Hierarchical adaptive sparse grids and quasi Monte Carlo for option pricing under the rough Bergomi model

Abstract

The rough Bergomi (rBergomi) model, introduced recently in [5], is a promising rough volatility model in quantitative finance. It is a parsimonious model depending on only three parameters, and yet remarkably fits with empirical implied volatility surfaces. In the absence of analytical European option pricing methods for the model, and due to the non-Markovian nature of the fractional driver, the prevalent option is to use the Monte Carlo (MC) simulation for pricing. Despite recent advances in the MC method in this context, pricing under the rBergomi model is still a time-consuming task. To overcome this issue, we have designed a novel, hierarchical approach, based on i) adaptive sparse grids quadrature (ASGQ), and ii) quasi Monte Carlo (QMC). Both techniques are coupled with a Brownian bridge construction and a Richardson extrapolation on the weak error. By uncovering the available regularity, our hierarchical methods demonstrate substantial computational gains with respect to the standard MC method, when reaching a sufficiently small relative error tolerance in the price estimates across different parameter constellations, even for very small values of the Hurst parameter. Our work opens a new research direction in this field, i.e., to investigate the performance of methods other than Monte Carlo for pricing and calibrating under the rBergomi model.

Keywords Rough volatility, Monte Carlo, Adaptive sparse grids, Quasi Monte Carlo, Brownian bridge construction, Richardson extrapolation.

1 Introduction

Modeling volatility to be stochastic, rather than deterministic as in the Black-Scholes model, enables quantitative analysts to explain certain phenomena observed in option price data, in particular the implied volatility smile. However, this family of models has a main drawback in failing to capture the true steepness of the implied volatility smile close to maturity. Jumps can be added to stock price models to overcome this undesired feature, for instance by modeling the stock price process as an exponential Lévy process. However, the addition of jumps to stock price processes remains controversial [15, 4].

Motivated by the statistical analysis of realized volatility by Gatheral, Jaisson and Rosenbaum [24] and the theoretical results on implied volatility [3, 22], rough stochastic volatility has emerged as a new paradigm in quantitative finance, overcoming the observed limitations of diffusive stochastic volatility models. In these models, the trajectories of the volatility have lower Hölder regularity than the trajectories of standard Brownian motion [5, 24]. In fact, they are based on fractional Brownian motion (fBm), which is a centered Gaussian process whose covariance structure depends on the so-called Hurst parameter, (we refer to [33, 17, 12] for more details regarding the fBm processes). In the rough volatility case, where , the fBm has negatively correlated increments and rough sample paths. Gatheral, Jaisson, and Rosenbaum [24] empirically demonstrated the advantages of such models. For instance, they showed that the log-volatility in practice has a similar behavior to fBm with the Hurst exponent at any reasonable time scale (see also [23]). These results were confirmed by Bennedsen, Lunde and Pakkanen [9], who studied over a thousand individual US equities and showed that lies in for each equity. Other works [9, 5, 24] showed additional benefits of such rough volatility models over standard stochastic volatility models, in terms of explaining crucial phenomena observed in financial markets.

The rough Bergomi (rBergomi) model, proposed by Bayer, Friz and Gatheral [5], was one of the first developed rough volatility models. This model, which depends on only three parameters, shows a remarkable fit to empirical implied volatility surfaces. The construction of the rBergomi model was performed by moving from a physical to a pricing measure and by simulating prices under that model to fit the implied volatility surface well in the case of the S&P index with few parameters. The model may be seen as a non-Markovian extension of the Bergomi variance curve model [11].

Despite the promising features of the rBergomi model, pricing and hedging under such a model still constitutes a challenging and time-consuming task due to the non-Markovian nature of the fractional driver. In fact, standard numerical pricing methods, such as PDE discretization schemes, asymptotic expansions and transform methods, although efficient in the case of diffusion, are not easily carried over to the rough setting (with the remarkable exception of the rough Heston model [18, 20, 1, 19] and its affine extensions [30, 25]). Furthermore, due to the lack of Markovianity and affine structure, conventional analytical pricing methods do not apply. To the best of our knowledge, the only prevalent method for pricing options under such models is the Monte Carlo (MC) simulation. In particular, recent advances in simulation methods for the rBergomi model and different variants of pricing methods based on MC under such a model have been proposed in [5, 6, 10, 35, 31]. For instance, in [35], the authors use a novel composition of variance reduction methods. When pricing under the rBergomi model, they achieved substantial computational gains over the standard MC method. Greater analytical understanding of option pricing and implied volatility under this model has been achieved in [32, 21, 7]. It is crucial to note that hierarchical variance reduction methods, such as multilevel Monte Carlo (MLMC), are inefficient in this context, because of the poor behavior of the strong error, that is of the order of [38].

Despite recent advances in the MC method, pricing under the rBergomi model is still computationally expensive. To overcome this issue, we design novel, fast option pricers for options whose underlyings follow the rBergomi model, based on i) adaptive sparse grids quadrature (ASGQ), and ii) quasi Monte Carlo (QMC). Both techniques are coupled with Brownian bridge construction and Richardson extrapolation. To use these two deterministic quadrature techniques (ASGQ and QMC) for our purposes, we solve two main issues that constitute the two stages of our newly designed method. In the first stage, we smoothen the integrand by using the conditional expectation tools, as was proposed in [41] in the context of Markovian stochastic volatility models, and in [8] in the context of basket options. In a second stage, we apply the deterministic quadrature method, to solve the integration problem. At this stage, we apply two hierarchical representations, before using the ASGQ or QMC method, to overcome the issue of facing a high-dimensional integrand due to the discretization scheme used for simulating the rBergomi dynamics. Given that ASGQ and QMC benefit from anisotropy, the first representation consists in applying a hierarchical path generation method, based on a Brownian bridge construction, with the aim of reducing the effective dimension. The second technique consists in applying Richardson extrapolation to reduce the bias (weak error), which, in turn, reduces the number of time steps needed in the coarsest level to achieve a certain error tolerance and consequently the maximum number of dimensions needed for the integration problem. We emphasize that we are interested in the pre-asymptotic regime (corresponding to a small number of time steps), and that the use of Richardson extrapolation is justified by conjectures 3.1 and 4.6, and our observed experimental results in that regime, which suggest, in particular, that we have convergence of order one for the weak error and that the pre-asymptotic regime is enough to achieve sufficiently accurate estimates for the option prices. Furthermore, we stress that no proper weak error analysis has been performed in the rough volatility context, which proves to be subtle, due to the absence of a Markovian structure. We also believe that we are the first to claim that both hybrid and exact schemes have a weak error of order one, which is justified at least numerically.

To the best of our knowledge, we are also the first to propose (and design) a pricing method, in the context of rough volatility models, one that is based on deterministic quadrature methods. As illustrated by our numerical experiments for different parameter constellations, our proposed methods appear to be competitive to the MC approach, which is the only prevalent method in this context. Assuming one targets price estimates with a sufficiently small relative error tolerance, our proposed methods demonstrate substantial computational gains over the standard MC method, even for very small values of . However, we do not claim that these gains will hold in the asymptotic regime, which requires a higher accuracy. Furthermore, in this work, we limit ourselves to comparing our novel proposed methods against the standard MC. A more systematic comparison with the variant of MC proposed in [35] is left for future research.

We emphasize that applying deterministic quadrature for the family of (rough) stochastic volatility models is not straightforward, but we propose an original way to overcome the high dimensionality of the integration domain, by first reducing the total dimension using Richardson extrapolation and then coupling Brownian bridge construction with ASGQ or QMC for an optimal performance of our proposed methods. Furthermore, our proposed methodology shows a robust performance with respect to the values of the Hurst parameter , as illustrated through the different numerical examples with even very low values of . We stress that the performance of hierarchical variance reduction methods such as MLMC is very sensitive to the values of , since rough volatility models are numerically tough in the sense that they admit low convergence rates for the mean square approximation (strong convergence rates) (see [38]).

While our focus is on the rBergomi model, our approach is applicable to a wide class of stochastic volatility models and in particular rough volatility models, since the approach that we propose does not use any particular property of the rBergomi model, and even the analytic smoothing step can be performed in almost similar manner for any stochastic volatility model.

This paper is structured as follows: We begin in Section 2 by introducing the pricing framework that we are considering in this study. We provide some details about the rBergomi model, option pricing under this model and the simulation schemes used to simulate asset prices following the rBergomi dynamics. We also explain how we choose the optimal simulation scheme for an optimal performance of our approach. In Section 3, we discuss the weak error in the context of the rBergomi. Then, in Section 4, we explain the different building blocks that constitute our proposed methods, which are basically ASGQ, QMC, Brownian bridge construction, and Richardson extrapolation. Finally, in Section 5 we show the results obtained through the different numerical experiments conducted across different parameter constellations for the rBergomi model. The reported results show the promising potential of our proposed methods in this context.

2 Problem setting

In this section, we introduce the pricing framework that we consider in this work. We start by giving some details on the rBergomi model proposed in [5]. We then derive the formula of the price of a European call option under the rBergomi model in Section 2.2. Finally, we explain some details about the schemes that we use to simulate the dynamics of asset prices under the rBergomi model.

2.1 The rBergomi model

We consider the rBergomi model for the price process as defined in [5], normalized to ( is the interest rate), which is defined by

| (2.1) |

where the Hurst parameter and . We refer to as the variance process, and is the forward variance curve. Here, is a certain Riemann-Liouville fBm process [34, 40], defined by

| (2.2) |

where the kernel is

By construction, is a centered, locally - Hölder continuous Gaussian process with , and a dependence structure defined by

where for and

In (2.1) and (2.2), denote two correlated standard Brownian motions with correlation , so that we can represent in terms of as

where are two independent standard Brownian motions. Therefore, the solution to (2.1), with , can be written as

| (2.3) |

2.2 Option pricing under the rBergomi model

We are interested in pricing European call options under the rBergomi model. Assuming , and using the conditioning argument on the -algebra generated by , and denoted by (an argument first used by [41] in the context of Markovian stochastic volatility models), we can show that the call price is given by

| (2.4) |

where denotes the Black-Scholes call price function, for initial spot price , strike price and volatility .

(2.2) can be obtained by using the orthogonal decomposition of into and , where

and denotes the stochastic exponential; then, by conditional log-normality, we have

We point out that the analytical smoothing, based on conditioning, performed in (2.2) enables us to uncover the available regularity, and hence get a smooth, analytic integrand inside the expectation. Therefore, applying a deterministic quadrature technique such as ASGQ or QMC becomes an adequate option for computing the call price, as we will investigate later. A similar conditioning was used in [35] but for variance reduction purposes only.

2.3 Simulation of the rBergomi model

One of the numerical challenges encountered in the simulation of rBergomi dynamics is the computation of and in (2.2), mainly because of the singularity of the Volterra kernel at the diagonal . In fact, one needs to jointly simulate two Gaussian processes , resulting in and along a given time grid . In the literature, there are essentially two suggested ways to achieve this:

-

i)

Covariance based approach (exact simulation) [5, 7]: together form a ()-dimensional Gaussian random vector with a computable covariance matrix, and therefore one can use Cholesky decomposition of the covariance matrix to produce exact samples of from -dimensional Gaussian random vector as an input. This method is exact but slow. The simulation requires flops. Note that the offline cost is flops.

-

ii)

The hybrid scheme of [10]: This scheme uses a different approach, which is essentially based on Euler discretization, and approximates the kernel function in (2.2) by a power function near zero and by a step function elsewhere, which results in an approximation combining Wiener integrals of the power function and a Riemann sum (see (2.5) and [10] for more details). This approximation is inexact in the sense that samples produced here do not exactly have the distribution of . However, they are much more accurate than the samples produced from a simple Euler discretization, and much faster than method . As in method , in this case, we need a -dimensional Gaussian random input vector to produce one sample of .

2.3.1 On the choice of the simulation scheme in our approach

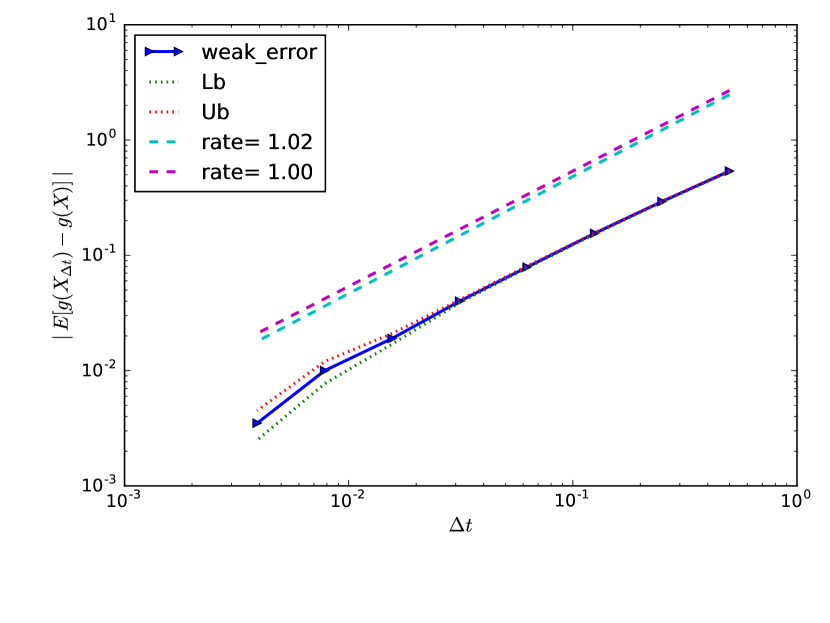

The choice of the simulation scheme in our approach was based on the observed behavior of the weak rates. Through our numerical experiments (see Table 5.1 for the tested examples), we observe that, although the hybrid and exact schemes seem to converge with a weak error of order , the pre-asymptotic behavior of the weak rate is different for both schemes (we provide a short discussion of the weak error in Section 3). As an illustration, from Figure 2.1 for Set parameter in Table 5.1, the hybrid scheme has a consistent convergence behavior in the sense that it behaves in an asymptotic manner, basically right from the beginning, whereas the exact scheme does not. On the other hand, the constant seems to be considerably smaller for the exact scheme. These two features make the hybrid scheme the best choice to work within our context, since our approach is based on hierarchical representations involving the use of Richardson extrapolation (see Section 4.4).

2.3.2 The hybrid scheme

Let us denote the number of time steps by . As motivated in Section 2.3.1, in this work we use the hybrid scheme, which, on an equidistant grid , is given by the following,

| (2.5) |

which results for in (2.6)

| (2.6) |

where

| (2.7) |

The sum in (2.6) requires the most computational effort in the simulation. Given that (2.6) can be seen as discrete convolution (see [10]), we employ the fast Fourier transform to evaluate it, which results in floating point operations.

We note that the variates are generated by sampling i.i.d draws from a -dimensional Gaussian distribution and computing a discrete convolution. For the case of , we denote these pairs of Gaussian random vectors from now on by , and we refer to [10] for more details.

3 Weak error discussion

To the best of our knowledge, no proper weak error analysis has been done in the rough volatility context, which proves to be subtle in the absence of a Markovian structure. However, we try in this Section to shortly discuss it in the context of the rBergomi model.

In this work, we are interested in approximating , where is some smooth function and is the asset price under the rBergomi dynamics such that , where is standard Brownian motion and is the fractional Brownian motion as given by (2.2). Then we can express the approximation of using the hybrid and exact schemes as the following

where is the approximation of as given by (2.5) and is the approximation of using time steps. In the following, to simplify notation, let , and . Then, the use of Richardson extrapolation in our methodology presented in Section 4 is mainly justified by the conjecture 3.1.

Conjecture 3.1.

If we denote by and the weak errors produced by the hybrid and Cholesky scheme respectively, then we have

We motivate Conjecture 3.1 by writing

| (3.1) |

From the construction of the Cholesky scheme, we expect that the weak error is purely the discretization error, that is

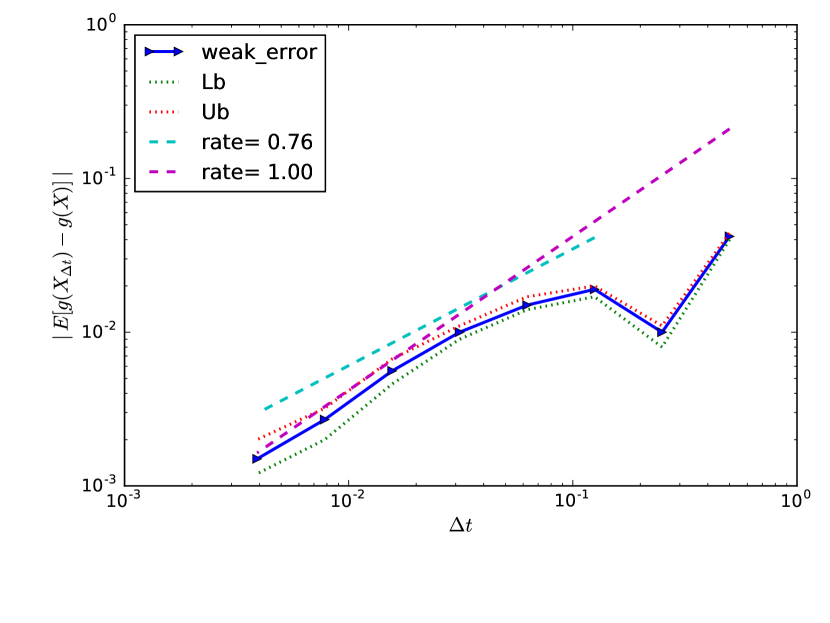

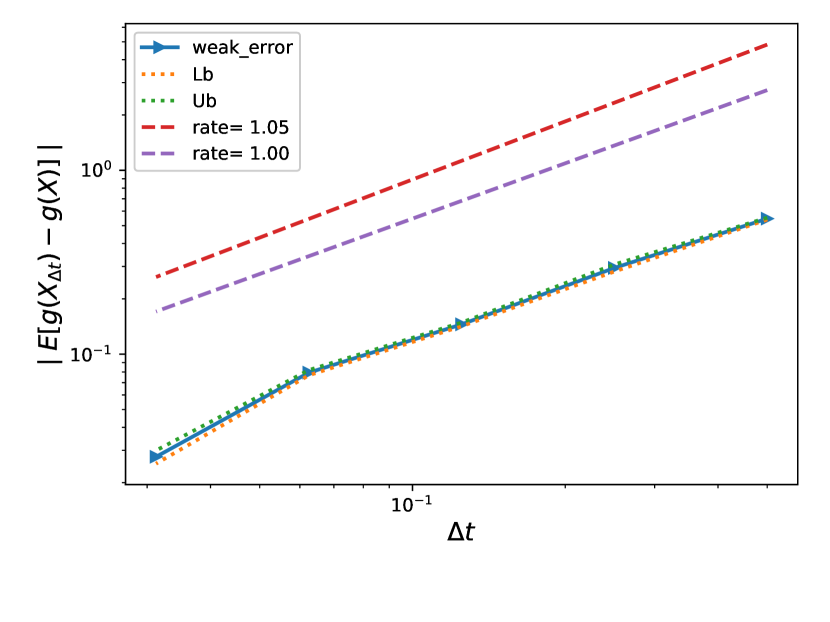

as it was observed by our numerical experiments (for illustration see Figure 1(b) for the case of Set in Table 5.1). The second term in the right-hand side of (3) is basically related to approximating the integral (2.2) by (2.6). From our numerical experiments, it seems that this term is at least of order and that its rate of convergence is independent of (for illustration see Figure 1(a) for the case of Set in Table 5.1).

4 Details of our hierarchical methods

We recall that our goal is to compute the expectation in (2.2), and we remind from Section 2.3.2 that we need -dimensional Gaussian inputs, for the used hybrid scheme ( is the number of time steps in the time grid). We can rewrite (2.2) as

| (4.1) |

where maps independent standard Gaussian random inputs, formed by , to the parameters fed to the Black-Scholes call price function, (defined in (2.2)), and is the multivariate Gaussian density, given by

Therefore, the initial integration problem that we are solving lives in -dimensional space, which becomes very large as the number of time steps , used in the hybrid scheme, increases.

Our approach of approximating the expectation in (4) is based on hierarchical deterministic quadratures, namely i) an ASGQ using the same construction as in [27] and ii) a randomized QMC based on lattice rules. In Section 4.1 we describe the ASGQ method in our context, and in Section 4.2 we provide details on the implemented QMC method. To make an effective use of either the ASGQ or the QMC method, we apply two techniques to overcome the issue of facing a high dimensional integrand due to the discretization scheme used for simulating the rBergomi dynamics. The first consists in applying a hierarchical path generation method, based on a Brownian bridge construction, with the aim of reducing the effective dimension, as described in Section 4.3. The second technique consists in applying Richardson extrapolation to reduce the bias, resulting in reducing the maximum number of dimensions needed for the integration problem. Details about the Richardson extrapolation are provided in Section 4.4.

If we denote by the total error of approximating the expectation in (2.2), using the ASGQ estimator, (defined by (4.4)), then we obtain a natural error decomposition

| (4.2) |

where is the quadrature error, is the bias, is a user-selected tolerance for the ASGQ method, and is the biased price computed with time steps, as given by (4).

On the other hand, the total error of approximating the expectation in (2.2) using the randomized QMC or MC estimator, can be bounded by

| (4.3) |

where is the statistical error111The statistical error estimate of MC or randomized QMC is , where is the number of samples and for confidence interval., is the number of samples used for the MC or the randomized QMC method.

Remark 4.1.

4.1 Adaptive sparse grids quadrature (ASGQ)

We assume that we want to approximate the expected value of an analytic function using a tensorization of quadrature formulas over .

To introduce simplified notations, we start with the one-dimensional case. Let us denote by a non-negative integer, referred to as a “stochastic discretization level”, and by a strictly increasing function with and , that we call “level-to-nodes function”. At level , we consider a set of distinct quadrature points in , , and a set of quadrature weights, . We also let be the set of real-valued continuous functions over . We then define the quadrature operator as

In our case, we have in (4) a multi-variate integration problem with, , , and , in the previous notations. Furthermore, since we are dealing with Gaussian densities, using Gauss-Hermite quadrature points is the appropriate choice.

We define for any multi-index

where the -th quadrature operator is understood to act only on the -th variable of . Practically, we obtain the value of by using the grid , with cardinality , and computing

where and are products of weights of the univariate quadrature rules. To simplify notation, hereafter, we replace by .

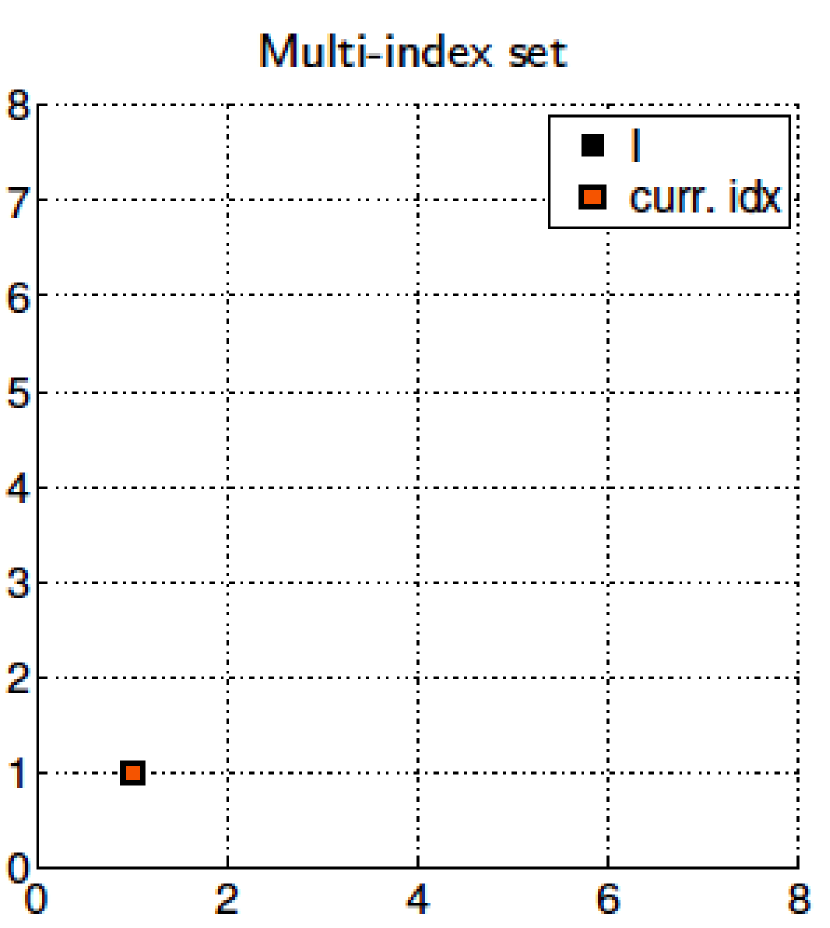

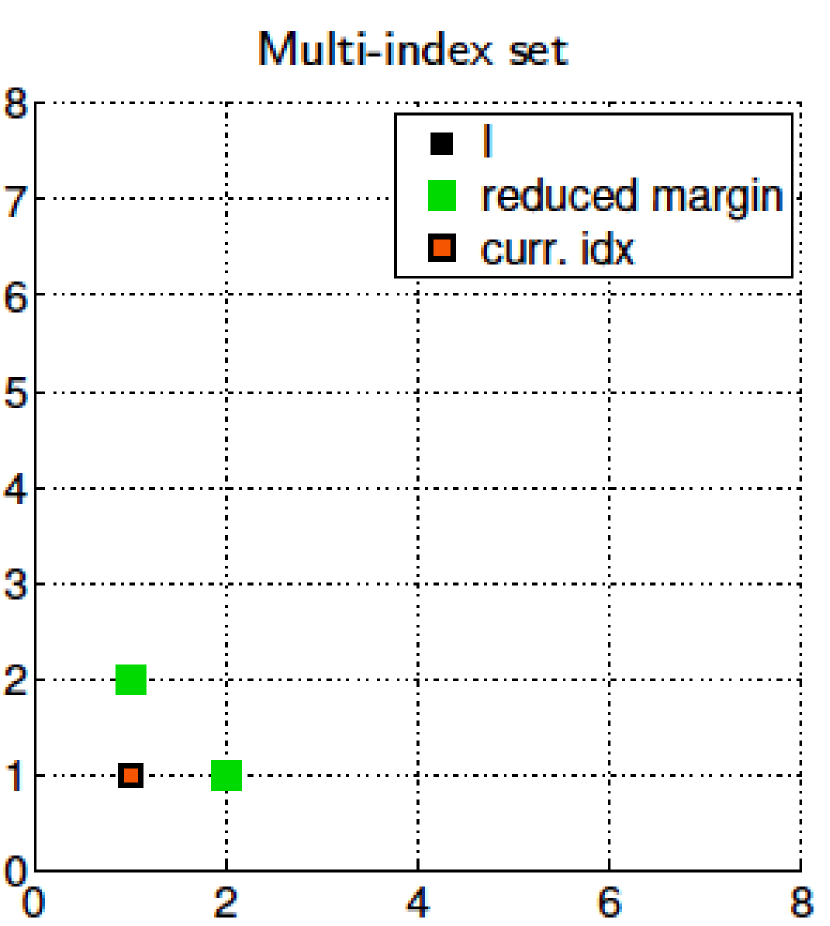

A direct approximation is not an appropriate option, due to the well-known “curse of dimensionality”. We use a hierarchical ASGQ222More details about sparse grids can be found in [13]. strategy, specifically using the same construction as in [27], and which uses stochastic discretizations and a classic sparsification approach to obtain an effective approximation scheme for .

To be concrete, in our setting, we are left with a -dimensional Gaussian random input, which is chosen independently, resulting in numerical parameters for ASGQ, which we use as the basis of the multi-index construction. For a multi-index , we denote by the result of approximating (4) with a number of quadrature points in the -th dimension equal to . We further define the set of differences as follows: for a single index , let

where denotes the th -dimensional unit vector. Then, is defined as

For instance, when , then

Given the definition of by (4), we have the telescoping property

The ASGQ estimator used for approximating (4), and using a set of multi-indices is given by

| (4.4) |

The quadrature error in this case is given by

| (4.5) |

We define the work contribution, , to be the computational cost required to add to , and the error contribution, , to be a measure of how much the quadrature error, defined in (4.5), would decrease once has been added to , that is

| (4.6) | ||||

| (4.7) |

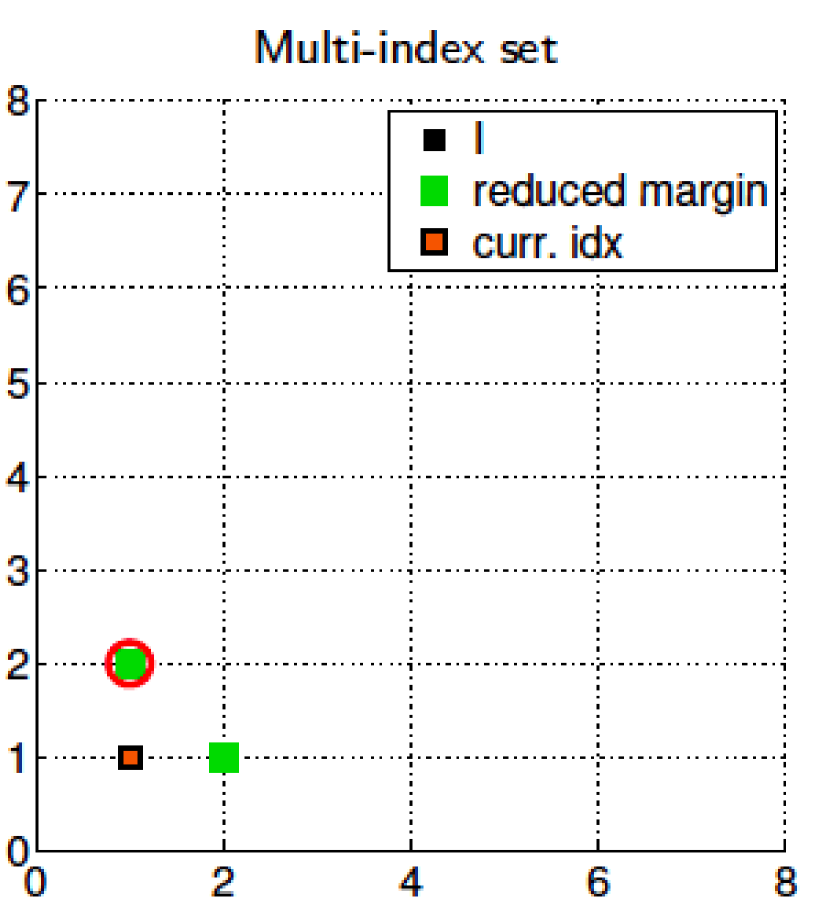

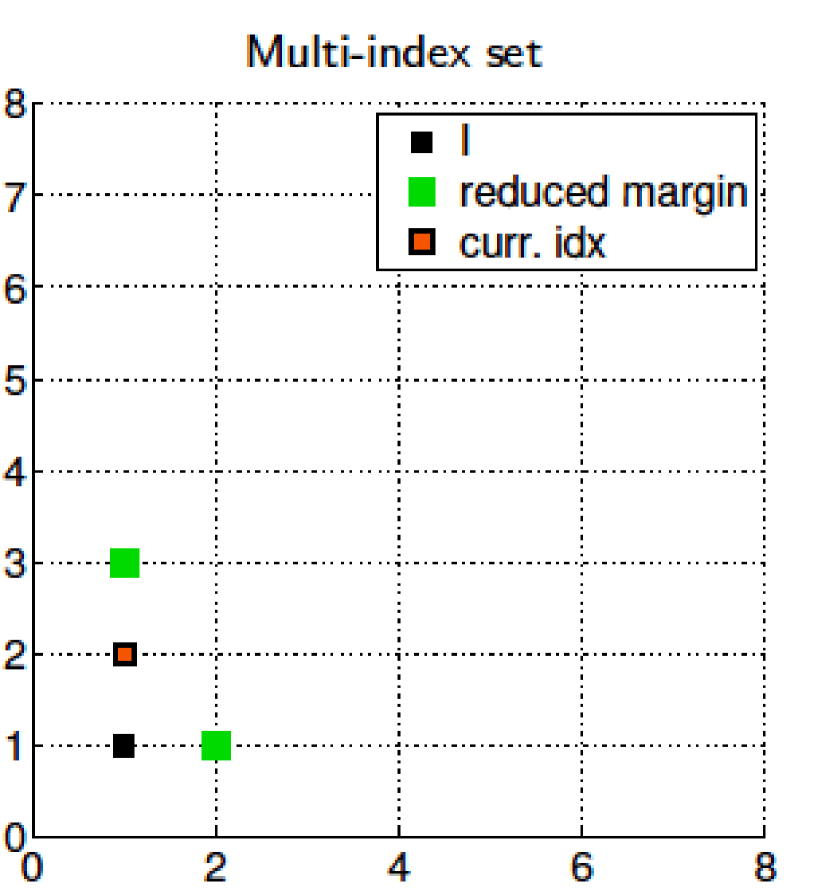

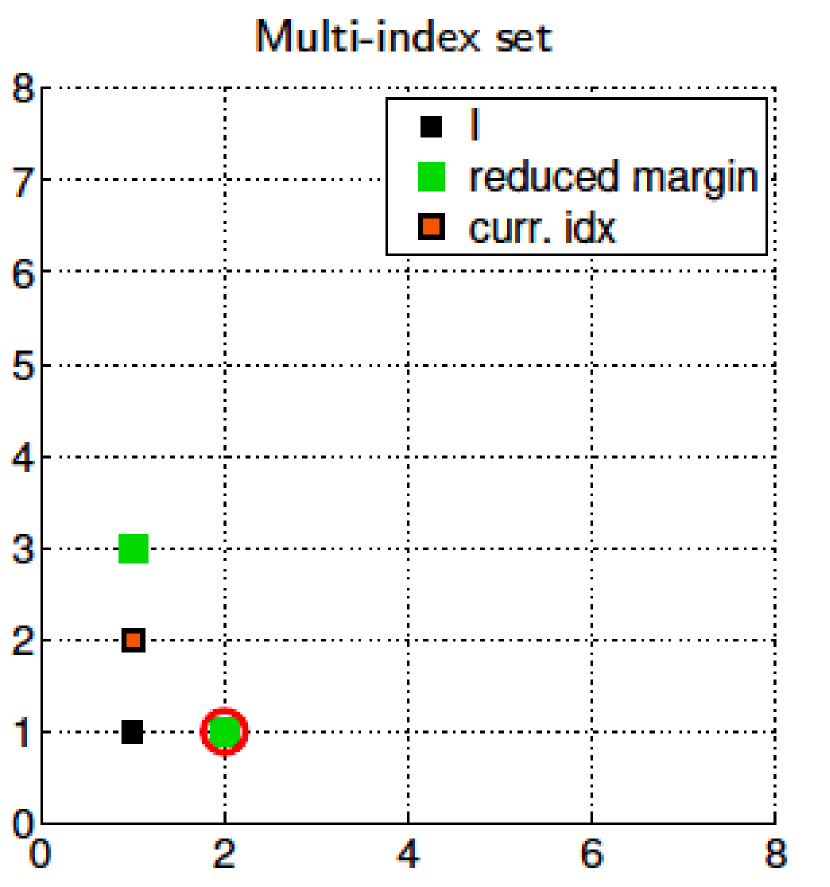

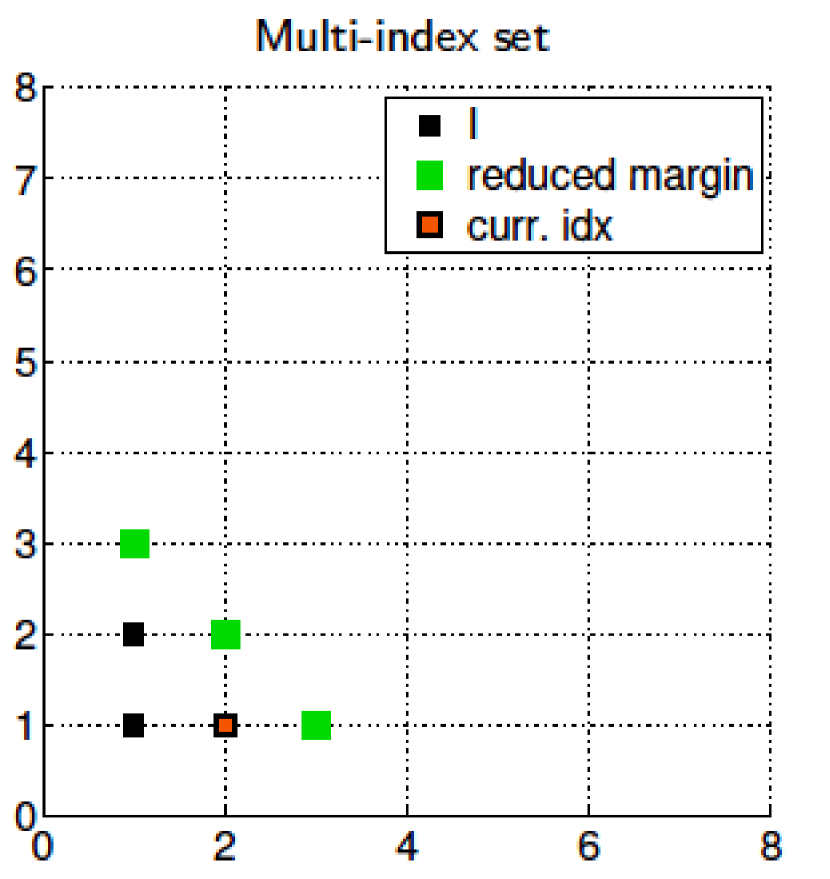

The construction of the optimal is done by profit thresholding (see Figure 4.1 for illustration), that is, for a certain threshold value , and a profit of a hierarchical surplus defined by

| (4.8) |

the optimal index set for our ASGQ is given by .

Remark 4.2.

The choice of the hierarchy of quadrature points, , is flexible in the ASGQ algorithm and can be fixed by the user, depending on the convergence properties of the problem at hand. For instance, for the sake of reproducibility, in our numerical experiments, we used a linear hierarchy: , for results of parameter set in Table 5.1. For the remaining parameter sets in Table 5.1, we used a geometric hierarchy: .

Remark 4.3.

As emphasized in [27], one important requirement to achieve the optimal performance of the ASGQ is to check the error convergence, defined by (4.6), of first and mixed difference operators. We checked this requirement in all our numerical experiments, and for illustration, we show in Figures 4.2 and 4.3 the error convergence of first and second order differences for the case of parameter set in Table 5.1. These plots show that: i) decreases exponentially fast with respect to , and ii) has a product structure since we observe a faster error decay for second differences, compared to corresponding first difference operators.

Remark 4.4.

The analiticity assumption, stated in the beginning of Section 4.1, is crucial for the optimal performance of our proposed method. In fact, although we face the issue of the “curse of dimensionality” when increasing , the analiticity of implies a spectral convergence for sparse grids quadrature.

4.2 Quasi Monte Carlo (QMC)

A second type of deterministic quadrature that we test in this work is the randomized QMC method. Specifically, we use the lattice rules family of QMC [42, 16, 39]. The main input for the lattice rule is one integer vector with components ( is the dimension of the integration problem).

In fact, given an integer vector known as the generating vector, a (rank-) lattice rule with points takes the form

| (4.9) |

The quality of the lattice rule depends on the choice of the generating vector. Due to the modulo operation, it is sufficient to consider the values from up to . Furthermore, we restrict the values to those relatively prime to , to ensure that every one-dimensional projection of the points yields distinct values. Thus, we write , with . For practical purposes, we choose to be a power of . The total number of possible choices for the generating vector is then .

To get an unbiased approximation of the integral, we use a randomly shifted lattice rule, which also allows us to obtain a practical error estimate in the same way as the MC method. It works as follows. We generate independent random shifts for from the uniform distribution of . For the same fixed lattice generating vector , we compute the different shifted lattice rule approximations and denote them by for .We then take the average

| (4.10) |

as our final approximation to the integral and the total number of samples of the randomized QMC method is .

We note that, since we are dealing with Gaussian randomness and with integrals in infinite support, we use the inverse of the standard normal cumulative distribution function as a pre-transformation to map the problem to , and then use the randomized QMC. Furthermore, in our numerical test, we use a pre-made point generator using latticeseq_b2.py in python from https://people.cs.kuleuven.be/~dirk.nuyens/qmc-generators/.

Remark 4.5.

We emphasize that we opt for one of the most simple rules (very easy to specify and implement) for QMC, that is the lattice rule, which, thanks to the hierarchical representations that we implemented (Richardson extrapolation and Brownian bridge construction) appears to give already a very good performance. Furthermore, we believe that using more sophisticated rules such as lattice sequences or interlaced Sobol sequences may have a similar or even better performance.

4.3 Brownian bridge construction

In the literature on ASGQ and QMC, several hierarchical path generation methods (PGMs) have been proposed to reduce the effective dimension. Among these techniques, we mention Brownian bridge construction [36, 37, 14], principal component analysis (PCA) [2] and linear transformation (LT) [29].

In our context, the Brownian motion on a time discretization can be constructed either sequentially using a standard random walk construction, or hierarchically using other PGMs, as listed above. For our purposes, to make an effective use of ASGQ or QMC methods, which benefit from anisotropy, we use the Brownian bridge construction that produces dimensions that are not equally important, contrary to a random walk procedure for which all the dimensions of the stochastic space have equal importance. In fact, Brownian bridge uses the first several coordinates of the low-discrepancy points to determine the general shape of the Brownian path, and the last few coordinates influence only the fine detail of the path. Consequently, this representation reduces the effective dimension of the problem, resulting in an acceleration of the ASGQ and QMC methods by reducing the computational cost.

Let us denote as the grid of time steps. Then the Brownian bridge construction [26] consists of the following: given a past value and a future value , the value (with ) can be generated according to

where .

4.4 Richardson extrapolation

Another representation that we couple with the ASGQ and QMC methods is the Richardson extrapolation [43]. In fact, applying level (level of extrapolation) of the Richardson extrapolation dramatically reduces the bias, and as a consequence, reduces the number of time steps needed in the coarsest level to achieve a certain error tolerance. As a consequence, the Richardson extrapolation directly reduces the total dimension of the integration problem for achieving some error tolerance.

Conjecture 4.6.

Applying (4.11) with discretization step , we obtain

implying

For higher levels of extrapolations, we use the following: Let us denote by the grid sizes (where is the coarsest grid size), by the level of the Richardson extrapolation, and by the approximation of by terms up to level (leading to a weak error of order ), then we have the following recursion

Remark 4.7.

We emphasize that, throughout our work, we are interested in the pre-asymptotic regime (a small number of time steps), and the use of Richardson extrapolation is justified by conjectures 3.1 and 4.6, and our observed experimental results in that regime (see Section 5.1), which suggest a convergence of order one for the weak error.

5 Numerical experiments

In this section, we show the results obtained through the different numerical experiments, conducted across different parameter constellations for the rBergomi model. Details about these examples are presented in Table 5.1. The first set is the one closest to the empirical findings [9, 24], which suggest that . The choice of parameter values of and is justified by [5], where it is shown that these values are remarkably consistent with the SPX market on th February . For the remaining three sets in Table 5.1, we want to test the potential of our method for a very rough case, that is , for three different scenarios of moneyness, . In fact, hierarchical variance reduction methods, such as MLMC, are inefficient in this context because of the poor behavior of the strong error, which is of the order of [38]. We emphasize that we checked the robustness of our method for other parameter sets, but for illustrative purposes, we only show results for the parameters sets presented in Table 5.1. For all our numerical experiments, we consider a number of time steps , and all reported errors are relative errors, normalized by the reference solutions provided in Table 5.1.

| Parameters | Reference solution |

|---|---|

| Set : | |

| Set : | |

| Set : | |

| Set : |

5.1 Weak error

We start our numerical experiments by accurately estimating the weak error (bias) discussed in Section 3, for the different sets of parameters in Table 5.1, with and without the Richardson extrapolation. For illustrative purposes, we only show the weak errors related to set in Table 5.1 (see Figure 5.1). We note that we observed a similar behavior for the other parameter sets, with slightly worse rates for some cases. We emphasize that the reported weak rates correspond to the pre-asymptotic regime that we are interested in. We are not interested in estimating the rates specifically but rather obtaining a sufficiently precise estimate of the weak error (bias), , for different numbers of time steps . For a fixed discretization, the corresponding estimated biased solution will be set as a reference solution to the ASGQ method in order to estimate the quadrature error .

5.2 Comparing the errors and computational time for MC, QMC and ASGQ

In this section, we conduct a comparison between MC, QMC and ASGQ, in terms of errors and computational time. We show tables and plots reporting the different relative errors involved in the MC and QMC methods (bias and statistical error estimates), and in ASGQ (bias and quadrature error estimates). While fixing a sufficiently small relative error tolerance in the price estimates, we compare the computational time needed for all methods to meet the desired error tolerance. We note that, in all cases, the actual work (runtime) is obtained using an Intel(R) Xeon(R) CPU E- architecture.

For the numerical experiments we conducted for each parameter set, we follow these steps to achieve the reported results:

-

i)

For a fixed number of time steps, , we compute an accurate estimate, using a large number of samples, , of the biased MC solution, . This step also provides us with an estimate of the bias error, , defined by (4.2).

-

ii)

The estimated biased solution, , is used as a reference solution to the ASGQ method to compute the quadrature error, , defined by (4.5).

-

iii)

In order to compare the different methods, the number of samples, and , are chosen so that the statistical errors of randomized QMC, , and MC, , satisfy

(5.1) where is the bias as defined in (4.2) and is the total error.

We show the summary of our numerical findings in Table 5.2, which highlights the computational gains achieved by ASGQ and QMC over the MC method to meet a certain error tolerance, which we set approximately to . We note that the results are reported using the best configuration with Richardson extrapolation for each method. More detailed results for each case of parameter set, as in Table 5.1, are provided in Sections 5.2.1, 5.2.2, 5.2.3 and 5.2.4.

| Parameter set | Total relative error | CPU time ratio | CPU time ratio |

|---|---|---|---|

| Set | |||

| Set | |||

| Set | |||

| Set |

5.2.1 Case of parameters in Set 1 in Table 5.1

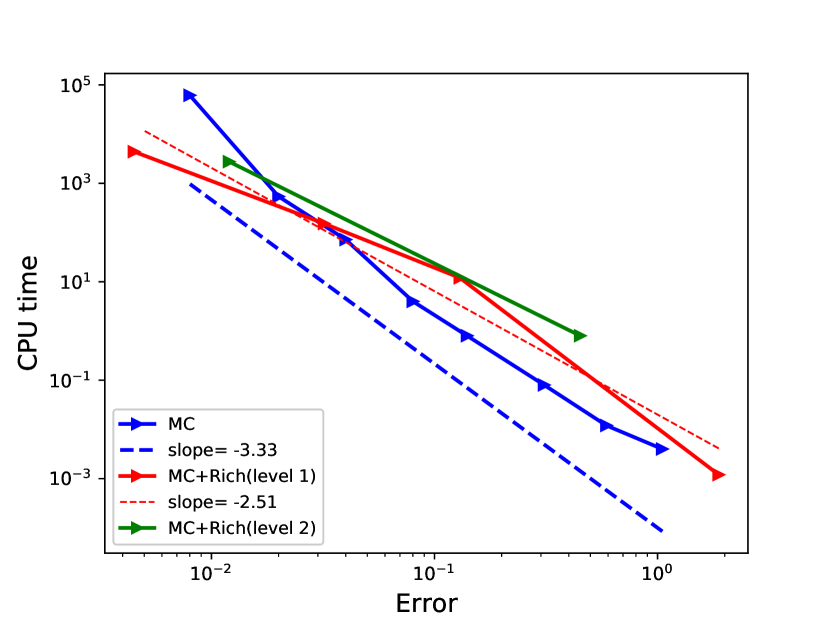

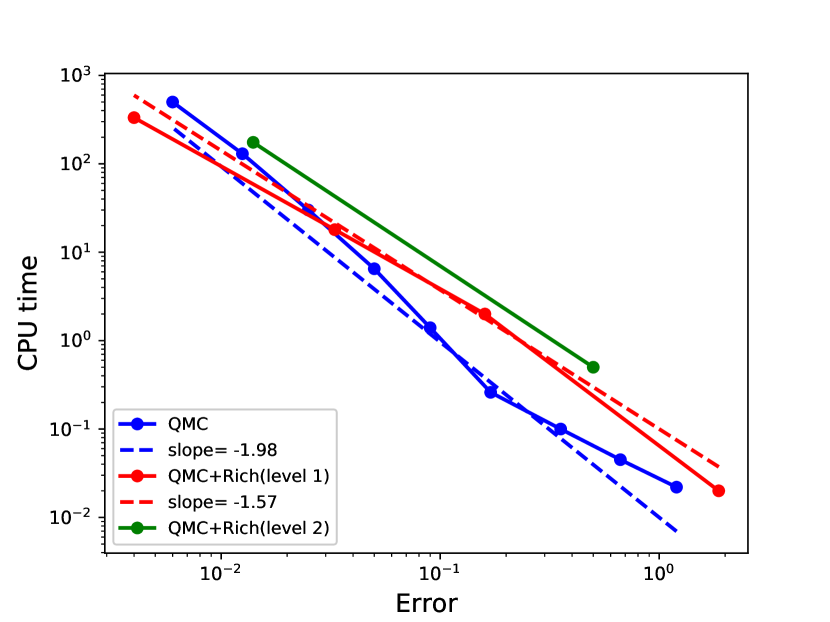

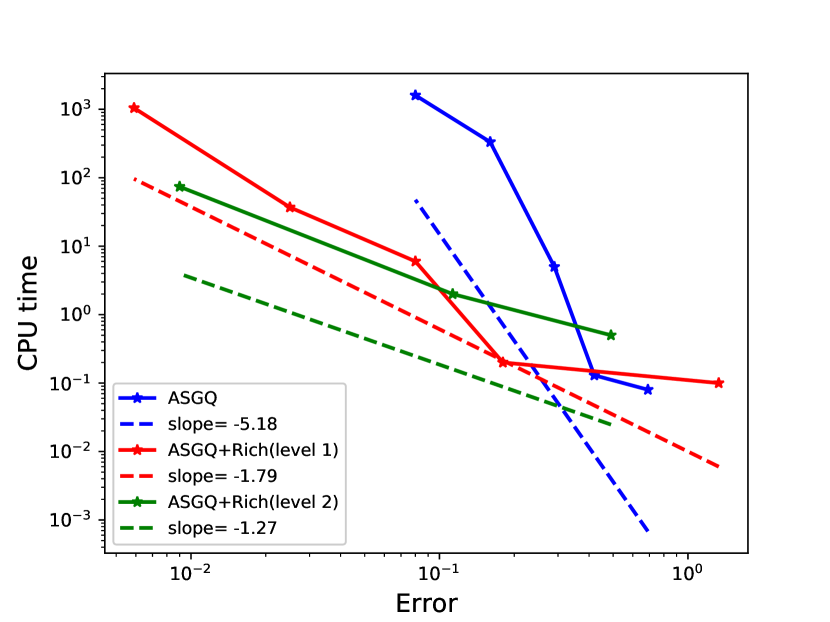

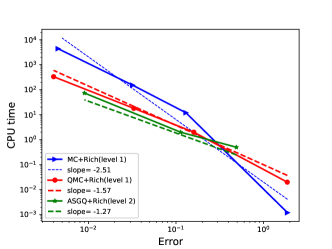

In this section, we conduct our numerical experiments for three different scenarios: i) without Richardson extrapolation, ii) with (level ) Richardson extrapolation, and iii) with (level ) Richardson extrapolation. Figure 5.2 shows a comparison of the numerical complexity for each method under the three different scenarios. From this Figure, we conclude that, to achieve a relative error of , the level of the Richardson extrapolation is the optimal configuration for both the MC and the randomized QMC methods, and that the level of the Richardson extrapolation is the optimal configuration for the ASGQ method.

We compare these optimal configurations for each method in Figure 5.3, and we show that both ASGQ and QMC outperform MC, in terms of numerical complexity. In particular, to achieve a total relative error of , ASGQ coupled with the level of the Richardson extrapolation requires approximately of the work of MC coupled with the level of the Richardson extrapolation, and QMC coupled with the level of the Richardson extrapolation requires approximately of the work of MC coupled with the level of the Richardson extrapolation. We show more detailed outputs for the methods that are compared in Figure 5.3 in Appendix A.1.

5.2.2 Case of parameters in Set 2 in Table 5.1

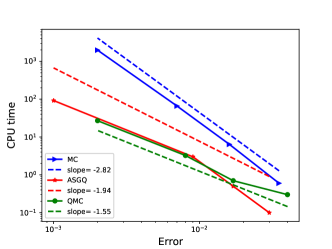

In this section, we only conduct our numerical experiments for the case without the Richardson extrapolation, since the results show that we meet a small enough relative error tolerance without the need to apply the Richardson extrapolation. We compare the different methods in Figure 5.4, and we determine that both ASGQ and QMC outperform MC, in terms of numerical complexity. In particular, to achieve a total relative error of approximately , ASGQ requires approximately of the work of MC, and that QMC requires approximately of the work of MC. We show more detailed outputs for the methods that are compared in Figure 5.4 in Appendix A.2.

5.2.3 Case of parameters in Set 3 in Table 5.1

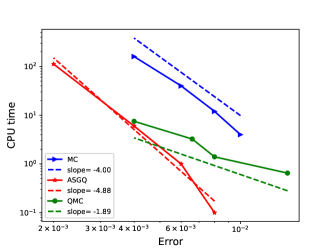

In this section, we only conduct our numerical experiments for the case without the Richardson extrapolation, since the results show that we meet a small enough relative error tolerance without the need to apply the Richardson extrapolation. We compare the different methods in Figure 5.5, and we determine that both ASGQ and QMC outperform MC, in terms of numerical complexity. In particular, to achieve a total relative error of approximately , ASGQ requires approximately of the work of MC, and that QMC requires approximately of the work of MC. We show more detailed outputs for the methods that are compared in Figure 5.5 in Appendix A.3.

5.2.4 Case of parameters in Set 4 in Table 5.1

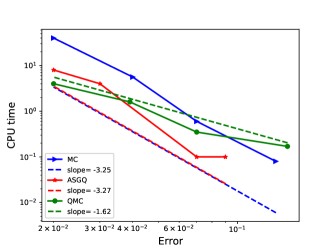

In this section, we only conduct our numerical experiments for the case the without Richardson extrapolation. We compare the different methods in Figure 5.6, and we determine that both ASGQ and QMC outperform MC, in terms of numerical complexity. In particular, to achieve a total relative error of approximately , ASGQ requires approximately of the work of MC, and QMC requires approximately of the work of MC. We show more detailed outputs for the methods that are compared in Figure 5.6 in Appendix A.4. Similar to the case of set parameters, illustrated in section 5.2.1, we believe that the Richardson extrapolation will improve the performance of the ASGQ and QMC methods. We should also point out that, since we are in the out of the money regime in this case, a fairer comparison of the methods may be done after coupling them with an importance sampling method, so that more points are sampled in the right region of the payoff function.

6 Conclusions and future work

In this work, we propose novel, fast option pricers, for options whose underlyings follow the rBergomi model, as in [5]. The new methods are based on hierarchical deterministic quadrature methods: i) ASGQ using the same construction as in [27], and ii) the QMC method. Both techniques are coupled with a Brownian bridge construction and the Richardson extrapolation on the weak error.

Given that the only prevalent option, in this context, is to use different variants of the MC method, which is computationally expensive, our main contribution is to propose a competitive alternative to the MC approach that is based on deterministic quadrature methods. We believe that we are the first to propose (and design) a pricing method, in the context of rough volatility models, that is based on deterministic quadrature, and that our approach opens a new research direction to investigate the performance of other methods besides MC, for pricing and calibrating under rough volatility models.

Assuming one targets price estimates with a sufficiently small relative error tolerance, our proposed methods demonstrate substantial computational gains over the standard MC method, when pricing under the rBergomi model, even for very small values of the Hurst parameter. We show these gains through our numerical experiments for different parameter constellations. We clarify that we do not claim that these gains will hold in the asymptotic regime, i.e., for higher accuracy requirements. Furthermore, the use of the Richardson extrapolation is justified in the pre-asymptotic regime, for which our observed experimental results suggest a convergence of order one for the weak error. We emphasize that, to the best of our knowledge, no proper weak error analysis has been done in the rough volatility context, but we claim that both hybrid and exact schemes have a weak error of order one, which is justified, at least numerically. While our focus is on the rBergomi model, our approach is applicable to a wide class of stochastic volatility models, in particular rough volatility models.

In this work, we limit ourselves to compare our novel proposed method against the standard MC. A more systematic comparison against the variant of MC proposed in [35] can be carried out, but this remains for a future study. Another future research direction is to provide a reliable method for controlling the quadrature error for ASGQ which is, to the best of our knowledge, still an open research problem. This is even more challenging in our context, especially for low values of . We emphasize that the main aim of this work is to illustrate the high potential of the deterministic quadrature, when coupled with hierarchical representations, for pricing options under the rBergomi model. Lastly, we note that accelerating our novel approach can be achieved by using better versions of the ASGQ and QMC methods or an alternative weak approximation of rough volatility models, based on a Donsker type approximation, as recently suggested in [28]. The ASGQ and QMC methods proposed in this work can also be applied in the context of this scheme; in this case, we only have an -dimensional input rather than a ()-dimensional input for the integration problem (4), with being the number of time steps. Further analysis, in particular regarding the Richardson approximation, will be done in future research.

Acknowledgments C. Bayer gratefully acknowledges support from the German Research Foundation (DFG), via the Cluster of Excellence MATH+ (project AA4-2) and the individual grant BA5484/1. This work was supported by the KAUST Office of Sponsored Research (OSR) under Award No. URF/1/2584-01-01 and the Alexander von Humboldt Foundation. C. Ben Hammouda and R. Tempone are members of the KAUST SRI Center for Uncertainty Quantification in Computational Science and Engineering. The authors would like to thank Joakim Beck, Eric Joseph Hall and Erik von Schwerin for their helpful and constructive comments. The authors are also very grateful to the anonymous referees for their valuable comments and suggestions that greatly contributed to shape the final version of the paper.

References Cited

- [1] Eduardo Abi Jaber. Lifting the Heston model. Quantitative Finance, 19(12):1995–2013, 2019.

- [2] Peter A Acworth, Mark Broadie, and Paul Glasserman. A comparison of some Monte Carlo and quasi Monte Carlo techniques for option pricing. In Monte Carlo and Quasi-Monte Carlo Methods 1996, pages 1–18. Springer, 1998.

- [3] Elisa Alòs, Jorge A León, and Josep Vives. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and Stochastics, 11(4):571–589, 2007.

- [4] Pierre Bajgrowicz, Olivier Scaillet, and Adrien Treccani. Jumps in high-frequency data: Spurious detections, dynamics, and news. Management Science, 62(8):2198–2217, 2015.

- [5] Christian Bayer, Peter Friz, and Jim Gatheral. Pricing under rough volatility. Quantitative Finance, 16(6):887–904, 2016.

- [6] Christian Bayer, Peter K Friz, Paul Gassiat, Joerg Martin, and Benjamin Stemper. A regularity structure for rough volatility. arXiv preprint arXiv:1710.07481, 2017.

- [7] Christian Bayer, Peter K Friz, Archil Gulisashvili, Blanka Horvath, and Benjamin Stemper. Short-time near-the-money skew in rough fractional volatility models. Quantitative Finance, pages 1–20, 2018.

- [8] Christian Bayer, Markus Siebenmorgen, and Rául Tempone. Smoothing the payoff for efficient computation of basket option pricing. Quantitative Finance, 18(3):491–505, 2018.

- [9] Mikkel Bennedsen, Asger Lunde, and Mikko S Pakkanen. Decoupling the short-and long-term behavior of stochastic volatility. arXiv preprint arXiv:1610.00332, 2016.

- [10] Mikkel Bennedsen, Asger Lunde, and Mikko S Pakkanen. Hybrid scheme for Brownian semistationary processes. Finance and Stochastics, 21(4):931–965, 2017.

- [11] Lorenzo Bergomi. Smile dynamics II. Risk, 18:67––73, 2005.

- [12] F. Biagini, Y. Hu, B. Øksendal, and T. Zhang. Stochastic calculus for fractional Brownian motion and applications. Probability and its Applications. Springer London, 2008.

- [13] Hans-Joachim Bungartz and Michael Griebel. Sparse grids. Acta numerica, 13:147–269, 2004.

- [14] Russel E Caflisch, William J Morokoff, and Art B Owen. Valuation of mortgage backed securities using Brownian bridges to reduce effective dimension. 1997.

- [15] Kim Christensen, Roel CA Oomen, and Mark Podolskij. Fact or friction: Jumps at ultra high frequency. Journal of Financial Economics, 114(3):576–599, 2014.

- [16] Ronald Cools and Dirk Nuyens. A Belgian view on lattice rules. In Monte Carlo and Quasi-Monte Carlo Methods 2006, pages 3–21. Springer, 2008.

- [17] Laure Coutin. An introduction to (stochastic) calculus with respect to fractional Brownian motion. In Séminaire de Probabilités XL, pages 3–65. Springer, 2007.

- [18] Omar El Euch, Jim Gatheral, and Mathieu Rosenbaum. Roughening Heston. Available at SSRN 3116887, 2018.

- [19] Omar El Euch and Mathieu Rosenbaum. The characteristic function of rough Heston models. Mathematical Finance, 29(1):3–38, 2019.

- [20] Omar El Euch, Mathieu Rosenbaum, et al. Perfect hedging in rough Heston models. The Annals of Applied Probability, 28(6):3813–3856, 2018.

- [21] Martin Forde and Hongzhong Zhang. Asymptotics for rough stochastic volatility models. SIAM Journal on Financial Mathematics, 8(1):114–145, 2017.

- [22] Masaaki Fukasawa. Asymptotic analysis for stochastic volatility: martingale expansion. Finance and Stochastics, 15(4):635–654, 2011.

- [23] Jim Gatheral, Thibault Jaisson, Andrew Lesniewski, and Mathieu Rosenbaum. Volatility is rough, part 2: Pricing. Workshop on Stochastic and Quantitative Finance, Imperial College London, London, 2014.

- [24] Jim Gatheral, Thibault Jaisson, and Mathieu Rosenbaum. Volatility is rough. Quantitative Finance, 18(6):933–949, 2018.

- [25] Jim Gatheral and Martin Keller-Ressel. Affine forward variance models. Finance and Stochastics, pages 1–33.

- [26] Paul Glasserman. Monte Carlo methods in financial engineering. Springer, New York, 2004.

- [27] Abdul-Lateef Haji-Ali, Fabio Nobile, Lorenzo Tamellini, and Rául Tempone. Multi-index stochastic collocation for random PDEs. Computer Methods in Applied Mechanics and Engineering, 306:95–122, 2016.

- [28] Blanka Horvath, Antoine Jacquier, and Aitor Muguruza. Functional central limit theorems for rough volatility. Available at SSRN 3078743, 2017.

- [29] Junichi Imai and Ken Seng Tan. Minimizing effective dimension using linear transformation. In Monte Carlo and Quasi-Monte Carlo Methods 2002, pages 275–292. Springer, 2004.

- [30] Eduardo Abi Jaber, Martin Larsson, Sergio Pulido, et al. Affine Volterra processes. The Annals of Applied Probability, 29(5):3155–3200, 2019.

- [31] Antoine Jacquier, Claude Martini, and Aitor Muguruza. On VIX futures in the rough Bergomi model. Quantitative Finance, 18(1):45–61, 2018.

- [32] Antoine Jacquier, Mikko S Pakkanen, and Henry Stone. Pathwise large deviations for the rough Bergomi model. Journal of Applied Probability, 55(4):1078–1092, 2018.

- [33] Benoit B Mandelbrot and John W Van Ness. Fractional Brownian motions, fractional noises and applications. SIAM review, 10(4):422–437, 1968.

- [34] Domenico Marinucci and Peter M Robinson. Alternative forms of fractional Brownian motion. Journal of statistical planning and inference, 80(1-2):111–122, 1999.

- [35] Ryan McCrickerd and Mikko S Pakkanen. Turbocharging Monte Carlo pricing for the rough Bergomi model. Quantitative Finance, pages 1–10, 2018.

- [36] William J Morokoff and Russel E Caflisch. Quasi-random sequences and their discrepancies. SIAM Journal on Scientific Computing, 15(6):1251–1279, 1994.

- [37] Bradley Moskowitz and Russel E Caflisch. Smoothness and dimension reduction in quasi-Monte Carlo methods. Mathematical and Computer Modelling, 23(8):37–54, 1996.

- [38] Andreas Neuenkirch and Taras Shalaiko. The order barrier for strong approximation of rough volatility models. arXiv preprint arXiv:1606.03854, 2016.

- [39] Dirk Nuyens. The construction of good lattice rules and polynomial lattice rules., 2014.

- [40] Jean Picard. Representation formulae for the fractional Brownian motion. In Séminaire de Probabilités XLIII, pages 3–70. Springer, 2011.

- [41] Marc Romano and Nizar Touzi. Contingent claims and market completeness in a stochastic volatility model. Mathematical Finance, 7(4):399–412, 1997.

- [42] Ian H Sloan. Lattice methods for multiple integration. Journal of Computational and Applied Mathematics, 12:131–143, 1985.

- [43] Denis Talay and Luciano Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stochastic analysis and applications, 8(4):483–509, 1990.

Appendix A Appendix

A.1 Case of set parameters in table 5.1

| Method | Steps | |||

|---|---|---|---|---|

| QMC + level of Richardson extrapolation | ||||

| M(# QMC samples) | ||||

| MC + level of Richardson extrapolation | ||||

| M(# MC samples) |

| Method | Steps | ||||

|---|---|---|---|---|---|

| QMC + level of Richardson extrapolation | |||||

| MC + level of Richardson extrapolation |

| Method | Steps | |||

|---|---|---|---|---|

| ASGQ + level of Richardson extrapolation () | ||||

| ASGQ + level of Richardson extrapolation () |

| Method | Steps | |||

|---|---|---|---|---|

| ASGQ + level of Richardson extrapolation () | ||||

| ASGQ + level of Richardson extrapolation () |

A.2 Case of set parameters in table 5.1

| Method | Steps | |||

|---|---|---|---|---|

| ASGQ () | ||||

| ASGQ () | ||||

| QMC | ||||

| M(# QMC samples) | ||||

| MC | ||||

| M(# MC samples) |

| Method | Steps | ||||

|---|---|---|---|---|---|

| ASGQ () | |||||

| ASGQ () | |||||

| QMC method | |||||

| MC method |

A.3 Case of set parameters in table 5.1

| Method | Steps | |||

|---|---|---|---|---|

| ASGQ () | ||||

| ASGQ () | ||||

| ASGQ () | ||||

| ASGQ () | ||||

| QMC | ||||

| M(# QMC samples) | ||||

| MC | ||||

| M(# MC samples) |

| Method | Steps | ||||

|---|---|---|---|---|---|

| ASGQ () | |||||

| ASGQ () | |||||

| ASGQ () | |||||

| ASGQ () | |||||

| QMC method | |||||

| MC method |

A.4 Case of set parameters in table 5.1

| Method | Steps | |||

|---|---|---|---|---|

| ASGQ () | ||||

| ASGQ () | ||||

| ASGQ () | ||||

| QMC | ||||

| M(# QMC samples) | ||||

| MC | ||||

| M(# MC samples) |

| Method | Steps | ||||

| ASGQ () | |||||

| ASGQ () | |||||

| ASGQ () | |||||

| QMC method | |||||

| MC method |