I INTRODUCTION

Mean field game theory has undergone a phenomenal growth. It provides a powerful methodology

for handling complexity in noncooperative mean field decision problems.

The readers are referred to [2, 3] for an overview of the theory and applications.

The analysis in the LQ setting has attracted

substantial interest due to its appealing analytical structure [8, 14, 16]. Specifically, the strategy of an individual player can be determined in a feedback form using its own state.

Two important methodologies called the top-down approach and

bottom-up approaches [3], respectively,

have been widely used in the analysis of mean field games.

By the top-down approach [8, 9], one determines the best response of a representative agent to a mean field of an infinite population, and next all the agents’s best responses should regenerate that mean field.

This procedure formalizes a fixed point problem which can be solved and further used to design decentralized strategies. The bottom-up

approach (also called the direct approach [11])

starts by formally solving an -player game to obtain a large coupled solution equation system. The next step is to derive a simple liming equation system by taking [13]; also see [12] for a probabilistic framework.

This paper considers the LQ mean field game and addresses the so-called asymptotic solvability.

We start with an entirely conventional solution of the game by dynamic programming and

derive a set of coupled Riccati ODEs. This method may be viewed as an instance of the bottom-up approach.

Our objective is to find a necessary and sufficient condition

for the sequence of games to be appropriately solvable. It turns out that such a condition

is completely determined by a single low dimensional non-symmetric Riccati ODE.

The derivation of this condition involves a novel re-scaling method for large-scale coupled equations with two-scales of interactions. We further determine the mean field limit of the individual strategies.

Our approach has connection with an early model of mean field social optimization, which studies a high dimensional algebraic Riccati equation and uses symmetry for dimension reduction [6, Sec. 6.3].

The methodology of extracting a low dimensional structure, here as a non-symmetric Riccati ODE, to capture essential information of the large scale decision model shares similarity to identifying low dimensional dynamics of coupled oscillators in the physics literature [15, 17, 19].

Other related works include [5, 18, 21].

An optimal control problem for a set of agents with mean field coupling

is solved in [5] by a large-scale Riccati ODE, where a mean field limit is derived for the Riccati equation using the scalar state and symmetry.

An LQ Nash game of infinite horizon is analyzed in [18] where the number of players increases to infinity. The method is to postulate the strategies of all players and examine the control problem of a fixed player subject to the mean field dynamics. Then a family of low dimensional control problems and the parameterized algebraic Riccati equations can be solved by an implicit function theorem. Sufficient conditions are obtained for solvability when the population size is large. The solvability of LQ games with increasing population sizes in the set-up of [13] is studied in [21] analyzing -coupled steady-state Hamilton-Jacobi-Bellman (HJB) and Fokker-Planck-Kolmogorov (FPK) equations, where each player’s control is restricted to be local state feedback from the beginning. Some algebraic conditions are obtained. However, it requires some restrictions on the model parameters, including symmetric state coefficients in dynamics.

Note that the top-down approach can also be used to solve the LQ mean field game [3].

In part II [11] of this paper, we investigate the relation between the top-down approach and

the bottom-up approach as developed in this paper. A surprising finding is that they are not

always equivalent.

The organization of the paper is as follows.

Section II describes the LQ Nash game together with its solution via dynamic programming and Riccati equations.

Section III presents the necessary and sufficient condition for asymptotic solvability, for which we give the proof in Section IV. Section V presents further mean field limits related to the dynamic programming equation and derives decentralized strategies. An illustrative example is provided in Section VI.

Section VII concludes the paper.

II The LQ Nash Game

Consider a population of players (or agents) denoted by , .

The state process of satisfies the following

stochastic differential equation (SDE)

|

|

|

(1) |

where the state , control

, and

. The initial states are independent with and finite second moment. The standard -dimensional Brownian motions are independent and also independent of the initial states.

For symmetric matrix , we may write . The cost of player is given by

|

|

|

|

|

|

|

|

(2) |

The constant matrices (or vectors)

, , , , , , , , , , above

have compatible dimensions, and , , .

For notational simplicity, we only consider constant parameters

for the model. Our analysis and results can be easily extended to

the case of time-dependent parameters.

Define

|

|

|

|

|

|

|

|

|

We denote by a matrix with all entries equal to 1, by the Kronecker product, and by the column vectors the canonical basis of . We may use a subscript to indicate the identity matrix to be .

Now we write (1) in the form

|

|

|

(3) |

Under closed-loop state information, we denote the value function of by , , which corresponds to the initial condition .

The set of value functions is determined by the system of HJB equations

|

|

|

|

|

|

|

|

(4) |

|

|

|

|

where and the minimizer is

|

|

|

Next we substitute into (II):

|

|

|

|

|

|

|

|

|

|

|

|

(5) |

Denote

|

|

|

|

|

|

|

|

|

where is the th submatrix.

We write

|

|

|

|

and we can write in a similar form.

Suppose has the following form

|

|

|

|

(6) |

where is symmetric.

Then

|

|

|

(7) |

We substitute (6) and (7) into (II) and derive the equation systems:

|

|

|

(8) |

|

|

|

(9) |

|

|

|

(10) |

For the -player game, we consider closed-loop perfect state information, so that the state vector is available to each player.

Theorem 1

Suppose that (8) has a unique solution on . Then we can uniquely solve (9), (10), and the game of players has a set of feedback Nash strategies given by

|

|

|

Proof:

This theorem follows the standard results in [1, Theorem 6.16, Corollary 6.5] .∎

By Theorem 1, the solution of the feedback Nash strategies with closed-loop perfect state information completely reduces to the study of (8).

For this reason, our subsequent analysis starts by analyzing (8).

III Asymptotic Solvability

For an real matrix , denote the -norm .

Definition 2

The sequence of Nash games (1)-(II) has asymptotic solvability if there exists such that for all ,

in (8) has a solution on and

|

|

|

(11) |

Definition 2 only involves the Riccati equations. This is sufficient due to Remark 2. The boundedness condition

(11) is to impose certain regularity of the solutions, which is necessary for

studying the asymptotic behavior of the system when .

Let the identity matrix be partitioned in the form:

|

|

|

For ,

exchanging the th and th rows of submatrices in , let denote the resulting matrix. For instance, we have

|

|

|

It is easy to check that .

Theorem 3

We assume that (8) has a solution

on . Then the following holds.

i) has the representation

|

|

|

(12) |

where and are symmetric matrices.

ii) For , .

By Theorem 3, (11) is equivalent to the following condition:

|

|

|

(13) |

We present some continuous dependence result of parameterized ODEs. This will play a key role in establishing Theorem 5 below.

Consider

|

|

|

(14) |

|

|

|

(15) |

where ,

Let or .

A1) .

A2) is Lebesgue measurable for each fixed .

A3) For each , is locally Lipschitz continuous in , uniformly with respect to , i.e., for any fixed , and which is the open ball of radius centering ,

|

|

|

where depends only on , not on .

A4) For each fixed ,

|

|

|

If the solutions to (14) and (15), denoted by and ,

exist on , they are unique by the local Lipschitz condition; for (14) in this case denote

, which converges to as due to A4).

Theorem 4

i) If (14) has a solution on , then there exists such that for all , (15) has a solution on and

|

|

|

(16) |

ii) Suppose there exists a sequence where and such that (15) with has a solution on and

for some constant . Then (14) has a solution on .

Let

|

|

|

Before presenting further results, we introduce two Riccati ODEs:

|

|

|

(17) |

and

|

|

|

(18) |

Note that (17) is the standard Riccati ODE in LQ optimal control and has a unique solution on . Equation

(18) is a non-symmetric Riccati ODE where is now treated as a known function. We state the main theorem on asymptotic solvability. The proof

is postponed to Section IV.

Theorem 5

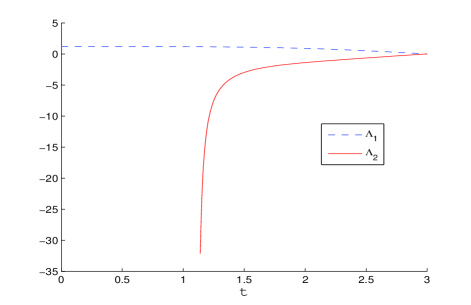

The sequence of games in (1)-(II) has asymptotic solvability if and only if (18) has a unique solution on .

Our method of proving Theorem 5 is to re-scale by

defining

|

|

|

|

(19) |

and examine their ODE system.

We introduce the additional equation

|

|

|

(20) |

Note that after (17) and (18) are solved on or otherwise on a maximal existence interval for the latter, (20) becomes a linear ODE.

Theorem 6

Suppose (18) has a solution on . Then we have

|

|

|

Proof:

The bound follows from Theorem 4 i) by use of

and the

initial conditions which appear in the equations of , , . ∎

IV Proof of Theorem 5

Note that .

We rewrite the system of (A.3), (A.4) and

(A.5)

by use of a set of new variables

|

|

|

Here and hereafter is used as a superscript in various places.

This should be clear from the context.

We can determine functions , , and obtain

|

|

|

|

|

|

(21) |

|

|

|

|

|

|

|

|

|

|

|

|

(22) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(23) |

|

|

|

In particular, we can determine

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The expressions of can be determined in a similar way and the detail is omitted here.

Note that if (18) has a unique solution on , we can uniquely solve .

In view of and the terminal conditions in (21)-(23),

by Theorem 4 and Remark 3, we obtain the desired result.