Stochastic approximations to the Pitman–Yor process

Julyan Arbel, Pierpaolo De Blasi, Igor Prünster

Abstract

In this paper we consider approximations to the popular Pitman–Yor process obtained by truncating the stick-breaking representation. The truncation is determined by a random stopping rule that achieves an almost sure control on the approximation error in total variation distance. We derive the asymptotic distribution of the random truncation point as the approximation error goes to zero in terms of a polynomially tilted positive stable random variable. The practical usefulness and effectiveness of this theoretical result is demonstrated by devising a sampling algorithm to approximate functionals of the -version of the Pitman–Yor process.

Keywords:

stochastic approximation;

asymptotic distribution;

Bayesian Nonparametrics;

Pitman–Yor process;

random functionals;

random probability measure;

stopping rule.

1 Introduction

The Pitman–Yor process defines a rich and flexible class of random probability measures used as prior distribution in Bayesian nonparametric inference. It originates from the work of Perman et al., (1992), further investigated in Pitman, (1995); Pitman and Yor, (1997), and its use in nonparametric inference was initiated by Ishwaran and James, (2001). Thanks to its analytical tractability and flexibility, it has found applications in a variety of inferential problems which include species sampling (Lijoi et al.,, 2007; Favaro et al.,, 2009; Navarrete et al.,, 2008), survival analysis and gene networks (Jara et al.,, 2010; Ni et al.,, 2018), linguistics and image segmentation (Teh,, 2006; Sudderth and Jordan,, 2009), curve estimation (Canale et al.,, 2017) and time-series and econometrics (Caron et al.,, 2017; Bassetti et al.,, 2014). The Pitman–Yor process is a discrete probability measure

| (1) |

where are independent and identically distributed (i.i.d.) random variables with common distribution on a Polish space , and are random frequencies, i.e. and , independent of . The distribution of the frequencies of the Pitman–Yor process is known in the literature as the two-parameter Poisson–Dirichlet distribution. Its distinctive property is that the frequencies in size-biased order, that is the random arrangement in the order of appearance in a simple random sampling without replacement, admit the stick-breaking representation, or residual allocation model,

| (2) |

for and , see Pitman and Yor, (1997). By setting one recovers the Dirichlet process of Ferguson, (1973). Representation (2) turns out very useful in devising finite support approximation to the Pitman–Yor process obtained by truncating the summation in (1). A general method consists in setting the truncation level by replacing with in (1). The key quantity is the truncation error of the infinite summation (1),

| (3) |

since the resulting truncated process, say , will be close to according to for any measurable . It is then important to study the distribution of the truncation error as gets large in order to control the approximation error. Ishwaran and James, (2001) proposes to determine the truncation level based on the moments of . Cf. also Ishwaran and Zarepour, (2002); Gelfand and Kottas, (2002). In this paper we propose and investigate a random truncation by setting such that is smaller than a predetermined value with probability one. Specifically, we define

| (4) |

as the stopping time of the multiplicative process and, following Ghosal and van der Vaart, (2017, Section 4.3.3), we call -Pitman–Yor (-PY) process the Pitman–Yor process truncated at , namely

| (5) |

where has distribution , independent of the sequences and . By construction, is the finite stick-breaking approximation to with the smallest number of support points given a predetermined approximation level. In fact controls the error of approximation according to the total variation bound

| (6) |

almost surely (a.s.). As such, it also guarantees the almost sure convergence of measurable functionals of by the corresponding functionals of as , cf. Ghosal and van der Vaart, (2017, Proposition 4.20). A typical application is in Bayesian nonparametric inference on mixture models where the Pitman–Yor process is used as prior distribution on the mixing measure. The approximation can be applied to the posterior distribution given the latent variables, cf. Section 2.2 for details. In the Dirichlet process case, has been studied by Muliere and Tardella, (1998). In this setting is Poisson distributed with parameter , which makes an exact sampling of the -approximation (5) feasible. This has been implemented in the highly popular R software DPpackage, see (Jara,, 2007; Jara et al.,, 2011), to draw posterior inference on the random effect distribution of linear and generalized linear mixed effect model. Finally, in Al Labadi and Zarepour, (2014) a different type of finite dimensional truncation of the Pitman–Yor process based on decreasing frequencies has been proposed, see Section 5 for a discussion.

The main theoretical contribution of this paper is the derivation of the asymptotic distribution of as for . As (4) suggests, the asymptotic distribution of is related to that of in (3) as . According to Pitman, (2006, Lemma 3.11), the latter involves a polynomially tilted stable random variable , see Section 2 for a formal definition. The main idea is to work with so to deal with sums of the independent random variables . The distribution of can be then studied in terms of the allied renewal counting process , according to the relation . The problem boils down to the derivation of an appropriate a.s. convergence of as , which, in turn, is obtained from the asymptotic distribution of by showing that a.s. as together with a (non standard) application of the law of large numbers for randomly indexed sequences. This strategy proves successful in establishing the almost sure convergence of to as . The form of the asymptotic distribution reveals how large the truncation point is as gets small in terms of the model parameters and . In particular, it highlights the power law behavior of as , namely the growth at the polynomial rate compared to the slower logarithmic rate in the Dirichlet process case. This is further illustrated by a simulation study in which we generate from the asymptotic distribution of by using Zolotarev’s integral representation of the positive stable distribution as in Devroye, (2009). As far as the simulation of the -PY process is concerned, exact sampling is feasible by implementing the stopping rule in (4), that is by simulating the stick breaking frequencies until the error crosses the approximation level . As this can be computationally expensive when is small, as an alternative we propose to use the asymptotic distribution of by simulating the truncation point first, then run the stick breaking procedure up to that point. It results in an approximate sampler of the -PY process that we compare with the exact sampler in a simulation study involving moments and mean functionals.

The rest of the paper is organized as follows. In Section 2, we derive the asymptotic distribution of and explain how to use it to simulate from the -PY process. Section 3 reports a simulation study on the distribution of and on functionals of the -PY process. In Section 4, to help the understanding and gain additional insight on the asymptotic distribution, we highlight the connections of with Pitman’s theory on random partition structures. We conclude with a discussion of open problems in Section 5. The details of Devroye’s algorithm for generating from a polynomially tilted positive stable random variable are given in Appendix A.

2 Theory and algorithms

2.1 Asymptotic distribution of

In this section we derive the asymptotic distribution of the stopping time and show how to simulate from it. We start by introducing the renewal process interpretation which is crucial for the asymptotic results. As explained in the previous section, in order to study the distribution of it is convenient to work with the log transformation of the truncation error in (3), that is

| (7) |

with as in (2). Being a sum of independent and nonnegative random variables, takes the interpretation of a (generalized) renewal process with independent waiting times . For define

| (8) |

to be the renewal counting process associated to , which is related to via . Classical renewal theory pertains to iid waiting times while here there is no identity in distribution unless , i.e. the Dirichlet process case. In the latter setting, one gets so that has gamma distribution with scale parameter . We immediately get from the relation that and, in turn, that has distribution. As far as asymptotics is concerned, satisfies the central limit theorem (CLT) with where . The asymptotic distribution of can be obtained via Ascombe theorem, cf. Gut, (2013, Theorem 7.4.1), to get , as , in accordance with the standard normal approximation of the Poisson distribution with large rate parameter.

In the general Pitman–Yor case , the waiting times are no more identically distributed. More importantly, generalizations of the CLT such as the Lindeberg–Feller theorem do not apply for , hence we cannot resort to Anscombe’s theorem to derive the asymptotic distribution of and, in turn, of . Nevertheless, the limit exists but is not normal as stated in Theorem 1 below. To this aim, let be a positive stable random variable with exponent , that is , and denote its density by . A polynomially tilted version of is defined as the random variable with density proportional to , that is

| (9) |

The random variable is of paramount importance in the theory of random partition structures associated to the frequency distribution of the Pitman–Yor process, see Section 4 for details. In particular, the convergence of can be expressed in terms of . In Theorem 1 the a.s. limit of as is obtained from that of as by showing that a.s. as and by an application of the law of large numbers for randomly indexed sequences.

Proof.

By definition (8), the renewal process is related to the sequence of renewal epochs through

| (10) |

Since , we have when , thus for . Moreover, since is increasing, when , , hence , i.e. . Together the two relations above yield

| (11) |

From Lemma 3.11 of Pitman, (2006) and an application of the continuous mapping theorem (see Theorem 10.1 in Gut,, 2013) the asymptotic distribution of is obtained as

Now we would like to take the limit with respect to as , that is apply the law of large numbers for randomly indexed sequence (see Theorem 6.8.1 in Gut,, 2013). To this aim, we first need to prove that as . Since is non decreasing, by an application of Theorem 5.3.5 in Gut, (2013), it is sufficient to prove that in probability as , that is as for any . But this is an immediate consequence of the inversion formula (10). We have then established that

To conclude the proof, we need to replace with in the limit above. Note that, from (11), so it is sufficient to show that the upper bound goes to zero a.s.. Actually, by a second application of Theorem 6.8.1 in Gut, (2013) it is sufficient to show that as . This last result is established as follows. Recall that for . For ,

| (12) |

where in equality (12) we have used Euler’s formula

for , see Tricomi and Erdélyi, (1951). Since , (12) implies that is exponentially decreasing in and, in turn, that . An application of Borel–Cantelli Lemma yields and the proof is complete. ∎

The asymptotic distribution of is readily derived from Theorem 1 via the formula and an application of the continuous mapping theorem. The proof is omitted.

In order to sample from the asymptotic distribution of , the key ingredient is random generation from the polynomially tilted stable random variable . Following Devroye, (2009), we resort to Zolotarev’s integral representation, so let be the Zolotarev function

and , and be a Zolotarev random variable with density given by

According to Theorem 1 of Devroye, (2009), for a gamma distributed random variable with shape and unit rate,

so that random variate generation simply requires one gamma random variable and one Zolotarev random variable. For the latter, rejection sampler can be used as detailed in Devroye, (2009). See Algorithm 3 in Appendix A.

2.2 Simulation of the -PY process

Given and a probability measure on , an -PY process can be generated by implementing the stopping rule in the definition of , cf. (4). The algorithm consists in a while loop as follows:

Algorithm 1 (Exact sampler of -PY)

1. set ,

2. while : generate from .

set , ,3. set ,

4. generate random variates from

5. set

When is small, the while loop happens to be computationally expensive since conditional evaluations at each iteration slow down computation, and memory allocation for the frequency and location vectors cannot be decided beforehand. In order to avoid these pitfalls and make the algorithm faster, one should generate the stopping time first, and the frequencies up to that point later. We propose to exploit the asymptotic distribution of in Theorem 2 as follows:

Algorithm 2 (Approximate sampler of -PY)

1: generate

2: set

3. for : generate from .

set4. set

5: generate random variates from

6: set

Algorithm 2 is an approximate sampler of the -PY process (while Algorithm 1 is an exact one) since it introduces two sources of approximations. First, through the use of the asymptotic distribution of . Second, through Step 3 since the ’s are not generated according to the conditional distribution given , rather unconditionally. Finding the conditional distribution of , or an asymptotic approximation thereof, is not an easy task and is object of current research. In terms of the renewal process interpretation in (7)–(8), the problem is to generate the waiting times , , from the conditional distribution of the renewal epochs given for .

A typical use of samples from the Pitman–Yor process we have in mind is in infinite mixture models. In fact, the discrete nature of the Pitman–Yor process makes it a suitable prior on the mixing distribution. Algorithm 1 or Algorithm 2 can be then applied to approximate a functional of the posterior distribution of the mixing distribution. In such models, the process components can be seen as latent features exhibited by the data. Let denote such a process, denote the sample size and be an exchangeable sequence from , that is . Variables are latent variables in a model conditionally on which observed data come from: where denotes a kernel density. Actually, independence is not necessary here and applications also encompass dependent models such as Markov chain transition density estimation. In order to deal with the infinite dimensionality of the process, a strategy is to marginalize it and to draw posterior inference with a marginal sampler. Since draws from a marginal sampler allows to make inference only on posterior expectations of the process, for more general functionals of , in the form of , one typically needs to resort to an additional sampling step. Exploiting the composition rule this additional step boils down to sampling conditional on latent variables . At this stage, recalling the conditional conjugacy of the Pitman–Yor process is useful. Among , there are a number of unique values that we denote by . Let denote their frequencies. Then the following identity in distribution holds

where, independently, and is a Pitman–Yor process of parameter , see Corollary 20 of Pitman, (1996). Thus sampling from , hence from , requires sampling the infinite dimensional . Cf. Ishwaran and James, (2001, Section 4.4). For the sake of comparison, the conjugacy of the Dirichlet process similarly leads to the need of sampling an infinite dimensional process, where takes the form of a Dirichlet process. As already noticed, the truncation of the Dirichlet process is very well understood, both theoretically and practically. The popular R package DPpackage (Jara,, 2007; Jara et al.,, 2011) makes use of the posterior truncation point , as defined in (5), but here with respect to the posterior distribution of the process. Thus, it satisfies where is the precision of the posterior Dirichlet process. Adopting here similar lines for the Pitman–Yor process, we replace by the truncated process

cf. equation (5). Here are defined according to (2) with in place of , i.e. . Hence, according to Theorem 2 we have

hence Algorithm 2 can be applied here.

3 Simulation study

3.1 Stopping time

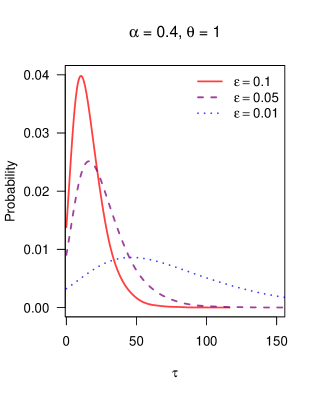

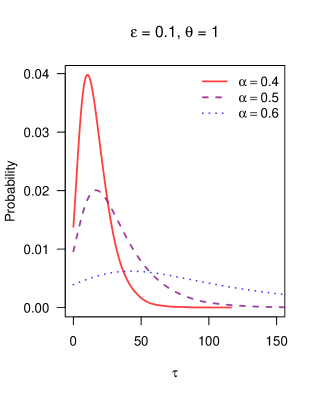

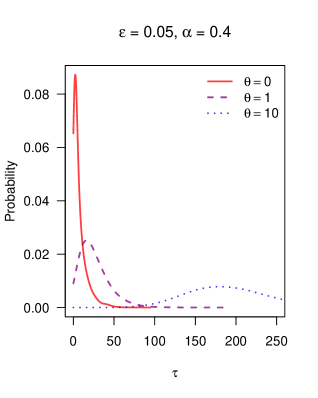

According to Theorem 2, the asymptotic distribution of changes with , and . For illustration, we simulate from Steps 1.-2. in Algorithm 2 using Devroye’s sampler, cf. Algorithm 3 in Appendix A. In Figure 1 we compare density plots obtained with iterations with respect to different combinations of , and . The plot in the left panel shows how smaller values of result in larger values of . In fact, as , increases proportional to . Note also that is nonnegative for , which happens with high probability when is small. As for , the plot in the central panel shows how increases as gets large. In fact, it is easy to see that is increasing in when , which also happens with high probability when is small, so the larger , the more stick-breaking frequencies are needed in order to account for a prescribed approximation error . Finally, the plot in the right panel shows that the larger , the larger . In fact, by definition, the polynomial tilting makes stochastically decreasing in .

|

|

In order to illustrate the rate of convergence in Theorem 2, we compare next the exact distribution of with the asymptotic one. To do so, we repeat the following experiment several times: we simulate from Steps 1.-3. in Algorithm 1, then we compare the empirical distribution of with , the latter corresponding to the -diversity of the PY process, see Section 4 for a formal definition. In Table 1 we report the Kolmogorov distance together with expected value, median, first and third quartiles for both the exact and the asymptotic distribution obtained with iterations. This is repeated for , and . As expected, as we decrease , the Kolmogorov distance gets smaller to somehow different rates according to the parameter choice. The derivation of convergence rates is left for future research.

| Mean | Median | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| As | Ex | As | Ex | As | Ex | As | Ex | |||

| 0 | 0.10 | 3.42 | 1.06 | 1.05 | 0.45 | 0.45 | 0.89 | 0.89 | 1.61 | 1.55 |

| 0 | 0.05 | 2.17 | 1.10 | 1.08 | 0.45 | 0.45 | 0.95 | 0.95 | 1.64 | 1.58 |

| 0 | 0.01 | 1.73 | 1.14 | 1.11 | 0.45 | 0.45 | 0.97 | 0.95 | 1.64 | 1.60 |

| 1 | 0.10 | 4.79 | 2.24 | 2.14 | 1.55 | 1.48 | 2.14 | 2.10 | 2.86 | 2.76 |

| 1 | 0.05 | 2.38 | 2.25 | 2.20 | 1.55 | 1.52 | 2.17 | 2.14 | 2.86 | 2.79 |

| 1 | 0.01 | 1.40 | 2.26 | 2.25 | 1.57 | 1.54 | 2.19 | 2.19 | 2.87 | 2.85 |

| 10 | 0.10 | 11.93 | 6.39 | 6.07 | 5.69 | 5.40 | 6.34 | 6.06 | 7.04 | 6.72 |

| 10 | 0.05 | 6.12 | 6.39 | 6.24 | 5.70 | 5.56 | 6.34 | 6.22 | 7.05 | 6.88 |

| 10 | 0.01 | 1.93 | 6.40 | 6.37 | 5.71 | 5.70 | 6.34 | 6.34 | 7.05 | 7.00 |

3.2 Functionals of the -PY process

In the case that is defined on , the total variation bound (6) implies that almost surely for any , where and are the cumulative distribution functions of and . Also, measurable functionals such as the mean can be approximated in distribution by the corresponding functionals . For illustration, we set and the uniform distribution on . For given and , we then compare the distribution under with that under the -PY process for , and . As for the distribution of the finite dimensional distributions and under the full process , we set so to exploit results in James et al., (2010). According to their Proposition 4.7, the finite dimensional distributions of when are given by

for any partition of with and . Direct calculation shows that has beta distribution with parameters while has density

As for the mean functional , the distribution under the full process is approximated by simulations by setting a deterministic truncation point sufficiently large. As for the distribution under , we use both Algorithm 1 and Algorithm 2.

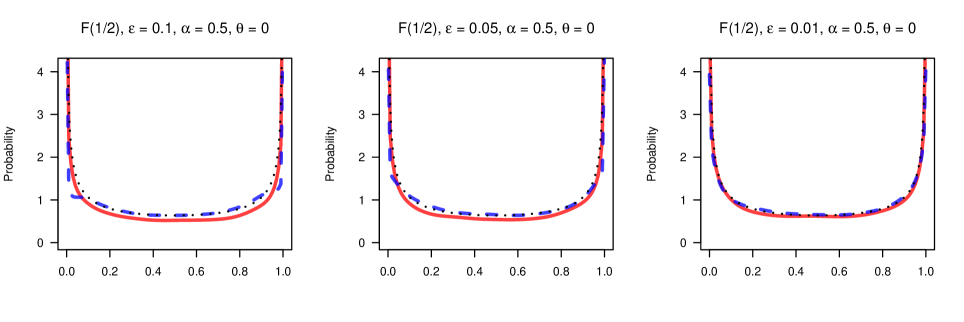

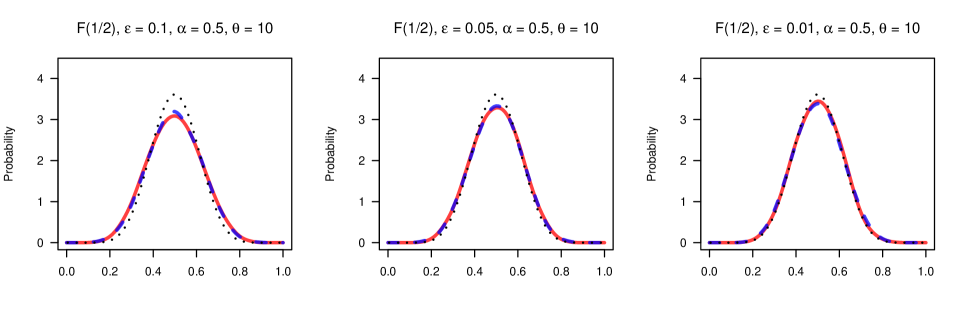

In Figure 2 we compare the density plots of for and under with the beta density under so to illustrate that the two distributions get close as gets small.

|

|

As for and , in Tables 3 and 3 we report the Kolmogorov distance between and for the two sampling algorithms, together with expected value, median, first and third quartiles. For each case and each parameter configuration, we have sampled trajectories from the -PY process and trajectories from the Pitman–Yor process in the case of . As expected, the Kolmogorov distances are generally larger, still close, when using Algorithm 2 versus Algorithm 1 due to the approximate nature of the former.

| Mean | Median | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Al1 | Al2 | Al1 | Al2 | PY | Al1 | Al2 | PY | Al1 | Al2 | PY | Al1 | Al2 | PY | ||

| 0 | 0.10 | 16.29 | 16.48 | 0.33 | 0.33 | 0.33 | 0.04 | 0.01 | 0.04 | 0.20 | 0.16 | 0.20 | 0.60 | 0.64 | 0.59 |

| 0 | 0.05 | 11.53 | 12.52 | 0.33 | 0.33 | 0.33 | 0.05 | 0.01 | 0.04 | 0.20 | 0.17 | 0.20 | 0.58 | 0.63 | 0.59 |

| 0 | 0.01 | 5.49 | 5.60 | 0.34 | 0.33 | 0.33 | 0.04 | 0.03 | 0.04 | 0.21 | 0.19 | 0.20 | 0.59 | 0.61 | 0.59 |

| 1 | 0.10 | 3.08 | 5.65 | 0.33 | 0.33 | 0.33 | 0.14 | 0.12 | 0.14 | 0.29 | 0.28 | 0.28 | 0.49 | 0.50 | 0.49 |

| 1 | 0.05 | 1.34 | 3.11 | 0.33 | 0.33 | 0.33 | 0.14 | 0.13 | 0.14 | 0.28 | 0.28 | 0.28 | 0.48 | 0.50 | 0.49 |

| 1 | 0.01 | 0.56 | 0.89 | 0.33 | 0.34 | 0.33 | 0.14 | 0.14 | 0.14 | 0.28 | 0.29 | 0.28 | 0.49 | 0.49 | 0.49 |

| 10 | 0.10 | 3.10 | 3.81 | 0.33 | 0.33 | 0.33 | 0.25 | 0.25 | 0.26 | 0.32 | 0.32 | 0.32 | 0.40 | 0.41 | 0.40 |

| 10 | 0.05 | 1.41 | 1.38 | 0.33 | 0.33 | 0.33 | 0.26 | 0.26 | 0.26 | 0.32 | 0.32 | 0.32 | 0.40 | 0.40 | 0.40 |

| 10 | 0.01 | 0.75 | 0.65 | 0.33 | 0.33 | 0.33 | 0.26 | 0.26 | 0.26 | 0.33 | 0.32 | 0.32 | 0.40 | 0.40 | 0.40 |

| Mean | Median | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Al1 | Al2 | Al1 | Al2 | PY | Al1 | Al2 | PY | Al1 | Al2 | PY | Al1 | Al2 | PY | ||

| 0 | 0.10 | 1.60 | 3.57 | 0.50 | 0.50 | 0.50 | 0.36 | 0.34 | 0.36 | 0.50 | 0.50 | 0.50 | 0.64 | 0.67 | 0.65 |

| 0 | 0.05 | 0.94 | 2.72 | 0.50 | 0.50 | 0.50 | 0.35 | 0.34 | 0.36 | 0.50 | 0.50 | 0.50 | 0.64 | 0.66 | 0.65 |

| 0 | 0.01 | 1.18 | 2.10 | 0.50 | 0.50 | 0.50 | 0.36 | 0.35 | 0.36 | 0.50 | 0.50 | 0.50 | 0.64 | 0.65 | 0.65 |

| 1 | 0.10 | 1.61 | 3.18 | 0.50 | 0.50 | 0.50 | 0.40 | 0.39 | 0.40 | 0.50 | 0.50 | 0.50 | 0.60 | 0.61 | 0.60 |

| 1 | 0.05 | 1.28 | 2.32 | 0.50 | 0.50 | 0.50 | 0.40 | 0.40 | 0.40 | 0.50 | 0.50 | 0.50 | 0.59 | 0.60 | 0.60 |

| 1 | 0.01 | 1.12 | 0.57 | 0.50 | 0.50 | 0.50 | 0.40 | 0.41 | 0.40 | 0.50 | 0.50 | 0.50 | 0.60 | 0.60 | 0.60 |

| 10 | 0.10 | 2.81 | 4.18 | 0.50 | 0.50 | 0.50 | 0.45 | 0.46 | 0.46 | 0.50 | 0.50 | 0.50 | 0.55 | 0.55 | 0.54 |

| 10 | 0.05 | 1.78 | 1.28 | 0.50 | 0.50 | 0.50 | 0.46 | 0.46 | 0.46 | 0.50 | 0.50 | 0.50 | 0.54 | 0.54 | 0.54 |

| 10 | 0.01 | 2.01 | 1.09 | 0.50 | 0.50 | 0.50 | 0.46 | 0.46 | 0.46 | 0.50 | 0.50 | 0.50 | 0.54 | 0.54 | 0.54 |

3.3 Computation time

In this section, we provide a concrete justification of the computational advantage of using Algorithm 2 versus Algorithm 1. We simulate -PY iterations by using Algorithm 1 and Algorithm 2 for different combinations of the and parameters and of the error threshold. In Table 5 (resp. Table 5), we report the average computing time111The experiments were conducted on an Intel Core i5 processor (3.1 GHz) computer. per iteration (resp. per support point) for Algorithm 1 and Algorithm 2. By iteration, we mean a full realization of the -PY process including frequencies and locations, while by support point, we mean that we divide the total time by the number of support points . In order to account for the computational task required per iteration, the expected stopping time is also reported. Both tables illustrate that our proposed approach is faster than Algorithm 1 when the -PY is composed of about 20 support points or more. The more support points, the faster Algorithm 2 is compared to Algorithm 1. This disadvantage of the former for small numbers of support points comes from the fixed cost of initially generating a random variable with the same distribution as . Conversely, as the number of support points increases, this fixed cost is largely counterbalanced by the fast vector-sampling of a prescribed size, which is in contrast with Algorithm 1 while loop whose cost increases with the number of support points. This can be seen in Table 5 where the actual sampling time per support point is essentially increasing for Algorithm 1 and decreasing for Algorithm 2. With the parameter configurations tested, Algorithm 2 can be up to 90 times faster Algorithm 1 for , and .

| Al1 | Al2 | Al1 | Al2 | Al1 | Al2 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.10 | 0.01 | 0.20 | 5 | 0.02 | 0.04 | 11 | 0.11 | 0.05 | 38 |

| 0 | 0.05 | 0.01 | 0.04 | 8 | 0.04 | 0.04 | 21 | 0.20 | 0.06 | 105 |

| 0 | 0.01 | 0.04 | 0.04 | 20 | 0.36 | 0.05 | 101 | 15.10 | 0.26 | 1163 |

| 1 | 0.10 | 0.03 | 0.19 | 17 | 0.07 | 0.05 | 31 | 0.23 | 0.07 | 92 |

| 1 | 0.05 | 0.06 | 0.06 | 26 | 0.13 | 0.06 | 61 | 0.80 | 0.12 | 258 |

| 1 | 0.01 | 0.18 | 0.09 | 73 | 0.80 | 0.12 | 301 | 27.75 | 0.57 | 2877 |

| 10 | 0.10 | 0.22 | 0.15 | 121 | 0.61 | 0.10 | 211 | 2.11 | 0.18 | 567 |

| 10 | 0.05 | 0.45 | 0.10 | 191 | 1.52 | 0.15 | 421 | 9.22 | 0.37 | 1603 |

| 10 | 0.01 | 1.93 | 0.20 | 558 | 13.24 | 0.48 | 2101 | 760.68 | 4.01 | 17911 |

| Al1 | Al2 | Al1 | Al2 | Al1 | Al2 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.10 | 1.92 | 38.46 | 5 | 1.82 | 3.64 | 11 | 2.91 | 1.32 | 38 |

| 0 | 0.05 | 1.30 | 5.22 | 8 | 1.90 | 1.90 | 21 | 1.91 | 0.57 | 105 |

| 0 | 0.01 | 1.95 | 1.95 | 20 | 3.56 | 0.50 | 101 | 12.98 | 0.22 | 1163 |

| 1 | 0.10 | 1.81 | 11.45 | 17 | 2.26 | 1.61 | 31 | 2.50 | 0.76 | 92 |

| 1 | 0.05 | 2.33 | 2.33 | 26 | 2.13 | 0.98 | 61 | 3.10 | 0.46 | 258 |

| 1 | 0.01 | 2.45 | 1.23 | 73 | 2.66 | 0.40 | 301 | 9.65 | 0.20 | 2877 |

| 10 | 0.10 | 1.82 | 1.24 | 121 | 2.89 | 0.47 | 211 | 3.72 | 0.32 | 567 |

| 10 | 0.05 | 2.35 | 0.52 | 191 | 3.61 | 0.36 | 421 | 5.75 | 0.23 | 1603 |

| 10 | 0.01 | 3.46 | 0.36 | 558 | 6.30 | 0.23 | 2101 | 42.47 | 0.22 | 17911 |

4 Connections with random partition structures

4.1 -diversity and asymptotic distribution of

The random variable in Theorem 1 plays a key role in the Pitman–Yor process, in particular for its link with the -diversity of the process. The -diversity is defined as the almost sure limit of where denotes the (random) number of unique values in the first terms of an exchangeable sequence from in (1). According to Theorem 3.8 in Pitman, (2006), , in particular, for , has a Mittag-Leffler distribution with -th moment , . According to Pitman, (2006, Lemma 3.11, eqn (3.36)), the asymptotic distribution of the truncation error can be derived from that of to get as . The proof relies on Kingman’s representation of random partitions (Kingman,, 1978) together with techniques set forth by Gnedin et al., (2007). In the proof of Theorem 1 the asymptotic distribution of is a direct consequence of the above by an application of the continuous mapping theorem.

When it is possible to give an interpretation of the asymptotic distribution of in terms of the jumps of a stable subordinator. In this case the weights of can be represented as the renormalized jumps of a stable subordinator, with denoting the total mass. Denote the (unormalized) jumps as in decreasing order and as when in size-biased order,

By the asymptotic distribution of , as . That is, once properly scaled, the small jumps of the stable subordinator (in size-biased random order), interpreted as the “ dust ”, converge to the “ proportion ” . This is reminiscent to the number of singletons which is asymptotically a proportion of the number of groups in a sample of size , see Lemma 3.11, eqn (3.39), of Pitman, (2006).

4.2 Regenerative random compositions and Anscombe’s theorem

We review next the connections of the counting renewal process defined in (7)–(8) and the theory of regenerative random compositions. The reader is referred to the survey of Gnedin, (2010) for a review. Recall that, when (Dirichlet process case), in the stick-breaking representation (2), and in turns and . By direct calculus, so that has distribution. More generally, the stick-breaking frequencies correspond to the gaps in identified by the multiplicative regenerative set consisting of the random partial sums . The complement open set can be represented as a disjoint union of countably many open intervals or gaps, , . A random composition of the integer into an ordered sequence of positive integers with can be generated as follows: independently of , sample from the uniform distribution on and group them in clusters by the rule: belong to the same cluster if they hit the same interval. The random composition of corresponds then to the record of positive counts in the left-to-right order of the intervals. The composition structure is called regenerative since for all , conditionally given the first part of is , if the part is deleted then the remaining composition of is distributed like . The regenerative set corresponds to the closed range of the multiplicative subordinator , where is the compound Poisson process with Lévy intensity . Since the range of is a homogeneous Poisson point process on with rate , is an inhomogeneous Poisson point process on with Lévy intensity so that, for ,

as expected. Suppose now that are independent copies of some random variable on , not necessarily distributed. The corresponding random composition structure has been studied in Gnedin, (2004); Gnedin et al., (2009) as the outcome of a Bernoulli sieve procedure. We recall here the relevant asymptotic analysis. Let and , equal respectively to and in the DP case, respectively. If those moments are finite, by the CLT,

where , and, by means of Anscobe’s Theorem, one obtains that

It turns out that the normal limit of corresponds to the normal limit of ,

provided that . To see why, consider iid random variables with values in such that . Hence . We then have that . Define . For denoting the order statistics corresponding to the uniform variates , we have upon transformation , where is the maximum of an iid sample of size from the standard exponential distribution. Since we have . Gnedin et al., (2009) proves the equivalence

where is a random variable with a proper and non degenerate distribution with , and . A key fact exploited in the proof is that, from extreme-value theory, has an asymptotic distribution of Gumbel type. That can be replaced by in the equivalence relation above follows from the fact that , the number of integers not appearing in the sample , is bounded in probability when , see Proposition 5.1 in Gnedin et al., (2009).

Back to the Pitman–Yor process case, by Theorem 1 we have while . So we see that and do not have the same asymptotic behavior as in the case. By using the fact that

and the fact that, conditional on , belongs to the domain of attraction of Fréchet distribution, Pitman and Yakubovich, (2017, Theorem 6.1) establishes that

so we see that and do not have the same asymptotic behavior as in the case, although they share the same growth rate . Finally, the non correspondence of the asymptotic distribution of and suggests that the behavior of is radically different with respect to the case.

5 Discussion

In this paper we have studied stochastic approximations of the Pitman–Yor process consisting in the truncation of the sequence of stick-breaking frequencies at a random stopping time that controls the accuracy of the approximation in the total variation distance by . We name this finite dimensional approximation the -Pitman–Yor process. We have derived the asymptotic distribution of as goes to zero and we have advanced its use to devise a sampling scheme that generates the stopping time first, and then the frequencies up to that point. The simulations in Section 3 show that the proposed sampler proves computationally very efficient in the moderate to large stopping time regime (for approximately ). The asymptotic distribution illustrates how large the stopping time is as the approximation error gets small in terms of the prior parameters and . In particular, it shows that the distribution of in the Dirichlet process case is not recovered in the limit in Theorem 2. In fact, in the Dirichlet process case grows at a logarithmic rate in while in Pitman–Yor case it grows at the polynomial rate and the first regime is not recovered by letting approach in the second regime. We have also drawn important connections with the theory of random partition structures developed by Jim Pitman and coauthors which highlight the relationship of the the stopping time with the number of unique values in a sample of size from the Pitman–Yor process.

We have left as open problem for future research the study of the conditional distribution of the stick-breaking frequencies given the stopping time. In the Dirichlet process case one can exploit the renewal process interpretation to generate exactly from this conditional distribution. In fact, when , the sequence corresponds to the jump times of a Poisson process and the conditional distribution of the jumps given the number of jumps at time can be described in terms of the ordered statistics of i.i.d. uniform random variates on . The case does not seem to be easily tractable, as it would be if the counting process associated to were a mixed sample process or, equivalently, a Cox process, cf. Grandell, (1997, Section 6.3).

It would be also interesting to compare the accuracy of our finite dimensional approximation of the Pitman–Yor process to the one proposed in Al Labadi and Zarepour, (2014). The latter is based on a representation of the frequencies in decreasing order, cf. Pitman and Yor, (1997, Proposition 22). Al Labadi and Zarepour, (2014) compare the accuracy of their approximation scheme to a stick-breaking truncation at a number of stick-breaking frequencies that matches the number of frequencies used in their scheme. Not surprisingly, their approximation is superior since it generates weights in decreasing order, specially when is large. In contrast, Theorem 2 describes precisely how large the truncation threshold should be as gets large for a given approximation level , cf. the center panel of Figure 1. It also underlines that the approximation deteriorates for fixed and increasing , which is coherent with the findings in Al Labadi and Zarepour, (2014). A fair comparison with their approach can only be done for a given nominal approximation error, but unfortunately the authors did not provide a precise assessment of it. The number of stick-breaking frequencies needed to match the approximation accuracy of Al Labadi and Zarepour, (2014) would be de facto larger due to the non monotonicity. However, since the stopping rule (4) adapts to the size of , we do not expect the accuracy of our approximation scheme to deteriorate for large. As for computation time, the techniques used by Al Labadi and Zarepour, (2014) in order to obtain decreasing frequencies are computational heavy. Their average computing time for is about seconds/iteration with locations. This amounts to milliseconds/support point, which is times slower than the computing time for our Algorithm 2 in the parameter configuration , and , equal to microsecond/support point. It would be interesting to investigate what are the consequences in terms of computation time per iteration for a given approximation error.

Appendix A Random generation of

Let be a standard random variable. Note that

so we have . For , , so we find that and

| (13) |

The normalizing constant in is , so set and note that . Let be a gamma random variable with shape and unit rate. Simple moment comparisons using (13) yield the distributional equality , which, however, does not provide a way to generate from . For this we resort to Devroye, (2009). First we recall how to generate a Zolotarev random variable for and . Let

and

A simple asymptotic argument yields the value . Then . The following bound holds

This Gaussian upper bound suggests a simple rejection sampler for sampling Zolotarev random variates. Following Devroye, (2009), it is most efficient to adapt the sampler to the value of . If , rejection from a uniform random variate is best. Otherwise, use a normal dominating curve as suggested in the bound above. The details are given below.

Algorithm 3 (Sampler of )

1. set and

2. if :

then repeat: generate and .

set , .

until

else repeat: generate and .

set , .

until and3. generate

4. set

5. return

References

- Al Labadi and Zarepour, (2014) Al Labadi, L. and Zarepour, M. (2014). On simulations from the two-parameter poisson-dirichlet process and the normalized inverse-gaussian process. Sankhya, 76-A:158–176.

- Bassetti et al., (2014) Bassetti, F., Casarin, R., and Leisen, F. (2014). Beta-product dependent pitman–yor processes for bayesian inference. Journal of Econometrics, 180(1):49 – 72.

- Canale et al., (2017) Canale, A., Lijoi, A., Nipoti, B., and Prünster, I. (2017). On the Pitman-Yor process with spike and slab base measure. Biometrika, 104:681–697.

- Caron et al., (2017) Caron, F., Neiswanger, W., Wood, F., Doucet, A., and Davy, M. (2017). Generalized pólya urn for time-varying pitman-yor processes. Journal of Machine Learning Research, 18(27):1–32.

- Devroye, (2009) Devroye, L. (2009). Random variate generation for exponentially and polynomially tilted stable distributions. ACM Transactions on Modeling and Computer Simulation (TOMACS), 19(4): Article No. 18.

- Favaro et al., (2009) Favaro, S., Lijoi, A., Mena, R., and Prünster, I. (2009). Bayesian non-parametric inference for species variety with a two-parameter Poisson–Dirichlet process prior. J. R. Stat. Soc. Ser. B, 71:993–1008.

- Ferguson, (1973) Ferguson, T. S. (1973). A Bayesian analysis of some nonparametric problems. Ann. Statist., 1:209–230.

- Gelfand and Kottas, (2002) Gelfand, A. and Kottas, A. (2002). A computational approach for full nonparametric Bayesian inference under Dirichlet process mixture models. J. Comput. Graph. Statist., 11:289–305.

- Ghosal and van der Vaart, (2017) Ghosal, S. and van der Vaart, A. W. (2017). Foundamentals of Nonparametric Bayesian Inference. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- Gnedin, (2004) Gnedin, A. (2004). The Bernoulli sieve. Bernoulli, 10:79–96.

- Gnedin, (2010) Gnedin, A. (2010). Regeneration in random combinatorial structures. Probability Surveys, 7:105–156.

- Gnedin et al., (2007) Gnedin, A., Hansen, B., and Pitman, J. (2007). Notes on the occupancy problem with infinitely many boxes: general asymptotics and power laws. Probability Surveys, 4:146–171.

- Gnedin et al., (2009) Gnedin, A., Iksanov, A. M., Pavlo, N., and Uwe, R. (2009). The Bernoulli sieve revisited. The Annals of Applied Probability, 19:1634–1655.

- Grandell, (1997) Grandell, J. (1997). Mixed Poisson Processes. Monographs on Statistics and Applied Probability. Springer US.

- Gut, (2013) Gut, A. (2013). Probability : a graduate course. Springer texts in statistics. Springer, 2nd ed edition.

- Ishwaran and James, (2001) Ishwaran, H. and James, L. F. (2001). Gibbs sampling methods for stick-breaking priors. J. Amer. Statist. Assoc., 96:161–173.

- Ishwaran and Zarepour, (2002) Ishwaran, H. and Zarepour, M. (2002). Exact and approximate sum representations for the Dirichlet process. Canad. J. Statist., 30:269–283.

- James et al., (2010) James, L. F., Lijoi, A., and Prünster, I. (2010). On the posterior distribution of classes of random means. Bernoulli, 16(1):155–180.

- Jara, (2007) Jara, A. (2007). Applied Bayesian non- and semi-parametric inference using DPpackage. Rnews, 7:17–26.

- Jara et al., (2011) Jara, A., Hanson, T. E., Quintana, F. A., Müller, P., and Rosner, G. L. (2011). DPpackage: Bayesian semi- and nonparametric modeling in R. Journal of Statistical Software, 40(5):1–30.

- Jara et al., (2010) Jara, A., Lesaffre, E., De Iorio, M., and Quintana, F. (2010). Bayesian semiparametric inference for multivariate doubly-interval-censored data. Ann. Appl. Stat., 4(4):2126–2149.

- Kingman, (1978) Kingman, J. F. C. (1978). The representation of partition structures. J. London Math. Soc., 18:374–380.

- Lijoi et al., (2007) Lijoi, A., Mena, R., and Prünster, I. (2007). Bayesian nonparametric estimation of the probability of discovering a new species. Biometrika, 94:769–786.

- Muliere and Tardella, (1998) Muliere, P. and Tardella, L. (1998). Approximating distributions of random functionals of Ferguson-Dirichlet priors. The Canadian Journal of Statistics, 26(2):283–297.

- Navarrete et al., (2008) Navarrete, C., Quintana, F. A., and Mueller, P. (2008). Some issues in nonparametric Bayesian modeling using species sampling models. Statistical Modelling, 8(1):3–21.

- Ni et al., (2018) Ni, Y., Müller, P., Zhu, Y., and Ji, Y. (2018). Heterogeneous reciprocal graphical models. Biometrics, 74(2):606–615.

- Perman et al., (1992) Perman, M., Pitman, J., and Yor, M. (1992). Size-biased sampling of Poisson point processes and excursions. Prob. Theory Relat. Fields, 92(1):21–39.

- Pitman, (1995) Pitman, J. (1995). Exchangeable and partially exchangeable random partitions. Prob. Theory Relat. Fields, 102(2):145–158.

- Pitman, (1996) Pitman, J. (1996). Some developments of the Blackwell-MacQueen urn scheme. In Statistics, probability and game theory, volume 30 of IMS Lecture Notes Monogr. Ser., pages 245–267. Inst. Math. Statist., Hayward, CA.

- Pitman, (2006) Pitman, J. (2006). Combinatorial stochastic processes. Ecole d’Eté de Probabilités de Saint-Flour XXXII. Lecture Notes in Mathematics N. 1875. Springer, New York.

- Pitman and Yakubovich, (2017) Pitman, J. and Yakubovich, Y. (2017). Extremes and gaps in sampling from a GEM random discrete distribution. Electronic Journal of Probability, 22.

- Pitman and Yor, (1997) Pitman, J. and Yor, M. (1997). The two-parameter Poisson-Dirichlet distribution derived from a stable subordinator. The Annals of Probability, 25(2):855–900.

- Sudderth and Jordan, (2009) Sudderth, E. B. and Jordan, M. I. (2009). Shared segmentation of natural scenes using dependent Pitman-Yor processes. In Advances in Neural Information Processing Systems 21, pages 1585–1592. Curran Associates, Inc.

- Teh, (2006) Teh, Y. W. (2006). A hierarchical Bayesian language model based on Pitman-Yor processes. In Proc. Coling/ACL, pages 985–992, Stroudsburg, PA, USA.

- Tricomi and Erdélyi, (1951) Tricomi, F. G. and Erdélyi, A. (1951). The asymptotic expansion of a ratio of gamma functions. Pacific Journal of Mathematics, 1(1):133–142.