Bregman Divergence Bounds and

Universality Properties of the

Logarithmic Loss

Abstract

A loss function measures the discrepancy between the true values and their estimated fits, for a given instance of data. In classification problems, a loss function is said to be proper if a minimizer of the expected loss is the true underlying probability. We show that for binary classification, the divergence associated with smooth, proper, and convex loss functions is upper bounded by the Kullback-Leibler (KL) divergence, to within a normalization constant. This implies that by minimizing the logarithmic loss associated with the KL divergence, we minimize an upper bound to any choice of loss from this set. As such the logarithmic loss is universal in the sense of providing performance guarantees with respect to a broad class of accuracy measures. Importantly, this notion of universality is not problem-specific, enabling its use in diverse applications, including predictive modeling, data clustering and sample complexity analysis. Generalizations to arbitary finite alphabets are also developed. The derived inequalities extend several well-known -divergence results.

Index Terms:

Kullback-Leibler (KL) divergence, logarithmic loss, Bregman divergences, Pinsker inequality..

I Introduction

One of the major roles of statistical analysis is making predictions about future events and providing suitable accuracy guarantees. For example, consider a weather forecaster that estimates the chances of rain on the following day. Its performance may be evaluated by multiple statistical measures. We may count the number of times it assessed the chance of rain as greater than 50%, when there was eventually no rain (and vice versa). This corresponds to the so-called 0-1 loss, with threshold parameter . Alternatively, we may consider a variety of values for , or even a completely different measure. Indeed, there are many candidates, including the quadratic loss, Bernoulli log-likelihood loss, boosting loss, etc. [2]. Choosing a good measure is a well-studied problem, mostly in the context of scoring rules in decision theory [3, 4, 5, 6].

Assuming that the desired measure is known in advance, the predictor may be designed accordingly—i.e., to minimize that measure. However, in practice, different tasks may require inferring different information from the provided estimates. Moreover, designing a predictor with respect to one measure may result in poor performance when evaluated by another. For example, the minimizer of a 0-1 loss may result in an unbounded loss, when measured with a Bernoulli log-likelihood loss. In such cases, it would be desireable to design a predictor according to a “universal” measure, i.e., one that is suitable for a variety of purposes, and provide performance guarantees for different uses.

In this paper, we show that for binary classification, the Bernoulli log-likelihood loss (log-loss) is such a universal choice, dominating all alternative “analytically convenient” (i.e., smooth, proper, and convex) loss functions. Specifically, we show that by minimizing the log-loss we minimize the regret associated with all possible alternatives from this set. Our result justifies the use of log-loss in many applications.

As we develop, our universality result may be equivalently viewed from a divergence analysis viewpoint. In particular, we establish that the divergence associated with the log-loss—i.e., Kullback Leibler (KL) divergence—upper bounds a set of Bregman divergences that satisfy a condition on its Hessian. Additionally, we show that any separable Bregman divergence that is convex in its second argument is a member of this set. This result provides a new set of Bregman divergence inequalities. In this sense, our Bregman analysis is complementary to the well-known -divergence inequality results [7, 8, 9, 10].

We further develop several applications for our results, including universal forecasting, universal data clustering, and universal sample complexity analysis for learning problems, in addition to establishing the universality of the information bottleneck principle. We emphasize that our universality results are derived in a rather general setting, and not restricted to a specific problem. As such, they may find a wide range of additional applications.

The remainder of the paper is organized as follows. Section II summarizes related work on loss function analysis, universality and divergence inequalities. Section III provides the needed notation, terminology, and definitions. Section IV contains the main results for binary alphabets, and their generalization to arbitrary finite alphabets is developed in Section V. Additional numerical analysis and experimental validation is provided in Section VI, and the implications of our results in three distinct applications is described in Section VII. Finally, Section VIII contains some concluding remarks.

II Related Work

The Bernoulli log-likelihood loss function plays a fundamental role in information theory, machine learning, statistics and many other disciplines. Its unique properties and broad applications have been extensively studied over the years.

The Bernoulli log-likelihood loss function arises naturally in the context of parameter estimation. Consider a set of independent, identically distributed (i.i.d.) observations drawn from a distribution whose parameter is unknown. Then the maximum likelihood estimate of in - is

where

Intuitively, it selects the parameters values that make the data most probable. Equivalently, this estimate minimizes a loss that is the (negative, normalized, natural) logarithm of the likelihood function, viz.,

whose mean is

Hence, by minimizing this Bernoulli log-likelihood loss, termed the log-loss, over a set of parameters we maximize the likelihood of the given observations.

The log-loss also arises naturally in information theory. The self-information loss function defines the ideal codeword length for describing the realization [11]. In this sense, minimizing the log-loss corresponds to minimizing the amount of information that are necessary to convey the observed realizations. Further, the expected self-information is simply Shannon’s entropy which reflects the average uncertainty associated with sampling the random variable .

The logarithmic loss function is known to be “universal” from several information-theoretic points of view. In [12], Feder and Merhav consider the problem of universal sequential prediction, where a future observation is to be estimated from a given set of past observations. The notion of universality comes from the assumption that the underlaying distribution is unknown, or even nonexistent. In this case, it is shown that if there exists a universal predictor (with a uniformly rapidly decaying redundancy rates) that minimizes the logarithmic loss function, then there exist universal predictors for any other loss function.

More recently, No and Weissman [13] introduced log-loss universality results in the context of lossy compression. They show that for any fixed length lossy compression problem under an arbitrary distortion criterion, there is an equivalent lossy compression problem under a log-loss criterion where the optimum schemes coincide. This result implies that without loss of generality, one may restrict attention to the log-loss problem (under an appropriate reconstruction alphabet). In addition, [13] considers the successive refinement problem, showing that if the first decoder operates under log-loss, then any discrete memoryless source is successively refinable under an arbitrary distortion criterion for the second decoder.

It is important to emphasize that universality results of the type discussed above are largely limited to relatively narrowly-defined problems and specific optimization criteria. By contrast, our development is aimed at a broader notion of universality that is not restricted to a specific problem, and considers a broader range of criteria.

An additional information-theoretic justification for the wide use of the log-loss is introduced in [14]. This work focuses on statistical inference with side information, showing that for an alphabet size greater than two, the log-loss is the only loss function that benefits from side information and satisfies the data processing lemma. This result extends some well-known properties of the log-loss with respect to the data processing lemma, as later described.

Within decision theory, statistical learning and inference problems, the log-loss also plays further key role in the context of proper loss function, which produce estimates that are unbiased with respect to the true underlaying distribution. Proper loss functions have been extensively studied, compared, and suggested for a variety of tasks [3, 4, 15, 5, 6]. Among these, the log-loss is special: it is the only proper loss that is local [16, 17]. This means that the log-loss is the only proper loss function that assigns an estimate for the probability of the event that depends only on the outcome .

In turn, proper loss functions are closely related to Bregman divergences, with which there exists a one-to-one correspondence [4]. For the log-loss, the associated Bregman divergence is KL divergence, which is also an instance of an -divergence [18]. Significantly, for probability distributions, the KL divergence is the only divergence measure that is a member of both of these classes of divergences [19]. The Bregman divergences are the only divergences that satisfy a “mean-as-minimizer” property [20], while any divergence that satisfy the data processing inequality is necessarily an -divergence (or a unique (one-to-one) mapping thereof) [21]. As a consequence, any divergence that satisfies both of these important properties simultaneously is necessarily proportional to the KL divergence [22, Corollary 6]. Additional properties of KL divergence are also discussed in [22].

Finally, divergences inequalities have been studied extensively. The most celebrated example is the Pinsker inequality [23], which expresses that KL divergence upper bounds the squared total-variation distance. More recently, the detailed studies of Reid and Williamson [10], Harremoës and Vajda [9], Sason and Verdú [8], and Sason [7] have extended this result to a broader set of -divergences inequalities. Moreover, -divergence inequalities for non-probability measures appear in, e.g., by Stummer and Vajda [24]. In [25], Zhang demonstrated an important Bregman inequality in the context of statistical learning, showing that the KL divergence upper bounds the squared excess-risk associated with the 0-1 loss, and thus controls this traditionally important performance measure. Within this context, our work can be viewed as extending such Bregman inequalities and their analysis.

III Notation, Terminology and Definitions

Let be a Bernoulli random variable with parameter , which may be unknown. A loss function quantifies the discrepancy between a realization and its corresponding estimate . In this work we focus on probabilistic estimates whereby is an estimate of rather than itself; as such, is a “soft” decision.

A loss function for such estimation takes the form

| (1) |

with denoting the Kronecker (indicator) function, where is a loss function associated with the event , for . In turn, the corresponding expected loss is

| (2) |

where we note that depends only on and the estimate . An example is the log-loss, for which

| (3) |

Loss functions with additional properties are of particular interest. A loss function is proper (or, equivalently, Fisher-consistent or unbiased) if a minimizer of the expected loss is the true underlying distribution of the random variable we are to estimate; specifically,

| (4) |

A strictly proper loss function means that is the unique minimizer, i.e.,

| (5) |

A proper loss function is fair if

| (6) |

in which case there is no loss incurred for accurate prediction. Additionally, a proper loss function is regular if

| (7) |

Intuitively, (7) ensures that making mistakes on events that cannot happen do not incur a penalty.

The minimum of the expected loss for proper loss functions, which we denote using

is referred to as the generalized entropy function [4], Bayes risk [26] or Bayesian envelope [27]. As an example, the Shannon entropy associated with the log-loss (3) is

| (8) |

The regret is defined as the difference between the expected loss and its minimum, so for proper loss functions takes the form

| (9) |

Savage [28] shows that a loss function is proper and regular if and only if is concave and for every we have that

| (10) |

This property allows us to draw an immediate connection between regret and Bregman divergence. In particular, let be a continuously differentiable, strictly convex function over some interval . Then its associated Bregman divergence takes the form

| (11) |

for any . We focus on closed intervals, in which case the formal definition of at boundary points requires more care; the details are summarized in Appendix A, following [29].

In the special case using (10) in (9) and comparing the result to (11) we obtain

| (12) |

i.e., the regret of a proper loss function is uniquely associated with a Bregman divergence. As an important example, associated with the Shannon entropy (8) is the KL divergence

| (13) |

Of particular interest are loss functions that are convex, i.e., such that is convex. Such loss functions play a special role in learning theory and optimization [2, 26]. For example, suppose111The sequence notation is convenient in our exposition. and is a set of explanatory variables (features) and a (target) variable, respectively. Then given a set of i.i.d. samples of and , the empirical risk minimization (ERM) criterion seeks to minimize

where denotes a functional of the th sample of . This minimization is much easier to carry out when the loss function is convex, particularly when is large. In addition, the minimum of the expected loss for a given subject to constraints is typically much easier to characterize and compute when is convex.

Conveniently, convex proper loss functions correspond to Bregman divergences such that is convex [26]. This family of divergences are of special interest in many applications [30, 31], and have an important role in our results, as will become apparent.

Accordingly, our development emphasizes the following class of analytically convenient loss functions.

Definition 1

For convenience, we refer to loss functions that satisfy property P1.3 as smooth.

As further terminology, for a proper, smooth loss function with generalized entropy ,

| (14) |

is referred to as its weight function, which we note is nonnegative. As an example, that corresponding to the log-loss is

| (15) |

Using (14), we obtain, for example,

| (16) |

by differentiating (10), which emphasizes the one-to-one correspondence between and for such loss functions; see Appendix B for additional properties and characterizations.

Finally, representative examples of loss functions are provided in Table I, along with their generalized entropies, their associated Bregman divergences, and their weight functions.

| \addstackgap[1] Loss function | |||||||||

\addstackgap[1]

|

|

|

|

|

|||||

\addstackgap[1]

|

|

|

|

|

|||||

\addstackgap[1]

|

|

|

|

|

IV Universality Properties of the Logarithmic Loss Function

Our main result is as follows, a proof of which is provided in Appendix C.

Theorem 1

Given a loss function satisfying Definition 1 with corresponding generalized entropy function , then for every ,

| (17a) | |||

| where | |||

| (17b) | |||

is a positive normalization constant (that does not depend on or ).

Note that a further consequence of Theorem 1 expresses that KL divergence is a “dominating” Bregman divergence in the sense that given another Bregman divergence such that [cf. (17a)]

holds for any Bregman divergence for some , then the theorem asserts that there exists such that

In essence, the dominating Bregman divergences form an equivalence class, of which KL divergence is a member.

We emphasize the necessity of scaling constants in Theorem 1. Indeed, the class of loss functions satisfying Definition 1 is closed under (nonnegative) scaling, i.e., if (with a corresponding ) satisfies Definition 1, then so does —with a corresponding —for any . A typical approach to placing loss functions on a common scale is to define a universal scaling by setting, for instance,

as appears, e.g., in [2, 10]. Theorem 1 avoids imposing such a normalization, and instead absorbs such scaling into the constant to obtain the desired invariance. As an example, for the quadratic loss , so any suffices in this case, whence

| (18) |

The practical implications of Theorem 1 are quite immediate. Assume that the performance measure according to which a learning algorithm is to be measured is unknown a priori to the application (as is the case, e.g., in the weather forecasting example of Section I). In such cases, minimizing the log-loss provides an upper bound on any possible choice of measure that is associated with an “analytically convenient” loss function. As such, the log-loss is a universal choice for classification problems with respect to this class of measures.

More generally, as discussed in Section II, designing suitable loss functions is an active research field with many applications. Via Theorem 1, one obtains universality guarantees for any (current or future) loss function that is proper, convex, and smooth. We emphasize that this class of loss functions is quite rich. For instance, it is straightforward to verify that the loss functions satisfying Definition 1 form a convex set: any convex combination of such loss functions also satisfies Definition 1.

The local behavior of proper, convex, and smooth loss functions can be derived from Theorem 1. In particular, we have the following corollary.

Corollary 2

Given a loss function satisfying Definition 1, whose corresponding generalized entropy function is , we have, for every and some finite ,

| (19a) | |||

| where | |||

| (19b) | |||

denotes the Fisher information of a Bernoulli distributed random variable with parameter .

Proof:

Corollary 2 establishes that when is sufficiently close to , the divergence associated with the set of smooth, proper and convex binary loss functions is effectively upper bounded by the Fisher information that locally characterizes KL divergence. As such, we conclude that the rate of convergence of any to zero as is upper bounded by the rate of . This reveals that the price paid for the universality of the log-loss is its slower rate of convergence. Such behavior will be demonstrated empirically in Section VI.

V Extended Bregman Divergence Inequalities

To extend our result to arbitrary finite alphabets, we consider the corresponding broader class of Bregman divergences. In particular, for a continuously differentiable, strictly convex function be a over some convex set , its associated Bregman divergence takes the form

| (21) |

for any when is open, where is the gradient of at .

We focus on the set , and let . We emphasize that this is an extension beyond the unit simplex. Let

| (22) |

denote the Hessian matrix of . For example, the divergence associated with

| (23) |

is the generalized divergence

| (24) |

the corresponding Hessian for which is

which we note is a diagonal matrix whose th diagonal element is . In the special case wherein and are probability measures (i.e., restricted to the unit simplex), we have

which generalizes the definition in Table I.

We focus on the following class of Bregman divergences.

Definition 2

For some integer , a Bregman divergence generator is -admissible if it satisfies the following properties:

-

P2.1)

is a strictly convex function that is well-defined on its boundaries, in the sense of generalizing the requirements of Appendix A.

-

P2.2)

, i.e., exist and are continuous for .

Our first generalization is the following theorem, whose proof is provided in Appendix D.

Theorem 3

Given a positive integer , let satisfy Definition 2 for , and let and denote the associated Bregman divergence and Hessian matrix, respectively. If there exists a (finite) positive constant such that222We use to denote that a matrix is positive definite.

| (25a) | |||

| then for every , | |||

| (25b) | |||

We emphasize that, in contrast to Theorem 1, the inequality (25b) applies to any Bregman divergence satisfying Definition 2, and in particular does not require to be convex for any . However, at the same time, we stress that Theorem 3 is restricted to the class of divergences satisfying (25a).

As an example application, when333Here, and elsewhere as needed, we construe a sequence as a column vector.

| (26) |

with positive definite matrix parameter , the corresponding the Bregman divergence

is the well-known Mahalanobis distance, and and the associated Hessian is

For this divergence we have the following corollary, whose proof is provided in Appendix E.

Corollary 4

Our second generalization of Theorem 1 focuses on the class of separable Bregman divergences, a member of which takes the form

| (28a) | |||

| with | |||

| (28b) | |||

for , where denote a continuously differentiable, strictly convex function with additional constraints discussed analogous to those discussed in Appendix A, and via which (28a) is extended to .

Such divergences hold a special role in divergence analysis, as discussed in, e.g., [22, 32]. Note that in this case, the Bregman generator function takes the form

| (29) |

via which we obtain the Hessian as

As an example,

| (30) |

matches (23), and when used in (28b) yields

| (31) |

so that (28a) specializes to the generalized KL divergence (24).

Our main result is the following theorem, a proof of which is provided in Appendix F.

Theorem 5

Given a positive integer , let be a separable Bregman divergence satisfying Definition 2 for and for which is convex for every . Then for every ,

| (32a) | |||

| when satisfies | |||

| (32b) | |||

We remark that when is unbounded, Corollary 5 does not yield a useful bound. By contrast, Theorem 1 is guaranteed to produce a bound, since is always finite.

It is important to emphasize that while Theorem 1 restricts attention to divergences defined both over binary alphabets and only on the unit simplex—i.e., in the notation of this section,

by contrast the divergences in Theorem 5 are defined for any positive integer and, in addition, over the entire hypercube . As such, we emphasize that Theorem 1 is not a special case of Theorem 5. In particular, because (17a) must hold for a domain that extends beyond the unit simplex, the smallest for which it is satisfied when must generally be bigger than the smallest for which (17a) holds.444That said, if desired, via similar analysis, together with the use of Lagrange multipliers, one can obtain a version of Theorem 5 restricted to the unit simplex, for which smaller constants will generally be obtained.

As a simple application of Theorem 5, choosing generates the quadratic divergence

which is a special case of the Mahalanobis distance. In this case, since , Theorem 5 requires , yielding

| (33) |

Consistent with the preceding discussion, corresponding to (33), is larger than the corresponding in the bound (18).

Additionally, it is worth noting that (33) resembles the well-known Pinsker inequality [11], viz.,

| (34) |

where

| (35) |

is the total-variation distance (or Csiszár divergence [11]), which is not a Bregman divergence, but rather an -divergence. It is straightforward to verify that (34) is tighter than (33) when and are restricted to the unit simplex. Nevertheless, this simple example serves to illustrate that Theorem 3 and Theorem 5 may be viewed as Bregman divergences extensions to some well-known -divergence results, as discussed in Section II.

VI Numerical Analysis and Experiments

To complement the results of Section V, we use numerical analysis to examine the dependence of

on and , for some choices of such that Theorem 3 applies, and with chosen according to (25a).

To begin, we consider a random variable with , and restrict to lie in a subset of the unit simplex . For a given , with

| (36) |

and, in turn,

| (37) |

where is as given in (29), the minimum KL divergence upper bounds the minimum of any Bregman divergence according to

| (38) |

where to obtain the first inequality we have used Theorem 3 with satisfying (25a), and to obtain the second inequality we have used (36).

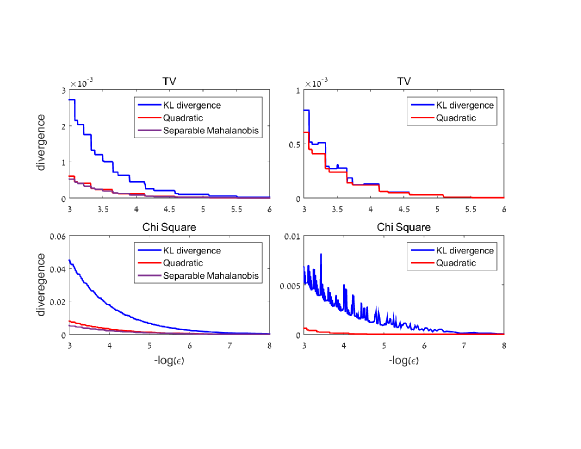

In the first experiment, we set

for some and , i.e., we constrain to lie in a hyperplane restricted to the unit simplex . More specifically, we choose , , and to illustrate our results. The results of our experiment, which compares the minima in (38) as a function of , are depicted in Fig. 1. The top (blue) curve is (with a minor abuse of notation) , and the progressively lower (red, purple, and black) curves are (with a similar abuse of notation) with corresponding to the quadratic divergence, the separable Mahalanobis distance with parameters , and the nonseparable Mahalanobis distance with parameters , respectively. The specific values of these parameters are

| (39) |

Note that since for our choice of , all the minimum divergences are zero at , and thus for all Bregman generators . However, when , the optimizing must differ from , and Fig. 1 quantifies these differences as a function of the bias . Consistent with the analysis of Section V, KL divergence upper bounds normalized measures of all these differences.

In the second experiment we show that the bounds (38) hold for a broader range of problems. To model a statistical, computational, or even algorithmic constraint that prevents from converging to some given , we impose that where

| (40) |

for some and . In Fig. 2, we compare the terms in (38) for different choices for , and two different (non-Bregman) examples of in (40). In particular, the upper plots corresponds to choosing for in (40) the total-variation distance as defined in (35). For constrast, the lower plots corresponds choosing for in (40) the (Neyman) chi-square divergence, i.e.,

| (41) |

The plots on the left compare with (37) to with (36), for corresponding to the quadratic and separable Mahalanobis distances (where the latter has parameters as specified in (39)). Consistent with (38), upper bounds for both the quadratic divergence and the separable Mahalanobis distance. Moreover, we see that larger values of result in a greater bias, as we would expect.

The plots on the right compare with (37) to the middle term in (38), i.e., , for corresponding to the quadratic distance. The results demonstrate that can, indeed, be an effective approximation to with respect to minimizing .

In the third experiment we demonstrate the application of our bounds to weather forecasting as discussed in Section I. Recall that weather forecasters typically assign probabilistic estimates to future meteorological events. The estimates are designed to minimize a performance measure, according to which the weather forecaster is evaluated. However, weather estimates serve a wide audience, within which different recipients may be interested in different and often conflicting measures. For example, by minimizing the quadratic loss, a forecaster may reasonably assign zero probability of occurrence to very rare events, but this would result in an unbounded logarithmic loss.

To demonstrate the value of using log-loss minimization to control a large set of commonly used performance measures, we analyze weather data collected by the Australian Bureau of Meteorology [33]. This publicly available dataset contains the observed weather and its corresponding forecasts in multiple weather stations in Australia. In our experiment we focus on the predicted chances of rain (where a rainfall is defined as over 2mm of rain) compared with the true event of rain. Our dataset contains pairs of forecasts and corresponding weather observations that were collected during the period Apr. 28–30, 2016. For reference, in this period, a fraction

of the observations correspond to an event of rain. We evaluate the accuracy of the Australian weather forecasts by the three commonly used proper loss measures: logarithmic, quadratic, and 0-1 losses, with the latter defined via

and where we choose as its parameter , following the Bureau’s guidelines. The first row of Table II summarizes our results.

| \addstackgap[1] Weather Forecaster | 0-1 loss | Quadratic loss | Logarithmic loss | ||

\addstackgap[1]

|

|||||

\addstackgap[1]

|

Note that the unbounded logarithmic loss is a consequence of the fact that there are several instances in which the forecaster predicted zero chance of rain but it ultimately rained. In correspondence with them, Australia’s National Meteorological Service confirmed that their forecasts are typically internally evaluated by both a quadratic loss and a 0-1 loss with parameter . In addition, they perform more sophisticated evaluation analysis which is not in the scope of this work.

Next, we consider a method for revising the existing forecasts based on our log-loss universality results. Since the available forecasts are generated by a prediction algorithm whose features unavailable to us, our revised forecasts can only be based on the existing forecasts. Accordingly, we make use of a simple logistic regression in which the target is the observed data and the single feature is the corresponding original forecast. Specifically, given an original weather forecast of , we generate the following updated weather forecast according to

| (42) |

where the regression parameters and are fit to training data according to

To avoid over-fitting, the training data was from Jan. 2016, and thus different from the test data . The accuracy of the resulting updated forecasts are presented in the second row of Table II.

Note that the updated forecasts now incur a bounded log-loss, and that this robustness is achieved without significantly affecting accuracy with respect to the other loss functions. Evidently, even such simple post-processing improves log-loss performance while controlling a large set of alternative measures, consistent with the results of Theorem 1 (and of those in [25] for the 0-1 loss).

VII Example Applications

The Bernoulli log-likelihood loss function is widely used in a variety of scientific fields. Several key examples, in addition to those discussed above, include logistic regression in statistical analysis [34], the info-max criterion in machine learning [35], independent component analysis in signal processing [36],[37], splitting criteria in classification trees [38], DNA sequence alignment [39], and many others. In this section we demonstrate the potential applicability of our universality results in the context of three key examples.

VII-A Universal Clustering with Bregman Divergences

Data clustering is an unsupervised learning procedure that has been extensively studied across a variety of disciplines over many decades. Most clustering methods assign each data sample to one of a pre-specified number of partitions, with each partition defined by a cluster representative, and where the quality of clustering is measured by the proximity of samples to their assigned cluster representatives, as measured by a pre-defined distance function.

Several popular algorithms for data clustering have been developed over the years. This includes the well-known -means algorithm [40] which minimizes the quadratic distance. Another widely used example is the Linde-Buzo-Gray (LBG) algorithm [41, 42] based on the Itakura-Saito distance [43]. More recently, Dhillion et al. [44] proposed an information-theoretic approach to clustering probability distributions based on KL divergence.

All of these clustering methods are based on an Expectation-Maximization (EM) framework for minimizing the aggregate distance, and share the same optimality property: the centroid (representative) of each cluster is the mean of the data points that are assigned to it. Moreover, all of these algorithms use a Bregman divergence as their measure of distance, as do some promising emerging methods. For example, a new class of clustering methods has been shown to offer significant improvement in various domains by utilizing so-called total Bregman divergence, a rotation-invariant version of classical Bregman divergence [45, 46, 47, 48, 49].

The connection between clustering and the Bregman divergence is developed in Banerjee et al. [20]. In particular, a key result is that a random variable satisfies

| (43) |

if and only if is a Bregman divergence. It follows that any clustering algorithm that satisfies the “mean-as-minimizer” property centroid property minimizes a Bregman divergence, and thus we need look no further than among the Bregman divergences in selecting a candidate distance measure for EM-based data clustering.

Even with this restriction, it is frequently not clear how to choose an appropriate Bregman divergence for a given clustering task. Banerjee et al. [20] show that there is a unique correspondence between exponential families and Bregman divergences. As such, if the data are from an exponential family, with different parameters for different clusters, then the natural distance for clustering is the corresponding Bregman divergence. As an example, for Gaussian distributions with differing means, the quadratic distance used by -means is the natural distance. However, in practice, information about the generative model for the data is rarely known.

As an alternative, our results suggest a “universal” approach to clustering that provides performance guarantees with respect to any Bregman divergence that might turn out to be relevant. Specifically, suppose we are given samples to be partitioned into clusters with corresponding representatives . Then the optimum solution for measure is

where555When a sample is equidistant to multiple representatives, we pick one arbitrarily.

Similarly, for measure , we use the (slightly simpler) notation , and .

Using Theorem 3 (for and satisfying the conditions of the theorem), we can then bound performance with respect to according to [cf. (38)]

| (44) |

where .

Via (44), we conclude that by applying a clustering algorithm that minimizes KL divergence, we provide performance guarantees for any (reasonable) choice of clustering method. As such, our analysis provides further justification for the popularity of the KL divergence in distributional clustering [50] and specifically in the context of natural language processing and text classification [51, 52, 53].

VII-B The Universality of the Information Bottleneck

The information bottleneck [54] is a conceptual machine learning framework for extracting an informative but compact representation of an explanatory variable666Note that can equivalently represent a collection of variables. with respect to inferences about a target , generalizing the notion of a minimal sufficient statistic from classical parametric statistics. Given the joint distribution , the method selects the compressed representation for that preserves the maximum amount of information about . As such, effectively regulates the compression of , so as to maintain a level of explanatory relevance with respect to . Specifically, with denoting the compressed representation, the information bottleneck problem is

| (45) |

where form a Markov chain, and thus the minimization is over all possible (generally randomized) mappings of to . Here, is a constant parameter that sets the level of compression to be attained. As is varied, the tradeoff between (corresponding to the representation complexity) and (corresponding to the predictive power) is a continuous, concave function.

Information bottleneck analysis is a powerful tool in a variety of machine learning domains and related areas; see, e.g., [55, 56, 57, 58, 59]. It is also applicable in a variety of other fields, including neuroscience [60] and optimal control [61]. Recently, there have been demonstrations of its ability to analyze the performance of deep neural networks [62, 63, 64].

It is useful to recognize that the information bottleneck problem (45) is an instance of a remote-source rate-distortion problem [11]. In particular, let be a remote source that is unavailable to the encoder, and let be a random variable that is dependent of through a (known) mapping , which is available to the encoder. The remote source coding problem is to achieve the highest possible compression rate for given a prescribed maximum tolerable reconstruction error of from the compressed representation . In this setting, the reconstruction error is measured by a predefined distortion (loss) function, where the choice of log-loss leads to the standard information bottleneck problem [65].

While the choice of log-loss is typically justified by several properties of KL divergence [22], the results of this paper can be applied to show that its use provides valuable universality guarantees for the remote source coding problem.

To develop this view, first note that

which follows from straightforward algebra. In this form, we recognize as the full predictive model and as the compressed predictive one. Since is given, we maximize (as (45) dictates) by minimizing . In the more general souce coding problem, we instead seek to minimize

| (46) |

with chosen as desired.

VII-C Universal PAC-Bayes Bounds

Probably approximately correct (PAC)-Bayes theory blends Bayesian and frequentist approaches to the analysis of machine learning. The PAC-Bayes formulation assumes a probability distribution on events occurring in nature and a prior on the class of candidate hypotheses (estimators) that express a learner’s preference for some hypotheses over others. PAC-Bayes generalization bounds [66, 67, 68] govern the performance (loss) when stochastically selecting hypotheses from a posterior distribution. We begin this section with a summary of those aspects of PAC-Bayes theory needed for our development.

Let be an explanatory variable777While the development generalizes naturally to collections of explanatory variables, to simplify the exposition we focus on a single such variable. (feature) and an independent variable (target). Assume that and follow a joint probability distribution . Let be a class of hypotheses (estimators) for , where each estimator is some functional of . As an example, in logistic regression, each hypothesis is an estimator of the form (42) for some constants and .

Next, we view as a realization of a random variable that is independent of and and governed by (prior) distribution on , and let be the loss between the realization and the estimate , for a given estimator and loss function , such that for some constant and all , , and . We select based on i.i.d. training samples

from so as to minimize the generalization loss

In particular, the selection is based on the training loss

An example of a standard generalization bound of this type is the following, in which is assumed to be countable.

Theorem 6 (PAC bound [68])

Given training data from , with probability at least ,

for all and all .

In the PAC-Bayes extensions of Theorem 6, we allow to be continuous (uncountable). Moreover, in addition to we let another distribution over , and define

| (48) |

and

| (49) |

where

| (50) |

While tighter PAC-Bayes bounds have been developed—see, e.g., [69, 70, 67, 71, 72]—the original is the following, which can be derived as a corollary of results by Catoni [69].

Theorem 7 (PAC-Bayes bound [66])

Given training data from , with probability at least ,

for all on and all .

Evidently, the bounds in both Theorem 6 and Theorem 7 are specific to the choice of loss function . For scenarios where such a choice is not clear, a “universal” PAC-Bayes bound based on log-loss, which we now develop, is useful.

A complication in the development is PAC-Bayes bounds apply only to bounded loss functions as they focus on worst-case performance [68], and thus log-loss is inadmissible. Different approaches have been introduced to overcome this limitation. In [68], McAllester suggests modifying an unbounded loss by applying an “outlier threshold” to replace with , which is always bounded.. This approach introduces analytical difficulties as the new loss is typically neither continuous nor convex.

An alternative approach, which we follow and whose use is more widespread, assumes that the underlying distribution for the data is bounded away from zero [73, 74, 75, 76]. Equivalently, the model is not deterministic (singular), and the hypothesis class is chosen accordingly. Specifically, for some we have for every , , and .

Via the latter methodology, the loss function is bounded on the domain of interest, and we obtain the following universal PAC-Bayes inequality, a proof of which is provided in Appendix G.

Theorem 8

Let be a loss function that satisfies Definition 1, and its corresponding generalized entropy function. If for some and every , , and , then with probability at least ,

| (51) |

for all on and all . In (51), ,

is a normalization constant that depends only on , and is of the form (49), where is specialized to [cf. (50)]

with as defined in (3).

Theorem 8 establishes that even when we do not know a priori the loss function with respect to which are to be measured, it is often possible to bound the generalization loss. Such universal generalization bounds have potentially wide range of applications.

VIII Discussion and Conclusions

In this work we introduce a fundamental inequality for two-class classification problems. We show that the KL divergence, associated with the Bernoulli log-likelihood loss, upper bounds any divergence measure that corresponds to a smooth, proper and convex binary loss function. This property makes the log-loss a universal choice, in the sense that it controls any “analytically convenient” alternative one may be interested in. This result has implications in a wide range of applications. There are many examples beyond those we have explicitly described. For instance, in binary classification trees [38], the split criterion in each node is typically chosen between the Gini impurity (which corresponds to quadratic loss) and information-gain (which corresponds to log-loss). The best choice for a splitting mechanism is a long standing open question with many statistical and computational implications; see, e.g., [77]. Our results indicate that by minimizing the information-gain we implicitly obtain guarantees for the Gini impurity (but not vice-versa). This provides a new and potentially useful perspective on the question.

Finally, by viewing our bounds from a Bregman divergence perspective, we extend the well-studied -divergence inequalities by providing complementary Bregman inequalities. Collectively, these results contribute to our growing understanding understanding of the fundamental role that KL divergence plays in these two important classes of divergences.

Appendix A Bregman Divergence Characterization

Following [29], a Bregman divergence generator is a continuous, strictly convex (finite) function on some appropriately chosen open interval such that covers (at least) the union of the ranges of and , as appears in (11)—e.g., in the binary classification problem of Section IV. Due to condition P2.2, we further restrict our attention to continuously differentiable .

We continuously extend to via

which can be infinite only for . Moreover, we continuously extend the derivative to via

Using these extensions, for , we let

where is following lower semi-continuous nonnegative function. First,

Next, for ,

and

where we note the limits exist but may be infinite. Finally,

Appendix B Weight Functions of Smooth Proper Losses

As a complementary view of weight functions, we note that when a smooth loss function is proper, its expected loss satisfies

whence

| (52) |

where the last equality in (52) is obtained by matching terms in the forms (2) and (10), and using (14). Shuford et al. [78] establish that the converse is also true: a smooth loss function is proper only if (52) holds for some nonnegative that satisfies , for all .

Appendix C Proof of Theorem 1

First, due to the convexity of the loss (with respect to ), we have

| (53) |

for every fixed and . Specializing (53) to the cases and then yields

| (54) |

for all . In turn, (54) implies

i.e.,

| (55a) | |||

| (55b) | |||

Similar results appear in, e.g., [26, Theorem 29]. We emphasize that we have not assumed that is integrable on , so as to accommodate loss functions such that and/or are unbounded at and , respectively[2].

Next, we show there exists a constant such that

| (56) |

is nonnegative for all . For any , since it suffices to show that has a minimum at for a suitable choice of . From

| (57) |

we see that is a unique stationary point. Moreover, this stationary point is a minimum when

| (58) |

for all .

Now for every , we have

| (59a) | |||

| where the first inequality follows since , and the last inequality follows from (55a). Similarly, for we have | |||

| (59b) | |||

where the first inequality follows since , and the last inequality follows from (55b). Hence, choosing

| (60) |

ensures the right-hand side of (the relevant variant of) (59b) is positive for all , and thus (58) holds for all . Hence, we conclude that for all .

Next consider the case and . If choose according to (60), then (58) holds for all . In this case, (57) must be strictly positive for all when , so is monotonically increasing, and thus its minimum is attained at . Likewise (57) must be strictly negative for all when , so is monotonically decreasing, and thus its minimum is attained at . In turn, since , it follows that also holds for and .

It remains to consider the case and . When we have since . Finally, when we have is unbounded, so (17a) holds trivially. ∎

Appendix D Proof of Theorem 3

It suffices to show that

is nonnegative for all . Using (21) in the form

| (61) |

we have

| (62) |

and, in turn,

| (63) |

where denotes the th element of its matrix argument. Hence, it follows that is strictly convex if there exists a constant such that (25a) is satisfied. Moreover, from (62) we have that is a stationary point, so provided (25a) is statisfied, this stationary point is a minimum. Finally, since , it follows that for all . ∎

Appendix E Proof of Corollary 4

First, let

with

denoting its eigenvalues, and note that according to (25a) it suffices to show that when satisfies (27), we have , for which the condition is equivalent.

Next, let , whose eigenvalues we denote via

and note that for every ,

Hence,

where the equalities follow from the Rayleigh quotient theorem [79, Theorem 4.2.2].

Finally, since888We use to denote the identity matrix. , so

Accordingly, setting yields for all . ∎

Appendix F Proof of Theorem 5

First, note that

| (64a) | ||||

| (64b) | ||||

Since is convex for every , (64b) is nonnegative for every and . Choosing we obtain

Hence, we have

whence

| (65) |

Next, following an approach similar to that in the proof of Theorem 1, we define

| (66a) | |||

| with | |||

| (66b) | |||

and show that when is chosen as prescribed, (66a) is nonnegative for . Note that it is sufficient to show that for such , (66b) is nonnegative for every .

Accordingly, we fix and analyze with respect to . Via (64) (including its specialization to (30)) we obtain

| (67a) | ||||

| (67b) | ||||

First, consider the case . Since , if then a global minimum of must occur at . Proceeding, from (67a), we see that the unique stationary point is . Moreover, this stationary point is a minimum when

is positive, from which we obtain the requirement

| (68) |

Choosing we obtain

where the last inequality follows from (65). Hence, for .

Next, consider the case . Again, with the choice , (68) holds for all , and thus (67a) is positive for when , so is an increasing function. Since , then, we conclude . Likewise, thus (67a) is negative for when , so is a decreasing function. Since , then, we conclude . Hence, for and .

It remains only to consider the case , for any . When , we have . When , (31) is unbounded so . For the case , straightforward calculation yields

| (69) |

But

which matches the left-hand side of (68), and thus is positive for all when , in which case is an increasing function. As a result, (69) is negative for , and thus is a decreasing function. Since, in addition, , we conclude . Hence, for and . ∎

Appendix G Proof of Theorem 8

The following lemma will be useful.

Lemma 9

Proof:

With

we have

| (71a) | ||||

| (71b) | ||||

| where to obtain the second equality in (71b) we have used (14). | ||||

In turn, using (59b) from the proof of Theorem 1, we likewise conclude that choosing according to (70) ensures that

in which case is strictly convex. In addition, we have

where the first and second qualities follow from (10) and (2), respectively, and thus using (7) we have for . Since for as a special case, it follows that for . Hence, . ∎

Proceeding to the proof of Theorem 8, from (12) with (9) we obtain , which when used in conjunction with (17a) of Theorem 1 yields

| (72) | ||||

| (73) |

where in (72)

Next, we have

| (74) | ||||

| (75) | ||||

| (76) |

where to obtain (75) we have used an instance of (73) to bound the inner expectation in (74).

Moreover, since we have

| (77) |

with probability one.

References

- [1] A. Painsky and G. Wornell, “On the universality of the logistic loss function,” in Proc. Int. Symp. Inform. Theory (ISIT), Vail, Colorado, June 2018, pp. 936–940.

- [2] A. Buja, W. Stuetzle, and Y. Shen, “Loss functions for binary class probability estimation and classification: Structure and applications,” Statistics Dept., Wharton School, University of Pennsylvania, Philadelphia, PA, Tech. Rep., Nov. 2005. [Online]. Available: https://faculty.wharton.upenn.edu/wp-content/uploads/2012/04/Paper-proper-scoring.pdf

- [3] R. L. Winkler, J. Munoz, J. L. Cervera, J. M. Bernardo, G. Blattenberger, J. B. Kadane, D. V. Lindley, A. H. Murphy, R. M. Oliver, and D. Ríos-Insua, “Scoring rules and the evaluation of probabilities,” Test, vol. 5, no. 1, pp. 1–60, June 1996.

- [4] T. Gneiting and A. E. Raftery, “Strictly proper scoring rules, prediction, and estimation,” J. Am. Stat. Assoc., vol. 102, no. 477, pp. 359–378, Mar. 2007.

- [5] E. C. Merkle and M. Steyvers, “Choosing a strictly proper scoring rule,” Decision Analysis, vol. 10, no. 4, pp. 292–304, Dec. 2013.

- [6] A. P. Dawid and M. Musio, “Theory and applications of proper scoring rules,” METRON, vol. 72, no. 2, pp. 169–183, Aug. 2014.

- [7] I. Sason, “On -divergences: Integral representations, local behavior, and inequalities,” Entropy, vol. 20, no. 5, 383, 2018.

- [8] I. Sason and S. Verdú, “-divergence inequalities,” IEEE Trans. Inform. Theory, vol. 62, no. 11, pp. 5973–6006, Nov. 2016.

- [9] P. Harremoës and I. Vajda, “On pairs of -divergences and their joint range,” IEEE Trans. Inform. Theory, vol. 57, no. 6, pp. 3230–3235, Jun. 2011.

- [10] M. D. Reid and R. C. Williamson, “Information, divergence and risk for binary experiments,” J. Mach. Learn. Res., vol. 12, no. Mar., pp. 731–817, 2011.

- [11] T. M. Cover and J. A. Thomas, Elements of Information Theory, 2nd ed. New York, NY: John Wiley & Sons, 2006.

- [12] N. Merhav and M. Feder, “Universal prediction,” IEEE Trans. Inform. Theory, vol. 44, no. 6, pp. 2124–2147, June 1998.

- [13] A. No and T. Weissman, “Universality of logarithmic loss in lossy compression,” in Proc. Int. Symp. Inform. Theory (ISIT). Hong Kong, China: IEEE, June 2015, pp. 2166–2170.

- [14] J. Jiao, T. A. Courtade, K. Venkat, and T. Weissman, “Justification of logarithmic loss via the benefit of side information,” IEEE Trans. Inform. Theory, vol. 61, no. 10, pp. 5357–5365, 2015.

- [15] J. E. Bickel, “Some comparisons among quadratic, spherical, and logarithmic scoring rules,” Decision Analysis, vol. 4, no. 2, pp. 49–65, June 2007.

- [16] J. M. Bernardo and A. F. M. Smith, Bayesian Theory. New York, NY: Wiley, 2000.

- [17] M. Parry, A. P. Dawid, and S. Lauritzen, “Proper local scoring rules,” Ann. Stat., vol. 40, no. 1, pp. 561–592, 2012.

- [18] I. Csiszár and P. C. Shields, “Information theory and statistics: A tutorial,” Foundations and Trends in Communications and Information Theory, vol. 1, no. 4, pp. 417–528, 2004.

- [19] I. Csiszár, “Generalized projections for non-negative functions,” Acta Math. Hungar., vol. 68, no. 1–2, pp. 161–185, 1995.

- [20] A. Banerjee, S. Merugu, I. S. Dhillon, and J. Ghosh, “Clustering with Bregman divergences,” J. Mach. Learn. Res., vol. 6, pp. 1705–1749, Oct. 2005.

- [21] M. Zakai and J. Ziv, “A generalization of the rate-distortion theory and applications,” in Information Theory New Trends and Open Problems, G. Longo, Ed. Vienna, Austria: Springer, 1975, pp. 87–123.

- [22] P. Harremoës and N. Tishby, “The information bottleneck revisited or how to choose a good distortion measure,” in Proc. Int. Symp. Inform. Theory (ISIT). Nice, France: IEEE, June 2007, pp. 566–570.

- [23] I. Csiszár, “Information-type measures of difference of probability distributions and indirect observations,” Studia Sci. Math. Hungar., vol. 2, no. Jan., pp. 299–318, 1967.

- [24] W. Stummer and I. Vajda, “On divergences of finite measures and their applicability in statistics and information theory,” Statistics, vol. 44, no. 2, pp. 169–187, 2010.

- [25] T. Zhang, “Statistical behavior and consistency of classification methods based on convex risk minimization,” Ann. Stat., vol. 32, no. 1, pp. 56–134, 2004.

- [26] M. D. Reid and R. C. Williamson, “Composite binary losses,” J. Mach. Learn. Res., vol. 11, no. Sep., pp. 2387–2422, 2010.

- [27] N. Merhav and M. Feder, “Universal schemes for sequential decision from individual data sequences,” IEEE Trans. Inform. Theory, vol. 39, no. 4, pp. 1280–1292, Apr. 1993.

- [28] L. J. Savage, “Elicitation of personal probabilities and expectations,” J. Am. Stat. Assoc., vol. 66, no. 336, pp. 783–801, Dec. 1971.

- [29] M. Broniatowski and W. Stummer, “Some universal insights on divergences for statistics, machine learning and artificial intelligence,” in Geometric Structures of Information, F. Nielsen, Ed. Cham, Switzerland: Springer International Publishing, 2019, pp. 149–211.

- [30] H. H. Bauschke and J. M. Borwein, “Joint and separate convexity of the Bregman distance,” in Inherently Parallel Algorithms in Feasibility and Optimization and their Applications, D. Butnariu, Y. Censor, and S. Reich, Eds. Elsevier, 2001, vol. 8, pp. 23–36.

- [31] C. L. Byrne, Iterative Optimization in Inverse Problems. Boca Raton, FL: CRC Press, 2014.

- [32] J. Jiao, T. A. Courtade, A. No, K. Venkat, and T. Weissman, “Information measures: the curious case of the binary alphabet,” IEEE Trans. Inform. Theory, vol. 60, no. 12, pp. 7616–7626, Dec. 2014.

- [33] Australian Bureau of Meteorology, “Australian data archive for meteorology,” http://www.bom.gov.au/climate/data/, retrieved 2017.

- [34] J. Friedman, T. Hastie, and R. Tibshirani, The Elements of Statistical Learning, 2nd ed. New York, NY: Springer-Verlag, 2009.

- [35] R. Linsker, “Self-organization in a perceptual network,” Computer, vol. 21, no. 3, pp. 105–117, Mar. 1988.

- [36] A. Painsky, S. Rosset, and M. Feder, “Generalized independent component analysis over finite alphabets,” IEEE Trans. Inform. Theory, vol. 62, no. 2, pp. 1038–1053, Feb. 2016.

- [37] ——, “Linear independent component analysis over finite fields: Algorithms and bounds,” IEEE Trans. Signal Processing, vol. 66, no. 22, Nov. 15, 2018.

- [38] L. Breiman, J. Friedman, C. J. Stone, and R. A. Olshen, Classification and Regression Trees. Boca Raton, FL: CRC Press, 1984.

- [39] J. Keith and D. P. Kroese, “Sequence alignment by rare event simulation,” in Proc. Winter Simulation Conf. (WSC), vol. 1. IEEE, 2002, pp. 320–327.

- [40] J. MacQueen, “Some methods for classification and analysis of multivariate observations,” in Proc. Berkeley Symp. Math. Stat., Prob., vol. 1, 1967, pp. 281–297.

- [41] Y. Linde, A. Buzo, and R. Gray, “An algorithm for vector quantizer design,” IEEE Trans. Commun., vol. 28, no. 1, pp. 84–95, Jan. 1980.

- [42] A. Buzo, A. Gray, R. Gray, and J. Markel, “Speech coding based upon vector quantization,” IEEE Trans. Acoustics, Speech, and Signal Processing, vol. 28, no. 5, pp. 562–574, 1980.

- [43] F. Itakura and S. Saito, “Analysis synthesis telephony based on the maximum likelihood method,” in Proc. Int. Congress Acoustics, Aug. 1968, pp. C17–C20.

- [44] I. S. Dhillon, S. Mallela, and R. Kumar, “A divisive information-theoretic feature clustering algorithm for text classification,” J. Mach. Learn. Res., vol. 3, no. Mar., pp. 1265–1287, 2003.

- [45] M. Liu, Total Bregman divergence, a robust divergence measure, and its applications. University of Florida, 2011.

- [46] M. Liu, B. C. Vemuri, S.-I. Amari, and F. Nielsen, “Total Bregman divergence and its applications to shape retrieval,” in Proc. Conf. Comp. Vision, Patt. Recog. (CVPR), San Francisco, CA, Jun. 2010, pp. 3463–3468.

- [47] B. C. Vemuri, M. Liu, S.-i. Amari, and F. Nielsen, “Total Bregman divergence and its applications to DTI analysis,” IEEE Trans. Med. Imag., vol. 30, no. 2, pp. 475–483, Feb. 2010.

- [48] M. Liu, B. C. Vemuri, S.-i. Amari, and F. Nielsen, “Shape retrieval using hierarchical total Bregman soft clustering,” IEEE Trans. Pattern Anal., Mach. Intell., vol. 34, no. 12, pp. 2407–2419, Dec. 2012.

- [49] R. Nock, F. Nielsen, and S.-i. Amari, “On conformal divergences and their population minimizers,” IEEE Trans. Inform. Theory, vol. 62, no. 1, pp. 527–538, Jan. 2015.

- [50] F. Pereira, N. Tishby, and L. Lee, “Distributional clustering of English words,” in Proc. Meet. Assoc. Comput. Ling. Columbus, OH: Association for Computational Linguistics, June 1993, pp. 183–190.

- [51] L. D. Baker and A. K. McCallum, “Distributional clustering of words for text classification,” in Proc. Int. Conf. Res., Dev. Inform. Retrieval (SIGIR), Melbourne, Australia, Aug. 1998, pp. 96–103.

- [52] A. Clark, “Unsupervised induction of stochastic context-free grammars using distributional clustering,” in Proc. Workshop Comput. Nat. Lang. Learn. (ConLL), vol. 7, Toulouse, France, July 2001.

- [53] R. Bekkerman, R. El-Yaniv, N. Tishby, and Y. Winter, “On feature distributional clustering for text categorization,” in Proc. Int. Conf. Res., Dev. Inform. Retrieval (SIGIR), New Orleans, LA, 2001, pp. 146–153.

- [54] N. Tishby, F. C. Pereira, and W. Bialek, “The information bottleneck method,” in Proc. Allerton Conf. Commun., Contr., Computing, Monticello, IL, Sep. 1999, pp. 368–377.

- [55] N. Slonim and N. Tishby, “Document clustering using word clusters via the information bottleneck method,” in Proc. Int. Conf. Res., Dev. Inform. Retrieval (SIGIR), Athens, Greece, July 2000, pp. 208–215.

- [56] N. Friedman, O. Mosenzon, N. Slonim, and N. Tishby, “Multivariate information bottleneck,” in Proc. Conf. Uncertainty in Artificial Intelligence (UAI), San Francisco, CA, Aug. 2001, pp. 152–161.

- [57] J. Sinkkonen and S. Kaski, “Clustering based on conditional distributions in an auxiliary space,” Neural Comput., vol. 14, no. 1, pp. 217–239, 2002.

- [58] N. Slonim, G. S. Atwal, G. Tkačik, and W. Bialek, “Information-based clustering,” Proc. Nat. Acad. Sci. (PNAS), vol. 102, no. 51, pp. 18 297–18 302, 2005.

- [59] R. M. Hecht, E. Noor, and N. Tishby, “Speaker recognition by Gaussian information bottleneck,” in Proc. Interspeech, Brighton, UK, Sep. 2009, pp. 1567–1570.

- [60] E. Schneidman, N. Slonim, N. Tishby, R. de Ruyter van Steveninck, and W. Bialek, “Analyzing neural codes using the information bottleneck method,” Unpublished manuscript, 2001. [Online]. Available: ftp://ftp.cis.upenn.edu/pub/cse140/public_html/2002/schneidman.pdf

- [61] N. Tishby and D. Polani, “Information theory of decisions and actions,” in Perception-Action Cycle: Models, Architectures, and Hardware, V. Cutsuridis, A. Hussain, and J. G. Taylor, Eds. New York, NY: Springer, 2011, pp. 601–636.

- [62] N. Tishby and N. Zaslavsky, “Deep learning and the information bottleneck principle,” in Proc. Inform. Theory Workshop (ITW), Apr. 2015.

- [63] R. Shwartz-Ziv and N. Tishby, “Opening the black box of deep neural networks via information,” CoRR, vol. abs/1703.00810, 2017. [Online]. Available: http://arxiv.org/abs/1703.00810

- [64] Z. Goldfeld, E. Van Den Berg, K. Greenewald, I. Melnyk, N. Nguyen, B. Kingsbury, and Y. Polyanskiy, “Estimating information flow in deep neural networks,” in Proc. Int. Conf. Mach. Learn. (ICML), vol. 97, Long Beach, CA, June 2019, pp. 2299–2308.

- [65] Y. Y. Shkel and S. Verdú, “A single-shot approach to lossy source coding under logarithmic loss,” IEEE Trans. Inform. Theory, vol. 64, no. 1, pp. 129–147, Jan. 2017.

- [66] D. A. McAllester, “PAC-Bayesian model averaging,” in Proc. Conf. Comput. Learn. Theory (COLT), Santa Cruz, CA, July 1999, pp. 164–170.

- [67] J. Langford, “Tutorial on practical prediction theory for classification,” J. Mach. Learn. Res., vol. 6, no. Mar., pp. 273–306, 2005.

- [68] D. A. McAllester, “A PAC-Bayesian tutorial with a dropout bound,” CoRR, vol. abs/1307.2118, 2013. [Online]. Available: http://arxiv.org/abs/1307.2118

- [69] O. Catoni, PAC-Bayesian Supervised Classification: The Thermodynamics of Statistical Learning, ser. Lecture Notes–Monograph. Beachwood, OH: Institute of Mathematical Statistics, 2007, vol. 56.

- [70] P. Germain, A. Lacasse, F. Laviolette, and M. Marchand, “PAC-Bayesian learning of linear classifiers,” in Proc. Int. Conf. Mach. Learn. (ICML), Montréal, Canada, 2009, pp. 353–360.

- [71] A. Maurer, “A note on the PAC Bayesian theorem,” CoRR, vol. cs.LG/0411099, 2004. [Online]. Available: http://arxiv.org/abs/cs.LG/0411099

- [72] M. Seeger, “PAC-Bayesian generalisation error bounds for Gaussian process classification,” J. Mach. Learn. Res., vol. 3, no. Oct., pp. 233–269, 2002.

- [73] D. Haussler, “Decision theoretic generalizations of the PAC model for neural net and other learning applications,” Inf. Comput., vol. 100, no. 1, pp. 78–150, Sep. 1992.

- [74] S. Bharadwaj and M. Hasegawa-Johnson, “A PAC-Bayesian approach to minimum perplexity language modeling,” in Proc. Int. Conf. Comput. Ling. (COLING), Dublin, Ireland, Aug. 2014, pp. 130–140.

- [75] N. Abe, J.-i. Takeuchi, and M. K. Warmuth, “Polynomial learnability of stochastic rules with respect to the KL-divergence and quadratic distance,” IEICE Trans. Inform., Syst., vol. 84, no. 3, pp. 299–316, Mar. 2001.

- [76] R. Shwartz-Ziv, A. Painsky, and N. Tishby, “Representation compression and generalization in deep neural networks,” Unpublished Manuscript, 2018. [Online]. Available: https://openreview.net/pdf?id=SkeL6sCqK7

- [77] A. Painsky and S. Rosset, “Cross-validated variable selection in tree-based methods improves predictive performance,” IEEE Trans. Pattern Anal. Mach. Intell., vol. 39, no. 11, pp. 2142–2153, Nov. 2017.

- [78] E. H. Shuford, A. Albert, and H. E. Massengill, “Admissible probability measurement procedures,” Psychometrika, vol. 31, no. 2, pp. 125–145, June 1966.

- [79] R. A. Horn and C. R. Johnson, Matrix Analysis, 2nd ed. Cambridge, UK: Cambridge Uiversity Press, 2012.

| Amichai Painsky (S’12–M’18) received his B.Sc. in Electrical Engineering from Tel Aviv University (2007), his M.Eng. degree in Electrical Engineering from Princeton University (2009) and his Ph.D. in Statistics from the School of Mathematical Sciences in Tel Aviv University. He was a Post-Doctoral Fellow, co-affiliated with the Israeli Center of Research Excellence in Algorithms (I-CORE) at the Hebrew University of Jerusalem, and the Signals, Information and Algorithms (SIA) Lab at MIT (2016-2018). Since 2019, he is a faculty member at the Industrial Engineering Department at Tel Aviv University, where he leads the Statistics and Data Science Laboratory. His research interests include Data Mining, Machine Learning, Statistical Learning and Inference, and their connection to Information Theory. |

| Gregory W. Wornell (S’83-M’91-SM’00-F’04) received the B.A.Sc. degree from the University of British Columbia, Canada, and the S.M. and Ph.D. degrees from the Massachusetts Institute of Technology, all in electrical engineering and computer science, in 1985, 1987 and 1991, respectively. Since 1991 he has been on the faculty at MIT, where he is the Sumitomo Professor of Engineering in the Department of Electrical Engineering and Computer Science. At MIT he leads the Signals, Information, and Algorithms Laboratory within the Research Laboratory of Electronics. He is also chair of Graduate Area I (information and system science, electronic and photonic systems, physical science and nanotechnology, and bioelectrical science and engineering) within the EECS department’s doctoral program. He has held visiting appointments at the former AT&T Bell Laboratories, Murray Hill, NJ, the University of California, Berkeley, CA, and Hewlett-Packard Laboratories, Palo Alto, CA. His research interests and publications span the areas of information theory, statistical inference, signal processing, digital communication, and information security, and include architectures for sensing, learning, computing, communication, and storage; systems for computational imaging, vision, and perception; aspects of computational biology and neuroscience; and the design of wireless networks. He has been involved in the Information Theory and Signal Processing societies of the IEEE in a variety of capacities, and maintains a number of close industrial relationships and activities. He has won a number of awards for both his research and teaching, including the 2019 IEEE Leon K. Kirchmayer Graduate Teaching Award. |