propositiontheorem \aliascntresettheproposition \newaliascntlemmatheorem \aliascntresetthelemma \newaliascntcorollarytheorem \aliascntresetthecorollary \newaliascntdefinitiontheorem \aliascntresetthedefinition \newaliascntremarktheorem \aliascntresettheremark \newaliascntexampletheorem \aliascntresettheexample

Bayesian variable selection in linear regression models with instrumental variables

Abstract.

Many papers on high-dimensional statistics have proposed methods for variable selection and inference in linear regression models by relying explicitly or implicitly on the assumption that all regressors are exogenous. However, applications abound where endogeneity arises from selection biases, omitted variables, measurement errors, unmeasured confounding and many other challenges common to data collection (Fan et al., 2014). The most common cure to endogeneity issues consists in resorting to instrumental variable (IV) inference. The objective of this paper is to present a Bayesian approach to tackling endogeneity in high-dimensional linear IV models. Using a working quasi-likelihood combined with an appropriate sparsity inducing spike-and-slab prior distribution, we develop a semi-parametric method for variable selection in high-dimensional linear models with endogeneous regressors within a quasi-Bayesian framework. We derive some conditions under which the quasi-posterior distribution is well defined and puts most of its probability mass around the true value of the parameter as . We demonstrate through empirical work the fine performance of the proposed approach relative to some other alternatives. We also include include an empirical application that assesses the return on education by revisiting the work of Angrist and Keueger (1991).

Key words and phrases:

High-dimensional Bayesian inference, Endogeneity, Variable selection, Posterior contraction, Markov Chain Monte Carlo, linear regression2010 Mathematics Subject Classification:

62F15, 62Jxx1. Introduction

The linear regression model has imposed itself as a benchmark for assessing the relationship between a response variable of interest and a set of covariates, or regressors. A critical issue in regression models is that of endogeneity, that is when a subset of regressors is correlated with the regression model error. Basically endogenous variables are those influenced by some of the same forces that influence the response variable. For example, economists examining the effects of education on earnings have long been concerned with the endogeneity of education (Angrist and Keueger, 1991). “Ability” is often cited as one factor possibly correlated with earnings (those with higher ability earn more) and education (those with higher ability obtain more education). Endogeneity also arises from measurement errors in the explanatory variables. It is well-known in regressions with small set of regressors that endogeneity causes standard estimators such as the ordinary least squares estimator to be inconsistent.

The most common cure to endogeneity issues consists in resorting to instrumental variable (IV) inference. Consistent estimation is commonly obtained by relying on the so-called valid instrumental variables (IV); i.e. variables uncorrelated with the regression error but correlated with the endogenous regressors. This gives rise to the IV model:

where is the response variable, is the vector of explanatory variables, the vector of instruments, the vector of parameters, and is the sample size. A good account of the IV methodology in low-dimensional problems can be found in Angrist and Keueger (1991); Hansen (1982), and the references therein.

In this paper we consider high-dimensional linear regression models where the number of regressors is potentially larger than the sample size . This set up is not immune to endogeneity. In fact, beside the usual sources mentioned above, in some settings endogeneity can arise incidentally from a large number of regressors (see e.g. Fan and Liao (2014)). Recent work related to high-dimensional inference on linear IV models include Belloni et al. (2012), Gautier and Tsybakov (2014); Fan and Liao (2014); Belloni et al. (2017). Belloni et al. (2012) propose a two-step lasso/post-lasso approach for instrument selection and inference in linear IV models where the number of explanatory variables () is fixed but the number of instrumental variables () is large. Gautier and Tsybakov (2014) consider large and possibly large and propose the so-called Self-tuning IV estimator and non-asymptotic confidence intervals based on the Dantzig selection of Candes et al. (2007). Belloni et al. (2017) consider and large and propose estimators and confidence regions that are honest and asymptotically correct by relying on a two-step procedure using suitably orthogonalized instruments. Fan and Liao (2014) follows the generalized method of moments (GMM) approach, as introduced by Hansen (1982). However, when , the GMM objective function is too noisy an estimator of its population version. This has led Fan and Liao (2014) to propose the focused GMM (FGMM), which minimizes a GMM criterion that ignores the non-selected regressors.

This paper relies on GMM settings and proposes a Bayesian method for variable selection and inference in high-dimensional IV models. One of the key advantages of the Bayesian framework is the ability to easily perform inference on the parameters of the model, and incorporate existing prior information in the analysis. By only restricting the moments of the data, IV models obviate the need to assume an underlying data distribution (or complete specification of a likelihood function), and allow inferences about the parameter of interest based only on the partial information supplied by a set of moment conditions. One interesting development in the Bayesian literature over the past few years is the quasi-Bayesian framework, which allows the development of Bayesian procedures without a complete specification of a likelihood function (Chernozhukov and Hong, 2003; Liao et al., 2011; Kato et al., 2013; Atchadé et al., 2017) and makes it possible to effectively develop semi-parametric models, and moment equation models.

The main contributions of this paper are threefold. First, using a working quasi-likelihood combined with an appropriate sparsity inducing spike-and-slab prior distribution (Mitchell and Beauchamp, 1988; George and McCulloch, 1997), we develop a semi-parametric method for variable selection in high-dimensional linear models with endogeneous regressors within a quasi-Bayesian framework. Second, we study the statistical properties of the quasi-posterior distribution, (defined later in 3), as the dimension increases. Under some minimal assumptions, we show (see Theorem 1) that puts most of its probability mass around the true value of the parameter as . Third, we develop a practical and efficient Markov Chain Monte Carlo algorithm to sample from . To the best of our knowledge, ours is the first paper to study in detail the Bayesian approach to tackling endogeneity in high-dimensional linear IV models. The performance of the Bayesian IV methods is highlighted by Monte Carlo simulations. The paper also includes an empirical application that assesses the return on education using US data by revisiting the work of Angrist and Keueger (1991).

The rest of the paper is organized as follows. The model and the Bayesian method proposed are presented in Section 2. This section also presents our main results establishing the consistency of the selection method proposed. The MCMC sampling algorithm is introduced in Section 3 which also contains our simulation results. Section 4 contains the empirical application and concluding remarks are included in Section 5.

1.1. Notation

For an integer , we equip the Euclidean space with its usual Euclidean inner product , associated norm , and its Borel sigma-algebra. We set . We will also use the following norms on : , and .

For , we set , that is . For , the sparsity structure of is the element defined as .

Throughout the paper denotes the Euler number and represents .

2. Model and Method

Suppose that we have independent subjects, and observe on subject the random vector . We postulate the following model: for some ,

| (1) |

for some zero-mean (un-observable) real-valued random variable . The regression parameter is the quantity of interest. We consider the setting where . This problem has attracted an impressive literature over the last two decades, and it is now well-known that the regression parameter can be recovered if it is sparse – or close to be sparse – under appropriate assumptions on the regression matrix (see e.g. Bühlmann and van de Geer (2011); Hastie et al. (2015) and the references therein). In this work we consider the setting where some of the components of the regressor are endogeneous, in the sense that there are correlated with the error , so that . As documented in the introduction, this issue is very common in applications, and it is well-known that standard inferential procedures that ignore endogeneity are inconsistent in general. A well-established approach to mitigate endogeneity is to use instrumental variables. This is the approach taken here, and the set of instruments at our disposal is . More precisely we make the following data-ganerating assumption.

H 1.

are independent and identically distributed random vectors, where , and there exists such that , for all . Furthermore we assume that is conditionally sub-Gaussian in the sense that there exists such that for all ,

| (2) |

almost surely, where .

Although not explicitly stated in H1, it is expected that the intruments are correlated to the endogeneous components of , and this correlation together with (2) are leveraged to derive better behaved inference. This is classically done via the GMM estimator that minimizes

or penalized versions thereof, where , has rows , has rows , and symmetric positive definite weight matrix. However in a context where and are potentially larger than , this approach of using all the intruments may not work, because the GMM functional could be too noisy estimate of its population version. To circumvent this problem Fan and Liao (2014) proposed the idea of focused GMM that incorporates a moment selection step: only instruments associated to selected regression parameters are included in the model. Note here that the idea of moment selection differs from previous works on moments selection (as in for instance ) which deal with the question of how to retain only valid moment conditions. In our case, all the moments conditions are assumed valid, but we face the challenge of having too many of them, given the available sample size. The purpose of this work is to develop a Bayesian version of focused GMM.

Let , . For , , we define

for some diagonal matrix with nonnegative diagonal elements. We make the following assumption on the prior distribution of .

H 2.

For , and some absolute constant ,

where , and . Furthermore, given the components of are independent and

for constants that we specify later in Theorem 1.

Remark \theremark.

Discrete priors distributions that put independent Bernoulli distribution on each are common in Bayesian variable selection problems (George and McCulloch (1997)). Note here however that the probability parameter q depends on the dimension . As shown in (Castillo and van der Vaart (2012)), this feature is key to achieve posterior consistency as diverges.

Since our objective at the onset is to fit a sparse model, the idea of imposing a hard constrain on the sparsity level seems reasonable, and has been explored by others (see for instance Banerjee and Ghosal (2013)). The parameter needs not be a good estimate of , but rather an upper bound derived for instance from prior information or from limitation imposed by the available sample size.

Let be the diagonal matrix such that if , and if . Under assumptions H1 and H2, the posterior distribution of can be written as

| (3) |

that we view as a random probability measure on , and we derive in Theorem 1 some simple conditions under which put most of its probability mass around , where denotes the sparsity structure of , that is .

Without any loss of generality we will assume that

| (4) |

where denotes the -th column of , and we assume that the matrix takes the form

| (5) |

for some constant , where , and if the -th instrument is included with model , otherwise. We will write to denote the -th column of the matrix . And in the same vein, since , we will write to denote the submatrix of obtained by keeping only the columns of for which the corresponding component of is . Under the prior distribution assumption H2, the maximum number of instruments used in any given model is

| (6) |

which is expected to be of the same order as , the maximum number of active regressors allowed under prior H1. The matrix

plays an important role in the analysis. Its restricted eigenvalues are defined as follows. For we define

and

Note that these quantities depend on the random variable .

Theorem 1.

Proof.

See Section 5.1. ∎

In general cannot achieve perfect model recovery since the non-zero components of could be arbitrarily small, and hence easily missed. With and as above we define

Set . Then, clearly the set of Theorem 1 can also be written as

In other words, Theorem 1 implies that does not miss any of the large magnitude components of .

Remark \theremark.

-

•

The result implies that we should let scale as

for some tuning constant , and then choose as

for some tuning parameter . Finally the result suggests setting

for a tuning parameter .

-

•

The key parameter in the theorem is which depends both on the design matrix and on the strength of the instruments. For instance, suppose that we are in the situation where one of the instruments, say the first instrument, is weak in the sense that

In that case, if denotes the first unit vector of , we have . Hence

3. Markov Chain Monte Carlo computation and numerical experiments

In this section we develop a practical Markov Chain Monte Carlo algorithm to sample from the posterior distribution , and we explore the behavior of on two simulated data examples.

3.1. A MCMC sampler for

We begin with a description of the MCMC sampler. To sample we use a Metropolis-Hastings-within-Gibbs sampler, where we update given , then we update the selected component given , and finally update given . We refer the reader to Tierney (1994); Robert and Casella (2004) for introduction to basic MCMC algorithms.

To update , we follow a specific form of Metropolis-Hastings update analyzed in (Yang et al., 2016). To develop the details we rewrite the posterior in (3) as follows,

| (11) |

where . We randomly select one of the following two schemes to update , each with probability 0.5.

Single flip update: Choose an index uniformly at random, and form the new state by setting . We denote this by .

Move to the state with probability Pr() where the acceptance ratio is given by

For a single flip on where ,

where , and .

For a single flip on where ,

where .

Double flip update: Define the subsets and let . Choose an index pair uniformly at random, and form the new state by flipping to and to . We denote this by .

Move to the state with probability Pr(,) where the acceptance ratio is given by

For a double flip on and where and ,

.

The full conditionals of are standard distributions due to the use of Gaussian prior. We partition into , where groups the components of for which , and groups the remaining components. The conditional distributions of the two components are given by

3.2. Numerical Experiments

In this section we investigate the performance of our proposed approach via numerical simulations, using the same set up as in Fan and Liao (2014); Belloni et al. (2017). We simulate from a linear model

For each component of , we write if is endogeneous, and if is exogeneous. , and are generated according to two different setups which we outline below.

Setup 1:

where are independent . Here and are the transformations of a three-dimensional instrumental variable and . There are endogeneous variables with .

The Fourier basis are applied as the working instruments,

Setup 2:

where , , , , and .

The two setups are taken from Fan and Liao (2014) and Belloni et al. (2017) respectively. For both setups, we choose the design vector with number of non-zero components, , that takes the value

where is a signal-to-noise parameter. Varying the SNR parameter allows us to explore the performance of our approach for varying levels of signal strength. We performed simulations for , sample size , and number of covariates . corresponds to high SNR (hSNR) while corresponds to weak SNR (wSNR).

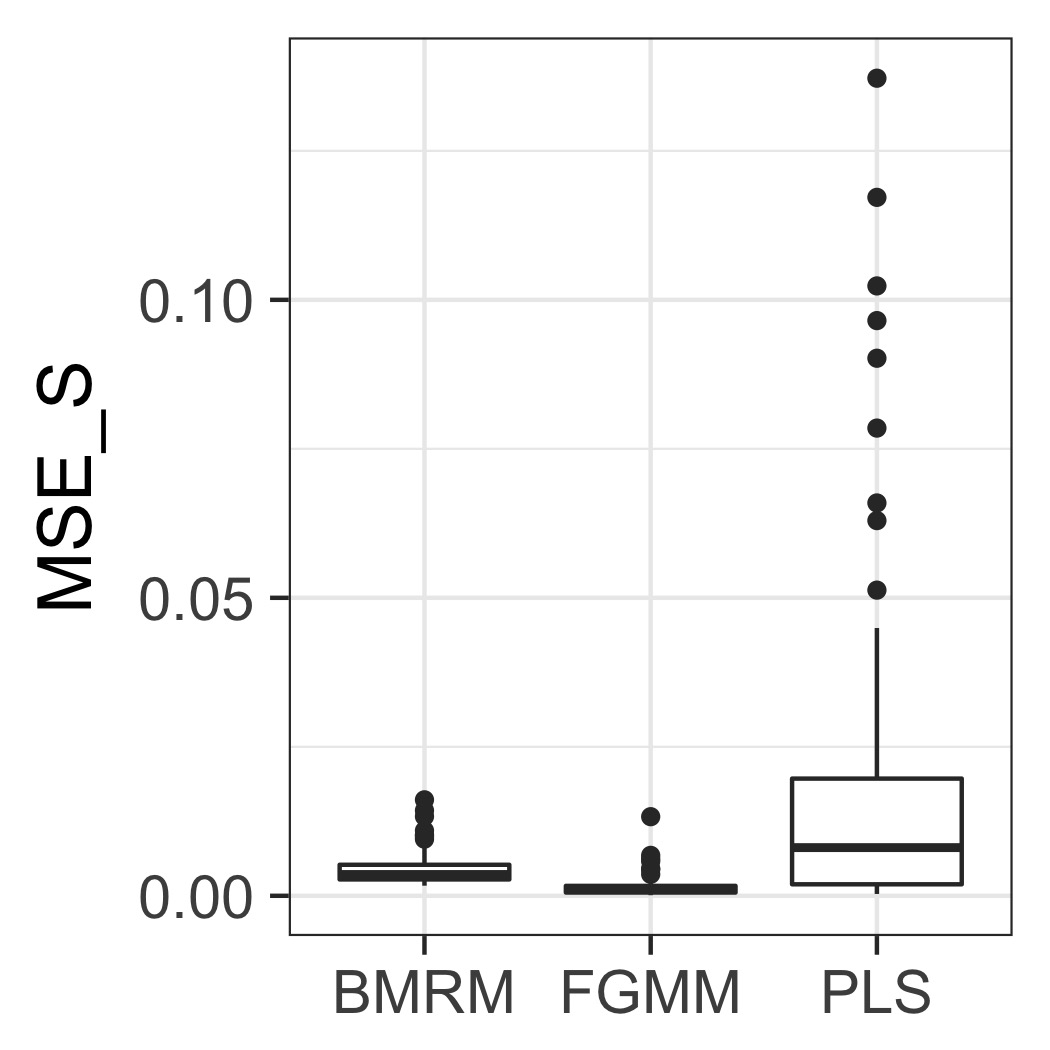

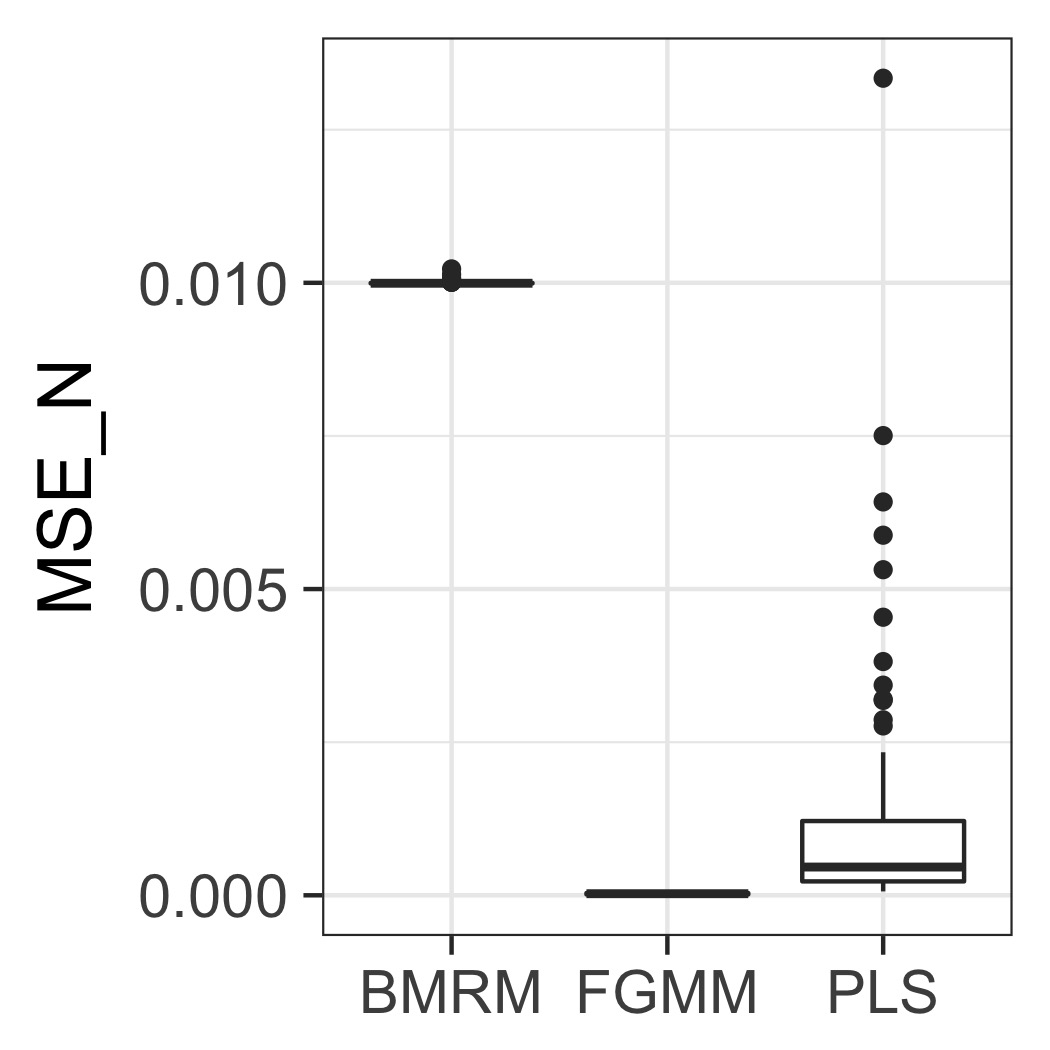

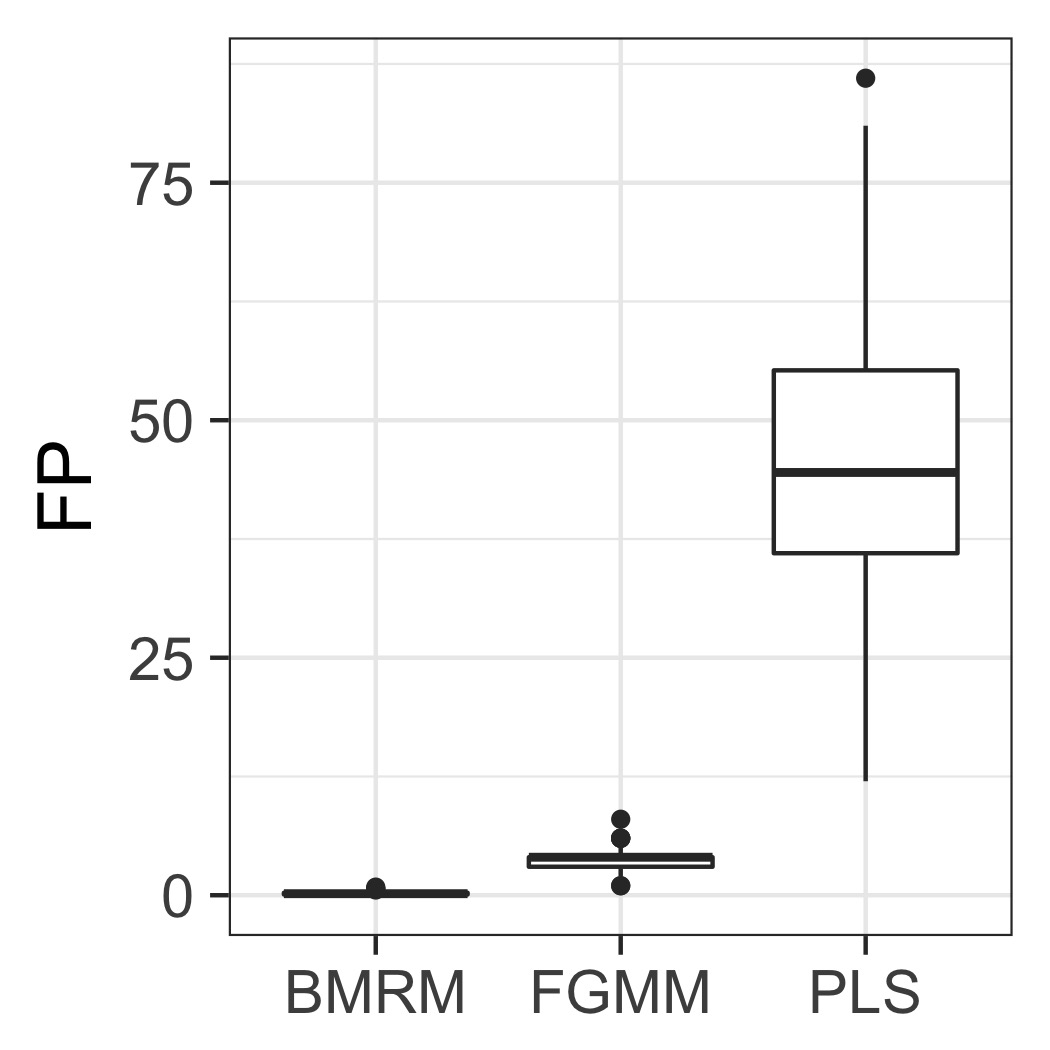

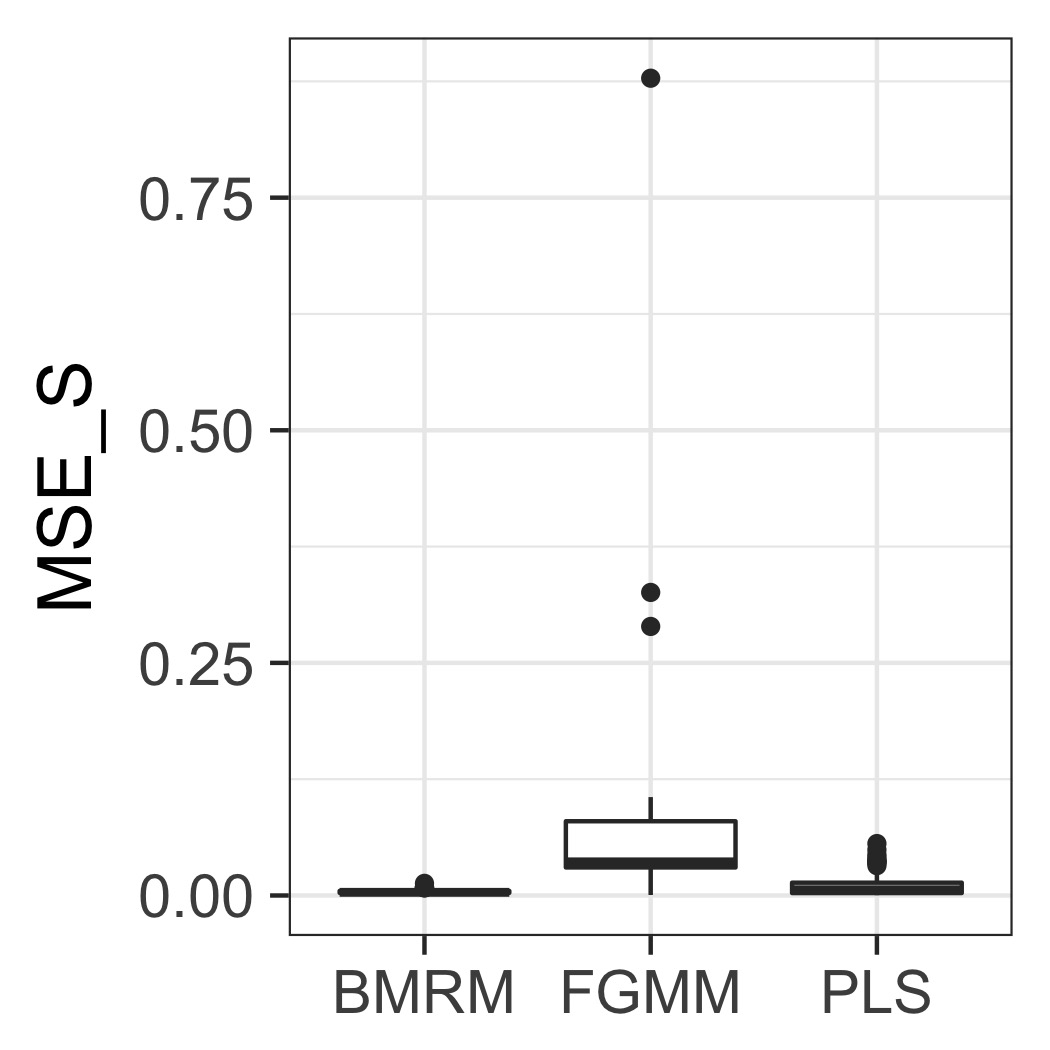

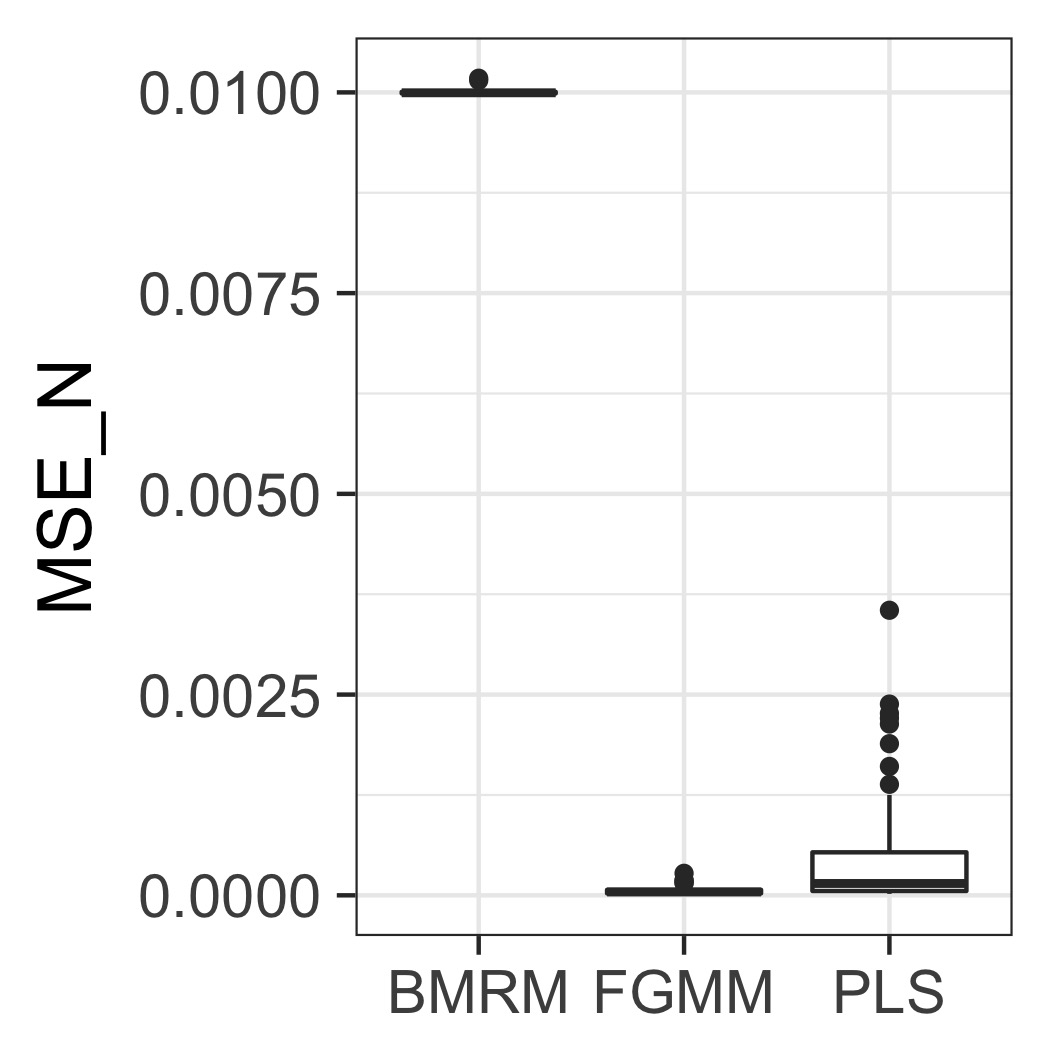

In our experiments, we used 100 replications to aggregate the results. Four performance measures are used to compare the methods. The first measure is the number of correctly identified nonzero coefficients, that is, the true positive (TP). The second measure is the number of incorrectly identified coefficients, the false positive (FP). The last two measures are mean squared errors, & , of the important and unimportant regressors respectively determined by averaging on and over 100 replications. The standard errors over 100 replications for each measure are also reported. In each run of the MCMC sampler, is initialized using penalized least squares with and is initialized by setting . FGMM results are obtained using the code on the authors’ website by setting the FGMM parameter . Our proposed method has three tuning parameters. In all our empirical work, we set

where is the number of instrumental variables.

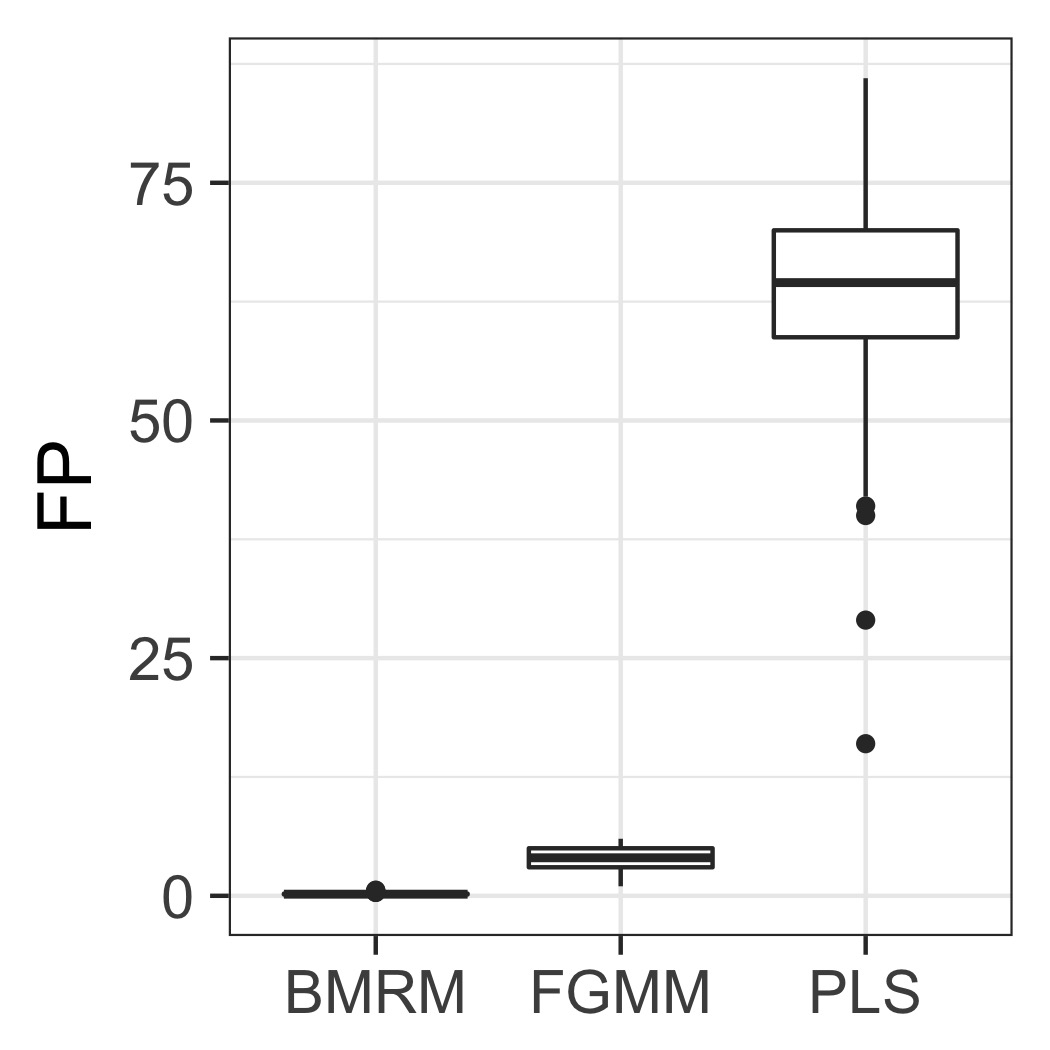

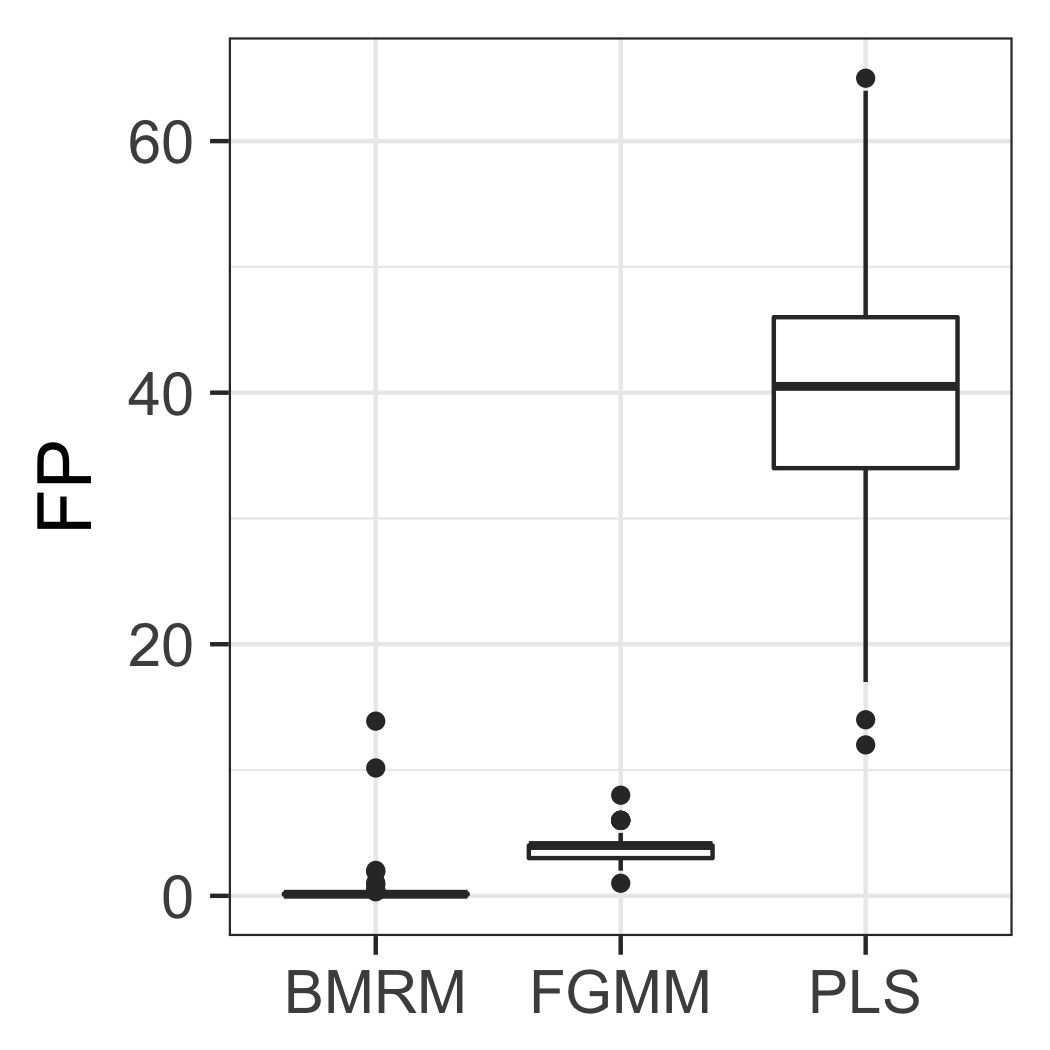

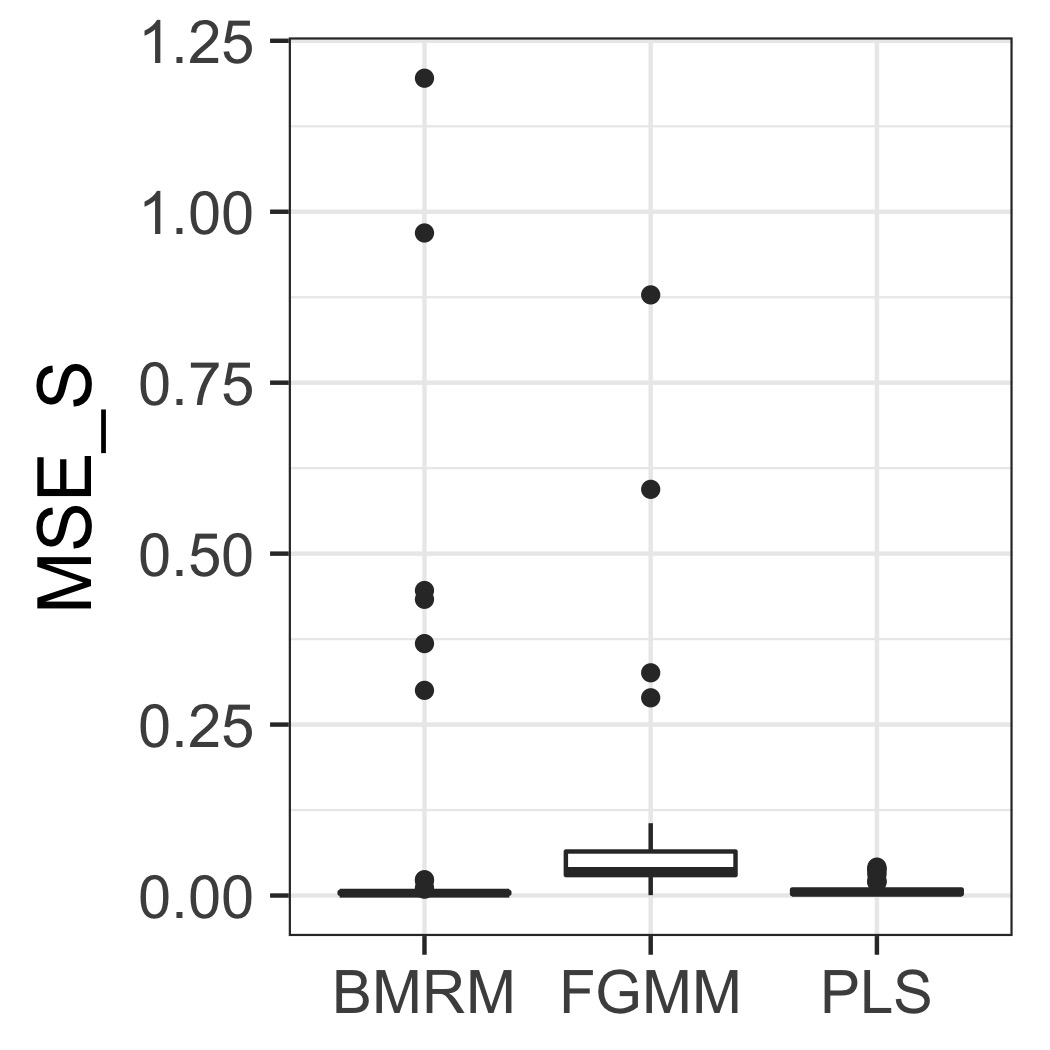

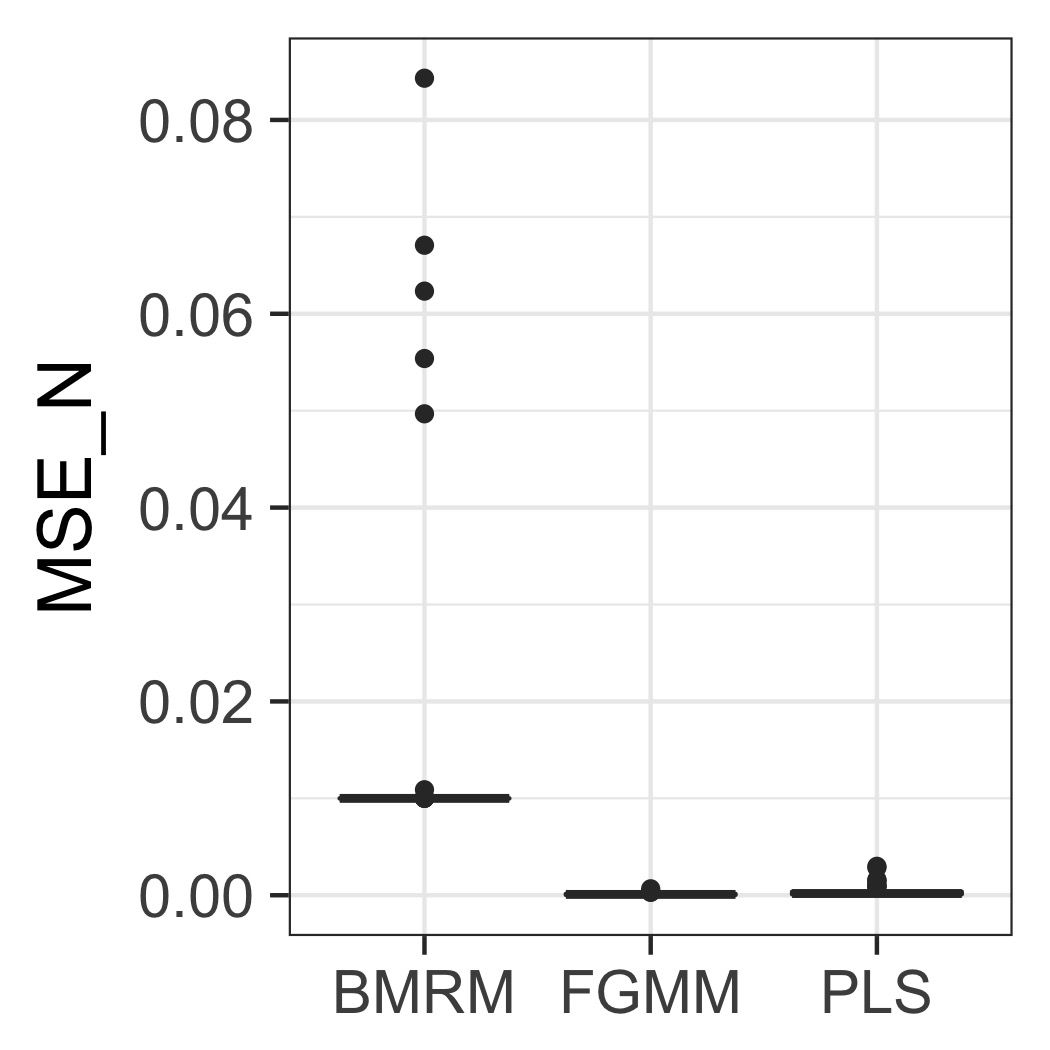

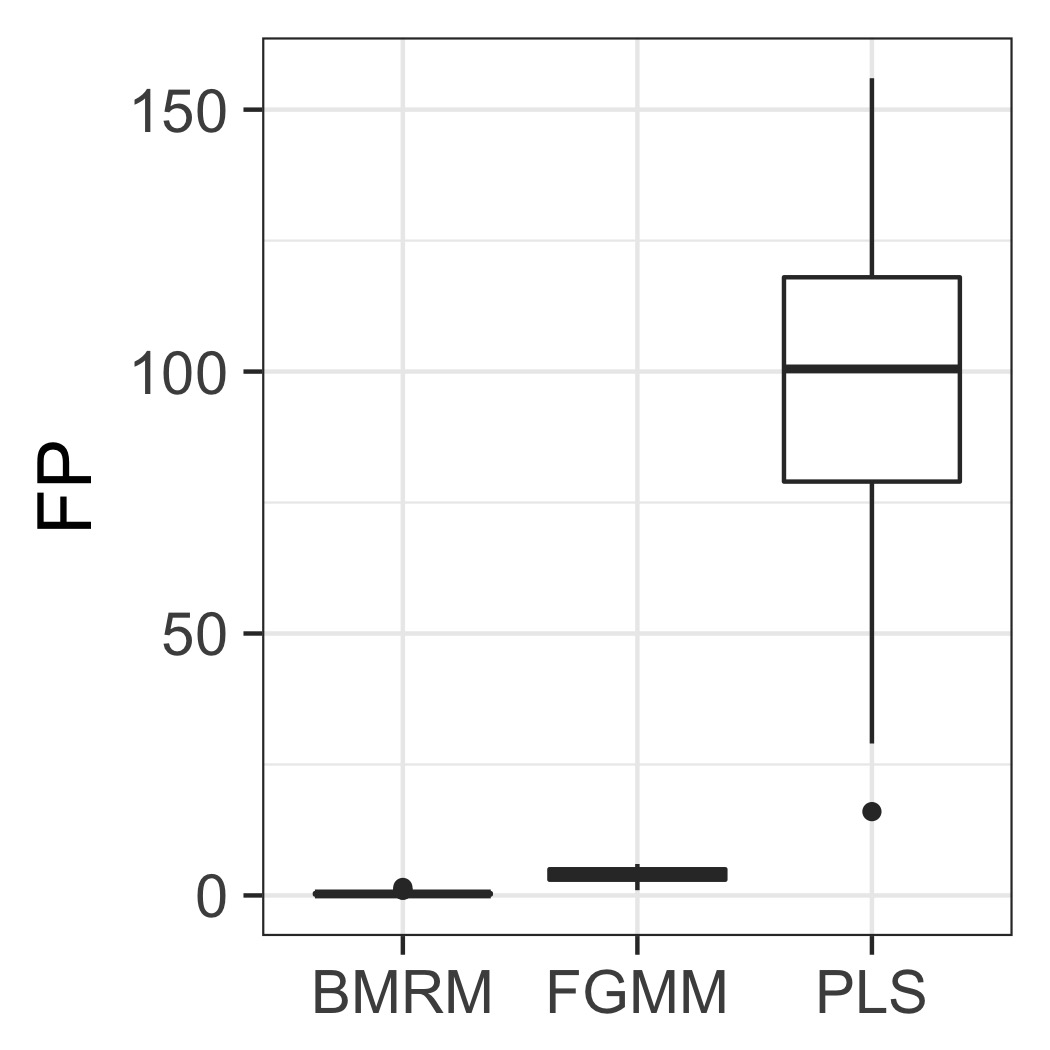

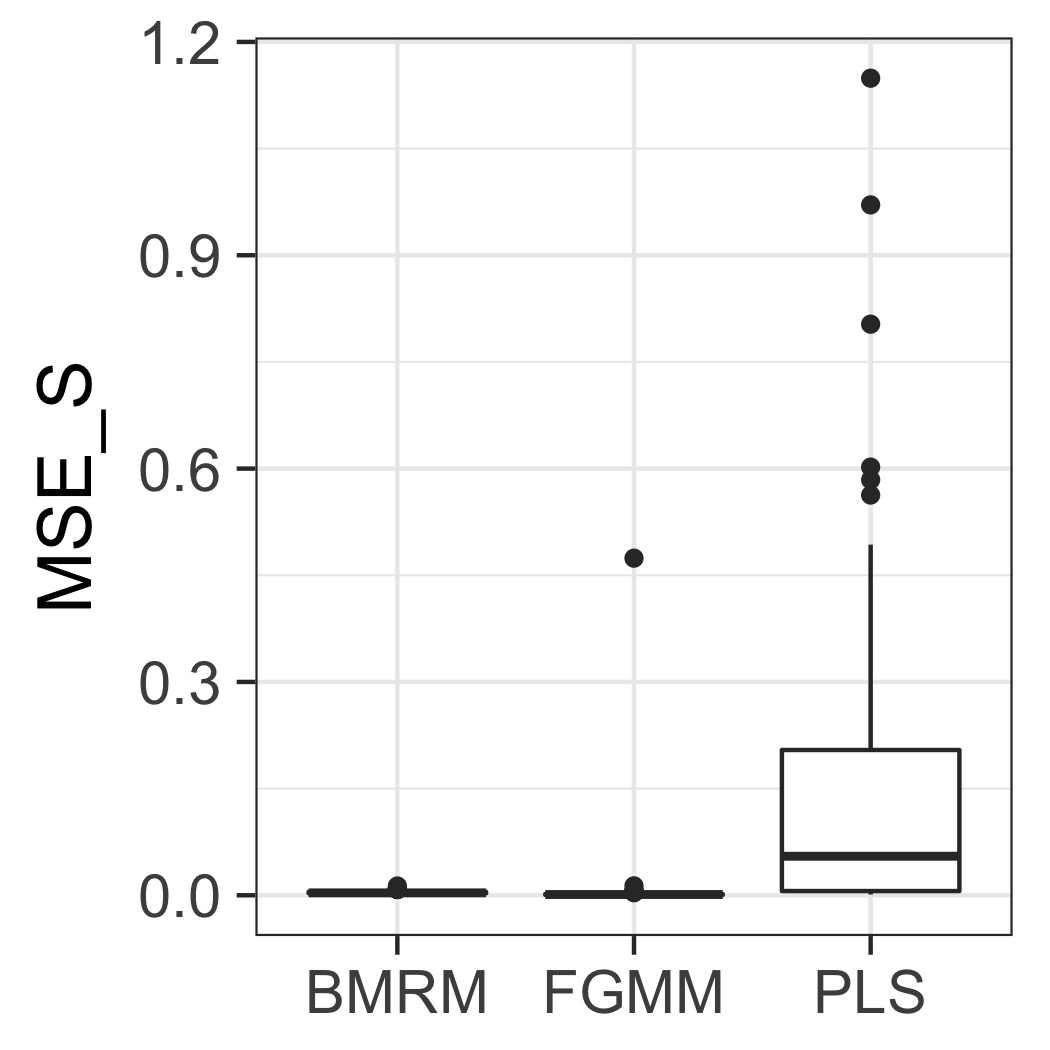

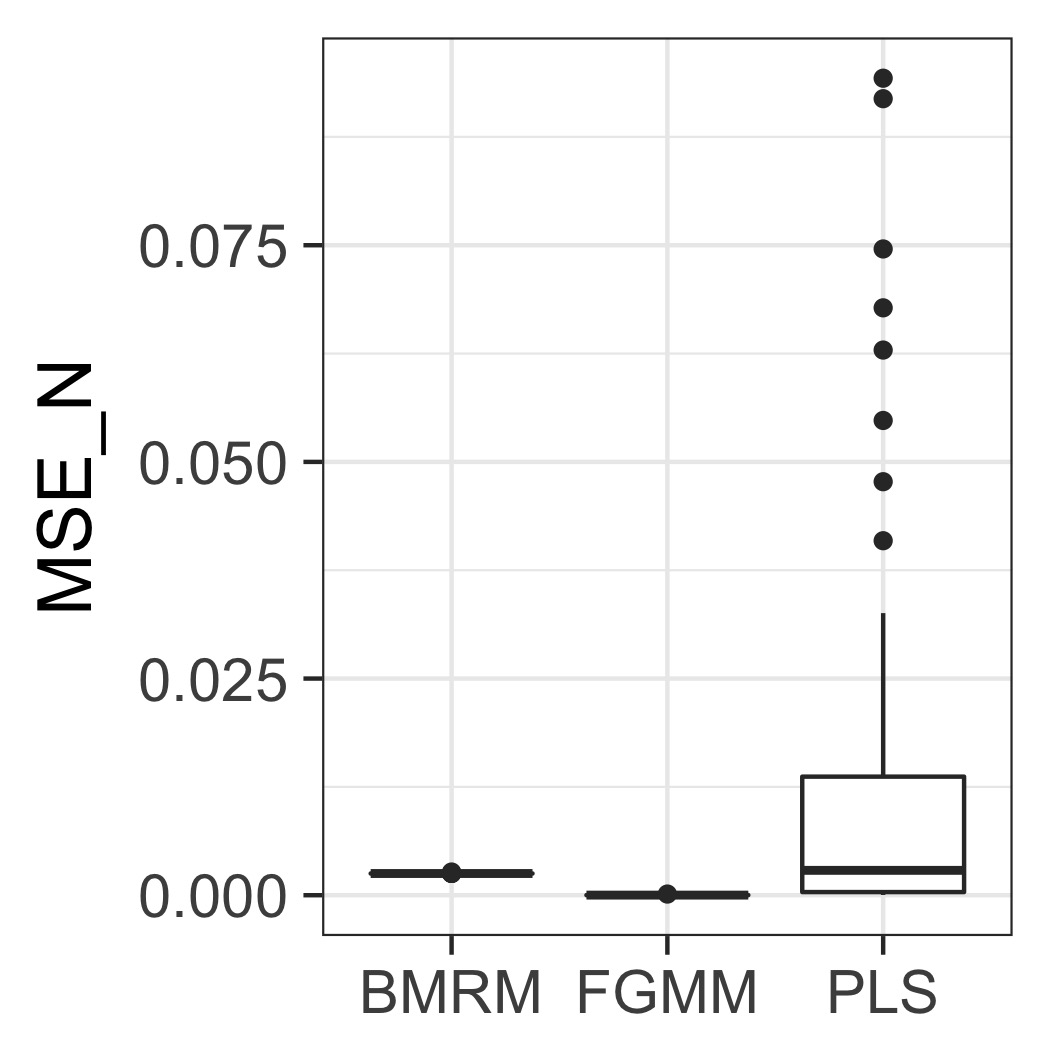

The summary of our results is presented in Tables 1 - 2 and figure 1. We compare our method, quasi-Bayesian moment restrictions model (BMRM), with FGMM and penalized least squares (PLS).

In Setup 1 and for the high signal-to-noise regime (), PLS performs well in selecting the true coefficients but, at the same time, includes a significantly large number of false positives. FGMM reduces the number of unimportant coefficients while keeping the important coefficients in the model. In contrast, BMRM not only selects all the important coefficients but also succeeds in weeding out almost all the unimportant coefficients. Our proposed method stands out in this regard. Further, the average of both FGMM and BMRM is less than that of PLS since the instrumental variables estimation is used for estimating the coefficients. The lower panel of 1 displays results for the weak signal-to-noise regime () case. Again, BMRM outperforms FGMM in selecting the important regressors and removing the unimportant regressors.

To study the effect of variable selection when the number of endogenous variables is increased, we run another set of simulations with the same data generating process as in table 1 but we increase from 10 to 50. Figure 1 display our results. It is clearly seen that BMRM outperforms FGMM and PLS.

In Setup 2 and for hSNR regime, PLS identifies the important covariates but it does so at the cost of overfitting resulting in false discoveries. In terms of TPs, although BMRM does not always outperform its competitors, it remains competitive. When signals are low (lower panel of Table 2), all methods under consideration have trouble finding the right model, highlighting the difficulty of identifying the right model with limited sample size. On the other hand, there is some promising news. In all cases, the proposed BMRM method leads to slightly lower false positive rates compared to FGMM and PLS.

| BMRM | FGMM | PLS | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| p | TP | FP | TP | FP | TP | FP | ||||||

| 100 | ||||||||||||

| 200 | ||||||||||||

| 100 | ||||||||||||

| 200 | ||||||||||||

| BMRM | FGMM | PLS | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| p | TP | FP | TP | FP | TP | FP | ||||||

| 100 | ||||||||||||

| 200 | ||||||||||||

| 100 | ||||||||||||

| 200 | ||||||||||||

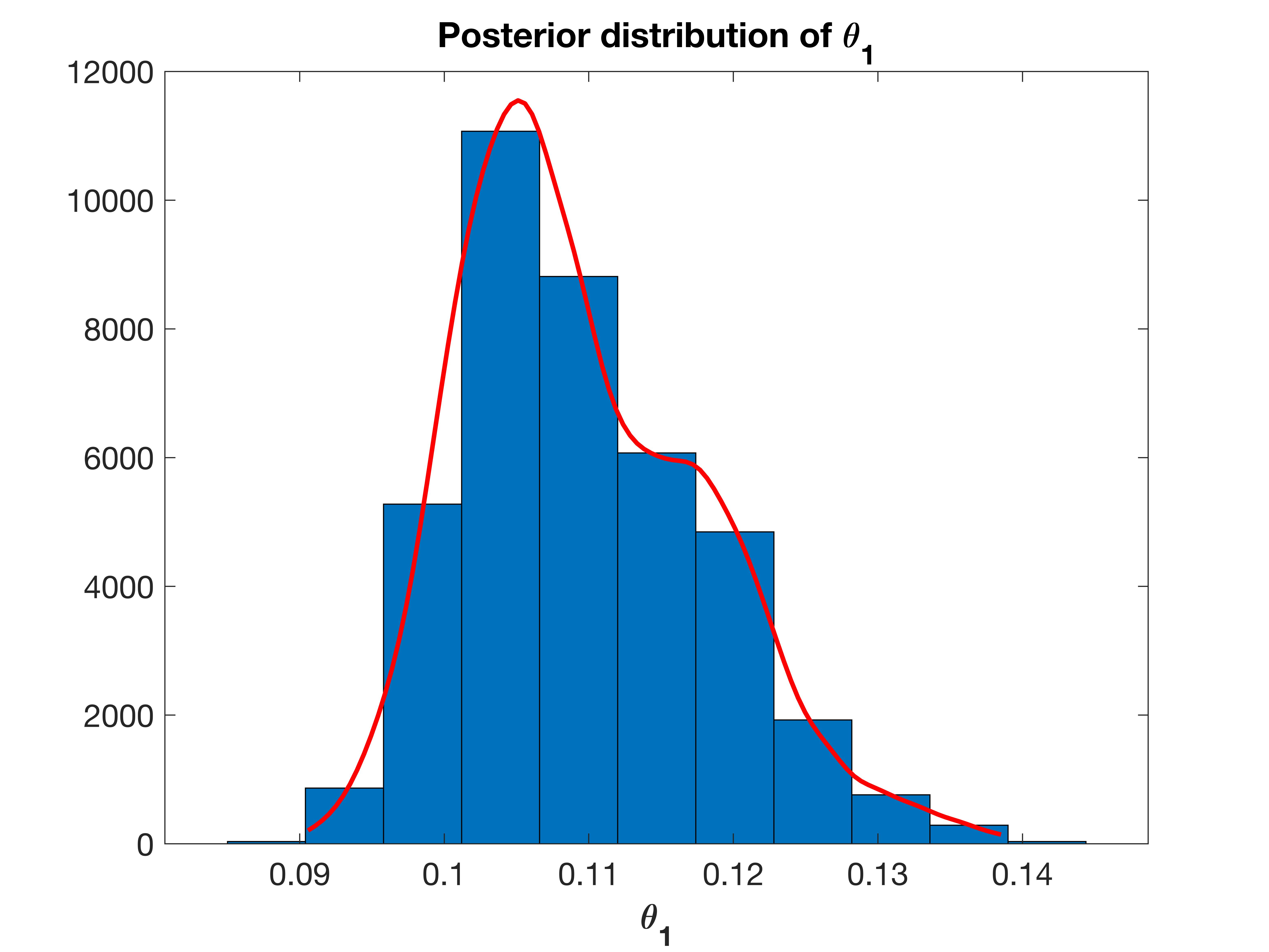

4. Endogeneity in Angrist & Krueger Data

Angrist and Keueger (1991) use the large samples available in the U.S. Census to estimate wage equations where quarter of birth is used as an instrument for educational attainment. The coefficient of interest is , which summarizes the causal impact of education on earning. We apply our method to the data that comes from the 1980 U.S. Census and consists of 329,509 males born in . Consider the model,

where is the log(wage) of individual and denotes a set of 510 variables: education, 9 year-of-birth (YOB) dummies, 50 state-of-birth (SOB) dummies, and 450 state-of-birth year-of-birth (YOBSOB) interactions. For individual , we write

As instruments, , we use 3 quarter-of-birth dummies (QOB) for the endogeneous variable education, and allow the exogeneous variables to be instruments for themselves. For individual , we write

Note that there is an irregular dependence between the variables and their corresponding instruments . For example, if the endogenous variable education is active, then all 3 instruments, corresponding to QOB, are included in the model.

BMRM selects a model with 9 covariates. The 95% credible interval of is given by .

5. Proofs

5.1. Proof of Theorem 1

Our methods of proof are similar to techniques developed in Castillo et al. (2015); Atchade (2017). For , we will write to denote the product measure on given by

where is the Dirac mass at , and is the Lebesgue measure on . First we derive a lower bound on the normalizing constant.

Proof.

By definition we have

With , we have

We recall that , so that for ,

Hence,

We have . Therefore,

and (12) also follows easily. ∎

Our proofs rely on the existence of some testing procedures that we take from A:B:2018. Let denote some sample space equipped with a reference sigma-finite measure. Let be a density on . For each , suppose that we have a jointly measurable -valued function on such that is continuously differentiable for all , and , and we denote its gradient by . Given , and given , we define

Lemma \thelemma.

With the notations above, set , . Then for any , there exists a measurable function such that

Furthermore, for all and all such that for some , we have

Proof.

See A:B:2018, Lemma 11. ∎

5.1.1. Proof of Theorem 1

We have , where

where , and

.

Since is supported by , we have

Setting , where , and , we have

| (13) |

where . By standard Guassian deviation bound, it is easy to see that for all . It follows that for all , .

Similarly, note that

We apply Lemma 5.1 with as in H1, equal to the joint density of as assumed in H1, and . In that case for , , we have

for . And . It follows that the -th component of – denoted – satisfies

for , where we recall that . Hence we can apply Lemma 5.1 with taken as and taken as . In that case we have

Let denote the test function asserted by Lemma 5.1 below, where is some arbitrary absolute constant. We can then write

| (14) |

Lemma 5.1 gives

| (15) |

for all large enough. By Lemma 5.1, we have

where . We have

and for , . It follows from the above and Fubini’s theorem that

| (16) |

We write , where . Using this and Lemma 5.1, we have

and

Therefore (16) becomes

| (17) |

where we use the fact that for , since , we have

We note that for , and since ,

provided that . It follows readily that for all large enough, and ,

| (18) |

The result follows by putting the pieces together.

References

- Angrist and Keueger (1991) Angrist, J. D. and Keueger, A. B. (1991). Does compulsory school attendance affect schooling and earnings? The Quarterly Journal of Economics 106 979–1014.

- Atchade (2017) Atchade, Y. A. (2017). On the contraction properties of some high-dimensional quasi-posterior distributions. Ann. Statist. 45 2248–2273.

- Atchadé et al. (2017) Atchadé, Y. A. et al. (2017). On the contraction properties of some high-dimensional quasi-posterior distributions. The Annals of Statistics 45 2248–2273.

- Banerjee and Ghosal (2013) Banerjee, S. and Ghosal, S. (2013). Posterior convergence rates for estimating large precision matrices using graphical models. ArXiv e-prints .

- Belloni et al. (2017) Belloni, A., Chernozhukov, V., Hansen, C. and Newey, W. (2017). Simultaneous confidence intervals for high-dimensional linear models with many endogenous variables. arXiv preprint arXiv:1712.08102 .

- Bühlmann and van de Geer (2011) Bühlmann, P. and van de Geer, S. (2011). Statistics for high-dimensional data. Springer Series in Statistics, Springer, Heidelberg. Methods, theory and applications.

- Candes et al. (2007) Candes, E., Tao, T. et al. (2007). The dantzig selector: Statistical estimation when p is much larger than n. The Annals of Statistics 35 2313–2351.

- Castillo et al. (2015) Castillo, I., Schmidt-Hieber, J. and van der Vaart, A. (2015). Bayesian linear regression with sparse priors. Ann. Statist. 43 1986–2018.

- Castillo and van der Vaart (2012) Castillo, I. and van der Vaart, A. (2012). Needles and straw in a haystack: Posterior concentration for possibly sparse sequences. Ann. Statist. 40 2069–2101.

- Chernozhukov and Hong (2003) Chernozhukov, V. and Hong, H. (2003). An mcmc approach to classical estimation. Journal of Econometrics 115 293–346.

- Fan et al. (2014) Fan, J., Han, F. and Liu, H. (2014). Challenges of big data analysis. National science review 1 293–314.

- Fan and Liao (2014) Fan, J. and Liao, Y. (2014). Endogeneity in high dimensions. Annals of statistics 42 872.

- Gautier and Tsybakov (2014) Gautier, E. and Tsybakov, A. (2014). High-dimensional instrumental variables regression and confidence sets. Tech. rep., HAL.

- George and McCulloch (1997) George, E. I. and McCulloch, R. E. (1997). Approaches for bayesian variable selection. Statistica sinica 339–373.

- Hansen (1982) Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society 1029–1054.

- Hastie et al. (2015) Hastie, T., Tibshirani, R. and Wainwright, M. (2015). Statistical Learning with Sparsity: The Lasso and Generalizations. Chapman and Hall/CRC.

- Kato et al. (2013) Kato, K. et al. (2013). Quasi-bayesian analysis of nonparametric instrumental variables models. The Annals of Statistics 41 2359–2390.

- Liao et al. (2011) Liao, Y., Jiang, W. et al. (2011). Posterior consistency of nonparametric conditional moment restricted models. The Annals of Statistics 39 3003–3031.

- Mitchell and Beauchamp (1988) Mitchell, T. J. and Beauchamp, J. J. (1988). Bayesian variable selection in linear regression. Journal of the American Statistical Association 83 1023–1032.

- Robert and Casella (2004) Robert, C. P. and Casella, G. (2004). Monte Carlo statistical methods. 2nd ed. Springer Texts in Statistics, Springer-Verlag, New York.

- Tierney (1994) Tierney, L. (1994). Markov chains for exploring posterior distributions. Ann. Statist. 22 1701–1762. With discussion and a rejoinder by the author.

- Yang et al. (2016) Yang, Y., Wainwright, M. J., Jordan, M. I. et al. (2016). On the computational complexity of high-dimensional bayesian variable selection. The Annals of Statistics 44 2497–2532.