed on according to for s.t. if and if .

Casting our limited consideration model as an ORUM clearly demonstrates its flexibility. In particular, our results show how to obtain identification when the errors are correlated with the excluded regressors, the preference parameter, and across alternatives.

| Error Structure | Mixed Logit | Basic ARC | Binary Types | Prop. Shifting | Generic Consideration |

|---|---|---|---|---|---|

| Support | |||||

| Independent of | Yes | Yes | Yes1 | Yes | No |

| Independent of | Yes | Yes | No1 | No | No |

| Independent across alternatives | Yes | Yes | Yes | Yes | No |

| Identical across alternatives | Yes | No | No | No | No |

We conclude this section with Table 2, listing the differences across the Mixed Logit and limited consideration models. The first two columns summarize the differences between the basic ARC model and the Mixed Logit. The third column and fourth column remind the reader our two models with consideration depending on preferences. Finally, the last column highlights the fact that with alternative-specific variation we may also have dependence of the error term on the excluded regressor(s) as well as on the preference parameter.

6 Application

We offer an empirical analysis of households’ decisions under risk. This analysis aims to illustrate how our method works and its ability to fit the data.

6.1 Data

We study households’ deductible choices across three lines of property insurance: auto collision, auto comprehensive, and home all perils. The data come from a U.S. insurance company. Our analysis uses a sample of 7,736 households who purchased their auto and home policies for the first time between 2003 and 2007 and within six months of each other.161616The dataset is an updated version of the one used in \@BBOPcite\@BAP\@BBNBarseghyan et al. (2013)\@BBCP. It contains information for an additional year of data and puts stricter restrictions on the timing of purchases across different lines. These restrictions are meant to minimize potential biases stemming from non-active choices, such as policy renewals, and temporal changes in socioeconomic conditions. Table D.1 provides descriptive statistics for households’ observable characteristics, which we use later to estimate households’ preferences.171717These are the same variables that are used in \@BBOPcite\@BAP\@BBNBarseghyan et al. (2013)\@BBCP to control for households’ characteristics. See discussion there for additional details. We observe the exact menu of alternatives available at the time of the purchase for each household and each line of coverage. The deductible alternatives vary across lines of coverage but not across households. Table D.2 presents the frequency of chosen deductibles in our data.

| Quantiles | 0.01 | 0.05 | 0.25 | 0.50 | 0.75 | 0.95 | 0.99 |

|---|---|---|---|---|---|---|---|

| Collision | 53 | 74 | 117 | 162 | 227 | 383 | 565 |

| Comprehensive | 29 | 41 | 69 | 99 | 141 | 242 | 427 |

| Home | 211 | 305 | 420 | 540 | 743 | 1,449 | 2,524 |

Premiums are set coverage-by-coverage as in the example from Section 2.1. Table D.5 reports the average premium by context and deductible, and Table 3 summarizes the premium distributions for the deductible. Premiums vary dramatically. The 99th percentile of the deductible is more than ten times the corresponding 1st percentile in each line of coverage.

Claim probabilities stem from \@BBOPcitep\@BAP\@BBN(Barseghyan, Teitelbaum, & Xu, 2018)\@BBCP, who derived them using coverage-by-coverage Poisson-Gamma Bayesian credibility models applied to a large auxiliary panel. Predicted claim probabilities (summarized in Table 4) exhibit extreme variation: The 99th percentile claim probability in collision (comprehensive and home) is 4.3 (12 and 7.6) times higher than the corresponding 1st percentile. Finally, the correlation between claim probabilities and premiums for the deductible is 0.38 for collision, 0.15 for comprehensive, and 0.11 for home all perils. Hence, there is independent variation in both.

| Quantiles | 0.01 | 0.05 | 0.25 | 0.50 | 0.75 | 0.95 | 0.99 |

|---|---|---|---|---|---|---|---|

| Collision | 0.036 | 0.045 | 0.062 | 0.077 | 0.096 | 0.128 | 0.156 |

| Comprehensive | 0.005 | 0.008 | 0.014 | 0.021 | 0.030 | 0.045 | 0.062 |

| Home | 0.024 | 0.032 | 0.048 | 0.064 | 0.084 | 0.130 | 0.183 |

6.2 Estimation Results

6.2.1 The basic ARC Model: Collision

We start by presenting estimation results in a simple setting where the only choice is the collision deductible and observable demographics do not affect preferences. To execute our estimation procedure we set , which is conservative \@BBOPcitep\@BAP\@BBN(see Barseghyan et al., 2016)\@BBCP. We ex post verify that this does not affect our estimation by checking that the density of the estimated distribution is close to zero at the upper bound. We approximate non-parametrically through a mixture of Beta distributions. In practice, however, both AIC/BIC criteria indicate that a single component is sufficient for our analysis, resulting in a total of seven parameters to be estimated. We let the data speak to the identity of the always-considered alternative.181818In fact, the estimation is run under the Coin Toss completion rule that nests the possibility that any alternative can be always considered. The data chooses .

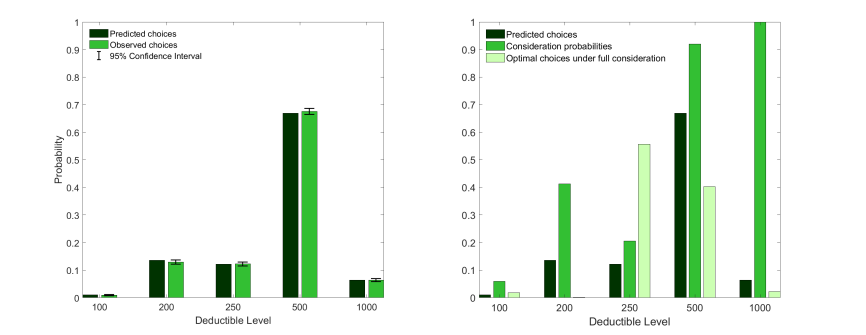

The estimated distribution and consideration parameters are reported in Table E.1. As the first panel in Figure 1 shows, the model closely matches the aggregate moments observed in the data. The second panel in Figure 1 illustrates side-by-side the frequency of predicted choices, consideration probabilities, and the distribution of households’ first-best alternatives (i.e., the distribution of optimal choices under full consideration). Predicted choices are determined jointly by the preference induced ranking of deductibles and by the consideration probabilities: Limited consideration forces households’ decision towards less desirable outcomes by stochastically eliminating better alternatives. The two highest deductibles ( and ) are considered at much higher frequency (1.00 and 0.92, respectively) than the other alternatives, suggesting that households have a tendency to regularly pay attention to the cheaper items in the choice set. Yet, the most frequent model-implied optimal choice under full consideration is the deductible, which is considered with low probability.

In this application, assuming full consideration leads to a significant downward bias in the estimation of the underlying risk preferences. To see why, consider increasing the consideration probabilities for the lower deductibles to the same levels as the deductible. Holding risk preferences fixed, the likelihood that the lower deductibles are chosen increases and therefore the higher deductibles are chosen with lower probability. Average risk aversion must decline to compensate for this shift. This is exactly the pattern we find when we estimate a near-full consideration model. In particular, we find that average risk aversion decreases by about 32% from 0.0037 to 0.0025 when all consideration parameters equal 0.9999.191919We cannot assume that all consideration probabilities are equal to one, since the deductible is never the first best under full consideration and is chosen with positive probability. To put these numbers into context, a DM with risk aversion equal to 0.0037 is willing to pay to avoid a loss with probability 0.1, while a DM with risk aversion equal to 0.0025 is only willing to pay to avoid the loss.

The basic ARC model’s ability to match the data extends also to conditional moments. The first two panels of Figure 2 show observed and predicted choices for the fraction of households facing low and high premiums, respectively, and the next two panels are for households facing low and high claim probabilities.202020Low and high groups here are defined as households whose claim rate (or baseline price) are in the first and third terciles, respectively. Finally, the last two panels display households who face both low claim probabilities and high prices and vice versa. It is transparent from Figure 2 that the model matches closely the observed frequency of choices across different subgroups of households facing a variety of prices and claim probabilities, even though some of these frequencies are quite different from the aggregate ones.

The ARC model’s ability to violate Generalized Dominance is key in matching the data. In our dataset, because of the pricing schedule in collision, the is never-the-first best among for of all households and of households who have chosen the deductible. It costs the same to get an additional of coverage by lowering the deductible from to as it does to get an additional of coverage by lowering the deductible from to . If a household’s risk aversion is sufficiently small, then it prefers the deductible to the deductible. If, on the other hand, the household’s level of risk aversion is such that it would prefer the deductible to the deductible, then it would also prefer getting twice the coverage for the same increase in the premium. That is, for any level of risk aversion, the deductible is dominated either by the deductible or by the deductible.212121This pattern is at odds not only with EUT but also many non-EU models \@BBOPcitep\@BAP\@BBN(Barseghyan et al., 2016)\@BBCP. Yet, overall the deductible is chosen roughly as often as the and deductibles combined. More so, for certain sub-groups the deductible is chosen much more often than the and deductible combined. It follows that a model satisfying Generalized Dominance cannot rationalize these choices.

Next we relax the assumption that demographic variables, , do not influence risk preferences. In particular, conditional on demographics, preferences are distributed Beta(), where , yielding a conditional mean preference value . The details of this step and the results are reported in Appendix E. Both consideration and preference estimates remain close to those reported above.

6.2.2 Proportionally Shifting Consideration

We estimate the model with proportionally shifting consideration where the preference distribution and function may depend on demographic variables (Table E.2). Motivated by the findings of the previous section, we assume that the cheapest/riskiest alternative is always considered. The consideration probability of the remaining alternatives is equal to , where , , and is positive. We continue to assume that preferences are distributed Beta().

The estimated average value of is , with the CI of . When , a risk-neutral DM considers each of the safer alternatives less often than does an extremely risk averse DM. The estimated value of is . This implies that as the risk aversion parameter increases from 0 to its estimated average median value of , consideration probability of the safer alternatives increases by , and it is essentially flat after that rising by an additional as risk aversion reaches its upper bound.

6.2.3 The Mixed Logit Random Utility Model

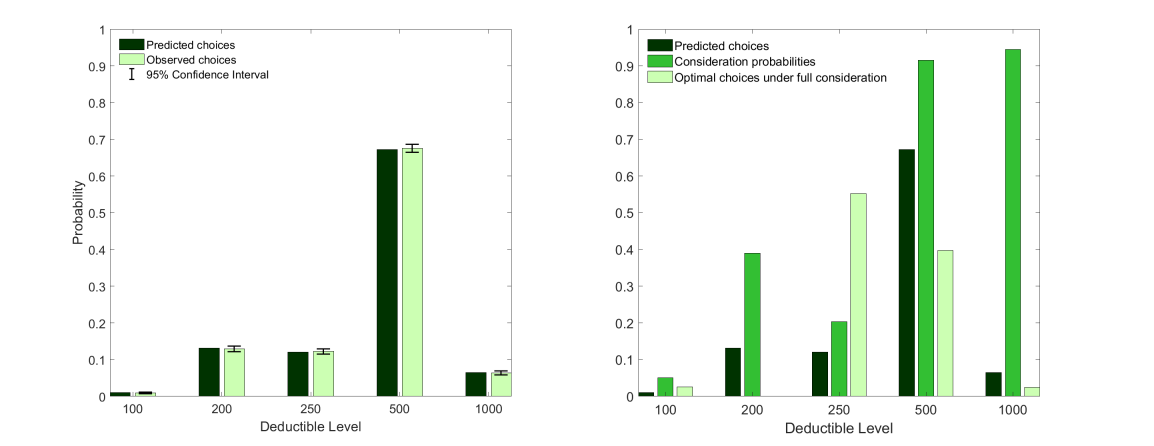

As in the case of the ARC model, we assume that is Beta distributed on , where . The Mixed Logit satisfies the Generalized Dominance and smoothly spreads households’ choices around their respective first bests. Consequently, it cannot match the observed distribution and, in particular, is unable to explain the relatively high observed share of the deductible. Table E.3 reports the estimation results and Figure E.3 compares the observed distribution of choices to the predicted choices. The predicted distribution is a much poorer fit relative to the ARC model. In fact, the \@BBOPcite\@BAP\@BBNVuong (1989)\@BBCP test soundly rejects (at 1 level) the Mixed Logit in favor of the ARC model.

6.2.4 The ARC Model: All Coverages

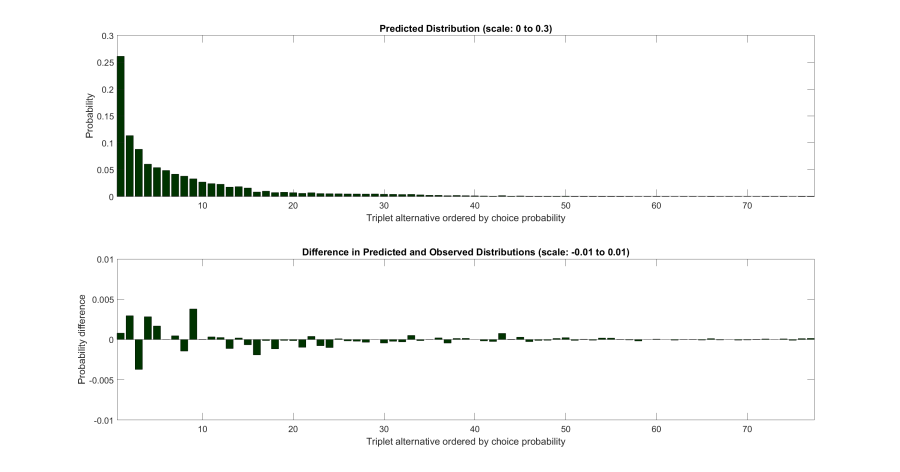

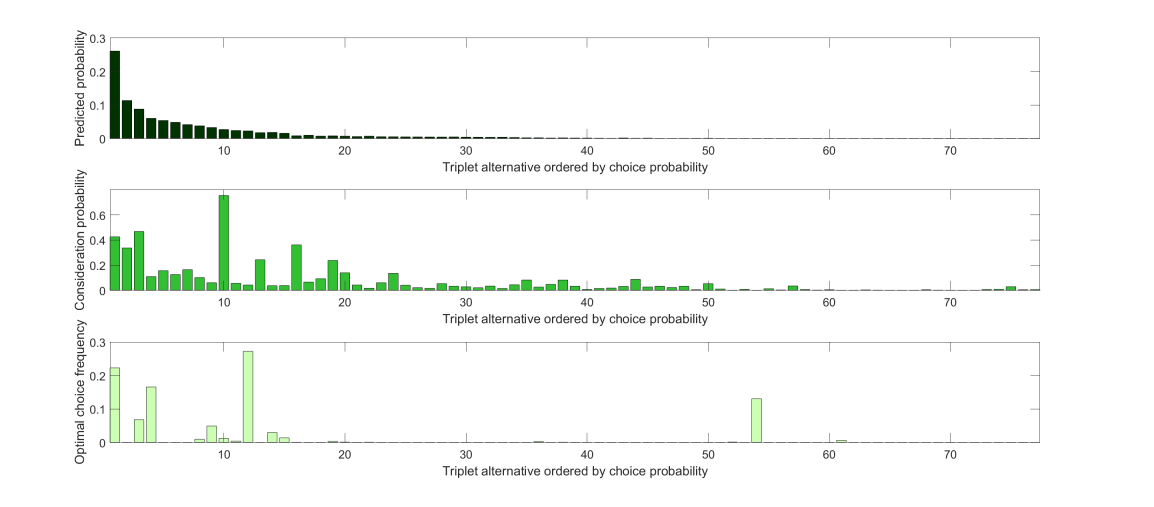

We now proceed with estimation of the full model. We assume that households’ consideration sets are formed over the entire deductible portfolio. There are 120 possible alternative triplets , each having its own probability of being considered. This model is flexible as it nests many rule of thumb assumptions such as only considering contracts with the same deductible level across the three contexts or only considering contracts with a larger collision deductible than comprehensive deductible. Figure 3 and Table E.4 present estimation results. The first panel of the figure shows the predicted distribution of choices across triplets, ranked in descending order by observed frequencies. The second panel plots the differences between predicted and observed choice distributions. Clearly, the predicted distribution is close to the observed distribution.

The largest difference between the predicted and observed shares equals percentage points, which is for the () triplet that is chosen by of the households. The integrated absolute error across all triplets is . In our data, 43 out of 120 triplets are never chosen (these are omitted from Figure 3). As discussed in Section 4, the likelihood maximization implies that the consideration probabilities for these triplets must be zero, so their predicted shares are zero. Hence, the likelihood maximization routine is faster and more reliable as we do not need to search for for these alternatives.

Another virtue of the ARC model is that it effortlessly reconciles two sides of the debate on stability of risk preferences \@BBOPcitep\@BAP\@BBN(Barseghyan et al., 2011; Einav et al., 2012; Barseghyan et al., 2016)\@BBCP. On the one hand, households’ risk aversion relative to their peers is correlated across lines of coverage, implying that households preferences have a stable component. On the other hand, analyses based on revealed preference reject the standard models: under full consideration, for the vast majority of households one cannot find a level of (household-specific) risk aversion that justifies their choices simultaneously across all contexts. Limited consideration allows the model to match the observed joint distribution of choices, and hence their rank correlations.

The estimated risk preferences are similar to those estimated with collision only data, although the variance is slightly smaller. The triplet considered most frequently is the cheapest one: (). Its consideration probability is 0.76, while the next two most considered triplets are ($500, $500, $1000) and ($500, $500, $500). These are considered with probability 0.47 and 0.43, respectively. Overall, there is a strong positive correlation between the consideration probability and the sum of the deductibles in a given alternative.

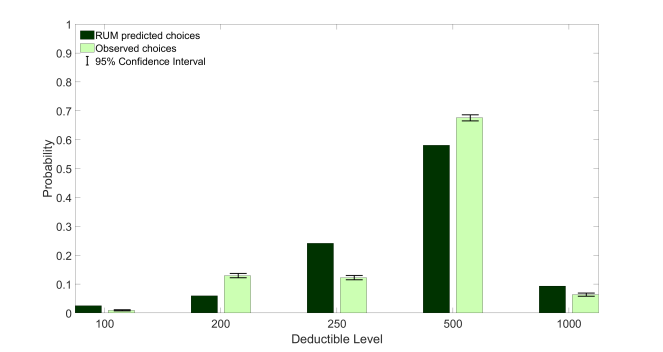

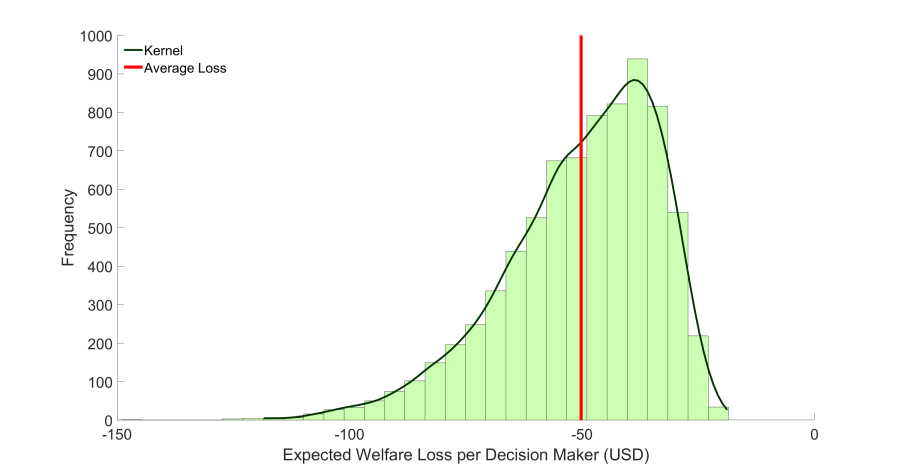

We summarize once more the computational advantages of our procedure. First, estimation of our model remains feasible for a large choice set.222222In our setting, it is feasible to estimate an additive error RUM assuming the DMs consider each deductible triplet as a separate alternative (Figure E.4 and Table E.5). As the figure shows, the failure to match the data is evident. The Vuong test formally rejects it in favor of the ARC model. Second, the model’s parameters grow linearly with the size of the choice set – one parameter per an additional alternative. Third, enlarging the choice set does not call for new independent sources of data variation. For example, in our model whether there are five deductible alternatives or one hundred twenty does not make any difference either from an identification or an estimation stand point: with sufficient variation in and/or , the model is identified and can be estimated. As a final remark, once the model is estimated, one can compute the average monetary cost of limited consideration. In our data it is (see Appendix C).

7 Discussion

The literature concerned with the formulation, identification, and estimation of discrete choice models with limited consideration is vast. However, to our knowledge, there is no previous work applying such models to the study of decision making under risk, except for the contemporaneous work of \@BBOPcite\@BAP\@BBNBarseghyan, Coughlin, et al. (2019)\@BBCP. In particular, this paper is the first to exploit the SCP for identification purposes. As a result, several fundamental differences emerge between our work and existing papers. First, we achieve identification in the most challenging case where there is a single excluded regressor that affects the utility of all alternatives.232323This setting is common in insurance markets, see, e.g.,\@BBOPcite\@BAP\@BBNCohen & Einav (2007); Einav et al. (2012); Sydnor (2010); Barseghyan et al. (2011, 2013); Handel (2013); Bhargava et al. (2017)\@BBCP. Second, we allow for consideration to depend on preferences. Third, with alternative-specific excluded regressors, this dependence can be essentially unrestricted and can be combined with dependence of consideration on (some of) the excluded regressors. Fourth, we scrutinize the large support assumption, show why it may be necessary, and when and how it is possible to make progress when it is not satisfied. Fifth, our approach comes with an easy to implement and computationally fast estimation strategy. Finally, we make a contribution specific to the study of decision making under risk by proposing a model that is immune from \@BBOPcite\@BAP\@BBNApesteguia & Ballester (2018)\@BBCP criticism and features two sources of unobserved heterogeneity – risk aversion and limited consideration – whose distributions are identified. More generally, the paper establishes that, as long as the DMs’ preferences satisfy the SCP, allowing for limited consideration does not hinder the model’s identifiability or applicability. Hence, we view our framework as a stepping stone for studies of consumer behavior in markets where limited consideration may be present \@BBOPcitep\@BAP\@BBN(one example is Coughlin, 2019, who builds on our framework to study consumer choice in Medicare Part D markets)\@BBCP.

Papers that allow for limited consideration or more broadly for choice set heterogeneity can be classified in four groups. The first relies on auxiliary information about the composition or distribution of DMs’ choice sets, such as brand awareness \@BBOPcitep\@BAP\@BBN(e.g., Draganska & Klapper, 2011; Honka & Chintagunta, 2017)\@BBCP or search activity \@BBOPcitep\@BAP\@BBN(e.g., Honka & Chintagunta, 2017; De los Santos et al., 2012; Kim et al., 2010; Honka et al., 2017)\@BBCP.242424For canonical cites see, e.g., \@BBOPcitet\@BAP\@BBNRoberts & Lattin (1991)\@BBCP and \@BBOPcitet\@BAP\@BBNBen-Akiva & Boccara (1995)\@BBCP. We do not require such information.

The second group attains identification via two-way exclusion restrictions, i.e., by assuming that some variables impact consideration but not utility and vice versa. A well-known example of this approach is \@BBOPcitet\@BAP\@BBNGoeree (2008)\@BBCP, who posits that advertising intensity affects the likelihood of considering a computer, but does not impact consumer preferences, while computer attributes such as CPU speed affect preferences but not consideration (see also \@BBOPcitet\@BAP\@BBNvan Nierop et al. (2010)\@BBCP and \@BBOPcitet\@BAP\@BBNGaynor et al. (2016)\@BBCP). \@BBOPcitet\@BAP\@BBNHortaçsu et al. (2017)\@BBCP create an exclusion restriction by exploiting the dynamic aspect of consumer choice.252525Time variation is used also in \@BBOPcitet\@BAP\@BBNCrawford et al. (2020)\@BBCP, who show that with panel data and preferences in the logit family, point identification of preferences is possible, without any exclusion restrictions, under the assumption that choice sets and preferences are independent conditional on observables and with restrictions on how choice sets evolve over time. These restrictions enable the construction of proper subsets of DMs’ true choice sets (‘sufficient sets’) that can be utilized to estimate the preference model. The consumer’s decision to consider alternatives to her current service provider is a function of (her experiences with) the last period provider but not her next period provider (see also \@BBOPcitet\@BAP\@BBNHeiss et al. (2016)\@BBCP). In contrast, we achieve identification with as little as one common excluded regressor and a single cross section.