Selection mechanisms affect volatility in evolving markets

Abstract.

Financial asset markets are sociotechnical systems whose constituent agents are subject to evolutionary pressure as unprofitable agents exit the marketplace and more profitable agents continue to trade assets. Using a population of evolving zero-intelligence agents and a frequent batch auction price-discovery mechanism as substrate, we analyze the role played by evolutionary selection mechanisms in determining macro-observable market statistics. Specifically, we show that selection mechanisms incorporating a local fitness-proportionate component are associated with high correlation between a micro, risk-aversion parameter and a commonly-used macro-volatility statistic, while a purely quantile-based selection mechanism shows significantly less correlation and is associated with higher absolute levels of fitness (profit) than other selection mechanisms. These results point the way to a possible restructuring of market incentives toward reduction in market-wide worst performance, leading profit-driven agents to behave in ways that are associated with beneficial macro-level outcomes.

1. Introduction

The concept of adaptive financial markets has been studied extensively in quantitative finance for nearly twenty years. The efficient markets hypothesis (EMH), which in its weakest form states that the price of an asset should, under conditions including costless information and agents with rational expectations about the future, reflect all publicly-available past information, has been an influential starting point for the study of financial theory since its initial publication in the late 1960s (Malkiel and Fama, 1970). However, there is empirical evidence that this hypothesis does not hold. A well-documented momentum effect exists for asset prices: assets that have done well (poorly) in past time periods will tend to do well (poorly) in future time periods, for periods ranging up to a year in the future (Jegadeesh and Titman, 1993). In addition, there have been objections to the rational expectations assumption of EMH on a theoretical basis (Lo, 2004, 2005; Kim et al., 2011). Critics of the EMH have proposed a so-called “adaptive-markets hypothesis” (AMH), in the framework of which the population of agents is in constant flux, adapting to changing market forces and subject to evolutionary pressure (Farmer and Lo, 1999). The rise of high-frequency trading (HFT) in response to a shift in the regulatory environment in U.S. asset markets in the mid-2000s is one factor that has lent credence to the AMH theory (Johnson et al., 2012; Smith, 2010; Menkveld, 2013).

As a result of the apparent adaptive nature of modern financial markets, there has been substantial application of agent-based model (ABM) methods to model various market features of interest (LeBaron, 2000; Savit et al., 1999; Hommes, 2002). Such models often assume constant a particular selection mechanism by which agents of low fitness (usually, low profitability) are selected out of the market and agents of higher fitness remain (Zhang, 1998; Kinoshita et al., 2013; Hommes and Wagener, 2009). However, the design of the selection mechanism may have a material effect on measurable quantities in the marketplace, such as price or return time series, preferences (parameters) of high-fitness agents, and volatility.

In this work, we analyze the role of various selection mechanisms in determining the preferences of a population of evolving zero-intelligence agents interacting through the means of an auction mechanism. Comparing two fundamentally distinct mechanisms—one a global mechanism based on population profit quantiles and the other a local mechanism based on sample profitability—we show that this choice not only affects the dynamic behavior and distribution of agent parameters as shown in Figures 2 and 3, but also has a significant effect on micro-macro volatility correlations. We find that incorporating local fitness-proportionate selection greatly increases the correlation between a micro-level, risk aversion parameter and macro-level volatility as measured by standard financial econometric machinery, compared to purely quantile-based selection.

2. Theory and simulation

We focus our attention on the mechanism by which agents of low fitness—unprofitable agents— are selected out of the market. In real-world financial markets, agents whose trading strategies produce low returns on capital can experience an outflow of funds to agents whose strategies produce better returns as investors seek the highest possible return subject to their risk preferences. In a world of perfect information, firms would thus be selected out of a market according to a type of fitness-proportionate selection. Real financial markets—and markets of all kinds—are rife with information asymmetries (Akerlof, 1978; Kim and Verrecchia, 1991); here, we focus on the situation of perfect information to highlight the importance of the selection mechanism on macro-level observables.

2.1. Agent specification

Agent ’s fitness function at time is given by its profit at that time, defined as

| (1) |

where and are the amount of cash held by agent (units of currency), and number of shares of the asset held by agent , respectively, and is the price of the asset. Agents are permitted to “sell short”: they are not restricted to have a non-negative amount of cash. Agents are zero-intelligence (Gode and Sunder, 1993; Farmer et al., 2005) in the sense that their actions are purely random given a set of parameters; agents do not adapt in our model but are subject to evolutionary pressure across generations. The behavior of an agent is determined by three parameters: , the probability of submitting a bid order in a time period given that the agent trades in that time period; , the mean number of shares submitted by the agent in a time period; and , the so-called “volatility preference” of the agent, the role of which we will describe presently. Given the asset price at time , , the agent submits a bid order with probability (equivalently, an ask order with probability ) with number of shares distributed as and price distributed according to the random variable

| (2) |

where . The volatility preference parameter thus encodes a measure of regard for the current price level : low implies a preference for the current price level, while larger values lead to larger moves in both positive and negative directions. This parameter is interpreted as a measure of risk aversion (small ) or risk neutrality / risk seeking (large ).

2.2. Price-discovery mechanism

Market price is determined by a frequent batch auction (FBA), introduced by Budish et al. as a response to HFT strategies (Budish et al., 2015, 2014), which we now describe briefly. Modern financial markets primarily use a continuous double auction (CDA) mechanism to match buyers and sellers, though FBA has recently attracted much theoretical and intellectual property interest (Cushing, 2013; Wah et al., 2016), and batch auctions more generally have been in use since at least 2001 on the Paris Bourse (Muscarella and Piwowar, 2001). CDA and FBA share several attributes. Both mechanisms are double-sided mechanisms in which any number of buyers and sellers may participate, and participants may enter or leave the market at any time under both mechanisms. Both mechanisms also maintain an order book, which accumulates orders that have not yet been executed. In practice, both mechanisms feature a similar price-time execution priority for resting orders, though the implementation may vary slightly. In other words, orders that have a better price, bids with higher prices or asks with lower prices, are executed first. Ties in price are broken by the age of the order, with older orders executing first.

CDAs allow agents to submit orders at any time, and these orders are immediately matched against resting orders if possible. Orders that are not immediately executed will be added to the order book, where they will wait for a counter-party to accept their conditions. This procedure results in trading that occurs continuously, aligning with the name of the mechanism. On the other hand, FBAs divide trading into discrete intervals. Within each interval agents may submit orders at any time, which are then placed in the order book. At the end of a trading interval, a single uniform execution price is selected by locating the intersection of the supply and demand curves (i.e. price and quantity of orders from both sides of the market are used to identify the execution price). Orders to buy with a limit price at least as high as the selected execution price and orders to sell with a limit price at least as low as the selected execution price are then eligible to execute. Eligible orders are then matched together following price-time priority, i.e. bids with higher prices and asks with lower prices are matched first, with ties broken by order age, and further ties broken by uniform random selection. The orders that did not execute at time remain in the book and are reconsidered for execution in future time periods until such time as the matching engine considers them to be “stale”, or too old for consideration. The implementation of FBA considered here sets the maximum allowed time for an order to remain in the book to be 24 time periods, or one day.

Since the aim of this work is to understand the effects of selection pressure and different selection mechanisms on macro-statistics of market activity, we attempt to abstract away other details of real-world asset markets. Though the U.S. National Market System (NMS) is a fragmented market with no fewer than thirteen exchanges operating at time of writing (O’Hara and Ye, 2011), we consider only a single exchange and matching engine here. As noted above, agents are effectively zero-intelligence; though they are subject to selective pressure and thus the population of agents may become more profitable over time as weak agents are selected out, individual agents do not adapt to changing market circumstances.

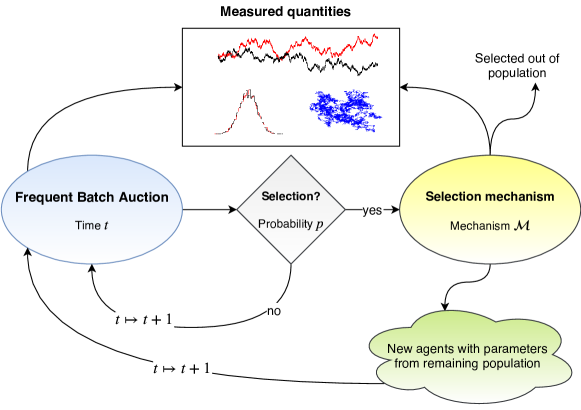

2.3. Selection mechanisms

Selection occurs with constant probability of each time period, so that there is a selection event in one out of every 24 time periods (hours) on average. We consider three selection mechanisms: a quantile-based mechanism (truncation selection), denoted by ; a type of fitness-proportionate selection, , and a mixture of the two mechanisms, , each of which is a well-known selection method (Blickle and Thiele, 1996). The quantile-based mechanism removes agents whose profit satisfies , where is a quantile (number between 0 and 1) and is the quantile function of the profit distribution across all agents active at time . We set to remove the bottom 10% of agents each time the quantile-based mechanism is activated. The fitness-proportional selection mechanism is a standard implementation of such a procedure: a random sample of agents is selected from the population and each is kept in the population with probability given by . We set in this implementation. The mixed selection mechanism interpolates between and . When a selection event occurs, with probability the mechanism is used and with probability , is used.

When agents are selected out of the population, new agents are added to replace the ones that have exited so that the number of agents in the population is conserved. We set the number of agents in each run of the simulation. When new agents enter the model after a selection event, with probability they draw their governing parameters (, , and ) from stationary probability distributions that do not change with selective pressure, and with probability they draw their governing parameters from the distributions of these parameters among the members of the population of agents that did not get selected out of the market. In this work, we set . We choose these selection mechanisms not because they are in some way optimal methods for selecting individuals in an evolving system—in fact, the disadvantages of fitness-proportionate selection are well-documented (Whitley et al., 1989)—but for their interpretation in the context of a financial market. The quantile-based method models an environment in which an investing public (individuals, firms, etc.) actively avoid firms that are performing badly in the market, but do not actively seek out firms whose profits are the highest. In contrast, a fitness-proportionate scheme models a scenario in which investors seek out the firms that have the highest total profits and allocate their funds to these firms in proportion to their past performance. We also included a control simulation model in which no selection was present and all agents initially in the simulation at time remained in the simulation for the entire time.

2.4. Theoretical models

We turn briefly to a theoretical model of the evolution of agents’ parameters: , , and . For the sake of convenience we pass to a continuous time description, though the discrete time of the simulation is recovered by simply setting . We assume that prices evolve according to a zero-mean Lévy flight,

| (3) |

with tail exponent as suggested by Mandelbrot (Mandelbrot, 1997). This model has been shown to give superior fit to real data when compared with the geometric Brownian motion model of asset prices (Mantegna and Stanley, 1997; Cont et al., 1997). Since any agent whose bid probability deviates too far from the natural equilibrium of will soon become rapidly unprofitable and hence be selected out of the market, we assume evolves according to a type of Ornstein-Uhlenbeck process,

| (4) |

In contrast, there is no logical steady state for , so we assume that its evolution is governed by a standard random walk with heavy-tailed increments arising from the auction mechanism,

| (5) |

The parameter is interpreted as evolutionary drift. The interpretation of volatility preference as a measure of risk aversion (small ) or risk neutrality / seeking (large ) gives insight into a possible model for its evolution. Simply put, volatility preference increments in proportion to the current level of volatility preference: if the population is risk averse, the variation in volatility preference should be low; if the population is risk neutral or risk-seeking, the variation in volatility preference will likely be high. Incorporating an evolutionary drift term, a reasonable model for this phenomenon is

| (6) |

For example, orders submitted according to Eq. 2 with much larger than the population average are unlikely to be executed if the resultant price is favorable to the submitting agent (i.e., very high ask price or very low bid price relative to the last equilibrium price) and will result in a large financial loss to the agent if the resultant price is likely to be executed (i.e., very high bid price or very low ask price).

2.5. Methodology

We seek an understanding of the effects of the selection mechanism on micro- and macro-market statistics.

Are there cross-mechanism differences between optimal parameter combinations, or, more fundamentally, is there a steady-state optimal parameter combination at all? How do the time series of parameters—which, in a real financial market, would be unobservable—affect macro-observable quantities such as leptokurticity of returns or volatility? To answer these questions, we first characterize basic macro properties of the simulations under each selection mechanism. Aside from the price and return time series, we calculate the price power spectral density, defined by , where we have defined the Fourier transform on the interval by

| (7) |

where , so that the units of the Fourier transform are . For financial price time series we expect , where .

Brownian motion has , while real asset markets exhibit in price dynamics (Mandelbrot, 1997; Carbone et al., 2004). Time series of the parameters , , and are described and their distributions are fit and compared with distributions predicted from the theoretical models described above. Finally, we analyze the link between the agent-level micro-volatility parameters and macro-volatility as measured from price or return time series and remark on its differentiation by selection mechanism.

3. Results

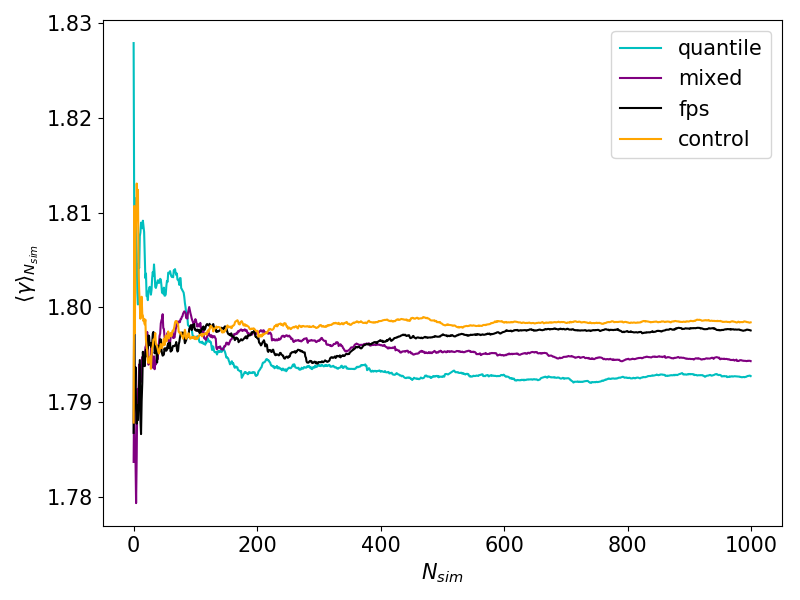

We ran 1000 runs of the artificial asset market simulation for each selection mechanism (control, , , and ) for a total of 4000 simulations. Each simulation was composed of 24 “hour” trading periods in each trading “day”. A total of 252 trading days per year (in analogy with the calendar of the U.S. national market system) resulted in a total of 6048 trading periods per simulation. The number of agents in each simulation was held constant at 100. To determine that the number of runs of the simulation was adequate for the calculation of population averages, we generated reruns of the simulation until temporal averages of the population price time series power spectral density exponents appeared to converge. This convergence is displayed in Figure 4.

3.1. Profitability and parameter evolution

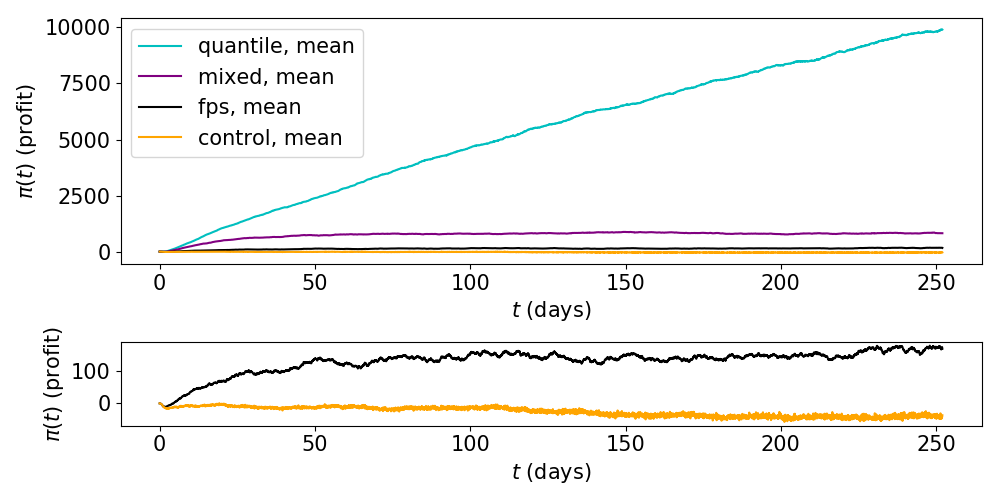

The mean profitability of agents under each selection mechanism is displayed in Figure 5. Here, we define an average over both runs of the simulation and active agents, viz.

| (8) |

The purely quantile-based mechanism displays average profitability that is over an order of magnitude greater than either or , while was still much more profitable on average than was . This differentiation is likely to due to the fact that selects out the ten worst-performing individuals each time it is active, while selects out on average individuals that are randomly sampled from the population; while the individuals selected out are, on average, the worst performing individuals in that particular , they are by no means the worst-performing individuals in the entire population. Though this implementation of results in significantly less selective pressure on the population than does , this choice is made to hold constant the number of individual agents involved in the selection step of the market simulation.

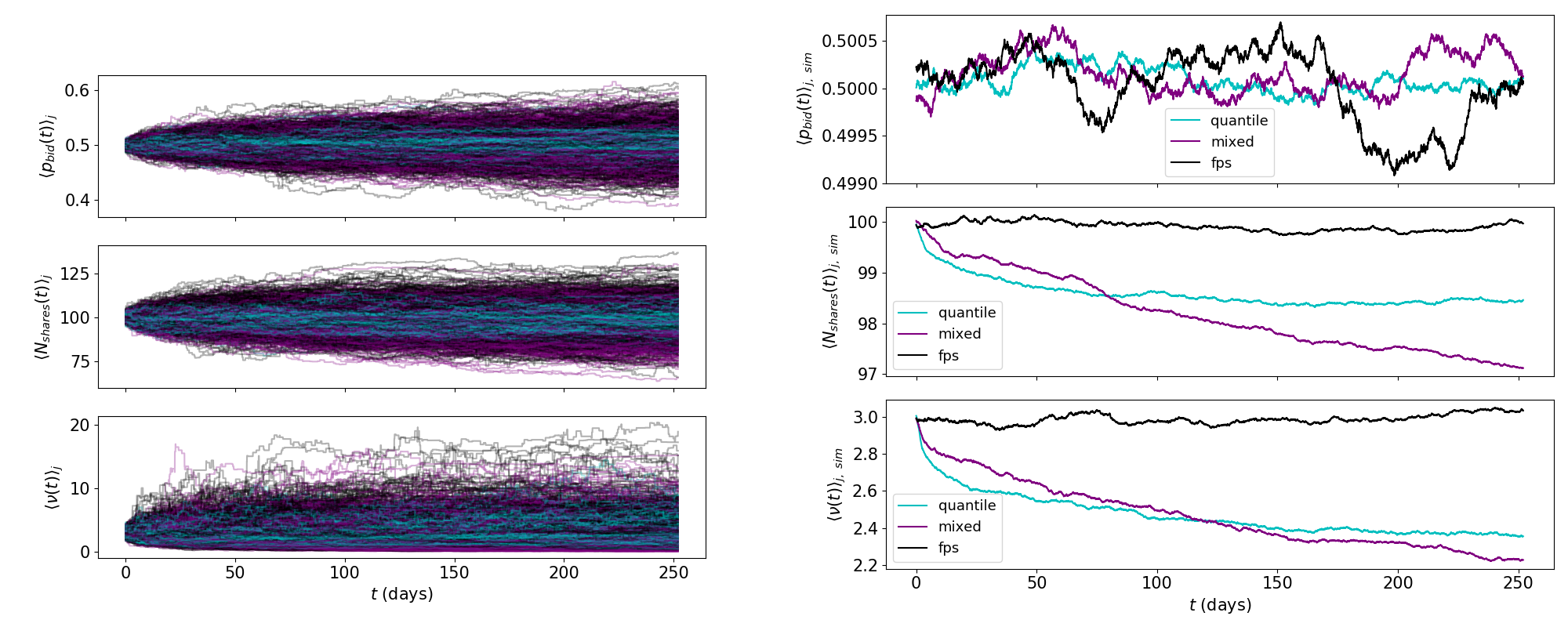

Agents’ parameters—the probability of submitting a bid, , the mean number of shares submitted in an order , and the volatility preference —were influenced by the choice of selection mechanism. Overall, was associated with lower standard deviations of parameter time series as calculated over runs of the simulation. Figure 2 displays parameter time series for all runs of the simulation in the left panel, and averages over runs of the simulation in the right panel. Both and showed time decay toward lower values in and when averaged over both active agents and runs of the simulation. On the contrary, showed no decay in either parameter when the same average was performed. When decoupled from time, distributions of the parameters showed remarkable similarity across mechanisms, showing evidence for a unified underlying evolutionary model as proposed in Eqs. 4 - 6, the parameters of which depend on the selection mechanism. These time-decoupled distributions are displayed in Figure 3.

3.2. Volatility correlation

Since it seems reasonable that a fitness-proportionate selection mechanism most closely approximates the selection mechanism operating in today’s financial asset markets, we are particularly interested in correlations between micro-volatility—agents’ volatility preferences —and macro measures of volatility. We are interested in the effects of mechanism on these macro measures of volatility, and particularly wish to test if micro-volatility is correlated with macro-volatility in the cases of and , as this could provide some insight into how volatility is generated in real financial markets.

Macro-volatility—volatility as measured from market-wide statistics such as price and returns—is often modeled using a generalized autoregressive conditional heteroskedasticity (GARCH) model (Bollerslev, 1986), which, in its most basic form, hypothesizes that log returns can be decomposed as

| (9) | ||||

| (10) | ||||

| (11) |

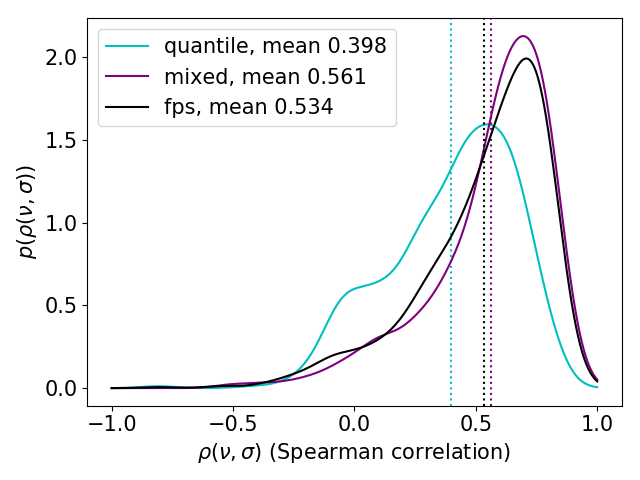

where . For each simulation, we compute a GARCH model of the form given above and calculate the Spearman correlation coefficient between the average agent volatility preference and the fitted volatility . Figure 6 displays and for an arbitrarily chosen run of the simulation. Figure 7 displays the empirical probability density function (pdf) of across all non-control simulations. (The pdf of correlations for the control is sharply peaked about zero and uninteresting as there is no evolution of in this case.) The pdf of correlation coefficients for is bimodal, with one mode about zero and another near , while for and the pdfs are are peaked near with a long left tail.

3.3. Theoretical fit

Since the theoretical models for the evolution of agents’ parameters given by Eqs. 4 - 6 contain nine free parameters in total, to assess their suitability as a first-order theoretical model of the evolutionary phenomena occurring here we must fit these parameters from the data generated by the agent-based model.

To do this we hypothesize a parametric form for each distribution: , , and . The optimal values of are defined as the vector that minimizes

| (12) |

the Kullback-Leibler (KL) divergence of the theoretical distribution away from the distribution produced by the ABM. The domain of integration is defined as all observed values of the quantity for each time step and each run of the simulation. This integral is minimized using differential evolution (Storn and Price, 1997), at each iteration of which a number of simulations of the theoretical model Eqs. 4 - 6 are calculated and the maximum likelihood estimation of the parameter vector is found, which is then substituted into the functional form of used in the definition of KL divergence.

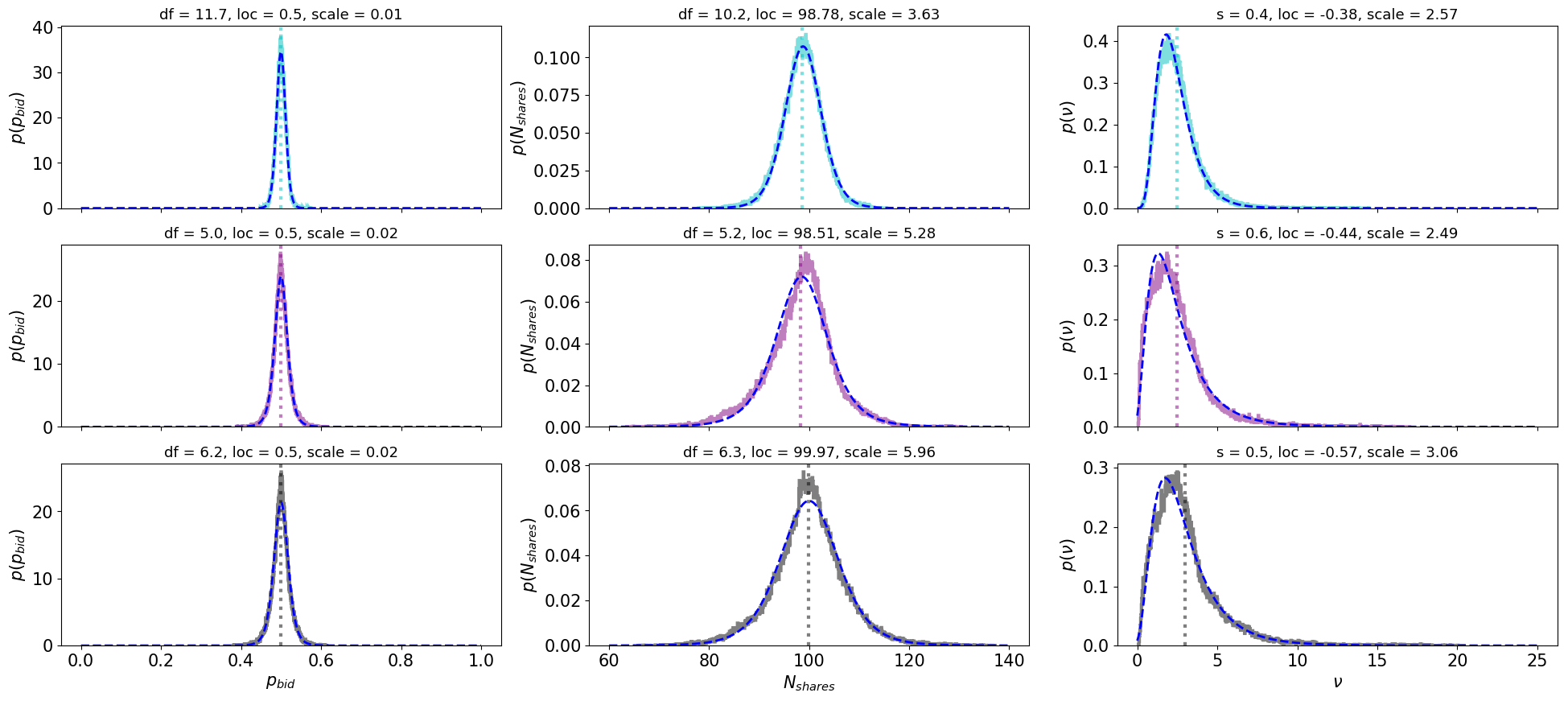

Figure 8 displays comparisons between the fitted theoretical distributions and distributions arising from the ABM for . To emphasize that the restriction of the fit distribution to a parameterized form does not result in a model that fits the data poorly, random variates drawn from each model are drawn and their histogram is plotted along with the fit distributions. The calculated optimal values of the free parameters for each model are displayed in the title of each panel. There is strong restorative force () to the equilibrium bid probability , while there is negative evolutionary drift in mean number of shares submitted per order () and volatility preference ().

4. Discussion and conclusion

We find that choice of selection mechanism is associated with differential behavior of asset price spectra, agent parameter distributions and time series, and volatility. While the probability of submitting a bid order fluctuates regularly about its natural equilibrium value of under all three mechanisms, the time series of the average number of shares traded and the volatility preference parameter varies functionally depending on the presence of a quantile-based component to the selection mechanism. When a quantile-based component is not present (), these time series vary in the mean case very little from their initial values, with a slight upward trend. However, when a quantile-based component is present, in the mean case these series exhibit a steady trend toward lower values. In both and , trends most strongly toward lower values and does not appear to converge in the time period covered by our simulation (252 days of trading once per hour), suggesting that longer simulation run times are necessary to discern the nature of the steady state of these parameters under mechanisms containing a quantile-based component, if such steady-states exist.

All three mechanisms show significant correlation between micro-volatility, as measured by the risk-aversion / volatility preference parameter , and market-wide volatility measured from the market price using standard econometric models (GARCH). All distributions of Pearson correlation coefficients of micro- and macro-volatility exhibited negative skew (more weight in the left-hand tail). The quantile-based mechanism displayed bimodality in this distribution, with a small peak near zero correlation and a large peak near . Contrasting with this, and were unimodal, with peaks near , displaying a strong median correlation between micro- and macro-volatility.

Taken together, these results paint a picture of nontrivial interaction between selection mechanism and market outcomes. Mechanisms that include a fitness-proportionate component show higher volatility than a purely quantile-based mechanism, and under those mechanisms micro-volatility is more highly correlated with observable macro-volatility, providing a possible mechanistic explanation for the generation of macro-volatility in real financial markets. However, mechanisms that contain a quantile-based component show significant evolutionary drift in the average number of shares submitted per order and in volatility preference. When taken along with the fact that these mechanisms produced far higher average profits than did the purely fitness-proportionate method, this suggests that lower values of these parameters are—in a population of zero-intelligence agents, at least—associated with higher average profit levels, possibly due to an increase in risk-aversion among the population of agents and a corresponding decrease in the frequency of agents that experience massive trading losses.

Our study has several areas on which future work could improve, the most important of which being our neglection of other selection mechanisms. There are far more—and more realistic!—mechanisms that provide a model for how agents may be removed from, and added to, a financial market. Drawing definitive conclusions about the nature of market selection and competition from a study of only two fundamental mechanisms is ill-advised, and we decline to do this. Another shortcoming is our lack of variation of many parameters in this study. In order to understand these mechanisms in more depth, a detailed study of macro-observable market statistics as a function of, e.g., tournament size, quantile, and mixture probability between the two fundamental mechanisms is required. Future work should focus on inclusion of more and different selection mechanisms, as well as inclusion of more advanced agents.

Acknowledgements.

The authors are grateful for helpful conversations with Laurent Hébert-Dufresne, Tyler John Gray, Brian F. Tivnan, Peter Sheridan Dodds, Chris Danforth, John Henry Ring IV, Sage Hahn, and Josh Bongard, and thankful for the insightful comments provided by three anonymous referees.References

- (1)

- Akerlof (1978) George A Akerlof. 1978. The market for “lemons”: Quality uncertainty and the market mechanism. In Uncertainty in Economics. Elsevier, 235–251.

- Blickle and Thiele (1996) Tobias Blickle and Lothar Thiele. 1996. A comparison of selection schemes used in evolutionary algorithms. Evolutionary Computation 4, 4 (1996), 361–394.

- Bollerslev (1986) Tim Bollerslev. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of econometrics 31, 3 (1986), 307–327.

- Budish et al. (2014) Eric Budish, Peter Cramton, and John Shim. 2014. Implementation details for frequent batch auctions: Slowing down markets to the blink of an eye. American Economic Review 104, 5 (2014), 418–24.

- Budish et al. (2015) Eric Budish, Peter Cramton, and John Shim. 2015. The high-frequency trading arms race: Frequent batch auctions as a market design response. The Quarterly Journal of Economics 130, 4 (2015), 1547–1621.

- Carbone et al. (2004) Anna Carbone, Giuliano Castelli, and H Eugene Stanley. 2004. Time-dependent Hurst exponent in financial time series. Physica A: Statistical Mechanics and its Applications 344, 1-2 (2004), 267–271.

- Cont et al. (1997) Rama Cont, Marc Potters, and Jean-Philippe Bouchaud. 1997. Scaling in stock market data: stable laws and beyond. In Scale invariance and beyond. Springer, 75–85.

- Cushing (2013) David Cushing. 2013. Automated batch auctions in conjunction with continuous financial markets. US Patent 8,533,100.

- Farmer and Lo (1999) J Doyne Farmer and Andrew W Lo. 1999. Frontiers of finance: Evolution and efficient markets. Proceedings of the National Academy of Sciences 96, 18 (1999), 9991–9992.

- Farmer et al. (2005) J Doyne Farmer, Paolo Patelli, and Ilija I Zovko. 2005. The predictive power of zero intelligence in financial markets. Proceedings of the National Academy of Sciences 102, 6 (2005), 2254–2259.

- Gode and Sunder (1993) Dhananjay K Gode and Shyam Sunder. 1993. Allocative efficiency of markets with zero-intelligence traders: Market as a partial substitute for individual rationality. Journal of political economy 101, 1 (1993), 119–137.

- Hommes and Wagener (2009) Cars Hommes and Florian Wagener. 2009. Complex evolutionary systems in behavioral finance. In Handbook of financial markets: Dynamics and evolution. Elsevier, 217–276.

- Hommes (2002) Cars H Hommes. 2002. Modeling the stylized facts in finance through simple nonlinear adaptive systems. Proceedings of the National Academy of Sciences 99, suppl 3 (2002), 7221–7228.

- Jegadeesh and Titman (1993) Narasimhan Jegadeesh and Sheridan Titman. 1993. Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of finance 48, 1 (1993), 65–91.

- Johnson et al. (2012) Neil Johnson, Guannan Zhao, Eric Hunsader, Jing Meng, Amith Ravindar, Spencer Carran, and Brian Tivnan. 2012. Financial black swans driven by ultrafast machine ecology. arXiv preprint arXiv:1202.1448 (2012).

- Kim et al. (2011) Jae H Kim, Abul Shamsuddin, and Kian-Ping Lim. 2011. Stock return predictability and the adaptive markets hypothesis: Evidence from century-long US data. Journal of Empirical Finance 18, 5 (2011), 868–879.

- Kim and Verrecchia (1991) Oliver Kim and Robert E Verrecchia. 1991. Market reaction to anticipated announcements. Journal of Financial Economics 30, 2 (1991), 273–309.

- Kinoshita et al. (2013) Kanta Kinoshita, Kyoko Suzuki, and Tetsuya Shimokawa. 2013. Evolutionary foundation of bounded rationality in a financial market. IEEE Transactions on Evolutionary Computation 17, 4 (2013), 528–544.

- LeBaron (2000) Blake LeBaron. 2000. Agent-based computational finance: Suggested readings and early research. Journal of Economic Dynamics and Control 24, 5-7 (2000), 679–702.

- Lo (2004) Andrew W Lo. 2004. The adaptive markets hypothesis: Market efficiency from an evolutionary perspective. (2004).

- Lo (2005) Andrew W Lo. 2005. Reconciling efficient markets with behavioral finance: the adaptive markets hypothesis. (2005).

- Malkiel and Fama (1970) Burton G Malkiel and Eugene F Fama. 1970. Efficient capital markets: A review of theory and empirical work. The journal of Finance 25, 2 (1970), 383–417.

- Mandelbrot (1997) Benoit B Mandelbrot. 1997. The variation of certain speculative prices. In Fractals and scaling in finance. Springer, 371–418.

- Mantegna and Stanley (1997) Rosario N Mantegna and H Eugene Stanley. 1997. Econophysics: Scaling and its breakdown in finance. Journal of statistical Physics 89, 1-2 (1997), 469–479.

- Menkveld (2013) Albert J Menkveld. 2013. High frequency trading and the new market makers. Journal of Financial Markets 16, 4 (2013), 712–740.

- Muscarella and Piwowar (2001) Chris J Muscarella and Michael S Piwowar. 2001. Market microstructure and securities values:: Evidence from the Paris Bourse. Journal of Financial Markets 4, 3 (2001), 209–229.

- O’Hara and Ye (2011) Maureen O’Hara and Mao Ye. 2011. Is market fragmentation harming market quality? Journal of Financial Economics 100, 3 (2011), 459–474.

- Savit et al. (1999) Robert Savit, Radu Manuca, and Rick Riolo. 1999. Adaptive competition, market efficiency, and phase transitions. Physical Review Letters 82, 10 (1999), 2203.

- Smith (2010) Reginald Smith. 2010. Is high-frequency trading inducing changes in market microstructure and dynamics? (2010).

- Storn and Price (1997) Rainer Storn and Kenneth Price. 1997. Differential evolution–a simple and efficient heuristic for global optimization over continuous spaces. Journal of global optimization 11, 4 (1997), 341–359.

- Wah et al. (2016) Elaine Wah, Dylan Hurd, and Michael P Wellman. 2016. Strategic Market Choice: Frequent Call Markets vs. Continuous Double Auctions for Fast and Slow Traders. EAI Endorsed Trans. Serious Games 3, 10 (2016), e1.

- Whitley et al. (1989) L Darrell Whitley et al. 1989. The GENITOR Algorithm and Selection Pressure: Why Rank-Based Allocation of Reproductive Trials is Best.. In ICGA, Vol. 89. Fairfax, VA, 116–123.

- Zhang (1998) Yi-Cheng Zhang. 1998. Modeling market mechanism with evolutionary games. arXiv preprint cond-mat/9803308 (1998).