Score-Matching Representative Approach for Big Data Analysis with Generalized Linear Models

Abstract

We propose a fast and efficient strategy, called the representative approach, for big data analysis with generalized linear models, especially for distributed data with localization requirements or limited network bandwidth. With a given partition of massive dataset, this approach constructs a representative data point for each data block and fits the target model using the representative dataset. In terms of time complexity, it is as fast as the subsampling approaches in the literature. As for efficiency, its accuracy in estimating parameters given a homogeneous partition is comparable with the divide-and-conquer method. Supported by comprehensive simulation studies and theoretical justifications, we conclude that mean representatives (MR) work fine for linear models or generalized linear models with a flat inverse link function and moderate coefficients of continuous predictors. For general cases, we recommend the proposed score-matching representatives (SMR), which may improve the accuracy of estimators significantly by matching the score function values. As an illustrative application to the Airline on-time performance data, we show that the MR and SMR estimates are as good as the full data estimate when available.

Key words and phrases: Big data regression, User data localization, Distributed database, Mean representative approach, Divide and conquer, Subsampling

1 Introduction

In the past decade, big data or massive data has drawn dramatically increasing attention all over the world. It was in the 2009 ASA Data Expo competition when people found out that no statistical software was available to analyze the massive Airline on-time performance data. At that time, the airline data file, about 12GB in size, consists of 123,534,969 records of domestic flights in the United States from October 1987 to April 2008 (Kane et al., 2013). Up to December 2019, the Airline on-time performance data collected from the Bureau of Transportation Statistics consists of 387 files and valid records in total.

The response in the Airline on-time performance data was treated as a binary variable Late Arrival with standing for late by minutes or more (Wang et al., 2016). Generalized linear models (GLMs) have been widely used for modeling binary responses, as well as Poisson, Gamma, and Inverse Gaussian responses (McCullagh and Nelder, 1989; Dobson and Barnett, 2018). In order to fit a GLM with predictors, a typical algorithm searching for the maximum likelihood estimate (MLE) based on the full data of size requires time to run, where is the number of iterations required for the convergence of the full data MLE algorithm (Wang et al., 2018).

Starting in 2009, substantial efforts have been made on developing both methodologies and algorithms towards big data analysis (see, for example, Wang et al. (2016), for a good survey on relevant statistical methods and computing). Divide-and-conquer, also known as divide-and-recombine, split-and-conquer, or split-and-merge, first partitions a big dataset into blocks, fits the target model block by block, and then aggregates the fitted models to form a final one (Wang et al., 2016). A divide-and-conquer algorithm proposed by Lin and Xi (2011) reaches the time complexity of , where is the number of iterations required by a GLM MLE algorithm with data points. The accuracy of the estimated parameters based on the divide-and-conquer algorithm relies on the block size , which typically depends on the computer memory. Therefore, as increases, has to increase accordingly. Typically, its accuracy is not as good as the full data estimate. The divide-and-conquer idea has been applied to numerous statistical problems (Chen and Xie, 2014; Schifano et al., 2016; Zhao et al., 2016; Lee et al., 2017; Battey et al., 2018; Shi et al., 2018; Chen et al., 2019). For example, Chen and Xie (2014) made an innovative attempt of majority voting on variable selection based on a divide-and-conquer framework that is similar in spirit to combining confidence distributions in meta-analysis (Singh et al., 2005; Xie et al., 2011). Schifano et al. (2016) extended the divide-and-conquer idea for online updating problems motivated from a Bayesian inference perspective.

Another popular strategy for big data analysis is subsampling. For example, leveraging technique has been used to sample a more informative subset of the full data for linear regression problems (Ma and Sun, 2014). Inspired by D-optimality in optimal design theory, Wang et al. (2019) proposed an information-based subsampling technique, called IBOSS, for big data linear regression problems. Its time complexity is while the ordinary least square (OLS) estimate for linear models takes time complexity. Motivated by A-optimality, Wang et al. (2018) developed an efficient two-step subsampling algorithm for large sample logistic regression, which is a special case of generalized linear models. The time complexity of the A-optimal subsampler is also . Compared with the divide-and-conquer strategy, the subsampling approach requires much less computational cost. Nevertheless, its accuracy relies on the subsample size and is typically not as good as the divide-and-conquer estimate.

Other developments include stochastic gradient descent and the polynomial approximate sufficient statistics approaches. Stochastic gradient descent algorithms (Tran et al. 2015; Lin and Rosasco 2017) update in a sequential manner based on a noisy gradient. Polynomial approximate sufficient statistics methods (Huggins et al. 2017; Keeley et al. 2020; Zoltowski and Pillow 2018) construct polynomial approximate sufficient statistics for GLMs for any combination of batch, parallel, or streaming. In terms of accuracy, their performances are comparable with subsampling techniques.

The success of divide-and-conquer methods relies on the similarity between blocks, which can be achieved by randomly partitioning the original dataset. In practice, however, a massive dataset is often stored in multiple files, within which data points have sort of similarity in some fields. We call it homogeneous partition. For example, the Airline on-time performance data (see Section 4) consists of 387 files labeled by month. In each file, all data points share the same values in fields YEAR, MONTH, and QUARTER, while between files these values are different. A divide-and-conquer strategy would not work directly with the original homogeneous partition due to distinct blocks. Even worse, a massive dataset is sometimes distributed in multiple hard disks, or even a network of interconnected computers, known as nodes (see, for example, a distributed database (Özsu and Valduriez, 2011)). If one needs to re-partition the data randomly, it may involve intensive communication between nodes and require extensive network bandwidth.

Another critical issue on massive data analysis is data localization requirements. Due to security or privacy concerns, data localization or data residency law prohibits health records, personal data, payment system data, etc, from being transferred freely (Bowman, 2017; Fefer, 2020). Technology companies, such as Microsoft, also use data storage locale controls in their cloud services (Vogel, 2014). The Irish Data Protection Commission sent Facebook a preliminary order to suspend moving data from its European users to the United States (Schechner and Glazer, 2020). Under such kind of circumstances, the partition of data is predetermined and raw data exchange between nodes is prohibited. We call such kind of data partition a natural partition.

In the computer science literature, algorithms of the CoCoA family have been developed for optimization problems with distributed dataset and a central server (see Smith et al. (2018) for a good review), which combine local solvers for subproblems in an efficient manner. He et al. (2018) further extended CoCoA to the COLA algorithm for decentralized environment, that is, distributed computing without a central coordinator.

To avoid intensive data communications between nodes and even avoid any raw data transfer, we propose a different data analysis strategy for distributed massive dataset with data localization requirements, named the representative approach. When a massive data is provided in data blocks, either naturally or partitioned by a data binning procedure, we construct a representative data point for each data block using only the data within the block and initial parameter values, and then run regression analysis on the representative data points. The constructed representatives are typically artificial ones which may not belong to the original dataset. The collection of representative data points may be used for further analysis and inference. Compared with the original data, its data volume is significantly reduced.

The representative approach provides an ideal solution for the analysis of naturally partitioned massive data. By exchanging only the estimated parameters and the representative data points among parallel computing computers, the representative approach can work well even with slow-speed or restricted network connection. It fulfills user privacy or security requirements since analysts perform regression analysis on the representatives without direct access to the raw data.

The representative approach is inspired by the data binning technique in the computer science literature. By discretizing continuous variables into categorical variables (see, for example, Kotsiantis and Kanellopoulos (2006)), a data binning procedure partitions a continuous feature space into blocks labeled by so-called smoothing values. It focuses on how to partition data into blocks or bins, while the smoothing values are typically chosen from class labels, boundary points, centers, means, or medians of the data blocks. A data binning procedure is often used for data pre-processing, whose performance is not guaranteed, especially for nonlinear models.

Different from the data binning technique, the representative approach proposed in this paper assumes a given data partition and concentrates on constructing the best smoothing values, which we call representatives, more efficiently for a pre-specified regression model. With a given partition, the goal of the representative approach is to run as fast as subsampling approaches, while estimating model parameters as accurately as the divide-and-conquer method.

Actually, using the proposed representative approach, a GLM is fitted on representatives constructed from the original data points (). Its time complexity is also , same as the subsampling approaches. On the other hand, the representatives are not a subset of the data points, but summarize the information from each single one of the original data points. Based on our comprehensive simulation studies, by matching the score function values of GLMs, the proposed score-matching representative (SMR) approach is often comparable with the full data estimate.

The data binning technique that we consider here is to partition the data according to the predictors. It is different from the sufficient dimension reduction techniques which start with a data partition based on the responses or the conditional class probabilities of binary responses (Shin et al., 2014, 2017).

The representatives described in this paper are different from the representative points (rep-points) developed in the statistical literature, which aims to represent a distribution the best. Research work on rep-points includes the principal points in Flury (1990), the mse-rep-points in Fang and Wang (1994), and the recent support points in Mak and Joseph (2017, 2018). Although the rep-points can capture the covariate distribution better, they may not be more informative in estimating model parameters, and thus are not as efficient as subsampling methods or the proposed representative approaches (see Section A.4 in the Supplementary Material for comparisons).

The remainder of this paper proceeds as follows. In Section 2 we describe the general framework of the representative approach and data partitions. After comparing mean, median and mid-point representatives, we recommend mean representative (MR) for big data linear regression analysis. In Section 3 we develop SMR along with its theoretical justifications. We recommend SMR for big data general linear regression analysis. In Section 4, we use the Airline on-time performance data as an illustrative example for real big data analysis. We show that the MR and SMR estimates are as accurate as the full data estimate when available. We conclude in Section 5. The proofs of theorems and corollaries, more corollaries, more simulations, as well as more details about the real case study, are relegated to the Supplementary Material.

2 GLM, Massive Data and Mean Representative

2.1 Generalized Linear Model and Score Function

Given the original data set with covariates and response , we consider a generalized linear model assuming independent response random variable ’s and the corresponding predictors . For model-based data analysis with fairly general known functions , we would rather regard the data set as . For many applications, corresponds to the intercept. For examples, for a main-effects model or , for a model with interactions.

Following McCullagh and Nelder (1989), there exists a link function and regression parameters , such that and , where has a distribution in the exponential family. For typical applications, the link function is one-to-one and differentiable.

According to McCullagh and Nelder (1989, Section 2.5), the maximum likelihood estimate of solves the score equation , where , , and the score function

| (2.1) |

with and , where . For commonly used GLMs, their and are listed in Table 1.

| Distribution of | link function | (up to a constant) | |

|---|---|---|---|

| Normal | identity | ||

| Bernoulli | logit | 1 | |

| Bernoulli | progit | ||

| Bernoulli | cloglog | ||

| Bernoulli | loglog | ||

| Bernoulli | cauchit | ||

| Poisson | log | 1 | |

| Gamma | reciprocal | 1 | |

| Inverse Gaussian | inverse squared | 1 |

2.2 Representative Approaches and Mean Representatives

In this paper, we assume that the data is given along with a data partition. Let be the data index set. The data partition can be denoted by a partition of . The th data block has block size .

A representative approach for model-based regression analysis constructs a representative data point for data block , , and then fit the regression model based on the weighted representative dataset . This procedure could be repeated to achieve a desired accuracy level of estimated model parameters.

Unlike subsampling approaches, a representative data point may not belong to the original data set. With a given data partition, the goal of the representative approach is to make the model parameter estimate based on the weighted representative dataset close enough to the full data estimate . Given an initial value of parameter estimate, the construction of representative data points in one block shall not be affected by another to facilitate parallel computing.

In practice, a massive dataset is often provided in multiple data files, which forms a natural partition with each block representing a data file. In order to improve the efficiency of the proposed representative approach, one may construct a sub-partition within each natural data block or data file such that the predictors have similar values in each finer block. Many partitioning methods have been proposed in the literature (see, for example, Fahad et al. (2014) for a good survey). From our point of view, there are two types of partitioning methods, grid or clustered. Grid partition is based on the feature space in , with cut points obtained from the summary information of data, such as quantiles (called equal-depth) or equal-width points, which is usually feasible with a moderate number of predictors (Kotsiantis and Kanellopoulos, 2006). Its time complexity is . Clustered partition is based on clustering algorithms. For example, Pakhira (2014) proposed a linear -means algorithm with time complexity , which is especially useful with large . When the massive data consists of multiple natural blocks or data files, these partitioning methods could be applied on the natural blocks one-by-one to obtain a finer partition of the whole dataset. In practice the sizes of natural blocks or data files are typically fixed. Only the number of data files increases when the massive dataset is updated in a time order. Therefore, the overall time complexity for obtaining all sub-partitions is still . Improving the efficiency of sub-partitioning is important but out of the scope of this paper.

There are lots of representative choices that could possibly work for the representative approach. A naive choice of the representative is the block center, which is popular in the data binning literature. More specifically, given the th data block with block size , the options for its representative include (1) mid-point of the rectangular block, when a grid partition is given; (2) (component-wise) median; (3) (vector) mean, that is, . Then the weighted representative data for the th block is defined as with , which will be justified in Theorem 3.2.

A comprehensive simulation study with linear models shows that using block means, the mean representative approach (MR), is more efficient than the mid-point and median options, as well as the IBOSS subsampling approach (Wang et al., 2019). For details please see Section A.1 in the Supplementary Material.

As for time complexity, the full data ordinary least squares (OLS) estimate takes . The IBOSS (Wang et al., 2019) costs . For typical applications, and , then the overall time complexity including constructing representatives and fitting models is for mid-point or for median and mean representative approaches for both linear regression models and GLMs.

The simulation studies in Section A.1 of the Supplementary Material also imply that the maximum Euclidean distance within data blocks plays an important role on the efficiency of mean representatives. For general representatives, the key quantity is the maximum deviation from the corresponding representatives .

3 Score-Matching Representative Approach for GLMs

The MR approach works very well for linear models and can be validated for GLMs when is sufficiently small. Nevertheless, for moderate with general GLMs, MR approach is not so satisfactory (see Section 3.2). In this section, we propose a much more efficient representative approach, called score-matching representative (SMR) approach for GLMs.

Recall that in Section 2.1 the maximum likelihood estimate solves the score equation . It is typically obtained numerically by the Fisher scoring method (McCullagh and Nelder, 1989), which iteratively updates the score function with the current estimate of . Inspired by the Fisher scoring method, given some initial values of the estimated parameters, our score-matching representative approach constructs data representatives by matching the values of the score function block by block, and then applies the Fisher scoring method on the representative dataset and gets estimated parameter values for the next iteration. We may repeat this procedure for a few times till a certain accuracy level is achieved. According to our comprehensive simulation studies (see Section A.2 in the Supplementary Material), three iterations are satisfactory for typical applications.

3.1 Score-Matching Representative Approach

Let denote the value of the score function contributed by the th data block , and denote the value of the score function based on the weighted representative data , where and are functions of .

Suppose the estimated parameter value is at the th iteration. For the th iteration, our strategy is to find the representative carrying the same score as the th data block at , that is, , or

| (3.1) |

Multiplying by on both sides of (3.1), we get

| (3.2) |

where and . The weight of in (3.2) suggests that we take as a weighted average of ’s for the SMR approach, that is,

| (3.3) |

Remark 3.1.

The defined by (3.3) is a natural generalization of the mean representative. Actually, let , , and denote the mean representative. Since , then it can be verified that as goes to , given that is bounded away from . In order to avoid , which may lead to unbounded when is close to , we split such a block into two pieces by the signs of ’s and generate two representatives, one for positive ’s and the other for negative ’s.

Theorem 3.1.

There exists an that solves equation (3.2).

The existence of the score-matching representative is guaranteed by Theorem 3.1, whose proof is relegated to the Appendix. Since the solution solving (3.2) may not be unique, we choose the closest to the mean representative to keep a smaller . Different from mean representatives, the coordinates of the score-matching representatives corresponding to the intercept term may not be exactly one.

The th weighted representative data point , which carries the same score value at as the th original data block, will be used for fitting via the Fisher scoring method. For typical applications, we may repeat this procedure for times to achieve the desired accuracy level (see Figure A.2 in the Supplementary Material for a trend of SMR iterations). The complete procedure of the -iteration SMR approach is described by Algorithm 1.

For a GLM, the time cost is for calculating all ’s, for calculating all ’s using (3.3), plus iterations for solving (3.2), and for calculating all ’s by (3.4). Along with the time cost for finding the MLE baesd on representative points, a 3-iteration SMR requires . Since , the time complexity of SMR for a GLM is essentially .

3.2 Simulation Studies with Logistic Regression Model

Logistic regression model is one of the most widely used generalized linear models. Wang et al. (2018) proposed an A-optimal subsampling approach for big data logistic regression. Following Wang et al. (2018), we run a comprehensive simulation study with the model

| (3.5) |

Analogue to the simulation setup in Wang et al. (2018), we choose , . For simulating , we consider six unbounded distributions plus a bounded one: (1) mzNormal, with having diagonal and off-diagonal ; (2) nzNormal, , a case with imbalanced responses, where is a vector of all ones; (3) ueNormal, with having diagonals and off-diagonal ; (4) mixNormal, , a case with bimodal ; (5) , Multivariate with degrees of freedom , a case with heavy tails; (6) EXP, , an iid case with a heavier tail on the right; (7) BETA, , a bounded iid case with “U” shaped distribution.

For illustration purpose, we choose a moderate population size in this simulation study. In the absence of a natural partition, we use two data-driven partitions: (1) An equal-depth partition with splits for each predictor, that is, using the three sample quartiles (25%, 50%, and 75%) as the cut points for each predictor and partitioning the whole data into up to blocks (after removing empty blocks, the number of blocks is actually between and ); (2) a -means partition with the number of blocks . The proposed SMR approach starts with MR estimates as its initial values and repeats the iterations for 3 times.

For comparison purpose, stochastic gradient descent (SGD) proposed by Tran et al. (2015), A-optimal subsampling (A-opt) by Wang et al. (2018) with subsample size , and divide-and-conquer (DC) by Lin and Xi (2011) with blocks from a random partition are applied to the simulated data.

Table 2 shows the average and standard deviation of the root mean squared errors (RMSEs, ) between the estimated parameter value ’s and the true value ’s across different simulation settings and each with 100 independent simulations.

| Simulation | Full | Equal-depth | -means | |||||

|---|---|---|---|---|---|---|---|---|

| setup | data | MR | SMR | MR | SMR | A-opt | DC | SGD |

| mzNormal | 3.7 (1.1) | 20.4 (1.0) | 3.9 (1.2) | 17.9 (1.0) | 4.1 (1.2) | 20.4 (5.7) | 7.9 (1.1) | 55.9 (14.8) |

| nzNormal | 7.2 (2.0) | 20.4 (1.7) | 9.6 (2.6) | 17.4 (1.7) | 8.3 (2.0) | 24.4 (6.1) | 21.5 (1.6) | 99.2 (27.8) |

| ueNormal | 2.1 (0.8) | 170.4 (0.7) | 4.4 (1.1) | 195.7 (3.8) | 14.8 (7.4) | 9.0 (3.3) | 13.2 (1.3) | 62.9 (77.0) |

| mixNormal | 5.0 (1.3) | 19.9 (1.1) | 5.4 (1.6) | 13.8 (1.2) | 5.7 (1.6) | 22.9 (5.5) | 12.1 (1.2) | 79.3 (21.0) |

| 16.0 (4.4) | 30.5 (4.2) | 20.9 (5.8) | 25.1 (7.5) | 23.4 (7.3) | 97.9 (30.1) | 19.6 (3.9) | 177.8 (17.8) | |

| EXP | 6.2 (1.7) | 23.0 (2.6) | 13.4 (2.4) | 20.3 (3.1) | 8.8 (2.5) | 31.3 (7.9) | 18.2 (2.3) | 147.9 (20.9) |

| BETA | 7.5 (2.4) | 7.6 (2.5) | 7.6 (2.5) | 11.4 (3.0) | 11.4 (3.7) | 39.9 (11.6) | 9.3 (2.5) | 179.4 (20.0) |

-

•

Sample size ; MR, SMR: equal-depth partition, or -means partition, ;

-

•

A-opt: A-optimal subsampler, subsamples; DC: Divide-and-Conquer, random blocks;

-

•

SGD: stochastic gradient descent

According to Table 2, MR, A-opt and SGD do not match either DC or SMR in terms of accuracy. SMR performs either the best or comparable with DC. For more than half of the scenarios, SMR is even comparable with the full data estimates. With the -means partition, SMR achieves roughly the same accuracy level with only representatives. A justification under linear models, which is relegated to the Supplementary Material (Section A.1), shows that a best partition keeps the cluster size the same for , which partially explains the better performance of -means partitions.

As a conclusion, when the predictors are bounded, MR is a fast and low-cost (computationally cheaper) solution for big data analysis with generalized linear models. For more general cases, especially when a higher accuracy level is desired, MR can be used as a pre-analysis for SMR, while the latter has a significant improvement across different scenarios and different partitions.

3.3 Other GLM Examples

Commonly used GLMs include binary responses with logit, probit, cloglog, loglog, and cauchit links, Poisson responses with log link, Gamma responses with reciprocal link, Inverse Gaussian responses with inverse squared link (see detailed formulae in Table 1).

| Binary with cloglog | Poisson with log | Logistic with interactions | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Full | MR | SMR | Full | MR | SMR | Full | MR | SMR | |

| From true | 2.81 | 43.73 | 3.88 | 0.22 | 29.87 | 12.17 | 3.51 | 7.40 | 5.12 |

| (0.75) | (0.99) | (1.04) | (0.06) | (9.86) | (10.41) | (1.20) | (2.01) | (1.52) | |

| From full | 0 | 43.57 | 2.57 | 0 | 29.88 | 12.17 | 0 | 6.45 | 3.79 |

| - | (0.55) | (0.67) | - | (9.86) | (10.41) | - | (0.42) | (0.99) | |

-

•

Sample size ; Covariate distribution: mzNormal; MR, SMR: -means partition,

In Table 3, we show the RMSEs () from the true parameter and the RMSEs () from the full data estimate . The representative approaches, MR and SMR, are based on -means partition with for the following three models: (1) Binary response with complementary log-log (or cloglog) link . Since is relatively flat, SMR estimate is comparable with the full data estimate even with a not-so-good MR estimate. (2) Poisson response with the canonical link . Since increases exponentially, the improvement of SMR is slowed down with a not-so-good MR estimate. The variances of MR and SMR estimates are both high. Thus a good initial value for Poisson regression is crucially important (see Section 3.5 for detailed discussion on how the slope of affects the performance of SMR). (3) Logistic model with interactions. In this case, we simulate from mzNormal and assume the non-intercept predictors to be . Both MR and SMR estimates work well.

3.4 Theoretical Justification of SMR

First of all, for the proposed SMR approach in Section 3.1, the full data estimate is a stationary point of the SMR iteration. That is, if the current estimate , then the representative dataset achieves score at and thus as well.

Recall that is the maximum likelihood estimate (MLE) based on the full data . Let be the MLE based on a weighted representative data , which could be obtained by MR, SMR, or other representative approaches. Since for any , then , where . Theorem 3.2 below provides asymptotic results for fairly general representative approaches, whose proof is relegated to the Supplementary Material (Section A.8).

Theorem 3.2.

For a generalized linear model with a given dataset, suppose its log-likelihood function is strictly concave and twice differentiable on a compact set and its maximum can be attained in the interior of . Suppose the representatives satisfies . Then as . Furthermore, .

Theorem 3.2 covers mean, median, and mid-point representatives. For mean and mid-point representatives, we actually have . For median representatives, we also have . Thus as direct corollaries, for all the three center representatives (see Corollaries A.1 & A.2 in Section A.8 of the Supplementary Material).

Theorem 3.3.

Suppose . Under the same conditions as in Theorem 3.2, for any given , the SMR estimate converges to if goes to zero, and .

Technically speaking, any representative approach satisfying (3.1) could be called a score-matching approach. The proposed SMR approach which satisfies (3.3) and (3.4) is one of the possible solutions for (3.1), which is a natural extension of the MR approach. Both Theorem 3.3 and the following theorem provide consistency results for general score-matching approaches, whose proofs are relegated to Section A.8 of the Supplementary Material.

Theorem 3.4.

Consider a more general iterative representative approach with estimated parameter at its th iteration. Suppose for the th iteration, for each , the obtained weighted representative data satisfies the following two conditions:

-

(a)

The representative matches the score function at , that is, (3.1) is true;

-

(b)

The representative response , where .

Then the estimated parameter based on the weighted representative data satisfies

| (3.6) |

where for small enough . Therefore, as and .

Remark 3.2.

We call in (3.6) the global rate of convergence, which depends on the size of . Its specific form can be found in the proof of Theorem 3.4. Based on our experience, even for moderate size of , can be significantly smaller than and the first few iterations can improve the accuracy level significantly.

For score-matching representatives, condition (a) of Theorem 3.4 holds instantly. As for condition (b) of Theorem 3.4, if for some as goes to , then (see Remark 3.1), and thus since . After splitting blocks according to the signs of ’s, the cases of data blocks with close to are rare. For those blocks, we may simply define . Thus condition (b) can be guaranteed in practice.

The conditions and conclusions of Theorem 3.4 are expressed in terms of . When applying the SMR approach, a slight modification may guarantee . Actually in our simulation studies, it is almost always the case for the proposed SMR approach. Occasionally, could be out of the convex hull of due to . For such kind of cases, we replace with the MR representative . The difference caused for the value of score function is negligible. By this way, the conclusions of Theorem 3.4 hold for as well.

Overall, Theorem 3.4 justifies why the proposed SMR approach works well.

Corollary 3.1.

When or , MR and SMR generate the same set of representatives. Both SMR and MR estimates are equal to the full data estimate for GLMs.

A special case of Corollary 3.1, whose proof is relegated to Section A.8 of the Supplementary Material, is when all covariates are categorical and the dataset is naturally partitioned by distinct covariate values. When most covariates are categorical except for a few continuous variables, for example, the Airline on-time performance data analysis in Section 4, the partition could be chosen such that is fairly small and thus both MR and SMR estimates work very well.

3.5 Asymptotic Properties of MR and SMR for Big Data

In order to study the asymptotic properties of MR and SMR estimates as goes to , we assume that the predictors are iid with a finite expectation, and the partition of the predictor space is fixed. To avoid trivial cases, we assume for each . Then the index block with size . By the strong law of large numbers (see, for example, Resnick (1999, Corollary 7.5.1)), as , almost surely. In order to investigate asymptotic properties, we consider the discrepancy from the true parameter value instead of the estimate based on the full data.

For the MR approach, as ,

| (3.7) |

almost surely. If the link function or is linear, then and thus the MR estimate . Nevertheless, in general is nonlinear, and the accuracy of the MR estimate mainly depends on the size of blocks, not the sample size . In other words, for a general GLM and a fixed partition of the predictor space, the accuracy of the MR estimate is restricted by (3.7) and thus will not benefit from an increased sample size.

Different from MR, by matching the score function of the full data, the proposed SMR approach can still improve its accuracy as the sample size increases, even with a fixed partition of the predictor space. Actually, for a general GLM, and , where . For a bounded block , is also bounded. By the strong law of large numbers for independent sequence of random variables (see, for example, Resnick (1999, Corollary 7.4.1)) and the first-order Taylor expansion, as and thus , the left hand side (LHS) of (3.2) after divided by is

| (3.8) | |||||

| (3.9) |

From (3.8) we see that as increases, the leading discrepancy of LHS caused by response ’s vanishes. Even if the maximum block size is fixed, when is close to , the LHS of (3.2) is small, and so is its right hand side. For blocks with away from , it indicates that and thus are small. That is, when , the SMR representatives stay close to the true curve, , which leads to a faster convergence rate of the SMR estimate towards than MR’s.

From (3.9) we conclude that a relatively large may slow down the convergence of the SMR estimate. For example, under a Poisson regression model with log link (see Model (2) in Section 3.3), . If the initial estimate of the regression parameter is not so accurate, SMR may converge slowly. For such kind of cases, we suggest a finer partition or smaller to obtain a good initial estimate. For models with fairly flat functions, such as models with logit link, is small for most blocks. For this kind of cases, even if the initial estimate for SMR is not so accurate, we can still improve the accuracy of the estimate significantly after a few iterations.

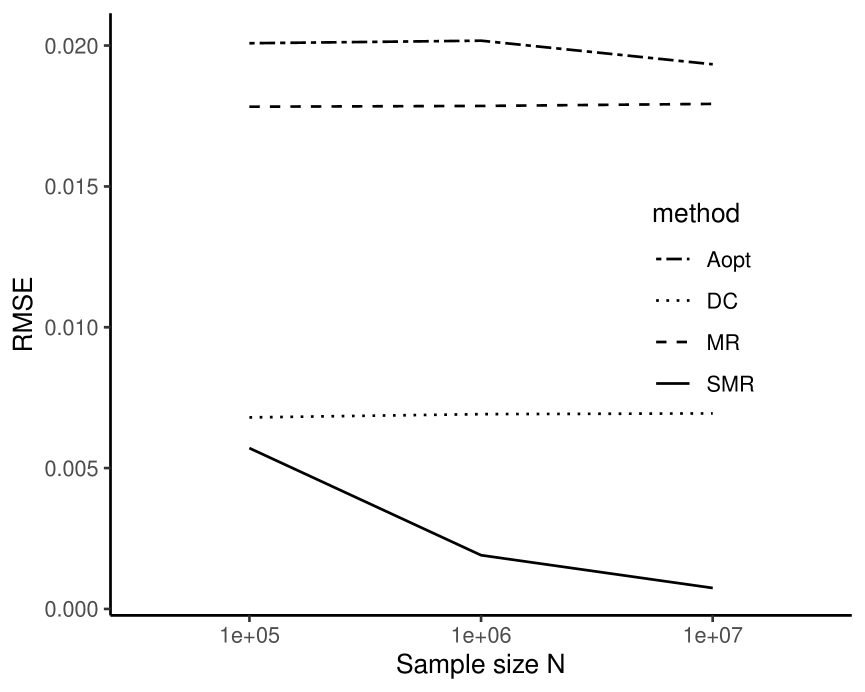

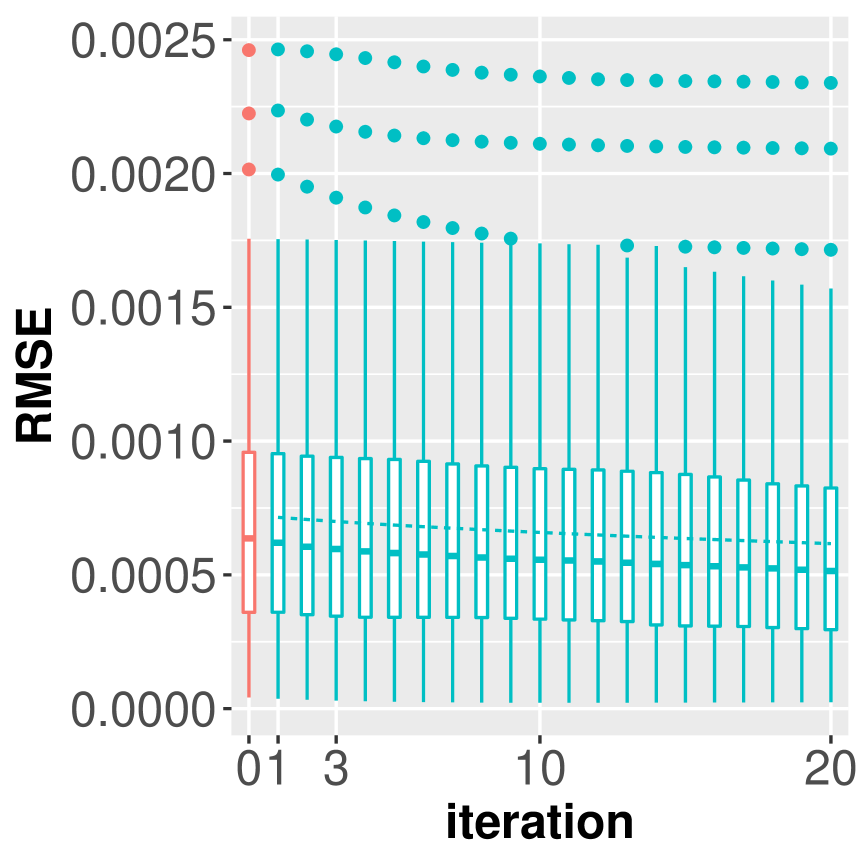

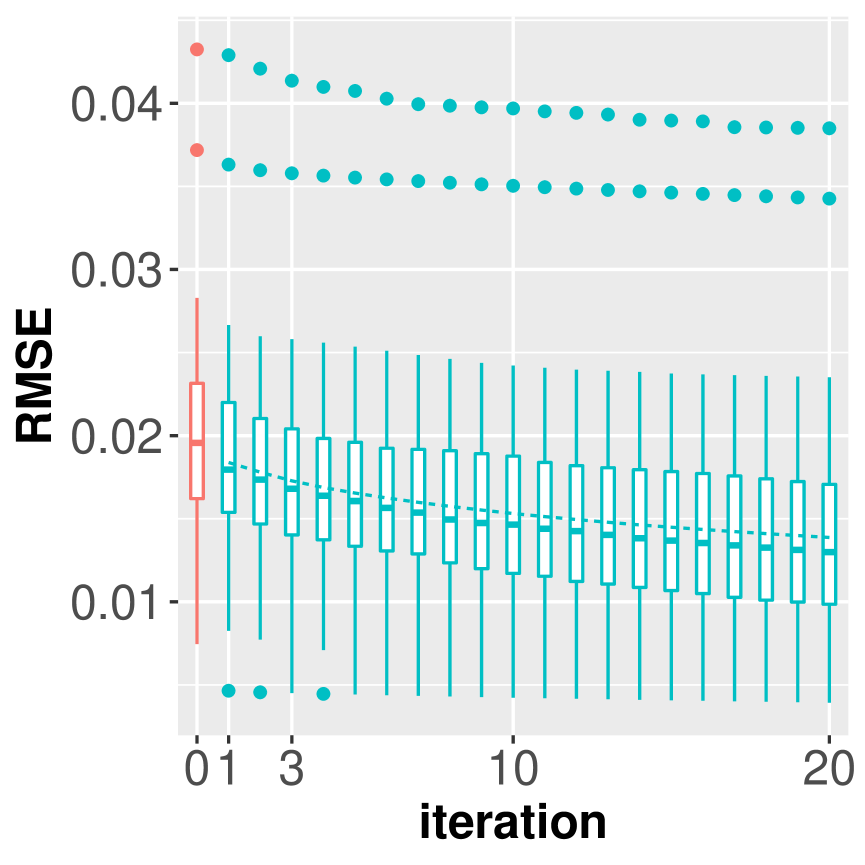

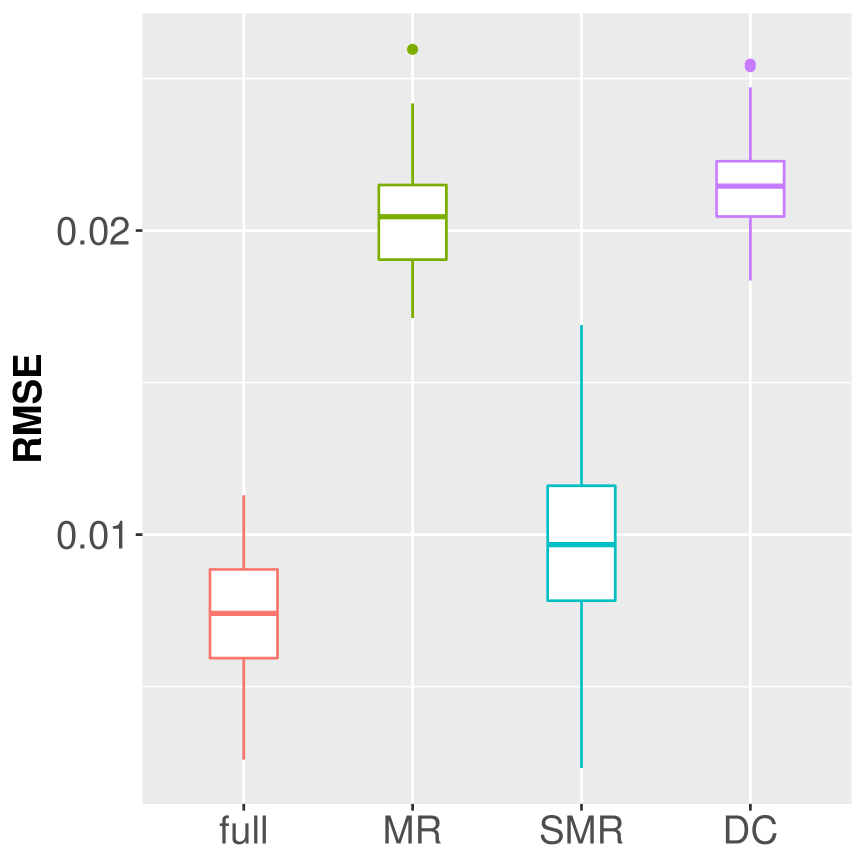

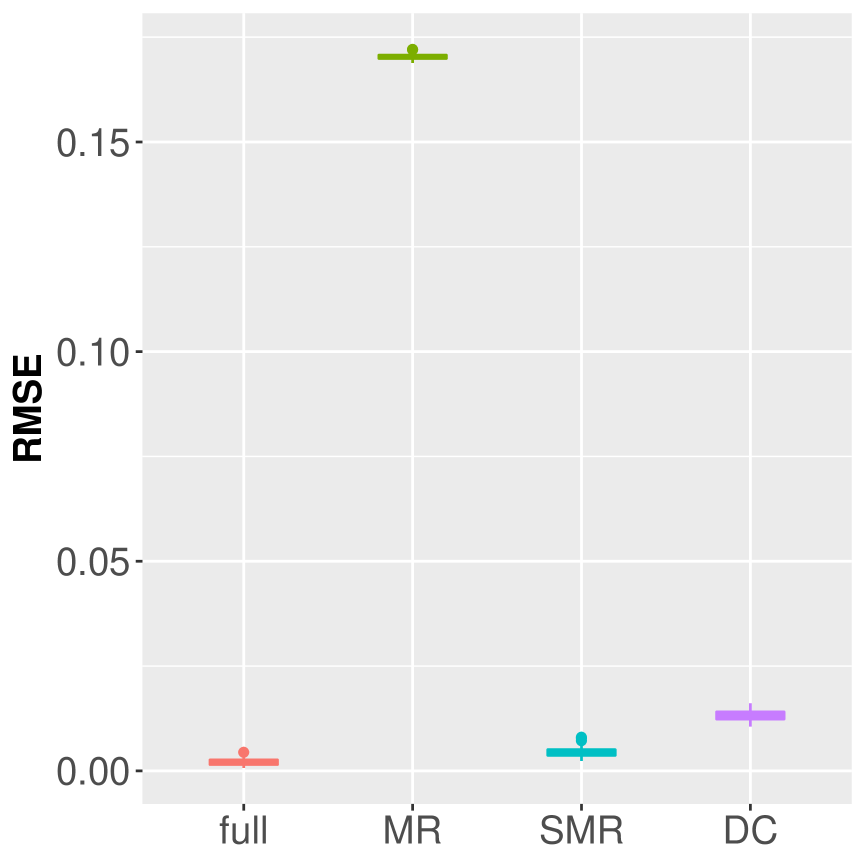

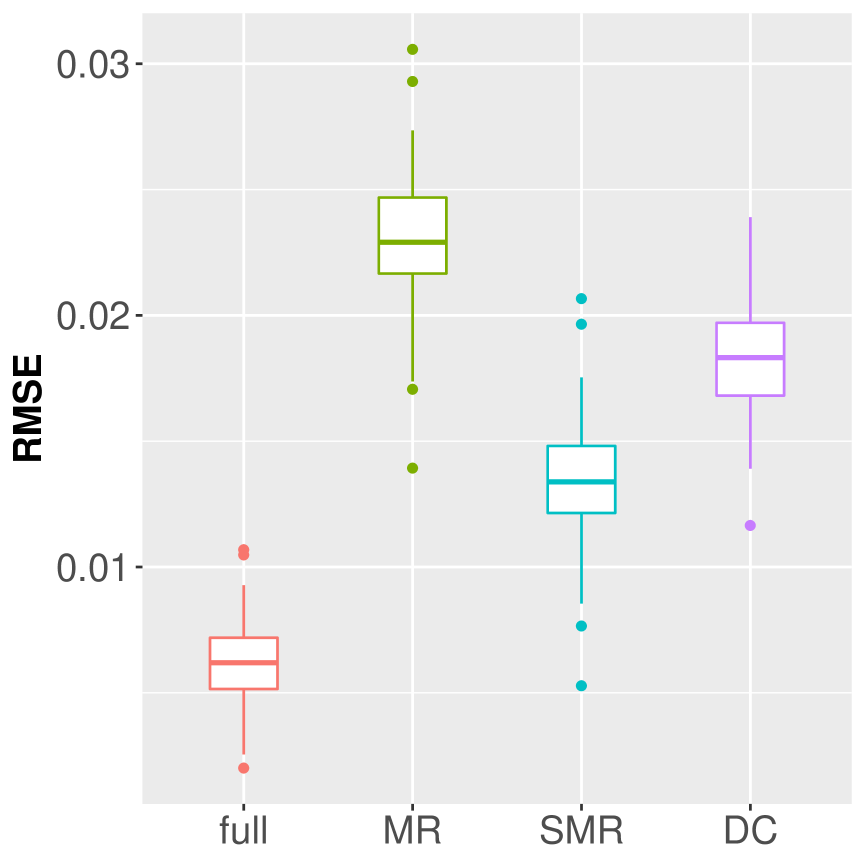

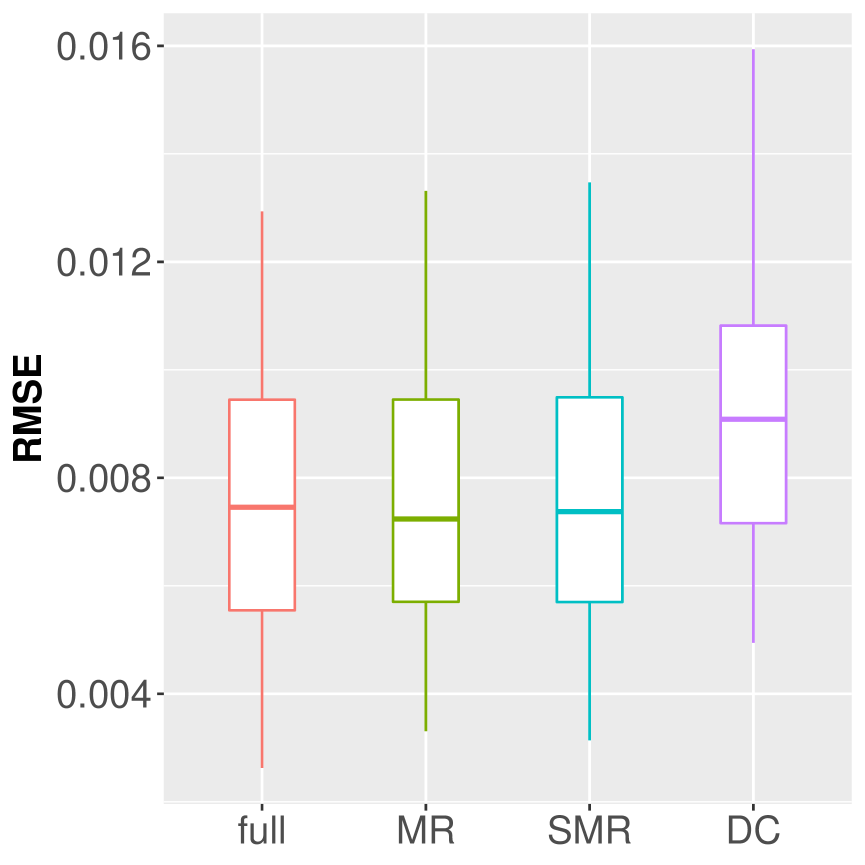

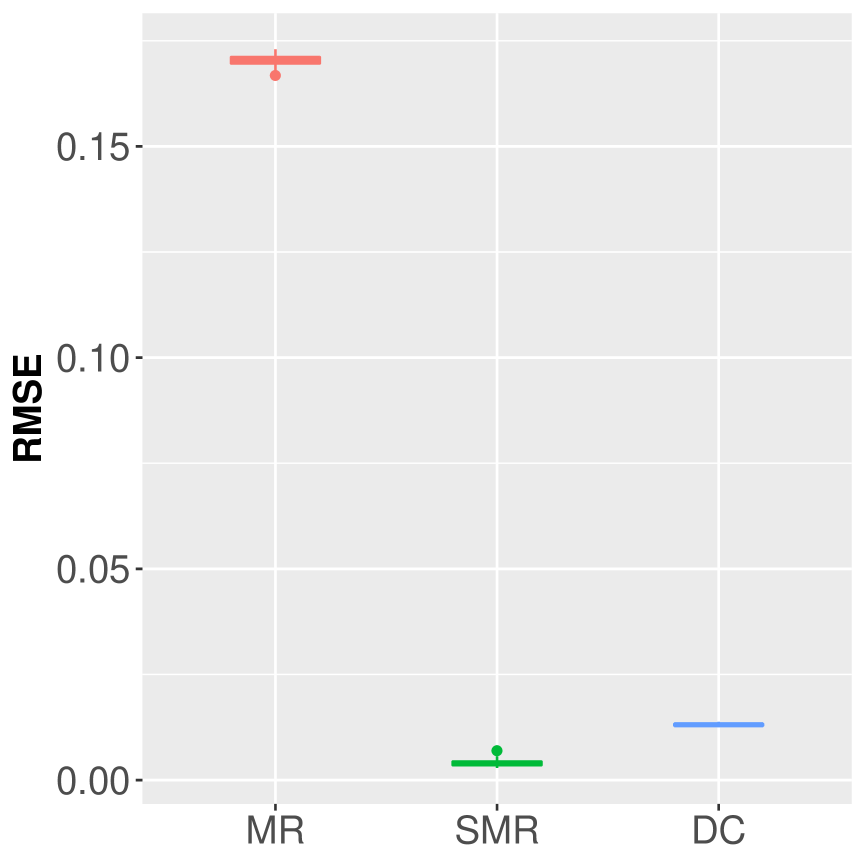

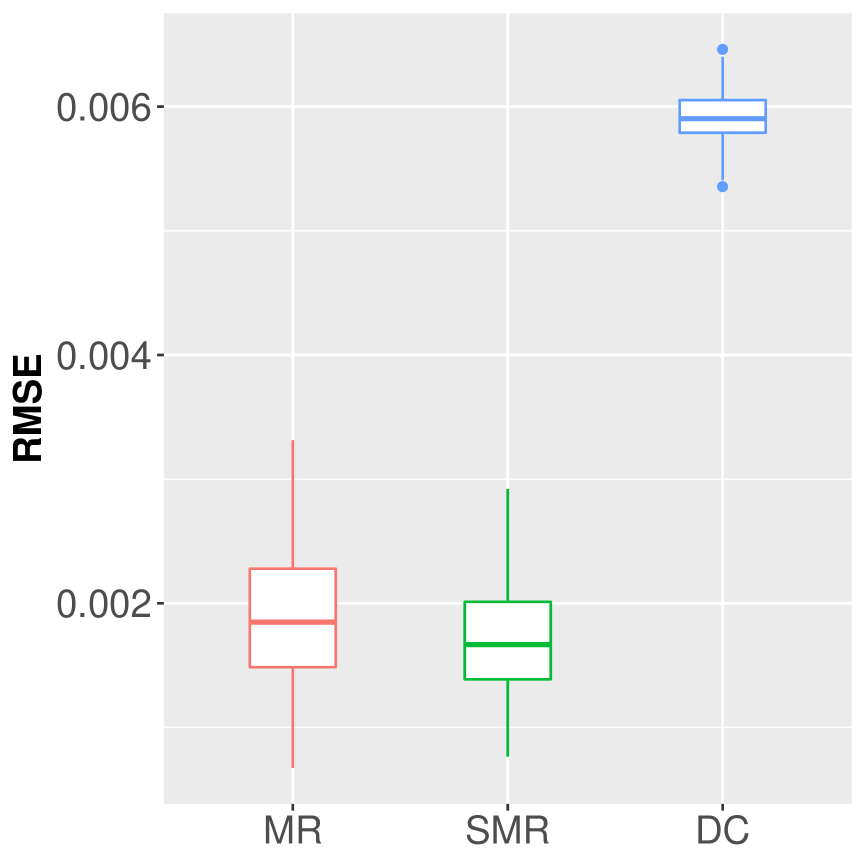

To reveal the performance of SMR visually over sample size , we use the first simulation setup mzNormal for illustration purpose, varying . For MR and SMR, the number of blocks is fixed at with a -means partition. For the divide-and-conquer method, the block size typically restricted by the computer memory and thus will not change as increases. For illustration purpose, we fix the same block size as in Section 3.2. As increases, the number of blocks for the divide-and-conquer method increases proportionally.

Figure 1 (see also Table 4) shows how much those methods benefit from increased sample size over 100 simulations for each . Figure 1(a) shows that in terms of RMSE from the true parameter value, SMR’s estimate is comparable with the full data estimate and converges to much faster than other methods. Figure 1(b) shows that SMR’s estimate quickly gets closer to the full data estimate as increases, while other methods’ estimates do not show a clear pattern getting closer. This simulation study confirms our conclusion in Section 3.5.

| RMSE from true | RMSE from full | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Full data | MR | SMR | Aopt | DC | MR | SMR | Aopt | DC | |

| 11.9 (3.5) | 21.2 (3.3) | 13.5 (3.6) | 23.6 (7.1) | 13.4 (3.5) | 17.8 (1.1) | 5.7 (1.7) | 20.1 (6.0) | 6.8 (0.4) | |

| 3.7 (1.1) | 18.3 (1.0) | 4.2 (1.2) | 20.4 (5.7) | 7.9 (1.1) | 17.9 (0.3) | 1.9 (0.6) | 20.2 (5.7) | 6.9 (0.1) | |

| 1.1 (0.3) | 17.9 (0.3) | 1.3 (0.4) | 19.5 (5.2) | 7.0 (0.3) | 17.9 (0.1) | 0.7 (0.2) | 19.3 (5.1) | 6.9 (0.0) | |

| - | 17.9 (0.1) | 0.6 (0.7) | 19.8 (5.0) | 6.9 (0.1) | - | - | - | - | |

-

•

Notes: Logistic model; predictor distribution: mzNormal;

-

•

MR, SMR: -means with ; DC: observations per block; Aopt: subsample size;

-

•

Full data estimate is not available at due to memory limit

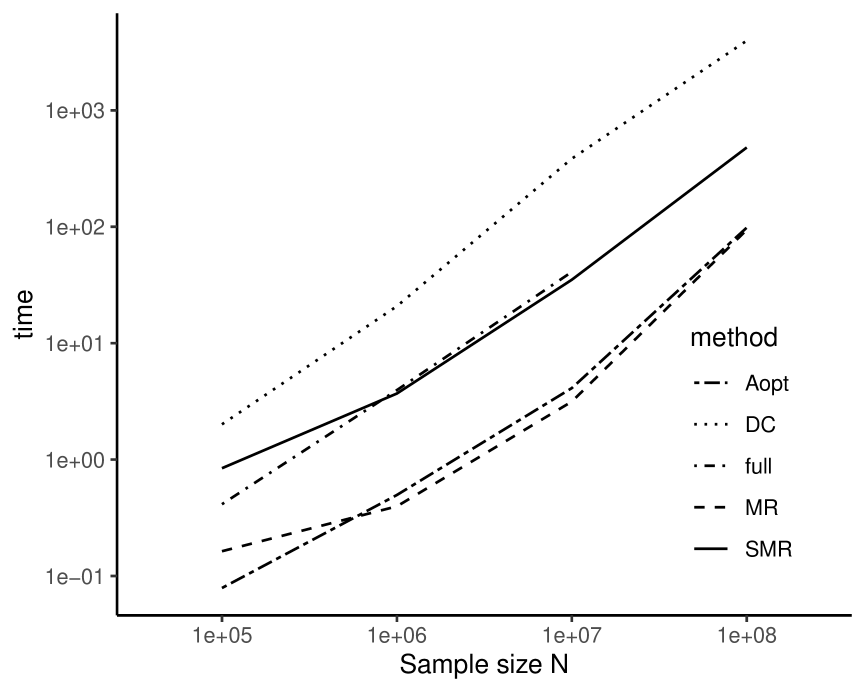

3.6 CPU Time

We use R (version 3.6.1) for all simulation studies listed in this paper. For the IBOSS (Wang et al., 2019) and A-optimal (Wang et al., 2018) subsampling methods, we use the R functions provided by the authors. We also use data.table format in R package data.table for calculating representatives or fitting by group, and KMeans_arma in R package ClusterR for faster -means clustering. All computations are carried out on a single thread of a MAC Pro running macOS 10.15.6 with 3.5 GHz 6-Core Intel Xeon E5 and 32GB 1866 MHz DDR3 memory.

The CPU time costs for MR and 1-iteration SMR with a given -means () partition, A-optimal subsampling with subsample size , and divide-and-conquer with random blocks are shown in Table A.7 and Figure A.5 in the Supplementary Material. With the given partition, MR is comparable to A-optimal subsampling method in terms of computational time; SMR is a little slower than MR but faster than the divide-and-conquer method.

One drawback of -means clustering algorithm is that its time cost grows fast as increases. In practice, we recommend a subset clustering strategy. That is, the clustering centers are determined by a subset of data points (), and the partition of the full data is determined by measuring the distance between the data points and the centers. Since the predetermined mainly depends on the number of predictors, not the sample size , the time cost of subset clustering is . According to our simulation study (see Section A.7 of the Supplementary Material), the subset clustering strategy can significantly reduce the clustering time cost, while keeping the efficiency of representative approaches.

4 A Case Study: Airline On-time Performance Data

The Airline on-time performance data for the US domestic flights of arrival time from October 1987 to December 2019 were collected from the Bureau of Transportation Statistics (https://www.transtats.bts.gov/) as a real example for big data analysis. The original dataset consists of 387 csv files with the total number of records (see Table A.11 in the Supplementary Material for more details). After cleaning, the total number of valid records is .

For illustration purpose, we consider a main-effects logistic regression model for binary response ArrDel15 (arrival delay for minutes or more, 1=YES) with three categorical covariates and one continuous covariate: QUARTER (season, ) instead of MONTH for simplification purpose; DayOfWeek (day of week, ); DepTimeBlk (departure time block, ) following the convention of the O’Hare International Airport; and DISTANCE (distance of flight, miles). More details about the data and the fitted models could be found in Section A.9 of the Supplementary Material.

In order to evaluate the performance of MR and SMR given that the full data estimate is not available, we choose the MR estimate of the main-effects logistic model on the last 5 years’ data (from January 2015 to December 2019) as the “oracle” regression coefficients (denoted by , see Table A.9 in the Supplementary Material), and simulate 10 independent replicates of responses using the logistic model with the oracle parameter values .

To show how MR and SMR work on the natural partition, we treat each data file (labeled by MONTH) as a node and prohibit raw data exchanging between nodes. Note that the natural partition in this example is pre-determined. The data from different nodes follow different distributions since the predictor QUARTER is a constant in each node but varies across different nodes. We further split each data file into sub-partitions by cutting the only continuous covariate DISTANCE at equal-depth points and combining distinct values of DayOfWeek and DepTimeBlk.

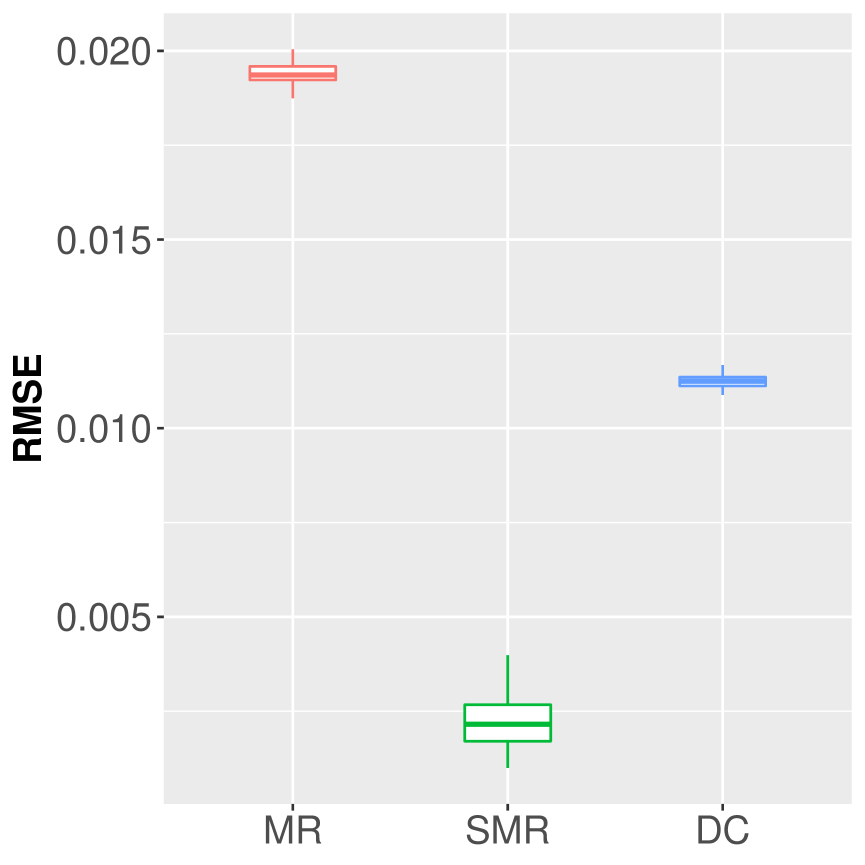

In order to show the change of estimate accuracy along with increased data size, we run a sequence of four experiments using the first months, months, months and all months of data, respectively. In each experiment, we obtain the full data estimate (not available for months and months due to too big data size), as well as the MR and SMR estimates, which are listed in Table 5. The average and standard deviation (std) of RMSEs are obtained from independent simulations.

In terms of RMSE from the oracle (see Table 5), MR and SMR perform as good as the full data estimate for 60 months and 120 months. The main reason is that the oracle coefficient of the only continuous predictor DISTANCE is as small as . Even multiplied by the largest value of DISTANCE, , the contribution of DISTANCE is still less than , which is too small compared with the oracle intercept . In other words, this scenario is fairly close to a case where all predictors are categorical. According to Corollary 3.1, both MR and SMR estimates match the full data estimate very well. Table 5 also shows that as the data size gets bigger, including 240 months and 387 months, both MR and SMR estimates are better than the last available full data estimate obtained at 120 months.

It is interesting that if we amplify the effect of the continuous predictor DISTANCE, say enlarge its oracle coefficient from to , SMR estimate will show clearly higher accuracy than MR estimate (see Section A.9 in the Supplementary Material for more details).

| Number of months | Full | MR | SMR |

|---|---|---|---|

| 60 months | 13.768 (5.155) | 13.763 (5.164) | 13.760 (5.175) |

| 120 months | 11.391 (4.417) | 11.384 (4.423) | 11.370 (4.415) |

| 240 months | - | 10.234 (4.068) | 10.225 (4.066) |

| 387 months | - | 9.058 (3.967) | 9.051 (3.966) |

-

•

Note: Full data estimates for 240 months and 387 months are not available due to memory limit.

5 Discussion and Conclusion

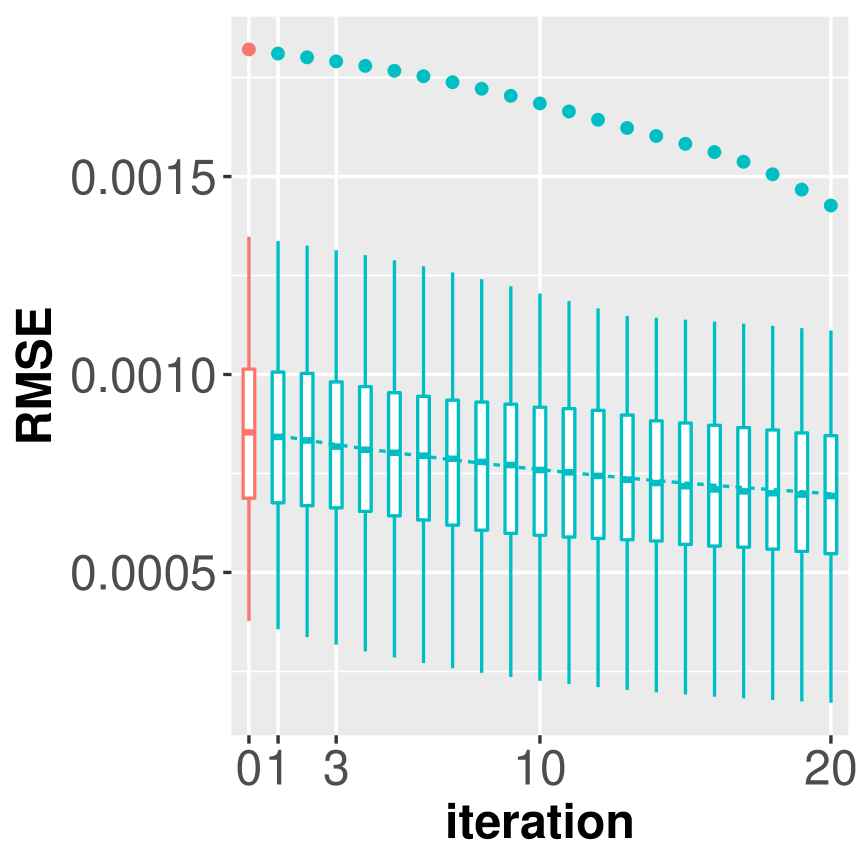

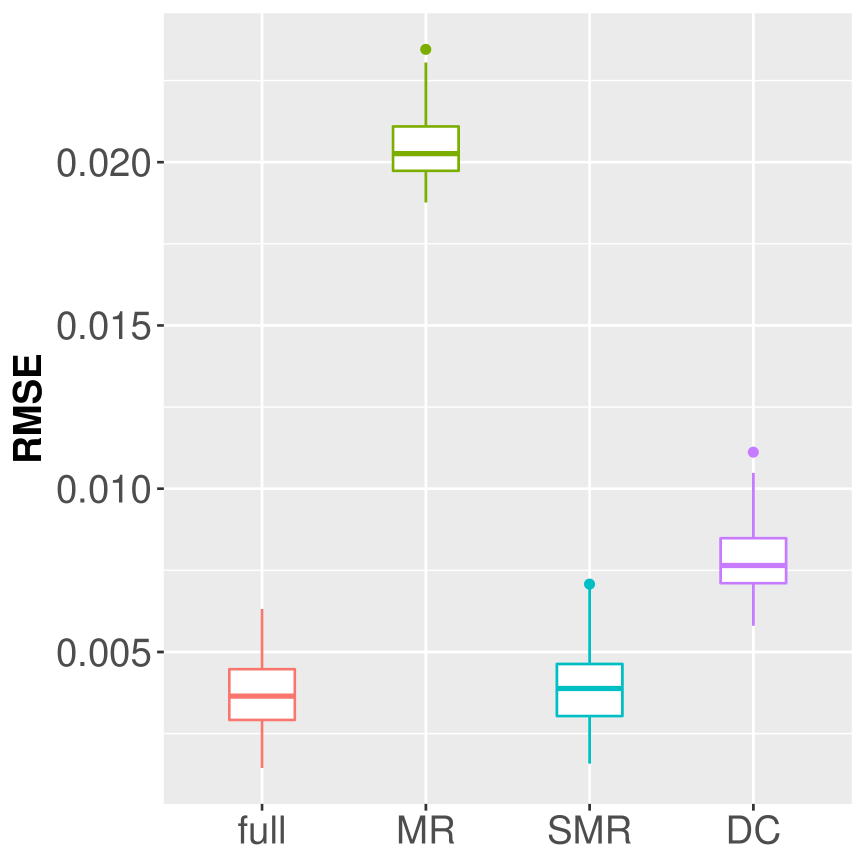

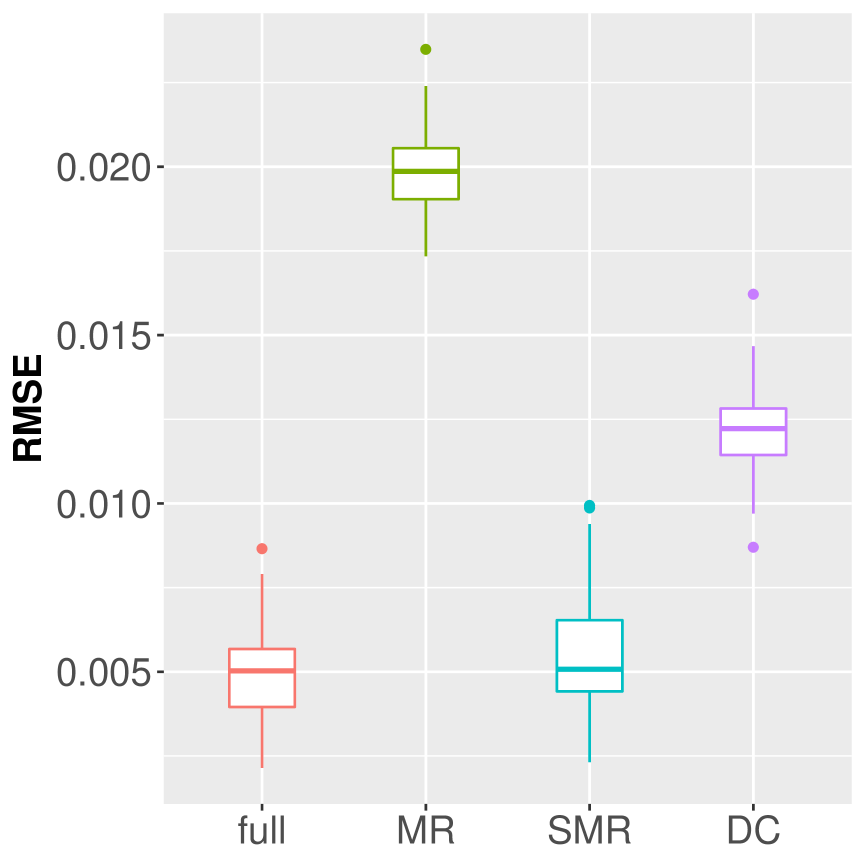

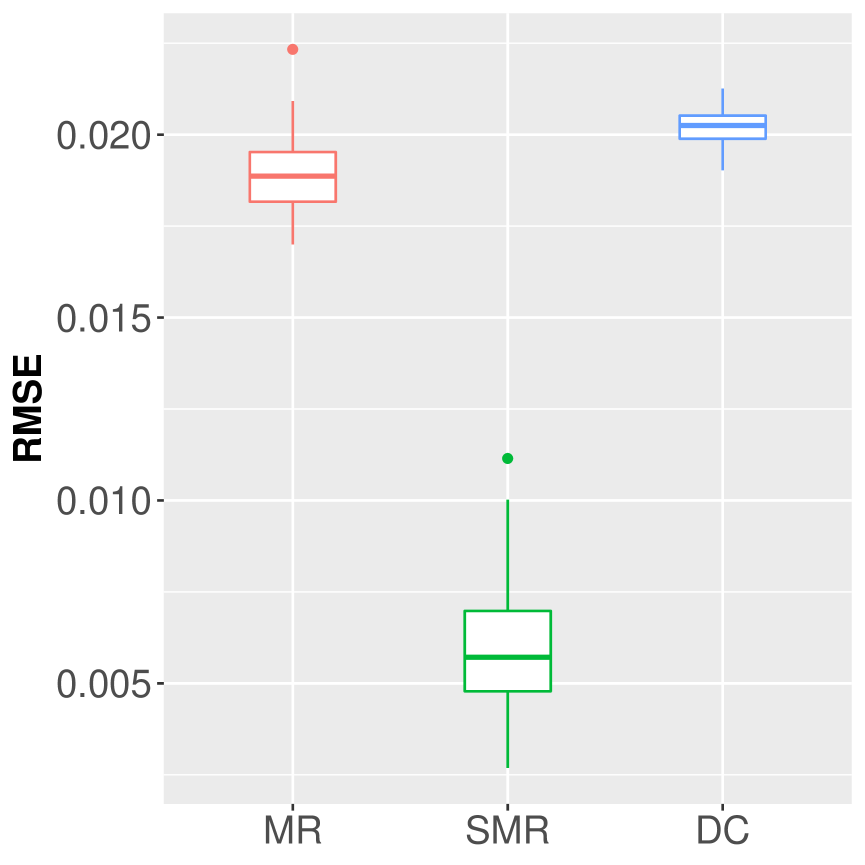

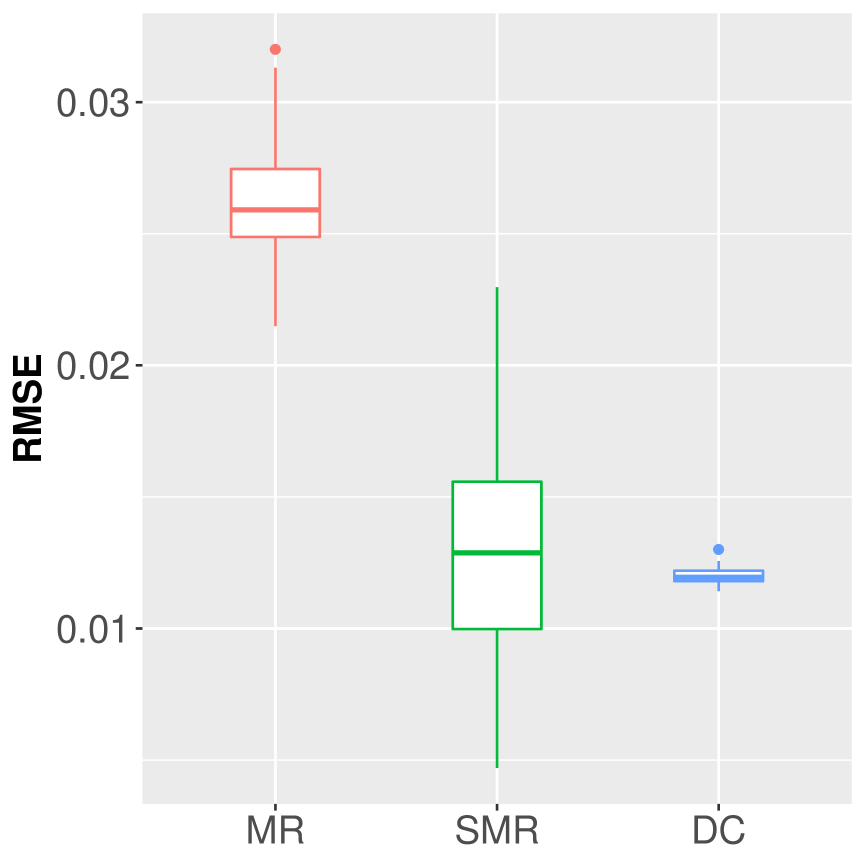

In practice, a natural partition may be provided with partially homogeneous blocks. In order to investigate the dependence of the proposed SMR approach on homogeneous partitions, we run another simulation study letting the given partition gradually change from a random partition to a homogeneous partition. More specifically, under the logistic regression model (3.5) with 7 covariates, for , we first partition the data according to the first covariates into blocks using the equal-depth criterion. We then, for each of the blocks, randomly divide the data in this block into sub-blocks. By this way, actually leads to a random partition of blocks, and corresponds to an equal-depth homogeneous partition. As increases from to , the partition becomes more and more homogeneous. The performance of MR and SMR on these partitions are displayed in Figure 2. In this simulation study, both MR and SMR are affected by the homogeneous level of the natural partition. The higher is, the better performance they have. Overall, MR seems to be the worst, which does not meet A-optimal sampler until . SMR is not as good as A-optimal one and DC when is small, while it surpasses A-optimal one at and does better than DC at . An implication is that sub-partitions are necessary for representative approaches when the natural partition is not homogeneous.

When all predictors of the GLMs are categorical or discrete, the best solution would be partitioning the data according to distinct predictor values if applicable. In this case, , both the MR and SMR estimates exactly match the full data estimate.

For GLMs with flat (that is, is bounded by some moderate number), such as logit, probit, cloglog, loglog, and cauchit links for binomial models, one may check the coefficients of the continuous variables fitted by MR. If all linear predictors contributed by continuous variables are relative small comparing to the intercept or linear predictors contributed by categorical ones, then the MR estimate might be good enough. Otherwise, we recommend the SMR solution. For GLMs with unbounded or large , such as Poisson model and Gamma model, we recommend SMR over MR with a finer partition (see Section 3.5 for more detailed discussion).

Data partition, or more specifically, the maximum block size , is critical for both MR and SMR. Asymptotically, the accuracy of MR estimate depends on and will not benefit from an increased sample size unless for linear models, while the accuracy of SMR estimate can still be improved with increased sample size and fixed partition of the predictor space (see Section 3.5 and Section A.5 in the Supplementary Material for more detailed discussion).

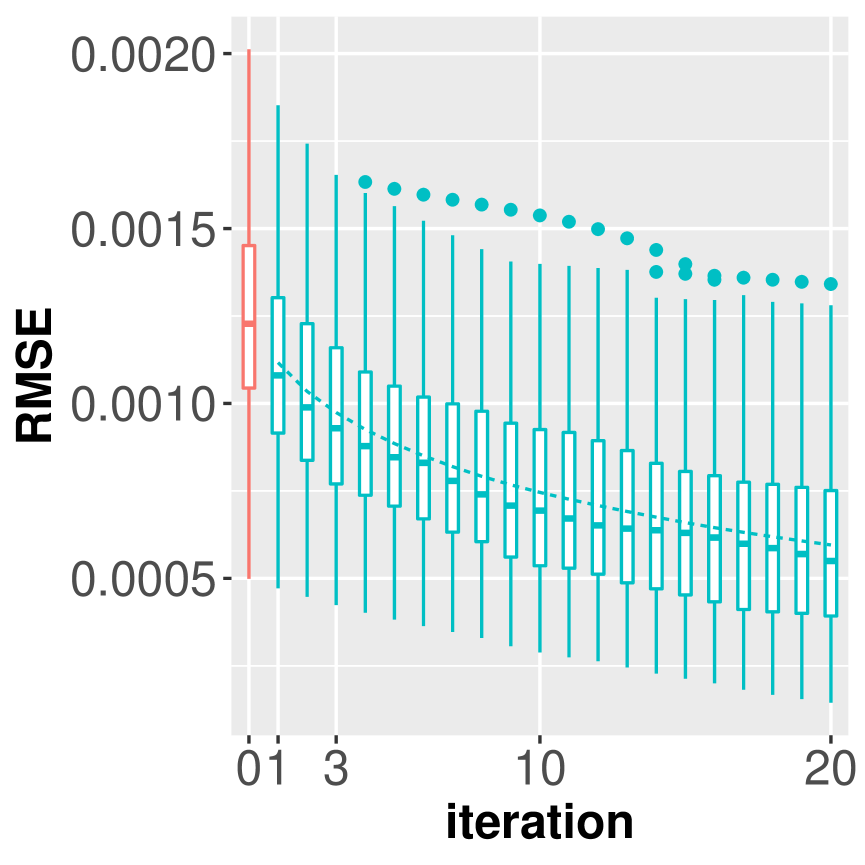

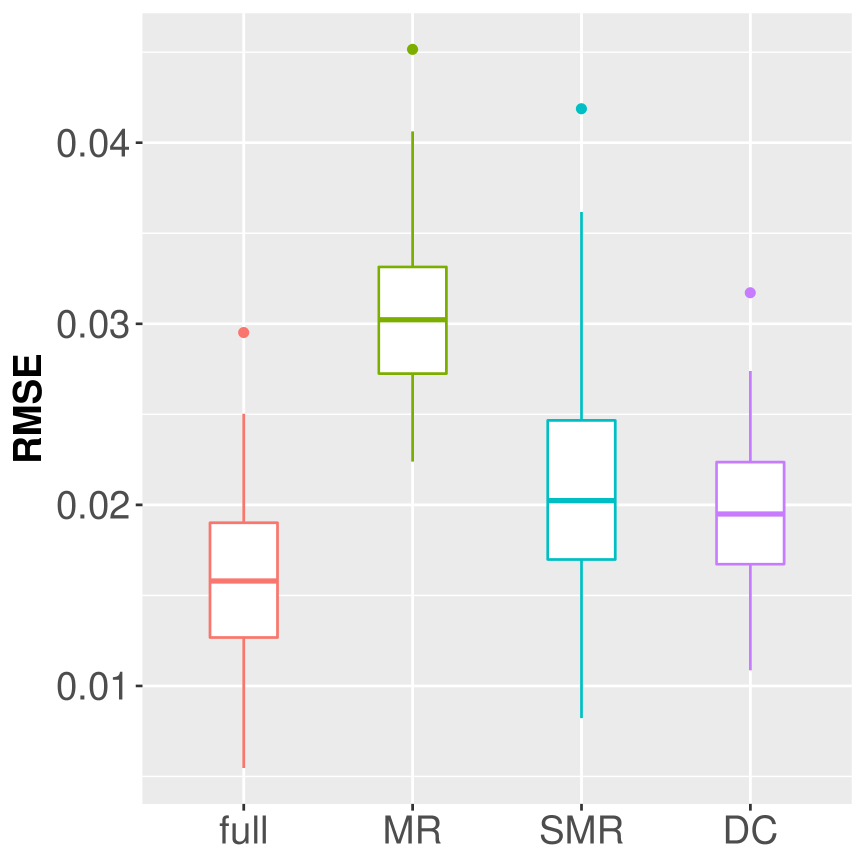

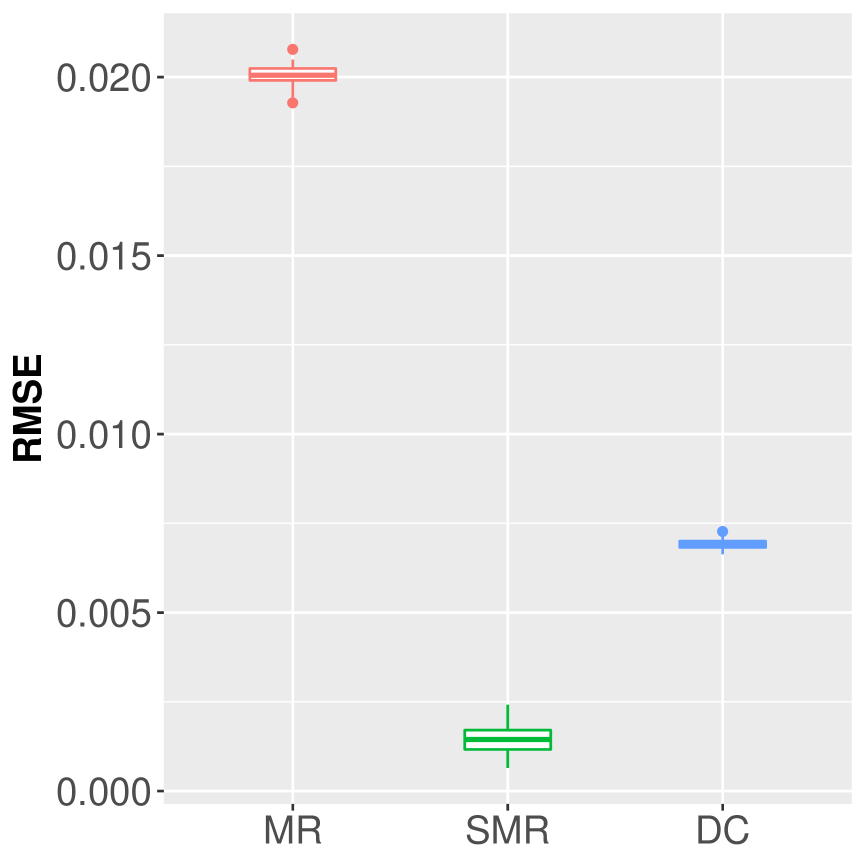

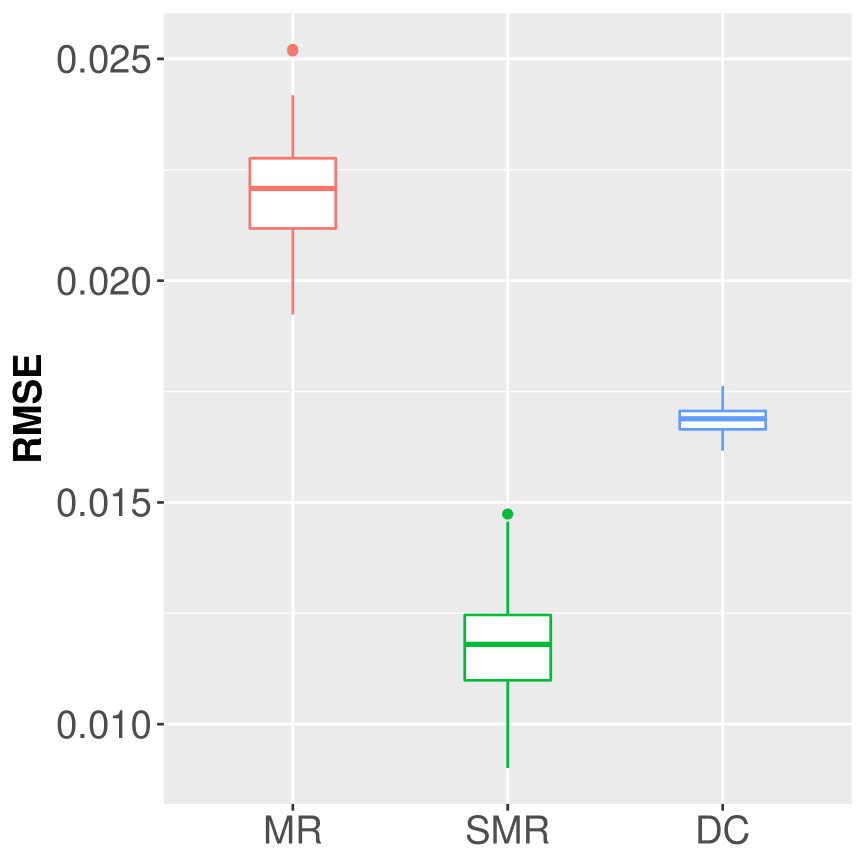

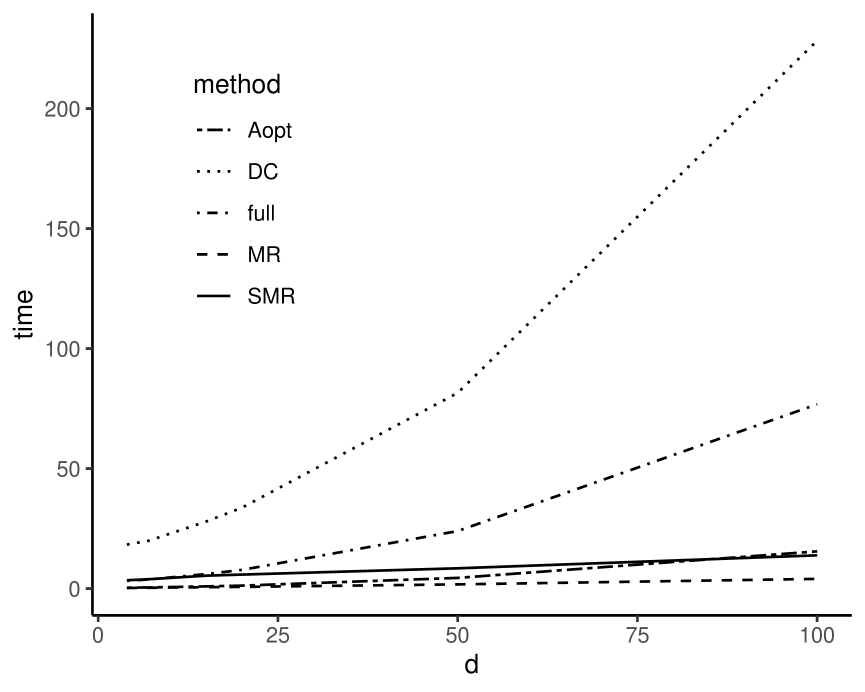

To illustrate how SMR scales with dimension , we also run simulations towards various covariate dimension using MR, SMR, A-opt, and DC. To avoid the increment of linear predictor along with dimension , we randomly generated a -dimensional for each simulation such that as the true regression coefficients. Figure 3 shows that, as the covariate dimension in the main-effects logistic model increases, the performance of the SMR estimate, using MR estimate as initial value, gets away from the full data estimate. As we expected, increases with , which leads to a challenge for both MR and SMR. It seems that A-optimal sampler is fairly robust across different dimensions. One strategy for solving large- problems is to use A-optimal estimate as the initial parameter value for SMR iterations.

When is large, it is also difficult to reduce the maximum block size efficiently due to the curse of dimensionality. How we can obtain an efficient partition or do variable selection for large dimension is critical for representative approaches, but is out of the scope of this paper.

The framework of representative approaches allows the data analysts to work with the representative data instead of the raw data. In the scenario where different sources of data are owned by different individuals, organizations, companies, or countries (also regarded as nodes) with competing interests, the exchange of raw data between nodes might be prohibited. In this scenario, neither divide-and-conquer nor subsampling approaches are feasible, while representative approaches may provide an ideal solution since the representative data points typically could not be used to track the raw data.

Compared with the CoCoA algorithms (Smith et al., 2018), the representative approaches introduced in this paper also require a central server to collect representative data points and process regression analysis. Utilizing a similar idea as in the COLA algorithm (He et al., 2018), the representative approaches may be applied to decentralized environment as well.

Appendix

Acknowledgments

This work was supported in part by the U.S. National Science Foundation. The authors thank the Editor, the Associate Editor and the referee for their constructive comments and suggestions. The authors also thank Mr. Lie He from the École Polytechnique Fédérale de Lausanne (EPFL) in Switzerland for his help with the COLA package.

References

- Battey et al. (2018) Battey, H., J. Fan, H. Liu, J. Lu, and Z. Zhu, 2018: Distributed testing and estimation under sparse high dimensional models. Annals of Statistics, 46(3), 1352–1382.

- Bowman (January 6, 2017) Bowman, C., January 6, 2017: Data localization laws: an emerging global trend. Jurist, https://www.jurist.org/commentary/2017/01/Courtney-Bowman-data-localization/.

- Chen et al. (2019) Chen, X., W. Liu, and Y. Zhang, 2019: Quantile regression under memory constraint. Annals of Statistics, 47(16), 3244–3273.

- Chen and Xie (2014) Chen, X. and M. G. Xie, 2014: A split-and-conquer approach for analysis of extraordinarily large data. Statistica Sinica, 24(4), 1655–1684.

- Dobson and Barnett (2018) Dobson, A. and A. Barnett, 2018: An Introduction to Generalized Linear Models. Chapman & Hall/CRC, 4th ed.

- Fahad et al. (2014) Fahad, A., N. Alshatri, Z. Tari, A. Alamri, I. Khalil, A. Zomaya, S. Foufou, and A. Bouras, 2014: A survey of clustering algorithms for big data: Taxonomy and empirical analysis. IEEE Transactions on Emerging Topics in Computing, 2, 267–279.

- Fang and Wang (1994) Fang, K. and Y. Wang, 1994: Number-theoretic methods in statistics. Chapman & Hall.

- Fefer (March 26, 2020) Fefer, R. F., March 26, 2020: Data flows, online privacy, and trade policy (crs report no. rl45584). Congressional Research Service, https://crsreports.congress.gov/product/pdf/R/R45584. Accessed October 11, 2020.

- Flury (1990) Flury, B., 1990: Principal points. Biometrika, 77, 33–41.

- He et al. (2018) He, L., A. Bian, and M. Jaggi, 2018: Cola: Decentralized linear learning. Curran Associates Inc., Red Hook, NY, USA, NIPS’18, pp. 4541–4551.

- Huggins et al. (2017) Huggins, J., R. Adams, and T. Broderick, 2017: Pass-glm: polynomial approximate sufficient statistics for scalable bayesian glm inference. Advances in Neural Information Processing Systems, 3611–3621.

- Kane et al. (2013) Kane, M., J. Emerson, and S. Weston, 2013: Scalable strategies for computing with massive data. Journal of Statistical Software, 55, 1–19.

- Kanniappan and Sastry (1983) Kanniappan, P. and S. M. Sastry, 1983: Uniform convergence of convex optimization problems. Journal of Mathematical Analysis and Applications, 96.1, 1–12.

- Keeley et al. (2020) Keeley, S., D. Zoltowski, Y. Yu, S. Smith, and J. Pillow, 2020: Efficient non-conjugate gaussian process factor models for spike count data using polynomial approximations. In International Conference on Machine Learning, PMLR, pp. 5177–5186.

- Kotsiantis and Kanellopoulos (2006) Kotsiantis, S. and D. Kanellopoulos, 2006: Discretization techniques: A recent survey. GESTS International Transactions on Computer Science and Engineering, 32(1), 47–58.

- Lee et al. (2017) Lee, J. D., Q. Liu, Y. Sun, and J. E. Taylor, 2017: Communication-efficient sparse regression. Journal of Machine Learning Research, 18(1), 115–144.

- Lin and Rosasco (2017) Lin, J. and L. Rosasco, 2017: Optimal rates for multi-pass stochastic gradient methods. Journal of Machine Learning Research, 18, 1–47.

- Lin and Xi (2011) Lin, N. and R. Xi, 2011: Aggregated estimating equation estimation. Statistics and Its Interface, 4, 73–83.

- Ma and Sun (2014) Ma, P. and X. Sun, 2014: Leveraging for big data regression. WIREs Computational Statistics, 7, 70–76.

- Mak and Joseph (2017) Mak, S. and V. Joseph, 2017: Projected support points: a new method for high-dimensional data reduction. arXiv preprint arXiv:1708.06897.

- Mak and Joseph (2018) —, 2018: Support points. Annals of Statistics, 46, 2562–2592.

- McCullagh and Nelder (1989) McCullagh, P. and J. Nelder, 1989: Generalized Linear Models. Chapman and Hall/CRC, 2nd ed.

- Özsu and Valduriez (2011) Özsu, M. and P. Valduriez, 2011: Principles of Distributed Database Systems. Springer Science & Business Media, 3rd ed.

- Pakhira (2014) Pakhira, M., 2014: A linear time-complexity k-means algorithm using cluster shifting. 2014 Sixth International Conference on Computational Intelligence and Communication Networks, 1047–1051.

- Raykov et al. (2016) Raykov, Y., A. Boukouvalas, F. Baig, and M. Little, 2016: What to do when k-means clustering fails: A simple yet principled alternative algorithm. PLoS ONE, 11, e0162259.

- Resnick (1999) Resnick, S., 1999: A Probability Path. Birkhäuser, Boston, MA.

- Schechner and Glazer (September 9, 2020) Schechner, S. and E. Glazer, September 9, 2020: Ireland to order facebook to stop sending user data to u.s. The Wall Street Journal, https://www.wsj.com/articles/ireland-to-order-facebook-to-stop-sending-user-data-to-u-s-11599671980.

- Schifano et al. (2016) Schifano, E. D., J. Wu, C. Wang, J. Yan, and M. H. Chen, 2016: Online updating of statistical inference in the big data setting. Technometrics, 58(3), 393–403.

- Shi et al. (2018) Shi, C., W. Lu, and R. Song, 2018: A massive data framework for m-estimators with cubic-rate. Journal of the American Statistical Association, 113(524), 1698–1709.

- Shin et al. (2014) Shin, S. J., Y. Wu, H. H. Zhang, and Y. Liu, 2014: Probability‐enhanced sufficient dimension reduction for binary classification. Biometrika, 70(3), 546–555.

- Shin et al. (2017) —, 2017: Principal weighted support vector machines for sufficient dimension reduction in binary classification. Biometrika, 104, 1, 67–81.

- Singh et al. (2005) Singh, K., M. G. Xie, and W. Strawderman, 2005: Combining information from independent sources through confidence distributions. Annals of Statistics, 33(1), 159–183.

- Smith et al. (2018) Smith, V., S. Forte, M. Chenxin, M. Takáč, M. I. Jordan, and M. Jaggi, 2018: Cocoa: A general framework for communication-efficient distributed optimization. Journal of Machine Learning Research, 18(230), 1–49.

- Tran et al. (2015) Tran, D., P. Toulis, and E. Airoldi, 2015: Stochastic gradient descent methods for estimation with large data sets. arXiv preprint arXiv:1509.06459.

- Vogel (February 10, 2014) Vogel, P. S., February 10, 2014: Will data localization kill the internet? eCommerce Times, https://www.ecommercetimes.com/story/79946.html.

- Wang et al. (2016) Wang, C., M. Chen, E. Schifano, J. Wu, and J. Yan, 2016: Statistical methods and computing for big data. Statistics and Its Interface, 9, 399–414.

- Wang et al. (2019) Wang, H., M. Yang, and J. Stufken, 2019: Information-based optimal subdata selection for big data linear regression. Journal of the American Statistical Association, 114:525, 393–405.

- Wang et al. (2018) Wang, H., R. Zhu, and P. Ma, 2018: Optimal subsampling for large sample logistic regression. Journal of the American Statistical Association, 113, 829–844.

- Xie et al. (2011) Xie, M., K. Singh, and W. Strawderman, 2011: Confidence distributions and a unifying framework for meta-analysis. Journal of the American Statistical Association, 106, 320–333.

- Zhao et al. (2016) Zhao, T., G. Cheng, and H. Liu, 2016: A partially linear framework for massive hetero- geneous data. Annals of Statistics, 44(4), 1400–1437.

- Zoltowski and Pillow (2018) Zoltowski, D. and J. Pillow, 2018: Scaling the poisson glm to massive neural datasets through polynomial approximations. Advances in Neural Information Processing Systems, 3517–3527.

Score-Matching Representative Approach for

Big Data Analysis with Generalized Linear Models

Keren Li and Jie Yang

Supplementary Material

A.1 SMR and MR for Linear Model

The simulation study in this section is based on the linear regression model

| (A.1) |

where and ’s are iid . Note that linear regression models are actually special cases of the generalized linear models with normally distributed responses and identity link (see Table 1). Analogue to the simulation setup in Section 3.2, we take , , , and , as well as the same distributions for simulating . The main-effects predictors in (A.1) are for illustration purpose. The representative approach can actually work with general predictors including, for example, interactions of covariates.

In the absence of a natural partition, we again use an equal-depth partition with splits for each predictor, and a -means partition with the number of blocks .

| Simulation | Full | Equal-depth () | -means () | |||||

|---|---|---|---|---|---|---|---|---|

| setup | data | Mid | Med | MR | SMR | MR | SMR | IBOSS |

| mzNormal | 1.2 (0.3) | 239.4 (2.8) | 28.7 (0.2) | 1.4 (0.4) | 1.4 (0.4) | 1.5 (0.4) | 1.5 (0.4) | 6.8 (1.9) |

| nzNormal | 1.2 (0.3) | 239.4 (2.8) | 28.7 (0.2) | 1.4 (0.4) | 1.4 (0.4) | 1.6 (0.4) | 1.5 (0.4) | 6.8 (1.9) |

| ueNormal | 0.5 (0.2) | 251 (3.4) | 43.6 (0.3) | 0.5 (0.2) | 0.5 (0.2) | 0.9 (0.6) | 0.9 (0.6) | 2.3 (1.0) |

| mixNormal | 1.3 (0.3) | 202.1 (2.9) | 16.4 (0.2) | 1.6 (0.5) | 1.6 (0.5) | 1.5 (0.4) | 1.5 (0.4) | 7.5 (2.0) |

| 7.4 (2.1) | 483 (4.2) | 106.8 (1.7) | 10.3 (2.8) | 10.2 (2.8) | 11.1 (3.1) | 10.7 (3.1) | 12.0 (4.1) | |

| EXP | 1.9 (0.5) | 368.9 (4.1) | 77 (1.1) | 2.2 (0.6) | 2.2 (0.6) | 2.3 (0.6) | 2.1 (0.6) | 6.0 (1.8) |

| BETA | 2.9 (0.7) | 27.7 (0.9) | 12.9 (0.9) | 2.9 (0.8) | 2.9 (0.8) | 3.7 (0.9) | 3.3 (0.9) | 18.2 (5.2) |

-

•

Mid: mid-point representative; Med: median representative;

-

•

IBOSS: information-based optimal subdata selection.

Table A.1 shows both the average and standard deviation of the root mean squared errors (RMSEs, ) between the estimated parameter value ’s and the true value ’s across different simulation settings and each with 100 independent simulations.

In terms of RMSE, Table A.1 clearly shows that MR outperforms both mid-point (Mid) and median (Med) representative approaches, as well as information-based optimal subdata selection (IBOSS) proposed by Wang et al. (2019) with subsamples, which is larger than the largest possible number of non-empty blocks or representatives. Compared with the true parameter value, MR estimates are comparable even with the estimates based on the full data.

From Table A.1, we also see that the RMSE of MR based on the equal-depth partition obtained from non-empty blocks or representatives on average are comparable with the RMSE of MR from the -means partition with representatives. It implies that representative approaches based on clustered partition are more efficient. Actually, the maximum distance within data blocks , may play an important role in extracting data information more efficiently. The following theorem shows that for linear models, the MR estimate is unbiased. It is also asymptotically efficient as .

Theorem A.1.

Suppose is positive definite. For linear model , , with iid , the MR estimator

has mean and covariance given that , where the induced matrix norm is the largest eigenvalue for positive semi-definite matrices. Furthermore, , as goes to zero.

Proof.

of Theorem A.1: Recall that is the th predictor vector, is the th response variable, ; and is the response vector of the full data, is the predictor matrix of the full data.

Given a data partition of , we denote by , , the predictor matrix, the response vector and the error vector of the th block, , respectively. Then , which is positive definite according to our assumption.

Denote by the induced matrix norm defined by , which is actually the square root of the largest eigenvalue of . If is positive semi-definite, then is simply its largest eigenvalue.

Denote by . Then for some ’s satisfying . By the definition of the matrix norm,

Therefore we have

| (A.2) |

Denote by and the smallest eigenvalues of and , respectively. According to our assumption, regardless of the partition. By (A.2), we have if . That is, is invertible when is sufficiently small.

Therefore, we have the weighted least squares (WLS) estimate from mean representative dataset

where is an vector of all ’s, and is an matrix of all ’s. Then the MR estimator is unbiased since

and the covariance matrix of the MR estimator is given by

and the matrix norm of difference between the Fisher information matrices of OLS and MR is given by

Consider the induced matrix norm of difference between covariance matrices of OLS and MR estimators

The last “” holds if . Therefore, as goes to zero, converges to in terms of the largest eigenvalue. ∎

Best Partition: From the proof of Theorem A.1, we know that the difference between the Fisher information matrices of and is actually bounded by up to a constant, where is the th block size. Fixing the number of blocks, a natural question is to find a partition that minimizes the upper bound .

Assume that the average density of the th block is , such that, for some constant and . Typically while in general depends on the mapping from the covariate vector to the predictor vector . Then the goal is to minimize subject to . Let . The goal is equivalent to minimize

| (A.3) |

subject to . Plugging into (A.3) and differentiating it with respect to , we get

For ,

, which implies . , which further implies

Therefore, the partition minimizing the upper bound satisfies

which is the same for . That is, the best partition keeps all the blocks about the same size. It explains why a -means partition works usually better than a equal-depth partition for MR in linear regressions, because it minimizes (Raykov et al., 2016).

From Theorem A.1, we also see that if the grids of partition are coarse, the variance of MR estimate could be large and away from the variance of OLS.

As for the comparison between MR and SMR, in terms of the RMSEs between and (such as in Table A.1), the performances of MR and SMR are similar and both comparable with the full data estimate (shown in Table A.1). Since for practical data “true” model or “true” parameter value may not exist, a more realistic goal is to match the full data estimate .

In Table A.2, we show the RMSEs between and . It confirms the conclusions in Theorem 3.4 and Section 3.5. That is, for linear models, both MR and SMR perform very well, while SMR is slightly better. Nevertheless, when the is small (for example, in the partition obtained by -means), the global rate of convergence (see Remark 3.2) is close to 0 and the improvement from MR to SMR is significant.

It is also interesting to see different estimates on the intercept . From Table A.3, it seems that MR and SMR are among the best and comparable with the full data estimate.

| Simulation | Equal-depth () | -means () | ||

|---|---|---|---|---|

| setup | MR | SMR | MR | SMR |

| mzNormal | 0.664 (0.183) | 0.660 (0.182) | 0.761 (0.214) | 0.733 (0.207) |

| nzNormal | 0.664 (0.183) | 0.657 (0.181) | 1.067 (0.300) | 0.980 (0.299) |

| ueNormal | 0.194 (0.106) | 0.192 (0.108) | 0.723 (0.482) | 0.699 (0.472) |

| mixNormal | 0.856 (0.240) | 0.845 (0.238) | 0.858 (0.243) | 0.823 (0.237) |

| 6.793 (1.938) | 6.729 (1.942) | 7.709 (2.326) | 7.226 (2.198) | |

| EXP | 1.175 (0.291) | 1.145 (0.288) | 1.250 (0.313) | 0.974 (0.276) |

| BETA | 0.627 (0.149) | 0.610 (0.144) | 2.286 (0.650) | 1.461 (0.568) |

| Simulation setup | Full data | Mid | Med | MR | SMR | IBOSS |

|---|---|---|---|---|---|---|

| mzNormal | 0.7 | 23.8 | 0.9 | 0.7 | 0.7 | 6.1 |

| nzNormal | 1.7 | 2512.8 | 300.6 | 1.8 | 1.8 | 8.0 |

| ueNormal | 0.7 | 104.3 | 1.9 | 0.7 | 0.7 | 4.0 |

| mixNormal | 0.8 | 29.5 | 0.8 | 0.8 | 0.8 | 5.2 |

| 0.7 | 46.9 | 0.7 | 0.7 | 0.7 | 5.3 | |

| EXP | 2.2 | 661.9 | 104.2 | 2.7 | 2.7 | 9.6 |

| BETA | 2.7 | 96.3 | 44.0 | 2.7 | 2.7 | 23.5 |

A.2 Practical Number of Iterations for SMR

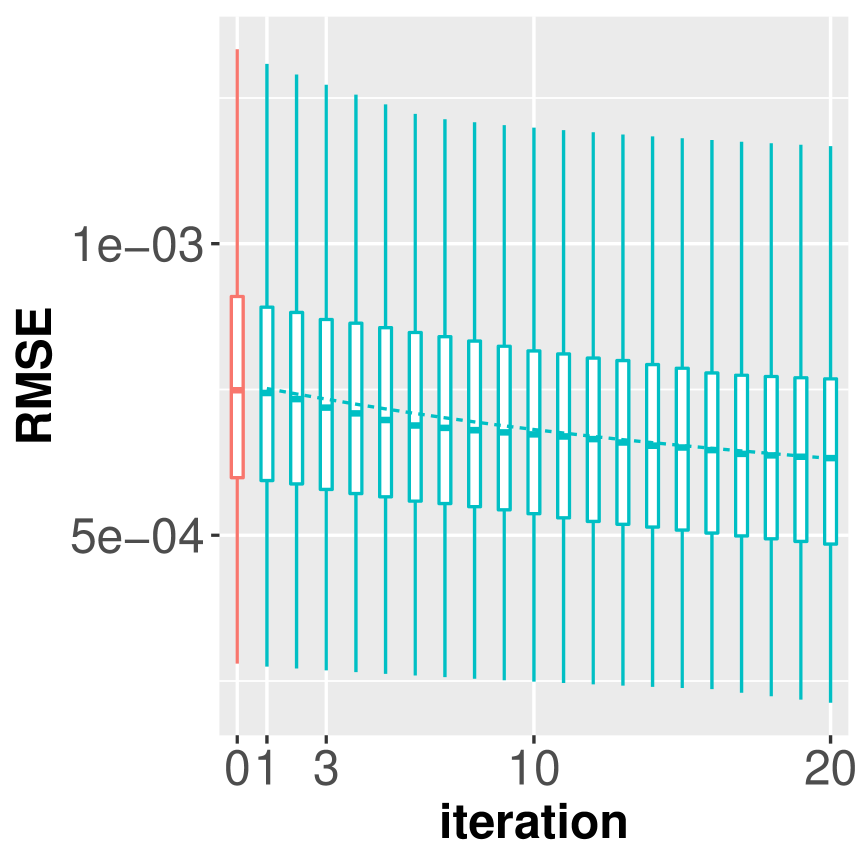

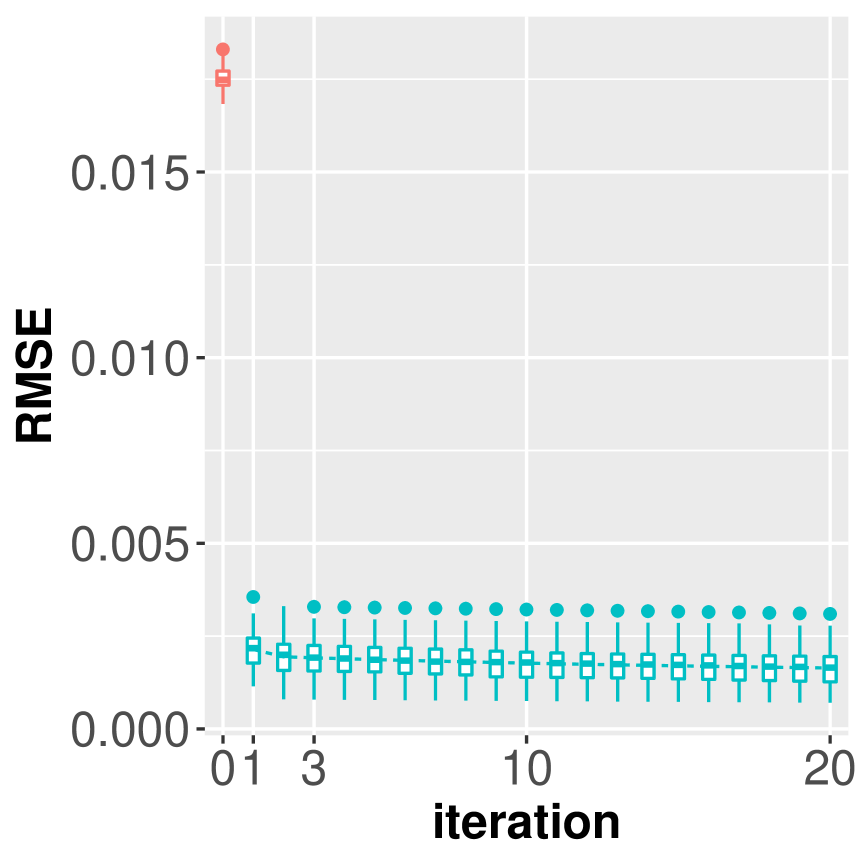

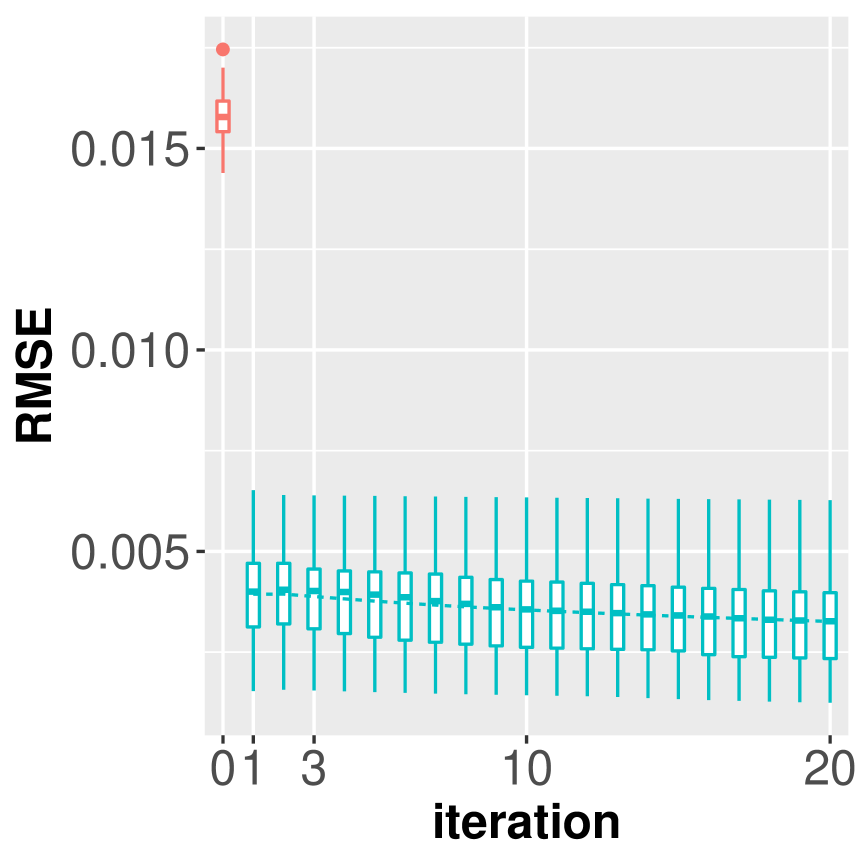

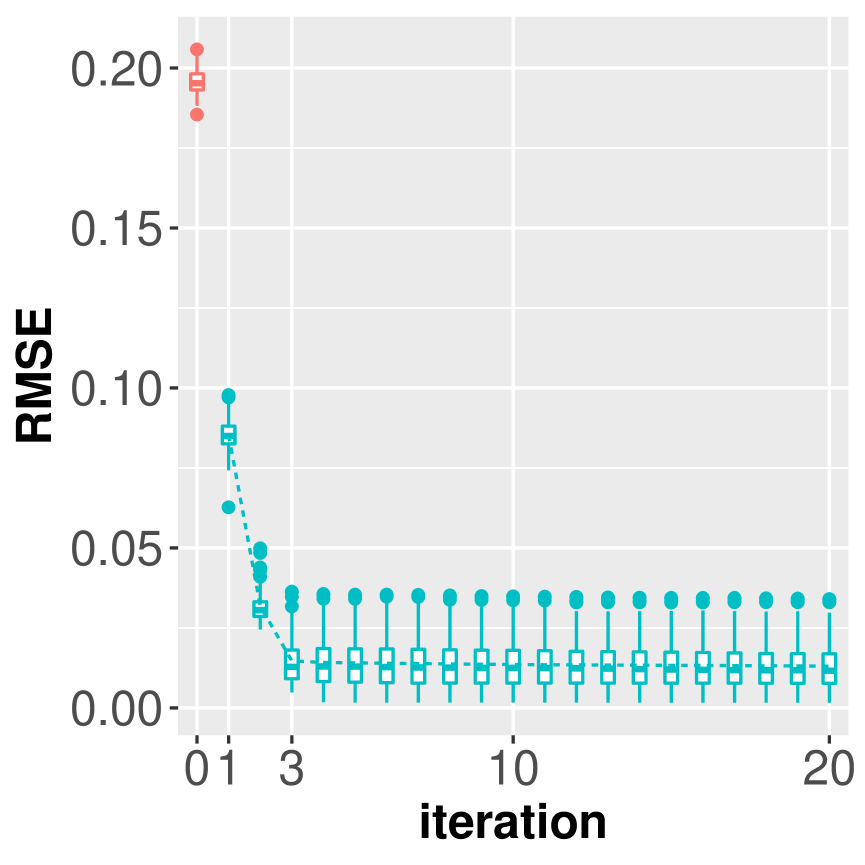

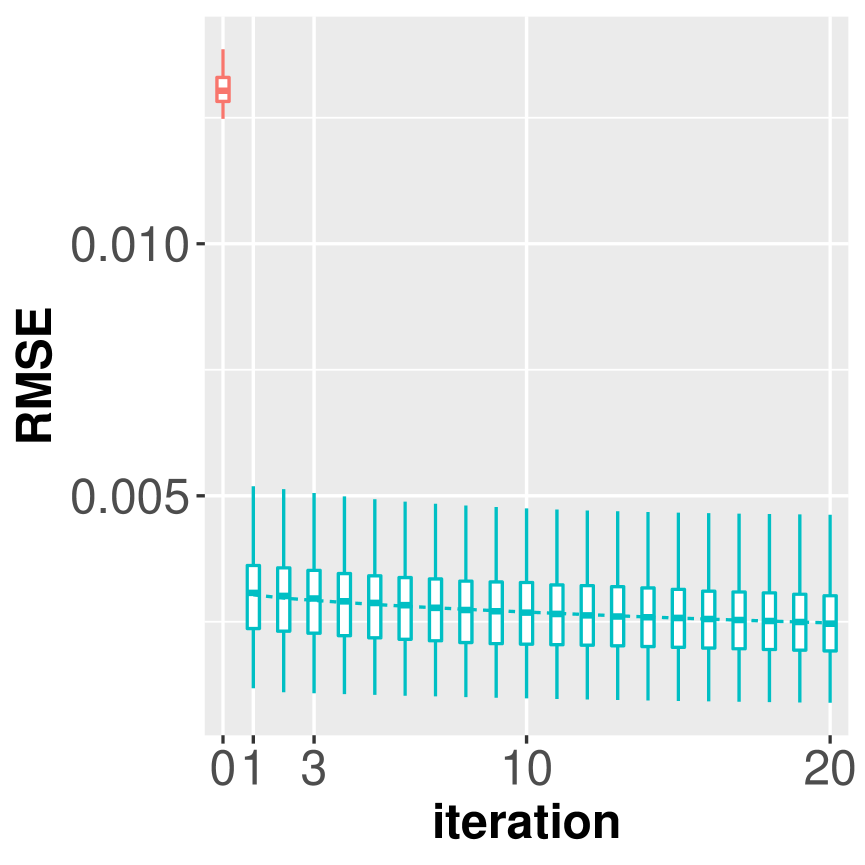

In order to determine a practical number of iterations for SMR algorithm, we simulate 100 datasets of size for each of the seven distributions of covariates in the linear model (A.1) and the logistic regression model (3.5). We apply 20 iteration steps of SMR for examining a practical number of iterations. Figure A.1 and Figure A.2 show that the iterative SMR based on a -means partition with improves the accuracy level significantly in the first 1 or 2 iterations. Starting from the 4th iteration, the relative improvements of RMSE are less than for ueNormal, and less than for other distribution settings.

For GLMs with flat such as linear model and logistic model, typically the first iteration based on the initial MR estimate improves the accuracy level significantly. For GLMs with steeper such as Poisson model with log link, we recommend (see also asymptotic properties discussed in Section 3.5).

A.3 SMR vs Divide-and-Conquer for Logistic Models

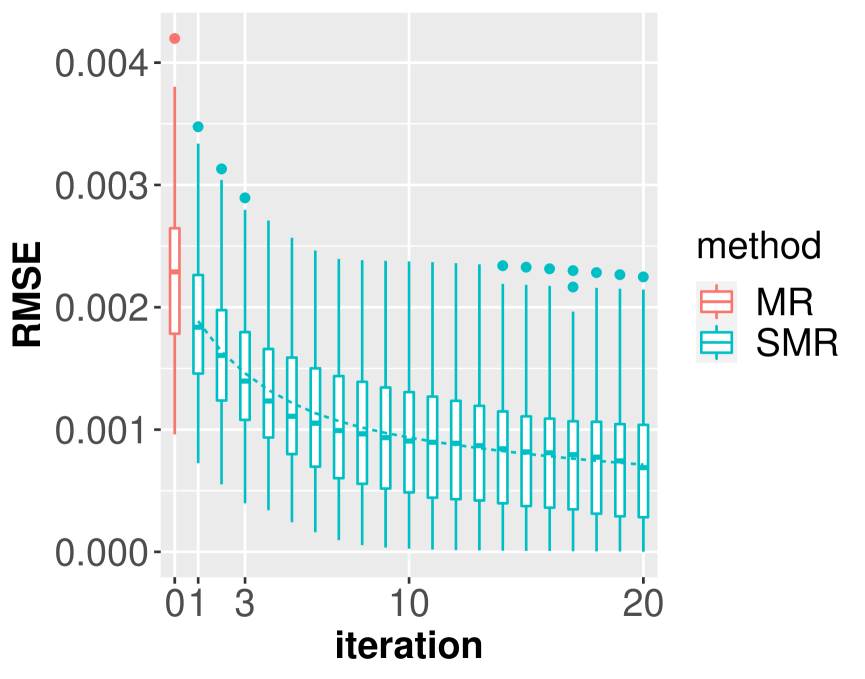

In this section, we use simulation studies to show that in terms of accuracy level the 3-iteration SMR is comparable with the divide-and-conquer approach (Lin and Xi, 2011), which is also known as divide and recombine, split and conquer, or split and merger in the literature (Wang et al., 2016). When there is no ambiguity, we call the 3-iteration SMR simply SMR.

We simulate 100 datasets of size for each of the seven distributions of covariates in the logistic regression model (3.5). We apply both SMR and the divide-and-conquer (DC) algorithm proposed by Lin and Xi (2011) to estimate the parameter values. Table 2 shows that SMR based on a -means partition with outperforms the divide-and-conquer method with blocks in most of simulation settings. Actually, the SMR estimates are comparable with the full data estimates in terms of RMSEs from the true parameter value. In Figure A.3 and Figure A.4, we plot the corresponding boxplots. For comparison purpose, we also list the corresponding MR estimates, which are overall not as good as DC’s.

SMR is ideal for massive data stored in multiple nodes, since it exchanges only the representative data points and estimated parameter values between nodes. It can perform well even with limited network bandwidth.

On the contrary, divide-and-conquer methods typically operate on random partitions. Each random data block for divide-and-conquer might consist of data points from many different nodes, which requires heavy communications between nodes. It may not be feasible when raw data transfer is prohibited.

A.4 SMR vs Support Points for Logistic Models

In order to compare the performance of the proposed methods and the support points techniques (Mak and Joseph, 2018), we run a simulation study under the logistic regression model with 7 covariates. We use R function sp in package support for searching support points for a given dataset. Since it takes sp more than one hour to generate 20,000 support points from 1,000,000 data points, we reduce the simulation setup to choosing 1,000 support points from 10,000 original data points, which is the simulation setup used by Wang et al. (2018).

| Simulation setup | SRS | Support | A-opt | MR | SMR |

|---|---|---|---|---|---|

| mzNormal | 111 (3.0) | 118 (3.4) | 93 (2.6) | 22 (0.4) | 16 (0.4) |

| nzNormal | 235 (7.5) | 237 (7.9) | 115 (3.6) | 41 (1.1) | 31 (1.0) |

| ueNormal | 65 (3.2) | 65 (3.3) | 45 (1.8) | 186 (1.0) | 11 (0.5) |

| mixNormal | 160 (4.7) | 162 (4.6) | 101 (3.7) | 28 (0.6) | 22 (0.6) |

| 493 (15.9) | 526 (14.3) | 472 (15.5) | 92 (2.6) | 87 (2.6) | |

| EXP | 193 (5.2) | 187 (4.8) | 137 (4.0) | 22 (0.6) | 17 (0.5) |

| BETA | 241 (6.5) | 233 (6.6) | 180 (5.2) | 23 (0.7) | 19 (0.6) |

In Table A.4, we list the average RMSE ( over 100 simulations, where is estimated by the full dataset consisting of 10,000 data points, is estimated by 1000 simple random samples (SRS), support points (Support), A-optimal sample points (Aopt), mean representatives (MR), or the proposed score-matching representatives (SMR).

In terms of RMSE, SMR still performs the best. The difference between MR and SMR is not as large as in Table 2 since the sample size is smaller in this simulation study.

A.5 MR and SMR with Finer Partition

According to Theorems 3.2 and 3.3, the estimate obtained by MR or SMR converges to the full data estimate as . That is, with a finer partition, gets closer to (but not necessarily closer to the true parameter once the dataset is given). Table A.5 and Table A.6 show that with finer and finer partitions, both MR and SMR estimates get closer to , while SMR is more robust to the block size than MR.

| RMSE from true | RMSE from full | ||||

|---|---|---|---|---|---|

| Full data | MR | SMR | MR | SMR | |

| 2 | 3.72 (1.08) | 69.82 (0.88) | 4.75 (1.40) | 69.67 (0.48) | 3.00 (1.00) |

| 3 | 3.72 (1.08) | 33.35 (1.05) | 4.20 (1.16) | 33.09 (0.36) | 1.90 (0.57) |

| 4 | 3.72 (1.08) | 20.44 (1.00) | 3.94 (1.15) | 20.06 (0.25) | 1.44 (0.39) |

| 5 | 3.72 (1.08) | 13.89 (1.06) | 3.85 (1.07) | 13.34 (0.20) | 1.01 (0.31) |

-

•

Sample size ; Covariate distribution: mzNormal

| RMSE from true | RMSE from full | ||||

|---|---|---|---|---|---|

| Full data | MR | SMR | MR | SMR | |

| 500 | 3.72 (1.08) | 21.14 (1.05) | 4.26 (1.26) | 20.76 (0.33) | 2.14 (0.69) |

| 1000 | 3.72 (1.08) | 17.95 (1.00) | 4.14 (1.22) | 17.51 (0.30) | 1.92 (0.49) |

| 2000 | 3.72 (1.08) | 15.17 (0.96) | 4.09 (1.12) | 14.66 (0.31) | 1.67 (0.51) |

| 3000 | 3.72 (1.08) | 13.75 (1.00) | 4.08 (1.19) | 13.17 (0.29) | 1.60 (0.47) |

-

•

Sample size ; covariate distribution: mzNormal

A.6 CPU Time of MR and SMR

In this section, we provide Table A.7 and Figure A.5 mentioned in Section A.6. All computations are carried out on a single thread of a MAC Pro running macOS 10.15.6 with 3.5 GHz 6-Core Intel Xeon E5 and 32GB 1866 MHz DDR3 memory.

| Simulation setup | Full data | MR | SMR | A-opt | DC |

|---|---|---|---|---|---|

| mzNormal | 5.22 | 0.72 | 3.25 | 0.55 | 20.49 |

| nzNormal | 6.45 | 0.67 | 3.19 | 0.57 | 21.58 |

| ueNormal | 6.50 | 0.67 | 3.64 | 0.57 | 21.48 |

| mixNormal | 5.85 | 0.68 | 3.17 | 0.54 | 21.05 |

| 3.42 | 0.68 | 3.36 | 0.55 | 19.55 | |

| EXP | 4.59 | 0.71 | 3.07 | 0.55 | 20.04 |

| BETA | 3.96 | 0.67 | 3.01 | 0.57 | 19.69 |

-

•

Distribution: mzNormal; ; MR and SMR (1-iteration): given a -means partition (); A-opt: subsample size ; DC: given a random partition with blocks

A.7 Subset Clustering Strategy

When there is no natural partition available or when sub-partitions are needed, a partitioning procedure is required by representative approaches. Based on our simulation study and justification (see Section 3.2 and Section A.1), a clustering procedure, such as -means, is more efficient than grid partitions. However, the computational cost of -means clustering is quite heavy especially for large sample size . We recommend the subset clustering strategy (see the last paragraph of Section 3.2), which can significantly reduce the clustering cost for representative approaches. More specifically, the cluster centers are determined by a clustering algorithm on a much smaller subset of size , which will not be changed as the full sample size increases. Once the centers are determined, each data point with predictor vector is assigned to the cluster whose center is closest to . Since both and will not change with and they are much less than , the time complexity of the overall clustering procedure is .

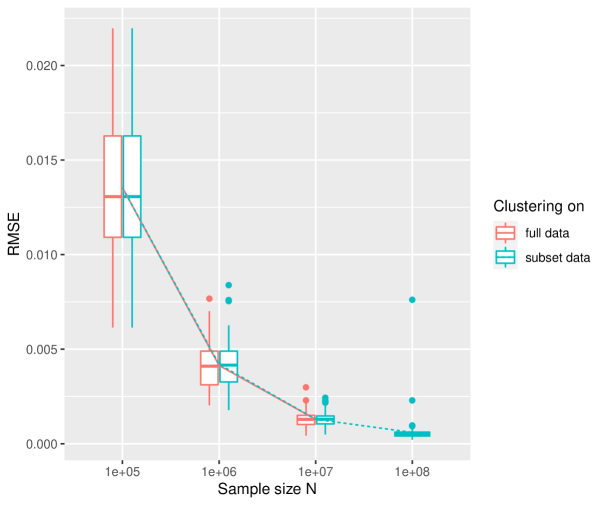

To illustrate the performance of the subset clustering strategy compared with a full data clustering for MR and SMR, we carry two simulation studies as follows. In the first simulation study, we generate datasets with sample size and covariates following mzNormal for the logistic model described in Section 3.2. For each , we generate independent replicates. The size of a randomly selected subset for locating clustering centers is fixed at . Figure A.6 shows in terms of the average SMR RMSE over 100 simulations the difference between the subset clustering and the full data clustering is negligible (the result of full data clustering is not available at due to too much computational time.

Table A.8 shows the computational time on clustering. For full data clustering, the time cost is proportional to the sample size . For subset clustering, we break the overall time cost into two parts. The first part is for locating the cluster centers based on the subset of size , whose time cost is fairly short and roughly constant. The second part is also full data clustering but with given cluster centers, whose time cost is also proportional to but much less than the original full data clustering. Overall, the subset clustering strategy reduces the clustering cost significantly.

To further explore the interaction between the dimension of predictors and the subset clustering strategy, we simulate datasets with covariates and sample size for logistic main-effects models. Since the dimension of covaraites changes, for each simulation we randomly generate the regression coefficients such that . We also adopt different subset size . Figure A.7 shows that in terms of MR and SMR RMSEs, the subset clustering strategy is not sensitive to the initial subset size across different dimensions of predictors.

| N | full data centers | subset cluster centers | full data clustering given centers |

|---|---|---|---|

| 4.96 | 4.97 | 1.02 | |

| 49.81 | 5.01 | 10.08 | |

| 478.85 | 4.81 | 96.48 | |

| 4812.69 | 6.46 | 973.98 |

-

•

Full data centers: Finding cluster centers based on the full data of size .

-

•

Subset cluster centers: Finding cluster centers based on the subset of size .

-

•

*: CPU time with is calculated over 30 replicates.

A.8 More Proofs

Lemma A.1 (Kanniappan and Sastry, 1983, Theorem 2.2).

Suppose is a finite dimensional space and , , are strictly convex. Suppose uniformly and exists uniquely. Then as goes to .

Proof.

of Theorem 3.2:

According to McCullagh and Nelder (1989, Section 2.5), the log-likelihood of a GLM with data , which is fixed throughout the proof, is given by

where , , and are known functions, and is the dispersion parameter. Given a data partition of , which will become finer and finer later, the log-likelihood contributed by the th block with block size is essentially

while the log-likelihood contributed by the weighted th representative is

since . Then the log-likelihood based on the full data is , and the log-likelihood based on the weighted representative data is .

Recall that the derivative is simply the score function (2.1). By plugging in the first order Taylor expansion of about at and the Cauchy-Schwarz inequality, we have

Denote . Then for sufficiently small and all , we have

| (A.4) |

for some , which depends on the data, which is given and fixed, but not the representatives or . That is, converges to uniformly for all as goes to .

The strict concavity of implies the existence and uniqueness of , such that . Let maximizes . For sufficiently small , is also strictly concave, which guarantees the existence and uniqueness of . By Lemma A.1, converges to as .

Since is twice differentiable and , the second-order Taylor expansion of at is

where is the Hessian matrix. Let be the smallest eigenvalue of . Since is strictly concave, then . For small enough ,

| (A.5) |

We claim that

| (A.6) |

Actually, if , then we have

| (A.7) |

due to (A.5) and . From (A.4) and (A.7), we have

| (A.8) |

On the other hand, since maximizes , we have

due to (A.4). That leads to a contradiction with (A.8). Thus (A.6) is justified and

∎

Recall that in general. Denote the th representative .

Corollary A.1.

All three center representative estimates as .

Proof.

For median representatives, , . Then

Therefore, . If , then for median representatives.

For mid-point representatives, the th block is typically defined by the grid points such that, if and only if , . In this case, we redefine . Then as . ∎

When all the covariates are categorical or have finite discrete values, one may partition the data according to distinct ’s. In this case, .

Corollary A.2.

Let be for mean and median representatives, and for mid-point representative. Under the conditions of Theorem 3.2, as and . If , then the mid-point, median, and mean representative approaches are the same and all satisfy .

Proof.

of Corollary A.2: Since for mean and mid-point representatives, and for median representatives, then under the conditions of Theorem 3.2, as and .

If , then in each block all the predictor variables are the same, that is, for , . Therefore, , and . ∎

Proof.

Proof.

of Theorem 3.4: Let as in (2.1) be the score function based on the full data satisfying . Let

be the score function based on the representative data points for the th iteration satisfying and . Consider their first-order Taylor expansions at :

| (A.9) | ||||

| (A.10) |

where

with and . Subtracting (A.9) from (A.10), we obtain

Therefore,

According to Theorem 3.3, as , and . Then . Thus

According to condition (b), . Since for , it can be verified that . Therefore, . Let be the largest eigenvalue of . Then , which is strictly less than for sufficiently small . Therefore,

| (A.11) |

It guarantees that as and . ∎

Proof.

of Corollary 3.1: If , by definition we have and for all . Therefore, and for both MR and SMR.

If , then and for all and thus according to (3.3). Since for all , then is a solution for solving (3.2). Since we always choose a solution closest to when the solutions are not unique, the proposed SMR have . In this case, we have by (3.4).

In both cases, SMR and MR estimates are the same. By Corollary A.2, we know both of them equal to the full data estimate . ∎

A.9 More on Airline on-time Performance Data

In the simulation study (see Table 5) based on the oracle regression coefficients , MR and SMR perform about the same, which is mainly due to the tiny oracle coefficient of the only continuous predictor DISTANCE.

In order to verify when SMR is better than MR, we inflate the oracle coefficient of DISTANCE by times to get a new oracle (see Table A.9). Then the maximum contribution of the predictor DISTANCE is about , which is expected to play a more important role in predicting Late Arrival. We redo the simulation study in Section 4 with the new oracle and list the corresponding results in Table A.10. Clearly the SMR estimates show consistent advantage over MR’s estimate throughout all data sizes. Both MR and SMR estimates based on -month data are better than the last available full-data estimate based on the -month data.

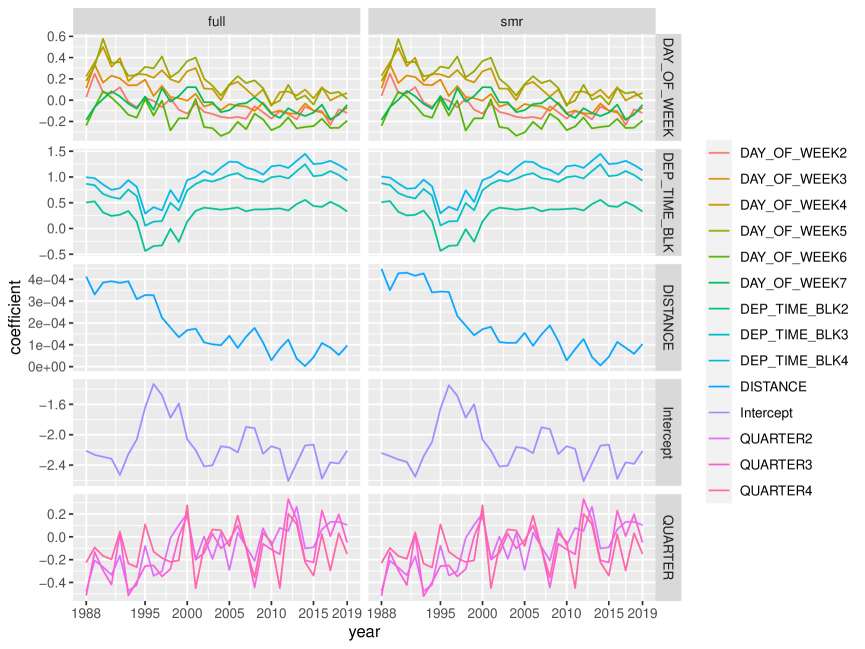

The rest of this section provides detailed description of the Airline raw data (Table A.11) and working data (Table A.12), the MR and SMR estimates based on all available months (Table A.13), and regression coefficients fitted yearly based on the original GLM (full) or SMR algorithm (Figure A.8).

| Predictor | Oracle | Inflated oracle |

|---|---|---|

| Intercept | -2.322 | -2.322 |