Many Server Queueing Models with Heterogeneous Servers and Parameter Uncertainty with Customer Contact Centre Applications

Abstract

In this thesis, we study the queueing systems with heterogeneous servers and service rate uncertainty under the Halfin-Whitt heavy traffic regime. First, we analyse many server queues with abandonments when service rates are i.i.d. random variables. We derive a diffusion approximation using a novel method. The diffusion has a random drift, and hence depending on the realisations of service rates, the system can be in Quality Driven (QD), Efficiency Driven (ED) or Quality-Efficiency-Driven (QED) regime. When the system is under QD or QED regime, the abandonments are negligible in the fluid limit, but when it is under ED regime, the probability of abandonment will converge to a non-zero value. We then analyse the optimal staffing levels to balance holding costs with staffing costs combining these three regimes. We also analyse how the variance of service rates influence abandonment rate.

Next, we focus on the state space collapse (SSC) phenomenon. We prove that under some assumptions, the system process will collapse to a lower dimensional process without losing essential information. We first formulate a general method to prove SSC results inside pools for heavy traffic systems using the hydrodynamic limit idea. Then we work on the SSC in multi-class queueing networks under the Halfin-Whitt heavy traffic when service rates are i.i.d. random variables within pools. For such systems, exact analysis provides limited insight on the general properties. Alternatively, asymptotic analysis by diffusion approximation proves to be effective. Further, limit theorems, which state the diffusively scaled system process weakly converges to a diffusion process, are usually the central part in such asymptotic analysis. The SSC result is key to proving such a limit. We conclude by giving examples on how SSC is applied to the analysis of systems.

Lay Summary

Contact centres have been playing a more and more important role in the society. Almost everyone has to interact with contact centres such as airline companies, banks, and utility companies. For managers, how to make decisions to balance the cost and service quality of the contact centre becomes a significant problem. Thus we need to analyse call centre properties such as the probability of waiting, staffing costs, holding costs (for delayed customers) and rate of customers abandoning the service without getting service. In reality, servers are unlikely to be identical in such systems. There are many reasons which will cause heterogeneity among servers, such as personal skills, health and weather. Hence we focus on systems where service rates are random variables. We develop approximations of the systems to analyse the basic properties and how they behave when the system becomes large. We then show that under some assumptions, the dimensions of the system process will reduce while still keeping the essential information. So called state space collapse (SSC) results will simplify the analysis of the system and help us gain key insights using approximations.

Declaration

I declare that this thesis was composed by myself, that the work contained herein is my own except where explicitly stated otherwise in the text, and that this work has not been submitted for any other degree or professional qualification except as specified.

()

Acknowledgements

I would like to express deep gratitude to my supervisor : Dr. Burak Büke, without whom I would never come to Edinburgh to pursue a PhD degree. He taught me to do research from the very beginning, and helped me during all these years. He was always patient with me when I faced troubles in research, from basic mathematics to more advanced problems. I also would like to thank my second supervisor Dr. Tibor Antal, who has always been nice and humorous. Thank you for the research advices and being supportive during my study.

I would like to thank Gill Law and Iain Dornan, who provided plenty of assistance and made my study smooth enough. I am very thankful to the China Scholarship Council for funding my research. I also wish to thank the School of Mathematics for financial support which helped me through final stages of my study, as well as allowed me to attend many conferences and summer schools.

I would like to thank my examiners Dr. Gonçalo dos Reis and Dr. Rouba Ibrahim for their valuable comments and feedback.

I would like to thank my friends in Edinburgh for all of the priceless memories we created together, and for their kindness when I needed help, including Xavier Cabezas, Lena Freire, Hanyi Chen, Robert Gower, Marie Humbert, Saranthorn Phusingha(Mook), Minerva Martín de Campo, Ivet Galabova, Marion Lemery, Rodrigo Garcia, Nicolas Loizou, Xiling Zhang, Dominik Csiba, Başak Gever and many others. I would like to thank my flatmate Hongsheng Dong, who is always kind and willing to help. Special thanks to Tom Byrne for proofreading this thesis, and to Jakub Konečný, who offered tremendous help in every facet of my life during these four years.

There are no words that can express my feelings for Edinburgh. It is such a fantastic city that magically combines nature and culture, tranquility and vitality, antiquity and modernity. It is also an open-minded city that welcomes people with all kinds of backgrounds. I am so lucky that I could spend one of the most important period of my life in this romantic city with many amazing people from different culture. Thanks Edinburgh.

Chapter 1 Introduction and Literature Review

1.1 Introduction

Many server queues are widely seen nowadays. For example, in banks, customers come for service, then staffs process customers’ requests, and after their services are completed, customers leave banks. This is a classical many server queue system with arrivals, services, and departures. It can also be observed in other scenarios such as emergency departments of hospitals, call centres, post offices, and computers. For these systems, servers are usually different from each other. They may possess different types of skills. Even when they have the same skill, their ability on this skill may be different. Such heterogeneous systems are not studied sufficiently in literature yet. We are going to investigate their behaviours and properties in this thesis. More specifically, call centres is a very important area where this heterogeneity can be applied. We are going to focus on the applications of heterogeneous systems in call centres.

A call centre is a service operation over the phone. It consists of groups of people, called agents or servers, who provide service to customers. Call centres are increasingly important in today’s business world since they have become a preferred and prevalent means for companies to communicate with their customers. Call centres are data rich environments which triggers many interesting mathematical problems. For call centre managers, it is important to guide the system to achieve certain service levels while the costs remain reasonable. There are many factors that can influence service levels. For example, the routing scheme which leads arriving customers to specific servers, the deployment of servers, and the scheduling policy which guides servers to accept customers. Existing research provides fruitful results regarding these problems for call centres with identical servers. However, in reality, it is usually the case that servers will be heterogeneous. Individual servers can possess unique skills, and even when a group of servers have the same skills, their abilities to show the skills are subject to environment. In this thesis, we are going to focus on call centres with heterogeneous servers and analyse their properties. Our proxy for heterogeneity is the servers’ service time distribution.

A call centre can be seen as a queueing system. Customers arrive at the centre according to a stochastic process, then they are routed to available idle servers based on some routing policies. If there are no idle servers available upon their arrival, they will wait in the queue, and they may wait until they get service or abandon the queue before they get service. On the other hand, a prescribed scheduling policy is used to dispatch a server to serve a customer. Once a customer is routed to a server, s/he will be served with a specific rate based on the server, and s/he will leave the system when the service is finished.

The cost-service level trade-off has a central place in quantitative call centre management. When the cost of capacity is dominated by the waiting cost of customers, the decision maker concentrates on the waiting cost and sets the staffing levels so that the utilisation ends up being less than one. This is called the Quality-Driven (QD) regime. The other extreme is when staffing costs dominate the waiting costs. In such case, utilisation of servers is fixed and is equal to one. In the long run, such a large scale system will be unstable. Customers will accumulate and a significant portion of the customers will abandon. This is called the Efficiency-Driven (ED) regime. In between these two extremes is the Quality-Efficiency-Driven (QED) regime, under which quality and efficiency are balanced. Under this regime, utilisations will approach to one from below as the system size increases, and the proportion of customers who wait before service converges to a constant which is related to the staffing level.

In this thesis, we focus on the QED regime. [Halfin and Whitt, 1981] proposed the approach to analyse the system performance under the QED regime for homogeneous servers. This work is a milestone in queueing theory which initiated a lot of research. We are going to modify their assumptions and apply it to systems where each server is unique and different. In particular, we assume service rates are i.i.d. random variables, and remain the same once the system starts operating, i.e. they do not change with time.

Apart from the staffing decisions, how to route customers to different servers will also influence the system quality. We have the routing policy to ensure customers are routed to servers in a certain way. For homogeneous systems, routing policy does not play a major role as no matter to which server a customer is routed, there is no change in the system process. For heterogeneous systems, each routing policy will yield different performances. We will mainly focus on two policies : Longest Idle Server First (LISF) policy, which will route a customer to the server who has been idle for the longest time, and Faster Server First (FSF) policy, which will always route a customer to the fastest server among those idle servers. As for scheduling policies, in our study we let it be First-In-First-Out (FIFO), i.e. when customers are queueing, they will get service by the order of their arrival.

Routing policies will cause not only difference in service levels, but also different fairness among servers, which is another measure for system quality. We also analyse fairness for heterogeneous servers under different routing policies.

For such large scale systems, exact analysis is usually intractable. Instead, we use asymptotic analysis. We use diffusion processes to approximate original queueing processes. By analysing properties of limiting diffusions, we can get insights for decision making in reality. Based on [Atar, 2008]’s result, first we analyse many server queues with random service rates under the QED regime. Then we use a similar framework as in [Borst et al., 2004] to obtain the optimal staffing levels while balancing waiting and staffing costs. Later in this thesis, we prove the diffusion limit result of [Atar, 2008] using a novel method.

Then, we analyse systems with random service rates and abandonments similarly as above. In addition to the same results for systems without abandonments, we also show that the influence of service rates variance on abandonment rate are different under different routing policies. For LISF, the abandonment rate is increasing with variance, while for FSF it may be decreasing.

Finally, we consider the state space collapse (SSC) phenomenon which implies that under some assumptions, the system process is asymptotically equivalent to a lower dimensional process. We first formulate a general method to prove SSC results for a single pool with random servers under the Halfin-Whitt regime, by which we can prove results presented in [Atar, 2008] in a different way. Then, adapting the results in [Dai and Tezcan, 2011], we show how SSC in multiclass queueing networks can be obtained under the Halfin-Whitt heavy traffic regime when service rates are i.i.d. random variables within pools.

Our main contributions can be summarised as follows.

-

•

Use a martingale method to prove the diffusion limit for many server queues with random service rates and abandonments.

-

•

Establish the optimal staffing problem for many server queues with random service rates. Provide a continuous approximation of this optimisation problem and validate it. Tightness of the steady state is proved in order to show the interchangeable limit.

-

•

Prove SSC results for parallel random server systems. Use a coupling method to prove the almost Lipschitz condition for departure processes.

The thesis is organised as follows. In the rest of this chapter, we review the literature, comparing existing results with our new results. In Chapter 2, we first present [Atar, 2008]’s results, and show the diffusion limit using the method developed by Atar. Then we include abandonments to Atar’s model, and also show its diffusion limit. In Chapter 3, we formulate an optimal staffing problem for models in [Atar, 2008]. Later we extend the problem to systems with abandonments. We also analyse how the variance of service rates influence abandonment rates. In Chapter 4, we talk about state space collapse results for many server queueing networks with server heterogeneity, and how it can be applied to system analysis. In Chapter 5, we conclude the thesis by summarising our contributions and point out future research directions.

1.2 Literature review

Queueing models are used broadly in many service systems such as call centres, healthcare and computer science. For systems with arrivals, service and departures, it is convenient to model them as queueing systems and analyse their performance. For example, for call centres, there are incoming calls, agents who answer calls and call departures, and such call centres can be analysed using queueing theory. As for queueing analysis used in other areas, [Mandelbaum et al., 2012] discuss fair routing between emergency departments and hospital wards under the QED regime. [Deo and Gurvich, 2011] use a game-theoretic queueing model and find an equilibrium on the accepted diverted ambulance from emergency departments of other hospitals. [Tezcan and Zhang, 2014] consider customer service chat systems where customers can receive real time service from agents using an instant messaging application over the internet. We will focus on call centres in this thesis using queueing modelling and analyse their performance.

The research on call centres can be viewed under different headings. [Gans et al., 2003] and [Aksin et al., 2007] review research on call centres, and provide a survey of literature on call centre operations management. They also identify some promising directions for future research. The most famous and basic queueing model for call centres is the Erlang-C or Erlang delay model, which deals with only one type of call and server without abandonments; thus every customer waits until s/he reaches a server. [Koole, 2007] gives a general idea of how the Erlang-C formula is used in call centre. More mathematical details on the Erlang-C formula can be found in [Cooper, 1981]. The Erlang-C formula is an important formula in the early stage of call centre research. It gives an explicit form of statistical-equilibrium distributions of the queueing process given the arrival rate, identical service rates, and number of servers. Thus, the probability of waiting can be calculated, to decide on the number of servers that are needed to make the system achieve a certain service level.

However, such direct analysis becomes impractical when the system grows large. Hence, the asymptotic analysis should be used. Diffusion approximations for stochastic processes in queueing models prove to be quite useful (see [Iglehart, 1965], [Stone, 1961], [Halfin and Whitt, 1981]); The work of [Halfin and Whitt, 1981] is the most relevant to our work. It considers a sequence of systems in which the traffic intensities converge to one from below, which brings the Halfin-Whitt heavy traffic regime into the picture. With arrival rate , service rate , and the Halfin-Whitt regime, under a certain scaling, the probability of waiting converges to a constant which is strictly greater than and less than . can be used to indicate the service level of the system. The offered load is a measure of traffic in a queue and is defined to be . The staffing level of such a system will be offered load plus the square root of the offered load multiplied by a constant , where the coefficient depends on the service level . The quantity is called the “safety staffing” level against stochastic variability. Using this approach, staffing and waiting costs are well balanced. The Halfin-Whitt regime has been extended in several directions. [Janssen et al., 2011] propose refinements of the celebrated square-root safety-staffing rule which have the appealing property that they are as simple as the conventional square-root safety-staffing rule. [Atar, 2008] introduces a new square root staffing policy for many servers systems with random service rates. [Puhalskii and Reiman, 2000] extend the results to a system with multiple customer classes, priorities, and phase-type service distributions. [Armony, 2005] establishes diffusion approximations and staffing levels for inverted-V systems. Our study also focuses on the Halfin-Whitt regime, and extends it to heterogeneous servers instead of identical ones.

Staffing has always been a central issue for call centre managers. There are many research papers on staffing problems for different models. See [Mandelbaum and Zeltyn, 2009], [Koçağa et al., 2015], [Whitt, 2006], [Mandelbaum and Zeltyn, 2009] and [Armony and Mandelbaum, 2011] for different discussions. Based on staffing level, systems can be in a QD, ED or QED regime. When the system is under a QD or QED regime, the abandonments are negligible in the limit, but when it is under an ED regime, the probability of abandonment will converge to a non-zero value. [Borst et al., 2004] determine the asymptotically optimal staffing level for queues under different regimes. [Whitt, 2004] investigates the ED many server heavy traffic regime for queues with abandonments. Our staffing model is based on the framework of [Borst et al., 2004].

For heterogeneous systems, how to route arriving customers to servers and how to schedule servers to serve customers are crucial decisions to the system performance. Routing and scheduling have been studied extensively in the literature. [Tezcan and Zhang, 2014] consider customer service chat systems where agents can serve multiple customers simultaneously. They propose routing policies for such system with impatient customers with the objective to minimise the probability of abandonment in steady state. [Gurvich et al., 2010] consider the staffing problem for call centres with multi-class customers and different agent types operating under QD constraints and arrival rate uncertainty. They propose a two-step solution which contains two actions: the number of agents of each type, and a dynamic routing policy. [Armony, 2005] shows that for the inverted-V model, the FSF policy is asymptotically optimal in the QED regime and no thresholds are needed. There is literature that carries out exact analysis and asymptotic analysis under conventional heavy traffic, such as [Rykov and Efrosinin, 2004] and [Kelly and Laws, 1993]. Routing policies also play an important role in staffing optimisation. Under different policies, the steady state behaviour of the system changes and fairness among servers is also different. FSF policy is commonly used. [Armony, 2005] establishes diffusion limits for the inverted-V systems under FSF policy and concludes they have a better performance than their corresponding homogeneous systems. [Atar, 2008] provides diffusion limits for many server queues with random servers under LISF and FSF policies. [Tezcan, 2008] develops limit theorems for inverted-V systems under minimum-expected-delay faster-server-first (MED-FSF) and minimum-expected-delay load-balancing (MED-LB) routing policies. Notice that LISF is a blind policy, i.e. it only needs to track the state of the process in order to make routing decisions, and information about service rates is not needed in this case. We will mainly use this policy in our model since our service rates are random variables and thus their realisations are unknown before the systems start to operate.

State space collapse is an important phenomenon when we analyse the system behaviour. [Harrison and Van Mieghem, 1997] explain the dimension reduction in general terms, using an orthogonal decomposition. For some examples of SSC one can check [Reiman, 1984]. [Puhalskii and Reiman, 2000] prove SSC for a particular system which has phase type distributed service rates. [Bramson, 1998] uses the hydrodynamic scaling to build up the state space collapse results for multi-class queueing networks under the conventional heavy traffic regime. He shows that we can use a lower dimensional process, the workload processes of each service station, to represent the system because the original system process, which is the number of each type of customers in every station, can be obtained through the workload processes and some lifting functions. The paper by [Dai and Tezcan, 2011] uses the hydrodynamic scaling proposed by [Bramson, 1998] in a many server setting. Their contribution is the definition of a SSC function, which is used in that paper to show the dimension reduction for many server networks under the Halfin-Whitt heavy traffic regime. Our SSC result is based on their framework. [Tezcan, 2008] applies this method to a distributed parallel server system and does optimal control analysis.

The key point in our research is heterogeneity and uncertainty in parameters. The uncertainty in arrival rates is investigated in some prior work. For example, [Zan, 2012] analyses the staffing problems when the arrival rate is uncertain. However, for uncertainty in the service rates, there is still plenty of space for us to explore. For a general non-technical introduction to this topic, [Gans et al., 2010] is an excellent reference. The heterogeneity in the servers is modelled in various ways. A commonly used one is the inverted-V system, which contains a single customer class and multiple server types. [Armony, 2005] considers the asymptotic framework for such systems. She shows that the FSF policy is asymptotically optimal in the QED regime. Later in [Armony and Ward, 2010], an optimisation problem for inverted V systems is formulated. They minimise the steady-state expected customer waiting time subject to a “fairness” constraint and propose a threshold routing policy which is asymptotically optimal in the Halfin-Whitt regime. [Mandelbaum et al., 2012] introduce the randomised most-idle (RMI) routing policy for the inverted-V model and analyse it in the QED regime. [Atar, 2008]’s results about random servers set the cornerstones for our work. The diffusion limit in [Atar, 2008] contains a random drift, which comes from the heterogeneity of servers. From the diffusion, we derive its steady state distribution, then formulate the optimisation staffing problem using the distribution.

Chapter 2 Diffusion Limits for Single Server Pool Systems

2.1 Introduction

In this chapter we focus on many server queueing systems with random service rates under the Halfin-Whitt heavy traffic regime. Many server queueing models have been studied extensively. However, there are only a few papers about many server queues when service rates are random variables instead of identities. Models with identical servers are not sufficient when it comes to modelling human behaviours. Individual abilities are always influenced by environment thus they can not be constants. To capture the feature more accurately, we assume our model has exponential servers with i.i.d. service rates . is also assumed to be a random variable. When customers arrive into the system they will either queue in a buffer with infinite room, or be routed to a server according to the LISF routing policy. Customers from the queue are routed to servers according to the FIFO rule. In this chapter, we first assume that the customers do not abandon and leave the system only after their service is completed. We relax this assumption later in the chapter. The routing policy is work conserving, in the sense that no server will be idle when there is at least one customer in the queue. The service policy is non-preemptive, i.e. once a customer is assigned to a server, it will continuously receive service until it is completed, i.e. the services will not be interrupted. This model is considered in [Atar, 2008]. [Atar, 2008] also analyses the same systems under the FSF routing policy. We will not focus on FSF policy because our decision is supposed to be made before the system starts running, and FSF policy requires the knowledge of each server’s rate, which does not suit our case. This chapter is organised as follows: in Section 2.1, we give the detailed description of the mathematical model and notations used throughout this chapter; in Section 2.2, we rewrite the proof of the central theorem in [Atar, 2008], although it is already proven by Atar, we present it here for completeness of our discussion; in Section 2.3, we formulate the optimal staffing problem and prove the validity of its asymptotic version.

2.2 Mathematical modelling and notation

First we introduce the notation used throughout the thesis. All of the random variables and stochastic processes are defined on a complete probability space . For a positive integer , we denote by the space of functions from to that are right continuous and left limits exist (RCLL), endowed with the usual Skorohod topology. (See [Billingsley, 1999] for the definition.) We use to denote weak convergence. And for , we write .

The model is parameterised by , where for each , is a random variable, representing number of servers. Service times for customers served at server are i.i.d. exponentially distributed with rate . The s are assumed to be nonnegative and lie in an interval . The distribution of is denoted by , and its expected value is

| (2.2.1) |

It is also assumed that satisfies the following two assumptions

The arrivals are assumed to be renewal processes with finite second moments for the interarrival times. Let the arrival rate be such that , and a sequence of strictly positive i.i.d. random variables , with mean and variance . The Halfin-Whitt heavy traffic condition, which makes the system critically loaded, is assumed to be

| (2.2.2) |

where , and .

For the th system, let be the total number of arrivals into the system up to time , be the total number of customers in the th system at (including customers both being served and waiting in the queue), be the number of jobs completed by server up to time , and be the accumulated busy time of server by time . Let if server is busy at time , and it equals to zero if the server is idle. Accordingly, let , indicating that server is idle if equals .

2.3 Atar’s results on many server queues with random servers

When there are no abandonments, it can be shown the systems satisfy the equation

| (2.3.1) |

We let be a renormalized version of the process , which is defined as

| (2.3.2) |

The initial value of and the random variable are assumed to satisfy

| (2.3.3) |

where is an -valued random variable.

[Atar, 2008]’s main result is the following theorem. It states that under the LISF policy, the sequence of the scaled processes of total number of customers weakly converges to a diffusion. What makes the diffusion distinctive from other diffusion limits is that it contains a random drift which arises from the randomness of service rates.

Theorem 2.3.1 ([Atar, 2008]).

Assume . Then, under the LISF policy, the processes weakly converge to the solution of the following SDE

| (2.3.4) |

where , and , is a normal random variable with parameters , , is a standard Brownian motion, and the three random elements and are mutually independent.

[Atar, 2008] proves his result using a method particular to this model. We give an explanation of his proof here. The detailed mathematical proof is included in Appendix A.2 for completeness. Later we will use another approach inspired by state space collapse phenomenon to prove this theorem again. For more detailed discussion on the new proof, see Section 4.5.

The process of scaled total number of customers are

| (2.3.5) |

The convergence of arrival process follows from the basic functional central limit theorem for renewal processes. Analysing the convergence of departure process is considerably harder. Each server needs to be considered individually because they have their unique service rate, and thus it is an dimensional process. However, as the system grows large, the number of servers tends to infinity; hence analysing each becomes intractable.

[Atar, 2008] solves this problem by partitioning the servers into finite pools. Within each pool, the supremum of the difference between two service rates is bounded by some small positive number .

To see how this idea is used in the proof, first we need to obtain more insights about the departure processes. The departure process of each server is treated as a time changing Poisson process. Let be independent standard Poisson processes. Since is the accumulated busy time for server by time , then by random time change, satisfies

| (2.3.6) |

where

| (2.3.7) |

Denote which has a.s. piecewise constant and right-continuous sample paths. [Atar, 2008] partitions servers into pools as mentioned above. Pools are indexed by . Using such configuration, the system can be regarded approximately as an inverted-V system, hence departure processes can be considered aggregately in each pool. Denote the total departure process of pool as . He further defines the total service rate of pool to be the sum of (the sum is over all of the servers in pool ). Then is also a time changing Poisson process and

where are independent standard Poisson processes. For simplicity denote the total service rate in pool to be

He shows in Proposition 3.1 (see AppendixA.1.1) that with this pooling method, the total departure process of the original system and the total departure process of the approximate inverted-V system are equal in distribution.

Using this equivalence, system equation (2.3.5) is equal in distribution to

With further manipulations, it can be expressed as

Convergence of the first four items are easy. Let us pay attention to the latter two. First, it is proved that converges to its fluid limit , where is the product of the expectation of and the weight probability of servers in pool . is a martingale, then [Atar, 2008] uses Functional Central Limit Theorem, and applies random time change to the fluid limit to show that converges to some Brownian motion.

is the most concerning part in the proof. It is actually equal to

which is the total amount of unused service capacities due to idleness. Denote this lost capacity as .

contains different idleness processes. It is later proved that there is a state space collapse (SSC) in such systems in the sense that, in the limit, the total lost capacities can be represented as the total accumulated idle time multiplied by some coefficient related to the service rate distribution and routing policy. Such a SSC result reduces the dimension of the original processes, which eventually helps to get a one dimensional diffusion limit.

To show such SSC result, [Atar, 2008] considers the difference between total lost capacities and the product of total accumulated idle time and . The difference consists of four s: . He proves that each tends to zero in the limit. These four s are unique to this system, thus cannot be directly extended to other models. In Chapter 4, we explain the SSC phenomenon in detail. Then we use a more generic method to prove this SSC result again.

2.4 Extension of Atar’s results to include abandonments

In this section, we assume customers may abandon the system prior to being served. Each customer has an associated patience time, and abandons the system without obtaining any service if the waiting time in the queue exceeds the customer’s patience. Once his/her service starts, s/he cannot abandon the system. Assume each customer’s patience time is exponentially distributed with rate . We will not deal with the abandonment processes directly due to complications of analysing each customer’s patience individually. Instead, we use a “perturbed” abandonment processes similar to the one described in Section 2.1 of [Dai and Tezcan, 2011]. In perturbed systems, only the customer at the head of the queue will be able to abandon, and her/his abandonment rate is the sum of abandonment rates of all of the customers in the queue. Under the assumption of exponential service and patience time, the equivalence of systems with original abandonment processes and perturbed abandonment processes is proved in [Dai and Tezcan, 2011]. Note that [Dai and Tezcan, 2011] use perturbed system technique to analyse both abandonment processes and service processes, while we only use it for our abandonment processes since our service rates are no longer deterministic thus the equivalence to the perturbed systems is invalid.

Let be the queue length at time , and let denotes the number of customers who have abandoned queue by time . The systems are assumed to be under LISF policy again.

Let be a standard Poisson process. We define

| (2.4.1) |

Then for the perturbed abandonment process

| (2.4.2) |

Using the same notations as in the previous section, we can write the system dynamic equations

| (2.4.3) |

We can show similarly that diffusion limits exist in the presence of abandonments.

Theorem 2.4.1.

Assume . Then, under LISF policy, the diffusively scaled processes weakly converge to the solution of the following SDE

| (2.4.4) |

where and are as in Theorem 2.3.1.

Proof.

The proof is quite similar to Theorem 2.3.1. We will focus on abandonment processes here since the proofs of other parts are the same.

Following arguments in the previous section we again omit the symbol , and thus we have

| (2.4.5) | ||||

| (2.4.6) |

under the LISF policy,

| (2.4.7) |

We already showed in the previous section that , , and u.o.c. in probability. For the newly added term , note that

Denote . Then by Theorem 7.2 in [Pang et al., 2007], is a square-integrable martingale with respect to the filtrations defined by

| (2.4.8) |

augmented by including all null sets. Its predictable quadratic variation is

| (2.4.9) |

By the same reasoning in Section 7.1 in [Pang et al., 2007], we obtain the deterministic limits

| (2.4.10) |

We explain the proof briefly. For more details, see [Pang et al., 2007]. We have that the sequence is stochastically bounded in . Then, by Lemma 5.9 and Section 6.1 in [Pang et al., 2007], we get the Functional Weak Law of Large Numbers (FWLLN) corresponding to Lemma 4.3, from which we can prove (2.4.10). Recall the basic Functional Central Limit Theorem (FCLT): , where is a standard Poisson process, and is a standard Brownian motion. Then

| (2.4.11) |

and by the lemma on random change of time in [Billingsley, 1999, p. 150], we have , in the uniform topology on the compact set for any . Thus,

| (2.4.12) |

By Skorohod Representation Theorem, we can assume without loss of generality that the random variables and , and the processes , and are realized in such a way that

| (2.4.13) |

Recall that . Combining (2.4.7), (2.4.11), and (2.4.4), the inequalities , and Gronwall’s inequality ( if is non-negative and satisfies .) together show that

where . By (2.4.13) and the uniform convergence of to zero, we have shown that converges to in probability, uniformly on . Since is arbitrary, this shows that . ∎

2.5 Summary

In this chapter, we show that diffusion limits are an effective way to approximate queuing processes because of its continuity feature. First we restate the limit theorem for many server queues with random service rates proved by [Atar, 2008]. The key part of this theorem is its random drift , which comes from the Central Limit Theorem applied on random service rates. Another thing which needs our attention is the coefficient of the integral of negative part of the diffusion limit, i.e. . approximates the capacities that are lost due to idleness. To some extent, reflects fairness of the routing policy. We will talk about this fairness issue more in the end of next chapter.

Then we extend the result of [Atar, 2008] to systems with abandonments. This is an important extension as it ensures the stability of the diffusion limits. We use a martingale central limit theorem to prove weak convergence. In the next chapter, we show how the diffusion limits are applied to our optimal staffing problems.

Chapter 3 Staffing and Routing for Single Server Pool Systems

3.1 Introduction

For call centre managers, how to decide on number of servers to be scheduled servers is one of the major problems. Overstaffing and understaffing will both cause immense unnecessary costs in the long term. Using queueing models, we can help managers make wise decisions on staffing levels. Particularly, the diffusion limits will be used in the analysis. In the last chapter, we proved diffusion limits for single server pool systems. Diffusion limits give us approximations of how the system processes behave. If steady states exist for diffusion limits, we can then have estimates for system steady states in the long run. In this chapter, first we formulate the optimisation problem for staffing single server pools without abandonments. Then in the second section, we extend this result to systems with abandonments. In the third section, we focus on the variance of service rates and show how the variance influences the abandonment rate, and thus the total costs. Finally in the fourth section, we analyse the coefficient in the diffusion limits and show how it reflects fairness among servers under different routing policies.

3.2 Staffing many server queues with random servers

We use a similar framework as in [Borst et al., 2004] for asymptotic optimisation of many-server queuing systems with random service rates. Consider the many-server queueing model without abandonments. In the th system, arrival rate , service rates and its expectation are as defined in Chapter 2.

Recall the second moment condition for arrival rate

| (3.2.1) |

where . It is easy to see that when , the system is unstable, thus in the limit, every customer will have to wait before getting service. To this end, we assume there is a fixed waiting cost for unstable systems.

In this work, we will mainly focus on the scenario where the service rates satisfy . For the diffusion limit in Theorem 2.3.1, this condition corresponds to . i.e. when the system is stable. From [Cooper, 1981], we know that, given the realisation of , the waiting time distribution is given by

| (3.2.2) |

where is the probability of waiting. Notice that has to be greater than for stability.

Let be the staffing cost per unit time, and be the waiting cost of a customer when s/he waits for time units. Without loss of generality we may take . Then the conditional expected total cost per unit of time is given by

where

| (3.2.3) |

We are interested in determining the expected optimal staffing level

| (3.2.4) |

where , and is the density function of .

3.2.1 Framework of the asymptotic optimisation problem

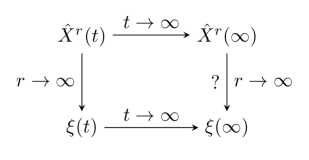

We use a similar framework as in [Borst et al., 2004], where, the cost function contains an expected waiting cost, which is the product of the arrival rate and the expected waiting time of a single customer. We use the same concept, but our expected waiting cost contains two recursive expectations instead of one. The first one is the normal expectation of the waiting cost when the sum of the service rate is given, then we take the second expectation over the sum. As the first step, we translate the discrete optimisation problem (3.2.4) to a continuous one, and approximate the latter problem by a related continuous version, which is easier to solve. Finally, we prove that the optimal solution to the approximating continuous problem provides an asymptotically optimal solution to the original discrete problem. Our main contribution is in the last step. To show the validity of the continuous approximation, we need to prove that limits are interchangeable as shown in Figure 3.1. And to show this, we prove tightness of the sequence of steady state distributions.

We first translate the discrete problem into a continuous one. Let

| (3.2.5) |

so that the variable is the normalized number of servers in excess of the minimum number required for stability. In terms of , we define

Then the total cost per unit of time can be rewritten as

| (3.2.6) |

Denote

| (3.2.7) |

Next, we a use simpler version of continuous function to approximate the function . If we can find simpler approximations for both and , we will have an approximation for the new cost function (3.2.6). In the next section, we will show the feasibility of such approximations.

3.2.2 Validity of the approximating model

In this section, we provide lemmas with proofs to show that we can use a simpler function to estimate the continuous cost function (3.2.6).

Approximation of

First, we will find an approximating version for . We achieve this by calculating the steady state of the diffusion limit in Theorem 2.1 in [Atar, 2008]. As we discussed before, when , the diffusion is not stable, so here we focus on the situation when , under which the limiting diffusion has following expressions

| (3.2.8) |

where

| (3.2.9) |

Then by Section 4 of [Browne and Whitt, 1994], when , it is a reflected Brownian motion. Thus its steady state density function conditional on is exponential, and will be . Similarly, the process restricted to the negative half-line is an O-U process , thus its steady state conditional on is normally distributed with density function . Hence, let be the probability of waiting when , the steady state distribution of has density function

| (3.2.10) |

Since the variance of the limiting diffusion is a constant on the real line, by [Browne and Whitt, 1994], the density function of its steady state should be continuous. may be solved by equating the right-handed limit of and the left-handed limit of at . This gives us

| (3.2.11) |

Thus we will have an analogue of Proposition 1 in [Halfin and Whitt, 1981] and Lemma 5.1 in [Borst et al., 2004], which gives us an approximation of .

Lemma 3.2.1.

For any function with ,

| (3.2.12) |

where .

Lemma 5.1 in [Borst et al., 2004] is a direct application of Proposition 1 in [Halfin and Whitt, 1981], which says that, under the Halfin-Whitt heavy traffic condition, the probability of waiting in many server queue (identical servers) converges to a constant between zero and one. For our systems, service rates are no longer identical, and thus we cannot use this result directly. We come up with another approach to prove the convergence, which involves an associated sequence of homogeneous systems.

The idea of the proof lies in Figure 3.1. In order to show the convergence of the probability of waiting in (3.2.12), we need to show that the sequence of steady states weakly converges to the steady state of the diffusion limit. To show weak convergence, the usual way is to first show tightness, then use the relations in Figure 3.1 to show that tightness of actually reflects the convergence on the right hand side.

The challenging part is to show the tightness. It is hard to come up with a direct way to show tightness if service rates are random and unknown. Instead, we compare our heterogeneous systems with a sequence of homogeneous systems which have identical service rates being less than , then use the properties of homogeneous systems to get tightness results.

More specifically, consider homogeneous systems with servers and identical service rates . Assume there is a fixed number for each , and denote as the family of sets containing numbers out of . Now our problem can be considered in the following two cases:

-

•

When , denote this scenario as . (This is independent from the arrival process .) There is a possibility that the heterogeneous systems serve faster than their corresponding homogeneous ones.

-

•

When , this scenario is marked as . The heterogeneous systems always serve faster than their corresponding homogeneous ones. Thus under such situations, . Therefore to show tightness of heterogeneous systems for this scenario, we only need to show the tightness of their corresponding homogeneous systems, i.e.

(3.2.13)

Combining these two scenarios, let . Then

| (3.2.14) |

If (3.2.13) is true, then after a reselection of , we can easily show . Furthermore, if we can also show as , then as , the tightness result will follow. Since the tightness result holds for every , it should also hold as , i.e. .

From the discussion above, it is important to define proper and to get our convergence results. We have three lemmas for that.

Lemma 3.2.2.

Let for any , then the sequence is tight.

Proof.

In order to show is tight, first we need to specify the heavy traffic condition for the homogeneous systems and the existence of their steady states.

When

| (3.2.15) |

the heavy traffic condition becomes

This also means .

To guarantee the existence of their steady states, we need

i.e.

| (3.2.16) |

and makes the inequality above hold.

Since we already showed the existence of , now we can prove the tightness of it, i.e. (3.2.13) is true when . Denote , then . Fix . We want to show

| (3.2.17) |

Choose . By (1.1) and (1.3) in [Halfin and Whitt, 1981], we have

where . Substitute into the equation above, and since , it becomes

, as long as

holds. Here has base . Thus (3.2.17) is proved.

For a sequence of homogeneous systems, take , then (3.2.13) holds when . ∎

From Lemma 3.2.2, in order to guarantee heavy traffic condition and stability of the homogeneous systems, service rate of homogeneous systems is chosen with

| (3.2.18) |

in the rest of this chapter.

As for the choice of , we will explain in the following two lemmas that when grows slower than , the convergence does not hold. Only when grows with the same rate as , the probability converges to zero.

Lemma 3.2.3.

Let . If grows slower than in the sense that , then .

Proof.

Fix . Since is one element in , denote , we have

| (3.2.19) |

Using stirling’s approximation, we have a lower bound for the combination factor

| (3.2.20) |

Thus as ,

| (3.2.21) |

Notice that the second item as , the third item can be considered as follows:

and the fourth item equals , where converges to . As for the integral, the upper limit is equal to

as , because . So as , (3.2.21) is equivalent to

| (3.2.22) |

Thus the original will not converge to zero, and therefore we rule out this situation. ∎

Now we conclude that there must be for some such that holds.

Lemma 3.2.4.

Let and for some . Then as .

Proof.

Assume as . Then weakly converges to a normal random variable with mean , variance as . Using the left bound for normal distribution,

As , we have

| (3.2.23) |

then applying stirling’s approximation again on the combination factor in (3.2.19) gives

| (3.2.24) |

Combine (3.2.23) and (3.2.24) and we have, as ,

| (3.2.25) |

For notational simplicity let . Since (3.2.25) is an upper bound of , if we can demonstrate (3.2.25) converges to zero as , then as .

Assume for some and , then the right hand side of (3.2.25) can be rewritten as

| (3.2.26) |

First notice that two items in the parentheses both converge to zero, because of the following:

| (3.2.27) |

Since , , (3.2.27) converges to zero as ; similarly,

| (3.2.28) |

Again, since , , as , (3.2.28) converges to zero as . Therefore the difference in the parentheses converges to zero as , as long as we can show the left factor in (3.2.26) converges to zero as , we can claim (3.2.26) converges to zero as .

Obviously, if , then the factor in (3.2.26) converges to zero as . The first is trivial, As for the second ,

| (3.2.29) |

The graph of function is shown in Figure 3.2.

Now we can prove Lemma 3.2.1.

Proof.

Since our system is under the Halfin-Whitt heavy traffic regime, assume the staffing is determined by

| (3.2.31) |

Then from Theorem 2.1 in [Atar, 2008], the random drift is

| (3.2.32) |

Here we take since the purpose of the term is just to make the random service rate more general. By substituting (2.3.3) and (3.2.31) into (3.2.32), we have

by (2.2.2) and the assumption . Denote

| (3.2.33) |

Recall that is a normal random variable with parameters , and . For the th system, let be its extra staffing which is required for stability, and

| (3.2.34) |

Keep fixed for every , then as . When , denote as .

Notice that

| (3.2.35) |

Choose such that

| (3.2.36) |

then

| (3.2.37) |

Then it remains to show that

| (3.2.38) |

If we can show the family of random variables is tight, then we can claim as when , thus (3.2.38) is satisfied.

To show the tightness of , we only need to show the tightness of . (If is tight, then , such that . Then .)

When and are defined as in Lemma 3.2.2 and 3.2.4, are tight, and as . Thus the right side of (3.2.14) converges to zero. Let on both sides of (3.2.14). We have that is tight, hence is tight.

Now by the definition of tightness, for every sequence in , there exists a subsequence weakly converging to a random variable . Figure 3.1 shows our goal. We already know the left, top and bottom arrows are true, now we need to prove the right one. Assume does not have the same distribution as when . Take an infinite sequence and , from the left and bottom arrows in Figure 3.1. The cumulative distribution functions (CDF) of random variables will converge to the CDF of as and . Next take a subsequence of and , i.e. and , then the CDFs of will converge to the CDF of as and . If and are different random variables, then we find two subsequences of random variables’ CDFs that converge to different limits, which means such a sequence does not converge, which furthermore contradicts the fact that it is convergent (see left and bottom arrows in Figure 3.1). Thus should equal in distribution, so we have proven that as . Therefore (3.2.38) is proved, hence (3.2.12) is true. The proof is completed.

∎

Approximation of

Next, we find an approximation for , which will be more straightforward.

Lemma 3.2.5.

Verification of approximating function

Now apply the change of variables (3.2.34) into the original cost function (3.2.6), it can be rewritten as

| (3.2.40) |

where

| (3.2.41) |

and is the probability density function of .

Now that we have approximations for both and , we will have an effective approximation for cost function (3.2.40). More specifically, with the new approximating function

| (3.2.42) |

where

| (3.2.43) |

and is the probability density function of , we have the following theorem

Theorem 3.2.1.

is a valid approximation for in the sense that

| (3.2.44) |

Proof.

Since we already have as and remains the same, we only need to show

| (3.2.45) |

To make it more clear, let

| (3.2.46) |

and

| (3.2.47) |

where . Then is actually

| (3.2.48) |

Since is proved, we only need to show is uniformly integrable when , and is a continuous function of . Then by the Continuous Mapping Theorem and Theorem 3.5 in [Billingsley, 1999], one can conclude (3.2.48) is true.

To show is uniformly integrable, we only need to show

is integrable when , since are the probability of waiting and thus are bounded by .

It is easy to see the uniform integrability of . is assumed to be a function such that is finite. Since , given the realisation of , , and , as . Thus, as . Hence , such that . Therefore using the Dominated Convergence Theorem,

and the uniform integrability is proved. The continuity of is obvious. We show continuity of when is fixed, ignoring in the proof for simplicity.

For every , we want to show, for every , . From the proof of Lemma 3.2.1 we know that for every realisation of , there always exists a such that has the same value as . We choose in such manner in the following proof. As ,

The first and third s come from convergence of to when is given, the second is because of the continuity of . Now we proved continuity of , hence the function is continuous with respect to .

3.3 Staffing many server queues with random service rates and abandonments

Following the result we obtained in Section 3.1, we add abandonments to the model and design a cost function which we will optimise later.

All of the basic settings and notations are the same, except there are abandonments in the queue. Each customer has an associated patience time which are i.i.d. exponential random variables with rate . A customer abandons the system without getting any service if the waiting time in the queue exceeds the customer’s patience. Once her/his service starts, s/he cannot abandon the system.

Adapting notations from Section 4.1, let be the scaled process of the number of customers in the th system. We have the cost function

| (3.3.1) |

where is the cost of every customer abandonment, and is the density function of . Notice that in this total cost function, we ignore the holding cost in the queue because abandonment and holding costs are both linear functions of expected queue length, and there is no need to consider expected queue length twice.

As proved in Section 3.3, where satisfies the equation

| (3.3.2) |

More specifically, (3.3.2) can be seen as

| (3.3.3) |

Then by Section 4 of [Browne and Whitt, 1994], when , it is an Ornstein-Uhlenbeck process, thus its steady state conditional on is normal distributed with density function . Similarly, when , it is also an O-U process, thus its steady state conditional on is a normal random variable with density function . Let . Then has density function

| (3.3.4) |

To find out , notice that is continuous because the infinitesimal variance of is constant on the real line. Thus by equating the limits of from both left and right we get

| (3.3.5) |

To this end, it is intuitive to use the following function as an approximation for the original cost function (3.3.1):

| (3.3.6) |

We have a similar theorem as 3.2.44.

To prove this convergence, we will need uniform integrability of the steady state. To achieve this, for each heterogeneous system, we compare it with a homogeneous system with the same number of servers and the service rate being the lower bound of , i.e. .

Lemma 3.3.1.

Let be the departure process of the th homogeneous system described above where all the service rates take their minimum value . Denote the departure process in the th heterogeneous system as . Then , where ‘st’ means the inequality holds stochastically.

Proof.

Denote the number of total customers in the th homogeneous system as . We have the system dynamic equations

| (3.3.8) | ||||

| (3.3.9) |

For simplicity let . The arrival process and abandonment process are independent of the service rates and departure process, thus we can take them to be the same for these two processes. Let be a generated poisson process with rate , where is the upper bound of , and be the sequence of its occurrence times, i.e. . Let be a sequence of independent uniform random variables, and be the indicator function for event which takes the value if occurs and otherwise. Assume all of the processes equal zero at . By splitting the process , we define the following processes

| (3.3.10) | |||

| (3.3.11) | |||

| (3.3.12) | |||

| (3.3.13) | |||

| (3.3.14) | |||

| (3.3.15) |

where is determined by the process , the sequence , and the selection scheme defined as follows: if, for some , , then we have that the potential departure occurring at time in process is accepted as the real departure for process . Assume there are busy servers just before this departure occurs (time ). Then after it is accepted as the real departure, one of the servers will be freed, which leads to our selection scheme. Let be a uniformly distributed random variable on . If , then server will be freed at time . Here we let .

Under such definition, the process and are stochastically equivalent to and respectively.

We prove this by contradiction. Define

| (3.3.16) |

Then we have

i.e.

Thus

| (3.3.17) |

Notice that implies . Since arrival processes and abandonment processes are identical, we have . Also, during the time , there are no departures, thus, by equations (3.3.8) and (3.3.9),

This shows us that Substituting this into (3.3.17) gives us

| (3.3.18) |

If , then , and (3.3.18) becomes , but since , this doesn’t hold. If , then , and (3.3.18) is , which is also not true because of .

Thereby we have found a contradiction to the assumption (3.3.16). Hence, we conclude that such an does not exist and for every . That means . ∎

Now we are ready to prove the theorem.

Proof of Theorem 3.3.7.

Since does not change in both cost functions, we only need to show

| (3.3.19) |

Consider a sequence of homogeneous systems with abandonment and service rates being the lower bound of , i.e. . All other settings are the same as in the heterogeneous systems. By Lemma 3.3.1 and equations (3.3.8) and (3.3.9), we know that , . Since and as , it is also true that . And by equations (3.3) and (3.4) in [Mandelbaum and Zeltyn, 2004],

where

| (3.3.20) |

Thus ,

Let . Then the equation above can be enlarged

| (3.3.21) |

From [Mandelbaum and Zeltyn, 2004], we know converges, thus , which means the expected queue length of the th homogeneous system is bounded. Since , we have

| (3.3.22) |

Scaling the inequality on both sides, we have

| (3.3.23) |

i.e.

| (3.3.24) |

Notice that the expected value on the left is a function of the random variable , thus it itself is also a random variable. (3.3.24) implies that in the th heterogeneous systems, the (scaled) expected queue length is always bounded no matter what values the service rates take, which further implies that the (scaled) queue length is uniformly integrable.

Using the same reasoning process for Figure 3.1, but with abandonment in the systems, we can get . Hence, by Theorem 3.5 in [Billingsley, 1999], (3.3.19) is proved. ∎

3.4 Impact of service rate variation on abandonment rate

In this section we want to see how the variance of the service rate influence the queue length, and thus the abandonment cost. We analyse this by considering the expected (scaled) queue length. The analytical result seems rather intractable, so instead we show their numerical results and explain how it reflects such influence. We mainly focus on systems under the LISF policy. To have a better idea of how variance plays its role in a system, we also include the numerical results for systems under the FSF policy.

According to (3.3.6), the approximating cost function for systems with abandonment is

| (3.4.1) |

We want to see how the variance of the service rate influences the steady state and, thus by (3.4.1), the abandonment cost. (3.4.1) contains a complicated integral which may not have a closed form. To simplify the problem, we consider a special distribution of service rates. Let the random service rates be uniformly distributed on , . Then has a random drift , where , and , and . Then, (3.4.1) becomes

| (3.4.2) |

Since the only part depending on the service rate variance is the double integral in (3.4.2), which is actually the expected (scaled) queue length, we let

| (3.4.3) |

After simplification, (3.4.3) is still hard to tackle, thus we employ a numerical integral. In Figure 3.3, we show the function vs . From the graph, is increasing. This implies that when all the other conditions remain the same, the total cost will grow as the service rate variance grows.

In contrast, we consider the same function for the FSF policy. The only difference in the limiting diffusion for FSF is , which is in the above-mentioned uniform distribution. Keeping other parameters unchanged, we plot its graph in Figure 3.4. The result is surprisingly counter-intuitive. It shows that the expected (scaled) queue length will decrease as the variance grows. One can explain such a situation as follows: the FSF policy always routes customers to the fastest available servers, thus in the long run, only the slowest server will have the chance to be idle. When the service rate variance increase, the minimum service rate will decrease, thus when the arrival rate remains the same, the ‘lost’ capacities due to idleness will also decrease. This implies that the total service rates that are indeed utilised will increase, thus the queue length decreases.

3.5 Fairness among severs under different routing policies

From [Atar, 2008] and our analysis above, for a heterogeneous system, the longest idle server first (LISF) policy expresses a form of fairness, because when several servers are free, the one selected for the next incoming job is the one that has been idle for the longest time. On the other hand, policy faster server first (FSF) always routes customer to the fastest idle servers. Such difference in the routing scheme shows that LISF is more fair for servers than FSF, which provokes a question: can we quantify the fairness level for different routing policies? In this section we will answer this question, and demonstrate how it can be used in real systems.

3.5.1 Fairness measure

We introduce a new concept called “fairness measure”. We still consider a sequence of many server queues with i.i.d. servers. For simplicity, we remove the randomness on the number of servers and assume the th system has exactly servers. Denote as the support of random variables . To analyse fairness among servers, it is intuitive to consider their idle times. As before, denote as the idleness process for server , i.e. equals if server is idle at , and is equal to if it is busy. For a routing policy , its fairness measure is defined as , such that , and ,

| (3.5.1) |

as , where is the indicator function

| (3.5.2) |

From the definition, it is easy to see that is a probability measure on . One can understand (3.5.1) that the number of idle servers whose service rates are in converges u.o.c to the product of the fairness measure of set and the total number of idle servers.

We need to be aware that although (3.5.1) reflects fairness of a policy to some degree, it does not hold in every situation. There should be some limitations on the policies such that (3.5.1) is true, e.g. the policy should not depend on the total number of idle servers. Denote the set of all the eligible policies as . We have the following assumption,

Assumption 3.5.1.

For any , (3.5.1) holds.

3.5.2 Application of fairness measure on LISF and FSF policies

To see how Assumption 3.5.1 is used, we consider the diffusion limits proved in [Atar, 2008]. In Section 2 of Chapter 2, we showed that after some manipulations on the process (diffusively scaled process of total number of customers in the system), it has expression

| (3.5.3) |

with being the only item that is troublesome to deal with and also the only item that depends on policies.

Now we show the convergence of under different policies. By Assumption 3.5.1,

| (3.5.4) |

in probability u.o.c as .

-

•

LISF

For any , define , then(3.5.5) and (3.5.4) becomes

(3.5.6) in probability u.o.c as . is actually in Theorem 2.1 in [Atar, 2008], and (3.5.6) matches with the result in that paper that in probability u.o.c as .

-

•

FSF

Similarly, for any , define . Then(3.5.7) and (3.5.4) becomes

(3.5.8) in probability u.o.c. as . Such a form also matches with the result of Theorem 2.2 in [Atar, 2008].

With fairness measure, we rephrase results in [Atar, 2008] in a more general way. The problem of proving diffusion limit of a particular system is reduced to finding the fairness measure of the policy that is used in the system. Thus it is possible to invent a standard method for proving diffusion limits, which is more insightful than the proof in [Atar, 2008].

Chapter 4 State Space Collapse for Many Server Queues and Queueing Networks with Parameter Uncertainty

4.1 Introduction

In this chapter, we discuss the state space collapse phenomenon. Throughout this chapter, we adapt the framework developed by [Dai and Tezcan, 2011]. They consider a queueing network with multi-class customers and several server pools. In each pool, servers have the same capacities and capabilities. Customer arrivals are exogenous and independent from service processes. For such systems, exact analysis provides limited insight into the general properties of performances. One general way to overcome this is to use diffusion approximations. Similar to Chapter 3, the central part of the diffusion approximation is some heavy traffic limit theorems that state that a certain diffusively scaled performance processes converges to a diffusion in heavy traffic. Since the system processes in such networks are multidimensional, it becomes difficult to deal with when the system size grows large. Here is where state space collapse (SSC) plays a role. The SSC result reveals that under some conditions, the dimensions of system processes can be significantly reduced in the heavy traffic limit, while the essential information of the systems is still maintained. [Dai and Tezcan, 2011] gain the SSC result by using what they call an SSC function. They show that under some assumptions on the networks, the SSC function evaluated at diffusively scaled processes converges to zero as the system grows large.

For administrative and economic reasons, servers can be categorized and allocated such that, within pools, servers have the same capabilities, i.e. the set of customer classes that one server in a pool is able to serve is the same as the set of customer class that any other server in the same pool can serve. This way of pooling reflects a kind of heterogeneity among servers. [Dai and Tezcan, 2011] also assume that within each pool, servers not only have the same capabilities, but also have the same capacities, i.e. when two servers in the same pool serve the same class of customers, their service rates are the same. However, in reality, it is more common that some differences are present among servers who are capable of doing the same tasks. Inside each pool, even though servers have the same capabilities, their skill levels can still be different, thus it will make more sense if we consider their rates to be different and random rather than identical.

In our work, service rates within pools are assumed to be i.i.d. random variables, and we also restrict our service times to being exponentially distributed. We analyse such networks, and demonstrate that with randomness within pools the SSC result still holds. We will show that the SSC function in such systems still converges to zero in the limit.

This chapter is organised as follows. In Section 4.2, we introduce our model and define parallel random server systems. In Section 4.3, we give our main result, the SSC for networks with random service rates. Then in Section 4.4, we provide essential proofs that are unique to our results. Proofs that are the same as in [Dai and Tezcan, 2011] are relegated to Appendix B.4. In Section 4.5, to show how the SSC can be used in queueing system analysis, we use the SSC method to show the diffusion limits proved in Chapter 3.

4.2 Notation and model descriptions

Our basic settings are similar to those in [Dai and Tezcan, 2011],but slightly different. Besides the randomness among servers, we do not include abandonments in our systems, and we also do not differentiate between the arrival streams and customer classes. Every arrival stream forms one class of customers. More specifically, we consider a system with parallel server pools and several customer classes. A server pool consists of several servers whose capabilities are the same, and their capacities are i.i.d. random variables (see more detailed definitions below). Customers of one class arrive in the system at a certain rate. Each class of customers have their own queue. Upon their arrival they will be routed to a capable server (idle and possesses the skill to serve this class of customer) if there is at least one; if all the capable servers are occupied, they will wait in their queues. Each customer is served by one of the servers. Once the service of a customer is completed by one of the servers, the customer leaves the system. And once a customer starts his service, he cannot abandon the service. For convenience, we refer to these systems as parallel random server systems.

4.2.1 Notation

We need to define some notation for convenience in presentation. Throughout this chapter, unless stated otherwise, for a vector , its norm is defined as . For an matrix , its norm is , where are the row vectors of .

In Chapter 2, we defined that for any function and any , . Now consider a sequence , we say uniformly on a compact set (u.o.c) if as for any .

4.2.2 Dynamics of the queueing networks

We use to denote the number of server pools, and to denote the number of customer classes. For notational convenience, we define . And denote the number of servers in pool by for and set . The total number of servers in the system is denoted by . Class customers arrive the system according to a Poisson process with rate . We assume that the set of pools that can handle class customers is fixed and denoted by . Similarly, the set of customer classes that pool can handle is fixed and denoted by .

Upon arrival, each customer of class is routed to a server if there is an available server in one of the pools in . Otherwise, the customer joins the queue of class , waiting to be served later. Assume the service time of a class customer by the th server in pool is exponentially distributed with rate , where . Then the service rates are i.i.d. random variables. Denote their expectation value as . We also assume that , .

The object of study in this paper is a stochastic process . Assume all of the components are right continuous with left limits. We provide definitions of individual processes below.

-

•

, is the total number of class arrivals by time .

-

•

, denotes the total number of class customers who are delayed and have to wait in the queue before their service starts.

-

•

, is the total number of class customers who are routed to a server and start service in pool immediately after their arrival by time .

-

•

, is the total number of class customers who are delayed in the queue and whose service started in pool before time .

-

•

, is the total number of class customers in queue at time .

-

•

, is the total number of servers in pool who are busy with serving class customers at time .

-

•

, denotes the total time spent by servers in pool in serving class customers by time .

-

•

, denotes the total number of class customers whose service are completed by servers in pool by time .

Since there is heterogeneity among servers, we need to deal with each server individually, thus we also need the following notations:

-

•

: busy server indicator function. If the th server in pool is busy with a class customer at time , , otherwise .

-

•

: total time spent by the th server in pool in serving class customers by time .

-

•

: total number of class customers whose service are completed by the th server in pool by time .

Notice have such relation:

for all .

The main goal of this chapter is to study the SSC results of the above-mentioned queueing networks in the diffusion limit manner. Therefore, we analyse a sequence of systems indexed by such that the arrival rate grows to infinity as . The number of servers also grows to infinity to meet the growing demand. We append to the processes that are associated with the th system, e.g. is used to denote the number of class customers in the queue in the th system at time . The arrival rate in the th system is given by , and we assume that

| (4.2.1) |

as .

Let be i.i.d. standard Poisson processes, each having right-continuous sample paths. Combining the settings in [Atar, 2008] and [Dai and Tezcan, 2011], the processes are assumed to satisfy

| (4.2.2) |

where

| (4.2.3) |

The process depends on the control policy used in the system. To emphasize the dependence on the control policy used, we use to denote the process. Clearly, each element of is a nondecreasing process, and each element of and is nonnegative. Furthermore, the process satisfies the following dynamic equations for all .

| (4.2.4) |

| (4.2.5) |

| (4.2.6) |

| (4.2.7) |

| (4.2.8) |

| (4.2.9) |

| (4.2.10) |

Equations (4.2.8) and (4.2.9) are based on the assumed non-idling property of a control policy. Equation (4.2.8) implies that there can be customers in the queue only when all of the servers that can serve that class of customers are busy. Equation (4.2.9) implies that an arriving customer is delayed in the queue only if there is no idle server that can serve that customer at the time of his arrival. Equation (4.2.10) indicates the scheduling decisions to be made according to the selected scheduling policies.

Let be the Poisson processes defined before, and be the corresponding sequence of i.i.d. exponential random variables. Since is a Poisson process, has exponential distribution with rate . We define by

| (4.2.11) |

where, by convention, empty sums are set to be zero. The term is the total service requirement of the first class customers who are served by the th server in pool , and is known as the cumulative service time process. By the duality of and , we have

| (4.2.12) |

It follows from (4.2.2) that

| (4.2.13) |

Next, we give the details of the arrival processes. Let be a delayed renewal process with rate . Let

| (4.2.14) |

Let be the sequence of interarrival times that are associated with the process . Note that they are independent and identically distributed. We define by

| (4.2.15) |

and so

| (4.2.16) |

We require that the interarrival times of the arrival processes satisfy the following condition, which is similar to condition (3.4) in [Bramson, 1998]:

| (4.2.17) |

Condition (4.2.17) is automatically satisfied by the service times because they are assumed to be exponentially distributed. For the rest of the paper, we assume that the primitive processes of the system satisfy (4.2.17). We also assume that and are independent.

We require that the number of servers in the th system is selected so that

| (4.2.18) | |||

| (4.2.19) | |||

| (4.2.20) |

We shall denote .

4.3 Main results

In this section, we state our main result as Theorem 4.3.2, which is an SSC result for parallel random server systems. We extend the SSC result for systems from identical servers in each pool which is proved by [Dai and Tezcan, 2011], to include random service rates in each pool. The proof framework of our results is similar to the one in [Dai and Tezcan, 2011]. Our main contribution is when showing almost Lipschitz condition for hydrodynamically scaled departure processes, the direct way in [Dai and Tezcan, 2011] is no longer valid, so instead we come up with a new coupling method. For more detailed differences between proofs of [Dai and Tezcan, 2011] and our results, see discussion at the beginning of Section 4.4.

Before stating the theorem, we need some preliminary definitions and assumptions.

We only consider systems under the heavy traffic condition. For a multi-class network with several server pools, it is not trivial to define the heavy traffic condition. Instead, we use the static planning problem (SPP) for the networks as a bridge to heavy traffic conditions.

4.3.1 The static planning problem

The SPP is introduced in [Dai and Tezcan, 2011]. We will modify the original problem such that it suits our models. The objective of an SPP is to minimise server utilisations in the network. [Dai and Tezcan, 2011] use identical service rates to define utilisations, while we consider their expected value instead.

Let , where is the long term proportion of pool servers’ working time in serving class customers. We define the static planning problem

| (4.3.1) | ||||

| s.t. | ||||