Randomization Tests for Weak Null Hypotheses in Randomized Experiments

Abstract

The Fisher randomization test (FRT) is appropriate for any test statistic, under a sharp null hypothesis that can recover all missing potential outcomes. However, it is often sought after to test a weak null hypothesis that the treatment does not affect the units on average. To use the FRT for a weak null hypothesis, we must address two issues. First, we need to impute the missing potential outcomes although the weak null hypothesis cannot determine all of them. Second, we need to choose a proper test statistic. For a general weak null hypothesis, we propose an approach to imputing missing potential outcomes under a compatible sharp null hypothesis. Building on this imputation scheme, we advocate a studentized statistic. The resulting FRT has multiple desirable features. First, it is model-free. Second, it is finite-sample exact under the sharp null hypothesis that we use to impute the potential outcomes. Third, it conservatively controls large-sample type I error under the weak null hypothesis of interest. Therefore, our FRT is agnostic to the treatment effect heterogeneity. We establish a unified theory for general factorial experiments and extend it to stratified and clustered experiments.

Key Words: Causal inference; Finite population asymptotics; Potential outcomes; Randomization-based inference; Sharp null hypothesis; Studentization

1 Introduction to the Fisher Randomization Test in Experiments

1.1 Literature Review

Randomization is the cornerstone of statistical causal inference (Fisher 1935, Section II). It creates comparable treatment groups on average. More fundamentally, it justifies the Fisher randomization test (FRT). Under Fisher’s sharp null hypothesis, the treatment does not affect any units whatsoever, and the distribution of any test statistic is known over all randomizations (Fisher 1935; Rubin 1980; Rosenbaum 2002b; Imbens and Rubin 2015). Therefore, the FRT delivers a finite-sample exact -value. What is more, many parametric and non-parametric tests are approximations to the FRT (Eden and Yates 1933; Pitman 1937; Kempthorne 1952; Box and Andersen 1955; Collier and Baker 1966; Bradley 1968; Lehmann 1975).

Another formulation of the FRT relies on exchangeability of outcomes under different treatments (Pitman 1937; Hoeffding 1952; Romano 1990). They called this formulation a “permutation test”. Kempthorne and Doerfler (1969) accentuated the importance of the treatment assignment mechanism to justify the FRT, without assuming that the outcomes are exchangeable. Rubin (1980) extended the FRT using Neyman (1923/1990)’s potential outcomes. He defined a null hypothesis to be sharp if it can determine all missing potential outcomes. One of his insights was that any test statistic has a known distribution under a sharp null hypothesis, and therefore the FRT is finite-sample exact.

Randomized experiments are increasingly popular in the social sciences (Duflo et al. 2007; Gerber and Green 2012; Imbens and Rubin 2015; Athey and Imbens 2017). In such applications, testing sharp null hypotheses may not answer the researchers’ queries. They often want to test weak null hypotheses that the treatment has zero effects on average. The ideal testing procedure must leave room for treatment effect heterogeneity. Unfortunately, weak null hypotheses cannot determine all missing potential outcomes, even though the distributions of test statistics depend on them in general. Consequently, simple FRTs may not be directly applicable for testing weak null hypotheses.

Having the FRT test weak null hypotheses is a delicate task. Although sometimes we can still wield the same FRTs, we need to modify the interpretations when the null hypothesis is not sharp (Rosenbaum 1999, 2001, 2003; Caughey et al. 2017). Not all FRTs can preserve type I errors for weak null hypotheses even asymptotically. The famous Neyman–Fisher controversy ties into this issue for randomized block designs and Latin square designs (Neyman 1935; Sabbaghi and Rubin 2014). Gail et al. (1996) and Lin et al. (2017) gave empirical evidence from simulations, and Ding and Dasgupta (2018) gave a theoretical analysis of the one-way layout. Two strategies exist for using FRTs to test weak null hypotheses. The first strategy realizes that weak null hypotheses become sharp given appropriate nuisance parameters. It maximizes the -values over all values of the nuisance parameters or their confidence sets (Nolen and Hudgens 2011; Rigdon and Hudgens 2015; Li and Ding 2016; Ding et al. 2016). However, it can be computationally expensive and lacks power when the nuisance parameters are high dimensional. The second strategy uses conditional FRTs. It relies on partitioning the space of all randomizations, and in some subspaces, certain test statistics have known distributions under the weak null hypotheses (Athey et al. 2018; Basse et al. 2019). It can be restrictive and is not applicable in general settings.

1.2 Our Contributions

We propose a strategy for testing a general hypothesis in a completely randomized factorial experiment. The null hypothesis asserts that certain average factorial effects are zero. It is therefore weak and cannot determine all missing potential outcomes. Our strategy has two components.

First, we specify a sharp null hypothesis. It must imply the weak null hypothesis being tested and be compatible with the observed data. Treatment-unit additivity holds under this sharp null hypothesis. In particular, it implies constant factorial effects of and beyond the weak null hypothesis. Under this sharp null hypothesis, we can impute all missing potential outcomes.

Second, we use the FRT with a studentized test statistic. Like other test statistics, its sampling distribution depends on unknown potential outcomes in general. Thus, this distribution is outside our grasp. Fortunately, the FRT generates a proxy distribution under the above sharp null hypothesis. This proxy distribution stochastically dominates the unknown one asymptotically. The stochastic dominance relationship between them enables us to construct an asymptotically conservative test. Therefore, for testing the weak null hypothesis, we recommend the FRT with the studentized statistic. Barring studentization, the FRT may not control type I error even asymptotically. We examine several existing test statistics that exhibit this unwanted behavior.

The idea of studentization already surfaces in the literature. Neuhaus (1993), Janssen (1997), Janssen (1999), Janssen and Pauls (2003) and Chung and Romano (2013) conducted permutation tests with studentization. These tests assumed that the outcomes are independent draws. In our formulation, the random treatment assignment drives the statistical inference on fixed potential outcomes. We do not assume any exchangeability of outcomes.

In this particular setting, our theory transmits many new features. First, the sampling distribution of the studentized statistic is not asymptotically pivotal, unlike in an independent samples setting. Rather, the approximate distribution generated by the FRT is. Second, the FRT is conservative for the weak null hypothesis. This aspect of finite-population causal inference (Neyman 1923/1990; Imbens and Rubin 2015) was absent in the literature on permutation tests. Third, studentizaion helps us achieve better first order accuracy, i.e., to control asymptotic type I error. Babu and Singh (1983) and Hall (1988), on the other hand, used it for better second order accuracy in the bootstrap.

The bootstrap is another resampling method for testing weak null hypotheses. Relative to the bootstrap, FRTs have an additional advantage of being finite-sample exact under sharp null hypotheses. Although the bootstrap has been a workhorse for many other statistical problems, Imbens and Menzel (2018) recently fused its ideas with finite population causal inference.

1.3 Organization and Notation

Let us preview how the rest of the paper is organized. Section 2 lays out the potential outcomes framework, FRTs, and the null hypotheses of interest. Section 3 formalizes what kind of test statistic can be used with the FRT to test weak null hypotheses. It then gives our advocated test statistic that meets the criterion, and also other popular test statistics that do not. Section 4 gives various examples of special cases covered by our results in Section 3. Section 5 shows how our results, with some modifications, can be extended to other classes of experiments. Section 6 uses simulations to look at the finite sample behavior of the FRT with studentization, complementing our asymptotic theory. Section 7 demonstrates further the application of our results by using data from real-world randomized experiments. Section 8 wraps up our paper. The online supplementary material has the proofs for all of our results.

Let and be vectors of ’s and ’s, respectively. Let denote the indicator that an event happens. Let and if is positive semi-definite and positive definite, respectively. Write if . For a diagonalizable matrix , let be its -th largest eigenvalue. Let diag be a diagonal or block-diagonal matrix. If is a sequence of random variables indexed by , write , , for convergence in distribution, probability, and almost surely (often abbreviated “a.s.”), respectively. For convergence in probability, we may also write . For random vectors or matrices, the same notation denotes such convergence, entry by entry. Let denote the set of permutations of . Let denote a generic element of , which is a mapping from to itself. Let Unif denote the uniform distribution over . Random variable stochastically dominates , written , if their cumulative distribution functions and satisfy for all . Let be independent and identically distributed (i.i.d.) random variables.

2 Framework

2.1 Completely Randomized Experiments

We adhere to the potential outcomes framework (Neyman 1923/1990; Rubin 1974). Let be the response of unit if it receives treatment , where and . Vectorize . The means of the potential outcomes are , vectorized as . The covariance between the potential outcomes is , which is a variance if . The covariance matrix has the -th entry .

Let represent the treatment that unit actually receives, and define the indicator . The are generated according to a completely randomized experiment (CRE). The experimenter picks that sum to , and assigns treatments randomly so that any realization satisfies for , and has probability .

Unit ’s observed outcome is . So the observed means are , vectorized as . The observed variances are , which is the sample analog of . Because and are not jointly observable, there is no sample analog for . In general, we cannot estimate consistently for . For regularity, we assume and for all .

2.2 Fisher Randomization Tests

The Fisher Randomization Test (FRT) was formulated by Fisher (1935) to analyze experimental data. Several flavors of it exist (Pitman 1937; Hoeffding 1952; Basu 1980; Romano 1990). We adopt that of Rubin (1980). It arises from the potential outcomes described in Section 2.1.

Rubin (2005) called the potential outcome matrix the Science Table. He termed a null hypothesis sharp if it, along with the observed data, can determine all the missing items in the Science Table. A test statistic is a function of the observed data and the null hypothesis. Under a sharp null hypothesis, any test statistic has a known distribution. In particular, we can cycle through the possible values of , and for each obtain the corresponding realization of observed data, and then compute the value of the test statistic. In this manner, the test statistic’s distribution becomes accessible, as does a -value. FRTs are therefore finite-sample exact for testing sharp null hypotheses, no matter the test statistic or data generating process for the potential outcomes (Rosenbaum 2002b; Imbens and Rubin 2015). In essence, randomization is fundamental for statistical inference. It justifies the FRT, and guarantees the validity of the resulting -value.

Practitioners typically brand sharp null hypotheses as too restrictive. In a general factorial experiment, our mission is to test

| (1) |

where and is a full row rank contrast matrix, i.e., . We pay extra attention to hypotheses where , but study general for completeness. A weak hypothesis is any that is not sharp by the definition of Rubin (2005). The hypothesis (1) is therefore weak. It is also referred to as an average/Neyman null hypothesis. It only confines the averages of the potential outcomes. Meanwhile, a sharp/strong/Fisher null hypothesis confines all individual potential outcomes.

Notwithstanding that the FRT is designed for sharp null hypotheses, we ask whether it can test (1) also. The FRT mandates that all potential outcomes be filled out. We do so aided by an artificial sharp null hypothesis. A sensible one is

| (2) |

where the matrix is invertible. When , and are empty, as already form an invertible square matrix. When , we can construct from and by Gram–Schmidt orthogonalization. We are then to select . Whatever we select here does not matter asymptotically, as we see later. For null hypotheses (1) where , we can go with to get the classical sharp null hypothesis of no individual effects whatsoever. Intuitively, the piece of (2) is “of” the weak null hypothesis (1), and the piece is “beyond” it. The hypothesis (2) induces two key features. The first is the weak null hypothesis (1). The second is strict additivity, i.e., does not depend on the unit , for .

With the sharp null hypothesis (2) and some test statistic that ideally can capture possible deviation from (2), the FRT proceeds as follows.

-

FRT-1.

Calculate from .

-

FRT-2.

Impute potential outcomes:

or, equivalently, .

-

FRT-3.

For a permutation , compute and calculate from the same way was calculated.

-

FRT-4.

The -value is .

As a sanity check, the imputed potential outcomes in FRT-2 satisfy (2) and for all . Given the Science Table, every realization of treatment assignment produces data . Henceforth, we call the values of that can possibly emerge from these data the sampling distribution of . Conditioning on the original data , we can fill out missing potential outcomes with FRT-2. We call the set of values defined in FRT-3 the randomization distribution of . Since this distribution depends on the original data, whose randomness comes solely from , we denote this distribution by .

Under the sharp null hypothesis that the treatment truly does not affect any unit whatsoever, the FRT just described reduces to the classical permutation test. In particular, in FRT-2, all potential outcomes are equal to the observed outcome , and in FRT-3, we just need to permute the treatment assignment because for every unit . Under this sharp null hypothesis, the FRT and permutation test are numerically identical. There is an isomorphism between the two in this sense. In general, the FRT admits a broader class of null hypotheses and experimental designs than the permutation test.

Step FRT-4 conveys that the FRT -value is a right-tail probability. A larger value of embodies a larger deviation from the null hypothesis. Even if is too large for a manageable exact computation of the -value, we are able to fall back on random i.i.d. draws from to approximate the -value in FRT-4 subject to Monte Carlo error. We are thus always at liberty to sample randomly from the randomization distribution.

For any test statistic , the -value in FRT-4 is valid under (2). Our overarching goal is to investigate whether the FRT can still control type I error for testing . Roughly speaking, this turns out to be affirmative asymptotically granted an appropriate test statistic . Before continuing, let us be specific that the FRT with conservatively controls type I error at level if . In words, the true probability of a conservative test incorrectly rejecting the null hypothesis is never greater than the nominal significance level. For conciseness, when we say a test controls type I error, we do not always mention explicitly that it does so conservatively.

2.3 Asymptotics for Finite Population Inference

We have contended that the exact sampling distribution of depends on unknown potential outcomes under in general. Instead of finite sample theory, we embrace an asymptotic theory. This gives us a feasible approximation to the sampling distribution of . Imagine a sequence of finite populations of potential outcomes. For each , we fix in advance . Independently across , we generate according to a CRE, from which we get and calculate a test statistic. We denote a sequence indexed by with by or . Technically, we should index finite population quantities by , and also index observed quantities by . For cleaner notation, and with a nod to the precedent of earlier authors, we drop these extra subscripts, unless to emphasize the dependence on . We now state our assumptions on the sequence of potential outcomes.

Assumption 1.

The sequence converges to for all . The sequences and converge to and , where has finite entries and positive main diagonal entries. Further, .

Assumption 2.

Same as Assumption 1 except the last sentence is replaced by: Further, there exists an such that for all and .

The design of experiments often guarantees the existence of because all treatment groups have comparable sizes in realistic scenarios. We can weaken the existence of and by standardizing the potential outcomes. Just as we drop , we might drop subscripts . For instance, can mean either the finite population covariance matrix or its limiting value, which will be clear from context. Intuitively, Assumption 1 requires more than two moments, and Assumption 2 requires four moments. Assumption 2 is thus stronger than Assumption 1. Below are our principal asymptotic tools, which are consequences of Li and Ding (2017).

Proposition 2.

Under Assumption 1, , and .

Proposition 3.

Under Assumption 1, , where

| (3) |

The limiting distribution in Proposition 3 depends on unknown quantities. We need to estimate . This covariance, however, depends on (), which do not have unbiased estimators in general. Prompted by Neyman (1923/1990), we estimate the main diagonal by:

Proposition 2 implies

| (4) |

Because , the estimator is asymptotically conservative for in the sense that . We will encounter this notion time after time. Aronow et al. (2014) brings up tight bounds for covariance estimation in treatment-control randomized experiments with . Their results suggest that we can further improve the estimator . Nevertheless, we will show that suffices for our goal of testing (1) with FRTs.

3 Test Statistics

We return to our main endeavor: whether the FRT with a test statistic can control type I error when testing . The next proposition demarcates precisely what kind of can accomplish this goal.

Proposition 4.

Consider testing . The FRT with test statistic controls type I error at any level if under , the sampling distribution of is stochastically dominated by its randomization distribution, that is, .

To test , we use a test statistic , but look upon its randomization distribution as the reference null distribution. The -value in FRT-4 is the probability that is at least the observed value of . If , then any quantile of the asymptotic distribution of is at least that of . Consequently, we have conservative tests at any level.

It is quite burdensome to ensure a meaningful test statistic satisfies the criterion of Proposition 4. For a candidate statistic , we instead settle for ascertaining whether its randomization distribution stochastically dominates its sampling distribution asymptotically under for almost all sequences of . Henceforth, we call proper if so.

3.1 Studentized statistic

We advocate using the following studentized statistic in the FRT:

| (5) |

It is a Wald-type statistic that has a conservative covariance estimator for .

Studentized statistics have appeared alongside permutation tests when the outcomes are independent samples. Romano (1990) was aware of the problem of test statistics that were not studentized in two-sample tests. For Janssen (1997), studentization was an avenue in the Behrens–Fisher problem to control the type I error. Chung and Romano (2013) studied the same phenomenon when the parameter being cared about could be more general than the mean. Pauly et al. (2015) and Konietschke et al. (2015) embraced an equivalent studentized statistic in general factorial experiments with independent samples. In the aforementioned settings, studentization works because the test statistic is asymptotically pivotal.

As for us, is itself not asymptotically pivotal. Rather, it is stochastically dominated by a pivotal distribution. This is a key reason it is exactly the statistic we seek based on Proposition 4. We now formally state our main result that is proper.

Theorem 1.

Immediate from this theorem is that the FRT using controls the asymptotic type I error under . This test also retains finite sample exactness under the sharp null hypothesis (2). As a result, it is robust for inference on two classes of null hypotheses.

Asymptotically, under , neither the sampling nor randomization distribution of depends on or , so the choice of does not matter. The randomization distribution also does not depend on . A violation of is likely to inflate the value of but not the values of . An appealing consequence of this fact is that the FRT using has power.

Echoing Chung and Romano (2013) and Pauly et al. (2015), one purpose of studentization for us is to control type I error. Yet, for us, the FRT using is asymptotically conservative, while the corresponding test in an independent samples setting is asymptotically exact. This stems from our potential outcomes framework: do not have vanishing correlations, even asymptotically.

Theorem 1 inspires another asymptotically conservative test besides the FRT. We can reject if the observed value of exceeds the quantile of . We call this alternative to the FRT the approximation. This is computationally efficient without Monte Carlo. The FRT has an additional property. It is concurrently finite-sample exact for the sharp null hypothesis (2). Our simulations and practical data examples compare these two classes of tests empirically.

3.2 Box-Type Statistic

We now steer toward an alternative statistic, one found in Brunner et al. (1997):

| (6) |

where is the projection matrix onto the row space of . Because we will deem it as not proper in our context, we can restrict the discussion to .

Under independent sampling, Brunner et al. (1997) approximated the asymptotic behavior of by an distribution through ideas from Box (1954), and called it a Box-type statistic. Their simulations found it to enjoy superior empirical small sample properties under their framework.

For our problem, the next result states the behavior of . Recall in (3) and define .

The asymptotic mean of is because , and the asymptotic mean of is . Therefore, the former mean does not exceed the latter. This is necessary but not sufficient for the stochastic dominance criterion of Proposition 4, which does not hold. Hence, the FRT with the Box-type statistic cannot control type I error in general, even asymptotically. This is the subject of a later simulation.

There are two situations where is proper: equal variances, and testing a one-dimensional hypothesis.

3.3 Statistics from Ordinary Least Squares

Ordinary least squares (OLS) tools are widespread in the analysis of experimental data (e.g., Morris 2010). We insert -treatment randomized experiments into the realm of linear models. We do this by encoding the treatments with dummy variables in the design matrix . The response vector consists of the corresponding observed outcomes from treatment groups . The OLS coefficients are the entries of , which has estimated covariance matrix , where is the mean residual sum of squares. The classical statistic for testing (1) is then

| (7) |

We do not stipulate the usual assumptions of linear regression, but just want a test statistic for the FRT.

We first record a peculiar situation where is identical to the Box-type statistic . This result will be valuable for our simulations and practical data examples.

Proposition 5.

if and has the same entries along its main diagonal.

Except for the scaling by and the presence of in place of each , is identical to . This pooled variance estimate is problematic for the statistic, spurring it to fall short of the criterion of Proposition 4, as we formalize next.

The classical linear model assumes a constant treatment effect for all units (Kempthorne 1952). This necessitates equal variances under all treatment levels. Yet, such homoscedasticity is not built into the potential outcomes framework. The assumptions underlying the statistic are not compatible with the potential outcomes framework in general. If the potential outcomes do have equal variance, then it is not surprising that is proper.

Huber–White covariance estimation for the OLS coefficients is frequently quoted as a fix to the classical statistic. Econometricians are especially inclined to such an estimate of the covariance when the linear model is possibly misspecified or the error terms are heteroscedastic. Define the residual . The Huber–White estimator for is

If we replace by in (7) and dismiss the scaling by , we get

is nearly identical to if for . Therefore, is asymptotically akin to . By this, the Huber–White covariance estimator successfully repairs the statistic.

4 Special Cases

Section 3 devises a strategy for testing weak null hypotheses in general experiments. The contents there speak directly to many worthwhile settings.

4.1 One-Way Analysis of Variance with Multi-Valued Treatments

In the one-way analysis of variance (ANOVA), the goal is to test . It is a special case of the null hypothesis (1) with and any contrast matrix for instance . Here, , which spares us from having to construct or select .

We impute potential outcomes in FRT-2 as for and under , for . To test , Fisher (1925) crafted the statistic

| (8) |

He argued that approximates the sampling distribution of . Ding and Dasgupta (2018) attested that (8) is not proper but

| (9) |

is for testing with the FRT. See Schochet (2018) for a related discussion.

It is immediate from the next proposition that our framework encompasses these results as special cases.

4.2 Treatment-Control Experiments

In the treatment-control setting, , and unit either receives the treatment (then ) or control (then ). A parameter we might inquire about is the average treatment effect . The weak null hypothesis is . This matches (1), where is a row vector. Thus, treatment-control is a special case of the one-way layout of Section 4.1. A popular statistic is , where is the sample difference-in-means of outcomes. However, Ding and Dasgupta (2018) showed that is not proper for testing .

Corollary 3.

Because is a monotone transform of , the FRT with is asymptotically conservative in the finite population setup. It also leads to exact type I errors for the sharp null hypothesis for all Not only is the statistic not proper, but it also has other “paradoxical” shortcomings (Ding 2017); see also the comment of Loh et al. (2017). Corollary 3 declares that a balanced design can salvage the and statistics, even without homoscedasticity. Perhaps counter to intuition, this protection does not endure when , as our simulations will soon demonstrate.

4.3 Trend Tests

Our perspective has been on type I error under null hypotheses without specifying alternative hypotheses. In experiments for dose-response relationships, we have ordered treatment and often specify the null and alternative hypotheses as and with at least one strict inequality. We can still carry forward the results in Section 4.1 on ANOVA. Power might shrink for the test if we do not account for the ordering of the dose-response relationship. Motivated by Armitage (1955) and Page (1963), we first choose doses for treatment levels . Then the test statistic is plausible, where is a contrast vector, and . In effect, we are testing . Previous theory suggests that is not proper but the studentized statistic is:

Note that under , we impute all missing potential outcomes as for each unit , albeit we fix a particular contrast vector to construct the studentized statistic. Moreover, in this case, we conduct a one-sided test, rejecting if is larger than the quantile of its randomization distribution.

4.4 Binary Outcomes

The theory for statistics does not insist that the outcome be of a particular type as long as the regularity conditions hold. In particular, it applies directly to binary outcomes. However, binary outcomes have a special feature that , i.e., the mean determines the variance . Therefore, under the null hypothesis , the variances are all the same too: . For binary outcomes, the difference-in-means statistic for in Section 4.2, the statistic for general in Section 4.1, and the statistic in Section 4.3 are all proper for testing . As pointed out by Ding (2017), for this weak null hypothesis, we do not need studentization to guarantee correct asymptotic type I error. However, this does not hold for general weak null hypotheses of binary potential outcomes because does not imply they have equal variances. In general, we always recommend using .

4.5 Factorial Designs

factorial designs seek to analyze binary treatment factors simultaneously. In total, we have possible treatment combinations. Dasgupta et al. (2015) tied these designs and the potential outcomes framework together. We summarize this setup. To do so, it is helpful to introduce the model matrix . Let denote the component-wise product. Lu (2016a) constructed the rows of , which we call , as follows:

-

•

for , let be repeated times;

-

•

the next values of ’s are where ;

-

•

the next are component-wise products of triplets of distinct , etc;

-

•

the bottom row is .

The matrix has rows orthogonal to each other and to , i.e., and . Let be the first rows of . Call its columns , which are the possible treatment combinations. An example elucidates the setup.

Example 1.

When , we have

The four possible treatment combinations are , , , and . We read these off from the first two rows of .∎

The rows of define factorial effects. Namely, correspond to main effects, correspond to two-way interactions, etc, and corresponds to the -way interaction. Let be the response of unit if it receives the treatment combination . Then we can transfer our previous notation to factorial designs. The general factorial effect for unit indexed by is , and the corresponding average factorial effect is . Vectorize these quantities: and .

We may perform inference on or any subset of its entries. Let be the target subset, and let have rows . Then . Testing whether is equivalent to testing . The FRT with is proper. The factorial design stimulates a natural choice of for the imputation step FRT-2. We let be a row of whenever .

Lu (2016a) discussed both randomization-based and regression-based inferences for factorial designs. He fixated on point estimation and proposed using the Huber–White covariance estimator. We have likewise highlighted that it is imperative to use the Huber–White covariance estimator and the statistic together in the FRT.

4.6 Hodges–Lehmann Estimation

Up to this stage, our developments have been on hypothesis testing. Drawing upon the duality between testing and estimation, our previous results shed light on the estimation of . This strategy is sometimes referred to as Hodges–Lehmann estimation (Hodges and Lehmann 1963; Rosenbaum 2002b). For a fixed , we can by means of the FRT obtain a -value for the null hypothesis . Let us denote this -value by to delineate its dependence on .

The Hodges–Lehmann point estimator for is the that results in the least significant -value for testing . In symbols, . Note that implies , which in turn implies . Thus , the usual unbiased estimator. Because is proper, the duality between hypothesis testing and confidence sets assures the following corollary.

Corollary 4.

For and almost all sequences of , an asymptotically conservative confidence set for is in the sense that .

Determining can be computationally intensive, so it is expedient to have the asymptotic approximation

| (11) |

where is the quantile of . Because the statistic is a quadratic form, is an ellipsoid centered at . The set can serve either directly as a approximate confidence set or as an initial guess in searching for the exact confidence region by inverting FRTs. We undertake this later by a simulation.

4.7 Testing Inequalities

FRTs can also handle hypotheses of inequalities:

| (12) |

We commence at the case where is a row vector with , and is a scalar.

Example 2.

In the two-sample problem with , we can test : whether treatment level results in smaller outcomes than treatment level on average. In this case, and .∎

Example 3.

In a gold standard design for three arms, let level be the placebo control, level be the active control, and level be the experimental treatment. Suppose that smaller outcomes are more desirable, and we know that from previous studies. Given , the goal is to test the hypothesis . When , this is a superiority test, and when , this is a non-inferiority test (Mutze et al. 2017). This null hypothesis is equivalent to with .∎

To impute the missing potential outcomes, we pretend that the null hypothesis is and utilize (2) as we did before. The statistic is not suitable here because it is intended for two-sided tests. For instance, can be large, even under . Instead we use a truncated statistic where

The FRT with also works for -values at most . Mutze et al. (2017) used the special case of in the setting of Example 3. We choose so that Proposition 4 directly covers our situation. We summarize the results below.

Corollary 5.

When and for , we can interpret (12) as component-wise inequalities. Neither nor are acceptable when . An elementary workaround is to test each component using and apply a Bonferroni correction.

4.8 Cluster-Randomized Experiments

In many applied settings, the units are partitioned into clusters (e.g., classrooms in educational studies, villages in public health studies). All units belonging to a cluster must receive the same treatment. A cluster-randomized experiment assigns treatments to clusters, i.e. it is a CRE treating clusters as units. For , let represent the treatment that cluster receives, and define the indicator . There are possible realizations of . The mechanism of treatment assignment to clusters is identical to that to individuals in a CRE.

Middleton and Aronow (2015) stressed that we cannot implement the same analysis as if we had a CRE on the units. For instance, is no longer an unbiased estimator for if the cluster sizes vary. Both Middleton and Aronow (2015) and Li and Ding (2017) advised a CRE-like analysis. Let represent the cluster membership of unit . Define cluster level aggregated potential outcomes , where . Define , , , to align with our previous notation for a CRE. Aggregated potential outcomes resolve the problem of unbiased estimation of : . Define and . We revise the statistic as

Then Theorem 1 tells us that is proper for as if Assumption 2 holds for the aggregated potential outcomes.

5 Extensions

5.1 Stratified Randomized Experiments

We extend previous results to the stratified randomized experiment (SRE), also called the randomized block design. The overall setup from the CRE still applies, but now for each unit we also observe an associated covariate . Thus, our data are . The treatment does not affect this covariate. The ’s remain the sole source of randomness. For , the -th stratum consists of all units where , whose size is and proportion is . For and , the experimenter predetermines the sample sizes . In a SRE, we assign treatments within each stratum just as we did in a CRE, and independently among different strata (Imbens and Rubin 2015).

To define within-stratum means and covariances, we mirror previous notation. For , the mean vector is , which has -th entry . The covariance has -th entry . We impose Assumption 2 on all strata.

Assumption 3.

For , (1) and ; (2) the sequences and converge to and ; (3) the matrix has strictly positive main diagonal entries; (4) there exists an such that for all and .

We do not distinguish between Assumptions 1 and 2 in the SRE for convenience. Tolerating a tiny abuse of notation, stands for both and its limit. The sample mean vector is , which has -th entry . The sample variance is . Under Assumption 3, we have from Proposition 3 that, inside stratum , the standardized stratum-wise sample mean is asymptotically Normal with mean and a covariance we denote . A conservative estimator for is

An unbiased estimator for is . Owing to the independence of treatment assignment across different strata, is asymptotically Normal with mean and covariance . A conservative variance estimator is .

We are now positioned to make an adjustment to that is proper when used with the FRT in a SRE:

| (13) |

The special case and (5) agree, so the same notation for this statistic is logical. Besides the form of the test statistic, the FRT entails two more modifications in the case of an SRE. First, we impute the potential outcomes stratum by stratum under the sharp null hypothesis

Since we still aim to test (1), the above null hypothesis must satisfy . If , it is natural to choose and for each . Under the above sharp null hypothesis, we can impute all potential outcomes: for units in stratum ,

or, equivalently, . Second, we ought to permute the treatment indicators within strata, independently across strata. Let be all such permutations from a SRE. The -value is .

Theorem 4.

Even if the original experiment is a CRE, if a discrete covariate is available, we can condition on the number of treated and control units landing in each stratum. Then the treatment assignment is identical to a SRE. Therefore, in a CRE, we can still permute the treatment indicators within each stratum of . This plan is billed as a conditional randomization test. Zheng and Zelen (2008) and Hennessy et al. (2016) perceived that conditional randomization tests typically enhance the power as long as the covariates are predictive of the outcomes.

We have focused on the SRE with large strata, i.e., for , and is fixed. Our theory does not encapsulate SREs with many small strata, i.e., the ’s are bounded but (Fogarty 2018a). Although we conjecture that similar results hold in such cases, we defer technical details to future research.

5.2 Multiple Outcomes and Multiple Testings

We can lengthen the reach of our framework to the case where all potential outcomes are vectors. Define and as before. It is convenient to gather these into long vectors

The covariances and are now matrices, for . The overall covariance matrix has -th block . Assume and are both positive definite for all realizations of .

Let be the components of the potential outcomes for all and . We wish to test the weak null hypothesis

| (14) |

where are contrast matrices that have columns and possibly varying row counts. We can condense notation via the Kronecker product: define

where are the standard basis vectors of . We can then write (14) in the form . It looks exactly like (1), but cannot be an arbitrary contrast matrix.

Example 4.

We lay out some possible contrast matrices when and . The hypothesis has the contrast matrix

Here, we test the same hypothesis entry by entry, and an equivalent contrast matrix is . We can also test different hypotheses entry by entry, for instance , . This hypothesis has the contrast matrix

The potential outcomes framework cannot withstand comparison of different entries under different treatments, for instance . Null hypotheses like these do not have a clear causal interpretation here. Under i.i.d. sampling, Friedrich et al. (2017) allow for a general contrast matrix , and even for the length of to depend on treatment . We constrain the contrast matrices that we accept, as we have just detailed.

Under i.i.d. sampling and vector potential outcomes, Chung and Romano (2016) address the two-sample problem with permutation tests. Srivastava and Kubokawa (2013), Konietschke et al. (2015) and Friedrich and Pauly (2018) test general linear hypotheses with bootstrap methods. We will use the FRT for (14). It is not a sharp null hypothesis, so we concoct one:

where the matrices through are invertible. We construct the ’s and ’s for each component of the outcome in the same way as the scalar case. In the hypothesis , our notation does not reflect its dependence on the ’s, ’s, ’s and ’s. We impute potential outcomes as if were the reality. For the first component:

| (15) |

and similarly for the second through the -th entries, replacing all subscripts by .

For vector potential outcomes, we tweak in (5):

where the block diagonal matrix is an asymptotically conservative estimator of . This is in sync with (4). The FRT with can control the asymptotic type I error under (14). We first give the asymptotic requirements and then adapt Theorem 1 to the vector case. Let be the Euclidean norm, which reduces to the usual absolute value for scalars.

Assumption 4.

The sequence converges to for all . The sequences and converge to and , where , is positive semi-definite, and is positive definite for all . Further, .

Assumption 5.

Same as Assumption 4 except the last sentence is replaced by: Further, there exists an such that for all and .

Theorem 5.

Theorem 5 puts in place a foundation for a single FRT for multiple outcomes. As done in Chung and Romano (2016, Section 4), we can join Theorem 5 and the closure procedure for multiple testings. We omit the details.

To conduct the FRT with at all, we require all realizations of to be invertible, for which it is necessary that . Friedrich and Pauly (2018) instead tried with a bootstrap, where is a diagonal matrix whose main diagonal is the same as . However, is not proper for the FRT because the asymptotic distribution of is not pivotal. So it is flawed for the same reason the Box type statistic in (6) is. We reserve FRTs with for future research.

6 Simulations

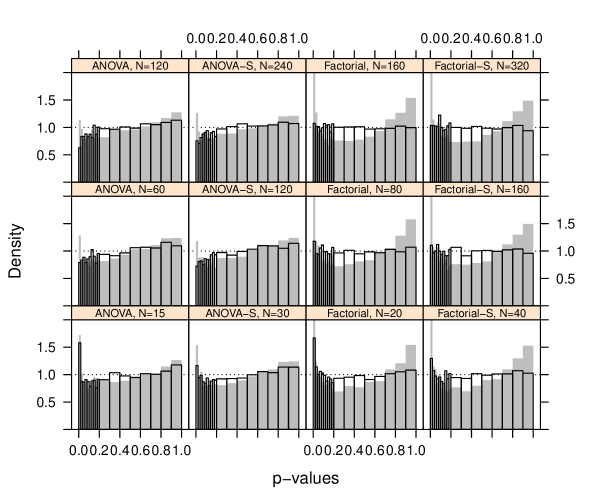

6.1 Type I Error Rates of FRTs with Different Statistics

We perceive from previous sections that is proper, but and are not. As a complement to this asymptotic fact, simulations reveal their finite sample behavior. To drive this point, we repeat the simulations with varying sample sizes. All the test statistics we brought up had other specific purposes in the literature. Thus, the simulations also serve to compare their efficacy with the FRT for testing weak null hypotheses.

6.1.1 Simulation Setup

We decided on the ANOVA with and the Factorial with setup, which we refer to as “ANOVA” and “Factorial” for short. The null hypotheses being tested, written in the form of (1), are

In words, the former tests for no effects of any treatments on average. The latter tests for no main effects of either of the two factors on average. Both setups shall have a balanced design for all . We then gain from Proposition 5 that . Thus, a comparison of and suffices. In all cases, we compel , so the weak null hypothesis of no treatment effects on average holds. We also compel force the covariance structure on the potential outcomes. For the ANOVA case, , and for the Factorial case, . We deliberately avoid any sharp null hypothesis being true by design. Otherwise, all test statistics would have correct type I error control.

Explicitly, we first generate for , center them, and scale them according to . For the hypothesis test itself, we simulate 10000 different realizations of the observed outcomes. For each set of , we run the FRT with both and , calculating -values from 2500 permutations.

For these potential outcomes, we compute the eigenvalues in Theorems 1 and 2 to derive that the asymptotic sampling distributions of and under are

| (16) | |||||

their randomization distributions are both asymptotically in both the ANOVA and factorial designs. This provides an illustrative and simple numerical example of our main results. Each weight for is at most , while the weights for are only at most on average. In the Factorial case, the FRT with is actually asymptotically exact because both the sampling and randomization distributions of approach .

We can naturally broaden the simulations just performed to SREs. We keep the ANOVA and Factorial setup, but now incorporate a SRE with strata. Remember that this means the observed data come from running a CRE within each stratum separately. The first stratum of potential outcomes shall be identical to those of the ANOVA simulation above. The second stratum shall be identical to the first, except a unit constant is added to all its potential outcomes. This between stratum effect merits a SRE analysis. We proceed with the statistic in (5.1), and only permute data within each stratum when obtaining -values.

The textbook suggestion Morris (2010) for testing the our null hypotheses in the SRE case involves the statistic from a linear regression of the observed response on stratum and treatment indicators, i.e., predictors. Although Morris (2010) has reiterated the usual OLS assumptions that justify the test, practitioners do not always check them. We therefore would like to compare and in this SRE setting. From Theorem 4, we know in (5.1) has the same asymptotic behavior as listed in (16). By intuition from Lin (2013), we anticipate that also has the same asymptotic behavior as before.

In all four settings we have put forth, we also fix three different sample size settings to pinpoint the rate that asymptotics take effect.

6.1.2 Results

Figure 1 contains the simulation results. For each setting and sample size, we plot histograms of -values from the FRT with and or . In all histograms, the left-most bin of -values ranging from 0 to 2% is most informative. For a successful control of type I error, the density of -values here should not surpass 1 by much. From the bottom row of Figure 1, or (bottom row) is evidently far from the asymptotic regime. When or (middle row), it appears that we move much closer to the expected behavior dictated by asymptotics. This is because, when these counts are 40 (top row), the histograms do not change much from the row below. That is, the first and second rows have a similar pattern. The similarity of the SRE histograms to the corresponding CRE ones buttresses our intuition that and have similar distributions as their “unstratified” twins for our simulated potential outcomes.

It is also confirmed that the FRT with or fails to control type I error at small -values for any sample size. We recollect from our theory that heteroscedasticity hampers its suitability. We have elected to balance the designs, so that it surfaces that, when , balanced designs do not guarantee the suitability of or as they do in treatment-control experiments (refer to Corollary 3). Of course, forgoing balanced designs can cause both and to fail more seriously. Ding and Dasgupta (2018) compare and in such cases through extensive simulation.

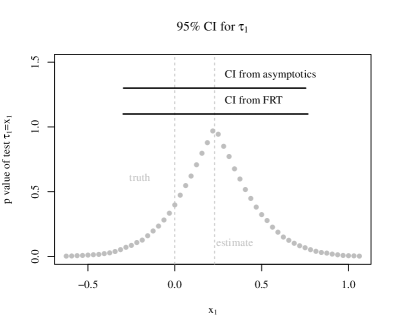

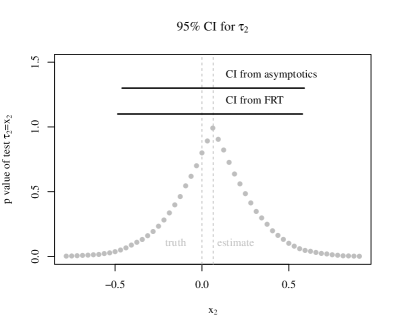

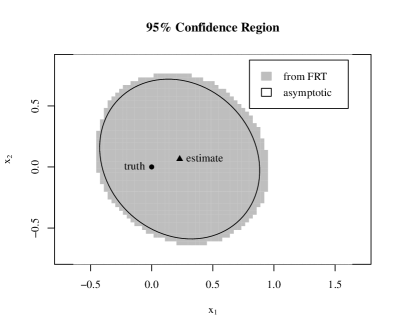

6.2 Confidence Regions

Our next simulation constructs confidence regions alluded to by Corollary 4. At the same time, we seize the opportunity to compare the FRT and approximations that are both asymptotically valid by Theorem 1. We decided on a balanced factorial design (, ) where for . We seek to infer the main effects , , both individually and jointly. Take where , and center so that each . This way, the true parameter values are , but takeaways of this simulation generalize to arbitrary . Next, multiply each by the same matrix

to inject correlation into the potential outcomes.

We assign treatments to units according to the CRE, and construct the confidence regions by means of a single realization of observed outcomes. The set in (11) is a means to compute an asymptotic confidence region for , . After finding it, we spread a grid of points centered at , that comfortably envelops this asymptotic region. At each point () of this grid, we run the FRT with to test , , both individually and jointly. We induct the point into our confidence region if and only if the -value exceeds .

Figure 2(a) shows the results for the marginal hypothesis tests. The behavior is very regular: the -value crests near or , and decays monotonically to the left and right. The FRT and approximation confidence intervals are nearly indistinguishable. Figure 2(b) shows the result for the joint test. The left graph shows the FRT confidence region is again close to its asymptotic approximation, but not as close as in the 1D case. In particular, the former is noticeably larger. The right graph explains this by exposing that the -values calculated from the FRT tend to be larger than those from the approximation.

Due to the duality between hypothesis testing and confidence regions, the empirical coverage of our confidence region is the proportion of time it includes over all realizations of the observed data. From the simulations in the previous section, which deals with the false rejection rate of the FRT, we expect this proportion to be at least 0.95. The closeness of the confidence regions to their asymptotic approximations suggests our results generalize to other realizations of the observed data. That is, those confidence regions will be centered at , but have similar shape.

7 Applications

We now try out our method on practical datasets, under a variety of possible weak null hypotheses. Our goal is not to do complete data analyses. We do not delve into issues of multiple comparisons. We pretend each null hypothesis is tested in isolation.

7.1 Financial Incentives for Exercise

Charness and Gneezy (2009) were interested in whether financial incentives caused college students to exercise more. They randomly assigned 40 students each to one of three possible treatments: no financial incentive (control), a small one, or a large one. We henceforth index these groups by , respectively. Then . For each student, the response was the average number of weekly gym visits after the study minus that before the study. Let denote this quantity for the -th student, if s/he received treatment . Many students had . This would be troublesome for the FRT with if, after a certain permutation, all permuted observations in a group were 0. To preclude this, we added a minuscule amount of random noise to all the . For this dataset, the sample means are , and the sample variances are , for groups , respectively. Mere inspection of these numbers posits that a large financial incentive has a positive effect while a small one does not. It is also apparent that the data are heteroscedastic.

We test these four hypotheses at level 1%: whether the two magnitudes of financial incentives have any effect on average, whether financial incentives have any effect ignoring the division between large and small, whether financial incentives have any effect, and whether small financial incentives have any effect. In symbols, these are , (here we collapse treatment levels to one), , and (here we ignore the observations), respectively.

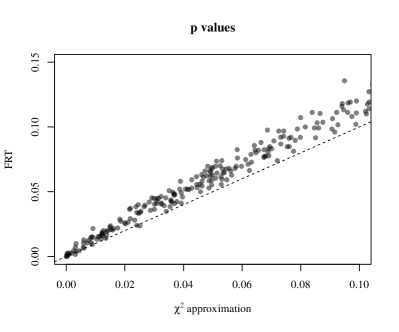

We use the and statistics, and get -values both by the FRT and the (or ) approximation. As we brought up earlier, -values from FRTs are also finite-sample exact for testing Fisher’s sharp null hypothesis. Consult Table 1 for the results. The class of hypothesis test (FRT and (or ) approximation) holds little sway. It seems, for , the FRT is slightly more conservative. For , the FRT is slightly less conservative.

| Hypothesis | FRT using | FRT using | ||

|---|---|---|---|---|

| 0.25 | 0.27 | 1.97 | 1.59 | |

| 0.42 | 0.49 | 0.06 | 0.01 | |

| 0.34 | 0.49 | 2.45 | 2.34 | |

| 47.15 | 47.93 | 47.37 | 47.93 |

Testing the first two hypotheses, financial incentives have a statistically significant impact on gym attendance. Guided by Theorems 1 and 3, we should trust the -values from more than those from . The latter statistic seems to have overly conservative behavior for this dataset. Testing the third hypothesis suggests that the treated group ( or ) has different behavior from the control in a statistically significant way.

Seeing evidence that financial incentives might be helpful, we test the fourth hypothesis only comparing the control and small incentive groups, and get insignificant -values. Note, in this case, by Corollary 3, thanks to the balanced design. To wrap up, we concur with the findings of Charness and Gneezy (2009), that large financial incentives seem to induce people to visit the gym more often, but not small ones.

7.2 A Factorial Experiment for Grades

We now undertake a similar analysis as in the previous section on another dataset. Angrist et al. (2009) wondered whether academic support services and/or financial incentives caused college students to improve their grades. Their data consisted of student grades for a certain semester on a 100 point scale. In that semester, students were either in a control group, offered a fellowship, offered services, or both. We thus have a factorial experiment, and henceforth index these treatment groups by , respectively. As opposed to the allocation in the previous section, this one is imbalanced: . The sample means are , and the sample variances are , for groups , respectively. By eye, there is less heteroscedasticity, and the sample means are less markedly off from each other than those of the previous section.

We test the following five hypotheses at level 1%: financial services have no effect, services have no effect, neither has an effect, no interactions, and that all group means are the same. In symbols, these are , , both of the previous two, , and .

We again use the and statistics, and get -values both by the FRT and the (or ) approximation. As we discussed earlier, -values from FRTs are also exact for testing Fisher’s sharp null hypothesis. Consult Table 2 for the results. The class of hypothesis test again holds little sway. The FRT seems as a whole slightly more conservative, though there are a few exceptions.

| Hypothesis | FRT using | FRT using | ||

| No effect from services | 72.84 | 72.34 | 73.92 | 73.58 |

| No effect from incentives | 1.19 | 1.43 | 1.60 | 1.80 |

| No effects from either | 3.65 | 3.99 | 5.26 | 5.28 |

| No interaction | 99.53 | 99.47 | 99.55 | 99.5 |

| 3.88 | 4.31 | 5.85 | 5.71 |

We cannot reject any of these null hypotheses at level 1%. From the second and fourth hypotheses, the data do not seem to suggest services have any effect, or that there is a non-additive effect from combining incentives and services. We do, however, almost reject the hypothesis of no effect from incentives alone: the -values are just over 1%.

Our finding that the effect of incentives is more significant than the effect of others conforms with the conclusions of Angrist et al. (2009). They went on to conduct subgroup analysis, and discovered that the observed effects on grades come nearly exclusively from female students.

8 Discussion

We have proposed a strategy for using the FRT to test a weak null hypothesis. It imputes the missing potential outcomes under a compatible sharp null hypothesis, and then uses the studentized statistic in the FRT. It furthers the current literature in two directions. First, it complements the tests centered on asymptotic distributions. Our FRT is also finite-sample exact under the sharp null hypothesis. Second, it guides the choice of test statistic for the sharp null hypothesis. Although the finite-sample exactness property of the FRT holds for any test statistic, the -values are sensitive to this choice. For example, all the -values in Tables 1 and 2 are valid for Fisher’s sharp null hypothesis. Unfortunately, these -values range above and below the nominal significance level. This can be confusing in practice. Therefore, we cannot overstate the crucial role of weak null hypotheses and studentized statistics. Our FRTs can control asymptotic type I error under weak null hypotheses and have power under corresponding alternative hypotheses.

Our theory ignores covariates. The analysis of covariance is a classical topic (Fisher 1935) and still attracts attention (Lin 2013; Lu 2016b; Fogarty 2018b, a; Middleton 2018). Bloniarz et al. (2016) and Lei and Ding (2018) widened it to the case where the number of covariates grows with the sample size. Tukey (1993) and Rosenbaum (2002a) discussed strategies for testing sharp null hypotheses. It is important to extend the theory to test weak null hypotheses with covariate adjustment, plus to the case with high dimensional covariates. We leave this to future work.

We have focused on completely randomized factorial experiments and extended the theory to stratified and clustered experiments. We conjecture that the strategy is also applicable for experiments with general treatment assignment mechanisms (Mukerjee et al. 2018). Fogarty (2019) also used the idea of studentization in sensitivity analysis of matched observational studies.

References

- Angrist et al. (2009) J. Angrist, D. Lang, and P. Oropoulos. Incentives and services for college achievement: Evidence from a randomized trial. American Economic Journal: Applied Economics, 1:136–163, 2009.

- Armitage (1955) P. Armitage. Tests for linear trends in proportions and frequencies. Biometrics, 11:375–386, 1955.

- Aronow et al. (2014) P. M. Aronow, D. P. Green, and D. K. Lee. Sharp bounds on the variance in randomized experiments. The Annals of Statistics, 42:850–871, 2014.

- Athey and Imbens (2017) S. Athey and G. W. Imbens. The Econometrics of Randomized Experiments, volume 1 of Handbook of Economic Field Experiments, chapter 3, pages 73–140. Elsevier B.V, 2017.

- Athey et al. (2018) S. Athey, D. Eckles, and G. W. Imbens. Exact -values for network interference. Journal of the American Statistical Association, 113:230–240, 2018.

- Babu and Singh (1983) G. J. Babu and K. Singh. Inference on means using the bootstrap. The Annals of Statistics, 11:999–1003, 1983.

- Basse et al. (2019) G. Basse, A. Feller, and P. Toulis. Randomization tests of causal effects under interference. Biometrika, 106:487–494, 2019.

- Basu (1980) D. Basu. Randomization analysis of experimental data: The Fisher randomization test. Journal of the American Statistical Association, 75:575–582, 1980.

- Bloniarz et al. (2016) A. Bloniarz, H. Liu, C. Zhang, J. Sekhon, and B. Yu. Lasso adjustments of treatment effect estimates in randomized experiments. Proceedings of the National Academy of Sciences of the United States of America, 113:7383–7390, 2016.

- Box (1954) G. Box. Some theorems on quadratic forms applied in the study of analysis of variance problems. Annals of Mathematical Statistics, 25:290–302, 1954.

- Box and Andersen (1955) G. E. P. Box and S. L. Andersen. Permutation theory in the derivation of robust criteria and the study of departures from assumption. Journal of the Royal Statistical Society, Series B (Methodological), 17:1–34, 1955.

- Bradley (1968) J. V. Bradley. Distribution-Free Statistical Tests. Upper Saddle River, NJ: Prentice Hall, 1968.

- Brunner et al. (1997) E. Brunner, H. Dette, and A. Munk. Box-type approximations in nonparametric factorial designs. Journal of the American Statistical Association, 92:1494–1502, 1997.

- Caughey et al. (2017) D. Caughey, A. Dafoe, and L. Miratrix. Beyond the sharp null: Randomization inference, bounded null hypotheses, and confidence intervals for maximum effects. arXiv preprint arXiv:1709.07339, 2017.

- Charness and Gneezy (2009) G. Charness and U. Gneezy. Incentives to exercise. Econometrica, 77:909–931, 2009.

- Chung and Romano (2013) E. Chung and J. P. Romano. Exact and asymptotically robust permutation tests. The Annals of Statistics, 41:484–507, 2013.

- Chung and Romano (2016) E. Chung and J. P. Romano. Multivariate and multiple permutation tests. Journal of Econometrics, 193:76–91, 2016.

- Collier and Baker (1966) R. O. Collier and F. B. Baker. Some Monte Carlo results on the power of the F-test under permutation in the simple randomized block design. Biometrika, 53:199–203, 1966.

- Dasgupta et al. (2015) T. Dasgupta, N. Pillai, and D. B. Rubin. Causal inference from factorial designs by using potential outcomes. Journal of the Royal Statistical Society, Series B (Statistical Methodology), 77:727–753, 2015.

- Ding (2017) P. Ding. A paradox from randomization-based causal inference (with discussion). Statistical Science, 32:331–345, 2017.

- Ding and Dasgupta (2018) P. Ding and T. Dasgupta. A randomization-based perspective of analysis of variance: a test statistic robust to treatment effect heterogeneity. Biometrika, 105:45–56, 2018.

- Ding et al. (2016) P. Ding, A. Feller, and L. Miratrix. Randomization inference for treatment effect variation. Journal of the Royal Statistical Society, Series B (Statistical Methodology), 78:655–671, 2016.

- Duflo et al. (2007) E. Duflo, R. Glennerster, and M. Kremer. Using randomization in development economics research: A toolkit, volume 4, chapter 61, pages 3895–3962. Elsevier, 2007.

- Eden and Yates (1933) T. Eden and F. Yates. On the validity of Fisher’s z test when applied to an actual example of non-normal data. The Journal of Agricultural Science, 23:6–17, 1933.

- Fisher (1925) R. A. Fisher. Statistical Methods for Research Workers. Edinburgh: Oliver and Boyd, 1925.

- Fisher (1935) R. A. Fisher. The Design of Experiments. Edinburgh, London: Oliver and Boyd, 1st edition, 1935.

- Fogarty (2018a) C. B. Fogarty. On mitigating the analytical limitations of finely stratified experiments. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80:1035–1056, 2018a.

- Fogarty (2018b) C. B. Fogarty. Regression assisted inference for the average treatment effect in paired experiments. Biometrika, 105:994–1000, 2018b.

- Fogarty (2019) C. B. Fogarty. Studentized sensitivity analysis for the sample average treatment effect in paired observational studies. Journal of the American Statistical Association, page in press, 2019.

- Friedrich and Pauly (2018) S. Friedrich and M. Pauly. Mats: Inference for potentially singular and heteroscedastic manova. Journal of Multivariate Analysis, 165:166–179, 2018.

- Friedrich et al. (2017) S. Friedrich, E. Brunner, and M. Pauly. Permuting longitudinal data in spite of the dependencies. Journal of Multivariate Analysis, 153:255–265, 2017.

- Gail et al. (1996) M. H. Gail, S. D. Mark, R. J. Carroll, S. B. Green, and D. Pee. On design considerations and randomization-based inference for community intervention trials. Statistics in Medicine, 15:1069–1092, 1996.

- Gerber and Green (2012) A. S. Gerber and D. P. Green. Field Experiments: Design, Analysis, and Interpretation. New York: W. W. Norton and Company, 2012.

- Hall (1988) P. Hall. Theoretical comparison of bootstrap confidence intervals. The Annals of Statistics, 16:927–953, 1988.

- Hennessy et al. (2016) J. Hennessy, T. Dasgupta, L. Miratrix, C. Pattanayak, and P. Sarkar. A conditional randomization test to account for covariate imbalance in randomized experiments. Journal of Causal Inference, 4:61–80, 2016.

- Hodges and Lehmann (1963) J. L. Hodges and E. L. Lehmann. Estimates of location based on rank tests. The Annals of Mathematical Statistics, 34:598–611, 1963.

- Hoeffding (1952) W. Hoeffding. The large-sample power of tests based on permutations of observations. The Annals of Mathematical Statistics, 23:169–192, 1952.

- Imbens and Menzel (2018) G. W. Imbens and K. Menzel. A causal bootstrap. Technical report, National Bureau of Economic Research, 2018.

- Imbens and Rubin (2015) G. W. Imbens and D. B. Rubin. Causal Inference for Statistics, Social, and Biomedical Sciences: An Introduction. Cambridge: Cambridge University Press, 2015.

- Janssen (1997) A. Janssen. Studentized permutation tests for non-iid hypotheses and the generalized behrens-fisher problem. Statistics and Probability Letters, 36:9–21, 1997.

- Janssen (1999) A. Janssen. Testing nonparametric statistical functionals with applications to rank tests. Journal of Statistical Planning and Inference, 81:71–93, 1999.

- Janssen and Pauls (2003) A. Janssen and T. Pauls. How do bootstrap and permutation tests work? Annals of Statistics, 31:768–806, 2003.

- Kempthorne (1952) O. Kempthorne. The Design and Analysis of Experiments. New York: John Wiley and Sons, 1952.

- Kempthorne and Doerfler (1969) O. Kempthorne and T. E. Doerfler. The behaviour of some significance tests under experimental randomization. Biometrika, 56:231–248, 1969.

- Konietschke et al. (2015) F. Konietschke, A. C. Bathke, S. W. Harrar, and M. Pauly. Parametric and nonparametric bootstrap methods for general manova. Journal of Multivariate Analysis, 140:291–301, 2015.

- Lehmann (1975) E. L. Lehmann. Nonparametrics: Statistical Methods Based on Ranks. San Francisco: Holden-Day, Inc., 1975.

- Lei and Ding (2018) L. Lei and P. Ding. Regression adjustment in completely randomized experiments with a diverging number of covariates. arXiv preprint arXiv:1806.07585, 2018.

- Li and Ding (2016) X. Li and P. Ding. Exact confidence intervals for the average causal effect on a binary outcome. Statistics in Medicine, 35:957–960, 2016.

- Li and Ding (2017) X. Li and P. Ding. General forms of finite population central limit theorems with applications to causal inference. Journal of the American Statistical Association, 112:1759–1169, 2017.

- Lin (2013) W. Lin. Agnostic notes on regression adjustments to experimental data: reexamining freedman’s critique. The Annals of Applied Statistics, 7:295–318, 2013.

- Lin et al. (2017) W. Lin, S. D. Halpern, M. Prasad Kerlin, and D. S. Small. A “placement of death” approach for studies of treatment effects on ICU length of stay. Statistical Methods in Medical Research, 26:292–311, 2017.

- Loh et al. (2017) W. W. Loh, T. S. Richardson, and J. M. Robins. An apparent paradox explained. Statistical Science, 32:356–361, 2017.

- Lu (2016a) J. Lu. On randomization-based and regression-based inferences for factorial designs. Statistics and Probability Letters, 112:72–78, 2016a.

- Lu (2016b) J. Lu. Covariate adjustment in randomization-based causal inference for factorial designs. Statistics and Probability Letters, 119:11–20, 2016b.

- Middleton (2018) J. A. Middleton. A unified theory of regression adjustment for design-based inference. arXiv preprint arXiv:1803.06011, 2018.

- Middleton and Aronow (2015) J. A. Middleton and P. M. Aronow. Unbiased estimation of the average treatment effect in cluster-randomized experiments. Statistics, Politics and Policy, 6:39–75, 2015.

- Morris (2010) M. Morris. Design of Experiments: An Introduction Based on Linear Models. London: Chapman and Hall/CRC, 2010.

- Mukerjee et al. (2018) R. Mukerjee, T. Dasgupta, and D. B. Rubin. Using standard tools from finite population sampling to improve causal inference for complex experiments. Journal of the American Statistical Association, 113:868–881, 2018.

- Mutze et al. (2017) T. Mutze, F. Konietschke, A. Munk, and T. Friede. A studentized permutation test for three-arm trials in the gold standard design. Statistics in Medicine, 36:883–898, 2017.

- Neuhaus (1993) G. Neuhaus. Conditional rank tests for the two-sample problem under random censorship. The Annals of Statistics, 21:1760–1779, 1993.

- Neyman (1923/1990) J. Neyman. On the application of probability theory to agricultural experiments. Statistical Science, 5:465–472, 1923/1990.

- Neyman (1935) J. Neyman. Statistical problems in agricultural experimentation (with discussion). Supplement to the Journal of the Royal Statistical Society, 2:107–180, 1935.

- Nolen and Hudgens (2011) T. L. Nolen and M. G. Hudgens. Randomization-based inference within principal strata. Journal of the American Statistical Association, 106:581–593, 2011.

- Page (1963) E. B. Page. Ordered hypotheses for multiple treatments: a significance test for linear ranks. Journal of the American Statistical Association, 58:216–230, 1963.

- Pauly et al. (2015) M. Pauly, E. Brunner, and F. Konietschke. Asymptotic permutation tests in general factorial designs. Journal of the Royal Statistical Society, Series B (Statistical Methodology), 77:461–473, 2015.

- Pitman (1937) E. J. G. Pitman. Significance tests which may be applied to samples from any populations. Supplement to the Journal of the Royal Statistical Society, 4:119–130, 1937.

- Rigdon and Hudgens (2015) J. Rigdon and M. G. Hudgens. Randomization inference for treatment effects on a binary outcome. Statistics in Medicine, 34:924–935, 2015.

- Romano (1990) J. P. Romano. On the behavior of randomization tests without a group invariance assumption. Journal of the American Statistical Association, 85:686–692, 1990.

- Rosenbaum (1999) P. R. Rosenbaum. Reduced sensitivity to hidden bias at upper quantiles in observational studies with dilated treatment effects. Biometrics, 55:560–564, 1999.

- Rosenbaum (2001) P. R. Rosenbaum. Effects attributable to treatment: Inference in experiments and observational studies with a discrete pivot. Biometrika, 88:219–231, 2001.

- Rosenbaum (2002a) P. R. Rosenbaum. Covariance adjustment in randomized experiments and observational studies. Statistical Science, 17:286–327, 2002a.

- Rosenbaum (2002b) P. R. Rosenbaum. Observational Studies. New York: Springer, 2 edition, 2002b.

- Rosenbaum (2003) P. R. Rosenbaum. Exact confidence intervals for nonconstant effects by inverting the signed rank test. The American Statistician, 57:132–138, 2003.

- Rubin (1974) D. B. Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Psychology, 66:688–701, 1974.

- Rubin (1980) D. B. Rubin. Comment on D. Basu. Journal of the American Statistical Association, 75:591–593, 1980.

- Rubin (2005) D. B. Rubin. Causal inference using potential outcomes: Design, modeling, decisions. Journal of the American Statistical Association, 100:322–331, 2005.

- Sabbaghi and Rubin (2014) A. Sabbaghi and D. B. Rubin. Comments on the Neyman–Fisher controversy and its consequences. Statistical Science, 29:267–284, 2014.

- Schochet (2018) P. Z. Schochet. Design-based estimators for average treatmenteffects for multi-armed RCTs. Journal of Educational and Behavioral Statistics, 43:586–593, 2018.

- Srivastava and Kubokawa (2013) M. S. Srivastava and T. Kubokawa. Tests for multivariate analysis of variance in high dimension under non-normality. Journal of Multivariate Analysis, 115:204–216, 2013.

- Tukey (1993) J. W. Tukey. Tightening the clinical trial. Controlled Clinical Trials, 14:266–285, 1993.

- Zheng and Zelen (2008) L. Zheng and M. Zelen. Multi-center clinical trials: Randomization and ancillary statistics. The Annals of Applied Statistics, 2:582–600, 2008.

Supplementary Material for “Randomization Tests for Weak Null Hypotheses in Randomized Experiments”

Let be the absolute value of a scalar or the Euclidean norm of a vector. Let be the Frobenius norm of a matrix. For , let be the component-wise product of and : . Let , , and denote the maximums over , , and both. Let be the maximum value of and .

Appendix A1 gives several useful lemmas and their proofs. Appendix A2 gives the proofs of the main theorems. Appendix A3 gives the proofs of other corollaries and propositions.

A1 Lemmas

Lemma A1.

-

(i)

If , then . If is a projection matrix, then each .

-

(ii)

If and is a correlation matrix, then .

-

(iii)

If , and , then . If , then each .

Proof.

(i) and (ii) come from Ding and Dasgupta (2018). We prove (iii). The Continuous Mapping Theorem implies , and Slutsky’s Theorem then implies . By (i), . If , then each . ∎

Lemma A2.

A finite population has mean and variance . Let be a simple random sample of size , and . Then for ,

where , and .

Proof.

Bloniarz et al. (2016) prove the first inequality. The second follows from ∎

Lemma A2 is crucial for our proof of almost sure convergence for sampling without replacement, as we are about to see.

Lemma A3.

Let be a sequence of populations with means and variances . Suppose we take a simple random sample from each population of size with sample mean and variance . Assume .

Proof.

(i) Because , we can pick a positive integer such that implies . Then by Lemma A2, there is a universal constant , independent of , such that, for and ,

By the Borel–Cantelli Lemma, .

(ii) First, by the Cauchy–Schwarz Inequality, we have that for all

which is bounded above as , so by (i), .

Second, let be the indicator for being in the simple random sample. Define as an intermediate quantity , which differs from by an almost surely zero quantity as :

Third, we note that the variance of is bounded above for all :

So by (i), , and therefore

We now finally have . ∎

Lemma A4.

Proof.

Recall the ’s in FRT-2 and define . Because converges for all , and the ’s do not depend on , we may pick such that for all ,

Put , which is by Assumption 1. Then

Next,

Recall that , and we have the following bounds:

Using the above bounds and the additional bound , we have

In FRT-2, we have and therefore . Finally, we have

which is as desired. ∎

Lemma A5.

Let be a sequence of populations with means and covariances . Suppose we take a simple random sample from each population of size with sample mean and covariance . Assume .

Proof.

(i) Note that each component of meets Lemma A3, so holds component by component.

(ii) Because each component of meets Lemma A3, each entry on the main diagonal of converges almost surely to 0. It is thus enough to show convergence of the th entry, for then identical logic will show convergence of an arbitrary off-diagonal entry. Let and be the first and second entries of .

We follow the steps of Lemma A3 closely. First, is bounded above:

where the first inequality follows from the Triangle Inequality and for two vectors and , and the second inequality by the Cauchy–Schwarz Inequality. By (i), .

Second, let be the indicator for being in the simple random sample. Define as an intermediate quantity , which differs from by an almost surely zero quantity as :

Third, we note that the variance of is bounded above for all :

So by (i), . In addition, is bounded from above. These imply that

We now finally have . ∎

Lemma A6.

Under Assumption 4 and for all sequences of , the imputed potential outcomes satisfy .

A2 Proofs of the Main Theorems

We make some preliminary observations and extend the notation to handle the randomization distributions as required by Theorems 1, 2, and 3. Throughout, we make heavy use of the mean of the observed values:

Recall the imputed potential outcomes FRT-2 are . They agree with the data in the sense for all . They are also strictly additive, as does not depend on the unit . The imputed potential outcomes have means and covariance , due to strict additivity. Recalling that , we have

| (A1) | ||||

| (A2) | ||||

| (A3) |

where (A2) follows from the facts that does not depend on due to strict additivity and , and (A3) follows from the bias-variance decomposition (add and subtract ) and noting when .

For asymptotic purposes, note that are fixed with respect to , hence is as well. They may be regarded as constants as we take .

The analogs of and , for imputed potential outcomes are, respectively

| (A4) |

Compare these to (4) and (3). We also have, conditional on , that . In general, consistent with previous patterns, analogs of population quantities have superscript “”, while those of observed quantities have subscript “”.

Proof of Theorems 1, 2, and 3.

We prove the sampling, followed by the randomization distribution claims.

Sampling distributions of , , and .

Randomization distributions.

We first show, for almost all realizations of the sequence of treatment assignments , that Assumption 1 holds for where are the standardized imputed potential outcomes. Clearly they always have mean 0 and variance 1, so it is enough to verify that, almost surely

| (A5) |

Starting with (A3), we have

where the last step is by Lemma A3. This shows the sequence is bounded away from 0, as and . Now we also have , no matter what the realization of the sequence is, by Lemma A4. These two facts together show (A5).

Because by Lemma A3, we for the rest of the proof fix a sequence of along which . The only remaining randomness then comes from . Note for that because from the fact that the imputed potential outcomes satisfy (2). In particular, the standardized imputed potential outcomes satisfy , i.e., . Hence, by Proposition 3, we have

because the standardized imputed potential outcomes have covariance structure and . Next, for , we have

by Proposition 2 and because the standardized imputed potential outcomes have variances 1. It follows by (A4) that

We thus finally have by Lemma A1

and with for the and statistics:

Extending Theorem 1 to the case of stratified experiments or vector potential outcomes is straightforward. We also supply their proofs for completeness.

Proof of Theorem 4.

We prove the sampling, followed by the randomization distribution claims.

Sampling distribution of .

Randomization distribution of .

We first show Assumption 1 holds almost surely within each stratum for the imputed potential outcomes . Because the original potential outcomes satisfy Assumption 1 in each stratum, Lemma A4 gives . Put . In stratum , the mean vector is and the covariance structure is , where