Higher Moment Estimation for Elliptically-distributed Data: Is it Necessary to Use a Sledgehammer to Crack an Egg?

Abstract

Multivariate elliptically-contoured distributions are widely used for modeling economic and financial data. We study the problem of estimating moment parameters of a semi-parametric elliptical model in a high-dimensional setting. Such estimators are useful for financial data analysis and quadratic discriminant analysis.

For low-dimensional elliptical models, efficient moment estimators can be obtained by plugging in an estimate of the precision matrix. Natural generalizations of the plug-in estimator to high-dimensional settings perform unsatisfactorily, due to estimating a large precision matrix. Do we really need a sledgehammer to crack an egg? Fortunately, we discover that moment parameters can be efficiently estimated without estimating the precision matrix in high-dimension.

We propose a marginal aggregation estimator (MAE) for moment parameters. The MAE only requires estimating the diagonal of covariance matrix and is convenient to implement. With mild sparsity on the covariance structure, we prove that the asymptotic variance of MAE is the same as the ideal plug-in estimator which knows the true precision matrix, so MAE is asymptotically efficient. We also extend MAE to a block-wise aggregation estimator (BAE) when estimates of diagonal blocks of covariance matrix are available. The performance of our methods is validated by extensive simulations and an application to financial returns.

1 Introduction

The classical multivariate statistics is largely motivated by relaxing the Gaussian assumption, which is not satisfied in many applications. There is an extensive literature in finance on the tail-index estimates of stock returns; while being unimodal and symmetric, the empirical returns exhibit leptokurtosis, which means that they have heavier tails and flatter peaks than those of normal data (Fama, 1965; Bollerslev and Wooldridge, 1992; Eberlein and Keller, 1995; Frahm et al., 2003; Cizek et al., 2005). Empirical evidence of the violation of Gaussian assumption has also been observed in genomics (Liu et al., 2003; Posekany et al., 2011; Hardin and Wilson, 2009) and in bioimaging (Ruttimann et al., 1998). The family of multivariate elliptically contoured distributions (Kelker, 1970), which we shall call elliptical distributions in short, provides a natural generalization of multivariate Gaussian distributions. Recently, many statistical methods for elliptically distributed data have been proposed, including works on covariance matrix estimation (Fan et al., 2018), graphical modeling (Han and Liu, 2012), classification (Fan et al., 2015b), etc.

The elliptical distributions are typically used as a semi-parametric model. Given a mean vector , a covariance matrix and a probability characteristic function , we say a random vector has an elliptical distribution if

| (1) |

where is a random vector that is uniformly distributed on the unit sphere , and independent of , is a nonnegative random variable whose characteristic function is . For model identifiability, we normalize such that

| (2) |

Under (1)-(2), and are the mean vector and covariance matrix of , respectively. The variable determines which sub-family the distribution belongs to. When is a chi-square random variable, it belongs to the multivariate Gaussian sub-family, and when follows an -distribution, it belongs to the multivariate sub-family or multivariate Cauchy sub-family. For most applications, the sub-family of the elliptical distribution is unknown, leaving the distribution of unspecified.

Although full knowledge of the distribution of is often not required, an estimate of its moment parameters is useful to statistical analysis and for understanding the tail of the distributions. One application is in quadratic classification. When data from two classes both follow elliptical distributions but have unequal covariance matrices, Fan et al. (2015b) showed that an estimate of is desired for building a quadratic classifier. Another application is to capture the tail behavior of financial returns by estimating the leptokurtosis. Modeling the returns of a set of financial assets by an elliptical distribution, the leptokurtosis equals to , so the problem reduces to estimating .

For any , define the -th scaled even moment of by

| (3) |

The first scaled even moment is . In this paper, we are interested in estimating for any fixed , given independent and identically distributed (i.i.d.) samples from (1).

1.1 The plug-in estimators

We consider an ideal case where are known. Given samples from an unknown elliptical distribution, each has a decomposition , and are copies of . Using the fact that takes values on the unit sphere, we observe for , where . Hence, in the ideal case, are directly observed. It motivates the following estimator of :

| (4) |

We call the Ideal Estimator. The ideal estimator is not feasible in practice, and a natural modification is to plug in estimates of . This gives rise to the plug-in estimator:

| (5) |

This estimator was proposed by Maruyama and Seo (2003) in the setting of a fixed dimension, where they used the sample mean to estimate and the inverse of the sample covariance matrix to estimate . In the modern high-dimensional settings where grows with , one can on longer use the inverse of sample covariance matrix to estimate ; Fan et al. (2015b) proposed plugging in an estimator of from high-dimensional sparse precision matrix estimation methods, with stringent structural assumptions on .

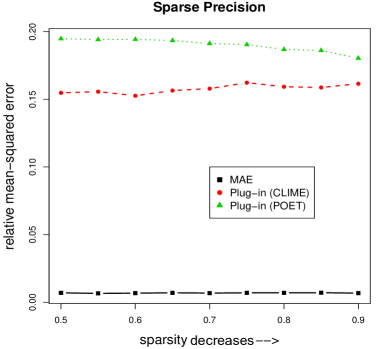

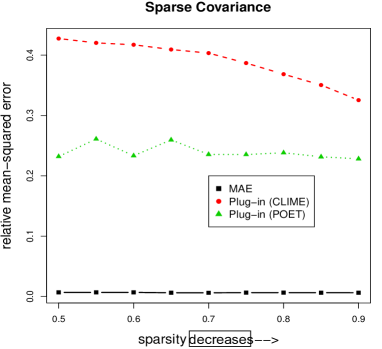

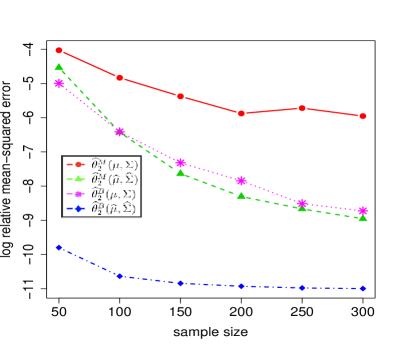

However, the plug-in estimators perform unsatisfactorily for high-dimensional settings due to the difficulty of estimating . Existing methods of estimating only perform well under stringent conditions, such as the sub-Gaussian assumption on the distribution and/or structural assumptions on (e.g., sparsity). Especially, the structural assumption on is critical for the success of these methods. Figure 1 shows the performance of the plug-in estimator when the structural assumption required by is violated. We consider two estimators of , the CLIME estimator (Cai et al., 2011) which requires sparsity of , and the POET estimator (Fan et al., 2013) which assumes a factor structure with sparse covariance of the idiosyncratic component. On the left panel of Figure 1, we generate elliptical data with a sparse covariance matrix, , , where controls the sparsity level and varies in . Here, the structural assumption of POET is not satisfied, and the associated plug-in estimator of performs unsatisfactorily. On the right panel, we generate data with a sparse precision matrix , where each entry of the upper triangle of has a probability of to be nonzero,444We generate using fastclime.generator() in the R package clime, where the graph argument is set “random”. with chosen from . The assumption of CLIME is violated, so the associated plug-in estimator of has a unsatisfactory performance.

In fact, the philosophy of plug-in estimators is problematic. Estimating large precision matrices is a well-known difficult problem (even for Gaussian data), as one needs to estimate a large number of parameters. On the other hand, our problem only involves estimating one single parameter . Intuitively, the latter should be much easier than the former. The plug-in estimators are realy using “a sledgehammer to crack an egg.”

1.2 The marginal aggregation estimator (MAE)

Is it possible to avoid using the “sledgehammer” of precision matrix estimation? We show that this is possible by a new marginal aggregation estimator. In model (1), letting be the -th coordinate of , we have

| (6) |

Our key observation is that each individual coordinate of contains information of . It motivates us to construct an estimator of using only one coordinate of samples. Let be the -th diagonal of . We notice that (6) implies . The random variable is unobserved, but its distribution is known once is given. It can be shown that (see Proposition 3.1)

| (7) |

Inspired by (6)-(7), we introduce an estimator of using the marginal data :

| (8) |

We call the Marginal Estimator. It only requires knowledge of and successfully avoids precision matrix estimation. For each , we can define a marginal estimator and we will show that all marginal estimator contains the same amount of information about (see Theorem 2.4). All these marginal estimators are unbiased, so taking their average gives rise to a new unbiased estimator:

| (9) |

We call the Marginal Aggregation Estimator (MAE). The “aggregation” of marginal estimators helps reduce the asymptotic variance. Our proposed estimator is a natural plug-in version of (9) given by

| (10) |

where is as in (7), is an estimator of , and are the estimators of .

Compared with the plug-in estimator (5), MAE is numerically more appealing, as it only needs to estimate the diagonal entries of . Back to the example in Figure 1, we implement MAE using sample mean as and sample covariance matrix as . MAE significantly outperforms the plug-in estimators, even when the structural assumptions of the plug-in estimators are satisfied.

1.3 Organization of the paper

In Section 2, we study the theoretical properties of MAE. Under mild regularity conditions, we show that MAE is unbiased and root- consistent, regardless of the structure of . We also show that MAE is asymptotically efficient, with an asymptotic variance matching that of the ideal estimator when are given. We also discuss how to construct a confidence interval of .

In Section 3, we generalize the idea of MAE to develop estimators of that use a small subset of the coordinates. We introduce the block-wise estimator and the blockwise aggregation estimator (BAE), analogous to the marginal estimator and MAE. These ideas help further reduce the estimation errors in the second order.

Section 4 validates the theoretical insight by extensive simulations. Section 5 gives an application of MAE to time series data. We consider an extension of model (1) to multivariate time series:

where is the time-varying mean, is a vector of observed factors, and is a matrix of factor loadings. We extend MAE to a method for estimating the realized . Its application to stock returns provides a new index that captures information of whole market. Section 6 contains conclusions and discussions. All the proofs are relegated to the appendix.

Notation: Throughout this paper, for any vector and matrix , we let denote the Euclidean norm of and let , and denote its spectral norm, Frobenius norm and entry-wise maximum norm, respectively. We use , , and to denote the Marginal Estimator, MAE, Ideal Estimator, and BAE (to be introduced), respectively, with given ; when are replaced by , it means we plug in estimators of the mean vector and covariance matrix. We frequently use notations , where is defined in (3), is defined in (7), and are defined in Definition 2.1. For all settings in this paper, is a constant, depend on but are at the constant scale.

2 Theoretical properties of MAE

We study the asymptotic properties of MAE defined in (10), assuming both tend to infinity. First, we study the consistency of MAE. The following theorem shows that, when the distribution is marginally sub-Gaussian, if we plug in the sample mean and sample covariance matrix as , then MAE is always root- consistent.

Theorem 2.1 (Root- consistency).

The root- consistency of MAE requires no conditions on either or . It confirms our previous insight that estimating moment parameters is an “easier” statistical problem than estimating large matrices. On the other hand, the plug-in estimators only perform well when the assumed structural assumptions (e.g., sparsity) on or are satisfied.

Many distributions in the elliptical family are heavy-tailed and don’t satisfy the marginal sub-Gaussianity assumption. In these cases, we prefer to use robust estimators of and (Fan et al., 2017; Sun et al., 2018+). They are M-estimators with robust loss functions or rank-based estimators. Compared to the sample mean and sample covariance estimators, these robust estimators lead to sharper bounds of and in the case of heavy-tailed data. The next theorem studies MAE with general mean/covariance estimators.

Theorem 2.2 (Consistency, with general mean/covariance estimators).

The typical error rate of robust estimators is and (Fan et al., 2017; Sun et al., 2018+), so the associated MAE satisfies . Compared with the rate in Theorem 2.1, the extra factor here is a price paid for heavy tails.

Next, we study the asymptotic variance of MAE. By Theorem 2.1, MAE is already rate-optimal. We would like to see whether it also achieves the optimal “constant”. We shall compare its asymptotic variance with that of the Ideal Estimator (4). Since the Ideal Estimator knows the true , for a fair comparison, we consider MAE with true .

Definition 2.1.

For any , let and , where denotes the chi-square distribution with degrees of freedom.

The quantities capture the difference between moments of an elliptical distribution and moments of a multivariate Gaussian distribution with matching mean and covariance matrix. It depends on but is at the constant scale under our settings.

Theorem 2.3 (Variance).

The upper bound for the variance has three terms: The first term is ; as we shall see, this term matches with the variance of the benchmark estimator. The second term is and is negligible for diverging . The third term is caused by correlations among different marginal estimators . This term is negligible as long as ; consider a special case where is bounded, then ; so the requirement of is mild. Indeed, if requires that the sparsity of correlation coefficients: , where . The next proposition confirms that the asymptotic variance of MAE is the same as the asymptotic variance of the Ideal Estimator:

Proposition 2.1 (Comparison with benchmark).

Last, we construct confidence intervals of . Since MAE is the average of strongly dependent marginal estimators, its asymptotic normality is hard to approach. We instead use the marginal estimator in (8) to construct confidence intervals.

Theorem 2.4 (Asymptotic normality).

This theorem shows somewhat surprisingly that all marginal estimator contains the same amount of information about . Given consistent estimators , the asymptotic level- confidence interval of is

| (11) |

where is the -quantile of a standard normal. It doesn’t matter which of we use, as these marginal estimators have the same asymptotic variance. For the estimators , we suggest using MAE.

If we only need a point estimator but not a confidence interval, we prefer MAE to the Marginal Estimator, as MAE has a smaller variance in many scenarios. For example, when , by plugging in the true ,

Since , the latter variance is strictly larger. In contrast, MAE is first-order efficient.

3 Extension to blockwise aggregation

In the construction of MAE, each marginal estimator only uses one coordinate of the samples. It is convenient to implement and gives rise to an estimator that is first-order efficient, provided that the third term in Theorem 2.3 is negligible. It turns out that, the second order term in the variance can be improved upon by using blockwise aggregation, and so is the third term, which is related to the correlation structure. Our simulation studies below show that the improvement is real. This motivates us to extend the marginal estimator to a blockwise estimator that uses a small number of coordinates of the samples and takes into account their correlation structures. We then generalize MAE to BAE — an aggregation of many blockwise estimators.

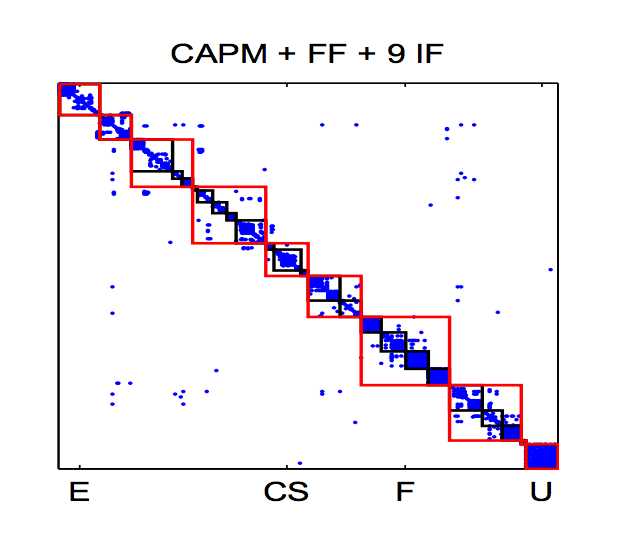

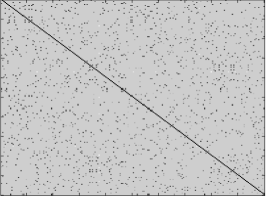

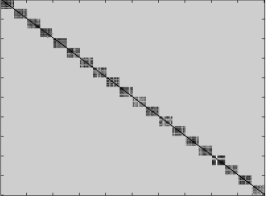

BAE can be applied to settings where the covariance matrix is approximately blockwise diagonal after row/column permutation. Figure 2 gives such an example, where the S&P 500 stocks divide into many small-size blocks according to sectors or industries of stocks and the stock returns within each block are correlated but admits block structure after taking out the market factor. BAE can take advantage of the within-block correlations and further improve MAE in the second order term.

3.1 A block-wise aggregation estimator (BAE)

We fix a block and let . For any vector and matrix , let be the subvector of containing the coordinates indexed by and let be the submatrix of containing the entries indexed by . By Fang and Zhang (1990), when follows an elliptical distribution (1), the subvector satisfies that

| (12) |

where is a random variable that follows a beta distribution Beta, the random vector follows a uniform distribution on the unit sphere , and are mutually independent. Since ,

The random variable is not directly observable, but its expectation is known:

Proposition 3.1.

For each and , define with . Then,

Replacing by its expectation, we immediately have an estimator of based on :

| (13) | ||||

| (14) |

We call the Blockwise Estimator. Now, given a collection of blocks , we can define a blockwise estimator for each and then take their average:

| (15) |

We call the Blockwise Aggregation Estimator (BAE). Here denotes the collection of diagonal blocks with . Our final estimator is a plug-in version of BAE by plugging in an estimator and estimators of those diagonal blocks of .

Since BAE only estimates the small-size diagonal blocks of and does not need to estimate , it inherits a nice property of MAE: root- consistency is guaranteed with no conditions on or .

Theorem 3.1 (Root- consistency).

Fix and . Under model (1), suppose and . We assume the minimum eigenvalue of any diagonal block of is lower bounded by . Let be a collection of nonrandom, non-overlapping blocks such that the size of each block is bounded by . Given iid samples , consider the BAE in (15), where are estimated by the sample mean vector and sample covariance matrix. Then,

Theorem 3.2 (Consistency, with general mean/covariance estimators).

Fix and . Under model (1), we assume , , and the minimum eigenvalue of any diagonal block of is lower bounded by . Let be a collection of nonrandom, non-overlapping blocks where the size of blocks is bounded by . Given iid samples , consider the BAE in (15), where satisfy and with probability , with and as . Then, for any , with probability , there is a constant such that

We note that MAE is a special case of BAE, with all block size equal to . The motivation of generalizing MAE to BAE is to better take advantage of correlation structures, and this is revealed by comparing the asymptotic variances of two methods; see Section 3.2 below. To implement BAE, we need to determine the collection of blocks, and in Section 3.3 we discuss how to select blocks.

3.2 Variance comparison

We compute the asymptotic variance of BAE and compare it with the asymptotic variances of MAE and Ideal Estimator. Same as before, in the variance calculation we assume are given.

Definition 3.1.

For each , let , where denotes the chi-square distribution with degrees of freedom. Given a collection of blocks , let .

Theorem 3.3 (Variance of BAE).

Let be samples of model (1). Fix and suppose . There exists a constant , independent of the distribution of , such that for any collection of non-overlapping blocks,

The upper bound of the variance has three terms:

-

•

The first term is , which also appears in the variance of MAE and Ideal Estimator. It is the dominating term of the variance.

-

•

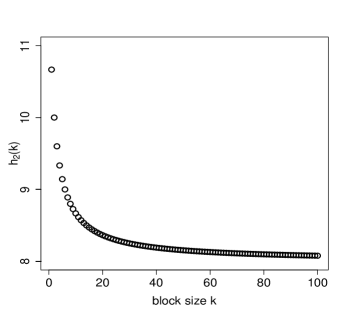

The second term is , where the constant in front of it is related to a quantity . We call the block-division factor, as it is only a function of . To see how this factor changes with block size, let’s consider a special case where all blocks have an equal size and is a multiple of . Then,

It is a monotone decreasing function of (see Figure 3). Hence, increasing the block size leads to a reduction of this term, which indicates that the second order efficiency of MAE can be improved with .

-

•

The last term comes from the correlations among estimators associated with different blocks. It doesn’t exist for the Ideal Estimator, but both MAE and BAE have this extra term. For MAE, all off-diagonal entries of contribute to this term. However, for BAE, only off-diagonal blocks contribute. Especially, when is blockwise diagonal with respect to , this extra term becomes zero. Again, increasing the block size leads to a reduction of this term.

From MAE to BAE, we can see that the dominating term in the variance bound remains the same, but the other two terms are reduced and the performance still improves. However, we cannot use too large blocks, because BAE needs to invert an estimate of and the error of estimating increases as the block size increases.

We now give a more thorough comparison of four estimators, the Ideal Estimator (IE) , the Marginal Estimator (ME) , the MAE , and the BAE ; see Table 1. We conclude that

-

•

IE has the optimal variance, but it works unsatisfactorialy in the real case of unknown , as it requires estimating .

-

•

ME avoids estimating and works in the real case, but its asymptotic variance is non-optimal.

-

•

MAE aggregates a number of ME’s and achieves the optimal variance when .

-

•

Compared with MAE, BAE relaxes the condition of and reduces the second-order term of the variance.

From ME to BAE, we have used two methodological ideas: to aggregate “local” estimators and to use a block of coordinates in each “local” estimator. Both help reduce the variance of the estimator, with the first idea playing a more significant role.

| IE | ME | MAE | BAE | |

|---|---|---|---|---|

| dominating term | ||||

| 2nd-order term | — | |||

| correlation term |

Remark 1. IE and MAE are special cases of BAE with equal-size blocks of and , respectively. We note that and , so Theorem 3.3 matches with the variance bounds of MAE (Theorem 2.3) and the IE (Proposition 2.1).

Remark 2 (multivariate Gaussian). Let’s consider a special case where the data are multivariate Gaussian but the user doesn’t know and still applies the estimators in this paper. For Gaussian distributions, the first term in the variance bound disappears, so the estimators considered here all have a faster rate of convergence as . This is the only case where a large helps, i.e., “dimensionality is a blessing.” Moreover, the difference between MAE and BAE is more prominent, as the second term in the variance bound is now dominating. Figure 4 displays the error bound according to Theorem 3.3 for the case of and being a blockwise diagonal matrix with blocks whose off-diagonal element is . The results favor BAE, especially for the blockwise with large within-block off-diagonals.

3.3 Construction of blocks

We provide two approaches of selecting the blocks. The first approach works well when the true is approximately block-wise diagonal, such as example on the returns of the S&P 500 components(see Figure 2). The second approach is a random scheme and works for general settings.

BAE1: Constructing blocks from a raw estimate of . Let be a raw estimate of ; for example, it can be the sample covariance matrix or the robust estimator of in Section 4. Fixing a threshold , we define a graph with nodes , where there is an undirected edge between nodes and if and only if the estimated absolute correlation exceeds , namely,

The nodes of this graph uniquely partitions into components (a component of a graph is a maximal connected subgraph). We propose using

See Figure 5 for an illustration of this procedure.

This approach guarantees that all blocks are non-overlapping. Numerical evidence suggests that it performs well with an appropriate choice of , especially when the true is blockwise diagonal. However, the threshold is a tuning parameter, and it can be inconvenient to select in a data-driven fashion. Below, we introduce a tuning-free approach.

BAE2: Randomly selecting pairs as blocks. In this approach, we let

This approach is designed for block size equal to , and the obtained blocks may overlap. Although it sounds ad-hoc, this approach has an appealing numerical performance. When the number of pairs are sampled sufficiently large, by the law of large numbers, it approaches the all pairwise aggregation estimator and this explains why the approach has an appealing numerical performance. This approach can easily be extended to blocks of any size that is smaller than so long as the estimated covariance matrix for each block can be easily inverted and estimated well.

4 Simulations

We investigate the performance of estimators on extensive simulations. To have realistic simulation settings, we use a calibrated from stock returns. The calibration procedure is the same as that in Fan et al. (2015c) and Fan et al. (2013). Fix . We take the daily returns of companies in S&P 500 index with the largest market capitalization from July 1st, 2013 to June 29th, 2018 (data were downloaded from the COMPUSTAT website). We fit the Fama-French three-factor model to the excess returns :

where is the factor loading matrix, denotes the Fama-French factors with covariance matrix and is the idiosyncratic component. This factor model induces a covariance structure for :

where is the covariance matrix of idiosyncratic noise . We downloaded the factors from the Kenneth French data library and used the method in Fan et al. (2013) with the recommended threshold (for estimating sparse ) to get and estimate . We then use as the true to generate data from model (1).

When implementing the estimators, we plug in two different estimators of . The first choice is to use sample mean and sample covariance matrix. The second choice is to use robust M-estimators, called adaptive Huber estimator (Fan et al., 2017; Sun et al., 2018+), which are designed for heavy-tailed data. These estimators lead to better large-deviation bounds. In detail, for a tuning parameter chosen by cross-validation, we estimate by , where

the Huber loss. We estimate by , where

Here, each tuning parameter is selected via cross-validation using the data .

Experiment 1: Performance of MAE.

Fix . We consider four sub-experiments:

-

•

Experiments 1.1 and 1.3: We fix and let vary in . The data follow multivariate Gaussian distributions (Experiment 1.1) or multivariate -distributions with degrees of freedom equal to (Experiment 1.3).

-

•

Experiments 1.2 and 1.4: We fix and let vary in . The data follow multivariate Gaussian distributions (Experiment 1.2) or multivariate -distributions with degrees of freedom equal to (Experiment 1.4).

In all settings, , so we focus on the challenging case of high-dimensionality. For each setting, we compare four estimators:

-

•

: Ideal Estimator, which knowns .

-

•

: MAE with given .

-

•

: MAE, where are estimated using the sample mean/covariance matrix in Experiment 1.1&1.2 and using the aforementioned robust-M estimators for Experiment 1.3&1.4.

-

•

: Plug-in Ideal Estimator, with plugged-in estimators of . We use the sample mean to estimate and use POET (Fan et al., 2013) (with a default threshold) to estimate .

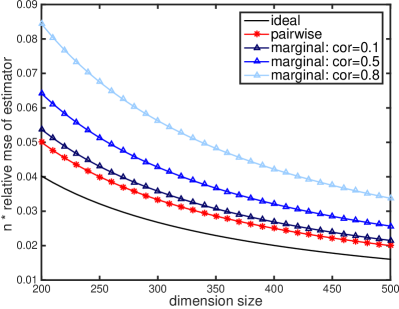

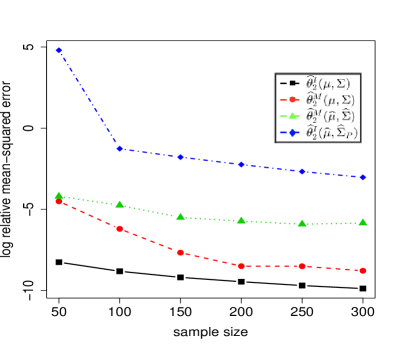

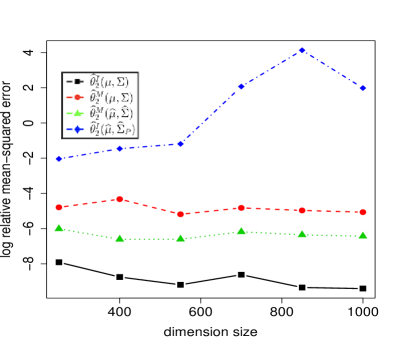

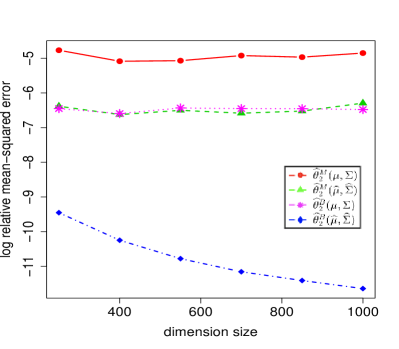

The results are presented in Figure 6, where the -axis is , based on the average over repetitions. As we have expected, the Ideal Estimator always gives the lowest error, however, such an estimator is not practically feasible. Instead, we plug estimates of into the Ideal Estimator to make it practically feasible, then it has an unsatisfactory performance; this confirms our previous insight about the drawback of the plug-in estimator. Our proposed MAE works well, always significantly better than the plug-in estimator. The performance of MAE becomes better as the sample size grows, and its performance stays relatively stable as the dimension grows. This is desirable: our proposed estimator doesn’t face any curse of dimensionality. The results are similar for the multivariate Gaussian data and the multivariate -data, except that for Gaussian data, MAE with even outperforms MAE with true . One possible reason is the self-normalization phenomenon: An estimator, when divided by its sample variance, gives better performance than that divided by the true variance.

Experiment 2: Confidence Interval.

For each of the experiments above: Experiments 1.1, 1.2, 1.3 and 1.4, we calculate the probability that the true value of lies in the confidence interval derived in Theorem 2.4 and presented in Equation (11). In Table 2, we see that for a confidence interval, the empirical coverage probabilities are close to the confidence level.

| 250 | 400 | 550 | 700 | 850 | 1000 | |

|---|---|---|---|---|---|---|

| Gaussian | 92.0% | 95.0% | 93.5% | 95.5% | 95.5% | 96.5% |

| Student’s | 96.5% | 98.0% | 94.5% | 97.0% | 96.0% | 96.5% |

| 50 | 100 | 150 | 200 | 250 | 300 | |

| Gaussian | 95.5% | 94.2% | 93.5% | 93.0% | 95.5% | 94.0% |

| Student’s | 98.0% | 96.0% | 95.5% | 93.5% | 94.5% | 97.0% |

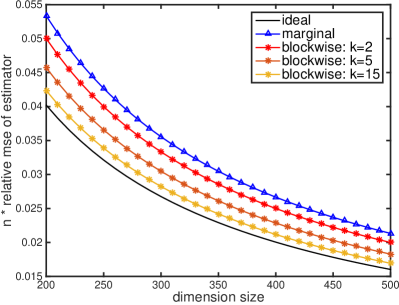

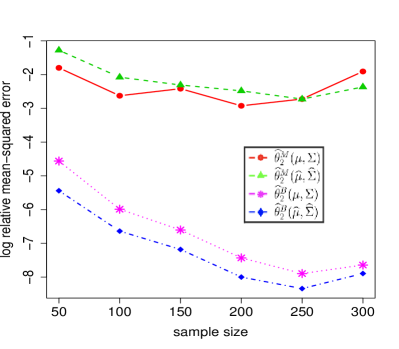

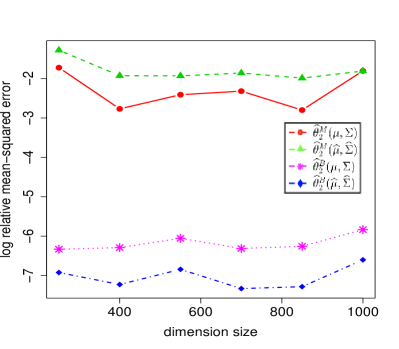

Experiment 3: Performance of BAE.

We study whether BAE, which uses a block of coordinates at a time and takes advantage of the correlation structure, can further improve the performance of MAE. The four sub-experiments, Experiments 3.1-3.4, have the same settings as those of Experiments 1.1-1.4. When implementing BAE, we use the second approach in Section 3.3 to choose the blocks; note that the blocks all have a size and may overlap. We use the sample mean/covariance to estimate for multivariate Gaussian data and the robust M-estimators for multivariate data. Since we focus on the comparison between MAE and BAE, we do not report the errors of the Ideal Estimator and plug-in estimator in this experiment.

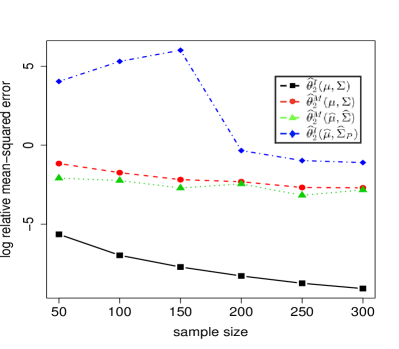

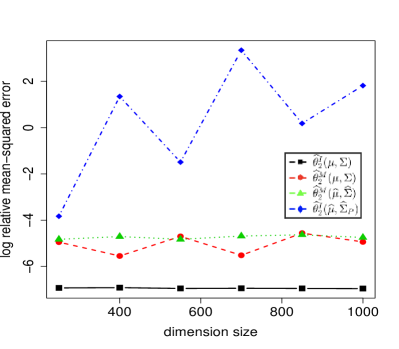

The results are presented in Figure 7. First, we can see that BAE improves the performance of MAE, especially when is large. Second, the self-normalization phenomenon is also observed: BAE with even outperforms BAE with true , especially for Gaussian data.

5 Application: Estimating realized in a time series

Given the returns of a panel of stocks, we are interested in extending the idea of MAE to provide a daily risk index for the whole panel of stocks. We cast it as the problem of estimating the realized in a multivariate time series with elliptically-distributed noise. Let be the returns of stocks during a time period of days. We extend model (1) to an elliptical model for multivariate time series

| (16) |

where is the time-varying mean, is a vector of factors, and is a matrix of factor loadings. We are interested in estimating the daily realized .

Our method has four steps:

-

1. Estimate . For daily or higher frequency data, we set , since it is commonly believed that the short-time returns are not predictable. For weekly or monthly data, we estimate by the weekly or monthly average.

-

3. Estimate . We assume is a diagonal matrix and estimate its diagonal elements by fitting an ARCH model on each coordinate of . In detail, for each , let be the -th coordinate of . We assume there is idiosyncratic noise such that

where is the order of ARCH model and are parameters. We estimate using the conditional maximum likelihood estimator and then construct . Let

-

4. Estimate . We adapt the idea of MAE to the current setting. Let . Our model becomes , i.e., the -th component of is . It follows that

where is the -th diagonal of . Here, the last equality is due to in Equation (7). We approximate by and get a marginal estimator of : . We then aggregate them:

(17)

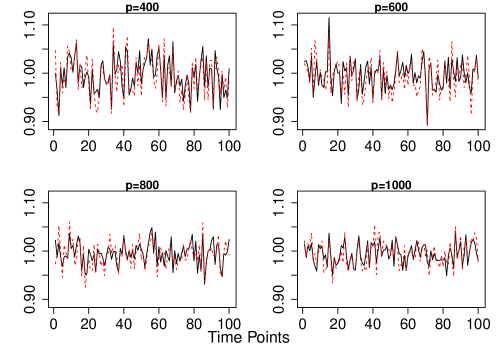

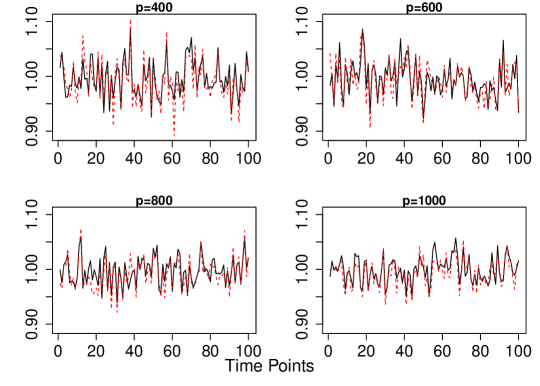

In Section D of the appendix, we investigate the performance of our estimator in simulations. Under a variety of settings, our estimated curve of fits the true curve of very well. See details therein.

We applied our estimator to the S&P 500 stock returns. We took the daily returns of stocks from the S&P 500 index with the largest market capitalization, from July 1, 2008 to June 29, 2012. Each stock is assigned a Global Industry Classification Standard (GCIS) code. The GCIS code divides stocks into eleven sectors: Energy, Consumer Discretionary, Communication Services, Consumer Staples, Financials, Health Care, Industrials, Information Technology, Materials, Real Estate, and Utilities. We applied our estimator to stocks in each sector. When implementing our method, we set in Step 1, used three observed Fama-French factors as in Step 2, and set the order of ARCH model to in Step 3.

The curves of estimated for sectors are displayed in Figure 8 (the curves are smoothed by taking a moving average on a -day window). The estimated for all sectors largely synchronize, reaching their peaks during the 2008 financial crisis. In the crisis, the estimated for the Financials sector is significantly larger than that of other sectors. The large value of for the Financials sector remains in the post-crisis period until May, 2009. We also computed the pairwise correlations among of sectors, as shown in Table 3. It suggests that the for the Energy sector and the Financials sector are highly correlated with each other. These two sectors are also highly correlated with sectors of Materials, Real Estate, and Utilities. In comparison, for the Consumer Discretionary sector and Information Technology sector, their are less correlated with those of other sectors.

| E | CD | CO | CS | F | HC | IN | IT | M | R | U | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Energy (E) | – | .36 | .43 | .42 | .37 | .44 | .35 | ||||

| Consumer Discretionary (CD) | .36 | – | .30 | .35 | .43 | .34 | .37 | .33 | .33 | .36 | .35 |

| Communication Services (CO) | .43 | .30 | – | .33 | .43 | .33 | .40 | .32 | .39 | .44 | .41 |

| Consumer Staples (CS) | .42 | .35 | .33 | – | .42 | .36 | .37 | .35 | .38 | .38 | .43 |

| Financials (F) | .43 | .43 | .42 | – | .42 | .40 | |||||

| Health Care (HC) | .37 | .34 | .33 | .36 | .42 | – | .40 | .39 | .37 | .36 | .33 |

| Industrials (IN) | .44 | .37 | .40 | .37 | .40 | – | .39 | .44 | |||

| Information Technology (IT) | .35 | .33 | .32 | .35 | .40 | .39 | .39 | – | .36 | .33 | .34 |

| Materials (M) | .33 | .39 | .38 | .37 | .49 | .36 | – | .42 | .43 | ||

| Real Estate (R) | .36 | .44 | .38 | .36 | .44 | .33 | .42 | – | |||

| Utilities (U) | .34 | .41 | .43 | .33 | .45 | .34 | .43 | .46 | – |

6 Discussion

In this paper, we consider the problem of estimating the even moments of in an elliptical distribution . A natural idea is the plug-in estimator (Maruyama and Seo, 2003; Fan et al., 2015b), which requires an estimator of the precision matrix and whose performance crucially relies on structural assumptions on or . Instead, we propose a marginal aggregation estimator (MAE) that only needs to estimate the diagonal of . Our approach validates the insight that estimating a large precision matrix is statistically more challenging than estimating a moment parameter—it is unnecessary to use the sledge hammer to crack an egg. We prove that MAE is root- consistent, under no conditions on or . We also show that MAE achieves the first-order efficiency, with an asymptotic variance matching with the variance of an ideal estimator when are given. We further generalize MAE to a block-wise aggregation estimator (BAE) that needs to estimate small-size diagonal blocks of . BAE takes advantage of correlations among coordinates and improves MAE on the second-order efficiency. Our proposed estimators are conceptually simple and easy to implement.

Estimating the moment parameters of an elliptical distribution is useful in quadratic discriminant analysis (Fan et al., 2015b) and estimating tail behavior of financial returns (Fama, 1965; Bollerslev and Wooldridge, 1992; Eberlein and Keller, 1995; Frahm et al., 2003; Cizek et al., 2005). In an application on the stock returns, we propose a multivariate time series model with factor structures and elliptically distributed idiosyncratic noise. We extend MAE to an estimator for estimating the day-to-day value of . We apply the method to stocks of each industry sector. It produces an “tail index” for each industry sector. These tail indices reveal interesting difference among industry sectors, especially during the financial crisis.

The study leaves a few open questions for future work. The first is how to improve the estimators for heavy tailed data. Our current approach plugs into MAE the robust estimators of mean and covariance matrix. Instead, we may construct a robust M-estimator for simultaneously estimating with marginal data and then aggregate these marginal estimators of in a similar way. We hope such an approach helps remove the -factor in the error rate of Theorem 2.2. The second is the optimal strategy of constructing blocks in BAE. There is a trade-off in choosing the blocks: With larger blocks, it reduces the variance of the estimator when true are plugged in, but at the same time, the errors of estimating diagonal blocks of increase. How to construct the blocks in a data-driven way is an interesting question. Third, the current theory for BAE assumes non-overlapping blocks. The results can be extended to overlapping blocks, with nontrivial efforts. We leave it for future work. The last problem is to extend our estimators to time dependent data, where the distribution of have change-points. For financial data, such change-points may relate to financial boom or crisis. We propose a kernel-smoothed version of MAE: Given data , for a kernel function with bandwidth , let

We can similarly define the one-sided versions of the kernel estimator. We can combine these estimators with change-point detection methods, which we leave for future work.

References

- Bollerslev and Wooldridge (1992) Bollerslev, T. and Wooldridge, J. (1992). Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariances. Econometric Reviews 11 143–172.

- Cai et al. (2011) Cai, T., Liu, W. and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association 106 594–607.

- Cizek et al. (2005) Cizek, P., Härdle, W. K. and Weron, R. (2005). Statistical Tools for Finance and Insurance. Springer-Verlag Berlin Heidelberg.

- Eberlein and Keller (1995) Eberlein, E. and Keller, U. (1995). Hyperbolic distributions in finance. Bernoulli 1 281–299.

- Fama (1965) Fama, E. (1965). The behavior of stock market prices. Journal of Business 38 34–105.

- Fan et al. (2015a) Fan, J., Furger, A. and Xiu, D. (2015a). Incorporating global industrial classification standard into portfolio allocation: A simple factor-based large covariance matrix estimator with high frequency data. Social Science Research Network, SSRN-id 2548613 .

- Fan et al. (2015b) Fan, J., Ke, Z., Liu, H. and Xia, L. (2015b). QUADRO: A supervised dimension reduction method via Rayleigh Quotient optimization. The Annals of Statistics 43 1498–1534.

- Fan et al. (2017) Fan, J., Li, Q. and Wang, Y. (2017). Estimation of high dimensional mean regression in the absence of symmetry and light tail assumptions. Journal of the Royal Statistical Society, Series B 79 247–265.

- Fan et al. (2013) Fan, J., Liao, Y. and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B 75 603–680.

- Fan et al. (2015c) Fan, J., Liao, Y. and Shi, X. (2015c). Risks of large portfolios. Journal of Econometrics 186 367–387.

- Fan et al. (2018) Fan, J., Liu, H. and Wang, W. (2018). Large covariance estimation through elliptical factor models. The Annals of Statistics 46 1383–1414.

- Fang and Zhang (1990) Fang, K. and Zhang, Y. T. (1990). Generalized Multivariate Analysis. Science Press.

- Frahm et al. (2003) Frahm, G., Junker, M. and Szimayer, A. (2003). Elliptical copulas: applicability and limitations. Statistics and Probability Letters 63 275–286.

- Han and Liu (2012) Han, F. and Liu, H. (2012). Transelliptical component analysis. Advances in Neural Information Processing Systems 25.

- Hardin and Wilson (2009) Hardin, J. and Wilson, J. (2009). A note on oligonucleotide expression values not being normally distributed,. Biostatistics 10 446–450.

- Kelker (1970) Kelker, D. (1970). Distribution theory of spherical distributions and a location-scale parameter generalization. Sankhya 32 419–430.

- Liu et al. (2003) Liu, L., Hawkins, D. M., Ghosh, S. and Young, S. S. (2003). Robust singular value decomposition analysis of microarray data. Proceedings of the National Academy of Sciences 100 13167–13172.

- Maruyama and Seo (2003) Maruyama, Y. and Seo, T. (2003). Estimation of moment parameters in elliptical distributions. Journal of Japan Statistical Society 33 215–229.

- Posekany et al. (2011) Posekany, A., Felsenstein, K., and Sykacek, P. (2011). Biological assessment of robust noise models in microarray data analysis. Bioinformatics 27 807–814.

- Ruttimann et al. (1998) Ruttimann, U. E., Unser, M., Rawlings, R. R., Rio, D., Ramsey, N. F., Mattay, V. S., Hommer, D. W., Frank, J. A. and Weinberger, D. R. (1998). Statistical analysis of functional MRI data in the wavelet domain. IEEE Transactions on Medical Imaging 17 142–154.

- Sun et al. (2018+) Sun, Q., Zhou, W.-X. and Fan, J. (2018+). Adaptive huber regression: Nonasymptotic optimality and phase transition.

Appendix A Proof of main results

A.1 Proof of Theorem 2.1

Write for short and . By Theorem 2.3, is unbiased and satisfies

We note that are constants, are bounded above/below by constants, and all entries of the correlation matrix are bounded by . Hence, the right hand side is , and it implies

To show the claim, it suffices to show that

| (18) |

Below, we show (18). Write for short , for . For any , let . Using these notations,

At the same time, noticing that and , we have

Combining the above gives

| (19) | ||||

| (20) | ||||

| (21) |

To bound the right hand side of (19), we define an event. By (6), . Let . Then, . It follows that

| (22) |

Note that . At the same time, since when , it holds that . Together, we have . Our assumption of guarantees for . It follows that and for . As a result,

| (23) |

Using the marginal sub-Gaussianity, for any , there exists a constant such that, with probability ,

| (24) |

Let be the event that (24) holds. To show (18), it suffices to show that

| (25) |

We now show (25). Consider and . By (22) and using that has a symmetric distribution, we have for any odd . As a result, over the event , , and , for all and . Additionally, since , where , it holds that over the event . It follows that

| (26) | ||||

| (27) |

Consider . Since , we write

Over the event , and . This means, for all , is contained in a diminishing neighborhood of . We use Taylor expansion of the function . It gives

| (28) | ||||

| (29) | ||||

| (30) | ||||

| (31) |

where the third line is due to over the event and the fourth line is due to (22). By (22) and (28),

| (32) | ||||

| (33) | ||||

| (34) |

Write for short. Then,

| (35) |

We introduce positive random variables such that and that are independent of . Then, . For even integers and ,

For all such that , the left hand side is uniformly bounded by a constant. Additionally, by elementary probability, . It follows that

| (36) |

In particular, by taking and in the above, we have for all . Additionally, by definition, so the assumption guarantees

| (37) |

Using (36)-(37), we first bound . It is seen that

As a result,

| (38) |

We then bound . Consider such that and . By (35), for . Therefore, if are mutually distinct, . It follows that

Moreover, the total number of such distinct is . It follows that

| (39) |

Pluging (38) and (39) into (32) gives

| (40) |

We further plug (26) and (40) into (19). It gives (25). The proof is now complete. ∎

A.2 Proof of Theorem 2.2

Similar to the proof of Theorem 2.1, let and denote the MAE with true and estimates ; here, are not necessarily the sample mean and sample covariance matrix. It follows from Theorem 2.3 that . By Markov’s inequality, for any constant ,

| (41) |

Hence, given , we can choose an appropriate such that the above probability is bounded by .

Below, we bound . Letting and , we have

where

It follows that

First, we consider . By direct calculations,

where for . Under our assumption, , and . Moreover, by similar technique in the proof of Theorem 2.3, we can prove that, , for . As a result, for any , there exists such that, simultaneously for , with probability . On this event,

| (42) |

Next, we consider . By our assumption, . It follows that

Plugging it into the definition of , we have

Again, we can easily prove that for all . It follows that, for any , there exists , such that simultaneously for all . On this event,

| (43) |

Combining (42)-(43) gives . We further combine it with (41). It gives the claim.

A.3 Proof of Theorem 2.3

Write for short and . First, we show that is unbiased. Recall that . It suffices to show is unbiased for each . Recall that

| (44) |

By the form of elliptical distribution, , where and are independent of each other. We have seen in Section 1.2 that . It follows that

Plugging it into (44) gives

| (45) |

This proves that each is unbiased. It follows that is also unbiased.

Next, we calculate the variance of . For each , let , where , . Noting that are random vectors, we have

| (46) |

It suffices to calculate the variance in the case of . From now on, we fix . Let be the observed realization of the elliptical distribution. Write

We now calculate and . Recalling that , we define random vectors

| (47) |

where is a chi-square random variable independent of . Since the multivariate normal distribution is a special elliptical distribution with , we immediately have . It follows that . At a result, for all ,

It follows that

| (48) | ||||

| (49) | ||||

| (50) |

Similarly, since and , we have

Therefore,

| (51) | ||||

| (52) | ||||

| (53) |

Combining (48) and (51) and noting that for all , we rewrite

As a result,

| (54) | ||||

| (55) | ||||

| (56) |

Moreover, since and , we have

Plugging it into (54) gives

This is for the case of . For a general , we combine it with (46) to get

| (57) |

What remains is to calculate the variance of . By definition,

Here coincides with the correlation matrix of the elliptical distribution. It is seen that

where denotes the covariance between and when follows a bivariate normal distribution with covariances and . The following lemma is proved in Section B.1:

Lemma A.1.

Let be a bivariate normal random vector satisfying and . Let and for . Define

Then, for all ,

As a result, for , and for , where is a constant that only depends on .

A.4 Proof of Proposition 2.1

A.5 Proof of Theorem 2.4

Fix . Using the Slutsky’s lemma, we only need to prove

| (67) |

Write for short . Let and , for and . Then, , , and

It follows that

| (68) | ||||

| (69) | ||||

| (70) |

Let . Below, we first derive the asymptotic normality of , then we use the delta method to prove (67).

First, we study the random vector . It is not hard to see that . By (6), , where are mutually indepependent and is the correlation matrix. Since when , the symmetry of implies that has a symmetric distribution. Hence, for an odd . For an even , by definition of in (7), ; also, ; combining them gives . It follows that

| (71) |

Moreover, . It follows that

| (72) |

By classical central limit theorem,

| (73) |

A.6 Proof of Theorem 3.1

Write for short and . It follows from Theorem 3.3 that . This implies . Hence, it suffices to show

| (75) |

First, we derive an expression of . Let and for all and . Then,

| (76) |

Let and . By direct calculations,

Define an event such that

| (77) |

It is not hard to see that the event holds with probability (see the proof of Theorem 2.1 for similar arguments). On the event , noting that , we have

It follows that

| (78) | ||||

| (79) | ||||

| (80) | ||||

| (81) |

Over the event , . As a result,

Plugging it into (76), we obtain

| (82) | ||||

| (83) | ||||

| (84) | ||||

| (85) |

Next, we bound and . Note that . This allows us to re-write

It is not hard to see that and that when has at least two distinct values (see the proof of Theorem 2.1 for similar arguments). As a result,

Moreover, noting that for , we have for that are mutually distinct. It follows that

Combining the above gives

| (86) |

Similarly, since , we re-write

Then, for , , and when has at least two distinct values. As a result,

We immediately have

| (87) |

Plugging (86)-(87) into (82) gives (75). The claim then follows.

A.7 Proof of Theorem 3.2

Similar to the proof of Theorem 2.1, let and denote the BAE with true and estimates ; here, may not be the sample mean and sample covariance matrix. By Theorem 3.3, . It follows from the Markov’s inequality that, for any , there is a constant such that, with probability ,

To show the claim, it suffices to show that, there is a constant such that with probability ,

| (88) |

We now show (88). Let and . Then,

By direct calculations,

| (89) | ||||

| (90) | ||||

| (91) | ||||

| (92) | ||||

| (93) |

As a result,

| (94) | ||||

| (95) | ||||

| (96) | ||||

| (97) | ||||

| (98) |

Introduce

Then, (94) can be rewritten as

| (99) | ||||

| (100) |

First, we study the main terms in (99). Note that is the sample covariance matrix of , and is the sample mean of . Using similar calculations as in the proof of Theorem 3.3, we can prove that

Combining it with the Markov inequality, for any , there is such that, with probability , and . On this event, the sum of the first two terms in (99) is bounded in absolute value by

| (101) | ||||

| (102) |

Next, we study the remainder terms in (99). By (89) and our assumption on , we have

It follows that . Then,

Using similar calculations as in the proof of Theorem 3.3, we can prove that , for all . It follows from the Markov inequality that, for a constant , with probability , , for all . On this event,

| (103) |

Combining (101) and (103) gives . This proves (88), and the claim follows immediately.

A.8 Proof of Theorem 3.3

Fix a collection of blocks. Write for short . For preparation, first, we verify that is an unbiased estimator. For any , by (12) and the fact that , we have

As a result,

| (104) |

In particular, it implies that

Therefore, is unbiased. Additionally, we have

| (105) |

Second, we introduce an alternative expression of . Consider the special case . Since in this case, we then have and . Hence, in (104), the left hand side equals to . At the same time, the right hand side is equal to . Equating the left/right hand sides gives

We combine it with the definition of and . It implies that

| (106) |

We now show the claim. For , let . By (105)-(106),

| (107) | ||||

| (108) | ||||

| (109) |

Consider . Combining (104) and (106), we have

| (110) |

Hence,

| (111) | ||||

| (112) | ||||

| (113) | ||||

| (114) |

where the last two lines are from Definition 3.1.

Consider . Fix and . Note that

We have had an expression of as in (110). We still need to get an expression of . For the set , we apply (12) and find that

where is a Beta distribution with parameters and . Let and be the vectors formed by the first coordinates and the last coordinates of , respectively. We then have and . As a result,

| (115) |

We then use the cross-moments of multivariate normal distributions to get the last term above. Let be a random variable independent of and . The random vector

It follows that

| (116) |

Write and . Note that

| (117) |

Combining (115) and (116) gives

| (118) |

We now combine (110) and (118) and note that and . It yields

As a result,

| (119) | ||||

| (120) |

We now plug (111) and (119) into (107). It gives

| (121) | ||||

| (122) |

What remains is to bound the last term. Since the random vectors and jointly follow a multivariate normal distribution as dictated in (117), we can apply the following lemma:

Lemma A.2.

Let and be two random vectors such that

Then, for a constant that only depends on but is independent of ,

Appendix B Supplementary proofs

B.1 Proof of Lemma A.1

Let . We then have and . Let be iid random variables. It is easy to see that

For notation simplicity, we omit the superscript in all equations. It follows that

Then,

Note that for random variables , when , and are mutually independent, . Plugging it into the above expression, we obtain

Using our previous notations, is the -th moment of . By elementary statistics, . Using this formula, we can prove . Hence,

At the same time, we note that and . It follows that

The claim then follows.

B.2 Proof of Lemma A.2

Suppose the rank of is . Let be the singular value decomposition of . We note that all singular values have an absolute value no larger than . For , let be such that form an orthogonal basis of . Define

It is easy to see that . Let , , and be mutually independent random variables. We claim that

This can be verified by computing the covariance matrix of the right hand side. We shall omit the superscript in all equations for notation simplicity. Write , corresponding to the first and the last coordinates, respectively, . It follows that

| (123) | ||||

| (124) | ||||

| (125) | ||||

| (126) |

where the third line is from the zero mean and mutual independence of and the last line is due to that and . Since are mutually independent, it follows that

| (127) | ||||

| (128) | ||||

| (129) |

It is not hard to see that . Hence, . Furthermore, since all entries of the diagonal matrix are between and , we have

where ’s and ’s are all standard normal variables. In particular,

Plugging these results into (127) gives

We note that is bounded, but can grow with . Note that for all . As a result,

Therefore,

| (130) |

Noticing that is a diagonal matrix containing the singular values of , we have proved the claim.

Appendix C The case of multivariate Gaussian distributions

We present a corollary about the errors of MAE and BAE for the special case of multivariate Gaussian distributions. Here . The proof is elementary and omitted.

Corollary C.1.

Let be i.i.d. samples of . For a constant integer , we assume the blocks in BAE are , .

-

•

Suppose . Then, , , and .

-

•

Suppose is a block-wise diagonal matrix with blocks, where each block has diagonals and off-diagonals . Let in BAE. Then, , , and .

Appendix D Simulations for the estimator in Section 5

We conducted simulations to investigate the performance of the estimator of realized in Section 5.

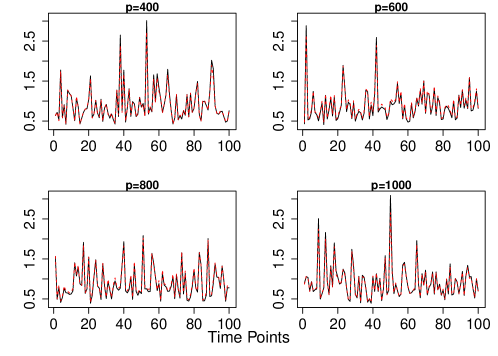

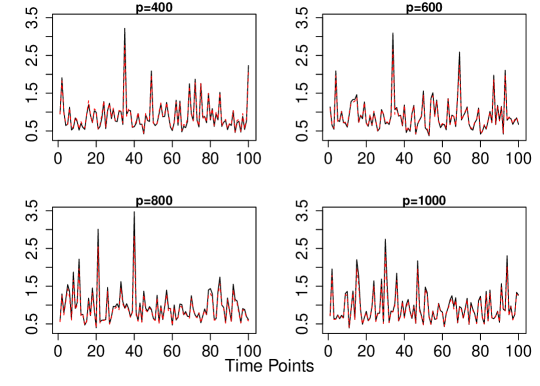

In the first experiment, we generate iid from model (1) with a constant covariance matrix . The covariance is set to be , which is approximately banded. We fix and let varies. The results are displayed in Figure 9, where we study both cases of multivariate Gaussian data and multivariate data. We see that the estimated values are very close to the true values in all the cases.

In the second experiment, we generate data using the calibrated covariance matrix from S&P500 stock returns as in Section 4. In this case, the covariance matrix is heavily non-sparse, however, our estimator still works very well, no matter for Gaussian data or heavy-tailed data with multivariate -distributions.