Quantile double autoregression

Abstract

Many financial time series have varying structures at different quantile levels, and also exhibit the phenomenon of conditional heteroscedasticity at the same time. In the meanwhile, it is still lack of a time series model to accommodate both of the above features simultaneously. This paper fills the gap by proposing a novel conditional heteroscedastic model, which is called the quantile double autoregression. The strict stationarity of the new model is derived, and a self-weighted conditional quantile estimation is suggested. Two promising properties of the original double autoregressive model are shown to be preserved. Based on the quantile autocorrelation function and self-weighting concept, three portmanteau tests are constructed to check the adequacy of fitted conditional quantiles. The finite-sample performance of the proposed inference tools is examined by simulation studies, and the necessity of the new model is further demonstrated by analyzing the S&P500 Index.

Key words: Autoregressive time series model; Conditional heteroscedasticity; Portmanteau test; Quantile model; Strict stationarity.

1 Introduction

The conditional heteroscedastic models have become a standard family of nonlinear time series models since the introduction of Engle’s (1982) autoregressive conditional heteroscedastic (ARCH) and Bollerslev’s (1986) generalized autoregressive conditional heteroscedastic (GARCH) models. Among existing conditional heteroscedastic models, the double autoregressive (AR) model recently has attracted more and more attentions; see Ling (2004, 2007), Ling and Li (2008), Zhu and Ling (2013), Li et al. (2016), Li et al. (2017), Zhu et al. (2018) and references therein. This model has the form of

| (1.1) |

where , with , and are identically and independently distributed () random variables with mean zero and variance one. It is a special case of AR-ARCH models in Weiss (1986), and will reduce to Engle’s (1982) ARCH model when all ’s are zero. The double AR model has two novel properties. First, it has a larger parameter space than that of the commonly used AR model. For example, when , the double AR model may still be stationary even as (Ling, 2004), whereas this is impossible for AR-ARCH models. Secondly, no moment condition on is needed to derive the asymptotic normality of the Gaussian quasi-maximum likelihood estimator (QMLE) (Ling, 2007). This is in contrast to the ARMA-GARCH model, for which the finite fourth moment of the process is unavoidable in deriving the asymptotic distribution of the Gaussian QMLE (Francq and Zakoian, 2004), resulting in a much narrower parameter space (Li and Li, 2009).

In the meanwhile, conditional heteroscedastic models are considered mainly for modeling volatility and financial risk. Some quantile-based measures, such as the value-at-risk (VaR), expected shortfall and limited expected loss, are intimately related to quantile estimation, see, e.g., Artzner et al. (1999), Wu and Xiao (2002), Bassett et al. (2004) and Francq and Zakoian (2015). Therefore, it is natural to consider the quantile estimation for conditional heteroscedastic models. Many researchers have investigated the conditional quantile estimation (CQE) for the (G)ARCH models; see Koenker and Zhao (1996) for linear ARCH models, Xiao and Koenker (2009) for linear GARCH models, Lee and Noh (2013) and Zheng et al. (2018) for quadratic GARCH models. Chan and Peng (2005) considered a weighted least absolute deviation estimation for double AR models with the order of , and Zhu and Ling (2013) studied the quasi-maximum exponential likelihood estimation for a general double AR model. Cai et al. (2013) considered a Bayesian estimation of model (1.1) with following a generalized lambda distribution. However, it is still open to perform the CQE for double AR models.

In addition, for the double AR process generated by model (1.1), its th conditional quantile has the form of

| (1.2) |

and the coefficients of ’s are all -independent, where is the -field generated by , and is the th quantile of ; see also Cai et al. (2013). However, when modeling the closing prices of S&P500 Index by the CQE, we found that the estimated coefficients of ’s depend on the quantile level significantly, while those of ’s also slightly depend on the quantile level; see Figures 6 and 7 in Section 6 for empirical evidences. Actually this phenomenon can also be found in many other stock indices. Koenker and Xiao (2006) proposed a quantile AR model by extending the common autoregression, and the corresponding coefficients are defined as functions of quantile levels. By adapting the method in Koenker and Xiao (2006), this paper attempts to introduce a new conditional heteroscedastic model, called the quantile double autoregression, to better interpret the financial time series with the above phenomenon. We state our first main contribution below in details.

-

(a)

A direct extension of Koenker and Xiao’s method will result in a strong constraint that the coefficients of ’s will be zero at a certain quantile level simultaneously; see Section 2. A novel transformation of is first introduced to the conditional scale structure in Section 2, and hence the drawback can be removed from the derived model. Moreover, there is no nonnegative constraint on coefficient functions, and this makes numerical optimization much flexible. Section 2 also establishes the strict stationarity and ergodicity of the newly proposed model, and the first novel property of double AR models is preserved.

In the meanwhile, many financial time series are heavy-tailed, and the least absolute deviation (LAD) estimator of infinite variance AR models usually has a faster convergence rate, but a more complicated asymptotic distribution, than the commonly encountered asymptotic normality; see, e.g., Gross and Steiger (1979), An and Chen (1982) and Davis et al. (1992). Ling (2005) proposed a self-weighted LAD estimation, and the weights are used to reduce the moment condition on processes. As a result, the asymptotic normality can be obtained although the super-consistency is sacrificed. The self-weighting approach has also been adopted to the quasi-maximum likelihood estimation for ARMA-GARCH models (Zhu and Ling, 2011) and augmented double AR models (Jiang et al., 2020), and to the conditional quantile estimation for linear double AR models (Zhu et al., 2018). The CQE may suffer from the similar problem. Actually the finite third moment on will be inevitable for the asymptotic normality of the CQE (Zhu and Ling, 2011), and this will make the resulting parameter space narrower; see Section 2.

-

(b)

Motivated by Ling (2005), this paper considers a self-weighted CQE for the newly proposed model in Section 3. Only a fractional moment on is needed for the asymptotic normality, and the second novel property of double AR models is hence preserved. As a result, the proposed methodology can be applied to very heavy-tailed data. Moreover, the objective function in this paper is non-differentiable and non-convex, and this causes great challenges in asymptotic derivations. Section 3 overcomes the difficulty by adopting the bracketing method in Pollard (1985), and this is another important contribution of this paper.

According to the Box-Jenkins’ three-stage modeling strategy, it is important to check the adequacy of fitted conditional quantiles, and the autocorrelation function of residuals is supposed to play an important role in this literature; see Box and Jenkins (1970) and Li (2004). Li et al. (2015) introduced a quantile correlation to measure the linear relationship between any two random variables for the given quantile in quantile regression settings, and proposed the quantile autocorrelation function (QACF) to assess the adequacy of fitted quantile AR models (Koenker and Xiao, 2006). In the meanwhile, the diagnostic checking for the conditional location usually uses fitted residuals (Ljung and Box, 1978), while that for the conditional scale employs the absolute residuals (Li and Li, 2005). It is noteworthy that the proposed quantile double AR model consists of both the conditional location and scale parts.

-

(c)

In line with the estimating procedure in Section 3, Section 4 first introduces a self-weighted QACF of residuals to measure the quantile correlation, and constructs two portmanteau tests to check the adequacy of the fitted conditional quantile in the conditional location and scale components, respectively. A combined test is also considered. This is the third main contribution of this paper.

In addition, Section 5 conducts simulation studies to evaluate the finite-sample performance of self-weighted estimators and portmanteau tests, and Section 6 presents an empirical example to illustrate the usefulness of the new model and its inference tools. Conclusion and discussion are made in Section 7. All the technical details are relegated to the Appendix. Throughout the paper, denotes the convergence in distribution, and denotes a sequence of random variables converging to zero in probability. We denote by the norm of a matrix or column vector, defined as .

2 Quantile double autoregression

This section introduces a new conditional heteroscedastic model by generalizing the double AR model at (1.2) or (1.1), and the new model can also be used to accommodate the phenomenon that the financial time series may have varying structures at different quantile levels.

We first consider a direct extension of model (1.2), which, as in Zhu et al. (2018), can be reparametrized into , where and with . Along the line of quantile autoregression (Koenker and Xiao, 2006), by letting the corresponding coefficients depend on the quantile level , we then have

| (2.1) |

However, if there exists such that , all ’s will then disappear from the quantile structure at this level, i.e. the contributions of all ’s are zero at a certain quantile level simultaneously. In addition, both coefficient functions and are related to the same term of , and it may not be a good idea to separate the influence of on into two -dependent functions. As a result, the extension at (2.1) may not be a good choice.

This paper attempts to tackle the drawback of model (2.1) by looking for a way to move at (1.2) inside the square root. It then leads to a transformation of , which is an extension of the square root function with the support from to , where is the sign function. Specifically, model (1.2) can be reparameterized into alternatively, where and with . By letting ’s, and ’s depend on the quantile level , we then propose the new conditional heteroscedastic model below,

| (2.2) |

where , ’s and ’s with are continuous functions , and it will reduce to model (1.2) when , and with . It is not necessary to assume that and ’s are all equal to zero at a certain quantile level, and the drawback of the definition at (2.1) is hence removed.

Assume that, as in Koenker and Xiao (2006), the right hand side of (2.2) is an increasing function with respect to . Let be a sequence of standard uniform random variables, and then model (2.2) has an equivalent form below,

| (2.3) |

It will reduce to the quantile AR model in Koenker and Xiao (2006) when ’s are zero with probability one. We call model (2.2) or (2.3) the quantile double autoregression (AR) for simplicity.

Remark 1.

Remark 2.

As mentioned by Koenker and Xiao (2006), it is very hard to give an explicit condition such that the right hand side of (2.2) is an increasing random function with respect to . We may assume that all and ’s with are all increasing functions. Note that is continuous and monotonically increasing, and hence the second term at the right hand side of (2.2) will be increasing with respect to . Following Koenker and Xiao (2006), we further assume that is an increasing function with respect to , and it is then guaranteed that (2.2) defines a qualified conditional quantile function.

Remark 3.

The AR-ARCH model is another popular conditional heteroscedastic model in the literature, and it is certainly of interest to consider a similar generalization for it. The AR-ARCH model has the form of,

where the coefficients and are defined as in (1.1), and its th conditional quantile is given below,

which, however, has a more complicated form than model (1.2). This makes it impossible to reach an easy-to-interpret quantile model. In addition, comparing with AR-ARCH models, the double AR has many other advantages; see Section 1.

Let , where is a quantile double AR process generated by model (2.3). It can be verified that is a homogeneous Markov chain on the state space , where is the class of Borel sets of , and is the Lebesgue measure on . Denote by and the distribution and density functions of , respectively. It holds that and for any .

Assumption 1.

The density function is positive and continuous on , and for some .

Theorem 1.

Since is a standard uniform random variable, the condition in the above theorem is equivalent to . Moreover, for the double AR model at (1.1), Ling (2007) derived its stationarity condition for the case with being a standard normal random variable, while it is still unknown for the other distributions of . From Theorem 1 and Remark 1, we can obtain a stationarity condition for a general double AR model below.

Corollary 1.

Suppose that has a positive and continuous density on its support, and for some . If , then there exists a strictly stationary solution to the double AR model at (1.1), and this solution is unique and geometrically ergodic with .

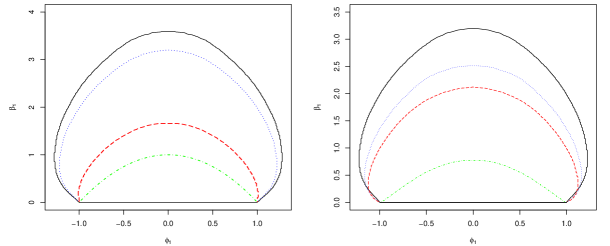

For the case with the order of , when is symmetrically distributed, the above condition can be simplified to . Moreover, if the normality of is further assumed, the necessary and sufficient condition for the strict stationarity is then (Ling, 2007). The comparison of the above stationarity regions is illustrated in the left panel of Figure 1. It can be seen that a larger value of in Corollary 1 leads to a higher moment of , and hence results in a narrower stationarity region. Figure 1 also gives the stationarity regions with different distributions of . As expected, the parameter space of model (1.1) becomes smaller as gets more heavy-tailed.

3 Self-weighted conditional quantile estimation

Let and . For the proposed quantile double AR model at (2.2), denote by the parameter vector, where and . We then can define the conditional quantile function below,

and this paper considers a self-weighted conditional quantile estimation (CQE) for model (2.2),

| (3.1) |

where is the check function, and are nonnegative random weights; see also Ling (2005) and Zhu and Ling (2011).

Remark 4.

When for all with probability one, the self-weighted CQE will become the common CQE. A third order moments will be needed for the asymptotic normality, and this will lead to a much narrower stationarity region; see Figure 1 for the illustration. For heavy-tailed data, the least absolute deviation (LAD) estimator of infinite variance AR models is shown to have a faster convergence rate and a more complicated asymptotic distribution (An and Chen, 1982; Davis et al., 1992), and the similar situation may be expected to the CQE. By adopting the self-weighting method in Ling (2005), this paper suggests the self-weighted CQE at (3.1) to maintain the asymptotic normality even for heavy-tailed data with only a finite fractional moment.

Denote the true parameter vector by , and it is assumed to be an interior point of the parameter space , which is a compact set. Moreover, let and be the distribution and density functions of conditional on , respectively.

Assumption 2.

is strictly stationary and ergodic with for some .

Assumption 3.

is strictly stationary and ergodic, and is nonnegative and measurable with respect to with .

Assumption 4.

With probability one, and its derivative function are uniformly bounded, and is positive on the support .

Theorem 1 in Section 2 provides a sufficient condition for Assumption 2, and the proposed self-weighted CQE can handle very heavy-tailed data since only a fractional moment is needed. Some discussions on random weights are delayed to Remark 7.

Remark 5.

Assumption 4 is commonly used in the literature; see, e.g, Assumption 3 of Ling (2005) for the self-weighted LAD estimator of infinite variance AR models, Assumption (A2) of Lee and Noh (2013) for the CQE of GARCH models, and Assumption 4 of Zhu et al. (2020) for the CQE of linear models with GARCH-X errors. Specifically, the strong consistency requires the positiveness and continuity of , while the boundedness of and is needed for the -consistency and asymptotic normality. Assumption 4 is mainly to simplify the technical proofs, and certainly can be weakened. For example, we may replace the boundedness of by assuming the uniform continuity of on a close interval. However, a lengthy technical proof will be required.

Remark 6.

The nonzero restriction on and with is due to two reasons: (i) the first order derivative of does not exist at , and we need to bound the term of away from zero such that the first derivative of exists and then the asymptotic variance in Theorem 3 is well defined; and (ii) this term will also be used to reduce the moment requirement on or in the technical proofs and, without it, a moment condition on will be required. For many financial time series, at quantile levels around , the values of and ’s are all close to zero, and hence we may fail to provide a reliable estimating result; see Figure 7 for details. This actually is a common problem for all CQE, and may be solved by assuming a parametric form to these coefficient functions. We leave it for future research.

Denote . Let be the first derivative of . Define symmetric matrices

and .

Theorem 3.

Suppose that the conditions of Theorem 2 hold. If is positive definite, then as .

The technical proof of Theorem 3 is nontrivial since the objective function of the self-weighted CQE is non-convex and non-differentiable, and the main difficulty is to prove the -consistency, i.e. . We overcome it by adopting the bracketing method (Pollard, 1985) as in Zhu and Ling (2011).

Remark 7.

For random weights , there are many choices satisfying Assumption 3. For the double AR model at (1.2) and Remark 1, by a method similar to that of proving Theorem 3 in Zhu et al. (2018), we can show that the asymptotic variance is minimized when and . However, for a general quantile double AR, the asymptotic variance depends on the weights in a complicated way, and the optimal weights do not have an explicit form. In fact, the selection of optimal weights is still an open problem for AR models (Ling, 2005), and it becomes more complicated for a quantile model with an additional conditional scale structure in (2.2). Note that the key step of using the weights in technical proofs is to bound the term of by for some fractional value . As a result, Ling (2005) heuristically used , where for some constant . Following Zhu et al. (2018) and Jiang et al. (2020) for AR-type conditional heteroscedastic models, we simply employ the weights with .

Remark 8.

To estimate the quantity of in the asymptotic variance at Theorem 3, we consider the difference quotient method (Koenker, 2005),

for some appropriate choices of bandwidth , where is the fitted th conditional quantile. As in Koenker and Xiao (2006) and Li et al. (2015), we employ two commonly used choices for the bandwidth as follows

| (3.2) |

where and are the standard normal density and distribution functions, respectively, and with being set to ; see Bofinger (1975) and Hall and Sheather (1988). The bandwidth is selected by minimizing the mean square error of Gaussian density estimation, while is obtained based on the Edgeworth expansion for studentized quantiles. Simulation results in Section 5 indicate that these two bandwidths have similar performance. As a result, the two matrices and can then be approximated by the sample averages,

where . Consequently, a consistent estimator of the asymptotic variance matrix can be constructed.

From the self-weighted CQE , the th quantile of conditional on can be estimated by . The following corollary provides the theoretical justification for one-step ahead forecasting, and it is a direct result from Taylor expansion and Theorem 3.

Corollary 2.

Under the conditions of Theorem 3 and , it holds that

In practice, we may consider multiple quantile levels simultaneously, say . Although from the proposed procedure may not be monotonically increasing in , it is convenient to employ the rearrangement method in Chernozhukov et al. (2010) to solve the quantile crossing problem after the estimation.

Remark 9.

In real applications, we do not know the order of at model (2.2), and an information criterion is thus introduced. At each quantile level of , we may consider the following Bayesian information criterion (BIC),

where is a predetermined positive integer, is the self-weighted CQE defined in (3.1) at order , and with ; see also Machado (1993) and Zhu et al. (2018). Note that the selected orders will depend on , while we may need an order uniformly for all quantile levels. As a result, we suggest a combined version below,

where with being a fixed integer. Let be the selected order. From simulation results in Section 5, the proposed BIC has satisfactory performance. Note that the likelihood function of model (2.2) or (2.3) will involve the inverse function of with respect to , which, however, has no close form. It hence is not feasible to use the likelihood function to design an information criterion.

Remark 10.

It is of interest to consider a quantile double autoregression with orders different for the conditional location and scale parts,

for all . The counterpart of model (2.3) can be given similarly. Let with for or for . Theorem 1 and Corollary 1 can then be used to establish the strict stationarity. For the case with , all theoretical results in this section still hold. However, when , the conditional scale of is not enough to reduce the moment requirement on , and hence a higher order moment of will be needed for theoretical justification. We prefer to the case with , and leave the general setting for future research.

4 Diagnostic checking for conditional quantiles

To check the adequacy of fitted conditional quantiles, we construct two portmanteau tests to detect possible misspecifications in the conditional location and scale, respectively, and a combined test is also considered.

Let be the conditional quantile error. Instead of applying the QACF to quantile errors directly, we alternatively introduce the self-weighted QACF which naturally combines the QACF in Li et al. (2015) and the idea of self-weighting in Ling (2005). Specifically, the self-weighted QACF of at lag is defined as

where , are random weights used in Section 3, and . By replacing with , a variant of can be defined as

where and . Note that if is correctly specified by model (2.2), then and for all .

Accordingly, denote by the conditional quantile residuals, where . The self-weighted residual QACFs at lag can then be defined as

and

where , , and . For a predetermined positive integer , let and . We first derive the asymptotic distribution of and .

Denote and . Let and . For and 2, denote the matrices and , and the matrices and

where . In addition, denote the matrices and , where . Define the matrices and

Theorem 4.

Suppose that the conditions of Theorem 3 hold and . It holds that as .

The finite second moment of is required in Theorem 4 since this condition is needed to show the consistency of for and 2. We have tried many other approaches, such as transforming the residuals by a bounded and strictly increasing function (Zhu et al., 2018) and then applying the self-weighted QACF to the transformed residuals, however, the condition of is still unavoidable. As a comparison, if we alternatively use the unweighted QACFs of residuals with for all , then the condition of is unavoidable for the asymptotic normality.

As for estimating in Section 3, we can employ the difference quotient method to estimate the quantity of , and then approximate the expectations in by sample averages with being replaced by . Consequently, a consistent estimator, denoted by , for the asymptotic covariance in Theorem 4 can be constructed. We then can check the significance of ’s and ’s individually by establishing their confidence intervals based on .

Let be a multivariate normal random vector with zero mean vector and covariance matrix , where . To check the first lags of ’s (or ’s) jointly, by Theorem 4, the Box-Pierce type test statistics can be designed below,

as . It is also of interest to consider a combined test, as . To calculate the critical value or -value of the three tests, we generate a sequence of, say , multivariate random vectors with the same distribution of , and then use the empirical distributions to approximate the corresponding null distributions. As expected, the simulation results in Section 5 suggest that is more powerful in detecting the misspecification in the conditional location, has a better performance in detecting the misspecification in the conditional scale, while has a performance between those of and . Therefore, we may first use to check the overall adequacy of the fitted conditional quantiles, and then employ and to look for more details; see also Li and Li (2008) and Zhu et al. (2018).

Remark 11.

There are two advantages to introduce the self-weights into the QACF. First, in line with the estimating procedure in Section 3, the self-weights can reduce the moment restriction on in establishing the asymptotic normality of and (see Theorem 4) and thus makes the diagnostic tools applicable for heavy-tailed data. Secondly, as validated by the simulation results in Section 5, the self-weighted residual QACFs and are more efficient than their unweighted counterparts with for all . In contrast to the efficiency loss in estimation due to the self-weights, interestingly, self-weights can improve the efficiency of QACFs in terms of standard deviations.

5 Simulation studies

5.1 Self-weighted CQE and model selection

The first experiment is to evaluate the self-weighted CQE in Section 3. The data generating process is

| (5.1) |

where are standard uniform random variables, and we consider two sets of coefficient functions below,

| (5.2) |

and

| (5.3) |

where is the inverse function of , and is the distribution function of the standard normal, the Student’s or the Student’s random variable. It holds that when with being a constant. Let , and then the coefficient functions at (5.2) and (5.3) correspond to

respectively. We consider two sample sizes, and 1000, and there are 1000 replications for each sample size. The self-weighted CQE in (3.1) is employed to fit the data, and the quasi-Newton algorithm can be used to obtain the estimate for each replication. To estimate the asymptotic standard deviation (ASD) of , two bandwidths, and at (3.2), are used to estimate in the difference quotient method, and the resulting ASDs are denoted as ASD1 and ASD2, respectively.

Tables 2 and 3 present the bias, empirical standard deviation (ESD) and ASD of at quantile level or for settings (5.2) and (5.3), respectively, and the corresponding values of are also given. We only report the results for the standard normal and the Student’s cases, and that for the Student’s case are relegated to the supplementary material to save space. It can be seen that, as the sample size increases, the biases, ESDs and ASDs decrease, and the ESDs get closer to their corresponding ASDs. Moreover, the biases, ESDs and ASDs get smaller as the quantile level increases from to . It is obvious since there are more observations as the quantile level gets near to the center, although the true values of and also become smaller as approaches . Finally, most biases, ESDs and ASDs increase as the distribution of gets heavy-tailed, and the bandwidth slightly outperforms .

The second experiment is to evaluate the proposed BIC in Remark 9. The data generating process is

| (5.4) |

with three sets of coefficient functions,

where the other settings are preserved as in the first experiment. The proposed BIC is used to select the order with . Since the true order is two, the cases of underfitting, correct selection and overfitting correspond to being 1, 2 and greater than 2, respectively. Table 4 gives the percentages of underfitted, correctly selected and overfitted models. It can be seen that the BIC performs well in general. It becomes better when the sample size increases, while gets slightly worse as the distribution of gets more heavy-tailed.

5.2 Three portmanteau tests

The third experiment considers the self-weighted residual QACFs, and , and the approximation of their asymptotic distributions. The number of lags is set to , and all the other settings are the same as in the first experiment. For model (5.1) with coefficient functions at (5.2), Tables 5 and 6 give the biases, ESDs and ASDs of and , respectively, with lags and 6. The results for Student’s case are relegated to the supplementary material to save space. We have four findings for both residual QACFs and : (1) the biases, ESDs and ASDs decrease as the sample size increases or as the quantile level increases from to ; (2) the ESDs and ASDs are very close to each other; (3) the biases, ESDs and ASDs get smaller as becomes heavy-tailed; (4) two bandwidths and perform similarly. Similar observations can be found for coefficient functions at (5.3), and the results are relegated to the supplmentary material to save space.

The fourth experiment is to evaluate the size and power of three portmanteau tests in Section 4, and the data generating process is

| (5.5) |

with being defined as in previous experiments, while a quantile double AR model with order one is fitted to the generated sequences. As a result, the case of corresponds to the size, the case of to the misspecification in the conditional location, and the case of to the misspecification in the conditional scale. Two departure levels, 0.1 and 0.3, are considered for both and , and we calculate the critical values by generating random vectors. Table 7 gives the rejection rates of , and , where the critical values of three tests are calculated based on estimated covariance matrix using the bandwidth . It can be seen that the size gets closer to the nominal rate as the sample size increases to 1000 or the quantile level increases to 0.25, and almost all powers increase as the sample size or departure level increases; Moreover, in general, is more powerful than in detecting the misspecification in the conditional location, is more powerful in detecting the misspecification in the conditional scale, and compromises between and . Finally, when the data are more heavy-tailed, becomes less powerful in detecting the misspecification in the conditional location, while is more powerful in detecting the misspecification in the conditional scale. This may be due to the mixture of two effects: the worse performance of the estimation and the larger value of in the conditional scale. We also calculate the rejection rates of three tests using the bandwidth and another data generating process, and similar findings can be observed; see the supplmentary material for details.

5.3 Random weights

The last experiment is to compare the proposed inference tools with and without random weights in term of efficiency. Note that , and are the self-weighted CQE and two self-weighted QACFs, respectively, and we denote their unweighted counterparts by , and .

The data are generated from the process (5.1), and two sets of coefficient functions are considered:

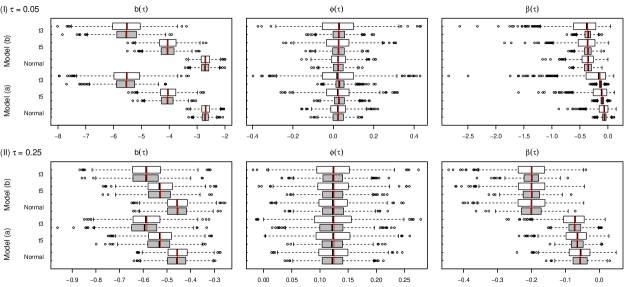

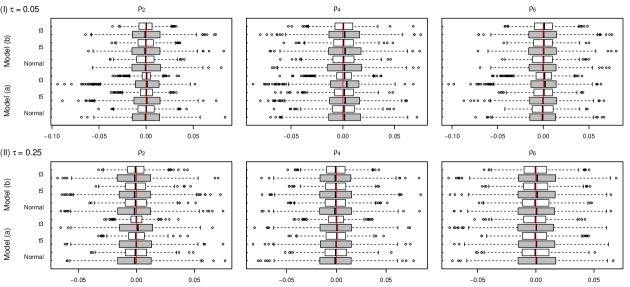

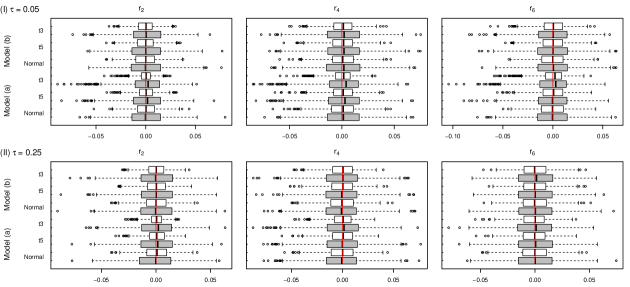

where is defined in the first experiment, and Set (a) is the same as in (5.3). We generate data of size 2000 with 1000 replications, and fit a quantile double AR model with order one to each replication using weighted and unweighted CQE at quantile levels and 0.25. Figure 2 presents the box plots for the weighted and unweighted CQE estimators, and Figures 3 and 4 give the box plots for residual QACFs of weighted and unweighted versions.

On one hand, the interquartile range of the weighted estimator is larger than that of the unweighted counterpart , however, the efficiency loss due to the random weights seems smaller as increases from 0.05 to 0.25 or the distribution of gets less heavy-tailed. On the other hand, the interquartile range of the weighted residual QACFs (or ) is smaller than that of the unweighted counterpart (or ), and the efficiency gain of residual QACFs owing to the random weights gets larger as the distribution of becomes more heavy-tailed. In other words, the random weights play the opposite role for estimators and residual QACFs, i.e., the weighted estimator is less efficient while the weighted residual QACFs are more efficient in finite samples. The case with the sample size of 1000 is similar, and its results can be found in the supplementary material.

In sum, both the self-weighted CQE and diagnostic tools can be used to handle the heavy-tailed time series by introducing self-weights at the sacrifice of efficiency in estimation, but the weights can lead to efficiency gain for residual QACFs. In terms of portmanteau tests, the combined test is preferred to check the overall adequacy of fitted conditional quantiles, while the tests and can be used to detect the possible misspecification in the conditional location and scale, respectively. For the selection of bandwidth in estimating the quantity of , although and perform very similarly in diagnostic checking, we recommend since it has more stable performance in estimation. Therefore, is used to estimate the covariance matrices of the self-weighted estimator and residual QACFs in the next section.

6 An empirical example

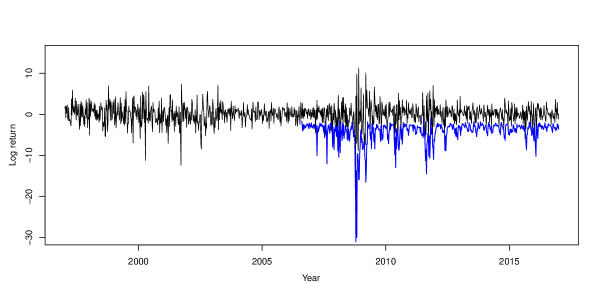

This section analyzes the weekly closing prices of S&P500 Index from January 10, 1997 to December 30, 2016. Figure 5 gives the time plot of log returns in percentage, denoted by , and there are 1043 observations in total. The summary statistics for are listed in Table 1, and it can be seen that the data is negatively skewed and heavy-tailed.

| Min | Max | Mean | Median | Std. Dev. | Skewness | Kurtosis |

| -20.189 | 11.251 | 0.000 | 0.097 | 2.488 | -0.746 | 6.119 |

The autocorrelation can be found from the sample autocorrelation functions (ACFs) of both and . We then consider a double AR model,

| (6.1) |

where the Gaussian QMLE is employed, standard errors are given in the corresponding subscripts, and the order is selected by the Bayesian information criterion (BIC) with . It can be seen that, at the 5% significance level, all fitted coefficients in the conditional mean are insignificant or marginally significant, while those in the conditional variance are significant.

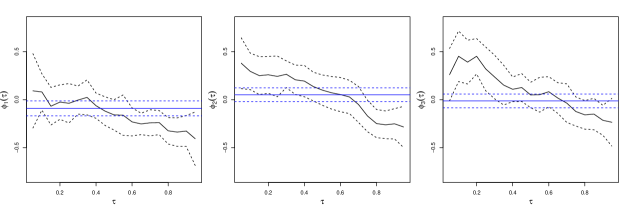

We apply the quantile double AR model to the sequence, and the quantile levels are set to with . The proposed BIC in Section 3 is employed with , and the selected order is . The estimates of for , together with their 95% confidence bands, are plotted against the quantile level in Figure 6, and those of in the fitted double AR model (6) are also given for the sake of comparison. The confidence bands of and at lags 1 and 2 are not overlapped at the quantile levels around , while those at lag 3 are significantly separated from each other around . We may conclude the -dependence of ’s, and the commonly used double AR model is limited in interpreting such type of financial time series.

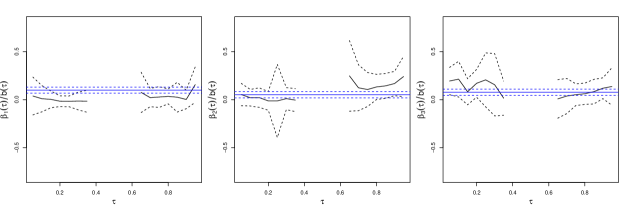

We next attempt to compare the fitted coefficients in the conditional scale of our model with those of model (6). Note that, from Remark 1, the quantity of for each in the quantile double AR model corresponds to in the double AR model. Moreover, when the quantile level is near to 0.5, the estimate of is very small, and this makes the value of abnormally large; see also Remark 6. As a result, Figure 7 plots the fitted values of for , together with their 95% confidence bands, against the quantile level with , and the fitted values of from model (6) are also reported. The confidence bands of and are separated from each other for the quantile levels around . Note that, for the double AR model (1.2), the coefficients in the conditional scale include with , which already depend on the quantile level. We may argue that it is still not flexible enough in interpreting this series.

Since 5% VaR is usually of interest for the practitioner, we give more details about the fitted conditional quantile at ,

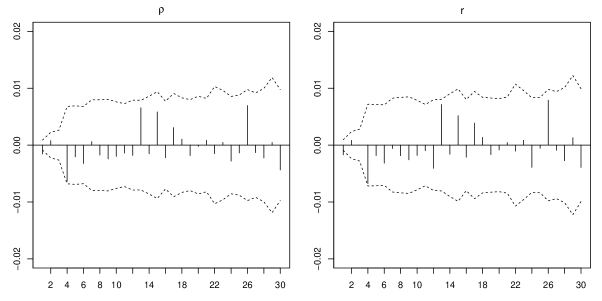

where standard errors are given in the corresponding subscripts of the estimated coefficients. Figure 8 plots the residual QACFs and , and they slightly stand out the 95% confidence bands only at lags 1 and 4. The -values of , and are all larger than 0.717 for , 20 and 30. We may conclude that both residual QACFs are insignificant both individually and jointly, and the fitted conditional quantile is adequate.

We consider the one-step ahead conditional quantile prediction at level , which is the negative values of 5% VaR forecast, and a rolling forecasting procedure is performed. Specifically, we begin with the forecast origin , which corresponds to the date of August 11, 2006, and obtain the estimated coefficients of the quantile double AR model with order three and using the data from the beginning to the forecast origin (exclusive). For each fitted model, we calculate the one-step ahead conditional quantile prediction for the next trading week by . Then we advance the forecast origin by one and repeat the previous estimation and prediction procedure until all data are utilized. These predicted values are displayed against the time plot in Figure 5. The magnitudes of VaRs become larger as the return becomes more volatile, and the returns fall below their calculated negative 5% VaRs occasionally.

In addition, we compare the forecasting performance of the proposed quantile double AR (QDAR) model with two commonly used models in the literature: the quantile AR (QAR) model in Koenker and Xiao (2006) and the two-regime threshold quantile AR (TQAR) model in (Galvao Jr et al., 2011). The order is fixed at three for all models. In estimating TQAR models, the delay parameter is searched among , and the threshold parameter is searched among a compact grid with the empirical percentiles of from the th quantile to the th quantile. The rolling forecasting procedure is employed again, and we consider VaRs at four levels, , 10%, 90% and 95%. To evaluate the forecasting performance, the empirical coverage rate (ECR) is calculated as the percentage of observations that fall below the corresponding conditional quantile forecast for the last 543 data points. Besides the ECR, we also conducts two VaR backtests: the likelihood ratio test for correct conditional coverage (CC) in Christoffersen (1998) and the dynamic quantile (DQ) test in Engle and Manganelli (2004). Specifically, the null hypothesis of CC test is that, conditional on , are Bernoulli random variables with success probability being , where the hit . For the DQ test, following Engle and Manganelli (2004), we regress on a constant, four lagged hits , and the contemporaneous VaR forecast. The null hypothesis of DQ test is that the intercept is equal to the quantile level and four regression coefficients are zero. If the null hypothesis of each VaR backtest cannot be rejected, it then indicates that the VaR forecasts are satisfactory.

Table 8 gives ECRs and -values of two VaR backtests for the one-step-ahead forecasts by three fitted models. It can be seen that the ECRs of three models are all close to the corresponding nominal levels. On the other hand, in terms of two backtests, the QDAR model performs satisfactorily at four quantile levels with all -values greater than . However, the QAR model performs poorly at all levels, and the TQAR model only performs well at the 90% quantile level. This may be due to the fact that both QAR and TQAR model ignore the conditional heteroscedastic structure in stock prices.

In sum, it is necessary to consider the quantile double AR model to interpret these stock indices, and the proposed inference tools can also provide reliable results.

7 Conclusion and discussion

This paper proposes a new conditional heteroscedastic model, which has varying structures at different quantile levels, and its necessity is illustrated by analyzing the weekly S&P500 Index. A simple but ingenious transformation is introduced to the conditional scale, and this makes the AR coefficients free from nonnegative constraints. The strict stationarity of the new model is derived, and inference tools, including a self-weighted CQE and self-weighted residual QACFs-based portmanteau tests, are also constructed.

Our model can be extended in two directions. First, as far as we know, this is the first quantile conditional heteroscedastic model in the literature, and it is certainly of interest to consider other types of quantile conditional heteroscedastic time series models (Francq and Zakoian, 2010). Moreover, based on the transformation of , the proposed quantile double AR model (2.3) has a seemingly linear structure. As a result, we may consider a multivariate quantile double AR model, say with order one,

where is an -dimensional time series, , and are coefficient matrices, , and the marginal distributions of are all standard uniform; see Tsay (2014). It may be even possible to be able to handle high-dimensional time series, when the coefficient matrices and are sparsed or have a low-rank structure (Zhu et al., 2017). We leave it for future research.

Supplementary Material

The supplementary material provides additional simulation results.

Acknowledgment

We are grateful to the co-editor, associate editor and three anonymous referees for their valuable comments and suggestions, which led to substantial improvement of this article. Zhu’s research was supported by a NSFC grant 12001355, Shanghai Pujiang Program 2019PJC051 and Shanghai Chenguang Program 19CG44. Li’s research was partially supported by a Hong Kong RGC grant 17304617 and a NSFC grant 72033002.

Appendix: Technical proofs

This appendix gives the technical proofs of Theorems 1-4 and Corollary 2. Moreover, Lemmas 1-2 with proofs are also included, and they provide some preliminary results for proving Theorem 3. Throughout the appendix, the notation is a generic constant which may take different values from lines to lines. The norm of a matrix or column vector is defined as .

Proof of Theorem 1.

Let , be the class of Borel sets of , and be the Lebesgue measure on . Denote by the projection map onto the first coordinate, i.e. for . Define the function for and vectors , where , and are defined as in Section 3. As a result, is a homogeneous Markov chain on the state space , with transition probability

for and , where , with being the inverse function of , is the density function of , and is the inverse function of .

Let and . We can further show that the -step transition probability of the Markov chain is

| (A.1) |

where . Observe that, by Assumption 1, for any and with , i.e., is -irreducible.

To show that is geometrically ergodic, next we verify the Tweedie’s drift criterion (Tweedie, 1983, Theorem 4). Note that for and . Moreover, since for any constants and . Then for any , it follows that

As a result, by Assumption 1, it can be verified that, for some ,

where for . Note that , and then we can find positive values such that

| (A.2) |

Consider the test function , and we have that

where, from (A.2),

Denote , and , where is a positive constant such that as . We can verify that

and

i.e. Tweedie’s drift criterion (Tweedie, 1983, Theorem 4) holds. Moreover, is a Feller chain since, for each bounded continuous function , is continuous with respect to , and then is a small set. As a result, from Theorem 4(ii) in Tweedie (1983) and Theorems 1 and 2 in Feigin and Tweedie (1985), is geometrically ergodic with a unique stationary distribution , and

which implies that . This accomplishes the proof. ∎

Proof of Theorem 2.

Recall that , where . Define , where . To show the consistency, it suffices to verify the following claims:

-

(i)

;

-

(ii)

has a unique minimum at ;

-

(iii)

For any , as , where is an open neighborhood of with radius .

We first prove Claim (i). By Assumptions 2-3, the boundedness of , and , and the fact that , it holds that

Hence, (i) is verified.

We next prove (ii). For , it holds that

| (A.3) |

where ; see Knight (1998). Let and . By (Proof of Theorem 2.), it follows that

This, together with by Assumption 3 and , implies that

| (A.4) |

By Assumption 4, is continuous at a neighborhood of , then the above equality holds if and only if a.s. for some . Then we have

Note that and, given , is independent of all the others. As a result, it holds that and . Sequentially we can show that and for , and hence . Therefore, and (ii) is verified.

Finally, we show (iii). By Taylor expansion, it holds that

where is between and . This together with the Lipschitz continuity of , by Assumption 3, we have

tends to 0 as . Hence, Claim (iii) holds.

Based on Claims (i)-(iii), by a method similar to that in Huber (1973), we next verify the consistency. Let be any open neighborhood of . By Claim (iii), for any and , there exists an such that

| (A.5) |

From Claim (i), by the ergodic theorem, it follows that

| (A.6) |

as is large enough. Since is compact, we can choose to be a finite covering of . Then by (A.5) and (A.6), we have

| (A.7) | |||||

as is large enough. Moreover, for each , by Claim (ii), there exists an such that

| (A.8) |

Therefore, by (A.7) and (A.8), taking , it holds that

| (A.9) |

Furthermore, by the ergodic theorem, it follows that

| (A.10) |

Combing (A.9) and (A.10), we have

| (A.11) |

which implies that

By the arbitrariness of , it implies that a.s. The proof of this theorem is complete. ∎

Proof of Theorem 3.

For , define , where . Denote . By Theorem 2, it holds that . Note that is the minimizer of , since minimizes . Define . By Assumption 3 and the ergodic theorem, , where is defined in Lemma 2. Moreover, from Lemma 2, it follows that

| (A.12) | ||||

where is the smallest eigenvalue of , and is defined in Lemma 2. Note that, as , converges in distribution to a normal random variable with mean zero and variance matrix .

Since , by Assumption 3, it holds that

| (A.13) |

This together with Theorem 2, verifies the -consistency. Hence, Statement (i) holds.

Let , then we have

in distribution as . Therefore, it suffices to show that . By (A.12) and (A.13), we have

and

It follows that

| (A.14) |

Since a.s., then (Proof of Theorem 3.) implies that . We verify the asymptotic normality in Statement (ii), the proof is hence accomplished.

∎

Proof of Corollary 2.

Recall that , and . Since for a constant is assumed for , then the first and second derivative functions of are well-defined. Specifically, the first derivative function is , and the second derivative function is

| (A.15) |

with . By Taylor expansion, we have

| (A.16) |

where is between and . By Theorem 3, we have . Then both and are well-defined. To show the representation of Corollary 2, it is sufficient to show that . The definition of in (A.15) together with implies that . The proof of this corollary is complete. ∎

Proof of Theorem 4.

We first show that and for and 2. Recall that and . By the Taylor expansion, we have

and

where is between and . Then by the law of large numbers, and the fact that , it holds that

| (A.17) |

and

| (A.18) |

Similarly, we can show that

and

Since , by an elementary calculation, we have

| (A.19) |

where

First, we consider . For any , denote

Note that . Then by the Taylor expansion and the Cauchy-Schiwarz inequality, together with by Assumption 3 and the fact that is bounded by Assumption 4, it holds that

where is between and . This together with , implies that

| (A.20) |

For any and , it holds that

Then by the Taylor expansion, for any and , it can be verified that

where is between and . This together with by Assumption 3, implies that

| (A.21) |

Therefore, it follows from (A.20), (A.21) and the finite covering theorem that

| (A.22) |

Note that . Moreover, by the Taylor expansion and by Assumption 3, we can show that

where and are between and , and , , are between and . Then by the law of large numbers, Assumptions 3 and 4, it follows that

This together with (A.22) and the fact that , implies that

| (A.23) |

Next, we consider . Since , it holds that . By the Taylor expansion, the law of large numbers and the fact that , we can verify that under Assumption 3. Hence,

| (A.24) |

Finally, we consider . For any , denote and

By a method similar to the proof of (A.20) and (A.22), we can show that, for any ,

and

As a result,

which together with , implies that

| (A.25) |

Combing (A.17)-(Proof of Theorem 4.), (A.23)-(A.25) and Theorem 3, we have

Therefore, for , we have

where and .

Let . Similar to the proof of , we can show that

where and . Therefore, it follows that

where and . Note that and . These together with the law of iterated expectations, we complete the proof by the central limit theorem and the Cramér-Wold device. ∎

The following two preliminary lemmas are used to prove Theorem 3. Specifically, Lemma 1 verifies the stochastic differentiability condition defined by Pollard (1985), and the bracketing method in Pollard (1985) is used for its proof. Lemma 2 is used to obtain the -consistency and the asymptotic normality of , and its proof needs Lemma 1.

Proof.

Note that

where with being the th element of . For , define or . Denote . Let and define

To establish Lemma 1, it suffices to show that, for any ,

| (A.26) |

We follow the method in Lemma 4 of Pollard (1985) to verify (A.26). Let be a collection of functions indexed by . First, we verify that satisfies the bracketing condition defined on page 304 of Pollard (1985). Let be an open neighborhood of with radius , and define a constant to be selected later. For any and , there exists a sequence of small cubes to cover , where is an integer less than , and the constant is not depending on and ; see Huber (1967), page 227. Denote , and let and for . Note that is a partition of . For each with , define the following bracketing functions

Since the indicator function is non-decreasing and , for any , we have

| (A.27) |

Furthermore, by Taylor expansion, it holds that

| (A.28) |

Denote . By Assumption 4, we have . Choose . Then by iterated-expectation and Assumption 3, it follows that

This together with (A.27), implies that the family satisfies the bracketing condition.

Put . Let and be the annulus . From the bracketing condition, for fixed , there is a partition of . First, consider the upper tail case. For , by (A.28), it holds that

| (A.29) |

where

Define the event

For , . Then by (Proof.) and the Chebyshev’s inequality, we have

| (A.30) |

Moreover, by iterated-expectation, Taylor expansion, Assumption 4 and for , we have

This, together with by Assumption 3, by Assumption 4 and the fact that is a martingale difference sequence, implies that

| (A.31) |

Combining (Proof.) and (Proof.), we have

Similar to the proof of the upper tail case, we can obtain the same bound for the lower tail case. Therefore,

| (A.32) |

Note that as , we can choose such that for . Let be the integer such that , and split into two events and . Note that and is bounded by Assumption 3. Then by (A.32), it holds that

| (A.33) |

Furthermore, for , we have and . Similar to the proof of (Proof.) and (Proof.), we can show that

We can obtain the same bound for the lower tail. Therefore, we have

| (A.34) |

Note that as . Moreover, by the ergodic theorem, and thus as . (Proof.) together with (Proof.) asserts (A.26). The proof of this lemma is accomplished. ∎

Proof.

Denote . Let , and define the function Recall that and . By the Knight identity (Proof of Theorem 2.), it can be verified that

| (A.35) |

where

By Taylor expansion, we have , where and for between and , and is defined as (A.15). Then it follows that

| (A.36) |

where

From by Assumption 3 and the fact that , we have

Moreover, by iterated-expectation and the fact that , it follows that

Then by Theorem 3.1 in Ling and McAleer (2003), we can show that

This together with (Proof.), implies that

| (A.37) |

Denote , where

Then for , it holds that

| (A.38) |

where

Note that

| (A.39) |

Then by Taylor expansion, together with Assumption 4, it follows that

where is between 0 and . Therefore, it follows that

| (A.40) |

where and

By Taylor expansion and Assumptions 3-4, for any , it holds that

tends to as . Therefore, for any , , there exists such that

| (A.41) |

for all . Since , it follows that

| (A.42) |

as is large enough. From (A.41) and (A.42), we have

as is large enough. Therefore, . This together with (A.40), implies that

| (A.43) |

For , by Lemma 1, it holds that

| (A.44) |

Note that

| (A.45) |

Then by iterated-expectation, Taylor expansion and the Cauchy-Schiwarz inequality, together with by Assumption 3 and by Assumption 4, for any , it holds that

tends to as . Similar to (A.41) and (A.42), we can show that

| (A.46) |

For , it follows that

| (A.47) |

where

Similar to the proof of , by (A.39) we can show that, for any ,

tends to as . And for , by (A.45) we have

tends to as . Similar to (A.41) and (A.42), we can show that and . Therefore, together with (A.47), it follows that

| (A.48) |

From (A.38), (A.43)-(A.46) and (A.48), we have

| (A.49) |

In view of (Proof.), (A.37) and (A.49), we accomplish the proof of this lemma. ∎

References

- An and Chen (1982) An, H. Z. and Z. G. Chen (1982). On convergence of LAD estimates in autoregresion with infinite variance. Journal of Multivariate Analysis 12, 335–345.

- Artzner et al. (1999) Artzner, P., F. Delbaen, J. M. Eber, and D. Heath (1999). Coherent measures of risk. Mathematical Finance 9, 203–228.

- Bassett et al. (2004) Bassett, G., R. Koenker, and G. Kordas (2004). Pessimistic portfolio allocation and choquet expected utility. Journal of Financial Econometrics 4, 477–492.

- Bofinger (1975) Bofinger, E. (1975). Estimation of a density function using order statistics. Australian Journal of Statistics 17, 1–7.

- Bollerslev (1986) Bollerslev, T. (1986). Generalized autoregression conditional heteroscedasticity. Journal of Econometrics 31, 307–327.

- Box and Jenkins (1970) Box, G. E. P. and G. M. Jenkins (1970). Time Series Analysis, Forecasting and Control. San Francisco: Holden-Day.

- Cai et al. (2013) Cai, Y., G. Montes-Rojas, and J. Olmo (2013). Quantile double ar time series models for financial returns. Journal of Forecasting 32, 551–560.

- Chan and Peng (2005) Chan, N. H. and L. Peng (2005). Weighted least absolute deviations estimation for an AR(1) process with ARCH(1) errors. Biometrika 92, 477–484.

- Chernozhukov et al. (2010) Chernozhukov, V., I. Fernández-Val, and A. Galichon (2010). Quantile and probability curves without crossing. Econometrica 78, 1093–1125.

- Christoffersen (1998) Christoffersen, P. F. (1998). Evaluating interval forecasts. International economic review, 841–862.

- Davis et al. (1992) Davis, R. A., K. Knight, and J. Liu (1992). M-estimation for autoregressions with infinite variances. Stochastic Processes and their Applications 40, 145–180.

- Engle (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50, 987–1007.

- Engle and Manganelli (2004) Engle, R. F. and S. Manganelli (2004). CAViaR: conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22, 367–381.

- Feigin and Tweedie (1985) Feigin, P. D. and R. L. Tweedie (1985). Random coefficient autoregressive processes: a markov chain analysis of stationarity and finiteness of moments. Journal of Time Series Analysis 6, 1–14.

- Francq and Zakoian (2004) Francq, C. and J.-M. Zakoian (2004). Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes. Bernoulli 10, 605–637.

- Francq and Zakoian (2010) Francq, C. and J.-M. Zakoian (2010). GARCH Models: Structure, Statistical Inference and Financial Applications. Chichester, UK: John Wiley & Sons.

- Francq and Zakoian (2015) Francq, C. and J.-M. Zakoian (2015). Risk-parameter estimation in volatility models. Journal of Econometrics 184, 158–174.

- Galvao Jr et al. (2011) Galvao Jr, A. F., G. Montes-Rojas, and J. Olmo (2011). Threshold quantile autoregressive models. Journal of Time Series Analysis 32(3), 253–267.

- Gross and Steiger (1979) Gross, S. and W. L. Steiger (1979). Least absolute deviation estimates in autoregression with infinite variance. Journal of Applied Probability 16, 104–116.

- Hall and Sheather (1988) Hall, P. and S. Sheather (1988). On the distribution of a studentized quantile. Journal of the Royal Statistical Society, Series B 50, 381–391.

- Huber (1967) Huber, P. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. Proceedings of the fifth Berkeley symposium on mathematical statistics and probability 1, 221–233.

- Huber (1973) Huber, P. (1973). Robust regression: Asymptotics, conjectures and monte carlo. Annals of Statistics 1, 799–821.

- Jiang et al. (2020) Jiang, F., D. Li, and K. Zhu (2020). Non-standard inference for augmented double autoregressive models with null volatility coefficients. Journal of Econometrics 215, 165–183.

- Knight (1998) Knight, K. (1998). Limiting distributions for regression estimators under general conditions. The Annals of Statistics 26, 755–770.

- Koenker (2005) Koenker, R. (2005). Quantile regression. Cambridge: Cambridge University Press.

- Koenker and Xiao (2006) Koenker, R. and Z. Xiao (2006). Quantile autoregression. Journal of the American Statistical Association 101, 980–990.

- Koenker and Zhao (1996) Koenker, R. and Q. Zhao (1996). Conditional quantile estimation and inference for ARCH models. Econometric Theory 12, 793–813.

- Lee and Noh (2013) Lee, S. and J. Noh (2013). Quantile regression estimator for GARCH models. Scandinavian Journal of Statistics 40, 2–20.

- Li et al. (2016) Li, D., S. Ling, and R. Zhang (2016). On a threshold double autoregressive model. Journal of Business & Economic Statistics 34, 68–80.

- Li and Li (2005) Li, G. and W. K. Li (2005). Diagnostic checking for time series models with conditional heteroscedasticity estimated by the least absolute deviation approach. Biometrika 92, 691–701.

- Li and Li (2008) Li, G. and W. K. Li (2008). Least absolute deviation estimation for fractionally integrated autoregressive moving average time series models with conditional heteroscedasticity. Biometrika 95, 399–414.

- Li and Li (2009) Li, G. and W. K. Li (2009). Least absolute deviation estimation for unit root processes with GARCH errors. Econometric Theory 25, 1208–1227.

- Li et al. (2015) Li, G., Y. Li, and C.-L. Tsai (2015). Quantile correlations and quantile autoregressive modeling. Journal of the American Statistical Association 110, 246–261.

- Li et al. (2017) Li, G., Q. Zhu, Z. Liu, and W. K. Li (2017). On mixture double autoregressive time series models. Journal of Business and Economic Statistics 35, 306–317.

- Li (2004) Li, W. K. (2004). Diagnostic Checks in Time Series. Boca Raton: Chapman and Hall.

- Ling (2004) Ling, S. (2004). Estimation and testing stationarity for double-autoregressive models. Journal of the Royal Statistical Society, Series B 66, 63–78.

- Ling (2005) Ling, S. (2005). Self-weighted least absolute deviation estimation for infinite variance autoregressive models. Journal of the Royal Statistical Society: Series B 67, 381–393.

- Ling (2007) Ling, S. (2007). A double AR(p) model: structure and estimation. Statistica Sinica 17, 161–175.

- Ling and Li (2008) Ling, S. and D. Li (2008). Asymptotic inference for a nonstationary double AR(1) model. Biometrika 95, 257–263.

- Ling and McAleer (2003) Ling, S. and M. McAleer (2003). Asymptotic theory for a vector ARMA–GARCH model. Econometric Theory 19, 280–310.

- Ljung and Box (1978) Ljung, G. M. and G. E. P. Box (1978). On a measure of lack of fit in time series models. Biometrika 65, 297–303.

- Machado (1993) Machado, J. A. (1993). Robust model selection and M-estimation. Econometric Theory 9(03), 478–493.

- Pollard (1985) Pollard, D. (1985). New ways to prove central limit theorems. Econometric Theory 1, 295–314.

- Tsay (2014) Tsay, R. S. (2014). Multivariate Time Series Analysis: With R and Financial Applications. Hoboken: John Wiley & Sons.

- Tweedie (1983) Tweedie, R. L. (1983). Criteria for rates of convergence of Markov chains, with application to queueing and storage theory. In J. F. C. Kingman and G. E. H. Reuter (Eds.), Probability, Statistics and Analysis, pp. 260–276. Cambridge: Cambridge University Press.

- Weiss (1986) Weiss, A. (1986). Asymptotic theory for ARCH models: estimation and testing. Econometric Theory 2, 107–131.

- Wu and Xiao (2002) Wu, G. and Z. Xiao (2002). An analysis of risk measures. Journal of Risk 4, 53–75.

- Xiao and Koenker (2009) Xiao, Z. and R. Koenker (2009). Conditional quantile estimation for generalized autoregressive conditional heteroscedasticity models. Journal of the American Statistical Association 104, 1696–1712.

- Zheng et al. (2018) Zheng, Y., Q. Zhu, G. Li, and Z. Xiao (2018). Hybrid quantile regression estimation for time series models with conditional heteroscedasticity. Journal of the Royal Statistical Society: Series B 80, 975–993.

- Zhu and Ling (2011) Zhu, K. and S. Ling (2011). Global self-weighted and local quasi-maximum exponential likelihood estimators for ARMA-GARCH/IGARCH models. The Annals of Statistics 39, 2131–2163.

- Zhu and Ling (2013) Zhu, K. and S. Ling (2013). Quasi-maximum exponential likelihood estimators for a double AR(p) model. Statistica Sinica 23, 251–270.

- Zhu et al. (2020) Zhu, Q., G. Li, and Z. Xiao (2020). Quantile estimation of regression models with GARCH-X errors. Statistica Sinica doi: 10.5705/ss.202019.0003. To appear.

- Zhu et al. (2018) Zhu, Q., Y. Zheng, and G. Li (2018). Linear double autoregression. Journal of Econometrics 207, 162–174.

- Zhu et al. (2017) Zhu, X., R. Pan, G. Li, Y. Liu, and H. Wang (2017). Network vector autoregression. The Annals of Statistics 45, 1096–1123.

| True | Bias | ESD | True | Bias | ESD | |||||||

| Normal distribution | ||||||||||||

| -2.706 | -0.015 | 0.489 | 0.743 | 0.529 | -0.455 | -0.004 | 0.134 | 0.137 | 0.133 | |||

| -0.200 | -0.003 | 0.143 | 0.215 | 0.155 | -0.200 | -0.003 | 0.085 | 0.095 | 0.093 | |||

| -1.082 | -0.052 | 0.525 | 1.066 | 0.578 | -0.182 | -0.011 | 0.134 | 0.140 | 0.136 | |||

| -2.706 | -0.003 | 0.350 | 0.379 | 0.409 | -0.455 | -0.007 | 0.094 | 0.097 | 0.095 | |||

| -0.200 | -0.002 | 0.098 | 0.109 | 0.116 | -0.200 | 0.000 | 0.064 | 0.066 | 0.065 | |||

| -1.082 | -0.029 | 0.370 | 0.398 | 0.495 | -0.182 | -0.004 | 0.096 | 0.099 | 0.096 | |||

| Student’s distribution | ||||||||||||

| -4.060 | -0.067 | 1.030 | 1.189 | 1.184 | -0.528 | -0.008 | 0.169 | 0.179 | 0.172 | |||

| -0.200 | -0.004 | 0.235 | 0.279 | 0.274 | -0.200 | -0.001 | 0.097 | 0.111 | 0.107 | |||

| -1.624 | -0.163 | 0.996 | 1.146 | 1.211 | -0.211 | -0.017 | 0.151 | 0.162 | 0.157 | |||

| -4.060 | -0.020 | 0.726 | 0.857 | 0.847 | -0.528 | -0.009 | 0.119 | 0.126 | 0.121 | |||

| -0.200 | -0.005 | 0.162 | 0.193 | 0.194 | -0.200 | 0.000 | 0.073 | 0.077 | 0.074 | |||

| -1.624 | -0.099 | 0.683 | 0.855 | 0.879 | -0.211 | -0.008 | 0.108 | 0.113 | 0.109 | |||

| True | Bias | ESD | True | Bias | ESD | |||||||

| Normal distribution | ||||||||||||

| -2.706 | 0.011 | 0.425 | 0.558 | 0.676 | -0.455 | -0.001 | 0.122 | 0.124 | 0.123 | |||

| 0.025 | -0.006 | 0.117 | 0.146 | 0.166 | 0.125 | -0.004 | 0.074 | 0.081 | 0.080 | |||

| -0.068 | -0.090 | 0.294 | 0.520 | 0.751 | -0.057 | -0.013 | 0.085 | 0.095 | 0.098 | |||

| -2.706 | 0.014 | 0.291 | 0.349 | 0.326 | -0.455 | -0.004 | 0.082 | 0.089 | 0.085 | |||

| 0.025 | -0.005 | 0.081 | 0.093 | 0.089 | 0.125 | -0.003 | 0.054 | 0.057 | 0.055 | |||

| -0.068 | -0.046 | 0.185 | 0.275 | 0.245 | -0.057 | -0.006 | 0.060 | 0.068 | 0.064 | |||

| Student’s distribution | ||||||||||||

| -4.060 | 0.010 | 0.869 | 1.316 | 1.028 | -0.528 | -0.003 | 0.153 | 0.157 | 0.155 | |||

| 0.025 | -0.010 | 0.194 | 0.268 | 0.230 | 0.125 | -0.004 | 0.082 | 0.091 | 0.090 | |||

| -0.102 | -0.238 | 0.538 | 1.222 | 0.748 | -0.066 | -0.018 | 0.091 | 0.099 | 0.105 | |||

| -4.060 | 0.025 | 0.588 | 0.759 | 0.729 | -0.528 | -0.005 | 0.102 | 0.112 | 0.116 | |||

| 0.025 | -0.009 | 0.131 | 0.164 | 0.158 | 0.125 | -0.002 | 0.060 | 0.063 | 0.068 | |||

| -0.102 | -0.128 | 0.311 | 0.543 | 0.530 | -0.066 | -0.008 | 0.062 | 0.072 | 0.085 | |||

| Set (i) | Set (ii) | Set (iii) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Under | Exact | Over | Under | Exact | Over | Under | Exact | Over | ||||

| Normal | 500 | 3.7 | 95.3 | 1.0 | 2.9 | 95.3 | 1.8 | 4.3 | 93.7 | 2.0 | ||

| 1000 | 0.0 | 99.3 | 0.7 | 0.0 | 99.7 | 0.3 | 0.0 | 98.9 | 1.1 | |||

| 500 | 6.9 | 90.0 | 3.1 | 5.3 | 92.1 | 2.6 | 11.7 | 86.0 | 2.3 | |||

| 1000 | 0.3 | 98.1 | 1.6 | 0.1 | 99.1 | 0.8 | 0.1 | 98.5 | 1.4 | |||

| 500 | 11.6 | 81.7 | 6.7 | 9.5 | 84.6 | 5.9 | 17.8 | 80.4 | 1.8 | |||

| 1000 | 0.5 | 96.1 | 3.4 | 1.2 | 96.2 | 2.6 | 1.1 | 97.6 | 1.3 | |||

| Lag | Bias | ESD | Bias | ESD | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Normal distribution | ||||||||||

| 2 | 0.01 | 2.64 | 3.04 | 2.70 | -0.20 | 2.71 | 2.65 | 2.65 | ||

| 4 | 0.04 | 3.03 | 5.60 | 3.01 | -0.11 | 3.06 | 3.00 | 3.00 | ||

| 6 | -0.01 | 3.07 | 3.33 | 3.06 | -0.17 | 3.10 | 3.04 | 3.04 | ||

| 2 | -0.06 | 1.94 | 1.89 | 2.07 | -0.13 | 1.94 | 1.87 | 1.87 | ||

| 4 | 0.05 | 2.10 | 2.12 | 2.14 | -0.04 | 2.15 | 2.12 | 2.12 | ||

| 6 | -0.08 | 2.13 | 2.15 | 2.22 | -0.10 | 2.25 | 2.15 | 2.15 | ||

| Student’s distribution | ||||||||||

| 2 | -0.01 | 2.15 | 2.13 | 2.17 | -0.12 | 2.11 | 2.04 | 2.05 | ||

| 4 | 0.08 | 2.63 | 2.67 | 2.68 | -0.13 | 2.75 | 2.64 | 2.65 | ||

| 6 | 0.00 | 2.84 | 2.81 | 2.83 | -0.14 | 2.89 | 2.80 | 2.81 | ||

| 2 | -0.01 | 1.50 | 1.53 | 1.50 | -0.06 | 1.44 | 1.42 | 1.42 | ||

| 4 | 0.05 | 1.84 | 1.97 | 1.91 | -0.04 | 1.90 | 1.86 | 1.86 | ||

| 6 | -0.04 | 1.94 | 2.07 | 2.00 | -0.12 | 2.03 | 1.97 | 1.97 | ||

| Lag | Bias | ESD | Bias | ESD | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Normal distribution | ||||||||||

| 2 | 0.02 | 2.67 | 3.09 | 2.73 | -0.10 | 2.72 | 2.69 | 2.69 | ||

| 4 | 0.07 | 3.03 | 5.69 | 3.01 | -0.06 | 3.06 | 3.00 | 3.00 | ||

| 6 | 0.03 | 3.09 | 3.33 | 3.06 | -0.04 | 3.03 | 3.03 | 3.03 | ||

| 2 | -0.06 | 1.96 | 1.91 | 2.09 | -0.07 | 1.99 | 1.90 | 1.90 | ||

| 4 | 0.05 | 2.09 | 2.13 | 2.14 | -0.02 | 2.17 | 2.12 | 2.12 | ||

| 6 | -0.06 | 2.12 | 2.15 | 2.23 | -0.04 | 2.20 | 2.15 | 2.15 | ||

| Student’s distribution | ||||||||||

| 2 | -0.01 | 2.22 | 2.17 | 2.21 | -0.06 | 2.06 | 2.03 | 2.04 | ||

| 4 | 0.10 | 2.63 | 2.68 | 2.69 | -0.04 | 2.71 | 2.62 | 2.62 | ||

| 6 | 0.04 | 2.85 | 2.81 | 2.83 | 0.00 | 2.78 | 2.79 | 2.79 | ||

| 2 | -0.01 | 1.52 | 1.56 | 1.53 | -0.03 | 1.46 | 1.40 | 1.40 | ||

| 4 | 0.04 | 1.84 | 1.97 | 1.91 | 0.00 | 1.93 | 1.84 | 1.84 | ||

| 6 | -0.02 | 1.93 | 2.00 | 2.01 | -0.07 | 1.97 | 1.96 | 1.96 | ||

| Normal distribution | |||||||||

| 500 | 0.0 | 0.0 | 3.5 | 3.7 | 3.6 | 5.5 | 4.4 | 5.8 | |

| 0.1 | 0.0 | 8.3 | 7.3 | 7.4 | 15.7 | 9.0 | 13.3 | ||

| 0.3 | 0.0 | 47.3 | 41.8 | 45.6 | 92.4 | 53.4 | 89.5 | ||

| 0.0 | 0.1 | 6.3 | 6.2 | 6.6 | 6.5 | 6.4 | 6.5 | ||

| 0.0 | 0.3 | 13.7 | 14.1 | 13.7 | 7.4 | 11.2 | 9.5 | ||

| 1000 | 0.0 | 0.0 | 5.2 | 5.2 | 5.3 | 4.7 | 6.2 | 5.7 | |

| 0.1 | 0.0 | 12.9 | 11.4 | 12.2 | 28.1 | 16.0 | 25.1 | ||

| 0.3 | 0.0 | 83.6 | 78.3 | 81.4 | 99.9 | 90.2 | 99.8 | ||

| 0.0 | 0.1 | 7.4 | 7.2 | 7.4 | 5.7 | 6.5 | 5.7 | ||

| 0.0 | 0.3 | 16.5 | 19.2 | 18.1 | 6.2 | 16.3 | 11.8 | ||

| Student’s distribution | |||||||||

| 500 | 0.0 | 0.0 | 5.6 | 5.5 | 5.6 | 5.7 | 5.2 | 5.3 | |

| 0.1 | 0.0 | 7.8 | 6.1 | 6.8 | 15.7 | 6.6 | 11.5 | ||

| 0.3 | 0.0 | 32.4 | 19.1 | 26.9 | 93.4 | 27.8 | 86.3 | ||

| 0.0 | 0.1 | 11.8 | 12.3 | 12.2 | 6.8 | 8.2 | 7.7 | ||

| 0.0 | 0.3 | 31.1 | 32.0 | 32.9 | 7.6 | 17.9 | 16.0 | ||

| 1000 | 0.0 | 0.0 | 5.6 | 5.6 | 5.6 | 4.6 | 6.5 | 5.2 | |

| 0.1 | 0.0 | 10.3 | 7.0 | 7.8 | 30.0 | 11.0 | 23.4 | ||

| 0.3 | 0.0 | 60.7 | 37.9 | 53.5 | 99.8 | 56.8 | 99.7 | ||

| 0.0 | 0.1 | 13.9 | 15.2 | 14.1 | 6.4 | 10.5 | 9.1 | ||

| 0.0 | 0.3 | 42.7 | 52.0 | 49.9 | 8.6 | 30.0 | 23.2 | ||

| Student’s distribution | |||||||||

| 500 | 0.0 | 0.0 | 6.9 | 6.3 | 6.6 | 5.3 | 4.6 | 5.2 | |

| 0.1 | 0.0 | 8.9 | 7.4 | 8.3 | 14.8 | 6.1 | 10.7 | ||

| 0.3 | 0.0 | 28.1 | 14.1 | 22.1 | 91.9 | 14.4 | 82.8 | ||

| 0.0 | 0.1 | 16.8 | 17.2 | 18.1 | 7.5 | 9.0 | 8.5 | ||

| 0.0 | 0.3 | 41.8 | 43.0 | 43.3 | 7.2 | 20.6 | 17.5 | ||

| 1000 | 0.0 | 0.0 | 5.8 | 6.3 | 6.5 | 4.5 | 5.4 | 5.2 | |

| 0.1 | 0.0 | 10.0 | 7.2 | 9.0 | 29.3 | 6.3 | 21.0 | ||

| 0.3 | 0.0 | 50.5 | 22.3 | 39.8 | 99.7 | 25.0 | 99.3 | ||

| 0.0 | 0.1 | 24.5 | 27.4 | 27.0 | 7.7 | 13.2 | 12.2 | ||

| 0.0 | 0.3 | 60.3 | 63.8 | 63.6 | 8.3 | 34.7 | 28.4 | ||

|

|

| ECR | CC | DQ | ECR | CC | DQ | ECR | CC | DQ | ECR | CC | DQ | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| M1 | 5.34 | 0.88 | 0.33 | 9.02 | 0.34 | 0.22 | 91.53 | 0.25 | 0.11 | 95.95 | 0.23 | 0.51 | |||

| M2 | 5.16 | 0.17 | 0.00 | 9.58 | 0.03 | 0.00 | 92.45 | 0.08 | 0.00 | 95.95 | 0.33 | 0.00 | |||

| M3 | 6.45 | 0.20 | 0.01 | 10.13 | 0.81 | 0.02 | 91.34 | 0.19 | 0.12 | 95.03 | 0.42 | 0.02 | |||