Tempered fractional Brownian motion: wavelet estimation, modeling and testing ††thanks: The second author was partially supported by the prime award no. W911NF-14-1-0475 from the Biomathematics subdivision of the Army Research Office, USA. The authors would like to thank Laurent Chevillard for his comments on this work. ††thanks: AMS Subject classification. Primary: 62M10, 60G18, 42C40. ††thanks: Keywords and phrases: fractional Brownian motion, semi-long range dependence, tempered fractional Brownian motion, turbulence, wavelets.

Abstract

The Davenport spectrum is a modification of the classical Kolmogorov spectrum for the inertial range of turbulence that accounts for non-scaling low frequency behavior. Like the classical fractional Brownian motion vis-à-vis the Kolmogorov spectrum, tempered fractional Brownian motion (tfBm) is a canonical model that displays the Davenport spectrum. The autocorrelation of the increments of tfBm displays semi-long range dependence (hyperbolic and quasi-exponential decays over moderate and large scales, respectively), a phenomenon that has been observed in wide a range of applications from wind speeds to geophysics to finance. In this paper, we use wavelets to construct the first estimation method for tfBm and a simple and computationally efficient test for fBm vs tfBm alternatives. The properties of the wavelet estimator and test are mathematically and computationally established. An application of the methodology to the analysis of geophysical flow data shows that tfBm provides a much closer fit than fBm.

1 Introduction

A tempered fractional Brownian motion (tfBm) with Hurst parameter and tempering parameter is the stochastic process defined by the moving average representation

| (1.1) |

where and is an independently scattered Gaussian random measure satisfying . In the boundary case (and ), tfBm reduces to a fractional Brownian motion (fBm), namely, a Gaussian, stationary-increment, self-similar process (e.g., Embrechts and Maejima (?), Taqqu (?)). TfBm is a new canonical model introduced in Meerschaert and Sabzikar (?, ?), Sabzikar et al. (?) that displays the so-named Davenport spectrum (Davenport (?)). The latter is a modification of the classical Kolmogorov spectrum for the inertial range of turbulence that accounts for low frequency behavior and has been successfully applied in wind speed modeling (Norton and Wolff (?), Li and Kareem (?), Beaupuits et al. (?)). On the other hand, a wavelet is a unit -norm function that annihilates a certain number of polynomials (see (A.1)). In this paper, we use wavelets to construct the first estimator for tfBm and a simple and computationally efficient test for fBm vs tfBm alternatives. The asymptotic properties of the wavelet estimator and test are mathematically established and their finite sample performance is computationally studied. An application of the methodology in geophysical flow data shows that tfBm provides a much closer fit than fBm.

Classical models of turbulence describe how kinetic energy at the largest length scales is progressively transferred down to smaller scales. In the complete Kolmogorov spectral model for turbulence (Kolmogorov (?, ?), Friedlander and Topper (?), Shiryaev (?)), large eddies are produced in the low frequency range of scales, whereas in the inertial range (moderate frequencies), larger eddies are continuously broken down into smaller eddies, until they eventually dissipate (high frequencies). In the landmark paper Mandelbrot and Van Ness (?), Kolmogorov’s model was revisited when fBm was proposed as a framework for the analysis of scale invariant, or non-Markovian, phenomena (see Graves et al. (?)). A system is called scale invariant if its dynamics are driven by a continuum of time scales instead of a few characteristic scales. Within the fBm family, the instance corresponds to the Kolmogorov spectrum for the inertial range.

Unlike fBm, tfBm is not self-similar. Instead, it satisfies the scaling property

where indicates equality of finite dimensional distributions. This is a consequence of the presence of the extra (tempering) parameter , which controls the deviation from a fBm’s power law spectrum at low frequencies. Notably, even though a stationary-increment process, tfBm converges almost surely to stationarity as . This property of tfBm makes it suitable for modeling data that looks stationary or approximately so. TfBm also exhibits semi-long range dependence, i.e., the correlation between its increments decays essentially like a power law over fine/moderate scales (fractional or scale invariant behavior), but quasi-exponentially over large scales (see (2.3); cf. Giraitis et al. (?)).

Research on tempered fractional processes has been expanding at a fast pace. Several models (ARTFIMA, tempered diffusion, tempered stable motions, tempered Lévy flights) have recently been studied and used in a wide range of modern applications such as in the physics and modeling of transient anomalous diffusion (Piryatinska et al. (?), Stanislavsky et al. (?), Sandev et al. (?), Wu et al. (?), Chen et al. (?), Liemert et al. (?), Chen et al. (?)), geophysical flows (Meerschaert et al. (?), Meerschaert et al. (?)) and finance (Dacorogna et al. (?), Granger and Ding (?), Cont et al. (?), Ling and Li (?), Zhang and Xiao (?)). See also Chevillard (?) on turbulence modeling based on regularization. In addition, tempered fractional processes are closely related to near integrated models in econometrics (Phillips et al. (?)). However, in spite of the fast growth of the literature on tempered fractional processes, little work has been done, in general, on their statistical methodology. In Meerschaert et al. (?), turbulence data is modeled in the Fourier domain within an ARTFIMA framework. In Anh, Heyde and Tieng (?) and Gao et al. (?), respectively, wavelet log-regression and Whittle-type methods are constructed for subclasses of tempered fractional processes assuming the tempering parameter is known (see also Anh, Angulo and Ruiz-Medina (?)).

The wavelet transform is a powerful tool for the analysis of scale invariant phenomena (Flandrin (?), Wornell and Oppenheim (?), Abry et al. (?), Percival and Walden (?)). Given an observed fractional time series , estimation of the parameter can be conducted by a log-regression procedure that draws upon the scaling property of the sample wavelet variance, i.e.,

| (1.2) |

where , , is the wavelet transform at scale and shift (Veitch and Abry (?), Bardet et al. (?); see (2.12) on ). Wavelet-based statistical inference has well-documented benefits, such as: for a sample of size , the fast wavelet transform may reach computational complexity , which is even lower than that of the fast Fourier transform (Mallat (?)); robustness with respect to contamination by polynomial trends (Craigmile et al. (?)); modeling of stationary or stationary increment processes of any order in the same framework (Moulines et al. (?, ?, ?)); quasi-decorrelation of several families of stochastic processes (Masry (?), Bardet (?)), which often leads to Gaussian confidence intervals.

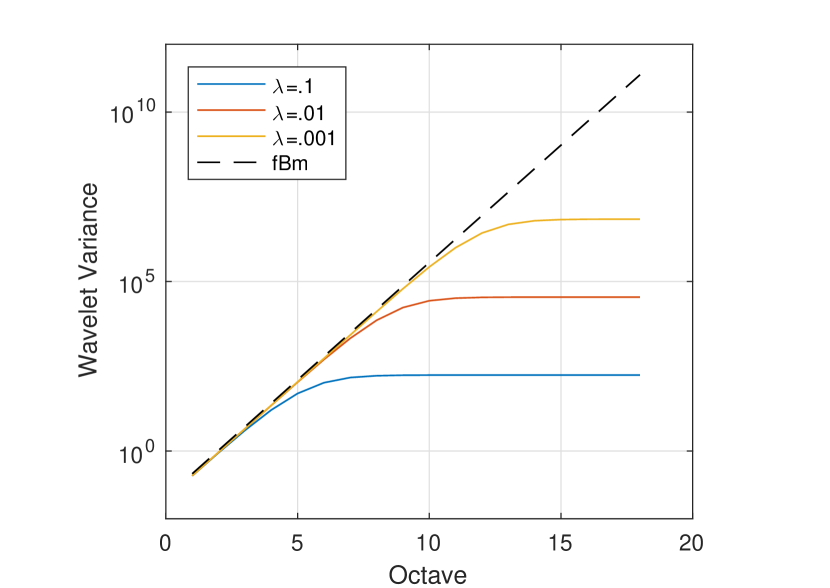

Following up on the work Boniece et al. (?), presented without proofs and containing preliminary computational studies, in this paper we construct the wavelet analysis of tfBm and the statistical theory for the first estimator for tfBm. We make the realistic assumption that only discrete time measurements are available. We characterize the phenomenon of semi-long range dependence in the wavelet domain, whereby the presence of the parameter determines that, for large octaves, the wavelet spectrum of tfBm deviates from that of fBm (see Figure 1, left plot, and (2.13)). In particular, the wavelet (or Fourier) spectrum of tfBm is not, in general, log-linear over a wide range of scales (cf. (1.2)). Hence, the proposed estimator is based on a nonlinear regression procedure in the wavelet domain (see (3.2); cf. Frecon et al. (?)). Its consistency and asymptotic normality are mathematically established (Theorem 3.1). Monte Carlo studies demonstrate the estimator’s efficacy over finite samples for different instances of tfBm, at an acceptable computational cost.

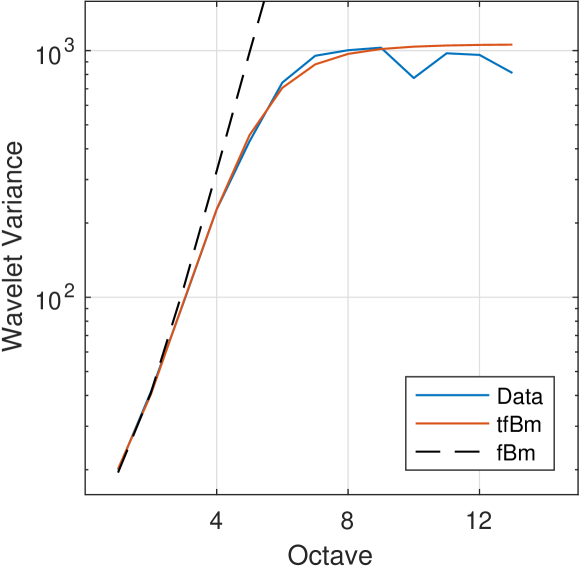

In physical and modeling practice, it is also of great interest to identify the estimable range of for given sample sizes (cf. Sabzikar et al. (?)). We further propose to investigate this issue from a hypothesis testing perspective (cf. Giraitis et al. (?)). We construct a simple and computationally efficient test for fBm vs tfBm alternatives based on comparing Hurst exponent estimates obtained from different regions of the sample wavelet spectrum. The asymptotic distribution of the test statistic is mathematically established under both the null and the alternative hypotheses (Theorem 3.2). Starting from the latter, we computationally develop power curves as a function of the sample size that hence quantify how distinguishable tfBm is from fBm for each value of , given . We apply the estimation and testing methodology to geophysical flow data from the Red Cedar river in Michigan, USA, and conclude that tfBm is a significantly better model than fBm. This complements and justifies the exploratory data analysis presented in Boniece et al. (?) (see Figure 1, right plot).

This work leads to a number of issues: in view of the convergence to stationarity of tfBm, is there a way of constructing a powerful test of tfBm vs ARMA-like alternatives?; is the parameter range , which is absent in the fBm framework, of physical interest? In addition, few statistical methods are available for other Gaussian or non-Gaussian tempered fractional models such as tempered fractional stable motion (Sabzikar and Surgailis (?)), tempered Hermite processes (Sabzikar (?)), tempered stable processes (Cohen and Rosiński (?), Rosiński (?), Baeumer and Meerschaert (?), Bianchi et al. (?), Gajda and Magdziarz (?), Kienitz (?), Rosiński and Sinclair (?), Kawai and Masuda (?), Küchler and Tappe (?)) or tempered fractional Langevin dynamics (Zeng et al. (?)).

This paper is organized as follows. In Section 2, we recall basic properties of tfBm and construct its wavelet analysis. Section 3 contains the main results of the paper. In Section 3.1, we develop asymptotic theory for the point estimator and also the testing framework. In Section 3.2, we present the Monte Carlo studies, and in Section 3.3, we model geophysical flow data. All proofs can be found in the Appendix, together with auxiliary results.

2 Preliminaries

2.1 Basic properties of tfBm

Let be a tfBm as in (1.1). Starting from its corresponding moving average representation, it can be shown that its covariance function is given by

| (2.1) |

where , , is the modified Bessel function of the second kind, and (Meerschaert and Sabzikar (?), Proposition 2.3). TfBm admits the harmonizable (Fourier domain) representation

| (2.2) |

where is a complex-valued Gaussian random measure such that and . Expression (1.1) or (2.2) implies that tfBm is Gaussian and has stationary increments. The increment process of tfBm, namely, , is called tempered fractional Gaussian noise (tfGn). Its covariance function , , has decay

| (2.3) |

(semi-long range dependence; cf. Chen et al. (?), Appendix 2).

2.2 Wavelet analysis

Throughout the paper, we make use of a wavelet multiresolution analysis (MRA; see Mallat (?), chapter 7), which decomposes into a sequence of approximation (low-frequency) and detail (high-frequency) subspaces and , respectively, associated with different scales of analysis . We always assume the MRA satisfies the technical conditions () (corresponding to expressions (A.1)–(A.4) in the Appendix), so such conditions are omitted in statements. Note that we work under assumptions that are closely related to the broad wavelet framework for the analysis of Gaussian stochastic processes laid out in Moulines et al. (?, ?, ?). We further suppose the wavelet coefficients stem from Mallat’s pyramidal algorithm (Mallat (?), chapter 7). Initially, suppose an infinite time series

| (2.4) |

associated with the starting scale (or octave ), is available. Then, we can apply Mallat’s algorithm to extract the so-named approximation and detail coefficients at coarser scales by means of an iterative procedure. In fact, as commonly done in the wavelet literature, we initialize the algorithm with the process

| (2.5) |

By the orthogonality of the shifted scaling functions ,

| (2.6) |

(see Stoev et al. (?), proof of Lemma 6.1, or Moulines et al. (?), p. 160; cf. Abry and Flandrin (?), p. 33). In other words, the initial sequence, at octave , of approximation coefficients is given by the original time series. To obtain approximation and detail coefficients at coarser scales, we use Mallat’s iterative procedure

| (2.7) |

where the filter sequences , are called low- and high-pass MRA filters, respectively. Due to the assumed compactness of the supports of and the associated scaling function (see condition (A.2)), only a finite number of filter terms is nonzero, which is convenient for computational purposes (Daubechies (?)). Hereinafter, we assume without loss of generality that (cf. Moulines et al (?), p. 160). Moreover, the wavelet (detail) coefficients of tfBm can be expressed as

| (2.8) |

where the filter terms are defined by

| (2.9) |

If we replace (2.4) with the realistic assumption that only a finite length time series

| (2.10) |

is available, writing , the finite-sample wavelet coefficients of satisfy

| (2.11) |

In other words, such subset of finite-sample wavelet coefficients is not affected by the so-named border effect (cf. Craigmile et al. (?), Percival and Walden (?), Didier and Pipiras (?)). Moreover, by (2.11) the number of such coefficients at octave is given by . Hence, for large . Thus, for notational simplicity we suppose

| (2.12) |

holds exactly and only work with wavelet coefficients unaffected by the border effect.

From the above assumptions, it can be shown that, for fixed scales and and some constant ,

| (2.13) |

when is not too small (see Proposition LABEL:p:tfbm_decorr, ). This is the algebraic expression of the semi-long range dependence phenomenon in the wavelet domain. Let

| (2.14) |

be the discrete Fourier transform of the sequence appearing in (2.8). The harmonizable representation of tfBm (2.2), expression (2.8) and the periodicity of imply that

| (2.15) |

regardless of (Proposition A.1). The wavelet spectrum of tfBm is depicted in Figure 1, left plot. One consequence of the semi-long range dependence phenomenon is the following. For small , the wavelet spectrum of mimics that of fBm for moderate scales , namely, it is approximately linear with slope . However,

| (2.16) |

i.e., it tends to a constant at large octaves, where the transition from linearity to constancy is controlled by the tempering parameter (Proposition A.1).

Remark 2.1

Assuming a continuous time tfBm sample path is available, its wavelet transform is given by

| (2.17) |

The integral in (2.17) is well-defined in the sense because the following two conditions are met (Cramér and Leadbetter (?), p. 86). First, the covariance function is continuous. Second, by an adaptation of the argument in Abry and Didier (?), Proposition 3.1, it can also be shown that .

The continuous time wavelet spectrum is

| (2.18) |

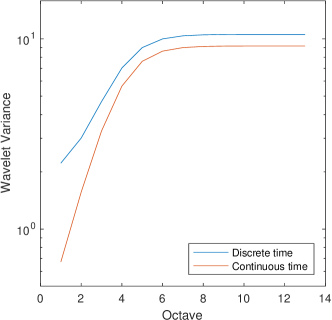

regardless of (Proposition LABEL:p:cont_time_wavelet_spec). However, unlike with fBm and related processes, the fundamental trait of the (wavelet or Fourier) log-spectrum of tfBm is not its slope over large scales. Hence, estimation based on the continuous time spectrum introduces non-negligible biases. Figure 2 illustrates the difference between the continuous and discrete time wavelet spectra of tfBm.

3 Main results

3.1 Estimation and testing

With classical fBm and related processes, only coarse scale information is generally of interest, which is given by the Hurst parameter . By contrast, with tfBm, fine/moderate scale information is also relevant and is provided by , whereas on coarse scales it is given by both and (see (2.15) and (2.16)). This points to parametric estimation. An -estimator (Van der Vaart (?)) can be constructed based on the log-wavelet spectrum of tfBm.

Definition 3.1

For a number of observations of a tfBm, define the sample wavelet variance

| (3.1) |

for some octave range , where the sample wavelet coefficients are computed by means of expression (2.8) and is given by (2.12).

Let be the parameter vector. We define a wavelet-based estimator by means of a weighted nonlinear log-regression

| (3.2) |

where the octaves are chosen so as to capture both the fine/moderate-scale behavior and the limiting behavior (2.16). In (3.2), and , , are appropriate choices of log-wavelet spectrum functions and regression weights.

There are two effects to consider when picking and in (3.2). First, estimation based on minimizing the distance between and is biased due to the fact that . Second, the variance of the sample wavelet variance changes across scales. In view of the near decorrelation property (2.13), we propose using bias-corrected and rescaled wavelet spectrum expressions in (3.2) by applying standard approximations to and (e.g., Veitch and Abry (?), Wendt et al. (?)). More precisely, on one hand we set the wavelet spectrum functions to

| (3.3) |

where

| (3.4) |

for , . On the other hand, we choose the weights , .

The consistency and asymptotic normality of the estimator (3.2) is established in the following theorem.

Theorem 3.1

Let

| (3.5) |

be the parameter space, and let be the true parameter value, where is a bounded vicinity.

-

Suppose the wavelet spectrum is identifiable for , i.e.,

(3.6) Then, for as in (3.2), there is a sequence of restricted minima of to such that

(3.7) -

if, in addition to the above,

(3.8) then

(3.9) for some symmetric positive semidefinite matrix .

Remark 3.1

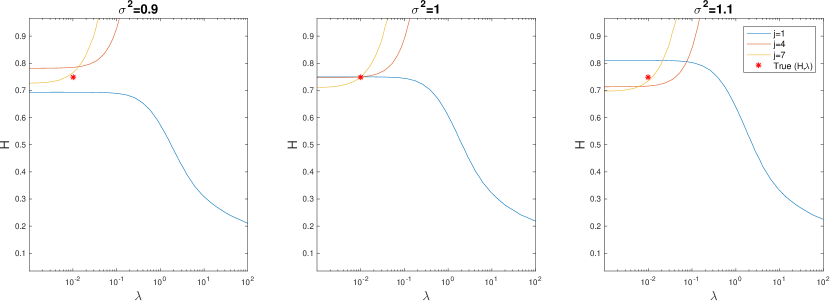

Note that the wavelet spectrum (variance) is a function of the octave and of the parameter vector . The identifiability condition (3.6) means that there is no pair of parameter vectors and for which over the available octave range. Computational studies indicate that (3.6) is mild and generally satisfied in practice (see, for example, Figure 3).

In turn, condition (3.8) is quite mild, and it amounts to requiring the full rank of a sum of rank 1 terms. Note that, for fixed , the corresponding matrix in the sum in (3.8) can be written as , where for some constant . So long as the vectors are linearly independent, (3.8) holds (see Appendix D in Abry et al. (?) for a more detailed discussion in a similar context).

In practice, it is of interest to test whether a sample path comes from a fBm as opposed to a tfBm alternative, which can be naturally framed as

| (3.10) |

If the null hypothesis of a fBm is rejected, then estimation of tfBm can be conducted by means of the estimator (3.2). A simple test consists of comparing Hurst exponent estimates obtained over different octave ranges. For fBm, the estimates should be approximately constant, whereas for tfBm, they should significantly differ assuming is not too small.

As to maximize test power, we propose to estimate the Hurst exponent over a fixed pair of small octaves and compare it with another estimate obtained over a range of large octaves. In regard to the latter estimate, note that for both fBm and tfBm the slope of the log-spectrum stabilizes in the limit. Hence, a traditional wavelet log-regression procedure is suitable. However, over small scales, either for fBm or tfBm, there is significant discrepancy between discrete and continuous time spectra (see Figure 2). For this reason, over small scales, we propose to parametrically fit the discrete time spectrum by means of wavelet-based -estimation.

Starting from the null hypothesis of a fBm, one can define an -estimator of over (small) octaves via

| (3.11) |

In (3.11), we set

| (3.12) |

where is given by (3.4) and . In other words, is the bias-corrected log-spectrum function of a fBm observed in discrete time. Moreover, for large scales, let be a traditional wavelet log-regression estimator

| (3.13) |

In (3.13), the linear regression weights satisfy

| (3.14) |

(Veitch and Abry (?), Abry et al. (?), Bardet (?), Stoev et al. (?)) and is a slow dyadic scaling factor (see (3.19)). Consider the test statistic defined by

| (3.15) |

where large values of are associated with evidence against in (3.15). In the following proposition, the asymptotic distribution of is established under both and . Under , the observed stochastic process is a tfBm. Hence, the objective function (3.11) is misspecified. So, we make the additional assumption that are chosen such that

| (3.16) |

Condition (3.16) ensures that there is a pair

| (3.17) |

in the fBm parametrization such that

| (3.18) |

where is the true parameter vector of the underlying tfBm (see Lemma LABEL:Hest_AN and also Remark 3.2).

Theorem 3.2

Consider the hypotheses (3.10) and let be the test statistic defined by (3.15). Assume that the condition (A.5) holds (for as in (A.3)), and that the dyadic scaling factor satisfies

| (3.19) |

for some and some small .

-

Under , suppose in addition that the rank condition

(3.20) holds at . Then,

(3.21) for some ;

The weak convergence (3.21) suggests the asymptotically valid rejection region

| (3.23) |

at level (see Section 3.2, Hypothesis testing, on finding the standard error).

Remark 3.2

Condition (3.20), akin to (3.8), is necessary to establish the asymptotic distribution of under each hypothesis, at different values of . Assumption (3.16) is mild and easily met in practice (i.e., for physically relevant tfBm parameter values) for , . The lefthand inequality states that the initial slope of the log-wavelet spectrum of tfBm is comparable to that of the whole class of fBm (any ). This ensures the tempering parameter is not too large; otherwise, the log-wavelet spectrum of tfBm quickly flattens as a function of the octave , which makes tfBm and fBm very distinguishable from one another. Moreover, the lefthand inequality in (3.16) guarantees a sequence of minima in (3.11) exists. On the other hand, as a result of tempering, for any fixed there always exists a , usually small, so that the righthand inequality is satisfied. This is a consequence of the fact that the slope of the log-wavelet spectrum of tfBm converges to zero (cf. Figure 1, left plot).

Remark 3.3

Picking the scales , , , is simple in practice. Computational experiments confirm that setting and is a good choice, in view of the large number of terms that go into the sample wavelet variances and . On the other hand, based on related work on the wavelet analysis of fractional processes, the choice of scales for the wavelet regression component of the test statistic (3.15) is well-understood. An example of a scaling sequence satisfying (3.19) for large enough is

In other words, a low parameter value implies that must grow slowly by comparison to . For a fixed octave range associated with an initial scaling factor value and sample size , define the scale range for a general sample size . Then, under (3.19), for every the range of useful octaves is constant and given by , where the new octaves are , . Selecting close to leads to using the coarsest available range of scales, hence favoring low bias in the estimation of the Hurst eigenvalues at the price of a larger variance. In contrast, picking close to the lower bound minimizes the variance at the cost of a larger bias. For further discussion of the choice of and and the scaling sequence in practice, see, for instance, Wendt et al. (?), Remark 3.1, or Abry and Didier (?), Remark 4.2.

3.2 Monte Carlo studies

Numerical experiment setting. The performance of the wavelet estimator was assessed through Monte Carlo studies over 5000 independent realizations of tfBm paths. The chosen parameter values were taken from . In all cases, each tfBm path was generated by circulant matrix embedding using tfGn (Davies and Harte (?), Wood and Chan (?)). The analysis was conducted using orthogonal least asymmetric Daubechies wavelets computed through Mallat’s pyramidal algorithm (2.7). Unless otherwise indicated, we set in computational studies.

To implement the discrete time wavelet variances (2.15) appearing in the objective function (3.2), several numerical considerations were made. First, the filter sequences require computation and numerical integration of the wavelet and scaling functions and . However, this needs only be done once, and the computed filters can be stored.

Second, for larger , the filters have a larger number of non-vanishing Fourier coefficients (related to high frequency behavior) and so for increasing , successively finer partitions of for the numerical integration of the wavelet spectrum (2.15) were implemented. Unreported computational experiments suggested that a mesh size was sufficiently large to yield negligible quadrature error, which was used for this study. Additionally, the infinite sum appearing in the integrand (2.15) was truncated at . To approximate truncated terms, noting that for sufficiently large we have for all , we used the integral . Minimization of the objective function (3.2) was implemented using the Matlab routine fmincon with constraints , . In all cases the initial values were set to . With regards to the octaves in (3.2), the largest octave is especially important in determining the lower bound of possible that can be estimated; larger values of correspond to improved estimation of increasingly smaller (cf. Figure 1, left plot). However, due to the aforementioned increasingly finer partitions , the inclusion of larger values of adds to the computational cost of the optimization. Thus, for each value of , we set , where is the largest available octave in the sample. In any case, all the remaining octaves are given by .

Bias correction and number of vanishing moments. In Table 1, one can see that the estimator performance is, in general, overall best with both bias correction and . Similarly to the classical fBm case (cf. Abry et al. (?)), picking instead of is more crucial when and small . This is due to the fact that, for these parameter values, tfBm behaves like fBm with long memory over a large number octaves. Unreported numerical results indicated that estimation with tends to diminish the estimation accuracy for most parameter values, especially for small .

| , no bias correction | ||||

|---|---|---|---|---|

| (.1511, .0032) | (.3542, .0025) | (.6671, .0023) | (.8837, .0023) | |

| (.0041, .0032) | (.0156, .0024) | (.0232, .0017) | (.0229, .0013) | |

| (.1507, .0134) | (.3533, .0127) | (.6585, .0123) | (.8599, .0119) | |

| (.0035, .0052) | (.0130, .0041) | (.0286, .0037) | (.0264, .0031) | |

| (.1498, .1103) | (.3499, .1067) | (.6642, .1076) | (.8824, .1111) | |

| (.0034, .0159) | (.0080, .0107) | (.0330, .0119) | (.0622, .0173) | |

| (.1480, 1.122) | (.3459, 1.046) | (.6421, 1.024) | (.8387, 1.019) | |

| (.0053, .2161) | (.0103, .0791) | (.0186, .0434) | (.0260, .0325) | |

| , with bias correction | ||||

|---|---|---|---|---|

| (.1521, .0018) | (.3570, .0015) | (.6674, .0015) | (.8822, .0017) | |

| (.0047, .0025) | (.0165, .0020) | (.0231, .0015) | (.0230, .0012) | |

| (.1502, .0103) | (.3504, .0103) | (.6508, .0103) | (.8517, .0102) | |

| (.0036, .0047) | (.0136, .0039) | (.0282, .0034) | (.0259, .0028) | |

| (.1502, .1007) | (.3499, .1001) | (.6517, .1005) | (.8538, .1013) | |

| (.0034, .0153) | (.0079, .0105) | (.0313, .0116) | (.0618, .0169) | |

| (.1502, 1.022) | (.3503, 1.004) | (.6502, 1.000) | (.8501, 1.001) | |

| (.0051, .1739) | (.0103, .0738) | (.0188, .0415) | (.0264, .0312) | |

| , no bias correction | ||||

|---|---|---|---|---|

| (.1513, .0054) | (.3528, .0043) | (.6538, .0032) | (.8538, .0028) | |

| (.0037, .0060) | (.0112, .0045) | (.0207, .0035) | (.0204, .0029) | |

| (.1506, .0144) | (.3516, .0133) | (.6537, .0125) | (.8541, .0122) | |

| (.0033, .0077) | (.0104, .0059) | (.0228, .0048) | (.0242, .0041) | |

| (.1502, .1105) | (.3505, .1075) | (.6554, .1066) | (.8631, .1072) | |

| (.0031, .0176) | (.0070, .0130) | (.0180, .0110) | (.0352, .0131) | |

| (.1487, 1.102) | (.3468, 1.042) | (.6443, 1.023) | (.8425, 1.017) | |

| (.0047, .193) | (.0091, .0756) | (.0161, .0432) | (.0218, .0328) | |

| , with bias correction | ||||

|---|---|---|---|---|

| (.1523, .0031) | (.3564, .0025) | (.6584, .0020) | (.8576, .0017) | |

| (.0041, .0048) | (.0124, .0037) | (.0206, .0030) | (.0199, .0025) | |

| (.1503, .0102) | (.3499, .0101) | (.6495, .0101) | (.8494, .0101) | |

| (.0034, .0073) | (.0110, .0057) | (.0231, .0046) | (.0244, .0039) | |

| (.1504, .1003) | (.3501, .1002) | (.6500, .1003) | (.8504, .1002) | |

| (.0031, .0170) | (.0070, .0128) | (.0184, .0111) | (.0349, .0129) | |

| (.1504, 1.016) | (.3502, 1.004) | (.6502, 1.001) | (.8505, 1.000) | |

| (.0046, .1648) | (.0090, .0715) | (.0161, .0417) | (.0220, .0318) | |

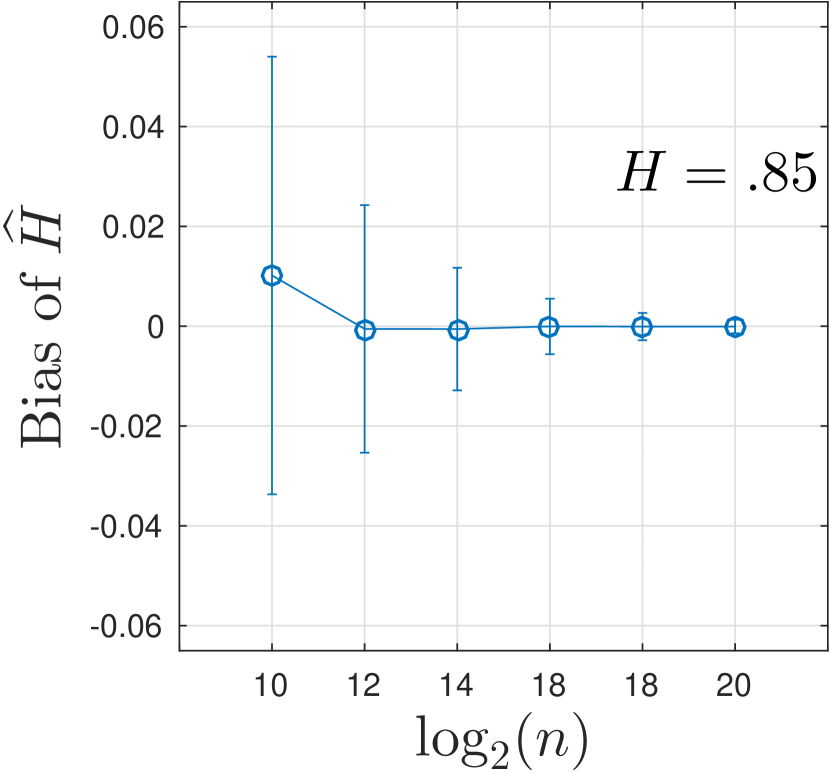

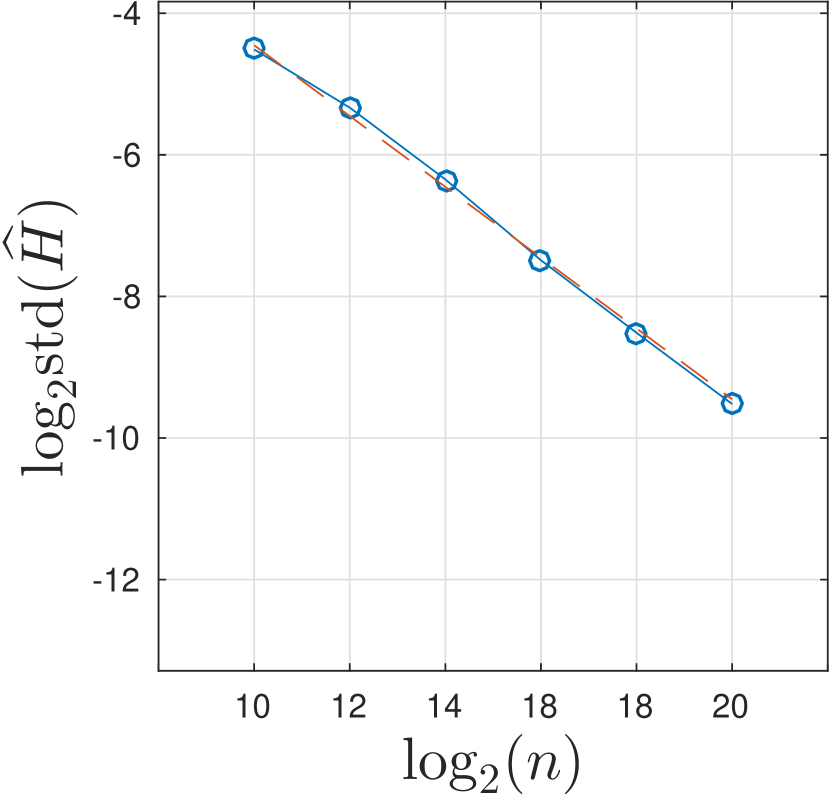

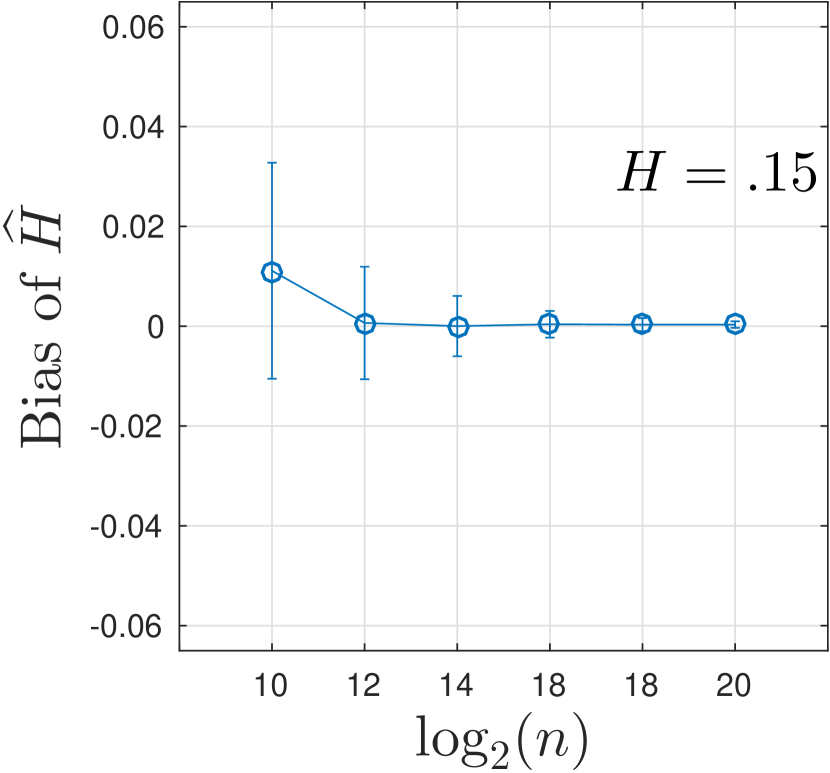

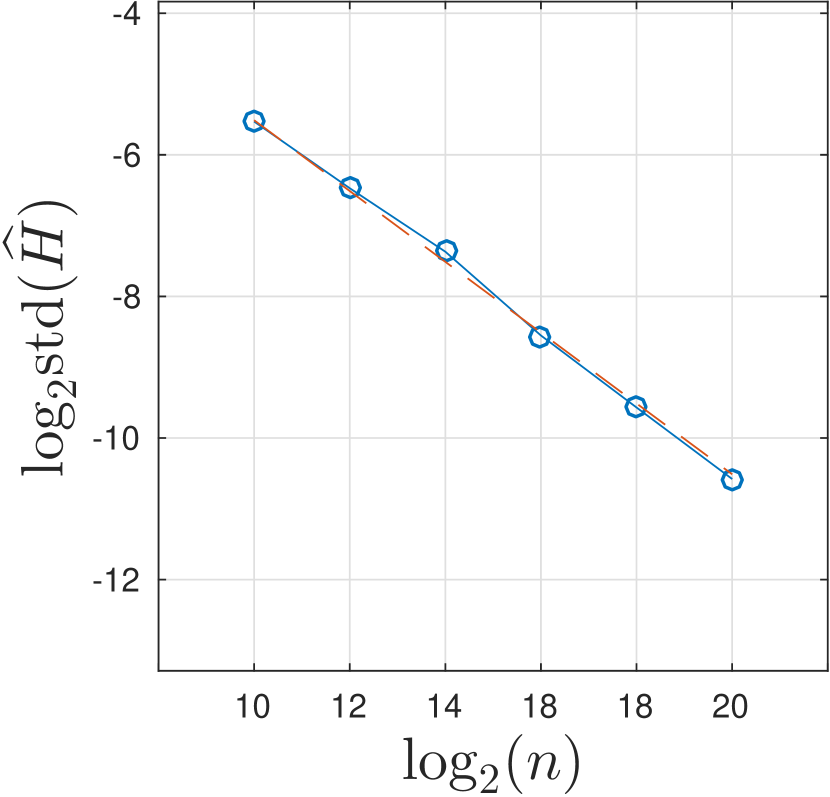

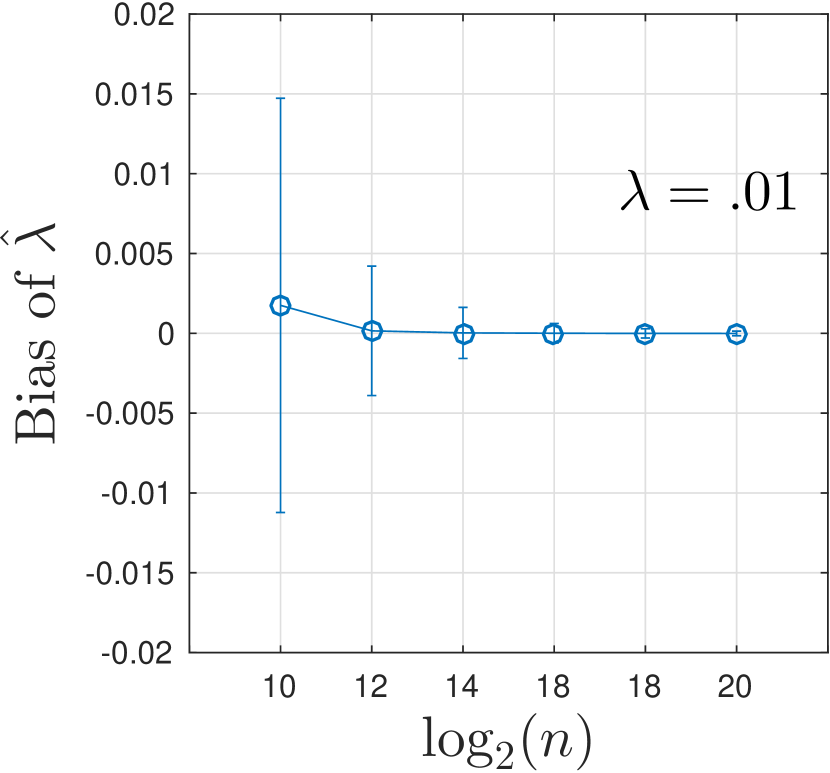

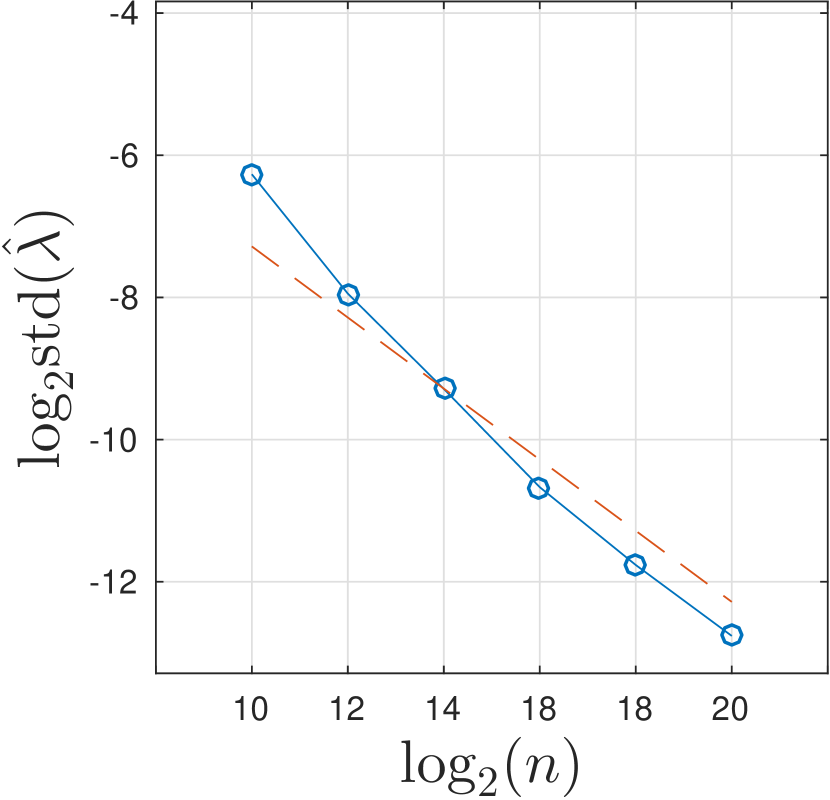

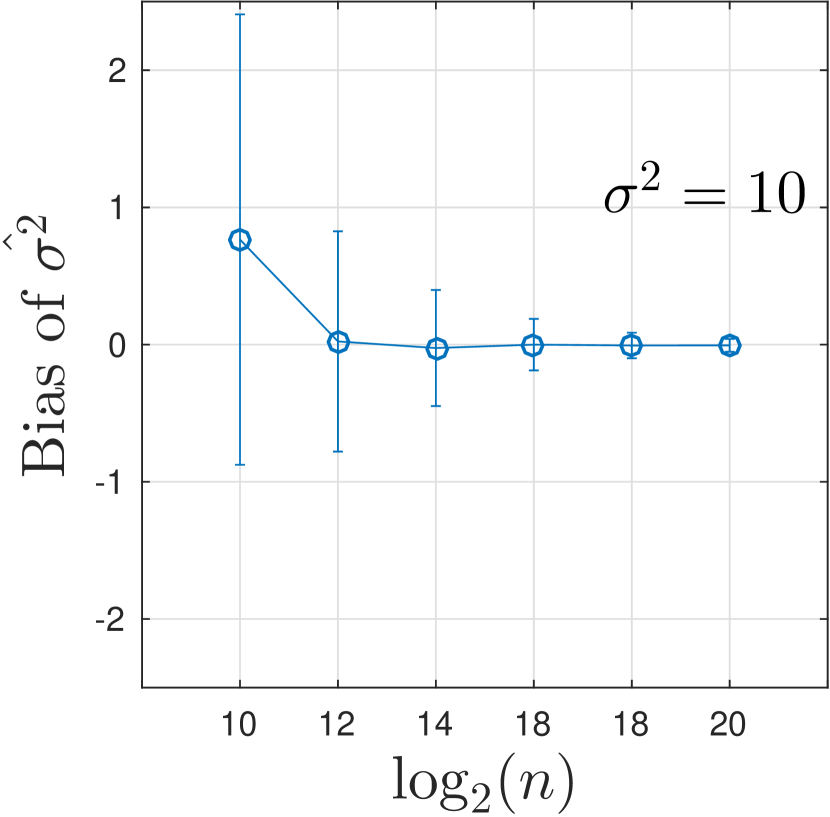

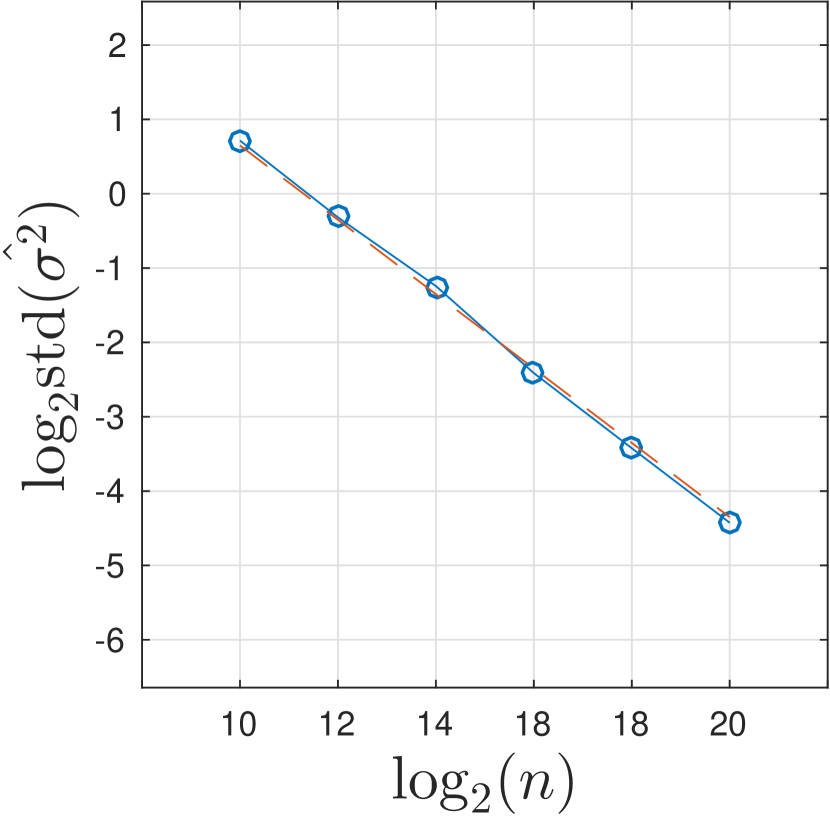

Bias and standard deviation. Figure 4 shows that, for all estimator entries , the bias becomes negligible as the sample size grows. This illustrates the estimator’s consistency. The plots further show that standard deviations for all estimator entries decrease as (the latter trend being plotted as superimposed red dashed lines), which illustrates the theoretical convergence rate to normality.

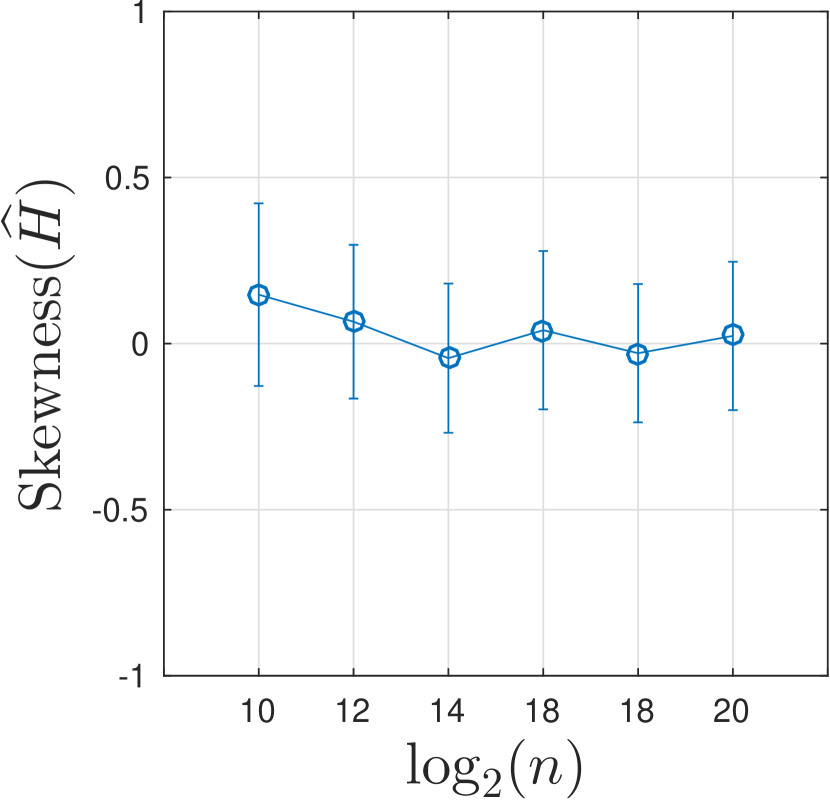

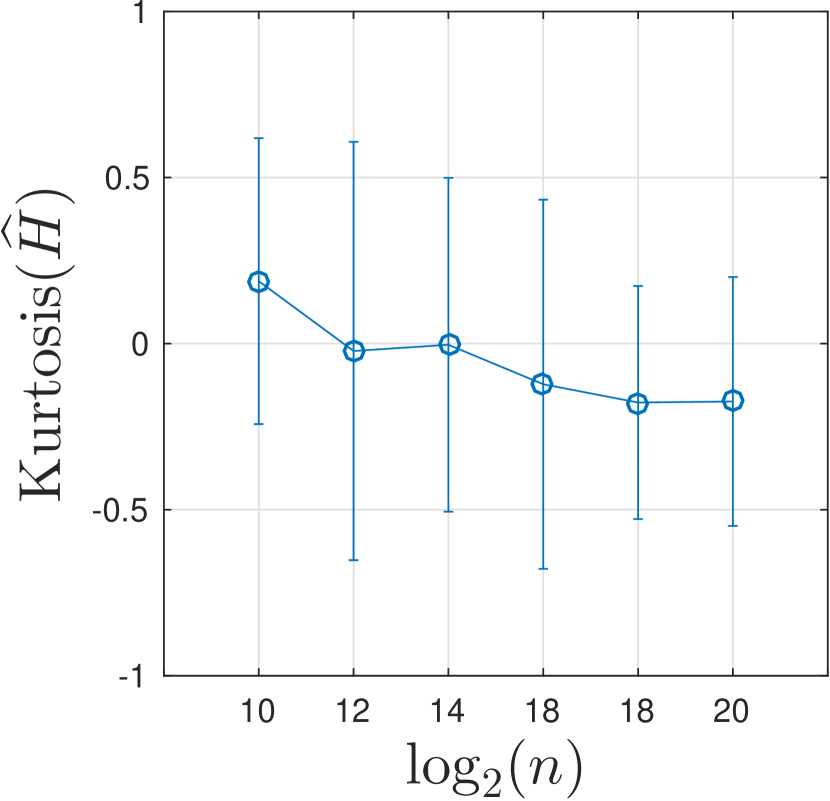

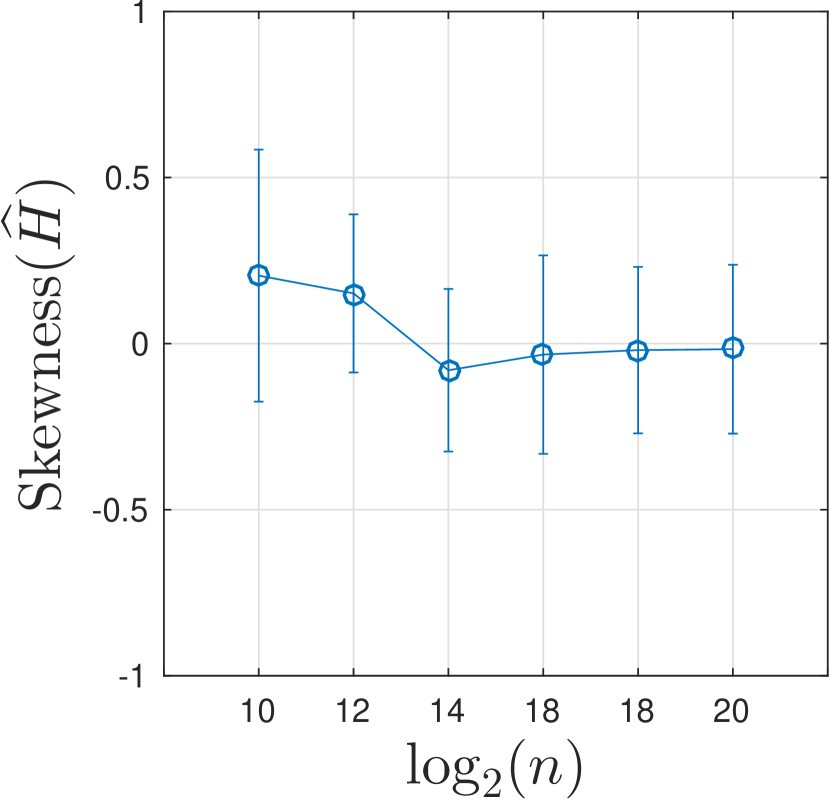

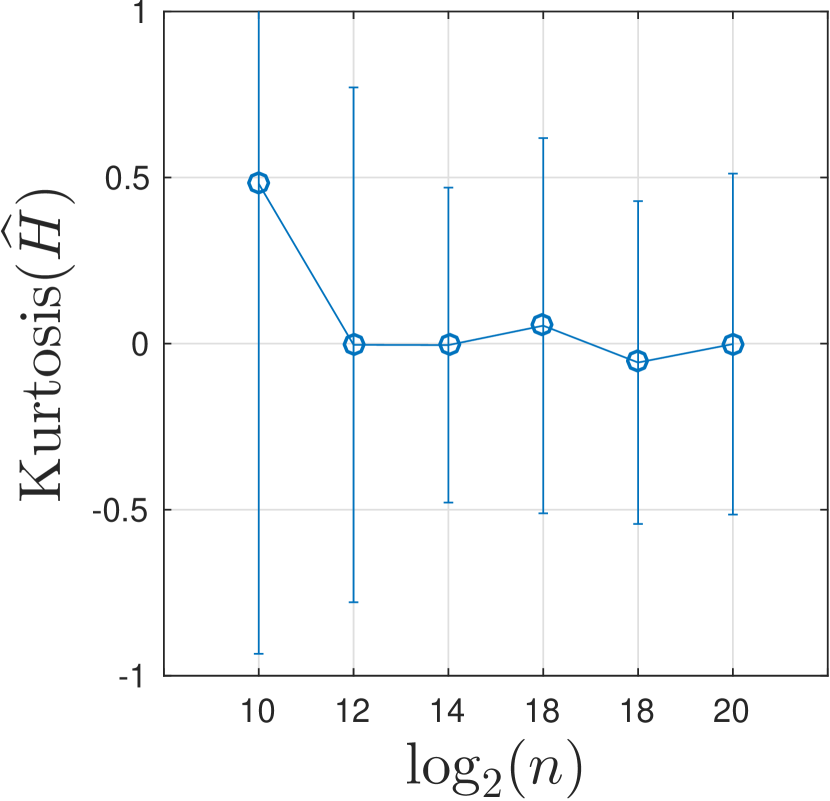

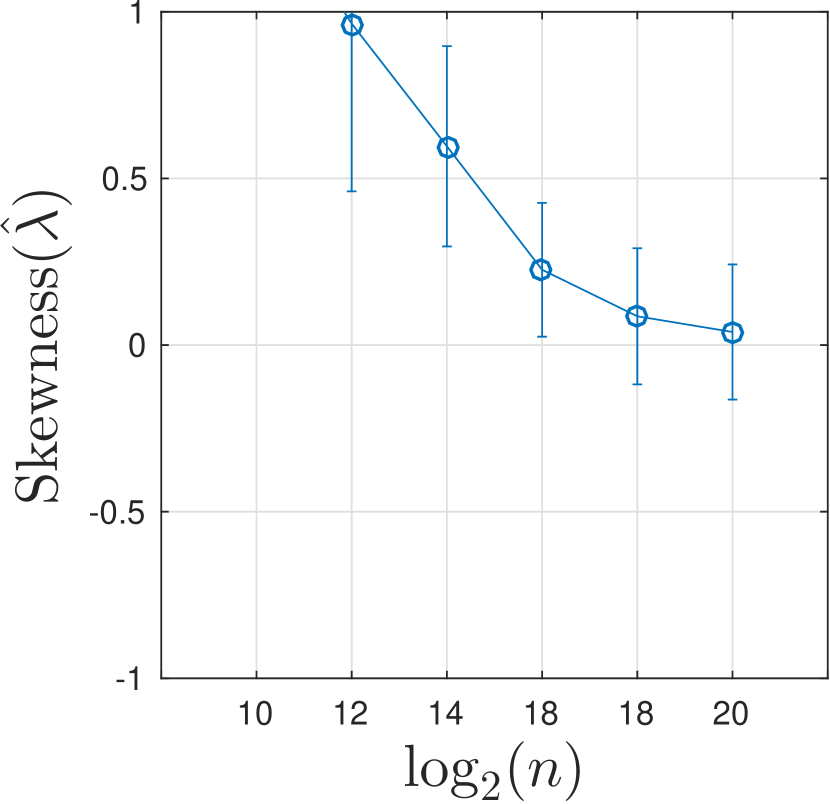

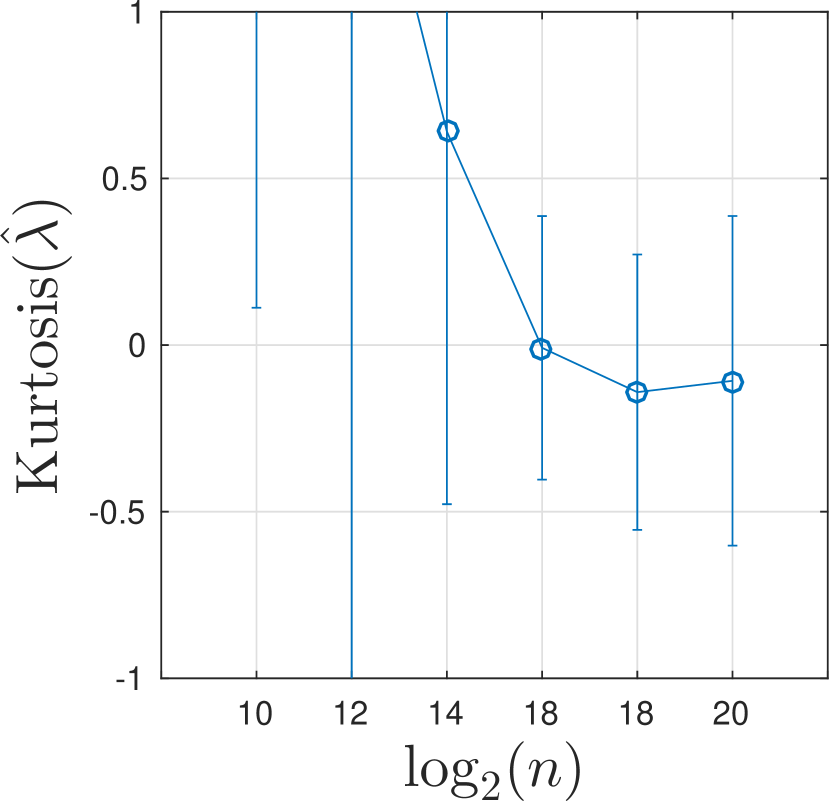

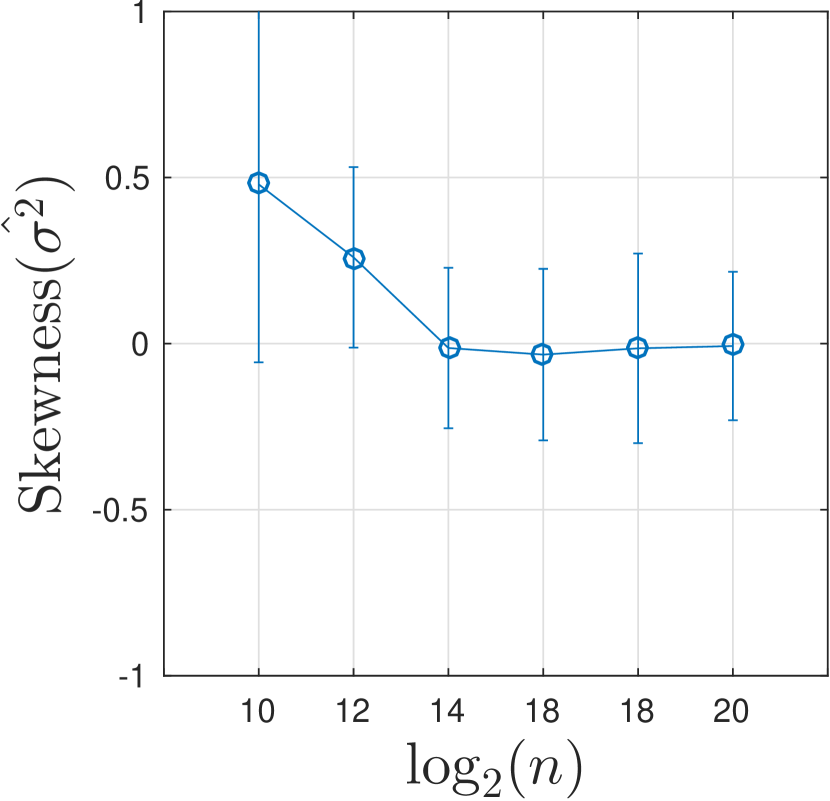

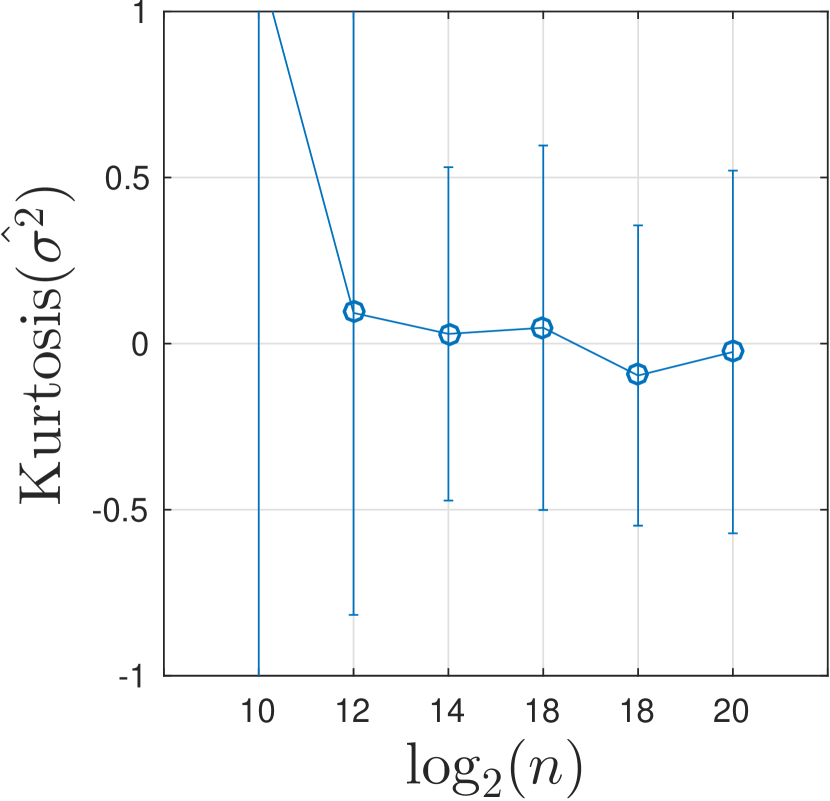

Asymptotic normality. Figure 4 displays the skewness and (excess) kurtosis of the finite sample distribution

of the estimator vector . Both measures decrease as the sample size increases. Moreover, the plots provide a measure of the sample sizes needed for an accurate Gaussian approximation to the distribution of each entry of . In particular, it can be seen that normality is reached faster (i.e., at smaller sample sizes) for than for and .

Computational cost (comparison with maximum likelihood estimation). To gauge the computational cost of the wavelet estimator (3.2), we implemented maximum likelihood estimation (of tfGn) in Matlab using the minimization routine fmincon. Unsurprisingly, maximum likelihood is extremely computationally inefficient, clocking in at roughly 15 minutes 23 seconds per estimate at the moderate sample size . By contrast, the wavelet method takes 3.86 seconds on average per estimate. Implementing maximum likelihood-based estimation beyond this sample size quickly becomes infeasible, whereas the proposed wavelet method can be used on large sample sizes at moderate computational cost. For example, at computing the wavelet estimator takes on average seconds per estimate.

Remark 3.4

For a comparative simulation study of the proposed wavelet and the Whittle estimators both in terms of statistical and computational performance, see Boniece et al. (?).

![[Uncaptioned image]](/html/1808.04935/assets/x21.png)

| under , , | |||||

|---|---|---|---|---|---|

| .0478 | .0480 | .0548 | .4298 | 1.0000 | |

| .0506 | .0478 | .0650 | .9370 | 1.0000 | |

| .0456 | .0554 | .1160 | 1.0000 | 1.0000 | |

| .0470 | .0554 | .3758 | 1.0000 | 1.0000 | |

| .0594 | .0676 | .9110 | 1.0000 | 1.0000 | |

| .0484 | .1036 | .9990 | 1.0000 | 1.0000 | |

| .0532 | .2622 | 1.0000 | 1.0000 | 1.0000 | |

| .0588 | .7712 | 1.0000 | 1.0000 | 1.0000 | |

| .0756 | .9972 | 1.0000 | 1.0000 | 1.0000 | |

| .1862 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| .5722 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

![[Uncaptioned image]](/html/1808.04935/assets/x22.png)

| under , , | |||||

|---|---|---|---|---|---|

| .0502 | .0508 | .0760 | .9434 | 1.0000 | |

| .0468 | .0498 | .1392 | 1.0000 | 1.0000 | |

| .0496 | .0492 | .4288 | 1.0000 | 1.0000 | |

| .0414 | .0622 | .9640 | 1.0000 | 1.0000 | |

| .0496 | .1172 | 1.0000 | 1.0000 | 1.0000 | |

| .0566 | .3352 | 1.0000 | 1.0000 | 1.0000 | |

| .0584 | .8702 | 1.0000 | 1.0000 | 1.0000 | |

| .1100 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| .2272 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| .7040 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| .9990 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

Hypothesis testing. To study the finite-sample performance of the test in Theorem 3.2, 5000 independent realization of tfBm paths were generated over the parameters at the sample sizes . The chosen octaves for the test statistic (3.15) were , , , , and in all cases we set . Simulation studies were conducted to estimate the quantiles used for the test in Table 2. Numerical results indicate that the asymptotic standard deviation (3.23) is not very sensitive to and lies between 0.080 and 0.101 for multiple choices of (a similar phenomenon is commonly found in the wavelet analysis of fractional stochastic processes; see, for instance, Wendt et al. (?), Section 4). So, in the simulation studies of the test we picked values for in the indicated range.

As can be seen in Table 2, for any fixed value of , reliable testing of fBm vs tfBm alternatives requires a certain sample size. For the moderate values , the test is very powerful at the moderate sample size of regardless of . However, for the small values , significantly larger sample sizes are required for attaining high power, especially for the small value . This confirms and quantifies what Figure 1, left plot, visually suggests.

3.3 River flow data modeling: fBm or tfBm?

As an application, we revisit velocity data associated with turbulent supercritical flow in the Red Cedar river, a fourth-order stream in Michigan, USA (Coordinates: 42.72908N, 84.48228W). The data was kindly provided by Prof. Mantha S. Phanikumar, from Michigan State University, and is also modeled in Meerschaert et al. (?) in the Fourier domain. The data set contains flow features over a range of spatial and temporal scales associated with turbulent flows in the natural environment and is believed to be appropriate for the analysis of energy spectra. The measurements ( points) were made at a sampling rate of 50 Hz using a 16 MHz Sontek Micro-ADV (Acoustic Doppler Velocimeter) on May 26, 2014.

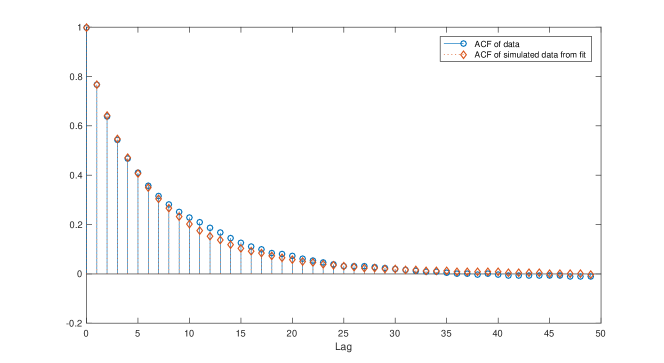

Inspection of the sample wavelet spectrum (Figure 1, right plot) shows that tfBm provides a close fit for turbulent flow data, and that a conspicuous deviation from fBm appears over large octaves. An application of (3.2) yields the wavelet-based estimates , , . In particular, is strikingly close to the value predicted by the Kolmogorov scaling model for the inertial range. Figure 5 further compares sample autocorrelation function plots of the flow data and of simulated tfBm based on the fitted values. As expected from a tfBm model, both look compatible with stationarity and the discrepancy between them is tiny. The visual impression that tfBm is a better model for the flow data than fBm is confirmed by the test (3.23). To conduct the test, we made the natural choice of low octaves and , as well as and for the large octaves. This yielded the value for the test statistic (3.15), with an associated -value of the order . Hence, and unsurprisingly, there is strong evidence against the null hypothesis of fBm. Other reasonable choices of octaves and lead to the same conclusion.

4 Conclusion

Tempered fractional Brownian motion (tfBm) is a canonical model that displays the so-named Davenport spectrum. The latter is a modification of the classical Kolmogorov spectrum for the inertial range of turbulence that includes non-scaling behavior at low frequencies. The autocorrelation of the increments of tfBm displays semi-long range dependence, a phenomenon that has been observed in a wide range of applications. In this paper, we use wavelets to construct the first estimator for tfBm and a simple and computationally efficient test for fBm vs tfBm alternatives. We make the realistic assumption that only discrete time measurements are available. The properties of the wavelet estimator and test are mathematically and computationally established. An application of the methodology to geophysical flow data from the Red Cedar river in Michigan, USA, showed that tfBm provides a much closer fit than fBm.

This work also points to a number of open research problems, such as the testing of tfBm vs stationary alternatives, physical modeling for , and the construction of statistical methodology for several other Gaussian or non-Gaussian tempered fractional models.

Appendix A Proofs and auxiliary results

Throughout the paper, we use the convention

to denote the Fourier transform for any . In all mathematical statements, we assume the following conditions hold on the underlying wavelet MRA.

Assumption : is a wavelet function, namely, it satisfies the relations

| (A.1) |

for some integer (number of vanishing moments) .

Assumption (): the scaling and wavelet functions

| and are compactly supported | (A.2) |

and .

Assumption : there is such that

| (A.3) |

Assumption (): the function

| (A.4) |

is a polynomial of degree for all .

Conditions (A.1) and (A.2) imply that exists, is everywhere differentiable and its first derivatives are zero at . Condition (A.3), in turn, implies that is continuous (see Mallat (?), Theorem 6.1) and, hence, bounded.

The Daubechies scaling and wavelet functions generally satisfy () (see Moulines et al. (?), p. 1927, or Mallat (?), p. 253). Usually, the parameter increases to infinity as goes to infinity (see Moulines et al. (?), p. 1927, or Cohen (?), Theorem 2.10.1). In some results, we will make use of the additional condition

| (A.5) |

which is assumed in Theorem 3.2.