Thresholding at the monopoly price: an agnostic way to improve bidding strategies in revenue-maximizing auctions

Abstract

We address the problem of improving bidders’ strategies in prior-dependent revenue-maximizing auctions and introduce a simple and generic method to design novel bidding strategies if the seller uses past bids to optimize her mechanism. We propose a simple and agnostic strategy, independent of the distribution of the competition, that is robust to mechanism changes and local (as opposed to global) optimization of e.g. reserve prices by the seller. This strategy guarantees an increase in utility compared to the truthful strategy for any distribution of the competition. In textbook-style examples, for instance with uniform [0,1] value distributions and two bidders, this no-side-information and mechanism-independent strategy yields an enormous 57% increase in buyer utility for lazy second price auctions with monopoly reserves.

When the bidder knows the distribution of the highest bid of the competition, we show how to optimize the tradeoff between reducing the reserve price and beating the competition. Our formulation enables to study some important robustness properties of the strategies, showing their impact even when the seller is using a data-driven approach to set the reserve prices. In this sample-size setting, we prove under what conditions, thresholding bidding strategies can still improve the buyer’s utility.

The gist of our approach is to see optimal auctions in practice as a Stackelberg game where the buyer is the leader, as he is the first one to move (here bid) when the seller is the follower as she has no prior information on the bidder.

Keywords:

Revenue-maximizing auctions strategic bidders reserve prices.1 Introduction

Auctions currently play a key role in the internet ecosystem through online advertising [3, 7, 4]. Ad slots are sold to advertisers by a publisher following more or less explicit mechanisms, i.e., a type of auction with specific rules. Those auctions take place on platforms called “ad exchanges” [29], either in a multi-item fashion in the search setting or in a single-item fashion in the display advertising setting. One of the most common type of auctions used in the latter setting is the classical second price auctions with reserve prices. These auctions are myopically truthful, as it is dominant for buyers to bid their true valuation at each individual auction, and even revenue-maximizing for identical bidders [30, 33].

Since the influential paper of Myerson [30], the revenue-maximizing auction literature has assumed that bidders’ value distributions are common knowledge among the seller and the bidders. The classical reasoning [3, 19] behind this traditional assumption is that the seller is choosing incentive compatible auctions such as Vickrey auctions; “hence”, since in a one shot second price auction it is optimal to bid one’s own valuations, the seller can safely expect that past bids reflect past valuations. An approximation of the buyer’s distribution of valuations easily follows. Then, to tackle the approximation error on the value distribution, a recent line of work has focused on learning the optimal mechanism assuming the seller has access to a batch of i.i.d. examples of bidders’ valuations [28, 32].

Several works have already shown that if bids are used in order to design the mechanism, the bidders should no longer bid truthfully [35, 22, 26, 2]. However, they do not exhibit strategies which work in the general setting with arbitrary value distributions and do not address cases where bidders only have partial and noisy access to the competition’s distribution. Indeed, in practice, ad platforms disclose little information to participants.

Our paper introduces a simple, general and robust method to design bidding strategies adaptive to prior-dependent revenue maximizing auctions. This method works with very general value distributions, asymmetries between bidders and various revenue maximizing mechanisms. It also tackles practical settings where no prior information on the competition is available. It should enable practitioners to easily improve their bidding strategies.

1.1 Framework and related work

Starting with the seminal work of [30], a rich line of works indicates the type of auctions that is revenue-maximizing for the seller. In the case of symmetric bidders [30], one revenue maximizing auction is a second price auction with a reserve price equal to the monopoly price, i.e, the price that maximizes ( being the value distribution of the bidder). However, in most applications, the symmetry assumption is not satisfied [19]. In the asymmetric case, the Myerson auction is optimal but difficult to implement in practice [27]. In this case, a second price auction with well-chosen reserve prices guarantees at least of the optimal revenue [20].

Revenue maximizing auctions play a big role in the internet economy [25, 32] because there exist a lot of heterogeneities between bidders and a low number of participants per auction [26]. In this context, they have a clear impact on sellers’ revenues since the ratio between revenues of the Myerson auction (the optimal revenue-maximizing auction) and those of a second price auction without a reserve price (the welfare-maximizing auction) is of order with the number of bidders [17].

Practical implementation of revenue-maximizing mechanisms requires that the seller knows the bidders’ value distributions beforehand, which practically may not be the case. More precisely, assume the valuation of a bidder is drawn from a specific distribution ; a bidding strategy for bidder is a mapping from into that indicates the actual bid when the value is . As a consequence, the distribution of bids is the push-forward of by . We can highlight different classes of auction problems depending on the information available to the seller that she might use to optimize her mechanism.

-

(S1)

is known to the seller. This is the traditional setting studied in Myerson’s seminal paper where he assumed that ’s are common knowledge among the bidders and the seller.

-

(S2)

is known to the seller. It is an idealized setting where the seller has no uncertainty about , e.g. because she receives an infinity of i.i.d. bids from the buyers.

-

(S3)

the seller has only access to a finite number of examples of bids. She can only compute an approximation of denoted by . This is the most realistic case.

The last setting (S3) best describes real-world practice and the objective of most of mechanisms is to make sure that bidders are truthful. Indeed, the bid distribution is then equal to the value distribution and the seller is back to the full information setting (S1) required to implement revenue-maximizing mechanisms. Hence, designing incentive compatible mechanisms is a crucial requirement to elicit the bidders’ private value distributions. The remaining question of empirical estimation was theoretically addressed by [10, 21, 12] looking at the sample complexity of a large class of auctions assuming access to i.i.d. examples of the value distribution.

In order to design such incentive compatible mechanisms, sellers have been relying on different assumptions. In the traditional setting of auction theory, sellers assume that bidders are myopic and do not optimize their long term-utility [31, 32]. However, in the context of internet auctions, given the volume and frequency of auctions - billions a day -, sellers cannot assume myopic behavior by the bidders. In this context, one needs to account for the dependency introduced by the seller on the bidder strategy when using past bids to adapt the mechanism (for instance by optimizing the reserve price). In such cases, non-myopic bidders optimizing their long-term expected utility have an incentive to be strategic against this adaptation of the mechanism. To solve this issue, [5, 26, 18] exhibited mechanisms that are incentive compatible (up to a small number of bids) under the assumption that bidders are almost myopic or impatient – i.e. they have a fixed discount on future utilities. Unfortunately, it comes at the cost of introducing an asymmetry between the bidders having a discounted long-term utility, and the seller having an undiscounted long-term revenue (in effect being infinitely patient). Another way to prevent bidders from being strategic is to adapt the mechanism (e.g. reserve price) based on the competition of a bidder rather than based on the bidder themselves [6, 22, 14]. A limitation of this type of approach is the need to rely on a (partial) symmetry of the bidders: any bidder needs to have competitors with (almost) the same value distribution as her. In particular and as noticed in [14], it cannot handle the existence of any dominant buyer, i.e., a buyer with higher values than the other bidders. This is a limited setting as revenue-optimizing mechanisms are mostly needed when the buyers are heterogenous, for otherwise the competition itself contributes to optimizing the revenue of the seller [9]. In the real-world setting of online advertising, with asymmetric bidders and no specific asymmetry between seller and buyers on future utilities, none of these mechanisms ends up being able to enforce truthful bidding. This is illustrated by recent works proposing a method to empirically detect when a mechanism is not truthful from the point of view of a non-myopic bidder [24, 16, 11]. In this setting, this leaves us with an important question:

What should “good” bidders’ strategies be?

Closely related to our work, Tang and Zeng [35] derive a Nash equilibrium in our specific setting but their approach does not enable them to derive equilibrium in some restricted class of strategies that are widely used in practice and do not tackle any robustness issues related to their strategies. The main objective of our work is to exhibit and prove the existence of simple and robust strategies that can be used by practitioners facing a smart data-driven selling mechanism. Understanding possible simple strategic behaviours will also help sellers to design robust strategy-proof selling mechanisms. On a technical level, our approach is based on calculus of variations ideas and appears to be new in the auction context.

1.2 Main contributions

We introduce a method to derive strategies for the bidder in the context of a seller using her past bids to adapt the mechanism towards a revenue-optimization objective. We mainly focus in this paper on the case where the mechanisms are lazy second price auctions with monopoly reserve price and extend some of the results to other classes of auctions such as the Myerson auction, the eager second price auction with monopoly price or the boosted second-price auction.

1.2.1 Timing of the game

We first consider an idealized game where the buyer discloses their bid distribution and the seller optimizes their auction mechanism based on this distribution. For concreteness, consider the case of second price auctions. In the classical setting of auction theory, the buyer is asked to reveal their bid distribution first; facing “truthful auctions”, they reveal their value distribution. The seller then optimizes their mechanism based on this information, finding an optimal reserve price for this buyer. This is a Stackelberg game, as the two players do not play at the same time. In this instance, the seller is the leader and the buyer is the follower. Most of the literature on optimal auctions is focused on this version of the Stackelberg game.

However, if the buyer knows that the seller is going to find an optimal mechanism, and hence will optimize the auction based on the information given by the buyer’s bid distribution, the buyer can anticipate this optimization to increase their utility. The order of the Stackelberg game is then reversed. The buyer becomes the leader and the seller the follower. The buyer reveals their bid distribution knowing the optimization problem that the seller will solve. In second price auctions with reserve prices, the buyer has an incentive to disclose a bid distribution that may be different from their value distribution as they then will be facing a more favorable reserve price by doing so. Our paper is focused on this version of the Stackelberg game, as we focus on the bidder standpoint.

More formally, the timing of the game we consider is the following :

-

1.

the seller chooses a mapping from to a specific auction mechanism ,

-

2.

based on this mapping, each buyer chooses a bidding strategy ,

-

3.

the payoff of the buyers is their utility under and the seller’s payoff is the revenue under this mechanism.

This objective is particularly relevant in modern applications as most of the data-driven selling mechanisms are using large batches of bids as examples to update their mechanism. In practice however, the problem is slightly different. Classically, the seller could first sell goods in a second price auction without reserve price [5, 26, 18]. The buyer would then be incentivized to reveal their value distribution - through participating in a large number of those auctions. And the seller would then optimize the reserve price based on this value distribution for the remaining auctions. This is again a Stackelberg game where the seller is the leader. However, if the buyer is aware that their bid distribution in the first phase is going to be used in a second phase to run seller-optimal auctions, the buyer can take the lead in the Stackelberg game by anticipating the optimization performed by the seller.

| Optimal reserve price | Utility | |||||||

| K=1 | K=2 | K=3 | K=4 | K=1 | K=2 | K=3 | K=4 | |

| Truthful bidding | 0.5 | 0.5 | 0.5 | 0.5 | 1/8 | 1/12 | 11/192 | 13/320 |

| Zero bidding | 0.0 | 0.0 | 0.0 | 0.0 | 1/2 | 0.0 | 0.0 | 0.0 |

| (+400%) | (-100%) | (-100%) | (-100%) | |||||

| Divide values by 2 | 0.25 | 0.25 | 0.25 | 0.25 | 1/4 | |||

| (+100%) | (+13%) | (-37%) | (-63%) | |||||

| Thresholded at | 0.25 | 0.25 | 0.25 | 0.25 | 1/4 | |||

| the monopoly price | ||||||||

| (Theorem 2.1) | (+100%) | (+57%) | (+33%) | (+20%) | ||||

| \hlineB4.0 Optimal regularity- | 0.0 | 0.162 | 0.204 | 0.22 | 1/2 | |||

| preserving strategies | ||||||||

| (Theorem 3.1) | (+400%) | (+76%) | (+38%) | (+21%) | ||||

1.2.2 A simple textbook example

To introduce our contribution, we first consider the posted price setting where bidder plays against one seller. We assume, for simplicity of this introductory example, that bidder’s value distributions is , i.e. uniform on the interval [0,1]. Let initially consider that the bidder is bidding truthfully, i.e, . In this case, and the seller will set as reserve price the monopoly price by maximizing the monopoly revenue . This monopoly price is equal to 0.5 in the case of . Note that this maximization problem is computationally simple as the monopoly revenue is a concave function if the value distribution is regular. The bidder can obviously do better. If he bids all the time zero (or arbitrarily close to zero), will be equal to a point mass at zero. Through computing the optimal reserve price corresponding to , the seller chooses zero, obviously maximizing bidder’s utility. The problem we consider derives from a simple extension of this example to the case of K bidders. In a lazy second price auction, the optimal reserve price for each bidder is still the monopoly price. Yet, as soon as there is some competition, bidders can not bid zero as they get zero utility in this case. They have to tradeoff between beating the competition and decreasing their reserve price.

Our first result consists in deriving a simple strategy which guarantees to the bidder an increase in utility compared to the truthful strategy for any distributions of the competition. This increase depends on the distribution of the competition. Yet, by playing this strategy, the bidder is sure to do better than by bidding truthfully. This is an important practical result as in many ad platforms, bidders have to bid without knowing the distribution of the competition. This strategy, that we call thresholding at the monopoly price, has also the key property of making simple the optimization problem of the seller, i.e. if is regular, induced by this strategy on is also regular. We say that this strategy is regularity-preserving.

Definition 1 (Regularity-preserving strategy)

Consider a bidder with a regular value distribution . We say that a bidding strategy is regularity-preserving, if the bid distribution induced by on is a regular distribution.

As shown in Table 1, we then extend our first result by deriving, for any given regular distribution, the optimal strategy in the class of increasing and regularity-preserving strategies. To compute this strategy, the bidder has to know exactly the distribution of the competition. Our result enables us to compute analytically by how much the bidder increases his utility when knowing precisely the distribution of the competition.

1.2.3 Our main results

The paper is organized as follows. Section 2 provides a walkthrough of the main technical ideas supporting our work to provably improve the response of one bidder independently from the behavior and knowledge of other bidders. In Theorem 1, we define this new strategy, independent of the distribution of the competition, which enables to increase the strategic bidder’s utility compared to the truthful strategy for any distribution of the competition. This theoretical study introduces a practical method to design bidding strategies in revenue-maximizing auctions that we call thresholding the virtual value. In Section 3, we generalize this result by exhibiting, for a given distribution of the competion, what is the optimal strategy in the class of regularity-preserving strategies (Theorem 2). We show that this strategy belongs to the class of strategies that we introduced in Section 2. This optimal strategy depends on the distribution of the competition and corresponds to the optimal tradeoff between decreasing the reserve price and beating the competition.

In Section 4, we show that our results can be made robust to other strategic bidders and in Section 5 to sample-approximation error by the seller, tackling the case where only an estimator is available to the seller. If the seller uses a data-driven approach as proposed in [32] to set the reserve prices in a lazy second-price auction, we show under what conditions thresholding bidding strategies can improve buyer’s utility.

2 Improving over the truthful strategy for any distributions of the competition

In this section, we show how to improve the strategy of one bidder when he does not have any information about the competition. We assume that the strategies of the other bidders are fixed and do not depend on the strategic bidder’s strategy and that the seller has perfect knowledge of the bid distributions to choose the mechanism. We relax this latter assumption in Section 5.

2.1 Notations and setting

We recall that is the value distribution of bidder and her strategy that maps values to bids. The corresponding distribution of bids is then , the push-forward of w.r.t. . Notice that we have implicitly identified the distribution (resp. ) with its cumulative distribution function (cdf) and use both terms exchangeably. We use (resp. ) for the corresponding probability density function (pdf).

We denote by the corresponding virtual value function defined as

We use (resp. when there is no ambiguity) for the distribution of the highest bid of the competition to bidder . We call (resp. ) the associated density.

Throughout the paper we assume that the random variables associated with and are drawn independently.

We denote by the uniform distribution and the uniform distribution on [0,1].

For each theorem, we provide quite minimal assumptions needed on the value distribution for the proof to go through. However, as a summary, all the main results on the best response of the strategic bidder are true provided

-

•

A1 : the value distribution has moments,

-

•

A2 : the value distribution has a density , with on the support of (in particular has no atoms and its cumulative distribution function is continuous)

-

•

A3 : the virtual value is increasing and crosses 0 (though in many instances we really only need that it crosses 0 exactly once - in which case we denote the assumption by A3w)

This includes among others distributions the uniform and the exponential distributions. Nevertheless, for most of theorems, we do not need any regularities assumptions on the value distribution. Our theorem on the Bayes-Nash equilibrium (Theorem 4.1) further requires (A4) a compact support for the distribution as well as continuity of the density at the edges of the support. We however explain after the theorem how to extend it to Generalized Pareto and log-normal distributions (when the latter distributions are regular [15]). Finally, our theorem on robustness to approximation error of the seller (Theorem 3) requires (A5) in its stated form that the density be bounded below under the monopoly price. In conclusion, all our results apply for the most common distributions used in auction theory, provided they are truncated in an infinitesimal neighborhood near 0 and away from infinity (if needed) to avoid minor technical problems in the proofs. This does not compromise their wide applicability.

We assume that the seller runs a lazy second price auction with monopoly reserve price computed according to the distribution of bids she is observing or knows. We recall that in a “lazy” second price auction, the item is attributed to the highest bidder, if she clears her reserve price, and not attributed otherwise; the winner pays the maximum of the second highest bid and her reserve price.

2.2 Improving any strategies for any competition distributions

In the initial example presented in the introduction, we considered several classical shading strategies, e.g. zero bidding or linear shading, that can be used by a strategic bidder. As shown in Table 1, they are suboptimal and perhaps more importantly do not guarantee a positive uplift relative to the truthful strategy for any distribution of the competition. For instance, in the textbook example with , dividing bids by two gets a positive uplift with two bidders but not with three. This is a severe limitation since in some situations, the seller prevents bidders from computing the distribution of the competition by e.g. not saying whether the bidder paid the second highest bid or their reserve price. In practice, approximating the distribution of the competition also requires an important infrastructure. We show that there exists a simple strategy that guarantees a positive uplift in utility compared to the truthful strategy for any distributions of the competition. This strategy is of practical interest since bidders only need to know their own value distribution to compute this strategy. We will extend this result in Section 3 by showing that the best response in this setting is a simple extension of the strategy that we now introduce.

When the reserve price is computed from - the bid distribution induced by using on - we have to make a distinction between the reserve price and the reserve value .

Definition 2 (Reserve value)

Consider a non-decreasing strategy . We call reserve value the smallest value above which the seller accepts bids.

If the bidder bids truthfully, their reserve value is equal to their reserve price. If is increasing and is the reserve price associated with the strategy , we have . If , if we consider , we have and . By dividing bids by two, the strategic bidder decreases their reserve price but does not change the reserve value : it is the same as if they were bidding truthfully.

By contrast, we now show that for any distributions of the competition, the bidder can improve a specific bidding strategy by giving an incentive to the seller to accept all bids. It does not decrease the payment of the strategic bidder and increases his utility for any distributions of the competition.

Theorem 2.1

Let be an increasing strategy with associated reserve value in a lazy second price auction. Suppose Assumption A2 applies to and that the left-end point of its support is 0. Suppose the bid distribution associated with has a virtual value. Assume that the other bidders’ strategies are fixed. Then there exists another bidding strategy such that for any distributions of the highest bid of the competition:

-

1.

A reserve value associated with is 0. is increasing.

-

2.

, i.e., the utility of bidder is higher;

-

3.

, i.e., the payment of bidder to the seller is also higher,

The following continuous function fulfills these conditions:

| (1) |

Having reserve value equal to zero means that the seller accepts all bids of the strategic bidder. It also means that the reserve price is equal to the minimum bid of the strategic bidder. This result can be applied to improve any preexisting shading strategy. A most important case is to apply this theorem to the truthful strategy, showing that there exists a strategy improving the truthful strategy regardless of the competition distribution. The proof is in Appendix. We now explain why we can improve any strategy in this setting without knowing the distribution of the competition. Myerson’s Lemma is a key element in this understanding.

2.2.1 The fundamental Myerson lemma

Myerson’s lemma [30] is a fundamental result in auction theory.

Lemma 1 (Integrated version of the Myerson lemma)

Assume that has a density (which is positive everywhere) and finite mean, i.e. Assumptions A1 (with ) and A2 are satisfied. Suppose that bidder ’s bids are independent of the bids of the other bidders and denote by the cdf of the maximum of the other bidders’ bids. Suppose a lazy second price auction with reserve price for bidder i denoted by is run. Then the payment of bidder to the seller can be expressed as

If the other bidders are bidding truthfully, is the distribution of the maximum value of the other bidders.

The formal proof is in Appendix. Lemma 1 yields that it is enough to consider the virtual value to deduce the payment in the lazy second price auction. This explains why the optimal reserve price is equal to when crosses 0 exactly once and is positive beyond that crossing point A3w (that is of course the case when is increasing and crosses 0 A3) : the derivative of with respect to the reserve price has the opposite sign as that of .

Using the notations introduced previously, it is optimal for the seller to choose as reserve price for bidder the monopoly price corresponding to her bid distribution, and Lemma 1 implies that the expected payment of bidder in the optimized lazy second price auction is equal to

In order to simplify the computation of the expectation and remove the dependence on , we rewrite this expected payment in the space of values using the fact that the strategic bidder is using an increasing strategy . We will only consider increasing strategies in the rest of the paper. To do so, we define:

With this new notation, we can rewrite the expected payment of the strategic bidder

and derive her expected utility as a function of as

| (2) |

where is the reserve value. If crosses 0 exactly once and is positive beyond that crossing point, i.e. it satisfies A3w, . If we call the reserve price of bidder and increasing , the reserve value is equal to .

If we consider only increasing differentiable strategies, and we denote by the class of such functions, the problem of the strategic bidder is therefore to solve with defined in Equation (2). This equation is crucial, as it indicates that optimizing over bidding strategies can be reduced to finding a distribution with a well-specified . Our results extend to the case where the strategies are increasing and differentiable except at finitely many points, as we only need to be absolutely continuous for the previous result to go through.

A crucial difference between the long term vision and the classical, myopic (or one-shot) auction theory is that in our setup bidders maximize expected utility globally over the full support of the value distribution. In the classical myopic setting, bidders determine their bids so as to maximize their expected utility at each value. In our setup, the strategic bidder also accounts for the computation of the reserve price, a function of her global bid distribution. He might therefore be willing to sometimes over-bid (incurring a negative utility at some specific auctions/values) or underbid (lose some auctions that he would have won otherwise) if this reduces her reserve price. Indeed, having a lower reserve price increases the utility of other auctions. Lose small to win big. In other words, the strategy trades-off ex-post individual rationality (IR) for higher utility (of course ex-ante IR still holds). This reasoning makes sense only with multiple interactions between bidders and seller.

2.2.2 Thresholding the virtual value

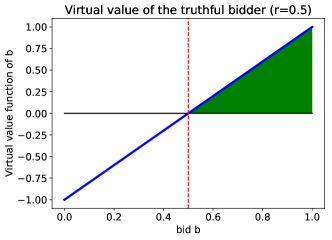

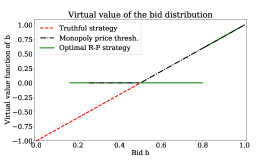

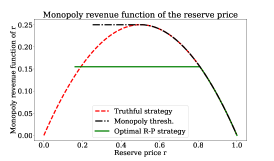

To explain why we can easily improve a bidding strategy, let us describe the following elementary example (see also Figures 1 for graphical illustrations). We assume that the value distribution of the bidder is uniform between 0 and 1 (denoted , a standard example in [23], see e.g. Example 2.1 and subsequent chapters). If the strategic bidder were bidding truthfully, her virtual value would be negative below 0.5 and the seller would set the reserve price to 0.5. What would happen if the bidder were able to send a virtual value equal to zero below 0.5? Then the seller would not have any incentives to block some of the bids since the virtual value is non-negative everywhere. Notice that, since the virtual value is zero below 0.5, the seller receives exactly the same expected payment as in the previous setup.

We define a welfare-benevolent seller as a seller who - when indifferent from a revenue standpoint between two reserve prices - chooses the lowest one, i.e, the one yielding the maximum welfare. This is a standard concept in game theory. In the framework where the seller has a cost to sell the item [8], it corresponds to a cost-to-sell of zero.

If the seller is not benevolent, instead of looking for a strategy such that on , the buyer will try to satisfy with small. In that case the seller has a strict incentive to take all bids and hence lower the reserve price.

We call this technique thresholding the virtual value: finding a bidding strategy such that the virtual value of the induced distribution is equal to zero (or to a threshold , for arbitrary small if the seller is not welfare benevolent) below the current reserve price.

We now show formally how to find a bidding strategy such that the virtual value of the induced bid distribution is equal to zero below a certain threshold.

|

|

2.3 Deriving formally the corresponding bidding strategy

Before carrying on with reasoning on the virtual value, such as in our motivating example, we need to ensure we can find the corresponding strategy that will expose a bid distribution with the corresponding virtual value to the seller. The two following technical lemmas show how to deduce from a given .

Lemma 2

Suppose , where is increasing and differentiable and is a random variable with cdf and pdf satisfying A2. Then

| (3) |

Proof

We have with and . Then,

The above results holds when is increasing, continuous, and differentiable except at finitely many points. in Equation (3) is then the definition at all the points of differentiability of . Note that Lemma 1 then applies as it relies on integration by parts which is valid for functions that are continuous and differentiable except at finitely many points.

The second lemma shows that for any function we can find a function such that .

Lemma 3

Let be a random variable with cdf and pdf satisfying A2. Let be in the support of , and . We call

| (4) |

Then, if ,

If for some , and is non-decreasing on , for . Hence is increasing on if is non-decreasing and .

Proof

The result follows by simply differentiating the expression for , and plugging-in the expression for obtained in Lemma 2. The result on the derivative is simple algebra.

The two technical lemmas 2 and 3 show that for any non-decreasing function , we can find a strategy such that the bid distribution induced by using on verifies for all in the support of , under Assumption A2.

In Section 2.2.2, we explained why sending to the seller a virtual value equal to zero when the initial one was negative increases the bidder’s expected utility. To derive the corresponding bidding strategy from the virtual value, we need to solve the simple ODE defined in Lemma 2. More formally, Theorem 2.1 shows how to improve any strategy assuming the bidder knows the current reserve price or value, which were computed to maximize bidders’ payment using Myerson’s Lemma above. This theorem still holds for non-regular value distributions and in the asymmetric case when the bidders have different value distributions.

|

|

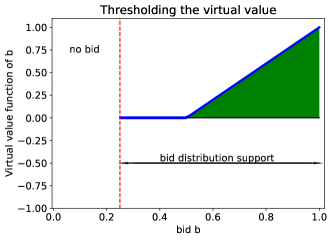

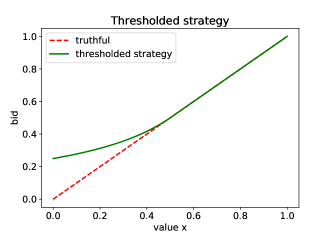

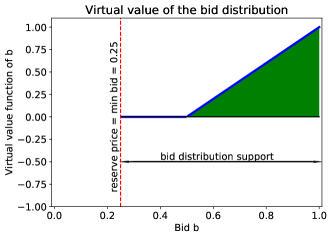

This improvement in bidder utility does not depend on the estimation of the competition and thus can easily be implemented in practice. We call this technique thresholding the virtual value at the monopoly price. We plot in Figure 2, the bidding strategy corresponding to “thresholding the virtual value at the monopoly price” - see formal definition in Equation (1) for in general form - when the strategic bidder’s value distribution is and the virtual value of the bid distribution induced by on . We recall that the monopoly price corresponding to is equal to . We remark that the strategy consists in overbidding below the monopoly price of the initial value distribution. The strategic bidder is ready to increase pointwise her payment when she wins auctions with low values in order to get a large decrease of the reserve price (going from to ). The minimum bid is equal to 0.25 and is equal to the reserve price. This explains why the expectation of the virtual value corresponding to the bid distribution is not equal to zero since the minimum bid is not zero.

Overall, the payment of the bidder remains unchanged compared to when the bidder was bidding truthfully with a reserve price equal to 0.5. Thresholding the virtual value at the monopoly price amounts to overbidding below the monopoly price, effectively providing over the course of the auctions an extra payment to the seller in exchange for lowering the reserve price/value faced by the strategic bidder. This strategy unlocks a very substantial utility gain for the bidder.

2.4 Impact on bidder’s utility

Naturally, a key question is to understand the impact of this new strategy on the utility of the strategic bidder. We compare the situation with two bidders bidding truthfully against an optimal reserve price and the new situation with one bidder using the thresholded strategy and the second one bidding truthfully. We assume, as is standard in many textbooks and research papers numerical examples, that their value distribution is .

Then, in this specific illustrative example, the strategic bidder utility increases from to (a 57% increase) and the welfare increases from 7/12 to . (a 8% increase).

Using our technique, the strategic bidder improves their tradeoff between having a low reserve price and beating the competition compare to truthful bidding. The bidder could also underbid to decrease the reserve price. However, by underbidding, they would decrease their probability to beat the competition in some situations. Using the same example, if the value distribution is , if the bidder divides their bid by two, they also get a reserve price of 0.25. Yet, if there are two competitors with , this strategy incurs a decreases in utility from 0.057 (utility when truthful) to 0.041 (-28%). Our strategy gets a utility 0.076 (+33%) in the case of two competitors. Another fundamental difference is that our strategy, by overbidding, in the symmetric setting where all bidders have the same value distributions, increases the welfare of the system while underbidding strategies decreases it (with one competitor, if one bidder divides their bids by two, the welfare goes from 0.583 to 0.289 (-50%). This is one reason explaining why the strategic bidder can get higher utility by overbidding : they capture a large fraction of the resulting increase in welfare.

In this example, as the initial reserve prices of the bidders are the same, we also remark that the utility of the truthful bidder and the global revenue of the seller remain unchanged.

To extend to other value distributions, with a log-normal distribution (which is widely used to model value distributions in online advertising) with parameters and , the utility of the strategic bidders goes from 0.791 to 1.025 (a 29.5% increase).

In this section, we introduced a simple strategy which guarantees a positive increase of utility for any possible distribution of the competition. In the next section, we show that by tuning a single parameter, i.e. the value where we threshold the virtual value, we can compute the optimal regularity-preserving strategy for a given distribution of the maximum bid of the competition.

3 Optimal bidder’s response given the distribution of the competition

The formulation introduced in the previous section offers a way to consider auction problems as functional-analytic problems and provides an alternative to game-theoretic methods used to derive optimal strategies and equilibria. We now extend the result of the previous section to the case where the strategic bidder has access to the distribution of the highest bid of the competition. We show, for a specific given distribution of the competition, what is the optimal increasing and regularity-preserving (RP) strategy (Definition 1)).

We impose the condition of being regularity-preserving since if the monopoly revenue curve function of the reserve price has multiple local optima (in the case where the bid distribution is not regular), it requires in practice that the seller runs a global optimization procedure to compute all possible equivalent reserve prices. In practice, sellers are using various gradient descent algorithms [32, 34], forcing the bidder to use regularity-preserving strategies guaranteeing the seller converges to the right reserve price. We show in Section LABEL:sec:numerical_approach in some numerical experiments that when a bidding strategy implies two local optima of the payment curve, it does not make a difference for the seller but can change drastically bidder’s utility.

We presented in the previous section a direct way to compute the expected utility of a bidding strategy when the seller is using a second price auction with personalized reserve price and the other bidders are bidding truthfully:

| (5) |

with and . In this section, we assume that the bidder has now access to the distribution of the highest bid of the competition that we denote by ( being the associated pdf).

In the following, unless otherwise stated, the expectation is taken according to the value distribution of the bidder. In order to be able to derive optimal strategies, we make use of the previous expression and obtain the following lemma (we remove the subscript as it is now clear we consider bidder ).

We can optimize among the strategies with thresholded virtual values that we introduced in Section 2. We define more formally this class of bidding strategies.

Definition 3 (Thresholded bidding strategies)

A bidding strategy is called a thresholded bidding strategy if and only if there exists such that for all . This family of functions can be parametrized with

with and continuous and increasing.

This class of continuous bidding strategies has two degrees of freedom : the threshold such that for all and the strategy used beyond the threshold. We do not restrict the functions that can be used beyond the threshold (beside being continuous and increasing). All the strategies defined in this class have the property that their reserve value is equal to zero, i.e. their reserve price is equal to their minimum bid, when the seller is welfare benevolent and the virtual value of is positive beyond . We first prove that the optimal regularity-preserving strategy belongs to the class of thresholded strategies. (We repeat that throughout the paper we assume that the strategic bidder draws values independently of the competition.)

Lemma 4

Let us consider regular (A2 and A3) and denote by and . Suppose further that (as implied by A1 with ) as where is the right-end of the support of ( could be infinite). If satisfies , a best-response in the class of increasing regularity-preserving strategies belongs to the class of thresholded strategies.

The formal proof is in Appendix. The proof is in several steps and exploits the property that has to be non-decreasing (since is regularity-preserving). We first show that, without loss of generality, the class of possible best-response strategies can be restricted to the class of strategies with non-negative . Then, given a best-response in the class of of strategies satisfying the properties above, we show that there exists a thresholded strategy with at least the same utility. A similar lemma can be found in [35]. One main difference is that we place ourselves in the space of strategies instead of the space of bid distributions, which enables us to characterize precisely the required properties of the class of strategies considered and then, very importantly, to derive numerical methods for other types of auctions.

We now show that there exists an optimal threshold for the strategic bidder that depends on the competition and that the optimal strategy to use for is to be truthful. We derive this result by computing the directional derivatives of the utility function defined in Equation (5).

Theorem 3.1

Under the same assumptions as in Lemma 4, a best response in the class of increasing and regularity-preserving strategies consists in thresholding at and bidding truthfully beyond , where satisfies the equation, if is the distribution of the largest bid of the competition,

|

|

|

In Theorem 2.1, we proved that when the strategic bidder does not know the distribution of the highest bid of the competition, he can use the thresholded strategy at his monopoly price and increases his utility compared to truthful bidding. Theorem 3.1 gives the optimal threshold when the strategic bidder knows .

Some numerical results We consider the situation where we have 1 strategic bidder, and 1 non-strategic one, both with value distribution. We recall that the strategy introduced in Section 2 was to bid truthfully beyond the monopoly price ( here) and using Theorem 2.1 before. This strategy yields a utility of , a increase over the standard truthful bidding revenue. The optimal strategy coming out of Theorem 3.1 consists in bidding truthfully beyond and using the thresholding completion before. The utility is then around 0.1468, a 76% percent increase in bidder utility compared to bidding truthfully (truthful bidding yields a utility of ). This second strategy yields a higher utility for the strategic bidder but requires some knowledge of the competition. The optimal strategy in Theorem 3.1 overbids on small values, underbids on intermediate values and is truthful on high values. We also recover that with no competition, the optimal strategy is to bid zero for any possible valuations. In Table 1, we also notice that the difference in utility is decreasing with the number of players since, with increasing competition, the strategic bidder can not lower his bid for values above his monopoly price.

4 Robustness to other strategic bidders

We have only discussed so far the situation where one bidder is strategic and the other bidders do not directly react to this strategy. It is a reasonable assumption in practice since the number of bidders able to implement sophisticated bidding strategies appears to be limited. We now investigate the case where all bidders are strategic. We assume that they all have the same value distribution . Interestingly, we can analytically compute what is the Nash equilibrium in the class of thresholded strategies introduced in Definition 3.

We can state a directional derivative result in this class of strategies by directionally-differentiating the expression of . As in Theorem 3.1, it implies the only strategy with 0 “gradient” in this class is truthful beyond a value ( is different from the one in Theorem 3.1), where can be determined through a non-linear equation. The proof is in Appendix. We can prove that there exists one unique symmetric Bayes-Nash equilibrium in the class of thresholded strategies which are robust to local optimization of the seller. In this equilibrium, bidders get the utility they receive in a second price auction without reserve price.

Theorem 4.1

We consider the symmetric setting where all the bidders have the same value distributions, satisfying Assumptions A1 and A2. We furthermore assume for simplicity that the distribution is supported on [0,1]. Suppose this distribution has density that is continuous at 0 and 1 with - i.e. A4 - and crosses exactly once and is positive beyond that crossing point, i.e. A3w. There is a unique symmetric Nash equilibrium in the class of thresholded bidding strategies defined in Definition 3. It is found by solving

| (6) |

to determine and bidding truthfully beyond .

Moreover, if all the bidders are playing this strategy corresponding to the unique Nash equilibrium, the revenue of the seller is the same as in a second price auction with no reserve price. The same is true of the utility of the buyers.

The formal proof is in Appendix.

With appropriate shading functions, the bidders can recover the utility they would get when the seller was not optimizing her mechanism to maximize her revenue, a result independently found in [35] with a different proof.

5 Robustness to approximation error of the seller

In practice the seller needs to estimate the distribution of the buyer and hence does not have perfect knowledge of the bid distribution . The buyer needs to find a robust shading method, making sure that the seller has an incentive to lower her reserve price, even if she misestimates the bid distribution. , If the seller is using a data-driven approach as in [32] to set the reserve prices, we can still show that thresholding bidding strategies can improve the buyer’s utility.

Lemma 5

Suppose that the buyer uses a strategy under her value distribution . Suppose the seller thinks that the value distribution of the buyer is . Call and the hazard rate functions of the two distributions Then the seller computes the virtual value function of the buyer under , denoted , as

As an aside, we note that by definition we have . We have the following useful corollary pertaining to the thresholded strategies described in Section 3.

Corollary 1

If the buyer uses the strategy defined as

we have, for , In particular, we have for

If for all , and , we have

The previous results already give some results about the impact of empirically estimating the value distribution by the empirical cumulative distribution function on setting the reserve price. However because our approximations are formulated in terms of hazard rate, applying those results would yield quite poor approximation results in the context of setting the monopoly price through ERM. This is due to the fact that estimating a density pointwise in supremum norm is a somewhat difficult problem in general, associated with poor rates of convergence. We refer the interested reader to [36] for more details on this question. So we now focus on the specific problem of empirical minimization and take advantage of its characteristics to obtain better results than would have been possible by applying the results of the previous section.

Theorem 3

Suppose the buyer has a continuous and increasing value distribution , supported on , , with the property that if , , where . Suppose that . Suppose the buyer uses the strategy defined as

Assume she samples values i.i.d according to the distribution and bids accordingly in second price auctions. Call . In this case the (population) reserve value is equal to 0. Assume that the seller uses empirical risk minimization to determine the monopoly price in a (lazy) second price auction, using these samples. Call the reserve value determined by the seller using ERM. We have, if and with probability at least ,

In particular, if is replaced by a sequence such that in probability, goes to 0 in probability like .

Informally speaking, our theorem says that using the strategy with slightly larger than will yield a reserve value arbitrarily close to 0. Hence the population results we derived in earlier sections apply to the sample version of the problem. In future work, we plan to design games between bidders and seller where the seller can change the mechanism at any point and bidders can update their bidding strategy changing the bid distribution observed by the seller. We also plan to consider the problem of the strategic reaction of the seller to the type of bidding strategies we have proposed in this paper. From an industrial standpoint, our work provides a new argument to come back to simple and more transparent auction mechanisms that are less subject to optimization on both the bidders’ and the seller’s sides.

6 Conclusion

Reserve prices are learned in many practical situations using past bids. In this case, the celebrated second price auction is not anymore truthful. We propose an easy-to-implement strategy - dubbed “thresholding the virtual value at the monopoly price” - which keeps unchanged the expected payment of the strategic bidder, and increases very substantially her utility, even when the bidder has no information about the competition. This is possible as the strategic bidder overbids below the monopoly price, which can be interpreted as a form of payment to the seller in exchange for a lower reserve price. When all the bidders become strategic, we show that they can recover all the utility lost due to the introduction of reserve prices at a Nash equilibrium in the class of strategies we propose. We proved that our strategies are robust to various information structure of the game and to sample approximation errors.

In future work, we plan to design games between bidders and seller where the seller can change the mechanism at any point and bidders can update their bidding strategy changing the bid distribution observed by the seller. We also plan to consider the problem of the strategic reaction of the seller to the type of bidding strategies we have proposed in this paper. From an industrial standpoint, our work provides a new argument to come back to simple and more transparent auction mechanisms that are less subject to optimization on both the bidders’ and the seller’s sides.

References

- [1]

- Abeille et al. [2018] Marc Abeille, Clément Calauzènes, Noureddine El Karoui, Thomas Nedelec, and Vianney Perchet. 2018. Explicit shading strategies for repeated truthful auctions. arXiv preprint arXiv:1805.00256 (2018).

- Allouah and Besbes [2017] A. Allouah and O. Besbes. 2017. Auctions in the Online Display Advertising Chain: A Case for Independent Campaign Management. Columbia Business School Research Paper No. 17-60 (2017).

- Amin et al. [2012] Kareem Amin, Michael Kearns, Peter Key, and Anton Schwaighofer. 2012. Budget optimization for sponsored search: censored learning in MDPs. In Proceedings of the Twenty-Eighth Conference on Uncertainty in Artificial Intelligence. 54–63.

- Amin et al. [2014] Kareem Amin, Afshin Rostamizadeh, and Umar Syed. 2014. Repeated contextual auctions with strategic buyers. In Proceedings of the 27th International Conference on Neural Information Processing Systems-Volume 1. 622–630.

- Ashlagi et al. [2016] Itai Ashlagi, Constantinos Daskalakis, and Nima Haghpanah. 2016. Sequential mechanisms with ex-post participation guarantees. In Proceedings of the 2016 ACM Conference on Economics and Computation. 213–214.

- Balseiro et al. [2020] Santiago R Balseiro, Ozan Candogan, and Huseyin Gurkan. 2020. Multistage Intermediation in Display Advertising. Manufacturing & Service Operations Management (2020).

- Balseiro et al. [2018] Santiago R Balseiro, Vahab S Mirrokni, and Renato Paes Leme. 2018. Dynamic mechanisms with martingale utilities. Management Science 64, 11 (2018), 5062–5082.

- Bulow and Klemperer [1996] Jeremy Bulow and Paul Klemperer. 1996. Auctions Versus Negotiations. The American Economic Review (1996), 180–194.

- Cole and Roughgarden [2014] Richard Cole and Tim Roughgarden. 2014. The sample complexity of revenue maximization. In Proceedings of the forty-sixth annual ACM symposium on Theory of computing. 243–252.

- Deng and Lahaie [2019] Yuan Deng and Sébastien Lahaie. 2019. Testing dynamic incentive compatibility in display ad auctions. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining. 1616–1624.

- Devanur et al. [2016] Nikhil R Devanur, Zhiyi Huang, and Christos-Alexandros Psomas. 2016. The sample complexity of auctions with side information. In Proceedings of the forty-eighth annual ACM symposium on Theory of Computing. 426–439.

- Dhangwatnotai et al. [2015] Peerapong Dhangwatnotai, Tim Roughgarden, and Qiqi Yan. 2015. Revenue maximization with a single sample. Games and Economic Behavior 91 (2015).

- Epasto et al. [2018] Alessandro Epasto, Mohammad Mahdian, Vahab Mirrokni, and Song Zuo. 2018. Incentive-aware learning for large markets. In Proceedings of the 2018 World Wide Web Conference. 1369–1378.

- Ewerhart [2013] Christian Ewerhart. 2013. Regular type distributions in mechanism design and -concavity. Economic Theory 53, 3 (2013), 591–603.

- Feng et al. [2019] Zhe Feng, Okke Schrijvers, and Eric Sodomka. 2019. Online learning for measuring incentive compatibility in ad auctions?. In The World Wide Web Conference. 2729–2735.

- Fu et al. [2015] Hu Fu, Nicole Immorlica, Brendan Lucier, and Philipp Strack. 2015. Randomization beats second price as a prior-independent auction. In Proceedings of the Sixteenth ACM Conference on Economics and Computation. 323–323.

- Golrezaei et al. [2021] Negin Golrezaei, Adel Javanmard, and Vahab Mirrokni. 2021. Dynamic incentive-aware learning: Robust pricing in contextual auctions. Operations Research 69, 1 (2021), 297–314.

- Golrezaei et al. [2017] N. Golrezaei, M. Lin, V. Mirrokni, and H. Nazerzadeh. 2017. Boosted Second-price Auctions for Heterogeneous Bidders. Management Science. (2017).

- Hartline and Roughgarden [2009] Jason D Hartline and Tim Roughgarden. 2009. Simple versus optimal mechanisms. In Proceedings of the 10th ACM conference on Electronic commerce. 225–234.

- Huang et al. [2018] Zhiyi Huang, Yishay Mansour, and Tim Roughgarden. 2018. Making the most of your samples. SIAM J. Comput. 47, 3 (2018), 651–674.

- Kanoria and Nazerzadeh [2014] Yash Kanoria and Hamid Nazerzadeh. 2014. Dynamic Reserve Prices for Repeated Auctions: Learning from Bids. In International Conference on Web and Internet Economics. 232–232.

- Krishna [2009] V. Krishna. 2009. Auction Theory.

- Lahaie et al. [2018] Sébastien Lahaie, Andrés Munoz Medina, Balasubramanian Sivan, and Sergei Vassilvitskii. 2018. Testing incentive compatibility in display ad auctions. In Proceedings of the 2018 World Wide Web Conference. 1419–1428.

- Mohri and Medina [2014] Mehryar Mohri and Andres Munoz Medina. 2014. Learning theory and algorithms for revenue optimization in second price auctions with reserve. In International Conference on Machine Learning. PMLR, 262–270.

- Mohri and Medina [2015] Mehryar Mohri and Andrés Muñoz Medina. 2015. Revenue optimization against strategic buyers. In Proceedings of the 28th International Conference on Neural Information Processing Systems-Volume 2. 2530–2538.

- Morgenstern and Roughgarden [2015] Jamie Morgenstern and Tim Roughgarden. 2015. The pseudo-dimension of near-optimal auctions. In Proceedings of the 28th International Conference on Neural Information Processing Systems-Volume 1. 136–144.

- Morgenstern and Roughgarden [2016] Jamie Morgenstern and Tim Roughgarden. 2016. Learning simple auctions. In Conference on Learning Theory. PMLR, 1298–1318.

- Muthukrishnan [2009] S Muthukrishnan. 2009. Ad exchanges: Research issues. In 5th International Workshop on Internet and Network Economics, WINE 2009. 1–12.

- Myerson [1981] Roger B Myerson. 1981. Optimal auction design. Mathematics of operations research 6, 1 (1981), 58–73.

- Ostrovsky and Schwarz [2011] Michael Ostrovsky and Michael Schwarz. 2011. Reserve prices in internet advertising auctions: A field experiment. In Proceedings of the 12th ACM conference on Electronic commerce. 59–60.

- Paes Leme et al. [2016] Renato Paes Leme, Martin Pál, and Sergei Vassilvitskii. 2016. A field guide to personalized reserve prices. In Proceedings of the 25th international conference on world wide web. 1093–1102.

- Riley and Samuelson [1981] J. Riley and W. Samuelson. 1981. Optimal auctions. American Economic Review 71 (1981).

- Shen et al. [2019] Weiran Shen, Sébastien Lahaie, and Renato Paes Leme. 2019. Learning to clear the market. In International Conference on Machine Learning. 5710–5718.

- Tang and Zeng [2018] Pingzhong Tang and Yulong Zeng. 2018. The price of prior dependence in auctions. In Proceedings of the 2018 ACM Conference on Economics and Computation. 485–502.

- Tsybakov [2009] Alexandre B. Tsybakov. 2009. Introduction to nonparametric estimation.

7 Proof of results of Section 2

7.1 Proof of Lemma 1

Lemma 1 (Integrated version of the Myerson lemma)

Let bidder have value distribution and call her strategy, the induced distribution of bids and the corresponding virtual value function. Assume that has a density and finite mean. Suppose that ’s bids are independent of the bids of the other bidders and denote by the cdf of the maximum of their bids. Suppose a lazy second price auction with reserve price denoted by is run. Then the payment of bidder to the seller can be expressed as

When the other bidders are bidding truthfully, is the distribution of the maximum value of the other bidders.

Proof

The proof is similar to the original one [30] (see [23] for more details). It consists in using Fubini’s theorem and integration by parts (this is why we need conditions on ) to transform the standard form of the seller revenue, i.e.

into the above equation. We consider a lazy second price auction. Call the reserve price for bidder . So the seller revenue from bidder is

In general, we could just call and say that the revenue from , or ’th expected payment is

Call the cdf of and the cdf of . Note that .

So if we note , we have

Integrating by parts we get

Hence,

The first term of this integral is simply

Note that to split the two terms of the integral we need to assume that , hence the first moment assumption on . The other part of the integral is

| (7) | |||

| (8) | |||

| (9) | |||

| (10) |

We used Fubini’s theorem to change order of integrations, since all functions are non-negative. The result follows.

Of course, when somewhere we understand as being equal to 1. To avoid this problem completely we can also simply write

If is not differentiable but absolutely continuous, its Radon-Nikodym derivative is used when interpreting the differentiation of with respect to .

7.2 Proof of Theorem 1

This theorem works for non-regular value distributions and in the asymmetric case when the bidders have different value distributions.

Theorem 1

Consider the one-strategic setting in a lazy second price auction with the value distribution of the strategic bidder and a seller computing the reserve prices to maximize her revenue. No assumptions are needed on the distributions of other bidders. Suppose is a shading function with associated reserve value . Then we can find such that: 1) The reserve value associated with is 0. 2) , being the utility of the buyer. 3) , being the payment of bidder to the seller. The following continuous functions fulfill these conditions for small enough:

Proof

The reserve value is given. Consider

To make things simple we require , so we have continuity. Note that beyond the seller revenue is unaffected. If the seller sets the reserve value at the extra benefit compared to setting it at is

Hence, as long as , the seller has an incentive to lower the reserve value. The extra gain to the buyer is

Now, if we take

it is easy to verify that

So in this limit case, there is no change in buyer’s payment and when the reserve price is moved by the seller to any value on . If we assume that the seller is welfare benevolent, she will set the reserve value to 0. To have continuity of the bid function, we just require that

Since there is no extra cost for the buyer, it is clear that his/her payoff is increased with this strategy. Taking such that

gives a strict incentive to the seller to move the reserve value to 0, (so the assumption that s/he is welfare benevolent is not required) even if it is slightly suboptimal for the buyer. Note that we explained in Lemma 3 how to construct such a . In particular,

works. Taking limits proves the result, i.e. for small enough the Lemma holds, since everything is continuous in .

Comment We note that the flexibility afforded by is two-fold: when , the extra seller revenue is a strictly decreasing function of the reserve price; hence even if for some reason reserve price movements are required to be small, the seller will have an incentive to make such move. The other reason is more related to estimation issues: if the reserve price is determined by empirical risk minimization, and hence affected by even small sampling noise, having big enough will guarantee that the mean extra gain of the seller will be above this sampling noise. Of course, the average cost for the bidder can be interpreted to just be at each value under the current reserve price and hence may not be a too hefty price to bear.

8 Proof of results of Section 3

8.1 Proof of Lemma 4

Lemma 4

Let us consider regular and denote by and . Suppose further that as . If verifies , a best-response in the class of increasing regularity-preserving strategies belongs to the class of thresholded strategies.

Proof

The proof is in several steps and exploits the property that has to be non-decreasing (since is regularity-preserving). Let us prove that .

Assume . Since is non-decreasing and increasing, . Applying Theorem 1 on , there exists in the class of thresholded strategies such that . Hence, without loss of generality, the class of possible best-response strategies can be restricted to the class of strategies with non-negative , whose corresponding reserve price is equal to their minimum bid.

We now focus on the class of strategies satisfying the properties above, a superset of the class of best response strategies. Since is regularity preserving, is concave. Since is non-negative we also see that is non-increasing. Therefore since is non-decreasing, we have that is non-increasing by composition and therefore is non-increasing.

Recall that , the leftmost point in the support of . Let us consider . As the reserve price is the minimum bid, . We call . As we explained above this function is non-increasing.

We now show that there is a best-response in the class of thresholded strategy. We split the argument into two, depending on the value of .

Case Suppose . We consider . Note that , and therefore .

Note that if , there is nothing to prove. Suppose . Then by definition, on . Let us replace on , by . is still non-decreasing and since , we also have . So on , . With this transformation, i.e. instead of using , using the strategy instead of , we decrease the reserve price (going from R to R’) and decrease the bid on ], an interval on which the strategic bidder was bidding above his value pointwise. Hence, using standard arguments about truthful bidding being pointwise optimal from a utility maximization standpoint in second price auctions (with fixed reserves, [23], Proposition 2.1 p.13), we see that the utility of the strategic bidder has increased by moving from to , since the utility increased pointwise and the reserve has decreased. Hence, if , we have shown that we can improve our strategy by thresholding. Hence any strategy in this case can be improved by thresholding. We have also shown that no-best response strategy exists when .

Case We split the argument in two subcases.

Case Let us define by . Since is concave and continuous exists and . Assume is not thresholded on . Let us now prove that and cross on . We have , by definition of . Using the fact that is not thresholded and is non-increasing, ; also, by definition, . As is non increasing on and is non decreasing on , if , there exists , s.t. . Let us pick one such and call . Consider the strategy

is increasing ( by construction), has a lower reserve price ( instead of ) and decreases bids where was over-bidding compared to truthful bidding, i.e. on . So it is at least as good as per our argument derived from [23] above.

Case We consider two subcases, depending on whether and cross on the support of or not. Recall that , so in the case under consideration,

a) If and do not cross on the support of F, we have for all , .

Let us define such that . By concavity and continuity of , and using the fact that at infinity, we have exists and .

Furthermore, since is concave, its super level-sets are convex so we have . We also have for all . Hence, Consider the strategy

We have . So is increasing, has the same reserve price as and increases bids where was under-bidding compared to truthful bidding. So it is at least as good as .

b) If they cross, let . Using the fact that is non-increasing and is concave, we have . By definition, we have , since for all and is non-increasing.

Consider the strategy, if :

We have on . So is non-decreasing (note that is non decreasing and for by definition of .) increasing, has the same reserve price and increases bids where was under-bidding compared to truthful bidding. So it is at least as good as by the same arguments as before.

If , and if , then and hence . But is non-increasing and . Hence we conclude that on and hence is thresholded on and there is nothing to show.

Now suppose is not attained; by definition of , we can find a decreasing sequence , with such that and , otherwise would not be the infimum of the set we consider. Along this sequence, we have . We also have , since for all . Using the fact that is non-increasing and is continuous to justify the existence of limits, we have

We conclude that . Using the fact is non-increasing, we have , since and taking the limit (since is non-increasing and is decreasing) we have

Since , we conclude that

Hence , is attained, is thresholded by our argument above and there is nothing to show.

8.2 Proof of Theorem 3.1

Theorem 2

Suppose that only one bidder is strategic, let G denote the CDF of the maximum value of the competition and g the corresponding pdf. Denote by the utility of the bidder using the strategy according to the parametrization of Definition 3. Assume that the seller is welfare-benevolent. Then if ,

The only strategy and threshold for which we can cancel the derivatives in all directions consists in bidding truthfully beyond , where satisfies the equation

Proof

Recall that our revenue in such a strategy (we take ) is just, when the seller is welfare-benevolent (and hence s/he will push the reserve value to 0 as long as for all )

Now if , as usual, we have . Because we assumed that , changing to won’t drastically change that; in particular if the seller is still going to take all bids after . In particular, we don’t have to deal with the fact that the optimal reserve value for the seller may be completely different for and . So the assumption is here for convenience and to avoid technical nuisances. In any case, we have

Now using integration by parts on , we have

Hence,

This gives the first equation of Theorem 3.1.

On the other hand, we have

Since

we have established that

We see that the only strategy and threshold for which we can cancel the derivatives in all directions consists in bidding truthfully beyond , where satisfies the equation

Theorem 3.1 is shown.

9 Optimal non-robust best-response

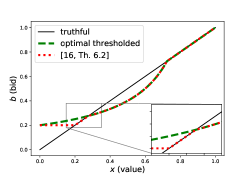

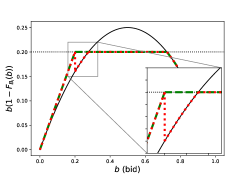

[35, Th. 6.2] exhibits the best response for the one-strategic case. Unfortunately, this best response induces a complicated optimization problem for the seller: is non-convex with several local optima and the global optimum is reached at a discontinuity of (see Fig. 4). This is especially problematic if sellers are known to optimize reserve prices conditionally on some available context using parametric models such as Deep Neural Networks [dutting2017optimal] whose fit is optimized via first-order optimization and hence would regularly fail to find the global optimum. This is undesirable for the bidders: in any Stackelberg game, the leader’s advantage comes from being able to predict the follower’s strategy.

To address this issue, [35, nedelec2018thresholding] proposed a thresholding strategy that is the best response in the restricted class of strategies that ensure to be concave as long as is so.

Figure 4 illustrates the different strategies as well as the corresponding optimization problems and the virtual values associated to the push-forward bid distributions. Understanding the strategic answer of the bidders helps avoiding worst-case scenario reasoning when studying the revenue of the sellers against strategic bidders. We now quantify precisely how the welfare is shared between strategic bidders and seller.

10 Proof of Section 4: deriving the Nash equilibrium

Lemma 6

Consider the symmetric setting. Suppose that all the bidders are strategic and that they are all except one using the strategy , denotes the CDF of the maximum bid of the competition when they use and the corresponding pdf, consider r and such that . Assuming that the seller is welfare-benevolent and that . Then

Also,

The only strategy and threshold for which we can cancel/put to zero the derivatives in all directions consists in bidding truthfully beyond , where satisfies the equation

| (11) |

Proof

To derive the lemma we need to do the same calculations as in the previous case but now the distribution of the highest bid of the competition depends on . In the case of symmetric bidders with the same value distributions , we have

The last result follows by plugging-in these expressions in the corresponding equations.

10.1 Proof of Theorem 4.1

Theorem 4.1

We consider the symmetric setting where all the bidders have the same value distributions. We assume for simplicity that the distribution is supported on [0,1]. Suppose this distribution has density that is continuous at 0 and 1 with and X has a distribution for which crosses 0 exactly once and is positive beyond that crossing point.

There is a unique symmetric Nash equilibrium in the class of thresholded bidding strategies defined in Definition 3. It is found by solving Equation (11) to determine and bidding truthfully beyond

Moreover, if all the bidders are playing this strategy corresponding to the unique Nash equilibrium, the revenue of the seller is the same as in a second price auction with no reserve price. The same is true of the utility of the buyers.

Sketch of proof:

-

•

State a directional derivative result in this class of strategies by directionally-differentiating the expression of .

-

•

Prove uniqueness of the Nash equilibrium.

-

•

Prove existence of the Nash equilibrium.

-

•

Show equivalence of revenue with a second price auction without reserve.

10.2 A directional derivative result

We can state a directional derivative result in this class of strategies by directionally-differentiating the expression of .It implies the only strategy with 0 “gradient” in this class is truthful beyond a value ( is different from the one in strategic case), where can be determined through a non-linear equation.

Lemma 7

Consider the symmetric setting. Suppose that all the bidders are strategic and that they are all except one using the strategy , denotes the CDF of the maximum bid of the competition when they use and the corresponding pdf, consider r and such that . Assuming that the seller is welfare-benevolent and that . Then

Also,

The only strategy and threshold for which we can cancel/put to zero the derivatives in all directions consists in bidding truthfully beyond , where satisfies the equation

| (12) |

Proof

In the case of symmetric bidders with the same value distributions , we have

The last result follows by plugging-in these expressions in the corresponding equations.

10.3 Uniqueness of the Nash equilibrium

We show that this strategy represents the unique symmetric Bayes-Nash equilibrium in the class of shading functions defined in Definition 3. At this equilibrium, the bidders recover the utility they would get in a second price auction without reserve price.

Lemma 8

Suppose has a distribution for which crosses exactly once and is positive beyond that crossing point. Then Equation (12) has a unique non-zero solution.

Proof

We have by integration by parts

Hence finding the root of

amounts to finding the root(s) of

0 is an obvious root of the above equation but does not work for the penultimate one. Note that for the class of distributions we consider (which is much larger than regular distributions but contains it), this function is decreasing and then increasing after , since the virtual value is negative and then positive. Since , it will have at most one non-zero root for the distributions we consider. The fact that this function is positive at infinity (or at the end of the support of ) comes from the fact that its value then is the revenue-per-buyer of a seller performing a second price auction with symmetric buyers bidding truthfully with a reserve price of 0. And this is by definition positive. So we have shown that for regular distributions and the much broader class of distributions we consider the function has exactly one non-zero root.

10.4 Existence of the Nash equilibrium

10.4.1 Best response strategy: one strategic case

Lemma 9

Suppose that only one bidder is strategic, let G denote the CDF of the maximum value of the competition and g the corresponding pdf. Denote by the utility of the bidder using the strategy according to the parametrization of Definition 3. Assume that the seller is welfare-benevolent. Then if ,

The only strategy and threshold for which we can cancel/put to zero the derivatives in all directions consists in bidding truthfully beyond , where satisfies the equation

| (13) |

Proof

Recall that our revenue in such a strategy (we take ) is just, when the seller is welfare-benevolent (and hence s/he will push the reserve value to 0 as long as for all )

Now if , as usual, we have . Because we assumed that , changing to won’t drastically change that; in particular if the seller is still going to take all bids after . In particular, we don’t have to deal with the fact that the optimal reserve value for the seller may be completely different for and . So the assumption is here for convenience and to avoid technical nuisances. In any case, we have

Now using integration by parts on , we have

Hence,

This gives the first equation of Lemma 13.

On the other hand, we have

Since

we have established that

We see that the only strategy and threshold for which we can cancel/put to zero the derivatives in all directions consists in bidding truthfully beyond , where satisfies the equation

Lemma 13 is shown.

10.4.2 Proof of existence of the Nash equilibrium

On Equation (13) and consequences

Lemma 10

Suppose has a regular distribution or a distribution whose virtual value crosses 0 exactly once and is negative to the left of this crossing point and positive to the right of that point. Suppose further that this distribution is compactly supported (on [0,1] for convenience). Equation (13) can be re-written as

| (14) |

Equation (13) has at most one solution on (0,1). This possible root is greater than . 0 is also a (trivial) solution of Equation (13).

The assumption that is supported on [0,1] can easily be replaced by the assumption that it is compactly supported, but it made notations more convenient.

Proof (Proof of Lemma 10)

We use again integration by parts :

So we are really looking at the properties of the solution of

We call

For regular distributions, or distribution for which crosses 0 exactly once and is negative to the left of this crossing point and positive to the right of it, it is clear that if , .

Now we note that

Using , we see that

So if is a solution of

we have, if and ,

So needs to be a solution of (which is equivalent to the initial equation for non-trivial solutions) and must have .

So we have shown that is a function such that its (non-trivial) zeros are such that is strictly increasing at those roots. Because is differentiable and hence continuous, this implies that can have at most one non-trivial root. (0 is a trivial root of , though it is not an acceptable solution of our initial problem.)

We note that the end point of the support of is also a trivial solution of , by the dominated convergence theorem, though not an acceptable solution of our initial problem, as shown by a simple inspection.

Lemma 11