alphastable: An R Package for Modelling Multivariate Stable and Mixture of Symmetric Stable Distributions

Mahdi Teimouri

Department of Statistics, Faculty of Science, Gonbad Kavous University

No.163, Basirat Blvd, Gonbad Kavous, Iran

teimouri@aut.ac.ir

Mahdi Torshizi

Department of Computer Engineering, Faculty of Science, Gonbad Kavous University

No.163, Basirat Blvd, Gonbad Kavous, Iran

mtorshizi@gonbad.ac.ir

Adel Mohammadpour

Department of Statistics, Faculty of Mathematics and Computer Science, Amirkabir University of Technology (Tehran Polytechnic)

424 Hafez Ave., Tehran 15914, Iran

adel@aut.ac.ir

Saralees Nadarajah

School of Mathematics, University of Manchester

Manchester M13 9PL, UK

mbbsssn2@manchester.ac.uk

Abstract:

The family of stable distributions received extensive applications in many fields of studies since it incorporates both the skewness and heavy tails. In this paper, we introduce a package written in the R language called alphastable. The alphastable performs a variety of tasks including: 1- generating random numbers from univariate, truncated, and multivariate stable distributions. 2- computing the probability density function of univariate and multivariate elliptically contoured stable distributions, 3- computing the distribution function of univariate stable distributions, 4- estimating the parameters of univariate symmetric stable, univariate Cauchy, mixture of Cauchy, mixture of univariate symmetric stable, multivariate elliptically contoured stable, and multivariate strictly stable distributions. This package, as it will be shown, is very useful for modelling data in univariate and multivariate cases that arise in the fields of finance and economics.

Keywords: EM algorithm, Maximum likelihood estimator, Model-based clustering, Price return, R language, Robust mixture modelling, Stable distribution

1 Introduction

Different types of data found in applications arise from a distribution whose probability density function (pdf) is heavy-tailed, asymmetric, or both heavy-tailed and asymmetric. Despite lack of closed-form expression for the pdf, the class of stable distributions is the most appropriate candidate for modelling processes whose frequency curve is heavy-tailed and skewed for which, the normal distribution is quite inappropriate. The family of stable distributions is becoming increasingly popular in some fields such as biology, ecology, economics, finance, genetics, insurance, physics, physiology, and telecommunications. Details for the applications of stable distributions in aforementioned fields can be found in [13], [16], [21], [24], [29], [32], [35], [38], [39], [40], and [42]. As the central member of this family, the Cauchy distribution itself received many applications in a variety of such fields, for example, as applied physics ([45, 23]), electrical engineering [58], seismology [15], and theoretical physics [20]. The class of stable distributions is introduced in terms of its characteristic function (chf). The chf of a univariate stable distribution takes different parameterizations. Among them, we shall refer to two important forms which, are known in the literature as and , see ([30, 59]). In what follows, we review briefly and parameterizations. If random variable follows a stable distribution, then the chf of , i.e. , in parameterization is given by

| (1.3) |

where =-1 and is the well-known sign function. The family of stable distributions has four parameters: tail index , skewness , scale , and location . If =0, it would be the class of symmetric stable distributions. If =1 and , we have the class of the positive stable distributions. In this case, varies over the positive semi-axis of real line. The chf of in parameterization is given by

| (1.6) |

where is the location parameter. The pdf and chf in parameterization are continuous functions of all four parameters while the pdf and chf in parameterization both have a discontinuity at . It can be seen that the location parameters in and parameterizations are related as

| (1.9) |

It is clear that in symmetric case, both parameterizations are equal. Hereafter, we write and to denote the class of stable distributions in and parameterizations, respectively. Also, we assume that follows stable distribution.

Frequency curve of phenomena such as asset return [32], flood [3], medical expenditure [55], rainfall [8], and precipitation [28] exhibits heavy tails, multimodality, or both heavy tails and multimodality. Mixture models are very useful tool for modelling data whose frequency curve is multimodal. Also, the mixture models are widely used in model-based clustering. The normal mixture models are frequently used for model-based clustering, but they show poor performance in the presence of outliers. So, the robust mixture models which, aim to tackle tail-weight ([1, 36]); deal with skewness [19]; or account for both ([2, 5, 18, 17, 46, 56]) are frequently used in model-based clustering. Since stable distributions have heavy tails, the symmetric stable mixture models (SSMM) can be considered as the best choice for robust mixture modelling. The pdf of a -component SSMM has the form

| (1.10) |

where ; for , , , and is the vector of parameters and denotes the pdf of th component which, follows a symmetric stable distribution. The mixing parameters s are non-negative and sum to one, i.e., . Using some type of the EM algorithm, namely the expectation conditional maximization either algorithm (ECME), the parameters of SSMM can be estimated, see [52]. The performance and robustness of the proposed EM algorithm versus model violations and presence of outliers were proved via comprehensive simulations for different scenarios. For example, when data follow mixture model, the SSMM outperforms other mixture models including generalized hyperbolic (GH), normal, skew normal, and skew . Also, when data follow a mixture of exponential power distribution, the SSMM performs better than a mixture of GH, normal, skew normal, and distributions.

Truncated stable random variables arise in many applied fields such as characterization of impulsive network traffic [47] and GARCH models and option pricing [22]. Some algorithms proposed in [27], [44], [43], [49], and [50] to simulate truncated stable random variables. In what follows, we give two definitions for stable random vector, see [42, p. 57; p. 65].

Definition 1.1

A random vector is said to be stable in if for any positive numbers and there is a positive number and a vector such that

| (1.11) |

where and are independent and identical copies of and .

Definition 1.2

Let . Then is a non-Gaussian stable random vector in if there exists a finite measure on the unit sphere and a vector such that

| (1.14) |

where for , , , and denotes the well-known sign function. The pair is unique.

Each -dimensional multivariate stable distribution is fully described by the triple . A random vector is said to be strictly stable in if for . We note that is strictly stable, in the sense of Definition 1.1, if . Throughout, we assume that follows a multivariate strictly stable distribution for .

The class of multivariate stable distributions are intractable for dimensions more than two, see [34]. As a computationally tractable subclass, the pdf a -dimensional elliptically contoured stable distribution can be computed numerically for any . Suppose follows a -dimensional elliptically contoured stable distribution with dispersion matrix and location vector , then the chf of is given by

| (1.15) |

where is a positive definite matrix, see [34]. Throughout, we assume that random vector has chf given by (1.15). Teimouri et al. (2018) proposed the EM algorithm to estimate the parameters of a -dimensional elliptically contoured stable distribution. Since finding the full maximum likelihood (ML) estimations of the parameters of a multivariate elliptically contoured stable distribution is computationally expensive, the projecting approach is suggested by which is projected into real line. Under this approach each projected random variable follows a univariate symmetric stable distribution and so the CF, ML, and SQ methods can be applied to estimate the parameters, see [34]. The results obtained in such a way are known as projected estimations and corresponding methods are called projected CF, ML, and SQ, respectively. It should be noted that the estimated dispersion matrix using the projection approach is not necessarily positive definite and is computationally expensive when gets large.

Free packages developed in the literature are stabledist [11] and libstableR [41]. The stabledist generates stable random variables, computes pdf(s), cumulative distribution function(s) (cdf) and quantiles of stable distribution for given admissible values of the parameters. The libstableR is developed for fast and accurate evaluation, generation, and parameter estimation of stable distributions. It should be noted that packages are not applicable for a mixture of univariate stable and multivariate stable distributions.

2 Methodology

In this section, we briefly provide some explanations about the methodology used in alphastable.

2.1 Simulation

2.1.1 Random variable generation from univariate stable distributions

2.1.2 Random variable generation from truncated stable distributions

2.1.3 Random vector generation from elliptically contoured stable distribution

Using the definition of an elliptically contoured stable distribution given in [42], we simulate -dimensional elliptically contoured stable random vector.

2.1.4 Random vector generation from multivariate stable distributions

An algorithm for random vector generation from multivariate stable distribution was given in [25]. Based on this algorithm, we simulate bivariate stable random vector.

2.2 Computing the pdf and cdf of univariate stable distributions

Using series given in [48], we compute the cdf and pdf of stable distribution in both and parameterizations for . These series provide a very accurate approximation of the cdf and pdf within their convergence regions. For those points that series are not convergent the R package stabledist is used to compute the pdf and cdf. Fortunately these series approximate accurately the pdf (or cdf) and have no computational problem in boundary cases including , , and , see [48]. Let , , , and

For any admissible quadruple we have the following approximations.

-

•

If , then

Also,

-

•

If , then

2.3 Parameter estimation for Cauchy and mixture of Cauchy distributions

Due to a wide range of applications received for the Cauchy distribution, estimation of the parameters of Cauchy and mixture of Cauchy distributions are important tasks. To perform these tasks, we employing the EM algorithm. Generally, the EM algorithm is employed for computing the ML estimations when the log-likelihood function is not tractable mathematically. This is done by considering an extra missing (or latent) variable when the conditional expectation of the complete data log-likelihood given observed data and a guess of unknown parameter(s) is maximized. So, we look for a stochastic representation that involves the latent variable(s). The representation given by the following proposition is valid for Cauchy distribution.

Proposition 2.1

Suppose and . Then

| (2.17) |

where denotes the equality in distribution and . The random variables , , and are mutually independent.

Simulations reveal that the derived EM algorithm based on Proposition 2.1 can be considered as a good competitor for the ML approach. We note that the EM algorithm outperforms the CF and SQ approaches and hence, two latter methods are removed by competitions, see Figure 7. To show the performance of the EM algorithm for estimating the parameters of Cauchy mixture model, we consider a two-component () Cauchy mixture model in which the pdf of each component takes the form ; for . The results of simulations are depicted in Figures 8-9.

2.4 Parameter estimation for symmetric and mixture of symmetric stable distributions

Similar to the previous subsection, by considering a latent variable such as , we consider the following representation for each symmetric stable distribution, see [42].

Proposition 2.2

Suppose and . Then

| (2.18) |

where . The random variables and are independent.

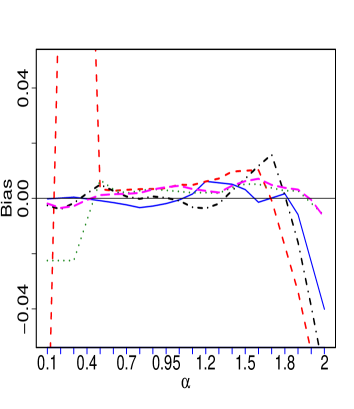

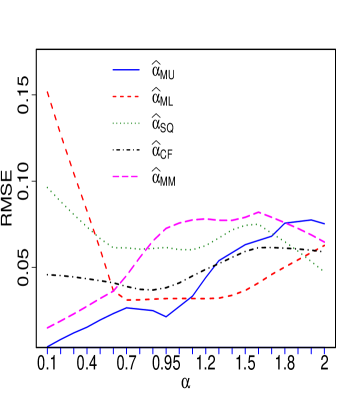

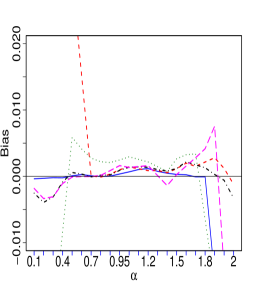

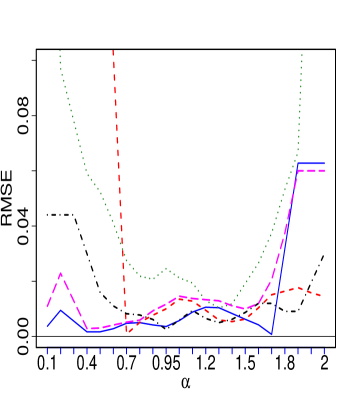

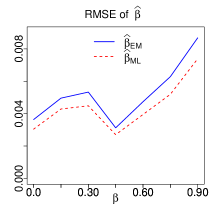

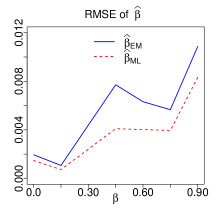

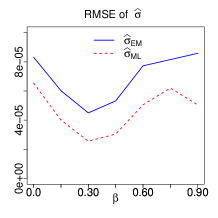

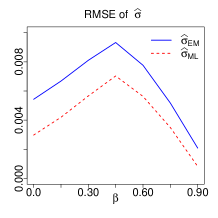

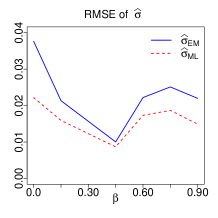

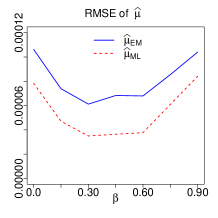

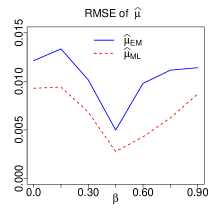

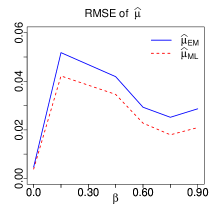

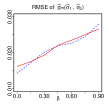

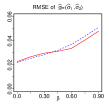

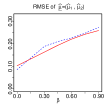

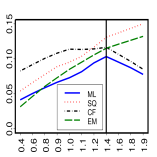

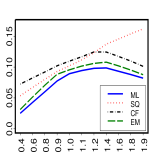

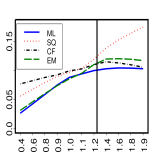

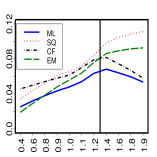

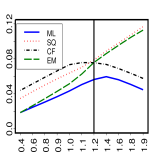

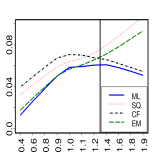

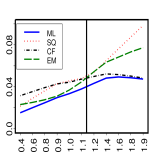

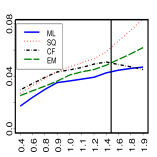

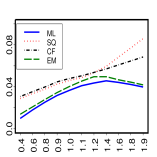

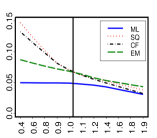

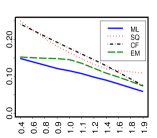

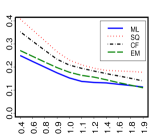

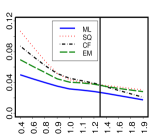

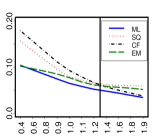

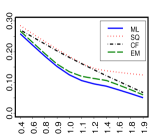

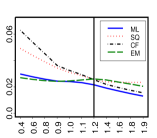

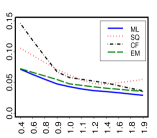

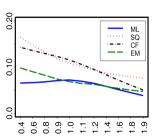

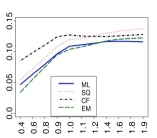

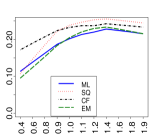

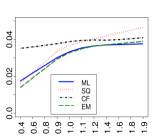

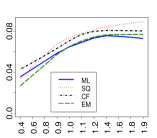

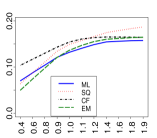

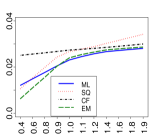

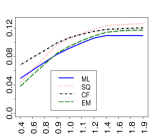

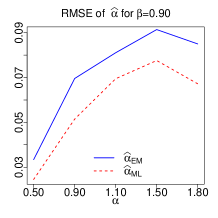

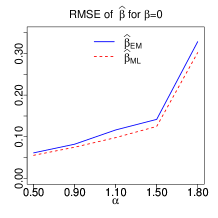

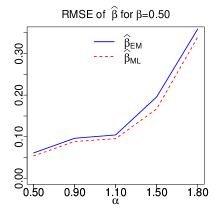

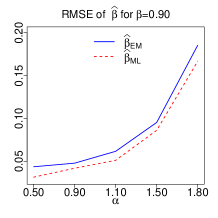

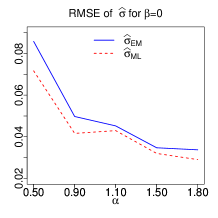

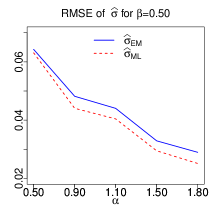

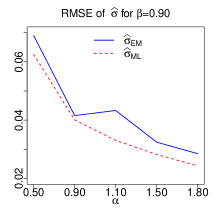

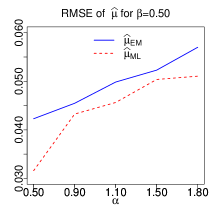

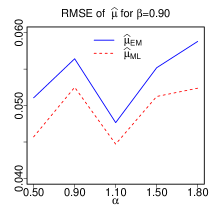

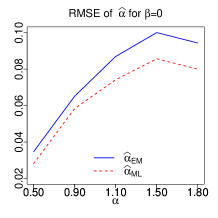

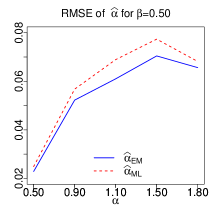

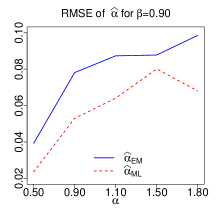

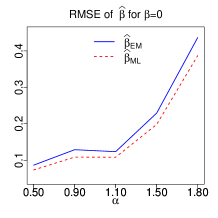

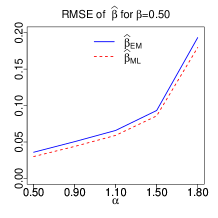

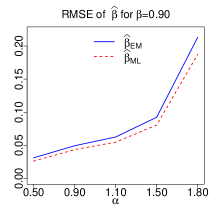

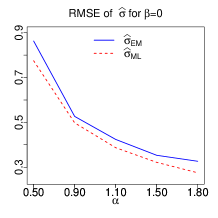

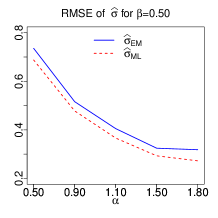

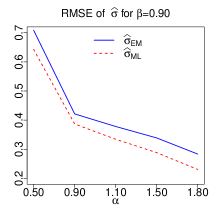

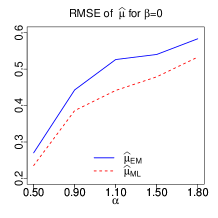

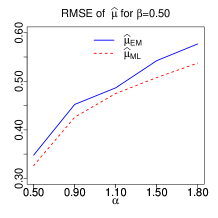

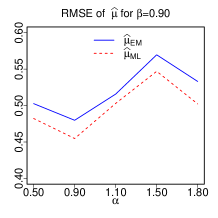

Using representation (2.18), the proposed EM algorithm is applied to estimate the parameters of symmetric stable distribution, see [53]. We compare the performance of the CF, ML, SQ, and the proposed EM methods for estimating the parameters of the symmetric stable distribution through simulations. For applying the CF, ML, and SQ approaches we use STABLE software, see [31]. In simulations, the root of mean square error (RMSE) is computed for sample sizes , and 1000. The number of replications is and parameter settings are: , , and . The simulations results under four methods are shown in Figures 10-12. It should be noted that the estimation results for the evaluated ML approach is not reliable for . The smoothed version of the actual values plotted in these figures are obtained using the lowess package with the following settings: the smoothing span is considered to be 2/3, number of iterations is 3, and the speed of computations is determined by 0.01th of the range of the values, see [10].

In each sub-figure through Figures 10-12, the vertical line indicates that the proposed EM algorithm works better than the CF and SQ methods for those s lie in the left side of the line. If the EM algorithm works as the best, such a line is disappeared. By considering the location parameter as zero, the following results are obtained from the simulations.

- 1.

-

2.

EM-based outperforms the CF and SQ methods, ref. Figure 12.

-

3.

EM-based outperforms the SQ-based .

-

4.

EM-based shows superior performance than the CF- and SQ-based .

-

5.

We know that ML method gives the efficient estimation, particularly when sample size gets large. But, sometimes EM-based and outperform the ML counterparts. This occurs because, STABLE gives the approximated ML estimation not the exact ML estimation and also we are using lowess package.

-

6.

RMSE of all estimators decreases by increasing the sample size .

Along with the simulations, we investigate the execution time for different sample sizes and scale parameter levels. The results are given in Table 1. For this purpose, all runs are performed on a machine with 3.5 GHz Core(TM) i7-2700K Intel(R) processor and 8 GB of RAM.

| n | 0.5 | 1 | 2 |

|---|---|---|---|

| 500 | 30(51) | 26(55) | 22(53) |

| 1000 | 70(118) | 55(110) | 43(112) |

| 5000 | 334(602) | 283(611) | 223(591) |

The performance analysis of the proposed EM algorithm for modelling a SSMM has been reported by [52].

2.5 Parameter estimation for skewed stable distribution

For skewed stable distribution, we give a new representation by the following.

Proposition 2.3

Suppose , , and . We have

| (2.19) |

where , , , and . All random variables , , and are mutually independent.

Using above representation, the methodology used for estimating the parameters of a symmetric stable distribution can be developed for estimating the parameters of a skewed stable distribution. To save the space, we refuse to describe the proposed EM algorithm. Performance of the proposed EM algorithm is proven via simulations. Some part of the simulations are shown in Figures 13-14. These figures demonstrate that the proposed EM algorithm for skewed stable distribution works as well as the ML approach but just with a slight difference. During simulations, we found that the proposed EM algorithm generally outperforms the CF and SQ approaches and so removed by competitions.

2.6 Parameter estimation for multivariate elliptically contoured stable distribution

Estimating the parameters of a multivariate elliptically contoured stable distribution is computationally expensive. The parameters of this distribution, as described in Introduction, are estimated using the projection method. While the dispersion matrix estimated using projection method is not always positive definite [34], the estimated dispersion matrix using the EM algorithm [53] is always positive definite. To show the performance of the EM algorithm, here we confine ourselves to the bivariate case. For higher dimensions the results are the same. Firstly, a simulation study is performed to compare the performance of the CF, EM, ML, and SQ approaches. Then, we apply all four methods to the real data. For simulation study, a sample of size vectors are simulated from a bivariate elliptically contoured stable distribution with , , and dispersion matrix

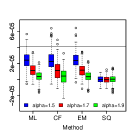

Above setting of the dispersion matrix was used by [39]. We follow the CF, ML, and SQ approaches using the STABLE software. The boxplots based on 250 runs are depicted in Figure 6. We note that the proposed EM algorithm is robust with respect to initial values. As it is seen, the proposed EM algorithm works as well as or better than the CF and SQ approaches in terms of bias (with respect to median) and length of the box. For analyzing real data, we apply the CF, EM, ML, and SQ methods to S&P500 and IPC indices. These indices are between 9 years of daily returns of 22 major worldwide market which, consists of 2535 observations from 1/4/2000 to 9/22/2009. This data set is available at the website of Yahoo finance. The empirical distribution of both S&P500 and IPC indices show a symmetric pattern around the origin and corresponding scatterplot is roughly elliptical contoured. Furthermore, estimated tail indices after fitting stable distribution to the S&P500 and IPC indices through the ML approach are 1.9003 and 1.9143, respectively, which are assumed to be equal. Thus, the assumption that follows an elliptically contoured stable distribution is acceptable, see [34]. The results of estimating parameters through the CF, EM, ML, and SQ methods are shown in Table 2. The log-likelihood value indicates that the EM algorithm gives better performance than the CF and SQ approaches.

| Parameters | ||||

|---|---|---|---|---|

| Method | Log-likelihood | |||

| ML | 1.9073 | -4967.706 | ||

| CF | 1.9530 | -4978.067 | ||

| EM | 1.7116 | -4975.581 | ||

| SQ | 1.8179 | -5176.572 | ||

Also, through a simulation study, we compare the execution times (in seconds) of the EM and ML methods. The results are given in Table 3.

| d | =1.5 | =1 |

|---|---|---|

| 5 | 181(1.2) | 165(0.6) |

| 10 | 202(3.3) | 190(3.5) |

| 20 | 220(7.6) | 223(7.8) |

| 50 | 245(42) | 228(40) |

| 100 | 416(193) | 359(173) |

2.7 Parameter estimation for multivariate strictly stable distribution

Estimating the parameters of a multivariate stable distribution is a great challenge. This is because the multivariate stable distributions are a semi-parametric model, i.e. these models involve an infinite number of parameters. To overcome this problem, the spectral measure given in Definition 1.2 is discretized at points as

| (2.20) |

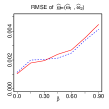

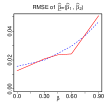

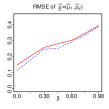

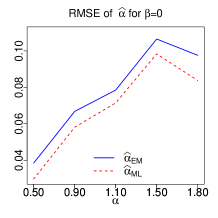

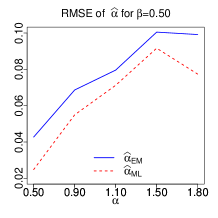

where is a mass at point in and is an indicator function at point ; for , see [7]. Assuming that the address of masses are known, discrete spectral measure given in (2.20) can be estimated through the projected CF, ML, or SQ approaches. Developing the idea proposed by [12], an estimator, shown here by , for the tail index of multivariate strictly stable distribution introduced by [51]. Suppose the tail index estimator using CF, ML, and SQ methods are shown by , , , respectively. A comparison will be made between , , , , and that introduced by [26], here shown by , through a simulation study. The following observations can be made from Figure 1.

-

•

and show better performance than for in the sense of RMSE.

-

•

is more efficient than all other estimators for in the sense of RMSE.

-

•

is more efficient than all other estimators for in the sense of bias for sample size .

-

•

shows better performance than in the sense of RMSE for sample size .

Also, an estimator of the discretized spectral measure can be constructed using , , , , and . A comprehensive comparison was made between the performance of these estimators by [51].

3 The R package alphastable

We develop the alphastable package for generating stable random variables (in univariate and multivariate cases), generating truncated stable random variables (in univariate case), computing pdfs and cdfs (in univariate case), estimating the parameters of stable distribution (in univariate and multivariate cases), and modelling mixture of Cauchy and symmetric stable distributions. In what follows, we describe how to use the alphastable. It depends on packages mvtnorm (http://cran.r-project.org/web/packages/mvtnorm/index.html), nnls (https://cran.r-pr oject.org/web/packages/nnls/index.html), and stabledist (https: //cran.r-project.org/ web/packages/stabledist/index.html). The alphastable package has been uploaded to comprehensive R archive network (CRAN), see https://CRAN.R-project.org/pac kage=alphastable.

3.1 Random generation

3.1.1 Random number generation from univariate stable distribution

Use the following command.

urstab(n,alpha,beta,sigma,mu,param)

The available arguments are:

n: the sample size

alpha: the tail index parameter

beta: the skewness parameter

sigma: the scale parameter

mu: the location parameter

param: type of parameterization must be 0 or 1 for and parameterizations, respectively.

Example: we use the following command to simulate realizations from univariate stable distribution with parameters , , , and in parameterization.

R>urstab(200,1.3,0.5,2,0,0)

3.1.2 Random number generation from truncated stable distribution

Use the following command.

urstab.trunc(n,alpha,sigma,mu,a,b,param)

The available arguments are:

verb—n—: the sample size

alpha: the tail index parameter

sigma: the scale parameter

mu: the location parameter

a: the lower bound of truncation

b: the upper bound of truncation

param: type of parameterization must be 0 or 1 for and parameterizations, respectively.

Example: we use the following command to simulate realizations from truncated stable distribution with parameters , , , which, is truncated over (-5,5) in parameterization.

R>urstab.trunc(200,1.3,0.5,2,0,-5,5,0)

3.1.3 Random vector generation from multivariate elliptically contoured stable distribution

Use the following command.

mrstab.elliptical(n,alpha,Sigma,Mu)

The available arguments are:

n: the sample size

alpha: the tail index parameter

Sigma: the dispersion matrix

Mu: the location vector

Example: we use the following command to simulate vectors from two-dimensional elliptically contoured stable distribution with parameters , , and .

R>library("stabledist")

R>library("mvtnorm")

R>mrstab.elliptical(200,1.3,matrix(c(1,.5,.5,1),2,2),c(0,0))

3.1.4 Random vector generation from multivariate stable distribution

Use the following command.

mrstab(n,m,alpha,Gamma,Mu)

The available arguments are:

n: the sample size

m: the number of masses

alpha: the tail index parameter

Gamma: the mass vector

Mu: the location vector

Example: we use the following command to simulate vectors from two-dimensional stable distribution with , the vector of masses , and .

R>library("stabledist")

R>mrstab(200,4,1.3,c(0.1,0.5,0.5,0.1),c(0,0))

3.1.5 computing the pdf and cdf of univariate and multivariate stable distributions

Use the following command for computing the pdf of univariate stable distribution.

udstab(y,alpha,beta,sigma,mu,param)

The available arguments are:

y: a real value at which pdf is computed

alpha: the tail index parameter

beta: the skewness parameter

sigma: the scale parameter

mu: the location parameter

param: type of parameterization must be 0 or 1 for and parameterizations, respectively.

Example: we use the following command to compute the pdf of a univariate stable distribution at point with parameters , , , and in parameterization.

R>library("stabledist")

R>udstab(2,1.2,0.9,1,0,1)

[1] 0.0240643

Use the following command for computing the cdf of univariate stable distribution.

upstab(y,alpha,beta,sigma,mu,param)

The available arguments are:

y: a real value at which cdf is computed

alpha: the tail index parameter

beta: the skewness parameter

sigma: the scale parameter

mu: the location parameter

param: type of parameterization must be 0 or 1 for and parameterizations, respectively.

Example: we use the following commands to compute the cdf of a univariate stable distribution at point with parameters , , , and in parameterization.

R>library("stabledist")

R>upstab(2,1.2,0.9,1,0,1)

[1] 0.9044019

We use the following command for computing the pdf of multivariate elliptically contoured stable distribution.

mdstab.elliptical(z,alpha,Sigma,Mu)

The available arguments are:

y: a real vector at which pdf is computed

alpha: the tail index parameter

Sigma: the dispersion matrix

Mu: the location vector

Example: we use the following command to compute the pdf of two-dimensional elliptically contoured stable distribution at point with parameters , , and .

R>library("stabledist")

R>mdstab.elliptical(c(5,5),1.2,matrix(c(1,0.5,0.5,1),2,2),c(0,0))

[1] 0.0005279

3.2 Parameter estimation for Cauchy and mixture of Cauchy distributions

Use the following command to estimate the parameters of Cauchy distribution.

ufitstab.cauchy(y,beta0,sigma0,mu0,param)

The available arguments are:

y: the vector of observations

beta0: the initial value of skewness parameter to start the EM algorithm

sigma0: the initial value of scale parameter to start the EM algorithm

mu0: the initial value of location parameter to start the EM algorithm

param: type of parameterization must be 0 or 1 for and parameterizations, respectively.

Example: we consider the large recorded intensities (in Richter scale) of the earthquake at seismometer locations in western North America between 1940 and 1980. The related features was reported by [14]. Among the features, we focus on the 182 distances from the seismological measuring station to the epicenter of the earthquake (in km) as the variable of interest. This set of data can be found in package nlme. Using the initial values as , , and , the EM estimations are , , and . The commands and related output are as the following.

R>library("nlme")

R>y<-Earthquake[,3]

R>ufitstab.cauchy(y,0.5,5,10,0)

$beta

[1] 0.91678

$sigma

[1] 11.5981

$mu

[1] 16.9498

The Kolmogorov-Smirnov (K-S) and Anderson-Darling (A-D) goodness-of-fit criteria are 0.0397 and 0.6980, respectively.

Use the following command for estimating the parameters of mixture of Cauchy distributions.

ufitstab.cauchy.mix(y,K,omega0,beta0,sigma0,mu0)

The available arguments are:

y: the vector of observations

K: the number of components

omega0: the initial value of weight vector to start the EM algorithm

beta0: the initial value of skewness vector to start the EM algorithm

sigma0: the initial value of scale vector to start the EM algorithm

mu0: the initial value of location vector to start the EM algorithm

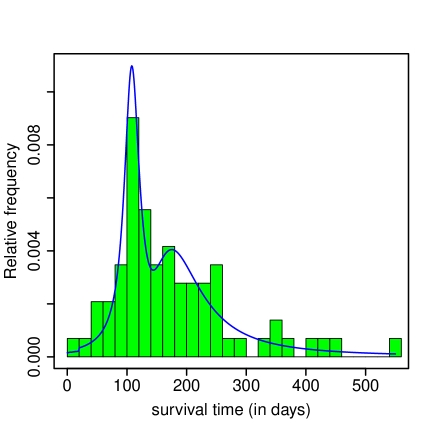

Example: We use the survival times in days of 72 guinea pigs infected with different doses of tubercle bacilli, see [4]. To implement the EM algorithm the initial values are: , , , and . The EM estimations are , , , and . The commands and related output are given by the following.

R>pig<-c(10,33,44,56,59,72,74,77,92,93,96,100,100,102,105,107,107,108,108,108,

+ 109,112,121,122,122,124,130,134,136,139,144,146,153,159,160,163,163,

+ 168,171,172,176,113,115,116,120,183,195,196,197,202,213,215,216,222,

+ 230,231,240,245,251,253,254,255,278,293,327,342,347,361,402,432,458,

+ 555)

R>library("stabledist")

R>ufitstab.cauchy.mix(pig,2,c(0.65,0.35),c(0.20,0.05),c(20,50),c(95,210))

$omega

[1] 0.5327 0.4673

$beta

[1] 0.05160 0.8233

$sigma

[1] 15.6626 39.1202

$mu

[1] 108.5602 194.5814

The corresponding K-S and A-D goodness-of-fit statistics are 0.04882 and 0.25062, respectively. Figure 5 displays fitted two-component Cauchy distribution to the guinea pigs survival times data.

3.3 Estimating the parameters of zero-location symmetric stable distribution using U-statistic

Use the following command.

ufitstab.ustat(y)

The available argument is:

y: the vector of observations

Example: Suppose the CAC40 (Bourse de Paris) data discussed in the previous section follow a zero-location symmetric stable distribution. The commands and related output for applying the U-statistic to these data are given as follows.

R>CAC40<-c(-0.020807,0.003035,-0.036817,...,-0.054140,-14.87798)

R>library("stabledist")

R>ufitstab.sym(CAC40)

$alpha

[1] 1.4643

$sigma

[1] 0.4725

The K-S and A-D statistics are 0.0290 and 4.0935, respectively.

3.4 Estimating the parameters of symmetric and mixture of symmetric stable distributions

We use the following command for estimating the parameters of symmetric stable distribution.

ufitstab.sym(y,alpha0,sigma0,mu0)

The available arguments are:

y: the vector of observations

alpha0: the initial value of tail index parameter to start the EM algorithm

sigma0: the initial value of scale parameter to start the EM algorithm

mu0: the initial value of location parameter to start the EM algorithm

Example: we apply the EM algorithm to CAC40 (Bourse de Paris) data. Using the initial values as , , and , the EM estimations are , , and . The commands and related output are given as follows.

R>CAC40<-c(-0.020807,0.003035,-0.036817,...,-0.054140,-14.87798)

R>library("stabledist")

R>ufitstab.sym(CAC40,1.2,1,1)

$alpha

[1] 1.7898

$sigma

[1] 0.5561

$mu

[1] 0.0111

The K-S and A-D statistics are 0.0192 and 1.6430, respectively. We use the following command to estimate the parameters of SSMM.

ufitstab.sym.mix(y,k,omega0,alpha0,sigma0,mu0)

The available arguments are:

y: the vector of observations

k: the number of components

omega0: the initial value of weight vector to start the EM algorithm

alpha0: the initial value of tail index vector to start the EM algorithm

sigma0: the initial value of scale vector to start the EM algorithm

mu0: the initial value of location vector to start the EM algorithm

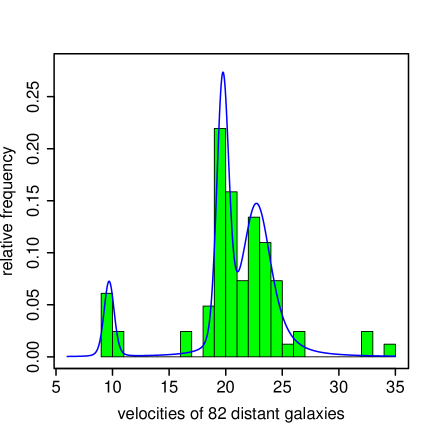

Example: For validating the performance of the proposed EM algorithm we use galaxy (velocities of 82 distant galaxies, diverging from our own galaxy) data. These data are available at https://people.maths.bris.ac.uk/mapjg/mixdata. The commands and related output are given by the following.

R>galaxy<-c(9.172,9.350,9.483,9.558,9.775,10.227,10.406,16.084,16.170,18.419,

+ 18.552,18.600,18.927,19.052,19.070,19.330,19.343,19.349,19.440,

+ 19.473,19.529,19.541,19.547,19.663,19.846,19.856,19.863,19.914,

+ 19.918,19.973,19.989,20.166,20.175,20.179,20.196,20.215,20.221,

+ 20.415,20.629,20.795,20.821,20.846,20.875,20.986,21.137,21.492,

+ 21.701,21.814,21.921,21.960,22.185,22.209,22.242,22.249,22.314,

+ 22.374,22.495,22.746,22.747,22.888,22.914,23.206,23.241,23.263,

+ 23.484,23.538,23.542,23.666,23.706,23.711,24.129,24.285,24.289,

+ 24.366,24.717,24.990,25.633,26.960,26.995,32.065,32.789,34.279)

R>library("stabledist")

R>y<-galaxy

R>ufitstab.sym.mix(y,3,c(0.1,0.35,0.55),c(1.2,1.2,1.2),c(1,1,1),c(8,20,22))

$omega

[1] 0.0842 0.3405 0.5753

$alpha

[1] 1.7781 1.8494 1.3695

$sigma

[1] 0.3307 0.3836 1.1388

$mu

[1] 9.6941 19.7442 22.7213

The K-S and A-D statistics are 0.0372 and 0.2040, respectively. The fitted pdf to the galaxy data is shown in Figure 2. We note that the SSMM outperforms the other mixture models including: skew normal ([19, 18, 2]), slash normal [2], [36], skew ([18, 56]), and GH [5], see [52]. For applying aforementioned models to the galaxy data, we use packages mixsmsn [37] and MixGHD [54]. Contrary to the SSMM, these models may give different estimation results when they are applied several times to the galaxy data. This privilege of SSMM put it into the class of models which, are appropriate for robust mixture modelling.

3.5 Estimating the parameters of skewed stable distribution

Use the following command.

ufitstab.skew(y,alpha0,beta0,sigma0,mu0,param)

The available arguments are:

y: the vector of observations

alpha0: the initial value of tail index parameter to start the EM algorithm

beta0: the initial value of skewness parameter to start the EM algorithm

sigma0: the initial value of scale parameter to start the EM algorithm

mu0: the initial value of location parameter to start the EM algorithm

param: type of parameterization must be 0 or 1 for and parameterizations, respectively.

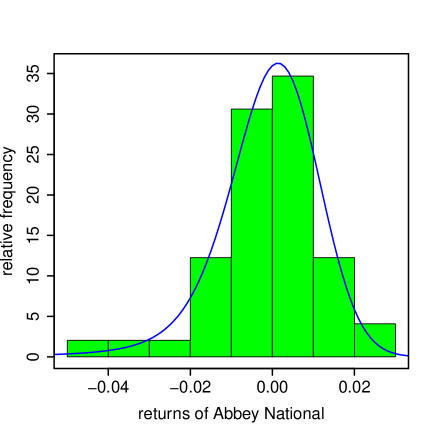

Example: We use the daily price returns of Abbey National shares between 31/7/91 and 8/10/91 (including business days). By assuming that denotes the price at th day, the price return at th day is defined as ; for , see [6]. Using the initial values as , , , and and param=1, the EM-based estimations are , , , and . The commands and related output are as the following.

R> price<-c(296,296,300,302,300,304,303,299,293,294,294,293,295,287,288,297,

+ 305,307,304,303,304,304,309,309,309,307,306,304,300,296,301,298,

+ 295,295,293,292,307,297,294,293,306,303,301,303,308,305,302,301,

+ 297,299)

R>y<-c()

R>n<-length(price)

R>for(i in 2:n){y[i]<-(price[i-1]-price[i])/price[i-1]}

R>library("stabledist")

R>ufitstab.skew(y[2:n],0.8,0,0.25,0.25,1)

$alpha

[1] 1.8046

$beta

[1] -0.9999

$sigma

[1] 0.0078

$mu

[1] 0.0009

The corresponding log-likelihood statistics for the ML and EM estimations are 146.3868 and 147.0238, respectively. Figure 3 displays the fitted stable pdf to the Abbey National returns data.

3.6 Estimating the parameter of multivariate elliptically contoured stable distribution

Use the following command.

mfitstab.elliptical(z,alpha0,Sigma0,Mu0)

The available arguments are:

z: an vector of observations

alpha0: the initial value of tail index parameter to start the EM algorithm

Sigma0: the initial value of dispersion matrix to start the EM algorithm

Mu0: the initial value of location vector to start the EM algorithm

Example: we follow for applying the EM algorithm to & introduced in the previous section. The initial values are , , and . The commands and related output are given by the following.

R>SandP<-c(-0.01602344,-0.01331844,1.51226709,...,-0.78849818,0.39571979)

R>IPC<-c(-0.03497474,-0.00589434,0.98289177,...,-0.42876127,0.21059706)

R>z<-cbind(SandP,IPC)

R>library("stabledist")

R>mfitstab.elliptical(z,1.2,matrix(c(0.75,0.25,0.25,0.75),2,2),c(0.5,0.5))

$alpha

[1] 1.7315

$Sigma

[,1] [,2]

[1,] 0.3995 0.3648

[2,] 0.3648 0.3968

$mu

[1] -0.0275 -0.0245

The estimated tail index, dispersion matrix, and location vector are and , and , respectively. The log-likelihood statistics correspond to the ML and EM estimations are -4967.706 and -4975.571, respectively. It should be noted that the EM algorithm outperforms the CF and SQ approaches.

3.7 Estimating the parameters of strictly multivariate stable distribution

Use the following command.

mfitstab.ustat(x,m,method=method)

The available arguments are:

x: an vector of observations

m: the number of masses

method: must be 1 or 2 which, corresponds to the method given by [51] and

[26], respectively

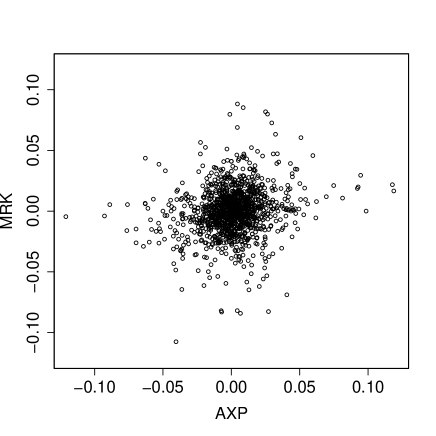

Example: Here, we focus on daily log-return (in percent) of 1247 closing prices of AXP (American Express Company) and MRK (Merck & Co. Inc.), see [34]. This set of data are between January 3, 2000 and December 31, 2004. The scatterplot of is shown in Figure 4. For , the masses of the spectral measure are addressed by ; for .

The commands and related report are given by the following.

R>AXP<-c(0.007512315,-0.005194817,-0.018692133,...,-0.007746755,-0.000507314)

R>MRK<-c(-0.020927520,0.016074450,-0.014427908,...,-0.004621792,-0.009931801)

R>x<-cbind(AXP,MRK)

R>library("nnls")

R>mfitstab.ustat(x,4,1)

$alpha

[1] 1.5881

$mass

[1] 0.000000 0.000176 0.000627 0.000019

R>mfitstab.ustat(x,4,2)

$alpha

[1] 1.6983

$mass

[1] 0.000000 0.000203 0.000590 0.000000

As it is seen, the estimated discrete spectral measure using the method proposed by [51] and [26] are and , respectively.

4 Conclusions

In this paper we introduce an R package called alphastable which, provides an environment for: 1- generating random numbers from univariate, truncated, and multivariate stable distributions. 2- computing the probability density function of univariate and multivariate elliptically contoured stable distributions, 3- computing the distribution function of univariate stable distributions, 4- estimating the parameters of univariate symmetric stable, univariate Cauchy, mixture of Cauchy, mixture of univariate symmetric stable, multivariate elliptically contoured stable, and multivariate strictly stable distributions. For computing the pdf and cdf of univariate stable distribution, we use asymptotic series which yield accurate results in their convergence regions. Using an estimator of the tail index based on U-statistic, the alphastable estimates the parameters of multivariate strictly stable distribution. Our proposed package uses the EM algorithm to estimate the parameters of univariate symmetric stable distribution, univariate Cauchy distribution, -dimensional elliptically contoured stable distribution, mixture of univariate Cauchy distributions, and mixture of univariate symmetric stable distributions. In just mentioned cases, the EM algorithm not only is robust with respect to the initial values but also performs accurately for entire parameter space. Other packages that developed freely for R environment, cannot be applied for estimating the parameters of mixture of stable and multivariate stable distributions. The present work is limited to the mixture of univariate symmetric stable distributions. This methodology can be developed for mixture of multivariate elliptically contoured stable distributions. We declare that all computations have been performed on a machine with 3.5 GHz Core(TM) i7-2700K Intel(R) processor and 8 GB of RAM. Our package depends on packages mvtnorm, nnls, and stabledist which, are available on CRAN at https://cran.r-project.org/web/packages/stabledist/index.html, https://cran.r -project.org/web/packages/mvtnorm/index.html, and https://cran. r-pro ject.org/web/packages/nnls/index.html, respectively. The alphastable package has been uploaded to the comprehensive R archive network (CRAN), see https://CRAN.R-pro ject.org/pac kage=alphastable.

References

- [1] J. L. Andrews and P. D. Mcnicholas. Model-based clustering, classification, and discriminant analysis via mixtures of multivariate t-distributions. Statistics and Computing, 22(5):1021–1029, 2012.

- [2] R. M. Basso, V. H. Lachos, C. R. B. Cabral, and P. Ghosh. Robust mixture modeling based on scale mixtures of skew-normal distributions. Computational Statistics & Data Analysis, 54(12):2926–2941, 2010.

- [3] P. Bernardara, D. Schertzer, E. Sauquet, I. Tchiguirinskaia, and M. Lang. The flood probability distribution tail: how heavy is it? Stochastic Environmental Research and Risk Assessment, 22(1):107–122, 2008.

- [4] T. Bjerkedal. Acquisition of resistance in guinea pigs infected with different doses of virulent tubercle bacilli. American Journal of Epidemiology, 72:130–148, 1960.

- [5] R. P. Browne and P. D. McNicholas. A mixture of generalized hyperbolic distributions. Canadian Journal of Statistics, 43(2):176–198, 2015.

- [6] D. Buckle. Bayesian inference for stable distributions. Journal of the American Statistical Association, 90(430):605–613, 1995.

- [7] T. Byczkowski, J. P. Nolan, and B. Rajput. Approximation of multidimensional stable densities. Journal of Multivariate Analysis, 46(1):13–31, 1993.

- [8] J. Carreau, P. Naveau, and E. Sauquet. A statistical rainfall-runoff mixture model with heavy-tailed components. Water Resources Research, 45(10), 2009.

- [9] J. M. Chambers, C. L. Mallows, and B. Stuck. A method for simulating stable random variables. Journal of the American Statistical Association, 71(354):340–344, 1976.

- [10] W. S. Cleveland. Lowess: A program for smoothing scatterplots by robust locally weighted regression. American Statistician, 35(1):54, 1981.

- [11] M. M. Diethelm Wuertz and R. core team members. stabledist: Stable Distribution Functions, 2016. R package version 0.7-1.

- [12] Z. Fan. Parameter estimation of stable distributions. Communications in Statistics-Theory and Methods, 35(2):245–255, 2006.

- [13] O. T. Johnson. Information Theory and the Central Limit Theorem. World Scientific, 2004.

- [14] W. B. Joyner and D. M. Boore. Peak horizontal acceleration and velocity from strong-motion records including records from the 1979 imperial valley, california, earthquake. Bulletin of the Seismological Society of America, 71(6):2011–2038, 1981.

- [15] Y. Kagan. Correlations of earthquake focal mechanisms. Geophysical Journal International, 110(2):305–320, 1992.

- [16] L. B. Klebanov, T. J. Kozubowski, and S. T. Rachev. Ill-Posed Problems in Probability and Stability of Random Sums. Nova Science, 2006.

- [17] S. Lee and G. J. McLachlan. Finite mixtures of multivariate skew t-distributions: some recent and new results. Statistics and Computing, 24(2):181–202, 2014.

- [18] S. X. Lee and G. J. McLachlan. On mixtures of skew normal and skew -distributions. Advances in Data Analysis and Classification, 7(3):241–266, 2013.

- [19] T. I. Lin, J. C. Lee, and S. Y. Yen. Finite mixture modelling using the skew normal distribution. Statistica Sinica, pages 909–927, 2007.

- [20] H. Lorentz. The absorption and emission lines of gaseous bodies. In Knaw, Proceedings, volume 8, pages 1905–1906, 1906.

- [21] B. Mandelbrot and R. L. Hudson. The Misbehavior of Markets: A Fractal View of Financial Turbulence. Basic Books, 2007.

- [22] C. Menn and S. T. Rachev. Smoothly truncated stable distributions, garch-models, and option pricing. Mathematical Methods of Operations Research, 69(3):411, 2009.

- [23] I. Min, I. Mezić, and A. Leonard. Levy stable distributions for velocity and velocity difference in systems of vortex elements. Physics of Fluids, 8(5):1169–1180, 1996.

- [24] S. Mittnik and M. S. Paolella. Prediction of financial downside-risk with heavy-tailed conditional distributions. Handbook of Heavy Tailed Distributions in Finance, 1:385–404, 2003.

- [25] R. Modarres and J. P. Nolan. A method for simulating stable random vectors. Computational Statistics, 9(1):11–19, 1994.

- [26] M. Mohammadi, A. Mohammadpour, and H. Ogata. On estimating the tail index and the spectral measure of multivariate -stable distributions. Metrika, 78(5):549–561, 2015.

- [27] S. Nadarajah and S. Kotz. Programs in r for cumputing truncated cauchy distributions. Quality Technology and Quantitative Management, 4(3):407–412, 2007.

- [28] N. Neykov, P. Neytchev, and W. Zucchini. Stochastic daily precipitation model with a heavy-tailed component. Natural Hazards and Earth System Science, 14(9):2321–2335, 2014.

- [29] C. L. Nikias and M. Shao. Signal Processing with Alpha-Stable Distributions and Applications. Wiley, 1995.

- [30] J. P. Nolan. Parameterizations and modes of stable distributions. Statistics & Probability Letters, 38(2):187–195, 1998.

- [31] J. P. Nolan. Maximum likelihood estimation and diagnostics for stable distributions. In Lévy processes, pages 379–400. Springer, 2001.

- [32] J. P. Nolan. Modeling financial data with stable distributions. Handbook of Heavy Tailed Distributions in Finance, 1:105–130, 2003.

- [33] J. P. Nolan. Stable Distributions: Models for Heavy Tailed Data. Springer, 2010.

- [34] J. P. Nolan. Multivariate elliptically contoured stable distributions: theory and estimation. Computational Statistics, 28(5):2067–2089, 2013.

- [35] S. Ortobelli, S. T. Rachev, and F. J. Fabozzi. Risk management and dynamic portfolio selection with stable paretian distributions. Journal of Empirical Finance, 17(2):195–211, 2010.

- [36] D. Peel and G. J. McLachlan. Robust mixture modelling using the t distribution. Statistics and Computing, 10(4):339–348, 2000.

- [37] M. O. Prates, V. H. Lachos, and C. Cabral. mixsmsn: Fitting finite mixture of scale mixture of skew-normal distributions. Journal of Statistical Software, 54(12):1–20, 2013.

- [38] S. Rachev and S. Mittnik. Stable Paretian Models in Finance. Willey, 2000.

- [39] S. T. Rachev. Handbook of Heavy Tailed Distributions in Finance: Handbooks in Finance, volume 1. Elsevier, 2003.

- [40] S. T. Rachev, C. Menn, and F. J. Fabozzi. Fat-Tailed and Skewed Asset Return Distributions: Implications for Risk Management, Portfolio Selection, and Option Pricing, volume 139. Wiley, 2005.

- [41] J. Royuela-del Val, F. Simmross-Wattenberg, and C. A. López. libstableR: Fast and Accurate Evaluation, Random Number Generation and Parameter Estimation of Skew Stable Distributions, 2018. R package version 1.0.

- [42] G. Samorodnitsky and M. Taqqu. Stable Non-Gaussian Random Processes: Stochastic Models and Infinite Variance. Chapman and Hall, 1994.

- [43] A. Shirvani and A. Soltani. A characterization for truncated cauchy random variables with nonzero skewness parameter. Computational Statistics, 28(3):1011–1016, 2013.

- [44] A. Soltani and A. Shirvani. Truncated stable random variables: characterization and simulation. Computational Statistics, 25(1):155–161, 2010.

- [45] S. Stapf, R. Kimmich, R.-O. Seitter, A. Maklakov, and V. Skirda. Proton and deuteron field-cycling nmr relaxometry of liquids confined in porous glasses. Colloids and Surfaces A: Physicochemical and Engineering Aspects, 115:107–114, 1996.

- [46] S. Subedi and P. D. McNicholas. Variational bayes approximations for clustering via mixtures of normal inverse gaussian distributions. Advances in Data Analysis and Classification, 8(2):167–193, 2014.

- [47] X. Tang, M. Ma, D. I. Ostry, B. Jiao, and Y. J. Guo. Characterizing impulsive network traffic using truncated -stable processes. IEEE Communications Letters, 13(12), 2009.

- [48] M. Teimouri and H. Amindavar. A novel approach to calculate stable densities. In Proceedings of the World Congress on Engineering, volume 1, pages 710–714, 2008.

- [49] M. Teimouri and S. Nadarajah. On simulating truncated stable random variables. Computational Statistics, 28(5):2367–2377, 2013.

- [50] M. Teimouri and S. Nadarajah. On simulating truncated skewed cauchy random variables. Communications in Statistics-Simulation and Computation, 46(2):1318–1321, 2017.

- [51] M. Teimouri, S. Rezakhah, and A. Mohammadpour. U-statistic for multivariate stable distributions. Journal of Probability and Statistics, 2017.

- [52] M. Teimouri, S. Rezakhah, and A. Mohammadpour. Em algorithm for symmetric stable mixture model. Communications in Statistics-Simulation and Computation, 47(2):582–604, 2018.

- [53] M. Teimouri, S. Rezakhah, and A. Mohammadpour. Parameter estimation using the em algorithm for symmetric stable random variables and sub-gaussian random vectors. Journal of Statistical Theory and Applications, 17(3):1–20, 2018.

- [54] C. Tortora, R. Browne, B. Franczak, and P. McNicholas. MixGHD: Model Based Clustering, Classification and Discriminant Analysis Using the Mixture of Generalized Hyperbolic Distributions, 2015. R package version 0.8-1.

- [55] S. Venturini, F. Dominici, and G. Parmigiani. Gamma shape mixtures for heavy-tailed distributions. The Annals of Applied Statistics, 2(2):756–776, 2008.

- [56] I. Vrbik and P. D. McNicholas. Parsimonious skew mixture models for model-based clustering and classification. Computational Statistics & Data Analysis, 71:196–210, 2014.

- [57] R. Weron. On the chambers-mallows-stuck method for simulating skewed stable random variables. Statistics & Probability Letters, 28(2):165–171, 1996.

- [58] S. Winterton, T. Smy, and N. Tarr. On the source of scatter in contact resistance data. Journal of Electronic Materials, 21(9):917–921, 1992.

- [59] V. M. Zolotarev. One-dimensional Stable Distributions, volume 65. American Mathematical Society, 1986.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| n=200 |  |

|

|

|

|---|---|---|---|---|

| n=500 |  |

|

|

|

| n=1000 |  |

|

|

| n=200 |  |

|

|

|

|---|---|---|---|---|

| n=500 |  |

|

|

|

| n=1000 |  |

|

|

| n=200 |  |

|

|

|

|---|---|---|---|---|

| n=500 |  |

|

|

|

| n=1000 |  |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|