V1 A Residual Bootstrap for Conditional Expected Shortfall

Abstract

This paper studies a fixed-design residual bootstrap method for the two-step estimator of Francq and

Zakoïan (2015) associated with the conditional Expected Shortfall. For a general class of volatility models the bootstrap is shown to be asymptotically valid under the conditions imposed by Beutner

et al. (2018). A simulation study is conducted revealing that the average coverage rates are satisfactory for most settings considered. There is no clear evidence to have a preference for any of the three proposed bootstrap intervals. This contrasts results in Beutner

et al. (2018) for the VaR, for which the reversed-tails interval has a superior performance.

Keywords: Residual bootstrap; Expected Shortfall; GARCH

JEL codes: C14; C15; C22; C58

A Residual Bootstrap for Conditional Expected Shortfall

Alexander Heinemann† Sean Telg†

†Department of Quantitative Economics

Maastricht University

March 2, 2024

1 Introduction

The assessment of market risk is a key challenge that financial market participants face on a daily basis. To evaluate the risk, financial institutions primarily employ the risk measure Value-at-Risk (VaR) to meet the capital requirements enforced by the Basel Committee on Banking Supervision. Despite its popularity, the VaR is not a coherent risk measure as it fails to fulfill the subadditivity property (Artzner et al., 1999). A coherent alternative is the related risk measure Expected Shortfall (ES). For a given level , it is defined as the expected return in the worst cases and is therefore sometimes called Expected Tail Loss.111In the literature, ES is also sometimes referred to as conditional VaR since it is defined as the expected loss given a VaR exceedence. Since conditional refers to temporal dependence (i.e. conditional on past returns) in this paper, we refrain from using this term to prevent any confusion. In contrast to the VaR, the ES provides valuable information on the severity of an incurred loss, which makes it the preferred risk measure in practice (c.f. Acerbi and Tasche, 2002a; 2002b). Consequently, the Basel Committee published revised standards in January 2016 resembling a shift from VaR towards ES as the underlying risk measure (Osmundsen, 2018).

In the literature there is an increasing interest in conditional risk measures, which take into account the temporal dependence of asset returns. Frequently, the volatility dynamics are specified by a (semi-) parametric model such that the conditional ES can be expressed as the product of the conditional volatility and the ES of the innovations’ distribution (c.f. Francq and Zakoïan, 2015, Example 2). The latter can be treated as additional parameter, which is generally unknown just like the parameters of the conditional volatility model. Inferring the parameters from data leads to an evaluation of the conditional ES that is prone to estimation risk. As argued in Beutner et al. (2018) this estimation uncertainty can be substantial for risk measures related to extreme events.

The uncertainty around point estimates is typically determined by asymptotic theory, in which one replaces unknown quantities in the limiting distribution by consistent estimates. For example, Cai and Wang (2008) and Martins-Filho et al. (2018) study the behavior of proposed nonparametric estimators for conditional VaR and ES, based on asymptotics and simulation studies. An alternative approach is based on bootstrap approximations. Regarding the estimators of the volatility model’s parameters, several bootstrap methods have been examined, among which the sub-sample bootstrap (Hall and Yao, 2003), the block bootstrap (Corradi and Iglesias, 2008), the wild bootstrap (Shimizu, 2009) and the residual bootstrap, both with recursive (Pascual et al., 2006; Hidalgo and Zaffaroni, 2007) and fixed design (Shimizu, 2009; Cavaliere et al., 2018, Beutner et al., 2018). However, the estimation of the conditional ES has received only limited attention in the bootstrap literature. Christoffersen and Gonçalves (2005) construct intervals for conditional ES based on a recursive-design residual bootstrap method. Gao and Song (2008) compare coverage probabilities for conditional ES based on this bootstrap method and asymptotic normality results in their simulation study.

In this paper, we extend results of Beutner et al. (2018) derived for conditional VaR to the conditional ES estimator. In particular, we follow the two-step procedure of Francq and Zakoïan (2015) for the estimation of the underlying parameters. In a first step, we obtain estimates of the parameters of the stochastic volatility model by quasi-maximum-likelihood (QML) estimation. Based on the model’s residuals, an estimate for the innovations’ ES is obtained in the second step. We propose a fixed-design residual bootstrap method to mimic the finite sample distribution of this two-step estimator for a general class of volatility models. Moreover, an algorithm is provided for the construction of bootstrap intervals for the conditional ES.

The remainder of the paper is organized as follows. Section 2 introduces a general class of volatility models and derives the conditional ES. The two-step estimation procedure is described in Section 3 and corresponding asymptotic results are provided under the assumptions imposed by Beutner et al. (2018). In Section 4, a fixed-design residual bootstrap method is proposed and proven to be consistent. In addition, bootstrap intervals are constructed for the conditional ES. Section 5 consists of a Monte Carlo study. Section 6 concludes. Auxiliary results and proofs of the main results are gathered in the Appendix.

2 Model

We consider conditional volatility models of the form

| (2.1) |

with , where denotes the log-return, is a volatility process and is a sequence of independent and identically distributed (i.i.d.) variables. The volatility is assumed to be a measurable function of past observations

| (2.2) |

with and denotes the true parameter vector belonging to the parameter space , . Various commonly used volatility models satisfy (2.1)–(2.2); for examples see Francq and Zakoïan (2015, Table 1). Consider an arbitrary real-valued random variable (e.g. stock return) with cdf . If with , then the ES at level is finite and given by . Let denote the -algebra generated by . It follows that the conditional ES of given at level is

| (2.3) |

As are i.i.d., the ES at level of is constant for a given and can be treated as a parameter. Setting with and denoting the cdf of , (2.3) reduces to

| (2.4) |

Typically, is chosen small (e.g. 5% and 1%) such that and hence . Except for special cases222We derive the analytical expressions for for the cases in which are normally as well as Student- distributed in Appendix B., is unknown and needs to estimated just like .

3 Estimation

For the estimation of the parameters and we employ the two-step procedure of Francq and Zakoïan (2015, Remark 3). First, the vector of the conditional volatility parameters is estimated by quasi-maximum-likelihood (QML). Since

| (3.1) |

can generally not be determined completely given a sample , we replace the unknown presample observations by arbitrary values, say , , yielding

| (3.2) |

Then the QML estimator of is defined as a measurable solution of

| (3.3) |

with the criterion function specified by

In the second step, can be estimated on the basis of the first-step residuals, i.e. . A reasonable estimator of (c.f. Gao and Song, 2008) is given by

| (3.4) |

where is the empirical -quantile of , i.e. with empirical distribution function .

Having obtained estimators for and , we turn to the estimation of the conditional ES of the one-period ahead observation at level . For notational convenience, we use the abbreviation to denote . Employing (3.2)–(3.4) we can estimate by

| (3.5) |

For the asymptotic analysis of (3.3)–(3.5) we assume the conditions of Beutner et al. (2018), which we restate for completeness.

Assumption 1.

(Compactness) is a compact subset of .

Assumption 2.

Assumption 3.

(Volatility process) For any real sequence , the function is continuous. Almost surely, for any and some and for some . Moreover, for any , we assume almost surely (a.s.) if and only if .

Assumption 4.

(Initial conditions) There exists a constant and a random variable measurable with respect to and for some such that

-

(i)

;

-

(ii)

has continuous second-order derivatives satisfying

where denotes the Euclidean norm.

Assumption 5.

(Innovation process) The innovations satisfy

-

(i)

with being continuous, and is independent of ;

-

(ii)

admits a density which is continuous and strictly positive around ;

-

(iii)

.

Assumption 6.

(Interior) belongs to the interior of denoted by .

Assumption 7.

(Non-degeneracy) There does not exist a non-zero such that almost surely.

Assumption 8.

(Monotonicity) For any real sequence and for any satisfying componentwise, we have .

Assumption 9.

(Moments) There exists a neighborhood of such that the following variables have finite expectation

for some , , (to be specified).

Assumption 10.

(Scaling Stability) There exists a function such that for any , for any , and any real sequence

where and is differentiable in .

For a discussion of the conditions we refer to Francq and Zakoïan (2015, Section 2 and 3) and Beutner et al. (2018, Section 3). On the basis of the previous assumptions we extend the strong consistency result of Francq and Zakoïan (2015, Theorem 1) to the estimator of the ES at level of .

Theorem 1.

Proof.

Francq and Zakoïan (2015, Theorem 1) establish . Moreover, we have

by Beutner et al. (2018, Lemma 2), which verifies the second claim. ∎

To lighten notation, we henceforth write and drop the argument when evaluated at the true parameter, i.e. . The next result provides the joint asymptotic distribution of and and is due to Francq and Zakoïan (2012).

Theorem 2.

In order to evaluate and in Theorem 2, we need expressions for the variance and covariance term respectively. After basic manipulation we find

with and . In a GARCH() setting, Gao and Song (2008) quantify the uncertainty around and using (3.6) while replacing the unknown quantities in by estimates. In the same spirit, and can be substituted by and while , , , and can be replaced by

| (3.7) | ||||

with and . The strong consistency of the estimators in (3.7) follows from Beutner et al. (2018, Lemma 2 and Theorem 1). Based on (3.7) we obtain a consistent estimator for denoted by . Note that in the joint asymptotic distribution in Theorem 2 the pdf of does not occur. This is in contrast to the limiting distribution of the parameters that comprise the conditional VaR estimator (Beutner et al., 2018). Hence, no density estimation (by e.g. kernel smoothing) is required here.

The asymptotic behavior of the conditional ES estimator can be studied by employing Theorem 2. Since the conditional volatility varies over time, a limiting distribution cannot exist and therefore the concept of weak convergence is not applicable in this context. Beutner et al. (2017, Section 4) advocate a merging concept that generalizes the notion of weak convergence, i.e. two sequences of (random) probability measures merge (in probability) if and only if their bounded Lipschitz distance converges to zero (in probability). Assuming two independent samples, one for parameter estimation and one for conditioning, the delta method suggests that the ES estimator, centered at and inflated by , and

| (3.8) |

given merge in probability. Equation (3.8) highlights once more the relevance of the merging concept since the conditional variance still depends on and does not converge as . In combination with Theorem 1 and , confidence intervals for can be constructed with bounds given by

| (3.9) |

where denotes the standard normal cdf. It has to be mentioned that researchers rarely have a replicate, independent of the original series, to their disposal.333Exceptions would include some experimental settings. An asymptotic justification for the interval on the basis of a single sample is given in Beutner et al. (2017). Bootstrap methods offer an alternative way to quantify the uncertainty around the estimators.

4 Bootstrap

4.1 Fixed-Design Residual Bootstrap

We propose a fixed-design residual bootstrap procedure, described in Algorithm 1, to approximate the distribution of the estimators in (3.3)-(3.5).

Algorithm 1.

(Fixed-design residual bootstrap)

- 1.

-

2.

Calculate the bootstrap estimator

(4.1) with the bootstrap criterion function given by

-

3.

For compute the bootstrap residual and obtain

(4.2) where is the empirical -quantile of .

-

4.

Obtain the bootstrap estimator of the conditional ES

(4.3)

In the following subsection we show the asymptotic validity of the fixed-design bootstrap procedure described in Algorithm 1.

4.2 Bootstrap Consistency

Subsequently, we employ the usual notation for bootstrap asymptotics, i.e. “” and “”, as well as the standard bootstrap stochastic order symbol “” (c.f. Chang and Park, 2003). The asymptotic validity of the bootstrap corresponding to the stochastic volatility part is shown in Beutner et al. (2018, Proposition 1). Therefore, we focus only on . By construction, we have , where denotes the largest integer not exceeding . Defining , we standardize (4.2) such that the bootstrap estimator satisfies

| (4.4) | ||||

where the scaling factor in (4.4) converges to since . The different terms in brackets are given by

Employing arguments of Chen (2008, Lemma 2) Lemma 1 in Appendix A.1 states the asymptotic negligibility of , i.e. in probability. The term since by construction. Further, Lemma 2 in Appendix A.1 states that in probability. Last, we have almost surely by Lemma 3 in Appendix A.1. The previous discussion together with the asymptotic expansion of in Beutner et al. (2018, Equation 4.4) yields

|

|

in probability. Employing Lemma 3 once more leads to the paper’s main result.

Theorem 3.

Theorem 3 is useful to validate the bootstrap for the conditional ES estimator. For the asymptotic behavior of the conditional ES estimator we refer to (3.8) and the text preceding it. The following corollary is established.

Corollary 1.

Having proven first-order asymptotic validity of the bootstrap procedure described in Section 4.1, we turn to constructing bootstrap confidence intervals for ES.

4.3 Bootstrap Confidence Intervals for ES

Clearly, the ES evaluation in (3.5) is subject to estimation risk that needs to be quantified. We propose the following algorithm to obtain approximately confidence intervals.

Algorithm 2.

(Fixed-design Bootstrap Confidence Intervals for ES)

-

1.

Acquire a set of bootstrap replicates, i.e. for , by repeating Algorithm 1.

-

2.1.

Obtain the equal-tailed percentile (EP) interval

(4.5) with .

-

2.2.

Calculate the reversed-tails (RT) interval

(4.6) -

2.3.

Compute the symmetric (SY) interval

(4.7) with .

For a discussion of the three interval types in Algorithm 2, we refer to Beutner et al. (2018, Section 4.3). In the next section, features of the fixed-design bootstrap confidence intervals for the conditional ES are studied by means of simulations.

5 Monte Carlo Experiment

To assess the proposed bootstrap procedure in finite samples, we consider a simulation setup similar to Beutner et al. (2018). The Data Generating Process (DGP) is a GARCH(), which falls in the class of conditional volatility models defined in (2.1)–(2.2). More specifically, we consider

with . Regarding the GARCH parameters we study two scenarios:

-

(i)

high persistence: ,

-

(ii)

low persistence: .

The innovations are drawn from two different distributions: the Student- distribution with degrees of freedom and the standard normal distribution (which corresponds to the case ). Whereas in the latter case the innovations are appropriately standardized, in the former we draw from the normalized density such that , where and . In this setting, the ES of the innovations’ distribution reduces to with and ; we refer to Appendix A.2 for details. For the experiment, the ES level takes two values: . We consider four different sample sizes and the number of bootstrap replicates is fixed at . For each model, we simulate independent Monte Carlo trajectories. All simulations are carried out on a HP Z640 workstation with 16 cores using Matlab R2016a. The numerical optimization of the log-likelihood function is performed using the built-in function fmincon. Parallel computing by means of parfor is employed to reduce running time significantly.

Beutner et al. (2018) demonstrate that the bootstrap distribution mimics adequately the finite sample distribution of the estimator of the volatility parameters. In a similar fashion, we assess whether the bootstrap distribution (given a particular sample) mimics the distribution of the ES parameter estimator.

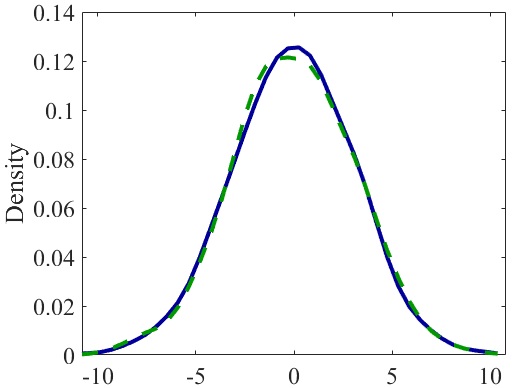

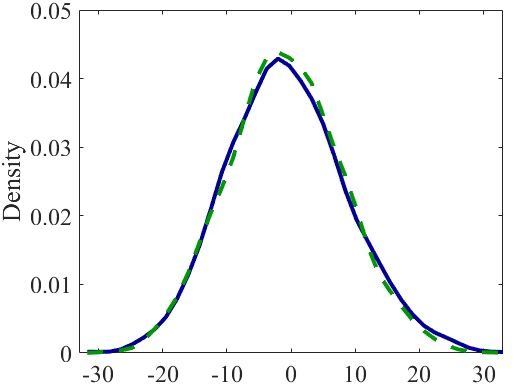

Figure 1 displays the density estimates for the distribution of and in the high persistence case for with . In both cases, we observe that the density plots are bell curves around the value zero, which supports the theoretical results of Theorem 2 and 3. Since the density graphs for the other scenarios are very similar, they are not reported in order to conserve space. We continue by studying the coverage probabilities of the three bootstrap intervals introduced in Section 4.3.

|

|

|

|

|

|

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| low persistence | high persistence | ||||||||||||||||||||

| EP | / | / | |||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

Table 1 reports the results of the three –bootstrap intervals for the –ES with Student- distributed innovations (which we consider as benchmark). For moderate sample sizes, we observe satisfactory coverage probabilities that lie relatively close to the nominal level of . For small sample size (, the intervals exhibit small under-coverage with values ranging from to percentage points () below the nominal value. For all three intervals, we find that the average rate of the conditional ES being below the interval is considerably less than it being above the interval. This phenomenon is most pronounced in smaller sample size. Concerning the average length of the intervals, we can make two important observations. Firstly, the SY interval is generally larger than the EP/RT interval.444By construction, the EP and the RT interval are of equal length. As sample size increases, this gap disappears and all intervals’ average lengths shrink. Secondly, the average length of intervals is larger in the high persistence case, as the conditional volatility varies more compared to the lower persistence case. In the following, we study deviations from the benchmark specification. Table 2 considers a change in the innovation distribution , while Table 3 and 4 take into account a change in the ES level and a change in the nominal coverage probability , respectively.

|

|

|

|

|

|

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| low persistence | high persistence | ||||||||||||||||||||

| EP | / | / | |||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

Table 2 considers the case where the innovations follow a standard normal distribution. Results are qualitatively similar to the benchmark. In particular, coverage rates are generally close to the nominal level for yet the under-coverage in smaller sample sizes is less in this scenario. For example, the average coverage is at most below the level even when . In general, results seem to be “less extreme” compared to the benchmark: the average length of all intervals is smaller for all sample sizes and the average rate of the conditional ES being above the interval lies closer to the corresponding rate below the interval. Moreover, we observe that there is no interval that outperforms the others in the case of being standard normally distributed.

|

|

|

|

|

|

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| low persistence | high persistence | ||||||||||||||||||||

| EP | / | / | |||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

Table 3 provides simulation results for the conditional ES at level , where the DGP is a GARCH() with Student- innovations (6 degrees of freedom). Unsurprisingly, we find that the average length of all intervals is considerably larger compared to the benchmark. More strikingly, we observe that the phenomenon of under-coverage appears across sample sizes. For the lowest sample size considered, i.e. , average coverage rates are between and below nominal value. This problem is still severe for the case , as rates are still approximately too low. Results are more satisfactory for the two highest sample sizes. An explanation for this result can be found in Gao and Song (2008, Remark 3.3) who assert that the effective sample size for the estimation of ES is solely . All in all, we conclude that larger sample sizes are needed to obtain acceptable coverage probabilities.

|

|

|

|

|

|

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| low persistence | high persistence | ||||||||||||||||||||

| EP | / | / | |||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

| \hdashline | EP | / | / | ||||||||||||||||||

| RT | / | / | |||||||||||||||||||

| SY | / | / | |||||||||||||||||||

Table 4 considers an increase in the interval’s nominal value from to . Once again we conclude that the results are qualitatively similar to the benchmark. The average lengths of the intervals are larger for every sample size considered. These results are to be expected for bootstrap intervals with higher nominal value.

It might be of interest to compare the results for the conditional ES with those reported in Beutner et al. (2018) for the conditional VaR. They find that the EP interval performs worse than the RT interval in small samples, which is in line with the theoretical findings in Falk and Kaufmann (1991). This result does not carry over to the conditional ES, since in most instances (except Table 4) the EP interval even outperforms the RT interval. To make a full comparison, we also computed the results where the DGP is a T-GARCH(). Results are vastly comparable and available upon request.

To summarize, the simulation study suggests that the fixed-design bootstrap works well in terms of average coverage. In comparison to the conditional VaR, higher sample sizes are necessary to obtain coverage rates close to the nominal value. There is no clear evidence to have a preference for any of the three intervals based on the simulation results in all different settings. This directly contrasts results for the conditional VaR in Beutner et al. (2018) for which the RT bootstrap interval is found superior.

6 Conclusion

This paper studies the two-step estimation procedure of Francq and Zakoïan (2015) associated with the conditional ES. In the first step, the conditional volatility parameters are estimated by QMLE, while the second step corresponds to the estimation of conditional ES based on the first-step residuals. We find that the estimators of the parameters that comprise the conditional ES have a joint asymptotic distribution that does not depend on any density. This is in direct contrast with the conditional VaR estimator for which density estimation is required. A fixed-design residual bootstrap method is proposed to mimic the finite sample distribution of the two-step estimator and its consistency is proven under mild assumptions. In addition, an algorithm is provided for the construction of bootstrap intervals for the conditional ES to take into account the uncertainty induced by estimation. Three interval types are suggested and a simulation study is conducted to investigate their performance in finite samples. Firstly, we find that average coverage rates of all intervals are close to nominal value, except when sample size is low. Secondly, we find that there is no clear evidence that any of the proposed intervals outperforms the others. This contrasts the results in Beutner et al. (2018) for the conditional VaR, who find superiority of the reversed-tails bootstrap interval.

The present work can be extended by developing a bootstrap procedure for the one-step approach estimator of Francq and Zakoïan (2015). This suggestion is left for future research.

Appendix A Appendix

A.1 Auxiliary Results and Proofs

Proof.

The proof is inspired by Chen (2008, proof of Lemma 2). Take , and expand

The first term can be bounded by

Note that, given the original sample, the random variables are i.i.d. The conditional mean satisfies ; to appreciate why, we have

where . The second equality follows from Beutner et al. (2018, Step 5 of the proof of Lemma 3) whereas the third equality is implied by , continuity of in a neighborhood of and . The fourth equality is due to Step 6 in the proof of Beutner et al. (2018, Lemma 3). The mean value theorem is applied to obtain the fifth equality and the last equality is due to continuity of in a neighborhood of and . Thus, we have

implying in probability and we conclude that in probability. Regarding the second term, we write and establish the following bound

The Taylor expansion in Beutner et al. (2018, Equation A.69) and gives

| (A.1) | ||||

with between and . Employing the Cauchy-Schwarz inequality we obtain

Hence, can further be bounded by

Since almost surely and in probability for some (see Beutner et al., 2018, Proposition 1 and Theorem 3), it remains to show that the under-braced terms converge in conditional probability to zero in probability. Consider ; for every we obtain

| (A.2) | ||||

where the last inequality is due to Markov. As , and by Beutner et al. (2018, Lemma 4 and proof of Lemma 10), we have and we conclude that in probability. Next, we focus on . For every we obtain

Previously, we have shown that , whereas the and can be made arbitrarily small in probability by choosing sufficiently large. Given , we find as . Recalling that almost surely and we find . The Cauchy-Schwarz inequality gives and together with almost surely (see Beutner et al., 2018, proof of Lemma 7), we get that . Thus, and we establish in probability. Regarding , Hölder’s inequality implies

We have almost surely as

by Beutner et al. (2018, Lemma 4). Recalling that almost surely and in probability we establish in probability. ∎

Lemma 2.

Proof.

Inserting (A.1) into the definition of we obtain

Since almost surely (Beutner et al., 2018, Proposition 1) and in probability by (A.1), it remains to show that in probability. Noting that , we obtain

by Beutner et al. (2018, Lemma 2 and 4), which completes the proof. ∎

Lemma 3.

Proof.

Beutner et al. (2018, proof of Lemma 7) shows that for sufficiently large almost surely since and whenever under Assumption 10. It remains to show that for each with

almost surely by the Cramér-Wold device. By construction, we have . Further, we have that is equal to

| (A.3) |

Beutner et al. (2018, Lemma 2) gives and . Further, Beutner et al. (2018, Lemma 5) implies

and

as well as

Thus, we get . Next, we verify Lindeberg condition. For any

holds, where . Employing the elementary inequalities and for all we find that

Thus, we obtain

and choosing sufficiently large yields . Given a value of , we have

as . Combining results, gives . The Central Limit Theorem for triangular arrays (c.f. Billingsley, 1986, Theorem 27.3) implies that converges in conditional distribution to almost surely, which completes the proof. ∎

A.2 Derivation of Analytical Expressions

Let with cdf and pdf , where denotes the Student- distribution with degrees of freedom. Define such that is now appropriately standardized such that . Then we get

The following relationship links the (conditional) moments of and :

| (A.4) |

with . Using moments of the truncated Student- distribution derived in Kim (2008, p. 84) we can find closed form expressions for the conditional expectations of . For and any we have555We only truncate from above, hence the lower truncation bound of Kim (2008) is .

where we recognize that . Together with (A.4) we have

| (A.5) |

Similarly, we can derive for and any

Combined with (A.4) we arrive at

Now, as , we obtain

| (A.6) |

Finally, we consider . Using or equivalently , it follows that

which leads to

Thus, we obtain

| (A.7) |

From (A.5)–(A.7), we get the following expressions for the quantities , and :

Note that the Student- distribution approaches the standard normal distribution as . In that case, and also and , i.e. the standard normal pdf and cdf, respectively. Hence, when is standard normally distributed, we have as well as , and .

References

- Acerbi and Tasche (2002a) Acerbi, C. and D. Tasche (2002a). Expected shortfall: A natural coherent alternative to value at risk. Economic Notes 31, 379–388.

- Acerbi and Tasche (2002b) Acerbi, C. and D. Tasche (2002b). On the coherence of expected shortfall. Journal of Banking and Finance 26, 487––1503.

- Artzner et al. (1999) Artzner, P., F. Delbaen, J.M. Eber, and D. Heath (1999). Coherent measures of risk. Mathematical Finance 9, 203––228.

- Beutner et al. (2017) Beutner, E., A. Heinemann, and S. Smeekes (2017). A justification of conditional confidence intervals. Preprint arXiv:1710.00643.

- Beutner et al. (2018) Beutner, E., A. Heinemann, and S. Smeekes (2018). A residual bootstrap for conditional value-at-risk. Preprint arXiv:1808.09125.

- Billingsley (1986) Billingsley, P. (1986). Probability and Measure (2nd ed.). New York: John Wiley & Sons.

- Cai and Wang (2008) Cai, Z. and X. Wang (2008). Nonparametric estimation of conditional var and expected shortfall. Journal of Econometrics 147, 120–130.

- Cavaliere et al. (2018) Cavaliere, G., R.S. Pedersen, and A. Rahbek (2018). The fixed volatility bootstrap for a class of ARCH() models. Journal of Time Series Analysis.

- Chang and Park (2003) Chang, Y. and J.Y. Park (2003). A sieve bootstrap for the test of a unit root. Journal of Time Series Analysis 24(4), 379–400.

- Chen (2008) Chen, S.X. (2008). Nonparametric estimation of expected shortfall. Journal of Financial Econometrics 6(1), 87–107.

- Christoffersen and Gonçalves (2005) Christoffersen, P. and S. Gonçalves (2005). Estimation risk in financial risk management. The Journal of Risk 7(3), 1–28.

- Corradi and Iglesias (2008) Corradi, V. and E.M. Iglesias (2008). Bootstrap refinements for QML estimators of the GARCH(1,1) parameters. Journal of Econometrics 144(2), 500–510.

- Falk and Kaufmann (1991) Falk, M. and E. Kaufmann (1991). Coverage probabilities of bootstrap-confidence intervals for quantiles. The Annals of Statistics 19(1), 485–495.

- Francq and Zakoïan (2012) Francq, C. and J.M. Zakoïan (2012). Risk-parameter estimation in volatility models. Working paper.

- Francq and Zakoïan (2015) Francq, C. and J.M. Zakoïan (2015). Risk-parameter estimation in volatility models. Journal of Econometrics 184(1), 158–173.

- Gao and Song (2008) Gao, F. and F. Song (2008). Estimation risk in GARCH VaR and ES estimates. Econometric Theory 24(5), 1404–1424.

- Hall and Yao (2003) Hall, P. and Q. Yao (2003). Inference in ARCH and GARCH models with heavy–tailed errors. Econometrica 71(1), 285–317.

- Hidalgo and Zaffaroni (2007) Hidalgo, J. and P. Zaffaroni (2007). A goodness-of-fit test for ARCH() models. Journal of Econometrics 141(2), 835–875.

- Kim (2008) Kim, H.J. (2008). Moments of truncated student- distribution. Journal of the Korean Statistical Society (37), 81–87.

- Martins-Filho et al. (2018) Martins-Filho, C., F. Yao, and M. Torero (2018). Nonparametric estimation of conditional value-at-risk and expected shortfall based on extreme value theory. Econometric Theory 34(1), 23–67.

- Osmundsen (2018) Osmundsen, K.K. (2018). Using expected shortfall for credit risk regulation. Journal of International Financial Markets, Institutions and Money.

- Pascual et al. (2006) Pascual, L., J. Romo, and E. Ruiz (2006). Bootstrap prediction for returns and volatilities in GARCH models. Computational Statistics & Data Analysis 50(9), 2293–2312.

- Shimizu (2009) Shimizu, K. (2009). Bootstrapping Stationary ARMA–GARCH Models. Springer.