The Perils of Exploration under Competition:

A Computational Modeling Approach

Abstract.

We empirically study the interplay between exploration and competition. Systems that learn from interactions with users often engage in exploration: making potentially suboptimal decisions in order to acquire new information for future decisions. However, when multiple systems are competing for the same market of users, exploration may hurt a system’s reputation in the near term, with adverse competitive effects. In particular, a system may enter a “death spiral”, when the short-term reputation cost decreases the number of users for the system to learn from, which degrades the system’s performance relative to competition and further decreases the market share.

We ask whether better exploration algorithms are incentivized under competition. We run extensive numerical experiments in a stylized duopoly model in which two firms deploy multi-armed bandit algorithms and compete for myopic users. We find that duopoly and monopoly tend to favor a primitive “greedy algorithm” that does not explore and leads to low consumer welfare, whereas a temporary monopoly (a duopoly with an early entrant) may incentivize better bandit algorithms and lead to higher consumer welfare. Our findings shed light on the first-mover advantage in the digital economy by exploring the role that data can play as a barrier to entry in online markets.

1. Introduction

Many modern online platforms simultaneously compete for users as well as learn from the users they manage to attract. This creates a tension between exploration and competition: firms experiment with potentially sub-optimal options for the sake of gaining information to make better decisions tomorrow, while they need to incentivize consumers to select them over their competitors today. For instance, Google Search and Bing compete for users in the search engine market yet at the same time need to experiment with their search and ranking algorithms to learn what works best. Similar exploration vs. competition tension arises in other application domains: recommendation systems, news and entertainment websites, online commerce, and so forth.

Online platforms routinely deploy A/B tests, and are increasingly adopting more sophisticated exploration methodologies based on multi-armed bandits, a well-known framework for making decisions under uncertainty and trading off exploration and exploitation (making good near-term decisions). While deploying “better” learning algorithms for exploration would improve performance, this is not necessarily beneficial under competition, even putting aside the deployment/maintenance costs. In particular, excessive experimentation may hurt a platform’s reputation and decrease its market share in the near term. This would leave the learning algorithm with less users to learn from, which may further degrade the platform’s performance relative to competitors who keep learning and improving from their users, and so forth. Taken to the extreme, such dynamics may create a “death spiral” effect when the vast majority of customers eventually switch to competitors.

In this paper, we ask how the interplay of exploration and competition affects platforms’ incentives. While some bandit algorithms are traditionally considered “better” than others in the literature, does competition incentivize the adoption of the better algorithms? How is this affected by the intensity of competition? We investigate these issues via extensive numerical experiments in a stylized duopoly model.

Our model. We consider two firms that compete for users and simultaneously learn from them. Each firm commits to a multi-armed bandit algorithm, and explores according to this algorithm. Users select between the two firms based on the current reputation score: rewards from the firm’s algorithm, averaged over a recent time window. Each firm’s objective is to maximize its market share (the fraction of users choosing this firm).

We consider a permanent duopoly in which both firms start at the same time, as well as temporary monopoly: a duopoly with a first-mover. Accordingly, the intensity of competition in the model varies from “permanent monopoly” (just one firm) to “incumbent” (the first-mover in temporary monopoly) to permanent duopoly to “entrant” (late-arriver in temporary monopoly).111We consider the “permanent monopoly” scenario for comparison only, without presenting any findings. We just assume that a monopolist chooses the greedy algorithm, because it is easier to deploy in practice. Implicitly, users have no “outside option”: the service provided is an improvement over not having it (and therefore the monopolist is not incentivized to deploy better learning algorithms). This is plausible with free ad-supported platforms such as Yelp or Google.

We focus on three classes of bandit algorithms, ranging from more primitive to more sophisticated: greedy algorithms that do not explicitly explore, algorithms that separate exploration and exploitation, and algorithms that combine the two. We know from prior work that in the absence of competition, “better” algorithms are better in the long run, but could be worse initially.

Main findings. We find that in the permanent duopoly, competition incentivizes firms to choose the “greedy algorithm”, and even more so if the firm is a late arriver in a market. This algorithm also prevails under monopoly, simply because it tends to be easier to deploy. Whereas the incumbent in the temporary monopoly is incentivized to deploy a more advanced exploration algorithm. As a result, consumer welfare is highest under temporary monopoly. We find strong evidence of the “death spiral” effect mentioned earlier; this effect is strongest under permanent duopoly.

Interpreting the adoption of better algorithms as “innovation”, our findings can be framed in terms of the “inverted-U relationship” between competition and innovation (see Figure 1). This is a well-established concept in the economics literature, dating back to (Schumpeter-42, ), whereby too little or too much competition is bad for innovation, but intermediate levels of competition tend to be better. However, the “inverted-U relationship” is driven by different aspects in our model than the ones in the existing literature in economics. In our case, the barriers for innovations arise entirely from the reputational consequences of exploration in competition, as opposed to the R&D costs (which is the more standard cause in prior work).

Additional findings. We investigate the “first-mover advantage” phenomenon in more detail. Being first in the market gives free data to learn from (a “data advantage”) as well as a more definite, and possibly better reputation compared to an entrant (a “reputation advantage”). We run additional experiments so as to isolate and compare these two effects. We find that either effect alone leads to a significant advantage under competition. The data advantage is larger than reputation advantage when the incumbent commits to a more advanced bandit algorithm.

Data advantage is significant from the anti-trust perspective, as a possible barrier to entry. We find that even a small amount “data advantage” gets amplified under competition, causing a large difference in eventual market shares. This observation runs contrary to prior work (varian2018artificial, ; lambrecht2015can, ; bajari2018impact, ), which studied learning without competition, and found that small amounts of additional data do not provide significant improvement in eventual outcomes. We conclude that competition dynamics – that firms compete as they learn over time – are pertinent to these anti-trust considerations.

We also investigate how algorithms’ performance “in isolation” (without competition) is predictive of the outcomes under competition. We find that mean reputation – arguably, the most natural performance measure “in isolation” – is sometimes not a good predictor. We suggest a more refined performance measure, and use it to explain some of the competition outcomes.

We also consider an alternative choice rule with explicit noise/randomness: a small fraction of users choose a firm uniformly at random.222Reputation scores already introduce some noise into users’ choices. However, the amount of noise due to this channel is typically small, both in our simulations and in practice, because reputation signals average over many datapoints. We confirm the theoretical intuition that better algorithms prevail if the expected number of “random” users is sufficiently large. However, we find that this effect is negligible for some smaller but still “relevant” parameter values.

1.1. Discussion

The present paper is an experimental counterpart to (CompetingBandits-itcs18, ), which considered a similar duopoly model and obtained a number of theoretical results with “asymptotic” flavor. For the sake of analytical tractability, that paper makes a somewhat unrealistic simplification that users do not observe any signals about firms’ ongoing performance. Instead, users choose between firms according to the firms’ Bayesian-expected rewards. The strength of competition is varied in a different way, using assumptions about (ir)rational user behavior. For these reasons, the theorems from (CompetingBandits-itcs18, ) have no direct bearing on our simulations. However, their high-level conclusion in is an inverted-U relationship similar to ours.

The present paper provides a more nuanced and “non-asymptotic” perspective. In essence, we look for substantial effects within relevant time scales. Indeed, we start our investigation by determining what time scales are relevant in the context of our model. The reputation-based choice model accounts for competition in a more direct way, allows to separate reputation vs. data advantage, and makes our model amenable to numerical simulations (unlike the model in (CompetingBandits-itcs18, )).

To elucidate the interplay of competition and exploration, our model is stylized in several important respects, some of which we discuss below. Firms compete only on the quality of service, rather than, say, pricing or the range of products. Various performance signals available to the users, from personal experience to word-of-mouth to consumer reports, are abstracted as persistent “reputation scores”, which further simplified to average performance over a time window. On the machine learning side, our setup is geared to distinguish between “simple” vs. “better” vs. “smart” bandit algorithms; we are not interested in state-of-art algorithms for very realistic bandit settings.

Even with a stylized model, numerical investigation is quite challenging. An “atomic experiment” is a competition game between a given pair of bandit algorithms, in a given competition model, on a given instance of a multi-armed bandit problem.333Each such experiment is run many times to reduce variance. Accordingly, we have a three-dimensional space of atomic experiments one needs to run and interpret: {pairs of algorithms} x {competition models} x {bandit instances}, and we are looking for findings that are consistent across this entire space. It is essential to keep each of the three dimensions small yet representative. In particular, we need to capture a huge variety of bandit instances with only a few representative examples. Further, one needs succinct and informative summarization of results within one atomic experiment and across multiple experiments (e.g., see Table 1).

While amenable to simulations, our model appears difficult to analyze. This is for several reasons: intricate feedback loop from performance to reputations to users to performance; mean reputation, most connected to our intuition, is sometimes a bad predictor in competition (see Sections 3 and 6); mathematical tools from regret-minimization would only produce “asymptotic” results, which do not seem to suffice. Further, we believe that resolving first-order theoretical questions about our model would not add much value to this paper. Indeed, we are in the realm of stylized economic models that provide mathematical intuition about the world, and (CompetingBandits-itcs18, ) already has an elaborate analysis with similar high-level conclusions.

1.2. Related work

Machine learning. Multi-armed bandits (MAB) is a tractable abstraction for the tradeoff between exploration and exploitation. MAB problems have been studied for many decades, see (Bubeck-survey12, ; LS19bandit-book, ) for background on this immense body of work; we only comment on the most related aspects.

We consider MAB with i.i.d. rewards, a well-studied and well-understood MAB model (bandits-ucb1, ). We focus on a well-known distinction between “greedy” (exploitation-only) algorithms, “naive” algorithms that separate exploration and exploitation, and “smart” algorithms that combine them. Switching from “greedy” to “naive” to “smart” algorithms involves substantial adoption costs in infrastructure and personnel training (MWT-WhitePaper-2016, ; DS-arxiv, ).

The study of competition vs. exploration has been initiated in (CompetingBandits-itcs18, ), as discussed above. Our setting is also closely related to the “dueling algorithms” framework (DuelingAlgs-stoc11, ), but this framework considers offline / full feedback scenarios whereas we focus on online machine learning problems.

In “dueling bandits” (e.g., (Yue-dueling-icml09, ; Yue-dueling12, )), an algorithm sets up a “duel” between a pair of arms in each round, and only learns which arm has “won”. While this setting features a form of competition inside an MAB problem, it is very different from ours.

The interplay between exploration, exploitation and incentives has been studied in other scenarios: incentivizing exploration in a recommendation system, e.g., (Kremer-JPE14, ; Frazier-ec14, ; Che-13, ; ICexploration-ec15, ; Bimpikis-exploration-ms17, ), dynamic auctions (see (DynAuctions-survey10, ) for background), online ad auctions, e.g., (MechMAB-ec09, ; DevanurK09, ; NSV08, ; Transform-ec10-jacm, ), human computation (RepeatedPA-ec14, ; Ghosh-itcs13, ; Krause-www13, ), and repeated auctions, e.g., (Amin-auctions-nips13, ; Amin-auctions-nips14, ; Jieming-ec18, ).

Economics. Our work is related to a longstanding economics literature on competition vs. innovation, e.g., (Schumpeter-42, ; barro2004economic, ; Aghion-QJE05, ). While this literature focuses on R&D costs of innovation, “reputational costs” seem new and specific to exploration.

Whether data gives competitive advantage has been studied theoretically in (varian2018artificial, ; lambrecht2015can, ) and empirically in (bajari2018impact, ). While these papers find that small amounts of additional data do not provide significant improvement, they focus on learning in isolation. The first-mover advantage has been well-studied in other settings in economics and marketing, see survey (kerin1992first, ).

The most common measures of market “competitiveness” such as the Lerner Index or the Herfindahl-Hirschman Index of a market rely on ex-post observable attributes of a market such as prices or market shares (tirole1988theory, ). However, neither is applicable to our setting: in our model, there are no prices, and market shares are endogenous.

2. Model and Preliminaries

We consider a game involving two firms and customers (henceforth, agents). The game lasts for rounds. In each round, a new agent arrives, chooses among the two firms, interacts with the chosen firm, and leaves forever.

Each interaction between a firm and an agent proceeds as follows. There is a set of actions, henceforth arms, same for both firms and all rounds. The firm chooses an arm, and the agent experiences a numerical reward observed by the firm. Each arm corresponds to a different version of the experience that a firm can provide for an agent, and the reward corresponds to the agent’s satisfaction level. The other firm does not observe anything about this interaction, not even the fact that this interaction has happened.

From each firm’s perspective, the interactions with agents follow the protocol of the multi-armed bandit problem (MAB). We focus on i.i.d. Bernoulli rewards: the reward of each arm is drawn from independently with expectation . The mean rewards are the same for all rounds and both firms, but initially unknown.

Before the game starts, each firm commits to an MAB algorithm, and uses this algorithm to choose its actions. Each algorithm receives a “warm start”: additional agents that arrive before the game starts, and interact with the firm as described above. The warm start ensures that each firm has a meaningful reputation when competition starts. Each firm’s objective is to maximize its market share: the fraction of users who chose this firm.

In some of our experiments, one firm is the “incumbent” who enters the market before the other (“late entrant”), and therefore enjoys a temporary monopoly. Formally, the incumbent enjoys additional rounds of the “warm start”. We treat as an exogenous element of the model, and study the consequences for a fixed .

Agents. Firms compete on a single dimension, quality of service, as expressed by agents’ rewards. Agents are myopic and non-strategic: they would like to choose among the firms so as to maximize their expected reward (i.e. select the firm with the highest quality), without attempting to influence the firms’ learning algorithms or rewards of the future users. Agents are not well-informed: they only receive a rough signal about each firm’s performance before they choose a firm, and no other information.

Concretely, each of the two firms has a reputation score, and each agent’s choice is driven by these two numbers. We posit a version of rational behavior: each agent chooses a firm with a maximal reputation score (breaking ties uniformly). The reputation score is simply a sliding window average: an average reward of the last agents that chose this firm.

MAB algorithms. We consider three classes of algorithms, ranging from more primitive to more sophisticated:

-

(1)

Greedy algorithms that strive to take actions with maximal mean reward, based on the current information.

-

(2)

Exploration-separating algorithms that separate exploration and exploitation. The “exploitation” choices strives to maximize mean reward in the next round, and the “exploration” choices do not use the rewards observed so far.

-

(3)

Adaptive exploration: algorithms that combine exploration and exploitation, and sway the exploration choices towards more promising alternatives.

We are mainly interested in qualitative differences between the three classes. For concreteness, we fix one algorithm from each class. Our pilot experiments indicate that our findings do not change substantially if other algorithms are chosen. For technical reasons, we consider Bayesian versions initialized with a “fake” prior (i.e., not based on actual knowledge). We consider:

-

(1)

a greedy algorithm that chooses an arm with largest posterior mean reward. We call it ”Dynamic Greedy” (because the chosen arm may change over time), in short.

-

(2)

an exploration-separated algorithm that in each round, explores with probability : chooses an arm independently and uniformly at random, and with the remaining probability exploits according to . We call it “dynamic epsilon-greedy”, in short.444Throughout, we fix . Our pilot experiments showed that different did not qualitatively change the results.

-

(3)

an adaptive-exploration algorithm called “Thompson Sampling” (). In each round, this algorithm updates the posterior distribution for the mean reward of each arm , draws an independent sample from this distribution, and chooses an arm with the largest .

For ease of comparison, all three algorithms are parameterized with the same fake prior: namely, the mean reward of each arm is drawn independently from a distribution. Recall that Beta priors with 0-1 rewards form a conjugate family, which allows for simple posterior updates.

Both and are classic and well-understood MAB algorithms, see (Bubeck-survey12, ; TS-survey-FTML18, ) for background. It is well-known that is near-optimal in terms of the cumulative rewards, and is very suboptimal, but still much better than .555Formally, achieves regret and , where is the gap in mean rewards between the best and second-best arms. has regret in the worst case. And can have regret as high as . Deeper discussion of these distinctions is not very relevant to this paper. In a stylized formula: as stand-alone MAB algorithms.

MAB instances. We consider instances with arms. Since we focus on 0-1 rewards, an instance of the MAB problem is specified by the mean reward vector . Initially this vector is drawn from some distribution, termed MAB instance. We consider three MAB instances:

-

(1)

Needle-In-Haystack: one arm (the “needle”) is chosen uniformly at random. This arm has mean reward , and the remaining ones have mean reward .

-

(2)

Uniform instance: the mean reward of each arm is drawn independently and uniformly from .

-

(3)

Heavy-Tail instance: the mean reward of each arm is drawn independently from distribution (which is known to have substantial “tail probabilities”).

We argue that these MAB instances are (somewhat) representative. Consider the “gap” between the best and the second-best arm, an essential parameter in the literature on MAB. The “gap” is fixed in Needle-in-Haystack, spread over a wide spectrum of values under the Uniform instance, and is spread but focused on the large values under the Heavy-Tail instance. We also ran smaller experiments with versions of these instances, and achieved similar qualitative results.

Terminology. Following a standard game-theoretic terminology, algorithm Alg1 (weakly) dominates algorithm Alg2 for a given firm if Alg1 provides a larger (or equal) market share than Alg2 at the end of the game. An algorithm is a (weakly) dominant strategy for the firm if it (weakly) dominates all other algorithms. This is for a particular MAB instance and a particular selection of the game parameters.

Simulation details. For each MAB instance we draw mean reward vectors independently from the corresponding distribution. We use this same collection of mean reward vectors for all experiments with this MAB instance. For each mean reward vector we draw a table of realized rewards (realization table), and use this same table for all experiments on this mean reward vector. This ensures that differences in algorithm performance are not due to noise in the realizations but due to differences in the algorithms in the different experimental settings.

More specifically, the realization table is a 0-1 matrix with columns which correspond to arms, and rows, which correspond to rounds. Here is the maximal duration of the “warm start” in our experiments, i.e., the maximal value of . For each arm , each value is drawn independently from Bernoulli distribution with expectation . Then in each experiment, the reward of this arm in round of the warm start is taken to be , and its reward in round of the game is .

We fix the sliding window size . We found that lower values induced too much random noise in the results, and increasing further did not make a qualitative difference. Unless otherwise noted, we used .

The simulations are computationally intensive. An experiment on a particular MAB instance comprised multiple runs of the competition game: mean reward vectors times pairs of algorithms times three values for the warm start. We used a parallel implementation over a cluster of 12 2.2 GHz CPU cores, with 8 GB RAM per core. Each experiment took about hours.

Consistency. While we experiment with various MAB instances and parameter settings, we only report on selected, representative experiments in the body of the paper. Additional plots and tables are provided in the appendix. Unless noted otherwise, our findings are based on and consistent with all these experiments.

3. Performance in Isolation

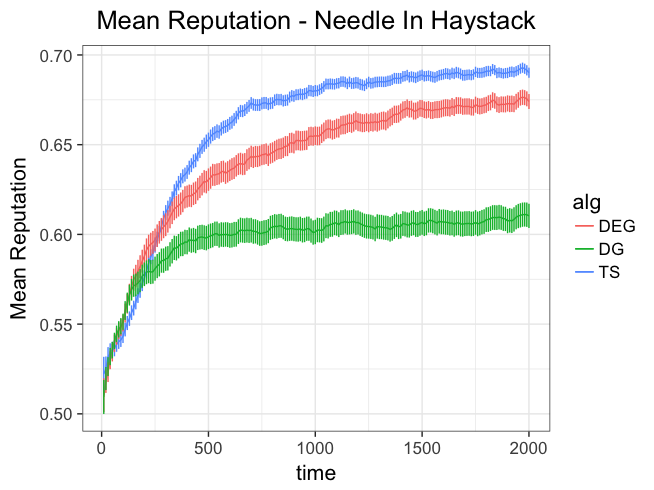

We start with a pilot experiment in which we investigate each algorithm’s performance “in isolation”: in a stand-alone MAB problem without competition. We focus on reputation scores generated by each algorithm. We confirm that algorithms’ performance is ordered as we’d expect: for a sufficiently long time horizon. For each algorithm and each MAB instance, we compute the mean reputation score at each round, averaged over all mean reward vectors. We plot the mean reputation trajectory: how this score evolves over time. Figure 2 shows such a plot for the Needle-in-Haystack instance; for other MAB instances the plots are similar. We summarize this finding as follows:

Finding 1.

The mean reputation trajectories are arranged as predicted by prior work: for a sufficiently long time horizon.

We also use Figure 2 to choose a reasonable time-horizon for the subsequent experiments, as . The idea is, we want to be large enough so that algorithms performance starts to plateau, but small enough such that algorithms are still learning.

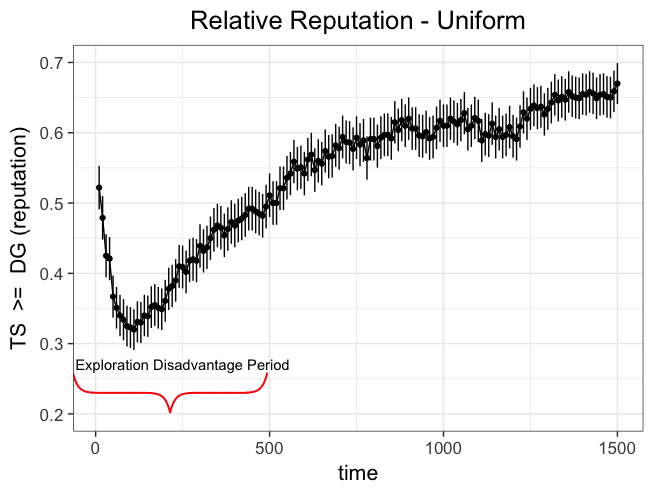

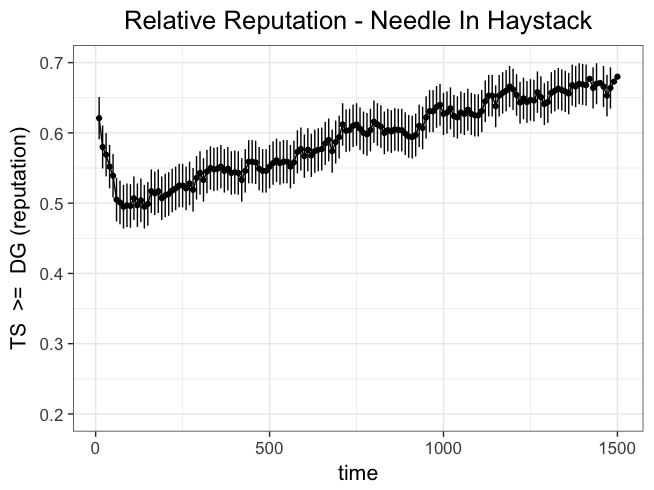

The mean reputation trajectory is probably the most natural way to represent an algorithm’s performance on a given MAB instance. However, we found that the outcomes of the competition game are better explained with a different “performance-in-isolation” statistic that is more directly connected to the game. Consider the performance of two algorithms, Alg1 and Alg2, “in isolation” on a particular MAB instance. The relative reputation of Alg1 (vs. Alg2) at a given time is the fraction of mean reward vectors/realization tables for which Alg1 has a higher reputation score than Alg2. The intuition is that agent’s selection in our model depends only on the comparison between the reputation scores.

This angle allows a more nuanced analysis of reputation costs vs. benefits under competition. Figure 3 (top) shows the relative reputation trajectory for vs for the Uniform instance. The relative reputation is less than in the early rounds, meaning that has a higher reputation score in a majority of the simulations, and more than later on. The reason is the exploration in leads to worse decisions initially, but allows for better decisions later. The time period when relative reputation vs. dips below can be seen as an explanation for the competitive disadvantage of exploration. Such period also exists for the Heavy-Tail MAB instance. However, it does not exist for the Needle-in-Haystack instance, see Figure 3 (bottom).666We see two explanations for this: identifies the best arm faster for the Needle-in-Haystack instance, and there are no “very bad” arms which make exploration very expensive in the short term.

Finding 2.

Exploration can lead to relative reputation vs. going below for some initial time period. This happens for some MAB instances but not for some others.

Definition 3.1.

For a particular MAB algorithm, a time period when relative reputation vs. goes below is called exploration disadvantage period. An MAB instance is called exploration-disadvantaged if such period exists.

Uniform and Heavy-tail instance are exploration-disadvantaged, but Needle-in-Haystack is not.

4. Competition vs. Better Algorithms

| Heavy-Tail | Needle-in-Haystack | |||||

| = 20 | = 250 | = 500 | = 20 | = 250 | = 500 | |

| vs | 0.29 0.03 55 (0) | 0.72 0.02 570 (0) | 0.76 0.02 620 (99) | 0.64 0.03 200 (27) | 0.6 0.03 370 (0) | 0.64 0.03 580 (122) |

| vs | 0.3 0.03 37 (0) | 0.88 0.01 480 (0) | 0.9 0.01 570 (114) | 0.57 0.03 150 (14) | 0.52 0.03 460 (79) | 0.56 0.02 740 (628) |

| vs | 0.62 0.03 410 (7) | 0.6 0.02 790 (762) | 0.57 0.03 730 (608) | 0.46 0.03 340 (129) | 0.42 0.02 650 (408) | 0.42 0.02 690 (467) |

Our main experiments are with the duopoly game defined in Section 2. As the “intensity of competition” varies from permanent monopoly to “incumbent” to permanent duopoly to “late entrant”, we find a stylized inverted-U relationship as in Figure 1. More formally, we look for equilibria in the duopoly game, where each firm’s choices are limited to , and . We do this for each “intensity level” and each MAB instance, and look for findings that are consistent across MAB instances. For cleaner results, we break ties towards less advanced algorithms (as they tend to have lower adoption costs (MWT-WhitePaper-2016, ; DS-arxiv, )). Note that is trivially the dominant strategy under permanent monopoly.

Permanent duopoly. The basic scenario is when both firms are competing from round . A crucial distinction is whether an MAB instance is exploration-disadvantaged:

Finding 3.

Under permanent duopoly:

-

(a)

(,) is the unique pure-strategy Nash equilibrium for exploration-disadvantaged MAB instances with a sufficiently small “warm start”.

-

(b)

This is not necessarily the case for MAB instances that are not exploration-disadvantaged. In particular, is a weakly dominant strategy for Needle-in-Haystack.

We investigate the firms’ market shares when they choose different algorithms (otherwise, by symmetry both firms get half of the agents). We report the market shares for Heavy-Tail and Needle-in-Haystack instances in Table 1 (see the first line in each cell), for a range of values of the warm start . Table 2 reports similarly on the Uniform instance. We find that is a weakly dominant strategy for the Heavy-Tail and Uniform instances, as long as is sufficiently small. However, is a weakly dominant strategy for the Needle-in-Haystack instance. We find that for a sufficiently small , yields more than half the market against , but achieves similar market share vs. and . By our tie-breaking rule, (,) is the only pure-strategy equilibrium.

| = 20 | = 250 | = 500 | |

| vs | 0.46 0.03 | 0.52 0.02 | 0.6 0.02 |

| vs | 0.41 0.03 | 0.51 0.02 | 0.55 0.02 |

| vs | 0.51 0.03 | 0.48 0.02 | 0.45 0.02 |

We attribute the prevalence of on exploration-disadvantaged MAB instances to its prevalence on the initial “exploration disadvantage period”, as described in Section 3. Increasing the warm start length makes this period shorter: indeed, considering relative reputation trajectory in Figure 3 (top), increasing effectively shifts the starting time point to the right. This is why it helps if is small.

Temporary Monopoly. We turn our attention to the temporary monopoly scenario. Recall that the incumbent firm enters the market and serves as a monopolist until the entrant firm enters at round . We make large enough, but still much smaller than the time horizon . We find that the incumbent is incentivized to choose , in a strong sense:

Finding 4.

Under temporary monopoly, is the dominant strategy for the incumbent. This holds across all MAB instances, if is large enough.

The simulation results for the Heavy-Tail MAB instance are reported in Table 3, for a particular . We see that is a dominant strategy for the incumbent. Similar tables for the other MAB instances and other values of are reported in the supplement, with the same conclusion.

| 0.0030.003 | 0.0830.02 | 0.170.02 | |

| 0.0450.01 | 0.250.02 | 0.230.02 | |

| 0.120.02 | 0.360.03 | 0.30.02 |

is a weakly dominant strategy for the entrant, for Heavy-Tail instance in Table 3 and the Uniform instance, but not for the Needle-in-Haystack instance. We attribute this finding to exploration-disadvantaged property of these two MAB instance, for the same reasons as discussed above.

Finding 5.

Under temporary monopoly, is a weakly dominant strategy for the entrant for exploration-disadvantaged MAB instances.

Inverted-U relationship. We interpret our findings through the lens of the inverted-U relationship between the “intensity of competition” and the “quality of technology”. The lowest level of competition is monopoly, when wins out for the trivial reason of tie-breaking. The highest levels are permanent duopoly and “late entrant”. We see that is incentivized for exploration-disadvantaged MAB instances. In fact, incentives for get stronger when the model transitions from permanent duopoly to “late entrant”.777For the Heavy-Tail instance, goes from a weakly dominant startegy to a strictly dominant one. For the Uniform instance, goes from a Nash equilibrium strategy to a weakly dominant one. Finally, the middle level of competition, “incumbent” in the temporary monopoly creates strong incentives for . In stylized form, this relationship is captured in Figure 1.

Our intuition for why incumbency creates more incentives for exploration is as follows. During the temporary monopoly period, reputation costs of exploration vanish. Instead, the firm wants to improve its performance as much as possible by the time competition starts. Essentially, the firm only faces a classical explore-exploit tradeoff, and is incentivized to choose algorithms that are best at optimizing this tradeoff.

Death spiral effect. Further, we investigate the “death spiral” effect mentioned in the Introduction. Restated in terms of our model, the effect is that one firm attracts new customers at a lower rate than the other, and falls behind in terms of performance because the other firm has more customers to learn from, and this gets worse over time until (almost) all new customers go to the other firm. With this intuition in mind, we define effective end of game () for a particular mean reward vector and realization table, as the last round such that the agents at this and previous round choose different firms. Indeed, the game, effectively, ends after this round. We interpret low as a strong evidence of the “death spiral” effect. Focusing on the permanent duopoly scenario, we specify the values in Table 1 (the second line of each cell). We find that the values are indeed small:

Finding 6.

Under permanent duopoly, values tend to be much smaller than the time horizon .

We also see that the values tend to increase as the warm start increases. We conjecture this is because larger tends to be more beneficial for a better algorithm (as it tends to follow a better learning curve). Indeed, we know that the “effective end of game” in this scenario typically occurs when a better algorithm loses, and helping it delays the loss.

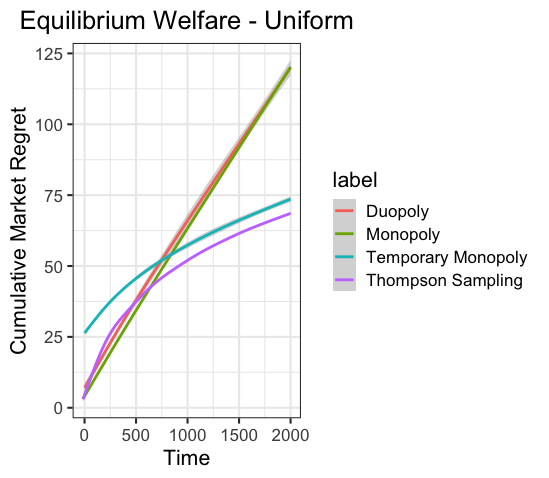

Welfare implications. We study the effects of competition on consumer welfare: the total reward collected by the users over time. Rather than welfare directly, we find it more lucid to consider market regret:

where is the arm chosen by agent . This is a standard performance measure in the literature on multi-armed bandits. Note that smaller regret means higher welfare.

We assume that both firms play their respective equilibrium strategies for the corresponding competition level. As discussed previously, these are:

-

•

in the monopoly,

-

•

for both firms in duopoly (Finding 3),

- •

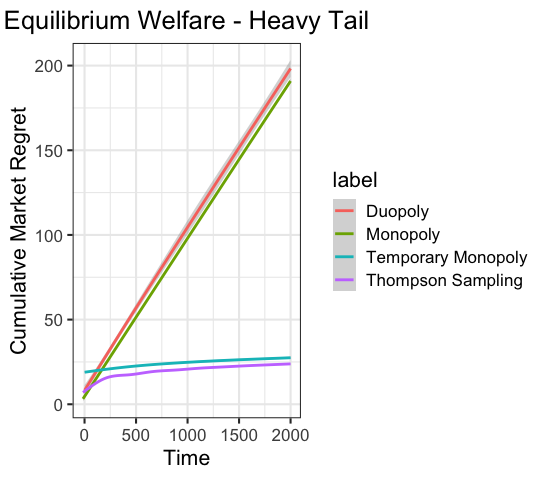

Figure 4 displays the market regret (averaged over multiple runs) under different levels of competition. Consumers are better off in the temporary monopoly case than in the duopoly case. Recall that under temporary monopoly, the incumbent is incentivized to play . Moreover, we find that the welfare is close to that of having a single firm for all agents and running . We also observe that monopoly and duopoly achieve similar welfare.

Finding 7.

In equilibrium, consumer welfare is (a) highest under temporary monopoly, (b) similar for monopoly and duopoly.

Finding 7(b) is interesting because, in equilibrium, both firms play in both settings, and one might conjecture that the welfare should increase with the number of firms playing . Indeed, one run of may get stuck on a bad arm. However, two firms independently playing are less likely to get stuck simultaneously. If one firm gets stuck and the other does not, then the latter should attract most agents, leading to improved welfare.

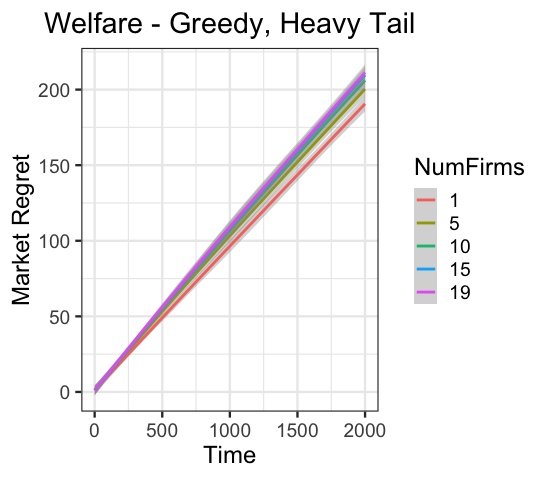

To study this phenomenon further, we go beyond the duopoly setting to more than two firms playing (and starting at the same time). Figure 5 reports the average welfare across these simulations. Welfare not only does not get better, but is weakly worse as we increase the number of firms.

Finding 8.

When all firms deploy , and start at the same time, welfare is weakly decreasing as the number of firms increases

We track the average in each of the simulations and notice that it increases with the number of firms. This observation also runs counter of the intuition that with more firms running , one of them is more likely to “get lucky” and take over the market (which would cause to decrease with the number of firms).

5. Data as a Barrier to Entry

Under temporary monopoly, the incumbent can explore without incurring immediate reputational costs, and build up a high reputation before the entrant appears. Thus, the early entry gives the incumbent both a data advantage and a reputational advantage over the entrant. We explore which of the two factors is more significant. Our findings provide a quantitative insight into the role of the classic “first mover advantage” phenomenon in the digital economy.

For a more succinct terminology, recall that the incumbent enjoys an extended warm start of rounds. Call the first of these rounds the monopoly period (and the rest is the proper “warm start”). The rounds when both firms are competing for customers are called competition period.

We run two additional experiments to isolate the effects of the two advantages mentioned above. The data-advantage experiment focuses on the data advantage by, essentially, erasing the reputation advantage. Namely, the data from the monopoly period is not used in the computation of the incumbent’s reputation score. Likewise, the reputation-advantage experiment erases the data advantage and focuses on the reputation advantage: namely, the incumbent’s algorithm ‘forgets’ the data gathered during the monopoly period.

We find that either data or reputational advantage alone gives a substantial boost to the incumbent, compared to permanent duopoly. The results for the Heavy-Tail instance are presented in Table 4, in the same structure as Table 3. For the other two instances, the results are qualitatively similar.

| Reputation advantage | Data advantage | |||||

| 0.0210.009 | 0.160.02 | 0.21 0.02 | 0.00960.006 | 0.110.02 | 0.180.02 | |

| 0.260.03 | 0.30.02 | 0.260.02 | 0.0730.01 | 0.290.02 | 0.250.02 | |

| 0.340.03 | 0.40.03 | 0.330.02 | 0.150.02 | 0.390.03 | 0.330.02 | |

We can quantitatively define the data (resp., reputation) advantage as the incumbent’s market share in the competition period in the data-advantage (resp., reputation advantage) experiment, minus the said share under permanent duopoly, for the same pair of algorithms and the same problem instance. In this language, our findings are as follows.

Finding 9.

(a) Data advantage and reputation advantage alone are substantially large, across all algorithms and all MAB instances.

(b) The data advantage is larger than the reputation advantage when the incumbent chooses .

(c) The two advantages are similar in magnitude when the incumbent chooses or .

Our intuition for Finding 9(b) is as follows. Suppose the incumbent switches from to . This switch allows the incumbent to explore actions more efficiently – collect better data in the same number of rounds – and therefore should benefit the data advantage. However, the same switch increases the reputation cost of exploration in the short run, which could weaken the reputation advantage.

6. Performance in Isolation, Revisited

We saw in Section 4 that mean reputation trajectories do not suffice to explain the outcomes under competition. Let us provide more evidence and intuition for this.

Mean reputation trajectories are so natural that one is tempted to conjecture that they determine the outcomes under competition. More specifically:

Conjecture 6.1.

If one algorithm’s mean reputation trajectory lies above another, perhaps after some initial time interval (e.g., as in Figure 2), then the first algorithm prevails under competition, for a sufficiently large warm start .

However, we find a more nuanced picture. For example, in Figure 1 we see that attains a larger market share than even for large warm starts. We find that this also holds for arms and longer time horizons, see the supplement for more details. We conclude:

Finding 10.

Conjecture 6.1 is false: mean reputation trajectories do not suffice to explain the outcomes under competition.

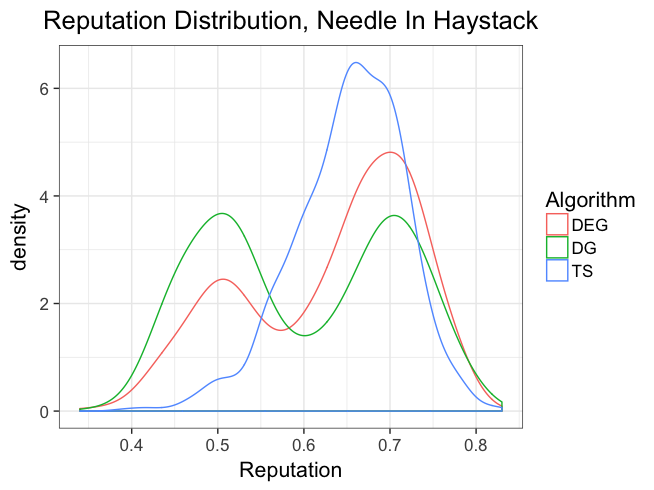

To see what could go wrong with Conjecture 6.1, consider how an algorithm’s reputation score is distributed at a particular time. That is, consider the empirical distribution of this score over different mean reward vectors.888Recall that each mean reward vector in our experimental setup comes with one specific realization table. For concreteness, consider the Needle-in-Haystack instance at time , plotted in Figure 6. (The other MAB instances lead to a similar intuition.)

We see that the “naive” algorithms and have a bi-modal reputation distribution, whereas does not. The reason is that for this MAB instance, either finds the best arm and sticks to it, or gets stuck on the bad arms. In the former case does slightly better than , and in the latter case it does substantially worse. However, the mean reputation trajectory may fail to capture this complexity since it simply takes average over different mean reward vectors. This may be inadequate for explaining the outcome of the duopoly game, given that the latter is determined by a simple comparison between the firm’s reputation scores.

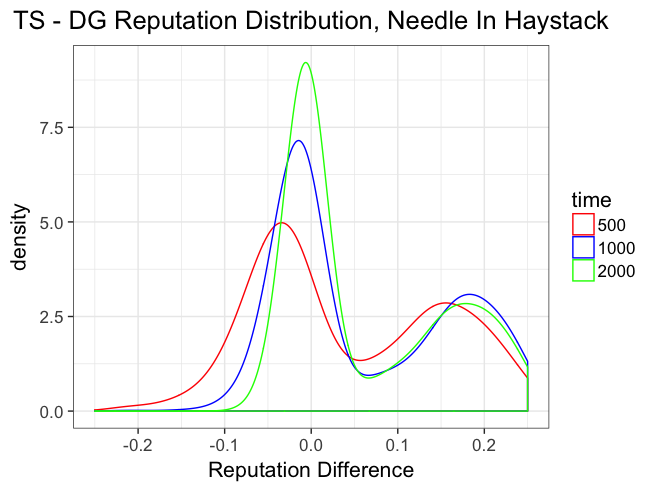

To further this intuition, consider the difference in reputation scores (reputation difference) between and on a particular mean reward vector. Let’s plot the empirical distribution of the reputation difference (over the mean reward vectors) at a particular time point. Figure 7 shows such plots for several time points. We observe that the distribution is skewed to the right, precisely due to the fact that either does slightly better than or does substantially worse. Therefore, the mean is not a good measure of the central tendency, or typical value, of this distribution.

7. Non-deterministic Choice Models

Let us consider an extension in which the agents’ choice is no longer deterministic. Recall that in our main model agents deterministically choose the firm with the higher reputation score; call this choice rule HardMax (). Now, we introduce some randomness: each agent selects between the firms uniformly with probability , and takes the firm with the higher reputation score with the remaining probability; call this choice rule HardMax with randomness ().

One can view as a version of “warm start”, where a firm receives some customers without competition, but these customers are dispersed throughout the game. The expected duration of this “dispersed warm start” is . If this quantity is large enough, we expect better algorithms to reach their long-term performance and prevail in competition. We confirm this intuition; we also find that this effect is negligible for smaller (but still relevant) values of or .

Finding 11.

is weakly dominant under the choice rule, if and only if is sufficiently large. leads to lower variance in market shares, compared to .

| Heavy-Tail ( with ) | Heavy-Tail () | |||||

| vs | vs | vs | vs | vs | vs | |

| 0.43 0.02 Var: 0.15 | 0.44 0.02 Var: 0.15 | 0.6 0.02 Var: 0.1 | 0.29 0.03 Var: 0.2 | 0.28 0.03 Var: 0.19 | 0.63 0.03 Var: 0.18 | |

| 0.66 0.01 Var: 0.056 | 0.59 0.02 Var: 0.092 | 0.56 0.02 Var: 0.098 | 0.29 0.03 Var: 0.2 | 0.29 0.03 Var: 0.2 | 0.62 0.03 Var: 0.19 | |

| 0.76 0.01 Var: 0.026 | 0.67 0.02 Var: 0.067 | 0.52 0.02 Var: 0.11 | 0.3 0.03 Var: 0.21 | 0.3 0.03 Var: 0.2 | 0.6 0.03 Var: 0.2 | |

| Uniform ( with ) | Needle-In-Haystack ( with ) | |||||

| vs | vs | vs | vs | vs | vs | |

| 0.42 0.02 Var: 0.13 | 0.45 0.02 Var: 0.13 | 0.49 0.02 Var: 0.093 | 0.55 0.02 Var: 0.15 | 0.61 0.02 Var: 0.13 | 0.46 0.02 Var: 0.12 | |

| 0.48 0.02 Var: 0.089 | 0.53 0.02 Var: 0.098 | 0.46 0.02 Var: 0.072 | 0.56 0.02 Var: 0.13 | 0.63 0.02 Var: 0.12 | 0.43 0.02 Var: 0.11 | |

| 0.54 0.01 Var: 0.055 | 0.6 0.02 Var: 0.073 | 0.44 0.02 Var: 0.064 | 0.58 0.02 Var: 0.083 | 0.65 0.02 Var: 0.096 | 0.4 0.02 Var: 0.1 | |

Table 5 shows the average market shares under the vs choice rule. In contrast to the model, becomes weakly dominant under the model, as gets sufficiently large. These findings hold across all problem instances, see Table 6 (with the same semantics as in Table 5).

However, it takes a significant amount of randomness and a relatively large time horizon for this effect to take place. Even with and we see that still outperforms on the Heavy-Tail MAB instance as well as that only starts to become weakly dominant at for the Uniform MAB instance.

8. Conclusion

We consider a stylized duopoly setting where firms simultaneously learn from and compete for users. We showed that competition may not always induce firms to commit to better exploration algorithms, resulting in welfare losses for consumers. The primary reason is that exploration may have short-term reputational consequences that lead to more naive algorithms winning in a long-term competition. Allowing one firm to have a head start, a.k.a. the first-mover advantage, incentivizes the first-mover to deploy “better” algorithms, which in turn leads to better welfare for consumers. Finally, we isolate the component of the first-mover advantage that is due to having more initial data, and find that even a small amount of this “data advantage” leads to substantial long-term market power.

References

- (1) Agarwal, A., Bird, S., Cozowicz, M., Dudik, M., Hoang, L., Langford, J., Li, L., Melamed, D., Oshri, G., Sen, S., and Slivkins, A. Multiworld testing: A system for experimentation, learning, and decision-making, 2016. A white paper, available at https://github.com/Microsoft/mwt-ds/raw/master/images/MWT-WhitePaper.pdf.

- (2) Agarwal, A., Bird, S., Cozowicz, M., Hoang, L., Langford, J., Lee, S., Li, J., Melamed, D., Oshri, G., Ribas, O., Sen, S., and Slivkins, A. Making contextual decisions with low technical debt, 2017. Techical report at arxiv.org/abs/1606.03966.

- (3) Aghion, P., Bloom, N., Blundell, R., Griffith, R., and Howitt, P. Competition and innovation: An inverted u relationship. Quaterly J. of Economics 120, 2 (2005), 701–728.

- (4) Amin, K., Rostamizadeh, A., and Syed, U. Learning prices for repeated auctions with strategic buyers. In 26th NIPS (2013), pp. 1169–1177.

- (5) Amin, K., Rostamizadeh, A., and Syed, U. Repeated contextual auctions with strategic buyers. In 27th NIPS (2014), pp. 622–630.

- (6) Auer, P., Cesa-Bianchi, N., and Fischer, P. Finite-time analysis of the multiarmed bandit problem. Machine Learning 47, 2-3 (2002), 235–256.

- (7) Babaioff, M., Kleinberg, R., and Slivkins, A. Truthful mechanisms with implicit payment computation. J. ACM 62, 2 (2015), 10. Subsumes the conference papers in ACM EC 2010 and ACM EC 2013.

- (8) Babaioff, M., Sharma, Y., and Slivkins, A. Characterizing truthful multi-armed bandit mechanisms. SIAM J. on Computing 43, 1 (2014), 194–230. Preliminary version in 10th ACM EC, 2009.

- (9) Bajari, P., Chernozhukov, V., Hortaçsu, A., and Suzuki, J. The impact of big data on firm performance: An empirical investigation. Tech. rep., National Bureau of Economic Research, 2018.

- (10) Barro, R. J., and Sala-i Martin, X. Economic growth: Mit press. Cambridge, Massachusettes (2004).

- (11) Bergemann, D., and Said, M. Dynamic auctions: A survey. In Wiley Encyclopedia of Operations Research and Management Science, Vol. 2. Wiley: New York, 2011, pp. 1511–1522.

- (12) Bimpikis, K., Papanastasiou, Y., and Savva, N. Crowdsourcing exploration. Management Science 64 (2018), 1477–1973.

- (13) Braverman, M., Mao, J., Schneider, J., and Weinberg, M. Selling to a no-regret buyer. In ACM EC (2018), pp. 523–538.

- (14) Bubeck, S., and Cesa-Bianchi, N. Regret Analysis of Stochastic and Nonstochastic Multi-armed Bandit Problems. Foundations and Trends in Machine Learning 5, 1 (2012).

- (15) Che, Y.-K., and Hörner, J. Optimal design for social learning. Quarterly Journal of Economics (2018). Forthcoming. First published draft: 2013.

- (16) Devanur, N., and Kakade, S. M. The price of truthfulness for pay-per-click auctions. In 10th ACM EC (2009), pp. 99–106.

- (17) Frazier, P., Kempe, D., Kleinberg, J. M., and Kleinberg, R. Incentivizing exploration. In ACM EC (2014), pp. 5–22.

- (18) Ghosh, A., and Hummel, P. Learning and incentives in user-generated content: multi-armed bandits with endogenous arms. In ITCS (2013), pp. 233–246.

- (19) Ho, C.-J., Slivkins, A., and Vaughan, J. W. Adaptive contract design for crowdsourcing markets: Bandit algorithms for repeated principal-agent problems. J. of Artificial Intelligence Research 55 (2016), 317–359. Preliminary version appeared in ACM EC 2014.

- (20) Immorlica, N., Kalai, A. T., Lucier, B., Moitra, A., Postlewaite, A., and Tennenholtz, M. Dueling algorithms. In 43rd ACM STOC (2011), pp. 215–224.

- (21) Kerin, R. A., Varadarajan, P. R., and Peterson, R. A. First-mover advantage: A synthesis, conceptual framework, and research propositions. The Journal of Marketing (1992), 33–52.

- (22) Kremer, I., Mansour, Y., and Perry, M. Implementing the “wisdom of the crowd”. J. of Political Economy 122 (2014), 988–1012. Preliminary version in ACM EC 2014.

- (23) Lambrecht, A., and Tucker, C. E. Can big data protect a firm from competition?

- (24) Lattimore, T., and Szepesvári, C. Bandit Algorithms. Cambridge University Press (preprint), 2019.

- (25) Mansour, Y., Slivkins, A., and Syrgkanis, V. Bayesian incentive-compatible bandit exploration. In 15th ACM EC (2015).

- (26) Mansour, Y., Slivkins, A., and Wu, S. Competing bandits: Learning under competition. In 9th ITCS (2018).

- (27) Nazerzadeh, H., Saberi, A., and Vohra, R. Dynamic cost-per-action mechanisms and applications to online advertising. In 17th WWW (2008).

- (28) Russo, D., Roy, B. V., Kazerouni, A., Osband, I., and Wen, Z. A tutorial on thompson sampling. Foundations and Trends in Machine Learning 11, 1 (2018), 1–96.

- (29) Schumpeter, J. Capitalism, Socialism and Democracy. Harper & Brothers, 1942.

- (30) Singla, A., and Krause, A. Truthful incentives in crowdsourcing tasks using regret minimization mechanisms. In 22nd WWW (2013), pp. 1167–1178.

- (31) Tirole, J. The theory of industrial organization. MIT press, 1988.

- (32) Varian, H. Artificial intelligence, economics, and industrial organization. In The Economics of Artificial Intelligence: An Agenda. University of Chicago Press, 2018.

- (33) Yue, Y., Broder, J., Kleinberg, R., and Joachims, T. The k-armed dueling bandits problem. J. Comput. Syst. Sci. 78, 5 (2012), 1538–1556. Preliminary version in COLT 2009.

- (34) Yue, Y., and Joachims, T. Interactively optimizing information retrieval systems as a dueling bandits problem. In 26th ICML (2009), pp. 1201–1208.

We provide plots and tables for our experiments, which were omitted from the main text due to page constraints. In all cases, the plots and tables here are in line with those in the main text, and lead to similar qualitative conclusions.

Appendix A Plots for “Performance In Isolation”

We present additional plots for Section 3. First, we provide mean reputation trajectories for Uniform and Heavy-Tail MAB instances. Second, we provide trajectories for instantaneous mean rewards, for all three MAB instances.999These trajectories are smoothed via a non-parametric regression. More concretely, we use this option in ggplot: https://ggplot2.tidyverse.org/reference/geom_smooth.html. In all plots, the shaded area represents 95% confidence interval.

![[Uncaptioned image]](/html/1902.05590/assets/uniform_mean.png)

![[Uncaptioned image]](/html/1902.05590/assets/ht_mean.png)

![[Uncaptioned image]](/html/1902.05590/assets/mean_inst_reward_ht.png)

![[Uncaptioned image]](/html/1902.05590/assets/mean_inst_reward_nih.png)

![[Uncaptioned image]](/html/1902.05590/assets/mean_inst_reward_uniform.png)

Appendix B Temporary Monopoly

We present additional experiments on temporary monopoly from Section 4, across various MAB instances and various values of the incumbent advantage parameter .

Each experiment is presented as a table with the same semantics as in the main text. Namely, each cell in the table describes the duopoly game between the entrant’s algorithm (the row) and the incumbent’s algorithm (the column). The cell specifies the entrant’s market share (fraction of rounds in which it was chosen) for the rounds in which he was present. We give the average (in bold) and the 95% confidence interval. NB: smaller average is better for the incumbent.

Heavy-Tail MAB Instance

| 0.054 0.01 | 0.16 0.02 | 0.18 0.02 | |

| 0.33 0.03 | 0.31 0.02 | 0.26 0.02 | |

| 0.39 0.03 | 0.41 0.03 | 0.33 0.02 |

| 0.003 0.003 | 0.083 0.02 | 0.17 0.02 | |

| 0.045 0.01 | 0.25 0.02 | 0.23 0.02 | |

| 0.12 0.02 | 0.36 0.03 | 0.3 0.02 |

| 0.0017 0.002 | 0.059 0.01 | 0.16 0.02 | |

| 0.029 0.007 | 0.23 0.02 | 0.23 0.02 | |

| 0.097 0.02 | 0.34 0.03 | 0.29 0.02 |

| 0.002 0.003 | 0.043 0.01 | 0.16 0.02 | |

| 0.03 0.007 | 0.21 0.02 | 0.24 0.02 | |

| 0.091 0.01 | 0.32 0.03 | 0.3 0.02 |

Needle-In-Haystack MAB Instance

| 0.34 0.03 | 0.4 0.03 | 0.48 0.03 | |

| 0.22 0.02 | 0.34 0.03 | 0.42 0.03 | |

| 0.18 0.02 | 0.28 0.02 | 0.37 0.03 |

| 0.17 0.02 | 0.31 0.03 | 0.41 0.03 | |

| 0.13 0.02 | 0.26 0.02 | 0.36 0.03 | |

| 0.093 0.02 | 0.23 0.02 | 0.33 0.03 |

| 0.1 0.02 | 0.28 0.03 | 0.39 0.03 | |

| 0.089 0.02 | 0.23 0.02 | 0.36 0.03 | |

| 0.05 0.01 | 0.21 0.02 | 0.33 0.03 |

| 0.053 0.01 | 0.23 0.02 | 0.37 0.03 | |

| 0.051 0.01 | 0.2 0.02 | 0.33 0.03 | |

| 0.031 0.009 | 0.18 0.02 | 0.31 0.02 |

Uniform MAB Instance

| 0.27 0.03 | 0.21 0.02 | 0.26 0.02 | |

| 0.39 0.03 | 0.3 0.03 | 0.34 0.03 | |

| 0.39 0.03 | 0.31 0.02 | 0.33 0.02 |

| 0.12 0.02 | 0.16 0.02 | 0.2 0.02 | |

| 0.25 0.02 | 0.24 0.02 | 0.29 0.02 | |

| 0.23 0.02 | 0.24 0.02 | 0.29 0.02 |

| 0.094 0.02 | 0.15 0.02 | 0.2 0.02 | |

| 0.2 0.02 | 0.23 0.02 | 0.29 0.02 | |

| 0.21 0.02 | 0.23 0.02 | 0.29 0.02 |

| 0.061 0.01 | 0.12 0.02 | 0.2 0.02 | |

| 0.17 0.02 | 0.21 0.02 | 0.29 0.02 | |

| 0.18 0.02 | 0.22 0.02 | 0.29 0.02 |

Appendix C Reputation vs. Data Advantage

This section presents all experiments on data vs. reputation advantage (Section 5).

Each experiment is presented as a table with the same semantics as in the main text. Namely, each cell in the table describes the duopoly game between the entrant’s algorithm (the row) and the incumbent’s algorithm (the column). The cell specifies the entrant’s market share for the rounds in which hit was present: the average (in bold) and the 95% confidence interval. NB: smaller average is better for the incumbent.

| 0.0096 0.006 | 0.11 0.02 | 0.18 0.02 | |

| 0.073 0.01 | 0.29 0.02 | 0.25 0.02 | |

| 0.15 0.02 | 0.39 0.03 | 0.33 0.02 |

| 0.021 0.009 | 0.16 0.02 | 0.21 0.02 | |

| 0.26 0.03 | 0.3 0.02 | 0.26 0.02 | |

| 0.34 0.03 | 0.4 0.03 | 0.33 0.02 |

| 0.25 0.03 | 0.36 0.03 | 0.45 0.03 | |

| 0.21 0.02 | 0.32 0.03 | 0.41 0.03 | |

| 0.18 0.02 | 0.29 0.03 | 0.4 0.03 |

| 0.35 0.03 | 0.43 0.03 | 0.52 0.03 | |

| 0.26 0.03 | 0.36 0.03 | 0.43 0.03 | |

| 0.19 0.02 | 0.3 0.02 | 0.36 0.02 |

| 0.27 0.03 | 0.23 0.02 | 0.27 0.02 | |

| 0.4 0.03 | 0.3 0.02 | 0.32 0.02 | |

| 0.36 0.03 | 0.29 0.02 | 0.3 0.02 |

| 0.2 0.02 | 0.22 0.02 | 0.27 0.03 | |

| 0.33 0.03 | 0.32 0.03 | 0.35 0.03 | |

| 0.32 0.03 | 0.31 0.03 | 0.35 0.03 |

| 0.0017 0.002 | 0.06 0.01 | 0.18 0.02 | |

| 0.04 0.009 | 0.24 0.02 | 0.25 0.02 | |

| 0.12 0.02 | 0.35 0.03 | 0.33 0.02 |

| 0.022 0.009 | 0.13 0.02 | 0.21 0.02 | |

| 0.26 0.03 | 0.29 0.02 | 0.28 0.02 | |

| 0.33 0.03 | 0.39 0.03 | 0.34 0.02 |

| 0.098 0.02 | 0.27 0.03 | 0.41 0.03 | |

| 0.093 0.02 | 0.24 0.02 | 0.38 0.03 | |

| 0.064 0.01 | 0.22 0.02 | 0.37 0.03 |

| 0.29 0.03 | 0.44 0.03 | 0.52 0.03 | |

| 0.19 0.02 | 0.35 0.03 | 0.42 0.03 | |

| 0.15 0.02 | 0.27 0.02 | 0.35 0.02 |

| 0.14 0.02 | 0.18 0.02 | 0.26 0.03 | |

| 0.26 0.02 | 0.26 0.02 | 0.34 0.03 | |

| 0.25 0.02 | 0.27 0.02 | 0.34 0.03 |

| 0.24 0.02 | 0.2 0.02 | 0.26 0.02 | |

| 0.37 0.03 | 0.29 0.02 | 0.31 0.02 | |

| 0.35 0.03 | 0.27 0.02 | 0.3 0.02 |

Appendix D Mean Reputation vs. Relative Reputation

We present the experiments omitted from Section 6. Namely, experiments on the Heavy-Tail MAB instance with arms, both for “performance in isolation” and the permanent duopoly game. We find that according to the mean reputation trajectory but that according to the relative reputation trajectory and in the competition game. As discussed in Section 6, the same results also hold for for the warm starts that we consider.

The result of the permanent duopoly experiment for this instance is shown in Table 31.

| Heavy-Tail | |||

| = 20 | = 250 | = 500 | |

| vs. | 0.4 0.02 770 (0) | 0.59 0.01 2700 (2979.5) | 0.6 0.01 2700 (3018) |

| vs. | 0.46 0.02 830 (0) | 0.73 0.01 2500 (2576.5) | 0.72 0.01 2700 (2862) |

| vs. | 0.61 0.01 1400 (556) | 0.61 0.01 2400 (2538.5) | 0.6 0.01 2400 (2587.5) |

Each cell describes a game between two algorithms, call them Alg1 vs. Alg2, for a particular value of the warm start . Line 1 in the cell is the market share of Alg 1: the average (in bold) and the 95% confidence band. Line 2 specifies the “effective end of game” (): the average and the median (in brackets).

The mean reputation trajectories for algorithms’ performance in isolation:

![[Uncaptioned image]](/html/1902.05590/assets/mean_ht_3_arms.png)

Finally, the relative reputation trajectory of vs. :

![[Uncaptioned image]](/html/1902.05590/assets/rel_rep_ht_3_arms.png)