An Approximate Message Passing Framework for Side Information††thanks: AM and DN were supported by NSF CAREER , and NSF BIGDATA ; DB and YZ were supported by NSF EECS . A subset of our results appeared in Baron et al. [5].

Abstract

Approximate message passing (AMP) methods have gained recent traction in sparse signal recovery. Additional information about the signal, or side information (SI), is commonly available and can aid in efficient signal recovery. This work presents an AMP-based framework that exploits SI and can be readily implemented in various settings for which the SI results in separable distributions. To illustrate the simplicity and applicability of our approach, this framework is applied to a Bernoulli-Gaussian (BG) model and a time-varying birth-death-drift (BDD) signal model, motivated by applications in channel estimation. We develop a suite of algorithms, called AMP-SI, and derive denoisers for the BDD and BG models. Numerical evidence demonstrating the advantages of our approach are presented alongside empirical evidence of the accuracy of a proposed state evolution.

1 Introduction

The core focus of research in many disciplines, including but not limited to communication [9], compressive imaging [2], matrix completion [10], quantizer design [24], large-scale signal recovery [48], and sparse signal processing [11], is on accurately recovering a high-dimensional, unknown signal from a limited number of noisy linear measurements by exploiting probabilistic characteristics and structure in the signal.

We consider the following model for this task. For an unknown signal ,

| (1) |

where are noisy measurements, is the measurement matrix, and is measurement noise. The objective of signal recovery is to recover or estimate from knowledge of only and , and in some cases statistical knowledge about and . A great deal of effort has gone into developing schemes for such signal recovery, for example minimization based approaches for sparse recovery [14, 44] and computationally efficient iterative algorithms [16, 34, 8], and supporting theory to tackle these challenges as datasets become larger and multidimensional. For scenarios in which the signal’s prior distribution is available, the approximate message passing framework is often utilized.

1.1 AMP for Signal Recovery

Approximate message passing or AMP [16, 23, 33] is a low-complexity algorithmic framework for efficiently recovering sparse signals in high-dimensional regression tasks (1). AMP algorithms are derived as Gaussian or quadratic approximations of loopy belief propagation algorithms (e.g., min-sum, sum-product) on the dense factor graph corresponding to (1).

AMP has a few features that make it attractive for signal recovery. In certain problem settings, AMP offers convergence in linear time, and its performance can be tracked accurately with a simple scalar iteration known as state evolution (SE), discussed below. In addition, it is well-accepted that the performance of AMP will be no worse than the best polynomial-time algorithms available [27].

AMP algorithm: The standard AMP algorithm [16] iteratively updates estimates of the unknown input signal, with being the estimate at iteration . The algorithm is given by the following set of updates. Assume that is the all-zero vector and update for with the following iterations:

| (2) | |||

| (3) |

Note that is an appropriately-chosen sequence of functions and is the measurement rate. The functions act element-wise on their vector inputs and have derivatives . Moreover, is the empirical mean, where . Here and throughout, we use capital letters to represent random variables (RVs) and lower case letters to represent realizations. We also denote a Gaussian RV with mean and variance by .

Assume that the measurement matrix has independent and identically distributed (i.i.d.) entries and the entries of the signal are i.i.d. , where is the probability density function (pdf) of the signal. Under these assumptions, one useful feature of AMP is that the input to the denoiser, , which we refer to as the pseudo-data, is almost surely equal in distribution, in the large system limit as with fixed , to the true signal plus i.i.d. Gaussian noise with variance , where is a constant value given by the SE equations, introduced in (4) below. These favorable statistical properties of the pseudo-data are due to the presence of the ‘Onsager’ term, , used in the residual step (2) of the AMP updates.

State evolution (SE): One of AMP’s attractive features is that under suitable conditions on and , its performance can be tracked accurately with a simple scalar iteration referred to as state evolution (SE) [6, 39]. In particular, performance measures such as the -error or the -error in the algorithm’s iterations concentrate to constants predicted by SE. Let the noise of (1) be element-wise i.i.d. and for let . Then the SE equations follow: let and for ,

| (4) |

where is independent of and tracks the variance of the difference between the pseudo-data and signal at iteration .

The AMP updates (2) - (3) rely on appropriately-chosen denoisers , which reduce the noise in the optimization task at each iteration. Owing to the favorable properties of the psuedo-data and the fact that one is often interested in evaluating the performance of the algorithm using the mean squared error (MSE), in iteration is often chosen to be the minimum mean squared error (MMSE) denoiser based on the pdf of :

| (5) |

where , and is a RV with the same pdf as that of . See Section 2.3.1 for further insights of how SE behaves in our framework.

1.2 Side information

In information theory [15, 18], it is well known that when different communication systems share side information (SI), overall communication can happen more efficiently. As an example, when running a Bayesian signal recovery algorithm on an input with an unknown probability density, feedback about the estimated density leads to improved signal recovery quality [22].

Signal recovery algorithms often have access to SI, denoted , that, as we will soon see, offers the potential to markedly improve recovery quality. For the noisy linear model of (1), SI has been shown to aid signal recovery when considering various application settings [46, 29, 32, 25, 38, 20, 45, 47, 12, 31, 30]. For example, three dimensional (3D) video acquisition could be performed by acquiring each frame of video, which is a 2D image, independently of other frames using a single pixel camera [42]. While recovering the current frame, it is likely that one is simultaneously recovering the previous and next frames, which can be used as SI.

We will demonstrate that our approach is potentially useful in applications by studying a channel estimation problem in wireless communication systems (Fig. 1). In typical channel estimation scenarios, a wireless device transmits a pilot sequence and data payload in batches. In batch , the pilot sequence is transmitted into the channel, where it is convolved with the channel response , yielding noisy linear measurements (details in Section 4.1). Not only is the channel response in batch sparse, the slowly time varying nature of the channel ensures that its differences relative to channel responses in previous batches are structured. Therefore, we can use , the channel response estimated in the previous batch, as SI while estimating in the current batch. In Section 5, we demonstrate that SI in the above-mentioned batched manner helps AMP achieve lower MSE for a model motivated by channel estimation.

1.3 Contributions and Organization

In this work we develop a class of sparse signal recovery algorithms that integrate SI into AMP. Our main contribution is a framework that incorporates SI in the denoiser of AMP that is Bayes-optimal in certain cases and can be adapted to arbitrary dependencies between the signal and the SI. Moreover, our framework’s conceptual simplicity allows us to extend existing SE results to AMP-SI as in (4); these SE results for signal recovery with SI are lacking in prior work [46], [49]. In the case where the SI is a Gaussian-noise corrupted view of the true signal, we rigorously show Bayes-optimality properties for AMP-SI. For more general cases, we demonstrate empirically that our proposed SE formulation tracks the AMP performance.

We demonstrate our framework through its application to two types of signals. First, a Bernoulli-Gaussian (BG) signal and second, motivated by the channel estimation problem discussed in Section 1.2, a time-varying birth-death-drift (BDD) signal. Our numerical experiments show that our proposed framework achieves a lower MSE than other previously-studied SI methods.

The remainder of the paper is organized as follows. In Section 2, we discuss the AMP algorithm and prior work in AMP approaches that utilize SI. We then present our AMP framework for SI. Next we discuss the BG model in Section 3, which is a simplified version of the BDD model studied in Section 4. In Section 5, we include numerical simulations demonstrating the good performance of AMP-SI. Section 6 concludes.

2 AMP with Side Information

2.1 Prior Work

While integrating SI (or prior information) into signal recovery algorithms is not new [46, 25, 38, 30, 13, 28], our work is a unified framework within AMP that supports arbitrary dependencies between the pairs. Prior work using SI has been either heuristic, limited to specific applications, or outside the AMP framework. For example, Wang and Liang [46] proposed the Generalized Elastic Net Prior approach, which integrates SI into AMP for a specific signal prior density, but the method lacks Bayes optimality properties and is difficult to apply to other signal models. Our algorithmic framework overcomes these limitations through a generalized, Bayes optimal framework.

Ziniel and Schniter [49] developed an AMP-based signal recovery algorithm, namely DCS-AMP, for a time-varying signal model based on Markov processes for the support and amplitude. The Markov processes and corresponding dependencies between variables are captured by factor graph models. While our BDD model (details in Section 4) is closely related to their time-varying signal model, our emphasis is to introduce the AMP-SI framework and demonstrate how SI can be incorporated in AMP without needing to carefully craft factor graphs for every new signal model.

Manoel et al. implemented an AMP-based algorithm called MINI-AMP in which the input signal is repeatedly reconstructed in a streaming fashion, and information from past reconstruction attempts is aggregated into a prior, thus improving ongoing reconstruction results [28]. Interestingly, the signal recovery approach of MINI-AMP resembles that of AMP-SI, in particular when the BG model of Section 3 is used. Finally, Manoel et al. proved that MINI-AMP is MMSE-optimal [28].

2.2 Our Approach: AMP-SI

In this paper we introduce an algorithmic framework that utilizes available SI. Our SI takes the form of an estimate , which is statistically dependent on the signal through some joint pdf . We propose a conditional denoiser,

| (6) |

where is independent of . The denoiser provides an MMSE estimate of the signal while incorporating SI. We refer to our framework using the proposed denoiser (6) within the standard AMP algorithm (2) - (3) as the AMP-SI method. The AMP-SI algorithm is the following. Assume is the all-zero vector and update for :

| (7) | |||

| (8) |

Note that is the denoising function proposed in (6), its derivative is with respect to the first input, and for . The value in (6) is given by SE equations for AMP-SI. Again, let the noise be element-wise i.i.d. and for , let . Then, and for ,

| (9) |

where are independent of , which is a standard Gaussian RV. In comparison to standard AMP, the conditional denoiser function uses SI to denoise the pseudo-data in AMP-SI.

We note that while there are rigorous theoretical results [6, 39] proving that for large the pseudo-data is approximately equal (in distribution) to the true signal plus i.i.d. Gaussian noise with variance in the case of standard AMP (2) - (3) with the standard SE (4), we only conjecture that such a result is true for AMP-SI (7) - (8) with the corresponding SE (9). This conjecture is supported by empirical evidence in Section 5 that shows that the SE accurately tracks the MSE of the AMP-SI estimates, and by a theoretical proof relating to the error (see Section 2.3).

To show that AMP-SI is conceptually intuitive to apply and can improve signal estimation quality in applications where SI is available, we apply AMP-SI to a preliminary channel estimation model (Section 4). More complex models, like those that incorporate element-wise dependencies between signal and SI, not only require more complicated denoiser and SE derivations but also need to be handled carefully theoretically. While using more realistic channel models is left for future work, our encouraging numerical results show that AMP-SI can be used beyond toy models such as BG (Section 3).

2.3 AMP-SI Theory

2.3.1 State Evolution Analysis

As mentioned previously, the performance of AMP (2)-(3) at each step of the algorithm can be rigorously characterized by the SE equations in (4). When the empirical density function of the unknown signal converges to some pdf on and the denoisers used in the AMP updates are applied element-wise to their input, Bayati and Montanari [6] proved that the SE accurately predicts AMP performance in the large system limit. For example, their result implies that the MSE, , equals almost surely in the large system limit, and additionally, it characterizes the limiting constant values for a fairly general class of loss functions. Rush and Venkataramanan [39] provide a concentration version of the asymptotic result when the prior density of is i.i.d. sub-Gaussian, showing that the probability of -deviation between various performance measures and their limiting constant values fall exponentially in .

Considering AMP-SI, however, we cannot directly apply the theoretical results of Bayati and Montanari [6] or Rush and Venkataramanan [39]. Each entry of our signal is generated according to the conditional density , where the conditioning is on the value of the corresponding entry of the SI, meaning the signal now has independent, but not identically distributed, entries. Owing to no longer being i.i.d., the conditional denoiser (6) depends on the index , meaning that different scalar denoisers will be used at different indices, based on different SI at different indices. Both results [6] and [39] require that the same denoiser function be applied to each element of the pseudo-data and our denoiser will change element-wise based on the SI.

Recent results [7] extend the asymptotic SE analysis to a larger class of possible denoisers, allowing, for example, each element of the input to use a different non-linearity as is the case in AMP-SI. We employ these results to rigorously relate the SE presented in (9) to the AMP algorithm in (7) - (8) when considering the error between the pseudo-data and the true signal. To do so, we make the following assumptions: (A1) The measurement matrix has i.i.d. mean-zero, Gaussian entries having variance . (A2) The noise is i.i.d. with finite variance . (A3) The signal and SI are sampled i.i.d. from the joint density . (A4) For , the denoisers defined in (6) are Lipschitz in their first argument. (A5) For any covariance matrix , let independent of Then for any ,

and

Under the above assumptions we have the following guarantee relating the SE to the error.

Theorem 1.

Proof.

In Appendix .4 we show an example of how to verify the assumptions (A4) and (A5) for a simple case where the signal is i.i.d. Gaussian and the SI is the signal plus i.i.d. Gaussian noise.

Ongoing work considers extensions of Theorem 1 to more general loss functions and weaker assumptions than those made in . We believe that by using the theory supporting non-separable denoisers provided in [7], it is possible to extend our AMP-SI framework to handle arbitrary joint distributions between the signal and SI (with element-wise dependencies) and that it is possible to extend the framework to the vector AMP algorithm [36, 17] allowing for a more general class of measurement matrices.

2.3.2 Bayes Optimality

When the conditional expectation denoiser (5) is used in AMP (2)-(3), the corresponding SE (4) in its convergent states coincides with Tanaka’s fixed point equation [43, 19], ensuring that if AMP runs until it converges, in the large system limit the result provides the best possible MSE achieved by any algorithm under certain problem conditions. Tanaka’s fixed point equation in the Gaussian case has been rigorously proven, see [37, 3].

In the case that the SI available to the system is a Gaussian-noise corrupted view of the true signal, i.e., , it can be shown [5] that the fixed points of AMP-SI SE (9) coincide with the fixed points of AMP SE (4) with ‘effective’ measurement rate and ‘effective’ measurement noise variance where and the depends on the prior density of the signal and the SI noise variance . The effective change in and implies that the incorporation of Gaussian-noise corrupted SI via the AMP-SI algorithm gives us Bayes-optimal signal recovery for a standard (without SI) linear regression problem (1) with more measurements and reduced measurement noise variance than our own. The details of this argument are provided in Appendix .3 and first appeared in [5]. We believe AMP-SI has similar Bayes-optimality properties to standard AMP, however, proving this rigorously is theoretically difficult since the above analysis relies heavily on the Gaussianity of the SI noise, and thus may be difficult to generalize.

3 Bernoulli-Gaussian Model

The BG model reflects the scenario in which one wants to recover a sparse signal and has access to SI in the form of the signal with additive white Gaussian noise (AWGN). In other words, at every iteration the algorithm has access to SI, and pseudo-data, , with

where the additive noise in the SI and pseudo-data are independent. The entries of follow a BG pdf:

| (10) |

so that is zero with probability and is standard Gaussian in nonzero entries. Here, represents the Dirac delta function at 0. We start with this model because it provides a closed form derivation of the denoiser with an intuitive interpretation. The next section will show that even for this toy model, the derivation is not trivial.

3.1 The Conditional Denoiser with SI for BG

In this section we will derive the following result:

Result 1.

Note that the denoiser given in (11) behaves as we would expect as the parameters in the problem change. Specifically, by considering the definition of in (14), we can see that the term approaches as the BG sparsity parameter, , approaches , and approaches as approaches , meaning that as the signal gets more sparse ( approaches ) the denoiser provides more shrinkage ( approaches ). The second term of (11), i.e. , is a weighted sum between the pseudo-data and the SI. As the SI noise increases, a larger weight is placed on the pseudo-data. Similarly as the noise in the pseudo-data increases, a larger weight is placed on the SI.

Now we derive Result 1. In what follows, the notation refers to the zero-mean Gaussian density with variance evaluated at . We will use (or , , and so on) to represent a generic pdf (or joint pdf) on the input. Before we begin the derivation, we introduce a few lemmas relating to computations involving two RVs and . Deriving the conditional denoiser for BG (and later BDD) requires the joint pdf between and (Lemma 1), the product of two Gaussian pdfs (Lemma 2), and the expectation of conditional on instances of and (Lemma 3).

Lemma 1.

Given instances and such that for some constant , , and , the joint pdf between and is:

assuming that the AWGN in , AWGN in , and are independent.

Below, we denote the density evaluated at by .

The next lemma provides a simplified expression for the product of two Gaussian densities.

Lemma 2.

For two Gaussian densities, equals

The proof of Lemma 2 involves straightforward algebra and completing the square; the lemma could also be formulated as a convolution of three Gaussian densities.

The final lemma generalizes the conditional expectation of a Gaussian random variable conditioned on the value of two noisy versions of , particularly and . We will use the shorthand notation to mean

Lemma 3.

The conditional expectation of a Gaussian RV given instances and such that for some constant and can be computed as:

assuming that the AWGN in , AWGN in , and are independent.

3.2 Derivation of the Denoiser with SI for BG

Using the aforementioned lemmas, we derive the conditional denoiser for the BG model.

Derivation of Result 1. To derive Result 1, note that

and therefore,

| (12) |

Simplifying the expression ,

| (13) | ||||

Note that here we slightly abuse the notation of a pdf with an event (i.e., or ) as an input to the density function. Considering the ratio in (13), define

Conditioned on , we can compute using Lemma 1 with , , , and :

Also, when , and are independent so

With these elements, we can compute :

| (14) |

The last term we must compute is the conditional expectation in (12). Using Lemma 3 with , , , and , we have that

| (15) |

3.3 State Evolution for BG

Using the denoiser in (11), we can compute the SE equations (9). Letting , we have and for ,

where is defined in (11), and are independent, standard Gaussian RVS that are independent of , and the expectation is with respect to , and . Because the form of the derived denoiser is complicated, it seems infeasible to find a closed-form expression for . Instead, we approximate the SE in our numerical experiments.

4 Birth-Death-Drift Model

In this section, we investigate the application of AMP-SI on a stochastic signal model closely resembling the channel estimation problem in wireless communications. Our birth-death-drift (BDD) model is based on Markov processes for the supports and amplitudes of signal elements, and has been studied in the time-varying signal literature [49]. This section presents the dynamics of individual elements more explicitly.

4.1 Connections to Channel Estimation

BDD Motivation: Our channel estimation scenario is illustrated in Fig. 1. Typical wireless devices transmit a pilot sequence and data payload in batches. In batch , the pilot sequence is transmitted into the channel, where it is convolved with the channel response , yielding noisy linear measurements,

This convolution, , can be expressed as the product of a Toeplitz matrix with a vector,

| (16) |

where is the Toeplitz matrix that corresponds to the pilot sequence . To perform channel estimation using AMP-SI, we will consider (16) as a linear inverse problem (1), where is the measurement matrix. Our goal will be to estimate the channel response in batch using the noisy measurements , matrix , and , our estimate of the channel response in the previous batch, (Fig. 1). Our resulting estimate for the channel response, , will then help us estimate the channel response in the next batch, . To develop a conditional denoiser, we need a channel model that describes the channel response , and especially its dependence on , the channel response in the previous batch. We model the channel as an (unknown) finite impulse response (FIR) filter, whose taps correspond to the amplitude of the channel response at different delays. Many filter taps are close to zero, and this sparsity makes the channel estimation problem a sparse signal recovery task.

Due to the slowly varying time dynamics of the channel, is not only sparse, but has strong dependencies with the channel response in adjacent batches. A possible model for changes from to involves (i) birth of new nonzeros in (corresponding to new wireless paths); (ii) death of nonzeros in that become zero in (existing paths are obscured as the user moves); and (iii) slow drift of existing nonzeros. We call these time-varying channel dynamics a birth-death-drift (BDD) model. To demonstrate the efficacy of our BDD model, we looked at ray tracing simulations for a mobile user moving in an urban environment. A photo of the urban environment (a suburb of Washington, DC) is shown in the top panel of Fig. 2. The bottom panel shows two realizations of the channel filter. The realization corresponding to the beginning of the mobile user’s motion is depicted by circles, and the realization corresponding to the end of the user’s motion is marked by squares. It can be seen that most nonzero taps of the channel filter drift slowly; birth and death events are highlighted for the reader’s convenience. Not only is the channel filter in each batch sparse, but its differences relative to filters in previous batches are highly structured.

For communication-minded readers, the proposed BDD model resembles that of Saleh and Valenzuela [40]. Our paper uses the BDD model for filter taps that are independent within each batch, meaning there are no inter-batch dependencies. Slow temporal dynamics over multiple batches are prevalent in real-world channels. For example, in typical wireless channels a death process involves the path energy shrinking gradually over multiple time batches [26]. However, our BDD model does not support such dynamics. Although we only demonstrate the efficacy of AMP-SI on the simplified BDD model, the framework can be adapted to other settings with SI. For example, BDD could be extended to assign different variances to the Gaussian distributions associated with different taps based on a predefined power delay profile (PDP).

Formal definition of BDD model: To formally introduce the BDD model, we start by considering a single time batch. Between the previous and current batch, the signal elements independently change according to a BDD process which defines the joint pdf , where ‘p’ denotes the previous signal, a noisy version that serves as SI, and ‘c’ the current signal.

The elements of the signal evolve following four cases in the BDD model: for any entry ,

Case 1: Zero entry remains zero, i.e., and .

Case 2: Death – nonzero entry becomes zero, i.e., and .

Case 3: Drift – nonzero entry remains nonzero, i.e., and .

Case 4: Birth – zero entry becomes nonzero, i.e., and .

We define to be the variance in the zero-mean Gaussian drift and to be the steady-state variance, or the variance of the nonzero entries in the signal at every batch. Indeed, an entry of

the current signal is nonzero in Cases 3 and 4,

and by choosing the constant such that , we ensure for both these cases.

Finally, Case j occurs with probability

and .

Remark 1.

The BG model is a simplified version of the BDD model. One can confirm that setting , , , , and obtains the model discussed in Section 3.

Remark 2.

In Case 3, a zero-mean Gaussian random variable with variance represents short-term fading due to multipath and oscillator drift. Similarly, represents inter-batch correlations or drift between nonzero elements of , and is inversely correlated to the amount of fading in a wireless channel [41].

In the BDD model, the SI takes the form of the previous batch’s signal with AWGN. The pseudo-data, which we label , is approximately the current batch’s signal with AWGN. That is, at every iteration the algorithm has access to:

where the additive noise in the SI and pseudo-data are independent. In the multiple batch setting, the pseudo-data in the final iteration of AMP-SI for approximating the signal, which is a noisy version of , becomes the SI for the approximation of the signal and the variance of this SI is available through given by the SE equations (9).

4.2 The Conditional Denoiser with SI for BDD

We now derive the conditional denoiser for the BDD model presented in Section 4.1. Recall that the inputs and of the conditional denoiser are instances of the pseudo-data and SI , respectively.

Result 2.

In what follows, the notation refers to the zero-mean Gaussian density with variance evaluated at .

| (18) |

4.3 Derivation of the Denoiser for BDD

Using the lemmas presented in Section 3, we derive the conditional denoiser for the BDD model.

Derivation of Result 2. To derive Result 2, note that

which we represent with shorthand . Then,

| (19) |

where we use the fact that in Cases 1 and 2, and so . Considering (19), let us simplify the expression . In the following we use (or , , and so on) to represent a generic pdf (or joint pdf) on the input. By Bayes’ Rule,

| (20) |

We first address Cases 1, 2, and 4 since and are independent in these cases. In Case 3, these values are dependent and therefore that case is handled carefully at the end.

Cases 1, 2, and 4: Here, we can simplify (21) by noting that due to the independence of and in these cases. For ,

| (22) |

where , and . We also compute . This equals since is independent of . Since , the conditional expectation is computed using a Wiener filter,

| (23) |

Case 3: Here, and which, in contrast to the above cases, are now dependent through . To compute note that conditional on Case 3, we may apply Lemma 1 to with , , and to obtain:

| (24) |

We also need to compute . By linearity of expectation we have

| (25) |

Conditional on Case 3, we can compute the first expectation in (25) using Lemma 3 with , since , and since :

| (26) |

where we use the fact that to simplify. Letting be such that , one can use the same approach as in Lemma 3 to obtain:

| (27) | |||

| (30) | |||

| (31) |

| (32) |

4.4 State Evolution for BDD

Using the results from the previous section, specifically the form of the denoiser in (17), we can calculate the SE equations (9). Letting , we have and for ,

where is defined in (17), and the RVs and are both zero mean unit norm Gaussian, and are independent of the RVs and , which are distributed according to the prior distributions of and . The expectation is with respect to , and , where and are dependent. Similarly to the SE equations for the BG signal model, it seems infeasible to find a closed-form value for the expectation in the SE equations due to the complicated form of the denoiser given in (17). We estimate these values numerically in the following section.

5 Numerical Results

Here, we present the empirical performance of AMP-SI for the BG and BDD signal models. All numerical results were generated using MATLAB.

BG signal: Fig. 3 presents the empirical performance of AMP-SI on a BG signal and the SE prediction of its performance. For this experiment, the signal has dimension , the SI has standard deviation , the number of measurements is , and the measurement noise standard deviation is . We set so that approximately of the entries in the signal are nonzero. The measurement matrix has i.i.d. standard Gaussian entries. The empirical normalized MSE for AMP-SI is averaged over 20 trials of a BG recovery problem. We are also plotting MSE results predicted by SE, and it can be seen that the SE prediction accurately tracks the empiricial performance of AMP-SI.

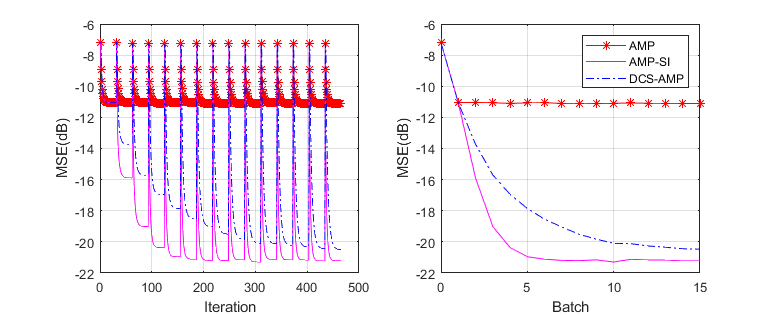

BDD signal: Fig. 4 presents experimental results for recovering a signal over 15 time batches following the BDD model of Section 4 using AMP, AMP-SI, and DCS-AMP, another AMP-based algorithm for time-varying signals [49]. In each time batch, the SI is the pseudo-data output of AMP-SI in the previous batch, except for the Batch 1 where SI is unavailable and we resort to standard AMP. For DCS-AMP, we implement the algorithm in filtering mode to match our SI setting. The signal is of dimension , the steady-state standard deviation is , the correlation among nonzero entries is , and the measurement noise has standard deviation , which corresponds to . The empirical MSE is averaged over 100 trials. For each batch, AMP-based approaches often converge within 10–20 iterations, and 30 iterations are used to play it safe. We set , , and so that there are approximately nonzero entries per signal. The measurement matrix has i.i.d. standard Gaussian entries in each batch, and the number of measurements is . It can be seen that AMP-SI outperforms DCS-AMP in every batch (except Batch 1 where they resort to AMP). This further supports our belief in AMP-SI’s Bayes-optimality properties.

Inspired by [49], we investigated how transition probabilities between different BDD states affected the performance of AMP-SI. Within the problem setting of Fig. 4, we varied , , and . We found that AMP-SI out-performed AMP at Batch 15 for all configurations. The performance gap was largest for large and small and ; the gap narrowed as decreased and and increased. We also experimented with holding constant and varied and . Again, as decreased, the gap between AMP-SI and AMP shrank. That said, for large , AMP-SI still improved reconstruction quality for small .

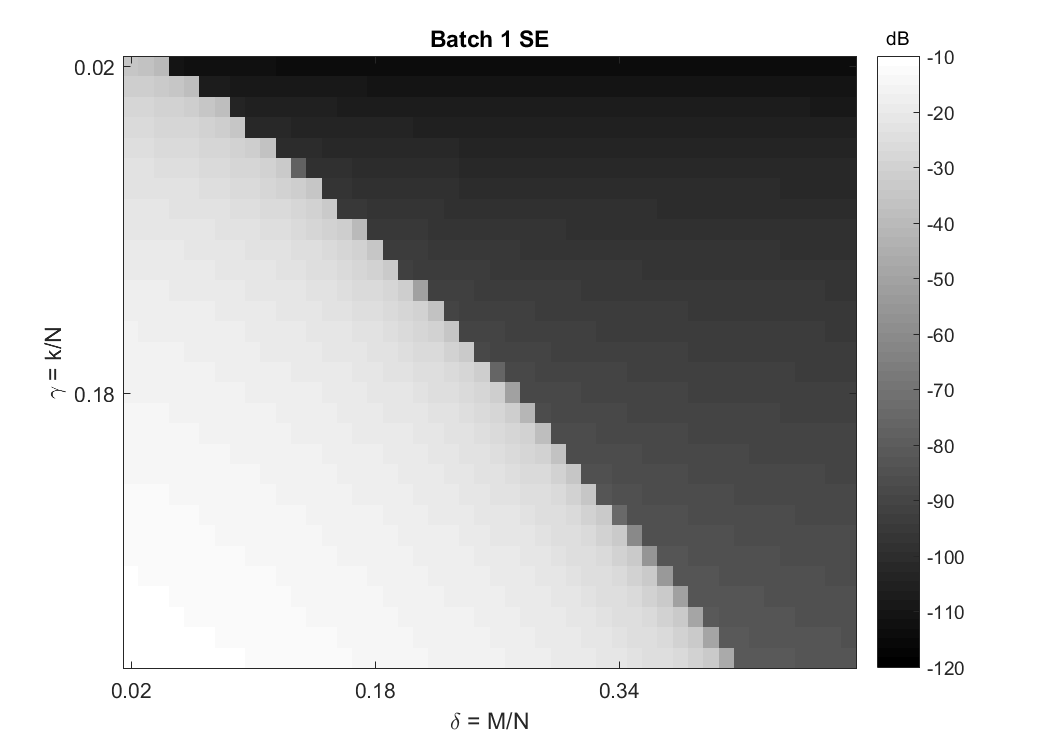

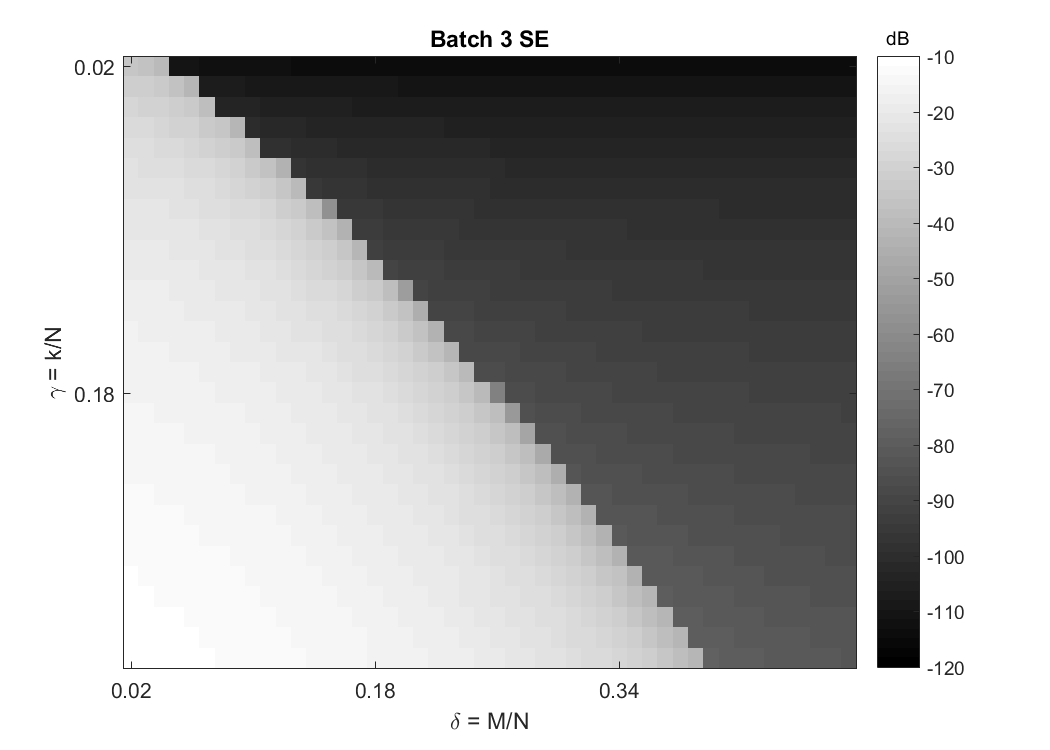

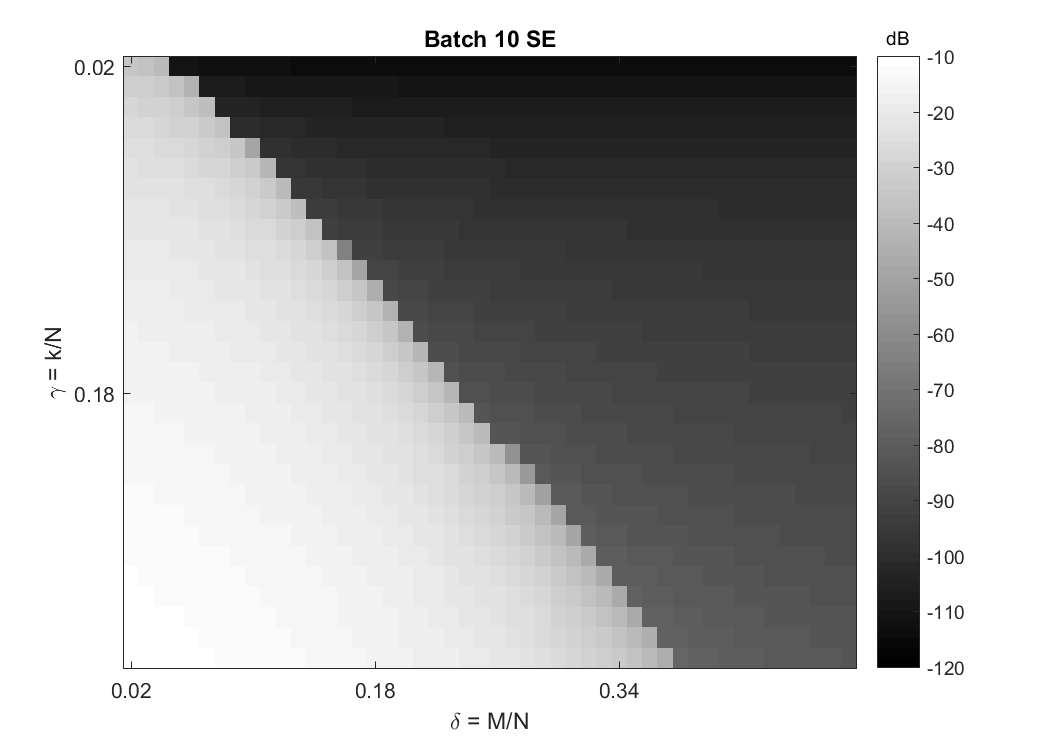

SE for BDD: To highlight the advantages of SI, Fig. 5 shows the recovery quality predicted by SE. Here, the SI dependencies remain identical to the experiments used for Fig. 4 as we vary the number of measurements (to show different ) and and (to show different percentages of nonzeros, ). We also hold the measurement noise constant. To vary , we keep while modifying the probability of the drift case, , accordingly. In each panel, the horizontal axis corresponds to , the vertical axis to , and shades of gray to the SE prediction of the MSE. Batch 1 corresponds to the first time the signal is recovered without SI, Batch 3 uses recovered signals from the second batch as SI, and Batch 10 uses the recovered signal from Batch 9 as SI. The high-quality dark gray region in the upper right portion of each panel is expanding, while the low-quality light gray region is shrinking, showing improved signal recovery due to the SI. More specifically, the proportion of the high-quality dark grey region in each subplot is 0.413 (Batch 1), 0.448 (Batch 3), and 0.562 (Batch 10). It can be seen that the same MSE quality is obtained from a measurement rate lower than without SI.

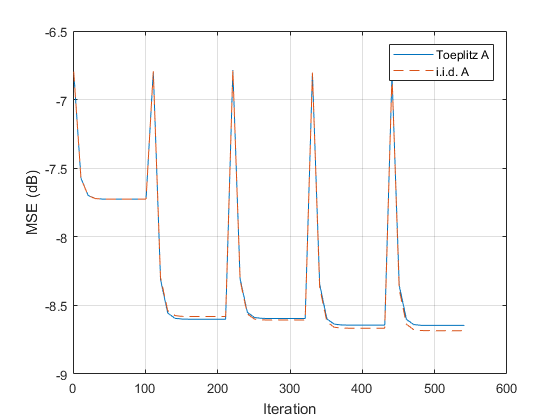

Channel estimation with Toeplitz matrices: So far we used i.i.d. Gaussian matrices, and we now transition to Toeplitz matrices in order to demonstrate that AMP-SI is suitable for channel estimation (details in Section 4). Based on (16), the channel estimation problem deviates from the BDD model in three aspects. First, as mentioned, is Toeplitz rather than i.i.d. Gaussian. It is well known that for non-i.i.d. sensing matrices, the standard AMP prescribed by (2) and (3) often suffers from divergence over iterations. A common approach to improve convergence of iterative algorithms is damping; in AMP, the standard iteration (3) is replaced by . Rangan et al. [35] demonstrate that damping is effective in aiding the convergence of AMP for some non-i.i.d. sensing matrices. It should be noted that supporting theory for AMP-based algorithms is only rigorous for certain classes of random matrices [6, 36], which exclude Toeplitz matrices. Thus we evaluate the performance of AMP-SI for Toeplitz matrices by comparing empirical reconstruction results to standard AMP-SI settings. Lastly, for a pilot sequence , the number of rows of the measurement matrix, , equals , which typically exceeds , the number of columns. This inverse problem is expansive () instead of compressive (, where we remind the reader that AMP and SE theory support arbitrary where .

Our experiment had 5 time batches. We set the length of the channel response to , the length of the pilot sequence , the standard deviation of the steady signal , the decay rate of nonzeros , and the measurement noise standard deviation . This setting corresponds to SNR= 0dB, 20dB and 40dB, and . For BDD model parameters, we set , . Thus at each time batch, of the entries of the channel response are nonzero. The individual entries of the pilot are , each with probability 0.5. We performed damping using parameter . Table 1 demonstrates the empirical channel estimation performance of AMP-SI averaged over 50 realizations. Compared to standard AMP (batch 1 in Table 1), AMP-SI consistently achieves lower MSE levels starting from batch 2. One striking observation from Fig. 6 is the similar performance of AMP-SI for Toeplitz (channel estimation) and i.i.d. matrices. This similarity leads us to conjecture that for the given BDD signal model, SE prediction tracks the performance of AMP/AMP-SI with Toeplitz matrices as well as the i.i.d. Gaussian case. The conjecture is further evident from Table 2. Observations from other BDD time batches resemble batch 5 (Table 2) and are not included.

| Channel Estimation MSE(dB) | ||||

|---|---|---|---|---|

| SNR | Batch 1 |

|

Batch 5 | |

| 0dB | -7.71 | -8.61 | -8.68 | |

| 20dB | -23.49 | -24.74 | -24.86 | |

| 40dB | -45.41 | -45.83 | -45.82 | |

| AMP-SI Performance in MSE(dB) at Time Batch 5 | |||

|---|---|---|---|

| SNR | i.i.d. A | SE Prediction | Toeplitz A |

| 0dB | -8.68 | -8.64 | -8.65 |

| 20dB | -24.86 | -24.86 | -24.77 |

| 40dB | -45.82 | -45.91 | -45.86 |

6 Challenges and Future Work

In this work, we presented AMP-SI, a suite of approximate message passing (AMP) based algorithms that utilize side information (SI) to aid in signal recovery using conditional denoisers. We derive conditional denoisers for a Bernoulli-Gaussian (BG) signal model and a more complicated time-varying birth-death-drift (BDD) signal model, motivated by channel estimation. We also conjectured state evolution (SE) properties. Numerical experiments show that the proposed SE accurately tracks the performance of AMP-SI, and that AMP-SI achieves the same MSE as AMP using a lower measurement rate.

To simulate the channel estimation task, we additionally consider a Toeplitz measurement matrix as opposed to the standard Gaussian i.i.d. matrix. Our results show that AMP-SI is able to obtain a lower MSE than AMP for such a setting. A challenge and future direction with this line of work is that the current theoretical guarantees for AMP assume that is an i.i.d. matrix. Although AMP often diverges when non-i.i.d. matrices are used, there is empirical evidence that AMP can successfully perform deconvolution and utilize other structures in various settings [21, 4]. We believe our AMP-SI framework will lead to new applications in a broad class of problems while also presenting interesting theoretical challenges.

Acknowledgments

We are grateful to Yavuz Yapici and Ismail Guvenc who helped us formulate the BDD model, and to Chethan Anjinappa whose numerical ray tracing simulation (Fig. 2) helped confirm the model. Our work originated from earlier work on AMP with SI, which was joint with Tina Woolf. We thank Hangjin Liu for conversations about using the recent results by Berthier et al. [7] for our SE proofs. Finally, we thank Junan Zhu and Yanting Ma for helping us formulate the problem and master some of the deeper technical details.

.1 Proof of Lemma 1

Recall from the Lemma statement that and where .

Then from Bayes’ rule, and computing we have:

where equality (1) relies on Bayes’ rule applied to . Therefore,

where equality (2) uses Lemma 2.

.2 Proof of Lemma 3

Recall from the Lemma statement that and where .

Because , , and are jointly Gaussian RVs, the MMSE-optimal estimator for conditioned on and is linear,

| (34) |

where , , and are constants. A well known result (see, e.g., Theorem 9.1 of [1]) states that , where

We compute these terms one by one. First, , , and all have zero mean, and so , which implies that the constant in the linear form (34) is zero. Second,

because the zero means ensure that only the cross terms and appear in the expression for . The cross terms are computed as

Therefore, . Third,

where once again only the cross terms need be computed. These cross terms are (i) ; (ii) ; and (iii)

The MMSE-optimal estimator is

| (35) |

.3 Fixed points of AMP-SI SE with Gaussian SI

This appendix will show that when the SI is a Gaussian-noise corrupted observation of the true signal, i.e., , the fixed points of AMP-SI SE (9) coincide with the fixed points of AMP SE (4) with ‘effective’ measurement rate and ‘effective’ measurement noise variance where and depends on the pdf of the signal and the SI noise variance .

Before demonstrating the aforementioned Bayes-optimality property of AMP-SI, we use matched filter arguments to provide a simplified representation of the conditional denoiser of (6) when the SI is the signal viewed with AWGN. In calculating the AMP-SI denoiser (6), we want to calculate the expectation of conditioned on the pseudo data, , and SI, , where and are independent, standard Gaussian RVs. We define signal and noise vectors as and , respectively, where is the transpose operator. The matched filter estimates the unknown by computing the inner product between

and a matched filter . An optimal that maximizes the signal to noise ratio while having unit norm is computed by inverting , the auto-covariance matrix of ,

It can be shown that , and the inner product is defined as

| (36) |

Note that equals

where is standard Gaussian, denotes equality in distribution, and the variance term, , is

| (37) |

The above provides us with the following simplification of the AMP-SI denoiser (6) for SI with AWGN,

| (38) |

where and are defined in (36) and (37). We note that is a function of , but for brevity we drop this dependence in the following. Considering (9) and (38),

| (39) |

We simplify the SE equations (9) using (39) and the definition of in (37). Let and for ,

| (40) |

The results in (38) and (40) provide a simplified way to calculate the conditional denoiser of (6) and the SE when the signal and the SI are related through Gaussian noise. Moreover, at the stationary point of (40) we have

| (41) |

where is the scalar channel variance. Comparing (4) (SE without SI) and (41), we denote the variance in the conditional expectation by . Note that , because , and we can rewrite the above as

| (42) |

We see that AMP-SI SE (9) has fixed points coinciding with the fixed points of standard AMP SE (4) with ‘effective’ measurement rate and ‘effective’ measurement noise variance where is the noise in the SI and is the stationary point of (40). This effective change in and implies that the incorporation of SI with AWGN via the AMP-SI algorithm gives us signal recovery for a standard (without SI) linear regression problem (1) with more measurements and/or reduced measurement noise variance than our own, and the effect becomes more pronounced, as the noise variance in the SI, , gets small.

The above analysis relies on the fact that for the conditional expectation denoiser in standard (without SI) AMP (2)-(3), the corresponding SE equation (4) in its convergent states coincides with Tanaka’s fixed point equation [43], ensuring that if AMP runs until it converges, the result provides the best possible MSE achieved by any algorithm under certain conditions. (These conditions on and , while outside the scope of this paper, ensure that there is a single solution to Tanaka’s fixed point equation, since multiple solutions may create a disparity between the MSE of AMP and the MMSE [23], implying that AMP-SI might be sub-optimal in such cases.) Our analysis relies heavily on the Gaussianity of the SI noise and may not easily be generalized.

.4 Theorem 1 Example

As an example, we study the simple Gaussian-Gaussian (GG) case. In the GG model one wants to recover a signal having i.i.d. zero-mean Gaussian elements with variance with SI equal to the signal plus additive white Gaussian noise (AWGN) with variance , meaning . We will show that for assumptions (A4) and (A5) to be true, we need finite fourth moments and .

| (43) |

Now we would like to prove the following assumptions needed for Theorem 1 to hold: (A4) For , the denoisers defined in (6) are Lipschitz in their first argument. (A5) For any covariance matrix , let independent of Then for any ,

| (44) |

and

| (45) |

Next we consider assumption (A5). We will show (44) and then demonstrating (45) follows similarly. First note

Then using , we see

References

- [1] Minimum mean square error. https://en.wikipedia.org/wiki/Minimum_mean_square_error#cite_note-1, Retrieved July 7, 2017.

- [2] H. Arguello and G. Arce. Code aperture optimization for spectrally agile compressive imaging. J. Opt. Soc. Am., 28(11):2400–2413, Nov. 2011.

- [3] J. Barbier, N. Macris, M. Dia, and F. Krzakala. Mutual information and optimality of approximate message-passing in random linear estimation. arXiv preprint arXiv:1701.05823, 2017.

- [4] J. Barbier, C. Schülke, and F. Krzakala. Approximate message-passing with spatially coupled structured operators, with applications to compressed sensing and sparse superposition codes. J. Stat. Mech-Theory E., 2015(5):P05013, May 2015.

- [5] D. Baron, A. Ma, D. Needell, C. Rush, and T. Woolf. Conditional approximate message passing with side information. In Proc. Asilomar Conf. Signals, Systems, and Computers, Pacific Grove, CA, Nov. 2017.

- [6] M. Bayati and A. Montanari. The dynamics of message passing on dense graphs, with applications to compressed sensing. IEEE Trans. Inf. Theory, 57(2):764–785, Feb. 2011.

- [7] R. Berthier, A. Montanari, and P.-M. Nguyen. State evolution for approximate message passing with non-separable functions. arXiv preprint arXiv:1708.03950, 2017.

- [8] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein. Distributed optimization and statistical learning via the alternating direction method of multipliers. Found. Trends Mach. Learn., 3(1):1–122, Jan. 2011.

- [9] G. Caire, R. Muller, and T. Tanaka. Iterative multiuser joint decoding: Optimal power allocation and low-complexity implementation. IEEE Trans. Inf. Theory, 50(9):1950–1973, Sept. 2004.

- [10] E. Candès and B. Recht. Exact matrix completion via convex optimization. Found. Comput. Math., 9:717–772, Dec. 2009.

- [11] E. Candès and T. Tao. Near-optimal signal recovery from random projections: Universal encoding strategies? IEEE Trans. Inf. Theory, 52(12):5406–5425, Dec. 2006.

- [12] G.-H. Chen, J. Tang, and S. Leng. Prior image constrained compressed sensing (PICCS): a method to accurately reconstruct dynamic CT images from highly undersampled projection data sets. Medical Physics, 35(2):600–663, Feb. 2008.

- [13] M. Chen, F. Renna, and M. Rodrigues. On the design of linear projections for compressive sensing with side information. In Proc. IEEE Int. Symp. Inf. Theory (ISIT), pages 670–674, Barcelona, Spain, July 2016.

- [14] S. Chen, D. Donoho, and M. Saunders. Atomic decomposition by basis pursuit. SIAM J. Sci. Comp., 20(1):33–61, Aug. 1998.

- [15] T. Cover and J. Thomas. Elements of Information Theory. New York, NY, USA: Wiley-Interscience, July 2006.

- [16] D. Donoho, A. Maleki, and A. Montanari. Message passing algorithms for compressed sensing. Proc. Natl. Acad. Sci., 106(45):18914–18919, Nov. 2009.

- [17] A. Fletcher, P. Pandit, S. Rangan, S. Sarkar, and P. Schniter. Plug-in estimation in high-dimensional linear inverse problems: A rigorous analysis. In Workshop Neural Info. Proc. Sys. (NIPS), pages 7451–7460, 2018.

- [18] R. Gallager. Information Theory and Reliable Communications. Wiley, Jan. 1968.

- [19] D. Guo and S. Verdú. Randomly spread CDMA: Asymptotics via statistical physics. IEEE Trans. Inf. Theory, 51(6):1983–2010, June 2005.

- [20] C. Herzet, C. Soussen, J. Idier, and R. Gribonval. Exact recovery conditions for sparse representation with partial support information. IEEE Trans. Inf. Theory, 59(11):7509–7524, Aug. 2013.

- [21] U. Kamilov, A. Bourquard, and M. Unser. Sparse image deconvolution with message passing. In Proc. 5th Workshop on Signal Process. with Adaptive Sparse Structured Representations (SPARS), Feb. 2013.

- [22] U. Kamilov, S. Rangan, A. Fletcher, and M. Unser. Approximate message passing with consistent parameter estimation and applications to sparse learning. In Workshop Neural Info. Proc. Sys. (NIPS), pages 2447–2455, Dec. 2012.

- [23] F. Krzakala, M. Mézard, F. Sausset, Y. Sun, and L. Zdeborová. Probabilistic reconstruction in compressed sensing: Algorithms, phase diagrams, and threshold achieving matrices. J. Stat. Mech. - Theory E., 2012(08):P08009, Aug. 2012.

- [24] S. Lloyd. Least squares quantization in PCM. IEEE Trans. Inf. Theory, 28(2):129–137, Mar. 1982.

- [25] H. V. Luong, J. Seiler, A. Kaup, S. Forchhammer, and N. Deligiannis. Measurement bounds for sparse signal reconstruction with multiple side information. Arxiv preprint arXiv:1605.03234, Jan. 2017.

- [26] G. MacCartney, T. Rappaport, and S. Rangan. Rapid fading due to human blockage in pedestrian crowds at 5g millimeter-wave frequencies. GLOBECOM 2017 - 2017 IEEE Global Communications Conference, Dec 2017.

- [27] A. Maleki. Approximate message passing algorithms for compressed sensing. Stanford University, Nov. 2010.

- [28] A. Manoel, F. Krzakala, E. W. Tramel, and L. Zdeborová. Streaming bayesian inference: theoretical limits and mini-batch approximate message-passing. In Communication, Control, and Computing (Allerton), 2017 55th Annual Allerton Conference on, pages 1048–1055. IEEE, 2017.

- [29] H. Mansour and R. Saab. Recovery analysis for weighted -minimization using the null space property. Appl. Comput. Harmon. Anal., 43(1):23–38, July 2017.

- [30] J. Mota, N. Deligiannis, and M. Rodrigues. Compressed sensing with prior information: Strategies, geometry, and bounds. IEEE Trans. Inf. Theory, 63(7):4472–4496, July 2017.

- [31] J. Mota, N. Deligiannis, A. Sankaranaraynan, V. Cevher, and M. Rodrigues. Adaptive-rate reconstruction of time-varying signals with application in compressive foreground extraction. IEEE Trans. Signal Process., 64(14):3651–3666, Mar. 2016.

- [32] D. Needell, R. Saab, and T. Woolf. Weighted-minimization for sparse recovery under arbitrary prior information. Inst. Math. Inf. Infer., 6(3):284–309, Jan. 2017.

- [33] S. Rangan. Generalized approximate message passing for estimation with random linear mixing. In Proc. IEEE Int. Symp. Inf. Theory (ISIT), pages 2168–2172, July 2011.

- [34] S. Rangan, A. Fletcher, P. Schniter, and U. Kamilov. Inference for generalized linear models via alternating directions and Bethe free energy minimization. In Proc. Int. Symp. Inf. Theory (ISIT), pages 1640–1644, June 2015.

- [35] S. Rangan, P. Schniter, and A. Fletcher. On the convergence of approximate message passing with arbitrary matrices. In Proc. IEEE Int. Symp. Inform. Theory (ISIT), pages 236–240, Feb. 2014.

- [36] S. Rangan, P. Schniter, and A. Fletcher. Vector approximate message passing. In Proc. IEEE Int. Symp. Inf. Theory (ISIT), pages 1588–1592, July 2017.

- [37] G. Reeves and H. D. Pfister. The replica-symmetric prediction for compressed sensing with gaussian matrices is exact. In Proc. IEEE Int. Symp. Inform. Theory (ISIT), pages 665–669. IEEE, 2016.

- [38] F. Renna, L. Wang, X. Yuan, J. Yang, G. Reeves, A. Calderbank, L.Carin, and M. Rodrigues. Classification and reconstruction of high-dimensional signals from low-dimensional features in the presence of side information. IEEE Trans. Inf. Theory, 62(11):6459–6492, Sept. 2016.

- [39] C. Rush and R. Venkataramanan. Finite sample analysis of approximate message passing. IEEE Trans. Inf. Theory, (forthcoming). Available: https://ieeexplore.ieee.org/document/8318695/.

- [40] A. Saleh and R. Valenzuela. A statistical model for indoor multipath propagation. IEEE J. Select. Areas Commun., 5(2):128–137, Feb. 1987.

- [41] P. Shankar. Fading and Shadowing in Wireless Systems. Springer, 2 edition, 2019.

- [42] D. Takhar, J. Laska, M. Wakin, M. Duarte, D. Baron, S. Sarvotham, K. Kelly, and R. Baraniuk. A new compressive imaging camera architecture using optical-domain compression. Feb. 2006.

- [43] T. Tanaka. A statistical-mechanics approach to large-system analysis of CDMA multiuser detectors. IEEE Trans. Inf. Theory, 48(11):2888–2910, Nov. 2002.

- [44] R. Tibshirani. Regression shrinkage and selection via the LASSO. J. Royal Stat. Soc. Series B (Methodological), 58(1):267–288, Jan. 1996.

- [45] N. Vaswani and W. Lu. Modified-CS: Modifying compressive sensing problems for partially known support. IEEE Trans. Signal Process., 58(9):4595–4607, May 2010.

- [46] X. Wang and J. Liang. Approximate message passing-based compressed sensing reconstruction with generalized elastic net prior. Signal Process. Image, 37:19–33, Sept. 2015.

- [47] L. Weizman, Y. Eldar, and D. Bashat. Compressed sensing for longitudinal MRI: An adaptive-weighted approach. Medical Physics, 42(9):5195–5208, Nov. 2015.

- [48] J. Zhu, D. Baron, and A. Beirami. Optimal trade-offs in multi-processor approximate message passing. Arxiv preprint arXiv:1601.03790, Nov. 2016.

- [49] J. Ziniel and P. Schniter. Dynamic compressive sensing of time-varying signals via approximate message passing. IEEE Trans. Signal Process., 61(21):5270–5284, Nov. 2013.