The Poisson random effect model for experience ratemaking: limitations and alternative solutions

Abstract

Poisson random effect models with a shared random effect have been widely used in actuarial science for analyzing the number of claims. In particular, the random effect is a key factor in a posteriori risk classification. However, the necessity of the random effect may not be properly assessed due to the dual role of the random effect; it affects both the marginal distribution of the number of claims and the dependence among the numbers of claims obtained from an individual over time. In line with such observations, we explain that one should be careful in using the score test for the nullity of the variance of the shared random effect, as a sufficient condition for the existence of the posteriori risk classification. To safely perform the a posteriori risk classification, we propose considering an alternative random effect model based on the negative binomial distribution, and show that safer conclusions about the a posteriori risk classification can be made based on it. We also derive the score test as a sufficient condition for the existence of the a posteriori risk classification based on the proposed model.

keywords:

Poisson random-effect model , Claim frequency , Dependence , Experience ratemaking , Negative binomial distribution JEL Classification: C3001 Introduction

Ratemaking is a key process in pricing risks in actuarial science. Risk classification enables ratemaking by grouping the insured into several homogeneous groups in terms of degree of risks. Following the terminology in Pinquet, (1997), Denuit et al., (2007) and Antonio and Valdez, (2012), the risk classification procedure is divided into a priori and a posteriori risk classifications. A priori risk classification uses the measured information of the policyholder, such as gender and age, which are available at the moment of contract. A standard statistical tool for a priori risk classification is the generalized linear model (GLM). However, hidden characteristics such as driving skill and knowledge of road conditions have an impact on risks of the policyholder; therefore, these become sources of heterogeneity in a portfolio. To reflect these unobserved risk characteristics of policyholders, random effects are added to GLMs. A standard tool for a posteriori risk classification is the generalized linear mixed model (GLMM). A book-length review for these models is given in De Jong and Heller, (2008) and Frees, (2010). In this study, our concern is the analysis of the number of claims applicable to automobile insurance. Specifically, we focus on a Poisson random effect model because it has been widely used in actuarial science as a claim frequency model for a posteriori risk classification. A good review of actuarial modeling of claim counts based on the Poisson or its variations distribution are given in Yip and Yau, (2005), Denuit et al., (2007), and Boucher and Denuit, (2008).

Pinquet, (1997) proposed an analysis pipeline for the number of claims based on a Poisson random effect model, where the random effect denotes the heterogeneity component for each policyholder. The first step is to perform a score test for the necessity of the random effect with a fitted Poisson GLM, that is, whether the random effect variance is zero or not. When the nullity of the random effect variance is rejected, Pinquet, (1997) performed a posteriori ratemaking by estimating the random effect. This procedure is simple to implement, and intuitively appealing. However, in this study, we emphasize that this approach should be used carefully because it does not contemplate the dual role of the random effect in the Poisson model. Introducing the random effect changes both the marginal distribution for the number of claims and the dependence among the numbers of claims obtained from an individual over time. Denuit et al., (2007) and Murray and Lucas, (2013) also highlight this, stating that the random effect induces both overdispersion and serial dependence. This implies that the score test detects not only changes in the marginal distribution, but also serial dependence. In other words, the testing procedure proposed in Pinquet, (1997) can reject the null hypothesis even when the data show pure overdispersion without serial dependence. This invokes an important problem in experience ratemaking because falsely detected serial dependence may spoil the fairness of the existing rating system. In this study, we first prove that the serial dependence is falsely detected with probability one when the score test is applied to independent, but overdispersed data. This implies that one should be careful in using the score test as a sufficient condition for the existence of the bonus-malus (BM) system. To mitigate this danger, we consider an alternative random effect model based on the negative binomial distribution. In addition, based on the proposed model, we develop a new score test for checking the necessity of the heterogeneity component for each policyholder.

The remainder of this paper is organized as follows. Section 2 reviews how experience ratemaking is performed with a Poisson random effect model. Section 3 explains possible dangers when the Poisson random effect model is used and asymptotic results are provided. We suggest an alternative random effect model to overcome the limitation in Section 4, and provide a new score test for the necessity of the heterogeneity component for each policyholder, followed by a numerical study in Section 5. Section 6 explains how a posteriori ratemaking is performed with with the proposed model and compares the performance of the a posteriori risk classification with the Poisson random effect model, followed by concluding remarks in Section 7.

2 Review of experience ratemaking for claim frequency

Let be a gamma distribution with mean and variance , where and are called shape and rate parameters, respectively. We also denote as a negative binomial distribution with mean and variance , where is called a dispersion parameter. Denote as log-normal distribution with mean and variance .

Following Pinquet, (1997) and Pinquet, (1998), we consider

| (1) |

where

| (2) |

and is the number of claims reported by the -th policyholder in period .

Here, is a covariate vector and denotes the random effect for the -th policyholder to explain the heterogeneity component. The random effect is assumed to follow where and , which leads to a negative binomial distribution for the marginal distribution of . This random intercept model has been widely used in actuarial science (Boucher and Denuit,, 2006). However, the gamma distribution for is not compulsory. Other distributions such as inverse Gaussian or log-normal distributions can be used. For the details, see Boucher and Denuit, (2006).

Pinquet, (1997) derived a sufficient condition for the existence of a BM system from the random effect model (1) without any parametric assumption for and showed that checking the condition is equivalent to performing a score test for . The analytic form for the score statistic and its asymptotic distribution is given as

| (3) |

where and denotes the maximum likelihood estimate for under . The null hypothesis is rejected when is greater than or equal to the quantile of . When the rejection occurs, Pinquet, (1997) used the following BM coefficient for experience ratemaking:

where was assumed to follow .

3 Problem of BM system based on the Poisson random effect model

Although the score statistic (3) is useful in investigating , caution is necessary when it involves the condition for the existence of a BM system, as Theorem 1 shows. We define related models before presenting the theorem.

Model 1 (No Random Effect Model).

Model 2 (Shared Random Effect Model).

For and , consider the following random effect model

where is defined in (2) and are i.i.d with mean 1 and variance .

Under Model 2, we have

| (4) |

and

| (5) |

Frequencies from the same policyholder are correlated through the shared random effect . Here, we note that the condition for the existence of a BM system is

| (6) |

and the condition for overdispersion is

| (7) |

Comparing Model 1 and 2, under the assumption , both the conditions in (6) and (7) are equivalent with . Hence, as shown in Pinquet, (1997), the score statistic (3) for testing overdispersion determines the condition for the existence of a BM system under Model 2. However, considering the following model, it is clear that the two conditions in (6) and (7) are not always equivalent.

Alternative Model 1 (Saturated Random Effect Model).

For and , consider the following random effect model

where is defined in (2) and are i.i.d with mean 1 and variance .

To distinguish from , we call and as shared random effect and saturated random effect, respectively. Under the Alternative Model 1, we have

and

| (8) |

Hence, the Alternative Model 1 does not require a BM system because there is no correlation between the frequencies from the same policyholder. However, as will be proved later, the score statistic (3) rejects the null hypothesis with probability one, as goes to infinity under the Alternative Model 1, which may result in erroneous a posteriori experience ratemaking. Alternative Model 1 highlights that the necessity of the random effect does not always support the use of the BM system.

3.1 Asymptotic result of the score statistic

An asymptotic property of the score statistic (3) is proved below. For simplicity, we assume that is bounded.

Theorem 1.

Proof.

Since the Poisson regression model (1) and Alternative Model 1 have the same marginal mean model, the Poisson regression model (1) provides a -consistent estimator for under Alternative Model 1. Therefore, we have . By the Cauchy-Schwartz inequality, also converges to a positive constant. Then, the score statistic becomes

Because ,

Therefore, the test statistic goes to infinity with probability one, as goes to infinity. ∎

In conclusion, although the test statistic proposed in Pinquet, (1997) supports the existence of the non-degenerate random effect, one needs to distinguish between Model 2 and Alternative Model 1 to determine the dependence between and . As the test statistic (3) rejects even for independent data showing overdispersion, caution is necessary in using the score test as a sufficient condition for the existence of the BM system.

3.2 Simulation Result

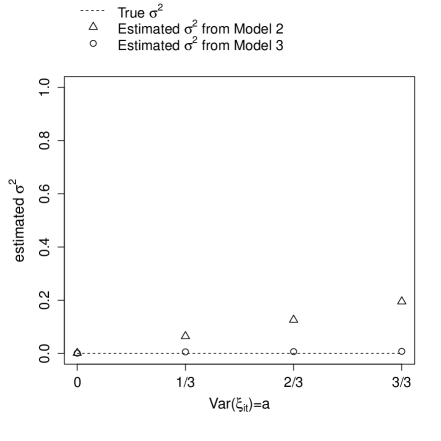

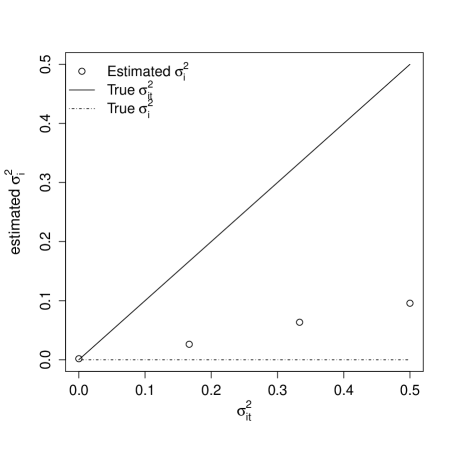

In connection with Theorem 1, the following simulation study shows that even for independent , Model 2 shows a considerable amount of variance for the shared random effect , which results in a false correlation between frequencies from the same policyholder. Assume that ( and ) are obtained from Alternative Model 1 with

| (9) |

where

| (10) |

Here, the variances of the saturate random effect are set as

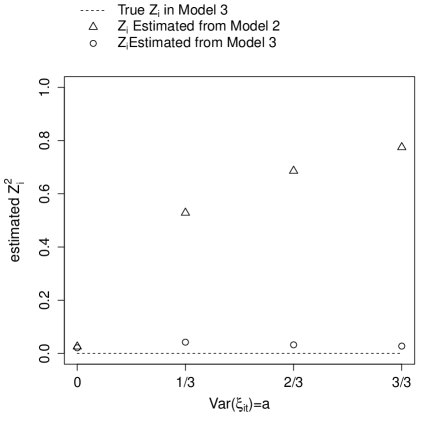

Detailed results, based on repetitions, are in Figure 1 and Table 1 when Model 2 is fitted to this data. Estimate for increases as the true value for increases.

4 Alternative model to overcome the limitation of the Poisson random effect model

The limitation of Model 2 results from using the random effect for not only explaining the correlation among individuals but also for changing the marginal distribution. To separate these two roles of , we need to incorporate the saturated random effect in Model 2 to solely capture overdispersion. Therefore, the proposed random effect model for the number of claims is

| (11) |

where is defined in (2) and . However, this model may not be preferred in terms of computation because incorporating the saturated random effect requires inversion and multiplications of high dimensional matrices if the number of observations is large. To make the model (11) practically useful, we employ a parametric assumption for . Our convenient choice is because this choice allows us to avoid such large matrix computations by analytically integrating out of the likelihood function.

Model 3.

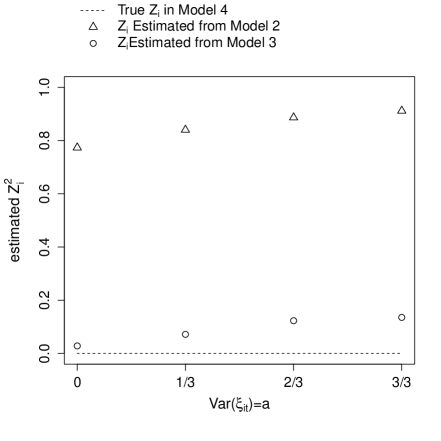

Model 2 is a special case of Model 3 with . In the numerical study in Section 3.2, we observe that Model 2 shows considerable shared random effect when fitted to the independent data showing overdispersion. On the other hand, because Model 3 already takes care of overdispersion, we expect that Model 3 does not have this problem. The following is a detailed simulation study to assess the performance of Model 2 and Model 3.

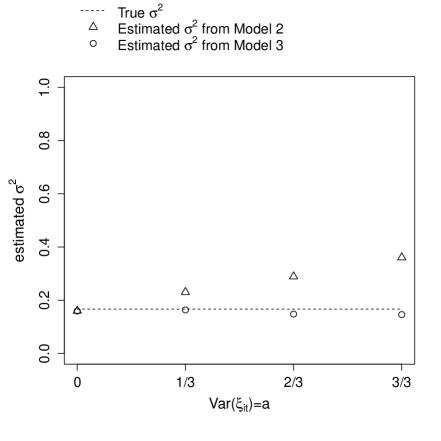

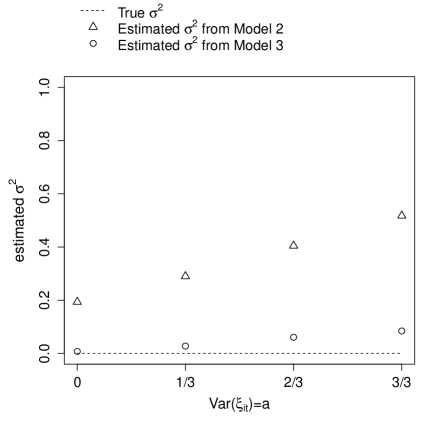

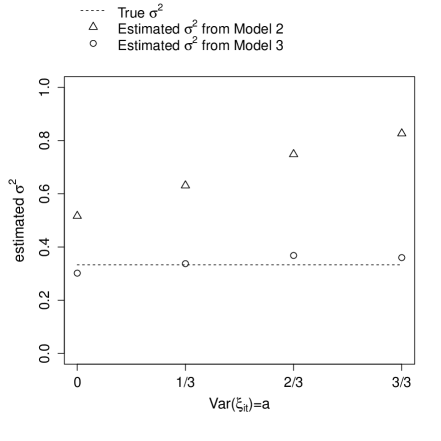

4.1 Simulation Study I

We compare the performance of Model 2 and Model 3 to estimate the variance of under various simulation settings. First, is generated from Model 3 with (9) and (10). For the random effects, we assume that

| (13) |

and

| (14) |

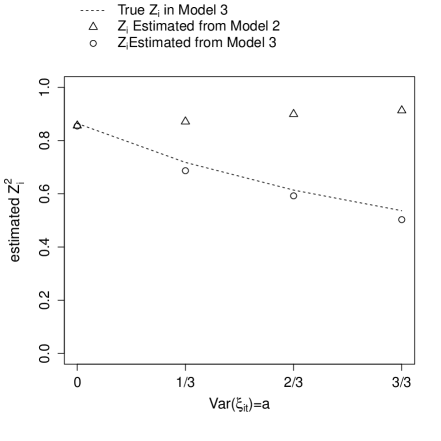

Here, and represent and , respectively. In total, we have 16 combinations of . For each combination, the following claim frequencies

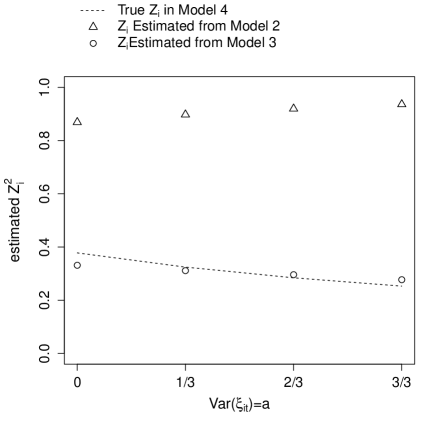

are generated, and Model 2 and Model 3 are fitted to the simulated data. Estimation results, based on repetitions, for the parameter in each setting are shown in Figure 3. As expected, Model 2 overestimates , and the bias becomes larger as becomes larger, whereas Model 3 shows an unbiased result for estimating , regardless of the size of .

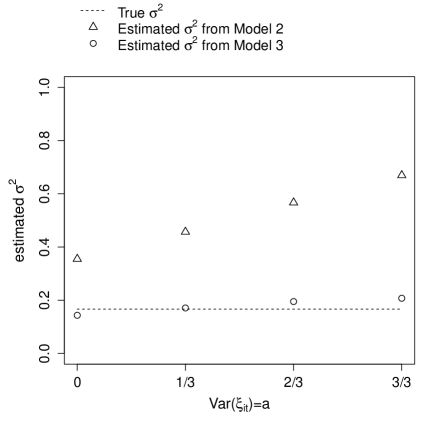

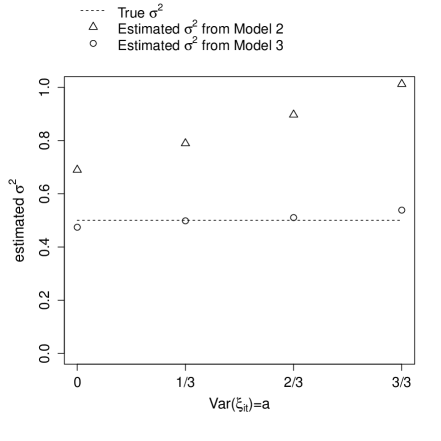

4.2 Simulation Study II

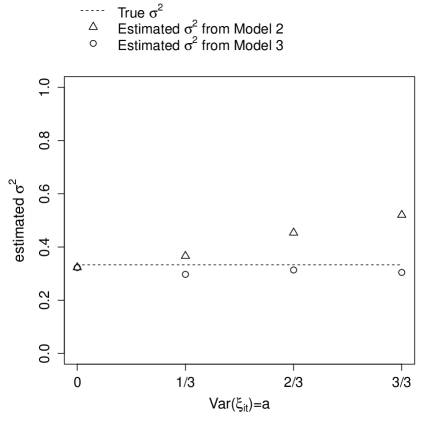

Although the NB distribution is a flexible model that can explain extra-Poisson variation, it does not capture all types of extra-Poisson variation. Therefore, our concern is the performance of Model 3 when there is overdispersion effect beyond the negative binomial distribution. Specifically, we consider the following random effect model, which has an additional independent random effect on Model 3:

Alternative Model 2.

| (15) |

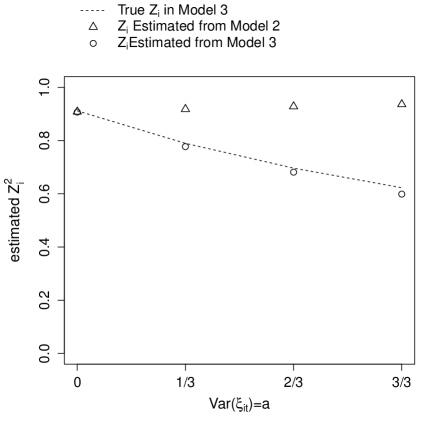

We generate the claim frequencies

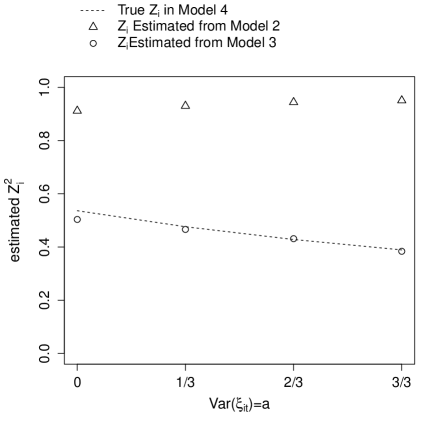

from Alternative Model 2. Then, Model 2 and Model 3 are fitted to this simulated data for comparison. The parameter settings for fixed and random effects are the same as in Section 4.1. For each of the simulation settings, estimation results, based on repetitions, for the parameter are in Figure 4. As expected, Model 2 shows severe upward bias, as the variance of becomes larger, whereas Model 3 shows much smaller bias; however, the amount of bias increases as the size of increases. From this observation, the dispersion parameter in the negative binomial distribution is effective in reducing the bias in the estimate of . In fact, we can obtain an unbiased estimate for by fitting Alternative Model 2 directly; however, as its use is often prohibited owing to heavy computational burden, we do not consider this model.

5 Score test for checking the existence of a BM system

In this section, we derive a sufficient condition for the existence of a BM system and perform a numerical study to check the performance of the proposed score test. First, similar to Pinquet, (1997), we propose using the score test for under Model 3. The following theorem gives an analytic form of the score statistic and its asymptotic distribution.

Theorem 2.

Assume that

is bounded. Let and and denote the maximum likelihood estimates from Model 3 under . Under , the score statistic and its asymptotic distribution is given as

where

and the analytic forms on , and are given in the proof.

Proof.

Let denote the log negative binomial likelihood function, given the random effect. Following Chesher, (1984) and Liang, (1987), the score function for under is

By taking into account the uncertainty of and in the asymptotic variance of , the following quantities become necessary:

Here, and is a block diagonal matrix expressed as

Where the -th element of is . The -th term of is equal to

All the expectations are evaluated under , and and are replaced with their MLEs and . The details for the above expectations are given in Lemma 1 in the Appendix. Based on Chesher, (1984)’s result, the score statistic follows asymptotically .

∎

As this score statistic requires only MLEs under , it is sufficient for fitting an ordinary NB regression model to perform the test.

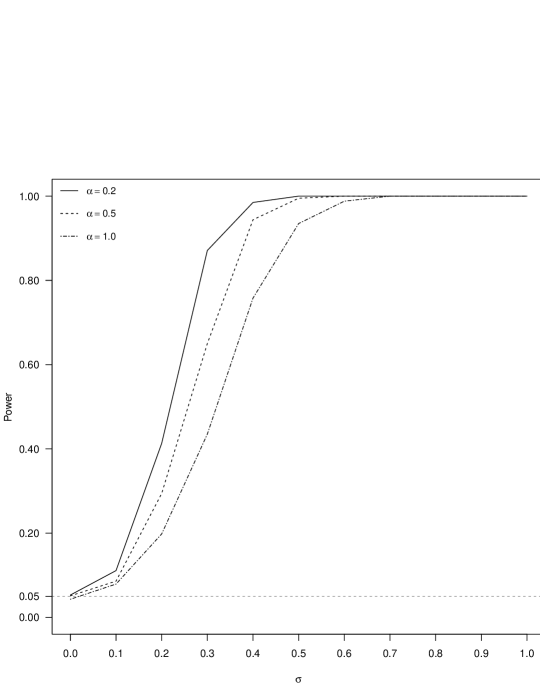

5.1 Simulation Study

We perform a numerical study to check the performance of the score test in terms of empirical type I error and power under Model 3. We generate

from with and . Therefore, and . For the variance of random effect , we consider . The are generated from , and and . For the parameter in the negative binomial distribution, and are considered. We report the proportion of rejecting based on 1000 replications. At , this proportion corresponds to the type I error, and at nonzero , it denotes the empirical power. The results are plotted in Figure 2. As similar results are observed under other settings, we omit them for convenience. In general, the proposed score test controls the type I error well at its nominal Level of and shows that its power increases with .

6 Experience ratemaking with Bühlmann Method

For a fair valuation of premium, insurers are interested in the following predictive distribution:

and especially, in the mean of predictive distribution

| (18) |

While the exact estimation of (18) is possible in some special cases, it is a common practice in insurance to use the Bühlmann method for estimating (18).

Define

Then, the Bühlmann factor and Bühlmann prediction of the -th individual are calculated as

and

respectively. For the details of the Bühlmann method, we refer to Bühlmann and Gisler, (2006). The performance of the Bühlmann prediction is determined by the accurate estimation of the Bühlmann factor. The following propositions provide the closed form expression of , , and in Model 2, Model 3 and Alternative Model 2, respectively.

Proposition 1.

Proposition 2.

Proposition 3.

Assume that are generated from Model 3. If Model 2 is fitted to this, as shown in Proposition 1, will be overestimated due to the overestimation of . Knowing that Bühlmann premium is the linear estimator that minimizes the mean squared error(MSE), the bias in the Bühlmann factor leads to increase in the mean squared error. In the following simulation studies, we compare the MSE of Bühlmann estimators from Model 2 and Model 3 under various settings described in Section 4.1 and 4.2.

6.1 Simulation Study I

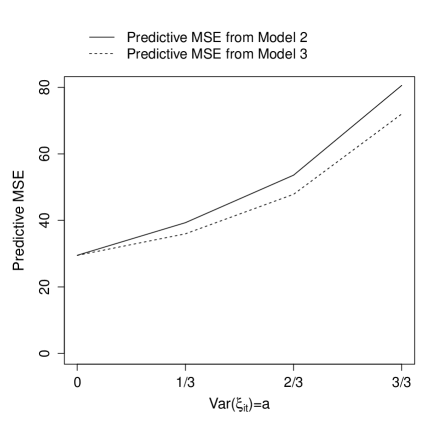

Under the same simulation setting in Section 4.1, we compare the performance of the two Bühlmann factors using Proposition 1 and 2. The numerical result is summarized in Figure 5. For comparison, the Bühlmann factor calculated in Proposition 2 with the true parameter values is also plotted as the dotted line in each setting. Model 2 overestimates the Bühlmann factor in every setting except the null saturated random effect case, that is, , whereas Model 3 estimates the Bühlmann factor well. We also calculate the predictive mean square error, which is defined as

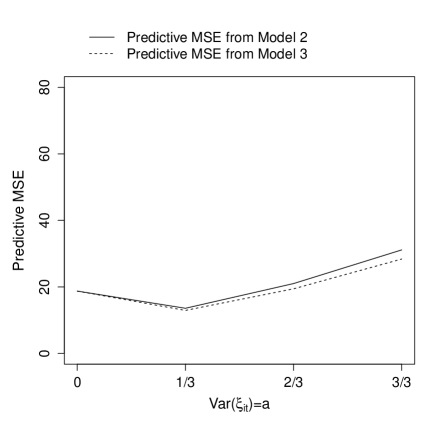

The numerical result is presented in Figure 7. In each setting, the predictive MSE of Model 3 is smaller than that of Model 2, and their difference becomes larger as increases.

6.2 Simulation Study II

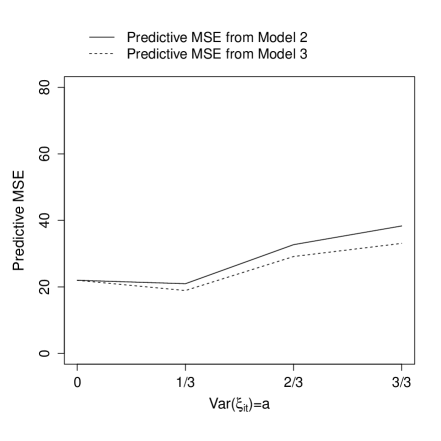

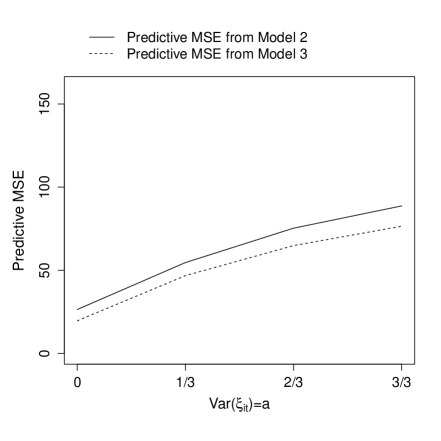

Under the same simulation setting in Section 4.2, we compare the performance of the two Bühlmann factors using Proposition 1 and 2. The numerical result is summarized in Figure 6. For comparison, the Bühlmann factor calculated in Proposition 3 with the true parameter values is also plotted as the dotted line in each setting. The bias of the Bühlmann factor calculated under Model 2 becomes larger than that of simulation study I, whereas Model 3 shows negligible bias of the Bühlmann factor. Figure 8 shows the predictive MSE. In each setting, the predictive MSE of Model 3 is smaller than that of Model 2, and their difference becomes larger as increases.

7 Discussion

Poisson random effect models with only a shared random effect can have a serious weakness, as a claim frequency model for a posteriori risk classification. In particular, one should be careful in using the score test by Pinquet, (1997) as a sufficient condition for the existence of the BM system. To prevent misleading experience ratemaking, it is necessary to incorporate shared and saturated random effects together in the Poisson random effect model. However, using the saturated random effect is often prohibited because of heavy computational problems for large sample sizes. Therefore, we argue that a random effect model based on NB distribution can be used to resolve the computation problem and deal with both shared and saturated random effects, demonstrating that it is possible to make safer conclusions about experience ratemaking based on it. However, we do not claim that the NB model is a flawless claim frequency model. Extending the explanation for the weakness of the Poisson random effect model with only a shared random effect, the proposed NB random effect model may have a similar weakness if the true model is an NB model with both shared and saturated random effects, although the current numerical study shows that the proposed model has substantial robustness. A systematic study of the robustness of the proposed NB random effect model will be an interesting future research topic.

Acknowledgements

Woojoo Lee was supported by the Basic Science Research Program through the National Research Foundation of Korea (NRF) funded by the Ministry of Education (NRF-2016R1D1A1B03936100). Jae Youn Ahn was supported by a National Research Foundation of Korea (NRF) grant funded by the Korean Government (NRF-2017R1D1A1B03032318).

References

- Antonio and Valdez, (2012) Antonio, K. and Valdez, E. A. (2012). Statistical concepts of a priori and a posteriori risk classification in insurance. AStA Advances in Statistical Analysis, 96(2):187–224.

- Boucher and Denuit, (2006) Boucher, J.-P. and Denuit, M. (2006). Fixed versus random effects in poisson regression models for claim counts: A case study with motor insurance. Astin Bulletin, 36(01):285–301.

- Boucher and Denuit, (2008) Boucher, J.-P. and Denuit, M. (2008). Credibility premiums for the zero-inflated poisson model and new hunger for bonus interpretation. Insurance: Mathematics and Economics, 42(2):727–735.

- Bühlmann and Gisler, (2006) Bühlmann, H. and Gisler, A. (2006). A course in credibility theory and its applications. Springer Science & Business Media.

- Chesher, (1984) Chesher, A. (1984). Testing for neglected heterogeneity. Econometrica, 52:865–872.

- De Jong and Heller, (2008) De Jong, P. and Heller, G. Z. (2008). Generalized linear models for insurance data. Cambridge University Press.

- Denuit et al., (2007) Denuit, M., Maréchal, X., Pitrebois, S., and Walhin, J.-F. (2007). Actuarial modelling of claim counts: Risk classification, credibility and bonus-malus systems. John Wiley & Sons.

- Frees, (2010) Frees, E. W. (2010). Regression modeling with actuarial and financial applications. Cambridge University Press.

- Lawless, (1987) Lawless, J. F. (1987). Negative binomial and mixed poisson regression. The Canadian Journal of Statistics, 15:209–225.

- Liang, (1987) Liang, K. (1987). A locally most powerful test for homogeneity with many strata. Biometrika, 74:259–264.

- Murray and Lucas, (2013) Murray, Jared S, D. D. B. C. L. and Lucas, J. E. (2013). Bayesian gaussian copula factor models for mixed data. Journal of the American Statistical Association, 108(502):656–665.

- Pinquet, (1997) Pinquet, J. (1997). Allowance for cost of claims in bonus-malus systems. Astin Bulletin, 27(01):33–57.

- Pinquet, (1998) Pinquet, J. (1998). Designing optimal bonus-malus systems from different types of claims. Astin Bulletin, 28(02):205–220.

- Yip and Yau, (2005) Yip, K. C. and Yau, K. K. (2005). On modeling claim frequency data in general insurance with extra zeros. Insurance: Mathematics and Economics, 36(2):153–163.

Appendix A Auxiliary result from Theorem 2

Proof.

For , the following basic results are repeatedly used:

and

From the first equality, we have

The second and third equalities are from

and

respectively. The fourth equation is from

Finally, following Lawless, (1987), we have the last equality as follows

∎

Appendix B Tables for the Simulation Results