Improved mathematical models of statistical regularities in precipitation

11footnotetext: Faculty of Computational Mathematics and Cybernetics, Lomonosov Moscow State University, Russia; Institute of Informatics Problems, Federal Research Center ‘‘Computer Science and Control’’ of Russian Academy of Sciences, Russia; Hangzhou Dianzi University, China; vkorolev@cs.msu.su22footnotetext: Institute of Informatics Problems, Federal Research Center ‘‘Computer Science and Control’’ of Russian Academy of Sciences, Russia; Faculty of Computational Mathematics and Cybernetics, Lomonosov Moscow State University, Russia; agorshenin@frccsc.ruAbstract. The paper presents improved mathematical models and methods for statistical regularities in the behavior of some important characteristics of precipitation: duration of a wet period, maximum daily and total precipitation volumes within a such period. The asymptotic approximations are deduced using limit theorems for statistics constructed from samples with random sizes having the generalized negative binomial (GNB) distribution. It demonstrates excellent concordance with the empirical distribution of the duration of wet periods measured in days. The asymptotic distribution of the maximum daily precipitation volume within a wet period turns out to be a tempered scale mixture of the gamma distribution with the scale factor having the Weibull distribution, whereas the asymptotic approximation to the total precipitation volume for a wet period turns out to be the generalized gamma (GG) distribution. Two approaches to the definition of abnormally extremal precipitation are presented. The first approach is based on an excess of a certain quantile of the asymptotic distribution of the maximum daily precipitation. The second approach is based on the GG model for the total precipitation volume. The corresponding statistical test is compared with a previously proposed one based on th classical gamma distribution using real precipitation data.

Keywords: Precipitation, generalized negative binomial distribution, generalized gamma distribution, asymptotic approximation, extreme order statistics, random sample size.

1 Introduction

In this paper improved mathematical models and methods for statistical regularities in the behavior of such characteristics of precipitation as the duration of a wet period, maximum daily precipitation within a wet period and total precipitation volume per a wet period are proposed. The importance of studying such objects for climate problems has been described, for example, in [20, 23, 24, 25, 26]. The base for the improved models (comparing of those proposed in [19]) is the generalized negative binomial (GNB) distribution. The results of fitting the GNB distribution to real data are presented and demonstrate excellent concordance of the GNB model with the empirical distribution of the duration of wet periods measured in days. Based on this GNB model, asymptotic approximations are proposed for the distributions of the maximum daily precipitation volume within a wet period and of the total precipitation volume for a wet period. The asymptotic distribution of the maximum daily precipitation volume within a wet period turns out to be a tempered scale mixture of the gamma distribution in which the scale factor has the Weibull distribution, whereas the asymptotic approximation for the total precipitation volume for a wet period turns out to be the generalized gamma (GG) distribution. Both approximations appear to be very accurate. These asymptotic approximations are deduced using limit theorems for statistics constructed from samples with random sizes having the generalized negative binomial distribution.

A rather reasonable approach to the unambiguous (algorithmic) determination of extreme or abnormally heavy total precipitation for a wet period [19] is realized with a GNB model for the duration of wet periods measured in days. This model is well justified statistically and theoretically by means of special limit theorems of probability theory which yield an asymptotic approximation to the distribution of the total precipitation volume within a wet period. This approximation has the form of a generalized gamma (GG) distribution. The proof of this result is based on the law of large numbers for random sums in which the number of summands has the GNB distribution. Hence, the hypothesis that the total precipitation volume during a certain wet period is abnormally large is re-formulated as the homogeneity hypothesis of a sample from the GG distribution.

The paper is organized as follows. In Section 2 necessary definitions and auxiliary results are given. GNB model for fitting the duration of wet periods is introduced in Section 3. In Section 4 the theorems about asymptotic probability distribution of extremal daily precipitation within a wet period and its properties are proved. A statistical method for estimating stability parameters of daily precipitation trends is demonstrated in Section 5. Also, the generalization of the Rényi theorem for GNB random sums is proved. In Section 6 an extremality statistical test based on assumptions about GG distribution of precipitation volumes is introduced. Also, the corresponding results are compared with the decisions of gamma distribution based test using real precipitation data for Potsdam and Elista. Section 7 is devoted to the main conclusions of the work.

2 Definitions and auxiliary results

A GG distribution is the absolutely continuous distribution defined by the density

| (1) |

with , , . A random value with the density will be denoted . The GG distributions were first described [22] as a unitary family of probability distributions simultaneously containing both Weibull and gamma distributions. A random value having the gamma distribution with shape parameter and scale parameter will be denoted (here symbol denotes the coincidence of distributions).

A random value with the Weibull distribution is a particular case of GG distributions corresponding to the density with , so, .

Let , and .The random value has the generalized negative binomial GNB distribution, if

| (2) |

where is determined by the formula (1).

The following asymptotic property of the GNB distribution [18] will play the fundamental role in the construction of asymptotic approximations to the distributions of extreme daily precipitation within a wet period and the total precipitation volume per a wet period and the corresponding statistical tests for precipitation to be abnormally heavy.

Lemma 1.

For , , let be a random value with the GNB distribution. We have

| (3) |

as . If, moreover, and , then the limit law can be represented as

| (4) |

where the random values , and are independent as well as the random values and , or the random values , and , and the random value has the Snedecor–Fisher distribution with parameters and .

Let , . Instead of an infinitesimal parameter , in order to construct asymptotic approximations with ‘‘large’’ sample size, introduce an auxiliary ‘‘infinitely large’’ parameter and assume that . Then from Lemma 1 and (3), it follows that for , we have

| (5) |

as .

Lemma 2.

Let be a sequence of positive random values such that for any the random value is independent of the Poisson process , . The convergence

as to some nonnegative random value takes place if and only if

| (6) |

as .

This statement is a particular case of Lemma 2 in [13].

Consider a sequence of independent identically distributed (i.i.d.) random values . Let be a sequence of natural-valued random values such that for each the random value is independent of the sequence . Denote .

Lemma 3.

Let be a sequence of positive random values such that for each the random value is independent of the Poisson process , . Let . Assume that there exists a nonnegative random value such that convergence (6) takes place. Let be i.i.d. random values with a common d.f. . Assume also that and there exists a number such that for each

| (7) |

Then

This statement is a particular case of Theorem 3.1 in [14].

Consider a sequence of random values Let be natural-valued random values such that for every the random value is independent of the sequence In the following statement [11, 12] the convergence is meant as .

Lemma 4.

Assume that there exist an infinitely increasing convergent to zero sequence of positive numbers and a random value such that

If there exist an infinitely increasing convergent to zero sequence of positive numbers and a random value such that

| (8) |

then

| (9) |

where the random values on the right-hand side of (9) are independent. If, in addition, in probability and the family of scale mixtures of the d.f. of the random value is identifiable, then condition (8) is not only sufficient for (9), but is necessary as well.

3 Generalized negative binomial model for the duration of wet periods

It turned out that the statistical regularities of the number of subsequent wet days can be very reliably modeled by the negative binomial distribution with the shape parameter less than one [4, 16]. The analytic and asymptotic properties of the GNB distributions were studied in [18]. Since the GG distribution is a more general and hence, more flexible model than the ‘‘pure’’ gamma-distribution, there arises a hope that the GNB distribution could provide even better goodness of fit to the statistical regularities in the duration of wet periods than the ‘‘pure’’ negative binomial distribution. Negative binomial distributions are special cases of the GNB distributions (the parameter in Eq. (2) should be equal ).

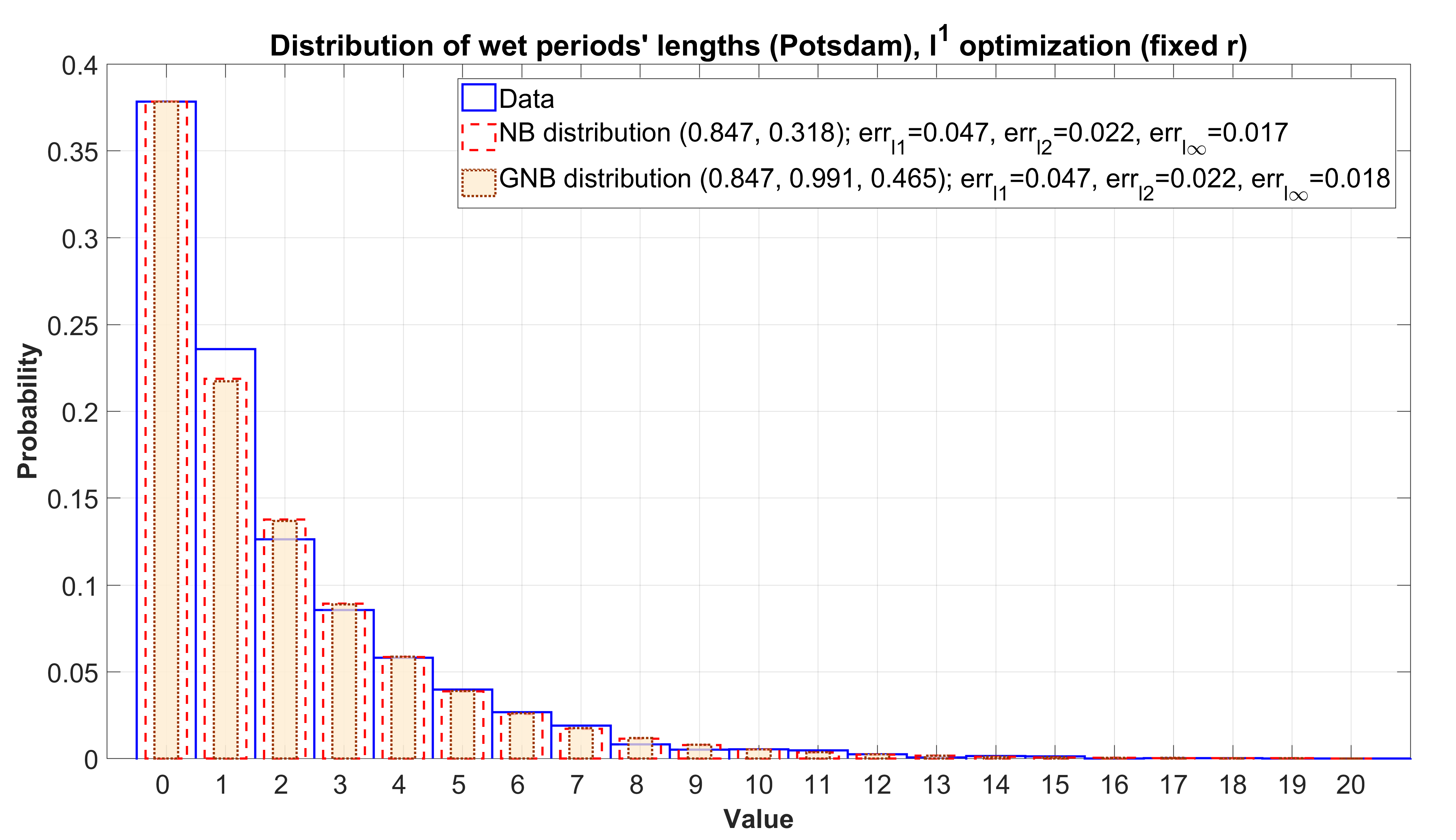

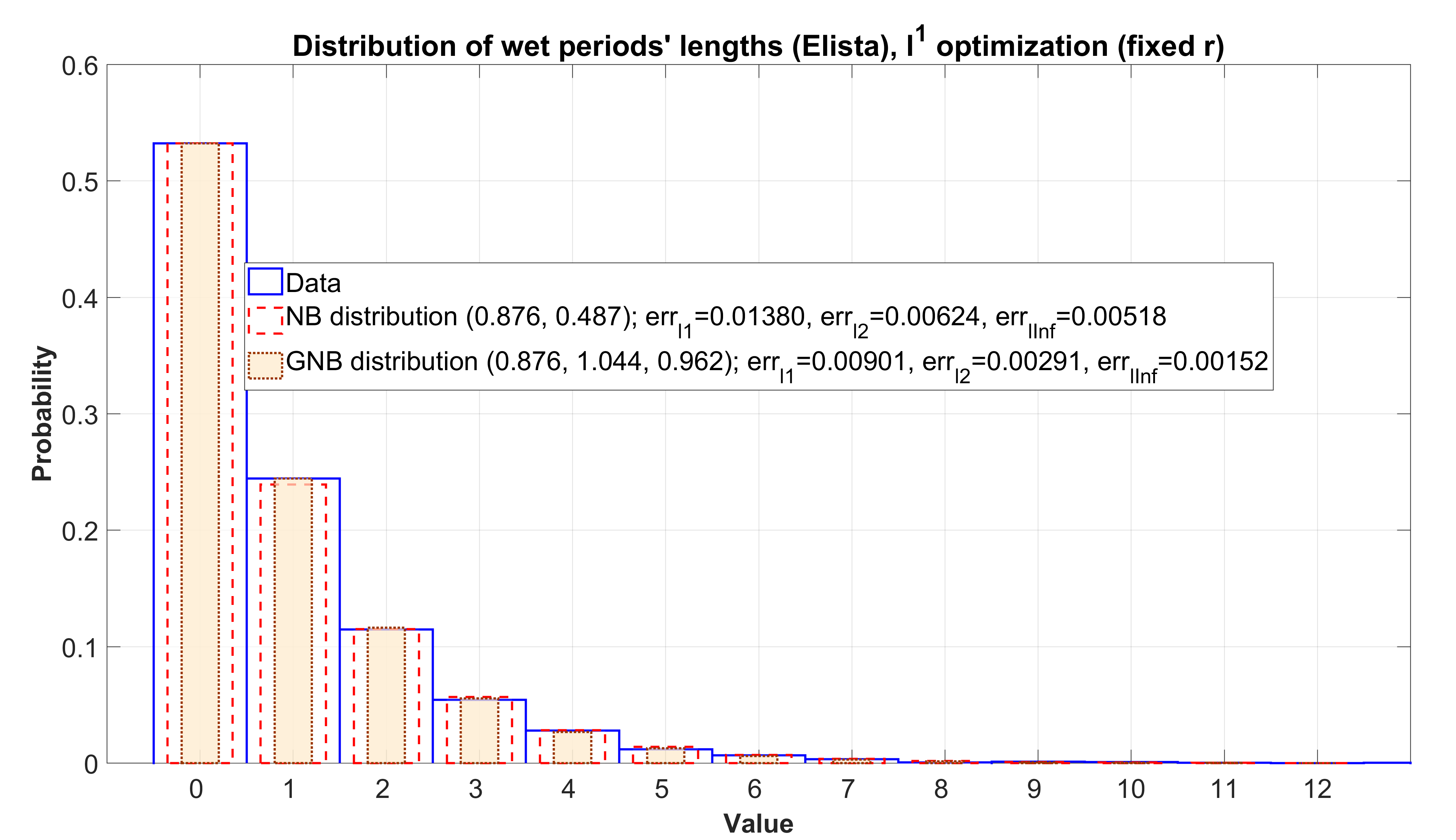

On Figs. 1 and 2 there are the histograms constructed from real data of wet periods in Potsdam and wet periods in Elista during almost years. On the same picture there are the graphs of the fitted negative binomial distribution and the fitted GNB distribution with additionally adjusted scale and power parameters. For vividness, in the GNB model the value of the shape parameter was taken the same as that obtained for the NB model and equal to for Elista and for Potsdam. For ‘‘fine tuning’’ of the GNB models with these fixed values of three procedures were used based on the minimization of the distance between the histogram and the fitted GNB model [5]:

-

•

minimization of the -distance;

-

•

minimization of the -distance;

-

•

minimization of the -distance (i. e., the uniform distance or the -norm).

On Figs. 1 and 2 the results of -distance minimization are presented. Other two procedures yield almost the same results. Minimization of the -distance results in that this distance between the histogram and the GNB distribution becomes almost 4.5 times less than the -distance between the histogram and the NB distribution. However, as this is so, the value of the -distance remain noticeably greater than those obtained by the minimization of the - and -distances which also give the GNB model an essential advantage over the NB model in the accuracy. But for Potsdam data the advantage of the adjusted GNB model over the NB model is not so crucial and does not exceed . It should be especially noted that the -values of the chi-square goodness-of-fit test are practically equal to 1 for all NB and GNB models mentioned above. So, the choice of a proper metric to be minimized remains an option. More examples of functional estimation GNB and GG distributions and implemented MATLAB software solutions are presented in [6].

4 The asymptotic approximation to the probability

distribution of extremal daily precipitation within a wet period

In this section we will deduce the probability distribution of extremal daily precipitation within a wet period.

Theorem 1.

Let , , and let be a random value with the GNB distribution with parameters , and . Let be i.i.d. random values with a common d.f. . Assume that and there exists a number such that relation (7) holds for any . Then

| (10) |

where , ,

| (11) |

and in each term the involved random variables are independent.

Proof.

It is well known that the negative binomial distribution is a mixed Poisson distribution with the gamma mixing distribution [8]. So, . Therefore, from (5), Lemma 2 with and Lemma 3 with the account of the absolute continuity of the limit distribution it immediately follows that

Since the Fréchet (inverse Weibull) d.f. with corresponds to the random value , it is easy to make sure

Moreover, using relation , it is easy to see that

where in each term the involved random variables are independent. ∎

It is worth noting that if , then the limit distribution corresponds to the results of [17].

Theorem 2.

The distribution of the random value can be represented as follows.

-

(i)

If , it is the scale mixture of the distribution of the ratio of two independent Weibull-distributed random variables:

All the involved random variables are independent, and random value defined as follows ()

where and are independent gamma-distributed random values.

-

(ii)

If , it is the scale mixture of the tempered Snedecor–Fisher distribution with parameters and :

where is a positive strictly stable random variable [27] with characteristic exponent independent of the random variable with the Snedecor–Fisher distribution with parameters and .

-

(iii)

If and , it is the scale mixture of the Pareto laws:

where , .

-

(iv)

If and , it is the scale mixture of the folded normal laws:

where all the involved random variables are independent.

Proof.

To prove (i) it suffices to consider the rightmost term in (11), apply relations and (here and the random variables and are independent, see [2]).

To prove (ii) it suffices to transform the rightmost term in (11) with the account of representation [21, 15]

(here and the random values on the right-hand side being independent) and use the definition of the Snedecor–Fisher distribution as the distribution of the ratio of two independent gamma-distributed random variables (see, e. g., Section in [9]).

Such product representations for the random value can be useful for its computer simulation.

Theorem 3.

If , and , then the d.f. is mixed exponential:

where , , and all the involved random values are independent.

Proof.

Theorem 4.

Let , , . Then the d.f. is infinitely divisible.

Proof.

It is possible to deduce explicit expressions for the moments of the random value .

Theorem 5.

Let . Then

Proof.

From (4) it follows that . It is easy to verify that , . Hence follows the desired result. ∎

So, the threshold method for extreme observations described in paper [19] can be improved using distribution function . It is worth noting that the estimation of parameters of this distribution is a rather complex computational problem.

5 The asymptotic approximation to the distribution of the total precipitation volume during a wet period

5.1 A statistical method for estimating stability parameters of daily precipitation trends

Let be be the observed values of nonzero daily precipitation volumes. The daily precipitation volumes possess the property of statistical stability [19]. It has been demonstrated that there are a slight ascending trend for Elista and a slight descending one for Potsdam [19]. In this section we will improve our model to obtain ‘‘horizontal’’ trends.

Suppose that for some

| (12) |

as . In [19] we use a value of parameter that equals . In practice, the parameter turns out to be close to , but slightly differs from representing (slow) global trends. Let us suggest a method for statistical estimating of the parameters and in relation (12).

Proposition 1.

Proof.

If condition (12) holds, the following approximate equality can be written:

| (15) | |||

| or, equivalently, | |||

Therefore, the estimates of the parameters and can be found as the solution of the least squares problem

The choice of the auxiliary parameter is an option and depends on, first, the time horizon over which the trend is considered and, second, on that the accuracy in (15) should be sufficient. The greater , the more ‘‘global’’ is the trend under consideration. It should be emphasized that in (12) we do not assume that are independent.

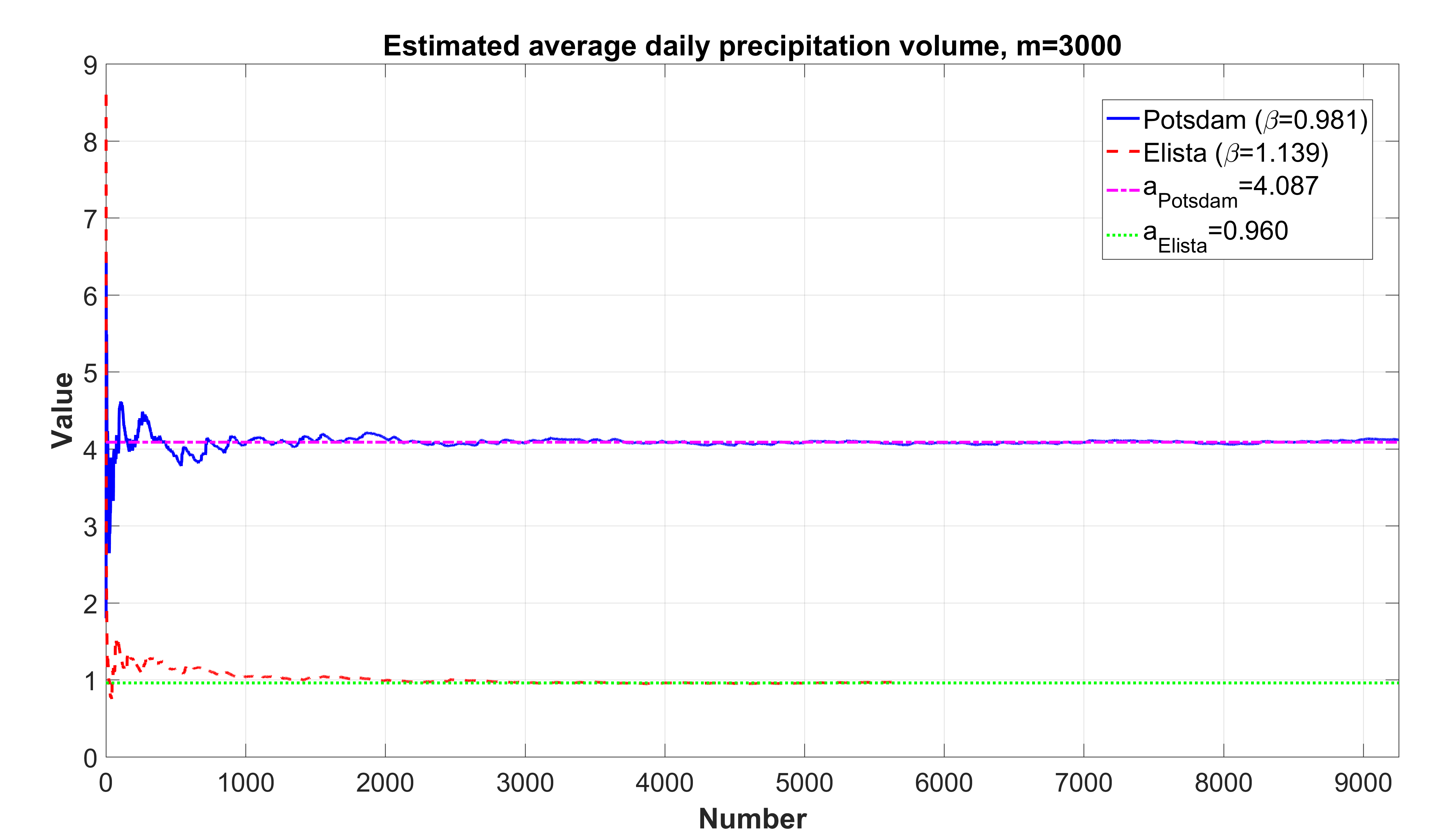

Fig. 3 illustrates the performance of the least squares algorithm described above with . On this figure the values of the parameter are estimated as for Potsdam and for Elista using formula (13), whereas the obtained by (14) values of appear to be equal to for Elista and for Potsdam, respectively. So, the corresponding trends are horizontal.

5.2 Generalization of the Rényi theorem for GNB random sums

The following theorem is a generalization of the Rényi theorem that dealt with rarefied renewal processes [10]. Instead of geometric sums of independent identically distributed random variables acting in the Rényi theorem, here we will consider the following analog of the law of large numbers for GNB random sums of not necessarily independent and not necessarily identically distributed random variables.

Theorem 6.

Assume that the daily precipitation volumes on wet days satisfy condition (12) with some and . Let the numbers , and be arbitrary. For each , let the random value have the GNB distribution with parameters , and . Assume that the random values are independent of the sequence Then

as .

Proof.

The proof is based on Lemma 4 and (5). From (5) it follows that

| (16) |

as . By virtue of condition (12), in Lemma 4 let . As in Lemma 4 take . Then . From (16) it follows that, as ,

| (17) |

Therefore, as we can take . So, using (17) in the role of (8) in Lemma 4, we obtain (9) in the form

| (18) |

whence follows the desired result. ∎

Theorem 6 presents a good tool for the account of the parameters and characterizing the deviation from traditional NB and arithmetic mean models due to the influence of possible (slow) global trends. If in Theorem 6 , then we obtain a version of the Rényi theorem [10] generalized to non-identically distributed and not necessarily independent summands. If in Theorem 6 , then we obtain the law of large numbers for negative binomial random sums [1].

Therefore, if daily precipitation volumes are considered as (of course, being non-identically distributed and not independent), with the account of the excellent fit of the GNB model for the duration of a wet period (see Fig. 1), with rather small , the GG distribution can be regarded as an adequate and theoretically well-based model for the total precipitation volume per (long enough) wet period.

6 Comparison of extremality tests based on assumptions about gamma and generalized gamma distributions of precipitation volumes

6.1 The test for data abnormality based on the GG distribution

Let and be independent random values having the same GG distribution with parameters , and . Also, let be independent random values having the same gamma distribution with parameters and .

The base for the first step in the construction of the desired test is the following obvious conclusion: if the random values are identically distributed (that is, the sample is homogeneous), then the random values are also identically distributed (that is, the sample is homogeneous. Consider the following relative contribution of the random value to the sum :

| (19) |

Here, relation is used. Therefore, the statistical approach introduced in [19] can be applied. The homogeneity test for a sample from the GG distribution is based on the random value (19) that has the Snedecor–Fisher distribution with parameters and .

Proposition 2.

Let ( for all ) be the total precipitation volumes during wet periods. Under the hypothesis (‘‘the precipitation volume under consideration is not abnormally large’’) the random value

| (20) |

has the Snedecor–Fisher distribution with parameters and .

Let be the -quantile of the corresponding Snedecor–Fisher distribution ( is a small number). If , then the hypothesis must be rejected.

If the hypothesis is rejected, the volume of precipitation during one wet period must be regarded as abnormally large. The probability of erroneous rejection of is equal to .

6.2 Comparison of statistical tests using real data

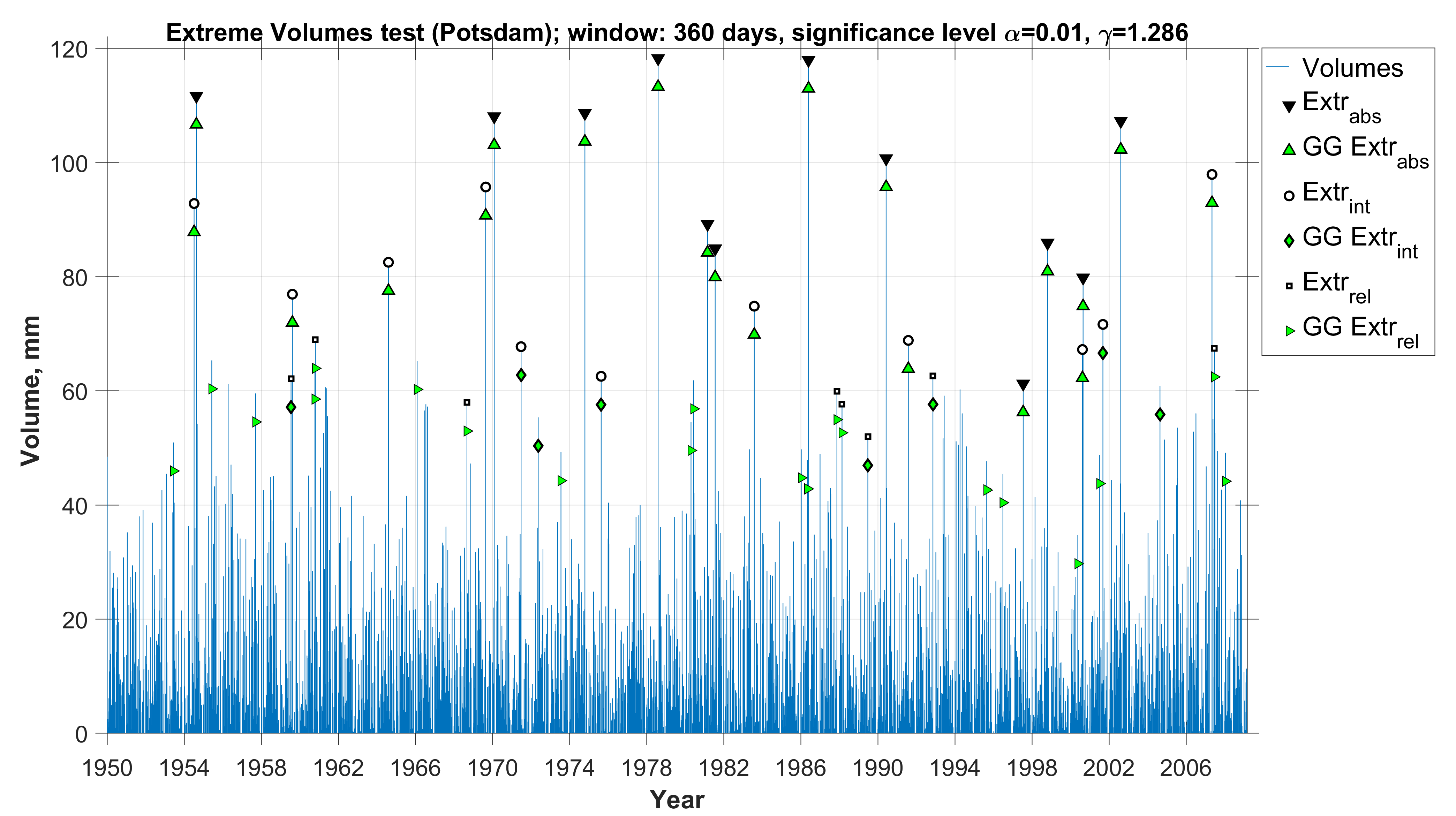

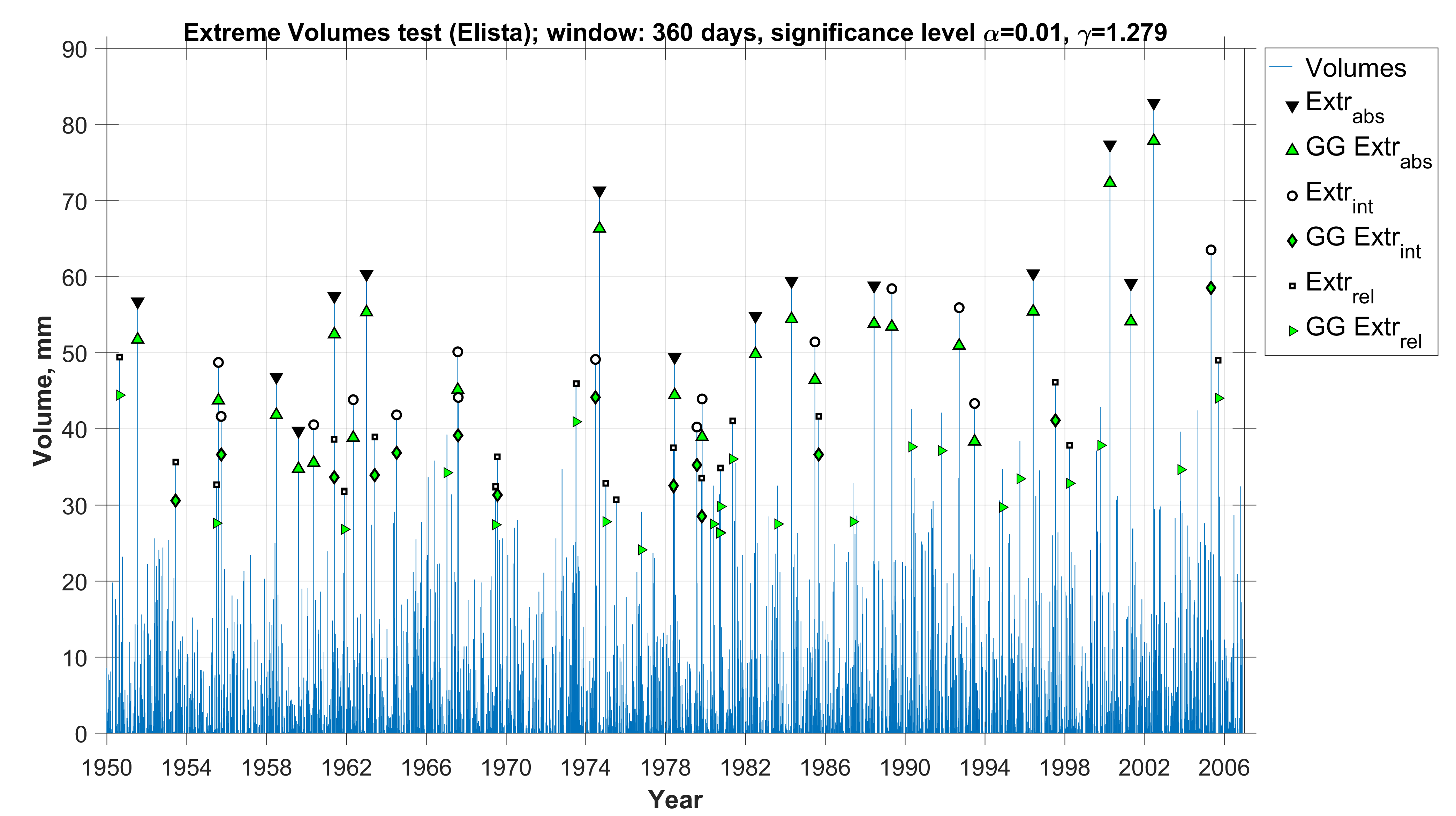

In this section we present the results of the application of the test based on the quantity (20) to the analysis of the time series of daily precipitation observed in Potsdam and Elista from to . Moreover, we compare potentially extreme values obtained by GG-test based on the statistic with test for gamma random values [19]. It uses the statistic that matches with the quantity , if the parameter in (20) equals .

The results of the application of the tests for a total precipitation volume during one wet period to be abnormally large based on and in the moving mode [19] are shown on Figs. 4 (Potsdam) and 5 (Elista). A fixed sample point can be one of the following types ( is a size of window):

-

•

absolutely extreme (if all windows contain this observation);

-

•

intermediate (if more than half windows contain it);

-

•

relatively (if at least one window contains it);

-

•

not extreme.

For the sake of vividness on these figures the time horizon equals days and the significance level of the tests is . The absolutely, intermediate and relatively abnormal precipitation volumes are marked with downward-pointing triangles, circles and squares, respectively, for test based on the statistic , whereas corresponding ones for the statistic based on the GG distribution are presented with upward-pointing triangles, diamonds and right-pointing triangles, respectively. It is worth noting that MATLAB’s notations are used here for these markers due to our implementation of corresponding computational procedures.

The Figs. 4 and 5 demonstrate non-trivial values of parameter , that is, . For Potsdam , whereas for Elista equals . At the same time, the results of the two methods are quite close, although the approach based on the GG distribution demonstrates a higher quality of determining potentially extreme observations. The same conclusions are valid for smaller window sizes, for example, days.

7 Conclusions and discussion

The article has considered asymptotic models for some precipitation characteristics based on GNB distributions. Also, a statistical test based on GG distribution to determine the type of precipitation extremes has proposed. These distributions are not quately widespread, so the methods for estimating their parameters are often not implemented in standard statistical packages. Therefore, the implementation of appropriate procedures requires the creation of specialized software solutions, for example, based on the functional approach, as was done in this article. However, as demonstrated in the article, the results of fitting such distributions to real data has turned out to be better compared with classical ones. Therefore, for processing spatial meteorological data from a large number of stations, the proposed methods and models can be effectively implemented as services using high-performance computing.

Acknowledgment

The research was partially supported by the Russian Foundation for Basic Research (project 17-07-00851) and the RF Presidential scholarship program (No. 538.2018.5).

References

- [1] H. Bevrani, V. Yu. Korolev, Some remarks on the asymptotic behavior of the sample availability function, Theory of Probability and its Applications, 61 (2) (2016) 384–394.

- [2] L. J. Gleser, The gamma distribution as a mixture of exponential distributions, American Statistician 43 (1989) 115–117.

- [3] C. M. Goldie, A class of infinitely divisible distributions, Mathematical Proceedings of the Cambridge Philosophical Society 63 (1967) 1141–1143.

- [4] A. K. Gorshenin, On some mathematical and programming methods for construction of structural models of information flows, Informatika i ee Primeneniya, 11 (1) (2017) 58–68.

- [5] A. K. Gorshenin and V. Yu. Korolev, A functional approach to estimation of the parameters of generalized negative binomial and gamma distributions, Communications in Computer and Information Science 919 (2018) 353–364.

- [6] A. K. Gorshenin, Software tools for statistical analysis of some precipitation characteristics, Pattern Recognition and Image Analysis 28 (4). (2018) 747–755.

- [7] A. K. Gorshenin and V. Yu. Korolev, Scale mixtures of Frechet distributions as asymptotic approximations of extreme precipitation, Journal of Mathematical Sciences 234 (6) (2018) 886–903.

- [8] M. Greenwoo and G. U. Yule, An inquiry into the nature of frequency-distributions of multiple happenings, etc., Journal of the Royal Statistical Society 83 (1920) 255–279.

- [9] N. L. Johnson, S. Kot and N. Balakrishnan, Continuous Univariate Distributions, Vol. 2 (2nd Edition) (Wiley, New York, 1995).

- [10] V. V. Kalashnikov, Geometric Sums: Bounds for Rare Events with Applications (Kluwer Academic Publishers, Dordrecht, 1997).

- [11] V. Yu. Korolev, Convergence of random sequences with independent random indexes. I, Theory of Probability and its Applications 39 (2) (1994) 313–333.

- [12] V. Yu. Korolev, Convergence of random sequences with independent random indexes. II, Theory of Probability and its Applications 40 (4) (1995) 770–772.

- [13] V. Yu. Korolev, On convergence of distributions of compound Cox processes to stable laws, Theory of Probability and its Applications 43 (4) (1999) 644–650.

- [14] V. Yu. Korolev and I. A. Sokolov, Mathematical Models of Inhomogeneous Flows of Extremal Events (Torus Press, Moscow, 2008).

- [15] V. Yu. Korolev, Product representations for random variables with the Weibull distributions and their applications, Journal of Mathematical Sciences 218 (3) (2016) 298–313.

- [16] V. Yu. Korolev, A. K. Gorshenin, S. K. Gulev, K. P. Belyaev and A. A. Grusho, Statistical Analysis of Precipitation Events, AIP Conference Proceedings 1863 (2017) 090011.

- [17] V. Yu. Korolev and A. K. Gorshenin, The probability distribution of extreme precipitation, Doklady Earth Sciences 477 (2) (2017)1461–1466.

- [18] V. Yu. Korolev and A. I. Zeifman, GG-mixed Poisson distributions as mixed geometric laws and related limit theorems, arXiv:1703.07276v2 [math.PR] (11 December, 2017).

- [19] V. Yu. Korolev, A. K. Gorshenin and K. P. Belyaev, Statistical tests for extreme precipitation volumes, arXiv:1802.02928v3 [stat.ME] (29 Nov 2018).

- [20] M. Lockhoff, O. Zolina, C. Simmer and J. Schulz, Evaluation of Satellite-Retrieved Extreme Precipitation over Europe using Gauge Observations, Journal of Climate 27 (2) (2014) 607–623.

- [21] D. N. Shanbhag, M. Sreehari, On certain self-decomposable distributions, Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete 38 (1977) 217–222.

- [22] E. W. Stacy, A generalization of the gamma distribution, Annals of Mathematical Statistics 33 (1962) 1187–1192.

- [23] O. Zolina, C. Simmer, A. Kapala and S. K. Gulev, On the robustness of the estimates of centennial-scale variability in heavy precipitation from station data over Europe, Geophysical Research Letters 32 (2005) L14707.

- [24] O. Zolina, C. Simmer, K. Belyaev, A. Kapala and S. K. Gulev, Improving estimates of heavy and extreme precipitation using daily records from European rain gauges, Journal of Applied Meteorology 10 (2009) 701–716.

- [25] O. Zolina, C. Simmer, K. Belyaev, A. Kapala, S.K. Gulev, P. Koltermann, Changes in the duration of European wet and dry spells during the last 60 years, Journal of Climate 26 (2013) 2022–2047.

- [26] O. Zolina, Multidecadal trends in the duration of wet spells and associated intensity of precipitation as revealed by a very dense observational German network, Environmental Research Letters 9 (2) (2014) 025003.

- [27] V. M. Zolotarev, One-Dimensional Stable Distributions, (American Mathematical Society, Providence, 1986).