A Splitting Strategy for the Calibration of Jump-Diffusion Models

Abstract

We present a detailed analysis and implementation of a splitting strategy to identify simultaneously the local-volatility surface and the jump-size distribution from quoted European prices. The underlying model consists of a jump-diffusion driven asset with time and price dependent volatility. Our approach uses a forward Dupire-type partial-integro-differential equations for the option prices to produce a parameter-to-solution map. The ill-posed inverse problem for such map is then solved by means of a Tikhonov-type convex regularization. The proofs of convergence and stability of the algorithm are provided together with numerical examples that substantiate the robustness of the method both for synthetic and real data.

keywords: Jump-Diffusion Simulation, Partial Integro-Differential Equations, Finite Difference Schemes, Inverse Problems, Tikhonov-type regularization.

1 Introduction

Model selection and calibration is still one of the crucial problems in derivative trading and hedging. From a mathematical view-point it should be treated as an ill-posed inverse problem by suitable regularization as in the work of Engl et al. (1996) and Scherzer et al. (2008). The subject is deeply connected to nonparametric statistics as described by Somersalo and Kapio (2004). The problem of model selection and calibration has thus attracted the attention of number of authors as can be seen in the book of Cont and Tankov (2003) and references therein.

Amongst the most successful nonparametric approaches, the local volatility model of Dupire (1994) has become one of the market’s standards. It consists in assuming that the underlying price satisfies a stochastic dynamics of the form

where is the Wiener process under the risk-neutral measure and is the so-called local volatility. Besides its intrinsic elegance and simplicity, Dupire’s model success is due to at least two factors: Firstly, the existence of a forward partial differential equation (PDE) satisfied by the price of call (or put) options when considered as functions of the strike price and the time to expiration . Secondly, to the importance of having a backwards pricing PDE to compute other (perhaps exotic) derivatives.

Yet, one of the main shortcomings of local volatility models is the fact that such models are still diffusive ones. Thus, well-known stylized facts such as fat tails and jumps in the log-returns become awkward to fit and justify (Cont and Tankov (2003)).

The present article is concerned with the calibration of jump-diffusion models with local volatility. We make use of a fairly recent contribution to the literature, namely the existence of a forward equation of Dupire’s type for such models present in Bentata and Cont (2015). The availability of a forward equation, allows us, for each fixed time and underlying price, to look at the option prices as a function of the time to expiration and the strike price. Furthermore, by considering collected data from past underlying and derivative prices, we can enrich our observed data and strive for better calibration prices.

Efforts to calibrate jump-diffusion models from option prices have been undertaken by a number of authors either from a parametric and a nonparametric perspective. See Andersen and Andreasen (2000), Cont and Tankov (2003) and Gatheral (2006). In this work, differently from previous efforts, we focus on using Dupire’s forward equation, as generalized in the work of Bentata and Cont (2015) and propose a splitting calibration methodology to recover simultaneously the local volatility surface and the jump-size distribution. For a fixed dataset of European vanilla option prices we calibrate, for example, the volatility surface for some fixed jump-size distribution. Then, we find a new reconstruction of the jump-size distribution for the volatility surface previously calibrated. We repeat these steps until a stopping criteria for convergence is satisfied. The resulting pair of functional parameters is indeed a stable approximation of the true local volatility surface and the jump-size distribution, whenever they exist. It is important to mention that, the dataset used to identify this pair of functional parameters is the same one used in Dupire’s local volatility calibration problem. No additional data is required as it would be necessary if we wanted to calibrate both parameters at the same time using standard regularization techniques (Engl et al. (1996)). The resulting methodology is amenable to regularization techniques as those studied in Albani and Zubelli (2014) and Albani et al. (2018). In particular, different a priori distributions could be used. As a byproduct, we prove convergence estimates for the calibration of the jump-diffusion models as the data noise decreases. We also obtain stable and robust calibration algorithms which perform well either under real or synthetic data.

The plan for this work is the following: In Section 2 we set the notation and review some basic facts, including the fundamental forward equation for jump-diffusion processes. In Section 3 we discuss the main functional-analytic properties of the parameter to solution map. Section 4 is concerned with the splitting strategy and the regularization of inverse problems. In particular, we review the tangential cone condition and prove its validity under certain assumptions in our context. This condition, in turn, ensures the convergence of Landweber type methods. The results in this section are not specific to the jump-diffusion model under consideration. Indeed, they apply to more general inverse problems, although, to the best of our knowledge we have not seen presented in this form. In Section 5 we compute the gradient of the nonlinear parameter-to-solution map, which is crucial for the iterative methods. Section 6 is concerned with the numerical methods for the solution of the calibration problem and its validation. Differently from Cont and Voltchkova (2005a; b), we consider also the case where the jumps may be infinite. Section 7 presents a number of numerical examples that validate the theoretical results and display the effectiveness of our methodology. We close in Section 8 with some final remarks and suggestions for further work.

2 Preliminaries

Let us consider the probability space with a filtration . Denote by the price at time of our underlying asset and assume that it satisfies

| (1) |

where is a Brownian motion, and is the compensated version of the Poisson probability measure on , denoted by , with compensator . See Cont and Tankov (2003).

Assume also that is positive and bounded from below and above by positive constants, and the compensator satisfies

| (2) |

Since is uniformly bounded and nonnegative, then, by setting and denoting the time to maturity and the strike price, the seminal work of Bentata and Cont (2015) shows that the price of an European call option on the asset in (1), defined by

is the unique solution in the sense of distributions of the partial integro-differential equation (PIDE):

| (3) |

with , , and the initial condition

| (4) |

Since the diffusion coefficient in Equation (3) is unbounded and goes to zero as , let us perform the change of variable and define

So, denoting , the PIDE problem (3)-(4) becomes

| (5) |

with , and the initial condition

| (6) |

Instead of using directly in the PIDE problem (5)-(6), we consider, as in Kindermann and Mayer (2011), the double-exponential tail of

| (7) |

and the convolution operator

Applying Lemma 2.6 in Bentata and Cont (2015) to the integral part of the PIDE (5),

| (8) |

In what follows, we replace the integral part of the PIDE (5) by the right-hand side of (8).

Remark 1.

Define , so, by the definition of , it follows that , where is the solution of the PIDE:

| (9) |

with homogeneous boundary and initial conditions, where

with and weak derivatives of .

By assuming that with and , for every , and is a Lévy measure satisfying , Theorem 3.9 in Kindermann and Mayer (2011) states the existence and uniqueness of . The proof that is a weak solution of the PIDE problem (5)-(6) is an easy adaptation of the proof of Theorem 3.9 in Kindermann and Mayer (2011). To see that, just replace the test functions in , by test functions with compact support in , as in Bentata and Cont (2015), and replace by .

Uniqueness of solution can also be proved by analytical methods as in Barles and Imbert (2008); Garroni and Menaldi (2002) or by probabilistic arguments as in Theorem 2.8 in Bentata and Cont (2015). An alternative proof is to consider the difference between two different solutions of the PIDE problem (5)-(6). The resulting function is the solution of the PIDE (9) with . By Theorem 3.7 in Kindermann and Mayer (2011), the norm of the solution of the PIDE (9) is dominated by the norm of , which is zero. So, the difference is also zero and uniqueness holds. Since and are continuous in , it follows that is also a continuous function.

3 The Parameter to Solution Map and its Properties

The goal of the present section is to show the well-posedness of the PIDE problem (5)-(6) and some regularity properties of the parameter-to-solution map.

We make the following additional assumption:

Assumption 1.

The restrictions of the double-exponential tail to the sets and are in the Sobolev spaces and , respectively.

(respectively ) is the Sobolev space of (respectively ) functions such that its first and second weak derivatives are in (respectively ).

The above assumption holds, for example, if we assume that the measure is such that the functions and are continuous.

We recall, that the set of non-negative non-increasing functions has a nonempty interior in as well as the set of non-negative non-decreasing functions in . This is of particular importance since we need to show that the direct operator has a Frechét derivative.

In order to define the domain of the direct operator in the Banach space

let be fixed constants and be a fixed continuous function such that its weak derivatives with respect to and are in .

It is easy to see that .

For simplicity, in what follows we shall write , meaning that and are given as in the definition of .

Proposition 1.

Proof.

The existence and uniqueness proof follows by a fixed point argument. Given in and , define the operator that associates each to , solution of

| (10) |

with homogeneous boundary conditions. By Young’s inequality, . So, by Proposition A.1 in Egger and Engl (2005), it follows that the PDE problem (10) has a unique solution and . Again, by Young’s inequality, . Since , it follows that, for any with , . Let us see that is a contraction. For any , set , and . It follows that is the solution of (10) with and . So, is indeed a contraction in and has a unique fixed point , which is the unique solution of

| (11) |

with homogeneous boundary conditions.

Any solution of the PIDE problem (5)-(6) can be written as , where is the solution of the PIDE problem (11) with and the solution of (10) with , and the same boundary and initial conditions as the PIDE problem (5)-(6). The existence and uniqueness of is guaranteed by Corollary A.1 in Egger and Engl (2005). Therefore, the assertion follows. ∎

Remark 2.

Since in the above proof is a fixed point of , it satisfies the inequality

Assuming further that with the constant , we have that

| (12) |

Definition 1.

Lemma 1.

Proof.

We can now state the following:

Proposition 2.

The map is continuous.

Proof.

Let the sequence in converge to . We must show that . Define

By the linearity of the PIDE problem (5)-(6), is the solution of the PIDE problem (11) with and replaced by and , respectively, homogeneous boundary conditions and

So, by the estimate (12) and Young’s inequality for convolutions,

By the Sobolev embedding (see Theorem 7.75 in Iorio and Iorio (2001)), it follows that

The above estimate and Equation (13) imply that

Summarizing,

and the assertion follows. ∎

Proposition 3.

The map is weakly continuous and compact.

Proof.

Let the sequence in converge weakly to . Proceeding as in the proof of Proposition 2 define

So it satisfies the PIDE (11) with and replaced by and , respectively, and homogeneous boundary condition. Furthermore, it satisfies

| (14) |

We shall prove that each of the two terms on the RHS of Equation (14) goes to zero as . In either case, we decompose the set as the disjoint union , where

with . Concerning the first term on the RHS of Equation (14), we have by Sobolev’s embedding that

| (15) |

By the compact immersion of into we have that weakly convergent sequences of are sent into norm convergent ones in (Proposition IV.4.4 in Taylor (2011)). Thus, . Now, we recall that as . To see that the RHS of Inequality (15) goes to zero, note that, given , for a sufficiently large , , since is dominated by , which is uniformly bounded. In addition, is bounded by , which is finite. Thus, for all sufficiently large , and with the same of the previous estimate, .

Concerning the convergence of the second term in Equation (14), by Jensen’s inequality, we have that

So, breaking it into the following two integrals we get

The integral goes to zero by the dominated convergence theorem as (Theorem 1.50 in Adams and Fournier (2003)). By Fubini’s Theorem, it follows that

For almost every , the Rellich-Kondrachov theorem (Part II of Theorem 6.3 in Adams and Fournier (2003)) implies that goes to zero. Just recall that and . By the estimate

we can apply the dominated convergence theorem to get that goes to zero as , for each fixed . Therefore, and the assertion follows. ∎

We formally define the derivative of and then we show that it is in fact the Frechét derivative of .

Definition 2.

Remark 3.

By the proof of Proposition 1, for any and any the PIDE problem of the definition above still has a solution in . In addition, such PIDE problem is linear with respect to . So, for every , is a linear and bounded map from to , satisfying

| (16) |

Proposition 4.

The map is Frechét differentiable and satisfies

| (17) |

for any and any , such that .

Proof.

Let be fixed and be such that . Define

and . By the linearity of the PIDE problems (5)-(6) and (11), is the solution of the PIDE problem (11), with homogeneous boundary conditions and

So, satisfies the estimate

By the triangle inequality, Young’s inequality for the convolution and Sobolev’s embedding’s theorem, it follows that

and the asserted estimate holds.

The set has a nonempty interior, is a bounded linear map from to , and the estimate (17) implies that

Thus, is Frechét differentiable. ∎

4 Splitting Strategy and Regularization

In this section, under an abstract setting, we consider a Tikhonov-type regularization of the simultaneous calibration of two parameters from a set of observations. A splitting strategy is used to solve the resulting minimization problem. Results concerning the convergence of this approach to an approximate solution of the inverse problem are provided. They rely on certain assumptions which will be shown to hold for the calibration problem at hand of jump-diffusion local volatility models.

4.1 Tikhonov-type Regularization

Firstly, let us introduce some basic notions of Tikhonov-type regularization. This methodology has been used extensively for the solution of ill-posed inverse problems. See Scherzer et al. (2008) and Engl et al. (1996) for more details.

Consider the map between two Banach spaces and . Given in the range of , , find some solution of the equation:

| (18) |

Since there may be more than one element in solving (18), it is common to search for a solution that minimizes some convex functional , which is related to some a priori information. So,

and is so-called a -minimizing solution.

In general, it is not possible to have access to the data in , but only some imperfect approximation satisfying

| (19) |

where is the noise level and is a projection onto some subspace of , where is defined. For example, can define the observation of in some discrete mesh.

Since the inverse problem (18) can be ill-posed, Tikhonov-type regularization is applied, i.e., we must find an element of that minimizes the (Tikhonov-type) functional:

| (20) |

where

| (21) |

is the data misfit or merit function, and is a constant so-called regularization parameter. The penalization is called the regularization functional. The minimizers of (20) in are called Tikhonov minimizers or reconstructions, and are denoted by .

The framework of convex regularization will now be used. See Scherzer et al. (2008) for more information. In what follows, we shall need:

Assumption 2 (Assumption 3.13 in Scherzer et al. (2008)).

Let us assume that

-

1.

The topologies and associated to and , respectively, are weaker than the corresponding norm topologies.

-

2.

The exponent in Equation (21) satisfies .

-

3.

The norm of is sequentially lower semi-continuous with respect to .

-

4.

is convex and continuous with respect to .

-

5.

The objective set satisfies , and has a nonempty interior.

-

6.

For every and the level set

is sequentially pre-compact with respect to .

-

7.

For every and the level set is sequentially closed w.r.t. and the restriction of to is sequentially continuous w.r.t. and .

By Assumption 2, the existence of stable Tikhonov minimizers is guaranteed by Theorems 3.22 and 3.23 in Scherzer et al. (2008). If the inverse problem in (18) has a solution, then, also based on Assumption 2, Theorem 3.25 in Scherzer et al. (2008) says that there exists an -minimizing solution of (18) and Theorem 3.26 states the convergence of a sequence of Tikhonov minimizers to an -minimizing solution whenever and satisfies the limits:

| (22) |

4.2 A Splitting Strategy Algorithm

The presence of jumps together with the diffusive parts motivates separating the regularization into two parts. In this section we shall now describe such approach in the general framework of convex regularization.

Let be given by , where and are Banach spaces. Consider and two topologies of and , respectively, which are assumed to be weaker than the norm topologies of each of the corresponding spaces. So, will be endowed with two natural topologies: The norm and the product topology which is weaker than the norm topology. Consider again the operator , where .

The penalty term in (20) can be rewritten as

| (23) |

where with , , and the functionals and are convex and continuous w.r.t. and , respectively. So, the Tikhonov-type functional now reads:

| (24) |

Let us assume that Assumption 2 holds. Thus, if , has minimizers in . Since the norm topology of and are defined by the products of the norm topologies of and , and and , respectively, the projection operators and are continuous with respect to the norm topologies of , and and to , and .

For each , define the operator as , the Tikhonov-type functional , and the set . Similarly , and are defined.

Assume also that Items 5, 6 and 7 in Assumption 2 remain valid whenever is replaced by or , by or and by or . In this case, Theorems 3.22 and 3.23 in Scherzer et al. (2008) guarantee the existence of stable Tikhonov minimizers of and , for each and .

Our approach is to split the iteration so that at each step the jump and the diffusive component are updated successively. More precisely, For any (or ), set () and consider the iterations with :

| (25) |

Repeat the iterations until some termination criteria.

If the algorithm starts with instead of , the order of the two iterations must be reversed.

Definition 3.

A stationary point of the functional is some point , such that

In what follows we shall assume the continuity of with respect to . This holds, for example, if and are -continuous. This hypothesis is necessary in the proof of the following proposition.

Proposition 5.

For every initializing pair , any convergent subsequence produced by the algorithm of Equation (25) converges to some stationary point of .

Proof.

Consider the sequence defined by the iterations in (25). By construction, the sequence is non-increasing and bounded, and thus it converges. In addition, is a subset of some level set , which is -pre-compact by Item 6 in Assumption 2. For every cluster point of , for all .

Given , it follows that by the -continuity of , since the subsequence converges to w.r.t . So, for each ,

because is a minimizer of . Applying more steps of the algorithm of Equation (25), it follows that

So, . In addition, for every ,

Hence, is a minimizer of . To see that is a minimizer of , note that, for any , Since is a minimizer of , it follows that, . By the fact that , for every , the assertion follows. ∎

Denote the stationary point obtained with Algorithm (25) by . Note that a stationary point need not to be a Tikhonov minimizer, since, in principle, it can be a saddle point. However, we shall see in Proposition 8 that such stationary point is indeed an approximation of the inverse problem solution.

Remark 4.

Recall the definition of the sub-differential of a convex function at the point , with a Banach space, which is the set of elements in the dual space satisfying

If and are Frechét differentiable, it follows that, for each and ,

Moreover, is also Frechét differentiable and

For a proof of Remark 4, see Item (c) of Exercise 8.8 and Proposition 10.5 in Rockafellar and Wets (2009). So, if and , then .

Let denote the stationary point obtained with the algorithm of Equation (25), this means that is a local minimum of and is a local minimum of . By Theorem 10.1 in Rockafellar and Wets (2009), and . So, . If, in addition, is convex, then, is a Tikhonov minimizer.

Definition 4.

A stationary point with data is stable, if for every sequence such that in norm, then, , the sequence of solutions obtained with the algorithm of Equation (25) considering the data for each has a -convergent subsequence. In addition, the limit of every -convergent subsequence is a stationary point of the Tikhonov functional with data .

Proposition 6.

The stationary point obtained by the algorithm of Equation (25) is stable.

Proof.

Consider the sequences and as in Definition 4. Firstly, it is necessary to prove that has a convergent subsequence. By Lemma 3.21 in Scherzer et al. (2008),

The sequence converges to , so is uniformly bounded in . In addition, if we assume further that, for each , the algorithm of Equation (25) is initialized with the same , it follows that

and applying Lemma 3.21 in Scherzer et al. (2008) again,

By the estimates above,

which implies that is a subset of some level set of . Item 6 in Assumption 2 implies that such level set is -pre-compact, and the assertion follows.

Suppose with no loss of generality that converges to , w.r.t. . For every , since is in ,

So, is in . Similarly, it follows that is in and the assertion follows. ∎

Since the stationary point obtained by the algorithm in Equation (25) is determined w.r.t and the regularization parameters and , let us denote it by . Let us also denote by an -minimizing solution of the inverse problem in (18), and by the noiseless data in (18).

Tangential Cone Condition

Now, we show that the tangential cone condition is a sufficient condition for the splitting strategy algorithm of Equation (25) to converge to some approximation of an -minimizing solution of the inverse problem (18).

Assumption 3.

Let the operator be Fréchet differentiable on each variable and , so it is Fréchet differentiable and its Fréchet derivative satisfies

In addition, there exist positive constants and such that, if are in the ball , centered at with radius , then the tangential cone condition is satisfied:

So, we can state the following result:

Proposition 7.

Proof.

By Proposition 5, the splitting algorithm converges to , a stationary point of the functional in (24). Since the operator is Fréchet differentiable, by Remark 4, zero is in the sub-differential of at . In other words, there exists and , such that

where is the duality map, and . See Margotti and Rieder (2014) and Chapter II in Cioranescu (1990) for more details on duality maps. Applying on both sides of the above equality, we have:

Note that,

Let us assume, by contradiction, that there is no such that . So, by the above estimates and assuming that , it follows

Since and are convex,

Summarizing,

| (27) |

and the right-hand side of the inequality (27) is positive. Since , by the estimate above, and . If , then,

Hence, we can find such that the left-hand side of (27) becomes smaller than the right-hand side, which is a contradiction. Therefore, there must exist such that

for each fixed . By the continuity of with respect to the norm topology of and to the topology the existence of some finite iterate number holds. To see that this also holds for any sufficiently small regularization parameters , just note that, by the same arguments above, there is no sequence , of regularization parameters with , such that for every . So, there must be , such that, for any and . It follows that . ∎

As a corollary of the proof above, we have the following estimate:

| (28) |

The following proposition states that the algorithm of Equation (25) produces a stable approximation of the solution of the inverse problem in (18).

Proposition 8.

If Assumptions 2 and 3 hold and the regularization parameters satisfy

| (29) |

then, every sequence of solutions obtained by the algorithm of Equation (25), satisfying the discrepancy (26), when , has a -convergent subsequence converging to some -minimizing solution of the Inverse Problem (18), with as in Equation (23).

Proof.

Consider , such that , for each , choose and such that the discrepancy principle in Equation (26) and the estimates in Equation (29) hold with data and noise level . Consider also the sequence of the corresponding stationary points generated by the algorithm of Equation (25).

We need to show that this sequence has a -convergent subsequence. Assume that the algorithm in Equation (25) initializes always with the same pair . So, for every ,

In addition, by the relation in Equation (23) and the estimate in (28),

| (30) |

So, taking , and since

it follows that,

i.e., there exists a constant such that the sequence is in the level set , which is pre-compact w.r.t. . Hence, it has a -convergent subsequence, which is denoted again by , and converging to , w.r.t. . Since, for each , , by the weakly lower semi-continuity of ,

This means that is a solution of the Inverse Problem (18). Note that, by the estimate in Equation (30),

So, is an -minimizing solution. ∎

The following proposition states the convergence of inexact solutions to some solution of the inverse problem in Equation (18). By inexact solution we mean the iterate satisfying the discrepancy in Equation (26).

Proposition 9.

Let the hypotheses of Proposition 26 be satisfied. Assume further that the functionals and are uniformly bounded for . Then, when , every sequence of inexact solutions satisfying the discrepancy in Equation (26) has a -convergent subsequence converging to a solution of the inverse problem in Equation (18).

Proof.

As in the proof of Proposition (8), let us consider , such that , for each , choose and such that the discrepancy principle in Equation (26) is satisfied and assume that for some finite constant . Consider also the iterates corresponding to and satisfying the discrepancy in Equation (26).

Since and by Lemma 3.21 in Scherzer et al. (2008),

Since and are uniformly bounded for , there exists some constant such that , where is replaced by in the Tikhonov-type functional. Since is pre-compact w.r.t. , the sequence of iterates has a -convergent subsequence, which is also denoted by and converges to w.r.t. . So, by the - continuity of and the norm of , it follows that

and the assertion follows. ∎

Remark 5.

It is not difficult to prove that, under the hypotheses of Proposition 8 there exists a sequence of finite iterates or inexact solutions that converges w.r.t. to some -minimizing solution of the inverse problem in Equation (18), when . Let us consider , such that and assume that for each , the solution provided by Algorithm 25 satisfies the discrepancy in Equation (26). Also, for each , find a subsequence of iterates converging w.r.t. to and select one iterate that also satisfies the discrepancy and is close to w.r.t. , and gets arbitrarily closer as increases. By Proposition 8, the sequence has a -convergent subsequence, converging to , a -minimizing solution of the inverse problem in Equation (18). It is easy to see that the corresponding subsequence of iterates also converges to w.r.t. .

5 The Calibration

This section is devoted to the solution of the calibration from quoted European vanilla option prices of the local volatility surface and the double exponential tail , by the splitting technique presented in Section 4. From the double-exponential tail, we estimate the jump-size distribution .

5.1 Calibration of Local Volatility Surface and Double Exponential Tail

The inverse problem can be stated as: Given a set of European call option prices , such that, is in the range of , , find in satisfying the equation

| (31) |

where is the solution of the PIDE problem in (5)-(6), using the integral representation (8).

In practice, it is only possible to observe noisy option data given in a sparse mesh of strikes. Such data is denoted by , where

| (32) |

and is the noise level.

To use the results from Section 4 in this context, we introduce the following notation:

where projects the solution of (5)-(6) onto the sparse mesh where is given. Since ,

Let and be the weak topologies of and , respectively. By assuming that and are convex, proper and weakly lower semi-continuous functionals, Propositions 2-4 imply that Assumptions 2-3 hold true. Note that, the tangential cone condition in Assumption 3 is an easy consequence of the Inequality (17) in Proposition 4. Hence, given the data , the splitting algorithm applied to the simultaneous calibration of and converges to some approximation of the true solution of the inverse problem (31), if the latter exists.

Since the inclusion of into is continuous, the existence and stability of solutions given by the splitting algorithm as well as its convergence to the true solution also hold whenever is replaced in the Tikhonov regularization functional in (24) and (21).

A possible choice of the penalization term to fulfill the weak pre-compactness of the level sets of the Tikhonov functional (24) is for the variable and for the variable , is

where the stands for the Kullback-Leibler divergence

with given. In this case, and are convex, weakly continuous and coercive. In addition, the level sets of the Kullback-Leibler divergence

are weakly pre-compact in . See Lemma 3.4 in Resmerita and Anderssen (2007).

5.2 Calibration of Jump-Size Distribution from Double Exponential Tail

One possible way, but not recommended, to obtain the jump-size distribution is by differentiating once the double exponential tail , since, is such that and . By Sobolev’s embedding (see Theorem 4.12 in Adams and Fournier (2003)), are continuous functions and

So, and are continuous functions.

By Proposition 5.2 in Kindermann and Mayer (2011), can be represented as

where and are finite measures, defined in and , respectively. This implies that, and are continuous functions, which implies that they are absolutely continuous with respect to the Lebesgue measure. See Lemma III.4.13 in Dunford and Schwartz (1958). So, there exist integrable functions , such that

Define , such that and .

Lemma 2.

The map is compact.

Proof.

Let the sequence converge weakly to some in . Define

for each and in the same way. It is easy to see that and . Note also that, by hypothesis, and . So, by Sobolev’s embedding (see Theorem 4.12 in Adams and Fournier (2003)), and .

The estimate

holds almost everywhere in , since is in . Similarly, almost everywhere. By the monotone convergence theorem the assertion follows. ∎

Since the map that associates to is compact, it follows that the corresponding inverse problem is ill-posed. So, the procedure of obtaining by differentiating is not stable.

The inverse problem of finding the jump-size distribution from the double exponential tail is: Given the output of the splitting algorithm , find satisfying

| (33) |

where is some subset of .

If we apply Tikhonov-type regularization to such inverse problem, it can be rewritten as: find minimizing

with in given.

Let us assume that is weakly lower-semi-continuous and convex. If the level sets of are weakly compact in (or is weakly compact), then, as in Section 4.1, there exists stable minimizers of in .

Summing up, the Tikhonov-type regularization provides a stable approximation for the jump-size distribution .

5.3 Gradient Evaluation

To implement a numerical gradient descent algorithm to minimize the Tikhonov-type functional with respect to each variable, as in Albani et al. (2018), it is necessary to evaluate the directional derivatives of a numerical approximation of the data misfit function . If and denote the iterates of and respectively in the gradient descent algorithm, evaluate

| (34) | |||

| (35) |

until some tolerance is reached, with and fixed. To perform this task, we shall present the evaluation of such derivatives in the continuous setting.

Since

to evaluate and , recall that the directional derivative of at in the direction , with , is denoted by and is the unique solution of the PIDE

| (36) |

with homogeneous boundary and initial conditions, where is the solution of the PIDE problem (5)-(6).

Note that, , and , so, for every ,

Since , where is the multiplication by operator and is the operator that maps the source onto the solution of the PIDE (36) with homogeneous boundary and initial conditions (with ), it follows that

where is the solution of the adjoint PIDE:

| (37) |

with homogeneous boundary and terminal conditions.

6 A Numerical Scheme

Differently from Cont and Voltchkova (2005a), we consider directly the case where the activity of jumps can be infinite. This is because we use the representation (8) for the integral term in the PIDE problem (5)-(6).

Firstly, let us restrict the log-moneyness range where the PIDE problem (5)-(6) is defined to , with , and then, . Outside , the numerical solution assumes the value of the payoff function at these points.

Let be fixed. We consider the discretization , with , and , with . Denote by , , and . Define also:

where these integrals are approximated by the trapezoidal rule.

The differential part of the PIDE problem (5)-(6) is approximated by the Crank-Nicolson scheme and the integral operator by the trapezoidal rule, leading to:

| (38) |

where

In Kindermann et al. (2008) a Crank-Nicholson-type algorithm was also used to solve the so-called direct problem. There, the authors were interested in the calibration of the local speed function, which here is set constant and equal to .

The numerical scheme for solving the adjoint PIDE (37) with homogeneous boundary and terminal conditions is quite similar to the one in Equation (38). Following the same ideas presented in Section 5.3 we find the discrete version of the gradients of the data misfit function .

6.1 Numerical Validation

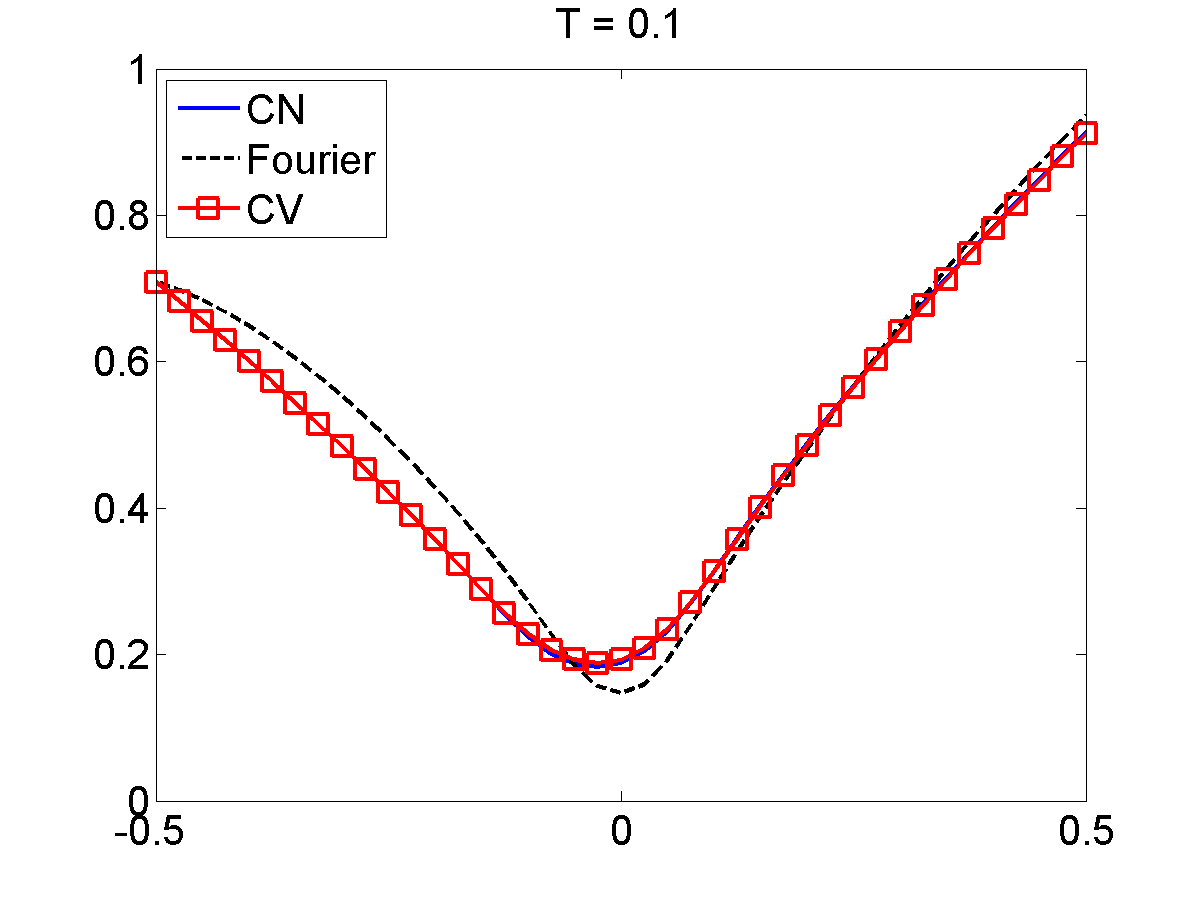

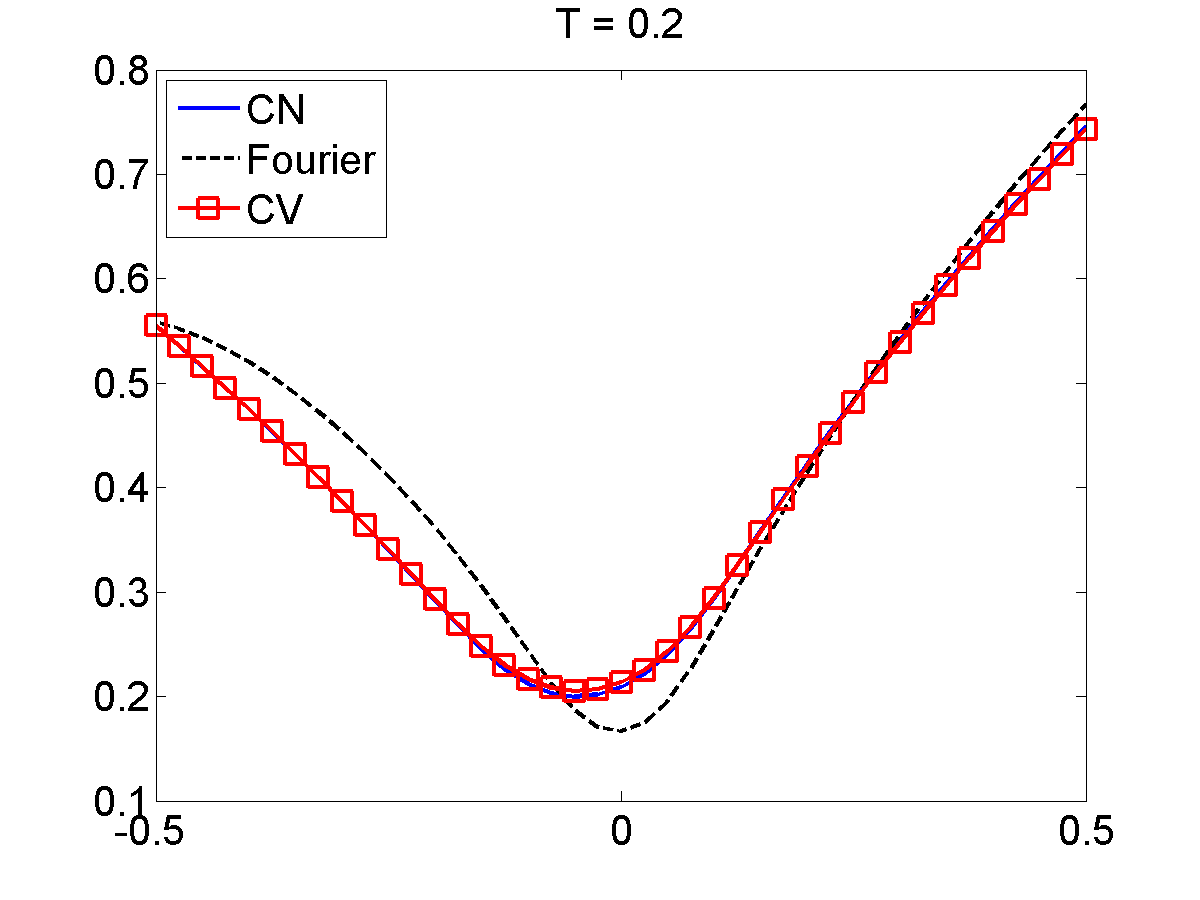

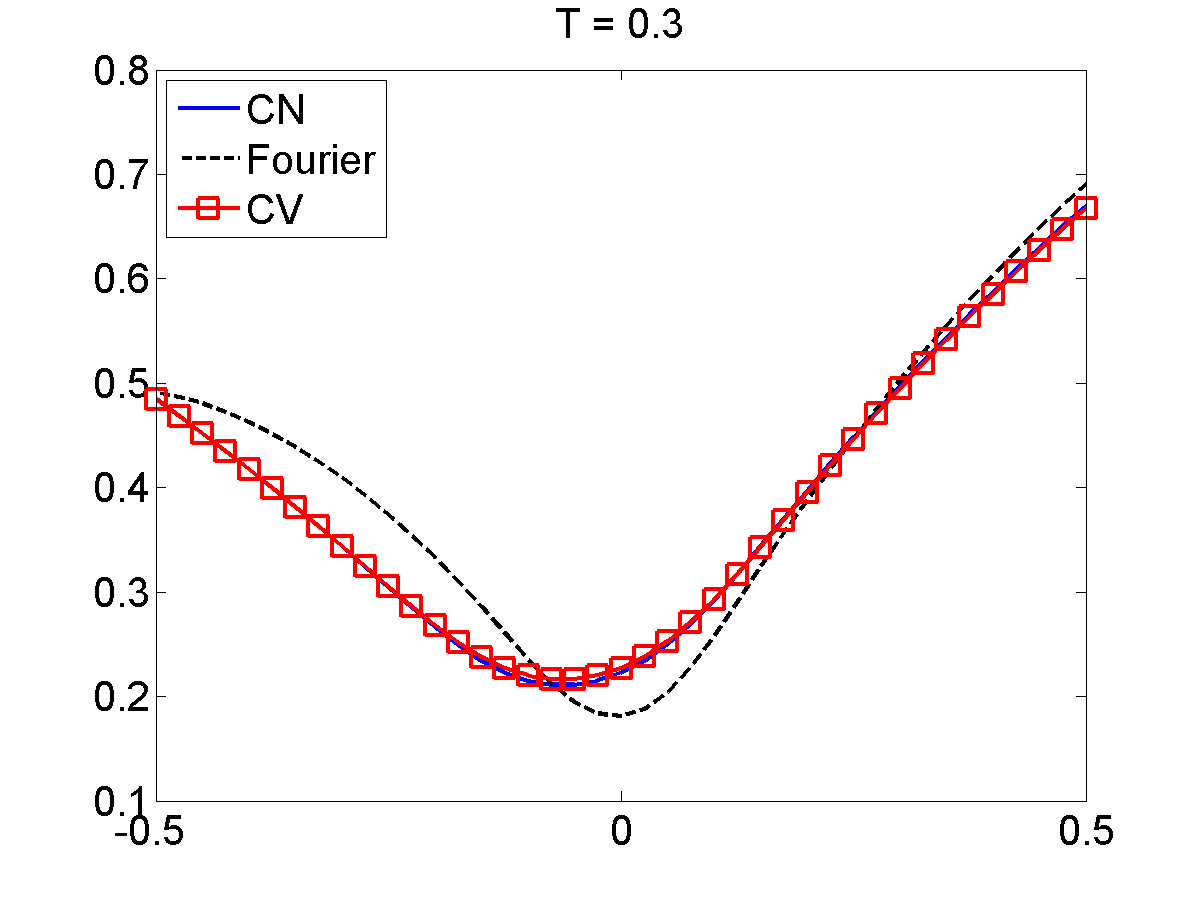

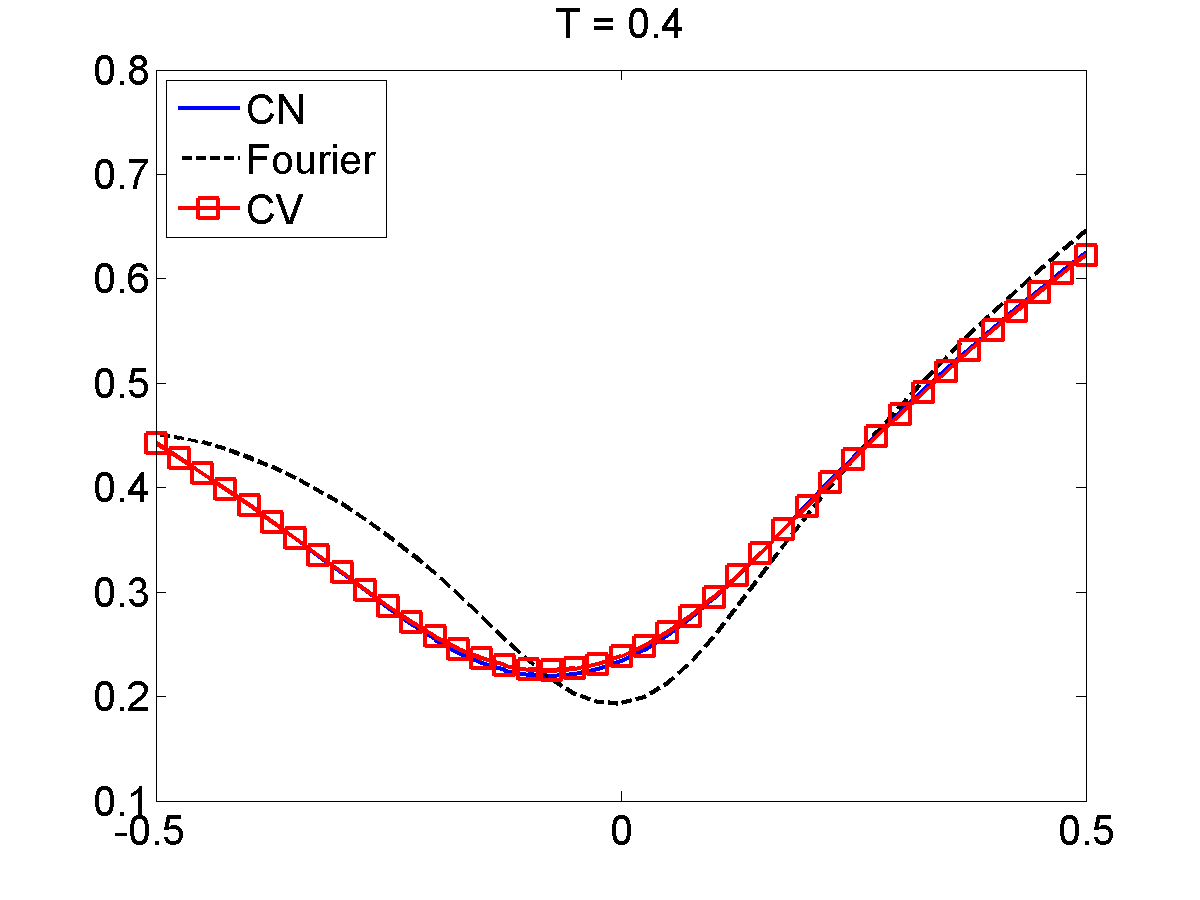

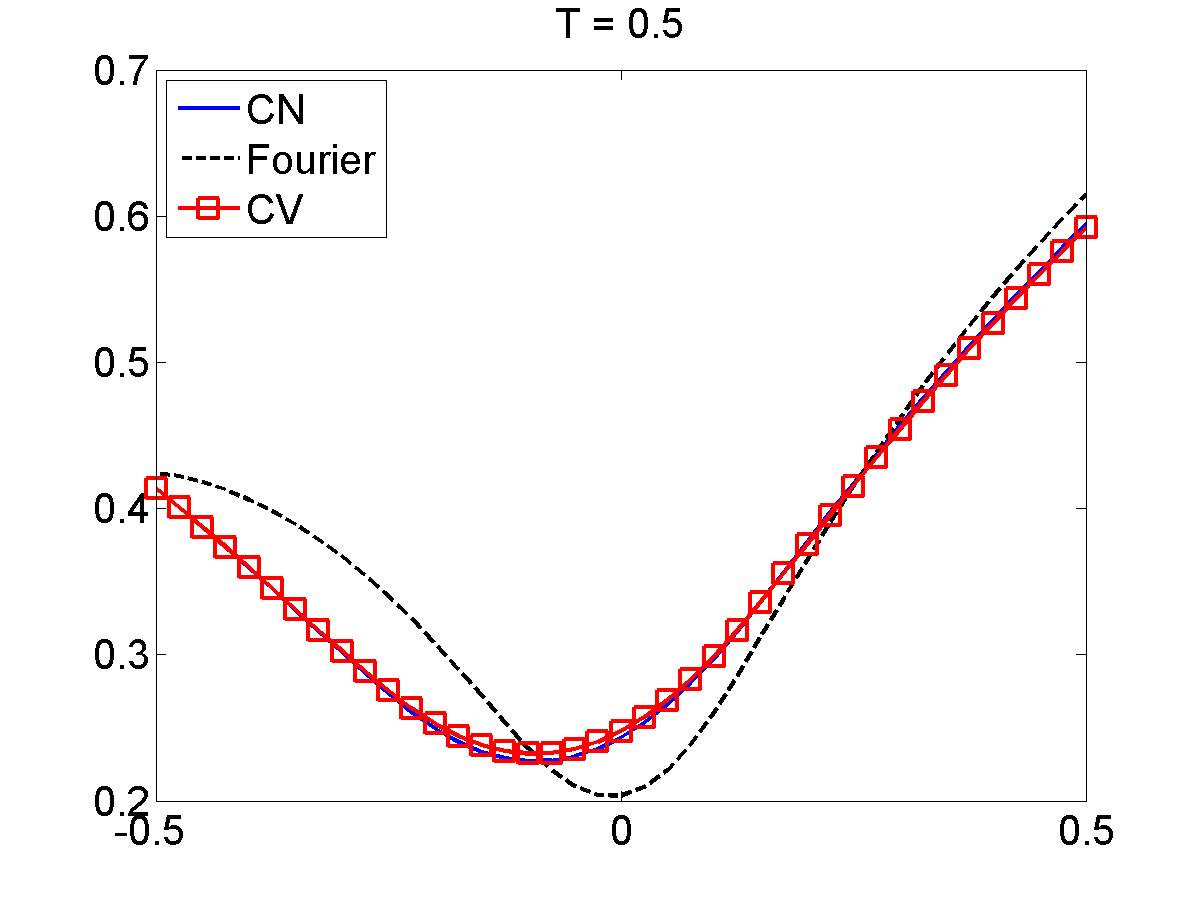

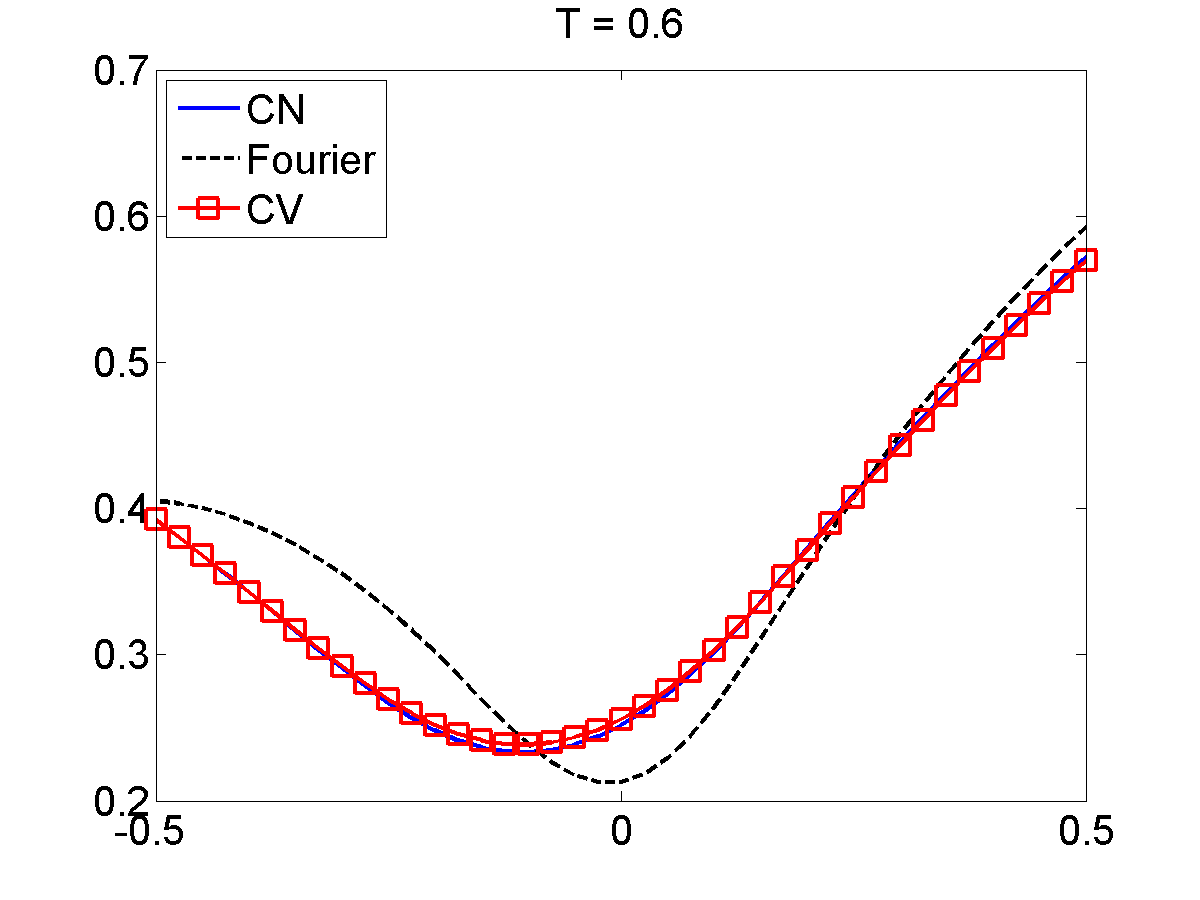

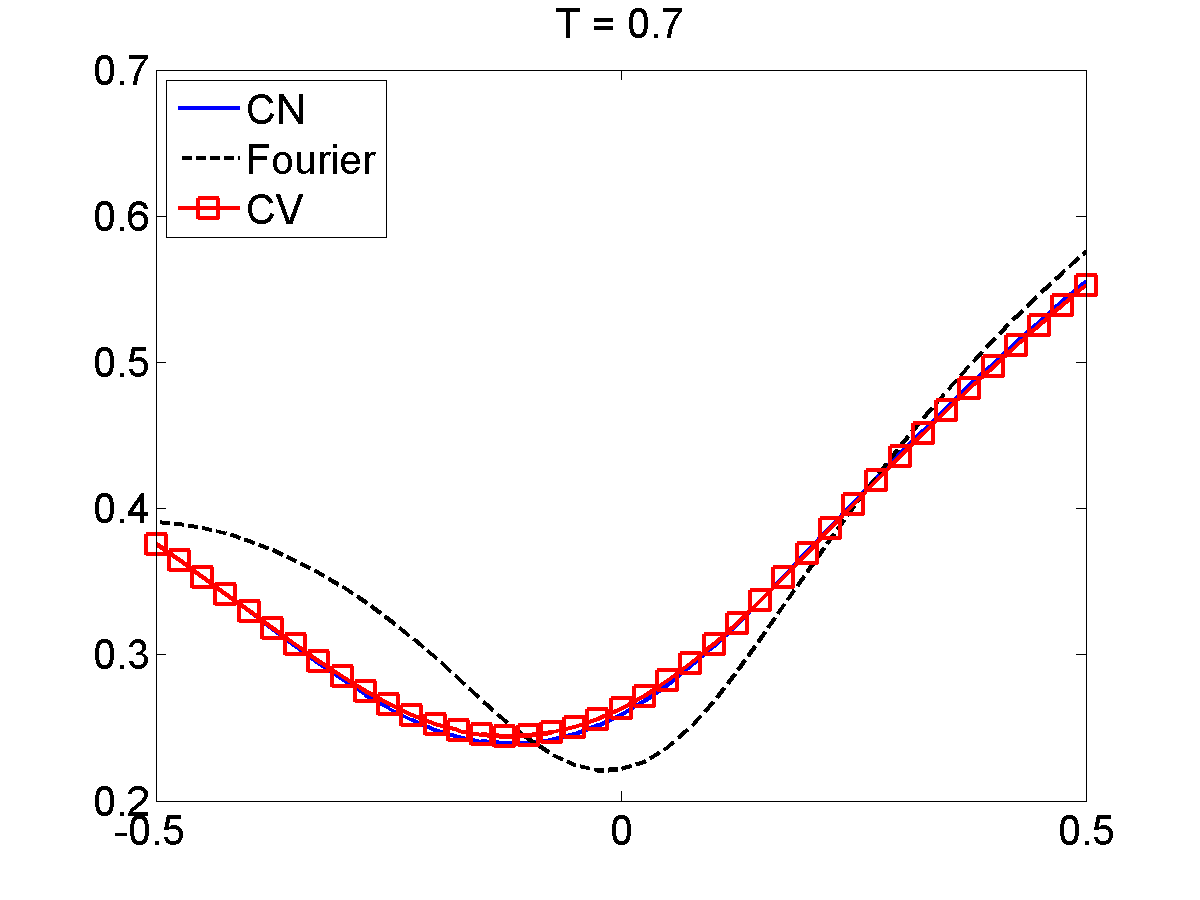

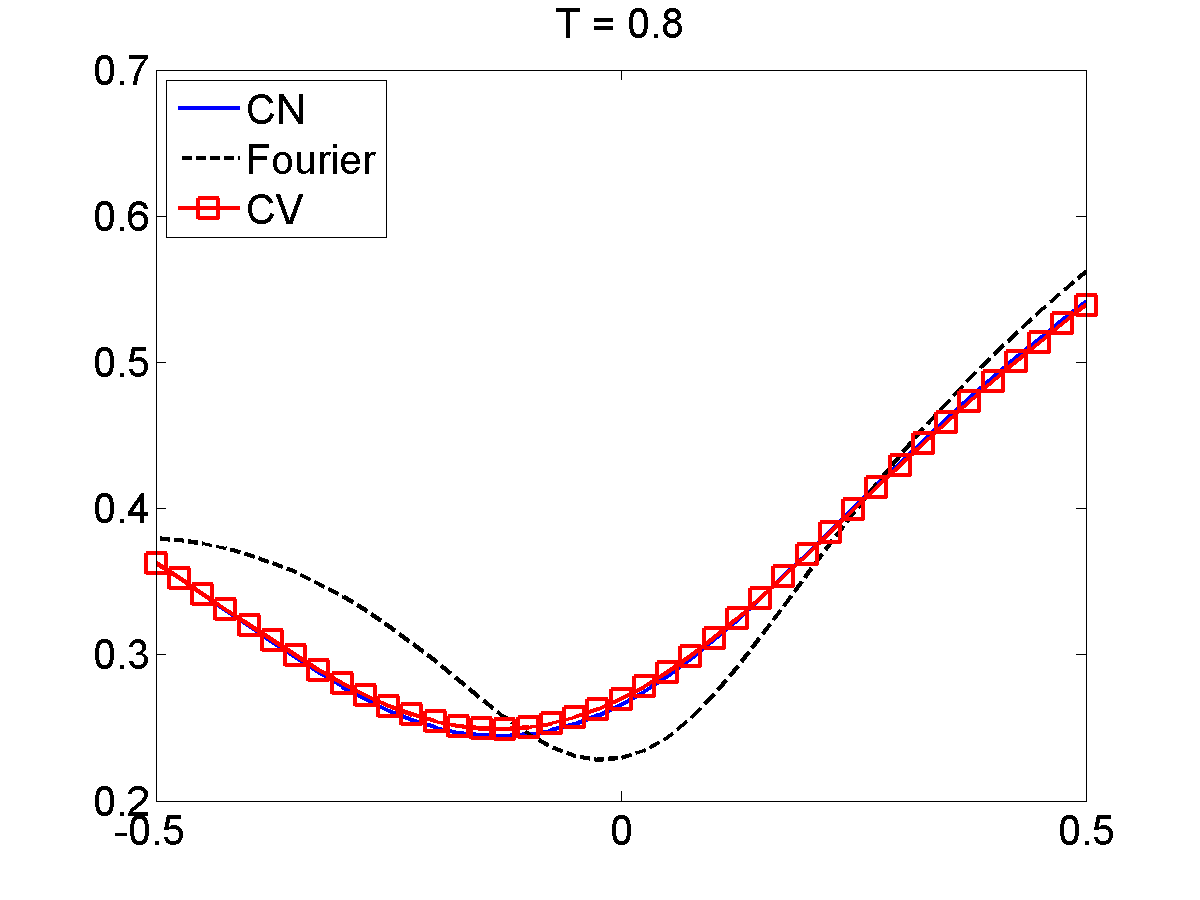

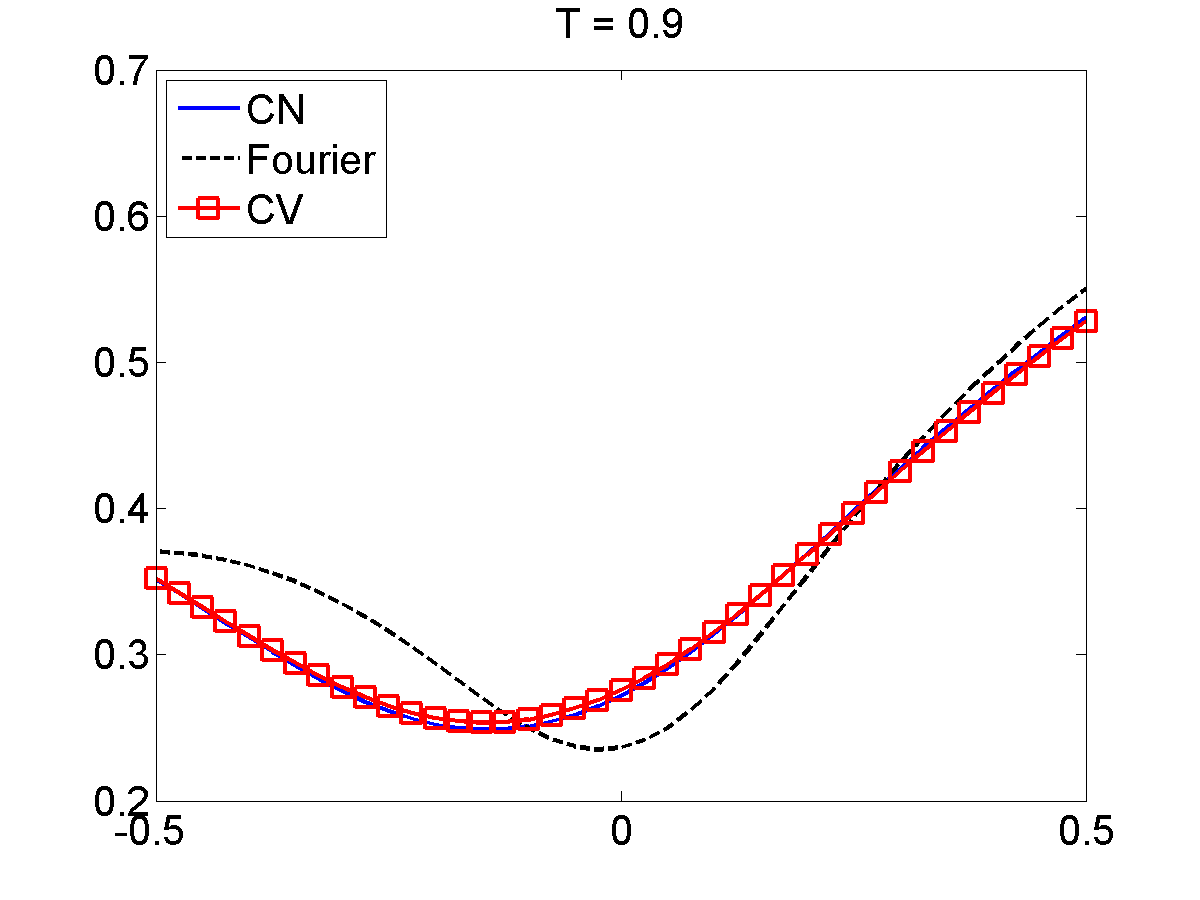

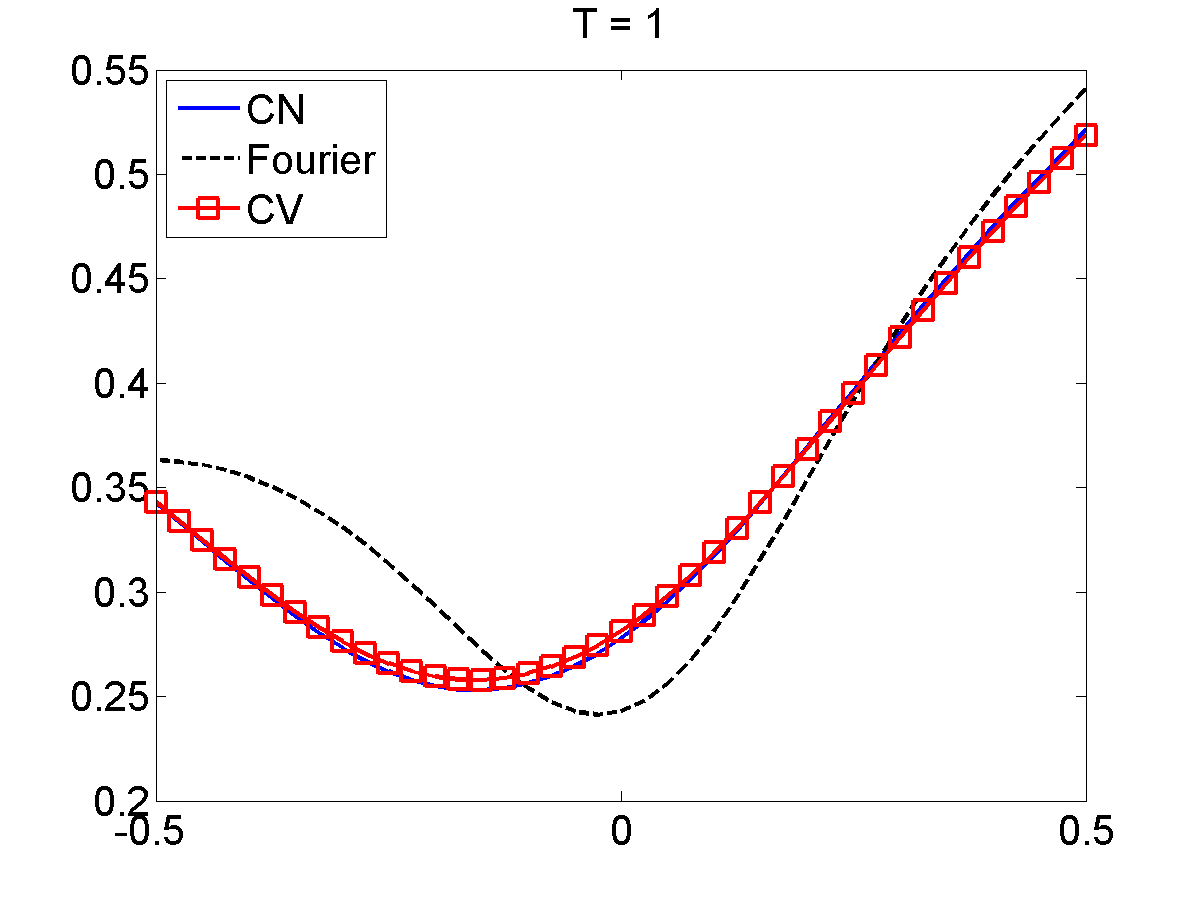

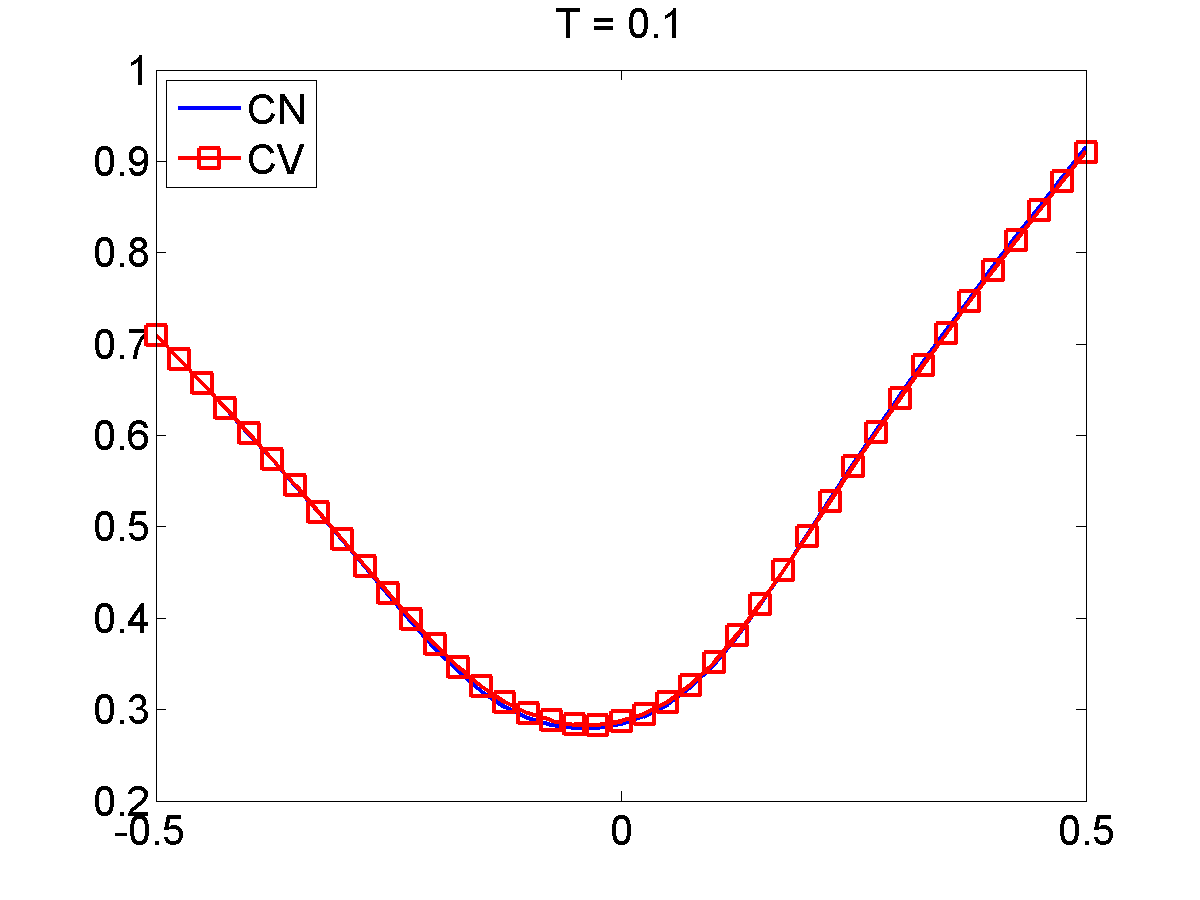

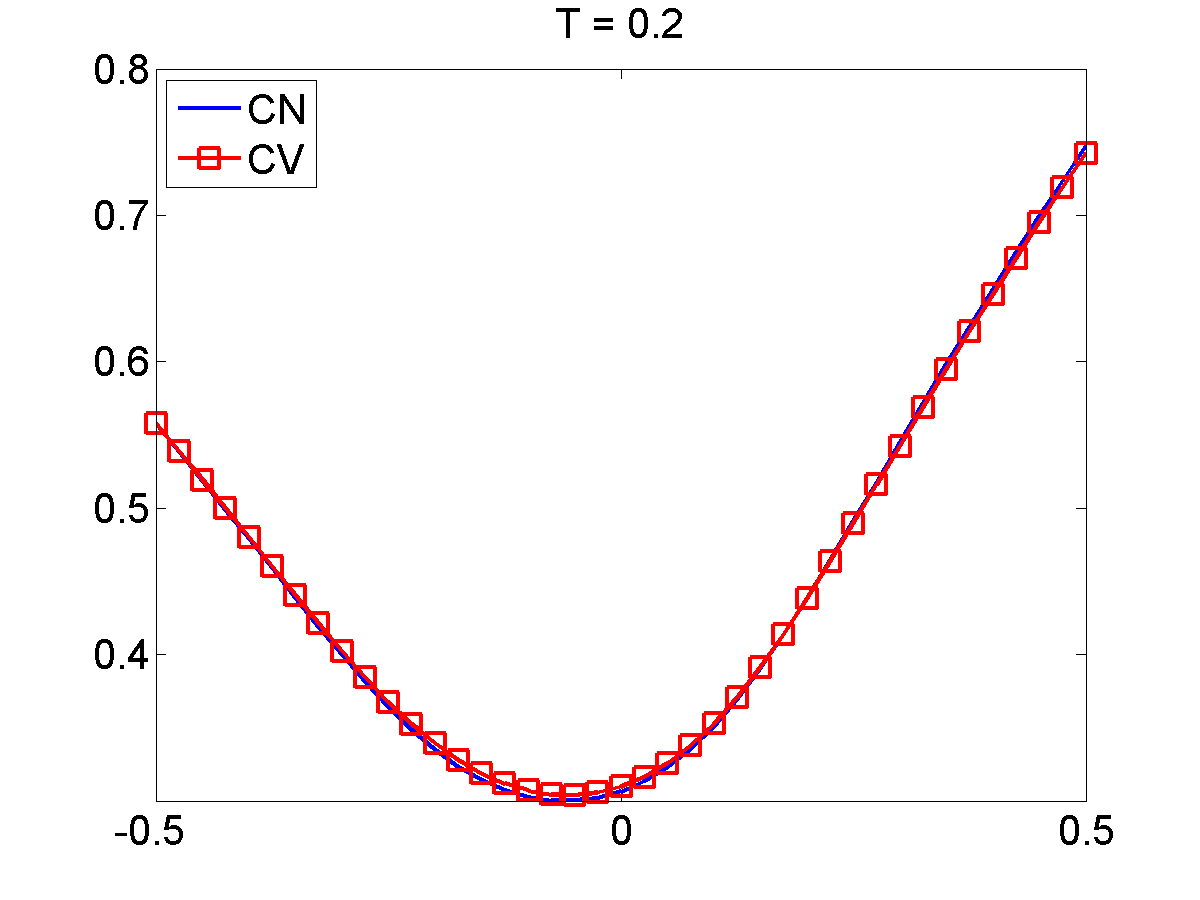

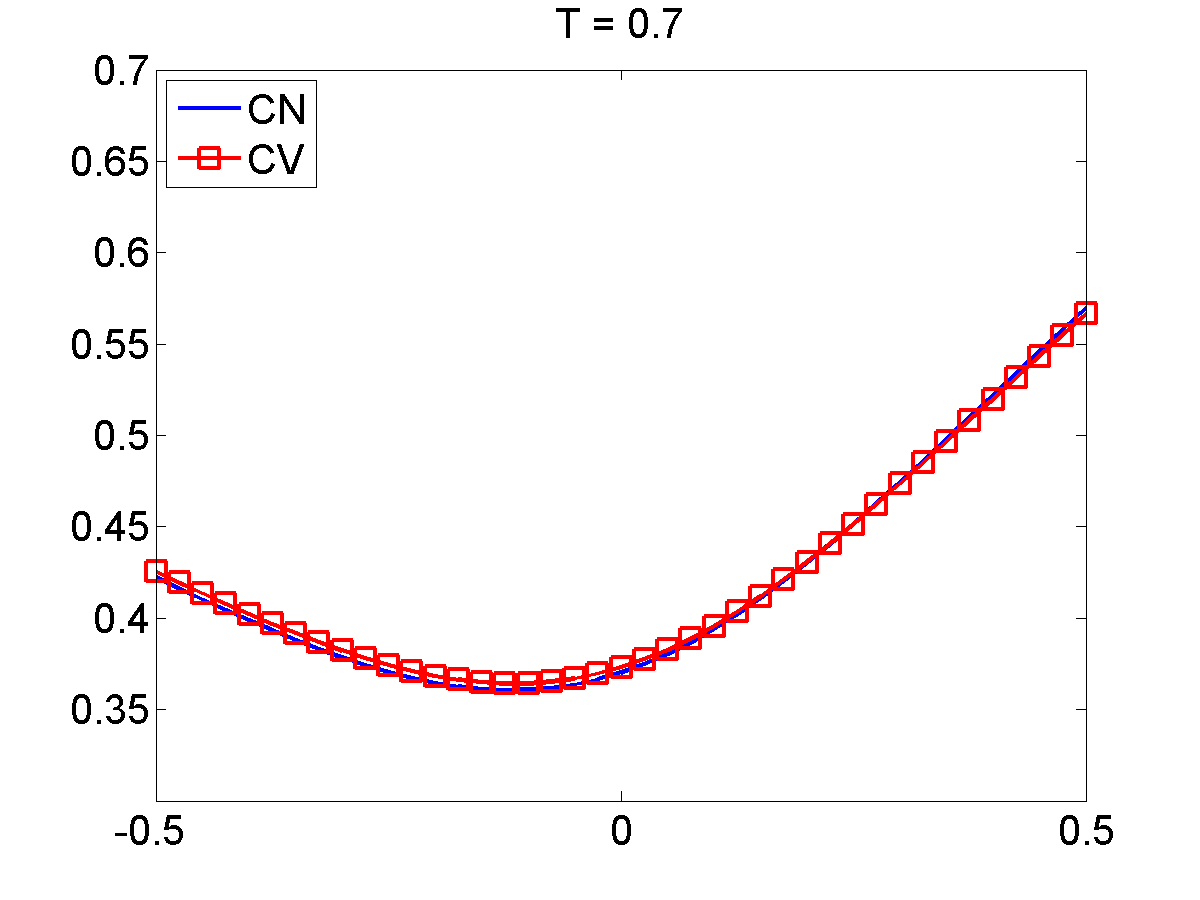

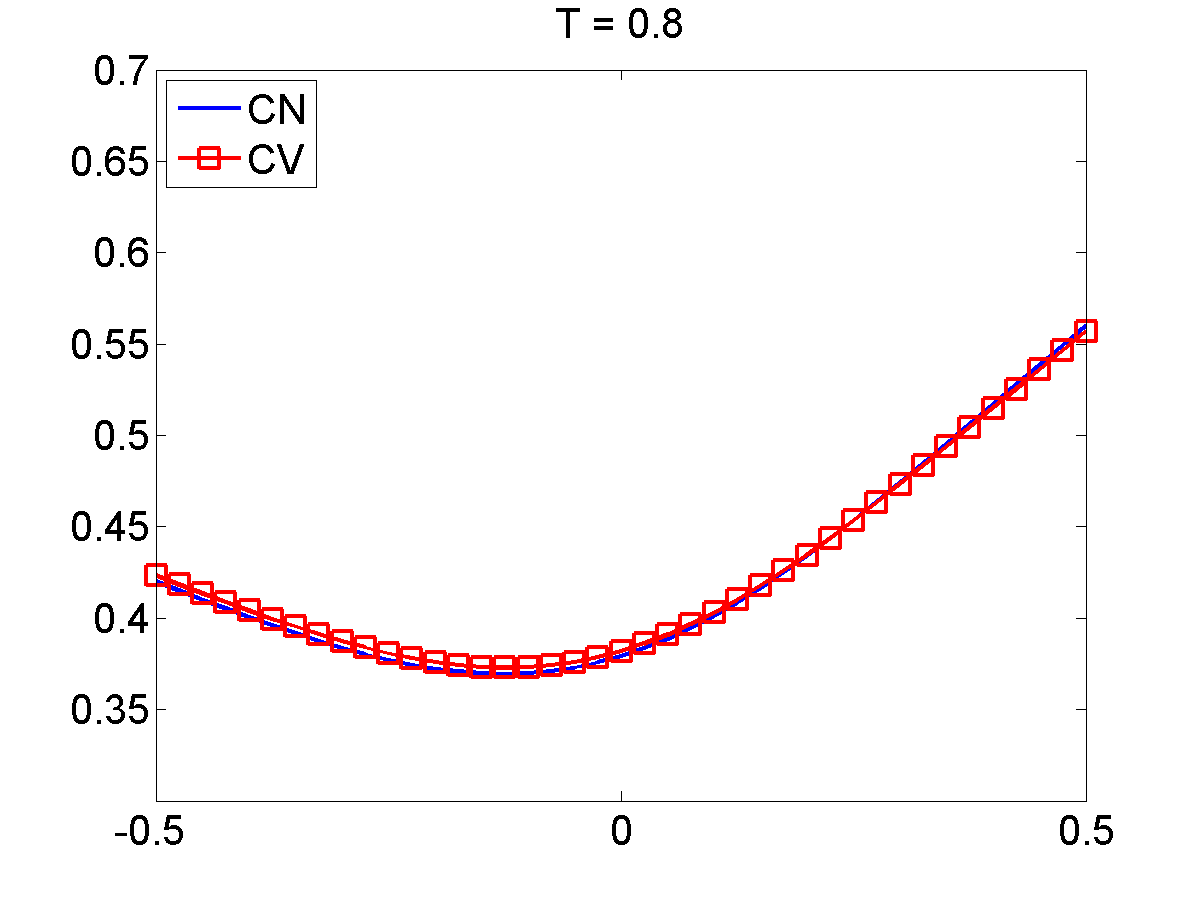

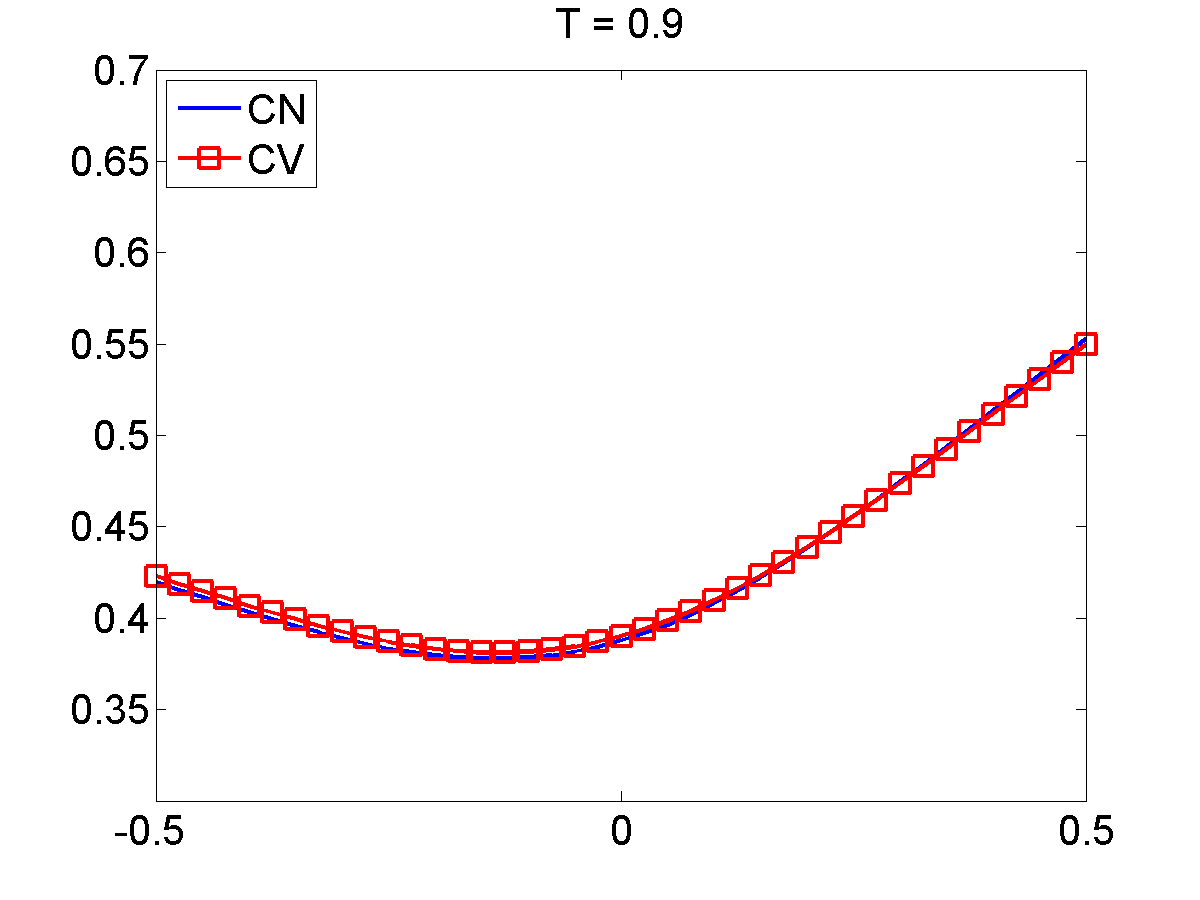

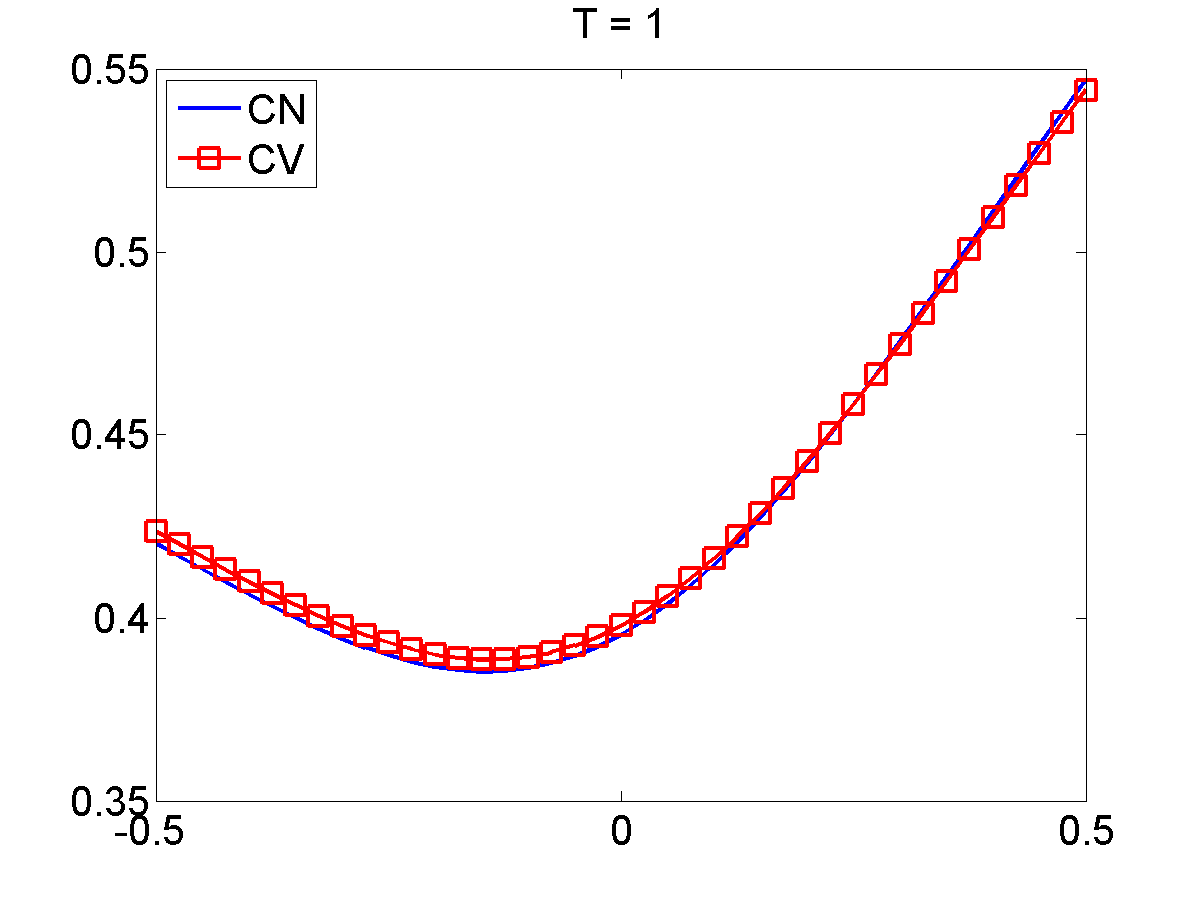

The purpose of this example is to illustrate the accuracy of the scheme in (38) by comparing it with other techniques.

Assume that , , , , , , and the local volatility surface is constant with . Then, we evaluate European call prices in three different ways, the scheme of Section 6, the implicit-explicit scheme from Cont and Voltchkova (2005a), and the Fourier transform method from Tankov and Voltchkova (2009), which is based on the pricing formula presented in Carr and Madan (1999).

In the following synthetic examples the measure is assumed to be absolutely continuous w.r.t. the Lebesgue measure and given by

| (39) |

We also consider a functional local volatility surface, given by

| (40) |

and compare the results given by the scheme (38) with the one presented in Cont and Voltchkova (2005a).

To measure the accuracy, we consider implied volatilities instead of prices. Let us denote by:

-

•

the set of implied volatilities corresponding to the prices evaluated with the schemes from Equation (38).

-

•

the set of implied volatilities corresponding to the prices evaluated with the schemes from Cont and Voltchkova (2005a).

-

•

the set of implied volatilities corresponding to the prices evaluated with the schemes from Tankov and Voltchkova (2009).

We estimate the normalized distance between them as follows:

We also estimate the mean and standard deviation of the absolute relative error (abs. rel. error), which is evaluated at each node as follows:

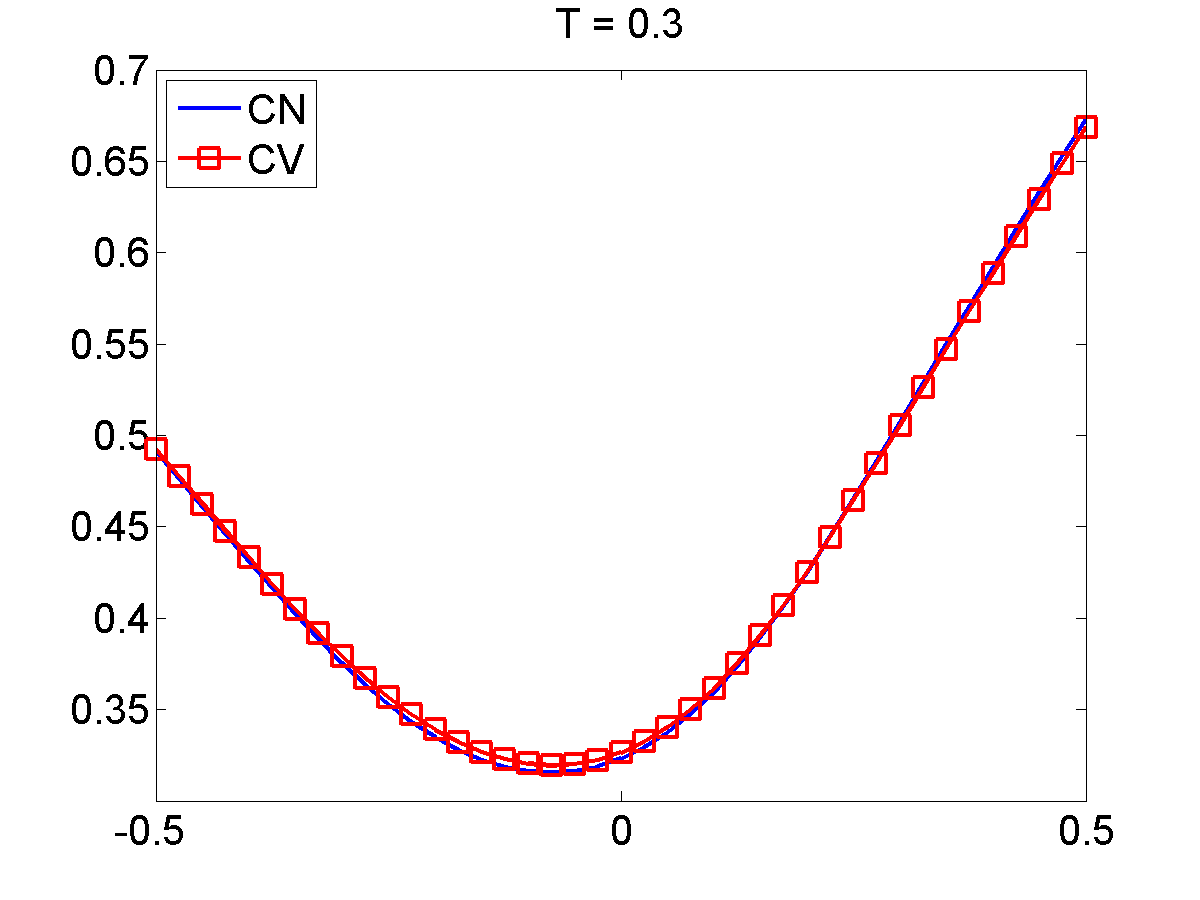

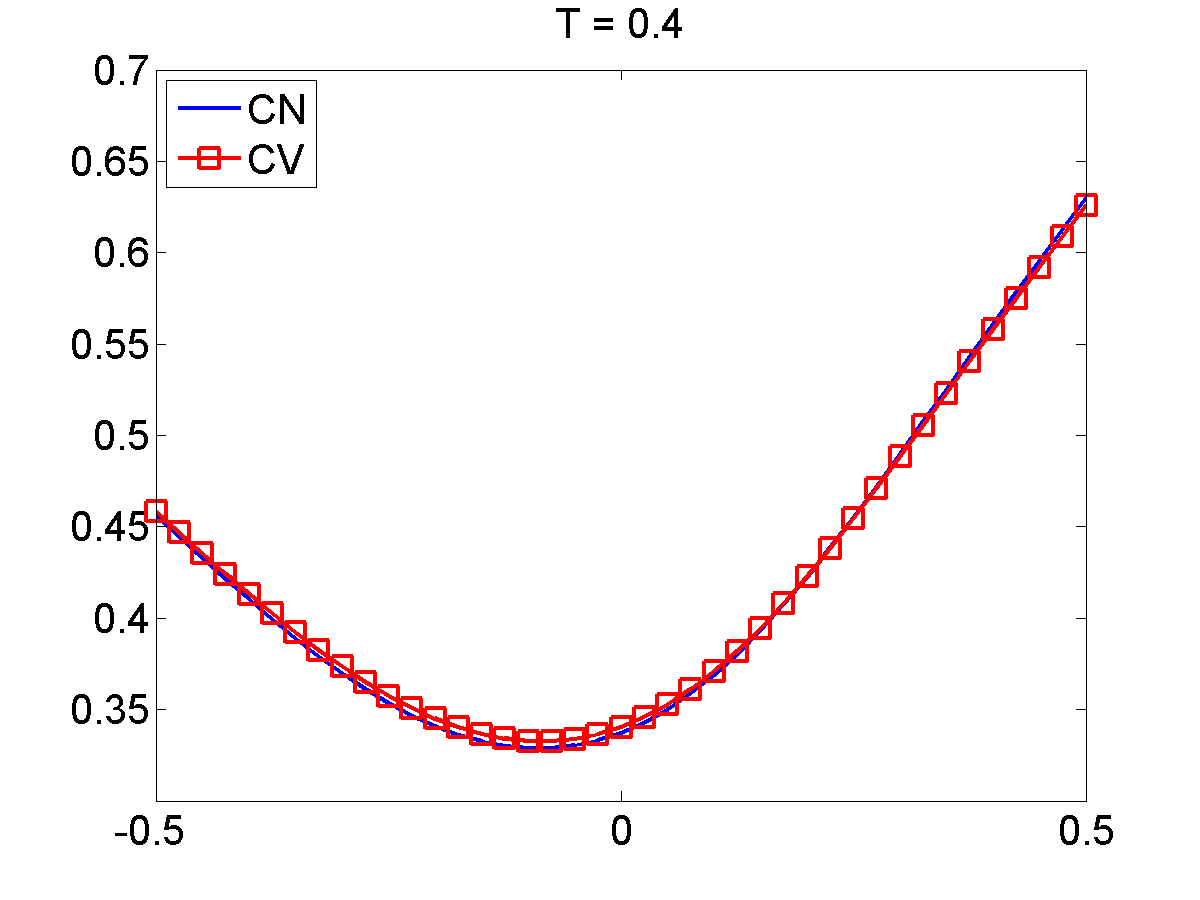

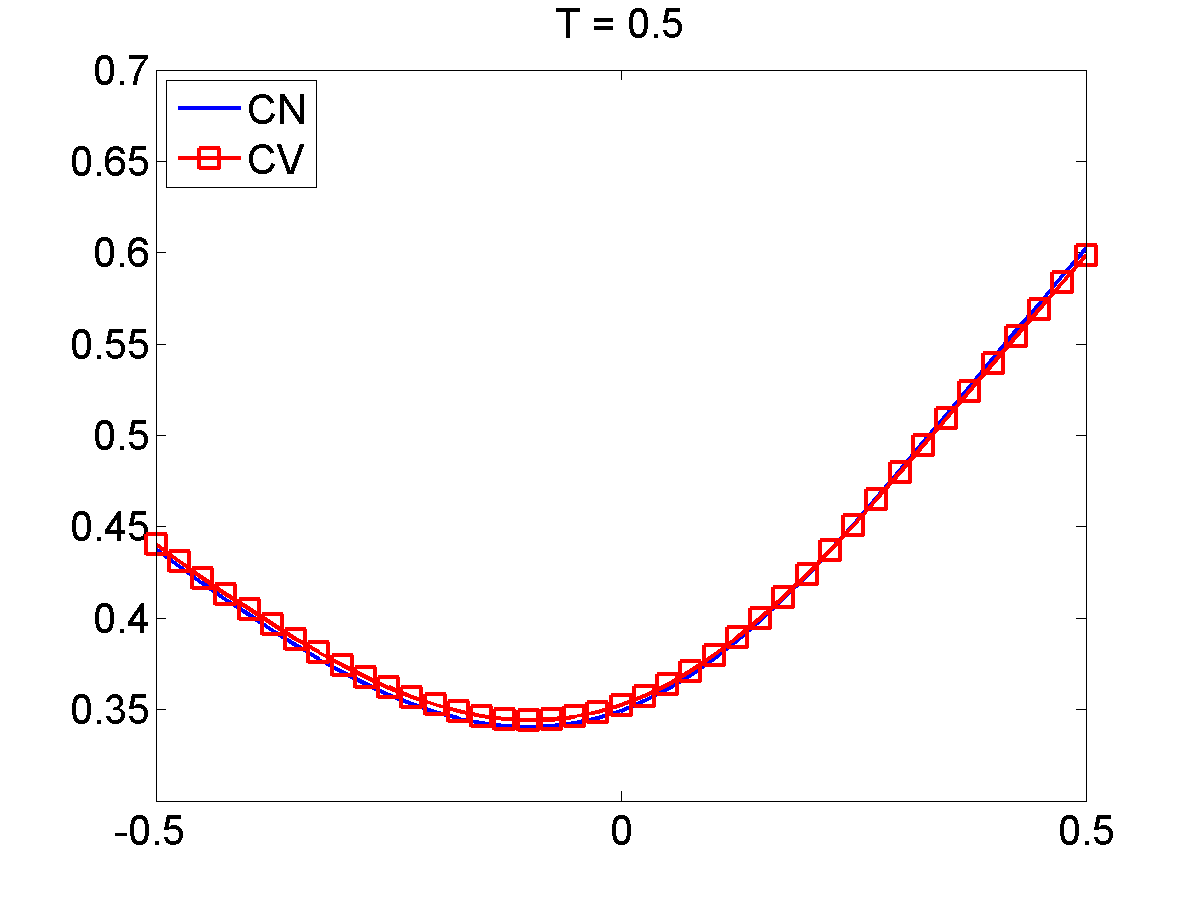

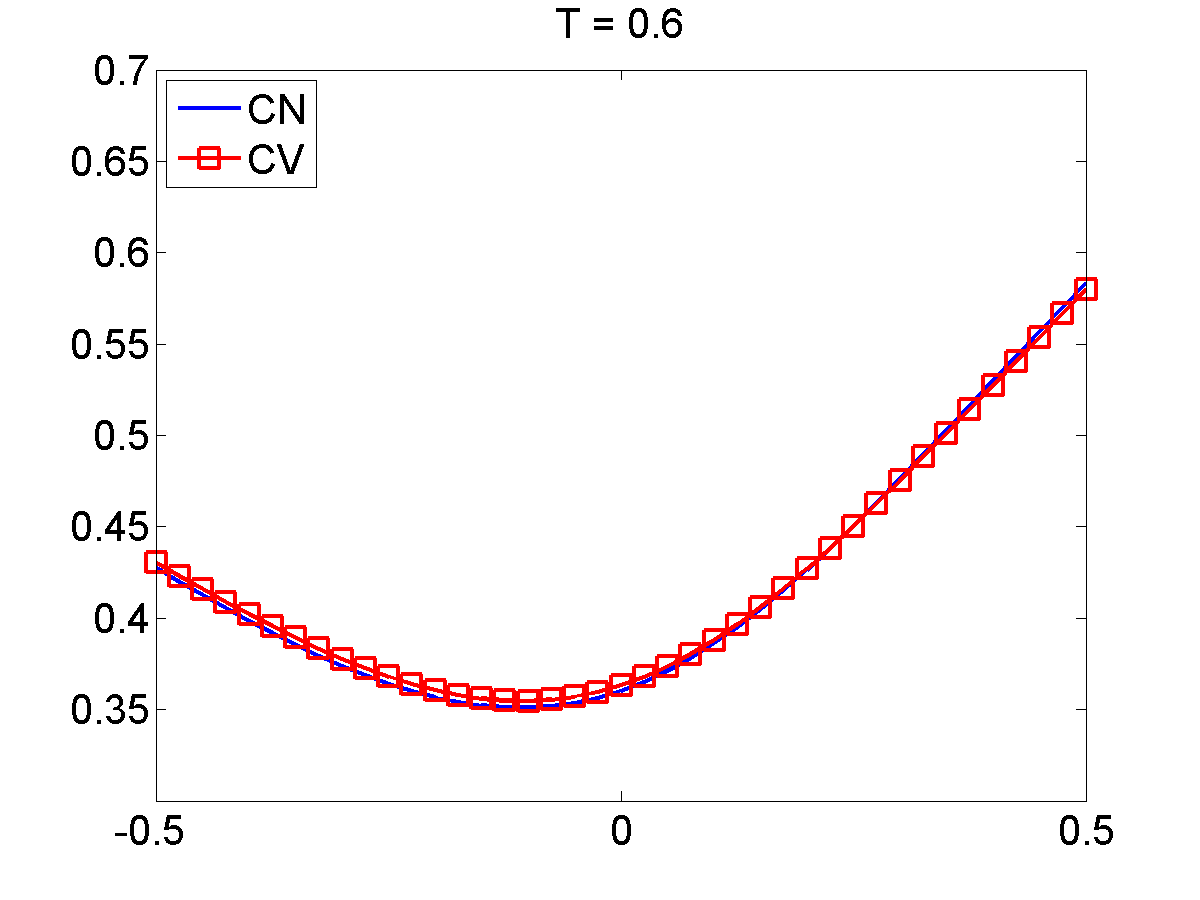

Such results can be seen in Table 1. A comparison between implied volatilities with constant and non-constant local volatility surface can be found in Figures 1 and 2, respectively.

| N.distance | Abs. Rel. Error | |||

|---|---|---|---|---|

| Mean | Std. Dev. | |||

| CV | 0.0064 | 0.0070 | 0.0072 | |

| Fourier | 0.0862 | 0.0923 | 0.0699 | |

| Non-constant | CV | 0.0064 | 0.0064 | 0.0038 |

As we can see, CN implied volatilities matched the CV ones with constant and a non-constant local volatility surface. When comparing with implied volatilities corresponding to the Fourier prices, the adherence of CN volatilities was not exact, but the result was satisfactory, since the relative error and the normalized distance are below of the norm of . These results illustrate the accuracy of the present scheme.

7 Numerical Examples

We shall now perform a set of illustrative numerical examples.

7.1 Local Volatility Calibration

This example is aimed to illustrate that, if is known, it is possible to calibrate the local volatility surface, as in Andersen and Andreasen (2000). The European call prices are generated by the difference scheme (38), with local volatility surface (40) and jump-size density (39), at the nodes , with and . This is a sparse grid in comparison with the one where the direct problem is solved, see the beginning of Section 6.1.

Under a discrete setting, set in the functional (24) the parameters as , , and define the penalty functional

| (41) |

where denotes the -norm and the operators and denote the forward finite difference approximation of the first derivatives w.r.t. and , respectively. The choice of the weights in the penalty functional is made heuristically and some hints about this choice can be found in Albani et al. (2018).

The minimization problem is solved by a gradient-descent method, the step sizes are chosen by a rule inspired by the steepest decent method and the iterations cease whenever the normalized -residual

is less than . For more details, see Albani et al. (2018).

The mesh step sizes used to evaluate the local volatility are the same as those used to generate the data. So, we use the following rule to evaluate the local volatility surface in the whole domain

combined with bilinear interpolation.

The normalized -distance between the implied volatility of the data and the prices obtained with the calibrated local volatility was , the mean and standard deviation of the associated absolute relative error at each node were and , respectively. With respect to the original and the calibrated local volatility surfaces, the normalized -distance was . The mean and the standard deviation of the corresponding absolute relative error at each node were and , respectively. The accuracy of our methodology can be also observed in Figures 3-4 where the implied volatilities of the model matched the data ones, and the reconstructed local volatility was quite similar to the original one. In both figures, “Calib.” stands for the calibrated local volatility and “Data” stands for the original one. Note that, the calibration was not perfect, since the data is collected in a sparse grid.

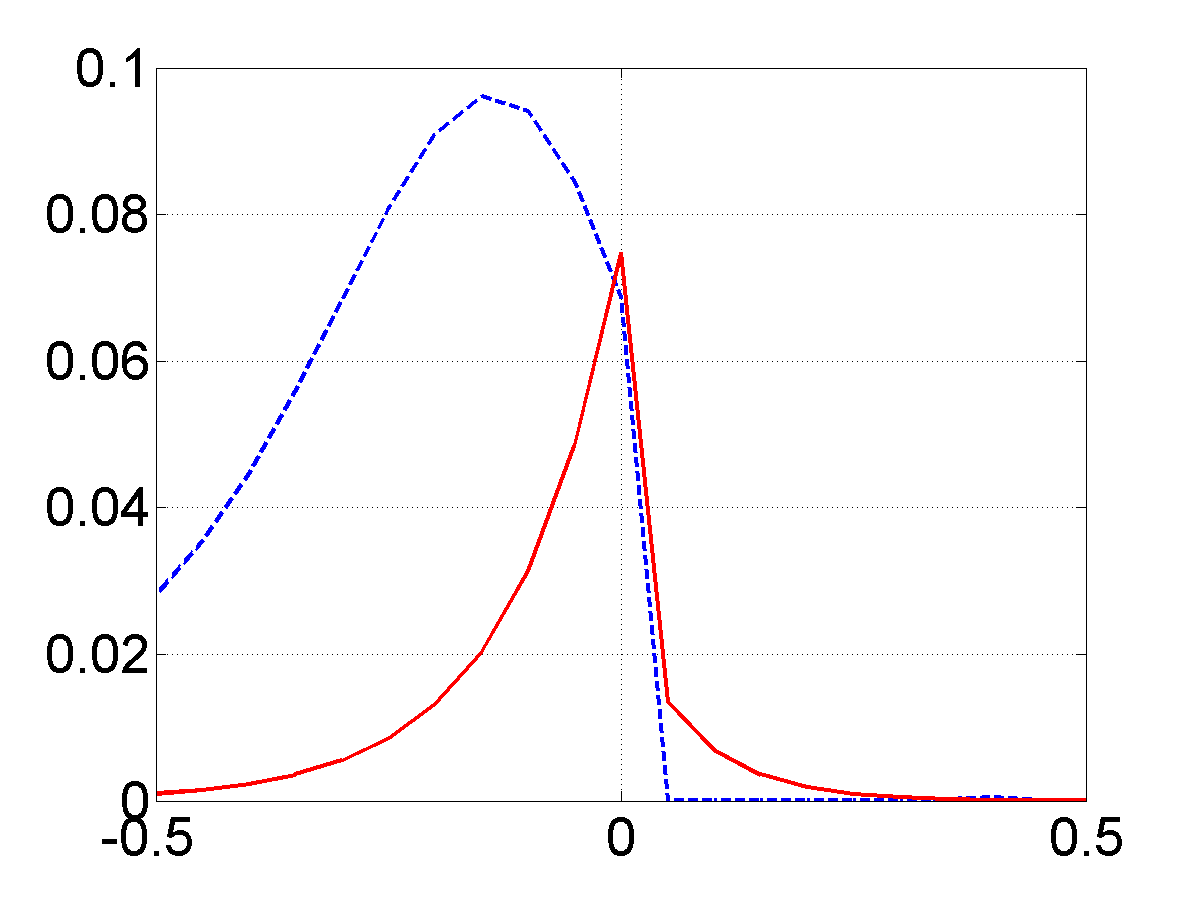

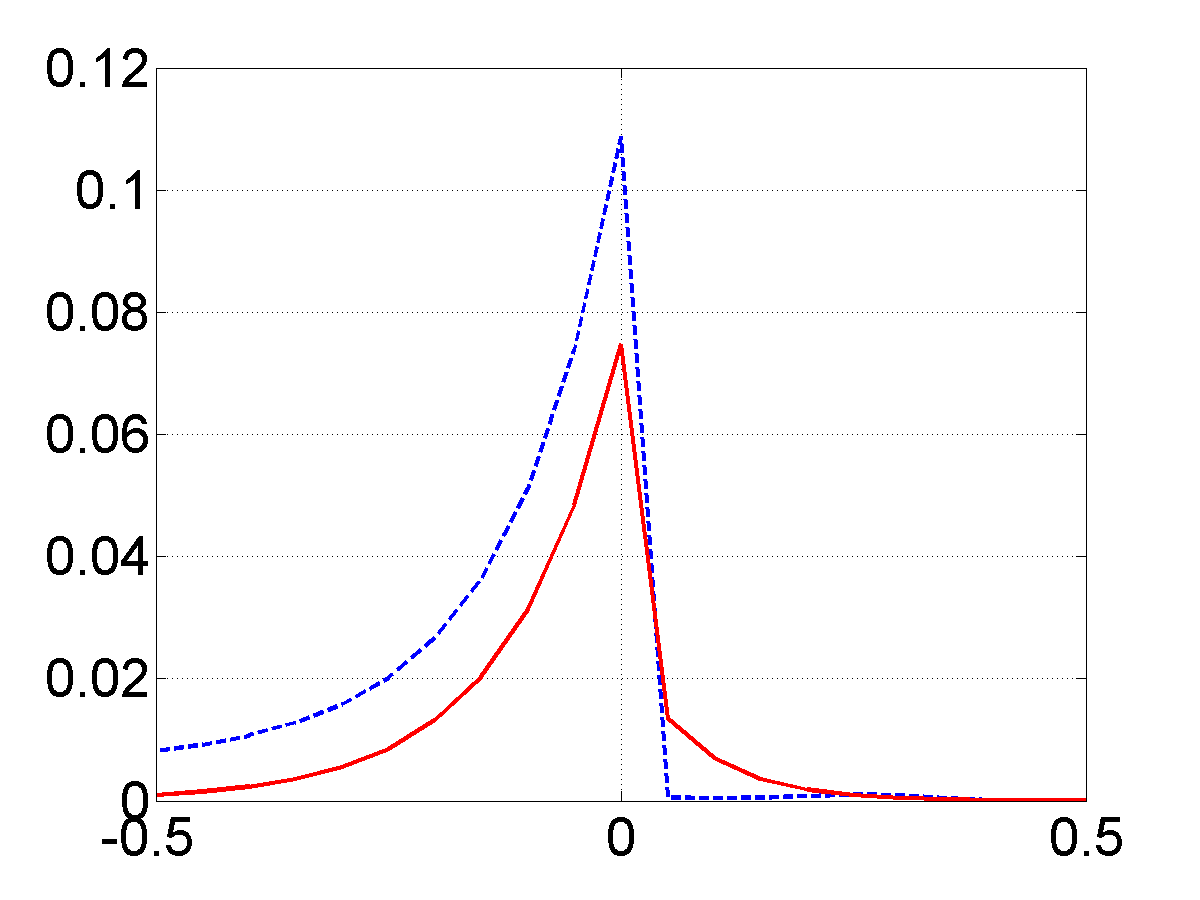

7.2 Calibration of jump-size distribution

Assuming that the local volatility surface is given, the double-exponential tail and the jump-size distribution are calibrated form observed prices. For this example, the same synthetic data and parameters presented in Section 7.1 are used.

Define

Firstly, we calibrate , and then, is reconstructed from , by minimizing the functional:

| (42) |

where is given by

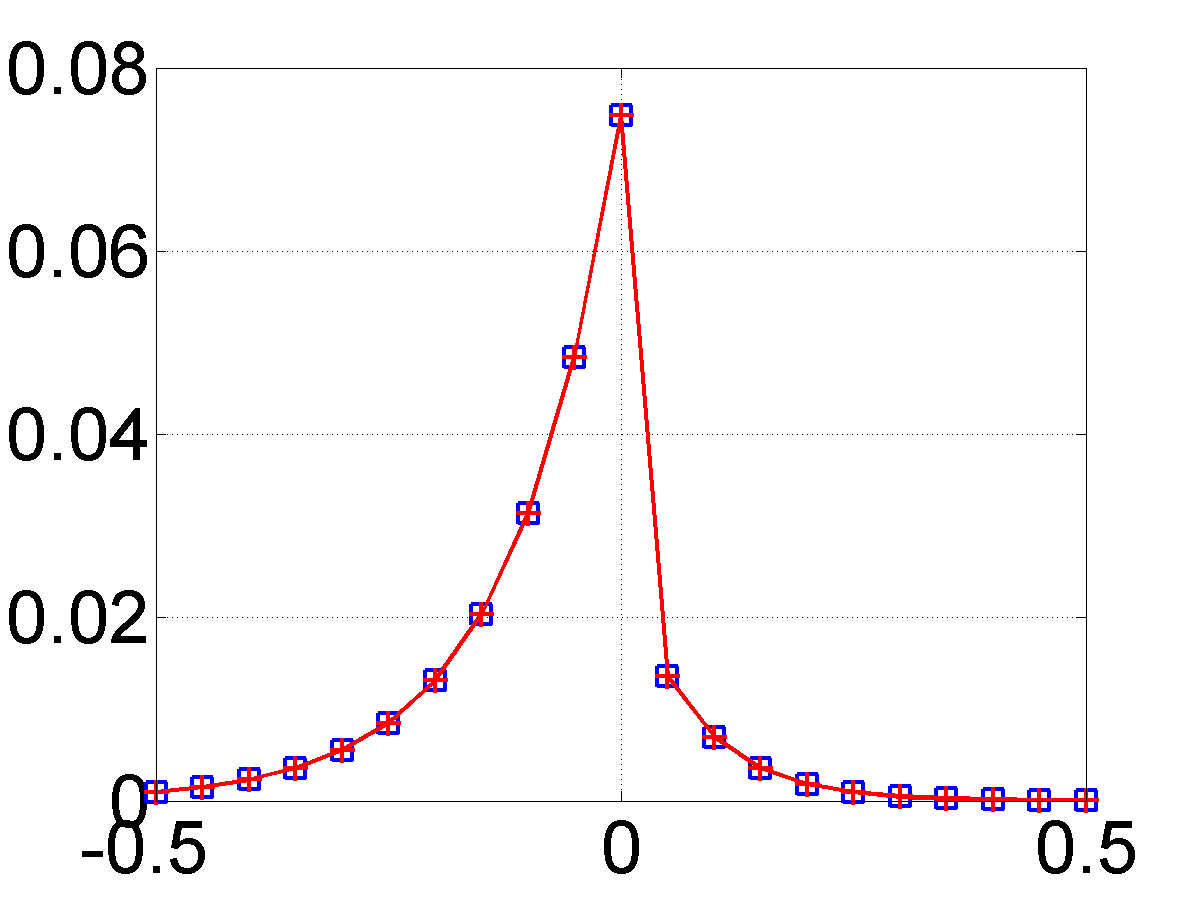

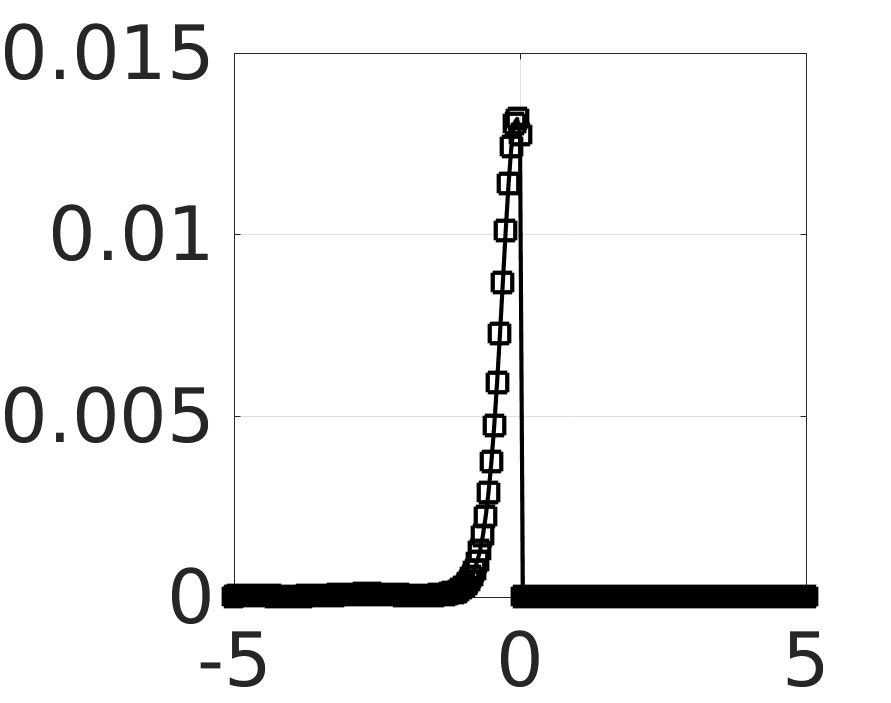

The regularization parameter is set as .

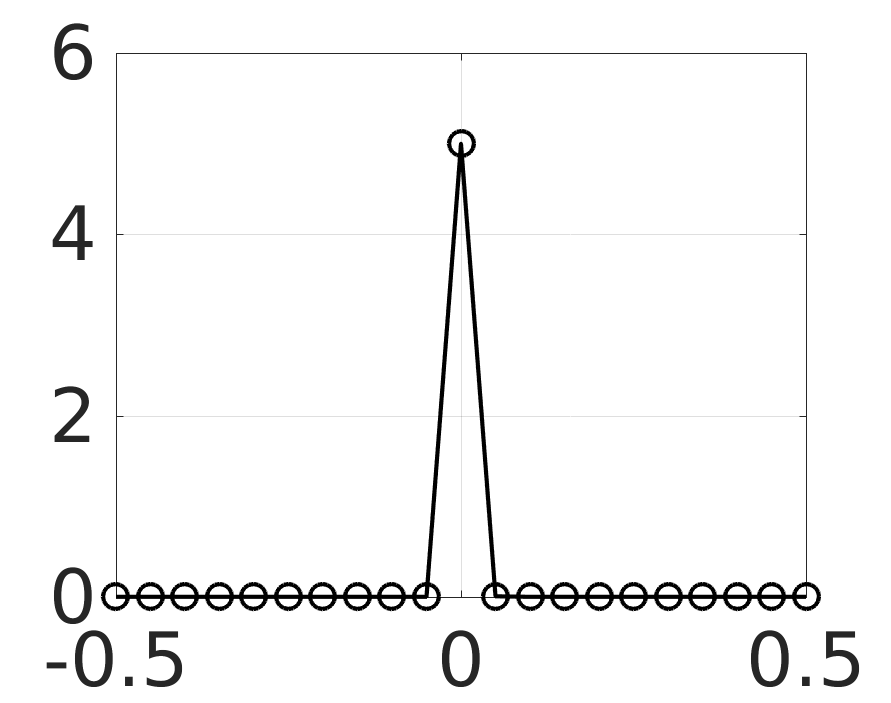

As we can see in Figure 5, the reconstructed double-exponential tail matched the true one. The calibrated jump-size distribution is also adherent to the original one except around zero, probably due to the discontinuity of at zero. The normalized distance between the true and reconstructed double-exponential tail functions was , and the mean and standard deviation of the associated absolute relative error at each node were and , respectively. The normalized -distance between the true and the calibrated jump-size distributions was , and the mean and standard deviation of the associated absolute relative error at each node were and , respectively. If we exclude the points , the values of the normalized distance, the mean and standard deviation become , and , respectively. So, excluding these two points, the calibration was perfect. The normalized residual was . This is probably due to the discontinuity of at zero, which introduces some noise into the reconstruction.

7.3 Testing the Splitting Algorithm

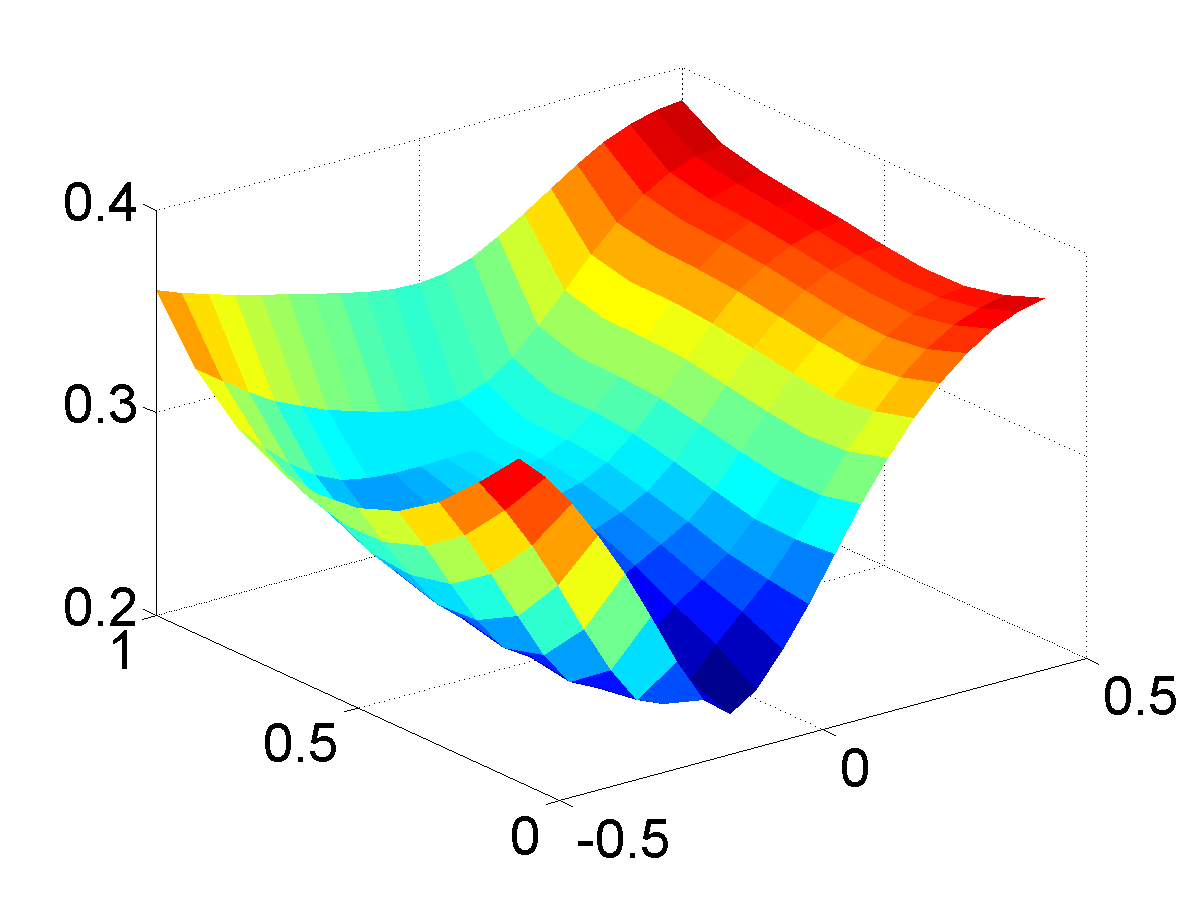

The goal of the present example is to illustrate that the splitting algorithm is able to calibrate simultaneously the local volatility function and the double exponential tail.

The call prices are given at the nodes , with and . This represents of the mesh where the direct problem is solved. The algorithm was initialized with the minimization of the Tikhonov functional w.r.t. the volatility parameter. The initial states of the local volatility surface and double exponential tail, as well as and in the penalty functional, were set as and

respectively. Here, is the characteristic or indicator function of the set .

The minimization w.r.t. the local volatility surface was performed as in Section 7.1. However, to proceed with the minimization w.r.t. the double exponential tail, firstly, we made the change of variable and considered the decomposition . Since the -domain now is bounded, and can be expressed in terms of Fourier series. So, we truncate its series at the third term and minimize the Tikhonov functional w.r.t. the Fourier coefficients.

In this example the Kullback-Leibler divergence in the definition of the penalty functional in Section 5.1 was replaced by the square of -norm.

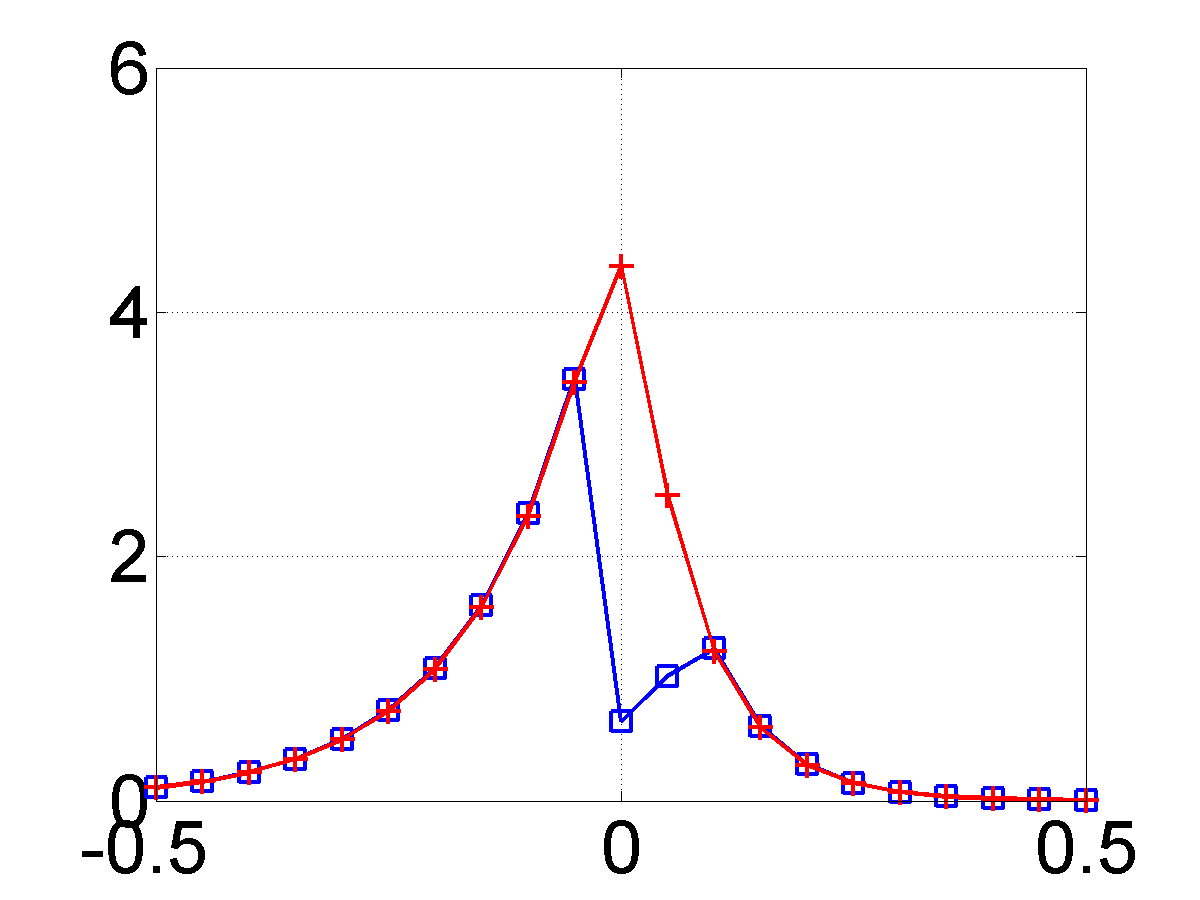

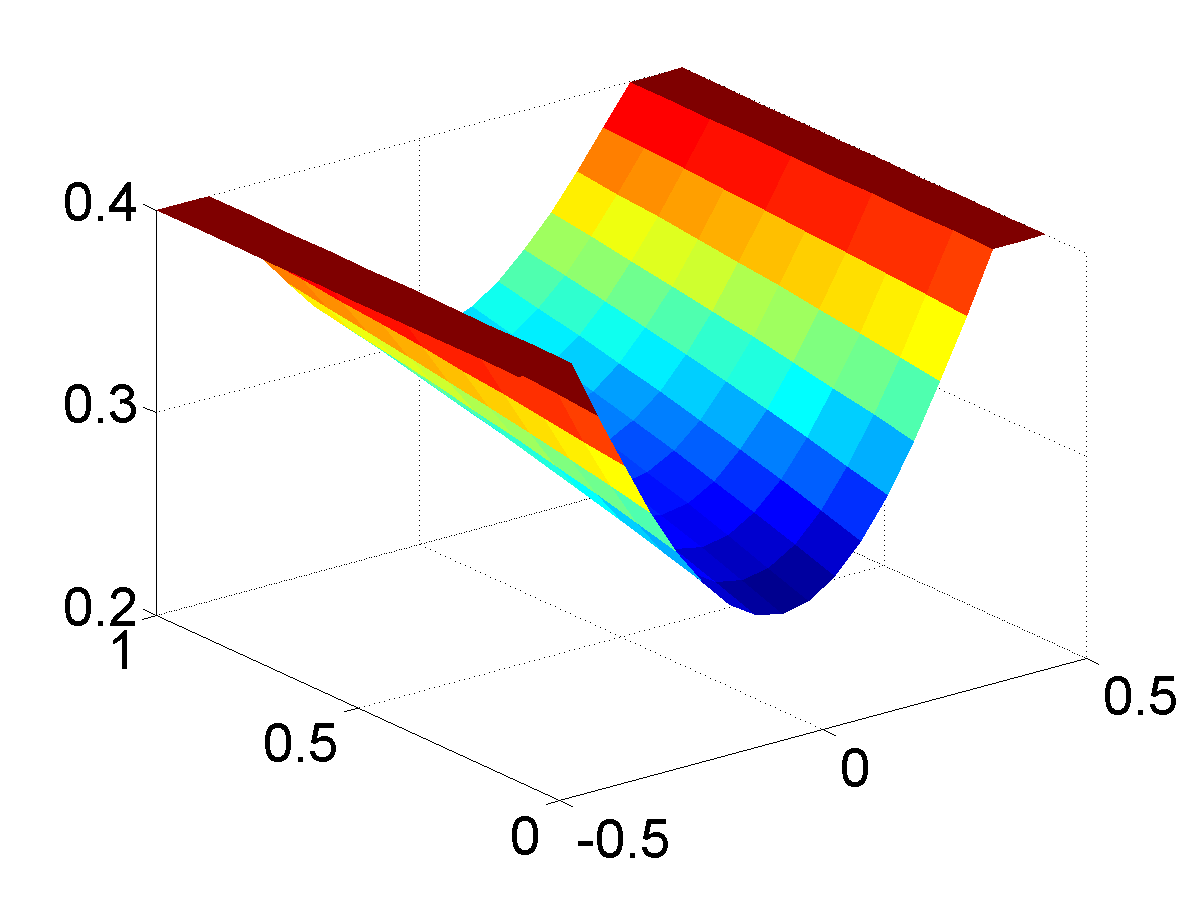

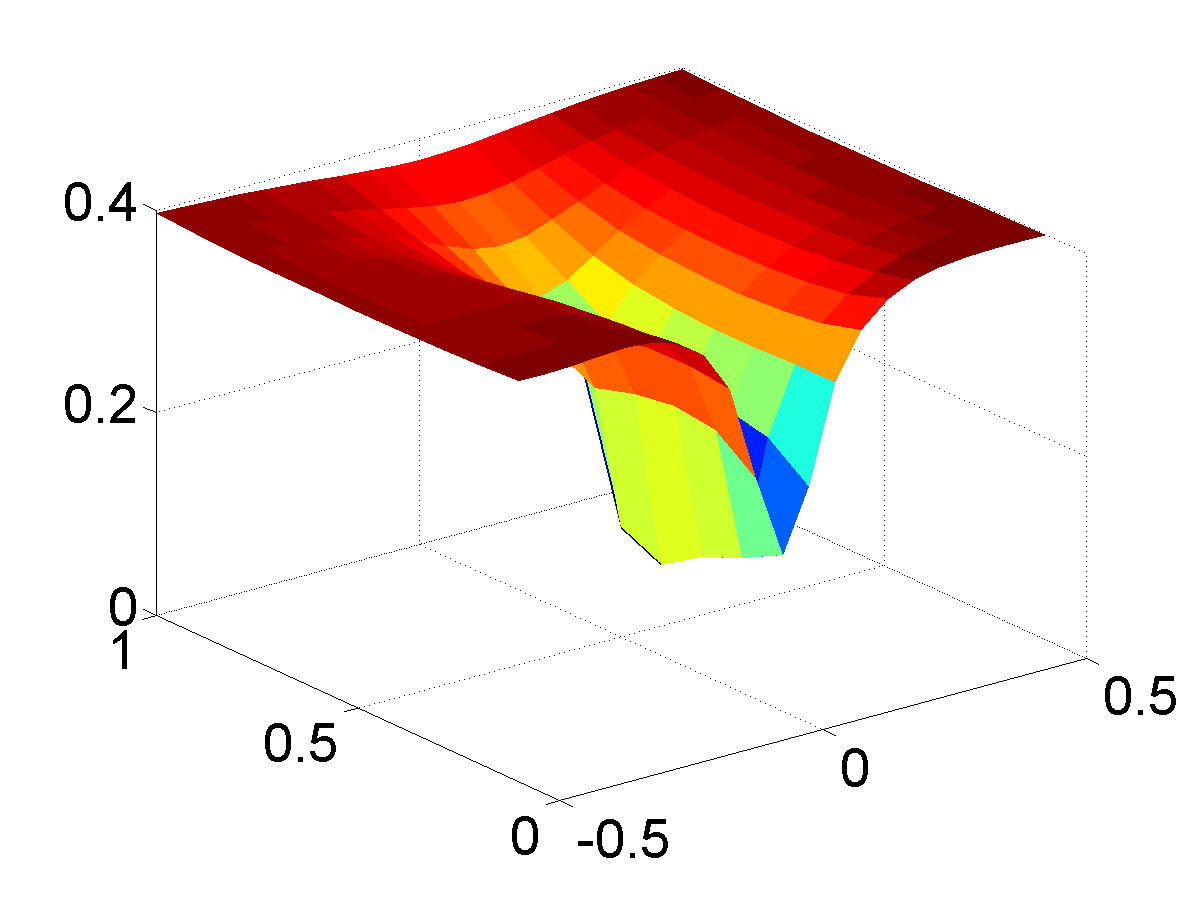

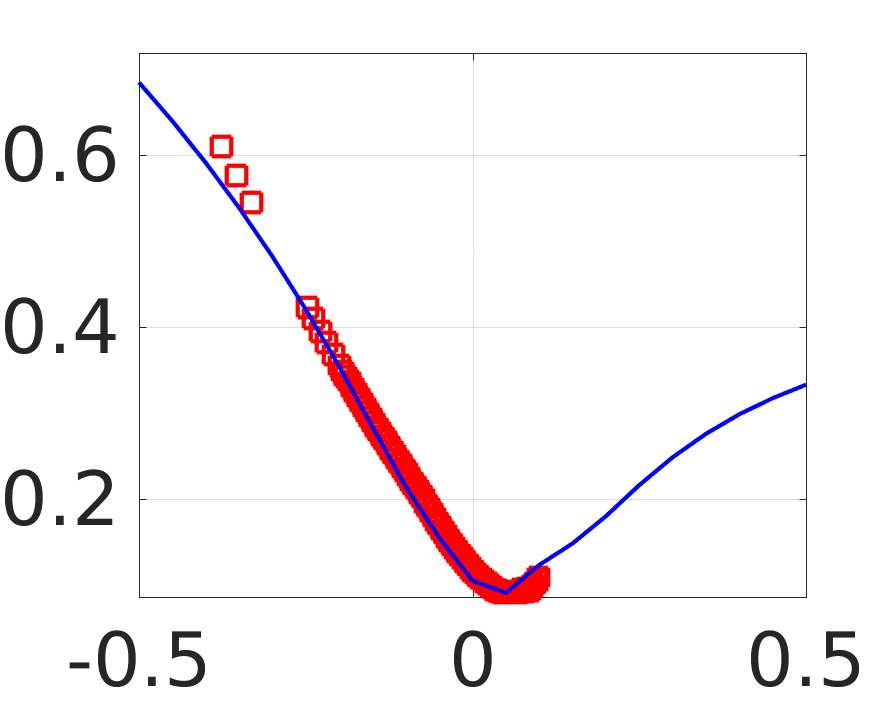

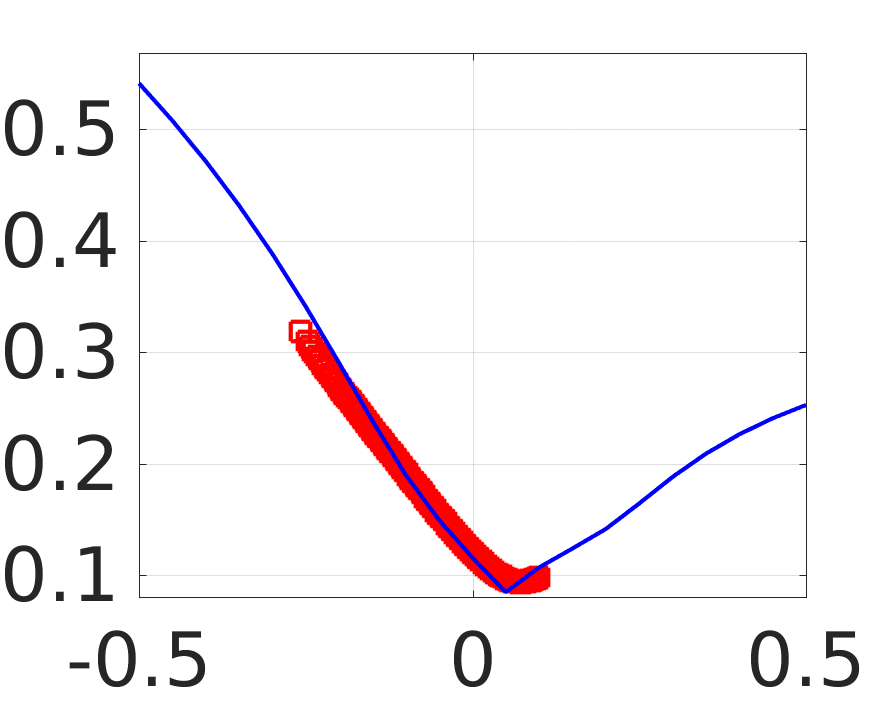

After two steps of the splitting algorithm, the normalized -residual was , below the tolerance which was set as . The normalized -distances between the reconstructed and true parameters were, for the local volatility surface and for the double exponential tail.

Figure 6 presents the true and the reconstructed local volatility surfaces at the first and second steps of the splitting algorithm. The comparison between the double-exponential tails is done in Figure 7.

If the reconstructions of each parameter are analyzed separately, it seems that the results were not as accurate as in the previous examples. However, this was expected since the amount of unknowns in this test is much larger than before. In addition, it is well known that the distribution of small jump-sizes and volatility are closely related. See Cont and Tankov (2003). This means that in simultaneous reconstructions, it is difficult to separate one from another. So, based on such observations, the results were satisfactorily accurate, since the main features of both parameters were incorporated by the reconstructions, as illustrated in Figures 6-7.

7.4 Pricing Exotic Options

To provide another illustration of the accuracy of the splitting algorithm, we evaluate the so-called Lookback call and put options, which have the following payoff functions:

respectively, where the time-to-maturity of the options are , the current time is given by , with , , and is the number of time steps, set to .

The price of the options are approximated by a Monte Carlo integration as in

where is the -th realization of the random variable , and is the total amount of realizations, which is set to . The realizations of and are generated by Dupire model and the jump-diffusion model in (1).

The Dupire model is solved by Euler-Naruyama method with local volatility calibrated from the European call price dataset of Section 7.3. The normalized residual in local volatility calibration is approximately the same achieved by the jump-diffusion calibration in Section 7.3. The jump-diffusion model is solved by the method in Giesecke et al. (2017) with the local volatility and the jump-size distribution calibrated in Section 7.3. The samples of the jump-sizes are given by inverse transform sampling, where the inverse of the cumulative distribution of jump-sizes was evaluated by least-squares. The ground truth prices are given by jump-diffusion model with the true local volatility and true jump-size distribution of Section 7.3.

| Jumps | ||||

|---|---|---|---|---|

| Dupire | ||||

| True |

| Jumps | ||||

|---|---|---|---|---|

| Dupire | ||||

| True |

| Jumps | ||||

|---|---|---|---|---|

| Dupire |

| Jumps | ||||

|---|---|---|---|---|

| Dupire |

Tables 2 and 3 present the prices of the lookback call and put options, respectively. The error in the prices can be found in Tables 4 and 5. In these tables, the word Jumps stands for jump-diffusion model, whereas the word Dupire stands for Dupire model and True stands for the ground truth prices. Based on these results, we can see that the jump-diffusion model with parameters calibrated by the splitting algorithm is more precise than the Dupire model with calibrated local volatility.

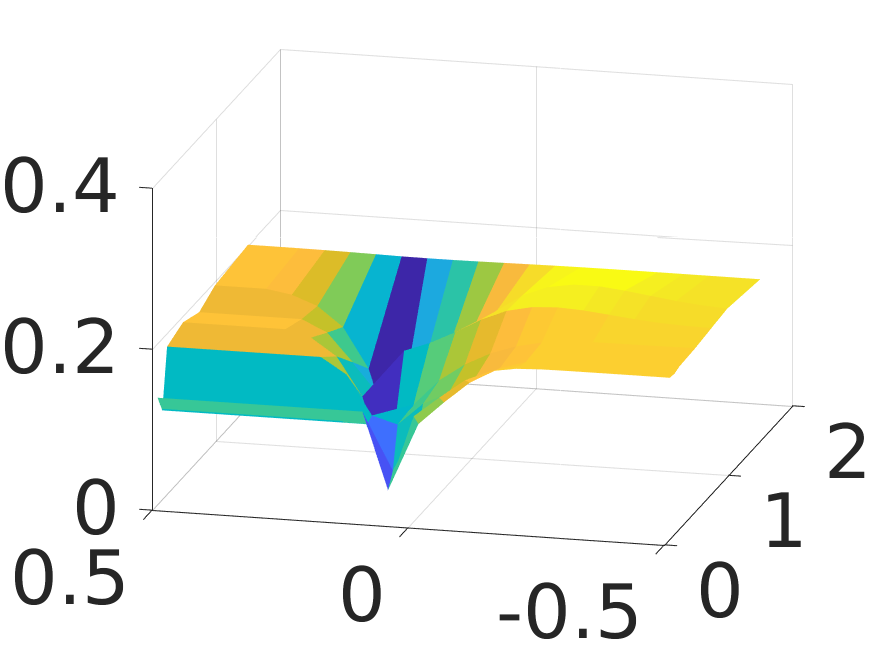

7.5 The Splitting Algorithm with DAX Options

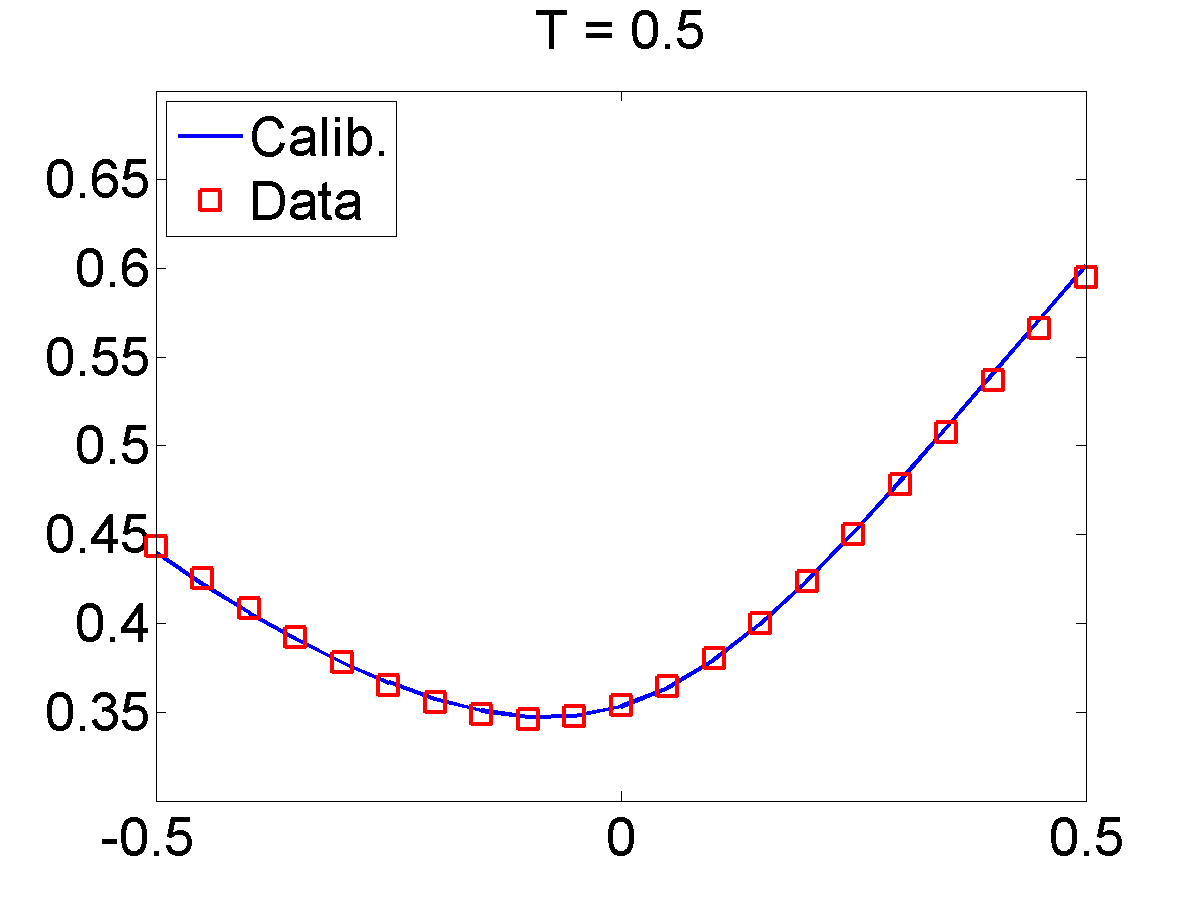

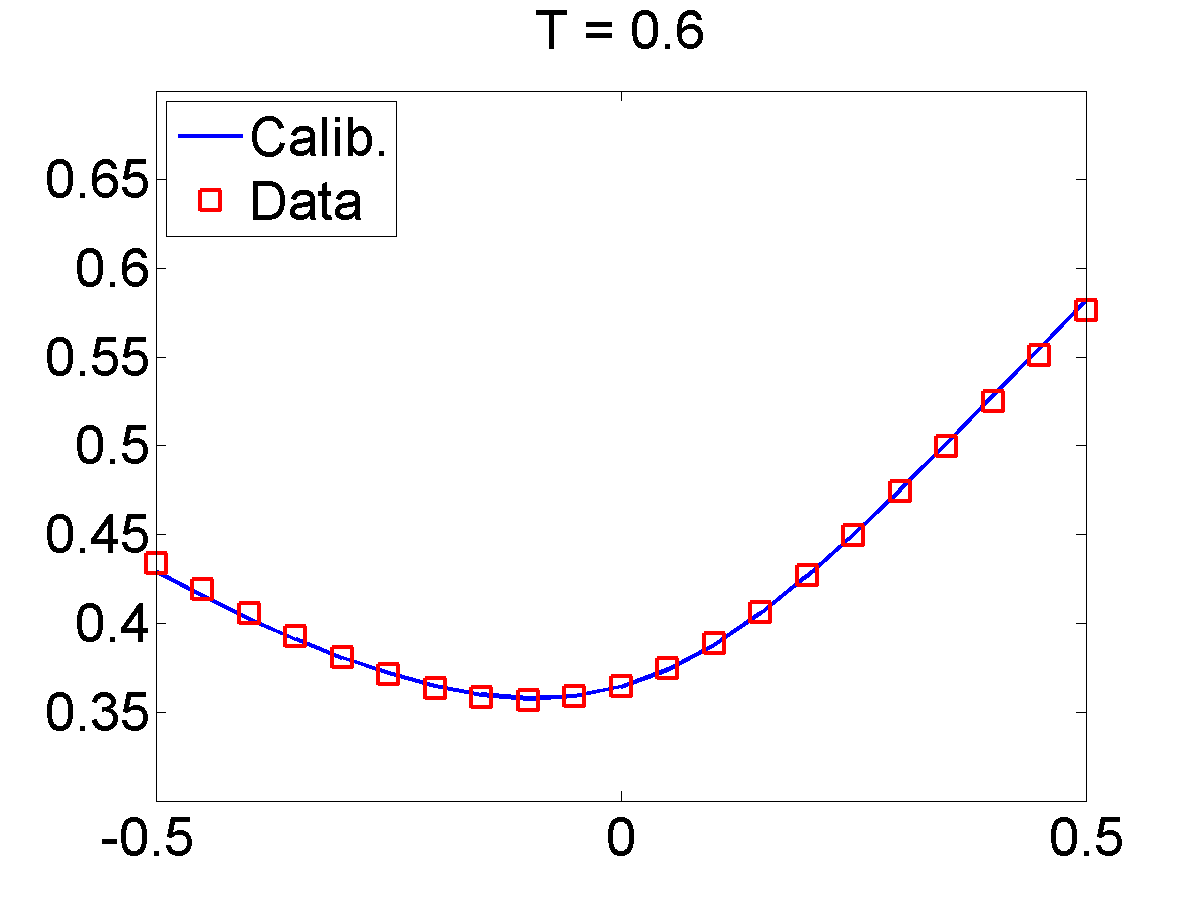

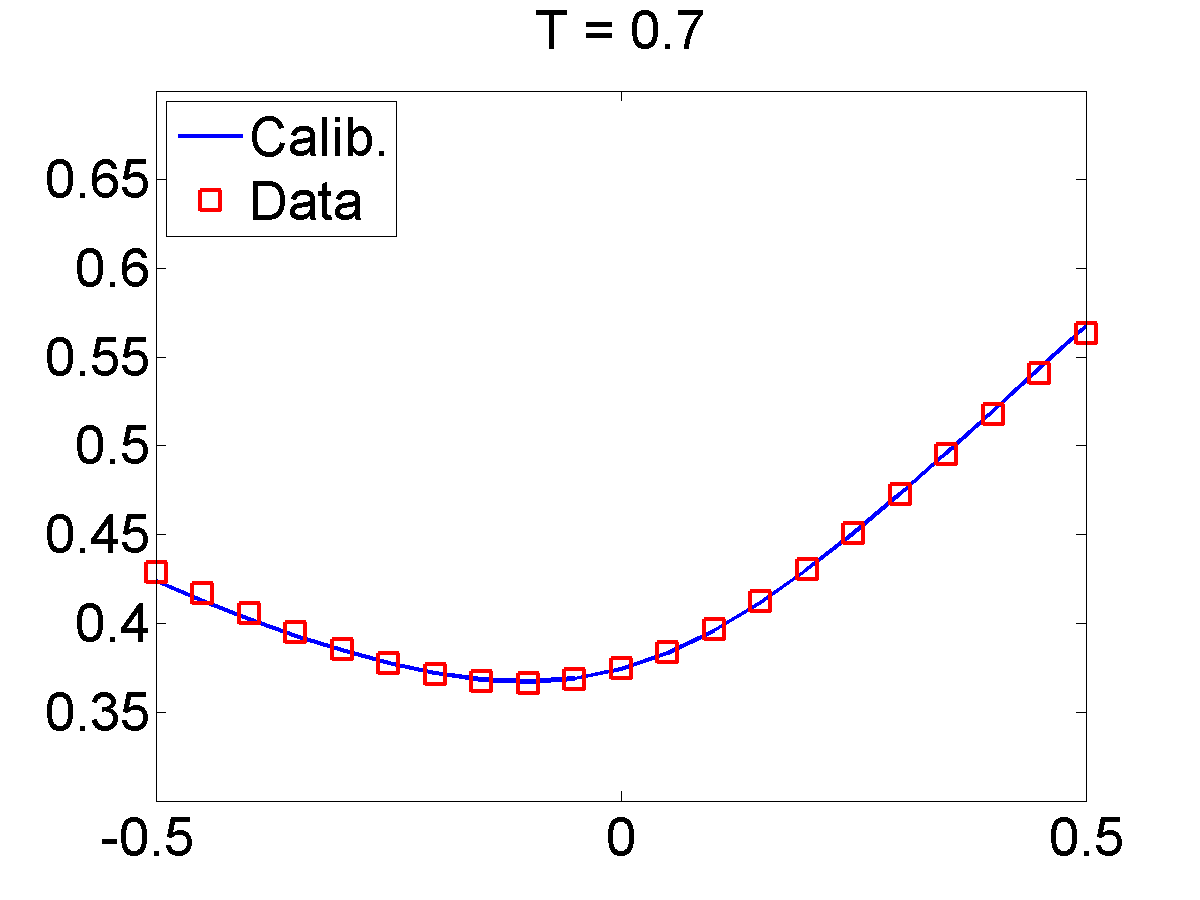

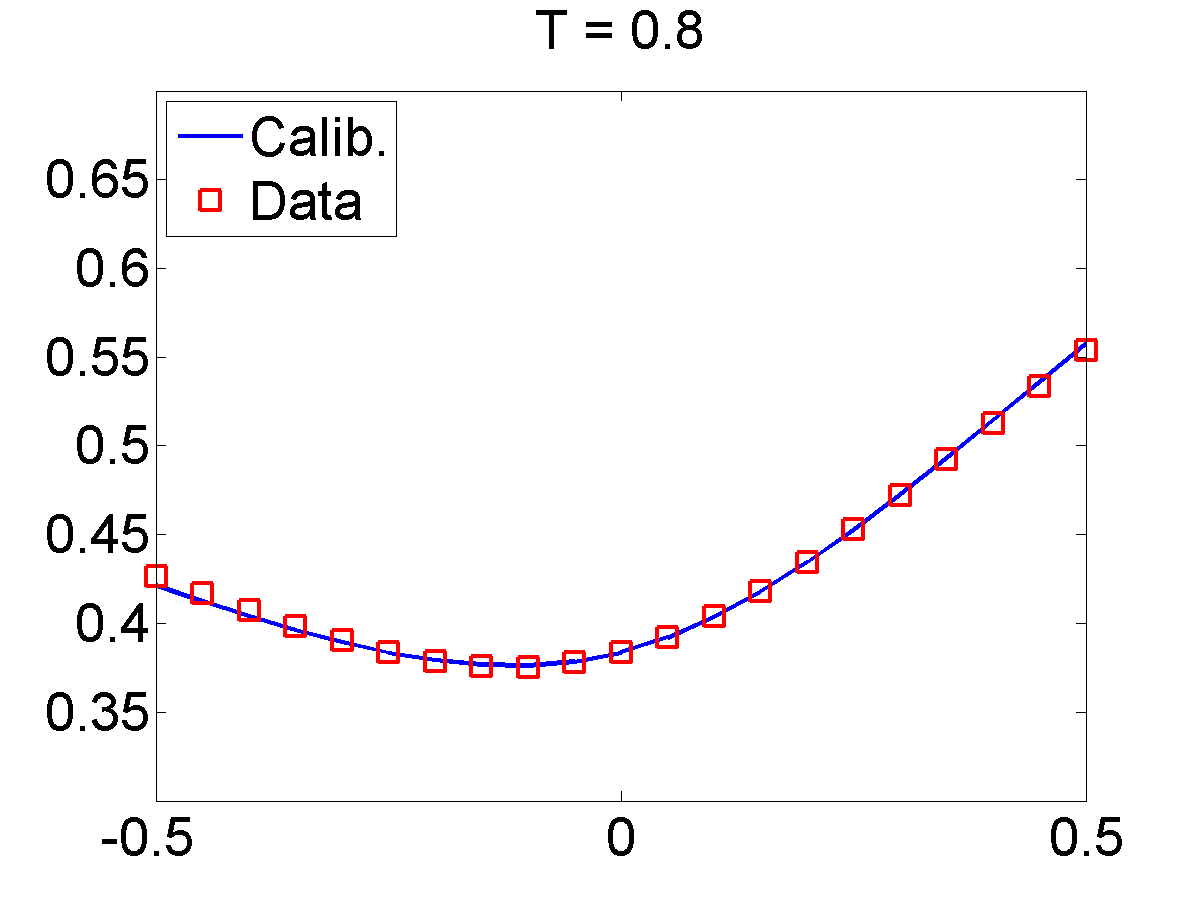

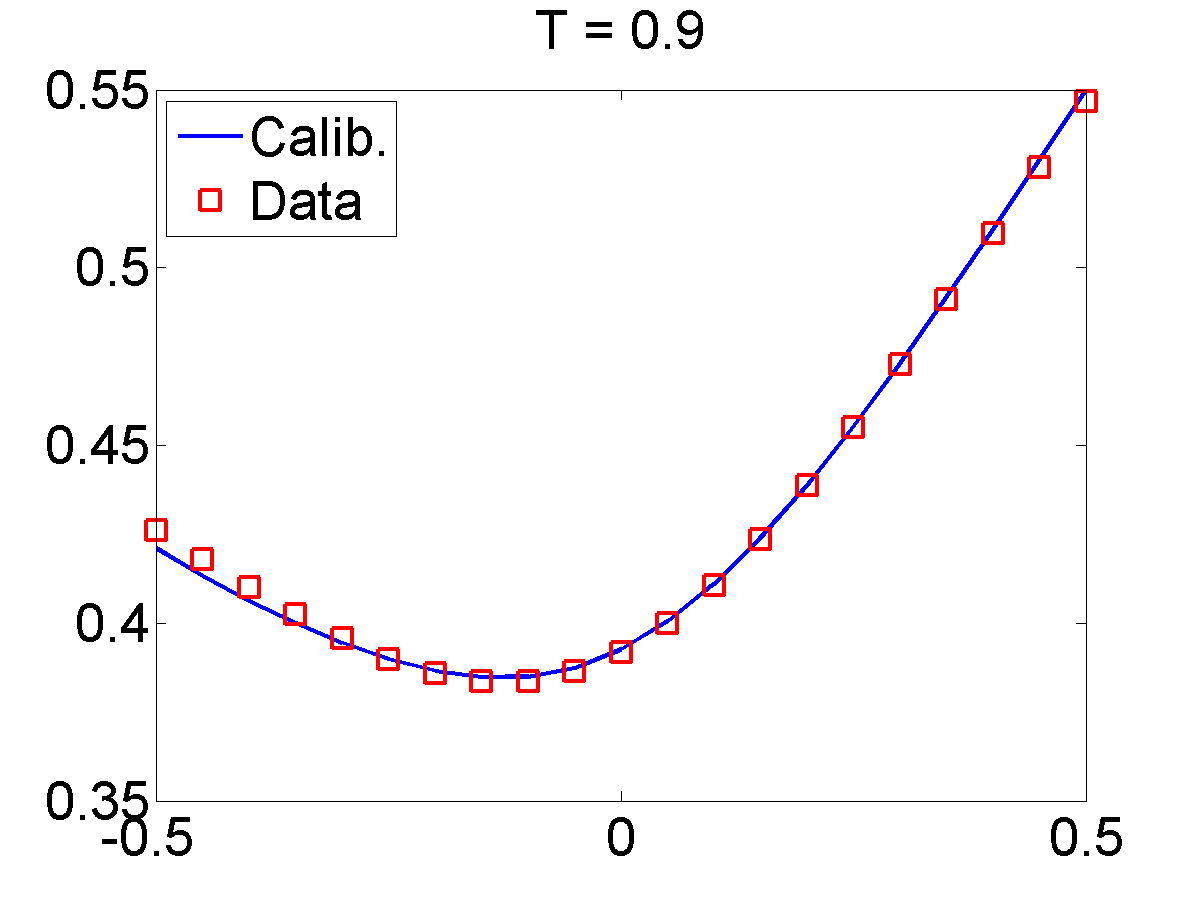

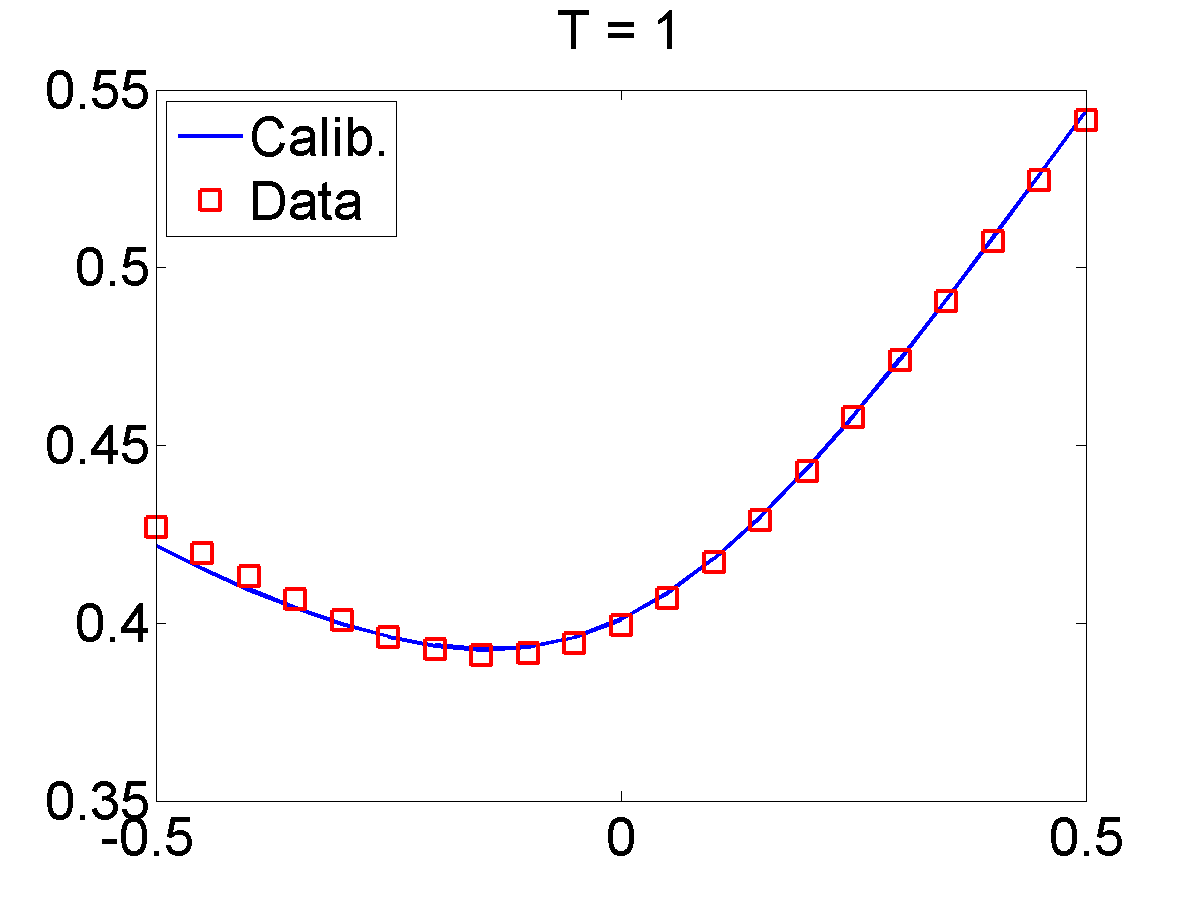

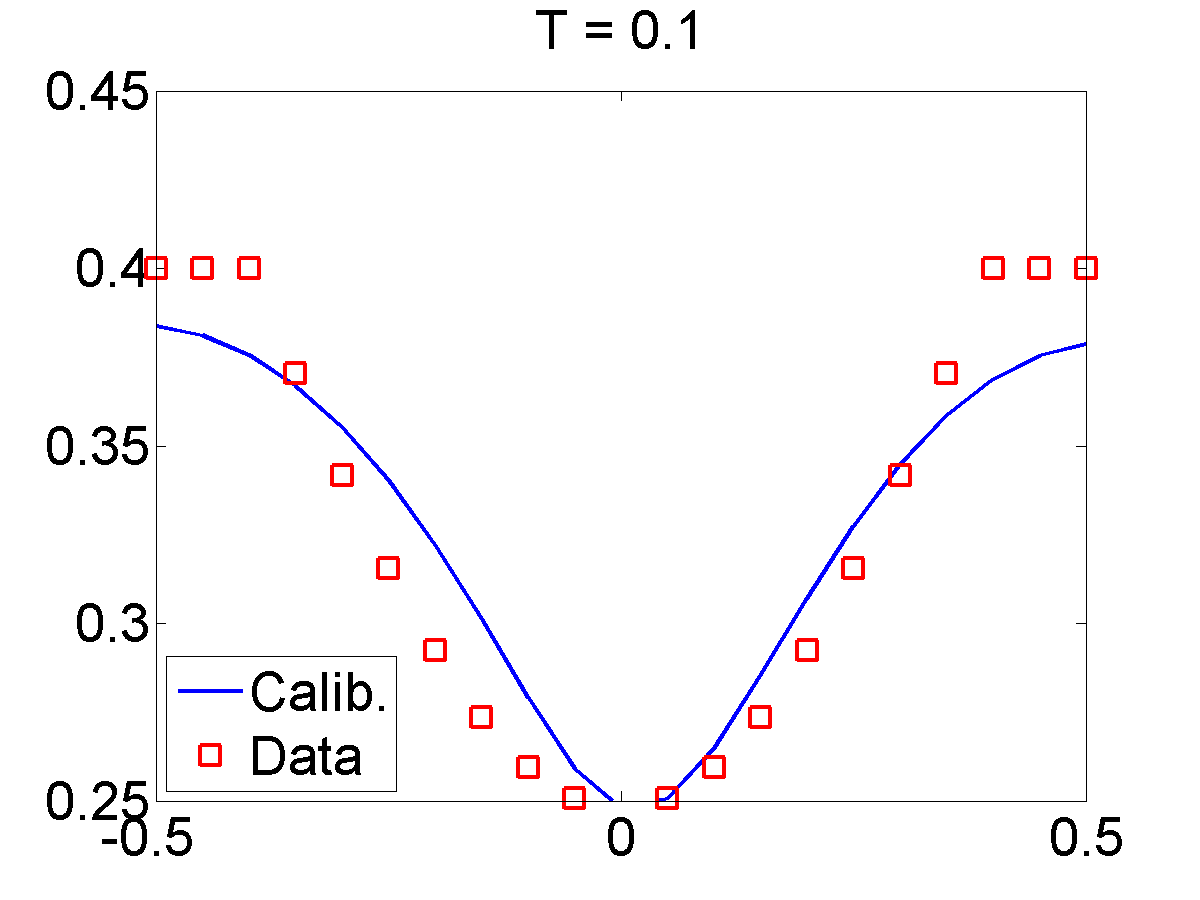

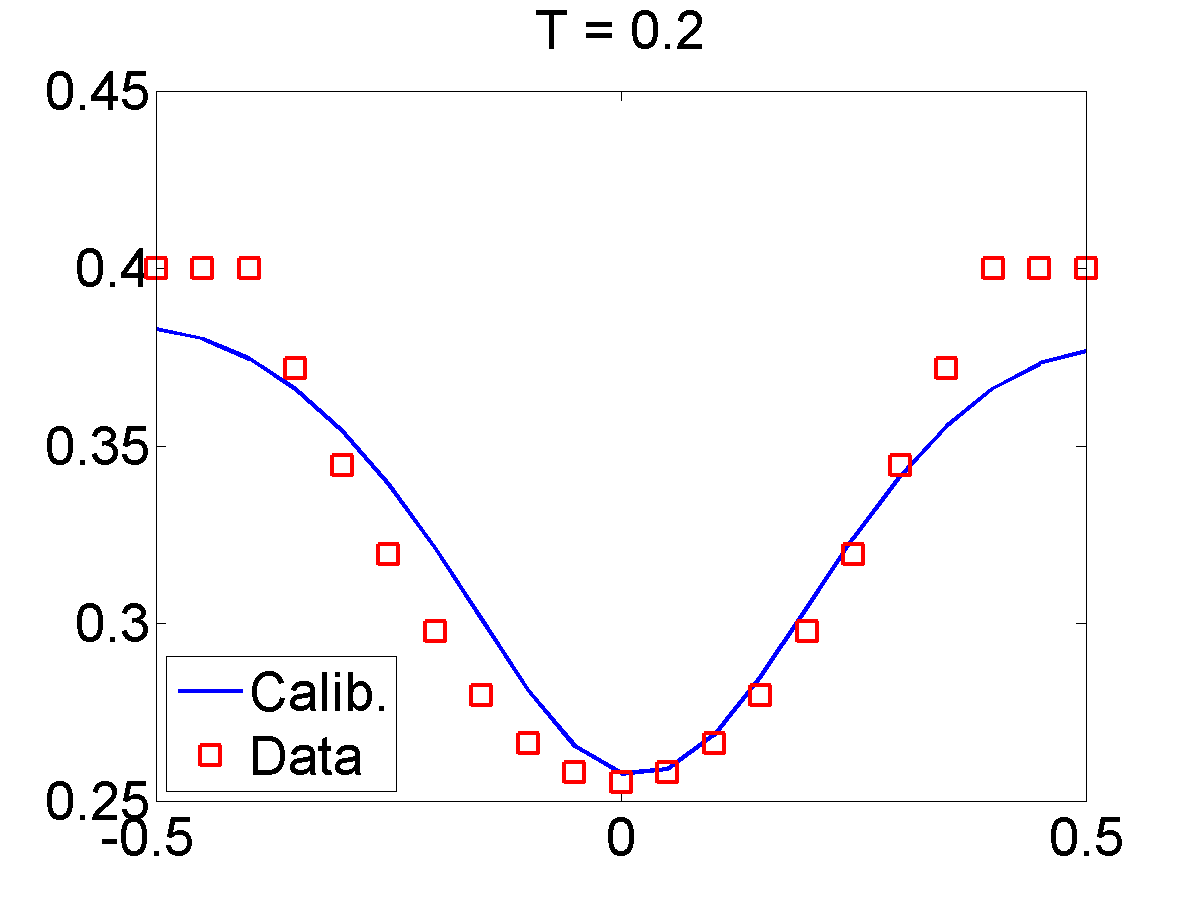

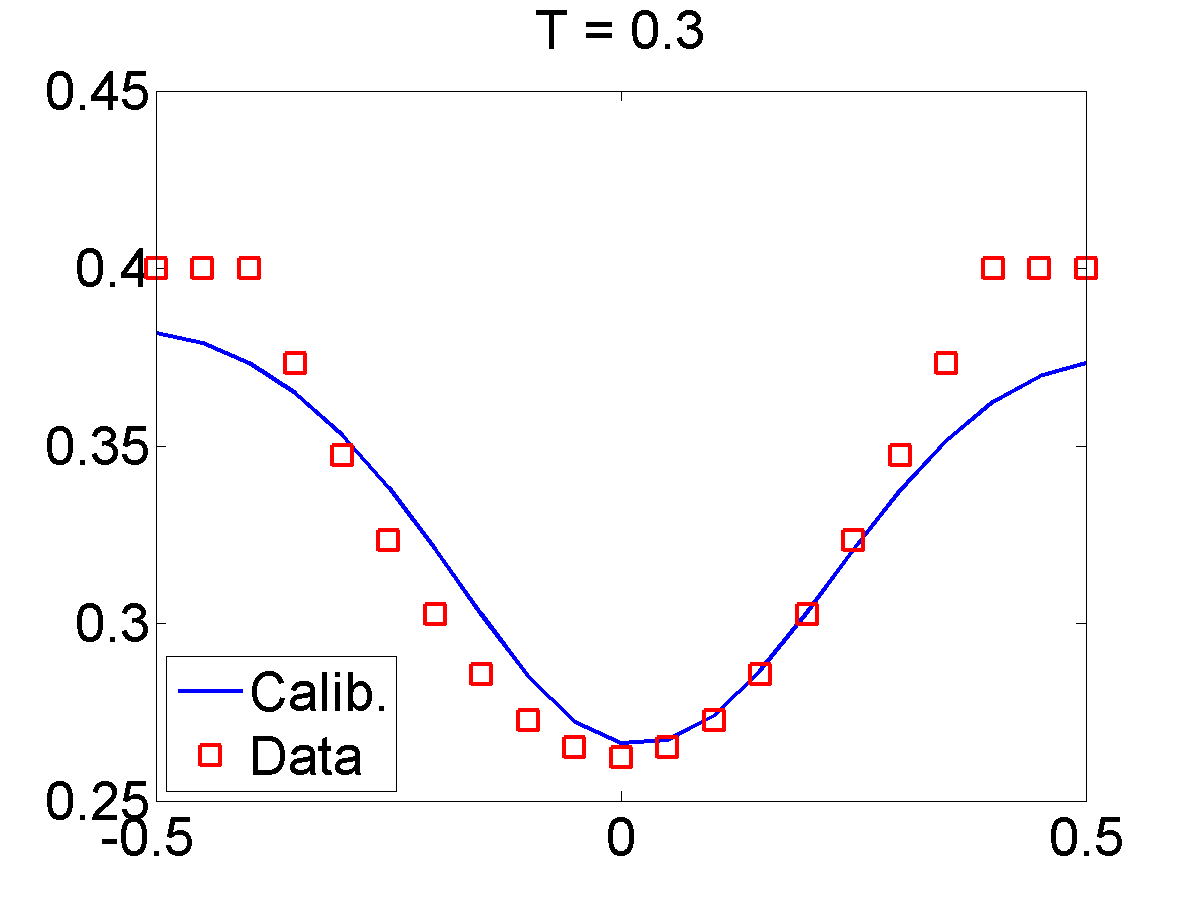

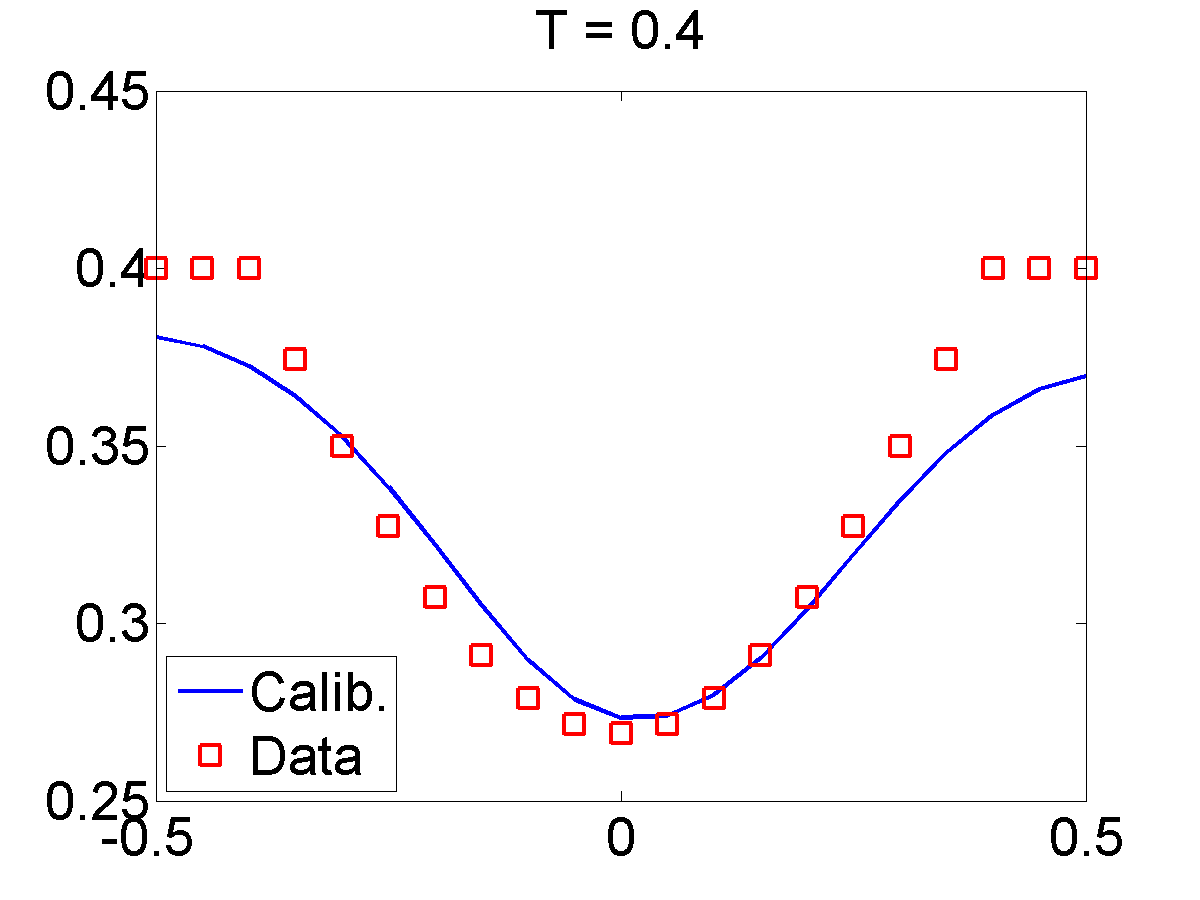

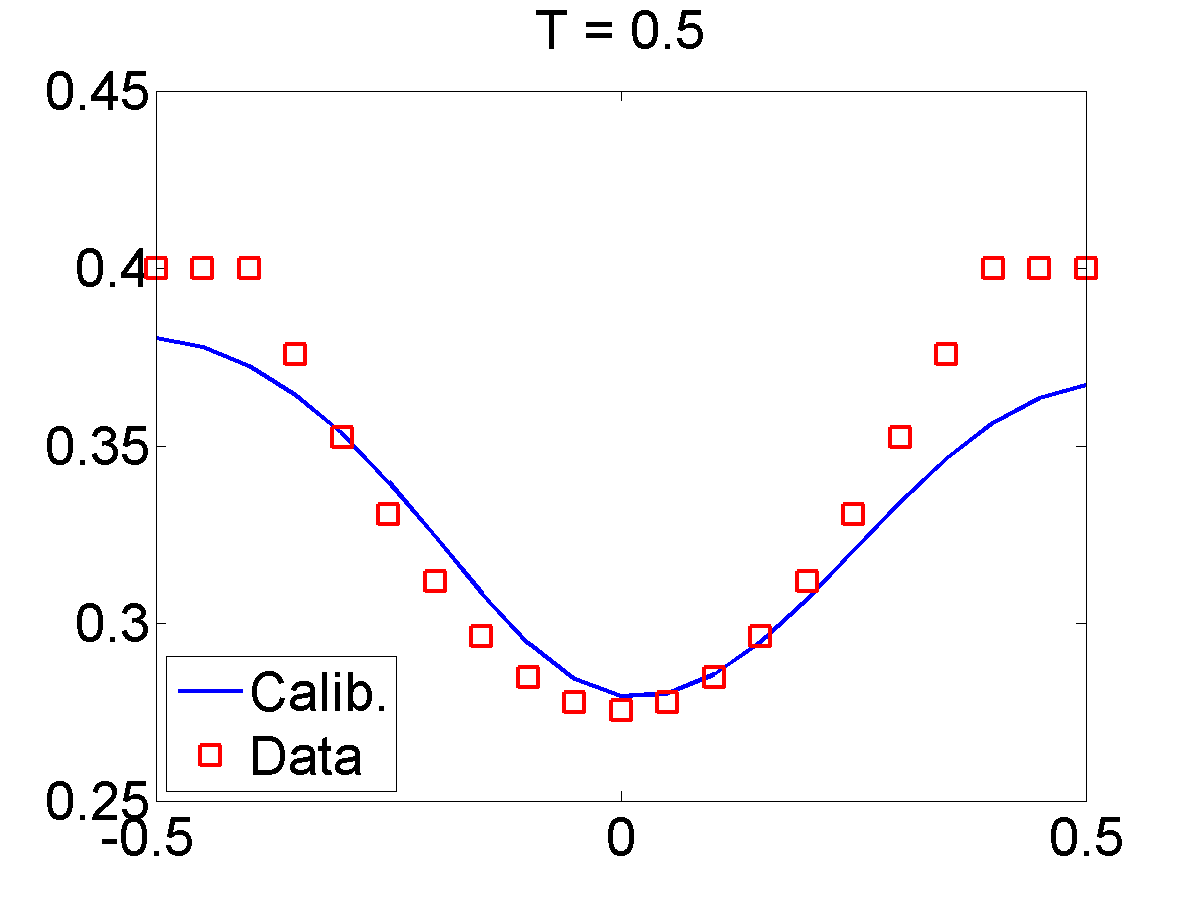

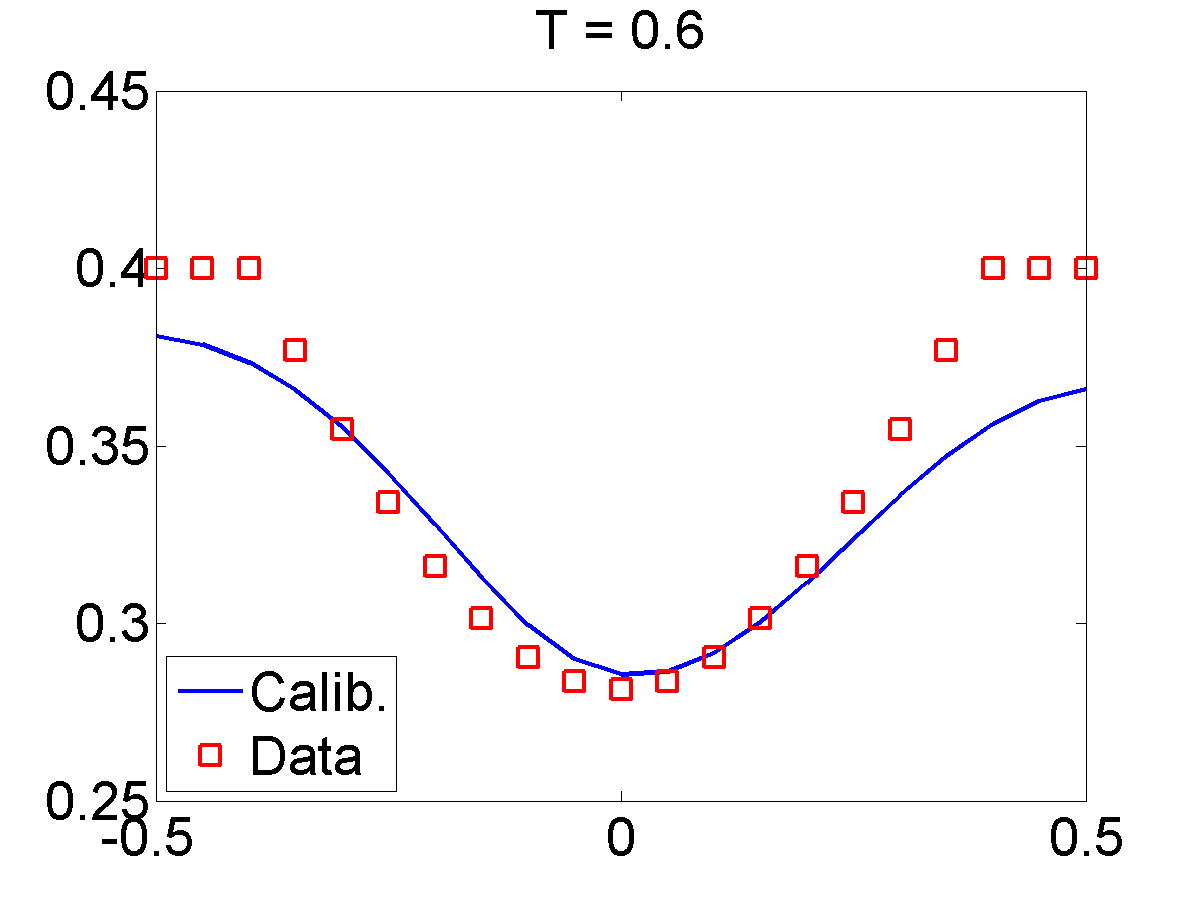

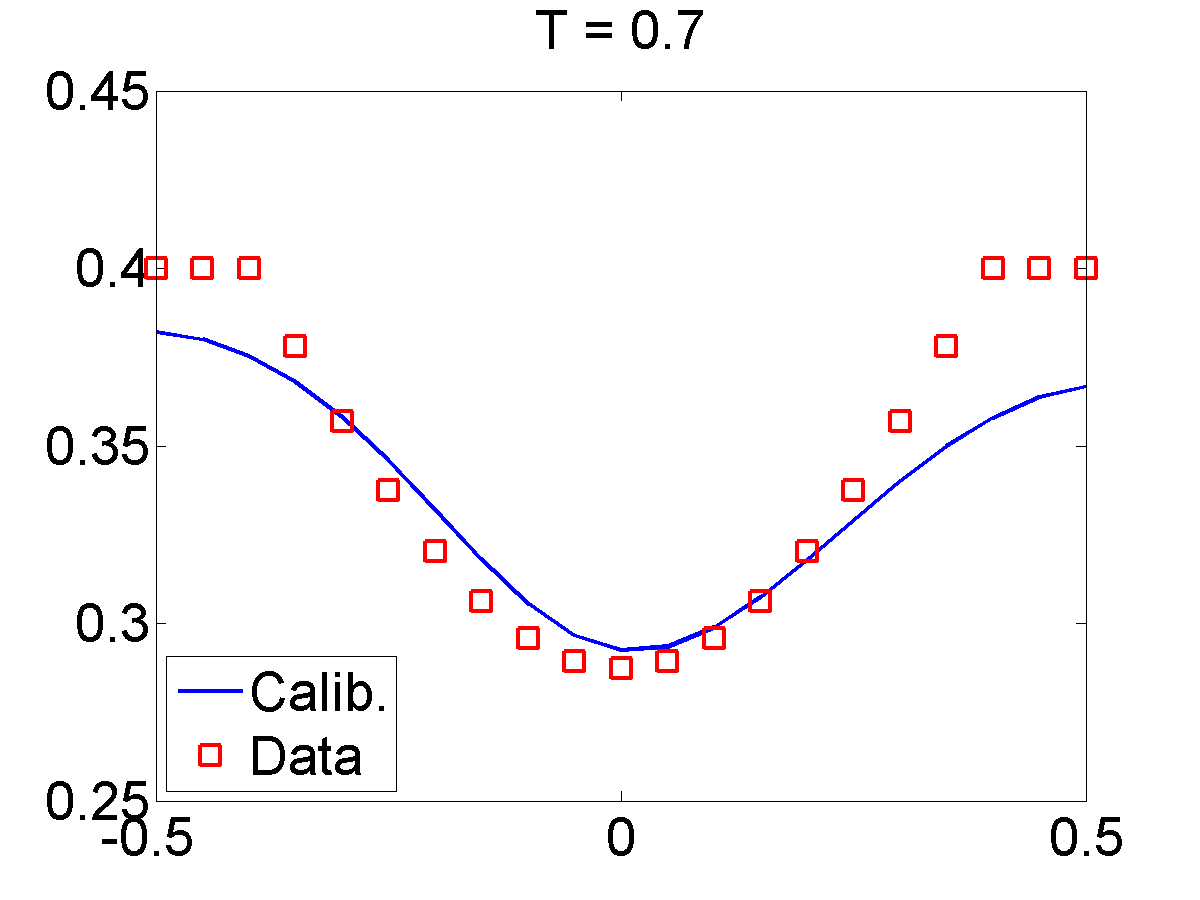

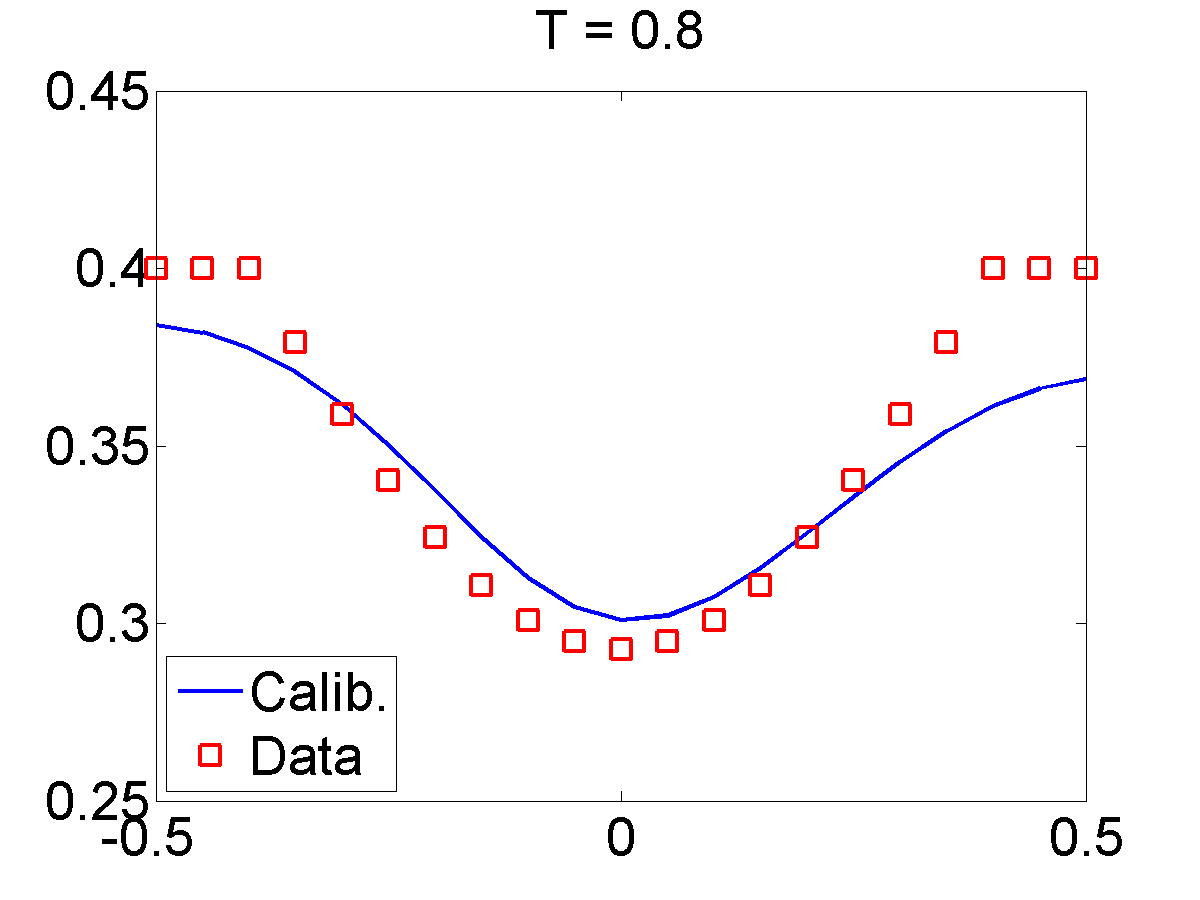

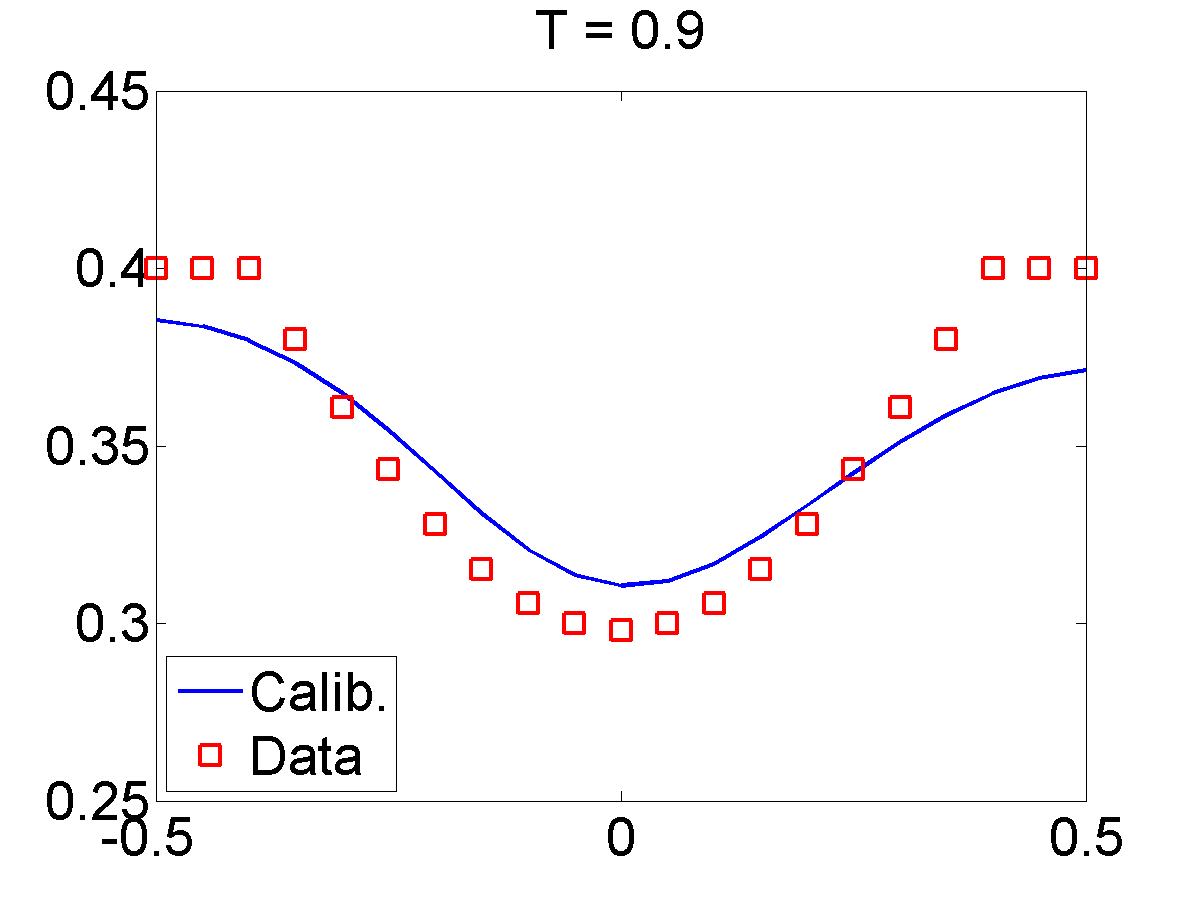

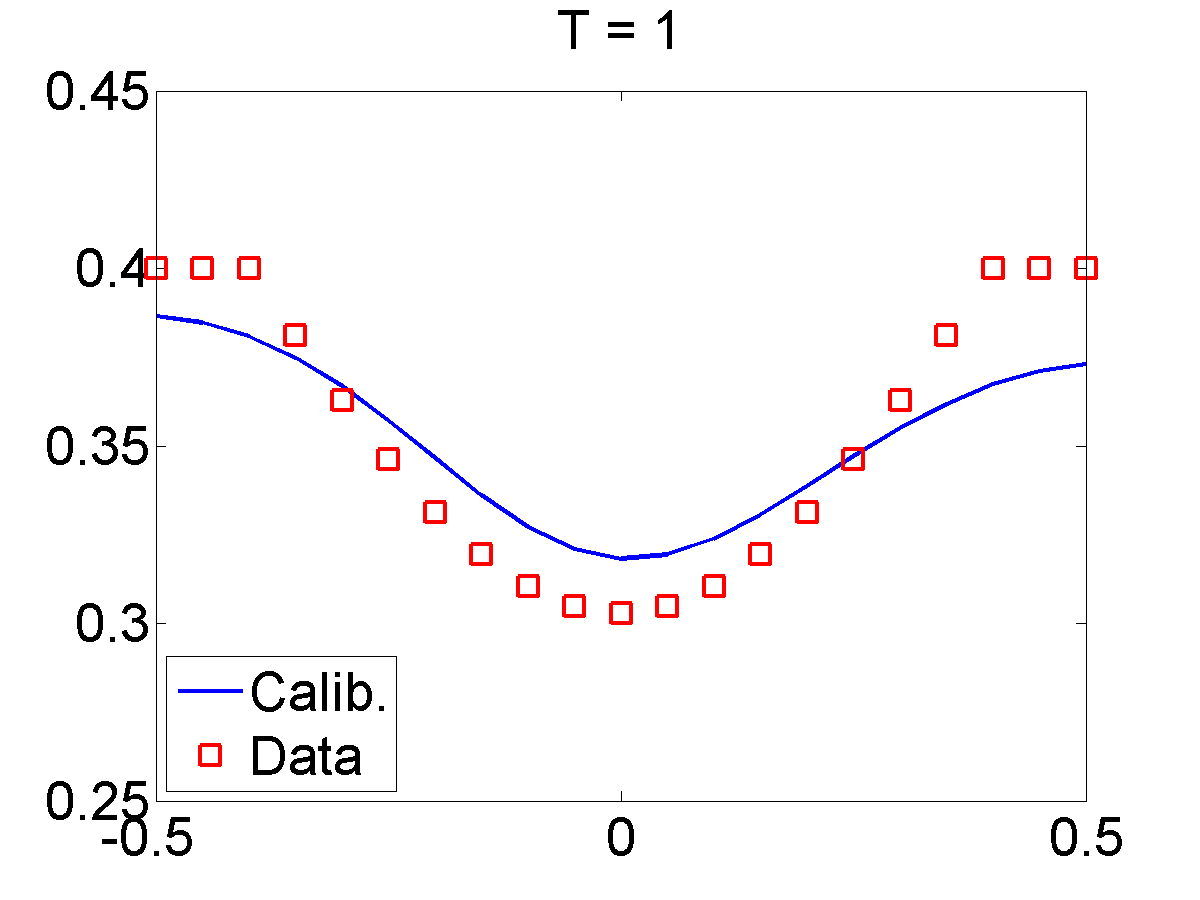

This experiment is aimed to illustrate that the splitting algorithm can be used with market data. The tests are performed with end-of-the-day DAX European call prices traded on 20-Jun-2017, and maturing on 21-Jun-2017, 18-Aug-2017, 15-Sep-2017, 15-Dec-2017, and 16-Mar-2018.

The mesh step lengths used here were and . The penalty term of the Tikhonov functional was the same used in Section 7.3, with . We used the same initial states for the local volatility surface and double exponential, as well as, the a priori parameters of Section 7.3. The interest rate was taken as 0, and USD. The data was given in the sparse mesh defined by transforming the market strikes into log-moneyness, and considering the time to maturity in years. Only three iterations of the splitting algorithm were needed until the data misfit function was below the tolerance, set as .

To reconstruct the jump-size distribution and the local volatility surface, we used the same parameters of Section 7.3.

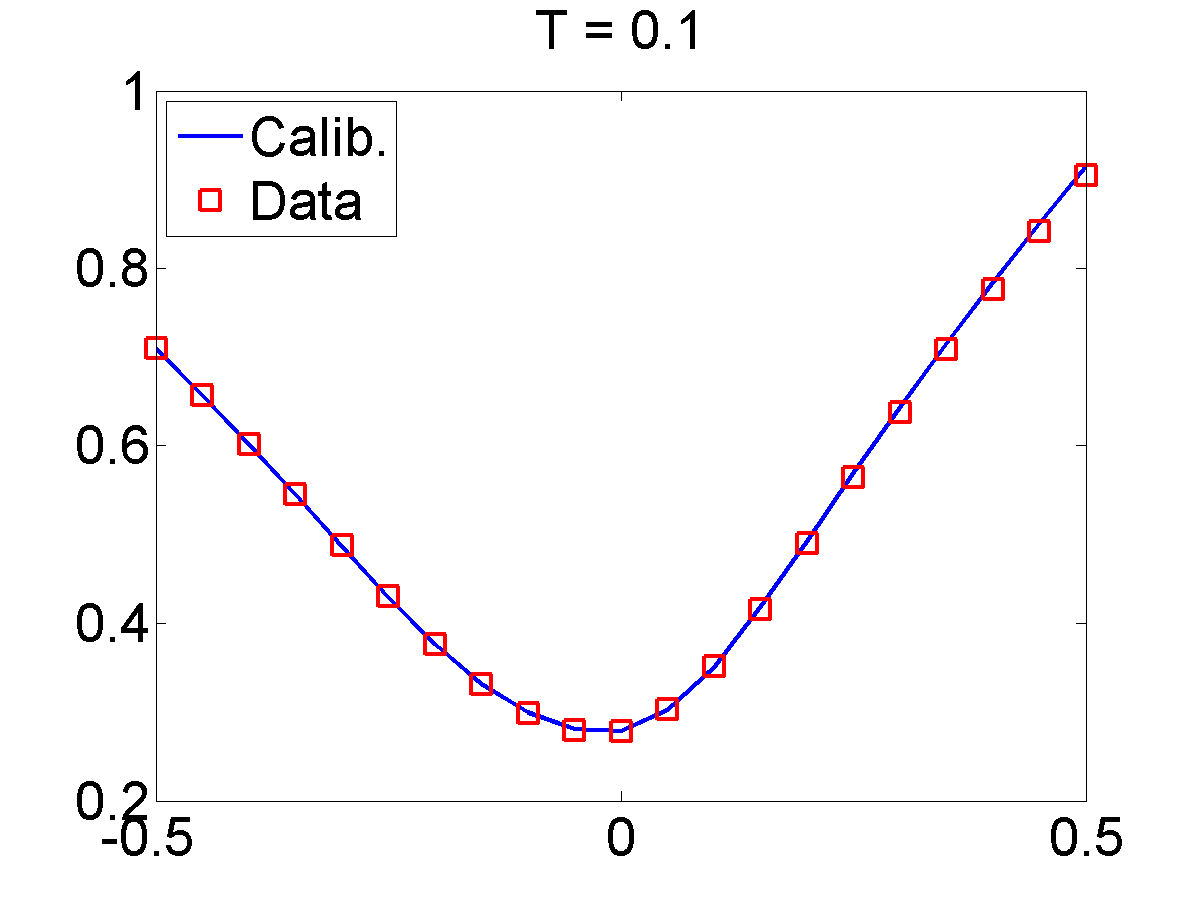

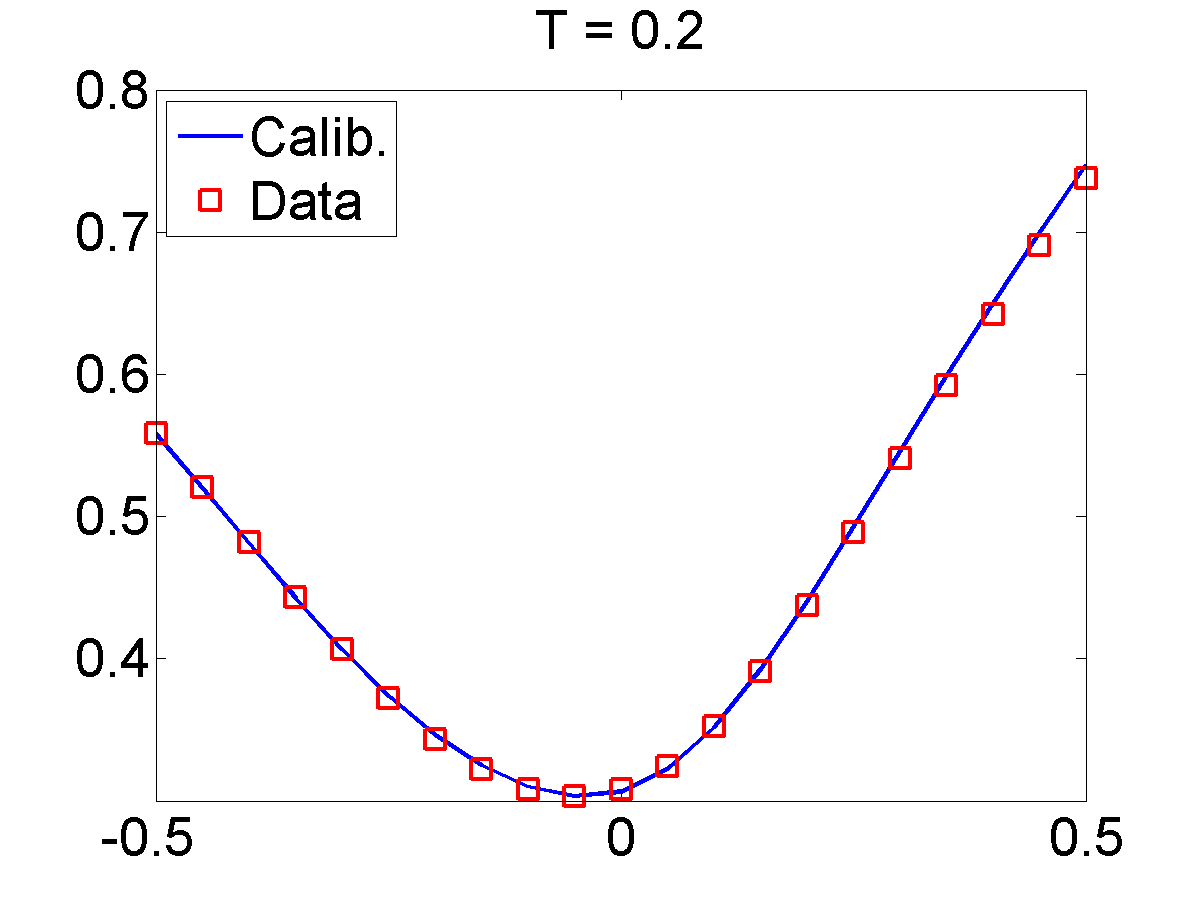

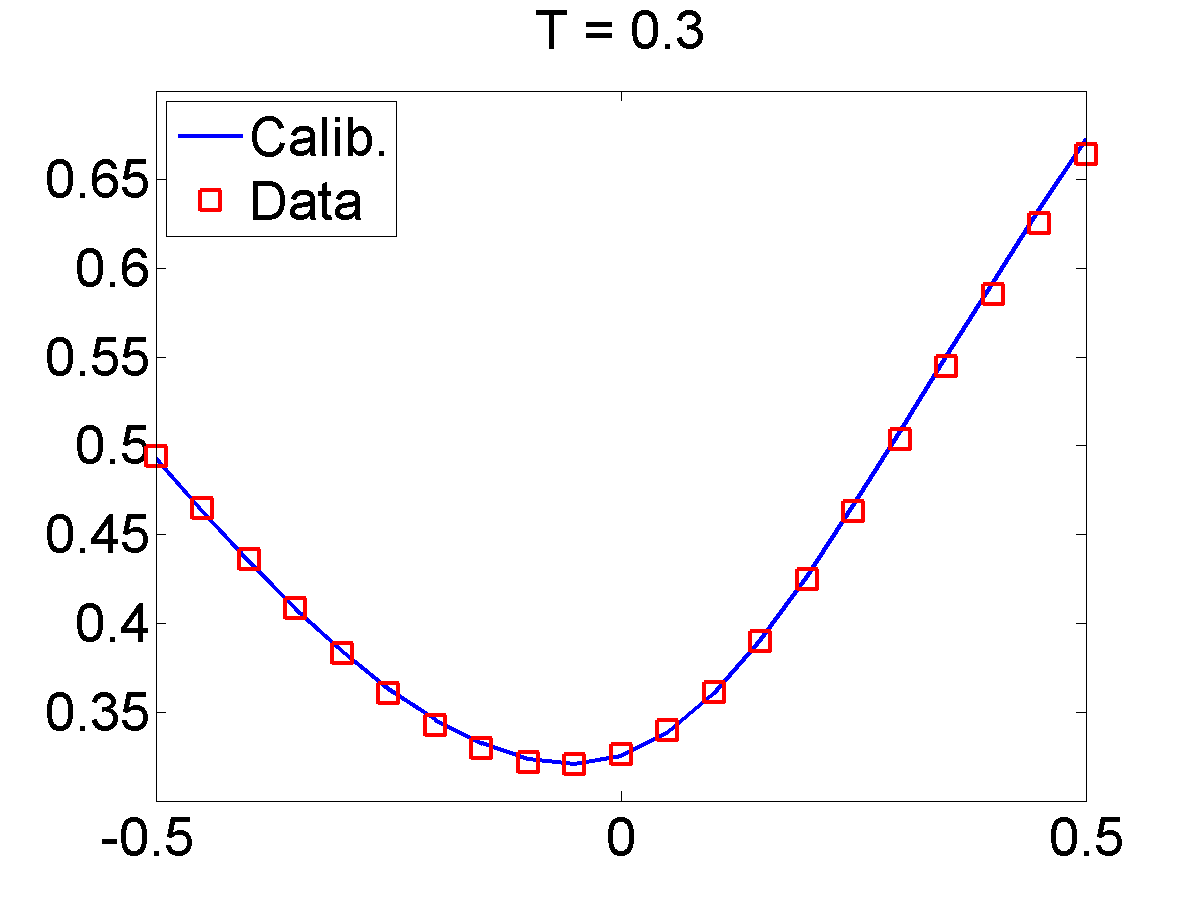

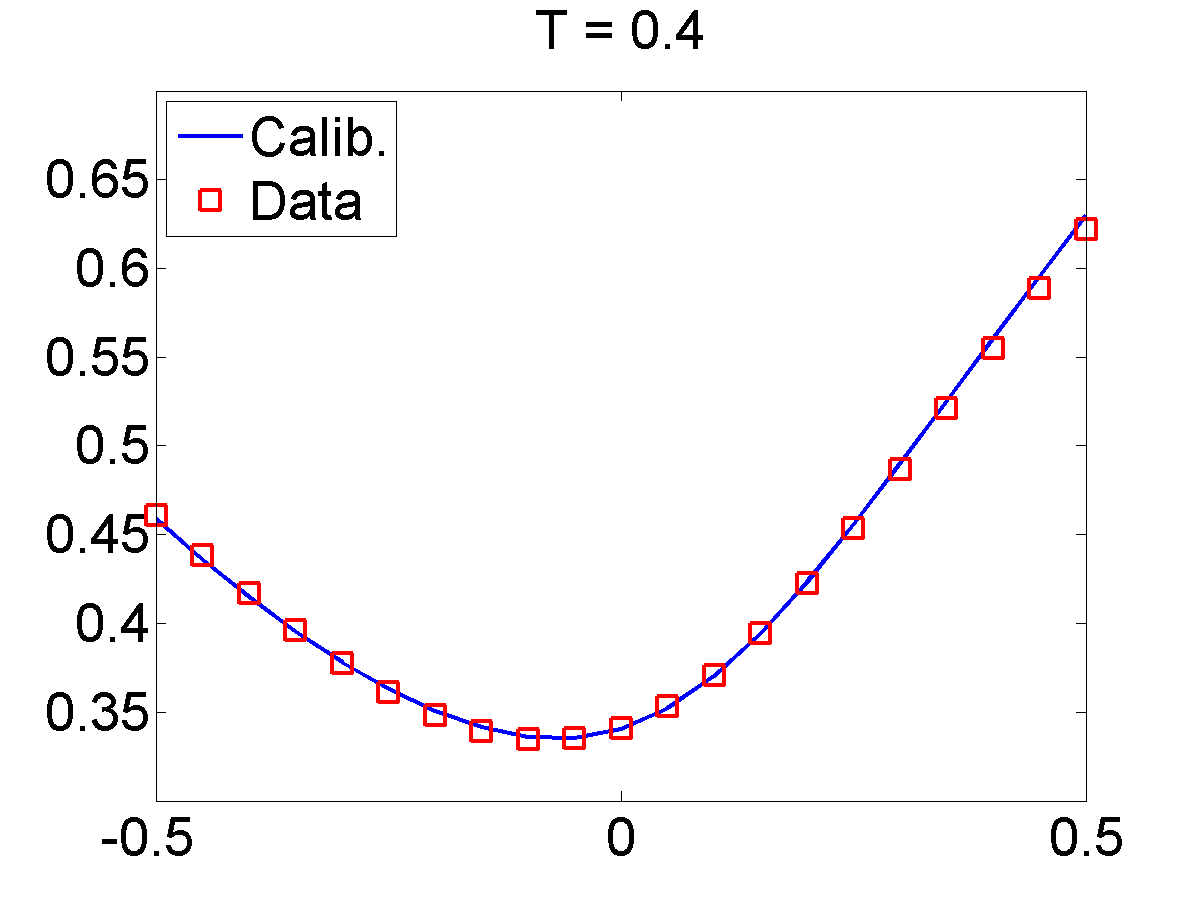

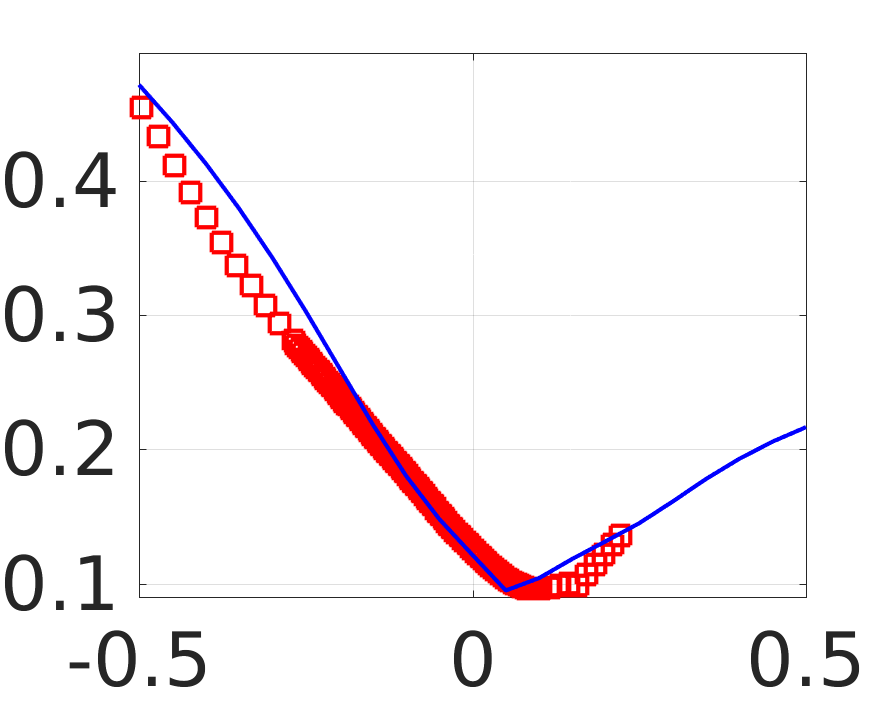

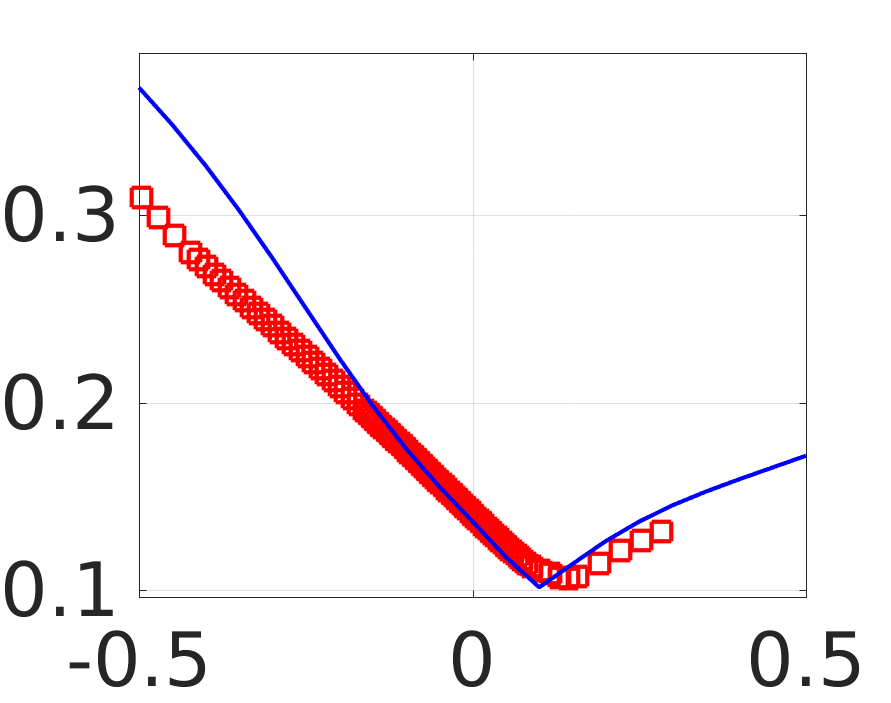

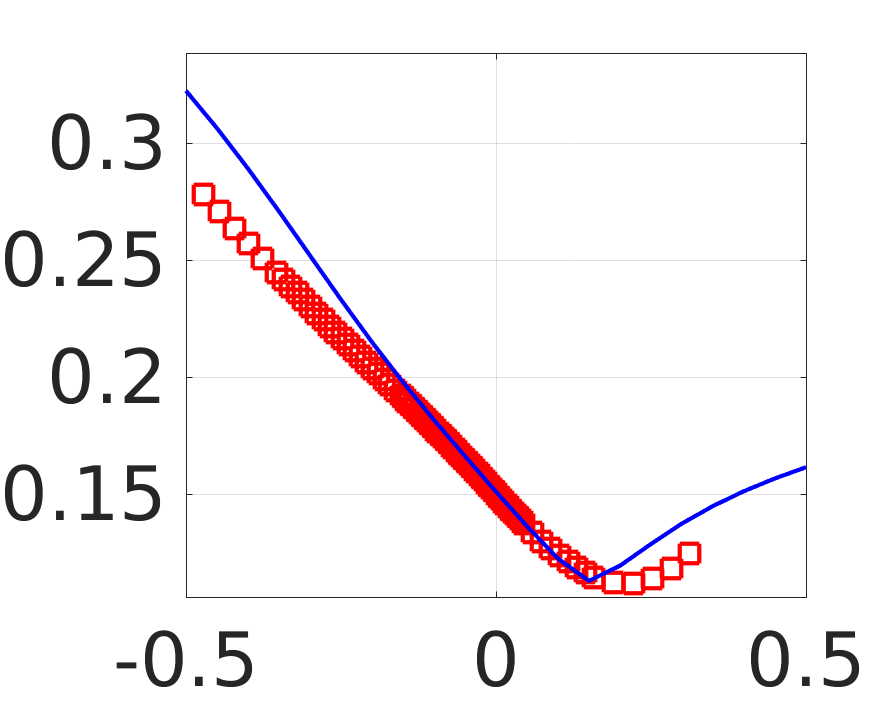

Figure 8 presents the calibrated local volatility surface, double exponential tail and jump-size density function. The corresponding implied volatilities of market data and of the model can be found in Figure 9. As can be observed from these figures, the local volatility surfaces have a nice smile adherence, especially close to the at-the-money strikes ().

8 Conclusion

In the present paper, we have explored the inverse problem of simultaneous calibration of the local volatility surface and the jump-size distribution from quoted European vanilla options when stock prices are modeled as jump-diffusion processes. This is a difficult task, since the complexity is higher than that of the calibration problem involving purely diffusive prices, as in the local volatility calibration studied by Crépey (2003a), Crépey (2003b), Egger and Engl (2005), Albani et al. (2017), and others.

Tikhonov-type regularization combined with a splitting strategy was applied to solve this inverse problem. We provided theoretical results showing that this methodology works for theoretical problem and it could be used with the specific problem under consideration. Numerical examples illustrated the effectiveness of this technique and provided stable approximations to the true local volatility and jump-size distribution with synthetic and real data.

References

- Adams and Fournier (2003) R. Adams and J. Fournier. Sobolev Spaces. Elsevier, second edition, 2003.

- Albani and Zubelli (2014) V. Albani and J. P. Zubelli. Online Local Volatility Calibration by Convex Regularization. Appl. Anal. Discrete Math., 8, 2014. doi: 10.2298/AADM140811012A.

- Albani et al. (2017) V. Albani, U. Ascher, X. Yang, and J. Zubelli. Data driven recovery of local volatility surfaces. Inverse Problems and Imaging, 11(5):799–823, 2017. doi: 10.3934/ipi.2017038. URL http://arxiv.org/abs/1512.07660.

- Albani et al. (2018) V. Albani, U. Ascher, and J. Zubelli. Local Volatility Models in Commodity Markets and Online Calibration. Journal of Computational Finance, 21:1–33, 2018. doi: 10.21314/JCF.2018.345. URL http://arxiv.org/abs/1602.04372.

- Andersen and Andreasen (2000) L. Andersen and J. Andreasen. Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of Derivatives Research, 4(3):231–262, 2000. doi: 10.1023/A:1011354913068. URL http://link.springer.com/article/10.1023/A:1011354913068.

- Barles and Imbert (2008) G. Barles and C. Imbert. Second order elliptic integro-differential equations: viscosity solutions theory revisited. Ann. Inst. H. Poincaré - Anal. Non Linéaire, 25(3):567–585, 2008. doi: 10.1016/j.anihpc.2007.02.007. URL http://archive.numdam.org/ARCHIVE/AIHPC/AIHPC_2008__25_3/AIHPC_2008__25_3_567_0/AIHPC_2008__25_3_567_0.pdf.

- Bentata and Cont (2015) A. Bentata and R. Cont. Forward equations for option prices in semimartingale models. Finance Stoch, 19:617–651, 2015. doi: 10.1007/s00780-015-0265-z. URL http://link.springer.com/article/10.1007/s00780-015-0265-z.

- Carr and Madan (1999) P. Carr and D. Madan. Option valuation using the fast Fourier transform. Journal of computational finance, 2(4):61–73, 1999. URL http://portal.tugraz.at/portal/page/portal/Files/i5060/files/staff/mueller/FinanzSeminar2012/CarrMadan_OptionValuationUsingtheFastFourierTransform_1999.pdf.

- Cioranescu (1990) I. Cioranescu. Geometry of Banach spaces, duality mappings and nonlinear problems, volume 62 of Mathematics and its Applications. Kluwer Academic Publishers Group, Dordrecht, 1990.

- Cont and Tankov (2003) R. Cont and P. Tankov. Financial Modelling with Jump Processes. CRC Financial Mathematics Series. Chapman and Hall, 2003.

- Cont and Tankov (2004) R. Cont and P. Tankov. Nonparametric calibration of jump-diffusion processes. J. Comput. Finance, 7(3):1–49, 2004. URL https://hal.archives-ouvertes.fr/hal-00002694/.

- Cont and Tankov (2006) R. Cont and P. Tankov. Retrieving Lévy Processes from Option Prices: Regularization of an Ill-posed Inverse Problem. SIAM J. Control Optim., 45(1):1–25, 2006. doi: 10.1137/040616267. URL http://epubs.siam.org/doi/abs/10.1137/040616267.

- Cont and Voltchkova (2005a) R. Cont and E. Voltchkova. A Finite Difference Scheme for Option Pricing in Jump Diffusion and Exponential Lévy Models. SIAM J. Numer. Anal., 43(4):1596–1626, 2005a. doi: 10.1137/S0036142903436186. URL http://epubs.siam.org/doi/abs/10.1137/S0036142903436186.

- Cont and Voltchkova (2005b) R. Cont and E. Voltchkova. Integro-differential equations for option prices in exponential Lévy models. Finance Stoch, 9(3):299–325, 2005b. doi: 10.1007/s00780-005-0153-z. URL http://link.springer.com/article/10.1007/s00780-005-0153-z.

- Crépey (2003a) S. Crépey. Calibration of the Local Volatility in a Generalized Black-Scholes Model Using Tikhonov Regularization. SIAM J. Math. Anal., 34:1183–1206, 2003a. doi: 10.1137/S0036141001400202.

- Crépey (2003b) S. Crépey. Calibration of the local volatility in a trinomial tree using Tikhonov regularization. Inverse Problems, 19(1):91–127, 2003b. ISSN 0266-5611. doi: 10.1137/S0036141001400202.

- Dunford and Schwartz (1958) N. Dunford and J. T. Schwartz. Linear Operators Part I: General Theory. Interscience Publishers, 1958.

- Dupire (1994) B. Dupire. Pricing with a smile. Risk Magazine, 7:18–20, 1994.

- Egger and Engl (2005) H. Egger and H. Engl. Tikhonov Regularization Applied to the Inverse Problem of Option Pricing: Convergence Analysis and Rates. Inverse Problems, 21:1027–1045, 2005.

- Engl et al. (1996) H. Engl, M. Hanke, and A. Neubauer. Regularization of Inverse Problems, volume 375 of Mathematics and its Applications. Kluwer Academic Publishers Group, Dordrecht, 1996.

- Garroni and Menaldi (2002) M.-G. Garroni and J.-L. Menaldi. Second order elliptic integro-differential problems. CRC Press, 2002.

- Gatheral (2006) J. Gatheral. The Volatility Surface: A Practitioner’s Guide. Wiley Finance. John Wiley & Sons, 2006.

- Giesecke et al. (2017) K. Giesecke, G. Teng, and Y. Wei. Numerical solution of jump-diffusion sdes. 2017.

- Iorio and Iorio (2001) R. Iorio and V. Iorio. Fourier Analysis and Partial Differential Equations, volume 70 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, 2001.

- Kindermann and Mayer (2011) S. Kindermann and P. Mayer. On the calibration of local jump-diffusion asset price models. Finance Stoch, 15(4):685–724, 2011. doi: 10.1007/s00780-011-0159-7. URL http://link.springer.com/article/10.1007/s00780-011-0159-7.

- Kindermann et al. (2008) S. Kindermann, P. Mayer, H. Albrecher, and H. Engl. Identification of the Local Speed Function in a Lévy Model for Option Pricing. J. Integral Equations Applications, 20(2):161–200, 2008. doi: 10.1216/JIE-2008-20-2-161. URL http://projecteuclid.org/euclid.jiea/1212765417.

- Ladyzenskaja et al. (1968) O. Ladyzenskaja, V. Solonnikov, and N. Ural’ceva. Linear and Quasi-linear Equations of Parabolic Type. Translations of Mathematical Monographs. AMS, 1968.

- Margotti and Rieder (2014) F. Margotti and A. Rieder. An inexact Newton regularization in Banach spaces based on the nonstationary iterated Tikhonov method. Journal of Inverse and Ill-posed Problems, 23(4):373–392, 2014. doi: 10.1515/jiip-2014-0035.

- Resmerita and Anderssen (2007) E. Resmerita and R. Anderssen. Joint Additive Kullback-Leibler Residual Minimization and Regularization for Linear Inverse Problems. Math. Methods Appl. Sci., 30:1527–1544, 2007. doi: 10.1002/mma.855.

- Rockafellar and Wets (2009) R. T. Rockafellar and R. J.-B. Wets. Variational Analysis. Springer, 2009.

- Scherzer et al. (2008) O. Scherzer, M. Grasmair, H. Grossauer, M. Haltmeier, and F. Lenzen. Variational Methods in Imaging, volume 167 of Applied Mathematical Sciences. Springer, New York, 2008.

- Somersalo and Kapio (2004) E. Somersalo and J. Kapio. Statistical and Computational Inverse Problems, volume 160 of Applied Mathematical Sciences. Springer, 2004.

- Tankov and Voltchkova (2009) P. Tankov and E. Voltchkova. Jump-diffusion models: a practitioner’s guide. Banques et Marchés, 2009. URL http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.543.6669&rep=rep1type=pdf.

- Taylor (2011) M. E. Taylor. Partial Differential Equations I: Basic Theory. Springer, second edition, 2011.