Dynamic Assortment Optimization with Changing Contextual Information

Abstract

In this paper, we study the dynamic assortment optimization problem under a finite selling season of length . At each time period, the seller offers an arriving customer an assortment of substitutable products under a cardinality constraint, and the customer makes the purchase among offered products according to a discrete choice model. Most existing work associates each product with a real-valued fixed mean utility and assumes a multinomial logit choice (MNL) model. In many practical applications, feature/contextual information of products is readily available. In this paper, we incorporate the feature information by assuming a linear relationship between the mean utility and the feature. In addition, we allow the feature information of products to change over time so that the underlying choice model can also be non-stationary. To solve the dynamic assortment optimization under this changing contextual MNL model, we need to simultaneously learn the underlying unknown coefficient and make the decision on the assortment. To this end, we develop an upper confidence bound (UCB) based policy and establish the regret bound on the order of , where is the dimension of the feature and suppresses logarithmic dependence. We further establish a lower bound , where is the cardinality constraint of an offered assortment, which is usually small. When is a constant, our policy is optimal up to logarithmic factors. In the exploitation phase of the UCB algorithm, we need to solve a combinatorial optimization for assortment optimization based on the learned information. We further develop an approximation algorithm and an efficient greedy heuristic. The effectiveness of the proposed policy is further demonstrated by our numerical studies.

keywords: Dynamic assortment optimization, regret analysis, contextual information, bandit learning, upper confidence bounds.

1 Introduction

In operations, an important research problem facing a retailer is the selection of products/advertisements for display. For example, due to the limited shelf space, stocking restrictions, or available slots on a website, the retailer needs to carefully choose an assortment from the set of substitutable products. In an assortment optimization problem, choice model plays an important role since it characterizes a customer’s choice behavior. However, in many scenarios, customers’ choice behavior (e.g., mean utilities of products) is not given as a priori and cannot be easily estimated due to the insufficiency of historical data. This motivates the research of dynamic assortment optimization, which has attracted a lot of attentions from the revenue management community in recent years. A typical dynamic assortment optimization problem assumes a finite selling horizon of length with a large . At each time period, the seller offers an assortment of products (with the size upper bounded by ) to an arriving customer. The seller observes the customer’s purchase decision, which further provides useful information for learning utility parameters of the underlying choice model. The multinomial logit model (MNL) has been widely used in dynamic assortment optimization literature, see, e.g., Caro & Gallien (2007); Rusmevichientong et al. (2010); Saure & Zeevi (2013); Agrawal et al. (2017a, b); Chen & Wang (2018); Wang et al. (2018).

In the age of e-commerce, side information of products is widely available (e.g., brand, color, size, texture, popularity, historical selling information), which is important in characterizing customers’ preferences for products. Moreover, some features are not static and could change over time (e.g., popularity score or ratings). The feature/contextual information of products will facilitate accurate assortment decisions that are tailored to customers’ preferences. In particular, we assume at each time , each product is associated with a -dimensional feature vector . To incorporate the feature information, following the classical conditional logit model (McFadden, 1973), we assume that the mean utility of product at time (denoted by ) obeys a linear model

| (1) |

Here, is the unknown coefficient to be learned. Based on this linear structure of the mean utility, we adopt the MNL model as the underlying choice model (see Section 2 and Eq. (3) for more details). As compared to the standard MNL, this changing contextual MNL model not only incorporates rich contextual information but also allows the utility to evolve over time. The changing utility is an attractive property as it captures the reality in many applications but also brings new technical challenges in learning and decision-making. For example, in existing works of (Agrawal et al., 2017a) for plain MNL choice models, upper confidence bands are constructed by providing the same assortment repetitively to incoming customers until a no-purchase activity is observed. Such an approach, however, can no longer be applied to MNL with changing contextual information as the utility parameters of products constantly evolve with time. To overcome such challenges, we propose a policy that performs optimization at every single time period, without repetitions of assortments in general.

Our model also allows the revenue for each product to change over time. In particular, we associate the revenue parameter for the product at time .

This model generalizes the widely adopted (generalized) linear contextual bandit from machine learning literature (see, e.g., Filippi et al. (2010); Chu et al. (2011); Abbasi-Yadkori et al. (2011); Agrawal & Goyal (2013); Li et al. (2017) and references therein) in a non-trivial way since the MNL cannot be written in a generalized linear model form (when an assortment contains more than one product, see Section 1.1 for more details). It is also worthwhile noting that this model incorporates a personalized MNL model proposed by Cheung & Simchi-Levi (2017) as a special case, where each product is associated with a fixed but unknown coefficient and each arriving customer at time with an observable feature vector (see Section 1.1 for a more detailed discussion). On the other hand, we choose to motivate our model from product contextual information since in practice, obtaining products’ features is usually easier (and less sensitive) than extracting customers’ preferences.

Given this contextual MNL choice model, the key challenge is how to design a policy that simultaneously learns the unknown coefficient and sequentially makes the decision on offered assortment. The performance of a dynamic policy is usually measured by the regret, which is defined as the gap between the expected revenue generated by the policy and the oracle expected revenue when (and thus the mean utilizes) is known as a priori.

The first contribution of the paper is the construction of an upper confidence bound (UCB) policy. Our UCB policy is based on the maximum likelihood estimator (MLE) and thus is named MLE-UCB. Although UCB has been a well-known technique for bandit problems, how to adopt this high-level idea to solve a problem with specific structures certainly requires technical innovations (e.g., how to build a confidence interval varies from one problem to another). In particular, our MLE-UCB contains two stages. The first stage is a pure exploration stage in which assortments are randomly offered and a “pilot MLE” is computed based on the observed purchase actions. As we will show in Lemma 7, this pilot estimator serves as a good initial estimator of . After the exploration phase, the MLE-UCB enters the simultaneous learning and decision-making phase. We carefully construct an upper confidence bound of the expected revenue when offering an assortment. The added interval is based on the Fisher information matrix of the computed MLE from the previous step. Then we solve a combinatorial optimization problem to search the assortment that maximizes the upper confidence bound. By observing the customer’s purchase action based on the offered assortment, the policy updates the estimated MLE. In this update, we propose to compute a “local MLE”, which requires the solution to be close enough to our pilot estimator. The local MLE plays an important role in MLE-UCB policy since it guarantees that the obtained estimator at each time period is also close to the unknown true coefficient .

Under some mild assumptions on features and coefficients, we are able to establish a regret bound , where the notation suppresses logarithmic dependence on , (cardinality constraint), and some other problem dependent parameters111For the ease of presentation in the introduction, we only present the dominating term under the common scenario that the selling horizon is larger than the dimensionality and the cardinality constraint . Please refer to Theorem 1 for a more explicit expression of the obtained regret.. One remarkable aspect of our regret bound is that our regret has no dependence on the total number of products (not even in a logarithmic factor). This makes the result attractive to online applications where is large (e.g., online advertisement). Moreover, it is also worthwhile noting the dependence of is only through a logarithmic term.

Our second contribution is to establish the lower bound result . When the maximum size of an assortment is small (which usually holds in practice), this result shows that our policy is almost optimal.

Moreover, at each time period in the exploitation phase, our UCB policy needs to solve a combinatorial optimization problem, which searches for the best assortment (under the cardinality constraint) that minimizes the upper confidence bound of the expected revenue. Given the complicated structure of the upper confidence bound, there is no simple solution for this combinatorial problem. When is small and is not too large, one can directly search over all the possible sets with the size less than or equal to . In addition to the solution of solving the combinatorial optimization exactly, the third contribution of the work is to provide an approximation algorithm based on dynamic programming that runs in polynomial time with respect to , , . Although the proposed approximation algorithm has a theoretical guarantee, it is still not efficient for dealing with large-scale applications. To this end, we further describe a computationally efficient greedy heuristic for solving this combinatorial optimization problem. The heuristic algorithm is based on the idea of local search by greedy swapping, with more details described in Sec. 5.2.

1.1 Related work

Due to the popularity of data-driven revenue management, dynamic assortment optimization, which adaptively learns unknown customers’ choice behavior, has received increasing attention in the past few years. Motivated by fast-fashion retailing, the work by Caro & Gallien (2007) first studied dynamic assortment optimization problem, but it makes a strong assumption that the demands for different product are independent. Recent works by Rusmevichientong et al. (2010); Saure & Zeevi (2013); Agrawal et al. (2017a, b); Chen & Wang (2018); Wang et al. (2018) incorporated MNL models into dynamic assortment optimization and formulated the problem into a online regret minimization problem. In particular, for capacitated MNL, Agrawal et al. (2017a) and Agrawal et al. (2017b) proposed UCB and Thompson sampling techniques and established the regret bound (when ). Chen & Wang (2018) further established a matching lower bound of . It is interesting to compare our regret to the bound for the standard MNL case. When the total number of products is much larger than (i.e., ), by incorporating the contextual information, the regret reduces from to . The latter one only depends on and is completely independent of the total number of products , which also demonstrates the usefulness of the contextual information. Chen et al. (2018) further studied the dynamic assortment optimization under nested logit models. We also note that to highlight our key idea and focus on the balance between learning of and revenue maximization, we study the stylized dynamic assortment optimization problems following the existing literature (Rusmevichientong et al., 2010; Saure & Zeevi, 2013; Agrawal et al., 2017a, b), which ignore operations considerations such as price decisions and inventory replenishment.

There is another line of recent research on investigating personalized assortment optimization. By incorporating the feature information of each arriving customer, both the static and dynamic assortment optimization problems are studied in Chen et al. (2015) and Cheung & Simchi-Levi (2017), respectively. It is worthwhile noting that although we do not approach our work from a personalized perspective222This is because in some applications, the product features are easier to obtain by the seller as compared to customer features., the personalized MNL considered in Cheung & Simchi-Levi (2017) can be viewed as a special of our model.

In particular, the personalized MNL assumes that each product is associated with an unknown coefficient . When a customer arrives at time with the observed feature , the utility of product at time is . Now we explain how to specialize our model to obtain the personalized MNL. Let us define and the feature vector , which is a concatenation of -dimensional vectors with the -th vector being and all other vectors being 0. Then according to our linear model in Eq. (1), we have , which recovers the personalized MNL model. Using our regret bound with as the dimensionality of , we directly obtain the regret for the dynamic assortment optimization under the personalized MNL. As compared to the Bayesian regret bound in Cheung & Simchi-Levi (2017) (see Theorem 3.3. therein), our approach still saves a factor of . We also remark that our results require a slightly stronger assumption on the contextual information vectors compared to Cheung & Simchi-Levi (2017), which allows customer feature vectors to be adversarially chosen. More specifically, a stochastic assumption is imposed on only during the pure exploration phase of our proposed policy. After this pure exploration phase, the feature vectors can also be adversarially chosen. We refer the readers to Sec. 3.1 for further details.

In addition, the developed techniques in our work and Cheung & Simchi-Levi (2017) are different, Our policy is based on UCB, while the policy in Cheung & Simchi-Levi (2017) is based on Thompson sampling. Furthermore, other research studies personalized assortment optimization in an adversarial setting rather than stochastic setting. For example, Golrezaei et al. (2014); Chen et al. (2016) assumed that each customer’s choice behavior is known, but that the customers’ arriving sequence (or customers’ types) can be adversarially chosen and took the inventory level into consideration. Since the arriving sequence can be arbitrary, there is no learning component in the problem and both Golrezaei et al. (2014) and Chen et al. (2016) adopted the competitive ratio as the performance evaluation metric.

Another field of related research is the contextual bandit literature, in which the linear contextual bandit has been widely studied as a special case (see, e.g., Dani et al. (2008); Rusmevichientong & Tsitsiklis (2010); Chu et al. (2011); Abbasi-Yadkori et al. (2011); Agrawal & Goyal (2013) and references therein). Some recent work extends the linear contextual bandit to generalized linear bandit (Filippi et al., 2010; Li et al., 2017), which assumes a generalized linear reward structure. In particular, the reward of pulling an arm given the observed feature vector of this arm is modeled by

| (2) |

for an unknown linear model and a known link function . For example, for a linear contextual bandit, is the identity mapping, i.e., . For the logistic contextual bandit, we have and . In a standard generalized linear bandit problem (see, e.g., Li et al. (2017)) with arms, it is assumed that a context vector is revealed at time for each arm . Given a selected arm at time , the expected reward follows Eq. (2), i.e., . At first glance, our contextual MNL model is a natural extension of the generalized linear bandit to the MNL choice model. However, when the size of an assortment , the contextual MNL cannot be written in the form of Eq. (2) and the denominator in the choice probability (see Eq. (3) in the next section) has a more complicated structure. Therefore, our problem is technically not a generalized linear model and is therefore more challenging. Moreover, in contextual bandit problems, only one arm is selected by the decision-maker at each time period. In contrast, each action in an assortment optimization problem involves a set of items, which makes the action space more complicated.

1.2 Notations and paper organization

Throughout the paper, we adopt the standard asymptotic notations. In particular, we use to denote that . Similarly, by , we denote . We also use for . Throughout this paper, we will use to denote universal constants. For a vector and a matrix , we will use and to denote the vector -norm and the matrix spectral norm (i.e., the maximum singular value), respectively. Moreover, for a real-valued symmetric matrix , we denote the maximum eigenvalue and the minimum eigenvalue of by and , respectively, and define for any given vector . For a given integer , we denote the set by .

The rest of the paper is organized as follows. In Section 2, we introduce the mathematical formulation of our models and define the regret. In Section 3, we describe the proposed MLE-UCB policy and provide the regret analysis. The lower bound result is provided in Section 4. In Section 5, we investigate the combinatorial optimization problem in MLE-UCB and propose the approximation algorithm and greedy heuristic. The multivariate case of the approximation algorithm is relegated to the appendix. In Section 6, we provide the numerical studies. The conclusion and future directions are discussed in Section 7. Some technical proofs are provided in the online supplementary material.

2 The problem setup

There are items, conveniently labeled as . At each time , a set of time-sensitive “feature vectors” and revenues are observed, reflecting time-varying changes of items’ revenues and customers’ preferences. A retailer, based on the features and previous purchasing actions, picks an assortment under the cardinality constraint to present to an incoming customer; the retailer then observes a purchasing action and collects the associated revenue of the purchased item (if then no item is purchased and zero revenue is collected).

We use an MNL model with features to characterize how a customer makes choices. Let be an unknown time-invariant coefficient. For any , the choice model is specified as (let and )

| (3) |

For simplicity, in the rest of the paper we use to denote the law of the purchased item conditioned on given assortment at time , parameterized by the coefficient . The expected revenue of assortment at time is then given by

| (4) |

Note that throughout the paper, we use to denote the expectation with respect to the choice probabilities defined in Eq. (3).

Our objective is to design policy such that the regret

| (5) |

is minimized. Here, is an optimal assortment chosen when the full knowledge of choice probabilities is available (i.e., is known).

3 An MLE-UCB policy and its regret

;

;

.

We propose an MLE-UCB policy, described in Algorithm 1.

The policy can be roughly divided into two phases. In the first pure exploration phase, the policy selects assortments uniformly at random, consisting of only one item. The objective of the pure exploration is to establish a “pilot” estimator of the unknown coefficient , i.e., a good initial estimator for . For the simplicity of the analysis, we choose one item for each assortment in this phase, which facilitates us to adapt existing analysis in (Filippi et al., 2010; Li et al., 2017) as the MNL-logit choice model reduces to a generalized linear model when only one item is present in the assortment. In the second phase, we use a UCB-type approach that selects as the assortment maximizing an upper bound of the expected revenue . Such upper bounds are built using a local Maximum Likelihood Estimation (MLE) of . In particular, in Step 5, instead of computing an MLE, we compute a local MLE, where the estimator lies in a ball centered at the pilot estimator with a radius . This localization also simplifies the technical analysis based on Taylor expansion, which benefits from the constraint that is not too far away from .

To construct the confidence bound, we introduce the matrices and in Step 6 of Algorithm 1, which are empirical estimates of the Fisher’s information matrices corresponding to the MNL choice model . The population version of the Fisher’s information matrices are presented in Eq. (8) in Sec. 3.2.2. These quantities play an essential role in classical statistical analysis of maximum likelihood estimators (see, e.g., (Van der Vaart, 2000)).

The proposed MLE-UCB policy has three hyper-parameters: the coefficient that controls the lengths of confidence intervals of , the number of pure exploration iterations , and the radius in the local MLE formulation. While theoretical values of and are given in Theorem 1, which potentially depend on several unknown problem parameters, in practice we recommend the usage of , and .

In the rest of this section, we give a regret analysis that shows an upper bound on the regret of the MLE-UCB policy. Additionally, we prove a lower bound of in Sec. 4 and show how the combinatorial optimization in Step 7 can be approximately computed efficiently in Sec. 5.

3.1 Regret analysis

To establish rigorous regret upper bounds on Algorithm 1, we impose the following assumptions:

-

(A1)

There exists a constant such that for all and . Moreover, for all and , are i.i.d. generated from an unknown distribution with the density satisfying that for some constant ;

-

(A2)

There exists a constant such that for all and with , for all .

The item (A1) assumes that the contextual information vectors in the pure-exploration phase with are randomly generated from a non-degenerate density. It also places a standard boundedness condition on for all time periods . Note that after the pure-exploration phase, we allow the contextual vectors to be adversarially chosen, only subject to boundedness conditions. (A2) additionally assumes a bounded ratio between the probability of choosing any two different items in an arbitrary assortment set. We remark that if , then the boundedness assumption in (A1) implies (A2) with .

We are now ready to state our main result that upper bounds the worst-case accumulated regret of the proposed MLE-UCB policy in Algorithm 1.

Theorem 1.

Suppose that and in Algorithm 1, then the regret of the MLE-UCB policy is upper bounded by

| (6) |

where are universal constants.

In addition to universal constants, the regret upper bound established in Theorem 1 has two terms. The first term, , is the main regret term that scales as dropping logarithmic dependency. The second term is a minor term, because it only scales logarithmically with the time horizon . One remarkable aspect of Theorem 1 is the fact that the regret upper bound has no dependency on the total number of items (even in a logarithmic term). This is an attractive property of the proposed policy, which allows to be very large, even exponentially large in and .

3.2 Proof sketch of Theorem 1

We provide a proof sketch of Theorem 1 in this section. The proofs of technical lemmas are relegated to the online supplement.

The proof is divided into four steps. In the first step, we analyze the pilot estimator obtained from the pure exploration phase of Algorithm 1, and show as a corollary that the true model is feasible to all subsequent local MLE formulations with high probability (see Corollary 1). In the second step, we use an -net argument to analyze the estimation error of the local MLE. Afterwards, we show in the third step that an upper bound on the estimation error implies an upper bound on the estimation error of the expected revenue , hence showing that are valid upper confidence bounds. Finally, we apply the elliptical potential lemma, which also plays a key role in linear stochastic bandit and its variants, to complete our proof.

3.2.1 Analysis of pure exploration and the pilot estimator

Our first step is to establish an upper bound on the estimation error of the pilot estimator , built using pure exploration data. It should be noted that in the pure exploration phase (), the assortments only consist of one item. Therefore the observation model reduces to a standard generalized linear model with the sigmoid function as the link function, which is essentially a logistic regression model of observing 1 if the customer makes a purchase.

Because the choice model in the pure exploration phase reduces to a generalized linear model, we can cite existing works to upper bound the error . In particular, the following lemma is cited from (Li et al., 2017, Eq. (18)), adapted to our model and parameter settings. The details on how to adapt the result from (Li et al., 2017) provided in the supplementary material.

Lemma 1.

With probability it holds that

| (7) |

The following corollary immediately follows Lemma 7, by lower bounding using standard matrix concentration inequalities. Its proof is again deferred to the supplementary material.

Corollary 1.

There exists a universal constant such that for arbitrary , if then with probability , .

The purpose of Corollary 1 is to establish a connection between the number of pure exploration iterations and the critical radius used in the local MLE formulation. It shows a lower bound on in order for the estimation error to be upper bounded by with high probability, which certifies that the true model is also a feasible local estimator in our MLE-UCB policy. This is an important property for later analysis of local MLE solutions .

3.2.2 Analysis of the local MLE

The following lemma upper bounds a Mahalanobis distance between and . For convenience, we adopt the notation that and for all throughout this section. We also define

| (8) | |||||

where denotes the expectation evaluated under the law ; that is, for and for .

Lemma 2.

Suppose . Then there exists a universal constant such that with probability the following holds uniformly over all :

| (9) |

Remark 1.

For , the expression of can be simplified as .

The complete proof of Lemma 9 is given in the supplementary material, and here we provide some high-level ideas behind our proof.

Our proof is inspired by the classical convergence rate analysis of M-estimators (Van der Vaart, 2000, Sec. 5.8). The main technical challenge is to provide finite-sample analysis of several components in the proof of (Van der Vaart, 2000, Sec. 5.8).

In particular, for any , consider

and its “sample” version

It is easy to verify by definition that and , because is a Kullback-Leibler divergence, is feasible to the local MLE formulation and is the optimal solution. On the other hand, it can be proved that is small for all with high probability, by using concentration inequalities for self-normalized empirical process (note that for any ). Moreover, by constructing a local quadratic approximation of around , we can show that is large when is far away from .

Following the above observations, we can use proof by contradiction to prove Lemma 9, which essentially claims that and are close under the quadratic distance . Suppose by contradiction that and are far apart, which implies that is large. On the other hand, by the fact that , we have

By the established concentration result, we have is small for all with high probability (including ). This leads to the desired contradiction.

3.2.3 Analysis of upper confidence bounds

The following technical lemma shows that the upper confidence bounds constructed in Algorithm 1 are valid with high probability. Additionally, we establish an upper bound on the discrepancy between and the true value defined in Eq. (4).

Lemma 3.

Suppose satisfies the condition in Lemma 9. With probability the following holds uniformly for all and , such that

-

1.

;

-

2.

.

At a higher level, the proof of Lemma 3 can be regarded as a “finite-sample” version of the classical Delta’s method, which upper bounds estimation error of some functional of parameters, i.e., using the estimation error of the parameters themselves . The complete proof is relegated to the supplementary material.

3.2.4 The elliptical potential lemma

Let be the assortment that maximizes the expected revenue (defined in Eq. (4)) at time period , and be the assortment selected by Algorithm 1. Because for all (see Lemma 3), we have the following upper bound for each term in the regret (see Eq. (5)):

| (10) |

where the last inequality holds because (note that maximizes ).

Subsequently, invoking Lemma 3 and the Cauchy-Schwarz inequality, we have

| (11) |

The following lemma is a key result that upper bounds . It is usually referred to as the elliptical potential lemma and has found many applications in contextual bandit-type problems (see, e.g., Dani et al. (2008); Rusmevichientong et al. (2010); Filippi et al. (2010); Li et al. (2017)).

Lemma 4.

It holds that

The proof of Lemma 4 is placed in the supplementary material. It is a routine proof following existing proofs of elliptical potential lemmas using matrix-determinant rank-1 updates.

We are now ready to give the final upper bound on defined in Eq. (5). Note that the total regret incurred by the pure exploration phase is upper bounded by , because the revenue parameters are normalized so that they are upper bounded by 1. In addition, as the failure event of for some occurs with probability , the total regret accumulated under the failure event is . Further invoking Eq. (11) and Lemma 4, we have

| (12) |

4 Lower bound

To complement our regret analysis in Sec. 3.1, in this section we prove a lower bound for worst-case regret. Our lower bound is information theoretical, and therefore applies to any policy for dynamic assortment optimization with changing contextual features.

Theorem 2.

Suppose is divisible by 4. There exists a universal constant such that for any sufficiently large and policy , there is a worst-case problem instance with items and uniformly bounded feature and coefficient vector (i.e., and for all , ) such that the regret of is lower bounded by .

Theorem 2 essentially implies that the regret upper bound established in Theorem 1 is tight (up to logarithmic factors) in and . Although there is an gap between the upper and lower regret bounds, in practical applications is usually small and can be generally regarded as a constant. It is an interesting technical open problem to close this gap of .

We also remark that an lower bound was established in (Dani et al., 2008) for contextual linear bandit problems. However, in assortment selection, the reward function is not coordinate-wise decomposable, making techniques in Dani et al. (2008) not directly applicable. In the following subsection, we provide a high-level proof sketch of Theorem 2, with complete proofs of technical lemmas relegated to the supplementary material.

4.1 Proof sketch of Theorem 2

At a higher level, the proof of Theorem 2 can be divided into three steps (separated into three different sub-sections below). In the first step, we construct an adversarial parameter set and reduce the task of lower bounding the worst-case regret of any policy to lower bounding the Bayes risk of the constructed parameter set. In the second step, we use a “counting argument” similar to the one developed in Chen & Wang (2018) to provide an explicit lower bound on the Bayes risk of the constructed adversarial parameter set, and finally we apply Pinsker’s inequality (see, e.g., Tsybakov (2009)) to derive a complete lower bound.

4.1.1 Adversarial construction and the Bayes risk

Let be a small positive parameter to be specified later. For every subset , define the corresponding parameter as for all , and for all . The parameter set we consider is

| (13) |

Note that is a positive integer because is divisible by 4, as assumed in Theorem 2. Also, to simplify notation, we use to denote the class of all subsets of whose size is .

The feature vectors are constructed to be invariant across time iterations . For each and , identical feature vectors are constructed as (recall that is the maximum allowed assortment capacity)

| (14) |

It is easy to check that with the condition , and for all . Hence the worst-case regret of any policy can be lower bounded by the worst-case regret of parameters belonging to , which can be further lower bounded by the “average” regret over a uniform prior over :

| (15) |

Here is the optimal assortment of size at most that maximizes (expected) revenue under parameterization . By construction, it is easy to verify that consists of all items corresponding to feature . We also employ constant revenue parameters for all , .

4.1.2 The counting argument

In this section we drive an explicit lower bound on the Bayes risk in Eq. (15). For any sequences produced by the policy , we first describe an alternative sequence that provably enjoys less regret under parameterization , while simplifying our analysis.

Let be the distinct feature vectors contained in assortment (if then one may choose an arbitrary feature ) with . Let be the subset among that maximizes , where is the underlying parameter. Let be the assortment consisting of all items corresponding to feature . We then have the following observation:

Proposition 1.

under .

Proof.

Because in our construction, we have where under .

Clearly is a monotonically non-decreasing function in .

By replacing all with , the values do not decrease and therefore the Proposition holds true.

To simplify notation we also use to denote the unique in . We also use and to denote the law parameterized by and policy . The following lemma gives a lower bound on by comparing it with , which is also proved in the supplementary material.

Lemma 5.

Suppose and define . Then

Define random variables . Lemma 5 immediately implies

| (16) |

Denote and . Averaging both sides of Eq. (16) with respect to all and swapping the summation order, we have

Note that for any fixed , . Also, . Subsequently,

| (17) |

4.1.3 Pinsker’s inequality

In this section we concentrate on upper bounding for any . Let and denote the laws under and , respectively. Then

where is the total variation distance between , , is the Kullback-Leibler (KL) divergence between , , and the inequality is the celebrated Pinsker’s inequality.

For every define random variables . The next lemma upper bound the KL divergence, which is proved in the supplementary material.

Lemma 6.

For any and , for some universal constant .

Further using Cauchy-Schwartz inequality, we have

which is further upper bounded by because . Subsequently,

| (18) |

where . Setting we complete the proof of Theorem 2.

5 The combinatorial optimization subproblem

The major computational bottleneck of our algorithm is its Step 9, which involves solving a combinatorial optimization problem. For notational simplicity, we equivalently reformulate this problem as follows:

| (19) | ||||

Here and , both of which can be pre-computed before solving Eq. (19).

A brute-force way to compute Eq. (19) is to enumerate all subsets , and select the one with the largest objective value. Such an approach is not an efficient (polynomial-time) algorithm and is therefore not scalable.

In this section we provide two alternative methods for (approximately) solving the combinatorial optimization problem in Eq. (19). Our first algorithm is based on discretized dynamic programming and enjoys rigorous approximation guarantees. The second algorithm is a computationally efficient greedy heuristic. Although the greedy heuristic does not have rigorous guarantees, our numerical result suggests it works reasonably well (see Sec. 6).

5.1 Approximation algorithms for assortment optimization

In this section we introduce algorithms with polynomial running times and rigorous approximation guarantees for the optimization task described in Eq. (19). We first formally introduce the concept of -approximation to characterize the approximation performance, and show that such approximation guarantees imply certain upper bounds on the final regret.

Definition 1 (-approximation).

Fix , and . An algorithm is an -approximation algorithm if it produces , such that with probability at least ,

| (20) |

where is the assortment set maximizing the actual objective in Eq. (19) 333We slightly abuse the notation here following the optimization convention that denotes the optimal solution. Note that is different from in (5), where the latter means the assortment that maximizes the expected revenue at time ..

The following lemma shows how -approximation algorithms imply an upper bound on the accumulated. It is proved using standard analysis of UCB type algorithms, with the complete proof given in the supplementary material.

Lemma 7.

In the rest of this section we introduce our proposed approximation algorithm and the approximation guarantee. To highlight the main idea of the approximation algorithm, we only describe how the algorithm operates in the univariate () case, while leaving the general multivariate () case to the appendix.

Our approximation algorithm can be roughly divided into three steps. In the first step, we use a “discretization” trick to approximate the objective function using “rounded” parameter values. Such rounding motivates the second step, in which we define “reachable states” and present a simple yet computationally expensive brute-force method to enumerate all reachable states, and establish approximation guarantees for such methods. This brute-force method is only presented for illustration purposes and will be replaced by a dynamic programing algorithm proposed in the third step. In particular, a dynamic programming algorithm is developed to compute which states are “reachable” in polynomial time.

5.1.1 The discretization trick

In the univariate case, are scalars and therefore is simply . Let be a small positive discretization parameter to be specified later. For all , define

| (21) |

where denotes the nearest integer a real number is rounded into. Intuitively, is the real number closest to that is an integer multiple of the discretization parameter , and similarly for .

The motivation for the definitions of is their sufficiency in computing the objective function . Indeed, for any , , define , , , and

Following the definition of and , it is easy to see that and as . The following lemma gives a more precise control of the error between , and , using the values of and the maximum utility parameter in .

Lemma 8.

For any , , suppose and for some . Suppose also for all . Then

| (22) |

The complete proof of Lemma 22 is relegated to the supplementary material.

5.1.2 Reachable states and a brute-force algorithm

To apply the estimation error bounds in Lemma 22 one needs to first enumerate giving rise to the item in with the largest utility parameter . After such an element is enumerated, the discretization parameter can be determined and discretized values can be computed for all . It is also easy to verify that there are at most possible values of , possible values of and possible values of (recall that is the upper bound of for all and ).

For any , and being integer multiples of , we use a tuple to denote a state. Here the indices and mean that the assortment and . Clearly there are at most different types of states. A state can be either reachable or non-reachable, as defined below:

Definition 2.

Let be the enumerated item with maximal utility parameter and , . A state is reachable if there exists satisfying the following:

-

1.

and ;

-

2.

for all ;

-

3.

if then ;

-

4.

, , and .

On the other hand, a state is non-reachable if at least one condition above is violated.

A simple way to find all reachable states is to enumerate all , and verify the three conditions in Definition 2. While such a procedure is clearly computationally intractable, in the next section we will present a dynamic programming approach to compute all reachable states in polynomial time. After all reachable states are computed, enumerate over every and reachable for and find that maximizes . The following corollary establishes the approximation guarantee for , following Lemma 22.

Corollary 2.

Let , be a subset corresponding to a reachable state for some , , that maximizes . Then

5.1.3 A dynamic programming method for computation of reachable states

In this section we describe a dynamic programming algorithm to compute reachable states in polynomial time. The dynamic programming algorithm is exact and deterministic, therefore approximation guarantees in Corollary 2 remain valid.

The first step is again to enumerate corresponding to the item in with the largest utility parameter , and calculating the discretization parameter . Afterwards, reachable states are computed in an iterative manner, from until . The initialization is that is reachable. Once a state is determined to be reachable, the following two states are potentially reachable:

The first future state corresponds to the case of . To determine when such a state is reachable, we review the conditions in Definition 2 and observe that whenever , the decision is legal because must belong to whenever (note that is the item in with the largest estimated utility). The second future state corresponds to the case of . Reviewing again the conditions listed in Definition 2, such a state is reachable if (meaning that there is still room to include a new item in ) and (meaning that the new item () to be included has an estimated utility smaller than ). Combining both cases, we arrive at the following updated rule of reachability:

-

1.

If , then is reachable;

-

2.

If and , then is reachable.

Algorithms 3 and 2 give pseudo-codes for the proposed dynamic programming approach of computing reachable states and an approximate optimizer of .

Finally, we remark on the time complexity of the proposed algorithm. Because the items we consider in the assortment satisfy , , and , and all are integral multiples of , we have (1) and take at most possible values; (2) takes at most possible values; and (3) takes at most values. Therefore, the total number of states for fixed , can be upper bounded by . The time complexity of Algorithm 3 is thus upper bounded by . Alternatively, to achieve -approximation, one may set as suggested by Corollary 2, resulting in a time complexity of .

This dynamic programming based approximation algorithm can be extended to multivariate feature vector with . The details are presented in Appendix A.

5.2 Greedy swapping heuristics

While the proposed approximation has rigorous approximation guarantees and runs in polynomial time, the large time complexity still prohibits its application to moderately large scale problem instances. In this subsection, we consider a practically efficient greedy swapping heuristic to approximately solve the combinatorial optimization problem in Eq. (19).

At a higher level, the heuristic algorithm is a “local search” method similar to the Lloyd’s algorithm for K-means clustering (Lloyd, 1982), which continuously tries to improve an assortment solution by considering local swapping/addition/deletions until no further improvements are possible. A pseudo-code description of our heuristic method is given in Algorithm 4.

While the greedy heuristic does not have rigorous guarantees in general, we would like to mention a special case of , in which Algorithm 4 does converge to the optimal assortment maximizing in polynomial time. More specifically, we have the following proposition which is proved in the supplementary material.

Proposition 2.

If , then Algorithm 4 terminates in iterations and produces an output that maximizes .

6 Numerical studies

In this section, we present numerical results of our proposed MLE-UCB algorithm. We use the greedy swapping heuristics (Algorithm 4) as the subroutine to solve the combinatorial optimization problem in Eq. (19). We will also study the quality of the solution of the greedy swapping heuristics.

Experiment setup.

The unknown model parameter is generated as a uniformly random unit -dimensional vector. The revenue parameters for are independently and identically generated from the uniform distribution . For the feature vectors , each of them is independently generated as a uniform random vector such that and . Here we set an upper bound of for the inner product so that the utility parameters are upper bounded by . We set such an upper bound because if the utility parameters are uniformly large, the optimal assortment is likely to pick very few items, leading to degenerated problem instances. In the implementation of our MLE-UCB algorithm, we simply set and .

The greedy swapping heuristics.

We first numerically evaluate the solution quality of the greedy swapping heuristic algorithm by focusing on the optimization problem in Eq. (19). We compare the obtained objective values in Eq. (19) to the proposed greedy heuristic and the optimal solution (obtained by brute-force search). Instead of generating purely random instances, we consider more realistic instances generated from a dynamic assortment planning process. In particular, for a given , we generate a dynamic assortment optimization problem with parameters , and , and run the MLE-UCB algorithm till the -th time period. Now the combinatorial optimization problem in Eq. (19) to be solved at the -th time is kept as one testing instance for the greedy swapping algorithm.

For each , we generate such test instances, and compare the solution of the greedy swapping heuristics with the optimal solution obtained by brute-force search in terms of the objective value in Eq. (19). Table 1 shows the relative differences between the two solutions at several percentiles, and the mean relative differences. We can see that the approximation quality of the greedy swapping algorithm has already been desirable when , and becomes even better as grows.

| percentile rank | mean relative difference in | |||||

|---|---|---|---|---|---|---|

| th | th | th | th | th | objective value | |

| 50 | 0 | 0.0159 | 0.0293 | 0.0393 | 0.0687 | 0.00207 |

| 200 | 0 | 0.0001 | 0.0040 | 0.0080 | 0.0123 | 0.00024 |

| 800 | 0 | 0 | 0 | 0.0014 | 0.0037 | 0.00004 |

Performance of the MLE-UCB algorithm.

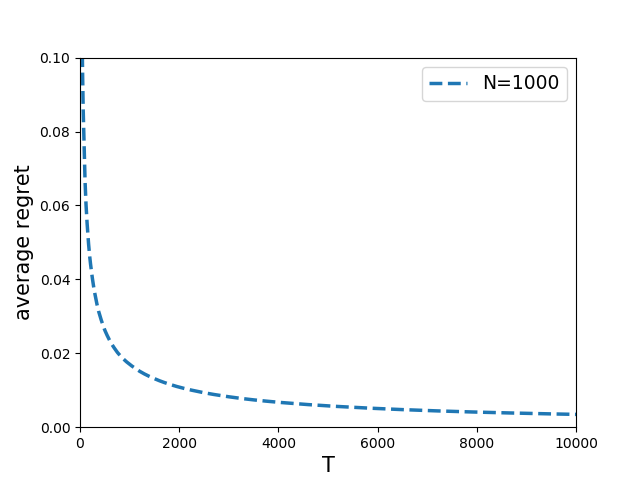

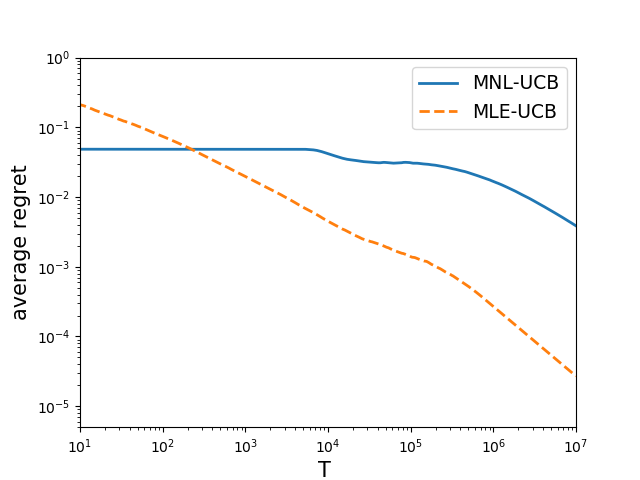

In Figure 1(a) we plot the average regret (i.e. ) of MLE-UCB algorithm with for the first time periods. For each experiment (in both Figure 1(a) and other figures), we repeat the experiment for 100 times and report the average value. In Figure 1(b) we compare our algorithm with the UCB algorithm for multinomial logit bandit (MNL-UCB) from Agrawal et al. (2017a) without utilizing the feature information. Since the MNL-UCB algorithm assumes fixed item utilities that do not change over time, in this experiment we randomly generate one feature vector for each of the items and this feature vector will be fixed for the entire time span. We can observe that our MLE-UCB algorithm performs much better than MNL-UCB, which suggests the importance of taking the advantage of the contextual information.

Impact of the dimension size .

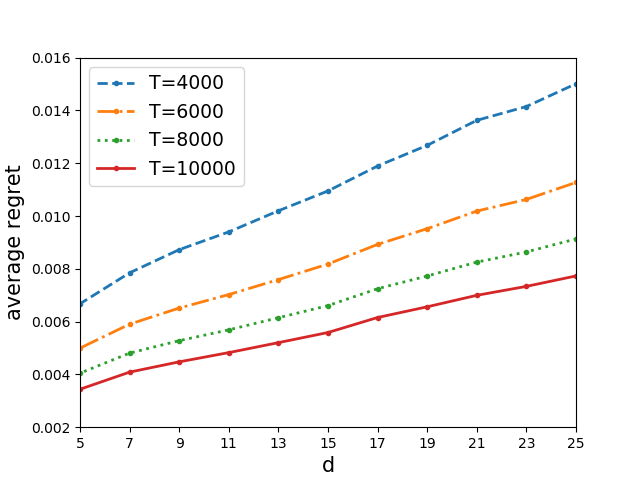

We study how the dimension of the feature vector impacts the performance of our MLE-UCB algorithm. We fix and and test our algorithm for dimension sizes in . In Figure 3, we report the average regret at times . We can see that the average regret increases approximately linearly with . This phenomenon matches the linear dependency on of the main term of the regret Eq. (6) of the MLE-UCB.

Impact of the number of items .

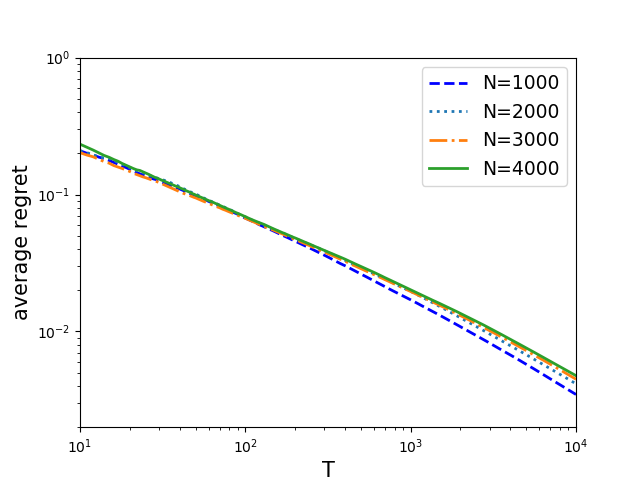

We compare the performance of our MLE-UCB algorithm for the varying number of items . We fix and , and test MLE-UCB for . In Figure 3, we report the average regret for the first time periods. We observe that the regret of the algorithm is almost not affected by a bigger . This confirms the fact that the regret Eq. (6) of MLE-UCB is totally independent of .

7 Conclusion and future directions

In this paper, we study the dynamic assortment planning problem under a contextual MNL model, which incorporates rich feature information into choice modeling. We propose an upper confidence bound (UCB) algorithm based on the local MLE that simultaneously learns the underlying coefficient and makes the decision on the assortment selection. We establish both the upper and lower bounds of the regret. Moreover, we develop an approximation algorithm and a greedy heuristic for solving the key optimization problem in our UCB algorithm.

There are a few possibilities for future work. Technically, there is still a gap of between our upper and lower bounds on regret. Although the cardinality constraint of an assortment is usually small in practice, it is still a technically interesting question to close this gap. Second, introducing contextual information into choice model is a natural idea for many online applications. This paper explores the standard MNL model, and it would be interesting to extend this work to contextual nested logit and other popular choice models. Finally, it is interesting to incorporate other operational considerations into the model, such as prices or inventory constraints.

Appendix A Multivariate approximation algorithm

In this appendix we describe an approximation algorithm for the combinatorial optimization problem studied in Sec. 5.1 for the general multivariate () case. The multivariate case is dealt with by randomized reductions to several univariate problem instances.

More specifically, for any , , a univariate problem instance can be constructed by replacing every occurrences of with . The univariate approximation Algorithm 3 is then invoked on independent univariate problem instances, each corresponding to a vector sampled uniformly at random from the -dimensional unit sphere. The output maximizers of Algorithm 3 are then compared against each other and the one leading to the largest value of is selected, where is the preset multiplicative approximation parameter. A pseudo-code description is given in Algorithm 5.

A.1 Approximation guarantees

The approximation performance of Algorithm 5 can be analyzed based on the following observation: if is close to , the leading eigenvector of

where is the exact maximizer of Eq. (19), then the reduction to a univariate problem instance does not lose much accuracy. More specifically, we have the following lemma:

Lemma 9.

Suppose there exists such that for some in Algorithm 5, then , where is the approximation parameter of the univariate problem instances.

Lemma 9 is proved in the supplementary material using elementary linear algebra. At a higher level, Lemma 9 shows that when the sampled vector is close to the underlying leading eigenvector (in the sense that the inner product between and is large), the produced subset will have good performance in maximizing the objective function .

The following proposition additionally gives the proximity between a random and .

Proposition 3.

Assume that . Let , be fixed and be sampled uniformly at random from the unit -dimensional sphere. Then

Proposition 3 is again proved in the supplementary material, using isotropy of and classical concentration inequalities.

Combining Lemma 9 and Proposition 3 we can give some recommendations on the choice of in Algorithm 5, which is the number of random vectors sampled. First, if initializations are taken, then with probability Lemma 9 is satisfied with , yielding a -approximation. Additionally, if initializations are taken, then with probability Lemma 9 is satisfied with , yielding a -approximation.

A.2 Time complexity analysis

To achieve a -approximation is set to and the overall running time of Algorithm 5 . To achieve a -approximation is set to and the overall running time of Algorithm 5 is .

Now we use Algorithm 5 to solve the combinatorial optimization problem in Step 9 of Algorithm 1 and examine the cumulative regret. If we let Algorithm 5 achieve to -approximation guarantee with and , the computational time complexity at each time slot will be ,444A polylogarithmic factor dependent on is hidden in the notation. and the cumulative regret will be upper bounded by . If we let Algorithm 5 to achieve -approximation guarantee with and , the computational time complexity at each time slot will be , and the cumulative regret will be upper bounded by .

Acknowledgement

: The authors would like to thank Vineet Goyal for helpful discussions, and Zikai Xiong for helping with the numerical studies.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Y., Pál, D., & Szepesvári, C. (2011). Improved algorithms for linear stochastic bandits. In Proceedings of the Advances in Neural Information Processing Systems (NIPS).

- Agrawal et al. (2017a) Agrawal, S., Avadhanula, V., Goyal, V., & Zeevi, A. (2017a). MNL-bandit: A dynamic learning approach to assortment selection. arXiv preprint arXiv:1706.03880.

- Agrawal et al. (2017b) Agrawal, S., Avandhanula, V., Goyal, V., & Zeevi, A. (2017b). Thompson sampling for MNL-bandit. In Proccedings of the Conference on Learning Theory (COLT).

- Agrawal & Goyal (2013) Agrawal, S., & Goyal, N. (2013). Thompson sampling for contextual bandits with linear payoffs. In Proceedings of the International Conference on Machine Learning (ICML).

- Caro & Gallien (2007) Caro, F., & Gallien, J. (2007). Dynamic Assortment with Demand Learning for Seasonal Consumer Goods. Management Science, 53(2), 276–292.

- Chen et al. (2016) Chen, X., Ma, W., Simchi-Levi, D., & Xin, L. (2016). Dynamic recommendation at checkout under inventory constraint. Available at SSRN: https://www.ssrn.com/abstract=2853093.

- Chen et al. (2015) Chen, X., Owen, Z., Pixton, C., & Simchi-Levi, D. (2015). A statistical learning approach to personalization in revenue management. Available at SSRN: http://ssrn.com/abstract=2579462.

- Chen & Wang (2018) Chen, X., & Wang, Y. (2018). A note on tight lower bound for mnl-bandit assortment selection models. Operations Research Letters, 46(5), 534–537.

- Chen et al. (2018) Chen, X., Wang, Y., & Zhou, Y. (2018). Dynamic assortment selection under nested logit models. arXiv preprint arXiv:1806.10410.

- Cheung & Simchi-Levi (2017) Cheung, W. C., & Simchi-Levi, D. (2017). Thompson sampling for online personalized assortment optimization problems with multinomial logit choice models. Available at SSRN: https://papers.ssrn.com/?abstract_id=3075658.

- Chu et al. (2011) Chu, W., Li, L., Reyzin, L., & Schapire, R. (2011). Contextual bandits with linear payoff functions. In Proceedings of the International Conference on Artificial Intelligence and Statistics (AISTATS).

- Dani et al. (2008) Dani, V., Hayes, T. P., & Kakade, S. M. (2008). Stochastic Linear Optimization under Bandit Feedback. In Proceedings of the Annual Conference on Learning Theory (COLT).

- Fan et al. (2015) Fan, X., Grama, I., & Liu, Q. (2015). Exponential inequalities for martingales with applications. Electronic Journal of Probability, 20(1), 1–22.

- Filippi et al. (2010) Filippi, S., Cappe, O., Garivier, A., & Szepesvári, C. (2010). Parametric bandits: The generalized linear case. In Proceedings of t he Advances in Neural Information Processing Systems (NIPS).

- Freedman (1975) Freedman, D. A. (1975). On tail probabilities for martingales. The Annals of Probability, 3(1), 100–118.

- Golrezaei et al. (2014) Golrezaei, N., Nazerzadeh, H., & Rusmevichientong, P. (2014). Real-time optimization of personalized assortments. Management Science, 60(6), 1532–1551.

- Li et al. (2017) Li, L., Lu, Y., & Zhou, D. (2017). Provably optimal algorithms for generalized linear contextual bandits. In Proceedings of International Conference on Machine Learning (ICML).

- Lloyd (1982) Lloyd, S. (1982). Least squares quantization in pcm. IEEE Transactions on Information Theory, 28(2), 129–137.

- McFadden (1973) McFadden, D. (1973). Conditional logit analysis of qualitative choice behaviour. In P. Zarembka (Ed.) Frontiers in Econometrics, (pp. 105–142). New York, NY, USA: Academic Press New York.

- Rusmevichientong et al. (2010) Rusmevichientong, P., Shen, Z.-J., & Shmoys, D. (2010). Dynamic assortment optimization with a multinomial logit choice model and capacity constraint. Operations Research, 58(6), 1666–1680.

- Rusmevichientong & Tsitsiklis (2010) Rusmevichientong, P., & Tsitsiklis, J. N. (2010). Linearly parameterized bandits. Mathematics of Operations Research, 35(2), 395–411.

- Saure & Zeevi (2013) Saure, D., & Zeevi, A. (2013). Optimal dynamic assortment planning with demand learning. Manufacturing & Service Operations Management, 15(3), 387–404.

- Tsybakov (2009) Tsybakov, A. B. (2009). Introduction to nonparametric estimation. Springer Series in Statistics. Springer, New York.

- van de Geer (2000) van de Geer, S. A. (2000). Empirical Processes in M-Estimation. Cambridge University Press.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic statistics. Cambridge university press.

- Vershynin (2012) Vershynin, R. (2012). How close is the sample covariance matrix to the actual covariance matrix? Journal of Theoretical Probability, 25(3), 655–686.

- Wang et al. (2018) Wang, Y., Chen, X., & Zhou, Y. (2018). Near-optimal policies for dynamic multinomial logit assortment selection models. In Advances in Neural Information Processing Systems (NeurIPS).

Supplementary Material for: Dynamic Assortment Optimization with Changing Contextual Information

This supplementary material provides detailed proofs for technical lemmas whose proofs are omitted in the main text.

A Proofs of technical lemmas for Theorem 1 (upper bound)

A.1 Proof of Lemma 7

Lemma 7 (restated).

With probability it holds that

| (S1) |

Proof. Because the noise in a logistic regression model is clearly centered and sub-Gaussian with parameter at most , it only remains to check (Li et al., 2017, Assumption 1), that where is the sigmoid link function. Because , we have where and . By (A2), we know that . Subsequently, for any and , we have

Lemma 7 is then an immediate consequence of (Li et al., 2017, Eq. (18)).

A.2 Proof of Corollary 1

Corollary 1 (restated).

There exists a universal constant such that for arbitrary , if then with probability , .

Proof.

Denote and .

Clearly .

In addition, because almost surely, are sub-Gaussian random variables with parameter .

By standard concentration inequalities (see, e.g., (Vershynin, 2012, Proposition 2.1)),

we have with probability that .

Hence, if for some sufficiently large universal constant ,

we have

and therefore .

The corollary then immediately follows Lemma 7.

A.3 Proof of Lemma 9

Lemma 9 (restated).

Suppose . Then there exists a universal constant such that with probability the following holds uniformly over all :

| (S2) |

Proof. For any define

By simple algebra calculations, the first and second order derivatives of with respect to can be computed as

| (S3) | ||||

| (S4) |

In the rest of the section we drop the subscript in , , and the , notations should always be understood as with respect to .

Define . It is easy to verify that is the Kullback-Leibler divergence between the conditional distribution of parameterized by and , respectively. Therefore, is always non-positive. Note also that , , and . By Taylor expansion with Lagrangian remainder, there exists for some such that

| (S5) |

Our next lemma shows that, if is close to (guaranteed by the constraint that ), then can be spectrally lower bounded by . It is proved in the supplementary material.

Lemma 12.

Suppose . Then for all .

As a corollary of Lemma 12, we have

| (S6) |

On the other hand, consider the “empirical” version , where

| (S7) |

It is easy to verify that remains true; in addition, for any fixed , forms a martingale 555 forms a martingale if for all . and satisfies for all . This leads to our following lemma, which upper bounds the uniform convergence of towards for all .

Lemma 13.

Suppose . Then there exists a universal constant such that with probability the following holds uniformly for all and :

| (S8) |

Lemma S8 can be proved by using a standard -net argument. Since the complete proof is quite involved, we defer it to the supplementary material.

We are now ready to prove Lemma 9. By Eq. (S8) and the fact that , we have

| (S9) |

Subsequently,

| (S10) |

In addition, because , by Eq. (S6) we have

| (S11) |

Lemma 9 is thus proved.

Proof of Lemma 12

Lemma 12 (restated).

Suppose . Then for all .

Proof. Because is a feasible solution of the local MLE, we know . Also by Corollary 1 we know that with high probability. By triangle inequality and the definition of we have that .

To prove we only need to show that for all . This reduces to proving

| (S12) |

Fix arbitrary , and for convenience denote as the feature vectors of items in (i.e., ). Let also and be the probability of choosing action corresponding to parameterized by or . Define , and . Recall also that and . Eq. (S12) is then equivalent to

| (S13) |

Let and be a whitening matrix such that , where is the identity matrix of size . Denote . We then have . Eq. (S13) is then equivalent to

| (S14) |

On the other hand, by (A2) we know that for all and therefore for all . Subsequently, we have

| (S15) |

Recall that where . Simple algebra yields that , where . Using the mean-value theorem, there exists for some such that

| (S16) |

Because almost surely for all and , we have

| (S17) |

The lemma is then proved by plugging in the condition on .

Proof of Lemma S8

Lemma S8 (restated).

Suppose . Then there exists a universal constant such that with probability the following holds uniformly for all and :

| (S18) |

Proof. We first consider a fixed , . Define

| (S19) |

Using an Azuma-Bernstein type inequality (see, for example, (Fan et al., 2015, Theorem A), (Freedman, 1975, Theorem (1.6))), we have

| (S20) |

The following lemma upper bounds and using and the fact that is close to . It will be proved right after this proof.

Lemma 16.

If then and .

Corollary 4.

Suppose satisfies the condition in Lemma 16. Then for any ,

| (S21) |

Our next step is to construct an -net over and apply union bound on the constructed -net. This together with a deterministic perturbation argument delivers uniform concentration of towards .

For any , let be a finite covering of in up to precision . That is, . By standard covering number arguments (e.g., (van de Geer, 2000)), such a finite covering set exists whose size can be upper bounded by . Subsequently, by Corollary S21 and the union bound, we have with probability that

| (S22) |

Proof of Lemma 16

Lemma 16 (restated).

If then and .

Proof. We first derive an upper bound for . By (A2), we know that for all . Also, Eqs. (S16,S17) shows that . If we have and therefore .

We next give upper bounds on . Fix arbitrary , and for notational simplicity let and . Because for all , we have

| (S27) |

On the other hand, by Taylor expansion we know that for any , there exists such that . Subsequently,

| (S28) | ||||

| (S29) | ||||

| (S30) |

Here and the last inequality holds because .

A.4 Proof of Lemma 3

Lemma 3 (restated).

Suppose satisfies the condition in Lemma 9. With probability the following holds uniformly for all and , such that

-

1.

;

-

2.

.

Proof. Without explicit clarification, all statements are conditioned on the success event in Lemma 9, which occurs with probability if is sufficiently large and satisfies the condition in Lemma 9.

We present below a key technical lemma in the proof of Lemma 3, which is an upper bound on the absolute value difference between and using and , where and . This key lemma can be regarded as a finite sample version of the celebrated Delta’s method (e.g., (Van der Vaart, 2000)) used widely in classical statistics to estimate and/or infer a functional of unknown quantities.

Lemma 19.

For all and , , it holds that , where in notation we only hide numerical constants.

Below we state our proof of Lemma 19, while deferring the proof of some detailed technical lemmas to the supplementary material. Fix . We use to denote the expected revenue of assortment at time , evaluated using a specific model . Then

| (S32) |

By the mean value theorem, there exists for some such that

| (S33) |

Recall that . Subsequently, by Jenson’s inequality and the fact that almost surely,

| (S34) |

Define , where is the assortment supplied at iteration . Combining Eqs. (S33,S34) with Lemma 9, we have

| (S35) |

It remains to show that and are close, for which we first recall the definitions of both quantities:

The next lemma shows that under suitable conditions is close to , implying that . It is proved in the supplementary material.

Lemma 20.

Suppose . Then for all , and .

Lemma 19 is thus proved. We are now ready to prove Lemma 3. By Lemma 19, we know that with high probability

| (S36) |

In addition, by Lemma 20 and the fact that thanks to the local MLE formulation, we have

and subsequently

because and are summations of

and terms.

Setting we proved that .

The second property of Lemma 3 can be proved similarly, by invoking the spectral similarities between ,

and , .

Proof of Lemma 20

Lemma 20 (restated).

Suppose . Then for all , and .

Proof. Define , where only the outermost expectation is replaced by taking with respect to the probability law under . Denote also . Then and , where . By Eq. (S16) and the fact that , , we have

| (S37) |

On the other hand, by (A2) we know that and therefore

| (S38) |

We next prove that which, together with established in the previous section, implies Lemma 20. Recall the definitions that

Adding and subtracting terms, we have

A.5 Proof of Lemma 4

Lemma 4 (restated).

It holds that

Proof. Denote as -dimensional positive semi-definite matrices with eigenvalues sorted as . By simple algebra,

| (S39) |

On the other hand, note that . Hence,

| (S40) |

We next prove the second inequality in Lemma 4. Because assortments have size 1 throughout the pure exploration phase (), we have

| (S42) |

where the last inequality holds thanks to assumption (A2), which implies . In addition, by the proof of Corollary 1, with high probability , where is a parameter specified in assumption (A1). Therefore,

| (S43) |

On the other hand, because we have and subsequently

| (S44) |

B Proofs of technical lemmas for Theorem 2 (lower bound)

B.1 Proof of Lemma 5

Lemma 5 (restated).

Suppose and define . Then

Proof. Let and be the corresponding feature vectors. Then

Here the last inequality holds because . In addition, by Taylor expansion we know that for all . Subsequently,

Finally, noting that provided that , we finish the proof of Lemma 5.

B.2 Proof of Lemma 6

Lemma 6 (restated).

For any and , for some universal constant .

Proof. Fix a time with policy’s assortment choice , and define . Let and be the probabilities of purchasing item under parameterization and , respectively. Then

| (S45) |

where the only inequality holds because for all . Because for all , Eq. (S45) is reduced to

| (S46) |

We next upper bound separately. First consider . We have

Here the first inequality holds because for all .

For corresponding to where , we have

Here the first inequality holds because , since .

For corresponding to and , we have

Combining all upper bounds on and Eq. (S46), we have

Here the last inequality holds because . Note also that by definition, and subsequently summing over all to we have

which is to be demonstrated.

C Proofs of approximation algorithms

C.1 Proof of Lemma 7

Lemma 7 (restated).

Proof. By union bound, we know the approximation guarantee in Eq. (20) for all with probability at least . In the event of failure, the accumulated regret is upper bounded by almost surely, because the regret incurred by each time period is at most . This gives rises to the term in Lemma 7, and in the rest of the proof we shall assume Eq. (20) holds for all .

Let be the solution to the exact optimization problem in Step 9 of Algorithm 1, be the assortment with the optimal revenue the same step, and be the solution by an -approximation algorithm.

For each , we bound the expected regret incurred at time by

Therefore, the total expected regret is bounded by

which, by the same analysis in Section 3.2.4, can be bounded by .

C.2 Proof of Lemma 22

Lemma 22 (restated).

For any , , suppose and for some . Suppose also for all . Then

| (S47) |

Proof. We first prove the upper bound on , which is

| (S48) |

where , .

Denote and . Because , we have . Let also and . Because , we have . Subsequently,

where the last inequality holds because . Using (since and , and , we have

provided that . Eq. (S48) is thus proved.

We next prove the upper bound on , which is

| (S49) |

where , , , .

Denote and . Because for all and , we have and . Denote also and . Using the same analysis as in the proof of Eq. (S48), we have and .

With the definitions of , , and , the left-hand side of Eq. (S49) can be re-written as

| (S50) |

Case 1: .

In this case, we have

| Eq. (S50) | |||

Case 2: .

In this case, we have and subsequently

Combining both cases we prove Eq. (S49).

C.3 Proof of Lemma 9

Lemma 9 (restated).

Suppose there exists such that for some in Algorithm 5, then , where is the approximation parameter of the univariate problem instances.

Proof. For each assortment , define by

Since , we have

| (S51) |

By the approximation guarantee of Algorithm 3, we have

| (S52) |

Since , we have . Therefore,

| (S53) |

C.4 Proof of Proposition 2

Proposition 2 (restated).

If , then Algorithm 4 terminates in iterations and produces an output that maximizes .

Proof. We first show that when the algorithm terminates with , is one of the optimal assortments. Suppose is not an optimal assortment, i.e. there exists such that , we show that the algorithm will not terminate. By the definition of we have and . By comparing and , one can find a new candidate assortment via swapping, adding, or deleting an item from/to such that . Therefore, and the algorithm will not terminate.

It remains to show that the algorithm terminates in iterations.

For each , we define a total order on , where corresponds to the items and is a special element with the definition for convenience, as follows: if and only if (and consequently if and only if ). It is straightforward to verify that there exists section points so that for any two that sandwiched by the same pair of neighboring section points (i.e. ), we have . Indeed, one can set the section points to be the solutions to the equalities for every pair of .

We will show that if for some , after at most iterations, either the algorithm terminates or . This directly leads to an upper bound on the total number of iterations that the algorithm performs. We pick an arbitrary and define the following two potential functions: , and . We have the following observations:

-

•

When a swapping operation is performed on , strictly decreases and does not increase.

-

•

When a deletion operation is performed on , increases by at most and strictly decreases.

-

•

When an addition operation is performed on , increases by at most and does not increase.

We let . Suppose there are swapping operations, deletion operations, and addition operations done in total, is the assortment that the algorithm begins with and is the last assortment satisfying . Observe that there are at most addition operations. Together with the three observations above, we have

In total, we have . Therefore, the total number of iterations where is .

C.5 Proof of Proposition 3

Proposition 3 (restated).

Assume that . Let , be fixed and be sampled uniformly at random from the unit -dimensional sphere. Then

Proof. Assume without loss of generality that , and let be sampled as follows. Sample independently for each , and let . Now, .

We first prove . Note that when and , we have , where the last inequality holds for . Therefore,

Now we prove . Similarly, when and , we have . Therefore,