A systematic investigation of classical causal inference strategies under mis-specification due to network interference

Abstract

We systematically investigate issues due to mis-specification that arise in estimating causal effects when (treatment) interference is informed by a network available pre-intervention, i.e., in situations where the outcome of a unit may depend on the treatment assigned to other units. We develop theory for several forms of interference through the concept of “exposure neighborhood”, and develop the corresponding semi-parametric representation for potential outcomes as a function of the exposure neighborhood. Using this representation, we extend the definition of two popular classes of causal estimands considered in the literature, marginal and average causal effects, to the case of network interference. We then turn to characterizing the bias and variance one incurs when combining classical randomization strategies (namely, Bernoulli, Completely Randomized, and Cluster Randomized designs) and estimators (namely, difference-in-means and Horvitz-Thompson) used to estimate average treatment effect and on the total treatment effect, under misspecification due to interference. We illustrate how difference-in-means estimators can have arbitrarily large bias when estimating average causal effects, depending on the form and strength of interference, which is unknown at design stage. Horvitz-Thompson estimators are unbiased when the correct weights are specified. Here, we derive the Horvitz-Thompson weights for unbiased estimation of different estimands, and illustrate how they depend on the design, the form of interference, which is unknown at design stage, and the estimand. More importantly, we show that Horvitz-Thompson estimators are in-admissible for a large class of randomization strategies, in the presence of interference. We develop new model-assisted and model-dependent strategies to improve Horvitz-Thompson estimators, and we develop new randomization strategies for estimating the average treatment effect and total treatment effect.

Keywords: Causal inference; potential outcomes; average treatment effect; total treatment effect; interference; network interference; statistical network analysis.

1 Introduction

The estimation of causal effects is a fundamental goal of many scientific studies. The framework of Potential Outcomes (Neyman 1923; Rubin 1974; Holland 1986) is a popular approach to formalize the problem of estimating causal effects of a treatment on an outcome, from a finite population of units. For instance, one can use the potential outcomes framework to formally define causal effects of interest called estimands or inferential targets, construct estimators that have desirable properties, such as, unbiasedness with respect to the randomization distribution, and formulate the assumptions under which the estimands and the estimators are well defined and causal conclusions hold.

An important assumption made in the classical potential outcomes framework is the no treatment-interference (or simply no interference111There can be other forms of interference; for e.g. the outcome of a unit may depend on the outcome of others. We are concerned only with treatment interference) assumption which can be stated as follows: The outcome of any unit depends only on its own treatment. In particular, the outcome of a unit does not depend on the treatment assigned to (or selected by) other units in the finite population of units. This assumption is implied by the so called Stable Unit Treatment Value Assumption or SUTVA as formulated in Rubin (1980), see also Rubin (1986). It is clear and well known (see for e.g. Section 3 in Rubin (1990)) that the classical framework of potential outcomes needs to be extended when estimating causal effects under interference.

When extending the classical potential outcomes framework and relaxing the assumption of no treatment-interference, the key natural question that arises is the following: What should be the form of interference? It is straightforward to specify what we mean by no treatment-interference, but the existence of treatment interference is not a concrete modeling assumption - there are many different ways to specify the exact form of interference and one needs to choose from various models of interference.

Once a model for interference is fixed, the next steps are to define causal estimands and develop designs and corresponding estimators. The classical versions of average treatment effects are no longer well defined when there is interference between units. This is due to the fact that the space of potential outcomes for each unit changes with the form of interference. In particular, the number of potential outcomes for each unit becomes a function of the form of interference. For example, consider a binary treatment . Under the no treatment-interference assumption, each unit has two potential outcomes and . The average causal effect is defined as the average of differences between these two potential outcomes. However, when there is arbitrary treatment-interference, the number of potential outcomes for each unit can be as large as and and are not well defined. There are many non-equivalent ways to define an estimand under interference and the choice depends on the scientific question that one is interested in answering. Once a choice has been made regarding the nature of interference and an estimand has been proposed, the next step is to develop (idealized) experimental designs along with corresponding estimators with good properties, such as unbiasedness with respect to the design, that allow us to estimate causal estimands.

Related work

Relaxing the assumption of no treatment-interference has been the subject of many works, see Halloran and Hudgens (2016) for a recent review. A classical line of work proceeds by limiting the interference to non-overlapping groups and assuming that there is no interference between groups. This setting is often referred to as partial interference (e.g., see Sobel 2006; Hudgens and Halloran 2008; Tchetgen and VanderWeele 2012; Liu and Hudgens 2014; Kang and Imbens 2016; Liu et al. 2016; Rigdon and Hudgens 2015; Basse and Feller 2017; Forastiere et al. 2016; Loh et al. 2018). Various types of estimands have been defined under partial interference. For instance, Sobel (2006) defined estimands that naturally arise in housing mobility studies and noted that under partial interference the classical estimators may be biased. Hudgens and Halloran (2008) considered potential outcomes marginalized over a randomization distribution, and use these marginal potential outcomes to define estimands. They considered two-stage designs and developed unbiased estimators for these marginal estimands. A different line of work has focused on designing experiments that eliminate or reduce partial interference, so that estimation can be carried out by ignoring interference (e.g., see David and Kempton 1996). In the modern setting, the assumption of partial interference has been relaxed by several authors to allow for arbitrary interference, or interference encoded by a network, see Bowers et al. (2012); Manski (2013); Goldsmith-Pinkham and Imbens (2013); Toulis and Kao (2013); Ugander et al. (2013); Aronow and Samii (2013); Basse and Airoldi (2015); Forastiere et al. (2016); Halloran and Hudgens (2016); Choi (2017); Athey et al. (2017). Manski (2013) considered the problem of whether causal effects are identifiable in presence of arbitrary interference. Aronow and Samii (2013) proposed Horvitz-Thompson estimators for estimating causal effects when there is arbitrary interference. Ugander et al. (2013) and Eckles et al. (2014) consider a cluster randomization design to reduce bias in estimating a specific estimand (i.e., total treatment effect). More recently, Sävje et al. (2017) study the large sample properties of estimating treatment effects, when the interference structure is unknown. They show (somewhat surprisingly) that in a large sample setup, the Horvitz-Thompson and Hajek estimators can be used to consistently estimate the expected average treatment effect, even if the structure of interference is incorrect. Jagadeesan et al. (2017) have proposed new designs for estimating the direct effect under interference. Ogburn et al. (2014) approach the problem of interference by using causal diagrams, and they present various causal Bayesian networks under different types of interference. Ogburn et al. (2017) use causal diagrams to develop GLM type estimators for contagion. Finally, Li et al. (2018) study peer effects using randomization based inference.

In this paper, we initiate a systematic investigation of issues that arise in definition and unbiased estimation of causal effects under arbitrary interference and develop possible solutions. Some of the key goals of our work are (a) to develop models of interference, (b) organize and place different estimands and estimators that have appeared in the literature under a common framework, (c) to clarify the issues present in existing definitions and estimators of causal effects and (d) study designs and unbiased estimation strategies under interference.

1.1 Summary of Contributions and Organization

Section 2 provides an overview of the key results of the paper. Here we present a informal summary of contributions.

Models for Potential Outcomes under Interference: We begin by revisiting the framework of potential outcomes under arbitrary interference in Section 3. Using the concept of exposure neighborhood, in Section 3.2, we develop non-parametric models potential outcomes to formalize the nature and form of interference. The exposure neighborhood allows one to explicitly model the form of interference, whereas the structural models formulate assumptions on the structure of potential outcomes under the assumed form of interference.

Choice of estimands: Unlike the classical no-interference setting, there are several non-equivalent ways of defining causal estimands under interference. In Section 3.3, we consider two different (overlapping) classes of estimands for formally defining causal effects - marginal causal effects (in the spirit of Hudgens and Halloran (2008)) and average causal effects. Marginal causal effects are defined as contrasts between expected values of potential outcomes under a fixed randomization scheme also called as policy, where as the average causal effects are defined as contrasts between averages of fixed potential outcomes. These classes include several estimands that have appeared in the literature as special cases.

Bias due to interference in difference-in-means estimators: In Section 4, we address some folklore about estimation strategies. In many cases, it is common to use a design along with classical difference-in-means like estimators to estimate an average causal effect, even when there is interference, with the hope that there might be little or no bias. In some settings, however, the definition of causal effect that is being estimated (the estimand) is not well specified. Our analysis makes it clear that certain classic versions of causal effects are not well defined when there is interference. In the cases where the estimand is well defined, we show that difference-in-means estimators can be biased for many types of estimands. We characterize the nature and sources of bias in estimating a large class of estimands. Our results also illustrate settings where simple estimators can yield little or no bias. For instance, when estimating the so called marginal causal effects, the difference-in-means estimators are unbiased. In general, the unbiasedness of the difference-of-means estimators depends on the nature and structure of interference, which we characterize in Section 4.2.

Liner Unbiased Estimation: We then consider the problem of unbiased estimation of causal effects with commonly used estimation strategies, in Section 5. We consider the Bernoulli, Completely Randomized and Cluster Randomized Designs and focus on the problem of unbiased estimation.

A popular estimation strategy is to use Horvitz-Thompson (HT) like estimators, which is the subject of Section 5. For instance, Aronow and Samii (2013) proposed using HT estimators for particular estimands (i.e., contrasts between potential outcomes corresponding to two different treatment assignment vectors). We consider the class of all linear weighted unbiased estimators and show that HT estimators can be used to obtain unbiased estimates for any estimand and design, as long as the correct weights are used and some regularity conditions on the design hold. However, we note that the weights depend on the design, the structure of interference (as specified by an interference model) and the estimand. We explicitly derive the weights of HT estimators for commonly used designs and estimands. We also show that the correct weights that endow HT estimators with good properties need not be unique. The question of optimality (e.g., minimum variance, unbiased) of HT weights is difficult, and has been recently addressed, in part (Sussman and Airoldi 2017).

We prove that Horvitz-Thompson estimators are inadmissible for estimating a large class of estimands and a large class of designs. The HT estimator is one of many estimators in the class of linear weighted unbiased estimators. Using ideas from survey sampling literature, we consider two strategies to improve upon the HT estimator. The non-parametric linear representation of potential outcomes we develop lends itself naturally to develop improved estimators either in a model dependent or a model assisted framework (à la Basse and Airoldi 2015). Finally, in section 6, we explore new designs to estimate two commonly used estimands: average treatment effect and total treatment effect, defined in Section 2. A key observation is that the optimal design for estimation may depend on the estimand.

2 Overview of the main results: Modes of failures and solutions

Consider a finite population of units indexed by . Let denote a vector of binary treatment assignments where each . Let denote the vector of potential outcomes when the finite population of units gets assigned the treatment vector z. For each unit , is a function of z. The no treatment-interference assumption ensures that for each , we can write the potential outcomes function as,

| (1) |

Thus, under the no treatment-interference assumption the total number of potential outcomes for each unit is . However, when there is interference, we can write

| (2) |

where is the vector of treatment assignments of all units except .

Explosion of Potential Outcomes

When there is arbitrary interference, the number of potential outcomes for each unit may explode, rendering causal inference impossible without modeling potential outcomes. In general, the total number of potential outcomes for each unit can be as high as .

Proposition 2.1.

Without any further assumptions on the function , causal inference is impossible.

Proposition 2.1 is simple, but has far reaching consequences. The key consequence is that under arbitrary treatment interference, one must model the potential outcomes, even under randomization inference. Indeed, the no-interference assumption is also a modeling assumption. Thus, the question becomes which model to use. We develop models for potential outcomes by specifying three components: An interference neighborhood, an exposure function and structural assumptions. Modeling potential outcomes allows one to reduce the number of potential outcomes per unit to a more manageable size. The total number of potential outcomes per unit is directly related to the interference neighborhood and an exposure model.

Table 1 gives three examples of exposure models and the number of potential outcomes per unit. We refer the reader to see Section 3.2 for precise definitions of these exposure models. Under the simplest exposure model, called the binary exposure, each unit has potential outcomes - this is twice as many when compared to the case of no-interference. On the other hand, for symmetric exposure, the number of potential outcomes for each unit grows linearly with the size of the exposure neighborhood. Finally, for a general exposure model, the number of potential outcomes for each unit grows exponentially with the size of the exposure neighborhood.

| Binary Exposure | Symmetric Exposure | General Exposure |

|---|---|---|

Non-parametric Decomposition of Potential Outcomes

Under arbitrary interference, we develop a non-parametric linear decomposition of the potential outcomes:

Proposition 2.2.

Let denote the vector of treatment assignments assigned to all but unit . There exist functions and where if , then every potential outcome function for unit can be decomposed as

Proposition 2.2 states that the potential outcome function for every unit can be decomposed linearly into three components: A component that depends on unit treatment, a component that depends on the treatment of all other units, and an interaction term. At first glance, this representation appears to be redundant as it is over-parametrized. But this decomposition offers three benefits: Firstly, the number of parameters and hence the number of potential outcomes can be now modeled by specification of these functions. Indeed, the explicit construction of the functions and in Proposition 2.2 requires modeling assumptions on the Potential outcomes which is the subject of Section 3.1. Secondly, the decomposition makes it clear that classical causal effects are ill-defined when there is interference because they ignore two components of the potential outcomes and use only the first component of direct effect. This decomposition allows us to define different types of causal estimands that focus on direct effects, interference effects or the interaction between the two. Finally, the decomposition also allows us to gain deeper insights into the nature and sources of biases for various classical estimators to estimate causal effects. We will discuss these issues next.

Different types of Average Treatment effects

We show that in presence of interference, there are many non-equivalent ways to define a treatment effect. In this summary, we will focus on two most popular treatment effects that fall under the class of average treatment effects. We also consider a different class called marginal treatment effects, see Section 3.3. The two average treatment effects that we consider are the direct effect

| (3) |

and the total effect

| (4) |

Proposition 2.3.

Under the no-interference assumption, . Under interference, .

In fact, one can show that under no-interference assumption, the marginal and the average causal effects are equivalent. This is no longer true in presence of interference, so one needs to be careful in defining what one is interested in estimating. An important point to note is that the causal estimands should not depend on the randomization design and must be defined independent of the actual design that was implemented.

Commonly used designs and estimators are biased

An intuitive approach to estimate average causal effects under interference in the literature is to use a difference-in-means estimator, with the hope that a mild form of interference may not effect the bias of the estimator We formalize this intuition and study the nature and sources of bias in various difference-in-means estimators under interference. Unfortunately, the situation is more complex. The nature of bias depends on the estimand, the exact form of the difference-in-means estimator, the design and finally the model for interference. This is the subject of Section 4. For estimating the marginal effects, the difference-in-means estimators are unbiased under certain mild conditions on the design. For estimating the total and the direct effect defined in equations 4 and 3, the situation is more nuanced.

In general, there are two sources of bias in estimating the direct and the total effects, see Proposition 4.1. The first source of bias is due to the so called nuisance potential outcomes. These are the potential outcomes that do not appear in the definition of the estimand and are irrelevant for estimation of certain classes of estimands, specially the average causal effects. The nuisance potential outcomes form a source of bias when estimating average causal effects, as shown in Section 4 and Proposition 4.1.

The second source of bias is due to incorrect weights used in the estimator. In some difference-in-means estimators and designs, the first source of bias can be completely eliminated, see Proposition 4.2 for an example. The second source of bias is due to the use of incorrect weights; these weights depend on the design and the nature of interference. For many commonly used designs such as the Completely Randomized Design, Bernoulli Design and the Cluster Randomized Design, assuming a mild form of interference, the second source of bias can be made very small. However, we must point out that the reduction of bias depends on the model of interference, which is not known in general. An incorrect assumption on the interference model may lead to bias, we do not investigate this source of bias.

Proposition 2.4.

Assume that the interference is specified by a graph on units, i.e., the treatment of unit effects the outcome of unit iff there is an edge between nodes and in . Further, assume that the Potential Outcomes follow a linear model: , where denotes the number of treated neighbors of unit in graph . Let be the total number of edges in . Under a completely randomized design and a Bernoulli trial, (defined in Section 3.4), consider the naive difference-in-means estimator:

The bias of the difference-in-means estimator for estimating the direct effect given in equation 3 is

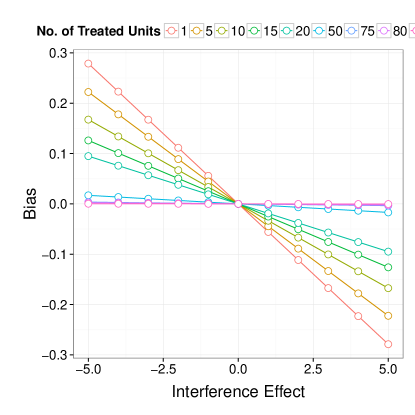

Proposition 2.4 is an example of the type of characterization of the nature and source of bias developed in Section 4 for various models of interference. This result shows that even under a simple linear model of potential outcomes, the difference-in-means estimator is biased for estimating the direct effect. The bias depends on the unknown interference parameter and the density of the interference graph given by . The bias is in the opposite direction of the interference effect: If there is positive interference, the estimated direct effect is smaller than the true direct effect and vice versa. Also, if the interference effect is small and the interference graph is sparse, then the bias is very small. However, as we can see, even in such a simple model, the nature of bias depends on unknown parameters such as the density of the interference graph and . For more general models, the qualitative results are similar, and the reader is refereed to Section 4 for more details.

Linear unbiased estimators and inadmissibility of the Horvitz-Thompson estimator

Section 5 is devoted to the theory of linear unbiased estimation. For any design, weighted unbiased linear estimators can be constructed using techniques from sampling theory. We study two classes of weighted linear unbiased estimators. We show that under some regularity conditions, there are infinitely many weighted linear unbiased estimators, see Theorem 5.1. Moreover, when the weights are allowed to depend only on the treatment and exposure status of a unit, the Horvitz-Thompson estimator is the only unbiased estimator, see Theorem 5.2. The weights used in the HT estimator depend on the interference model, the design and the estimand. In Theorem 5.4, we derive the formula for the weights used in HT estimators for Bernoulli, CRD and the Cluster Randomized designs for different interference models for estimating the direct effect. A point to note is that unbiased estimators of the direct effect do not exist when using cluster randomized designs. This illustrates the fact that an estimation strategy that is considered optimal for one type of estimand may not necessarily be optimal for a different estimand, in fact, it can be far from optimal. The optimality criteria can be as simple as existence or unbiasedness.222It remains an open question to find estimation strategies that can be simultaneously optimal for a large class of estimands.

Although the H-T estimator is unbiased, its performance can be very poor in practice because of high variance. An estimator is inadmissible if there exists a uniformly better estimator in terms of the mean squared error. In Theorem 5.5, we show that for a large class of designs that satisfy some natural regularity conditions, the HT estimator is inadmissible. We discuss various improvements to the HT estimator, which are inspired by the survey sampling literature, that aim to reduce the variance at the cost of a mild bias.

New Designs

We consider new designs for estimating causal effects when there is treatment interference. There are two key considerations when thinking about new designs. The first consideration is that the optimality of a design may depend on the estimand: A design that is considered optimal for estimating the direct effect may be far from optimal for estimating the total effect. The second consideration is that the optimal design may need to depend on the interference graph and the exposure model. Classical designs such as CRD and Bernoulli designs are oblivious to the interference graph and the exposure model. They can generate units with potential outcomes that are nuisance when estimating the direct and the total effect.

To this end, we discuss two designs, one old and one new for estimating the direct and the total effect under the symmetric exposure model, when the interference graph is known. For estimating the direct effect, we develop a new design inspired by the concept of an independent set in graph theory. The independent set design attempts to maximize the number of units that reveal the relevant potential outcomes required for estimating the direct treatment effect. For estimating the total effect, we consider the cluster randomized design discussed in Ugander et al. (2013).

Optimality of Estimation Strategies.

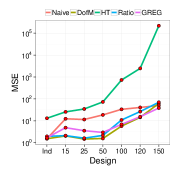

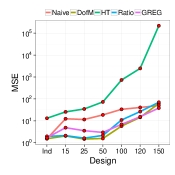

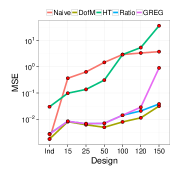

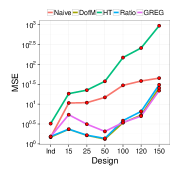

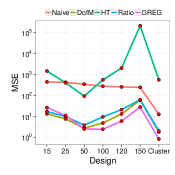

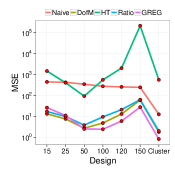

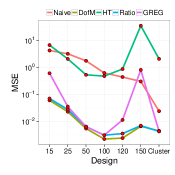

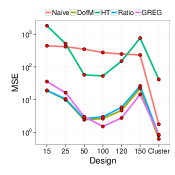

We evaluate several estimation strategies for estimating the total and the direct effect using simulation studies. The key lessons of the simulation studies can be summarized as follows: The bias of the difference of means estimator in estimating the direct effect depends on the unknown interference effects. Estimation strategies that are unbiased for one estimand may be severly biased for a different estimand. For e.g. we find that the Independent set designs along with any estimator is approximately unbiased for the direct effect and has superior performance in terms of mean squared error when compared with other designs. On the other hand, the cluster randomized design along with any estimator is approximately unbiased for estimating the total effect. Moreover, the Horvitz-Thompson estimator has the worst performance in terms of mean-squared error - even the biased naive difference-in-means estimator is beats it.

3 Revisiting the Potential Outcomes framework under arbitrary treatment interference

In this section, we revisit the definition of potential outcomes when there is arbitrary treatment interference. We develop a framework for specifying models for potential outcomes under interference. Such models are necessary when there is treatment-interference. We consider two classes of causal effects and study the conditions under which unbiased estimators exist for estimating causal effects.

3.1 Potential Outcomes under arbitrary interference

Consider a finite population of units indexed by the set and a binary treatment for each unit . Let denote the vector of treatment assignments. Let be the set of relevant treatment assignments and let . In general, and .

Under arbitrary treatment interference, let be the fixed potential outcome of unit under the treatment assignment vector z. The potential outcome of a unit can also be considered as a function from the set of possible treatment assignments to . For example, in case of a binary outcome, . Under this notation, the potential outcome of unit depends on the treatment assignment of all units under the study. Thus, there are a total of potential outcomes, which can be assembled in the form of an table, as shown in Table 2. The rows in Table 2 correspond to the units and the columns correspond to the treatment assignments; the entry corresponds to the potential outcome of unit under treatment represented by column . This table is referred to as the Table of Science and denoted by .

Remark 1.

We have made an implicit assumption of no hidden versions of a treatment which appears as the second part of the SUTVA, see section 3.5 for more details.

Causal effects are defined as functions of the entries of Table of Science. In particular, Causal effects can be defined as contrasts between functions of potential outcomes under two distinct treatment assignments. For example, let and be two distinct treatment allocations in , i.e., , then an example of a causal effect is

In Section 3.3 we consider two different classes of estimands or causal effects. The fundamental problem of Causal Inference is that the table of science is unknown and only one entry of Table 2 can be observed.

More specifically, let denote the random vector of treatment assignments and be a probability distribution defined over the set of all possible treatment assignments . is called the treatment assignment mechanism or a design. In many cases, we can also restrict ourselves to , the support of the treatment assignment mechanism. Under a random treatment assignment , without any further assumptions, only one random entry of each row of Table 2 can be observed, i.e. for each unit , only one of it’s potential outcome can be observed. For example, if the realized treatment Z corresponds to column , then only column is observed. Since causal effects are defined as contrasts between two different treatment assignments, they cannot be estimated if only one column is observed.

| Treatment | ||||||

|---|---|---|---|---|---|---|

| Units | ||||||

Proposition 3.1.

Causal effects are unidentifiable without any assumptions on the potential outcome functions .

Proof.

Since there are no further assumptions on the potential outcomes, only one entry of the table of science is observable due to the fundamental problem of causal inference. As causal effects are defined as contrasts between two distinct treatment assignments, they are unidentifiable as only one entry of the Table 2 is observed. ∎

Proposition 3.1 is a simple observation but has profound consequences. It implies that Causal Inference is impossible without further assumptions on the potential outcomes. Hence we are forced to make modeling choices to make progress. Indeed the bulk of Causal Inference since past 40 years has been centered around the no-treatment interference assumption, which is embedded in SUTVA assumption. One can consider the no-interference assumption as a very specific model on the potential outcomes. Under SUTVA, and Table 2 reduces to an table. Thus, the question is not “why a model”, but rather “which model”? We discuss a series of modeling assumptions on potential outcomes that allow tractable causal inference.

3.2 Modeling Potential Outcomes under Network Interference

In this section, we describe models for potential outcomes when there is arbitrary interference due to treatment. As we saw in the previous section, when there is arbitrary interference, modeling potential outcomes becomes necessary without which Causal Inference is impossible. Our framework makes these modeling choices easy to specify and transparent to present. This framework unifies existing models for potential outcomes under treatment interference - many existing models can be instantiated as special cases of our framework. We also develop a linear decomposition of potential outcomes that is useful for interpreting causal effects and studying estimators.

Models of potential outcomes are specified by specifying three different components: an interference neighborhood, an exposure model and a structural model. These components are hierarchical in nature. Each of these components build upon the other, and they need to be defined in this order. For example, to define an exposure model, we need to define the interference neighborhood, and so on. We give an informal description of these components before moving to the formal definitions.

The interference neighborhood, denoted by , defines the set of units whose treatment assignment can potentially influence unit ’s outcomes. Any unit outside the interference neighborhood cannot influence ’s potential outcomes. For example, in educational studies, can be the school that unit belongs to. Any unit outside unit ’s school does not effect the outcome of unit . In this example, interference neighborhoods can be partitioned into non-overlapping sets. In more general settings, e.g. in the context of social networks or vaccination studies, the interference neighborhoods of units may overlap with each other and can be more complex. Next, the exposure model defines what it means for a unit to be exposed and defines the set of relevant exposure conditions of a unit . For example, a unit may be said to be exposed to the treatment if all the units in it’s interference neighborhood are treated, or if a fraction of them are treated and so on. The exposure level of a unit need not be a binary variable, but a continuous quantity. For example, it could be the case that there is a gradual increase in exposure, i.e. as more and more units in ’s interference neighborhood get treated, gets “more” exposed. Finally, a structural model defines or imposes structural constraints on different potential outcomes of each unit . One can think of structural models as a way to specify null hypothesis of interests on individual level potential outcomes. For example, a linear model specifies that the potential outcomes are linearly related to the treatment and the exposure conditions. We will discuss these three components in more detail and give their formal definitions along with several examples.

3.2.1 Interference Neighborhood

The interference neighborhood or neighborhood of a unit (not to be confused with the neighborhood of a node in a graph) is denoted by and is defined as the set of units whose treatment status may effect the outcome of unit . Let denote the vector z sub-setted by the indices in . Let z and be two distinct potential outcomes. Then given a choice of the interference neighborhood for each unit , we make the following assumption:

| (5) |

This allows us to write down the potential outcome of each unit in the following manner:

| (6) |

where denotes the treatment assigned to unit and denotes the vector of treatment assigned to units in the interference neighborhood of unit .

Remark 2.

Note that the interference neighborhood of each unit can be different and hence can be of different length. Moreover, a unit may be in unit ’s interference neighborhood, but may not be in ’s neighborhood. Finally, Interference neighborhoods of two units may overlap, they may be disjoint or they can also be the same.

We will now consider two simple, but extreme examples of interference neighborhoods.

-

1.

No treatment interference: for each unit

-

2.

Complete interference:

The simplest example is the setting of no treatment interference, which amounts to saying that the outcome of unit does not depend on the treatment of any other unit. At the other extreme is complete interference, where the treatment of every unit can effect the outcome of unit . The first example reduces to the classical SUTVA setting, and in the second example, there is no causal inference possible, unless we make additional assumptions (specified by an exposure model and/or a structural model to be defined below). The most interesting cases are when we can consider interference neighborhoods that lie in between no-interference and complete-interference. To model these intermediate cases, it turns out to be convenient to define interference neighborhoods using a graph.

Graph Induced Interference Neighborhoods

A convenient way to specify the interference neighborhood of a unit is by the means of an interference graph. Let be a fixed, known graph on nodes with as its vertex set and as its edge set. The introduction of an interference graph allows us to introduce additional structure into the nature of interference. Note that in general, can be asymmetric and even weighted. For simplicity of notation, we will assume for the rest of the paper that is symmetric and un-weighted, i.e. if denotes the edge from unit to unit , we will assume . All these ideas apply to an asymmetric weighted graph with additional notation.

We now consider a few examples of graph induced interference neighborhood:

-

1.

1 hops interference:

-

2.

2 hops interference:

-

3.

hops interference:

Remark 3.

The interference graph is an abstract representation of the interference that may exist in the real world setting. In general may not be observable, random or may not even be well defined. How does one choose ? This is an important question and beyond the scope of this paper. But we will give some remarks. In many cases, may be clear from the study. For example, consider the setting of partial interference. In this setting, the units can be partitioned into disjoint groups . Interference may happen within the groups but not between the groups, see for e.g. Sobel (2006) or Hudgens and Halloran (2008). The interference graph in this case consists of a collection of disjoint cliques. In many other settings, one may observe a social graph which can serve as a good approximation for , (e.g. Facebook). It may also be the case that we observe a network but posit that the interference may happen only along stronger social ties, for e.g. frequently contacted friends, as opposed to all friends in a social network. In such cases, the interference graph may be an induced subgraph of the social graph. One may also consider as random and posit a distribution over . This leads to additional complexities that are beyond the scope of this paper.

For the remainder of the paper, we will assume that the interference neighborhood for each unit is defined through a fixed graph on units.

3.2.2 Exposure Models

After defining the interference neighborhood, there are two modeling choices remaining for specifying potential outcomes and for making causal inference tractable (i.e. to ensure that the table of science as shown in Table 2 not too wide) - the so called exposure model and the structural model. The exposure model specifies how the treatment status of units in effect the outcome of . It defines the relevant levels of exposure and how the treatment levels of the interference neighborhood get mapped to these levels.

Formally, the exposure model is specified by an exposure function that maps to a range . The range of specifies the relevant exposure levels and the mapping specifies how the treatment patterns of map to different exposure levels. To this end, let us assume that the potential outcome function depends on through a function

Let be the number of units in the interference neighborhood of . The domain of is the set of all possible treatment assignments of the neighborhood of a unit . The domain of has at most elements and is finite. Hence the range of is also finite. This is because for each treatment assignment , can map to at most one exposure level. Let denote the size of the range. Thus, for every unit , there are different levels of exposure. Without loss of generality, we can write the range of as .

Given an exposure function , let . Thus we can write the potential outcome function for each unit as

| (7) |

and takes values in .

To specify an exposure model, one must specify the function and the levels of exposure . The total number of exposure patterns depends on the choice of and . When is a one to one mapping, there are a total of levels of exposure for each unit . Clearly, an that is onto reduces the number of exposure levels and hence the total number of possible potential outcomes.

In the most general case, one can set and to be a one to one function. In this case, and there is no reduction in the number of potential outcomes. On the other extreme, when , we are in the setting of no interference. Intermediate cases are more interesting and can be defined by a network interference graph . To ensure identifiability we need .

Remark 4.

Note that is a way of indexing the different types of possible exposure patterns or levels and the symbols denote these exposure patterns as defined by the function . The interpretation of the symbols is a choice of the definition of . For example, statements such as “a unit is exposed if of it’s neighbors are treated” can be the modeled by mapping to the appropriate fractions.

We will define two special symbols for two commonly used values of the exposure patterns: is called no exposure and is full exposure. The exposure function also specifies what it means for a unit to be fully exposed and not exposed. We give two examples:

-

1.

, when all elements of are 0 and when all elements are 1.

-

2.

when all elements of are and when at least one element is .

Remark 5.

A possible exposure function is one that maps to the number of units in that are treated. One subtle issue with choosing such an exposure function is that the levels of exposure function depends on the maximum degree in the graph . If is not a regular graph, i.e. the degree of each node is different, then the exposure levels of each unit is different, which may not be desirable depending on the application. These are subtle issues that need to be resolved and are out of the scope of our paper.

Let us consider a few examples of exposure functions:

-

1.

Symmetric Exposure: is symmetric in the indices of

-

2.

Linear and Additive Exposure:

-

3.

Linear Exposure: .

It is also possible to define more complex exposure functions. For example, consider a setting when the interference neighborhood is specified through a graph . The interference neighborhood of unit is the set of units in that have a connected by a path of size to , i.e. through friends and friends of friends of unit . The exposure function can be parametric that allows the potential outcomes to depend on through a weighted combination of the number of treated friends in and the number of treated friends of treated friends.

Remark 6.

Note that we have made an assumption that the exposure function is independent of the unit , i.e. we do not allow to depend on . For example, we do not allow exposure functions where unit ’s exposure depends on the number of treated friends and unit ’s exposure depends on both the number of treated friends and the number of treated friends of friends. However, the range of may depend on .

3.2.3 Structural Models

Parametrization of Potential Outcomes under Neighborhood Interference

Before defining a structural model, it is convenient to introduce a parametrization or a linear decomposition of potential outcomes into direct and indirect effects. This parametrized form of potential outcomes allows one to define and focus on various treatment effects of interests. We present one such parameterization. When is the interference neighborhood and is the exposure model, every unit has potential outcomes, that can be parametrized by parameters, as given in Proposition 3.2.

Proposition 3.2.

For each unit , let where is the interference neighborhood. The potential outcomes can be parametrized as

| (8) |

where , and .

Remark 7.

Equation 8 resembles a linear model for Potential Outcomes. However, it is not a linear model in the usual sense of linear regression. Unlike regression, which is a model of conditional expectation, there are no random variables. Moreover, the parameters are not linear, and they depend on .

This parametrization has a nice interpretation: The parameters represent the direct treatment effects or the part of the Potential outcome that depends only on a unit ’s treatment. The and parameters represent the indirect or interference effects, i.e. the part of the potential outcome that depends on the exposure level. In particular, the parameters represent the additive interference effect and the parameters represent the interaction between the additive interference and the direct treatment effects, see also section 3.3. Given this linear parametrization, we are now ready to specify structural models.

Structural Model

Up to this point, we have made no assumptions on how the potential outcomes relate to each other, we have only focused on reducing the number of potential outcomes. However, in some cases, we may also make additional modeling assumptions on how one potential outcome relates to another. Sometimes these assumptions serve as null hypothesis for treatment effects. These are called structural modeling assumptions as they impose a structure on different potential outcomes. Given the parameterization in equation 8, structural assumptions can be regarded as restrictions on the parameters of the potential outcomes. Without any structural assumptions, the parameterizations are functionally independent of each other. Structural assumptions make the parameters functionally dependent. Examples include, linear models, additive models and so on. Some examples of structural assumptions are stated below:

-

1.

Additivity: .

-

2.

Constant effects: , and .

-

3.

Linear Effects:

-

4.

Constant Additive Effects and .

-

5.

Sharp Null: .

Remark 8.

The interference neighborhood reduces the number of potential outcomes for each unit from to . An exposure model of the Potential Outcomes further reduces the number of potential outcomes for each unit from to a tractable number . On the other hand, a structural model of the Potential Outcomes specifies a relationship between the different potential outcomes by imposing constraints on the parameters.

3.2.4 Some models of Potential Outcomes under interference

Different choices of the interference neighborhood, the exposure function and the structural model lead to different models for the potential outcomes. In this section, we present specific choices that give rise to some models used in the paper. These examples illustrate how one can use the framework to reduce the number of potential outcomes and model them. We start with the parametrized model of potential outcomes modeled using the interference neighborhood and the exposure function :

| (9) |

where and .

Symmetric Exposure Models

Model 1: Symmetric Exposure

Let denote the neighborhood of a unit as specified by the interference graph , i.e.

Next, let , then we get the following model:

| (10) |

where and is the degree of unit in the interference graph . Under this model, each unit has potential outcomes.

Starting with equation 9, we can make additional structural assumptions to get simpler models for the potential outcomes. We give two examples below.

Model 2: Symmetric Linear exposure

In Model 1, Let and

| (11) |

Model 3: Symmetric Additive Linear exposure

In Model 2, Let

| (12) |

Binary Exposure Models

The binary exposure model is te simplest exposure model that weakens the no-interference assumption. In these models, the range of the exposure function is always , where is interpreted as not exposed and is interpreted as exposed. The definition of specifies which treatment levels get mapped to or and is chosen based on the application. In the binary exposure model, each unit has potential outcomes, in contrast to 2 potential outcomes per unit in the SUTVA case. The binary exposure model is the simplest possible model of potential outcomes when there is interference. We present below a simple but natural choice of such a binary exposure function where a unit is said to be exposed if at least one of it’s neighbor is treated.

Model 4: Binary exposure

Let be

Let if all elements of are and if at least one element of is . This gives us the so called two by two potential outcomes model or the binary exposure model:

| (13) |

where and .

As in the previous case, one can impose structural assumptions on the binary exposure model to generate simpler models.

Model 5: Additive Binary exposure

Let in model 4, then we get the additive two by two model of potential outcomes

| (14) |

3.3 Defining Causal Effects under Network Interference

Given an interference neighborhood and a corresponding exposure function , causal effects or estimands are defined as contrasts between potential outcomes under distinct treatment and exposure assignments. Under interference, there are many non-equivalent ways of defining causal effects. The definition of the estimand depends on the question one is interested in answering. It is important to note that the estimands are defined only using the table of science, and they do not depend on the actual treatment assignment mechanism used to estimate them.

For a given exposure function , each unit has distinct potential outcomes denoted by where and . These potential outcomes can be assembled in the form of a Table of Science as before. The number of columns of the Table of Science in Table 2 reduce from to columns where is the number of exposure levels for each unit . The columns of the table of science now correspond to the relevant treatment and exposure conditions as specified by . For instance, under the binary exposure model, the table of science has columns and rows. This is the simplest setting of a Table of Science that relaxes the no-treatment interference assumption. Causal effects are functions of at least two columns of .

Before we define causal effects, we need some additional notation. A fixed treatment assigned vector z gets mapped to different treatment and exposure combination for each unit . Moreover, different treatment assignment vectors can get mapped to the same treatment and exposure combination. Formally, let and denote a generic treatment and exposure condition. Let

be the set of all treatment assignment vectors that give rise to treatment and exposure for a unit .

We will consider two classes of estimands: marginal and average causal effects: The marginal effects are defined as contrasts between two different randomized treatment policies. The average effects are a contrast between two different types of potential outcomes. In some cases, both definitions can lead to the same estimand, but it is not true in general.

Marginal Effects

Let us first consider the marginal effects that are defined as contrasts between two randomized treatment assignment mechanisms. We will refer to such treatment assignments as policies to distinguish them from the actual treatment assignment mechanism used in the experiment. For instance, a policy can be to treat randomly chosen of the units in the population, or to treat of the units in the population and so on. Let and be two policies, i.e. and are two distributions over Z. Similar to Hudgens and Halloran (2008), we define conditional and marginal potential outcomes of a unit as expectations of potential outcomes under a treatment policy. Let denote the random exposure condition of unit .

Definition 1 (Conditional and Marginal Potential Outcomes).

Here and . Given the conditional and marginal potential outcomes, various causal effects can be defined as follows:

One can define total, direct and indirect causal effects using these definitions, and consider various decompositions among them.

Average Causal Effects

An alternate way to define causal effects is to consider contrasts between two fixed types of potential outcomes. Let us consider a generic causal estimand defined as a contrast between two different treatment and exposure combinations: and :

| (15) |

The most popular average causal effects are the Average treatment effects and the Average interference effects. We will consider two types of average treatment effects: the direct treatment effect (DTE) and the total treatment effect (TTE) that are defined below. Recall that the exposure levels and are special values defined to represent the situations when a unit is not exposed or exposed respectively. Direct effects are defined as contrasts between the conditions and , i.e. when a unit is treated and not exposed vs when a unit is neither treated nor exposed.

Definition 2 (Direct Treatment Effect).

Similarly, one can consider the total treatment that is a contrast between and when a unit is treated and exposed vs when a unit is neither treated nor exposed.

Definition 3 (Total Treatment Effect).

Similarly, one can also define average estimands that measure interference effects:

Definition 4 (Average Interference Effects).

Relation between the estimands

As we saw, there are two ways to define causal effects. The marginal effects defined as a contrast between expectations of the potential outcomes under two different randomization policies, and the average effects defined as a contrast between averages of potential outcomes. These two definitions are non-equivalent in general. However, under SUTVA, the marginal effects and the average effects reduce to the classical ATE, as the following proposition shows:

Proposition 3.3.

Assume that . Then we have where

Remark 9.

Under the no interference assumption, the direct and the total effect reduce to the “usual” classical version of ATE. Moreover, the average interference effects are under no-interference. But under interference, the direct and the total effects are different, and the average interference effects are not . For example, consider the following linear model of the potential outcomes:

Let . Under this model, and . where is the number of treated neighbors of unit in . However, if and , then . Hence we have the following proposition:

Proposition 3.4.

Consider the linear additive symmetric exposure model of Potential Outcomes given by equation 3.2.4, and let , and and . We have , , , and .

Note that one can obtain as a special case of , but this is not the case for .

Proposition 3.5.

Consider the following two degenerate policies and

Then .

Obtaining as a special case of is not possible. This is because there is no single policy (degenerate or non-degenerate) that allows us to estimate . We need to define different degenerate policies, where

then

A similar analysis can be done for the interference effects and .

Definition 5 (Irrelevant or nuisance potential outcomes).

Let a causal estimand be a function of . We will call such potential outcomes as relevant. Potential outcomes that are not relevant are nuisance or irrelevant potential outcomes.

For instance, consider the average causal estimands defined as contrasts between fixed potential outcomes, i.e. the direct treatment effect and the total treatment effect. If we make no structural assumptions, then each causal effect is a function of only two columns in the Table of science, and the other columns are irrelevant. For e.g. potential outcomes of the form are not relevant for estimating , since is a function of only and . In this sense, if the goal is to only estimate , then designs that generate other potential outcomes are wasteful.

Similarly, consider the marginal causal effects defined as contrast between expected potential outcomes under different policies. All the potential outcomes that have positive probability under the policy are relevant. On the other hand, potential outcomes that have probability under the policy are nuisance. If support of the policy is , the causal effect is a function of the entire table of science and all potential outcomes are relevant.

As we will see in Section 4, average causal effects like the DTE and TTE are more difficult to estimate, and the nuisance potential outcomes form a source of bias when using difference-in-means estimators. We need new designs along with Horvitz-Thompson estimators for unbiased estimation of average estimands. On the other hand, it is simpler to estimate marginal estimands as long as the actual randomization follows the policies of interest. One can use difference of means estimators to estimate marginal estimands.

3.4 Designs, Estimators and Strategies

We will now consider the problem of estimation of causal effects and the existence of estimators. Our focus will be on randomization based inference where the potential outcomes are considered to be fixed and the only source of randomness is due to the random assignment of treatment vector z. Under this setting, a random assignment Z is sampled according to and the units are assigned to the treatment Z. The outcome observed for each unit is denoted by .

Consider an interference and exposure model of potential outcomes specified by a graph and an exposure function . Let be a generic causal estimand defined as a function of .

Definition 6 (Design).

A design is a probability distribution supported over , the set of all possible treatment assignments for units.

In general, the design may depend on the interference graph and the exposure function . We will suppress the dependence on and for simplicity. Designs that do not depend on the interference graph are called network-oblivious designs. Such designs are preferred in the case when is unknown, however, these designs may not be optimal.

Given a realization z of a design , let be the set of observed potential outcomes, where is the Table of Science.

Definition 7 (Estimator).

An estimator for is a function of the observed potential outcomes .

We are now ready to define an estimation strategy. An estimation strategy for estimating a causal effect is a combination of a design and an estimator to be used with that design.

Definition 8 (Estimation Strategy).

An estimation strategy or simply, a strategy for estimating is a pair .

Estimation strategies are evaluated based on their properties such as unbiasedness and variance. An estimation strategy is said to be unbiased for estimating if

An estimator is said to be unbiased for if it is unbiased for any design . For a given , one goal is to construct strategies that are so called uniformly minimum variance unbiased (UMVU), see for e.g. Särndal et al. (2003). It is well known that such strategies don’t exist, even with the no-interference assumption. We will focus only on the unbiasedness properties of an estimation strategy.

3.5 Existence of estimators

We will now consider the assumption to ensure causal estimates are identified. We first start with the classic SUTVA assumption and present it’s counterpart when there is treatment interference. When there is no interference, Stable Unit Treatment Value Assumption (SUTVA) has two parts:

-

1.

No Interference: The potential outcome of unit depends only on the treatment of unit .

-

2.

Consistency or Stability: There are no hidden versions of the treatment.

The first part of SUTVA says that the potential outcome of a unit depends only on its treatment assignment. The second part says that there are no hidden versions of the treatment. Put in a different way, the stability assumption states that there is only one column corresponding to a treatment in the table of science. Under interference, we consider both these parts of SUTVA separately. The first part of SUTVA is relaxed to neighborhood interference by considering models of potential outcomes, and the second part of SUTVA is modified to the “no hidden versions of treatment and exposure assumption”.

Neighborhood Interference

The neighborhood interference assumption states that the potential outcome of unit depends on its treatment and the treatment status of it’s interference neighborhood as specified by the exposure models, i.e.

where and is the exposure model.

Consistency or Stability

The consistency assumption states that the observed outcome of a unit is exactly equal to the unit’s potential outcome under the assigned treatment and exposure combination, that is, there are no hidden versions of the treatment and exposure combination.

| (16) |

Unconfoundedness

Unconfoundedness assumption states that the treatment assignment mechanism does not depend on the potential outcomes .

Positivity

To state the positivity assumption, we need some preliminary definitions. Recall that . Let and denote a generic treatment and exposure condition. Recall that

is the set of all treatment vectors that give rise to and for unit .

Definition 9 (Propensity Scores).

The propensity score for each unit for treatment and exposure pair denoted by is defined as follows:

| (17) |

Let the causal estimand be a function of . We will call such potential outcomes relevant. Potential outcomes that are not relevant are nuisance. Then we need

| (18) |

The positivity assumption implies that there is a positive probability of observing the relevant potential outcomes for each unit.

Example 1.

For example, is a function of and . Hence the positivity condition requires that

| (19) |

If the positivity condition is not satisfied, the relevant potential outcomes are not observable and causal inference is not possible. In particular,

Theorem 3.1.

Let be any design and let be the set of relevant potential outcomes for any estimand . Without any structural assumptions on the Potential Outcomes, unbiased estimators of under a design exist iff

Example 2.

The positivity assumption depends not only on the design, but also on the interference graph and the exposure model. Consider an interference graph with a linear exposure model. If there is a unit with degree , then either or for all . This is because the only way can be observed if all units are assigned to control, i.e. . However, under this assignment, is unobservable for any . That is when degree is , it is impossible to observe both and . A solution is to allow for biased estimators or to exclude nodes with degree from the definition of causal effect. Note that in practice, such networks may be rare.

3.6 Commonly used designs and estimators

In this section we will consider some classical designs and estimators that are used for estimating causal effects. We will start by considering three classic designs used for estimating causal effects; these designs are commonly used when there is no treatment interference. Since these designs no not depend on the interference graph and the exposure function, they are network-oblivious. We will examine the applicability of these designs in estimating causal effects when there is interference.

Completely Randomized Design

In a Completely Randomized Design (CRD), the treatment is assigned by fixing the number of treated and control units to and such that , and choosing random units without replacement to be assigned to treatment, the rest of the units are assigned to control. The probability distribution is hyper-geometric:

Note that the entries of Z are correlated.

Bernoulli Randomization

In a Bernoulli trial, each unit is assigned to treatment independently with probability . The total number of treated and control units are random. The probability distribution of a Bernoulli trial is:

In the Bernoulli trial, there is a positive probability that all units get assigned to either the treatment or control, violating the positivity assumption. A simple way to avoid this is to consider a restricted Bernoulli trial. Under a restricted Bernoulli trial, the number of treated unit and control units is always at least . The probability distribution of a restricted Bernoulli trial is:

Cluster Randomization

In a cluster randomized design, units are grouped to form clusters and these clusters are randomly assigned to the treatment or control condition, i.e. the randomization happens at the cluster level. The treatment status of a unit is equal to the treatment assigned to it’s cluster.

Formally, let the units be partitioned into clusters. Let be the number of units in each cluster where . Note that the ’s are fixed. Let denote the treatment assignment of cluster and let denote the cluster that unit belongs to. Thus we have . The random assignment of clusters to treatment or control is done by a completely randomized design. Let and denote the number of treated and control clusters respectively. Let be the total number of treated nodes and be the total number of control nodes. Note that and and hence and are random.

Remark 10.

One can consider a Bernoulli assignment of clusters to treatment and control. The Bernoulli assignment is not preferred as one has no control over the number of clusters assigned to treatment or control.

Next, we will discuss two classes of estimators.

Difference-in-Means Estimators

The difference-in-means estimators are simplest estimators. These estimators are defined as difference of means between two types of observed potential outcomes. We consider the following three difference-in-means estimators, the first one of which is the classic difference-in-means:

| (20a) | ||||

| (20b) | ||||

| (20c) | ||||

Linear Estimators

4 Analytical insights for Difference-in-Means Estimators

In this section we study various estimation strategies that use a combination of difference-in-means estimators and classical designs for estimating causal effects when there is interference. We will focus on the nature and source of bias, if any, for estimating average and marginal causal effects. The nature and source of bias depends on the estimand, the estimation strategy (i.e. the design and the estimator) and the model for potential outcomes.

In Section C we show that the difference-in-means estimator is unbiased for estimating marginal effects. This section is devoted to understanding the nature of bias when using difference-means estimators to estimate the direct treatment effect (DTE). We will consider different models of potential outcomes when estimating the direct effect using the difference of means estimators. The role of these models is to gain some analytical insights into the nature of bias and it’s dependence on the modeling assumptions.

4.1 Sources of bias in estimating the direct and the total effect

Without making any structural assumptions on the potential outcomes, (i.e. without any assumptions on how one potential outcome is related to another) the difference-in-means estimators given in equation 20 have two different sources of bias for estimating the total effect and the direct effect:

-

1.

The first source of bias is due to unequal weights given to the potential outcomes, or equivalently, unequal probability of including in the sample for estimating the mean potential outcomes. For some designs, this source of bias can be eliminated.

-

2.

The second source of bias is due to the inclusion of irrelevant potential outcomes, i.e. potential outcomes other than those used in the definition of the corresponding causal effect. For example, when estimating DTE, these would be any other potential outcomes other than and .

Proposition 4.1 characterizes the bias of the naive estimator in estimating the direct treatment effect. For the bias of estimating using the naive estimator, see Proposition D.1 in Appendix.

Proposition 4.1.

Next Proposition 4.2 shows that the difference of means estimators and are also biased, but the source of bias is milder when compared to the naive estimator.

Proposition 4.2.

where,

Propositions 4.1, 4.2 and D.1 suggests that for any design , the biases in estimating the direct and the total treatment effects using difference-in-means estimators are controlled by the weighted exposure probabilities under that design. For instance, as Proposition 4.1 shows, without making any structural assumptions on the potential outcomes , the bias of in estimating is only if and . The first condition removes the first source of bias by placing equal weights on the relevant potential outcomes, and the second condition removes the second source of bias by placing weights on irrelevant potential outcomes. Similarly, as seen by Proposition 4.2, the estimators and remove the second source of bias by eliminating irrelevant potential outcomes, but the first source of bias remains.

4.2 Characterization of bias under various models of Potential Outcomes

The bias of the difference-in-means estimators depends on the weights . These weights depend on the design and the exposure model. To gain additional insight into the nature of the bias, we will make several modeling assumptions on the potential outcomes. These assumptions allow us to computing the exposure weights analytically for commonly used designs. We will focus on the bias of estimating the direct effect using the naive estimator . We also ask the related question: Does the bias in the difference-in-means estimator disappear if we make structural assumptions on the Potential Outcomes?

4.2.1 Symmetric Exposure Model

We begin by considering the Symmetric exposure model given in equation 10 and computing the exposure weights for CRD and Bernoulli designs.

Theorem 4.1 (Exposure Weights for Symmetric Exposure).

Consider the symmetric exposure model of potential outcomes given in equation 10. Under a CRD and a Bernoulli design, we have . On the other hand, under a cluster randomized design, . For a CRD design,

For a Bernoulli design, let be a restricted binomial random variable with support on and . Then,

Theorem 4.1 shows that the first source of bias gets eliminated under the CRD and the Bernoulli designs. Does the second source of bias disappear under these designs? Without any further assumptions, the answer is no. However, under additional assumptions, the second source of bias can go to asymptotically, or even be made exactly . Examination of the second source of bias requires computing the weighted exposure probabilities under the CRD, Bernoulli designs and Cluster Randomized designs, which depend on the exposure model. Computing under the Bernoulli and cluster randomized designs is further complicated by the fact that, unlike the CRD, the denominator is a random variable that is correlated with numerator. Moreover, due to the overlapping neighborhoods, the correlation depends on a complicated manner on the graph . Similar issues prevent us from obtaining explicit formula for . However, progress can be made by computing the bias directly under some structural assumptions.

4.2.2 Additive Symmetric Exposure model

Let us consider the additive symmetric model given by equation 21 below which is obtained by making the structural assumption in equation 10.

| (21) |

where .

Corollary 1.

Let , . The bias in estimating using the difference-in-means estimator under the CRD and Bernoulli designs is

4.2.3 Symmetric Additive Linear exposure

Consider the symmetric additive linear model of the potential outcomes model specified by equation 3.2.4 and further assume constant interference effects, i.e. . This gives us the following linear model of Potential outcomes:

Proposition 4.3.

Under a completely randomized design, we have,

where is the number of edges in the interference graph.

Bernoulli Randomization

Proposition 4.4.

Under a restricted Bernoulli trial, we have,

Remark

Propositions 4.3 and 4.4 show that even under the structural assumptions of additivity, linearity and constant interference effect, there is always a bias due to the interference. The bias is independent of and in the CRD and in the Bernoulli designs. The bias is in the opposite direction of the interference effect, i.e. a positive interference leads to smaller estimate of the average treatment effect when compared to the true . The bias scales as , hence for sparse and large network, asymptotically, the bias goes to 0. Is it possible for the bias to be exactly ? The answer is yes, and further explained in the next section.

4.2.4 Binary Exposure Model

In this section we consider the binary exposure model given in equation 13 and study the bias of for estimating DTE.

Completely Randomized Design

Proposition 4.5.

Under model 13, we have, for a CRD

Bernoulli Randomization

Proposition 4.6.

For a Bernoulli trial, we have

Under the structural assumption of additivity we have . In this case, by Proposition 4.5 it follows that the bias of the difference-in-means estimator can be when . Thus, we have the following result:

Proposition 4.7.

Consider the binary additive exposure model 14. Under the completely randomized design, if , then the bias of the difference-in-means estimator in estimating is .

5 Linear Unbiased Estimators

For any design , we can construct unbiased estimators of causal effects by using standard techniques from the survey sampling literature. Let us consider a generic average causal estimand defined as a contrast between two different treatment and exposure combinations: and :

| (22) |

For example, if and , and so on. Following Godambe (1955), let us consider the most general class of linear weighted estimators for estimating , i.e

| (23) |

Here is the weight assigned to unit . Note that the weight assigned to unit depends on the treatment assigned to all the units in the finite population, i.e it depends on z. The set of weights that lead to unbiased estimators of can be characterized as a solution to a system of equations that depend on the design, interference graph and the exposure model.

Theorem 5.1.

Consider an exposure model where is specified by an interference graph . Assume that there are no structural assumptions on the potential outcomes. Let . Similarly, let . The estimator in equation 23 is unbiased for if and only if and and satisfy the following system of equations:

Recall that are the set of treatment allocations that reveal the potential outcome for unit . Note that these sets depend on and are different for each unit. In general, there can be infinitely many solutions to the system of equations in Theorem 5.1 depending on the interference graph, exposure model, and the design. Hence there can be infinitely many unbiased estimators of . For each unit , let us consider the number of equations and the number of unknowns . For each , there are unknown weights which depend on the support of the design. On the other hand, there are linearly independent equations in Theorem 5.1 which depend on the exposure model. Recall that is the number of levels of exposure for unit . Hence linear weighted unbiased estimators don’t exist if for each , . We have the following result:

Proposition 5.1.

Let be the number of allocations and be the number of levels of the exposure model for each unit . If for each , and , there are infinitely many linear unbiased estimators of .

Table 3 gives the values of and for some exposure models and designs. For instance, under a restricted Bernoulli design, there are unknown weights, since and is not allowed as it violates the positivity assumption. On the other hand, for a symmetric exposure model, there are equations where is the number of units in .

| Symmetric Exposure | Binary Exposure | General Exposure | |

|---|---|---|---|

| Bernoulli | |||

| CRD | |||

5.1 Horvitz-Thompson Estimator

If the weight of a unit is allowed to depend on z only through and , then we get a smaller class of linear estimators of the following form:

| (24) |

The restriction on the weights is a form of sufficiency: instead of the weight depending on the entire vector z, it depends only on . Since the potential outcomes are reduced from to , it is natural to consider such a reduction of the weights from to .

Theorem 5.2 shows that under no structural assumptions on the potential outcomes, the only unbiased estimator of type is the Horvitz-Thompson estimator.

Theorem 5.2.

Consider the estimators of type given by equation 24. Without any structural assumptions on the potential outcomes, the only unbiased estimator of in this class is the Horvitz-Thompson estimator where

The HT estimator eliminates both sources of bias mentioned in Section 4 by choosing the correct weights. In particular, the HT estimator assigns a weight of to nuisance potential outcomes, and a positive weight to relevant potential outcomes. The positive weight is inversely proportional to the probability of observing that potential outcome under the design . The HT estimator depends on the propensity scores . As mentioned before, these probabilities depend on the design and the exposure model. We compute an analytical formula of these probabilities for the CRD and the Bernoulli designs for different exposure models.

Theorem 5.3 (Propensity Scores for Symmetric Exposure).

Consider the symmetric exposure function, , . For a CRD Design,

For a Bernoulli Design,

Theorem 5.4 (Propensity Scores for Binary Exposure).

Consider the symmetric exposure function, , . i.e a unit is exposed if at least 1 of its neighbor is treated. For a CRD,

Similarly, for a Bernoulli trial with probability of success , we have

Under a cluster randomized design, let be the number of clusters of unit and it’s neighbors. Assume .

Remark 11.

The weights of the HT estimator depend on the exposure model and the interference graph . In cases where the interference graph is not known, the HT estimator may not be usable.

Remark 12.

The weights of the HT estimator depend only on the exposure model and the design. They do not depend on the structural model. For example, in the linear model of Potential Outcomes, the HT weights do not depend on the linearity of the model, but only on the exposure neighborhood.

Remark 13.

For a clustered randomized design, we cannot estimate using HT estimators because some propensity scores are .

5.2 Inadmissibility of the Horvitz-Thompson estimator