Rank-one convexification for sparse regression

Abstract.

Sparse regression models are increasingly prevalent due to their ease of interpretability and superior out-of-sample performance. However, the exact model of sparse regression with an constraint restricting the support of the estimators is a challenging (-hard) non-convex optimization problem. In this paper, we derive new strong convex relaxations for sparse regression. These relaxations are based on the ideal (convex-hull) formulations for rank-one quadratic terms with indicator variables. The new relaxations can be formulated as semidefinite optimization problems in an extended space and are stronger and more general than the state-of-the-art formulations, including the perspective reformulation and formulations with the reverse Huber penalty and the minimax concave penalty functions. Furthermore, the proposed rank-one strengthening can be interpreted as a non-separable, non-convex, unbiased sparsity-inducing regularizer, which dynamically adjusts its penalty according to the shape of the error function without inducing bias for the sparse solutions. In our computational experiments with benchmark datasets, the proposed conic formulations are solved within seconds and result in near-optimal solutions (with 0.4% optimality gap) for non-convex -problems. Moreover, the resulting estimators also outperform alternative convex approaches from a statistical perspective, achieving high prediction accuracy and good interpretability. Keywords Sparse regression, best subset selection, lasso, elastic net, conic formulations, non-convex regularization

A. Gómez: Department of Industrial Engineering, Swanson School of Engineering, University of Pittsburgh, PA 15261. agomez@pitt.edu

January 2019; October 2020

![[Uncaptioned image]](/html/1901.10334/assets/x1.png)

BCOL RESEARCH REPORT 19.01

Industrial Engineering & Operations Research

University of California, Berkeley, CA 94720–1777

1. Introduction

Given a model matrix of explanatory variables, a vector of response variables, regularization parameters and a desired sparsity , we consider the least squares regression problem

| (1) |

where denotes cardinality of the support of . Problem (1) encompasses a broad range of the regression models. It includes as special cases: ridge regression [28], when , and ; lasso [43], when , and ; elastic net [53] when and ; best subset selection [37], when and . Additionally, Bertsimas and Van Parys, [7] propose to solve (1) with , and for high-dimensional regression problems, while Mazumder et al., [36] study (1) with , and for problems with low Signal-to-Noise Ratios (SNR). The results in this paper cover all versions of (1) with ; moreover, they can be extended to problems with non-separable regularizations of the form , resulting in sparse variants of the fused lasso [41, 44], generalized lasso [34, 45] and smooth lasso [27], among others.

Regularization techniques

The motivation and benefits of the regularization are well-documented in the literature. Hastie et al., [22] coined the bet on sparsity principle, i.e., using an inference procedure that performs well in sparse problems since no procedure can do well in dense problems. Best subset selection with and is the direct approach to enforce sparsity without incurring bias. In contrast, ridge regression with (Tikhonov regularization) is known to induce shrinkage and bias, which can be desirable, for example, when is not orthogonal, but it does not result in sparsity. On the other hand, lasso, the regularization with simultaneously causes shrinkage and induces sparsity, but the inability to separately control for shrinkage and sparsity may result in subpar performance in some cases [37, 48, 49, 50, 51, 52]. Moreover, achieving a target sparsity level with lasso requires significant experimentation with the penalty parameter [9]. When , the cardinality constraint on is redundant and (1) reduces to a convex optimization problem and can be solved easily. On the other hand, when , problem (1) is non-convex and -hard [39], thus finding an optimal solution may require excessive computational effort and methods to solve it approximately are used instead [29, 40]. Due to the perceived difficulties of tackling the non-convex constraint in (1), lasso-type simpler approaches are still preferred for inference problems with sparsity [24].

Nonetheless, there has been a substantial effort to develop sparsity-inducing methodologies that do not incur as much shrinkage and bias as lasso does. The resulting techniques often result in optimization problems of the form

| (2) |

where are non-convex regularization functions. Examples of such regularization functions include penalties with [17] and SCAD [14]. Although optimal solutions of (2) with non-convex regularizations may substantially improve upon the estimators obtained by lasso, solving (2) to optimality is still a difficult task [30, 35, 54], and suboptimal solutions may not benefit from the improved statistical properties. To address such difficulties, Zhang et al., [47] propose the minimax concave penalty (MC+), a class of sparsity-inducing penalty functions where the non-convexity of is offset by the convexity of for sufficiently sparse solutions, so that (2) remains convex – Zhang et al., [47] refer to this property as sparse convexity. Thus, in the ideal scenario (and with proper tuning of the parameter controlling the concavity of ), the MC+ penalty is able to retain the sparsity and unbiasedness of best subset selection while preserving convexity, resulting in the best of both worlds. However, due to the separable form of the regularization term, the effectiveness of MC+ greatly depends on the diagonal dominance of the matrix (this statement will be made more precise in §3), and may result in poor performance when the diagonal dominance is low.

Unfortunately, in many practical applications, the matrix has low eigenvalues and is not diagonally dominant at all. To illustrate, Table 1 presents the diagonal dominance of five datasets from the UCI Machine Learning Repository [11] used in [19, 38], as well as the diabetes dataset with all second interactions used in [6, 13]. The diagonal dominance of a positive semidefinite matrix is computed as

where is the -dimensional vector of ones, is the diagonal matrix such that and denotes the trace of . Accordingly, the diagonal dominance is the trace of the largest diagonal matrix that can be extracted from without violating positive semidefiniteness, divided by the trace of . Observe in Table 1 that the diagonal dominance of is very low or even , and MC+ struggles for these datasets as we demonstrate in §5.

| dataset | dd | ||

|---|---|---|---|

| housing | 13 | 506 | 26.7% |

| servo | 19 | 167 | 0.0% |

| auto MPG | 25 | 392 | 1.5% |

| solar flare | 26 | 1,066 | 8.8% |

| breast cancer | 37 | 196 | 3.6% |

| diabetes | 64 | 442 | 0.0% |

| crime | 100 | 1993 | 13.5 % |

Mixed-integer optimization formulations

An alternative to utilizing non-convex regularizations is to leverage the recent advances in mixed-integer optimization (MIO) to tackle (1) exactly [5, 6, 10]. By introducing indicator variables , where , problem (1) can be reformulated as

| (3a) | ||||

| s.t. | (3b) | |||

| (3c) | ||||

| (3d) | ||||

| (3e) | ||||

The non-convexity of (1) is captured by the complementary constraints (3d) and the integrality constraints . In fact, one of the main challenges for solving (3) is handling constraints (3d). A standard approach in the MIO literature is to use the so-called big- constraints and replace (3d) with

| (4) |

for a sufficiently large number to bound the variables . However, these so-called big- constraints (4) are poor approximations of constraints (3d), especially in the case of regression problems where no natural big- value is available. Bertsimas et al., [6] propose approaches to compute provable big- values, but such values often result in prohibitively large computational times even in problems with a few dozens variables (or, even worse, may lead to numerical instabilities and cause convex solvers to crash). Alternatively, heuristic values for the big- values can be estimated, e.g., setting where and is a feasible solution of (1) found via a heuristic111This method with was used in the computations in [6].. While using such heuristic values yield reasonable performance for small enough values of , it may eliminate optimal solutions.

Branch-and-bound algorithms for MIO leverage strong convex relaxations of problems to prune the search space and reduce the number of sub-problems to be enumerated (and, in some cases, eliminate the need for enumeration altogether). Thus, a critical step to speed-up the solution times for (3) is to derive convex relaxations that approximate the non-convex problem well [4]. Such strong relaxations can also be used directly to find good estimators for the inference problems (without branch-and-bound); in fact, it is well-known than the natural convex relaxation of (3) with and big- constraints is precisely lasso, see [12] for example. Therefore, sparsity-inducing techniques that more accurately capture the properties of the non-convex constraint can be found by deriving tighter convex relaxations of (1). Pilanci et al., [42] exploit the Tikhonov regularization term and convex analysis to construct an improved convex relaxation using the reverse Huber penalty. In a similar vein, Bertsimas and Van Parys, [7] leverage the Tikhonov regularization and duality to propose an efficient algorithm for high-dimensional sparse regression.

The perspective relaxation

Problem (3) is a mixed-integer convex quadratic optimization problem with indicator variables, a class of problems which has received a fair amount of attention in the optimization literature. In particular, the perspective relaxation [1, 15, 20] is, by now, a standard technique that can be used to substantially strengthen the convex relaxations by exploiting separable quadratic terms. Specifically, consider the mixed-integer epigraph of a one-dimensional quadratic function with an indicator constraint,

The convex hull of is obtained by relaxing the integrality constraint to bound constraints and using the closure of the perspective function222We use the convention that when and if and . of , expressed as a rotated cone constraint:

Xie and Deng, [46] apply the perspective relaxation to the separable quadratic regularization term , i.e., reformulate (3) as

| (5a) | ||||

| s.t. | (5b) | |||

| (5c) | ||||

| (5d) | ||||

Moreover, they show that the continuous relaxation of (5) is equivalent to the continuous relaxation of the formulation used by Bertsimas and Van Parys, [7]. Dong et al., [12] also study the perspective relaxation in the context of regression: first, they show that using the reverse Huber penalty [42] is, in fact, equivalent to just solving the convex relaxation of (5) — thus the relaxations of [7, 42, 46] all coincide; second, they propose to use an optimal perspective relaxation, i.e., by applying the perspective relaxation to a separable quadratic function , where is a nonnegative diagonal matrix such that ; finally, they show that solving this stronger convex relaxation of the optimal perspective relaxation is, in fact, equivalent to using the MC+ penalty [47].

The perspective relaxation is now a state-of-the-art method to convexify problems with separable terms and indicators variables. However, there are relatively few convexification techniques for problems without separable terms [16, 18, 21, 31]. In fact, among the previously discussed methods for sparse regression, the optimal perspective relaxation of Dong et al., [12] is the only one that does not explicitly require the use of the Tikhonov regularization . Nonetheless, as the authors point out, if then the method is effective only when the matrix is sufficiently diagonally dominant, which, as illustrated in Table 1, is not necessarily the case in practice. As a consequence, perspective relaxation techniques may be insufficient to tackle problems when large shrinkage is undesirable and, hence, is small.

Our contributions

In this paper we derive stronger convex relaxations of (3) than the optimal perspective relaxation. These relaxations are obtained from the study of ideal (convex-hull) formulations of the mixed-integer epigraphs of non-separable rank-one quadratic functions with indicators. Since the perspective relaxation corresponds to the ideal formulation of a one-dimensional rank-one quadratic function, the proposed relaxations generalize and strengthen the existing results. In particular, they dominate perspective relaxation approaches for all values of the regularization parameter and, critically, are able to achieve high-quality approximations of (1) even in low diagonal dominance settings with . Alternatively, our results can also be interpreted as a new non-separable, non-convex, unbiased regularization penalty which: (i) imposes larger penalties than the separable minimax concave penalty [47] to dense estimators, thus achieving better sparsity-inducing properties; and (ii) the nonconvexity of the penalty function is offset by the convexity of the term , and the resulting continuous problem can be solved to global optimality using convex optimization tools. In fact, they can be formulated as semidefinite optimization and, in certain special cases, as conic quadratic optimization.

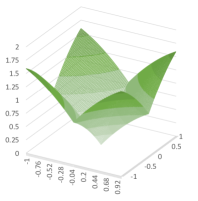

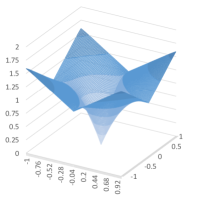

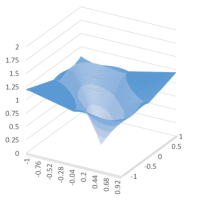

To illustrate the regularization point of view for the proposed relaxations, consider a two-predictor regression problem in Lagrangean form:

| (6) |

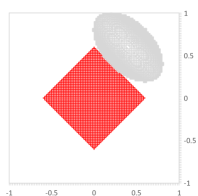

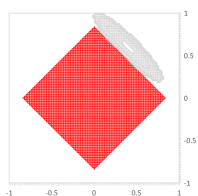

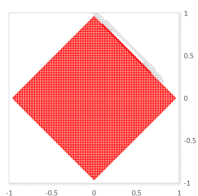

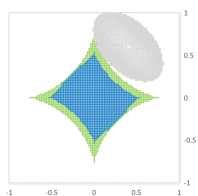

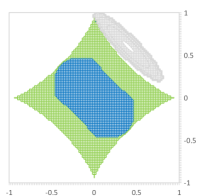

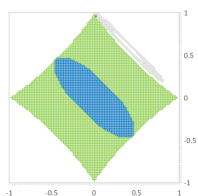

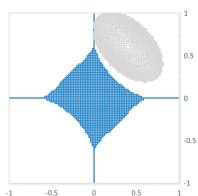

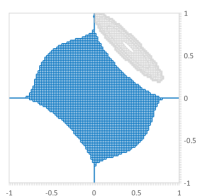

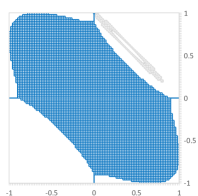

where and is a parameter controlling the diagonal dominance. Figure 1 depicts the graphs of well-known regularizations including lasso (, ), ridge (, ), elastic net (, ), the MC+penalty for different values of and the proposed rank-one R1 regularization. The graphs of MC+ and R1 are obtained by setting and , and using the appropriate convex strengthening, see §3 for details. Observe that the R1 regularization results in larger penalties than MC+for all values of , and the improvement increases as . In addition, Figure 2 shows the effect of using the lasso constraint , the MC+ constraint , and the rank-one constraint in a two-dimensional problem to achieve sparse solutions satisfying . Specifically, let

be the minimum residual error of a sparse solution of the least squares problem. Figure 2 shows in gray the (possibly dense) points satisfying , and it shows in color the set of feasible points satisfying , where is a given regularization and is chosen so that the feasible region (color) intersects the level sets (gray). We see that neither lasso nor MC+ is able to exactly recover an optimal sparse solution for any diagonal dominance parameter , despite significant shrinkage (). In contrast, the rank-one constraint adapts to the curvature of the error function to induce higher sparsity: in particular, the “natural” constraint , with the target sparsity , results in exact recovery without shrinkage in all cases.

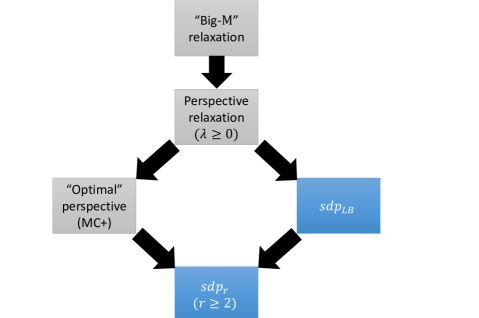

Finally, Figure 3 shows the strength of relaxations of (1) discussed in this paper. The “big-” relaxation is the natural convex relaxation of (3) obtained by replacing by , used in [6, 10]. The perspective relaxation is the natural convex relaxation of (5), which is the basis of recent methods [7, 26, 42, 46] – note that this formulation may only be used if . The “optimal perspective” relaxation, also referred to as in this paper, was explicitly given in [12]. This paper proposes new relaxations , discussed in §2, which dominate all existing relaxations in terms of strength. It also proposes the new formulation , discussed in §4, which is easier to solve than but still compares favorably with the “big-” and perspective formulations.

Outline

The rest of the paper is organized as follows. In §2 we derive the proposed convex relaxations based on ideal formulations for rank-one quadratic terms with indicator variables. We also give an interpretation of the convex relaxations as unbiased regularization penalties, and we give an explicit semidefinite optimization (SDP) formulation in an extended space, which can be implemented with off-the-shelf conic optimization solvers. In §3 we derive an explicit form of the regularization penalty for the two-dimensional case. In §4 we discuss the implementation of the proposed relaxation in a conic quadratic framework. In §5 we present computational experiments with synthetic as well as benchmark datasets, demonstrating that (i) the proposed formulation delivers near-optimal solutions (with provable optimality gaps) of (1) in most cases, (ii) using the proposed convex relaxation results in superior statistical performance when compared with usual estimators obtained from convex optimization approaches. In §6 we conclude the paper with a few final remarks.

Notation

Define and be the vector of ones. Given and a vector , define as the subvector of induced by , as the -th element of , and define . Given a symmetric matrix , let be the submatrix of induced by , and let be the set of symmetric positive semidefinite matrices, i.e., . We use or to make explicit that a given vector or matrix is indexed by the elements of or , respectively. Given matrices , of the same dimension, denotes the Hadamard product of and , and denotes their inner product. Given a vector , let be the diagonal matrix with . For a set , denotes the closure of the convex hull of . Throughout the paper, we adopt the following convention for division by 0: given a scalar , if and if . For a scalar , let .

2. Convexification

In this section we introduce the proposed relaxations of problem (1). First, in §2.1, we describe the ideal relaxations for the mixed-integer epigraph of a rank-one quadratic term. Then, in §2.2, we use the relaxations derived in §2.1 to give strong relaxations of (1). Next, in §2.3, we give an interpretation of the proposed relaxations as unbiased sparsity-inducing regularizations. Finally, in §2.4 we present an explicit SDP representation of the proposed relaxations in an extended space.

2.1. Rank-one case

We first give a valid inequality for the mixed-integer epigraph of a convex quadratic function defined over the subsets of . Given , consider the set

Proposition 1.

The inequality

| (7) |

is valid for .

Proof.

Observe that if is a singleton, i.e., , then (7) reduces to the well-known perspective inequality . Moreover, if and is rank-one, i.e., with and for and , then (7) reduces to

| (8) |

one of the inequalities proposed in [31] in the context of quadratic optimization with indicators and bounded continuous variables. Note that inequality (8) is, in general, weak for bounded continuous variables (as non-negativity or other bounds can be used to strengthen the inequalities, see [2] for additional discussion); and inequality (7) is, in general, weak for arbitrary matrices . Nonetheless, as we show next, inequality (7) is sufficient to describe the ideal (convex hull) description for if is a rank-one matrix. Consider the special case of defined with a rank-one matrix:

Theorem 1.

If for all , then

Proof.

Consider the optimization of an arbitrary linear function over and :

| (9) | |||

| (10) |

where and . We now show that either there exists an optimal solution of (10) that is feasible for (9), hence also optimal for (9) as is a relaxation of , or that (9) and (10) are both unbounded.

Observe that if , then letting and we see that both problems are unbounded. If and , then (10) reduces to , which has an optimal integral solution , and is optimal for (9) and (10). If and for some , then letting , , and for , we find that both problems are unbounded. Thus, we may assume, without loss of generality that , and, by scaling, .

Additionally, as has no zero entry, we may assume, without loss of generality, that , since otherwise and can be scaled by letting and to arrive at an equivalent problem. Moreover, a necessary condition for (9)–(10) to be bounded is that

| (11) |

for any fixed . It is easily seen that (11) has an optimal solution if and only if for all . Thus, we may also assume without loss of generality that for some scalar . Performing the above simplifications, we find that (10) reduces to

| (12) |

Since the one-dimensional optimization has an optimal solution, it follows that (12) is bounded and has an optimal solution. We now prove that (12) has an optimal solution that is integral in and satisfies .

Let be an optimal solution of (12). First note that if , then is feasible for (10) for sufficiently close to , with objective value . If , then for , has an objective value equal or lower. Otherwise, for , is feasible and has a lower objective value. Thus, we find that either is optimal for (12) (and the proof is complete), or there exists an optimal solution with . In the later case, observe that any with is also optimal for (12), an in particular there exists an optimal solution with integral.

Remark 1.

Observe that describing requires two nonlinear inequalities in the original space of variables. More compactly, we can specify using a single convex inequality, as

Finally, we point out that is conic quadratic representable, as if and only if there exists such that the system

is feasible, where the last constraint is a rotated conic quadratic constraint and all other constraints are linear.∎

2.2. General case

Now consider again the mixed-integer optimization (3)

| (13a) | ||||

| s.t. | (13b) | |||

| (13c) | ||||

| (13d) | ||||

| (13e) | ||||

| (13f) | ||||

where the nonlinear terms of the objective is moved to constraint (13b). A direct application of (7) yields the inequality , which is weak and has no effect when . Instead, a more effective approach is to decompose the matrix into a sum of low-dimensional rank-one matrices, and use inequality (7) to strengthen each quadratic term in the decomposition separately, as illustrated in Example 1 bellow.

Example 1.

Consider the example with and Then, it follows that

and we have the corresponding valid inequality

| (14) |

∎

The decomposition of illustrated in Example 1 is not unique. Since one does not obtain a strengthening when the denominator is one, it is important to have decomposition both rank-one and sparse. This motivates the question on how to find a decomposition that results in the best convex relaxation, i.e., that maximizes the left hand side of (14). Specifically, let be a subset of the power set of , i.e.,

with , . For each , define a matrix variable whose nonzero elements correspond to the submatrix induced by , and consider the valid inequality , where is defined as

| (15a) | |||||

| s.t. | (15b) | ||||

| (15c) | |||||

| (15d) | |||||

| (15e) | |||||

where strengthening (7) is applied to each low-dimensional quadratic term . For a fixed value of , problem (15) finds the best decomposition of the matrix as a sum of positive semidefinite matrices , , and a remainder positive semidefinite matrix to maximize the strengthening.

For a given decomposition, the objective (15a) is convex in , thus is a supremum of convex functions and is convex on its domain. Observe that the inclusion or omission of the empty set does not affect function , and we assume for simplicity that .

Since inequalities (7) are ideal for rank-one matrices, inequality is particularly strong if matrices are rank-one in optimal solutions of (15). As we now show, this is indeed the case if is downward closed.

Proposition 2.

If is downward closed, i.e., for all , then there exists an optimal solution to (15) where all matrices are rank-one.

Proof.

Let , let be the matrix variable associated with , and suppose is not rank-one in an optimal solution to (15), also suppose for simplicity that for some , and let for . Since is positive semidefinite, there exists a Cholesky decomposition where is a lower triangular matrix (possibly with zeros on the diagonal if is not positive definite). Let denote the -the column of . Since is not a rank-one matrix, there exist at least two non-zero columns of . Let with be the second non-zero column. Then

| (16) |

Finally, since , the (better) decomposition (16) is feasible for (15), and the proposition is proven. ∎

By dropping the complementary constraints (13e), replacing the integrality constraints with bound constraints , and utilizing the convex function to reformulate (13b), we obtain the convex relaxation of (1)

| (17a) | ||||

| (17b) | ||||

| (17c) | ||||

| (17d) | ||||

for a given . In the next section, we give an interpretation of formulation (17) as a sparsity-inducing regularization penalty.

2.3. Interpretation as regularization

Note that the relaxation (17) can be rewritten as:

where

| (18) |

is the (non-convex) rank-one regularization penalty. Observe that is the difference of two convex functions: the quadratic function arising from the fitness term and the Tikhonov regularization; and the projection of its convexification in the original space of the regression variables . As we now show, unlike the usual penalty, the rank-one regularization penalty does not induce a bias when is sparse.

Theorem 2.

If , then .

Proof.

The rank-one regularization penalty can also be interpreted from an optimization perspective: note that problem (15) is the separation problem that, given , finds a decomposition that results in a most violated inequality after applying the rank-one strengthening. Thus, the regularization penalty is precisely the violation of this inequality when is chosen optimally.

In §3 we derive an explicit form of when ; Figure 1 plots the graphs of the usual regularization penalties and for the two-dimensional case, and Figure 2 illustrates the better sparsity inducing properties of regularization . Deriving explicit forms of is cumbersome for . Fortunately, problem (17) can be explicitly reformulated in an extended space as an SDP and tackled using off-the-shelf conic optimization solvers.

2.4. Extended SDP formulation

To state the extended SDP formulation, in addition to variables and , we introduce variables corresponding to terms and corresponding to terms .

Theorem 3.

Problem (17) is equivalent to the SDP

| (19a) | ||||

| s.t. | (19b) | |||

| (19c) | ||||

| (19d) | ||||

| (19e) | ||||

| (19f) | ||||

| (19g) | ||||

Observe that (19) is indeed an SDP, as

thus constraints (19e) and (19f) are indeed SDP-representable and the remaining constraints and objective are linear.

Proof of Theorem 3.

It is easy to check that (19) is strictly feasible (set , , and ). Adding surplus variables , for , write (19) as

| s.t. | () | |||

| () | ||||

where . Using conic duality for the inner minimization problem, we find the dual

| s.t. | |||

After substituting and noting that there exists an optimal solution with , we obtain formulation (15). ∎

Note that if , there is no strengthening and (19) is equivalent to elastic net (), lasso (, ), ridge regression (, ) or ordinary least squares (). As increases, the quality of the conic relaxation (19) for the non-convex -problem (1) improves, but the computational burden required to solve the resulting SDP also increases. In particular, the full rank-one strengthening with requires semidefinite constraints and is impractical. Proposition 2 suggests using down-monotone sets with limited size

| (20a) | |||||

| s.t. | (20b) | ||||

| (20c) | |||||

| (20d) | |||||

| (20e) | |||||

| (20f) | |||||

| (20g) | |||||

for some – note that in the above formulation, is a scalar corresponding to the -th coordinate of the -dimensional vector . In fact, if , then reduces to the formulation of the optimal perspective relaxation proposed in [12], which is equivalent to using MC+ regularization. Our computations experiments show that whereas may be a weak convex relaxation for problems with low diagonal dominance, achieves excellent relaxation bounds even for the case of low diagonal-dominance within reasonable compute times. For clarity, we give the explicit form of the case :

| (21a) | |||||

| s.t. | (21b) | ||||

| (21c) | |||||

| (21d) | |||||

| (21e) | |||||

| (21f) | |||||

| (21g) | |||||

| (21h) | |||||

3. Regularization for the two-dimensional case

To better understand the properties of the proposed conic relaxations, in this section, we study them from a regularization perspective. Consider formulation (17b) in Lagrangean form with multiplier :

| (22a) | ||||

| (22b) | ||||

| (22c) | ||||

where , and

| (23) |

Observe that assumption (23) is without loss of generality, provided that is not diagonal: given a two-dimensional convex quadratic function (with ), the substitution and with yields a quadratic form satisfying (23). Also note that we are using the Lagrangean form instead of the cardinality constrained form given in (18) for simplicity; however, since is convex in , there exists a value of such that both forms are equivalent, i.e., result in the same optimal solutions for the regression problem, and the objective values differ by the constant .

If , then (22) reduces to a perspective strengthening of the form

| (24) |

The links between (24) and regularization were studied333The case with is explicitly considered in Dong et al., [12], but the results extend straightforwardly to the case with . The results presented here differ slightly from those in [12] to account for a different scaling in the objective function. in [12].

Regularization is non-convex and separable. Moreover, as pointed out in [12], the regularization given in Proposition 3 is the same as the Minimax Concave Penalty given in [47]; and, if , then the regularization given in Proposition 3 reduces to the reverse Huber penalty derived in [42]. Observe that the regularization function is highly dependent on the diagonal dominance : specifically, in the low diagonal dominance setting with , we find that .

We now consider conic formulation (22) for the case , corresponding to the full rank-one strengthening:

| (25) |

Proposition 4.

Observe that, unlike , the function is not separable in and and does not vanish when : indeed, for we find that

Proof of Proposition 4.

We prove the result by projecting out the variables in (25), i.e., giving closed form solutions for them. There are three cases to consider, depending on the optimal value for .

Case 1:

Case 2:

In this case, we find by setting the derivatives of the objective in (25) with respect to and that for . Thus, in this case, for an optimal solution of (25), we have , and problem (25) reduces to

Finally, this case happens when . Observe that, in this case, the penalty function is precisely the one given in Proposition 3.

Case 3:

4. Conic quadratic relaxations

As mentioned in §1, strong convex relaxations of problem (1), such as , can either be directly used to obtain good estimators via conic optimization, which is the approach we use in our computations, or can be embedded in a branch-and-bound algorithm to solve (1) to optimality. However, using SDP formulations such as (19) in branch-and-bound may be daunting since, to date, efficient branch-and-bound algorithms with SDP relaxations are not available. In contrast, conic quadratic optimization problems are considerably easier to solve that semidefinite optimization problems, thus scaling to larger dimensions. Moreover there exist off-the-shelf mixed-integer conic quadratic optimization solvers that are actively maintained and improved by numerous software vendors. In this section we show how the proposed conic relaxations, and specifically , can be implemented in a conic quadratic framework. The resulting convex formulations can then be directly used as a fast approximation to the SDP formulations presented in §2, and pave the way towards an integration with branch-and-bound solvers444An effective implementation would require careful constraint management strategies and integration with the different aspects of branch-and-bound solvers, e.g., branching strategies and heuristics. Such an implementation is beyond the scope of the paper..

4.1. Two-dimensional PSD constraints

4.2. Three-dimensional PSD constraints

As we now show, constraints (21f) can be accurately approximated using conic quadratic constraints.

Proposition 5.

Problem is equivalent to the optimization problem

| (28a) | ||||||

| s.t. | (28b) | |||||

| (28c) | ||||||

| (28d) | ||||||

| (28e) | ||||||

| (28f) | ||||||

| (28g) | ||||||

| (28h) | ||||||

| (28i) | ||||||

Proof.

It suffices to compute the optimal value of in (28f)–(28g). Observe that the rhs of (28f) can be written as

| (29) |

Moreover, in an optimal solution of (28), we have that . Thus, due to constraints (28d), we find that in optimal solutions of (28), and equality only occurs if either or . If either or , then the optimal value of (29) is , by setting or , respectively. Otherwise, the optimal equals

| (30) |

with the objective value

Observe that this expression is also correct when or . Thus, constraint (28f) reduces to

| (31) |

Similarly, it can be shown that constraint (28g) reduces to

| (32) |

More compactly, constraints (31)–(32) are equivalent to

| (33) |

Observe that, for any fixed value of , constraints (28f)–(28g) are conic quadratic representable. Thus, we can obtain relaxations of (28) of the form

| (34a) | ||||

| s.t. | (34b) | |||

| (34c) | ||||

| (34d) | ||||

where and are any finite subsets of . Relaxation (34) can be refined dynamically: given an optimal solution of (34), new values of generated according to (30) (resulting in most violated constraints) can be added to sets and , resulting in tighter relaxations. Note that the use of cuts (as described here) to improve the continuous relaxations of mixed-integer optimization problems is one of the main reasons of the dramatic improvements of MIO software [8].

In relaxation (34), and can be initialized with any (possibly empty) subsets of . However, setting yields a relaxation with a simple interpretation, discussed next.

4.3. Diagonally dominant matrix relaxation

Let be diagonally dominant matrix. Observe that for any such that ,

| (35) |

where the last line follows from using perspective strengthening for the separable quadratic terms, and using (7) for the non-separable, rank-one terms. See [3] for a similar strengthening for signal estimation based on nonnegative pairwise quadratic terms.

We now consider using decompositions of the form , where is a diagonally dominant matrix and . Given such a decomposition, inequalities (35) can be used to strengthen the formulations. Specifically, we consider relaxations of (3) of the form

| (36a) | ||||

| (36b) | ||||

where

| (37a) | ||||

| s.t. | (37b) | |||

| (37c) | ||||

| (37d) | ||||

Proposition 6.

Problem (36) is equivalent to

| (38a) | |||||

| s.t. | (38b) | ||||

| (38c) | |||||

| (38d) | |||||

| (38e) | |||||

| (38f) | |||||

| (38g) | |||||

| (38h) | |||||

| (38i) | |||||

4.4. Relaxing the -dimensional PSD constraint

We now discuss a relaxation of the -dimensional semidefinite constraint , present in all formulations. Let be a matrix whose -th column is an eigenvector of . Consider the optimization problem

| (40a) | |||||

| s.t. | (40b) | ||||

| (40c) | |||||

| (40d) | |||||

| (40e) | |||||

Observe that the objective and constraints (40a)–(40c) are identical to (15). However, instead of (15e), we have . Moreover, since , in any feasible solution of (40), thus (15) is a relaxation of (40), and, hence, is indeed a lower bound on . Finally, (40) is feasible if or contains all singletons, as it is possible to set , for , and set equal to the eigenvalues of . Therefore, instead of (17), one may use the simpler convex relaxation

| (41a) | ||||

| (41b) | ||||

| (41c) | ||||

| (41d) | ||||

for (1).

Proposition 7.

If , then problem (41) is equivalent to

| (42a) | |||||

| s.t. | (42b) | ||||

| (42c) | |||||

| (42d) | |||||

| (42e) | |||||

| (42f) | |||||

| (42g) | |||||

| (42h) | |||||

Proof.

The proof is based on conic duality similar to the proof of Theorem 3. ∎

Observe that in formulation (42), the -dimensional semidefinite constraint (19f) is replaced with rank-one quadratic constraints (42g). We denote by the relaxation of obtained by replacing (20f) with (42g). In general, is still an SDP due to constraints (42f); however, note that can be implemented in a conic quadratic framework by using cuts, as described in §4.2. Moreover, constraints (42g) could also be dynamically refined to better approximate the SDP constraint, or formulation (42) could be improved with ongoing research on approximating SDP via mixed-integer conic quadratic optimization, e.g., see [32, 33].

Remark 2.

We observe that formulation (42) is solved substantially faster than (with Mosek) with constraints (42f) formulated as semi-definite constraints. Indeed, the low-dimensional constraints (21f) can actually be handled efficiently, but the major computational bottleneck towards solving is handling the single large-dimensional positive semi-definite constraint (21g).

5. Computations

In this section, we report computational experiments with the proposed conic relaxations on synthetic as well as benchmark datasets. Semidefinite optimization problems are solved with MOSEK 8.1 solver, and conic quadratic optimization problems (continuous and mixed-integer) are solved with CPLEX 12.8 solver. All computations are performed on a laptop with a 1.80GHz Intel®CoreTM i7-8550U CPU and 16 GB main memory. All solver parameters were set to their default values. We divide our discussion in two parts: first, in §5.2, we focus on the relaxation quality of and its ability to approximate the exact -problem (1); then, in §5.3, we adopt the same experimental framework used in [6, 23] to generate synthetic instances and evaluate the proposed conic formulations from an inference perspective. In both cases, our results compare favorably with existing approaches in the literature.

5.1. Datasets

We use the benchmark datasets in Table 1. The first five were first used in [38] in the context of MIO algorithms for best subset selection, and later used in [19]. The diabetes dataset with all second interactions was introduced in [13] in the context of lasso, and later used in [6]. A few datasets require some manipulation to eliminate missing values and handle categorical variables. The processed datasets before standardization555In our experiments, the datasets were standardized first. can be downloaded from

http://atamturk.ieor.berkeley.edu/data/sparse.regression.

In addition, we also use synthetic datasets generated similarly to [6, 23]. Here we present a summary of the simulation setup and refer the readers to [23] for an extended description. . For given dimensions , sparsity , predictor autocorrelation , and signal-to-noise ratio SNR, the instances are generated as follows:

-

(1)

The (true) coefficients have the first components equal to one, and the rest equal to zero.

-

(2)

The rows of the predictor matrix are drawn from i.i.d. distributions , where has entry equal to .

-

(3)

The response vector is drawn from , where .

Similar data generation has been used in the literature [6, 23].

5.2. Relaxation quality

In this section we test the ability of , given in (21), and of , given in (42), to provide near-optimal solutions to problem (1), and compare its performance with MIO approaches. In §5.2.1, we focus on the pure best subset selection problem with , which has received relatively little attention in the literature [6]; in §5.2.2 we consider problems with - regularization, which has received more attention in the literature [7, 25, 26, 46]; in §5.2.3 we study the impact of model complexity parameter on the relaxation quality, and in §5.2.4 we study the scalability of the proposed methods.

Computing optimality gaps for

The optimal objective value of provides a lower bound on the optimal objective value of (1). To obtain an upper bound, we use a simple greedy heuristic to retrieve a feasible solution for (1): given an optimal solution vector for , let denote the -th largest absolute value. For , let be the -dimensional ols/ridge estimator using only predictors in , i.e.,

where denotes the matrix obtained by removing the columns with indexes not in , and let be the -dimensional vector obtained by filling the missing entries in with zeros. Since by construction, is feasible for (1), and its objective value is an upper bound on the optimal objective value of (1). Moreover, the optimality gap provided by any approach can be computed as

| (43) |

While stronger relaxations result in improved lower bounds , the corresponding heuristic upper bounds are not necessarily better; thus, the optimality gaps are not guaranteed to improve with stronger relaxations. Nevertheless, as shown next, stronger relaxations in general yield much smaller gaps in practice.

We point out that the main focus of the strong relaxations is to obtain improved lower bounds . Randomized rounding methods [42, 46], more sophisticated rounding heuristics [12], or alternative heuristic methods [25] can be used to obtain improved upper bounds. Nevertheless, the quality of the upper bounds obtained from the greedy rounding method can be used to estimate how well the solutions from the relaxations match the sparsity pattern of the optimal solution.

5.2.1. case

For each dataset with , we solve the conic relaxations of (1) and as well as and the mixed-integer formulation big-M given by (3)–(4). In our experiments, we set , where is the ordinary least square estimator666Bertsimas et al., [6] set for some heuristic solution and set a time limit of 10 minutes. For data with we solve problems with cardinalities , and for diabetes and crime we solve problems with . Table 2 shows, for each dataset and method, the average lower bound (LB) and upper bound (UB) found by each method, the gap (43), and the time required to solve the problems (in seconds) – the average is taken across all values. In all cases, lower and upper bounds are scaled so that the best upper bound for any given instance has value .

| dataset | method | LB | UB | gap(%) | time |

| housing | 99.40.6 | 100.10.1 | 0.70.0 | 0.030.02 | |

| 99.60.6 | 100.10.1 | 0.50.6 | 0.070.03 | ||

| 98.80.6 | 100.40.1 | 1.60.8 | 0.060.03 | ||

| big-M | 100.00.0 | 100.00.0 | 0.00.0 | 0.010.01 | |

| servo | 86.85.5 | 109.510.3 | 27.320.6 | 0.020.01 | |

| 94.92.9 | 106.216.5 | 12.219.8 | 0.100.01 | ||

| 89.52.7 | 109.215.5 | 21.814.9 | 0.170.03 | ||

| big-M | |||||

| auto MPG | 75.310.3 | 115.36.0 | 55.823.7 | 0.070.04 | |

| 96.73.3 | 100.50.8 | 4.04.2 | 0.240.02 | ||

| 78.87.7 | 101.62.7 | 30.014.0 | 0.400.09 | ||

| big-M | |||||

| solar flare | 97.51.5 | 103.31.1 | 6.02.0 | 0.070.03 | |

| 99.20.8 | 100.00.0 | 1.00.6 | 0.280.06 | ||

| 97.81.6 | 102.31.9 | 4.62.7 | 0.130.02 | ||

| big-M | 98.11.7 | 98.11.7 | - | 0.010.01 | |

| breast cancer | 88.93.1 | 101.51.7 | 14.45.6 | 0.150.02 | |

| 98.00.6 | 100.40.8 | 2.41.1 | 0.770.07 | ||

| 94.80.5 | 100.50.7 | 6.00.5 | 0.400.03 | ||

| big-M | |||||

| diabetes | 95.23.2 | 115.211.8 | 22.216.3 | 3.580.77 | |

| 97.41.3 | 105.44.2 | 8.25.2 | 9.281.12 | ||

| big-M | 99.00.9 | 100.00.0 | 1.00.9 | 416.17260.57 | |

| crime | 97.81.3 | 103.22.4 | 5.63.6 | 17.820.98 | |

| 99.00.8 | 101.62.0 | 2.72.7 | 45.294.06 | ||

| 94.62.0 | 109.72.8 | 16.04.9 | 5.870.43 | ||

| big-M | 96.41.7 | 100.00.0 | 3.71.8 | 527.03185.64 | |

| Error in solving problem. | |||||

| Infeasible solution is reported as optimal. | |||||

The big-M method is highly inconsistent and prone to numerical difficulties, due to the use of big- constraints. First, for three datasets (servo, auto MPG and breast cancer) the method fails due to numerical issues (“failure to solve MIP subproblem”). In addition, for solar flare the solver reports very fast solution times but the solutions are in fact infeasible for problem (1): by default in CPLEX, if in a solution then is deemed to satisfy the integrality constraint . Thus, if the big- constant is large enough, then constraint (4) may in fact allow nonzero values for even when “”. In particular, in solar flare we found that the solution reported by the MIO solver satisfies777We consider whenever . , regardless of the value of used, violating the sparsity constraint. We also point out that struggles with numerical difficulties in diabetes: the problems are incorrectly found to be unbounded. In contrast, methods are solved without numerical difficulties.

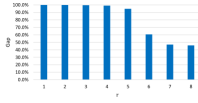

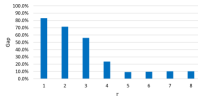

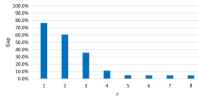

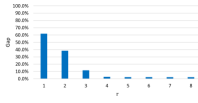

In terms of the relaxation quality, we find that is the best as expected. It consistently delivers better lower and upper bounds compared to the other conic relaxations, and even outperforming big-M in terms of lower bounds and gaps in the largest dataset (crime). The strength of the relaxation comes at the expense 2–4-fold larger computation time than , but on the other hand is substantially faster than big-M on large datasets. We see that neither nor dominates each other in terms of relaxation quality. While is faster on the smaller datasets, is faster on crime, indicating that may scale better (we corroborate this statement in §5.2.4). Finally big-M, in datasets where numerical issues do not occur, is able to find high quality solutions consistently, but struggles to find matching lower bound in larger instances, despite significantly higher computation time spent.

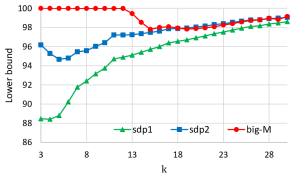

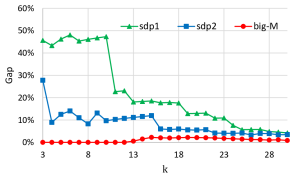

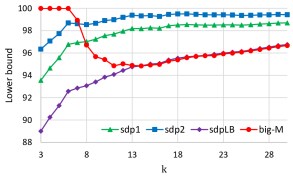

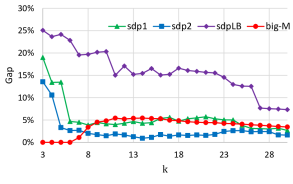

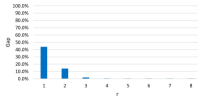

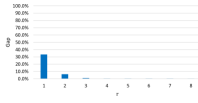

Figures 4 and 5 present detailed results on lower bounds and gaps as a function of the sparsity parameter for the diabetes and crime datasets. For small values of , big-M is arguably the best method, solving the problems to optimality. However, as increases, the quality of the lower bounds and gaps deteriorate: for diabetes, finds better solutions than big-M for ; for crime, and find better lower bounds for (and, in the case of , better gaps as well), and matches the lower bound found by big-M for , despite requiring only five seconds (instead of 10 minutes) to find such lower bounds. Observe that the number of possible supports for problem (1) scales exponentially with , thus enumerative methods such as branch-and-bound may struggle as grows.

5.2.2. case

For each dataset with888Since data is standardized so that each column has unit norm, a value of corresponds to an increase of 5% in the diagonal elements of the matrix . and , we solve the conic relaxations of (1) , and and the “big- free” mixed-integer formulation (5) with a time limit of 10 minutes (persp). This MIO formulation is possible since , and has been shown to be competitive [46, 26] with the tailored algorithm proposed in [7]. For datasets with we solve the problems with cardinalities , and for diabetes and crime we solve the problems with . Table 3 shows, for each dataset and method, the average lower bound (LB) and upper bound (UB) found by each method, the gap (43), and the time required to solve the problems (in seconds) – the average is taken across all values. In all cases, lower and upper bounds are scaled so that the best upper bound for any given instance has value .

| dataset | method | LB | UB | gap(%) | time |

|---|---|---|---|---|---|

| housing | 99.70.4 | 100.20.3 | 0.50.6 | 0.030.02 | |

| 99.80.3 | 100.10.2 | 0.30.5 | 0.060.02 | ||

| 99.50.4 | 100.30.3 | 0.80.6 | 0.060.02 | ||

| persp | 100.00.0 | 100.00.0 | 0.00.0 | 0.110.03 | |

| servo | 95.93.0 | 102.26.7 | 6.74.1 | 0.030.01 | |

| 99.50.5 | 100.61.1 | 1.11.6 | 0.110.01 | ||

| 97.61.4 | 102.02.1 | 4.63.3 | 0.160.02 | ||

| persp | 100.00.0 | 100.00.0 | 0.00.0 | 0.280.13 | |

| auto MPG | 89.16.1 | 101.41.2 | 14.48.5 | 0.050.01 | |

| 99.80.2 | 100.00.1 | 0.20.3 | 0.250.04 | ||

| 92.73.1 | 101.11.5 | 9.24.0 | 0.350.02 | ||

| persp | 100.00.0 | 100.00.0 | 0.00.0 | 1.290.60 | |

| solar flare | 99.30.5 | 100.10.1 | 0.80.5 | 0.070.01 | |

| 99.90.1 | 100.10.1 | 0.20.1 | 0.280.03 | ||

| 99.20.7 | 100.41.2 | 1.21.0 | 0.160.03 | ||

| persp | 100.00.0 | 100.00.0 | 0.00.0 | 1.751.07 | |

| breast cancer | 94.91.8 | 100.80.4 | 6.32.4 | 0.180.04 | |

| 99.60.2 | 100.10.2 | 0.50.3 | 0.720.06 | ||

| 97.50.6 | 100.50.4 | 2.90.9 | 0.360.05 | ||

| persp | 100.00.0 | 100.00.0 | 0.00.0 | 56.1244.34 | |

| diabetes | 98.90.6 | 100.20.2 | 1.20.7 | 2.130.24 | |

| 99.60.2 | 100.10.1 | 0.50.3 | 5.830.79 | ||

| 98.21.3 | 100.30.3 | 2.21.4 | 1.480.18 | ||

| persp | 99.40.5 | 100.00.0 | 0.60.5 | 441.90258.29 | |

| crime | 99.30.9 | 100.30.9 | 1.11.7 | 19.151.30 | |

| 99.70.4 | 100.20.8 | 0.51.0 | 43.862.38 | ||

| 98.71.0 | 100.71.3 | 2.02.3 | 5.300.35 | ||

| persp | 99.50.4 | 100.10.1 | 0.60.4 | 518.03175.65 |

We observe that instances with are much easier to solve than those with : no numerical issues occur for or persp, and lower and upper bounds are much better for all methods. The mixed integer formulation persp comfortably solves the small instances with to optimality, but yields better lower bounds and gaps for the larger instances diabetes and crime in a fraction of the time used by persp.

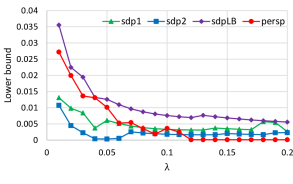

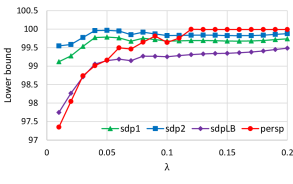

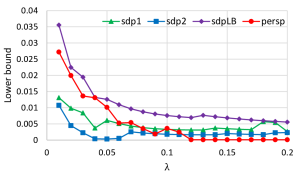

Figures 6 and 7 present lower bounds and gaps as a function of the regularization parameter , for diabetes and crime datasets (with ). We observe that for low value of , persp struggles to find good lower bounds, e.g., it is outperformed by all conic relaxations in crime for , and is worse than for in terms of lower bounds and gaps in both datasets. As increases, all methods deliver better bounds, and persp is eventually able to solve all problems to optimality.

As expected, the performance of persp improves as increases. The perspective relaxation discussed in §1 exploits the separable terms introduced by the -regularization: as increases, this separable terms have a larger weight in the objective, and the strength of the relaxation improves as a consequence. Note that the conic relaxations also improve with larger : they are based on decompositions of the matrix into one- and two-variable terms, and the addition of the separable terms allows for a much richer set of decompositions. For large values of , becomes highly diagonal dominant, and the perspective relaxation alone provides a substantial strengthening. In this case, the advanced conic relaxations have a marginal impact and MIO methods with perspective strengthening performs better overall. In contrast, for low values of , the conic relaxations result in substantial strengthening over the perspective relaxation, and outperforms persp as a consequence.

5.2.3. The effect of model complexity

In §5.2.1–5.2.2 we reported computations with with . In experiments with those datasets, yields almost the same strengthening as , but with much larger computational cost. Since already achieves gaps close to in those instances, there is little room for improvement with higher values of .

If the matrix has high rank, which happens if or if is large, then there are many ways to decompose it into low-dimensional rank-one terms, and with small achieves good relaxations. In contrast, if the matrix has low rank, it may be difficult to extract low-dimensional rank-one terms. In the extreme case of a rank-one case matrix, while results in the convex description, with achieves no improvement. In this section we illustrate this phenomenon on small synthetic instances with and .

Specifically, we set the true sparsity to , autocorrelation , signal-noise-ration , sparsity , and for each combination of parameters we generate five instances. We report in Figure 8 the gaps obtained by for different values of and – averaging across instances and different values of SNR and . In addition, Figure 9 depicts the distribution of computational times required to solve the problems.

We observe that for , with results in no strengthening and gaps of 100%; results in a small improvement (note that ), while with results in larger improvements. These results suggest that, with , stronger formulations require rank-one strengthening with at least variables. We also observe that, as increases, the gaps reported by all methods decrease substantially, and the incremental strengthening obtained from larger values of decreases: for performs almost identical to , and for is similar to and already results in low optimality gaps. The computational time required to solve scales exponentially with since the number of constraints increases exponentially as well. We conclude that is well suited for the case or for medium values of (for larger values or even the simple perspective relaxation may be preferable), while with achieves a good improvement in relaxation quality for low values of , at the expense of larger computational times.

5.2.4. On scalability

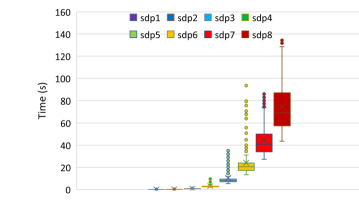

As discussed in §5.2.3, formulation for large values of can be expensive to solve. Moreover, even and are semidefinite programs, which may not scale well for large values of . In this section we present computations illustrating that while this is indeed the case, formulation –which replaces the semidefinite constraint with the quadratic constraints (42g)– scales much better and in fact can significantly outperform persp in terms of relaxation quality.

We generate synthetic instances with , , true sparsity parameter , autocorrelation , signal-noise-ration , sparsity ; for each combination of parameters we generate five instances, and solve them for and . Table 4 reports, for , , and persp –using formulation (5) with a time limit of 600 seconds–, the time required to solve the problems and the optimality gap proven.

| persp | ||||||||

|---|---|---|---|---|---|---|---|---|

| time(s) | gap(%) | time(s) | gap(%) | time(s) | gap(%) | time(s) | gap(%) | |

| 100 | 193 | 0.50.6 | 449 | 0.10.1 | 51 | 1.01.1 | TL | 3.34.2 |

| 150 | 15319 | 1.11.5 | 35661 | 0.20.4 | 202 | 1.92.2 | TL | 6.27.2 |

| 200 | 67364 | 2.73.0 | 1,691165 | 0.60.9 | 423 | 4.34.0 | TL | 12.510.5 |

| 250 | 794 | 7.15.6 | TL | 17.213.2 | ||||

| 300 | 1477 | 12.27.6 | TL | 21.714.6 | ||||

| 350 | 24814 | 17.611.0 | TL | 25.917.0 | ||||

| 400 | 39136 | 24.014.9 | TL | 29.118.9 | ||||

| 450 | 39446 | 32.218.3 | TL | 34.321.0 | ||||

| 500 | 46243 | 39.321.9 | TL | 38.822.8 | ||||

We observe that persp is unable to solve the problems within the 10 minute time limit and results in larger gaps than all other approaches, despite using substantially more time in most cases. We also observe that formulations struggle in instances with . Interestingly, requires consistently 2-4 times more than regardless of the dimension . A similar factor was observed in Tables 2 and 3 with real data, suggesting that computational times with are within the same order-of-magnitude as . Finally, is substantially faster than both and . While it results in larger gaps than as expected, since the high-dimensional constraint (21g) is relaxed, it still yields better optimality gaps than persp.

5.3. Inference study on synthetic instances

We now present inference results on synthetic data using the same simulation setup as in [6, 23], see [23] for an extended description. Specifically, we generate synthetic data as described in §5.1, and use the evaluation metrics used in [23], described next.

5.3.1. Evaluation metrics

Let denote the test predictor drawn from and let denote its associated response value drawn from . Given an estimator of , the following metrics are reported:

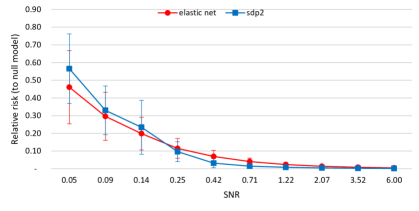

- Relative risk:

-

with a perfect score and null score of .

- Relative test error:

-

with a perfect score of and null score of SNR+1.

- Proportion of variance explained:

-

with perfect score of SNR/(1+SNR) and null score of 0.

- Sparsity:

-

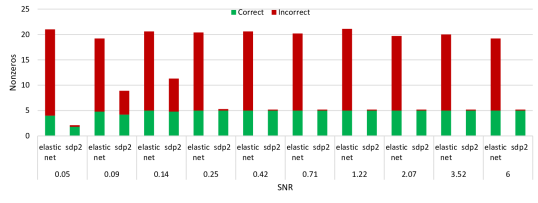

We record the number of nonzeros999An entry is deemed to be non-zero if . This is the default integrality precision in commercial MIO solvers., , as done in [23]. Additionally, we also report the number of variables correctly identified, given by .

5.3.2. Procedures

In addition to the training set of size , a validation set of size is generated with the same parameters, matching the precision of leave-one-out cross-validation. We use the following procedures to obtain estimators .

- elastic net:

-

We solve the elastic net procedure using the parametrization

where are the regularization parameters. We let for integer , we generated 50 values of ranging from to on a log scale, and using the pair that results in the best prediction error on the validation set. A total of 500 pairs are tested.

- :

-

The estimator obtained from solving () for all values of and choosing the one that results in the best prediction error on the validation set.

The elastic net procedure approximately corresponds to the lasso procedure with 100 tuning parameters used in [23]. Similarly, with cross-validation approximately corresponds to the best subset procedure with tuning parameters101010Hastie et al., [23] use values of . Nonetheless, in our computations with the same tuning parameters, we found that values of are never selected after cross-validation. Thus our procedure with tuning parameters results in the same results as the one with 51 parameters from a statistical viewpoint, but requires only a fraction of the computational effort. used in [23]; nonetheless, the estimators from [23] are obtained by running a MIO solver for 3 minutes, while ours are obtained from solving to optimality a strong convex relaxation.

5.3.3. Optimality gaps and computation times

Before describing the statistical results, we briefly comment on the relaxation quality and computation time of . Table 5 shows, for instances with , , and , the optimality gap and relaxation quality of — each column represents the average over ten instances generated with the same parameters. In all cases, produces optimal or near-optimal estimators, with optimality gap at most . In fact, with , we find that 97% of the estimators for and 68% of the estimators with are provably optimal111111A solution is deemed optimal if gap, which is the default parameter in MIO solvers. for (1). For a comparison, Hastie et al., [23] report that, in their experiments, the MIO solver (with a time limit of three minutes) is able to prove optimality for only 35% of the instances generated with similar parameters. Although Hastie et al., [23] do not report optimality gaps for the instances where optimality is not proven, we conjecture that such gaps are significantly larger than those reported in Table 5 due to weak relaxations with big- formulations. In summary, for this class of instances, is able produce optimal or practically optimal estimators of (1) in about 30 seconds.

| SNR | 0.05 | 0.09 | 0.14 | 0.25 | 0.42 | 0.71 | 1.22 | 2.07 | 3.52 | 6.00 | avg | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| gap | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | |

| time | 45.2 | 38.8 | 38.6 | 29.5 | 29.3 | 28.4 | 27.4 | 26.3 | 26.4 | 25.9 | 31.6 | |

| gap | 0.3 | 0.2 | 0.3 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.1 | |

| time | 48.0 | 47.6 | 49.4 | 44.1 | 39.3 | 30.7 | 29.0 | 29.1 | 27.3 | 28.0 | 37.3 | |

5.3.4. Results: accuracy metrics

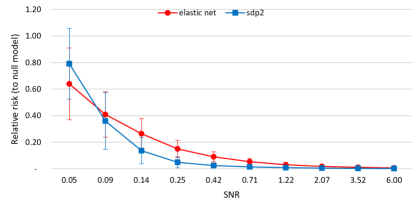

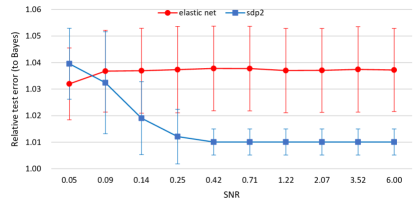

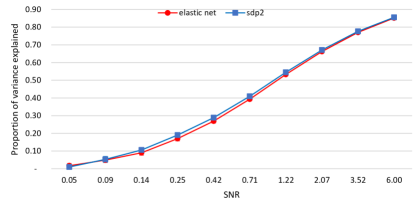

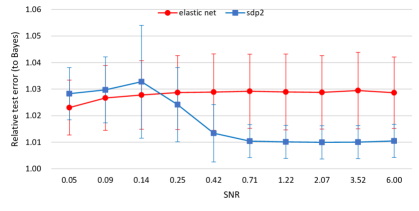

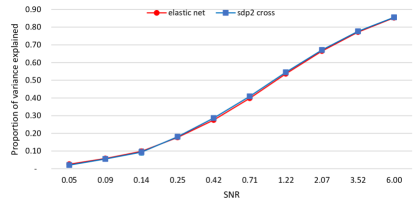

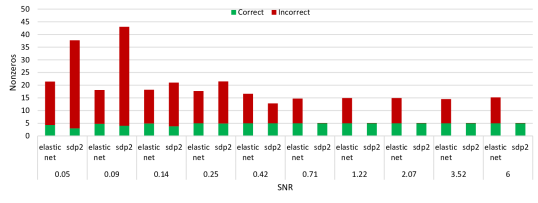

Figure 10 plots the relative risk, relative test error, proportion of variance explained and sparsity results as a function of the SNR for instances with , , and . Figure 11 plots the same results for instances with . The setting with was also presented in [23].

We see that elastic net outperforms in low SNR settings, i.e., in SNR for and SNR for , but results in worse predictive performance for all other SNRs. Moreover, is able to recover the true sparsity pattern of for sufficiently large SNR, while elastic net is unable to do so. We also see that performs comparatively better than elastic net in instances with . Indeed, for large autocorrelations , features where still have predictive value, thus the dense estimator obtained by elastic net retains a relatively good predictive performance (however, such dense solutions are undesirable from an interpretability perspective). In contrast, when , such features are simply noise and elastic net results in overfitting, while methods that deliver sparse solution such as perform much better in comparison. We also note that selects model corresponding to sparsities in low SNRs, while it consistently selects models with in high SNRs. We point out that, as suggested in [36], the results for low SNR could potentially be improved by fitting models with .

6. Conclusions

In this paper we derive strong convex relaxations for sparse regression. The relaxations are based on the ideal formulations for rank-one quadratic terms with indicator variables. The new relaxations are formulated as semidefinite optimization problems in an extended space and are stronger and more general than the state-of-the-art formulations. In our computational experiments, the proposed conic formulations outperform the existing approaches, both in terms of accurately approximating the best subset selection problems and of achieving desirable estimation properties in statistical inference problems with sparsity.

Acknowledgments

A. Atamtürk is supported, in part, by Grant No. 1807260 from the National Science Foundation. A. Gómez is supported, in part, by Grants No. 1818700 and 2006762 from the National Science Foundation.

References

- Aktürk et al., [2009] Aktürk, M. S., Atamtürk, A., and Gürel, S. (2009). A strong conic quadratic reformulation for machine-job assignment with controllable processing times. Operations Research Letters, 37:187–191.

- Atamtürk and Gómez, [2018] Atamtürk, A. and Gómez, A. (2018). Strong formulations for quadratic optimization with M-matrices and indicator variables. Mathematical Programming, 170:141–176.

- Atamtürk et al., [2018] Atamtürk, A., Gómez, A., and Han, S. (2018). Sparse and smooth signal estimation: Convexification of formulations. arXiv preprint arXiv:1811.02655. BCOL Research Report 18.05, IEOR, UC Berkeley.

- Atamtürk and Narayanan, [2007] Atamtürk, A. and Narayanan, V. (2007). Cuts for conic mixed integer programming. In Fischetti, M. and Williamson, D. P., editors, Proceedings of the 12th International IPCO Conference, pages 16–29.

- Bertsimas and King, [2015] Bertsimas, D. and King, A. (2015). OR forum – an algorithmic approach to linear regression. Operations Research, 64:2–16.

- Bertsimas et al., [2016] Bertsimas, D., King, A., Mazumder, R., et al. (2016). Best subset selection via a modern optimization lens. The Annals of Statistics, 44:813–852.

- Bertsimas and Van Parys, [2017] Bertsimas, D. and Van Parys, B. (2017). Sparse high-dimensional regression: Exact scalable algorithms and phase transitions. arXiv preprint arXiv:1709.10029.

- Bixby, [2012] Bixby, R. E. (2012). A brief history of linear and mixed-integer programming computation. Documenta Mathematica, pages 107–121.

- Chichignoud et al., [2016] Chichignoud, M., Lederer, J., and Wainwright, M. J. (2016). A practical scheme and fast algorithm to tune the lasso with optimality guarantees. The Journal of Machine Learning Research, 17:8162–8181.

- Cozad et al., [2014] Cozad, A., Sahinidis, N. V., and Miller, D. C. (2014). Learning surrogate models for simulation-based optimization. AIChE Journal, 60:2211–2227.

- Dheeru and Karra Taniskidou, [2017] Dheeru, D. and Karra Taniskidou, E. (2017). UCI machine learning repository.

- Dong et al., [2015] Dong, H., Chen, K., and Linderoth, J. (2015). Regularization vs. relaxation: A conic optimization perspective of statistical variable selection. arXiv preprint arXiv:1510.06083.

- Efron et al., [2004] Efron, B., Hastie, T., Johnstone, I., Tibshirani, R., et al. (2004). Least angle regression. The Annals of Statistics, 32:407–499.

- Fan and Li, [2001] Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96:1348–1360.

- Frangioni and Gentile, [2006] Frangioni, A. and Gentile, C. (2006). Perspective cuts for a class of convex 0–1 mixed integer programs. Mathematical Programming, 106:225–236.

- Frangioni et al., [2020] Frangioni, A., Gentile, C., and Hungerford, J. (2020). Decompositions of semidefinite matrices and the perspective reformulation of nonseparable quadratic programs. Mathematics of Operations Research, 45(1):15–33.

- Frank and Friedman, [1993] Frank, L. E. and Friedman, J. H. (1993). A statistical view of some chemometrics regression tools. Technometrics, 35:109–135.

- Gómez, [2018] Gómez, A. (2018). Strong formulations for conic quadratic optimization with indicator variables. Forthcoming in Mathematical Programming.

- Gómez and Prokopyev, [2020] Gómez, A. and Prokopyev, O. (2020). A mixed-integer fractional optimization approach to best subset selection. Forthcoming in INFORMS Journal on Computing.

- Günlük and Linderoth, [2010] Günlük, O. and Linderoth, J. (2010). Perspective reformulations of mixed integer nonlinear programs with indicator variables. Mathematical Programming, 124:183–205.

- Han et al., [2020] Han, S., Gómez, A., and Atamtürk, A. (2020). 2x2 convexifications for convex quadratic optimization with indicator variables. arXiv preprint arXiv:2004.07448.

- Hastie et al., [2001] Hastie, T., Tibshirani, R., and Friedman, J. (2001). The elements of statistical learning: Data mining, inference, and prediction, volume 1. Springer series in statistics New York, NY, USA.

- Hastie et al., [2017] Hastie, T., Tibshirani, R., and Tibshirani, R. J. (2017). Extended comparisons of best subset selection, forward stepwise selection, and the lasso. arXiv preprint arXiv:1707.08692.

- Hastie et al., [2015] Hastie, T., Tibshirani, R., and Wainwright, M. (2015). Statistical learning with sparsity: The lasso and generalizations. CRC press.

- Hazimeh and Mazumder, [2018] Hazimeh, H. and Mazumder, R. (2018). Fast best subset selection: Coordinate descent and local combinatorial optimization algorithms. arXiv preprint arXiv:1803.01454.

- Hazimeh et al., [2020] Hazimeh, H., Mazumder, R., and Saab, A. (2020). Sparse regression at scale: Branch-and-bound rooted in first-order optimization. arXiv preprint arXiv:2004.06152.

- Hebiri et al., [2011] Hebiri, M., Van De Geer, S., et al. (2011). The smooth-lasso and other + -penalized methods. Electronic Journal of Statistics, 5:1184–1226.

- Hoerl and Kennard, [1970] Hoerl, A. E. and Kennard, R. W. (1970). Ridge regression: Biased estimation for nonorthogonal problems. Technometrics, 12:55–67.

- Huang et al., [2018] Huang, J., Jiao, Y., Liu, Y., and Lu, X. (2018). A constructive approach to L0 penalized regression. The Journal of Machine Learning Research, 19:403–439.

- Hunter and Li, [2005] Hunter, D. R. and Li, R. (2005). Variable selection using MM algorithms. Annals of Statistics, 33:1617.

- Jeon et al., [2017] Jeon, H., Linderoth, J., and Miller, A. (2017). Quadratic cone cutting surfaces for quadratic programs with on–off constraints. Discrete Optimization, 24:32–50.

- Kocuk et al., [2016] Kocuk, B., Dey, S. S., and Sun, X. A. (2016). Strong socp relaxations for the optimal power flow problem. Operations Research, 64:1177–1196.

- Kocuk et al., [2018] Kocuk, B., Dey, S. S., and Sun, X. A. (2018). Matrix minor reformulation and SOCP-based spatial branch-and-cut method for the AC optimal power flow problem. Mathematical Programming Computation, 10:557–596.

- Lin et al., [2014] Lin, X., Pham, M., and Ruszczyński, A. (2014). Alternating linearization for structured regularization problems. The Journal of Machine Learning Research, 15:3447–3481.

- Mazumder et al., [2011] Mazumder, R., Friedman, J. H., and Hastie, T. (2011). Sparsenet: Coordinate descent with nonconvex penalties. Journal of the American Statistical Association, 106:1125–1138.

- Mazumder et al., [2017] Mazumder, R., Radchenko, P., and Dedieu, A. (2017). Subset selection with shrinkage: Sparse linear modeling when the SNR is low. arXiv preprint arXiv:1708.03288.

- Miller, [2002] Miller, A. (2002). Subset selection in regression. CRC Press.

- Miyashiro and Takano, [2015] Miyashiro, R. and Takano, Y. (2015). Mixed integer second-order cone programming formulations for variable selection in linear regression. European Journal of Operational Research, 247:721–731.

- Natarajan, [1995] Natarajan, B. K. (1995). Sparse approximate solutions to linear systems. SIAM Journal on Computing, 24:227–234.

- Nevo and Ritov, [2017] Nevo, D. and Ritov, Y. (2017). Identifying a minimal class of models for high-dimensional data. The Journal of Machine Learning Research, 18:797–825.

- Padilla et al., [2017] Padilla, O. H. M., Sharpnack, J., Scott, J. G., and Tibshirani, R. J. (2017). The dfs fused lasso: Linear-time denoising over general graphs. The Journal of Machine Learning Research, 18:176–1.

- Pilanci et al., [2015] Pilanci, P., Wainwright, M. J., and El Ghaoui, L. (2015). Sparse learning via boolean relaxations. Mathematical Programming, 151:63–87.

- Tibshirani, [1996] Tibshirani, R. (1996). Regression shrinkage and selection via the Lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288.

- Tibshirani et al., [2005] Tibshirani, R., Saunders, M., Rosset, S., Zhu, J., and Knight, K. (2005). Sparsity and smoothness via the fused lasso. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67:91–108.

- Tibshirani, [2011] Tibshirani, R. J. (2011). The solution path of the generalized lasso. Stanford University.

- Xie and Deng, [2018] Xie, W. and Deng, X. (2018). The CCP selector: Scalable algorithms for sparse ridge regression from chance-constrained programming. arXiv preprint arXiv:1806.03756.

- Zhang et al., [2010] Zhang, C.-H. et al. (2010). Nearly unbiased variable selection under minimax concave penalty. The Annals of Statistics, 38:894–942.

- Zhang et al., [2008] Zhang, C.-H., Huang, J., et al. (2008). The sparsity and bias of the Lasso selection in high-dimensional linear regression. The Annals of Statistics, 36:1567–1594.

- Zhang et al., [2012] Zhang, C.-H., Zhang, T., et al. (2012). A general theory of concave regularization for high-dimensional sparse estimation problems. Statistical Science, 27:576–593.

- Zhang et al., [2014] Zhang, Y., Wainwright, M. J., and Jordan, M. I. (2014). Lower bounds on the performance of polynomial-time algorithms for sparse linear regression. In Conference on Learning Theory, pages 921–948.

- Zhao and Yu, [2006] Zhao, P. and Yu, B. (2006). On model selection consistency of lasso. The Journal of Machine Learning Research, 7(Nov):2541–2563.

- Zou, [2006] Zou, H. (2006). The adaptive lasso and its oracle properties. Journal of the American Statistical Association, 101:1418–1429.

- Zou and Hastie, [2005] Zou, H. and Hastie, T. (2005). Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67:301–320.

- Zou and Li, [2008] Zou, H. and Li, R. (2008). One-step sparse estimates in nonconcave penalized likelihood models. The Annals of Statistics, 36:1509.