Non-Linear Non-Stationary Heteroscedasticity Volatility for Tracking of Jump Processes

Abstract

In this paper, we introduce a new jump process modeling which involves a particular kind of non-Gaussian stochastic processes with random jumps at random time points. The main goal of this study is to provide an accurate tracking technique based on non-linear non-stationary heteroscedasticity (NNH) time series. It is, in fact, difficult to track jump processes regarding the fact that non-Gaussianity is an inherent feature in these processes. The proposed NNH model is conditionally Gaussian whose conditional variance is time-varying. Therefore, we use Kalman filter for state tracking. We show analytically that the proposed NNH model is superior to the traditional methods. Furthermore, to validate the findings, simulations are performed. Finally, the comparison between the proposed method and other alternatives techniques has been made.

Index Terms:

Non-linear non-stationary heteroscedasticity, Jump process, Tracking, Non-Gaussian process.I Introduction

Non-linear and non-Gaussian state-space models have attracted an increasing attention in recent years due to their significant importance to a wide range of applications such as radar, biomedical signal and image processing, and wireless communications [1, 2, 3, 4, 5, 6, 7, 8]. In these practical dynamic systems, the jump process is found to be helpful when abrupt changes occur within limited time intervals. Therefore, the variation of state variables can be modeled by jump processes. In [9], it is mathematically proved that a time varying process can be modeled by a heteroscedastic process properly. In [10, 11], the generalized autoregressive conditional heteroskedasticity (GARCH) process was used as a residual error of state model in the maneuvering target tracking which is one of the jumpy process applications. The GARCH model outperformed in comparison to the traditional models such as input estimation (IE), modified input estimation (MIE), and singer model.

These traditional models either fail to track jumpy points or result high errors in the flat or smooth parts of the jump processes. In this paper, we solved this problem by proposing a new non-linear non-stationary heteroscedasticity (NNH) model. The stochastic non-linear volatility leads the error covariance model to be time varying. We consider time varying conditional covariance for state equation which can describe both jumpy and non-jumpy time intervals. The featured characteristic of the NNH model is the heterogeneity generating function (HGF) [12]. In our approach this function is considered as an exponential function. This function is particularly useful for modeling of state space variance when a jump process is to be tracked where a very large variance is observed at a jump point; meanwhile during flat intervals, low variance is experienced. This new proposed model outperformed compared to other proposed models especially regarding steady state time periods, because its error variance will be close to zero in these time slots.

The paper is organized as follows. In Section 2, the jump processes are introduced and their properties are explained. The proposed model is presented in Section 3. Section 4 renders the modification of Kalman filter (KF) tracking algorithm to encompass our problem; i.e., modeling the stochastic jump process by the NNH time series for jump process tracking. The simulation results with various scenarios are given in Section 5. Finally, the conclusion is given.

II Problem formulation

The purpose of this study is tracking of the jump process The definition and properties of jump process are discussed.

Following the literature [13], compound Poisson processes is considered as a sub-class of the jump processes. Compound Poisson processes are pure jump Lévy processes [14], with paths that are constant apart from a finite number of jumps in finite time.

We consider the following linear discrete state space model formulation for modeling a jumpy system

| (1) | |||||

| (2) |

where is a state vector at the th instant, is the measurement, is the transition matrix, is the measurement matrix and and are modeling and measurement noise with covariance matrices and respectively. Based on the pure modeling, the relation between current and previous states is

| (3) |

where the jump size is an arbitrary distribution. In this formulation, we assume as a Gaussian random variable which is a least informative distribution given the variance. For (3), it is assumed that the sampling time is small enough relative to the reciprocal of the constant jump density (), which is Poisson process parameter (). Therefore, more than one jump may happen during this interval with small probability which tends to zero. Let us denote the number of Poisson points in one sampling interval by , where is a Poisson process with a constant jump density , so

| (4) | |||||

| (5) |

Since we have assumed that , then

| (6) |

According to (6), , which shows more than one jump in sampling interval is completely rare. Consequently, (1), (3), and (6), are simplified as

| (7) |

where is a non-Gaussian process noise which is given by

| (8) |

The distribution of this random variable is approximated by solution of a SDE [13]. In the next section, the mathematical formulation of the problem of tracking jump process using the NNH volatility model will be discussed.

III NNH for Jump process Modeling

Autoregressive Conditional Heteroscedasticity (ARCH) and GARCH models have widely been used to describe time varying conditional variances for many econometric applications [15, 16]. Although ARCH and GARCH models can capture abrupt changes well, their performances deteriorate in the time interval with flat behavior. The NNH model was proposed in [17] in which it is considered a time series with the conditional heteroscedasticities captured by a non-linear function. The NNH model provides a better result in the flat time intervals while preserves a good performance at the jump points. In the following, we establish the mathematical formulation of the model for jump process tracking.

We write the process noise model of (7), , as

| (9) |

and let be a filtration, denoting the information available at time interval and be an i.i.d. Gaussian random process with unit variance. Then, is a zero mean process noise with conditional variance .

The process noise model, , is conditionally heteroscedastic. Let the stochastic volatility, , be considered as

| (10) |

for non-negative function, and

| (11) |

where is an explanatory variable and by considering becomes a non-stationary integrated process. Thus, explanatory variable, , defined in (11) becomes a non-stationary integrated process. In this paper, we refer to as NNH which constitutes our novel volatility model. The behavior of the proposed NNH model depends critically on the HGF, in (10).

III-A Estimation of HGF

Let HGF, , in (10) be specified in a parametric form as

| (12) |

where is a known function and is a set of unknown parameters. Therefore, can be expressed as

| (13) |

where

| (14) |

The nonlinear regression with integrated regressor such as the one in (13) has been studied in [17]. The HGF for jumpy behavior is subsequently fitted to a parametric model using the weighted non-linear least squares (WNLS) method introduced in [17]. In what follows, we simply assume that satisfies the conditions in [17]. Therefore, we model the stochastic non-linear volatility in terms of an exponential function as in

| (15) |

where is the time index, , and , are the unknown HGF parameters and are the explanatory variables. As it is mentioned in (11), , therefore,

| (16) |

which according to (7), , and using (10), it is expressed as

| (17) |

where are the unknown parameter to control the behavior of HGF. The HGFs are considered as , , and in earlier research [17]. In the following section, we use the proposed new HGF in (17) to model the volatility in Kalman filtering procedure in equation (1). Subsequently, (1) and (2) using (17) are explained in details to elaborate more our proposed NNH approach.

IV Kalman Filtering Modification for NNH Modeling

The state non-stationary equation given by (7) has the structure for which the linear Kalman filter approach fails because of non-Gaussianity of noise process in (7). But, an attractive feature of Kalman filtering is its ease of implementation which we do not intend to forsake. While the other filtering approaches; i.e., particle filters, can be used to estimate the target state vector, but at very high computational complexities. Hence, we modify the Kalman filter procedure by adapting the volatility of the process noise in each filtering step. By this scheme, the non-Gaussian process noise is modeled by time-varying variance Gaussian process. The obtained formulation is as follows

| (18) | |||||

| (19) |

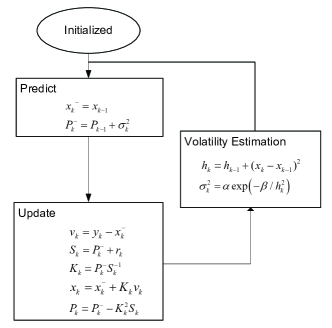

The volatility of motion equation (18), , is a stochastic process; therefore, its estimate is sought to implement the modified Kalman filter. Hence, the performance of tracking obtained from the estimate of in (18,19) is sensitive to this estimate. The proposed NNH estimator is dealt with the accurate estimation of We consider the parameter as a random parameter and predict its sample at each step by (17), thus, our uncertainties for state equation (18) in a highly jumpy process, is compensated by adding a flexibility to determine through (17). The algorithm is initiated by a small value for Then, is determined from the update equation of Kalman filtering in Fig. 1 and (17). This modification of variance during the algorithm, results in a better performance, especially in a highly jumpy process. The flowchart in Fig. 1 illustrates the functional structure of the proposed NNH method.

V SIMULATION AND RESULTS

A set of scenarios is simulated to investigation of the performance of the proposed NNH model in comparison with the traditional approaches. These simulations involve an ensemble of compound Poisson processes as the jump process. In the simulations, the observation interval [] is large enough compared to the sampling interval. The sampling time is sec. At first, we simulate and track the jump process with various parameters shown in Table I. The variance of the measurement noise for our simulation was selected as . The variance of modeling noise, for the traditional Kalman filters. The values of the proposed HGF parameters are assumed to be known as and . Simulations were run for different parameters to demonstrate the robustness of the new approach versus the performances for Kalman filter and GARCH approaches. For quantitative analysis, mean square error (MSE) of tracking results are calculated. In Table I, the average of MSEs over 200 trials are shown. As it can be seen in the table, the proposed model performs better than two other approaches.

| KF | GARCH | Proposed | |

| NNH | |||

| 6.78 | 4.14 | 3.76 | |

| 5.96 | 4.06 | 3.47 | |

| 7.13 | 5.32 | 4.63 | |

| 8.2 | 5.27 | 4.5 |

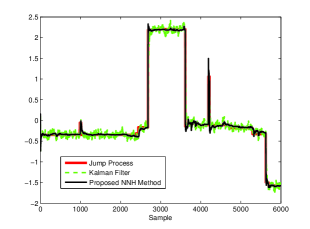

(a) The original and the estimated signal.

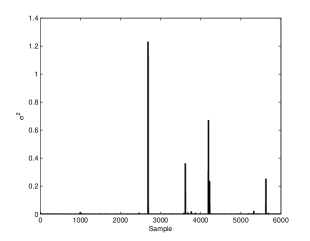

(b) The estimated volatility by the proposed NNH model

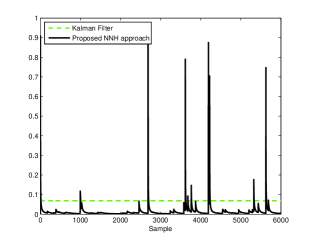

(c) The gains for Kalman filter and proposed NNH approach

Moreover, Fig.2(a) illustrates the original signal and the estimated signals by the proposed method and the GARCH method. As it can be seen, the proposed model outperforms compared to the GARCH approach. In addition, the estimated volatilities of the proposed NNH model of this jump process is shown in Fig.2(b). In Fig.2(c), the gains in update step (in Fig.1) are represented for proposed NNH approach and Kalman filter. By looking at Fig.2, we observe increases when there is an abrupt change in the original signal (in jump condition). On the other hand, for the time intervals with flat behavior, the estimated stochastic volatility is approximately zero. However, Fig.2(c) shows that the variance of GARCH is near five in the steady state time slots. Therefore, this feature of the proposed NNH method provides a smooth behavior in tracking in comparison with the traditional methods during the flat behavior of signal. In other word, the proposed NNH model adapts to the volatility of process noise. Using this information, estimation filter has an acceptable performance for abrupt change or jumps tracking.

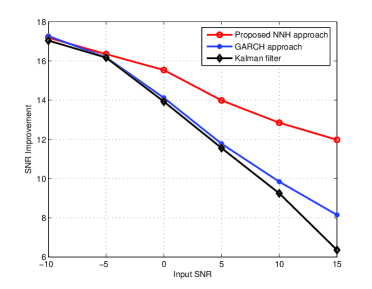

Furthermore, in order to show the performance of our proposed tracking approach in comparison with other methods, a jump process is generated and is contaminated by an additive non-Gaussian noise with different powers. We generate the non-Gaussian observation noise in equation (19) by,

| (20) |

where is i.i.d. discrete uniform random process with values and is i.i.d. exponential random process. We represent signal to noise ratio (SNR) Improvements by NNH method, GARCH approach and Kalman filter in Fig.3 in terms of input SNR. The SNR Improvement is calculated as: SNR Improvement (dB)= Output SNR (dB) - Input SNR (dB). It can be seen that the proposed method outperforms other approaches in non-Gaussian noise.

VI Conclusion

In this paper, we focused on tracking of jump processes. The properties of a jump process make it an appropriate model for modeling signals and state variations in dynamic systems with abrupt changes. Since Kalman filter exploits an Gaussian model, it fails to track jump processes with non-Gaussian distribution. Although GARCH process is a non-Gaussian model, this model has a high variance at non-jumpy points which leads to a poor tracking performance. The proposed approach uses NNH model with a nonlinear function estimating conditional variance over time. This gives the capability to have high variance values at jumpy points and very low variance values in other time intervals. This property is served to track sudden changes and also results a smooth estimated signal in non-jumpy parts. The simulation results showed that the traditional Kalman filter approach did not succeed under the circumstances as expected. We extended the Kalman filter by exploiting NNH model. By modifying the Kalman filter, the constant conditional variance of the process noise is adapted to the stochastic volatility of the process noise by applying a non-linear function on explanatory variable. The result of this model described the jump process at the jump points and the time intervals with flat behavior well. Simulation results illustrated that the proposed NNH method outperformed in comparison with the traditional approaches in both Gaussian and non-Gaussian noise scenarios.

References

- [1] Ehsan Hajiramezanali, Mahdi Imani, Ulisses Braga-Neto, Xiaoning Qian, and Edward R Dougherty, “Scalable optimal bayesian classification of single-cell trajectories under regulatory model uncertainty,” in Proceedings of the 2018 ACM International Conference on Bioinformatics, Computational Biology, and Health Informatics. ACM, 2018, pp. 596–597.

- [2] Mohammadehsan Hajiramezanali and Hamidreza Amindavar, “Maneuvering target tracking based on combined stochastic differential equations and garch process,” in Information Science, Signal Processing and their Applications (ISSPA), 2012 11th International Conference on. IEEE, 2012, pp. 1293–1297.

- [3] Chunyan Han and Huanshui Zhang, “Linear optimal filtering for discrete-time systems with random jump delays,” Signal Processing, vol. 89, no. 6, pp. 1121–1128, 2009.

- [4] Steven T Smith, “The jump tracker: Nonlinear bayesian tracking with adaptive meshes and a markov jump process model,” in Signals, Systems and Computers, 2006. ACSSC’06. Fortieth Asilomar Conference on. IEEE, 2006, pp. 2004–2008.

- [5] Ehsan Hajiramezanali, Siamak Zamani Dadaneh, Paul de Figueiredo, Sing-Hoi Sze, Mingyuan Zhou, and Xiaoning Qian, “Differential expression analysis of dynamical sequencing count data with a gamma markov chain,” arXiv preprint arXiv:1803.02527, 2018.

- [6] Ehsan Hajiramezanali, Siamak Zamani Dadaneh, Alireza Karbalayghareh, Mingyuan Zhou, and Xiaoning Qian, “Bayesian multi-domain learning for cancer subtype discovery from next-generation sequencing count data,” in Advances in Neural Information Processing Systems, 2018, pp. 9133–9142.

- [7] Noémie Bardel, Noufel Abbassi, François Desbouvries, Wojciech Pieczynski, and Frédéric Barbaresco, “A bayesian filtering algorithm in jump markov systems with application to track-before-detect,” in Radar Conference, 2010 IEEE. IEEE, 2010, pp. 1397–1402.

- [8] Mohammad Ehsan Haji Ramezan Ali and Mahmoud Ahmadian Attari, “Design and implementation of anc algorithm for engine noise reduction inside an automotive cabin using tms320c5510,” in Electrical Engineering (ICEE), 2011 19th Iranian Conference on. IEEE, 2011, pp. 1–6.

- [9] Seyyed Hamed Fouladi, Mohammadehsan Hajiramezanali, Hamidreza Amindavar, James A Ritcey, and Payman Arabshahi, “Denoising based on multivariate stochastic volatility modeling of multiwavelet coefficients.,” IEEE Trans. Signal Processing, vol. 61, no. 22, pp. 5578–5589, 2013.

- [10] Mohammadehsan Hajiramezanali, Seyyed Hamed Fouladi, James A Ritcey, and Hamidreza Amindavar, “Stochastic differential equations for modeling of high maneuvering target tracking,” ETRI Journal, vol. 35, no. 5, pp. 849–858, 2013.

- [11] Mohammadehsan Hajiramezanali and Hamidreza Amindavar, “Maneuvering target tracking based on sde driven by garch volatility,” in Statistical Signal Processing Workshop (SSP), 2012 IEEE. IEEE, 2012, pp. 764–767.

- [12] Ming Liu, Daniel WC Ho, and Yugang Niu, “Robust filtering design for stochastic system with mode-dependent output quantization,” IEEE Transactions on Signal Processing, vol. 58, no. 12, pp. 6410–6416, 2010.

- [13] Shin Ichi Aihara, Arunabha Bagchi, and Saikat Saha, “Estimating volatility and model parameters of stochastic volatility models with jumps using particle filter,” IFAC Proceedings Volumes, vol. 41, no. 2, pp. 6490–6495, 2008.

- [14] Peter Tankov, Financial modelling with jump processes, vol. 2, CRC press, 2003.

- [15] Robert F Engle, “Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation,” Econometrica: Journal of the Econometric Society, pp. 987–1007, 1982.

- [16] Tim Bollerslev, “Generalized autoregressive conditional heteroskedasticity,” Journal of econometrics, vol. 31, no. 3, pp. 307–327, 1986.

- [17] Joon Y Park, “Nonstationary nonlinear heteroskedasticity,” Journal of econometrics, vol. 110, no. 2, pp. 383–415, 2002.