Stagewise Training Accelerates Convergence of Testing Error Over SGD

Abstract

Stagewise training strategy is widely used for learning neural networks, which runs a stochastic algorithm (e.g., SGD) starting with a relatively large step size (aka learning rate) and geometrically decreasing the step size after a number of iterations. It has been observed that the stagewise SGD has much faster convergence than the vanilla SGD with a polynomially decaying step size in terms of both training error and testing error. But how to explain this phenomenon has been largely ignored by existing studies. This paper provides some theoretical evidence for explaining this faster convergence. In particular, we consider a stagewise training strategy for minimizing empirical risk that satisfies the Polyak-Łojasiewicz (PL) condition, which has been observed/proved for neural networks and also holds for a broad family of convex functions. For convex loss functions and two classes of “nice-behaviored" non-convex objectives that are close to a convex function, we establish faster convergence of stagewise training than the vanilla SGD under the PL condition on both training error and testing error. Experiments on stagewise learning of deep residual networks exhibits that it satisfies one type of non-convexity assumption and therefore can be explained by our theory. Of independent interest, the testing error bounds for the considered non-convex loss functions are dimensionality and norm independent.

First version: December 8, 2018

Revised version: February 2, 2019

1 Introduction

In this paper, we consider learning a predictive model by using a stochastic algorithm to minimize the expected risk via solving the following empirical risk problem:

| (1) |

where is a smooth loss function of the model on the data , is a closed convex set, and denotes a set of observed data points that are sampled from an underlying distribution with support on .

There are tremendous studies devoted to solving this empirical risk minimization (ERM) problem in machine learning and related fields. Among all existing algorithms, stochastic gradient descent (SGD) is probably the simplest and attracts most attention, which takes the following update:

| (2) |

where is randomly sampled, is the projection operator, and is the step size that is usually decreasing to . Convergence theories have been extensively studied for SGD with a polynomially decaying step size (e.g., , ) for an objective that satisfies various assumptions, e.g., convexity (Nemirovski et al., 2009), non-convexity (Ghadimi and Lan, 2013), strong convexity (Hazan et al., 2007), local strong convexity (Qu et al., 2016), Polyak-Łojasiewicz inequality (Karimi et al., 2016), Kurdyka-Łojasiewicz inequality (Xu et al., 2017), etc. The list of papers about SGD is so long that can not be exhausted here.

The success of deep learning is mostly driven by stochastic algorithms as simple as SGD running on big data sets (Krizhevsky et al., 2012; He et al., 2016). However, an interesting phenomenon that can be observed in practice for deep learning is that no one is actually using the vanilla SGD with a polynomially decaying step size that is well studied in theory for non-convex optimization (Karimi et al., 2016; Ghadimi and Lan, 2013; Davis and Drusvyatskiy, 2018). Instead, a common trick used to speed up the convergence of SGD is by using a stagewise step size strategy, i.e., starting from a relatively large step size and decreasing it geometrically after a number of iterations (Krizhevsky et al., 2012; He et al., 2016). Not only the convergence of training error is accelerated but also is the convergence of testing error. However, there is still a lack of theory for explaining this phenomenon. Although a stagewise step size strategy has been considered in some studies (Hazan and Kale, 2011; Xu et al., 2017; Karimi et al., 2016; Kleinberg et al., 2018; Chen et al., 2018), none of them explains the benefit of stagewise training used in practice compared with standard SGD with a decreasing step size, especially on the convergence of testing error for non-convex problems.

1.1 Our Contributions

This paper aims to provide some theoretical evidence to show that an appropriate stagewise training algorithm can have faster convergence than SGD with a polynomially deccaying step size under some condition. In particular, we analyze a stagewise training algorithm under the Polyak-Łojasiewicz condition (Polyak, 1963):

This property has been recently observed/proved for learning deep and shallow neural networks (Hardt and Ma, 2016; Xie et al., 2016; Li and Yuan, 2017; Zhou and Liang, 2017; Charles and Papailiopoulos, 2018), and it also holds for a broad family of convex functions (Xu et al., 2017). We will focus on the scenario that is a small positive value and is large, which corresponds to ill-conditioned big data problems and is indeed the case for many problems (Hardt and Ma, 2016; Charles and Papailiopoulos, 2018). We compare with two popular vanilla SGD variants with or step size scheme for both the convex loss and two classes of non-convex objectives that are close to a convex function. We show that the considered stagewise training algorithm has a better dependence on than the vanilla SGD with step size scheme for both the training error (under the same number of iterations) and the testing error (under the same number of data and a less number of iterations), while keeping the same dependence on the number of data for the testing error bound. Additionally, it has faster convergence and a smaller testing error bound than the vanilla SGD with step size scheme for big data.

To be fair for comparison between two algorithms, we adopt a unified approach that considers both the optimization error and the generalization error, which together with algorithm-independent optimal empirical risk constitute the testing error. In addition, we use the same tool for analysis of the generalization error - a key component in the testing error. We would like to point out that the techniques for us to prove the convergence of optimization error and testing error are simple and standard. In particular, the optimization error analysis is built on existing convergence analysis for solving convex problems, and the testing error analysis is built on the uniform stability analysis of a stochastic algorithm introduced by Hardt et al. (2016). It is of great interest to us that simple analysis of the widely used learning strategy can possibly explain its greater success in practice than using the standard SGD method with a decaying step size.

Besides theoretical contributions, the considered algorithm also has additional features that come with theoretical guarantee for the considered non-convex problems and help improve the generalization performance, including allowing for explicit algorithmic regularization at each stage, using an averaged solution for restarting, and returning the last stagewise solution as the final solution. It is also notable that the widely used stagewise SGD is covered by the proposed framework. We refer to the considered algorithm as stagewise regularized training algorithm or Start.

1.2 Other related works assuming PL conditions

It is notable that many papers have proposed and analyzed deterministic/stochastic optimization algorithms under the PL condition, e.g., (Karimi et al., 2016; Lei et al., 2017; Reddi et al., 2016; Bassily et al., 2018). This list could be long if we consider its equivalent condition in the convex case. However, none of them exhibits the benefit of stagewise learning strategy used in practice. One may also notice that linear convergence for the optimization error was proved for a stochastic variance reduction gradient method (Reddi et al., 2016). Nevertheless, its uniform stability bound remains unclear for making a fair comparison with the considered algorithms in this paper, and variance reduction method is not widely used for deep learning.

We also notice that some recent studies (Kuzborskij and Lampert, 2018; Zhou et al., 2018; Charles and Papailiopoulos, 2018) have used other techniques (e.g., data-dependent bound, average stability, point-wise stability) to analyze the generalization error of a stochastic algorithm. Nevertheless, we believe similar techniques can be also used for analyzing stagewise learning algorithm, which is beyond the scope of this paper. Among these studies, Zhou et al. (2018); Charles and Papailiopoulos (2018) have analyzed the generalization error (or stability) of stochastic algorithms (e.g., the vanilla SGD with a decreasing step size or small constant step size) under the PL condition and other conditions. We emphasize that their results are not directly comparable to the results presented in this work. In particular, Zhou et al. (2018) considered the generalization error of SGD with a decreasing step size in the form with and being smoothness parameter, which corresponds to a good conditioned setting 111this could never happen in unconstrained optimization where (Nesterov, 2004)[Theorem 2.1.5]. Together with the PL condition, it implies .. Charles and Papailiopoulos (2018) made a strong technical assumption (e.g., the global minimizer is unique) for deriving their uniform stability results, which is unlikely to hold in the real-word and is avoided in this work for establishing a generalization error bound for the standard SGD.

Finally, it was brought to our attention 222personal communication with Jason D. Lee at NeurIPS 2018. when a preliminary version of this paper is almost done that an independent work (Ge et al., 2019) observes a similar advantage of stagewise SGD over SGD with a polynomially decaying step size lying at the better dependence on the condition number. However, they only analyze the strongly convex quadratic case and the training error of ERM.

2 Preliminaries and Notations

Let denote a randomized algorithm, which returns a randomized solution based on the given data set . Denote by the expectation over the randomness in the algorithm and by expectation over the randomness in the data set. When it is clear from the context, we will omit the subscript and in the expectation notations. Let denote an empirical risk minimizer, and denote the true risk of (also called testing error in this paper). We use to denote the Euclidean norm, and use .

In order to analyze the testing error convergence of a random solution, we use the following decomposition of testing error.

where measures the optimization error, i.e., the difference between empirical risk (or called training error) of the returned solution and the optimal value of the empirical risk, and measures the generalization error, i.e., the difference between the true risk of the returned solution and the empirical risk of the returned solution. The difference is an upper bound of the so-called excess risk bound in the literature, which is defined as . It is notable that the first term in the above bound is independent of the choice of randomized algorithms. Hence, in order to compare the performance of different randomized algorithms, we can focus on analyzing and . For analyzing the generalization error, we will leverage the uniform stability tool (Bousquet and Elisseeff, 2002). The definition of uniform stability is given below.

Definition 2.1.

A randomized algorithm is called -uniformly stable if for all data sets that differs at most one example the following holds:

A well-known result is that if is -uniformly stable, then its generalization error is bounded by (Bousquet and Elisseeff, 2002), i.e.,

Lemma 2.2.

If is -uniformly stable, we have .

In light of the above results, in order to compare the convergence of testing error of different randomized algorithms, it suffices to analyze their convergence in terms of optimization error and their uniform stability.

A function is -smooth if it is differentiable and its gradient is -Lipchitz continuous, i.e., . A function is -Lipchitz continuous if . Throughout the paper, we will make the following assumptions with some positive , , , and .

Assumption 1

Assume that

-

(i)

is -smooth in terms of for every .

-

(ii)

is finite-valued and -Lipchitz continuous in terms of for every .

-

(iii)

there exists such that for .

-

(iv)

satisfies the PL condition, i.e., there exists

-

(v)

For an initial solution , there exists such that .

Remark 1: The second assumption is imposed for the analysis of uniform stability of a randomized algorithm. W.o.l.g we assume . The third assumption is for the purpose of analyzing optimization error. It is notable that . It is known that the PL condition is much weaker than strong convexity. If is a strongly convex function, corresponds to the strong convexity parameter. In this paper, we are particularly interested in the case when is small, i.e. the condition number is large.

Remark 2: It is worth mentioning that we do not assume the PL condition holds in the whose space . Hence, our analysis presented below can capture some cases that the PL condition only holds in a local space that contains a global minimum. For example, the recent paper by (Du et al., 2019) shows that the global minimum of learning a two-layer neural network resides in a ball centered around the initial solution and the PL condition holds in the ball (Xie et al., 2016).

3 Review: SGD under PL Condition

In this section, we review the training error convergence and generalization error of SGD with a decreasing step size for functions satisfying the PL condition in order to derive its testing error bound. We will focus on SGD using the step size and briefly mention the results corresponding to at the end of this section. We would like to emphasize the results presented in this section are mainly from existing works (Karimi et al., 2016; Hardt et al., 2016). The optimization error and the uniform stability of SGD have been studied in these two papers separately. Since we are not aware of any studies that piece them together, it is of our interest to summarize these results here for comparing with our new results established later in this paper.

Let us first consider the optimization error convergence, which has been analyzed in (Karimi et al., 2016) and is summarized below.

Theorem 1.

Remark 3: In order to have an optimization error, one can set in the decreasing step size setting. In the constant step size setting, one can set and , where is the initial optimization error bound. Karimi et al. (2016) also mentioned a stagewise step size strategy based on the second result above. By starting with and running for iterations, and restarting the second stage with and , then after stages, we have optimization error less than , and the total iteration complexity is . We can see that the analysis of Karimi et al. (2016) cannot explain why stagewise optimization strategy brings any improvement compared with SGD with a decreasing step size of . No matter which step size strategy is used among the ones discussed above, the total iteration complexity is . It is also interesting to know that the above convergence result does not require the convexity of . On the other hand, it is unclear how to directly analyze SGD with a polynomially decaying step size for a convex loss to obtain a better convergence rate than (3).

The generalization error bound by uniform stability for both convex and non-convex losses have been analyzed in (Hardt et al., 2016). We just need to plug the step size of SGD in Theorem 1 into their results (Theorem 3.7 and Theorem 3.8) to prove the uniform stability, which is presented as follow.

Theorem 2.

Suppose Assumption 1 holds and is sufficiently large. If is convex for any , then SGD with step size satisfies uniform stability with

If is non-convex for any , then SGD with step size satisfies uniform stability with

Proof 3.1.

We combine the proof of Theorem 3.8 and the result of Lemma 3.11 in the long version of Hardt et al. (2016). For applying Theorem 3.8, we need to have , i.e., . Let us define . Then . Then conditioned on , we apply Lemma 3.11 in Hardt et al. (2016) and have

| (4) |

Next we consider the case when is non-convex. By noting , we can directly applying their Theorem 3.12 of the long version of Hardt et al. (2016) and get

Combining the optimization error and uniform stability, we obtain the convergence of testing error of SGD for smooth loss functions under the PL condition.

Theorem 3.

Suppose , Assumption 1 holds and let . If is convex for any , with step size and iterations SGD returns a solution satisfying

If is non-convex for any , with the same setting SGD returns a solution satisfying

Proof 3.2.

Based on the decomposition of testing error, the result of Theorem 1 and Theorem 2, we could upper bound the testing error by combining optimization error and generalization error together. For convex problems, we have

For non-convex problems, we have

Let , which is positive when is very small. Given , we have

We also have given that and for small . Thus, we complete the proof.

By optimizing the value of in the above bounds, we obtain the testing error bound dependent on only. The results are summarized in the following corollary.

Corollary 4.

Suppose Assumption 1 holds. If is convex for any , with step size and iterations SGD returns a solution satisfying

If is non-convex for any , with step size and iterations SGD returns a solution satisfying

Remark 4: If the loss is convex, the excess risk bound is in the order of by running SGD with iterations. It notable that an excess risk bound is called the fast rate in the literature. If the loss is non-convex and (an interesting case 333We can always scale up such that is a small constant, which only scales up the bound by a constant factor.), the excess risk bound is in the order of by running SGD with iterations. When is very small, the convergence of testing error is very slow. In addition, the number of iterations is also scaled by for achieving a minimal excess risk bound.

Remark 5: Another possible choice of decreasing step size is , which yields an convergence rate for in the convex case (Nemirovski et al., 2009) or for in the non-convex case with a randomly sampled (Ghadimi and Lan, 2013). In the latter case, it also implies a worse convergence rate of for the optimization error under the PL condition. Regarding the uniform stability, the step size of will also yield a worse growth rate in terms of Hardt et al. (2016). For example, if the loss function is convex, the generalization error by uniform stability scales as and hence the testing error bound is in the order of , which is worse than the above testing error bound for the big data setting . Hence, below we will focus on the comparison with the theoretical results in Corollary 4.

4 Start for a Convex Function

First, let us present the algorithm that we intend to analyze in Algorithm 1. At the -th stage, a regularized funciton is constructed that consists of the original objective and a quadratic regularizer . The reference point is a returned solution from the previous stage, which is also used for an initial solution for the current stage. Adding the strongly convex regularizer at each stage is not essential but could be helpful for reducing the generalization error and is also important for one class of non-convex loss considered in next section. For each regularized problem, the SGD with a constant step size is employed for a number of iterations with an appropriate returned solution. We will reveal the value of step size, the number of iterations and the returned solution for each class of problems separately. Note that the widely used stagewise SGD falls into the framework of Start when and .

In this section, we will analyze Start algorithm for a convex function under the PL condition. We would like to point out that similar algorithms have been proposed and analyzed in (Hazan and Kale, 2011; Xu et al., 2017) for convex problems. They focus on analyzing the convergence of optimization error for convex problems under a quadratic growth condition or more general local error bound condition. In the following, we will show that the PL condition implies a quadratic growth condition. Hence, their algorithms can be used for optimizing as well enjoying a similar convergence rate in terms of optimization error. However, there is still slight difference between the analyzed algorithm from their considered algorithms. In particular, the regularization term is absent in (Hazan and Kale, 2011), which corresponds to in our case. However, adding a small regularization (with not too large ) can possibly help reduce the generalization error. In addition, their initial step size is scaled by . The initial step size of our algorithm depends on the quality of initial solution that seems more natural and practical. A similar regularization at each stage is also used in (Xu et al., 2017). But their algorithm will suffer from a large generalization error, which is due to the key difference between Start and their algorithm (ASSG-r). In particular, they use a geometrically decreasing the parameter starting from a relatively large value in the order of with a total iteration number . According to our analysis of generalization error (see Theorem 6), their algorithm has a generalization error in the order of in contrast to of our algorithm.

4.1 Convergence of Optimization Error

We need the following lemma for our analysis.

Lemma 4.1.

If satisfies the PL condition, then for any we have

| (5) |

where is the closest optimal solution to .

Remark 6: The above result does not require the convexity of . For a proof, please refer to (Bolte et al., 2015; Karimi et al., 2016). Indeed, this error bound condition instead of the PL condition is enough to derive the results in Section 4 and Section 5.

Below, we let denote the solution computed during the -th stage at the -th iteration, and denote the conditional expectation given the randomness before -th stage. We first analyze the convergence of SGD for one stage.

Lemma 4.2.

The above convergence result can be boosted for showing the faster convergence of Start under the PL condition.

Theorem 5.

Suppose Assumption 1, and is a convex function of . Then by setting and , where , after stages we have

The total iteration complexity is .

Remark 7: Compared to the result in Theorem 1, the convergence rate of Start is faster by a factor of . It is also notable that can be as large as in the convex case.

Proof 4.3.

We will prove by induction that , where , which is true for by the assumption. By applying Lemma 4.2 to the -th stage, for any

| (6) |

By plugging (the closest optimal solution to ) into the above inequality we have

where we use the result in Lemma 4.1. Since and and , we have

By induction, after stages, we have

The total iteration complexity is .

4.2 Analysis of Generalization Error

In this subsection, we analyze the uniform stability of Start. By showing , we can show the generalization error is bounded by , where is learned on a data set and is learned a different data set that only differs from at most one example. Our analysis is closely following the route in (Hardt et al., 2016). The difference is that we have to consider the difference on the reference points of two copies of our algorithm on two data sets . We first give the following lemma regarding the growth of stability within one stage of Start. To this end, we let denote the loss functions used at the -th iteration of the two copies of algorithm.

Lemma 4.4.

Assume is smooth and convex. Let denote the sequence learned on and be the sequence learned on by Start at one stage, . If , then

Based on the above result, we can establish the uniform stability of Start.

Theorem 6.

After stages, Start satisfies uniform stability with

Proof 4.5.

By applying the result in Lemma 4.4 to the -th stage, omitting in the notation, for we have

Then,

For the -stage, we have and . Then

where . By summing the above inequality for stages and noting that , we prove the theorem.

4.3 Put them Together

Finally, we have the following testing error bound of returned by Start.

Theorem 7.

After stages with a total number of iterations . The testing error of is bounded by

Remark 8: Let , the excess risk bound becomes and the total iteration complexity is . This improves the convergence of testing error of SGD stated in Corollary 4 for the convex case when , which needs iterations and has a testing error bound of .

5 Start for Non-Convex Functions

Next, we will establish faster convergence of Start than SGD for “nice-behaviored" non-convex functions. In particular, we will consider two classes of non-convex functions that are close to a convex function, namely one-point weakly quasi-convex and weakly convex functions. We first introduce the definitions of these functions and then present some discussions followed by their convergence results.

Definition 5.1 (One-point Weakly Quasi-Convex).

A non-convex function is called one-point -weakly quasi-convex for if there exists a global minimum such that

| (7) |

Definition 5.2 (Weakly Convex).

A non-convex function is -weakly convex for if is convex.

It is interesting to connect one-point weakly quasi-convexity to one-point strong convexity that has been considered for non-convex optimization, especially optimizing neural networks (Li and Yuan, 2017; Kleinberg et al., 2018).

Definition 5.3 (One-point Strongly Convex).

A non-convex function is one-point strongly convex with respect to a global minimum if there exists such that

The following lemma shows that one-point strong convexity implies both the PL condition and the one-point weakly quasi-convexity.

Lemma 5.4.

Suppose is -smooth and one-point strongly convex w.r.t with and , then

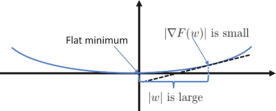

For “nice-behaviored" one-point weakly quasi-convex function that satisfies the PL condition, we are interested in the case that is a constant close to or larger than . Note that a convex function has and a strongly convex function has . For the case of in the PL condition, this indicates that is larger than , which further implies that . Intuitively, this inequality (illustrated in Figure 1) also connects itself to the flat minimum that has been observed in deep learning experiments Chaudhari et al. (2016). For “nice-behaviored" weakly convex function, we are interested in the case that is close to zero. Weakly convex functions with a small have been considered in the literature of non-convex optimization (Lan and Yang, 2018). In both cases, we will establish faster convergence of optimization error and testing error of Start.

5.1 Convergence of Optimization Error

The approach of analysis for the considered non-convex functions is similar to that of convex functions. We also first analyze the convergence of SGD for each stage in Lemma 5.5 and Lemma 5.7 for one-point weakly quasi-convex and weakly convex functions, respectively. Then we extend these results to stages for Start in Theorem 8 and Theorem 9.

Lemma 5.5.

Assume is one-point -weakly quasi-convex w.r.t . By applying SGD (Algorithm 2) to with where is randomly sampled, we have

Theorem 8.

Suppose is one-point -weakly quasi-convex w.r.t and (5) holds for the same . Then by setting , , and where is randomly sampled, after stages we have

The total iteration complexity is .

Proof 5.6.

We will prove by induction that , where , which is true for by the assumption. By applying Lemma 5.5 to the -th stage,

By the setting and and , we have

By induction, after stages, we have

The total iteration complexity is .

The following is the results for -weakly convex.

Lemma 5.7.

Assume is -weakly convex. By applying SGD (Algorithm 2) to with , and , for any , we have

Remark 9: The above result indicates that can not be as large as infinity. However, for a small value , the added regularization term is not large.

Theorem 9.

Suppose Assumption 1 holds, and is -weakly convex with . Then by setting , , and , where , and after stages we have

The total iteration complexity is .

Remark 10: Several differences are noticeable between the two classes of non-convex functions: (i) in the weakly quasi-convex case can be as large as , in contrast it is required to be smaller than in the weakly convex case; (ii) the returned solution by SGD at the end of each stage is a randomly selected solution in the weakly quasi-convex case and is an averaged solution in the weakly convex case. Finally, we note that the total iteration complexity for both cases is under and , which is better than of SGD as in Theorem 1.

Proof 5.8.

We will prove by induction that , where , which is true for by the assumption. By applying Lemma 4.2 to the -th stage, for any

By plugging into the above inequality we have

where we use Lemma 4.1. By the setting and and , we have

By induction, after stages, we have

The total iteration complexity is .

5.2 Generalization Error

The analysis of generalization error for the two cases are similar with a unified result presented below. We will first establish the recurrence of stability within one stage in Lemma 5.9 and then use it to analyze the convergence of Start.

Lemma 5.9.

Assume is -smooth. Let denote the sequence learned on and be the sequence learned on by Start at one stage, . Then

Next, we can establish the uniform stability of Start.

Theorem 10.

Let and , where in the one-point weakly quasi-convex case and in the weakly convex case. Then we have

Proof 5.10.

After establishing the recurrence of stability within one stage in Lemma 5.9, we will apply the similar conditional analysis for the non-convex loss as in (Hardt et al., 2016). In particular, we will condition on , i.e., the different example will be used within the last stage, and prove the bound for . The result of Theorem 10 follows directly from Theorem 3.8 in (Hardt et al., 2016) and Lemma 3.11 in the long version of (Hardt et al., 2016).

By putting the optimization error and generalization error together, we have the following testing error bound.

Theorem 11.

Remark 11: We are mostly interested in the case when is constant close to or larger than . By setting , we have the excess risk bounded by under the total iteration complexity . This improves the testing error bound of SGD stated in Corollary 4 for the non-convex case when , which needs iterations and suffers a testing error bound of .

Proof 5.11.

The proof is done simply by combining the convergence of optimization error and generalization error bound with the following simplification as done in the proof of Theorem 3:

6 Numerical Experiments

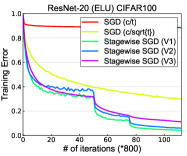

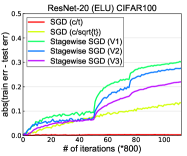

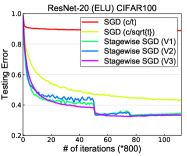

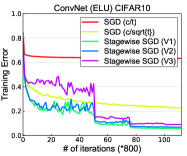

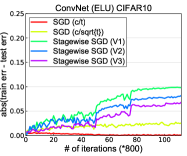

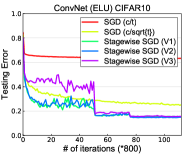

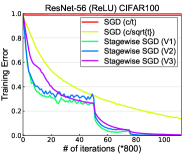

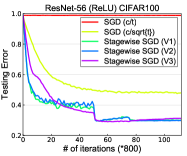

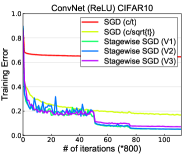

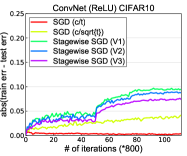

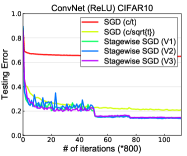

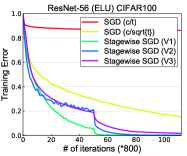

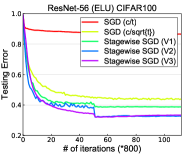

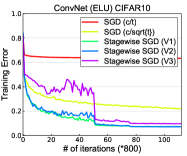

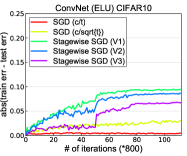

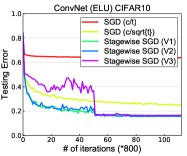

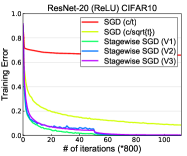

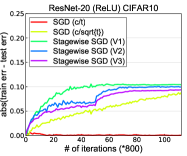

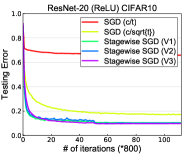

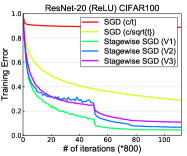

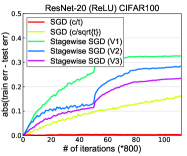

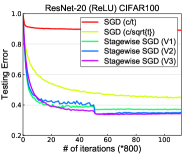

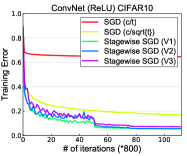

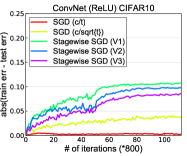

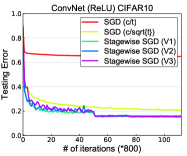

In this section, we perform experiments grouped into two subsections, i.e., non-convex deep learning and convex problems. In both subsections, we study the covergence of Start and compare it with commonly used SGD with polynomially decaying step size. Additionally, we verify two assumptions (i.e., one-point weakly quasi-convex and PL condition) made in non-convex problems.

6.1 Learning with Non-convex Deep Learning

In this subsection, we focus experiments on non-convex deep learning, and also include in the supplement some experimental results of Start for convex functions that satisfy the PL condition. The numerical experiments in this subsection mainly serve two purposes: (i) verifying that using different algorithmic choices in practice (e.g, regularization, averaged solution) is consistent with the provided theory; (ii) verifying the assumptions made for non-convex objectives in our analysis in order to explain the great performance of stagewise learning.

We compare stagewise learning with different algorithmic choices against SGD using two polynomially decaying step sizes (i.e., and ). For stagewise learning, we consider the widely used version that corresponds to Start with and the returned solution at each stage being the last solution, which is denoted as stagewise SGD (V1). We also implement other two variants of Start that solves a regularized function at each stage (corresponding to ) and uses the last solution or the averaged solution for the returned solution at each stage. We refer to these variants as stagewise SGD (V2) and (V3), respectively.

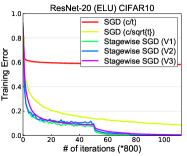

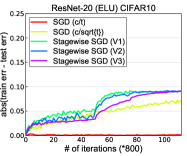

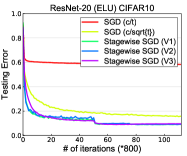

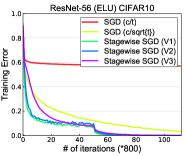

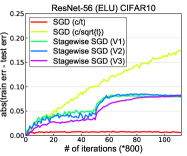

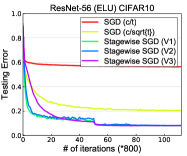

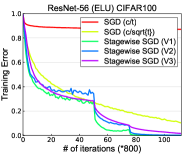

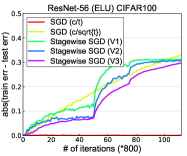

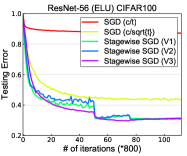

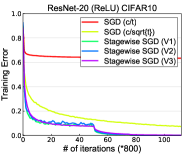

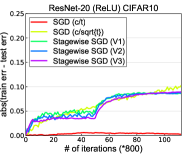

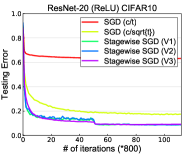

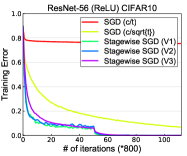

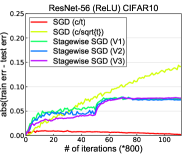

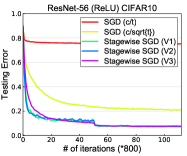

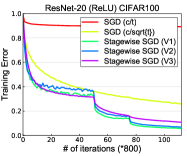

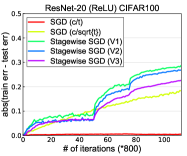

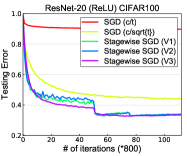

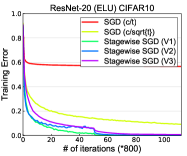

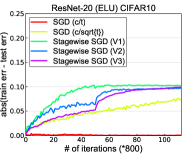

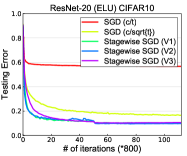

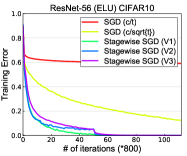

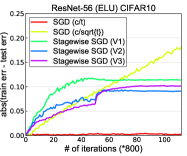

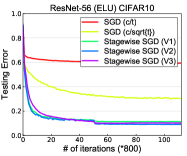

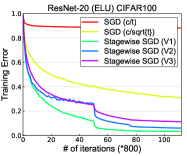

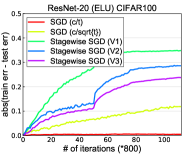

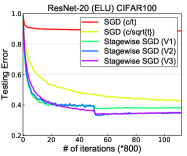

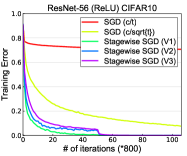

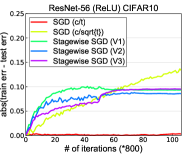

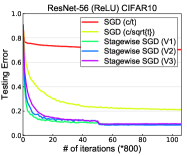

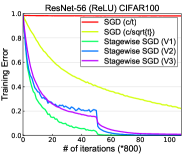

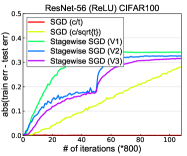

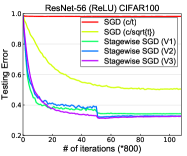

We conduct experiments on two datasets CIFAR-10, -100 using different neural network structures, including residual nets and convolutional neural nets without skip connection. Two residual nets namely ResNet20 and ResNet56 (He et al., 2016) are used for CIFAR-10 and CIFAR-100. For each network structure, we use two types of activation functions, namely RELU and ELU () (Clevert et al., 2015). ELU is smooth that is consistent with our assumption. Although RELU is non-smooth, we would like to show that the provided theory can also explain the good performance of stagewise SGD. For stagewise SGD on CIFAR datasets, we use the same stagewise step size strategy as in (He et al., 2016), i.e., the step size is decreased by at 40k, 60k iterations. For all algorithms, we select the best initial step size from and the best regularization parameter of stagewise SGD (V2, V3) from by cross-validation based on performance on a validation data. We report the results for using ResNets and ConvNet without weight decay in this section, and include the results with weight decay (i.e., including regularization) in the Appendix.

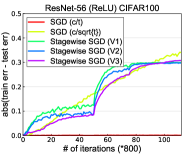

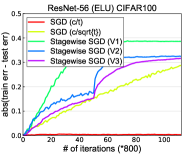

The training error, generalization error and testing error are shown in Figure 2 and Figure 3 where we employ ELU and RELU as activation functions, respectively. We can see that SGD with a decreasing step size converges slowly, especially SGD with a step size proportional to . It is because that the initial step size of SGD () is selected as a small value less than 1. We observe that when using a large step size it cannot lead to convergence. In terms of different algorithmic choices of Start, we can see that using an explicit regularization as in V2, V3 can help reduce the generalization error that is consistent with theory, but also slows down the training a little. Using an averaged solution as the returned solution in V3 can further reduce the generalization error but also further slow downs the training. Overall, stagwise SGD (V2) achieves the best tradeoff in training error convergence and generalization error, which leads to the best testing error.

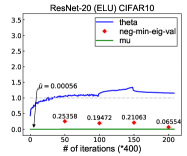

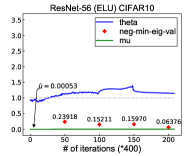

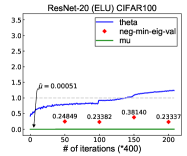

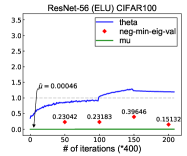

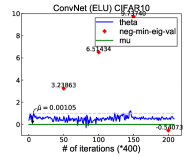

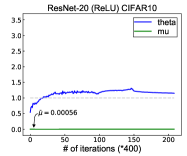

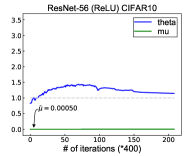

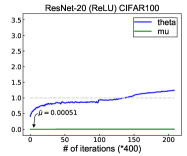

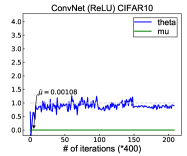

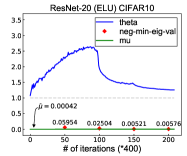

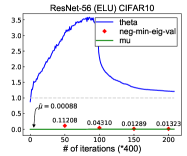

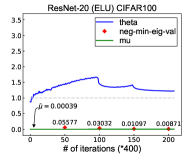

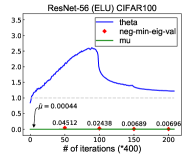

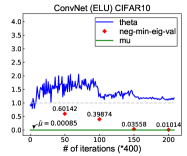

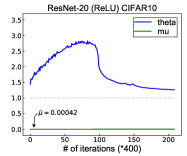

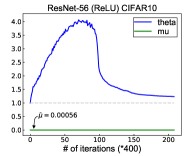

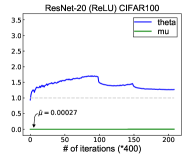

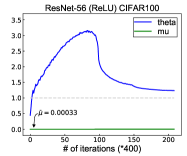

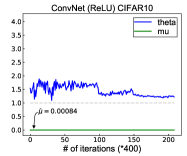

Finally, we verify the assumptions about the non-convexity made in Section 5. To this end, on a selected we compute the value of , i.e., the ratio of to as in (7), and the value of , i.e., the ratio of to as in (5). For , we use the solution found by stagewise SGD (V1) after a large number of iterations (200k), which gives a small objective value close to zero. We select 200 points during the process of training by stagewise SGD (V1) across all stages, and plot the curves for the values of and averaged over 5 trials in the most right panel of Figure 2 and Figure 3. We can clearly see that our assumptions about and one-point weakly quasi-convexity with are satisfied. Hence, the provided theory for stagewise learning is applicable.

We also compute the minimum eigen-value of the Hessian on several selected solutions by the Lanczos method. The Hessian-vector product is approximated by the finite-difference using gradients. The negative value of minimum eigen-value is marked as in the same figure of . We can see that the assumption about seems not hold for learning deep neural networks.

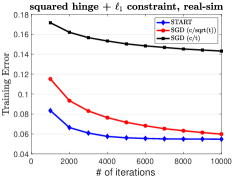

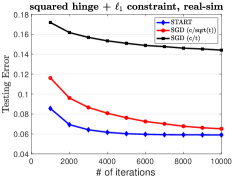

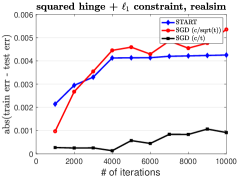

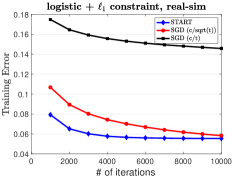

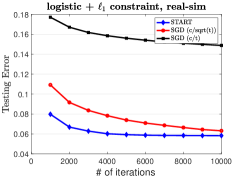

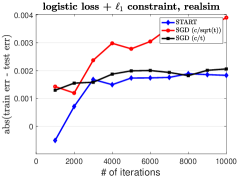

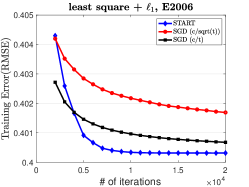

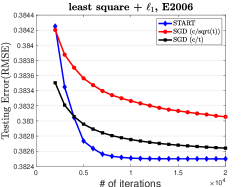

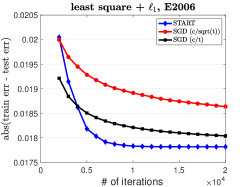

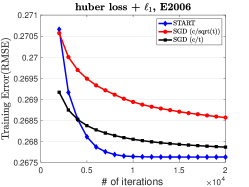

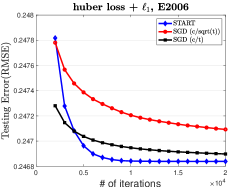

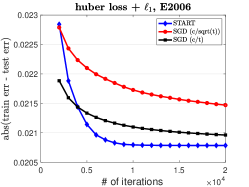

6.2 Learning with Convex Loss Functions

We consider minimizing an empirical loss under an norm constraint, i.e.,

where denotes the feature vector of the -th example and is the corresponding label for classification or is continuous for regression. Two loss functions are used for classification, namely squared hinge loss and logistic loss . Two loss functions are also used for regression, namely square loss and Huber loss ():

For all considered problems here, the PL condition (or the equivalent the quadratic growth condition) holds (Xu et al., 2017).

For classification, we use real-sim data from the libsvm website, which has total examples and features. For regression, we use the E2006-tfidf data from the libsvm website, which has (training examples), (testing examples), and features. For real-sim data, we randomly select examples for testing, and for E2006, we use the provided testing set. For parameter selection, we also divide the training examples into two parts, i.e., the validation data and the training data. The size of the validation set is the same as the testing set. We run the analyzed Start algorithm with and the averaged solution as a returned solution at each stage. The number of iterations per-stage is determined according to the performance on the validation data, i.e., when the error on the validation data does not change significantly after 1000 iterations we terminate one stage and restart the next stage. For classification, the insignificant change means the error rate does not improve by and for regression it means the relative improvement on root mean square error does not change by a factor of . The initial step sizes are tuned to get the fast training convergence and the value of are is tuned based on the performance on the validation data.

The results averaged over 5 random trials are shown in Figure 4. They clearly show the superior performance of Start comparing with SGD with polynomially decaying step size (i.e., and ).

7 Conclusion

In this paper, we have analyzed the convergence of training error and testing error of a stagewise regularized training algorithm for solving empirical risk minimization under the Polyak-Łojasiewicz condition. For non-convex objectives, we consider two classes of functions that are close to a convex function for which stagewise learning is proved to yield faster convergence than vanilla SGD with a polynomially decreasing step size on both training and testing error. Our numerical experiments on deep learning verify that one class of non-convexity assumption holds and hence the provided theory of faster convergence applies. In future, we consider extending the theory to the non-smooth RELU activation.

References

- Bassily et al. (2018) Raef Bassily, Mikhail Belkin, and Siyuan Ma. On exponential convergence of sgd in non-convex over-parametrized learning. CoRR, abs/1811.02564, 2018.

- Bolte et al. (2015) Jerome Bolte, Trong Phong Nguyen, Juan Peypouquet, and Bruce Suter. From error bounds to the complexity of first-order descent methods for convex functions. CoRR, abs/1510.08234, 2015.

- Bousquet and Elisseeff (2002) Olivier Bousquet and André Elisseeff. Stability and generalization. J. Mach. Learn. Res., 2:499–526, March 2002. ISSN 1532-4435. 10.1162/153244302760200704. URL https://doi.org/10.1162/153244302760200704.

- Charles and Papailiopoulos (2018) Zachary Charles and Dimitris Papailiopoulos. Stability and generalization of learning algorithms that converge to global optima. In Jennifer Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning (ICML), volume 80 of Proceedings of Machine Learning Research, pages 745–754, Stockholmsm ssan, Stockholm Sweden, 10–15 Jul 2018.

- Chaudhari et al. (2016) Pratik Chaudhari, Anna Choromanska, Stefano Soatto, Yann LeCun, Carlo Baldassi, Christian Borgs, Jennifer Chayes, Levent Sagun, and Riccardo Zecchina. Entropy-sgd: Biasing gradient descent into wide valleys. arXiv preprint arXiv:1611.01838, 2016.

- Chen et al. (2018) Zaiyi Chen, Tianbao Yang, Jinfeng Yi, Bowen Zhou, and Enhong Chen. Universal stagewise learning for non-convex problems with convergence on averaged solutions. CoRR, /abs/1808.06296, 2018.

- Clevert et al. (2015) Djork-Arné Clevert, Thomas Unterthiner, and Sepp Hochreiter. Fast and accurate deep network learning by exponential linear units (elus). arXiv preprint arXiv:1511.07289, 2015.

- Davis and Drusvyatskiy (2018) Damek Davis and Dmitriy Drusvyatskiy. Stochastic subgradient method converges at the rate on weakly convex functions. CoRR, /abs/1802.02988, 2018.

- Du et al. (2019) Simon S. Du, Xiyu Zhai, Barnabas Poczos, and Aarti Singh. Gradient descent provably optimizes over-parameterized neural networks. In International Conference on Learning Representations, 2019. URL https://openreview.net/forum?id=S1eK3i09YQ.

- Ge et al. (2019) Rong Ge, Sham M. Kakade, Rahul Kidambi, and Praneeth Netrapalli. Rethinking learning rate schedules for stochastic optimization, 2019. URL https://openreview.net/forum?id=HJePy3RcF7.

- Ghadimi and Lan (2013) Saeed Ghadimi and Guanghui Lan. Stochastic first- and zeroth-order methods for nonconvex stochastic programming. SIAM Journal on Optimization, 23(4):2341–2368, 2013.

- Hardt and Ma (2016) Moritz Hardt and Tengyu Ma. Identity matters in deep learning. CoRR, abs/1611.04231, 2016.

- Hardt et al. (2016) Moritz Hardt, Ben Recht, and Yoram Singer. Train faster, generalize better: Stability of stochastic gradient descent. In Proceedings of the 33nd International Conference on Machine Learning (ICML), pages 1225–1234, 2016.

- Hazan and Kale (2011) Elad Hazan and Satyen Kale. Beyond the regret minimization barrier: an optimal algorithm for stochastic strongly-convex optimization. In Proceedings of the 24th Annual Conference on Learning Theory (COLT), pages 421–436, 2011.

- Hazan et al. (2007) Elad Hazan, Amit Agarwal, and Satyen Kale. Logarithmic regret algorithms for online convex optimization. Machine Learning, 69(2-3):169–192, 2007.

- He et al. (2016) Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. Deep residual learning for image recognition. In CVPR, pages 770–778. IEEE Computer Society, 2016.

- Karimi et al. (2016) Hamed Karimi, Julie Nutini, and Mark W. Schmidt. Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. In Machine Learning and Knowledge Discovery in Databases - European Conference (ECML-PKDD), pages 795–811, 2016.

- Kleinberg et al. (2018) Bobby Kleinberg, Yuanzhi Li, and Yang Yuan. An alternative view: When does SGD escape local minima? In Proceedings of the 35th International Conference on Machine Learning, pages 2698–2707, 2018.

- Krizhevsky et al. (2012) Alex Krizhevsky, Ilya Sutskever, and Geoffrey E. Hinton. Imagenet classification with deep convolutional neural networks. In Advances in Neural Information Processing Systems (NIPS), pages 1106–1114, 2012.

- Kuzborskij and Lampert (2018) Ilja Kuzborskij and Christoph H. Lampert. Data-dependent stability of stochastic gradient descent. In Proceedings of the 35nd International Conference on Machine Learning (ICML), volume 80 of JMLR Workshop and Conference Proceedings, pages 2820–2829. JMLR.org, 2018.

- Lan and Yang (2018) Guanghui Lan and Yu Yang. Accelerated stochastic algorithms for nonconvex finite-sum and multi-block optimization. CoRR, abs/1805.05411, 2018.

- Lei et al. (2017) Lihua Lei, Cheng Ju, Jianbo Chen, and Michael I. Jordan. Non-convex finite-sum optimization via SCSG methods. In Advances in Neural Information Processing Systems 30 (NIPS), pages 2345–2355, 2017.

- Li and Yuan (2017) Yuanzhi Li and Yang Yuan. Convergence analysis of two-layer neural networks with relu activation. In Advances in Neural Information Processing Systems 30 (NIPS, pages 597–607, 2017.

- Nemirovski et al. (2009) Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19:1574–1609, 2009. URL http://dx.doi.org/10.1137/070704277.

- Nesterov (2004) Yurii Nesterov. Introductory lectures on convex optimization : a basic course. Applied optimization. Kluwer Academic Publ., 2004. ISBN 1-4020-7553-7.

- Polyak (1963) B. T. Polyak. Gradient methods for minimizing functionals. Zh. Vychisl. Mat. Mat. Fiz., 3:4:864?878, 1963.

- Qu et al. (2016) Chao Qu, Huan Xu, and Chong Ong. Fast rate analysis of some stochastic optimization algorithms. In Maria Florina Balcan and Kilian Q. Weinberger, editors, Proceedings of The 33rd International Conference on Machine Learning, volume 48 of Proceedings of Machine Learning Research, pages 662–670, New York, New York, USA, 20–22 Jun 2016. PMLR. URL http://proceedings.mlr.press/v48/qua16.html.

- Reddi et al. (2016) Sashank J. Reddi, Ahmed Hefny, Suvrit Sra, Barnabas Poczos, and Alex Smola. Stochastic variance reduction for nonconvex optimization. In Proceedings of The 33rd International Conference on Machine Learning (ICML), volume 48, pages 314–323, 2016.

- Xie et al. (2016) Bo Xie, Yingyu Liang, and Le Song. Diversity leads to generalization in neural networks. CoRR, abs/1611.03131, 2016. URL http://arxiv.org/abs/1611.03131.

- Xu et al. (2017) Yi Xu, Qihang Lin, and Tianbao Yang. Stochastic convex optimization: Faster local growth implies faster global convergence. In Proceedings of the 34th International Conference on Machine Learning (ICML), pages 3821 – 3830, 2017.

- Xu et al. (2018) Yi Xu, Qi Qi, Qihang Lin, Rong Jin, and Tianbao Yang. Stochastic optimization for dc functions and non-smooth non-convex regularizers with non-asymptotic convergence. arXiv preprint arXiv:1811.11829, 2018.

- Zhao and Zhang (2015) Peilin Zhao and Tong Zhang. Stochastic optimization with importance sampling for regularized loss minimization. In Proceedings of the 32nd International Conference on Machine Learning (ICML), pages 1–9, 2015.

- Zhou and Liang (2017) Yi Zhou and Yingbin Liang. Characterization of gradient dominance and regularity conditions for neural networks. CoRR, abs/1710.06910, 2017.

- Zhou et al. (2018) Yi Zhou, Yingbin Liang, and Huishuai Zhang. Generalization error bounds with probabilistic guarantee for SGD in nonconvex optimization. CoRR, abs/1802.06903, 2018.

A. Proofs of Section 4

A1. Proof of Lemma 4.2

Proof .1.

The proof of Lemma 4.2 follows similarly as the one of Lemma 1 in (Zhao and Zhang, 2015). For completeness, we prove our result.

Recall that . Let , so , where is the indicator function of . Due to the convexity of , the -strong convexity of and the -smoothness of , we have the following three inequalities

| (8) | ||||

| (9) |

Combining them together, we have

| (10) |

Recall Line 3 of Algorithm 2, we update as follows

If we set the gradient of the above problem in to , there exists such that

Plugging the above equation to (.1), we have

The first equality is due to

and . The second inequality is due to Cauchy-Schwarz inequality and setting . The third inequality is due to Lemma 3 of Xu et al. (2018).

Taking expectation on both sides, we have

where by assumption.

Taking summation of the above inequality from to , we have

By employing Jensens’ inequality on LHS, denoting the output of the -th stage by and taking expectation, we have

A2. Proof of Lemma 4.4

Proof .2.

Let us define

It is not difficult to show that , where denotes the projection operator. Due to non-expansive of the projection operator, it suffices to bound . Let us consider two scenarios. The first scenario is (using the same data). Then

where last inequality is due to -expansive of GD update with for a convex function (Hardt et al., 2016). Next, let us consider the second scenario . Then

B. Proofs of Section 5

B1. Proof of Lemma 5.4

Proof .3.

The inequality regarding can be found in (Karimi et al., 2016). The inequality regarding can be easily seen from the definition of one-point strong convexity and the -smoothness condition of and the condition , i.e.,

B2. Proof of Lemma 5.5

Proof .4.

Without loss of generality, we consider minimizing . Let . The initial solution of SGD . Following the standard analysis of stochastic proximal SGD, we have

Taking expectation on both sides, we have

Plugging , summing over and using the one-point weakly quasi-convexity, we have

As a result,

where is randomly selected. Applying the above result to the -th stage, we complete the proof.

B3. Proof of Lemma 5.7

Proof .5.

The proof of Lemma 5.7 follows the one of Lemma 4.2. The only difference lies on the weak convexity of .

We could replace the first inequality in (8) by the following -weak convexity condition of :

Then we combine it with other two inequalities as follows

Then following the proof of Lemma 4.2 under the condition we have

Taking expectation on both sides, summing from to and applying Jensen’s inequality, we have

The proof of Lemma 5.7 follows the one of Lemma 4.2. The only difference lies on the weak convexity of .

We could replace the first inequality in (8) by the following -weak convexity condition of :

Then we combine it with other two inequalities as follows

Then following the proof of Lemma 4.2 under the condition we have

Taking expectation on both sides, summing from to and applying Jensen’s inequality, we have

B4. Proof of Lemma 5.9

Proof .6.

Let us consider two scenarios. The first scenario is . Then

Next, let us consider the second scenario . Then

C. More Experimental Results

In this section, we include more experimental results of non-convex deep learning. The settings in this section are almost the same with those in Section 6.1 except that we train the networks with weight decay (i.e. including regularization). The results are shown in Figure 5, 6 with captions self-explaining the corresponding setting.