Finite Time Analysis of Vector Autoregressive Models under Linear Restrictions

Abstract

This paper develops a unified finite-time theory for the ordinary least squares estimation of possibly unstable and even slightly explosive vector autoregressive models under linear restrictions, with the applicable region , where is the spectral radius of the transition matrix in the var(1) representation, is the time horizon and is a universal constant. The linear restriction framework encompasses various existing models such as banded/network vector autoregressive models. We show that the restrictions reduce the error bounds via not only the reduced dimensionality but also a scale factor resembling the asymptotic covariance matrix of the estimator in the fixed-dimensional setup: as long as the model is correctly specified, this scale factor is decreasing in the number of restrictions. It is revealed that the phase transition from slow to fast error rate regimes is determined by the smallest singular value of , a measure of the least excitable mode of the system. The minimax lower bounds are derived across different regimes. The developed non-asymptotic theory not only bridges the theoretical gap between stable and unstable regimes but precisely characterizes the effect of restrictions and its interplay with model parameters. Simulations support our theoretical results.

Abstract

This supplementary material contains all technical proofs of the main paper. S1 gives the proofs of Theorem 1 and Proposition 1, which rely on three auxiliary lemmas, Lemmas S1–S3, whose proofs are relegated to S1.4. S2 contains the proofs of Lemmas 1–3. In S3, we first verify equation (3.10) in the main paper and then prove Proposition 2 through four auxiliary lemmas, Lemmas S5–S8. S4 contains the proof of Theorem 3. Lastly S5 proves Theorem 4 and Corollary 1 after introducing two auxiliary lemmas, Lemmas S9 and S10.

Keywords: Consistency; Empirical process theory; Least squares; Non-asymptotic analysis; Stochastic regression; Unstable process; Vector autoregressive model.

1 Introduction

The vector autoregressive model (Sims,, 1980) is arguably the most fundamental model for multivariate time series (Lütkepohl,, 2005; Tsay,, 2013). Applications of the model and its variants can be found in almost any field that involves learning the temporal dependency: economics and finance (Wu and Xia,, 2016), energy forecasting (Dowell and Pinson,, 2016), psychopathology (Bringmann et al.,, 2013), neuroscience (Gorrostieta et al.,, 2012) and reinforcement learning (Recht,, 2018), etc.

Consider the vector autoregressive model of order one, var(1), in the following form:

where is the observed time series, is the unknown transition matrix, and is the innovation. In modern applications, the dimension is often relatively large. However, since the number of unknown parameters increases as , leading to problems such as over-parametrization, the model cannot provide reliable estimates or forecasts without further restrictions (Stock and Watson,, 2001). A classical approach to dimensionality reduction for vector autoregressive models, which recently has enjoyed a resurgence of interest, advocates the incorporation of prior knowledge into modelling. For example, motivated by the fact that in spatio-temporal studies, it is often sufficient to collect information from ‘neighbors’, Guo et al., (2016) proposed the banded vector autoregressive model, where the nonzero entries of are assumed to form a narrow band along the main diagonal, after arranging the components of by geographic location. To analyse users’ time series over large social networks, the network vector autoregressive model of Zhu et al., (2017) used the follower-followee adjacency matrix to determine the zero-nonzero pattern of , together with equality restrictions to further reduce the dimensionality. In fact, the above models can both be incorporated by the general framework of linear restrictions

| (1.1) |

where is a prespecified restriction matrix, is a known constant vector, and is the transpose of . This form of restrictions is traditionally well known by time series modellers; see books on multivariate time series analysis such as Reinsel, (1993), Lütkepohl, (2005) and Tsay, (2013).

Meanwhile, drawing inspiration from recent developments in high-dimensional regression, another well studied approach concerns the penalized estimation, where the modeller is agnostic to the locations of nonzero coordinates in while assuming certain sparsity (Davis et al.,, 2015; Han et al., 2015a, ; Basu and Michailidis,, 2015), or the directions of low-dimensional projections while, e.g., assuming a low rank structure of (Ahn and Reinsel,, 1988; Negahban and Wainwright,, 2011). Note that in the former case, once the locations of nonzero coordinates are identified, the model can be formulated as an instance of (1.1). Although we focus on fully known restrictions, the framework of (1.1) allows us to study the theoretical properties of a much richer variety of restriction patterns in this paper.

On the other hand, in the literature on large vector autoregressive models, there has been an almost exclusive focus on stable processes. Technically, this means requiring that the spectral radius , or often more stringently, that the spectral norm . However, the analysis of stable processes typically cannot be carried over to unstable processes. In this paper, we provide a novel finite-time (non-asymptotic) analysis of the ordinary least squares estimator for stable, unstable and even slightly explosive vector autoregressive models within the general framework of (1.1).

Our analysis sheds new light on the phase transition phenomenon of the ordinary least squares estimator across different stability regimes. This is made possible by adopting the non-asymptotic, non-mixing approach of Simchowitz et al., (2018). Resting upon a generalization of Mendelson’s (2014) small-ball method, this approach is particularly attractive because: (i) it unifies stable and unstable cases, whereas in asymptotic theory these two cases would require substantially different techniques; and (ii) in contrast to existing non-asymptotic methods, it can well capture the fundamental trait that the estimation will be more accurate as . While relaxing the normality assumption in Simchowitz et al., (2018), we precisely characterize the impact of imposing restrictions on the estimation error. More importantly, we reveal for the first time that the phase transition from slow to fast error rates depends on the the smallest singular value of , a measure of the least excitable mode of the system. In addition, we expand the applicable region in the above paper to , where is a universal constant, so slightly explosive processes are also included. Compared to Guo et al., (2016) which focused on the case with , our assumption on the innovation distribution is stronger, and our error rate for the stable regime is larger by a logarithmic factor which, however, can be dropped under the normality assumption; see 3.4 for details. Note that although Zhu et al., (2017) relied on even milder assumptions on the innovations than Guo et al., (2016), they assumed that the number of unknown parameters is fixed, and hence their theoretical analysis is incomparable to ours; see Example 3 in 3.1.

Throughout we denote by the Euclidean norm and by the unit sphere in . For a real matrix , we let and (or and ) be its largest and smallest eigenvalues (or singular values), respectively; additionally, we let and be the spectral radius, spectral norm and Frobenius norm of , respectively. For , let and , where is the set of integers. We write (or ) if is a positive definite (or positive semidefinite) matrix. Moreover, for any real symmetric matrices and , we write (or ) if (or ), and write (or ) if (or ) does not hold. For any quantities and , we write if there exists a universal constant independent of , whose meaning will become clear later, such that .

2 Linearly restricted stochastic regression

2.1 Problem formulation

Consider a sequence of time-dependent covariate-response pairs following

| (2.1) |

where , , and . In particular, (2.1) becomes the var(1) model when . In model (2.1), the process is adapted to the filtration

Let , where . The parameter space of the linearly restricted model can be defined as

where is a known matrix of rank , representing independent restrictions, and is a known constant vector which may simply be set to zero in practice. Let be an complement of such that is invertible, with its inverse partitioned into two blocks as , where is the matrix of the first columns of . Additionally, define . Then it holds . Note that if , then , where . Conversely, for any , if , then . Thus, we have

i.e., the linear space spanned by columns of the restriction matrix , shifted by the constant vector . This immediately implies that, given , there exists a unique unrestricted parameter such that . Note that if and only if . Moreover, the unrestricted model corresponds to the special case where and .

The following examples illustrate how the linear restrictions can be encoded by or , where without loss of generality we set . Let denote the th entry of .

Example 1 (Zero restriction).

The restriction may be encoded by setting the th row of to zero, or by setting a row of to , where the th entry is one.

Example 2 (Equality restriction).

Consider the restriction . Suppose that the value of is , the th entry of . Then this restriction may be encoded by setting both the th and th rows of to , where the th entry is one. Alternatively, we may set a row of to the vector whose th element is defined as , where is the indicator function.

Define matrices and , and the matrix . Then (2.1) has the matrix form . Let , , , and . By vectorization and reparameterization, we have

As a result, the ordinary least squares estimator of for the linearly restricted model is

| (2.2) |

Notice that . To ensure the feasibility of (2.2), we need . Let and , where are matrices and are vectors. Then, , where

Consequently, the ordinary least squares estimator of is .

2.2 General upper bounds analysis

To derive upper estimation error bounds for the stochastic regression model in 2.1, we begin by introducing a key technical ingredient, namely the block martingale small ball condition (Simchowitz et al.,, 2018). As a generalization of Mendelson’s (2014) small-ball method to time-dependent data, this condition can be viewed as a non-asymptotic stability assumption for controlling the lower tail behavior of the Gram matrix , or in our context.

Definition 1 (Block Martingale Small Ball Condition).

(i) For a real-valued time series adapted to the filtration , we say that satisfies the -bmsb condition if there exist an integer and constants and such that, for every integer , with probability one. (ii) For a time series taking values in , we say that satisfies the -bmsb condition if there exists such that, for every , the real-valued time series satisfies the -bmsb condition.

The value of the probability is unimportant for our purpose as long as it exists. The thresholding matrix , or in the univariate case, captures the average cumulative excitability over any size- block; e.g., if is a mean-zero vector autoregressive process, then will scale proportionally no less than , which is constant for all . Since every time point is associated with a new shock to the process, will increase as increases. Consequently, will be monotonic increasing in ; see Lemma 1 in 3.2. Moreover, by aggregating all the size- blocks, will essentially become the lower bound of . Note that for the ordinary least squares estimation, a larger lower bound on the Gram matrix will yield a sharper estimation error bound. Thus, a larger block size is generally preferred; see Theorem 3 in 3 for details.

Let and be positive definite matrices, and denote

| (2.3) |

In our theoretical analysis, properly rescaled matrices and will serve as lower and upper bounds of the Gram matrix , respectively, and the covering numbers derived from them will give rise to the quantity in Theorem 1 below. The regularity conditions underlying our upper bound analysis are listed as follows:

Assumption 1.

The covariates process satisfies the -bmsb condition.

Assumption 2.

For any , there exists defined as in (2.3) such that , where , and is dependent on .

Assumption 3.

For every integer , is mean-zero and -sub-Gaussian.

Theorem 1.

Note that . The result in Theorem 1 is new even for the unrestricted stochastic regression, where . For vector autoregressive processes, we will specify the matrices and in 3.2, where will depend on the block size through . As increases, will become larger and hence the factor will become smaller, resulting in a sharper error bound. However, cannot be too large due to condition (2.4). Specifically, this condition arises from applying the Chernoff bound technique to lower bound the Gram matrix via aggregation of all the size- blocks, since the probability guarantee of the Chernoff bound will degrade as the number of blocks decreases; see Lemma S2 in the supplementary material. Therefore, to apply Theorem 1 to vector autoregressive processes, a crucial step will be to derive a feasible region for that guarantees condition (2.4); see 3.3 for details.

Similarly, we can obtain an analogous upper bound for in the spectral norm:

Proposition 1.

Let be generated by the linearly restricted stochastic regression model. Fix . Then, under the conditions of Theorem 1, with probability at least , we have

3 Linearly restricted vector autoregression

3.1 Representative examples

We begin by illustrating how the formulation in 2 can be used to study vector autoregressive models. Four representative examples will be discussed: var() model, banded vector autoregressive model, network vector autoregressive model, and pure unit root process.

Consider the var() model, i.e., model (2.1) with :

| (3.1) |

subject to , where , with being matrices, , and with .

Example 1 (var() model).

Interestingly, vector autoregressive models of order can be viewed as linearly restricted var() models. Consider the var() model

| (3.2) |

where , and for . Denote , , , and

| (3.3) |

As a result, (3.2) can be written into the var() form in (3.1). As shown in (3.3), all entries in the last rows of are restricted to either zero or one. The restriction can be encoded in in the same way as Example 1 in 2.1 but with the th entry of set to one. Thus, with or without restrictions, the var() model can be studied by the same method as that for a linearly restricted var(1) model. Note that the special structure of the innovation that some entries of are fixed at zero will not pose any extra difficulty.

In the following examples, we consider var(1) models with various structures for , and set so that the restrictions are in the form of :

Example 2 (Banded vector autoregression).

Guo et al., (2016) proposed the vector autoregressive model with the following zero restrictions:

| (3.4) |

where the integer is called the bandwidth parameter. Let be the transpose of the th row of . Hence, . Note that the restrictions are imposed on each separately. As a result, the ’s are determined by non-overlapping subsets of entries in ; that is, we can write , where , , , and . In this case, is a block diagonal matrix:

and (3.4) can be encoded in as follows: (1) and if ; (2) and if ; and (3) and if .

Example 3 (Network vector autoregression).

Consider the network model in Zhu et al., (2017). Let us drop the individual effect and the intercept to ease the notations. This model assumes that all diagonal entries of are equal: for . For the off-diagonal entries, the zero-nonzero pattern is known and completely determined by the social network: if and only if individual follows individual . Moreover, all nonzero off-diagonal entries are assumed to be equal: if , for . This model is actually very parsimonious, with only , while the network size can be extremely large. To incorporate the above restrictions, we may define the matrix as follows: for , the th row of is if corresponds to a diagonal entry of , if corresponds to a nonzero off-diagonal entry of , and if corresponds to a zero off-diagonal entry of .

Example 4 (Pure unit root process).

Another simple but important case is with . Then, the smallest true model has , and the corresponding restrictions, and for , can be imposed by setting , where is the vector with all elements zero except the th being one. When , the underlying model becomes the pure unit root process, a classic example of unstable vector autoregressive processes (Hamilton,, 1994). In particular, the problem of testing , or unit root testing in panel data, has been extensively studied in the asymptotic literature; see Chang, (2004) and Zhang et al., (2018) for studies in low and high dimensions, respectively. Note that Zhang et al., (2018) focused on asymptotic distributions of the largest eigenvalues of the sample covariance matrix of the pure unit root process under . It does not involve parameter estimation and hence cannot be directly compared to this paper.

The stochastic regression can also incorporate possibly time-dependent exogenous inputs such as individual effects (Zhu et al.,, 2017) and observable factors (Zhou et al.,, 2018), leading to the class of varx models (see, e.g., Wilms et al.,, 2017). Since varx models can be analyzed similarly to vector autoregressive models, we do not pursue the details in this paper.

3.2 Verification of Assumptions 1–3 in Theorem 1

In light of the generalisability to var() models via the var() representation, to apply the general results in § 2.2 to linearly restricted vector autoregressive models, it suffices to restrict our attention to the var() model in (3.1) from now on.

Following the notations in 2, let , , and , where and . Note that for the var() model. In addition, is adapted to the filtration

The following conditions on will be invoked in our analysis:

Assumption 4.

(i) The process starts at with ; (ii) the innovations are independent and identically distributed with and ; (iii) there is a universal constant such that, for every with , the density of is bounded from above by almost everywhere; and (iv) are -sub-Gaussian.

Under Assumption 4(i), we can simply write in the finite-order moving average form, for any . Then, by Assumption 4(ii), , where

| (3.5) |

is called the finite-time controllability Gramian (Simchowitz et al.,, 2018). Note that for whatever . By contrast, the typical setup in asymptotic theory of stable processes assumes that starts at . In this case, has the infinite-order moving average form , so if and only if . Thus, an important benefit of Assumption 4(i) is that it allows us to capture the possibly explosive behavior of over any finite time horizon, and derive upper bounds of the Gram matrix over different stability regimes; see Lemmas 2 and 3 in this subsection.

The condition in Assumption 4(ii) is imposed for simplicity. However, we can easily extend all the proofs in this paper to the general case with any symmetric matrix : we only need to rederive all results with the role of replaced by . Assumption 4(iii) is used to establish the block martingale small ball condition, i.e., Assumption 1, for vector autoregressive processes, and it allows us to lower bound the small ball probability by leveraging Theorem 1.2 in Rudelson and Vershynin, (2015) on densities of sums of independent random variables; see also Remark 3. Essentially, Assumption 4(iii) only requires that the distribution of any one-dimensional projection of the innovation is well spread on the real line. Examples of such distributions include multivariate normal and multivariate (Kotz and Nadarajah,, 2004) distribution and, more generally, elliptical distributions (Fang et al.,, 1990) with the consistency property in Kano, (1994). Lastly, it is clear that Assumptions 4(ii) and (iv) guarantee Assumption 3.

Remark 1.

In asymptotic theory, stable and unstable processes require substantially different techniques, and results derived under typically cannot be carried over to unstable processes. For example, the convergence rate of the ordinary least squares estimator for fixed-dimensional unstable var(1) processes is instead of , and the limiting distribution is no longer normal (Hamilton,, 1994).

Remark 2.

The controllability Gramian is interpretable even without Assumption 4(i). By recursion, we have for any time point and duration . As a result, , and it simply becomes if . Note that , or equivalently , is a partial sum of a geometric sequence due to the autoregressive structure. Roughly speaking, larger means more persistent impact of .

In the following, we present three lemmas for the linearly restricted vector autoregressive model. Lemma 1 establishes the block martingale small ball condition by specifying , while Lemmas 2 and 3 verify Assumption 2 by providing two possible specifications of .

Some additional notations to be used in Lemma 3 are introduced as follows: Denote by the covariance matrix of the vector , so the th block of is , for . Then define

| (3.6) |

where , and is a universal constant.

Lemma 1.

Suppose that follows for . Under Assumptions 4(ii) and (iii), for any , satisfies the -bmsb condition, where .

Lemma 2.

Let be generated by the linearly restricted vector autoregressive model. Under Assumptions 4(i) and (ii), for any , it holds , where , with .

Lemma 3.

Remark 3.

Unlike Simchowitz et al., (2018), by leveraging Rudelson and Vershynin, (2015), we establish the block martingale small ball condition without the normality assumption. If Assumption 4(ii) is relaxed to the general , by a straightforward extension of the proof of Lemma 1, we can show that Lemma 1 holds with .

Remark 4.

Lemma 2 is a simple consequence of the Markov inequality and the property that , so no distributional assumption on is required. However, Lemma 3 relies on the Hanson-Wright inequality (Vershynin,, 2018), where the normality assumption is invoked. Although adopting the in Lemma 3 can eliminate a factor of in the resulting estimation error bounds, the in Lemma 2 actually leads to sharper bounds under certain conditions on ; see 3.3 and 3.4 for details.

By Lemma 1, for any , the matrix in Theorem 1 can be specified as

| (3.7) |

By Lemmas 2 and 3, the matrix in Theorem 1 can be chosen as or , where

| (3.8) |

recall the definitions of and in (2.3), where for the var() model. Furthermore, observe that in (3.7) and the two ’s in (3.8), which serve as lower and upper bounds of , respectively, are all related to the controllability Gramian , and .

3.3 Feasible region of

With and chosen as in (3.7) and (3.8), the term in condition (2.4) in Theorem 1 is intricately dependent on both and . Thus, in order to apply the theorem to model (3.1), we need to verify the existence of the block size satisfying (2.4). This boils down to deriving an explicit upper bound of free of .

By (3.5) and (3.7), it is easy to show that is monotonic increasing in . Then, as is free of , is maximized when . As a result, we can first upper bound by its value at to get rid of its dependence on . That is,

| (3.9) |

Now it suffices to upper bound the right-hand side of (3.9), where can be chosen from and in (3.8). As shown in the supplementary material,

| (3.10) |

where is defined as in (3.6), and

| (3.11) |

Obviously, without imposing normality, we can only choose ; see Lemmas 2 and 3 in 3.2. However, if are normal, can be set to whichever of and delivers the sharper upper bound. Note that both and depend on , and their growth rates with respect to depend on the magnitude of . This will ultimately affect the choice between and ; e.g., if is the dominating term in both upper bounds in (3.10), we will be indifferent between the two. Assumptions 5–6′ below summarize the three cases of we consider:

Assumption 5.

It holds , where is a universal constant.

Assumption 6.

It holds and , where are universal constants.

Assumption 6′.

It holds , , and for any integer , where and are universal constants, and for any complex number .

Assumption 5 is the most general case among the above three, and Assumption 6 is weaker than Assumption 6′. Notably, Assumption 6′ does not require because may be greater than one. Guo et al., (2016) assumed for and any positive integer , while it is unclear if this can be relaxed to as in Assumption 6′. We need to be bounded away from zero in order to derive a sharp upper bound on ; see Remark 6 below. This condition is also necessary for the estimation error rates derived in Basu and Michailidis, (2015) for a similar reason. In particular, if is diagonalizable, it is shown in Proposition 2.2 therein that , where is defined in (3.12) below.

Remark 5.

From (3.11), is dependent on through . If , it holds , and then , an upper bound free of . By contrast, if , no longer exists, and we need to carefully control the growth rate of ; see Lemma S7 in the supplementary material. This is achieved via the Jordan decomposition of in (3.12) below, and the mildest condition we need is Assumption 5. The upper bound of under Assumption 5 or 6 is given by Lemma S5 in the supplementary material.

Remark 6.

For defined in (3.6), it is worth noting that depends on , as , where for under Assumptions 4(i) and (ii). Unlike discussed in Remark 5, even under Assumption 6, is not guaranteed to be bounded by a constant free of ; indeed, we need Assumption 6′ for this purpose, since is affected by not only the growing diagonal blocks but also the growing off-diagonal blocks; see Lemma S8 in the supplementary material for details. The upper bound of under Assumption 5 or 6′ is given by Lemma S6 in the supplementary material.

Let the Jordan decomposition of be

| (3.12) |

where has blocks with sizes , and both and are complex matrices. Let and denote the condition number of by , where is the conjugate transpose of .

The following proposition, which follows from (3.9), (3.10) and upper bounds of and under Assumptions 5, 6 or 6′, is proved in S3 of the supplementary material.

Proposition 2.

The condition in Proposition 2 is not stringent, because it is necessary for condition (2.4) in Theorem 1, where for the model. By Proposition 2, yields a sharper upper bound of than does only under Assumption 6′. Thus, we shall always set unless Assumption 6′ holds and are normal. As a result, under Assumption 4, the feasible region of that is sufficient for condition (2.4) in Theorem 1 is

| (3.13) |

3.4 Analysis of upper bounds in vector autoregression

We focus on the upper bound analysis of ; nevertheless, from Proposition 1 we can readily obtain analogous results for , which are omitted here. For simplicity, denote

Theorem 2.

Let be generated by the linearly restricted vector autoregressive model. Fix . For any satisfying (3.13), under Assumption 4, we have the following results: (i) If Assumption 5 holds, with probability at least ,

(ii) If Assumption 6 holds, with probability at least ,

(iii) If Assumption 6′ holds and are normal, with probability at least ,

To gain an intuitive understanding of the factor in Theorem 2, consider the asymptotic distribution of under the assumptions that and that and are all fixed:

| (3.14) |

in distribution as , where ; see Lütkepohl, (2005). Thus, in Theorem 2 resembles the limiting covariance matrix . However, it is noteworthy that by adopting a non-asymptotic approach, Theorem 2 retains the dependence of the estimation error on across stable, unstable and slightly explosive regimes. Also note that, similarly to (3.14), the error bounds in Theorem 2 are free of , as the scaling effect of on is canceled out by that on due to the autoregressive structure.

As a special case, if is diagonalizable. Moreover, if , then , , , with , and thus

| (3.15) |

where the second equality is due to the fact that, for any matrices and , and have the same nonzero eigenvalues (Theorem 1.3.20, Horn and Johnson,, 1985).

By Theorem 2, The linear restrictions affect the error bounds through both the factor and the explicit rate function of and . To further illustrate this, suppose that

where has rank , and has rank , with . Then . By an argument similar to that in Lütkepohl, (2005, p. 199), we can show that , so

| (3.16) |

Note that the parameter space has fewer restrictions than . Therefore, with fewer restrictions, the effective model size will increase from to , and meanwhile will increase to , both leading to deterioration of the error bound.

Remark 7.

The preservation of the factor in Theorem 2 is achieved by bounding and simultaneously through the Moore-Penrose pseudoinverse , and note that if ; see also Simchowitz et al., (2018). This key advantage is not enjoyed by the non-asymptotic analyses in Basu and Michailidis, (2015) and Faradonbeh et al., (2018). In their analyses, and , or and in our context, were bounded separately. This would not only break down , but also cause degradation of the error bound as due to the inevitable involvement of the condition number of in the resulting error bound.

Remark 8.

The next theorem sharpens the error bounds in Theorem 2 by utilizing the largest possible , since is monotonic decreasing in . The dependence of on will be captured by , a measure of the least excitable mode of the underlying dynamics.

Theorem 3.

Suppose that the conditions of Theorem 2 hold. Fix , and let be a universal constant.

(i) Under Assumption 5, if

| (A.1) |

then, with probability at least ,

| (S.1) |

and if inequality (A.1) holds in the reverse direction, then, with probability at least ,

| (F.1) |

Theorem 3 reveals an interesting phenomenon of phase transition from slow to fast error rate regimes, i.e., from about as in (S.1)–(S.3) to about as in (F.1)–(F.3), up to logarithmic factors. Within the slow rate regime, the estimation error decreases as increases. Note that the slow rates in (S.1)–(S.3) differ from each other only by logarithmic factors, and so do the fast rates in (F.1)–(F.3). Moreover, the point at which the transition occurs is dependent on instead of ; see conditions (A.1)–(A.3). Since , conditions (A.1)–(A.3) may be mild as long as is not too large. However, the fast rates require the opposite of (A.1)–(A.3), which cannot be directly inferred from .

Remark 9.

For the special case of with , Assumptions 6 and 6′ both simply reduce to , and Assumption 5 to . Also, and . Thus, under Assumption 4, by (F.1), (S.2) and (F.2), the following holds with high probability:

Moreover, if are normal, by (S.3) and (F.3), we can eliminate all factors of in the above results; that is, every will be replaced by .

Remark 10.

Faradonbeh et al., (2018) derived error bounds for the ordinary least squares estimator of explosive unrestricted vector autoregressive processes when (1) or (2) has no unit eigenvalue. In contrast to case (1), we focus on slightly explosive processes with . Moreover, the no unit root requirement of case (2) may be quite restrictive; e.g., it excludes the case of in Remark 9. Thus, the conditions in Theorem 3 may be more reasonable in practice.

Remark 11.

Guo et al., (2016) obtained the error rate for the banded vector autoregressive model under weaker conditions on yet stronger conditions on than those in this paper; see Theorem 2 therein. Particularly, they required . Note that this rate matches (S.3). In view of the lower bounds to be presented in 4, we conjecture that the rate in (S.2) is larger than the actual rate by a factor of .

4 Analysis of lower bounds

For any , let , and the corresponding transition matrix is denoted by , where , , and are defined as in 3.1. As is completely determined by , it is more convenient to index the probability law of the model by the unrestricted parameter . Thus, we denote by the distribution of the sample on , where and . For any fixed , we write the subspace of such that the spectral radius of is bounded above by as

The corresponding linearly restricted subspace of is denoted by .

The minimax rate of estimation over , or , is provided by the next theorem.

Theorem 4.

As a result, we have the following minimax rates of estimation across different values of .

Corollary 1.

For the linearly restricted vector autoregressive model in Theorem 4, the minimax rates of estimation over are given as follows:

(i) , if ;

(ii) , if for a fixed ; and

(iii) , if .

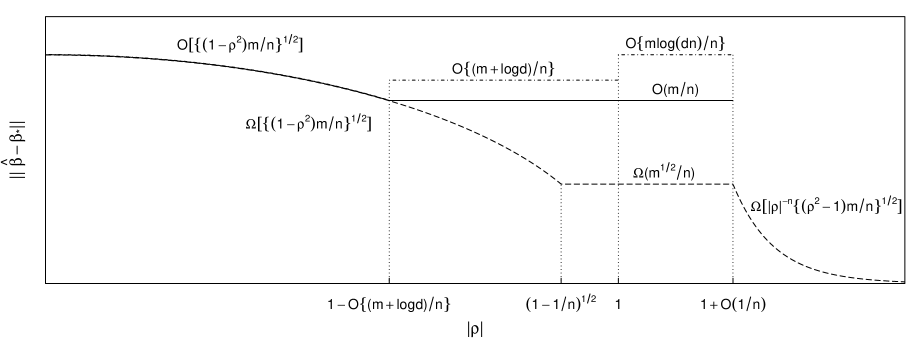

While the phase transition in Corollary 1 depends on instead of , we may still compare the lower bounds to the upper bounds in Theorem 3. For case (i) in Corollary 1, since , we may expect that condition (A.2) will hold in most cases, and hence the upper bound differs from the lower bound by a factor of . However, for case (ii), the upper bound may lie in either the slow or fast rate regime, depending on the magnitude of , whereas the lower bound lies in the fast rate regime. As shown by our first experiment in 5, the transition from slow to fast error rates actually depends on instead of . This also suggests that the results in Theorem 3 are sharp in the sense that they correctly capture the transition behavior.

Remark 12.

If with and are normal, in view of Remark 9 and Corollary 1, a more straightforward comparison of the upper and lower bounds can be made:

| Range of | Lower bound | Upper bound |

|---|---|---|

See Figure 1 for an illustration of the theoretical bounds and actual rates suggested by simulation results in 5. Note that the actual rates and the theoretical upper and lower bounds exactly match when . In addition, the suggested actual rate is for and even faster for beyond this range.

Remark 13.

Han et al., 2015b considered the estimation of a class of copula-based stationary vector autoregressive processes which includes the Gaussian var() process as a special case, and extended the theoretical properties to processes by arguments similar to those in Example 1. Under a strong-mixing condition on the process and the low-rank assumption , the proposed estimator was proved to attain the minimax error rate . While we consider different restrictions and estimation method, the rate in Corollary 1 for the stable regime resembles that in Han et al., 2015b if we regard as the effective model size of the low-rank model. However, similarly to our upper analysis in 3, the factor of in our lower bound also reveals that the estimation error may decrease as approaches the stability boundary.

5 Simulation experiments

We conduct three simulation experiments to verify the theoretical results in previous sections, including (i) the estimation error rates, (ii) the transition from slow to fast rates regimes, and (iii) the effect of the ambient dimension on the estimation. The data are generated from var processes with drawn independently from and the following structures of :

DGP1: Banded structure defined by the zero restrictions if , where is the bandwidth parameter; see Example 2 in 3.1. As a result, if all restrictions are imposed, the size of the model is .

DGP2: Group structure defined by equality restrictions as follows. Partition the index set of the coordinates of into groups of size as , where

In each row of , the off-diagonal entries with belonging to the same group are assumed to be equal: for any and , all elements of are equal. Thus, , as there are free parameters in each row of .

DGP3: , where . Note that the smallest true model with size results from imposing zero restrictions on all off-diagonal entries of and equality restrictions on all diagonal entries; see Example 4 in 3.1.

Throughout the experiments, the estimation error is calculated by averaging over replications. Except for DGP3, nonzero entries of are generated independently from and then rescaled such that is equal to a certain value.

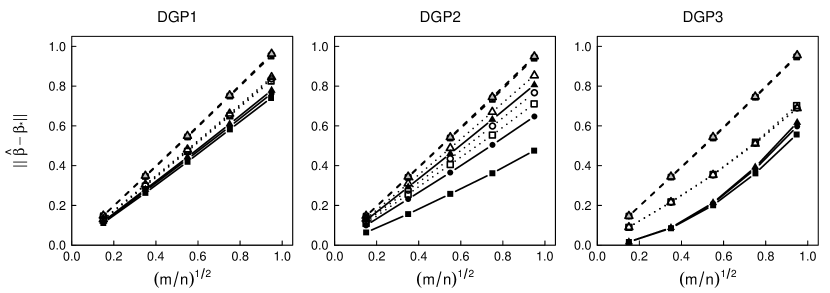

The first experiment aims to verify the error rates in Theorem 3 and the implication of Theorem 2 that the restrictions can reduce the estimation error through both the explicit rate and the decrease in the factor . Fixing and or , we generate data from DGP1 with , DGP2 with , and DGP3. For DGP1 and DGP3, we fit banded vector autoregressive models with or such that or , respectively. For DGP2, we fit the group-structured model with or such that or , respectively. Note that for DGP1 and DGP2, even when the randomly generated matrix has . However, for DGP3, it holds . The estimation error is plotted against in Figure 2, where we consider . Our findings are summarized as follows:

(i) When , for all data generating processes, the lines for different coincide completely with each other and scale perfectly linearly with . This suggests that the actual error rate is when lies in the slow rate regime of Theorem 3.

(ii) When or 1, for DGP1 and DGP2, although is still proportional to , the three lines for the same but different do not coincide: fixing , the slope increases as increases, and the variation in slope is greater as is larger. Note that for DGP1 and DGP2, is very small. As finding (i) suggests that the actual error rate is for small , this extra variation in slope may be partially explained by the factor in the error bound in Theorem 2 due to the effect of . However, actually depends on the spectrum of , and its largest eigenvalue merely serves as an upper bound. When is smaller, we will have more control over the spectrum of and hence that of . This may explain why the variation in slope is smaller when is smaller.

(iii) For DGP3 with or , the three lines corresponding to different still completely coincide with each other. This can be explained by the fact that is independent of when ; see (3.15).

(iv) For DGP3 with , in sharp contrast to all other cases, the error rate appears to be a quadratic function of . This matches the implication of Theorem 3 that when , the error rate falls into the fast rate regime.

(v) Fixing both and , always decreases as increases. Moreover, when , fixing , the lines become less steep as increases. Note that is larger when is, due to our method of generating . Thus, this finding can be explained by the factor in the error bound for the slow rate regime in Theorem 3.

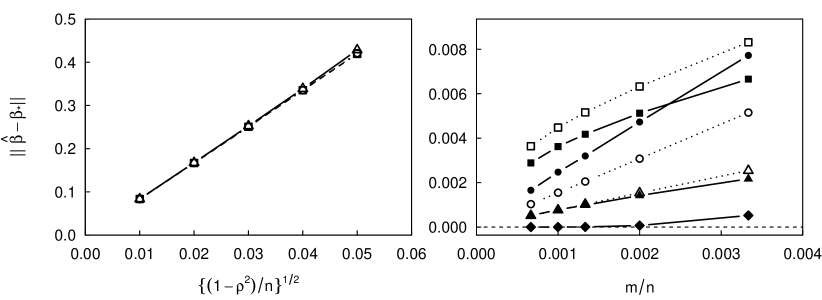

In the second experiment, we focus on DGP3 to further investigate the error rates and the phase transition. We set and or , where results from fitting the smallest true model, and or from fitting a banded model with or , respectively. Figures 3 and 4 display the results, where we have the following findings:

(i) The combination of results from the first experiment and the left panel of Figure 3 suggests that scales as when is fixed at a level well below one.

(ii) Figure 4 suggests that when the actual error rate is . Specifically, when is fixed, the left panel shows that becomes stable for sufficiently large, while multiplied by or appears to diminish as . On the other hand, when is fixed, the right panel shows that becomes stable for sufficiently large.

(iii) The right panel of Figure 3 suggests that the regime of rate is reached as early as and maintains even as the process becomes slightly explosive with . This lends support to the boundaries of the fast rate regime suggested by Theorem 3; see Remarks 9 and 12. By contrast, when , the rate appears to be , similarly to our findings in the first experiment. On the other hand, when is fixed at a level slightly above one, the rate becomes even faster than . This matches the conclusion in Remark 12 that the corresponding lower bound diminishes at a rate faster than as increases.

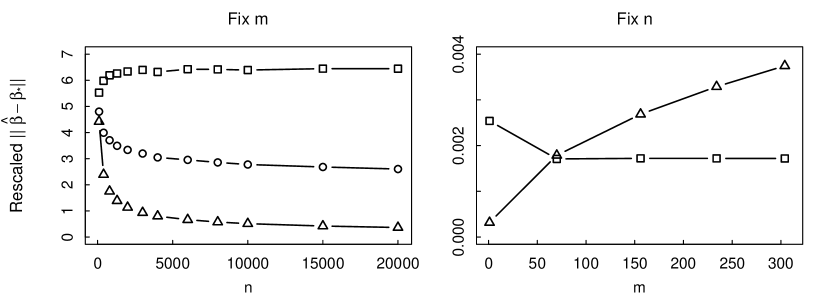

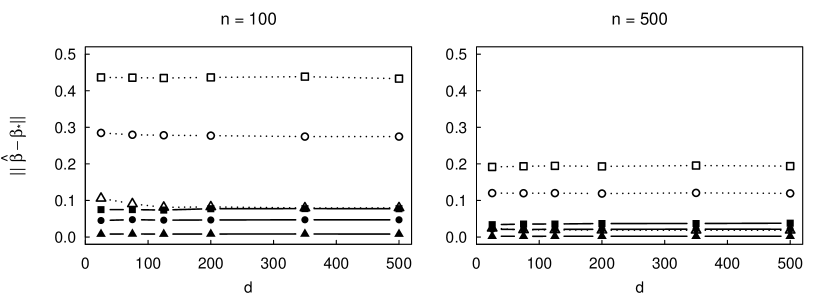

The third experiment aims to check if the ambient dimension directly affects the estimation error. We generate data from DGP3 with or , or and . For the estimation, we consider or , where corresponds to the smallest true model, and corresponds to a model subject to (1) and (2) the restriction that all but of the off-diagonal entries of are zero. To generate the pattern in (2), we sample the positions uniformly without replacement from all off-diagonal positions of .

Figure 5 shows that the estimation error is constant in for almost all cases. This confirms that does not affect the estimation error when ; see Remark 12. Moreover, the extra factor of in the theoretical upper bounds for the other regimes might not be necessary. For , the estimation error seems less stable when ; see the left panel of Figure 5. This might be explained by the indirect effect of on in Theorem 2. As is fixed at , different corresponds to different . The spectrum of may be more sensitive to when is smaller, and the resulting impact on the estimation error may be more pronounced when is smaller. However, as grows, the restrictions will become relatively more sparse, so eventually the spectrum of will be stable, and the impact of will be negligible.

6 Discussion

An interesting future direction is dimensionality reduction for vector autoregressive models with data-driven restrictions. Such a procedure involves first suggesting possible restrictions based on subject knowledge and then selecting the true restrictions by a data-driven approach. Note that the lasso method (Davis et al.,, 2015; Basu and Michailidis,, 2015) can be viewed as a procedure where zero restrictions are initially suggested for all entries of , and then the true zeros are identified by penalized estimation. Adopting a more general point of view, the modeller can initially suggest the general linear restrictions (1.1) instead. This will enable a more flexible and data-driven integration of expert knowledge. On the other hand, if it is known that only zero and equality restrictions are true, yet the locations of the restrictions are unknown, we can select the true restrictions efficiently by the delete or merge regressors algorithm proposed by Maj-Kańska et al., (2015) based on the Bayesian information criterion. The consistency of this procedure can be easily extended to vector autoregressive models.

Acknowledgement

We thank the editor, associate editor and two referees for their invaluable comments, which have led to substantial improvements of our paper. Cheng’s research was partially supported by the U.S. National Science Foundation and the Office of Naval Research, and he wishes to thank the Institute for Advanced Study at Princeton for its hospitality during his visit in Fall 2019.

Supplementary material

Supplementary material available at Biometrika online includes all technical proofs of this paper.

References

- Ahn and Reinsel, (1988) Ahn, S. K. and Reinsel, G. C. (1988). Nested reduced-rank autogressive models for multiple time series. Journal of the American Statistical Association, 83:849–856.

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43:1535–1567.

- Boucheron et al., (2013) Boucheron, S., Lugosi, G., and Massart, P. (2013). Concentration inequalities: A nonasymptotic theory of independence. Oxford University Press, Oxford.

- Bringmann et al., (2013) Bringmann, L. F., Vissers, N., Wichers, M., Geschwind, N., Kuppens, P., Peeters, F., Borsboom, D., and Tuerlinckx, F. (2013). A network approach to psychopathology: New insights into clinical longitudinal data. PLoS ONE, 8:e60188.

- Chang, (2004) Chang, Y. (2004). Bootstrap unit root tests in panels with cross-sectional dependency. Journal of Econometrics, 120:263–293.

- Davis et al., (2015) Davis, R. A., Zang, P., and Zheng, T. (2015). Sparse vector autoregressive modeling. Journal of Computational and Graphical Statistics, 25:1077–1096.

- Dowell and Pinson, (2016) Dowell, J. and Pinson, P. (2016). Very-short-term probabilistic wind power forecasts by sparse vector autoregression. IEEE Transactions on Smart Grid, 7:763–770.

- Fang et al., (1990) Fang, K.-T., Kotz, S., and Ng, K. W. (1990). Symmetric Multivariate and Related Distributions. Chapman and Hall/CRC, New York.

- Faradonbeh et al., (2018) Faradonbeh, M. K. S., Tewari, A., and Michailidis, G. (2018). Finite time identification in unstable linear systems. Automatica, 96:342–353.

- Gorrostieta et al., (2012) Gorrostieta, C., Ombao, H., Bédard, P., and Sanes, J. N. (2012). Investigating brain connectivity using mixed effects vector autoregressive models. NeuroImage, 59:3347–3355.

- Guo et al., (2016) Guo, S., Wang, Y., and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika, 103:889–903.

- Hamilton, (1994) Hamilton, J. D. (1994). Time Series Analysis. Princeton University Press, Princeton.

- (13) Han, F., Lu, H., and Liu, H. (2015a). A direct estimation of high dimensional stationary vector autoregressions. Journal of Machine Learning Research, 16:3115–3150.

- (14) Han, F., Xu, S., and Liu, H. (2015b). Rate-optimal estimation of a high-dimensional semiparametric time series model. Preprint.

- Horn and Johnson, (1985) Horn, R. A. and Johnson, C. R. (1985). Matrix Analysis. Cambridge University Press, New York.

- Kano, (1994) Kano, Y. (1994). Consistency property of elliptical probability density functions. Journal of Multivariate Analysis, 51:139–147.

- Kotz and Nadarajah, (2004) Kotz, S. and Nadarajah, S. (2004). Multivariate t-Distributions and Their Applications. Cambridge University Press.

- Lütkepohl, (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer-Verlag Berlin Heidelberg.

- Maj-Kańska et al., (2015) Maj-Kańska, A., Pokarowski, P., and Prochenka, A. (2015). Delete or merge regressors for linear model selection. Electronic Journal of Statistics, 9:1749–1778.

- Mendelson, (2014) Mendelson, S. (2014). Learning without concentration. In JMLR: Workshop and Conference Proceedings, volume 35, pages 1–15.

- Negahban and Wainwright, (2011) Negahban, S. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, 39:1069–1097.

- Recht, (2018) Recht, B. (2018). A tour of reinforcement learning: The view from continuous control. arXiv:1806.09460.

- Reinsel, (1993) Reinsel, G. C. (1993). Elements of Multivariate Time Series Analysis. Springer-Verlag, New York.

- Rudelson and Vershynin, (2015) Rudelson, M. and Vershynin, R. (2015). Small ball probabilities for linear images of high-dimensional distributions. International Mathematics Research Notices, 2015:9594–9617.

- Simchowitz et al., (2018) Simchowitz, M., Mania, H., Tu, S., Jordan, M., and Recht, B. (2018). Learning without mixing: Towards a sharp analysis of linear system identification. In Proceedings of Machine Learning Research, volume 75, pages 439–473. 31st Annual Conference on Learning Theory.

- Sims, (1980) Sims, C. A. (1980). Macroeconomics and reality. Econometrica, 48:1–48.

- Stock and Watson, (2001) Stock, J. H. and Watson, M. W. (2001). Vector autoregressions. Journal of Economic Perspectives, 15:101–115.

- Tsay, (2013) Tsay, R. S. (2013). Multivariate Time Series Analysis: With R and Financial Applications. John Wiley & Sons.

- Vershynin, (2012) Vershynin, R. (2012). Introduction to the nonasymptotic analysis of random matrices. In Eldar, Y. and Kutyniok, G., editors, Compressed Sensing: Theory and Applications, chapter 5, pages 210–268. Cambridge University Press.

- Vershynin, (2018) Vershynin, R. (2018). High-Dimensional Probability: An Introduction with Applications in Data Science. Cambridge University Press, Cambridge.

- Wilms et al., (2017) Wilms, I., Basu, S., Bien, J., and Matteson, D. S. (2017). Interpretable vector autoregressions with exogenous time series. In Symposium on Interpretable Machine Learning, 31st Conference on Neural Information Processing Systems (NIPS 2017).

- Wu and Xia, (2016) Wu, J. C. and Xia, F. D. (2016). Measuring the macroeconomic impact of monetary policy at the zero lower bound. Journal of Money, Credit and Banking, 48:253–291.

- Zhang et al., (2018) Zhang, B., Pan, G., and Gao, J. (2018). CLT for largest eigenvalues and unit root testing for high-dimensional nonstationary time series. The Annals of Statistics, 46:2186–2215.

- Zhou et al., (2018) Zhou, W.-X., Bose, K., Fan, J., and Liu, H. (2018). A new perspective on robust M-estimation: Finite sample theory and applications to dependence-adjusted multiple testing. The Annals of Statistics, 46:1904–1931.

- Zhu et al., (2017) Zhu, X., Pan, R., Li, G., Liu, Y., and Wang, H. (2017). Network vector autoregression. The Annals of Statistics, 45:1096–1123.

Supplementary Material: Finite Time Analysis of Vector Autoregressive Models under Linear Restrictions

S1 Proofs of Theorem 1 and Proposition 1

S1.1 Three Auxiliary Lemmas

The proofs of Theorem 1 and Proposition 1 rely on three auxiliary lemmas, Lemmas S1–S3. Lemma S1 contains key results on covering and discretization. Lemma S2 gives a poinwise lower bound of through aggregation of all the blocks of size using the Chernoff bound. Notice that the probability guarantee in Lemma S2 will degrade as increases, since the probability guarantee of the Chernoff bound will degrade as the number of blocks decreases. Lemma S3 is a multivariate concentration bound for dependent data, respectively. We state these lemmas first and relegate their proofs to S1.4.

The following notations will be used throughout our proofs: For any integer and matrix , let be the ellipsoidal vector norm associated to , i.e., the mapping from to . In addition, we denote the corresponding unit ball, or ellipsoid, by . For any set , we denote its cardinality, complement and volume by , and , respectively.

Lemma S1.

Suppose that and . Let be a -net of in the norm . Then, the following holds:

(i) If , then .

(ii) If is a minimal -net, then .

(iii) If , then for any , we have

Lemma S2.

Suppose that the process taking values in satisfies the -bmsb condition. Let . Then, for any , we have

Lemma S3.

Let be a filtration. Suppose that and are processes taking values in , and for each integer , is -measurable, is -measurable, and is mean-zero and -sub-Gaussian. Then, for any constants , we have

| (S1) |

S1.2 Proof of Theorem 1

Define the matrices

| (S2) |

where and . Since has full column rank, and are both positive definite matrices. Thus, .

Consider the singular value decomposition , where , , and . Let be the Moore-Penrose pseudoinverse of , i.e., , where the diagonal matrix is defined by taking the reciprocal of each nonzero diagonal entry of ; in particular, if . Then, we have . As a result,

Furthermore, since , it holds on the event that

| (S3) |

Note that (S1.2) exploits the self-cancellation effect inside the pseudoinverse : the bound would not be as sharp if , and were bounded separately.

Notice that condition (2.4) implies , so that

| (S5) |

As a result,

| (S6) |

In view of (S1.2) and (S6), to prove this theorem, it remains to show that is bounded below and is bounded above, with high probability. Specifically, we will prove that

| (S7) |

if condition (2.4) of the theorem holds, and

| (S8) |

if we choose

Note that , where each is a block in . Likewise, . By a change of variables and Lemma S2, we have

where we used (S5) again in the last inequality. This, together with (S9) and (S1.2), yields

as long as condition (2.4) of the theorem holds.

Proof of (S8): Recall that and . Thus, on the event , we have

where the second equality uses the fact that is nonsingular if . Then it follows from Lemma S1(iii) that, on the event , we have

where is a -net of in the norm . Therefore,

| (S11) | ||||

Similarly to (S1.2), we can show that

| (S12) |

Now it remains to derive a pointwise upper bound on the probability in (S11) for any fixed . Let be the th element of , and denote

Note that . Fixing , define , where , and denote

Then, we have . As a result,

and

Applying Lemma S3 to and , with and , we have

| (S13) |

Moreover, by a method similar to that for (S12), we can show that

| (S14) |

S1.3 Proof of Proposition 1

Define the matrices and as in (S2), and consider the singular value decomposition of as in the proof of Theorem 1. Note that

Since , it holds on the event that

Consequently, by a method similar to that for (S1.2), under Assumption 2, we can show that

for any . Moreover, similarly to (S6), we have

Then, along the same lines of the arguments for Theorem 1, we accomplish the proof of this proposition.

S1.4 Proofs of Lemmas S1–S3

The covering and discretization results in Lemma S1 are modified from Lemmas 4.1, D.1 and D.2 in Simchowitz et al., (2018). For clarity, we rewrite the proofs of Lemma S1(i)–(ii) to correct any typographical error in their proofs, and present our own proof of Lemma S1(iii). Lemma S2 establishes a pointwise lower bound on via the bmsb condition, which will be strengthened into a union bound in the proof of Theorem 1 via Lemma S1(i); see also Proposition 2.5 in the above paper. Finally, as a multivariate generalization of Lemma 4.2(b) in their paper, Lemma S3 gives a concentration bound on . Note that it is crucial to bound this self-normalized process as a whole, instead of bounding the numerator and the denominator separately; otherwise, the bound would degrade for slower-mixing processes.

Proof of Lemma S1.

Note that claim (i) will be used to cover in terms of and for deriving the union upper bound on in the proof of Theorem 1. The corresponding covering number is given in claim (ii), which is larger when is farther away from as measured by . Claim (iii) is a discretization result for .

To prove (i), it is equivalent to show that

| (S15) |

Since is a -net of in the norm , on the event , we have

where the second and last inequalities are due to and , respectively. As a result,

Therefore, , i.e., (S15) holds.

The proof of claim (ii) is basically the same as that in Simchowitz et al., (2018), except for some minor corrections. Note that is equal to the covering number of the shell of the ellipsoid in the Euclidean norm. Let be the unit ball in , and denote by the Minkowski sum. If is a minimal -net of in the norm , then it follows from a standard volumetric argument that

Taking yields the result in (ii).

Finally, we prove (iii). First note that since , we have

For a fixed , define by

To prove (iii), we will show that for any , there exist and such that

| (S16) |

Let

Then, as long as , and we have

Therefore, to prove (S16), it suffices to show that

| (S17) |

Note that

As a result,

| (S18) |

S2 Proofs of Lemmas 1–3

S2.1 Proof of Lemma 1

First note that for any and positive integer ,

where, by Assumption 4(ii), is independent of , and . Then, for any , we have

where , and can be written as a weighted sum of real-valued independent random variables,

with

Notice that , and are real-valued independent random variables. Moreover, by Assumption 4(iii), the density of each is bounded by almost everywhere. Applying Theorem 1.2 in Rudelson and Vershynin, (2015), it follows that the density of is bounded by almost everywhere. In addition, is independent of , and . Therefore,

| (S1) |

For any integer , by (S2.1) and the fact that for , we have

Choosing , we accomplish the proof of this lemma.

S2.2 Proof of Lemma 2

Since , we have

Then, with , it follows from the Markov inequality that

which completes the proof of this lemma. Note that the factor of in the definition of is a consequence of upper bounding by .

S2.3 Proof of Lemma 3

Recall that , where each is a block. For simplicity, denote with , where . To prove this lemma, it suffices to verify the following two results:

| (S2) |

where , and

| (S3) |

We first prove (S2). Note that and . Then, since , we have

As a result,

| (S4) |

Moreover, for , we have

which implies

| (S5) |

Next we prove (S3). Let be a minimal -net of the sphere in the Euclidean norm. It follows from a standard volumetric argument that . Moreover, by Lemma 5.4 in Vershynin, (2012), we have

| (S6) |

Furthermore, since are normal, follows the multivariate normal distribution with mean zero and covariance matrix . Then, for any , we have

where

and hence there exists such that . As a result, it follows from the Hanson-Wright inequality (Vershynin,, 2018) that, for every ,

| (S7) |

where is a universal constant. In view of (S6) and (S2.3), we have

as long as

| (S8) |

where .

To prove (S3), it now remains to choose such that (S8) holds. Note that

| (S9) |

Moreover, since

in light of (S9), we have

| (S10) |

Replacing and in (S8) by their upper bounds in (S9) and (S10), respectively, it follows that (S3) holds if we choose as in (3.6) in the main paper. The proof of this lemma is complete.

S3 Proofs of Equation (3.10) and Proposition 2

S3.1 Proof of Equation (3.10)

The proof of Equation (3.10) relies on the following lemma:

Lemma S4.

Let and be symmetric positive definite matrices such that . For any , it holds .

Proof of Lemma S4.

Now we prove Equation (3.10). First note that

| (S1) |

If , it is easy to see that

| (S2) |

where .

S3.2 Proof of Proposition 2

Proposition 2 is a direct consequence of Equations (3.9) and (3.10) in the main paper and the upper bounds of and in Lemmas S5 and S6 below. Note that the proofs of Lemmas S5 and S6 rely crucially on the intermediate results on upper bounds of and as given in Lemmas S7 and S8 below, respectively. The proofs of Lemmas S5–S8 are collected in S3.3.

As in the main paper, let the Jordan decomposition of be , where has blocks with sizes , and both and are complex matrices. Let and denote the condition number of by , where is the conjugate transpose of .

S3.3 Proofs of Lemmas S5–S8

Proof of Lemma S6.

Proof of Lemma S7.

For , denote by the th block of with size and diagonal entries . Note that the th block of the block diagonal matrix is . Moreover, the th entry of is

where . Then the th diagonal entry of is

| (S5) |

By Assumption 5, for . Thus

Note that monotonically increases to as , which implies that is uniformly bounded by a universal constant . Moreover, for and , in (S5) is uniformly bounded above by . As a result, for any and , we have

Notice that the diagonal entries of are . Therefore

| (S6) |

Combining (S4) and (S6), we obtain the upper bound of under Assumption 5 as stated in this lemma.

Next we verify the conclusion under Assumption 6. Since , we have . Note that . Thus, for any , there exists a positive integer such that for all . Taking , we have . As a result,

where the last upper bound is a fixed constant. The proof of this lemma is complete. ∎

Proof of Lemma S8.

The result under Assumption 5 is straightforward, since

However, showing that is bounded by a fixed constant proportional to under Assumption 6′ requires a much more delicate argument. This is largely because is affected by not only the growing diagonal blocks but also the growing off-diagonal blocks; note that for any , the th block of is

| (S7) |

To overcome this difficulty, under Assumption 6′, we consider the following ‘coupled’ stable process with independent and identically distributed innovations such that and , but assuming that starts from :

| (S8) |

Unlike in the main paper, this process is weakly stationary. Indeed, for any , it holds and

| (S9) |

where . Analogously to , let be the symmetric matrix with its th block being for . In other words, is the covariance matrix of the vector . Note that in contrast to , the blocks of do not grow in the diagonal direction, in the sense that all ’s share the same factor matrix . By Basu and Michailidis, (2015), for the weakly stationary process in (S8), it holds

| (S10) |

where is defined as in Assumption 6′.

In view of (S10) and the triangle inequality

| (S11) |

it remains to prove that . To this end, for any , consider the difference between the th blocks of and :

| (S12) |

Note that under Assumption 6′, , where . This, together with (S3.3), implies that for any ,

Consequently, for any with , we have

Thus,

| (S13) |

Combining (S10), (S11) and (S13), the proof of this lemma is complete. ∎

S4 Proof of Theorem 3

We will prove claim (i) of Theorem 3 only, as claims (ii) and (iii) can be proved by a method similar to that for (i).

First, by an argument similar to that in Lütkepohl, (2005, p. 199), we can show that

In addition, note that

As a result,

| (S1) |

Now we prove the rate in (S.1) under condition (A.1). By the existence condition of in (3.13), we can choose

| (S2) |

where is a universal constant. Then, (A.1) can be written as

| (S3) |

where . Since

by Theorem 2(i) and (S1), to prove the rate for in (S.1), it suffices to show that there exists a universal constant such that

| (S4) |

Moreover, by (S3), we can show that (S4) is satisfied if

| (S5) |

Note that the function monotonically deceases to as . Thus, by choosing such that , i.e., , we accomplish the proof of (S.1).

Next we prove the rate in (F.1) when the opposite of (A.1) is true, i.e., when

| (S6) |

Again, we choose in (S2), and then (S6) becomes

where is defined as in (S3). Thus,

| (S7) |

In view of Theorem 2(i), (S1), (S2) and (S7), to prove the rate for in (F.1), we only need to show that there exists a universal constant such that

| (S8) |

By the choice of in (S2), we have . Hence, there exists such that . Moreover, notice that the function is monotonically increasing in . As a result, by choosing , we complete the proof of (F.1).

S5 Proofs of Theorem 4 and Corollary 1

S5.1 Two Auxiliary Lemmas

The proof of Theorem 4 is based upon Lemmas S9 and S10 below. Denote by the Kullback-Leibler divergence between two probability measures and on the same measurable space.

Lemma S9.

Fix , and . Suppose that is a finite subset of such that . If

| (S1) |

where the infimum is taken over all estimators of which are -measurable, then

Proof of Lemma S9.

For any -measurable estimator , let for . Since is a -packing of , the events ’s with are pairwise disjoint in . By (S1), there exists a such that , i.e., . Applying Birgé’s inequality (Boucheron et al.,, 2013, Theorem 4.21) and an argument similar to that for Lemma F.1 in Simchowitz et al., (2018), we can readily prove that for any ,

Taking the infimum over , we accomplish the proof of this lemma. ∎

Lemma S10.

For the linearly restricted vector autoregressive model, under the conditions of Theorem 4, for any , we have

where .

Proof of Lemma S10.

Without loss of generality, we assume that , so that . Let be the th entry of , and denote . For any , under we have , where and . Hence, the log-likelihood of under is

As a result,

where the last equality is because of . The proof is complete. ∎

S5.2 Proof of Theorem 4

Without loss of generality, we assume that , so that . Define the ellipsoid , where denotes the Euclidean ball in with center zero and radius . Since , we have .

For any , let be a maximal -packing of in , and define . Then, is a -packing of in the norm . As a result, for all . In addition, by a standard volumetric argument, we have . By Lemma S9, for any , this theorem holds if

| (S2) |

S5.3 Proof of Corollary 1

Under the conditions of Theorem 4, we have

where is fixed. It then suffices to derive lower bounds of for .

First, suppose that . Then we have , and therefore

| (S4) |

Next, suppose that for a fixed . Then

Since monotonically increases to as , there exists a constant free of such that is uniformly bounded above by , i.e.,

| (S5) |

Moreover, for any , we have

| (S6) |

References

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43:1535–1567.

- Boucheron et al., (2013) Boucheron, S., Lugosi, G., and Massart, P. (2013). Concentration inequalities: A nonasymptotic theory of independence. Oxford University Press, Oxford.

- Horn and Johnson, (1985) Horn, R. A. and Johnson, C. R. (1985). Matrix Analysis. Cambridge University Press, New York.

- Lütkepohl, (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer-Verlag Berlin Heidelberg.

- Rudelson and Vershynin, (2015) Rudelson, M. and Vershynin, R. (2015). Small ball probabilities for linear images of high-dimensional distributions. International Mathematics Research Notices, 2015:9594–9617.

- Simchowitz et al., (2018) Simchowitz, M., Mania, H., Tu, S., Jordan, M., and Recht, B. (2018). Learning without mixing: Towards a sharp analysis of linear system identification. In Proceedings of Machine Learning Research, volume 75, pages 439–473. 31st Annual Conference on Learning Theory.

- Vershynin, (2012) Vershynin, R. (2012). Introduction to the nonasymptotic analysis of random matrices. In Eldar, Y. and Kutyniok, G., editors, Compressed Sensing: Theory and Applications, chapter 5, pages 210–268. Cambridge University Press.

- Vershynin, (2018) Vershynin, R. (2018). High-Dimensional Probability: An Introduction with Applications in Data Science. Cambridge University Press, Cambridge.