Options on CPPI with guaranteed minimum equity exposure

Abstract

In the present paper we provide a two-step principal protection strategy obtained by combining a modification of the Constant Proportion Portfolio Insurance (CPPI) algorithm and a classical Option Based Portfolio Insurance (OBPI) mechanism. Such a novel approach consists in assuming that the percentage of wealth invested in stocks cannot go under a fixed level, called guaranteed minimum equity exposure, and using such an adjusted CPPI portfolio as the underlying of an option. The first stage ensures to overcome the so called cash-in risk, typically related to a standard CPPI technique, while the second one guarantees the equity market participation. To show the effectiveness of our proposal we provide a detailed computational analysis within the Heston-Vasicek framework, numerically comparing the evaluation of the price of European plain vanilla options when the underlying is either a purely risky asset, a standard CPPI portfolio and a CPPI with guaranteed minimum equity exposure.

Keywords: portfolio insurance, CPPI, OBPI, Option on CPPI, stochastic volatility, guaranteed minimum equity exposure.

JEL classification: C63, G11, G13

AMS classification: 91G20, 91G60, 65C30, 68U20

1 Introduction

During recent years, financial markets have been mainly characterized by the consequences of the great financial crisis happened in 2008 and, afterward, by the linked increasing of equity markets and related decreasing of interest rate levels around the world, until a significant market drop in 2018. While interest rate levels still remained on record lows, volatility in the market increased again significantly in the last 12 months.

Such a market framework costitutes a big challenge for institutional as well as for retail investors, who are looking for an equity market participation plus a downside protection.

The literature has tried to solve this puzzle in terms of portfolio insurance strategies, at least starting from the early 70s of the last century, see, e.g., [6, 10, 11, 17], and references therein. Roughly speaking, a portfolio insurance strategy is a protection blueprint, based on the definition of a fixed threshold such that the terminal portfolio value always lies above it. This approach bypasses the risk of the actual return being below the expected return, or the uncertainty about the magnitude of that difference, see, e.g., [18, 22].

The portfolio insurance strategies were first introduced in [21], after the collapse of stock markets (the New York Stock Exchange’s Dow Jones Industrial Average and the London Stock Exchange’s FT 30, see, e.g., [14]) which implied the pension funds withdrawal. In particular, the authors noted ex-post that the presence of an insurance of the above mentioned type of risk could have convinced the investors not to leave the market, guarantying them later the opportunity to take advantage of the rise of the same, an event that really happened just a couple of years later. In this context, the insurance can be interpreted as a put option on the whole portfolio.

Portfolio insurance strategies can be pigeonholed into three different classes, see, e.g., [25, 26]: the option-based strategies, the option-duplicating strategies and the derivative-independent strategies. A technical analysis, also in terms of performance evaluation, of such strategies can be found in [12], where bull, bear and no-trend markets are considered, while an overview of portfolio insurance strategies, along with their possible connections with financial instability, is provided in [23], and interesting numerical insights have been reported in [20].

An early approach, related to the first class of strategies, is the so called Option-Based Portfolio Insurance (OBPI) method, see, e.g., [8], which consists of buying a zero-coupon bond with maturity equal to the investment time horizon plus an option written on the portfolio risky asset. As an alternative, in [3] a minimum-cost portfolio insurance strategy is presented. Here, the idea is to solve a portfolio optimization problem in incomplete markets by minimizing costs of a portfolio under the constraint that the payoff is greater than the insured one, avoiding losses and capturing gains.

The option-duplicating strategy is an approach in which the option is replicated with a self-financing strategy, in order to overcome the lack of liquid options for long maturities.

It is worth to mention that low interest rate levels are reducing the available risk budgets significantly, forcing practitioners to rethink at how to optimize portfolios’ design by offering a sustainable equity market participation plus a capital protection of the initial investment. In this direction, one choice consists in considering dynamic risk management tools to protect portions of the initial investment by dynamically allocating both in risky and riskless assets, based on available portfolio risk budgets. In this framework the Constant Portfolio Protection Insurance (CPPI) is one of the most used approaches, see, e.g., [4, 7, 9, 10, 19, 24, 27], and references therein. The CPPI method is obtained by rebalancing an initial portfolio at each observation time, evaluating a present value of the aspired capital protection and then investing the available risk budget times a market-depending multiplier into risky assets, while investing the remaining part of the portfolio in time-congruent risk-free assets. An interesting analysis of portfolio insurance strategies, including the CPPI methodology, is provided in [5], where the authors exploit Value-at-Risk, Expected Shortfall and stochastic dominance to measure the portfolio performance of the above-mentioned techniques.

By assuming that the CPPI portfolio evolves according to a Markov process, in [24] the authors focus on a discrete-time CPPI-based portfolio allocation method. More recently, a machine learning approach to determine the value of the parameters used to evaluate the correct proportion of wealth to be invested in stock is given in [15].

Despite a significant simplicity and a remarkable ease of implementation, the CPPI strategy suffers a fundamental drawback represented by the risk that, after a severe market draw-down, the risk budget erases with a consequent reduction to zero of the market participation, hence potentially allowing for what practitioners call the cash-in event. To overcome the latter scenario, most of the practitioners resort to different routines, such as using an intertemporal risk budgeting which allows the full use of the available risk budget over time. Alternatively, they adopt the multiplier related to market volatility. However, while both methods can reduce the probability of cash-in event to happen, they cannot guarantee to avoid it within the traditional CPPI approaches.

To close this gap, we introduce an innovative method consisting in a combination of a CPPI strategy and an OBPI one. In particular, we overcome two different problems by annihilating the cash-in risk, simultaneously ensuring some participation in upside markets. Our solution is based on the following: starting from the CPPI portfolio dynamics, a threshold is included in the proportion of wealth invested in stocks. Such a threshold is dubbed guaranteed minimum equity exposure (GMEE) and represents the minimum investment value in the risky asset. The portfolio obtained through the previous mechanism can be used as underlying of an option.

We would like to highlight that, although such an approach has been selectively used in practice, no rigorous mathematical treatment of it has been provided up to now, at least to the best of our knowledge. Therefore, our work represents the first rigorous analytical treatment toward this direction. Even if within well establlished literature the aforementioned topics have been already described, such analysis have been separately provided. In particular, the analysis of factors that can potentially lead to gap risk in portfolio insurance framework, mainly taking into account the asset price behavior and the trading frequency, is described in [13]. Conversely, we refer to [16], resp. to [1], for related studies on options on a standard CPPI logic, resp. on options linked to the so called VolTarget strategies.

In this sense, the present paper can be considered the first attempt to combine the above mentioned topics in a unified framework. To better explain the concreteness as well as the goodness of our approach, we shall show how our proposal would have worked in the past, providing some historical simulations of structured products with CPPI and CPPI-GMEE. We scrutinize both versions of the CPPI logic in different market scenarios, to better appreciate the sensitivities of the strategies. Such an investigation enables to figure out the behaviour of the risk–return profile, as well as of the asset allocation in different market cycles. Thereafter, we also determine the prices of the corresponding CPPI options for different set of product levels for a market model where both the volatility and the interest rate parameters are assumed to be stochastic processes.

The paper is structured as follows: in Section 2 we recall the key concepts related to CPPI and OBPI strategies and we introduce the new CPPI–GMEE approach in more details; in Section 3 we compare the CPPI versus the CPPI with guaranteed minimum equity exposure approaches, mainly exploiting historical simulations; in Section 4 we provide numerical experiments to show the differences of plain vanilla options, options on CPPI and options on CPPI–GMEE; in Section 5 we recap results obtained in the paper also giving an outlook to related future developments.

2 OBPI-CPPI hybrid portfolio allocation strategy

Our idea is to introduce a principal protection strategy, which is a mixture of an OBPI and a CPPI approach. As a result of the merge between two portfolio insurance strategies, our proposal must first consider that the investor can not suffer losses related to the amount of her initial wealth. For this reason, in the following we will extensively make use of the so called protection level (PL), defined as the percentage of the initial capital guaranteed at maturity.

Besides, we will take into account the following key points:

-

•

we invest a significant portion of the portfolio in time-congruent zero coupon bonds following a classical OBPI approach. This assures to achieve the capital protection at maturity;

-

•

the remaining part of the portfolio is put into an exotic call option linked to a CPPI strategy, where the CPPI portfolio has an equity index as risky asset. This provides the participation in the equity market;

-

•

we adjust the CPPI algorithm as underlying of the option in such a way that at any time the equity exposure will not fall below a predefined level. This helps to avoid the occurrence of the well known cash-in risk.

Before going into details about the concrete realization of the above described method, let us first describe the standard OBPI and CPPI portfolio allocation mechanisms. Throughout the paper, we let be the time horizon of the investment, while is a filtered probability space, with and we assume that all the processes introduced in what follows are -adapted.

We consider a market consisting of a risky asset whose dynamics will be specified later on, and a risk-less asset such that

2.1 The OBPI portfolio allocation strategy

The OBPI strategy is a portfolio insurance procedure characterized by ensuring a minimum terminal portfolio value, see, e.g., [29].

According with standard literature, see, e.g., [8], we define the OBPI portfolio process with initial value as follows

where represents the number of riskless assets acquired by the investor to protect the capital, is the call option at time , written on , having strike price and maturity , while is the number of calls which can be purchased at time given the risk budget, see, e.g., [2].

The OBPI approach is said to be static in the sense that no trading occurs in so that the unique portfolio values we are interested in are

therefore, at maturity, the client gets the capital plus times any positive performance of greater than In case and the client gets exactly the performance of the underlying asset.

2.2 The CPPI portfolio allocation strategy

In order to define the CPPI portfolio process we begin by specifying the so called floor representing the lowest acceptable value of the portfolio. In particular, we consider the process with dynamic

and initial value where is the fixed amount of capital guaranteed at maturity.

We define the process with initial value representing the portfolio value associated to the CPPI strategy, namely

| (2.1) |

where resp. represents the portfolio proportion invested in the risky, resp. in the riskless asset.

By assuming that the portfolio strategy is self-financing, the dynamics of the CPPI portfolio can be easily obtained from eq. (2.1) as follows

| (2.2) |

Moreover, we assume that is, the guaranteed return must be less than the market interest rate.

Since we are interested in determining the optimal allocation, then, for all , we evluate the excess of the portfolio value over the floor dubbed cushion, as

| (2.3) |

so that

The investment in stock represents the exposure, which is given by

| (2.4) |

the constant being a multiplier representing the factor by which the risk budget is amplified, giving rise to the risky asset.

Remark 2.1.

Let us note that since we are dealing with a dynamic leverage adjustment mechanism, if we consider a general setting, the multiplier can be represented in terms of a suitable continuous function depending on different model parameter, see, e.g., [27]. While, for the sake of simplicity, in our case we will consider a constant multiplier where ONR factor represents the Over-Night risk of the risky asset. The market practice usually assumes for a given equity index that serves as underlying, implying that

2.3 The CPPI with Guaranteed Minimum Equity Exposure

As regards the evaluation of the percentage of wealth to be invested in the risky asset, eq. (2.4) gives

| (2.5) |

by assuming -a.e.

In particular, eq. (2.5) implies that the investment in the risky asset might be potentially unbounded. To limit such a potential leverage effect in the optimal allocation, the market practice suggests to introduce the so called maximum leverage factor in the equity weights such that

| (2.6) |

Motivated by some regulatory constraints, see, e.g., [28] , is tipically setted to , or

However, it may happen that, due to sudden events, the price of the risky asset, on which the value of the CPPI portfolio depends, is significantly reduced. As a consequence, the value of the portfolio will be lower than the bound assigned through the floor, and from that moment on the manager will be able to allocate wealth only in the risk-less security until the contract expires. This situation is referred to as cash-in risk.

3 Historical simulation of structured products with CPPI vs. CPPI with guaranteed minimum equity exposure

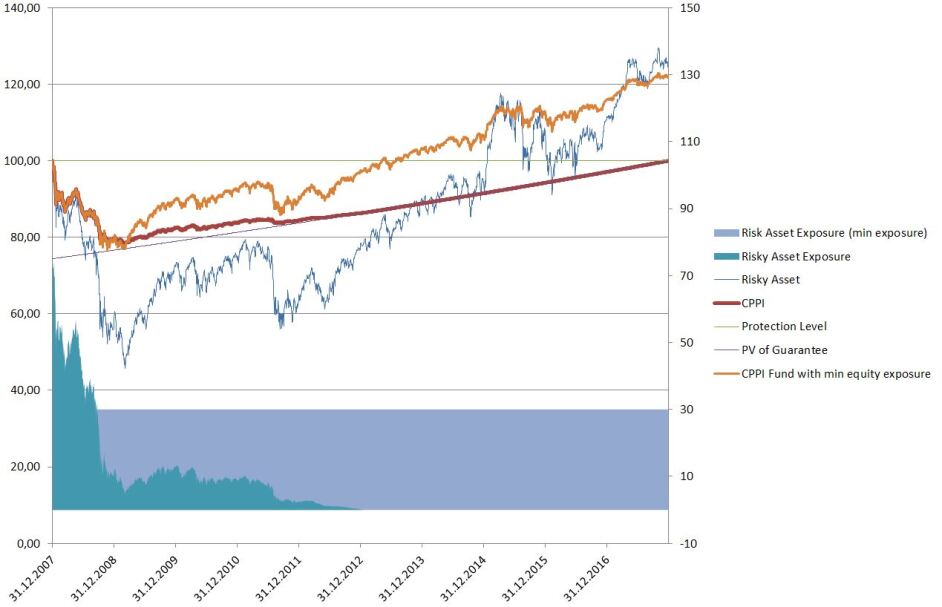

In order to verify weather the presence of the GMEE threshold permits to dodge cash-in events, in this section we simulate CPPI portfolio allocation strategies, with and without guaranteed minimum equity exposure, linked to European equity markets. To capture the sensitivities of the proposed strategies, we propose two different scenarios. In the first case we consider , in the time interval 2007 to 2017, whereas, in the second example, we analyze the case, referring to the time period 2000 to 2010.

The 100%-protection case.

The CPPI simulation has been conducted assuming the following

-

•

the underlying is given by a Euroland large and mid cap equity index as risky asset between 31st of December 2007 and 29th of December 2017;

-

•

the CPPI mechanism should protect of the initial investment after 10 years. For the sake of simplicity, we assume a constant risk-free rate of since the risk-free rates in 2008 were close to such a level. The latter would have also determined the risk budget of the associated strategy. Moreover, starting with a new CPPI within today’s financial scenario, hence taking into consideration interest rates’ levels near to zero, the related risk budget would be also close to zero. In this framework, one can either extend the investment time horizon, to benefit from higher interest rates deriving from considering related longer maturities, or set up the investment w.r.t. a lower protection level, e.g. at instead of

-

•

according to the CPPI methodology, we choose a multiplier and a maximum leverage factor of , while the guaranteed minimum equity exposure is set to

In Fig. 3.1 we report the obtained results to better motivate our key idea.

The left hand axis gives the performance of the risky asset, of a standard CPPI approach and a CPPI approach with guaranteed minimum equity exposure, also providing the present value of the guarantee in percentage of the initial investment. The right hand axis shows the risky asset exposure over time for a CPPI and a CPPI–GMEE portfolio in percentage of the overall portfolio allocation.

The key findings can be summarized as follows. Looking at the risky asset itself, we see that the considered market index significantly lost in value between 2007 and March 2009. In fact, during this period the index lost close to of its initial value. After that, the equity index recovered nicely and over the full 10 year horizon the index generated a positive performance of more than Nevertheless, from the point of view of a conservative investor, an equity index might be too volatile. Focusing on a traditional CPPI allocation logic, we can see that the red line gives the performance of a CPPI strategy linked to this equity index as risky asset, exploiting the parameters mentioned above. For the sake of simplicity, we do not consider transaction costs.

The standard CPPI has an initial exposure to the risky asset of more than Due to the extreme losses in the risky asset, the risk budget quickly decreases, and the CPPI needs to reduce the risky asset exposure to less than after 10 months. The CPPI approach itself can limit the losses successfully compared to the pure risky asset investment in this time, but it cannot participate in any upwards markets afterward. After some further volatilities in the risky asset over the next 4 years, we can see that the risky asset allocation drops to zero at the end of 2012, hence no market participation exists afterward. Overall, the CPPI can achieve but it cannot benefit from the overall positive return in the equity market. The CPPI with guaranteed minimum equity exposure starts with the same risky asset allocation as the standard CPPI. Also this CPPI approach is forced to reduce its risky asset exposure significantly due to negative risky asset performance. Nevertheless, by definition, the risky asset exposure never drops below the predefined threshold of Therefore, the proposed CPPI alternative approach can benefit from rising equity markets again and over the full remaining life time, the CPPI with guaranteed minimum equity exposure achieves a return which is quite comparable to the pure risky asset.

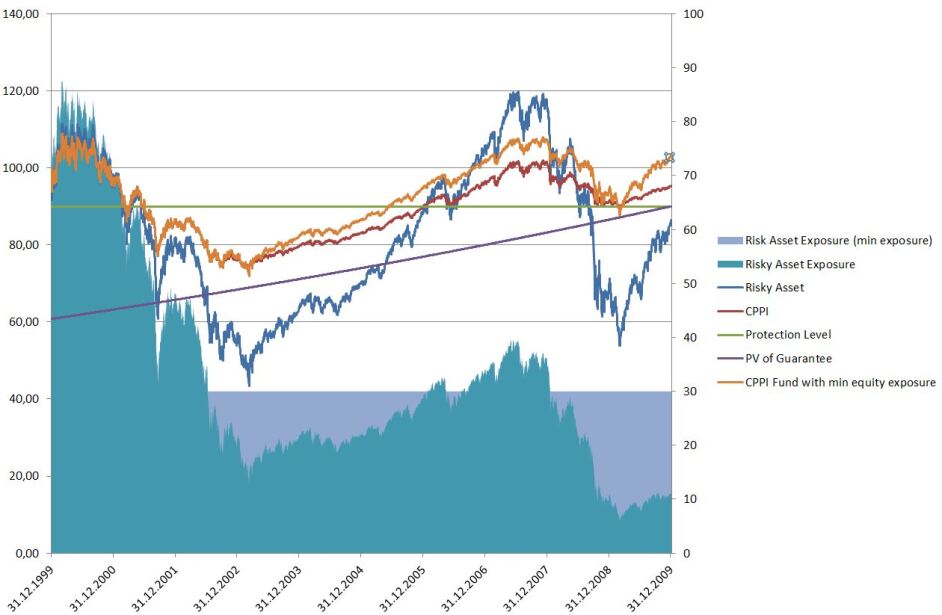

The 90%-protection case.

For the CPPI has been conducted assuming the following

-

•

to hold a Euroland large and mid cap equity index as risky asset, considered between the 31st of December 1999 and the 31st of December 2009;

-

•

the considered CPPI mechanism should protect of the initial investment after 10 years, and, for the sake of clarity, we assume a constant risk-free rate of

-

•

within the CPPI we choose conservative multiplier , capping the maximum leverage factor at . The guaranteed minimum equity exposure is set at and we do not consider any transaction costs.

As can be seen in Fig. 3.2, the risky asset during this period of time starts positively, then achivieng a return of close to , in the first year. But, between 2000 and 2002, the equity index loses about of its initial value. Then, it well recovers until mid of 2007, when the worldwide financial crisis causes new severe losses. Therefore, after 10 years, the index loses about of its initial value.

The standard CPPI linked to this index has an initial exposure of about as a result of higher risk budget given the lower protection level of just and a higher risk-free rate of compared to the previous case. When the equity index increases initially in value then the exposure of the standard CPPI increases to close to But, during following years, the exposure is significantly reduced to less than in 2003. When markets are recovering, also the risky asset exposure increases to roughly but during the financial crisis it falls below in early 2009. Therefore, after 10 years, the exposure is at and the performance of the CPPI ends with namely it could achieve a higher return than the index itself and than the aspired capital protection level of but still the investor made a loss.

The CPPI with guaranteed minimum equity exposure shows initially a similar behavior like the traditional CPPI. It also starts with an equity exposure of around which increases to even and then falls to the guaranteed minimum equity exposure of in 2002. The equity exposure remains there, between 2005 and 2007 it increases again to ca. During the financial crisis it drops back again, but, by definition, not below the minimum exposure of As a result, the CPPI with guaranteed minimum equity exposure could limit losses from equity markets in 2001 and 2002, and also during the financial crisis. Nevertheless, it could especially benefit from recovering markets more than a standard CPPI. After 10 years the new CPPI approach generated a positive return of more than Moreover, it could achieve and it could generate a much better risk-return profile than a pure equity investment.

4 Numerical Pricing of Options on CPPI with guaranteed minimum equity exposure

By eq. (2.7) we have that, even in case of a severe market drop, the equity participation will never go below , while, at the same time it would mean that this adjusted CPPI allocation implemented in a real portfolio might not be able to protect the invested capital.

This justifies the second step of our proposal, namely our CPPI mechanism is always applied in an OBPI-based portfolio approach, in which the call option is linked to the CPPI allocation logic with guaranteed minimum equity exposure. Thus, we now consider options on CPPI and CPPI–GMEE strategies. More precisely, in what follows we provide the mathematical setting of our options on CPPI-GMEE as well as in depth numerical analysis related to the its implementation in the option pricing context.

4.1 The financial model

Assuming there exists a measure with respect to the filtered probability space consider a portfolio allocation strategy in which a financial agent invest his wealth in one riskless asset, e.g. a bond, and in one risky asset, e.g., an equity index, over a time interval More precisely, we take a risk-free asset whose dynamics reads as follows

| (4.1) |

with a return at time and a risky asset such that

| (4.2) | ||||

| (4.3) | ||||

| (4.4) |

The stochastic processes are three correlated -adapted Wiener processes, with

where , resp. represents the volatility, resp. the interest rate, stochastic process, with positive speed of reversion , resp. , long-term mean levels , resp. , and variance , resp. .

In such an economy, we consider a European contingent claim with maturity whose payoff is a real-valued function The payoff function may either depend just on the final value of the underlyings, namely and or relies upon the whole underlying path over In the former case we refer to plain vanilla call/put options, otherwise we might consider path-dependent options, e.g., considering options on CPPI.

At any rate, we can define the price of the contingent claim as

| (4.5) |

where is the conditional expectation taken w.r.t. the initial filtration to which the Wiener processes have been defined to be adapted and under the risk-neutral measure

Equivalently, we may consider a contingent claim with maturity whose payoff is a real-valued function relying upon the CPPI portfolio strategy. More precisely, we assume that the underlying asset for is measured in units of the CPPI strategy, instead of units of stock, see, e.g., [1, 16] for further details. In this case, the price of the contingent claim , at time reads as follows

| (4.6) |

4.2 Options on CPPI and CPPI-GMEE

In this section we are going to compare At-The-Money (ATM) European call/put option prices, evaluated both in the standard case, i.e. when the underlying is the stock dynamics, and when the underlying equals the CPPI portfolio allocation strategy, the second type of computations has been conducted both with and without Guaranteed Minimum Equity Exposure. Let us assume the following:

-

•

for normal CPPI-based strategies, the at the end of the option life time, the multiplier is , while the Maximum Leverage is equal to

-

•

for options linked to CPPI strategies with guaranteed minimum equity exposure, the protection level, the multiplier and the Maximum Exposure are as in the previous case, while the guaranteed minimum equity exposure is

We assume no transaction costs and dividends are directly reinvested into the strategy. We also assume that all the CPPI strategies are re-allocated each business day. From a practical perspective, this implies that the manager assumes that trading actions are discretized in time, namely according to a subdivision of the following type , where , represent fixed trading dates, so that we have

| (4.7) |

with initial condition

Remark 4.1.

There does not exist a fixed rule to determine the time grid used for rebalancing the CPPI portfolio. In the market practice often a so called trading filter is applied, namely, as long the real allocation deviates not significantly to the theoretical CPPI allocation, no trading happens. This is to avoid trading on noise and also to reduce transaction costs.

Overall a weekly allocation is probably a reasonable assumption. In case of financial distress the rebalancing frequency can increase, and managers might have to trade daily or, in extreme cases, even two or three times a day.

Concerning the numerical values for the parameters, we consider four time horizons (measured in years) an initial interest rate and an initial volatility level The remaining parameters are described in Table 4.1.

| Vasicek model | Heston model | |

|---|---|---|

| Long-run mean | ||

| Rate of mean reversion | ||

| Volatility | ||

| Correlation |

4.2.1 Comparison of call options

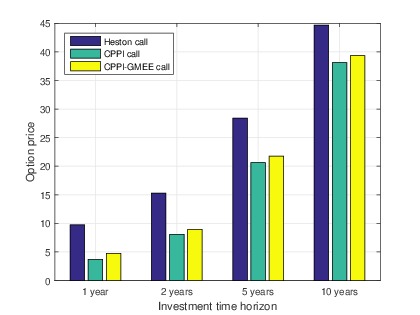

In what follows, numerical results for the CPPI strategy exploited as European call option underlying are provided. To better understand sensitivities, we compare the values of a European call option when the underlying is a pure risky asset, within the Vasicek-Heston model, the CPPI strategy, and the CPPI with guaranteed minimum equity exposure, respectively. In Fig. 4.1 we report the call option price for different maturities in each of the aforementioned scenarios.

Considering an initial volatility level of and an initial interest rate level of we observe that the price obtained by taking the pure risky asset as the derivative’s underlying results is the most expensive strategy. Instead, the option pricing with respect to the CPPI strategy leads to a reduction of the option price. As expected, the CPPI with guaranteed minimum equity exposure leads to higher prices rather than the simple CPPI, this due to the cost we pay for having fixed a lower threshold of the risky asset exposure at

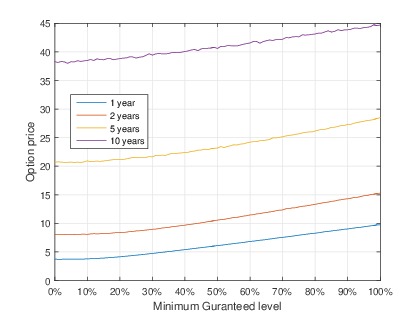

In order to stress the role of the guaranteed minimum exposure, we study the call option value as a function of the parameter for different maturity levels.

In Fig. 4.2 we observe that the option price increases as the minimum guarantee threshold raises.

The lowest price is reached when the minimum guaranteed exposure is zero, which corresponds to the case of an usual CPPI strategy as underlying of the option. The case coincides with the plain vanilla call option, as in this case the allocation to risky asset is always 100%. Since we assumed the effect of a rising option price with a rising minimum guaranteed equity exposure is also true for longer maturities.

In Table 4.2 we report the results obtained by exploiting the different allocation strategies for the evaluation of the call option prices, w.r.t. different initial interest rates and volatilities, and considering a short investment time horizon, i.e. taking year. In Panel A we reported the plain vanilla call option prices, while Panel B contains the normal CPPI-based options, and Panel C refers to the options linked to the CPPI with guaranteed minimum equity exposure.

Panel A: option on pure risky asset Initial interest rate Initial annual volatility 0.10 0.20 0.30 0.40 0.50 0.01 5.29 9.19 13.06 16.89 20.68 0.03 6.07 9.77 13.57 17.38 21.18 0.05 6.84 10.35 14.14 17.88 21.57 0.07 7.65 11.06 14.73 18.38 22.01 0.10 8.93 12.05 15.61 19.24 22.88 Panel B: option on CPPI Initial interest rate Initial annual volatility 0.10 0.20 0.30 0.40 0.50 0.01 2.64 2.64 2.65 2.65 2.62 0.03 3.72 3.72 3.71 3.72 3.66 0.05 4.78 4.78 4.78 4.78 4.72 0.07 5.82 5.82 5.84 5.82 5.86 0.10 7.35 7.35 7.35 7.35 7.42 Panel C: option on CPPI with Guaranteed Minimum Equity Exposure Initial interest rate Initial annual volatility 0.10 0.20 0.30 0.40 0.50 0.01 3.02 3.97 5.07 6.28 7.55 0.03 3.97 4.74 5.76 6.94 8.27 0.05 4.94 5.55 6.50 7.64 8.96 0.07 5.92 6.43 7.31 8.38 9.65 0.10 7.41 7.79 8.56 9.65 10.90

We would like to underline that, while the call options linked to traditional CPPI-based approach remain almost constant for different volatility levels, no matter about the initial interest rate value, higher volatilities might increase the option price for a pure risky asset underlying, and higher volatilities for a CPPI strategy increase the risk of a cash-in event such that a higher number of simulated paths ends up with the minimum protection level of As a result, the option price is less depending on volatility levels.

Let us note that options linked to CPPI-based strategies are significantly cheaper than plain vanilla ones, thanks to the embedded risk management features. Moreover, below an annual market volatility of the CPPI with and without minimum exposure give a comparable price range. When the volatility exceeds the former becomes more expensive.

4.2.2 Comparison of put options

In this subsection we provide numerical results for the put option case.

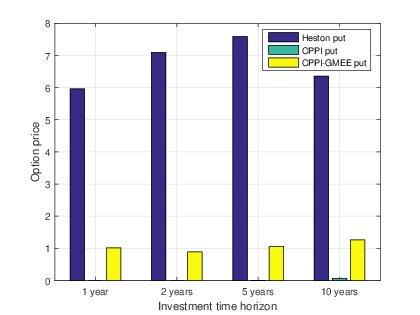

Fig. 4.3 shows the put option price for different maturities when the underlying is represented by a pure risky asset, resp. by a standard CPPI portfolio, resp. by a CPPI strategy with guaranteed minimum equity exposure.

As expected, the put option over the standard CPPI strategy provides a zero-value price. Interestingly, we see some cases in which also the value of the put option linked to a CPPI is positive, i.e. we have some paths for which the CPPI logic does not achieve the protection level of The latter is due to the fact that, especially for longer time horizon, the risk increases that in certain cases the overnight loss is higher than the assumptions embedded in the multiplier. As seen in Sect. 4.2.1, we obtain that the put options linked to CPPI-based strategies are cheaper than the standard derivative options based on a pure risky underlying.

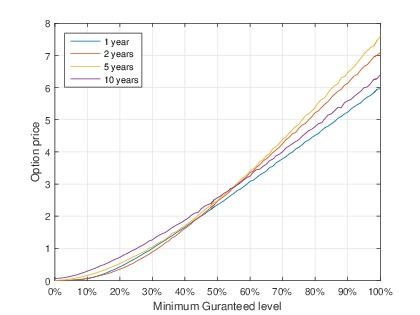

Moreover, see Fig. 4.4, we study the put option value as a function of the minimum exposure for different maturity levels. As before, the case of coincides with the put on a standard CPPI. That is why the resulting option values are close to zero. For the results coincide with put option prices using a pure risky asset as underlying.

Finally, in Table 4.3 we evaluate the put option prices for different initial interest rates and volatilities, for an investment time year. Panel A refers to put options on a pure risky asset, while Panel B refers to the standard CPPI case, and Panel C reports data for a CPPI with guaranteed minimum equity exposure. It can be seen that put options linked to CPPI-based strategies with minimum exposure to the risky asset are positive and significantly more expansive than put options on a normal CPPI. These results show, as expected, there exists a number of paths in which the CPPI with guaranteed minimum exposure can lead to real losses and cannot achieve capital preservation like the standard CPPI approach.

Panel A: option on pure risky asset Initial interest rate Initial annual volatility 0.10 0.20 0.30 0.40 0.50 0.01 2.62 6.49 10.35 14.18 18.02 0.03 2.29 5.99 9.80 13.57 17.38 0.05 1.97 5.49 9.25 13.00 16.74 0.07 1.69 5.09 8.78 12.43 16.12 0.10 1.36 4.49 8.06 11.68 15.33 Panel B: option on CPPI Initial interest rate Initial annual volatility 0.10 0.20 0.30 0.40 0.50 0.01 0.00 0.00 0.00 0.00 0.00 0.03 0.00 0.00 0.00 0.00 0.00 0.05 0.00 0.00 0.00 0.00 0.00 0.07 0.00 0.00 0.00 0.00 0.02 0.10 0.00 0.00 0.00 0.00 0.07 Panel C: option on CPPI with Guaranteed Minimum Equity Exposure Initial interest rate Initial annual volatility 0.01 0.37 1.31 2.41 3.62 4.93 0.03 0.24 1.01 2.03 3.21 4.51 0.05 0.15 0.76 1.71 2.85 4.13 0.07 0.09 0.59 1.47 2.56 3.84 0.10 0.05 0.42 1.20 2.27 3.53

4.2.3 CPPI-based option pricing strategies for different protection levels

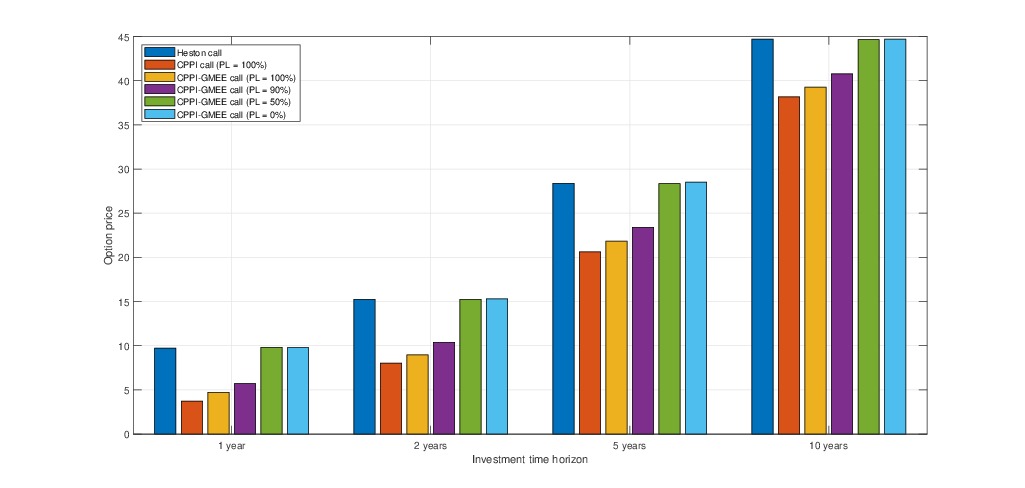

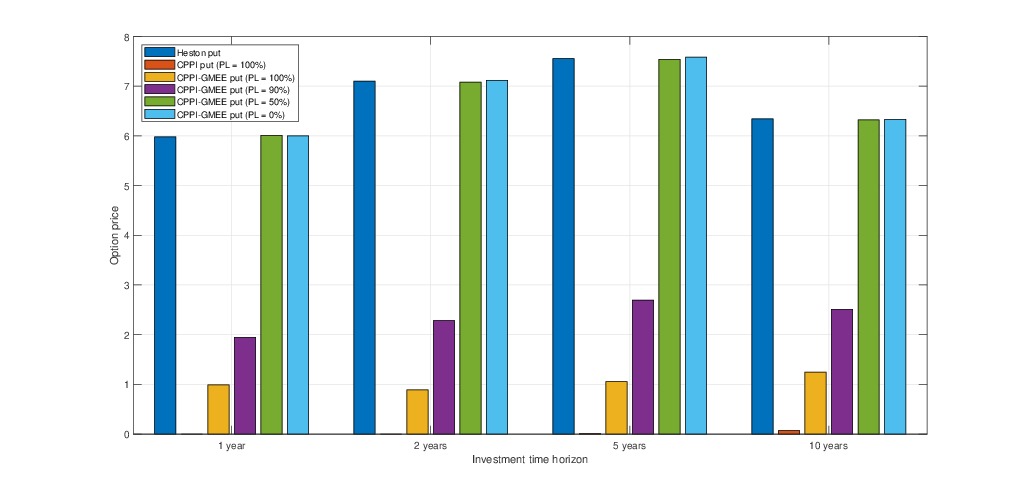

An alternative way to adjust the portfolio allocation is to modify the protection level. More precisely, we consider a CPPI-GMEE allocation with different protection levels, ranging between and A reduction of the protection level increases the risk budget and, consequently, the equity exposure of the portfolio. For the standard CPPI strategy the protection level remains at The numerical results for ATM call/put options are provided in Fig. 4.5 and 4.6.

We observe that:

-

•

by reducing the protection level of the CPPI-GMEE approach from to the CPPI-GMEE strategy gets riskier. This implies that the corresponding option price increases significantly. The same behavior can be spotted when the protection level is even more reduced, e.g. when we consider

Such a circumstance is more evident in the case of put options, where the option price doubles when the protection level halves;

-

•

the case in which equals the case with a pure risky asset as the derivative underlying, hence we see the square option price;

-

•

there exists the risk that the CPPI strategy ends below implying that also the put option price on standard CPPI is greater than zero for long maturities.

5 Conclusion

In this paper we have introduced a novel extension within the set of investment insurance strategies by combining an OBPI approach with a CPPI logic, reflecting a minimum guaranteed equity exposure. Indeed, besides using the CPPI portfolio as an underlying of suitable options to meet investors’ capital protection needs, we consider the so called Guaranteed Minimum Equity Exposure, hence imposing that the percentage of wealth invested in the risky security cannot fall below a fixed threshold. This allows to provide a CPPI-based strategy avoiding the cash-in event after the critical situation where the price of the underlying suddenly collapses, because of, e.g., market shocks. This represents a concrete innovation in the literature related to the portfolio protection strategies based on OBPI or CPPI.

We have provided historical simulations showing how the risk-return profile changes, according to the market environment, and describing the option prices’ behaviors under different frameworks, namely, when the underlying is pure risky asset, a CPPI strategy, or a CPPI–GMEE based one. Obtained results clearly illustrate that, depending on the parameters choice, our method provides a valuable compromise between a pure risky asset investment strategy and a traditional CPPI one. In fact, it ensures to avoid the aforementioned cash-in risk of a standard CPPI, although it is rather more expensive than the options on standard CPPI.

We would like to underline that the present work represents a first step in our research agenda. Further contributions, that are subject of our on-going research, include more structured derivatives evaluated with respect to general stochastic volatility models, also including the presence of jumps. Concurrently, we plan to study the sensitivity of the CPPI-GMEE approach to the changes of market parameters, and to compare options on CPPI with options on other dynamic asset allocation strategies, such as the VolTarget ones, also allowing the CPPI-GMEE to have lock-in elements. Finally, we intend to examine the role played by transaction costs in the option valuation on CPPI-GMEE framework.

References

- [1] Albeverio, S., Steblovskaya, V. and Wallbaum, K. (2017) The volatility target effect in structured investment products with capital protection, Rev. Deriv. Res., 21(2) 201–229.

- [2] Albeverio, S., Steblovskaya, V. and Wallbaum, K. (2013) Investment instruments with volatility target mechanism, Quantitative Finance, 13(10) 1519–1528.

- [3] Aliprantis, C.D., Brown, D.J. and Werner, J. (2000) Minimum-cost portfolio insurance, Journal of Economic Dynamics and Control, 24(11-12), 1703–1719.

- [4] Ameur, H.B., Prigent, J.-L. (2011) CPPI Method with a conditional floor, International Journal of Business, 16 (3), 218–230.

- [5] Annaert, J., Van Osselaer, S. and Verstraete, B. (2009) Performance evaluation of portfolio insurance strategies using stochastic dominance criteria, Journal of Banking and Finance, 33(2), 272–280.

- [6] Balder, S., Brandl, M., Mahayni, A. (2009) Effectiveness of CPPI strategies under discrete-time trading, Journal of Economic Dynamics and Control, 33 (1), 204–220.

- [7] Basak, S. (2002) A comparative study of portfolio insurance, Journal of Economic Dynamics and Control, 26(7-8), 1217–1241.

- [8] Bertrand, P. and Prigent, J–L. (2005) Portfolio Insurance Strategies: OBPI versus CPPI, Finance, 26(1) 5–32.

- [9] Black, F. and Johns, R. (1987) Simplifying portfolio insurance, The Journal of Portfolio Management, 14(1) 48–51.

- [10] Black, F. and Perold, A.F. (1992) Theory of constant proportion portfolio insurance, Journal of Economic Dynamics and Control, 16(3–4) 403–426.

- [11] Brennan, M.J., Schwartz, E.S. (1976) The pricing of equity-linked life insurance policies with an asset value guarantee, Journal of Financial Economics, 3 (3), pp. 195-213.

- [12] Cesari, R. and Cremonini, D. (2003) Benchmarking, portfolio insurance and technical analysis: a Monte Carlo comparison of dynamic strategies of asset allocation, Journal of Economic Dynamics and Control, 27(6), 987–1011.

- [13] Constantinou, N., Khuman, A.D. and Maringer, D. (2008), Constant Proportion Portfolio Insurance: Statistical Properties and Practical Implications, Working Paper No. 023-08, University of Essex, August 2008.

- [14] Davis, E.P. (2003) Comparing bear markets – 1973 and 2000, National Institute Economic Review, 183(1), 78–79.

- [15] Dehghanpour, S. and Esfahanipour, A. (2018) Dynamic portfolio insurance strategy: a robust machine learning approach, Journal of Information and Telecommunication, doi:10.1080/24751839.2018.1431447.

- [16] Escobar, M., Kiechle, A. and Zagst, R. (2011) Option on a CPPI, International Mathematical Forum 6, 5–8 229–262.

- [17] Grossman, S.J., Zhou, Z.(1993) Optimal Investment Strategies for Controlling Drawdowns, Mathematical Finance, 3 (3) pp. 241–276.

- [18] Horcher, K. A. (2005) Essentials of financial risk management. John Wiley and Son.

- [19] Jessen, C. (2014) Constant proportion portfolio insurance: Discrete-time trading and gap risk coverage Journal of Derivatives, 21 (3), 36–53.

- [20] Kosowski, R. and Neftci S. (2015) Principles of Financial Engineering, Third Edition, London, Academic Press.

- [21] Leland, H.E. and Rubinstein, M. (1976) The Evolution of Portfolio Insurance. In: Luskin, D.L., Ed., Portfolio Insurance: A Guide to Dynamic Hedging, Wiley.

- [22] McNeil, A. J., Rüdiger, F. and Embrechts, P. (2005) Quantitative risk management: concepts, techniques and tools. Princeton University Press.

- [23] Pain, D. and Rand, J. (2008) Recent Developments in Portfolio Insurance, Bank of England Quarterly Bulletin 48(1), 37–46.

- [24] Paulot, L. and Lacroze, X. (2011) One-Dimensional Pricing of CPPI, Applied Mathematical Finance, 18(3),

- [25] Perold, A.F. and Sharpe, W.F. (1995) Dynamic strategies for asset allocation, Financial Analysts Journal, 51(2) 149–160.

- [26] Rudolf, M. (1995) Algorithms for Portfolio Optimization and Portfolio Insurance, Ph.D. thesis, St.Gallen University, Verlag Paul Haupt Bern Stuttgart Vienna.

- [27] Schied, A. (2014) Model-free CPPI Journal of Economic Dynamics and Control, 40, 84–94.

- [28] UCITS IV, (2009) On the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities, Directive 2009/65/EC. Undertakings for Collective Investment in Transferable Securities (UCITS) – Financial Derivative Instruments, Guidance Note 3/03.

- [29] Zagst, R. and Kraus, J. (2011) Stochastic Dominance of Portfolio Insurance Strategies, Annals of Operations Research, 185, 75–103.