Necessary and Probably Sufficient Test for Finding Valid Instrumental Variables

Abstract

Can instrumental variables be found from data? While instrumental variable (IV) methods are widely used to identify causal effect, testing their validity from observed data remains a challenge. This is because validity of an IV depends on two assumptions, exclusion and as-if-random, that are largely believed to be untestable from data.

In this paper, we show that under certain conditions, testing for instrumental variables is possible. We build upon prior work on necessary tests to derive a test that characterizes the odds of being a valid instrument, thus yielding the name “necessary and probably sufficient”.

The test works by defining the class of invalid-IV and valid-IV causal models as Bayesian generative models and comparing their marginal likelihood based on observed data. When all variables are discrete, we also provide a method to efficiently compute these marginal likelihoods.

We evaluate the test on an extensive set of simulations for binary data, inspired by an open problem for IV testing proposed in past work. We find that the test is most powerful when an instrument follows monotonicity—effect on treatment is either non-decreasing or non-increasing—and has moderate-to-weak strength; incidentally, such instruments are commonly used in observational studies. Among as-if-random and exclusion, it detects exclusion violations with higher power.

Applying the test to IVs from two seminal studies on instrumental variables and five recent studies from the American Economic Review shows that many of the instruments may be flawed, at least when all variables are discretized.

The proposed test opens the possibility of data-driven validation and search for instrumental variables.

Keywords: Instrumental variable, Sensitivity analysis, Bayesian model comparison

1 INTRODUCTION

The method of instrumental variables is one of the most popular ways to estimate causal effects from observational data in the social and biomedical sciences. The key idea is to find subsets of the data that resemble a randomized experiment, and use those subsets to estimate causal effect. For example, instrumental variables have been used in economics to study the effect of policies such as military conscription and compulsory schooling on future earnings (Angrist and Krueger, 1991; Angrist and Pischke, 2008), and in epidemiology (under the name Mendelian randomization) to study the effect of risk factors on disease outcomes (Lawlor et al., 2008).

Inspite of their popularity, basic questions about the design, analysis and evaluation of instrumental variable (IV) studies remain elusive. In the design phase, it is unclear how to find a suitable instrumental variable. Even with access to bigger and more granular datasets, finding an instrument requires ingenuity and a laborious manual search, thereby restricting most IV studies to instruments derived from a small set of events such as the weather, lotteries or sudden shocks (Dunning, 2012). In the analysis phase, arguments are proposed to justify selection of an instrument, but it is hard to ascertain the extent to, or for which populations, the instrument is likely to be valid. Finally, in the evaluation phase, it is unclear how to evaluate the estimates produced by multiple IV studies due to the absence of any objective criteria of comparing relative validity of instruments, even on the same dataset.

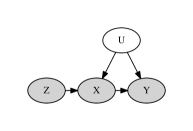

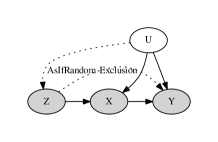

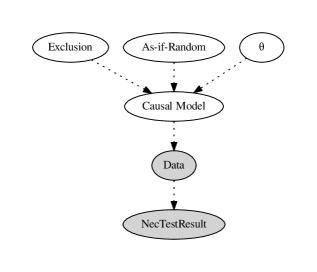

Specifically, consider the canonical causal inference problem shown in Figure 1a. The goal is to estimate the effect of a variable on another variable based on observed data, where is commonly referred to as the treatment and as the outcome. However, there are unobserved (and possibly unknown) common causes for X and Y that confound observed association between X and Y, making the isolation of X’s effect on Y a non-trivial problem. Unlike methods such as stratification or matching that condition on all observed common causes (Stuart, 2010), the instrumental variable method relies on finding an additional variable that acts as an instrument to modify the distribution of , as shown by the arrow in Figure 1a. The advantage is that we do not need to assume that all confounding common causes are observed to estimate the causal effect. To be a valid instrument, however, should satisfy three conditions (Angrist and Pischke, 2008). First, should have a substantial effect on . That is, causes (Relevance). Second, should not cause directly (Exclusion); the only association between and should be through . Third, should be independent of all the common causes of and (As-if-random). The latter two conditions are shown in the graphical model in Figure 1b. These conditions can also be expressed as conditional independence constraints: exclusion and as-if-random conditions imply and respectively.

However, the Achilles’ heel of any instrumental variable analysis is that these core conditions are never tested systematically. Except for relevance (which can be tested by measuring observed correlation between and ), the other two conditions depend on unobserved variables and thus are harder to check. Although necessary tests do exist that can weed out bad instruments (Pearl, 1995; Bonet, 2001), in practice exclusion and as-if-random as considered as assumptions and often defended with qualitative domain knowledge. This can be problematic because the entire validity of the IV estimate depends on the exclusion and as-if-random conditions.

In this paper, therefore we propose a test for validating instrumental variables that can be used to find, evaluate and compare potential instruments for their validity. Although instruments are untestable in general (Morgan and Winship, 2014; Dunning, 2012), we find that in many cases it is possible to distinguish between invalid and valid instruments. To do so, the proposed test applies the principles of Bayesian model comparison to causal models and estimates marginal likelihood of an valid instrument given the observed data. Comparing this to the corresponding marginal likelihood for an invalid instrument provides a metric for evaluating the validity of an instrument. The intuition is that if the instrument is valid, then causal models with an instrument as in Figure 1a should be able to generate observed data with higher likelihood than all other causal models. Specifically, let Valid-IV refer to the class of all causal models that yield a valid instrument and Invalid-IV to the class of causal models that yield an invalid instrument. Given an observed data distribution , the proposed method computes the ratio of marginal likelihoods for Valid-IV and Invalid-IV models. Whenever this marginal likelihood ratio is above a pre-determined acceptance threshold, we can conclude that the instrument is likely to be valid. To distinguish this probabilistic notion from deterministic sufficiency—conditions that would determine in absolute whether an instrument is valid or not—we call an instrument that passes the marginal likelihood ratio test as probably sufficient.

Combining the above approach with necessary tests proposed in past work leads to a Necessary and Probably Sufficient (NPS) test for instrumental variables. The combined NPS test proceeds as follows. If the observed data does not satisfy the necessary conditions, then it is declared invalid. If it does, then we proceed to estimate the marginal likelihood ratio over Valid-IV and Invalid-IV models. When all variables are discrete, we provide a general implementation of this test that makes no assumptions about the nature of functional relationships between the treatment, outcome and instrument.

Finally, any statistical test is only as good as the decisions it helps to support. Among the two IV assumptions, simulations show that the NPS test is more effective at detecting violations of the exclusion restriction. In particular, for certain instrumental variable designs where we restrict the direction of causal effects, such as stipulating that the instrument can only have a monotonic effect on treatment and possibly also the outcome, the NPS test is able to detect invalid instruments with high power. We also find that the proposed NPS test is most effective for validating instruments having low correlation with the treatment . Incidentally, most of the instruments used in observational studies in the social and biomedical sciences have weak to moderate strength, well-suited to the NPS test. To demonstrate the test’s usefulness in practice, we first consider an open problem proposed by Palmer et al. (2011) for validating an instrumental variable and show that the NPS test is able to identify valid instruments in that setting. Second, we apply the test to datasets from two seminal studies and five recent papers on instrumental variables from the American Economic Review, a premier economics journal. In many cases, we find that instrumental assumptions used in the corresponding papers were possibly flawed, at least when variables are binarized. We provide an R package ivtest that provides an implementation of the NPS test.

2 BACKGROUND: TESTABILITY OF AN INSTRUMENTAL VARIABLE

Since sufficient conditions for validity of an instrument ( and ) depend on an unobserved variable , the validity of an instrumental variable is largely believed to be untestable from observational data alone (Morgan and Winship, 2014). Pearl (1995), however, discovered that the specific causal graph structure in Figure 1 imposes constraints on the observed probability distribution over , and . These constraints can be used to derive a necessary test for IV conditions (Pearl, 1995; Bonet, 2001). Such a test weeds out bad instruments, but is inconclusive whenever an instrument passes the test. Sufficient tests exist, but require prohibitive assumptions such as knowing another valid instrumental variable as in the Durbin-Wu-Hausman test (Nakamura and Nakamura, 1981), or stipulating that confounders have no effect on the outcome. Due to these shortcomings, the dominant method to evaluate IV estimates involves a sensitivity analysis (Small, 2007), where we estimate the impact on the causal estimate when assumptions are violated with varying severity. We review prior tests and sensitivity analysis for instrumental variables below.

2.1 Tests for an instrumental variable

A classic test for instrumental variables is the Durbin-Wu-Hausman test (Nakamura and Nakamura, 1981). Given a subset of valid instrumental variables, it can identify whether other potential candidates are also valid instrumental variables. However, it provides no guidance on how to find the initial set of valid instrumental variables.

Without having an initial set of valid instrumental variables, an intuitive idea is to test whether the instrument is independent of the outcome whenever the treatment is constant () (Balke and Pearl, 1993). This can be seen as an approximation of the exclusion restriction using only observed data. It is sufficient under the assumption that either all common causes are constant throughout the data measurement period or trivially are not common causes—each of them can affect either or , but not both111Here we make the standard assumption of faithfulness. That is, observed conditional independence between variables implies causal independence. . However, under any non-trivial common cause , it will be implausible that and are independent, because conditioning on induces a correlation between and (and thus ). Further, because we ignore the contribution of unobserved confounders, this test is not a necessary condition for a valid instrument.

More admissive tests can be obtained by considering the restriction on probability distribution for imposed by a valid IV model. Consider the causal IV model from Figure 1a. In structural equations, the model can be equivalently expressed as:

| (1) |

where and are arbitrary deterministic functions and represents arbitrary, unobserved random variables that are independent of . Using this framework, Pearl derived conditions that any observed data generated from a valid instrumental variable model must satisfy (Pearl, 1995). For binary variables , and , the Pearl’s IV test can be written as the following set of instrumental inequalities.

| (2) |

Typically, researchers make an additional assumption that helps to derive a point estimate for the Local Average Treatment Effect (LATE). This assumption, called monotonicity (Angrist and Imbens, 1994), precludes any defiers to treatment in the population (Angrist and Pischke, 2008). That is, we assume that whenever . Under these conditions, Pearl showed that we can obtain tighter inequalities. For binary variables , and , the instrumental inequalities become:

| (3) | |||||

| (4) |

Whenever any of these inequalities are violated, it implies that one or more of the IV assumptions—exclusion, as-if-random or monotonicity—are violated. Based on these instrumental inequalities, different hypothesis tests have been proposed to account for sampling variability in observing the true conditional distributions. For example, a null hypothesis tests based on the chi-squared statistic (Ramsahai and Lauritzen, 2011) or the Kolmogorov-Smirnov test statistic (Kitagawa, 2015) can be applied.

Moreover, when , and are binary, this test is not only necessary, it is the strongest necessary test possible (Bonet, 2001; Kitagawa, 2015). In other words, if an observed data distribution satisfies the test, then there does exist at least one valid-IV causal model that could have generated the data; we call this the existence property. However, the test does not satisfy the existence property when all variables are not binary, allowing probability distributions that cannot be generated by any valid-IV model. To rectify this, Bonet proposed a more general version of the test that ensures the existence property for any discrete-valued , and . (Bonet, 2001). We refer to this version of the test as the Pearl-Bonet necessary and existence test for instrumental variables, or simply the Pearl-Bonet test.

While Bonet presented theoretical properties of the test for discrete variables, implementing the test in practice is non-trivial because it involves testing membership of a convex polytope in high-dimensional space. Further, the test does not support the monotonicity assumption, a popular assumption in instrumental variable studies. In this paper, therefore, we extend Bonet’s work by incorporating monotonicity and present a practical method for testing IVs when variables can have arbitrary number of discrete levels.

2.2 Sensitivity analysis for instrumental variables

Still, the above tests can refute an invalid-IV model, but are unable to verify a valid-IV model (Kitagawa, 2015). That is, even when an observed data distribution passes the necessary test, it does not exclude the possibility that data was generated by an invalid-IV model. As an example, consider the following data distribution presented by Palmer et al. (2011) which passes the Pearl-Bonet test, but violates the exclusion restriction because the instrument causes directly.

| (5) |

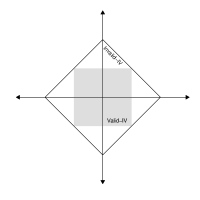

More generally, let us look at Figure 2 that shows the relationship between an observed data distribution and Valid-IV or Invalid-IV models. Each point in Figure 2a represents a probability distribution over , and .222The axes represent the space of conditional probabilities . We use the fact that any observed probability distribution over , and can be specified by a set of conditional probabilities of the form . For example, for binary variables, this would be a set of eight conditional probabilities (Bonet, 2001). The corresponding 8-dimensional real vector would be: (6) The 2-D squares represented in Figures 2a,b are actually polytopes in this multi-dimensional space. The extreme points for , or equivalently for invalid-IV models are characterized by . The boundary shown for NPS test in Figure 2c is however, an oversimplification. The set of conditional distributions (or equivalently, instruments) that can be validated by the NPS test is unknown and most likely will constitute many regions in the probability space, instead of a single bounded region as shown. The two squares bound the probability distributions that can be generated by any Valid-IV or Invalid-IV model. As can be seen from the figure, probability distributions generatable from the class of Valid-IV models are a strict subset of the distributions generatable by the class of invalid-IV models. This implies that even if a statistical test can accurately identify the boundary for valid-IV models, as in Figure 2b, we can never be sure whether the probability distribution was actually generated by a valid-IV or invalid-IV model.

As a partial remedy, researchers employ a sensitivity analysis to check the brittleness of a causal estimate when required assumptions are violated. For instance, one may progressively increase the magnitude of violation of the exclusion restriction, and observe when a resultant causal estimate flips in its direction of stated effect (Small, 2007). A Bayesian framework presents an intuitive way to conceptualize sensitivity analysis. The idea is to first estimate a causal effect assuming that the data is generated from a valid-IV causal model. One can then change parameters of the causal model to violate key assumptions and observe how fast the causal estimate changes. As an example, Aart (2010) proposes a Bayesian analysis to check the sensitivity to assumptions for a linear IV model. This analysis shows that even moderate uncertainty in the prior for the exclusion restriction lead to considerable loss of precision in estimating causal effects.

2.3 Developing a sufficient test for instrumental variables

In an ideal world, we would like to reduce uncertainty about assumptions as much as possible and determine precisely whether observed data was generated from a valid-IV model or not. However, as Figure 2 indicates, establishing sufficiency for a validity test is non-trivial. In particular, the usual method of comparing the maximum data likelihood of the two classes of IV models, Valid-IV or Invalid-IV, provides us no information. This is because Invalid-IV class of models (as shown in Figures 1b and 2b) is more general than the Valid-IV class and thus is always as likely (or more) to generate the observed data.

Instead of comparing maximum likelihoods of model classes, we turn to estimating likelihoods of individual causal models from Invalid-IV and Valid-IV classes. The intuition is that while the Invalid-IV class may always have a causal model that matches likelihood of the Valid-IV class for a valid instrument, there will be many other Invalid-IV models that provide a lower likelihood for the data. By generating models with different violations of the Exclusion and As-if-random conditions, we can estimate the data likelihood over individual models in the Invalid-IV class. Averaging over all models in the Valid-IV and Invalid-IV classes, we expect marginal likelihood to be higher for the Valid-IV class for data generated from a Valid-IV model. The idea of comparing different models from Valid-IV and Invalid-IV classes is similar to sensitivity analysis, except that we are interested in the likelihood of data rather than resultant causal estimates.

Unlike necessary tests (Ramsahai and Lauritzen, 2011; Kitagawa, 2015) that refute a null hypothesis that observed data was generated from a valid-IV model, probable sufficiency requires estimating the relative probability of valid-IV and invalid-IV models given observed data. When the relative probability—formally, marginal likelihood—is high, the instrument is likely to be valid. Conversely, when it is low, the instrument is likely to be invalid. Based on this motivation, we now provide a definition for probable sufficiency.

Probable Sufficiency for Instrumental Variables: If an observed data distribution passes the Pearl-Bonet necessary test, how likely is it that it was generated from a valid-IV model compared to an invalid-IV model?

Intuitively, we wish to find out how often does the Pearl-Bonet test accept an Invalid-IV model. That is, how often does an observed distribution that was generated by an invalid-IV model pass the necessary test? Once we know that, we can compute the probability that a given observed distribution was generated by a valid-IV model, based on the result of Pearl-Bonet test.

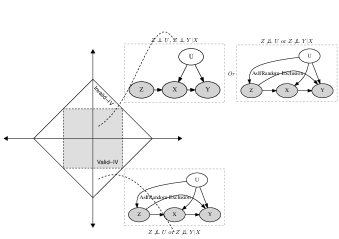

Combined, the Pearl-Bonet test and our probable sufficiency test provide a framework for testing instrumental variables, which we call the Necessary and Probably Sufficient (NPS) test for instrumental variables. Any valid instrument needs to pass Pearl-Bonet test. Therefore, NPS test provides necessity: any instrument that fails instrumentality inequalities is not a valid instrument. Further, NPS test provides sufficiency: any instrument that satisfies Pearl’s instrumental inequalities and passes the probable sufficiency test can be accepted as a valid instrument. That said, NPS test will be inconclusive for some instruments: those that satisfy Pearl’s inequalities but the marginal likelihood ratio remains close to 1. Figure 2 shows these possibilities. As shown by the dark grey box in the center, NPS test validates a subset of all possible valid-IV models.

In the next two sections, we describe the NPS test formally. Section 3 presents a general Validity Ratio statistic that can be used to compare Valid-IV and Invalid-IV models. We do so by introducing a probabilistic generative meta-model that formalizes the connection between IV assumptions, causal models and the observed data. The key detail for computing the Validity Ratio is in selecing a suitable sampling strategy for causal models. Section 4 describes one such strategy based on the response variable framework (Balke and Pearl, 1993). For the rest of the paper, we assume that , and are all discrete. In principle, we can apply the NPS testing framework to both continuous and discrete values for , and . However, the test is expected to be most informative when is discrete. This is because when is continuous, the region for Valid-IV identified by Pearl’s necessary test coincides with the Invalid-IV region and the necessary test becomes uninformative (Bonet, 2001). For ease of exposition, we present the NPS test using binary , and . In Section 5, we discuss how the test extends to the case where , and can be arbitrary discrete variables. Finally, Sections 6 and 7 demonstrate the practical applicability of the test using simulation and data from past IV studies.

3 A NECESSARY AND PROBABLY SUFFICIENT (NPS) TEST

The key idea behind the NPS test is that we can compare marginal likelihoods of valid-IV and invalid-IV class of models. To do so, we first present a Bayesian meta-model that describes how observed data can be generated from different values of the exclusion and as-if-random conditions. We then provide our main result that proposes a Validity Ratio to compare valid-IV and invalid-IV models, followed by pseudo-code for an algorithm that uses the NPS test to validate an instrumental variable. Throughout, we assume that , and are all discrete variables.

3.1 Generating valid-IV and invalid-IV causal models

As mentioned above, our strategy depends on simulating all causal models—both valid-IV and invalid-IV models—that could have generated the observed data. Therefore, we first describe a probabilistic generative meta-model of how the observed data is generated from a causal model, which in turn, is generated based on the as-if-random and exclusion assumptions.

Let us first define the valid-IV and invalid-IV models formally in terms of the two IV assumptions: exclusion and as-if-random. A valid IV model does not contain an edge from or from , as shown in Figure 1a. This implies that both Exclusion and As-if-random conditions hold for a valid-IV model. Conversely, a causal model is an invalid IV model when at least one of Exclusion or As-if-random conditions is violated, as shown by the dotted arrows in Figure 1b. Therefore, given the causal structure , there are two classes of causal models that can generate observed data distributions over , and :

-

•

Valid-IV model: and

-

•

Invalid-IV model: Not ( and )

where denotes the exclusion assumption and denotes the as-if-random assumption.

Each of these classes of causal models—valid and invalid IV—in turn contains multiple causal models, based on the specific parameters () describing each edge of the graph. This one-to-many relationship between conditions for IV validity and causal models can be made precise using a generative meta-model, as shown in Figure 3. We show dotted arrows to distinguish this (probabilistic) generative meta-model from the causal models described earlier. The meta-model entails the following generative process: Based on the configuration of the Exclusion and As-if-Random conditions, one of the causal model classes—Valid or Invalid IV—is selected. A specific model (Causal Model node) is then generated by parameterizing the selected class of causal models, where we use to denote model parameters. The causal model results in a probability distribution over , and , from which observed data (Data node) is sampled. Finally, we can apply Pearl-Bonet necessary test on the observed data, which leads to the binary variable .

For a given problem, we observe the data and result of the Pearl-Bonet necessary test. All other variables in the meta-model are unobserved.

3.2 Comparing marginal likelihood of Valid-IV and Invalid-IV model classes

Let denote whether the observed data passed the necessary test. We wish to estimate whether the data was generated from a Valid IV model. We can compare the likelihood of observing and given that both Exclusion and As-if-random conditions are valid, versus when they are not.

Theorem 1

Given a representative data sample drawn from over variables , , , and result of the Pearl-Bonet necessary test on the data sample, the validity of as an instrument for estimating causal effect of on can be decided using the following evidence-ratio of valid and invalid classes of models:

| Validity-Ratio | ||||

| (7) |

where and denote classes of valid-IV and invalid-IV causal models respectively. represents the likelihood of the data given a causal model . and denote the prior probability of any model within the class of valid-IV and invalid-IV causal models respectively.

While we are additionally using the result of the Pearl-Bonet necessary test to compute evidence, the Validity-Ratio reduces to the Bayes Factor (Kass and Raftery, 1995). The proof of the theorem follows from the structure of the generative meta-model and properties of the Pearl-Bonet necessary test.

Proof Let us first consider the ratio of marginal likelihoods of the two model classes.

| ML-Ratio | (8) |

Since the Pearl-Bonet test is a necessary test, we know that if the true data distributions are known. However, in practice, we will have a data sample and apply a statistical test. Therefore in some cases the test may return Fail even if and are satisfied, leading to the following expression for the numerator:

| (9) |

Further, for any causal model , we know with certainty whether it follows exclusion and as-if-random restrictions. In particular, . Using this observation, we can write as:

| (11) |

Similarly, the denominator can be expressed by,

| (12) |

where we use the conditional independencies entailed by the generative meta-model.

Combining Equations 3.2, 3.2 and 3.2, we obtain the ratio of marginal likelihoods:

| ML-Ratio | (13) |

Finally, by definition of model classes and , they correspond to valid and invalid classes of causal models. Thus,

| (14) |

The above two equations lead us to the main statement of the theorem:

| (15) |

As with the Bayes Factor, estimation of the Validity-Ratio depends on the prior on causal models because the model is not identified. Since the configuration of Exclusion and As-if-random conditions does not provide any more information apart from restricting the class of causal models, we can assume a uninformative uniform prior on causal models within each of the Valid-IV and Invalid-IV classes. If sufficient data is available, one may use the fractional Bayes Factor (O’Hagan, 1995) to split the sample and use the first subsample to find a prior on causal models using data likelihood, and the second to estimate the Validity Ratio. We discuss the effect of using other model priors in Section 8. Using a uniform model prior leads to the following corollary.

Corollary 2

Using a uniform model prior for valid-IV models, for invalid-IV models, the Validity-Ratio from Theorem 1 reduces to:

| Validity-Ratio | (16) |

where and are normalization constants.

3.3 NPS Algorithm for testing IVs

Based on the above theorem, we present the NPS algorithm for testing the validity of an instrumental variable below. Assume that the observational dataset contains values for three discrete variables: cause , outcome and a candidate instrument .

-

1.

Estimate using observational data and run the Pearl-Bonet necessary test. If the necessary test fails, Return REJECT-IV.

-

2.

Else, compute the Validity-Ratio from Equation 1 for the one or more of the following types of violations (can exclude violations that are known apriori to be impossible):

-

•

Exclusion may be violated:

-

•

As-if-random may be violated:

-

•

Both may be violated:

-

•

-

3.

If all Validity Ratios are above a pre-determined threshold , then return ACCEPT-IV. Else if any Validity Ratio is less than , then return REJECT-IV. Else, return INCONCLUSIVE.

Although the NPS algorithm seems straightforward, in practice, the first two steps involve a number of smaller steps that we discuss in the next two sections. Section 4 describes how to compute the Validity Ratio for the three kinds of violations listed above and Section 5 discusses extensions of the Pearl-Bonet test that enable its empirical application to discrete variables.

4 COMPUTING THE VALIDITY RATIO

The key detail in implementing the NPS test is in evaluating the integrals in Equation 1, since there can be infinitely many valid-IV or invalid-IV causal models. In this section we first present the response variables framework from Balke and Pearl (1994) that provides a finite representation for any non-parametric causal model with discrete , and . We then extend this framework to also work with invalid-IV causal models. Armed with this characterization, we describe methods for computing the Validity-Ratio in Section 4.2. Note that neither our finite characterization of causal models nor our methods for computing the integrals are unique; any other suitable strategy can be used to implement the NPS test.

4.1 The response variable framework

One way to characterize causal models is to assume specific functional relationships between observed variables, such as in the popular linear model for instrumental variables (Imbens and Rubin, 2015). In most cases, however, the nature of the functional form is not known and thus parameterization in this way arbitrarily restricts the complexity of a causal model. A more general way to make no assumptions on the functional relationships or the unobserved confounders, but rather reason about the space of all possible functions between observed variables. We will use this approach for characterizing valid-IV and invalid-IV causal models.

As an example, suppose we observe the following functional relationship between Y and X, , where the true causal relationship is . Conceptually, the variables are simply additional inputs to this function. Thus the effect of unobserved confounders can be seen as simply transformation the observed relationship to another function . However, it is hard to reason about this transformation because the confounders are unobserved and may even be unknown. Here we make use of a property of discrete variables that stipulates a finite number of functions between any two discrete variables. Because the number of possible functions is finite, the combined effect of unobserved confounders can be characterized by a finite set of parameters, without making any assumptions about . We will call these parameters response variables, in line with past work. Note that we make no restriction on U—they can be discrete or continuous—but instead restrict the observed variables to be discrete.

More formally, a response variable acts as a selector on a non-deterministic function and converts it into a a set of deterministic functions, indexed by the response variable. Depending on the value of the response variable, one of the deterministic functions is invoked. Under this transformation, the response variables become the only random variables in the system, and therefore any causal model can be expressed as a probability distribution over the response variables.

4.1.1 Response variables framework for valid-IV models

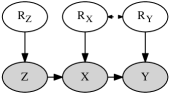

Let us first construct response variables for a valid-IV model, as in Balke and Pearl (1994). To do so, we will transform to a different response variable for each observed variable in the causal model. For ease of exposition, we will assume that , and are binary variables; however, the analysis follows through for any number of discrete levels.

For valid-IV causal models, we can write the following structural equations for observed variables , and (from Equation 1).

| (17) |

where , and represent error terms. and are correlated. As-if-random condition () stipulates that . Exclusion condition is satisfied because function does not depend on .

Since there are a finite number of functions between discrete variables, we can represent the effect of unknown confounders as a selection over those functions, indexed by a variable known as a response variable. For example, in Equation 4.1.1, can be written as a combination of 4 deterministic functions of , after introducing a response variable, .

| (18) |

That is, different values of U change the value of Y from what it would have been without U’s effect, which we capture through . Intuitively, these refer to different ways in which individuals may respond to the treatment . Some may have no effect irrespective of treatment(), some may only have an effect when (), some may only have an effect when X=0 (), while others would always have an effect irrespective of (). Such response behavior, as denoted by , is analogous to never-recover, helped, hurt, and always-recover behavior in prior instrumental variable studies (Heckerman and Shachter, 1995).

Similarly, we can write a deterministic functional form for , leading to the transformed causal diagram with response variables in Figure 4a.

| (19) |

Similar to , can be interpreted in terms of a subject’s compliance behavior to an instrument: never-taker, complier, defier, and always-taker (Angrist and Pischke, 2008).

Finally, can be assumed to be generated by its own response variable, .

| (20) |

Trivially, .

Given this framework, a specific value of the joint probability distribution defines a specific, valid causal model for an instrument . Exclusion condition is satisfied because the structural equation for does not depend on Z. For as-if-random condition, we additionally require that . Since and represent the effect of as shown in Figure 4a, the as-if-random condition translates to , implying that . Using this joint probability distribution over , , and , any valid-IV causal model for , and can be parameterized. For instance, when all three variables are binary, , and will be 2-level, 4-level and 4-level discrete variables respectively. Therefore, each unique causal model can be represented by 2+4x4=18 dimensional probability vector where each . In general, for discrete-valued Z, X and Y with levels , and respectively, will be a -dimensional vector.

4.1.2 Response variable framework for invalid IVs

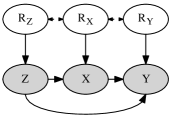

While past work only considered Valid-IV models, we now show that the same framework can also be used to represent invalid-IV models. As defined in Section 3.1, a causal model is invalid when either of the IV conditions is violated: Exclusion or As-if-random.

Exclusion is violated

When exclusion is violated, it is no longer true that . This implies that may affect Y directly. To account for this, we redefine the structural equation for to depend on both and : . This corresponds to adding a direct arrow from to as shown in Figure 4b. In response variables framework, this translates to:

| (21) |

where now has 16 discrete levels, each corresponding to a deterministic function from the tuple to .

As with valid-IV causal models, any invalid-IV causal model can be denoted by a probability vector for and . However, the dimensions of the probability vector will increase based on the extent of Exclusion violation. For full exclusion violation, dimensions will be .

As-if-random is violated

Violation of as-if-random does not change the structural equations, but it changes the dependence between and . If as-if-random assumption does not hold, then is no longer independent of . Therefore, we can no longer decompose as the product of independent distributions and and dimensions of will be .

Both exclusion and as-if-random are violated

In this case the structural equation for is given by Equation 21 and is not independent of . Thus the dimensions of increase to .

4.2 Computing marginal likelihood for Valid-IV and Invalid-IV models

The response variable framework provides a convenient way to specify an individual causal model: choosing a causal model is equivalent to sampling a probability vector from the joint probability distribution , , . The dimensions of this probability vector will vary based on the extent of violations of the instrumental variable conditions, from for the valid-IV model to for invalid-IV model in which both exclusion and as-if-random conditions are violated. Below we describe how to compute the validity ratio for a given observed dataset.

-

•

Only Exclusion may be violated: Assume . Sample , separately. Use Equation 33 to compute marginal likelihood .

-

•

Only As-if-random may be violated: Assume . Sample as a joint distribution. Use Equation 35 to compute marginal likelihood .

-

•

Both conditions may be violated: Assume . Sample as a joint distribution. Use Equation When both are violated to compute marginal likelihood

To compute the Validity-Ratio, we return to Equation 2.

| Validity-Ratio | (22) |

To compute the integrals in the numerator and the denominator of the above expression, we utilize the fact that there can be a finite number of unique observed data points (Z, X, Y) when all three variables are discrete. For example, for binary Z, X and Y, there can be 2x2x2=8 unique observations. In general, the number of unique data points is . Making the standard assumption of independent data points, we obtain the following likelihood for any causal model ,

| (23) |

where N is the number of observed data points and the number of times each unique value of repeats in the dataset. Since the model can be equivalently represented by its probability vector , we can rewrite the above equation as:

| (24) |

For illustration, we derive the closed form expressions for the numerator and denominator of Equation 22 when all variables are binary, in Appendix A. In general the method works for any number of discrete levels.

Finally, based on the above details, Algorithm 1 summarizes the algorithm for computing validity ratio for any observed dataset.

5 EXTENSIONS TO THE PEARL-BONET TEST

In this section we describe extensions to the Pearl-Bonet test that are required for empirical application of the test for discrete variables. First, we present an efficient way to evaluate the necessary test for any number of discrete levels. Second, we show how to extend the monotonicity condition to more than two levels. Third, we discuss how to use the test in finite samples, by utilizing an exact test proposed by Wang et al. (2016).

5.1 Implementing Pearl-Bonet test for discrete variables

Specifying a closed form for the necessary test becomes complicated when we generalize from binary to discrete variables. Bonet (2001) showed that Pearl’s instrumental inequalities for binary variables do not satisfy the existence requirement from Section 2 and more inequalities are needed. Further, it is not always feasible to construct analytically all the necessary inequalities for discrete variables.

To derive a practical test for IVs with discrete variables, we employ Bonet’s framework that specifies Valid-IV and Invalid-IV class of causal models as convex polytopes in multi-dimensional probability space. In Figure 2, we showed a schematic of Bonet’s framework, representing Valid-IV and Invalid-IV classes as polygons on a 2D surface. We now make these notions precise. The axes represent different dimensions of the probability vector . Assuming discrete levels for , for and for , will be a dimension vector, given by:

| (25) |

may be either discrete or continuous, we do not impose any restrictions on unobserved variables. Any observed probability distribution over , and can be expressed as a point in this -dimension space. Since , the extreme points of for valid probability distributions are given by . We showed a square region as the set of all valid probability distributions in Figure 2, but more generally the region constitutes a -dimensional convex polytope (Bonet, 2001).

Based on the models defined in Figure 1, the set of all valid probability distributions can be generated by Invalid-IV class of models. Within that set, we are interested in the probability distributions that can be generated by a valid-IV model. Knowing this subset provides a necessary test for instrumental variables; any observed data distribution that cannot be generated from a valid-IV model fails the test. Bonet showed that such a subset forms another convex polytope (the Valid-IV region in Figure 2) whose extreme points can be enumerated analytically. However, he did not provide an efficient way to check whether a given data distribution lies within this polytope. Below we provide an approach for checking this, thus yielding a practical implementation for a necessary test for discrete variables.

Theorem 3

Given data on discrete variables , and , their observational probability vector , and extreme points of the polytope containing distributions generatable from a Valid-IV model, the following linear program serves as a necessary and existence test for instrumental variables:

| (26) |

where represents -dimensional extreme points of and are non-negative real numbers. If the linear program has no solution, then the data distribution cannot be generated from a Valid-IV causal model.

Proof

The proof is based on properties of a convex polytope, which is also a convex set. A point lies inside a convex polytope if it can be expressed as a linear combination of the polytope’s extreme points. Therefore, an observed data distribution could not have been generated from a Valid IV model if there is no real-valued solution to Equation 26.

While the test works for any discrete variables, in practice the test becomes computationally prohibitive for variables with large number of discrete levels, because the number of extreme points grows exponentially with , and . If the number of discrete levels is large, we can an entropy-based approximation instead, as in Chaves et al. (2014).

5.2 Extending Pearl-Bonet test to include Monotonicity

Monotonicity is a common assumption made in instrumental variables studies, so it will be useful to extend the necessary test for discrete variables when monotonicity holds. No prior necessary test for monotonicity exists for discrete variables with more than two levels, so here we propose a test for monotonicity that can be used in conjunction with Theorem 3.

As defined in Section 2.1, monotonicity implies that:

| (27) |

That is, increasing can cause to either increase or stay constant, but never decrease. Note that the above definition is without any loss of generality. In case has a negative effect on , we can do a simple transformation by inverting the discrete levels on so that Equation 27 holds.

By requiring this constraint on the structural equation between and , monotonicity restricts the observed data distribution. We use this observation to test for monotonicity.

Theorem 4

For any data distribution generated from a valid-IV model that also satisfies monotonicity, the following inequalities hold:

| (28) |

where , and are ordered discrete variables of levels , and respectively and .

5.3 Finite sample testing for Pearl-Bonet test

Finally, Pearl-Bonet test assumes that we can infer conditional probabilities accurately. However, in any finite observed sample, we will only be able to compute a sample probability estimate. Therefore, we need a statistical test that accounts for the finite sample properties of any observed dataset. There are many tests proposed to deal with finite samples, such as by Kitagawa (2015); Huber and Mellace (2015); Wang et al. (2016); Ramsahai and Lauritzen (2011). In this paper we use an exact test proposed by Wang et al. (2016), both for its simplicity and because it makes no assumptions about the data-generating causal models. This test converts the inequalities of the necessary test into a version of one-tailed Fisher’s exact test. As with all null hypothesis tests, the goal is to refute the null hypothesis. Here the null hypothesis is that the conditional probability distribution satisfies the inequalities of the Pearl-Bonet test. We then quantify the likelihood of seeing the obseved data under this null hypothesis, thus providing us with a p-value for the test. Because we are testing 4 inequalities at once, our analysis can be prone to multiple comparisons. Therefore, Wang et al. recommend a significance level of for each test, where is the desired significance level.

However, this test does not work under monotonicity assumption. We extend their method for monotonicity, by using the same transformation to convert monotonicity inequalities to the Fisher’s exact test. Again, to prevent false positives due to multiple comparisons, it would be ideal to choose a smaller significance level for each inequality, but the results we present are without any correction.

6 SIMULATIONS: HOW POWERFUL IS THE NPS TEST?

We now report simulation results for the NPS test, with the goal of determining the extent to which NPS test can distinguish between a valid and invalid instrumental variable. We evaluate the two parts of the NPS test separately. First, we present simulations for testing the power of the Pearl-Bonet necessary test for different violations of the IV assumptions, and then move on to evaluating the Validity Ratio for simulated datasets.

6.1 Evaluating the necessary test

Since the Pearl-Bonet test is a necessary test, it can admit datasets generated by Invalid-IV models. Therefore, here our goal is to estimate how often data generated by Invalid-IV models pass the Pearl-Bonet test. To do so, we consider different Invalid-IV models and check whether observed data distributions generated from these models pass the test. Instead of testing on a particular Invalid-IV model, we consider simulations over types of causal models that one might encounter in empirical IV studies. That is, we consider different model configurations based on key properties of an IV causal model such as the strength of the instrument, monotonicity of relationship between the instrument and outcome, and similarly between the cause and outcome. Under each of these model configurations, we would like to know how likely it is that an instrument is valid, given that it passes the Pearl-Bonet necessary test.

We consider model configurations in each of the three types of violations: exclusion, as-if-random, and both violated. For exclusion, we start with two cases—when the instrument has a monotonic effect on the outcome, and when both instrument and cause have a monotonic relationship with outcome—and construct different configurations as we vary the strength of these relationships. These model configurations are motivated by encouragement design studies (West et al., 2008; Sovey and Green, 2011), where it is plausible to assume a non-decreasing relationship between the instrument and outcome. We then relax the non-decreasing assumption to study more general scenarios. For as-if-random, we consider configurations based on the strength of relationship between confounders and the instrument, or equivalently, between response variables for the instrument on the one hand, and the cause and outcome on the other. Finally, we consider configurations where both exclusion and as-if-random are violated.

For all model configurations, we sample uniformly at random invalid-IV causal models each. We do so by identifying the specific violation in each configuration and then using the appropriate conditions on response variables from Section 4.1.2. In effect, we sample response variables to sample different causal models. Then, for each causal model, we generate the true probabilities, required to evaluate the Pearl-Bonet test, using the corresponding response variables. We compute true probabilities instead of sampling a dataset, to eliminate errors in estimating probabilities from data (due to sampling variation in simulating a dataset of from each model). Finally, we compute the fraction of invalid-IV causal models that pass the Pearl-Bonet necessary test for each model configuration.

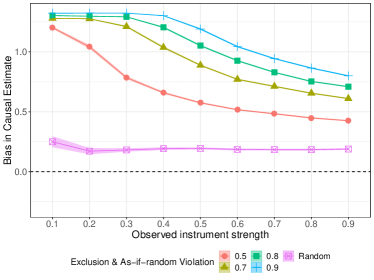

In addition to checking IV validity, we also estimate the resultant bias in the IV estimate, when using data distribution from an invalid-IV causal model. It could be possible that an instrument is invalid in the strict sense defined above, but still provides a causal estimate with low bias. To estimate the causal effect , we use the Wald estimator (Wald, 1940), which for binary variables, can be written as (Balke and Pearl, 1993):

Because the causal effect between binary variables ranges from , we bound the estimate within this interval. We will compare the effectiveness of the Pearl-Bonet test at different values of instrument strength, which is defined as . Note that the instrument strength also appears in the denominator of the Wald estimator.

We characterize the response variables for Valid-IV and Invalid-IV models below.

Valid-IV: Both conditions are satisfied

When both Exclusion and As-if-random conditions are satisfied, is a 4-level discrete variable as in Equation 18. Because , we sample independently and separately sample the joint distribution vector of .

Invalid-IV: At least one of the conditions is violated

When as-if-random assumption is not violated (such as when is randomized), we sample independently as for a Valid-IV model. However, since Exclusion may be violated, will be a 4x16-level discrete variable as in Equation 21. Otherwise, if Exclusion is not violated, then remains a 4-level discrete variable. However, is no longer independent of because as-if-random may be violated. Therefore, we will sample a joint probability distribution vector from all possible joint probability vectors. Since our goal is to only generate invalid IV models, we reject any generated probability vector where turns out to be independent of . When both conditions are violated, is a 16-level discrete variable and is not independent of . Thus, we sample a (2x4x16)-dimensional probability vector .

For all simulations, we assume that , and are binary variables. Further, since monotonicity is a required assumption for obtaining the interpretation of a local average causal effect (Angrist and Imbens, 1994), we also assume monotonicity throughout. Below we present results separately for the three kinds of violations of the IV conditions: exclusion only, as-if-random only, and both violated.

6.1.1 Exclusion may be violated

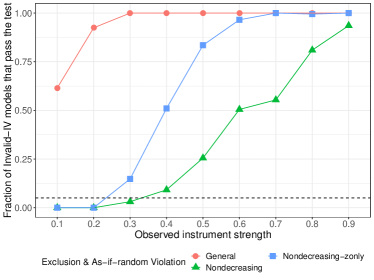

We first test for violation of exclusion only. That is, we assume that as-if-random is satisfied (e.g. through random assignment). As described in Section 4.1.2, violation of the exclusion restriction implies that and thus there can be 16 different levels. Following the NPS Algorithm, we sample and jointly and sample independently.

The remaining detail is how to sample invalid-IV models that violate exclusion condition. This is non-trival because the degree of violation of the exclusion restriction can vary based on known properties of the underlying causal model. We take one of the simplest properties of the unobserved true causal model—the direction of effect from Z or X to Y—and characterize the power of the Pearl-Bonet test as we vary this property. First we will consider a scenario where either of or has a non-decreasing effect on and then gradually weaken this requirement to obtain a more general scenario. This is motivated by encouragement design IV studies where we may know apriori that or have a non-decreasing effect on because there is no plausible mechanism that leads to a decrease in with increase in or .

However, in other studies, completely ruling out model configurations where the non-decreasing property does not hold is too strong a condition. We therefore relax this restriction and instead stipulate the percentage of data points where this restriction is satisfied. We do so by fixing the probability of the relevant response variables which correspond to a nondecreasing effect. Driving this percentage down to 50% essentially provides the general case, where the direction of the effect from Z to Y is equally likely to be positive or negative.

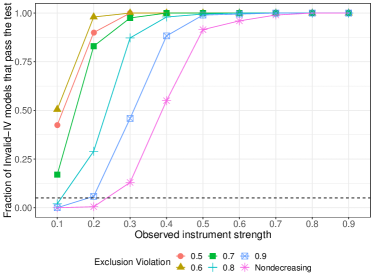

Extent of non-decreasing effect of instrument on outcome

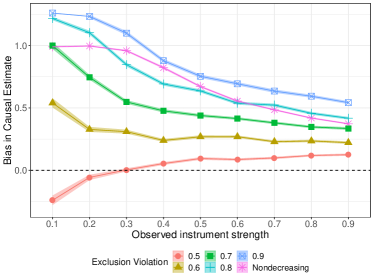

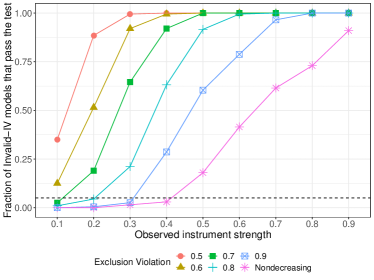

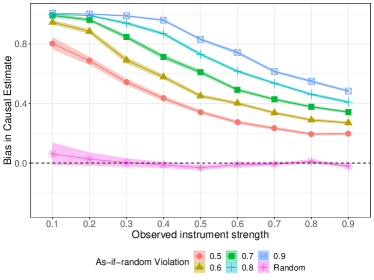

First, we simulate the model configurations where exclusion is violated by varying the extent to which has a non-decreasing effect on . Let us first consider the scenario where the non-decreasing effect is strict: the instrument cannot cause the outcome to decrease. Figure 6a shows the fraction of such Invalid-IV models that pass the test at varying observed instrument strength (marked as the ‘Nondecreasing’ line). At low instrument strength, less than 5% of invalid-IV models pass the necessary test. This simulation result indicates that if we observe empirically that a weak instrument passes the necessary test, it is likely to be a valid instrument assuming that cannot decrease . However, as instrument strength increases, utility of the Pearl-Bonet test decreases.

To relax the non-decreasing assumption, we simulate -non-decreasing cases such that fraction of the units have a non-decreasing relationship; the rest do not. When , there is an equal chance of Z decreasing or increasing the value of Y. Each of the different lines in Figure 6a corresponds to a class of Invalid-IV models with a specified probability of non-decreasing effect between Z and Y. We observe that the utility of the Pearl-Bonet test decreases as decreases. Even at , however, the test is only able to identify invalid-IV models with less than error for instruments with strength less than or equal to . When non-decreasing relationship does not exist (e.g., ), the test performs poorly and cannot identify an invalid-IV model reliably. Thus, as we relax the strictness of the non-decreasing effect assumption, more invalid-IV models are passed by the necessary test and thus the test remains inconclusive.

Contrasting these results with estimated bias in the Wald estimate of the causal effect provides more context. Even when the test is unable to detect violation of exclusion, it is also likely that the bias is relatively low (Figure 6b). The magnitude of the bias is larger for weak instruments and for higher values of , both scenarios where the Pearl-Bonet test is the most discriminative. When the observed strength of the instrument is high, even clearly invalid-IV models lead to comparatively lower bias (less than ).

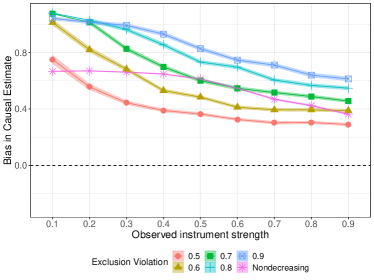

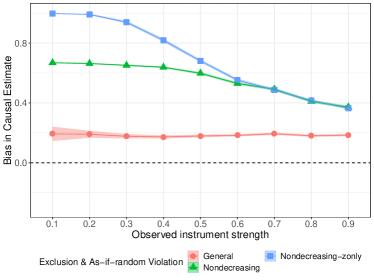

Extent of non-decreasing effect of both instrument and cause on outcome

In some IV studies, we may know that both instrument and cause have a non-decreasing effect on the outcome. In such cases, we can strengthen the above assumption by assuming that both and have a non-decreasing effect on . Figure 6c shows the fraction of invalid-IV models that pass the Pearl-Bonet test under these conditions. When the non-decreasing condition is satisfied strictly—that is, neither Z nor X can have an increasing effect on Y—less than 5% of invalid-IV models pass the test up to a maximum instrument strength of . The discriminatory power of the Pearl-Bonet test for other scenarios also increases compared to Figure 6a. For thresholds of non-decreasing effect at least , fraction of incorrectly identified Invalid-IV models lies below at instrument strength of 0.1. Similar to the previous results for bias, Figure 6d shows that bias is highest for weak instruments or when the probability of having a non-decreasing effect is the highest. Happily, in both of these situations, the Pearl-Bonet test is the most effective at filtering out Invalid-IV models.

The lack of Pearl-Bonet test’s effectiveness with a strong instrument is not surprising: in the limit, could be identical to X (an experiment with full compliance) and then Pearl-Bonet test inequalities (Equation 3) are satisfied trivially because the RHS will be 0. Clearly, these inequalities will be most discriminative when the instrument is weak. As we will see, this pattern will be consistent in the all results we obtain. Similarly, we saw that bias in the causal estimate is highest for weak instruments; this trend also repeats across our simulations, consistent with past results that show even small violations in IV conditions can lead to big finite sample biases in the IV estimates, especially when the instrument is weak (Bound et al., 1995).

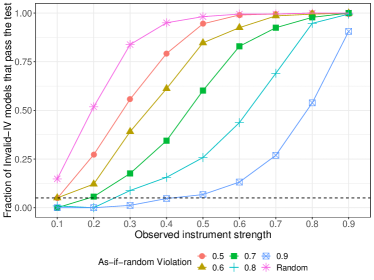

6.1.2 As-if-random may be violated

Violation of the as-if-random condition implies that is not independent of and . Here we assume that Exclusion is not violated. Following Algorithm 1, we generate a joint distribution over , and variables, sampling them uniformly at random. As with the exclusion restriction, there can be a number of ways to define the strength of an as-if-random violation, depending on how we specify the dependence between , and . For the results presented, we define the strength of the violation as the mutual information between and . When as-if-random is satisfied, mutual information will be zero. As we increase the mutual information, violation of as-if-random is expected to become more and more severe. Since correlation between and is necessary and sufficient for a violation of the as-if-random condition (but not correlation between and ), we modulate the severity of violation by changing the correlation between and . To do so, we vary a single conditional probability, for simplicity; similar results can be obtained by varying other probabilities. We choose because of the intuitive property that when it is high, Z and Y will also be highly correlated.

Figure 7a shows the results of the Pearl-Bonet test when as-if-random condition is violated. When we sample uniformly at random, the test is unable to distinguish effectively between invalid-IV and valid-IV models. Even at low values of instrument strength (), nearly half of invalid-IV models pass the Pearl-Bonet test. However, we also see the Wald estimator is reasonably accurate at all levels of instrument strength, even though the as-if-random condition is not satisfied. This indicates that complete uniform sampling of causal models does not introduce a strong enough as-if-random violation to be either detected by the test or result in a noticeable biased estimate.

When the mutual information is increased beteen and , we find that the discriminatory power of the Pearl-Bonet test increases. When the mutual information threshold is , instruments with strength up to 0.2 have an errror rate of roughly . Thus, the test is more powerful for stronger violations of the as-if-random assumption. That said, the test is unable to capture all violations that lead to noticeable bias. For instance, at a threshold of , bias in the causal estimate can be as high as , but the necessary test is unable to detect invalid-IV models more than of the time.

6.1.3 Both exclusion and as-if-random may be violated

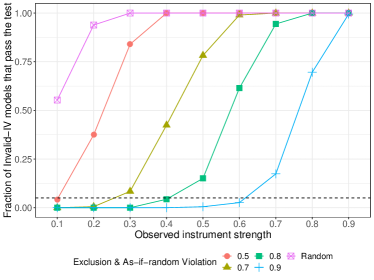

Finally, we consider the case when both conditions may be violated. First, let us consider the straightforward case when both exclusion and as-if-random violating models are uniformly sampled. The red line in Figure 8a shows that the Pearl-Bonet test performs poorly for such invalid-IV models; even for weak instrument strength, the test can correctly identify invalid-IV models less than of the time. Fortunately, the bias is also negligible (Figure 8b), indicating that uniform violation does not lead to a noticeable bias in causal IV estimates.

When we stipulate that Z can only have a non-decreasing effect on Y, as in the above subsection, discriminatory power of the test improves. The error rate for identifying invalid-IV models is less than for instruments with strength up to 0.2. However, the bias also shoots up. When the observed instrument strength is high (say 0.5), bias in the causal estimate is over 0.6, but the necessary test can correctly identify an invalid-IV model less than of the time. Assuming that both and have a non-decreasing effect on Y provides slightly better results. Instruments of strength up to have error rates nearly 5% and the bias also decreases.

When we modulate the severity of the as-if-random condition (while keeping exclusion violation uniformly at random), the utility of the Pearl-Bonet test improves substantially (Figure 8c). For thresholds at least , the test misses less than of the invalid-IV models at an instrument strength of . Bias is also high for these thresholds, but we have a higher chance of correctly filtering out invalid-IV models.

6.1.4 Summary of results

Two key patterns emerge. First, the test is more powerful in recognizing violations that also lead to a substantial bias. This is encouraging because the kind of violations that bias the causal estimate are exactly the invalid-IV datasets we want to eliminate. On average, these results suggest that when the Pearl-Bonet test is inconclusive, it is unlikely that applying the Wald Estimator will lead to substantial bias in the causal estimate. Conversely, in cases when the Pearl-Bonet test has high discriminatory power, eliminating invalid-IV data models will avoid computing Wald Estimates with high bias.

Second, the above results show that detecting the violation of IV conditions is sensitive to the strength of the instrument. This may seem as a big limitation; however, in most observational studies, instruments with high strength are rare. For instance, in economics, (Staiger and Stock, 1994) recommend an F-value of to prevent weak instrument bias. At such a low value for , the instrument is likely to have to low correlation with X. Similarly, in epigenetics, of 0.1 between Z and X is typical (Pierce et al., 2010). In these low strength regimes, the Pearl-Bonet test can be effective in testing for validity of an instrumental variable.

6.2 An example open problem for binary instrumental variables

The above results are indicative and they do not provide evidence on how the NPS test will perform on a particular single dataset. Moreover, computing the Validity-Ratio for datasets that pass the Pearl-Bonet test can further improve effectiveness in detecting Valid-IV models. Therefore, we now simulate datasets and check whether estimating the Validity Ratio can correctly identify whether they contain a valid instrumental variable or not. To start with, we consider the following causal model from Palmer et al. (2011) where the Pearl-Bonet necessary test fails to detect violation of IV assumptions.

| (29) |

where , , are the instrument, cause and outcome respectively and all variables are binary. There can be three possible datasets depending on which Y is chosen as the outcome: , ,. is a valid instrument only when the outcome is , not for and because they violate the exclusion restriction. Although Pearl-Bonet test is able to rule out as an invalid-IV dataset, Palmer et al. find that it is inconclusive for and .

We validate the same three datasets using the NPS test by simulating 2000 data points from each of their causal models. Table 1 shows that comparing Validity-Ratio can be used to identify the datasets for which is a valid instrument. We assume a uniform prior over models within valid-IV and invalid-IV model classes and use the equation from Corollary 2. Further, in the absence of any additional information, we can assume an equal probability of the instrument being valid or invalid (). The second and third columns show the log marginal likelihood for invalid-IV models when either of exclusion or as-if-random is violated. This leads to the Validity Ratio shown in the fifth column, as a ratio of marginal likelihood of the Valid-IV model class over marginal likelihood of the Invalid-IV model class. Validity Ratio is the highest (nearly 20) for and the lowest () for , thereby clearly distinguishing between the two datasets. Dataset has a Validity Ratio less than 1, indicating that it is less likely to be a valid instrument, especially in comparison to dataset .

In practice, a common goal is to select a single instrument among multiple candidate instruments. Results from the NPS test indicate that should be chosen; it has the highest Validity-Ratio among candidate datasets. Further, given that the Validity-Ratio is greater than 1, it is also likely to be a valid instrument. In general, to determine validity, one way would be to prespecify standard thresholds for the Validity-Ratio above which an instrument is valid, as suggested by Kass and Raftery (1995). However, we deliberately refrain from providing standard thresholds, because the judgment for validity of an instrument will anyways depend on the prior assumed for Invalid-IV and Valid-IV model classes. We recommend instead to interpret the ratio of marginal likelihoods as a benchmark for priors: a Validity Ratio of assuming uniform priors indicates that for to be an invalid-IV dataset, a researcher’s prior on finding an invalid-IV dataset should be at least times as strong as the prior for valid-IV dataset. In addition, note that the Validity-Ratio may also be sensitive to the assumption of uniform priors over models within invalid-IV and valid-IV classes. We leave exploration of other priors over models for future work.

| Log Marginal Likelihood | ||||

|---|---|---|---|---|

| Dataset | Exclusion Violated | As-if-random Violated | Valid IV | Validity Ratio |

| -3080 | -3086 | -3077 | 20.1 | |

| -3168 | -3161 | -3163 | 0.13 | |

| -3366 | -3367 | -3397 | x | |

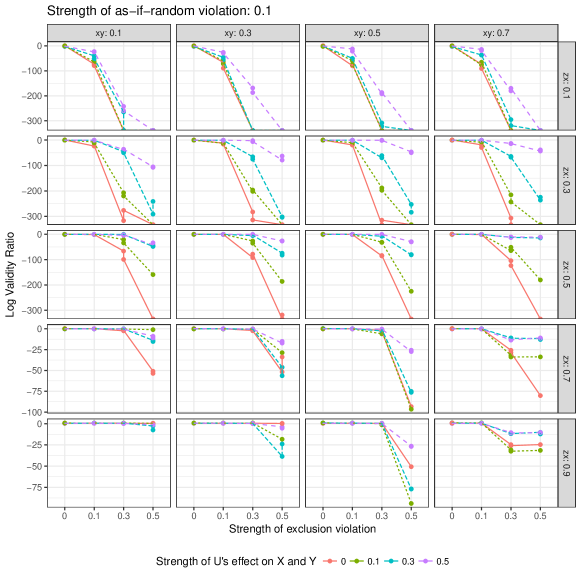

6.3 Simulating a broad range of binary datasets

Motivated by the example from Palmer et al. (2011), we now construct a set of datasets that cover a broad spectrum of possible datasets with binary variables. We do so by changing the parameters of the Palmer et al.’s example model presented above. Z and U are generated from a Bernoulli distribution as before, but parameter for effect of Z on X can have five different values: . Similarly, the effect of X on Y takes values in this set. Each of U’s effect on X, U’s effect on Y, U’s effect on Z, and Z’s effect on Y takes on values from the set . For simplicity, we assume that U’s effect on X and Y is the same. Combined, these parameters lead to 5x5x4x4x4=1600 simulations, each of which yields a different causal model. From each causal model, we generate an i.i.d. dataset with size=50000 of tuples.

These simulated datasets span the range of datasets with a valid or invalid instrument. When the parameters for the effect of U on Z and the effect of Z on Y are zero, the causal model contains a valid instrument. Otherwise, it contains an invalid instrument. We make the same assumptions as before: equal prior probability of an invalid or valid instrument, and a uniform prior over causal models within both Valid-IV and Invalid-IV model classes. On each dataset, we compute the Validity-Ratio using the equation from Corollary 2.333Unlike the NPS algorithm, here we compute the Validity-Ratio for all datasets for comparison, irrespective of whether they pass the Pearl-Bonet necessary test.

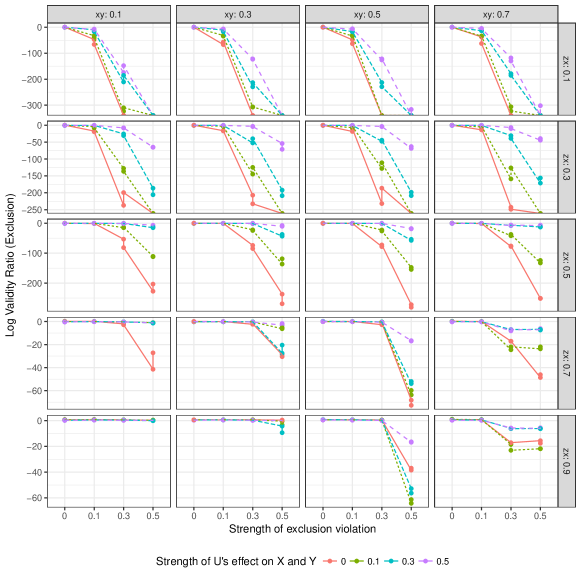

6.3.1 NPS test can detect exclusion violation, except when instrument is strong

We first look at violation of the exclusion restriction. For this case, we consider all datasets where as-if-random is satisfied (i.e., effect of on is zero). Figure 9 shows the log Validity-Ratio as the strength of the exclusion violation is increased. We find that when the parameter for effect of Z on X (instrument strength) is below 0.5, Validity Ratio is below 1 consistently even for minor violation of the exclusion restriction. This holds true even as the true causal effect is varied: scanning horizontally through the rows shows a similar trend. In addition, the detectability of exclusion violation depends on the effect of confounders U on X and Y. When confounders do not affect X and Y (red line), Validity Ratio is the most sensitive to violations of exclusion. As the effect of confounders increases, Validity Ratio becomes less sensitive in detecting exclusion violation. In addition to detecting violations, the NPS test also correctly returns a Validity Ratio close to 1 or higher for valid instruments. The mean Validity-Ratio across all valid instruments is 1.8, with a maximum value of 12. There are some valid-IV models for which the Validity-Ratio falls below 1, but in all cases it is higher than 0.3 (or roughly, -1 on the log scale).

Above results indicate that exclusion can be tested by inspecting the Validity-Ratio as long as the instrument is not too strong (effect parameters ). Further, the NPS test is able to identify violation of the exclusion restriction best when there is little confounding between X and Y. However, this is still a secondary effect and even at a confounding effect of U on X and Y at 0.5, the NPS test can successfully identify instruments that violate exclusion.

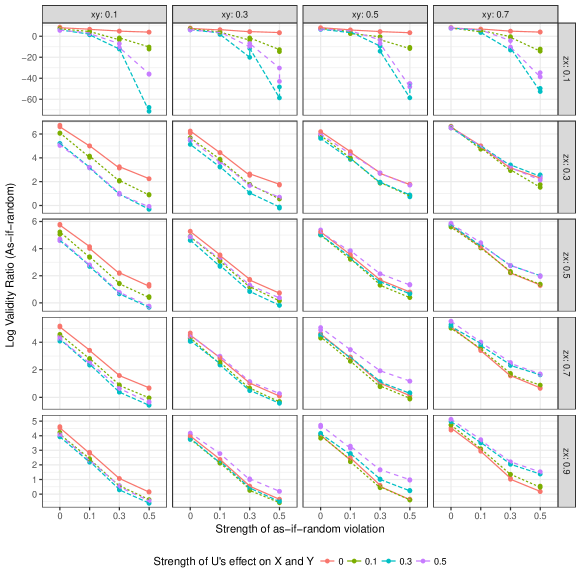

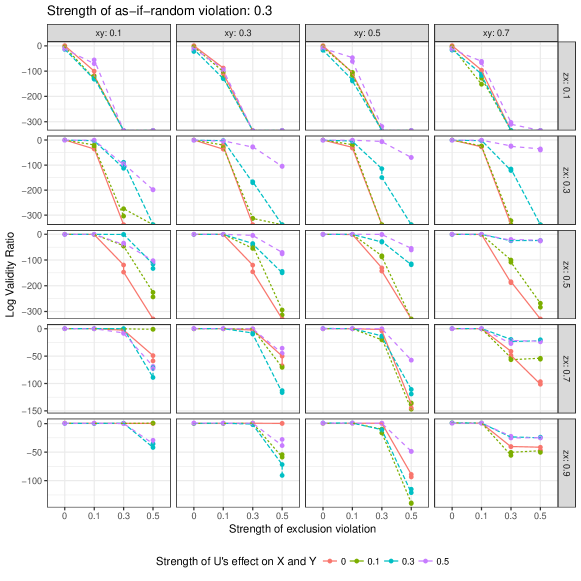

6.3.2 As-if-random is hard to detect, except when instrument is very weak

Next, we look at violation of the as-if-random restriction only. For this case, we consider all datasets where the exclusion condition is satisfied (i.e., effect of Z on Y is zero). The obtained log Validity-Ratio as the parameter for effect of U on Z is varied is shown in Figure 10. We find that violation of the as-if-random is harder to detect than exclusion. When the instrument is very weak (effect parameter for Z on X is 0.1), the Validity-Ratio goes below 1 as the strength of as-if-random violation is increased. This result is consistent even as the direct causal effect from X to Y is varied. Interestingly, the detection of a violation is better when there is a strong confounding effect of U on X and Y, and worse when the confounding effect is near zero. We conjecture that this is because the test is trying to detect an effect of U on Z and it is helpful if U also has a non-trivial on X and Y to gain comparison from. As for the exclusion assumption above, Validity-Ratio for datasets with a valid instrument is close to or higher than 1, indicating that they are probably valid.

However, in the case where instrument strength increases to 0.3 and above, the Validity Ratio stays above 1 even when as-if-random is violated. As we found in Section 6.1.2, these results indicate that the NPS test is unable to detect violations of the as-if-random assumption. As in that section, it is also likely that violations of as-if-random assumption lead to lesser bias in causal estimation than the exclusion assumption.

6.3.3 Violations of both assumptions is easier to detect

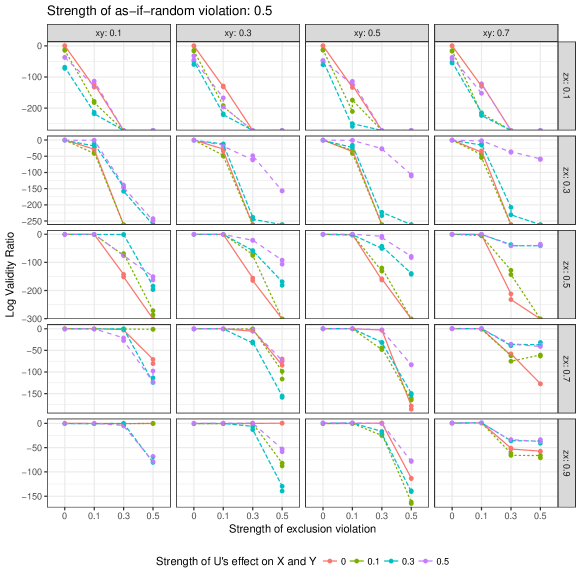

Finally, we look at the case when both exclusion and as-if-random are violated. Here we considered all simulated datasets. Figure 14 shows the log Validity-Ratio as the strength of exclusion violation varies, for a fixed as-if-random violation of 0.5 (i.e., the parameter for U’s effect on Z is 0.5). When both exclusion and as-if-random are violated, it becomes easier to identify datasets with invalid instruments. Even when the is instrument is moderately strong (effect of Z on X is 0.7), we find that Validity Ratio quickly drops to less than 1 as the strength of exclusion violation increases. This pattern is consistent as the true causal effect of X on Y is varied across datasets. When the instrument’s effect on X is the strongest at 0.9, NPS test can still detect violations of exclusion with a severity higher than 0.3. Detection of invalid instruments becomes weaker as the strength of as-if-random violation is decreased. We include results for other values of the as-if-random violation (i.e., effect of U on Z) in Appendix C.

6.3.4 Summary of results

Overall, these results show that the NPS test can detect violations of exclusion, but violations of as-if-random are not detected as reliably. Further, if both exclusion and as-if-random are violated, the NPS test can detect them more easily. In all cases, distinguishing between an invalid and valid instrument is more reliable when the instrument’s effect on the cause is weak, as is the case with many observational studies. Finally, for all datasets that contained a valid instrument, the NPS test correctly returns a Validity Ratio close to or higher than 1, thus indicating the probable validity of the instrument.

7 USING NPS TEST TO VALIDATE PAST IV STUDIES

In this section we use the NPS test to evaluate empirical studies based on instrumental variables. We select two seminal and highly cited studies on instrumental variables and a sample of recent studies from a leading economics journal, American Economic Review.

7.1 Seminal IV studies on the effect of schooling on wages

Returns of schooling on future income was one of the first applications that instrumental variable studies were applied to. We apply the NPS test to two of the seminal instrumental variable studies (Angrist and Krueger, 1991; Card, 1993). These studies are both highly cited, yet concerns about their validity continue until today (Bound et al., 1995; Buckles and Hungerman, 2013). We show how the NPS test can provide evidence and help evaluate the instruments used in these studies.

7.1.1 Effect of compulsory schooling on future wages

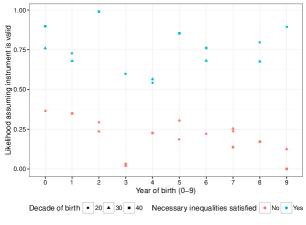

The first paper estimates the effect of compulsory schooling on future earnings of students Angrist and Krueger (1991). In the original analysis, is the quarter of birth, which was binarized to indicate that the student was either born in the first quarter or the last three quarters. is years of schooling and is the (log) weekly earnings of individuals. Using yearly cohorts, the authors define a separate instrumental variable for each year of birth. The causal effect of interest is the effect of years of schooling on future earnings.444Dataset available at http://economics.mit.edu/faculty/angrist/data1/data/angkru1991 Years of schooling and earnings are both reported as continuous numbers, in a bounded range. We follow the simplest discretization by binarizing both these variables at their mean. To check robustness against outliers, we also tried using median as the cutoff and obtained similar results.

As in the original paper, we first use the IV method without conditioning on any covariates. Applying the NPS Algorithm shows that nearly half of the instruments do not satisfy the inequalities of the necessary test. However, some of these may be due to sampling variability. At a significance level of , 3 yearly instruments do not pass the necessary test, as Figure 12a shows. This indicates that one or more of the three assumptions—monotonicity, exclusion and as-if-random—is violated, at least when all variables are binary. The null hypothesis in the necessary test is that an instrument is valid.

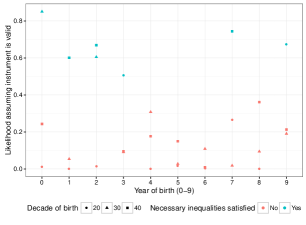

In practice, however, unconditional instrumental variables are rare. The original paper proceeds to construct conditional instrumental variables based on related covariates in the dataset. We replicate conditioning on covariates by implementing a “partialling out” technique (Baum et al., 2007). Based on the Frisch-Waugh-Lovell theorem, the partialling out technique provides the equivalent effect of conditioning on covariates, provided the underlying causal model is linear (which the authors assume). Figure 12b shows the results of the necessary test when all instruments are conditioned on covariates. Contrary to intuition, a bigger fraction of conditional instruments are now invalid at the significance level using the necessary test. Combined, our results on unconditional and conditional IVs suggest that many of the instruments used in the original analysis may not be valid, at least under the transformation when treatment and outcome are binarized. Note that these results do not necessarily invalidate the analysis in the paper: the instruments in the original data may still be valid when X and Y are continuous, as binarizing the variables can also lead to violation of one of the assumptions.

We also estimate the Validity Ratio for the instruments that pass the necessary test. We find that more than one quarter of the instruments have a Validity-Ratio lower than , with the minimum and maximum validity ratio being x and respectively. Thus, while some of the instruments may be probably valid, the NPS test indicates that many others are likely to be invalid. In this example study, the NPS test can be used to select the top-ranked probably valid instruments for analysis, and filter out the rest.

7.1.2 Return of college education on future earnings