22email: damien.challet@centralesupelec.fr

Strategic behaviour and indicative price diffusion in Paris Stock Exchange auctions

Abstract

We report statistical regularities of the opening and closing auctions of French equities, focusing on the diffusive properties of the indicative auction price. Two mechanisms are at play as the auction end time nears: the typical price change magnitude decreases, favoring underdiffusion, while the rate of these events increases, potentially leading to overdiffusion. A third mechanism, caused by the strategic behavior of traders, is needed to produce nearly diffusive prices: waiting to submit buy orders until sell orders have decreased the indicative price and vice-versa.

Research in market micro-structure has focused on the dynamical properties of open markets (O’Hara, 1997; Bouchaud et al., 2009). However, main stock exchanges have been using auction phases when they open and close for a long time111London Stock Exchange and XETRA (Germany) recently added a mid-day short auction phase.. Auctions are known to have many advantages, provided that there are enough participants: for example, auction prices are well-defined, correspond to larger liquidity, and decrease price volatility (and bid-ask spreads) shortly after the opening time and before closing time (see e.g. Pagano and Schwartz (2003); Chelley-Steeley (2008); Pagano et al. (2013)).

Only a handful of papers are devoted to the dynamics of auction phases, i.e., periods during which market participants may send limit or market orders specifically for the auction. Boussetta et al. (2016) investigate when fast and slow traders send their orders during the opening auction phase of the Paris Stock Exchange and find markedly different behaviors: the slow brokers are active first, while high-frequency traders are mostly active near the end of auctions. In the same vein, Bellia et al. (2016) show how and when low-latency traders (identified as high frequency traders) add or remove liquidity in the pre-opening auction of the Tokyo Stock Exchange. Accordingly, Yergeau (2018) finds typical patterns of high-frequency algorithmic trading in the auctions of XTRA. Challet and Gourianov (2018) analyze anonymous data from US equities and compute the response functions of the final auction price to the addition or cancellation of auction orders as a function of the time remaining until the auction, which have strikingly different behaviors in the opening and closing auction phases. Finally, chapter 2 of Lehalle and Laruelle (2018) reports typical daily patterns of matched volume, in a spirit similar to that of the present chapter.

1 Auctions, data and notations

The opening auction phase of Paris Stock Exchange starts at 7:15 and ends at 9:00 while the closing auction phase is limited to the period 17:30 to 17:35. The auction price maximises the matched volume.

From the Thomson Reuters Tick History, we extract auction phase data for the 2013-04-16 components of the CAC40 index. This database contains all the updates to either the indicative match price or the indicative matched volume in the 2010-08-02 to 2017-04-12 period, which amounts to 8,095,524 data points for the opening auctions and 15,007,048 for the closing auctions. Note that the closing auction phase has about twice as many updates despite being considerably shorter.

For each asset , we denote the indicative price of auction of day at time by , the time of auction by and the auction price by . Dropping the index since this paper focuses on a single asset at a time, the -th indicative price change occurs at physical time and its log-return equals . It is useful to work in the time-to-auction (TTA henceforth) time arrow: setting , the log-return between the final auction price and the current indicative is then

Similarly, the indicative matched volume is written as , while the final volume is . Finally, when computing averages over days, since updates occur at random times, we will use time coarsening by seconds, i.e. compute quantity averages over days within time slices of seconds.

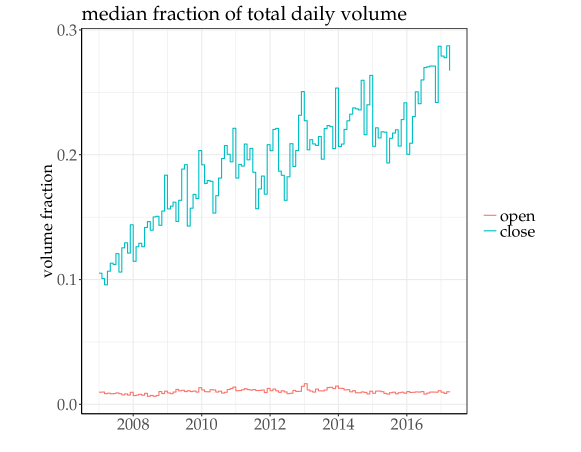

Figure 1 illustrates why auctions deserve attention: the relative importance of the closing auction volume has more than doubled in the last 10 years. Note that the relative opening auction volume of French equities is quite small (typically around 1%) and has stayed remarkably constant.

2 From collisions in event time to diffusion in physical time

It is useful to consider the price as the position of a uni-dimensional random walker and assume that each price change is caused by a collision: if collision shifts the price by , after collisions the mean square displacement equals

| (1) |

if the increments are i.i.d, a straightforward consequence of the central limit theorem. This corresponds to standard diffusion. In addition, if the collisions occur at a constant rate , then time is homogeneous and . As we shall see, none of these assumptions is true during auctions, which makes them quite interesting dynamical systems.

2.1 Event rates

In the case of indicative auction prices, the event rate is not constant: the activity usually increases just before the auction time. This finding is a generic feature of auctions with fixed end time (Borle et al., 2006), and more generally of human procrastinating nature when faced with a deadline, be it conference registration (Alfi et al., 2007) or paying its fee (Alfi et al., 2009).

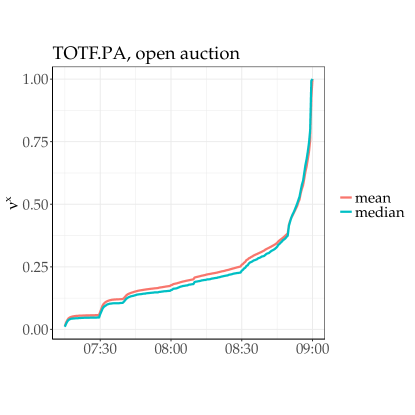

Let us denote by the number of price events (changes) having occurred up to time on day for auction . The activity pattern of day can be measured by the ratio between the number of events up to time on day and the total number of events which happened that day, defined as . The average and median , where stands for either average or median over days, can be seen in Fig. 2. One similarly defines the fraction between the indicative matched volume at time and the auction volume , reported in the same figure.

There are clear peaks of changes for both and at unimaginative physical times such as 7:30, 8:30, etc., and at round minutes and multiples of 30 seconds during the closing auction. This of course denotes a regular behavior of some investors. If each peak is systematically caused by a single trader, there are reasons to think that this regularity does inject information and that it will be exploited by more flexible traders. However, sending orders at the same time as other traders is a rational behavior as it allows one to hide in the crowd, unless one’s orders are systematically of the same imbalance sign as the aggregate volume at that time. Thus, from a game theoretical point of view, the emergence of activity peaks is self-organized and stable. Nothing constrains the number of peaks and their locations, which are hence instances of emerging, self-organized conventions. The closing auction being much shorter than the opening one, it is natural that the peaks should appear at round minutes, as this somehow provides more obvious peak locations than the opening auction. When the closing auction lasts for a much longer time, e.g. for US equities, there are much fewer price activity peaks (Challet and Gourianov, 2018).

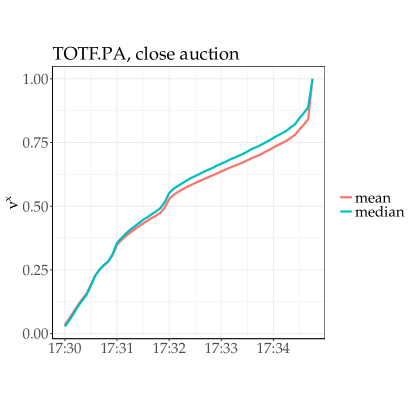

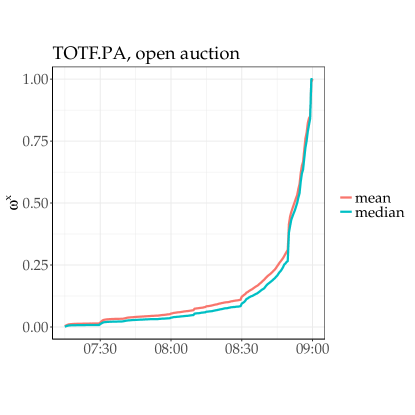

The global pattern of price changes and total volume matched clearly differs between both types of auctions. During opening auctions, the price change rate increases much, starting from a low baseline. During closing auctions, the opposite happens: price change activity is first large, slows down during the first 2-3 minutes and then picks up again just before the cut-off time (17:34:45). The average relative matched volume behaves similarly as during the opening auctions, probably because prices changes are mostly caused by the arrival of new matchable volume, not cancellations. Indeed, half of the open auction events typically happen in the last 10 minutes for most assets, and half of the volume is matched in the last minutes. Closing auctions display a different behavior: more than half of the volume is matched during the first minute, and 80% during the first two minutes. For a few assets (TOTF.PA, UNBP.PA, for ones), there is a peak of indicative matched volume up to 10% larger than the auction volume about one minute before the end of the auction; the same behavior is found in US equity markets (Challet and Gourianov, 2018).

2.2 Activity acceleration

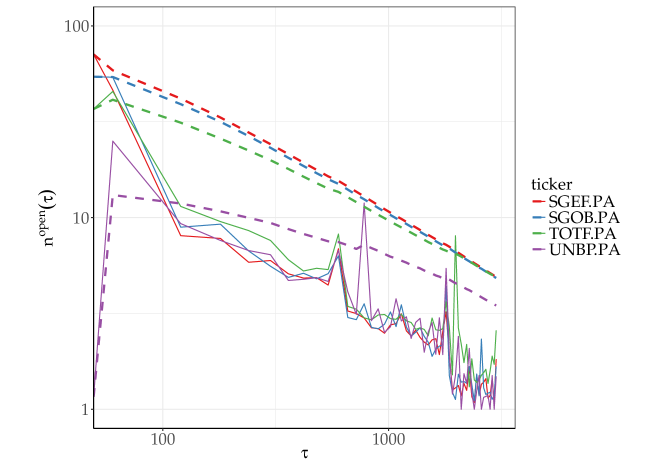

The acceleration pattern of price change rate follows some regularity. To characterize it in a simpler way, it is useful to work in Time-To-Auction frame. Since the latter reverts the time arrow, the activity decelerates as a function of . Let us denote the average event rate so that the expected number of event in the period to is . Figure 3 shows of several assets, together with the smoothed version of , denoted by : if , so does but with much less noise, which helps assessing the presence of a power-law visually. We shall drop the superscript when no confusion is possible.

Assuming that , we perform a robust linear fit of for seconds and only keep the fits whose t-statistics associated with is larger than 5. This particular choice of interval for corresponds to a typical period during which the autocorrelation of at one lag is roughly constant (see subsection 2.4). In addition, for each asset, we only keep days during which there were at least 50 price changes.

If the typical absolute value of price change does not depend on and is still i.i.d., Eq. (1) becomes

| (2) |

hence the Hurst exponent in time, denoted by , equals : the price change rate influences the diffusive pattern in a simple way, given the above approximations. It is worth noting at this juncture that in the normal time frame the price is overdiffusive if does not depend on and if , i.e., if the rate of price changes increases near the auction end time and the Hurst exponent in the normal time arrow is .

2.3 Typical price change

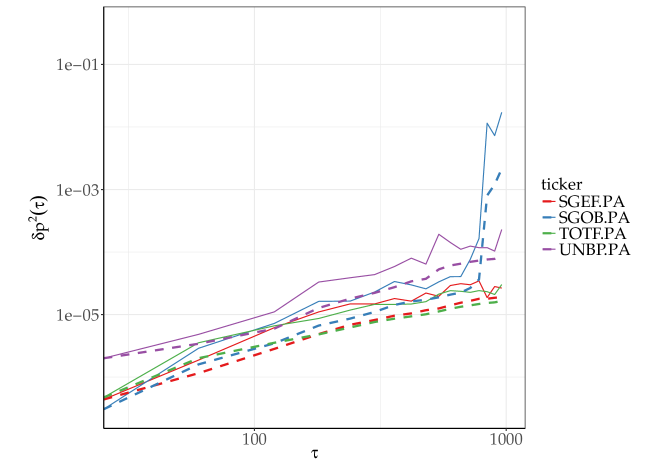

When the indicative price changes, it jumps to the next non-empty tick of the auction order book. Thus, the typical indicative price change reflects the density of the latter, which increases as the auction time nears. As a consequence, the typical price change magnitude is not constant but decreases near the auction end time, or equivalently increases as a function of . Once again, for opening auctions, we find an approximate power-law relationship (see Fig. 4). We apply the same method as for to estimate : we only keep days during which there were at least 50 price changes for a given asset; robust fits of for are carried out. Only fits whose t-statistics associated with are larger than 5 are kept.

2.4 Diffusive properties of indicative prices

It is easy to see why the increase of activity and decrease of the typical magnitude of price changes have antagonistic and purely mechanistic effects on the diffusive properties of the indicative auction price in the simplest case: neglecting the autocorrelations and cross-correlations of both and , Eq. (2) becomes indeed

| (3) | ||||

| (4) |

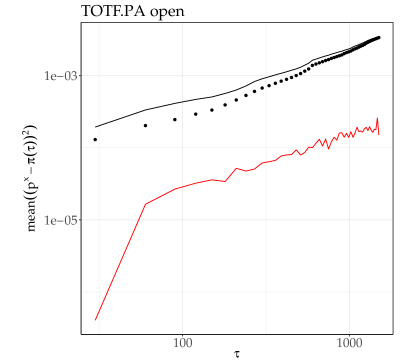

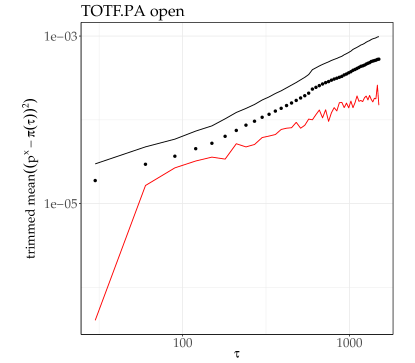

The first approximation assumes that all within a time slice are i.i.d, while the second one assumes no correlation between and . The relative merits of both approximations can be assessed in Fig. 5. The first approximation corresponds to the continuous black line and the second one to the black dots. Both curves are close together; however neglecting the dependence between and underestimates the typical magnitude of . The same figure makes it clear that something is wrong even in the first approximation, as is about 10 times larger than . This discrepancy is mainly due to the bouncing behavior of for large : a large is typically followed by large of opposite sign, which inflates and does not correspond to significant price change as the latter reverts immediately to a value close to that before event . This is why trimmed means, which removes a given fraction of the largest for each time slice and each day, decrease much this discrepancy. The latter is also due in part to a simple strategic behavior: during the auction phase, negative indicative price change triggers the sending of buy orders and vice-versa, causing an intrinsically smaller than expected (see below for a more detailed discussion).

Let us now compare the TTA Hurst exponents of the above quantities, plotted in Fig. 7 for the 6 stocks whose fits of both and are deemed significant. Two features stand out. First, overestimates , even when accounting for the fairly large error bars. This implies that the dynamics caused by the interplay between typical price change shrinking and the acceleration of the activity is more subtle than the simple approximation above. In fact, interestingly, also overestimates the Hurst exponent: this emphasizes the fact that the are not i.i.d.

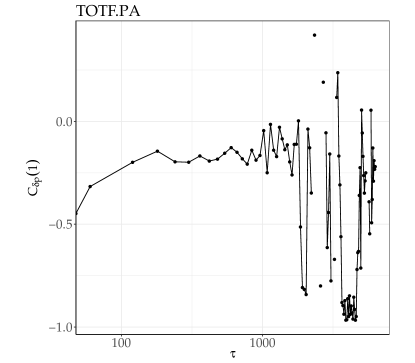

Indeed, in practice, even linear autocorrelation of both and and the cross-correlation between them are not negligible. Let us focus on the autocorrelation of , denoted by . For each time slice , we average over all the days for a given asset. Figure 6 plots this quantity versus for TOTF.PA, the most active asset in our dataset. Generally, ; even more, it becomes more and more negative near the auction time, i.e., for small . Since the price changes become relatively smaller in that limit, this reflects a purposeful bounce of the indicative auction price between two close price ticks; the large negative autocorrelation points to strategic behavior, by which traders try to decrease the immediate impact of their auction orders by submitting their orders after other orders of the opposite sign (hence to hide their actions); in fact, the autocorrelation of the sign of , is even smaller than for small . For large , this auto-correlation also tends to have very small values, which is reinforced by the fact that an outstandingly large is often followed by a similarly large of opposite sign. Thus strategic behavior is more common for small .

When does not depend on , it only modifies the prefactor of in Eq. (3) by a factor of the order , not the Hurst exponent, and thus explains in part the discrepancy between and . The dependence of on modifies the apparent Hurst exponent in a nontrivial way. This is why we measured for , i.e., in a region where is the most constant.

3 Discussion

Indicative auction prices display non-trivial properties due in part to the antagonistic effects of both the acceleration of activity and the reduction of the typical price change magnitude. However, the indicative price is much less over-diffusive than what these two effects alone imply. In other words, the deviation from purely mechanistic effects points to a more subtle dynamics. This makes sense, as the traders have a clear incentive to minimize their easily detectable impact. Their strategic behavior results in often alternatively positive and negative indicative price changes, i.e., in a clearly anti-correlated price changes. Quite tellingly, this negative auto-correlation is more and more pronounced as the auction end nears.

So far, we have used a basic data type, which nevertheless has a rich behavior. More detailed data, such as data from the auction book, will allow us to characterize order strategic placement, the evolution of the average auction book density and the price impact of new orders and order cancellations much before the auction time, in the spirit of the response function of Challet and Gourianov (2018), but accounting for both the volume of new auction orders and their immediate impact on the auction order book.

References

- Alfi et al. [2007] Valentina Alfi, Giorgio Parisi, and Luciano Pietronero. Conference registration: How people react to a deadline. Nature Physics, 3(11):746–746, 2007.

- Alfi et al. [2009] Valentina Alfi, Andrea Gabrielli, and Luciano Pietronero. How people react to a deadline: Time distribution of conference registrations and fee payments. Open Physics, 7(3):483–489, 2009.

- Bellia et al. [2016] Mario Bellia, Loriana Pelizzon, Marti G Subrahmanyam, Jun Uno, and Darya Yuferova. Low-latency trading and price discovery: Evidence from the Tokyo stock exchange in the pre-opening and opening periods. 2016.

- Borle et al. [2006] Sharad Borle, Peter Boatwright, and Joseph B Kadane. The timing of bid placement and extent of multiple bidding: An empirical investigation using eBay online auctions. Statistical Science, pages 194–205, 2006.

- Bouchaud et al. [2009] Jean-Philippe Bouchaud, J. Doyne Farmer, and Fabrizio Lillo. How markets slowly digest changes in supply and demand. In T. Hens and K.R. Schenk-Hoppè, editors, Handbook of Financial Markets: Dynamics and Evolution, pages 57–160. Elsevier, 2009.

- Boussetta et al. [2016] Selma Boussetta, Laurence Lescourret, and Sophie Moinas. The role of pre-opening mechanisms in fragmented markets. 2016.

- Challet and Gourianov [2018] Damien Challet and Nikita Gourianov. Dynamical regularities of US equities opening and closing auctions. submitted to Market Microstructure and Liquidity, arXiv preprint arXiv:1802.01921, 2018.

- Chelley-Steeley [2008] Patricia L Chelley-Steeley. Market quality changes in the London stock market. Journal of Banking & Finance, 32(10):2248–2253, 2008.

- Lehalle and Laruelle [2018] Charles-Albert Lehalle and Sophie Laruelle. Market microstructure in practice. World Scientific, 2nd edition edition, 2018.

- O’Hara [1997] M. O’Hara. Market microstructure theory. Wiley, 1997.

- Pagano and Schwartz [2003] Michael S Pagano and Robert A Schwartz. A closing call’s impact on market quality at Euronext Paris. Journal of Financial Economics, 68(3):439–484, 2003.

- Pagano et al. [2013] Michael S Pagano, Lin Peng, and Robert A Schwartz. A call auction’s impact on price formation and erder routing: Evidence from the NASDAQ stock market. Journal of Financial Markets, 16(2):331–361, 2013.

- Yergeau [2018] Gabriel Yergeau. Machine learning and high-frequency algorithms during batch auctions. 2018.