We describe Mêlée, a meta-learning algorithm for learning a good exploration policy in the interactive contextual bandit setting.

Here, an algorithm must take actions based on contexts, and learn based only on a reward signal from the action taken, thereby generating an exploration/exploitation trade-off.

Mêlée addresses this trade-off by learning a good exploration strategy for offline tasks based on synthetic data, on which it can simulate the contextual bandit setting.

Based on these simulations, Mêlée uses an imitation learning strategy to learn a good exploration policy that can then be applied to true contextual bandit tasks at test time.

We compare Mêlée to seven strong baseline contextual bandit algorithms on a set of three hundred real-world datasets, on which it outperforms alternatives in most settings, especially when differences in rewards are large.

Finally, we demonstrate the importance of having a rich feature representation for learning how to explore.

Machine Learning, ICML

1 Introduction

In a contextual bandit problem, an agent attempts to optimize its behavior over a sequence of rounds based on limited feedback (Kaelbling, 1994; Auer, 2003; Langford & Zhang, 2008).

In each round, the agent chooses an action based on a context (features) for that round, and observes a reward for that action but no others (§ 2).

Contextual bandit problems arise in many real-world settings like online recommendations and personalized medicine.

As in reinforcement learning, the agent must learn to balance exploitation (taking actions that, based on past experience, it believes will lead to high instantaneous reward) and exploration (trying actions that it knows less about).

In this paper, we present a meta-learning approach to automatically learn a good exploration mechanism from data. To achieve this, we use synthetic supervised learning data sets on which we can simulate contextual bandit tasks in an offline setting.

Based on these simulations, our algorithm, Mêlée (MEta LEarner for Exploration)111Code release: the code is available online https://www.dropbox.com/sh/dc3v8po5cbu8zaw/AACu1f_4c4wIZxD1e7W0KVZ0a?dl=0, learns a good heuristic exploration strategy that should ideally generalize to future contextual bandit problems.

Mêlée contrasts with more classical approaches to exploration (like -greedy or LinUCB; see § 5), in which exploration strategies are constructed by expert algorithm designers.

These approaches often achieve provably good exploration strategies in the worst case, but are potentially overly pessimistic and are sometimes computationally intractable.

At training time (§ 2.3), Mêlée simulates many contextual bandit problems from fully labeled synthetic data.

Using this data, in each round, Mêlée is able to counterfactually simulate what would happen under all possible action choices.

We can then use this information to compute regret estimates for each action, which can be optimized using the AggreVaTe imitation learning algorithm (Ross & Bagnell, 2014).

Our imitation learning strategy mirrors that of the meta-learning approach of Bachman et al. (2017) in the active learning setting.

We present a simplified, stylized analysis of the behavior of Mêlée to ensure that our cost function encourages good behavior (§ 3).

Empirically, we use Mêlée to train an exploration policy on only synthetic datasets and evaluate the resulting bandit performance across three hundred (simulated) contextual bandit tasks (§ 4.4), comparing to a number of alternative exploration algorithms, and showing the efficacy of our approach (§ 4.6).

2 Meta-Learning for Contextual Bandits

Contextual bandits is a model of interaction in which an agent chooses actions (based on contexts) and receives immediate rewards for that action alone.

For example, in a simplified news personalization setting, at each time step , a user arrives and the system must choose a news article to display to them.

Each possible news article corresponds to an action , and the user corresponds to a context .

After the system chooses an article to display, it can observe, for instance, the amount of time that the user spends reading that article, which it can use as a reward .

The goal of the system is to choose articles to display that maximize the cumulative sum of rewards, but it has to do this without ever being able to know what the reward would have been had it shown a different article .

Formally, we largely follow the setup and notation of Agarwal et al. (2014).

Let be an input space of contexts (users) and be a finite action space (articles).

We consider the statistical setting in which there exists a fixed but unknown distribution over pairs , where is a vector of rewards (for convenience, we assume all rewards are bounded in ).

In this setting, the world operates iteratively over rounds .

Each round :

1.

The world draws and reveals context .

2.

The agent (randomly) chooses action based on , and observes reward .

The goal of an algorithm is to maximize the cumulative sum of rewards over time.

Typically the primary quantity considered is the average regret of a sequence of actions to the behavior of the best possible function in a prespecified class :

(1)

An agent is call no-regret if its average regret is zero in the limit of large .

2.1 Policy Optimization over Fixed Histories

To produce a good agent for interacting with the world, we assume access to a function class and to an oracle policy optimizer for that function class.

For example, may be a set of single layer neural networks mapping user features (e.g., IP, browser, etc.)

to predicted rewards for actions (articles) , where is the total number of actions.

Formally, the observable record of interaction resulting from round is the tuple , where is the probability that the agent chose action , and the full history of interaction is .

The oracle policy optimizer, PolOpt, takes as input a history of user interactions with the news recommendation system and outputs an with low expected regret.

A standard example of a policy optimizer is to combine inverse propensity scaling (IPS) with a regression algorithm (Dudik et al., 2011).

Here, given a history , each tuple in that history is mapped to a multiple-output regression example.

The input for this regression example is the same ; the output is a vector of costs, all of which are zero except the component, which takes value .

For example, if the agent chose to show to user article , made that decision with probability, and received a reward of , then the corresponding output vector would be .

This mapping is done for all tuples in the history, and then a supervised learning algorithm on the function class is used to produce a low-regret regressor . This is the function returned by the underlying policy optimizer.

IPS has this nice property that it is an unbiased estimator; unfortunately, it tends to have large variance especially when some probabilities are small.

In addition to IPS, there are several standard policy optimizers that mostly attempt to reduce variance while remaining unbiased: the direct method (which estimates the reward function from given data and

uses this estimate in place of actual reward), the double-robust estimator, and multitask regression.

In our experiments, we use the direct method because we found it best on average, but in principle any could be used.

2.2 Test Time Behavior of Mêlée

In order to have an effective approach to the contextual bandit problem, one must be able to both optimize a policy based on historic data and make decisions about how to explore.

After all, in order for the example news recommendation system to learn whether a particular user is interested in news articles on some topic is to try showing such articles to see how the user responds (or to generalize from related articles or users).

The exploration/exploitation dilemma is fundamentally about long-term payoffs: is it worth trying something potentially suboptimal now in order to learn how to behave better in the future?

A particularly simple and effective form of exploration is -greedy: given a function output by PolOpt, act according to with probability and act uniformly at random with probability .

Intuitively, one would hope to improve on such a strategy by taking more (any!) information into account; for instance, basing the probability of exploration on ’s uncertainty.

Our goal in this paper is to learn how to explore from experience.

The training procedure for Mêlée will use offline supervised learning problems to learn an exploration policy , which takes two inputs: a function and a context , and outputs an action.

In our example, will be the output of the policy optimizer on all historic data, and will be the current user.

This is used to produce an agent which interacts with the world, maintaining an initially empty history buffer , as:

1.

The world draws and reveals context .

2.

The agent computes and a greedy action .

3.

The agent plays with probability , and uniformly at random otherwise.

4.

The agent observes and appends to the history ,

where if ; and if .

Here, is the function optimized on the historical data, and uses it and to choose an action.

Intuitively, might choose to use the prediction most of the time, unless is quite uncertain on this example, in which case might choose to return the second (or third) most likely action according to .

The agent then performs a small amount of additional -greedy-style exploration: most of the time it acts according to but occasionally it explores some more.

In practice (§ 4), we find that setting is optimal in aggregate, but non-zero is necessary for our theory (§ 3).

2.3 Training Mêlée by Imitation Learning

The meta-learning challenge is: how do we learn a good exploration policy ?

We assume we have access to fully labeled data on which we can train ; this data must include context/reward pairs, but where the reward for all actions is known.

This is a weak assumption: in practice, we use purely synthetic data as this training data; one could alternatively use any fully labeled classification dataset (this is inspired by Beygelzimer & Langford (2009)).

Under this assumption about the data, it is natural to think of ’s behavior as a sequential decision making problem in a simulated setting, for which a natural class of learning algorithms to consider are imitation learning algorithms (Daumé et al., 2009; Ross et al., 2011; Ross & Bagnell, 2014; Chang et al., 2015).222In other work on meta-learning, such problems are often cast as full reinforcement-learning problems. We opt for imitation learning instead because it is computationally attractive and effective when a simulator exists.

Informally, at training time, Mêlée will treat one of these synthetic datasets as if it were a contextual bandit dataset.

At each time step , it will compute by running PolOpt on the historical data, and then ask: for each action, what would the long time reward look like if I were to take this action.

Because the training data for Mêlée is fully labeled, this can be evaluated for each possible action, and a policy can be learned to maximize these rewards.

Importantly, we wish to train using one set of tasks (for which we have fully supervised data on which to run simulations) and apply it to wholly different tasks (for which we only have bandit feedback).

To achieve this, we allow to depend representationally on in arbitrary ways: for instance, it might use features that capture ’s uncertainty on the current example (see § 4.1 for details).

We additionally allow to depend in a task-independent manner on the history (for instance, which actions have not yet been tried): it can use features of the actions, rewards and probabilities in the history but not depend directly on the contexts .

This is to ensure that only learns to explore and not also to solve the underlying task-dependent classification problem.

More formally, in imitation learning, we assume training-time access to an expert, , whose behavior we wish to learn to imitate at test-time.

From this, we can define an optimal reference policy , which effectively “cheats” at training time by looking at the true labels.

The learning problem is then to estimate to have as similar behavior to as possible, but without access to those labels.

Suppose we wish to learn an exploration policy for a contextual bandit problem with actions.

We assume access to supervised learning datasets , where each of size , where each is from a (possibly different) input space and the reward vectors are all in .We wish to learn an exploration policy with maximal reward: therefore, should imitate a that always chooses its action optimally.

We additionally allow to depend on a very small amount of fully labeled data from the task at hand, which we use to allow to calibrate ’s predictions.Because needs to learn to be task independent, we found that if s were uncalibrated, it was very difficult for to generalize well to unseen tasks. In our experiments we use only fully labeled examples, but alternative approaches to calibrating that do not require this data would be ideal.

Algorithm 1Mêlée supervised training sets , hypothesis class , exploration rate , number of validation examples , feature extractor

1:for round do

2: initialize meta-dataset and choose dataset at random from

3: partition and permute randomly into train Tr and validation Val where

4: set history

5:for round do

6: let

7:for each action do

8: optimize -- on augmented history

9: roll-out: estimate , the value of , using and a roll-out policy

10:endfor

11: compute

12: aggregate

13: roll-in: with probability , is an indicator function

14: append history

15:endfor

16: update

17:endfor

18:return

The imitation learning algorithm we use is AggreVaTe (Ross & Bagnell, 2014) (closely related to DAgger (Ross et al., 2011)), and is instantiated for the contextual bandits meta-learning problem in Alg 1. AggreVaTe learns to choose actions to minimize the cost-to-go of the expert

rather than the zero-one classification loss of mimicking its actions. On the first iteration AggreVaTe collects data

by observing the expert perform the task, and in each trajectory, at time , explores an action in state , and

observes the cost-to-go of the expert after performing this action.

Each of these steps generates a cost-weighted training example and AggreVaTe trains a policy to

minimize the expected cost-to-go on this dataset. At each following iteration , AggreVaTe collects data through

interaction with the learner as follows: for each trajectory, begin by using the current learner’s policy to

perform the task, interrupt at time , explore a roll-in action in the current state , after which control is

provided back to the expert to continue up to time-horizon . This results in new examples of the cost-to-go

(roll-out value) of the expert , under the distribution of states visited

by the current policy . This new data is aggregated with all previous data to train the next policy ;

more generally, this data can be used by a no-regret online learner to update the policy and obtain . This is

iterated for some number of iterations and the best policy found is returned. AggreVaTe optionally allow the algorithm

to continue executing the expert’s actions with small probability , instead of always executing , up to the

time step where an action is explored and control is shifted to the expert.

Mêlée operates in an iterative fashion, starting with an arbitrary and improving it through interaction with an expert.

Over rounds, Mêlée selects random training sets and simulates the test-time behavior on that training set.

The core functionality is to generate a number of states on which to train , and to use the supervised data to estimate the value of every action from those states.

Mêlée achieves this by sampling a random supervised training set and setting aside some validation data from it (3).

It then simulates a contextual bandit problem on this training data; at each time step , it tries all actions and “pretends” like they were appended to the current history (8) on which it trains a new policy and evaluates it’s roll-out value (9, described below).

This yields, for each , a new training example for , which is added to ’s training set (12); the features for this example are features of the classifier based on true history (11) (and possibly statistics of the history itself), with a label that gives, for each action, the corresponding value of that action (the s computed in 9).

Mêlée then must commit to a roll-in action to actually take; it chooses this according to a roll-in policy (13), described below.

The two key questions are: how to choose roll-in actions and how to evaluate roll-out values.

Roll-in actions. The distribution over states visited by Mêlée depends on the actions taken, and in general it is good to have that distribution match what is seen at test time as closely as possible.

This distribution is determined by a roll-in policy (13), controlled in Mêlée by exploration parameter .

As , the roll-in policy approaches a uniform random policy; as , the roll-in policy becomes deterministic.

When the roll-in policy does not explore, it acts according to .

Roll-out values. The ideal value to assign to an action (from the perspective of the imitation learning procedure) is that total reward (or advantage) that would be achieved in the long run if we took this action and then behaved according to our final learned policy.

Unfortunately, during training, we do not yet know the final learned policy. Thus, a surrogate roll-out policy

is used instead. A convenient, and often computationally efficient alternative, is to evaluate the value assuming all future actions were taken by the expert (Langford & Zadrozny, 2005; Daumé et al., 2009; Ross & Bagnell, 2014). In our setting, at any time step , the expert has access to the fully supervised reward vector for the context

. When estimating the roll-out value for an action , the expert will return the true reward value for this action and we use this as our estimate for the roll-out value.

3 Theoretical Guarantees

We analyze Mêlée, showing that the no-regret property of AggreVaTe can be leveraged in our meta-learning setting for learning contextual bandit exploration. In particular, we first relate the regret of the learner in line 16 to the overall regret of . This will show that, if the underlying classifier improves sufficiently quickly, Mêlée will achieve sublinear regret. We then show that for a specific choice of underlying classifier (Banditron), this is achieved.

Mêlée is an instantiation of AggreVaTe (Ross & Bagnell, 2014); as such, it inherits AggreVaTe’s regret guarantees.

Let denote the empirical minimum expected cost-sensitive classification regret achieved by policies in the class on all the data over the iterations of training when compared to the Bayes optimal regressor, for the uniform distribution over , the distribution of states at time induced by executing policy , and the cost-to-go of the expert:

Theorem 1 (Thm 2.2 of Ross & Bagnell (2014), adapted)

After rounds in the parameter-free setting, if a Learn (16) is no-regret algorithm, then as , with probability , it holds that

,

where is the reward of the exploration policy, is the average policy returned, and is the average regression regret for each accurately predicting .

This says that if we can achieve low regret at the problem of learning on the training data it observes (“” in Mêlée), i.e. is small, then this translates into low regret in the contextual-bandit setting.

At first glance this bound looks like it may scale linearly with . However, the bound in Theorem 1 is dependent on .

Note however, that is a combination of the context vector and the classification function .

As , one would hope that improves significantly and decays quickly.

Thus, sublinear regret may still be achievable when learns sufficiently quickly as a function of .

For instance, if is optimizing a strongly convex loss function, online gradient descent achieves a regret guarantee of (e.g., Theorem 3.3 of Hazan et al. (2016)), potentially leading to a regret for Mêlée of .

The above statement is informal (it does not take into account the interaction between learning and ).

However, we can show a specific concrete example: we analyze Mêlée’s test-time behavior when the underlying learning algorithm is Banditron.

Banditron is a variant of the multiclass Perceptron that operates under bandit feedback.

Details of this analysis (and proofs, which directly follow the original Banditron analysis) are given in Appendix A; here we state the main result.

Let be the edge of over , and let be an overall measure of the edge. For instance if simply returns ’s prediction, then all and .

We can then show the following:

Theorem 2

Assume that for the sequence of examples, , we have, for all , .

Let be any matrix, let be the cumulative hinge-loss of , let be a uniform exploration probability, and let be the complexity of .

Assume that for all .

Then the number of mistakes made by Mêlée with Banditron as PolOpt satisfies:

(2)

where the expectation is taken with respect to the randomness of the algorithm.

Note that under the assumption for all , we have .

The analysis gives the same mistake bound for Banditron but with the additional factor of , hence this result improves upon the standard Banditron analysis only when .

This result is highly stylized and the assumption that is overly strong. This assumption ensures that never decreases the probability of a “correct” action.

It does, however, help us understand the behavior of Mêlée, qualitatively:

First, the quantity that matters in Theorem 2, is (in the 0/1 loss case) exactly what Mêlée is optimizing: the expected improvement for choosing an action against ’s recommendation.

Second, the benefit of using within Banditron is a local benefit: because is trained with expert rollouts, as discussed in § 3, the primary improvement in the analysis is to ensure that does a better job predicting (in a single step) than does.

An obvious open question is whether it is possible to base the analysis on the regret of (rather than its error) and whether it is possible to extend beyond the simple Banditron setting.

4 Experimental Setup and Results

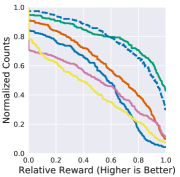

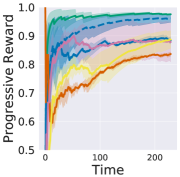

Figure 1: Comparison of algorithms on

classification problems. (Left)

Comparison of all exploration algorithms using the empirical

cumulative distribution function of the relative progressive validation

return (upper-right is optimal). The curves for -decreasing & -greedy coincide.

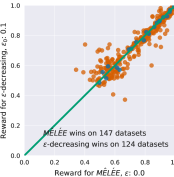

(Middle) Comparison of Mêlée to the second best

performing exploration algorithm (-decreasing), every data point represents

one of the datasets, x-axis shows the reward of , y-axis show

the reward of -decreasing, and red dots represent

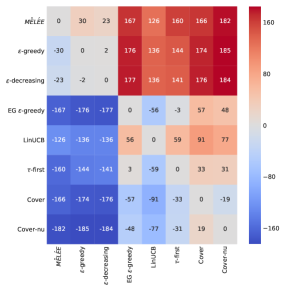

statistically significant runs. (Right) A representative learning curve on dataset #1144.Figure 2: Win statistics: each (row, column) entry shows the number of times the row algorithm won

against the column, minus the number of losses.

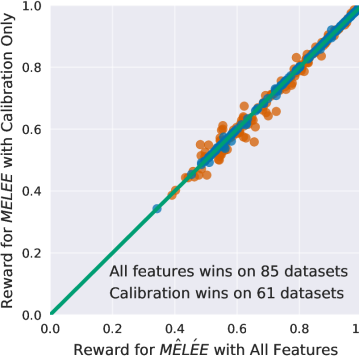

Figure 3: Comparison of training Mêlée with all the features (§ 4.1, y-axis) vs

training using only the calibrated prediction probabilities (x-axis). Mêlée gets

an additional leverage when using all the features.

Our experimental setup operates as follows:

Using a collection of synthetically generated classification problems, we train an exploration policy using Mêlée (Alg 1).

This exploration policy learns to explore on the basis of calibrated probabilistic predictions from together with a predefined set of exploration features (§ 4.1).

Once is learned and fixed, we follow the test-time behavior described in § 2.2 on a set of “simulated” contextual bandit problems, derived from standard classification tasks.

In all cases, the underlying classifier is a linear model trained with a policy optimizer that runs stochastic gradient descent.

We seek to answer two questions experimentally: (1) How

does Mêlée compare empirically to alternative (expert designed) exploration strategies?

(2) How important are the additional features used by Mêlée in comparison to using calibrated probability

predictions from as features?

4.1 Training Details for the Exploration Policy

Exploration Features.

In our experiments, the exploration policy is trained based on features (Alg 1, 12).

These features are allowed to depend on the current classifier , and on any part of the history except the inputs in order to maintain task independence.

We additionally ensure that its features are independent of the dimensionality of the inputs, so that can generalize to datasets of arbitrary dimensions.

The specific features we use are listed below; these are largely inspired by Konyushkova et al. (2017) but adapted and augmented to our setting.

The features of that we use are:

a)predicted probability ;

b)entropy of the predicted probability distribution;

c)a one-hot encoding for the predicted action .

The features of that we use are:

a)current time step ;

b)normalized counts for all previous actions predicted so far;

c)average observed rewards for each action;

d)empirical variance of the observed rewards for each action in the history.

In our experiments, we found that it is essential to calibrate the predicted probabilities of the classifier .

We use a very small held-out dataset, of size , to achieve this.

We use Platt’s scaling (Platt, 1999; Lin et al., 2007) method to calibrate

the predicted probabilities. Platt’s scaling works by fitting a logistic regression

model to the classifier’s predicted scores.

Training Datasets. In our experiments, we follow Konyushkova et al. (2017) (and also Peters et al. (2014), in a different setting) and train the exploration policy only on synthetic data.

This is possible because the exploration policy never makes use of explicitly

and instead only accesses it via ’s behavior on it. We generate datasets

with uniformly distributed class conditional distributions. The datasets are always

two-dimensional. Details are in § 4.2.

4.2 Details of Synthetic Datasets

We generate datasets with uniformly distributed class conditional distributions.

We generate 2D datasets by first sampling a random variable representing the

Bayes classification error. The Bayes error is sampled uniformly from the interval to .

Next, we generate a balanced dataset where the data for each class lies within a

unit rectangle and sampled uniformly. We overlap the sampling rectangular

regions to generate a dataset with the desired Bayes error selected in the first

step.

4.3 Implementation Details.

Our implementation is based on scikit-learn (Pedregosa et al., 2011). We fix the training time exploration parameter

to . We train the exploration policy on synthetic datasets each of size with uniform class conditional distributions, a total of samples (§ 4.2).

We train using a linear classifier (Breiman, 2001) and set the hyper-parameters for the

learning rate, and data scaling methods using three-fold cross-validation on the whole meta-training dataset.

For the classifier class , we use a linear model trained with stochastic gradient descent. We standardize all features

to zero mean and unit variance, or scale the features to lie between zero and one. To select between the two scaling

methods, and tune the classifier’s learning rate, we use three-fold cross-validation on a small fully supervised

training set of size samples. The same set is used to calibrate the predicted probabilities of .

4.4 Evaluation Tasks and Metrics

Following Bietti et al. (2018), we use a collection of binary

classification datasets from

openml.org for evaluation; the precise list and download instructions is in Appendix B. These datasets cover a variety of different domains

including text & image processing, medical diagnosis, and sensory data.

We convert multi-class classification datasets into cost-sensitive

classification problems by using a encoding.Given these fully supervised cost-sensitive multi-class datasets, we simulate

the contextual bandit setting by only revealing the reward for

the selected actions.

For evaluation, we use progressive validation (Blum et al., 1999), which is exactly computing the reward of the algorithm.

Specifically, to evaluate the performance of an

exploration algorithm on a dataset of size , we compute the

progressive validation return as the average reward up to , where is the action chosen by the algorithm and is

the true reward vector.

Because our evaluation is over datasets, we report aggregate results in two forms.

The simpler one is Win/Loss Statistics:

We compare two exploration methods on a given

dataset by counting the number of statistically significant wins and losses.

An exploration algorithm wins over another algorithm if the

progressive validation return is statistically significantly larger than ’s return

at the level using a paired sample t-test.

We also report cumulative distributions of rewards for each algorithm. In particular, for a given

relative reward value (), the corresponding CDF value for a given algorithm is the fraction of datasets on

which this algorithm achieved reward at least . We compute relative reward by Min-Max normalization.

Min-Max normalization linearly transforms reward to , where min & max are the minimum & maximum rewards among all exploration algorithms.

4.5 Baseline Exploration Algorithms

Our experiments aim to determine how Mêlée compares to other standard exploration strategies.

In particular, we compare to:

-greedy:

With probability , explore uniformly at random; with probability act greedily according to (Sutton, 1996). Experimentally, we found optimal on average, consistent with the results of Bietti et al. (2018).

-decreasing:

selects a random action with probabilities , where ,

and is the index of the current round. In our experiments we set . (Sutton & Barto, 1998)

Exponentiated Gradient -greedy:

maintains a set of candidate values for -greedy exploration. At each

iteration, it runs a sampling procedure to select a new from a finite set of candidates. The probabilities

associated with the candidates are initialized uniformly and updated with the Exponentiated Gradient (EG) algorithm.

Following (Li et al., 2010b), we use the

candidate set for .

LinUCB:

Maintains confidence bounds for reward payoffs and selects actions with the highest confidence bound.

It is impractical to run “as is” due to high-dimensional matrix inversions. We use diagonal approximation to the

covariance when the dimensions exceeds . (Li et al., 2010a)

-first:

Explore uniformly on the first fraction of the data; after that, act greedily.

Cover:

Maintains a uniform distribution over a fixed number of policies. The policies are used to approximate a covering distribution

over policies that are good for both exploration and exploitation (Agarwal et al., 2014).

Cover Non-Uniform:

similar to Cover, but reduces the level of exploration of Cover to be more competitive with the Greedy method. Cover-Nu doesn’t

add extra exploration beyond the actions chose by the covering policies (Bietti et al., 2018).

In all cases, we select the best hyperparameters for each exploration algorithm following (Bietti et al., 2018).

These hyperparameters are: the choice of in -greedy, in -first, the number of bags, and the

tolerance for Cover and Cover-NU. We set , , , and .

4.6 Experimental Results

The overall results are shown in Figure 1. In the left-most figure, we see the CDFs for the different

algorithms. To help read this, note that at , we see that Mêlée has a relative reward at least on

more than 40% of datasets, while -decreasing and -greedy achieve this on about 30% of datasets.

We find that the two strongest baselines are -decreasing and -greedy (better when reward differences

are small, toward the left of the graph). The two curves for -decreasing and -greedy coincide. This happens

because the exploration probability for -decreasing decays rapidly approaching zero with a rate of

, where is the index of the current round. Mêlée outperforms the baselines in the “large reward”

regimes (right of graph) but underperforms -decreasing and -greedy in low reward regimes (left of graph).

In Figure 2, we show statistically-significant win/loss differences for each of the algorithms. Mêlée is the only algorithm that always wins more than it loses against other algorithms.

To understand more directly how Mêlée compares to -decreasing, in the middle figure of Figure 1, we

show a scatter plot of rewards achieved by Mêlée (x-axis) and -decreasing (y-axis) on each of the datasets,

with statistically significant differences highlighted in red and insignificant differences in blue.

Points below the diagonal line correspond to better performance by Mêlée (147 datasets) and points above to

-decreasing (124 datasets). The remaining 29 had no significant difference.

In the right-most graph in Figure 1, we show a representative example of learning curves for the various algorithms.

Here, we see that as more data becomes available, all the approaches improve (except -first, which has ceased to learn after of the data).

Finally, we consider the effect that the additional features have on Mêlée’s performance.

In particular, we consider a version of Mêlée with all features (this is the version used in all other experiments)

with an ablated version that only has access to the (calibrated) probabilities of each action from the underlying classifier .

The comparison is shown as a scatter plot in Figure 3.

Here, we can see that the full feature set does provide lift over just the calibrated probabilities,

with a win-minus-loss improvement of .

5 Related Work and Discussion

The field of meta-learning is based on the idea of replacing hand-engineered learning heuristics with heuristics learned from data.

One of the most relevant settings for meta-learning to ours is active learning, in which one aims to learn a decision function to decide which examples, from a pool of unlabeled examples, should be labeled.

Past approaches to meta-learning for active learning include reinforcement learning-based strategies (Woodward & Finn, 2017; Fang et al., 2017), imitation learning-based strategies (Bachman et al., 2017), and batch supervised learning-based strategies (Konyushkova et al., 2017).

Similar approaches have been used to learn heuristics for optimization (Li & Malik, 2016; Andrychowicz et al., 2016),

multiarm (non-contextual) bandits (Maes et al., 2012),

and neural architecture search (Zoph & Le, 2016), recently mostly based on (deep) reinforcement learning.

While meta-learning for contextual bandits is most similar to meta-learning for active learning, there is a fundamental difference that makes it significantly more challenging:

in active learning, the goal is to select as few examples as you can to learn, so by definition the horizon is short;

in contextual bandits, learning to explore is fundamentally a long-horizon problem, because what matters is not immediate reward but long term learning.

In reinforcement learning, Gupta et al. (2018) investigated the task of meta-learning an exploration strategy for a distribution of related tasks by learning a latent exploration space.

Similarly, Xu et al. (2018) proposed a teacher-student approach for learning to do exploration in off-policy reinforcement learning.

While these approaches are effective if the distribution of tasks is very similar and the state space is shared among different tasks, they fail to generalize when the tasks are different.

Our approach targets an easier problem than exploration in full reinforcement learning environments, and can generalize well across a wide range of different tasks with completely unrelated features spaces.

There has also been a substantial amount of work on constructing “good” exploration policies, in problems of varying complexity: traditional bandit settings (Karnin & Anava, 2016), contextual bandits (Féraud et al., 2016) and reinforcement learning (Osband et al., 2016).

In both bandit settings, most of this work has focused on the learning theory aspect of exploration: what exploration distributions guarantee that learning will succeed (with high probability)?

Mêlée, lacks such guarantees: in particular, if the data distribution of the observed contexts () in some test problem differs substantially from that on which Mêlée was trained, we can say nothing about the quality of the learned exploration.

Nevertheless, despite fairly substantial distribution mismatch (synthetic real-world), Mêlée works well in practice, and our stylized theory (§ 3) suggests that there may be an interesting avenue for developing strong theoretical results for contextual bandit learning with learned exploration policies, and perhaps other meta-learning problems.

In conclusion, we presented Mêlée, a meta-learning algorithm for learning exploration policies in the contextual bandit setting. Mêlée enjoys no-regret guarantees, and empirically it outperforms alternative exploration algorithm in most settings. One limitation of Mêlée is the computational resources required during the offline training phase on the synthetic datasets. In the future, we will work on improving the computational efficiency for Mêlée in the offline training phase and scale the experimental analysis to problems with larger number of classes.

References

Agarwal et al. (2014)

Agarwal, A., Hsu, D., Kale, S., Langford, J., Li, L., and Schapire, R. E.

Taming the monster: A fast and simple algorithm for contextual

bandits.

In In Proceedings of the 31st International Conference on

Machine Learning (ICML-14, pp. 1638–1646, 2014.

Andrychowicz et al. (2016)

Andrychowicz, M., Denil, M., Gomez, S., Hoffman, M. W., Pfau, D., Schaul, T.,

and de Freitas, N.

Learning to learn by gradient descent by gradient descent.

In Advances in Neural Information Processing Systems, pp. 3981–3989, 2016.

Auer (2003)

Auer, P.

Using confidence bounds for exploitation-exploration trade-offs.

The Journal of Machine Learning Research, 3:397–422, 2003.

Bachman et al. (2017)

Bachman, P., Sordoni, A., and Trischler, A.

Learning algorithms for active learning.

In ICML, 2017.

Beygelzimer & Langford (2009)

Beygelzimer, A. and Langford, J.

The offset tree for learning with partial labels.

In Proceedings of the 15th ACM SIGKDD international conference

on Knowledge discovery and data mining, pp. 129–138. ACM, 2009.

Bietti et al. (2018)

Bietti, A., Agarwal, A., and Langford, J.

A Contextual Bandit Bake-off.

working paper or preprint, May 2018.

Blum et al. (1999)

Blum, A., Kalai, A., and Langford, J.

Beating the hold-out: Bounds for k-fold and progressive

cross-validation.

In Proceedings of the twelfth annual conference on

Computational learning theory, pp. 203–208. ACM, 1999.

Breiman (2001)

Breiman, L.

Random forests.

Mach. Learn., 45(1):5–32, October 2001.

ISSN 0885-6125.

doi: 10.1023/A:1010933404324.

Chang et al. (2015)

Chang, K.-W., Krishnamurthy, A., Agarwal, A., Daumé, III, H., and Langford,

J.

Learning to search better than your teacher.

In Proceedings of the 32Nd International Conference on

International Conference on Machine Learning - Volume 37, ICML, pp. 2058–2066. JMLR.org, 2015.

Daumé et al. (2009)

Daumé, III, H., Langford, J., and Marcu, D.

Search-based structured prediction.

Machine Learning, 75(3):297–325, Jun

2009.

ISSN 1573-0565.

doi: 10.1007/s10994-009-5106-x.

Dudik et al. (2011)

Dudik, M., Hsu, D., Kale, S., Karampatziakis, N., Langford, J., Reyzin, L., and

Zhang, T.

Efficient optimal learning for contextual bandits.

arXiv preprint arXiv:1106.2369, 2011.

Fang et al. (2017)

Fang, M., Li, Y., and Cohn, T.

Learning how to active learn: A deep reinforcement learning approach.

In EMNLP, 2017.

Féraud et al. (2016)

Féraud, R., Allesiardo, R., Urvoy, T., and Clérot, F.

Random forest for the contextual bandit problem.

In Gretton, A. and Robert, C. C. (eds.), Proceedings of the

19th International Conference on Artificial Intelligence and Statistics,

volume 51 of Proceedings of Machine Learning Research, pp. 93–101,

Cadiz, Spain, 09–11 May 2016. PMLR.

Gupta et al. (2018)

Gupta, A., Mendonca, R., Liu, Y., Abbeel, P., and Levine, S.

Meta-reinforcement learning of structured exploration strategies.

arXiv preprint arXiv:1802.07245, 2018.

Hazan et al. (2016)

Hazan, E. et al.

Introduction to online convex optimization.

Foundations and Trends® in Optimization,

2(3-4):157–325, 2016.

Kaelbling (1994)

Kaelbling, L. P.

Associative reinforcement learning: Functions ink-dnf.

Machine Learning, 15(3):279–298, 1994.

Kakade et al. (2008)

Kakade, S. M., Shalev-Shwart, S., and Tewari, A.

Efficient bandit algorithms for online multiclass prediction.

In ICML, 2008.

Karnin & Anava (2016)

Karnin, Z. S. and Anava, O.

Multi-armed bandits: Competing with optimal sequences.

In Lee, D. D., Sugiyama, M., Luxburg, U. V., Guyon, I., and Garnett,

R. (eds.), Advances in Neural Information Processing Systems 29, pp. 199–207. Curran Associates, Inc., 2016.

Konyushkova et al. (2017)

Konyushkova, K., Sznitman, R., and Fua, P.

Learning active learning from data.

In Advances in Neural Information Processing Systems, 2017.

Langford & Zadrozny (2005)

Langford, J. and Zadrozny, B.

Relating reinforcement learning performance to classification

performance.

In Proceedings of the 22nd international conference on Machine

learning, pp. 473–480. ACM, 2005.

Langford & Zhang (2008)

Langford, J. and Zhang, T.

The epoch-greedy algorithm for multi-armed bandits with side

information.

In Advances in Neural Information Processing Systems 20, pp. 817–824. Curran Associates, Inc., 2008.

Li & Malik (2016)

Li, K. and Malik, J.

Learning to optimize.

arXiv preprint arXiv:1606.01885, 2016.

Li et al. (2010a)

Li, L., Chu, W., Langford, J., and Schapire, R. E.

A contextual-bandit approach to personalized news article

recommendation.

In Proceedings of the 19th International Conference on World

Wide Web, WWW ’10, pp. 661–670, New York, NY, USA, 2010a.

ACM.

ISBN 978-1-60558-799-8.

doi: 10.1145/1772690.1772758.

Li et al. (2010b)

Li, W., Wang, X., Zhang, R., Cui, Y., Mao, J., and Jin, R.

Exploitation and exploration in a performance based contextual

advertising system.

In Proceedings of the 16th ACM SIGKDD International Conference

on Knowledge Discovery and Data Mining, KDD ’10, pp. 27–36, New York, NY,

USA, 2010b. ACM.

Lin et al. (2007)

Lin, H.-T., Lin, C.-J., and Weng, R. C.

A note on platt’s probabilistic outputs for support vector machines.

Machine Learning, 68(3):267–276, Oct

2007.

ISSN 1573-0565.

doi: 10.1007/s10994-007-5018-6.

Maes et al. (2012)

Maes, F., Wehenkel, L., and Ernst, D.

Meta-learning of exploration/exploitation strategies: The multi-armed

bandit case.

In International Conference on Agents and Artificial

Intelligence, pp. 100–115. Springer, 2012.

Osband et al. (2016)

Osband, I., Blundell, C., Pritzel, A., and Van Roy, B.

Deep exploration via bootstrapped dqn.

In Lee, D. D., Sugiyama, M., Luxburg, U. V., Guyon, I., and Garnett,

R. (eds.), Advances in Neural Information Processing Systems 29, pp. 4026–4034. Curran Associates, Inc., 2016.

Pedregosa et al. (2011)

Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel,

O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V., Vanderplas, J.,

Passos, A., Cournapeau, D., Brucher, M., Perrot, M., and Duchesnay, E.

Scikit-learn: Machine learning in Python.

Journal of Machine Learning Research, 12:2825–2830,

2011.

Peters et al. (2014)

Peters, J., Mooij, J. M., Janzing, D., and Schölkopf, B.

Causal discovery with continuous additive noise models.

The Journal of Machine Learning Research, 15(1):2009–2053, 2014.

Platt (1999)

Platt, J. C.

Probabilistic outputs for support vector machines and comparisons to

regularized likelihood methods.

In ADVANCES IN LARGE MARGIN CLASSIFIERS, pp. 61–74. MIT

Press, 1999.

Ross & Bagnell (2014)

Ross, S. and Bagnell, J. A.

Reinforcement and imitation learning via interactive no-regret

learning.

arXiv preprint arXiv:1406.5979, 2014.

Ross et al. (2011)

Ross, S., Gordon, G., and Bagnell, J. A.

A reduction of imitation learning and structured prediction to

no-regret online learning.

In Proceedings of the Fourteenth International Conference on

Artificial Intelligence and Statistics, volume 15 of Proceedings of

Machine Learning Research, pp. 627–635, Fort Lauderdale, FL, USA, 11–13

Apr 2011. PMLR.

Sutton (1996)

Sutton, R. S.

Generalization in reinforcement learning: Successful examples using

sparse coarse coding.

In Advances in neural information processing systems, pp. 1038–1044, 1996.

Sutton & Barto (1998)

Sutton, R. S. and Barto, A. G.

Introduction to Reinforcement Learning.

MIT Press, Cambridge, MA, USA, 1st edition, 1998.

ISBN 0262193981.

Woodward & Finn (2017)

Woodward, M. and Finn, C.

Active one-shot learning.

arXiv preprint arXiv:1702.06559, 2017.

Xu et al. (2018)

Xu, T., Liu, Q., Zhao, L., Xu, W., and Peng, J.

Learning to explore with meta-policy gradient.

arXiv preprint arXiv:1803.05044, 2018.

Zoph & Le (2016)

Zoph, B. and Le, Q. V.

Neural architecture search with reinforcement learning.

arXiv preprint arXiv:1611.01578, 2016.

Supplementary Material For:

Meta-Learning for Contextual Bandit Exploration

Appendix A Stylized test-time analysis for Banditron: Details

The BanditronMêlée algorithm is specified in Alg 2. The is exactly the same as the typical test time behavior, except it uses a Banditron-type strategy for learning the underlying classifier in the place of PolOpt. PolicyEliminationMeta takes as arguments: (the learned exploration policy) and an added uniform exploration parameter.

The Banditron learns a linear multi-class classifier parameterized by a weight matrix of size , where is the input dimensionality.

The Banditron assumes a pure multi-class setting in which the reward for one (“correct”) action is 1 and the reward for all other actions is zero.

At each round , a prediction is made according to (summarized by ).

We then define an exploration distribution that “most of the time” acts according to , but smooths each action with probability.

The chosen action is sampled from this distribution and a binary reward is observed.

The weights of the Banditron are updated according to the Banditron update rule using .

Algorithm 2BanditronMêlée

1: initialize

2:for rounds : do

3: observe

4: compute

5: define

6: sample

7: observe reward

8: define as:

9: update

10:endfor

The only difference between BanditronMêlée and the original Banditron is the introduction of in the sampling distribution. The original algorithm achieves the following mistake bound shown below, which depends on the notion of multi-class hinge-loss.

In particular, the hinge-loss of on is , where is the for which . The overall hinge-loss is the sum of over the sequence of examples.

Theorem 3 (Thm. 1 and Corr. 2 of Kakade et al. (2008))

Assume that for the sequence of examples, , we have, for all , .

Let be any matrix, let be the cumulative hinge-loss of , and let be the complexity of .

The number of mistakes made by the Banditron satisfies

(3)

where the expectation is taken with respect to the randomness of the algorithm.

Furthermore, in a low noise setting (there exists with fixed complexity and loss ), then by setting , we obtain .

We can prove an analogous result for BanditronMêlée.

The key quantity that will control how much improves the execution of BanditronMêlée is how much improves on when is wrong.

In particular, let be the edge of over , and let be an overall measure of the edge. (If does nothing, then all and .)

Given this quantity, we can prove the following Theorem 2.

Proof:

[sketch]

The proof is a small modification of the original proof of Theorem 3.

The only change is that in the original proof, the following bound is used:

.

We use, instead:

.

The rest of the proof goes through identically.

Appendix B List of Datasets

The datasets we used can be accessed at https://www.openml.org/d/<id>.

The list of pairs below shows the (¡id¿ for the

datasets we used and the dataset size in number of examples: