Optimal control under uncertainty: Application to the issue of CAT bonds

Abstract

We propose a general framework for studying optimal issue of CAT bonds in the presence of uncertainty on the parameters. In particular, the intensity of arrival of natural disasters is inhomogeneous and may depend on unknown parameters. Given a prior on the distribution of the unknown parameters, we explain how it should evolve according to the classical Bayes rule. Taking these progressive prior-adjustments into account, we characterize the optimal policy through a quasi-variational parabolic equation, which can be solved numerically. We provide examples of application in the context of hurricanes in Florida.

1 Introduction

We consider an insurer or a reinsurer who holds a portfolio in non-life insurance exposed to one or several natural disasters. He can issue one or several CAT bonds222Catastrophe bonds, or CAT bonds, are tradable floating rate notes. The risk associated with a CAT bond is not linked to the default of one entity (state or corporate) but is related to the occurrence of a catastrophe. in order to reduce the risk taken, see e.g. [7] or [8] for a general introduction to CAT bonds.

The first CAT bonds where issued at the end of the 1990s and the market is globally increasing, with a total risk capital outstanding greater that USD 30 billion at the end of 2017, see [1] and [5]. CAT bonds give a strong alternative to the classical reinsurance market.

However, issuing a CAT bond leads to the choice of several parameters, as the layer e.g. and the date of issuance. The coupon is not a priori perfectly known as well as the claim distribution. Moreover, the global warming will lead to an increase of several natural disasters which is a source of uncertainty on the distribution of future claims. For example, in [13], the authors estimate that if the temperature rises of 2.5 degrees in the next decades, the frequency of Hurricanes in North Atlantic will rise by 30%.

The aim of this paper is to provide a rigorous continuous-time framework in which we can establish the optimal behavior policy in issuing CAT bonds, taking into account the uncertainty described above as the risk evolution.

The coupon of the CAT bond is generally not known in advance, even its distribution is not always clearly fixed. We therefore need to model it as a random variable whose distribution depends on unknown parameters. It is the same for the distribution of the natural disasters.

The particular case of acting on a system with partially unknown response distributions has been studied in [3] in a Brownian framework, and widely for the case of discrete settings; see, e.g., [9, 10] for references. They fix a prior distribution on the unknown parameter and introduce a stochastic process on the space of measures which leads to a dynamic programming principle and a PDE characterization of the value function (in the viscosity solution sense). We will adapt [3] in a new context, dealing with CAT bonds.

In this paper, the natural disasters will be represented by a random Poisson measure333The activity of the random Poisson measure will be finite, by construction and two parameters are unknown: the distribution of the severity of the natural disasters and the intensity of their arrivals. As in [3], we allow the agent to issue new CAT bonds at any time, the actions are discrete but chosen in a continuous time framework.

To the best of our knowledge, the study of such a general problem with an application to the CAT bonds seems to be new in the literature, even in the case where all parameters are known. From a mathematical point of view, the main difficulty comes from the fact that the conditional distribution on the unknown parameters evolves continuously and jumps at the occurrence times of a catastrophic event. In [3], it was only evolving when an action was taken on the system. For tractability, we assume that the associated process remains in a finite-dimensional space which can be linked smoothly to a subset of for some . Moreover, in [3], only one action could be running at the same time. In this paper, we will deal with CAT bonds that are active simultaneously. This leads to specific boundary conditions on the characterization of the value function.

Although the model presented below has been designed for the particular case of CAT bonds, it is quite general from a mathematical view-point and can be applied to all cases where the agent faces a random Poisson measure and can issue contracts from which he pays a premium and receives a specific payoff depending on some event.

The paper is organized as follows. Section 2 presents the framework. It introduces all concepts in order to describe the controlled problem. Section 3 gives the characterization of the associated value function as a PDE in the viscosity sense. Section 4 shows the viscosity properties, following and adapting the arguments of [3] in our context. Section 5 provides a sufficient condition for a comparison principle for the PDE satisfied by the value function. Section 6 gives a numerical scheme in order to solve numerically the controlled problem in practice. Finally, section 7 provides a case study of issuing CAT bonds in a optimal way, in the context of Hurricanes in Florida.

2 The framework

2.1 General framework

All over this paper, is the Skorohod space of càdlàg444 Continue à droite, limite à gauche (right continuous with left limits) functions from into , is a probability measure on this space, and is a fixed time horizon.

We consider three Polish spaces: , and that will support three unknown parameters, respectively , and . Here denotes the Borel -algebra. We set

Let be a random Poisson measure with compensator such that is finite on where . The intensity of the random Poisson measure is supposed to be inhomogeneous of the form where is a random variable valued in . The jump distribution is assumed to be where is a random variable valued in . We denote by a subset of the set of Borel probability measures on and by the product of two locally compact subsets of the set of Borel probability measures, respectively on and , endowed with the weak topology.

We also allow an additional randomness when acting on the system and consider another Polish space on which is defined a family of i.i.d. random variables with common probability measure on .

On the product space , we consider the family of measures where . We denote by an element of this family whenever is fixed. The operator is the expectation associated with . Note that and are independent under each . For given, we let denote the -augmentation of the filtration defined by . Hereafter, all random variables are considered with respect to the probability space with given by the context.

2.2 CAT bond framework

In this framework, is the number of perils. The insurer has some exposure related to these perils and may issue CAT bonds to reduce the risk taken. The random Poisson measure represents the arrival of claims. The intensity of arrival is in which , valued in , may be unknown to the insurer. The dependence in time may represent the seasonality or a structural change, for example caused by the global warming.

The measure is the initial knowledge of the insurer on and will evolve through the observations of , whose jumps model the arrival of natural disasters. The severity distribution of the claims may also be unknown, it depends on the unknown parameter , valued in . An initial prior is given as an element . Acting on the system consists in issuing a CAT bond, which means transferring a part of the risk to the market. The equilibrium premium that the insurer will pay is random (since it comes from the law of supply and demand and is not know when the decision to issue is taken), and the distribution may not be perfectly known. We assume that it depends on the unknown parameter , valued in . Its prior distribution is represented by some .

2.3 The control

Let be a non-empty compact set. Let be the time-length of each action on the controlled system. Given , we denote by the collection of random variables on with values in such that is a non-decreasing sequence of -stopping times and each is -measurable for . We shall write where and are and -valued. To each , we associate a non-empty closed set through a one-to-one map.

The ’s will be the times at which a CAT bond is issued. The fixed value is the time-length (or maturity) of all CAT bonds. In , is related to the notional and is the layer chosen for one peril and one region: it is the characteristics of the CAT bonds associated with the risk covered. If a natural disaster occurs and its severity is in the layer , i.e. the random Poisson measure has a jump in , then the associated CAT bond ends and the reinsurer gains a payoff proportional to the notional .

We denote by the end of the -th CAT bond defined by:

| (2.1) |

Remark 2.1.

According to the definition of , it can happen that for . Moreover,

For , we say that belongs to if the condition

| (2.2) |

holds. This means that the insurer can hold a maximum of running CAT bonds simultaneously.

2.4 The CAT bonds process

We need to keep track of how many CAT bonds are running, and which parameters are associated with, in order to get a Markovian framework. A CAT bond will has its characteristics determined at , for . Moreover, a CAT bond will end from a jump or after the time-length . We need to define a process which will keep track the characteristics and the time-length elapsed. We introduce the sets , , in which

-

•

An element of the set represents the initial parameters (characteristics) of the CAT bond;

-

•

An element of the set represents the time-length elapsed of a running CAT bond;

-

•

The point represents the absence of CAT bond, it is a cemetery point.

The set of CAT bonds is

and we denote by its closure. We set and we define by the set of subsets of . We can now define the sets with :

which represent the sets of CAT bonds in which there are CAT bonds running exactly in the indexes of .

Moreover, for , we introduce:

which is the first index with no CAT bond.

For and a control , we now define the process valued in and denoted hereafter for ease of notation. The process will jump at the (new CAT bond) and at the ’s (end of one or several CAT bonds). will be a pure jump process whereas the indexes of will evolve continuously over time, recall that it represents the elapsed time-length of the CAT bonds.

We now define the functions associated with the jumps of . The first one, denoted by , represents the arrival of one new CAT bond with parameters and is defined by

such that,

| (2.3) | |||||

The second function, denoted by , represents the end of the CAT bonds by an event associated with the random Poisson measure, of severity , and is defined by

Nonetheless, several CAT bonds may end with a single event. We define the set of indexes in which end after the natural disaster , by

| (2.4) |

Using this set, is defined simply through its -component

| (2.5) |

It remains to consider the case where a CAT bond ends because for some . We define:

where, for all ,

We are now in position to define the processes and for . The process evolves at and , for , according to:

| (2.6) | ||||

in which

-

•

is the output process, defined in the next section,

-

•

with a measurable function is the coupon size. It has a common noise with and a specific noise .

Elsewhere, is constant. For , evolves according to:

This closes the definition of the process . Note that we separated both the initial parameters with the elapsed time-length since the second one will play a different role in the PDE characterization in consequence of its continuous part.

Remark 2.2.

If , the process (and also, by construction, satisfies :

We also give a metric on .

Definition 2.1.

We associate to the metric defined by

where and are respectively the set of running CAT bonds of parameters and .

2.5 The output process

We are now in position to describe the controlled state process. Given some initial data , and , we let be a strong solution on of

| (2.7) | ||||

in which

-

•

is a function which gives the total coupon associated to the CAT bonds,

-

•

is the payoff of the running CAT bonds after a natural disaster, defined by

where was defined in (2.4) and is the payoff for the end of the CAT bond according to the jump ,

-

•

is a function that gives the initial cost of issuing a CAT bond.

To guarantee existence and uniqueness of the above, we make the following standard assumptions.

Assumption 2.1.

, and , are assumed to be measurable, continuous, and Lipschitz with linear growth in their second argument, uniformly in the other ones. The maps , and are assumed to be measurable. Moreover, and have linear growth in their second component.

This dynamics means the following. Without any CAT bond, the process follows a pure jump process with a drift described by and in (2.7). In pratice, a component will be the cash. The function is the instantaneous cash flow generated by the running CAT bonds whearas the function represents the payoff of the CAT bonds that ends at the jump . The second line refers to a jump of the whole process when a CAT bond is issued, for example, for a fixed cost.

For , we shall write for the process starting with the CAT bonds . We denote by the -augmentation of the filtration generated by .

For , we say that belongs to if it is adapted. The set is the set of admissible controls. Recall that it satisfies the constraint (2.2) which refers to the fact that the controller cannot have more than simultaneous running CAT bonds at each time.

2.6 Bayesian updates

Obviously, the prior will evolve over time. Recall that and denote by the corresponding element. The observation of over time will lead to a continuous update of , whereas will be updated by observing the size of a jump from and the measure will be updated by acting on the system at times . This leads to the definition of the process valued in . We first focus on .

2.6.1 Evolution of the intensity

We start with the assumption associated with the unknown and inhomogeneous intensity of the random Poisson measure.

Assumption 2.2.

For all ,

is a càdlàg process

Given , we set for and .

From now on, we denote by the jump times associated with the random Poisson measure. We shall prove the following proposition.

Proposition 2.1.

Under Assumption 2.2, the process is

The rest of this subsection is dedicated to the proof of the above proposition. To this aim, we first describe how evolves between two jumps and after at a jump. We will need the following technical remarks.

Remark 2.3.

Remark 2.4.

Under Assumption 2.2, for all , there exists such that, for all ,

Remark 2.5.

Since a càdlàg function has at most a countable set of points of discontinuity, under Assumption 2.2 we have

| (2.8) |

for almost all .

We now describe the volution between two jumps.

Lemma 2.1.

For all and ,

where

Proof.

Let be a Borel bounded function on . Set , , and . Note that is -measurable. We can find a Borel measurable map such that

In view of Remark 2.5, it then follows:

This shows that -a.s. ∎

Lemma 2.2.

For all and almost all , we have

-

i)

-

ii)

-

iii)

Proof.

Step 1. For almost all , we fix the set of discontinuity of which is, at most, countable. We introduce:

We shall show that by showing that for all . Fix and remark that, given , the distribution of is absolutely continuous with respect to the Lebesgue measure. Denote by a corresponding density function. Then,

on . On the other hand, using Lemma 2.1,

on . This shows that, for almost all ,

This leads to the result since when for almost all .

Step 3. We show ii). Since evolves continuously on all , we also have,

Moreover, on , cannot be on a discontinuity of by construction, . Then, we have, on ,

Step 4. We show iii). We introduce:

Recall that, by construction, for all . If , . If , the distribution of is equivalent to the Lebesgue measure and then, by , we get the result. ∎

We now look at the intensity at the observation of a jump .

Lemma 2.3.

For all and ,

Proof.

We use the same notations as in the proof of Lemma 2.1.

1. For ease of notation, we set . For , we show that, with ,

| (2.9) |

where

Let be a Borel bounded function of , we can find a Borel measurable map such that

We shall write for . It then follows:

This shows that (2.9) hold -a.s.

2. For , on , by Lemma 2.2, for almost all . Using remark 2.4, by the dominated convergence theorem, we deduce that

i.e., since the law of is absolutely continuous with respect to the Lebesgue measure,

Since almost surely, , and since the law of each is absolutely continuous with respect to the Lebesgue measure, we deduce the result by a straightforward induction. ∎

2.6.2 Evolution of the parameters and

We use the notations of Section 2.6.1. We define and

.

Between two jumps of the random Poisson measure, no information about the size distribution of the jumps is revealed, and therefore, about . Whereas no information is revealed about between two jumps from our control. In this case, both processes should remain constant. At the -th Poisson jump of size , the process should evolve according to the classical Bayes rule. The process should evolve at the time of issuance of the -th CAT bond with the coupon according to, again, the Bayes rule.

Lemma 2.4.

Fix . Assume that, for almost all , the claim size distribution is dominated by some common measure . We have

in which

for almost all , in which is the conditional density, with respect to , of observing a jump of size knowing .

Moreover,

in which

for almost all , in which is the conditional density, with respect to , of observing a jump of size knowing .

Proof.

Use the same arguments as in the proof of Proposition 2.1 in [3]. ∎

2.7 Parametrization of the set

Here, we have three measures on which will depend the value function. The one associated with the distribution of the jumps of the Poisson measure (parameter ) and the one from the coupon distribution (parameter ) evolve by a finite number of jumps on each bounded interval. Those will not lead to deal with derivatives on the space of measures and a specific Itô formula nor generator of the diffusion. However, the measure associated with the intensity (parameter ) evolves continuously. To deal with this, we will assume that the associated space of measures can be linked smoothly to a subset of for some .

Assumption 2.3.

We assume that there exists an open or compact set , for some , and a function

which is a homeomorphism between and .

Remark 2.6.

The process defined by:

According to Remark 2.6, we formulate the following assumption.

Assumption 2.4.

Let be the process defined in Remark 2.6.

There exist Lipschitz maps and with linear growth (uniformly in time) such that

where we use the notation: .

Example 2.1.

Assume that there exists a càdlàg function such that for all . Set , where denotes the Gamma distribution. Then, if we define

it follows that

and satisfies Assumption 2.4.

Example 2.2.

Assume that Define, for with , the distribution by:

Set, for ,

Then and the process above satisfies the stochastic differential equation:

2.8 Gain function

Given and , the aim of the controller is to maximize the expected value of the gain functional

in which is a continuous and bounded function on .

Given , the expected gain is

and

is the corresponding value function. Note that is bounded.

3 Value function characterization

For ease of notation, we define , and for , . To , we denote by the vector in in which if , 0 else.

For and , we introduce the operator defined, for all , by:

Thus, the Dynkin operator associated with our problem with policies running in indexes is:

in which recall that denotes the size distribution of the jumps of the random Poisson measure . Moreover, we introduce:

and

Then, we expect that is a viscosity solution of, for each and non-empty ,

| (3.1) | ||||

| (3.2) | ||||

| (3.3) |

in which, for and a control such that holds with probability one,

and, for ,

| (3.4) | ||||

| (3.5) |

where .

Remark 3.1.

Note that the above corresponds to the definition of a system of PDEs linked by the common boundary conditions.

Definition 3.1.

We say that a upper-semicontinuous function on is a viscosity sub-solution of (3.1)-(3.2)-(3.3) if, for any , , and such that we have, if ,

if , for any non-empty , with and ,

and, if ,

To ensure that the above operator is continuous, we first assume that:

Assumption 3.1.

is upper- (resp. lower-) semicontinuous, for all upper- (resp. lower-) semicontinuous bounded function .

A sufficient condition for Assumption 3.1 to hold is provided in [3], see the discussion after equation (3.6).

In order to ensure that is continuous for all , we make the following assumption.

Assumption 3.2.

We assume that

-

•

The functions and are continuous ;

-

•

The stochastic kernel is continuous ;

-

•

The map is continuous.

Lemma 3.1.

Assume that Assumption 3.2 holds. Then, for all , with , and for all bounded function , the operator is continuous.

Proof.

Let and defined as above. Recall that

For the first line above, since all involved functions are continuous, the operator is continuous. For the second line, since is bounded, one easily checks that the expected value with respect to is well defined and one can apply Fubini’s theorem. This is rewritten:

with which is continuous, see [15, Proposition 7.30 p145].

Now, remark that the function integrated through with fixed is continuous by definition. Since the stochastic kernel is assumed to be continuous, we get again from [15, Proposition 7.30 p145] that the function integrated through is continuous and bounded. And then, the operator is continuous. ∎

We now assume that we have a comparison principle. A sufficient condition is provided in Proposition 5.1 below.

4 Viscosity solution properties

This part is dedicated to the proof of the viscosity solution characterization of Theorem 3.1. We start with the sub-solution property and continue with the super-solution property. The main difficulty relies on the fact that the filtration depends on the initial data. The results can be obtained along the lines of [3].

4.1 Sub-solution property

The proof of this proposition, as usual, relies on a dynamic programming principle. For this part, the dependency of the filtration on the initial data in not problematic as it only requires a conditioning argument. We have the following result:

Proposition 4.2.

Fix and , and let be the first exit time of from a Borel set containing where is a control such that . Then,

| (4.1) |

in which , .

Proof.

It suffices to follow the arguments of Proposition 4.2 in [3]. ∎

We now prove Proposition 4.1.

4.2 Super-solution property

Because of the non-trivial dependence of the filtration with respect to the initial data, in order to prove the super-solution property associated with Theorem 3.1, we shall use a discrete version of our impulse control problem, as in [3]. We shall show that the limit problem is a super-solution of (3.1)-(3.2)-(3.3). Proposition 4.1 and the comparison assumption will show that the limit problem is .

We shall use a dynamic programing principle in some discrete form defined below.

Proposition 4.3.

Fix and . Let be the subset of elements of such that the stopping times are valued in with . The corresponding value function is:

Let be such that is a -stopping time valued in . Then,

Proof.

It suffices to follow the arguments of Lemma 4.1, Proposition 4.3 and Corollary 4.1 in [3]. ∎

We now consider the limit . Let us set, for ,

Proof.

The equations (3.1) and (3.2) can be obtained by using Proposition 4.3 and following the arguments in the proof of Proposition 4.4 in [3]. We now prove the boundary condition (3.3).

Step 1. Fix and .

Let and such that . Let and define the lower semi-continuous function as in the proof of Proposition 4.4 in [3]. Then, from Proposition 4.3, with a control such that , we get for

Then, leads to

and, again from the proof of Proposition 4.4 in [3], we get that . By Fatou’s lemma we have

Step 2. Now fix and . Let and such that

We introduce . Then, for large enough, we can find such that . Then, for ,

Now, we send , since the functions in the diffusion are Lipschitz, using Fatou’s lemma leads to

Since, under the control , the processes , and are driven here by the random Poisson measure with finite activity, they satisfy the stochastic continuity property. Moreover, since the probability of observing a jump decreases to 0 when , one easily shows that,

by using the fact that is bounded and the definition of the process and after the end of one or several CAT bonds.

Step 3. In order to show the second inequality, repeat Step 1. and Step 2. using, instead of , a control such that holds with probability one.

∎

We now prove Theorem 3.1.

Proof of Theorem 3.1..

Remark 4.1.

If we denote by the set of permutation of , then, by symmetry,

for each , . From a numerical point of view, this make it easier to compute the value function.

5 A sufficient condition for the comparison

In this section, we provide a sufficient condition for Assumption 3.3 to hold.

Proposition 5.1.

Assumption 3.3 holds whenever there exists a function on such that, for each ,

-

(i)

for all ,

-

(ii)

on for some ,

-

(iii)

on for some ,

-

(iv)

on with and is defined in (ii),

-

(v)

for all ,

-

(vi)

as for some .

Proof.

Step 1. As usual, we shall argue by contradiction. We assume that there exists some and some such that , in which is a sub-solution of (3.1)-(3.2)-(3.3) and is a super-solution of (3.1)-(3.2)-(3.3). Recall the definition of and in Proposition 5.1. We set and for all for all . Then, there exists such that

| (5.1) |

in which . Note that and are sub and super-solution on of

for each , with the boundary conditions

| (5.2) |

and

| (5.3) |

Step 2. Let be a metric on compatible with the weak topology. For , we set :

| (5.4) | ||||

with small enough such that . Although is not closed, note that the supremum is achieved for some by some . This follows from the upper-semicontinuity of , the fact that and are bounded from above, and by the fact that

For , we set

Again, there is such that

It is standard to show that, after possibly considering a subsequence,

| (5.5) | ||||

see e.g. [6, Lemma 3.1]. Moreover, up to a subsequence, there exists , such that, for all , and .

Step 3. We first assume that, up to a subsequence, , for . Then, it follows from the supersolution property of and Condition (iii) that

Passing to the and using (5.5) and (3.1), we obtain

Now let us observe that

| (5.6) | ||||

in which the last identity follows from (5.5). Combined with the above inequality, this shows that , which leads to a contradiction for small enough.

Step 4. We now show that there is a subsequence such that for all . If not, one can assume that . If, up to a subsequence, one can have , then it follows from (5.2) and Condition (iv) that,

Hence,

and (5.5) with (5.6) leads to , a contradiction. If, up to a subsequence, , by (5.2) and Condition (iv),

Hence,

and combining Assumption 3.1 with (5.5) and (5.6) leads to , the same contradiction.

Step 5. In view of step 2, 3, 4, one can assume that , and for all . Using Ishii’s Lemma and following standard arguments, see Theorem 8.3 and the discussion after Theorem 3.2 in [6], we deduce from the sub- and supersolution viscosity solutions property of and , and the Lipschitz continuity assumptions on and , that

for some , independent of and . In view of (5.4) and (5.5), we get

| (5.7) |

We shall prove in next step that the right-hand side of (5.7) goes to 0 as , up to a subsequence. Combined with (5.6), this leads to a contradiction of (5.1).

Step 6. We conclude the proof by proving the claim used above. First note that we can always construct a sequence such that

By (5.5), . Hence, .

∎

6 Numerical Scheme

We let be a time-discretization step such that both and are an integer. In order to ensure the existence of such a , we shall assume that which does not appear as a restriction from a practical point of view. We set and, for , we set in which .

The space is discretized with a space step on a rectangle containing points on each direction. The corresponding set is denoted by . Recall that is a subset of . We again discretise with the same step space on a rectangle containing points. The corresponding set is denoted by , thus, the discretization of is .

We set . The first order derivatives , , and are approximated by using the standard up-wind approximations:

in which is unit vector of .

We shall assume that is finite. We introduce:

in which .

Then, the discrete counter-part of the set of policies running in indexes is defined by

We introduce:

in which is completely determined by , recall Assumption 2.3.

Note that, for , we may have . One needs to approximate with the closest points in . We have the same issue with . We define as an approximation of by

in which (resp. ) denotes the corners of the cube of (resp. ) in which (resp. ) belongs too and is a weight function.

Moreover, in order to integrate the boundary condition when for some , we define and . We introduce

And finally,

The discrete counterpart of for all is

| (6.1) | ||||

If correspond to a discret distribution, the corresponding integral is explicit. In the examples in next section, we shall use a discrete approximation.

For the sequel, we set a control such that a.s. and a control such that a.s. and a.s. for . Thus, the discrete counterpart of is

| (6.2) |

We set , and . Our numerical scheme consists in solving, for all :

| (6.3) | |||||

| (6.4) | |||||

| (6.5) |

7 Example: CAT bonds in a per event framework for Hurricanes in Florida

We focus on a simple example where the controller is an insurance or a reinsurance company which can issue CAT bonds in order to cover its risk in natural disasters.

We consider CAT bonds of per event type. The framework is the following:

-

•

The studied risk is the hurricanes ;

-

•

We only consider one region : Florida ;

-

•

The time-unit will be the year and we fix which corresponds to the average maturity of CAT bonds in years ;

-

•

The insurer can issue CAT bonds on different layers.

The motivation of considering hurricanes in Florida comes from the fact that this region is well exposed, about one hurricane every two years in average, see [12] ; and has an important and increasing insured value about 4000 billion in 2015, see [16]. Therefore, it has been well studied and we will take the parameters of our toy model from different papers.

We consider a 1-dimension random Poisson measure , which represents the intensity of arrival and the severity of hurricanes. Only the intensity of arrival of the hurricanes is unknown. We use two different priors. The first one is the case with a Gamma distribution on the unknown parameter. The second one is the case with a Bernoulli distribution.

This leads to two different definitions of the intensity that we first explain in subsection 7.1 and 7.2. We describe in subsection 7.3 the severity of the hurricanes, which is assumed to be known. In subsection 7.4, we give the set of controls (which kind of CAT bonds the insurer can issue) and the output process (the process defined in equation (2.7)). In subsection 7.5 we describe the gain function and a specific dimension reduction that can be used for the numerical implementation. In subsection 7.6, we fix and explain the numerical values chosen for the parameters of the control problem. The numerical results are presented in subsection 7.7. Finally, we discuss in subsection 7.8 about the benefits and the limits in practice of this approach for a decision making process.

7.1 Intensity of Hurricanes: the Gamma case

We define the intensity as the function:

in which is a positive continuous function which represents the seasonality of the arrival of hurricanes and some growth according to the global warming. The parameter , which is unknown, represents a level of intensity.

We set with as an initial prior on . Thus, by Example 2.1, we deduce that the process , starting from at , remains in the family of Gamma distributions and, for all ,

Moreover, we can define two processes and :

and, by construction, .

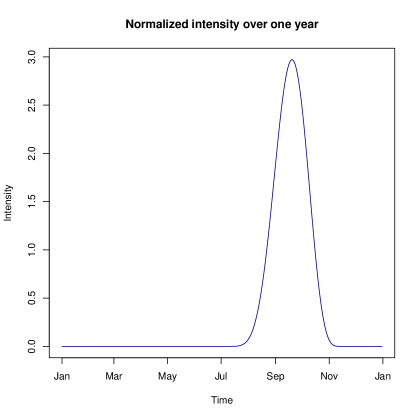

It remains to define the function . The seasonality of hurricanes has been studied, especially on big Hurricanes, in [14] in which the authors give a curve based on a kernel density estimation. One close parametric density function over one year can be found in the form:

| (7.1) | ||||

| (7.4) |

in which is the density function of the Beta distribution of parameters .

The function is simply defined by for , in which is the integer part function. is 1-periodic. Here we do not consider a global warming effect, which would have been deterministic through the function .

7.2 Intensity of Hurricanes: the Bernoulli case

Although the Gamma prior gives parameters that belongs in , in order to remains in the Gamma distribution over time, it requires the form and then the intensity of the whole period is proportional to . We introduce a Bernoulli case with three alternatives in which we can choose any function depending on time with each alternative.

With the integer part function, we define the intensity as:

| (7.5) |

in which the parameter represents 3 scenarios of the evolution of the intensity, as a consequence of the global warming.

Following Example 2.2, we can define 3 processes, starting from at time :

| (7.6) |

7.3 Severity of the Hurricanes

As in [12], we use a Generalized Pareto Distribution for the simulation of the severity of the claim, over the exposure of 4000 billion. Their threshold (minimum claim size) is billion for an exposure of 2000 billion. Here, we shall use: , and . To fix ideas, the median is 4.5 billion, the quantile at 90% is 22 billion and the quantile at 99.5% is 132 billion. We also bound the distribution by the total exposure of 4000 billion.

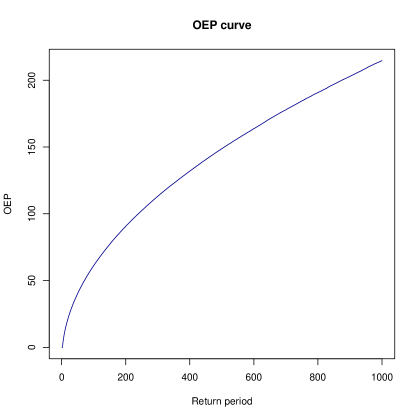

We also introduce the so-called Occurrence Exceedance Probability (OEP) curve. To this aim, we introduce the random variable:

which is the greatest Hurricane in for . The OEP curve is simply:

in which is called the Return period. By construction, is the quantile of order of .

The Figure 7.2 shows the corresponding OEP curve with the Gamma prior .

We now define the set of controls and the output process.

7.4 The set of controls and the output process

Recall that a control has the form . Here, is the linked to the notional of the CAT bonds. A CAT bond covers a layer (defined hereafter) of the portfolio of the insurer. We fix for simplicity, so if the insurer issue a CAT bond, the whole corresponding layer will be covered.

We introduce . We define what will be the capacity of the CAT bonds: for and .

The value can be chosen in and the associated sets are defined by:

If a Hurricane leads to a cost in , then the default of the CAT bond is activated. It remains to define the payout for the insurer in the default case. It corresponds to cover the layer at a ratio of . We define the payout of the CAT bonds as:

Note that, in our example, the risk cannot be covered above the return period of 1000.

We consider the process valued in . The first component represents the cash of the Insurer/Reinsurer and the second component represents the risk premium, in term of percentage of the pure premium, of the market about the CAT bonds, defined later.

We set, with :

in which:

-

•

represents the premium rate, the insurer is profitable if ;

-

•

is the constant interest rate ;

-

•

is the speed return to 0 of the risk premium of the CAT bonds ;

-

•

is an increasing function which represents the immediate increase of the premium rate after a claim ;

-

•

is the initial cost of issuing a CAT bond.

How the coupon is fixed when issuing a CAT bond and is defined in subsection 7.6.

7.5 Gain function and dimension reduction

The controller wants to maximize, with , for some , the criteria

The right part inside the exponential function compensates the initial cost for remaining CAT bonds, in order to avoid particular behaviors of issuing nothing close to the end. We take which ensures that is bounded and big enough such that it will not play an essential role.

Note that in the Gamma prior case, we have which is a function of time with no randomness. Then, we can avoid it in the numerical scheme since it is a function of time fully characterized by the initial prior.

In the Bernoulli case, one can see that, if we set for the prior

for some , then, for all , we have and then . One can normalize such that the sum is 1 and avoid the last component.

Moreover, the associated value function satisfies:

which avoids in computation the dimension of .

7.6 The choice of the parameters

We choose here the form, the functions and the parameters for our toy example. We first describe the Gamma case (for the prior) and then describe the Bernoulli case.

Just after the occurrence of Katrina, the price of the reinsurance was about two or three times greater with a persistence of about two years and can be also seen on the CAT bond market, see Figure 9 in [8]. Thus, we set

Moreover, the estimated return-period of such event is about -year return period, see [11]. Since the increase was about two of three times greater, we set

in which denotes the cumulative distribution function of the Pareto distribution of parameters . Then, here, for a return period of 40 years (recall that we have in average one claim each 2-year period), it gives an increase of 100% of the price.

The insurer has a market share of that we fix at 10%. We shall assume that, the insurer is profitable until . Then, the premium rate is

We now define the coupon fixing. If with (recall that is the choice of the layer for the CAT bond), the coupon is:

| (7.7) |

Thus, the CAT bond price is decomposed by:

-

•

The part which is the probability that a claim is above the layer within one year and then the payout is the layer

-

•

The part which is the probability that the greatest claim is in the layer, and we multiply it by one half like if it was uniformly distributed in the layer, which is greater than the true value.

-

•

The factor is the risk aversion of the market, and is some random value about the price the coupon.

Finally, the cost of issuing a CAT bond is fixed at: , the interest rate is fixed at .

Remark 7.1.

In these examples, we deal with per event CAT bonds. One also can deal with aggregated losses within the period. In this case, it requires to record the current accumulation of claims and to introduce another dimension in the output process .

Remark 7.2.

In practice, in general, a partial default below 70%-80% of the capacity does not end the CAT bonds: the coupon is reduced by the proportional loss and another loss may lead to the complete default, using the same limits. Here, for simplification, the CAT bond ends whenever the layer is attained.

Remark 7.3.

Note that the function satisfies the conditions of Proposition 5.1, for great enough.

7.6.1 With the Bernoulli prior

To be consistent, we say that the premium rate also rises over time following the rise of intensity, but by 35%, and then is:

We assume that the market is updating the OEP with the same rate:

7.7 Results

Recall that, for each CAT bond that the insurer can issue, we need to add its characteristics and the complexity increases hugely in , depending on possible policies. Thus, in our simulation, we use . The controller can choose at most 2 layers among the three available (recall them in term of return periods: [10, 50], [50, 200] and [200, 1000] which corresponds to [1.23, 4], [4, 9], and [9, 21.5] in billion dollars).

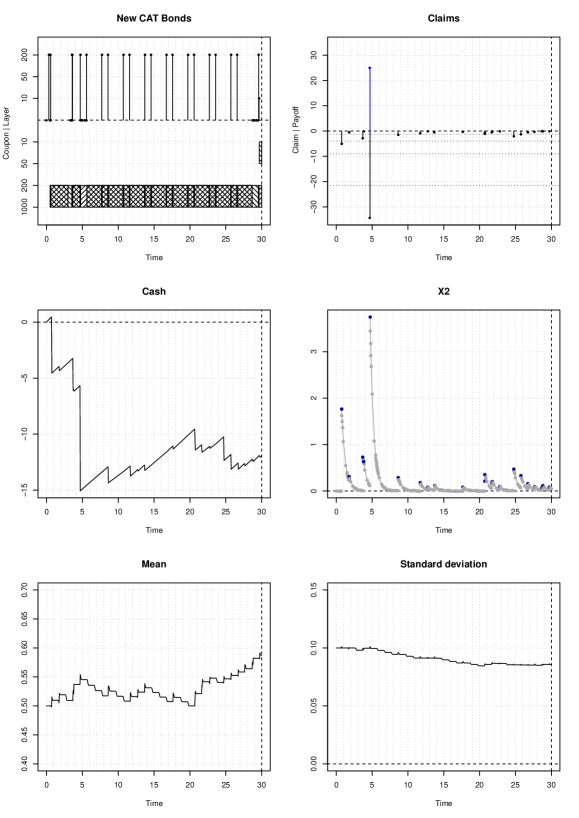

7.7.1 With the Gamma prior

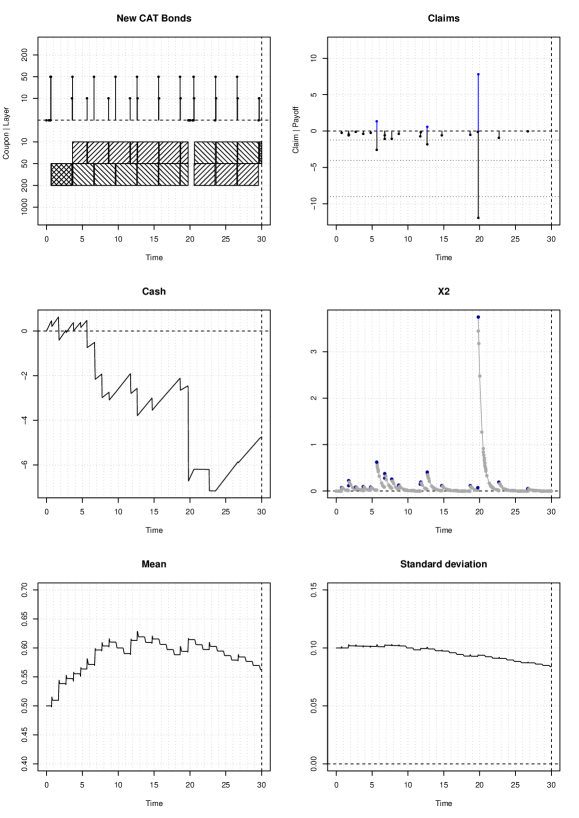

In Figure 7.3, we provide a simulated path of the optimal strategy in which the Pareto distribution is discretized in 2500 points (the highest possible value is 49 billion dollars). The top left graphic describes the control played by the insurer. The top part represents the issue of CAT bonds, the level is the lower bound of the layer. The bottom part represents the running CAT bonds with respect to the layer. The double dash says that two CAT bonds at the same layer are running. The top right graphic describes the arrival of natural disasters. The bottom part gives the size of the claim of the insurer while the top part gives the payoff of the CAT bond(s). The middle left graphic describes the evolution of the cash of the insurer. The middle right graphic gives the evolution of , the price penalty of the CAT bonds which appears in (7.7). The bottom left graphic gives the evolution of the mean of the estimated distribution of (true value is 0.6), defined by , and the bottom right graphic gives the evolution of the standard deviation, defined by .

At the beginning, the insurer does not issue any CAT bond. Since we start in January, there is no risk to experiment a claim and thus the insurer delays the issue. Just when the season starts, he first chooses to issue two CAT bonds on the layer . Recall that it is the highest layer which corresponds to in billion dollars. It is possible to have a claim highly above the layer and having a double cover on this big layer gives, indirectly, a cover against huge claims above the layer (recall that the maximum claim size is 49 billion dollars). He renews each CAT bond at the maturity until he meets a claim with a return period above 1000 during the year. He gets the associated payoff. Despite the huge increase of the price of CAT bonds, by almost , he immediately issues a new one on the layer [200, 1000], but only one. He waits the next season, with a better expected price, to issue the other one. After, he follows this strategy to the end.

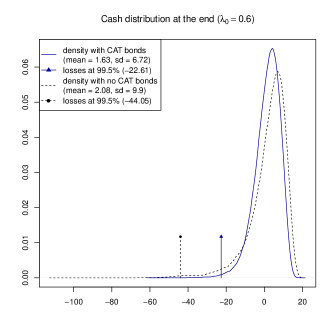

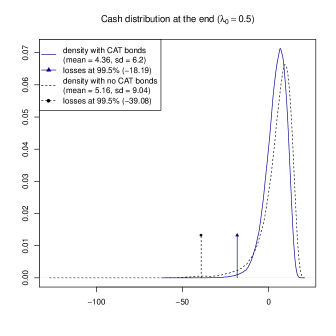

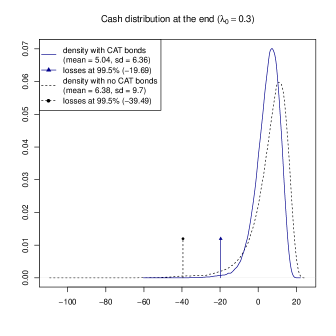

In Figure 7.4, we represent the approximated density (by kernel estimation) of the total cash of the insurer at the end of the 30 years. On the left, it is the case with ( the value used in the simulated path of Figure 7.3) and on the right with , i.e. what believes the insurer at the beginning. The solid curve is the case when the insurer plays the optimal control and the dashed curve is when he never issues any CAT bond. We also add the quantiles at 99.5% in term of losses, see the legend. In the case with (left), from which the path in Figure 7.3 comes from, we can see that the standard deviation is reduced. And the quantile at 99.5% is strongly reduced. One can observe that the case strongly reduces the expected net return in average.

We now look at the case with a discretization of 500 of the Pareto distribution. In particular, the maximum claim size is 21.4 billion which does not exceed the maximum layer . In Figure 7.5, we show a simulated path. This time, the insurer chooses to get two CAT bonds at the layer . Actually, with this discretization, the layer appears to be less competitive since the discretization of 500 leads to a lower expected payoff. In the first years, the expected intensity is revised higher and the relative price of the layer decreases (this layer requires the highest coupon since it is frequently hit). At the year, he changes his strategy and gets one CAT bond on the layer and the other one on the layer . A catastrophe above the return period of 200 occurs at the year and both CAT bonds end. He prefers to wait the next season because of the consecutive price increase. Note that, in the previous cases (with Pareto distribution discretized in 2500 points), he was never without any CAT bond, even after an increase of . Then, he continues his strategy to get a CAT bond on the layer and the other one on the layer , until the end.

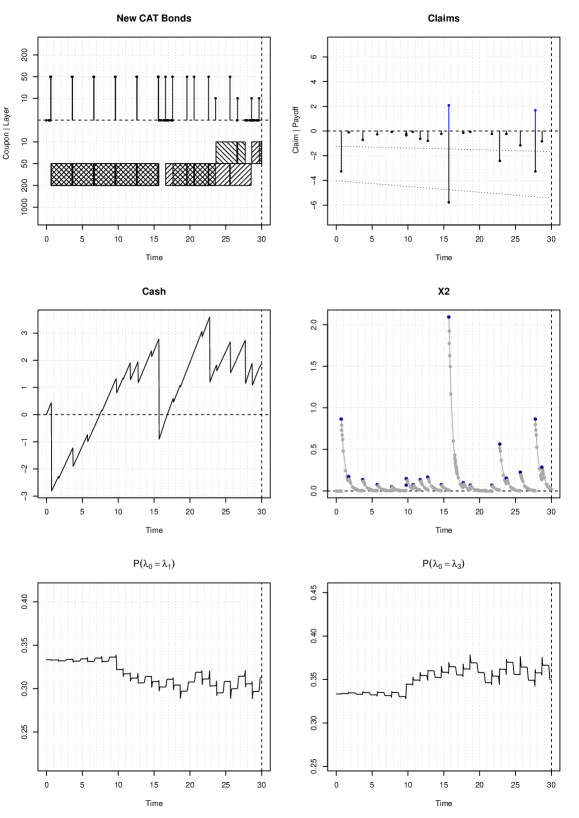

7.7.2 With the Bernoulli prior

In Figure 7.6, we provide a simulated path of the optimal strategy in which the Pareto distribution is discretized in 2500 points (recall that the highest possible value is 49 billion dollars). As in the Gamma prior case, the insurer chooses to get two CAT bonds at the highest layer. When he experiences a huge claim during the second year, he still gets twice the layer but prefers to wait before to take a new CAT bond, according to the huge rise of the price. He waits the next year and restarts the same strategy until the year. Then, he issues CAT bonds on the layer and until close to the end.

The estimated probabilities on evolve slowly at the beginning since has an impact which rises over time.

In Figure 7.7, we represent the approximated density (by kernel estimation) of the total cash of the insurer at the end of the 30 years. On the left, it is the case with (as it is also the case in Figure 7.3) and on the right with . The legend is the same as in Figure 7.4 and we get close distributions.

We now look at the case with a discretization of 500 of the Pareto distribution and show a simulated path in Figure 7.8. As in the Gamma prior case, at the beginning, the insurer chooses to get two CAT bonds at the layer . He follows this strategy until he meets a huge claim in the year. He waits the next season and restarts the same strategy. At the year, he chooses to issue CAT bonds on two different layers, at and . As in Figure 7.5, this results in a change on the belief on the intensity.

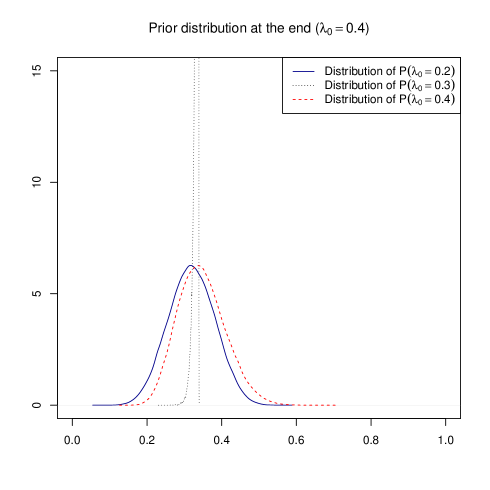

Finally, in Figure 7.9, we display the distribution of the probabilities on . This highlights the fact that it is very difficult to estimate it with observations through time.

7.8 Benefits and limits

The framework given is quite general. In addition to CAT bonds, it could handle reinsurance treaties and to choice between them. It also tackles some lack of information about some parameters or their evolution, and the framework is adaptive. Corresponding to the expected prices on the CAT bond market for each layer, it could help in a decision process by telling which CAT bonds to issue and at which notional.

Nonetheless, the curse of dimensionality is important, especially in the number of CAT bonds and their admissible characteristics. Adding the ability to hold one more CAT bond ask to up the dimension by its characteristics and the time-length elapsed. The uncertainty on one parameter also requires at least one dimension for the prior evolution. The most heavy example provided, from a computing time point of view, is the Bernoulli case with the Pareto Distribution discretized by 2500. On a Ryzen 7 1800X (8 cores, 16 threads, at 3.6 Ghz), with a program written in C++ completely multi-threaded, it takes around 120 hours (5 days) in order to compute the optimal control of this example. In practice, it appears complicated to use without restriction, and one should consider each peril / region separately.

References

- [1] ARTEMIS. Q4 2017 catastrophe bond & ils market report. Technical report, 2018.

- [2] Nicolas Baradel, Bruno Bouchard, and Ngoc Minh Dang. Optimal trading with online parameter revisions. Market microstructure and liquidity, 2(03n04):1750003, 2016.

- [3] Nicolas Baradel, Bruno Bouchard, and Ngoc Minh Dang. Optimal control under uncertainty and bayesian parameters adjustments. SIAM Journal on Control and Optimization, 56(2):1038–1057, 2018.

- [4] Guy Barles and Panagiotis E Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic analysis, 4(3):271–283, 1991.

- [5] Guy Carpenter. Catastrophe bond update: Fourth quarter and full year 2015. Technical report, 2016.

- [6] Michael G Crandall, Hitoshi Ishii, and Pierre-Louis Lions. User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American Mathematical Society, 27(1):1–67, 1992.

- [7] J David Cummins. Cat bonds and other risk-linked securities: state of the market and recent developments. Risk Management and Insurance Review, 11(1):23–47, 2008.

- [8] J David Cummins. Cat bonds and other risk-linked securities: product design and evolution of the market. The Geneva Reports, 39, 2012.

- [9] David Easley and Nicholas M Kiefer Controlling a stochastic process with unknown parameters. Econometrica: Journal of the Econometric Society, 1045–1064, 1988.

- [10] Onésimo Hernández-Lerma Adaptive Markov control processes. Springer Science & Business Media, 79, 2012.

- [11] Robert William Kates, Craig E Colten, Shirley Laska, and Stephen P Leatherman. Reconstruction of new orleans after hurricane katrina: a research perspective. Proceedings of the national Academy of Sciences, 103(40):14653–14660, 2006.

- [12] Jill Malmstadt, Kelsey Scheitlin, and James Elsner. Florida hurricanes and damage costs. southeastern geographer, 49(2):108–131, 2009.

- [13] Kazuyoshi Oouchi, Jun Yoshimura, Hiromasa Yoshimura, Ryo Mizuta, Shoji Kusunoki, and Akira Noda. Tropical cyclone climatology in a global-warming climate as simulated in a 20 km-mesh global atmospheric model: Frequency and wind intensity analyses. Journal of the Meteorological Society of Japan. Ser. II, 84(2):259–276, 2006.

- [14] Francis Parisi and Robert Lund. Seasonality and return periods of landfalling atlantic basin hurricanes. Australian & New Zealand Journal of Statistics, 42(3):271–282, 2000.

- [15] S.E. Shreve and D.P. Bertsekas. Stochastic optimal control: The discrete time case. Athena Scientific, 1996.

- [16] AIR Worldwide. The coastline at risk: 2016 update to the estimated insured value of u.s. coastal properties. Technical report, 2016.