Game-theoretic derivation of upper hedging prices of multivariate contingent claims and submodularity

Abstract

We investigate upper and lower hedging prices of multivariate contingent claims from the viewpoint of game-theoretic probability and submodularity. By considering a game between “Market” and “Investor” in discrete time, the pricing problem is reduced to a backward induction of an optimization over simplexes. For European options with payoff functions satisfying a combinatorial property called submodularity or supermodularity, this optimization is solved in closed form by using the Lovász extension and the upper and lower hedging prices can be calculated efficiently. This class includes the options on the maximum or the minimum of several assets. We also study the asymptotic behavior as the number of game rounds goes to infinity. The upper and lower hedging prices of European options converge to the solutions of the Black-Scholes-Barenblatt equations. For European options with submodular or supermodular payoff functions, the Black-Scholes-Barenblatt equation is reduced to the linear Black-Scholes equation and it is solved in closed form. Numerical results show the validity of the theoretical results.

1 Introduction

The pricing of contingent claims is a central problem in mathematical finance (Karatzas and Shreve, 1998). The fundamental models of financial markets are the binomial model (Shreve, 2003) and the geometric Brownian motion model (Shreve, 2005) in discrete-time and continuous-time setting, respectively. These models describe complete markets and therefore the price of any contingent claim is obtained by arbitrage argument. Specifically, the Cox-Ross-Rubinstein formula (Cox et al., 1979) and the Black-Scholes formula (Black and Scholes, 1973) provide the exact price in the binomial model and the geometric Brownian motion model, respectively. These formulas are derived by constructing a hedging portfolio for the seller to replicate the contingent claim.

In general, the market is incomplete and the above formulas are not applicable. Even in incomplete markets, we can define the upper and lower hedging prices of a contingent claim by considering superreplication (Karatzas and Shreve, 1998). Musiela (1997) and El Karoui and Quenez (1995) provide fundamental results on the upper hedging price in discrete-time models and continuous-time models, respectively. As a special case, for discrete-time models with bounded martingale differences, Ruschendorf (2002) pointed out the upper hedging price of a convex contingent claim is obtained by the extremal binomial model.

Although the above studies focused on contingent claims depending on a single asset, there are contingent claims for which the payoff depends on two or more assets (Stapleton, 1984), which are called multivariate contingent claims. For example, Stulz (1982) and Johnson (1987) investigated the pricing of options on the maximum or the minimum of several assets. Boyle et al. (1989) developed a numerical method for pricing multivariate contingent claims in discrete-time models. Although their method is based on a lattice binomial model that is originally incomplete, they change the model to make it complete by specifying correlation coefficients between all the pairs of assets. Thus, their method does not compute the upper hedging price. On the other hand, Romagnoli and Vargiolu (2000) considered superreplication in continuous-time models and derived the pricing formula based on the Black-Scholes-Barenblatt equation. They also provided some sufficient conditions on payoff functions for reduction of the Black-Scholes-Barenblatt equation to the linear Black-Scholes equation.

Whereas existing studies on the upper and lower hedging price are based on stochastic models of financial markets, Nakajima et al. (2012) investigated this problem from the viewpoint of the game-theoretic probability (Shafer and Vovk, 2001), in which only the protocol of a game between “Investor” and “Market” is formulated without specification of a probability measure. They showed that the upper hedging price in the discrete-time multinomial model is obtained by a backward induction of linear programs, and that the upper hedging price of a European option converges to the solution of the one-dimensional Black-Scholes-Barenblatt equation as the number of game rounds goes to infinity.

In this paper, we investigate the upper hedging price of multivariate contingent claims by extending the game-theoretic probability approach of Nakajima et al. (2012). We consider a discrete-time multinomial model with several assets and show that the upper hedging price of multivariate contingent claims is given by a backward induction of a maximization problem whose domain is a set of simplexes, which becomes intractable in general as the number of assets increases. However, we find that this maximization is solved in closed form if the contingent claim satisfies a combinatorial property called submodularity or supermodularity (Fujishige, 2005). Specifically, the maximizing simplex is determined by using the Lovász extension (Lovász, 1983) for European options with supermodular payoff function on two or more assets and also European options with submodular payoff function on two assets. As realistic examples, we prove that options on the maximum and the minimum of several assets are submodular and supermodular, respectively. Then, by considering the asymptotics of the number of game rounds, we show that the upper hedging price of a European option converges to the solution of the Black-Scholes-Barenblatt equation. In particular, for European options with supermodular payoff function on two or more assets and also European options with submodular payoff function on two assets, the Black-Scholes-Barenblatt equation reduces to the linear Black-Scholes equation, which is solved in closed form. Finally, we confirm the validity of the theoretical results by numerical experiments.

As in Nakajima et al. (2012), we consider the price processes in an additive form and the Black-Scholes-Barenblatt equation in section 4 is actually an additive form of the Black-Scholes-Barenblatt equation in the standard finance literature. Similarly, the linear Black-Scholes equation is given in the form of a heat equation. However, the results of this paper holds for the usual multiplicative model with simple exponential transformations. Except for a few places we do not specifically indicate that our equations are in the additive form.

In section 2, we provide a formulation of the upper hedging price based on the game-theoretic probability. In section 3, we derive results for the special case of European options with submodular or supermodular payoff function, which include the option on the maximum or the minimum. In section 4, we derive PDE for asymptotic upper hedging prices. In section 5, we confirm the theoretical results by numerical experiments. In section 6, we give some concluding remarks and discuss future works.

2 Game-theoretic derivation of upper hedging prices of multivariate contingent claims

In this section, we present a formulation of the upper hedging price based on the game-theoretic probability (Shafer and Vovk, 2001). The pricing problem is reduced to a backward induction of linear programs. As special cases, we consider convex or separable payoff functions.

2.1 Definitions and notation

Let , , be a finite set, which we call a move set. Let denote the convex hull of . We assume that the dimension of is and contains the origin in its interior. The protocol of the -round multinomial game with assets is defined as follows:

FOR

Investor announces

Market announces

END FOR

Here, denotes the initial capital of Investor, corresponds to the vector of amounts Investor buys the assets, corresponds to the vector of price changes of the assets and corresponds to Investor’s capital at the end of round . When , this game reduces to the game analyzed in Nakajima et al. (2012). One natural candidate for is a product set

| (1) |

where . Such with was adopted by the lattice binomial model (Boyle et al., 1989).

We call the sample space and a path of Market’s moves. For , is a partial path. The initial empty path is denoted as . We call a strategy. When Investor adopts the strategy , his capital at the end of round is given by , where

We call a function a payoff function or a contingent claim. If depends only on , then is called a European option. The upper hedging price (or simply upper price) of is defined as

| (2) |

and the lower hedging price is defined as

A strategy attaining the infimum in (2) is called a superreplicating strategy for .

A market is called complete if the upper hedging price and the lower hedging price coincide for any payoff function. For example, the binomial model, which corresponds to and , is complete (Shreve, 2003).

As discussed in section 1 we consider an additive form of the game where the prices changes ’s are added rather than multiplied in .

2.2 Formulation with linear programming

Following Nakajima et al. (2012), we formulate the pricing problem as a recursive linear programming.

First, we consider the single-round game (). Note that the payoff function is . Let be the set of simplexes of dimension containing the origin. For each , define

where the probability vector is defined as the unique solution of the linear equations

| (3) |

By extending Proposition 2.1 of Nakajima et al. (2012), we obtain the following.

Proposition 2.1.

For a single-round game, the upper hedging price of a payoff function is given by

| (4) |

Proof.

From (2), the upper hedging price of is the optimal value of the following linear program:

The dual of this linear program is

From the complementary condition (Boyd and Vandenberghe, 2004), there exists an optimal solution of the dual problem that has at most nonzero variables. Then, from the constraint of the dual problem, we have for some . Therefore, we obtain (4). ∎

Similarly, the lower hedging price of for a single-round game is

The relation (4) is interpreted as follows. A probability vector is called a risk neutral measure on if the expectation under is zero:

Let be the set of risk neutral measures on . Note that is closed and convex. Then, the set coincides with the set of extreme points (vertices) of . Since the maximum of a linear function on a closed convex set is attained at extreme points, the maximization in (4) is interpreted as searching over all risk neutral measures:

where denotes the expectation with respect to .

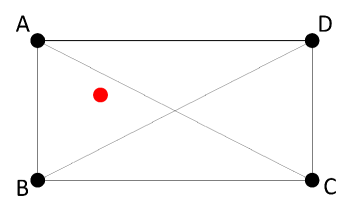

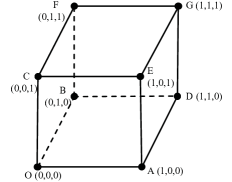

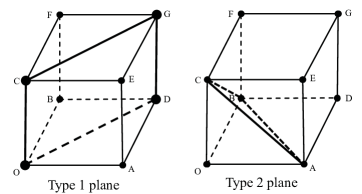

When and , the maximization in (4) involves two candidates of . Specifically, the possible is ABC or ABD in Figure 1. When and , the maximization in (4) becomes more difficult since the number of possible becomes large. For example, when , the number of possible can be as large as 14, as shown in Appendix A. In general, the number of possible is at least , as shown in Appendix B. In the next section, we will provide some sufficient conditions on for the maximization in (4) to be solved explicitly.

Now, we consider the -round game. As discussed by Nakajima et al. (2012) for , the upper hedging price is calculated by solving linear programs recursively. Specifically, let , be given by

| (5) |

with the initial condition for . Here, denotes a function defined by . Then, we have the following result.

Proposition 2.2.

The upper hedging price of is given by

Therefore, the upper hedging price is calculated by a backward induction of (5). In particular, for a European option, depends only on and so the required number of calculations (5) grows only polynomially with .

The lower hedging price is also calculated by a backward induction. In general, a market with is complete since , irrespective of .

2.3 Convex payoff functions

Here, we consider the case where the payoff function is a European option with convex function . When , the calculation of the upper hedging price of a convex payoff function is reduced to the binomial model (Ruschendorf, 2002), since the maximization in (4) is always uniquely attained by the extreme pair . For general , we have the following result.

Proposition 2.3.

Suppose that is a European option with convex function . Let be the set of vertices of . Then, the upper hedging price of with move set coincides with that with move set :

| (6) |

Proof.

We provide a proof for the single-round game. By applying it to each induction step, the proof for the multi-round game is obtained.

Since , we obtain

| (7) |

Let . From Caratheodory’s Theorem (Rockafeller, 1997), for each , there exists a subset of and a probability vector such that

Thus, from the convexity of ,

Therefore,

for any . By summing up the right hand side for each point of , we obtain

where since

and

Thus, for every , there exists such that

By taking the maximum in the left hand side, we obtain

| (8) |

Suppose and the move set is a product set (1). Then, Proposition 2.3 implies that we can redefine as the move set. However, unlike the case , even with this reduction to , the maximizing in (4) is not unique in general. One example is the option on the maximum with , as we will see in the next section.

2.4 Separable payoff functions

We call a European option separable if it can be decomposed as

| (9) |

where is a partition of :

We assume that the move set is a direct product of move sets for each subset . For example, when and , the move set is a product set as in (3). Then, the calculation of the upper hedging price of a separable European option is reduced to that for each component European option as follows.

Proposition 2.4.

Suppose is separable (9) and is a direct product of move sets for each subset . Then, the upper hedging price of coincides with the sum of the upper hedging prices of :

| (10) |

Proof.

We provide a proof for the single-round game. By applying it to each round, the proof for the multi-step game is obtained.

For simplicity of notation we consider the case and without essential loss of generality. Then, the move set is a product set and the payoff function is written as

| (11) |

Let be an arbitrary risk neutral measure on and let be its marginals. Then, each is a risk neutral measure on . By taking expectations in (11),

Since ,

Therefore,

| (12) |

Conversely, let be arbitrary risk neutral measures on , respectively. Define . Then, is a risk neutral measure on and it satisfies

Since ,

Therefore,

| (13) |

3 Submodular and supermodular payoff functions

We have seen that the calculation of the upper hedging price reduces to backward induction of the maximization (4). In this section, we show that this maximization is solved in closed form if the payoff function satisfies a combinatorial property called submodularity or supermodularity. As a special case, we discuss the options on the maximum or the minimum. Throughout this section, we assume that the move set is a product set (1) with , i.e., the lattice binomial model. Note that for , because we are assuming that contains the origin in its interior.

3.1 Submodular and supermodular functions

The concept of submodularity is fundamental in combinatorial optimization theory (Fujishige, 2005).

Definition 3.1.

-

•

A set function is said to be submodular if it satisfies

for every .

-

•

A set function is said to be supermodular if it satisfies

for every .

It is well known (Theorem 44.1 of Schrijver (2003)) that in Definition 3.1 we only need to consider and such that

| (14) |

We can extend the definition of submodularity and supermodularity to functions on the hypercube and . For vectors , we denote the vectors of componentwise minimum and maximum by and , respectively:

Then, submodular and supermodular functions on the hypercube and are defined as follows.

Definition 3.2.

-

•

A function or is said to be submodular if it satisfies

(15) for every or .

-

•

A function or is said to be supermodular if it satisfies

for every or .

We note that the concept of multivariate total positivity (MTP2) is closely related to submodularity (Karlin, 1968; Fallat et al., 2017). Namely, a positive function is MTP2 if and only if its logarithm is supermodular.

When or is twice continuously differentiable, the submodularity and supermodularity of are characterized by the signs of the mixed second order derivatives as follows.

Lemma 3.1.

-

•

A twice continuously differentiable function or is submodular if and only if

(16) for every .

-

•

A twice continuously differentiable function or is supermodular if and only if

for every .

3.2 Convex closure and Lovász extension

In considering the maximization (4), the concepts of convex closure and Lovász extension are useful. Dughmi (2009) presents a brief survey on these topics.

Let be a finite set. For a subset of , its characteristic vector is defined as

In the following, we identify with by the bijection . For a set function , a function or is said to be its extension if it satisfies .

Definition 3.3.

For a set function , its convex closure and concave closure are extensions of defined as

From the definition, and are convex and concave, respectively.

Lemma 3.2.

For a set function , its convex closure and concave closure are given by

| (17) |

Proof.

See section 3.1.1 of Dughmi (2009). ∎

Another type of extension was introduced by Lovász (1983) and it plays an important role in submodular function optimization (Fujishige, 2005).

Definition 3.4.

Note that the Lovász extension can be viewed as taking a special value of in (17). Lovász (1983) showed that the submodularity of a set function is equivalent to the convexity of its Lovász extension . In fact, there is a stronger result as follows.

Lemma 3.3.

-

•

The convex closure of a submodular function is equal to the Lovász extension of : .

-

•

The concave closure of a supermodular function is equal to the Lovász extension of : .

Proof.

See section 3.1.3 of Dughmi (2009). ∎

3.3 Relation between upper hedging price and concave closure

Let be a bijective affine map defined by and be its restriction to . By using , we can identify the payoff function of the single-round game with a set function . Then, its concave closure is closely related to the maximization (4) as follows.

Proposition 3.1.

For a single-round game, the upper hedging price is given by

Proof.

From Lemma 3.2,

| (18) |

Since is a bijective affine map, the first constraint on in (18) is equivalent to

| (19) |

Here, for , each entry of is

Thus, (19) is rewritten as

Therefore, each satisfying the constraints in (18) is viewed as a risk neutral measure on . Since is the maximum over all risk neutral measures, we obtain .

3.4 Two assets case

Suppose and , where and .

For a single-round game, the maximization in (4) involves two candidates of . One of them () has positive correlation while the other () has negative correlation. For example, in Figure 1, ABD and BCD have positive correlation while ABC and ACD have negative correlation. Similarly to section 3.3, the payoff function is identified with a set function . If is submodular or supermodular, then the maximizer in (4) is determined as follows.

Proposition 3.2.

Proof.

From the definition of the Lovász extension,

Now, consider the -round game and assume that the payoff function is a European option , where and . Recall that depends only on for a European option. The submodularity or supermodularity of the payoff function is preserved throughout backward induction of (5) as follows.

Lemma 3.4.

-

•

Suppose is submodular. Then, for , the composite function of and is submodular for every .

-

•

Suppose is supermodular. Then, for , the composite function of and is supermodular for every .

Proof.

We prove the first statement by induction on . The proof of the second statement is similar.

The case is trivial from , and Definition 3.2.

Now, assume that the composite function of and for every is submodular as a set function. Since depends only on , we write . Then, for every and , from (5) and Theorem 3.1,

where . Therefore,

For every , the function is the composition of and and therefore it is submodular from assumption. Then, since the submodularity is preserved under a convex combination, the composite function of and is also submodular. ∎

3.5 The case of more assets

Suppose and , where .

Consider a single-round game. Similarly to section 3.3, the payoff function is identified with a set function . If is supermodular, then as in the second part of Proposition 3.2, the maximizer in (4) is determined as follows.

Proposition 3.3.

Now, consider the -round game and assume that the payoff function is a European option , where and . Lemma 3.4 is extended to general by the same proof as follows.

Lemma 3.5.

Suppose is supermodular. Then, for , the composite function of and is supermodular as a set function for every .

Combining Lemma 3.5 and Proposition 3.3, each maximization in (5) is solved in closed form as follows.

Thus, when is supermodular, the upper hedging price can be calculated efficiently. On the other hand, when is submodular, the maximization in (4) cannot be solved in closed form (Calinescu et al., 2007). Since the number of possible grows at least as fast as (see Appendix B), the calculation of the upper hedging price of a European option with a submodular payoff function becomes intractable when is large.

3.6 Options on the maximum or the minimum

A typical and realistic example of multivariate contingent claims is the option on the maximum or the minimum of several assets (Stulz, 1982; Johnson, 1987). The option on the maximum is a European option with the payoff function

where . Similarly, the option on the minimum is a European option with the payoff function

Proposition 3.4.

-

•

The function is submodular.

-

•

The function is supermodular.

Proof.

Assume without loss of generality. Then since . Also, since . Therefore, we obtain .

Assume without loss of generality. Then since . Also, since . Therefore, we obtain . ∎

Corollary 3.1.

Suppose and .

4 Limiting behavior of upper hedging price of a European option

In this section, we show that the upper hedging price of a European option converges to the solution of the Black-Scholes-Barenblatt equation as the number of game rounds goes to infinity. We also show that, when the payoff function is submodular or supermodular, the Black-Scholes-Barenblatt equation reduces to the linear Black-Scholes equation and it is solved in closed form.

4.1 Derivation of the Black-Scholes-Barenblatt equation

Consider an -round multinomial game with a European option

| (21) |

Recall . For each , the risk neutral measure was defined as the solution of the linear equations (3). Let be the covariance matrix of :

For a twice continuously differentiable we denote its Hessian matrix as

Then, by extending Theorem 4.1 of Nakajima et al. (2012), we obtain the following.

Theorem 4.1.

Consider an -round multinomial game with a European option (21), where has a compact support and twice continuously differentiable. Assume .

-

•

The limit of the upper hedging price of a European option (21) is

where is the solution of the partial differential equation

(22) with the initial condition .

-

•

The limit of the lower hedging price of a European option (21) is

where is the solution of the partial differential equation

(23) with the initial condition .

By Theorem 4.6.9 of Pham (2009) a smooth solution of (22) and (23) exists under the assumptions of Theorem 4.1. The notion of viscosity solution is needed if or is only continuous. As discussed in Section 6.3 of Shafer and Vovk (2001) the result of this theorem can be extended to the case that the third and the fourth order derivatives of are bounded. The PDE (22) is (the additive form of) the Black-Scholes-Barenblatt equation (Romagnoli and Vargiolu, 2000).

When , the maximum in (22) only depends on the sign of the second derivative of and (22) reduces to the equation (13) in Nakajima et al. (2012). This case is also discussed in Peng (2007) and Section 5 of Romagnoli and Vargiolu (2000). However, when , the maximization in (22) becomes more complicated. This maximization is discussed from the viewpoint of optimization theory in Section 4 of Romagnoli and Vargiolu (2000).

The Black-Scholes-Barenblatt equation in Romagnoli and Vargiolu (2000) is

| (24) |

with the initial condition . Here, is a closed bounded set in the space of real matrices. The PDE (22) is viewed as a special case of the PDE (24) where is a finite set. In other words, the PDE (24) is a generalization of the PDE (22) to bounded forecasting games. Nakajima et al. (2012) also discussed this point.

4.2 Reduction to the linear Black-Scholes equation

Romagnoli and Vargiolu (2000) stated that the Black-Scholes-Barenblatt equation (24) reduces to the ordinary linear Black-Scholes equation

| (25) |

if the maximizing does not depend on nor . Note that this PDE has the same form with the heat equation with anisotropic conductivity. Such reduction occurs when the payoff function is submodular or supermodular and the move set is a product set (1) with . Specifically, by taking in Theorem 3.1 and 3.2, we obtain the following.

Proposition 4.1.

Suppose , and is twice continuously differentiable.

Proposition 4.2.

Suppose , and is twice continuously differentiable. Define by (20).

The linear Black-Scholes equation (25) is solved in closed form by convolution of Gaussian densities. Specifically, if is smooth and has its third and fourth derivatives bounded,

with initial condition is given by

where is the Gaussian density with covariance :

Thus,

which is the expected value of where has the distribution . Below we write . Based on this, the upper and lower hedging prices are explicitly obtained as follows.

Theorem 4.2.

Suppose , and is smooth and has its third and fourth derivatives bounded.

-

•

If is submodular,

-

•

If is supermodular,

-

•

If is submodular,

-

•

If is supermodular,

Theorem 4.3.

Suppose , and is smooth and has its third and fourth derivatives bounded. Define by (20).

-

•

If is supermodular

-

•

If is submodular

In Theorem 4.2 and 4.3 we assumed that is smooth and has its third and fourth derivatives bounded. However Theorem 4.2 and 4.3 hold for non-smooth payoff functions, such as options on the maximum or the minimum, because these payoff functions can be uniformly approximated by smooth payoff functions.

5 Numerical results

In this section, we confirm the validity of the theoretical results by numerical experiments.

To calculate the asymptotic value of the upper and lower hedging prices, we solve the Black-Scholes-Barenblatt equation

with the initial condition by the finite difference method (Smith, 1985). We explain the method for in the following. Let and be the step sizes in space and time, respectively. Here, we use the same value of step size in each space dimension for simplicity and is an integer. We restrict the domain of to the rectangle , where is a sufficiently large integer. Let be the numerical value of for , and . From the initial condition, we set . To calculate for iteratively, we employ the explicit Euler scheme and select at each step by comparing all elements in , following the approach of Nakajima et al. (2012) for . Specifically, the scheme is written as

| (26) |

where is the discretization of the Hessian defined as

We solve (26) iteratively for with the Dirichlet boundary condition where . Then, we adopt as the approximate value of the upper hedging price. To avoid numerical instability, the step sizes must satisfy

which is called the Crank-Nicolson condition (Smith, 1985).

5.1 Options on the maximum or the minimum of two assets

Here, we calculate the upper and lower hedging prices of options on the maximum or the minimum of two assets (Stulz, 1982). Specifically, the option on the maximum of two assets is defined as

| (27) |

and the option on the minimum of two assets is defined as

| (28) |

In our experiments we take .

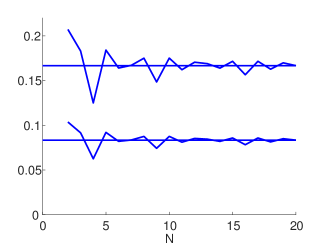

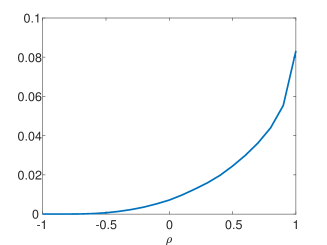

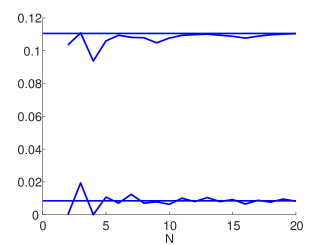

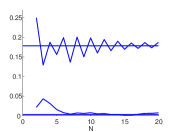

Suppose the move set is . Figure 2 plots the upper and lower hedging prices calculated by solving (5) recursively for each . The calculated prices almost converge around . In this case, from Theorem 4.2, the limits of upper and lower hedging prices are obtained in closed form. Note that

Thus, means while means . Therefore, the limits of the upper hedging prices are

and the limits of the lower hedging prices are

These values are shown in Figure 2 by the horizontal lines. They agree well with the convergence values.

(a)

(b)

The move set corresponds to a lattice binomial model considered in Boyle et al. (1989). Based on this model, Boyle et al. (1989) proposed a method for pricing multivariate contingent claims by specifying the correlation coefficient between two assets. Specifically, if the correlation coefficient between two assets under a risk neutral measure is given, then is uniquely determined as

Then, we can use the Cox-Ross-Rubinstein formula (Cox et al., 1979) to calculate the prices. Namely, we take the expectation with respect to :

| (29) |

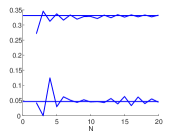

Note that this method does not provide the upper or lower hedging price in general. Figure 3 plots the prices calculated by (29) for each value of where . For the option on the maximum (27), the prices for and coincide with the upper and lower hedging prices, respectively. For the option on the minimum (28), the prices for and coincide with the upper and lower hedging prices, respectively. These are understood from Corollary 3.1, because means that is always taken while means that is always taken. When , the risk neutral measure is not uniquely determined by specifying correlation coefficients because . Although Boyle et al. (1989) select one risk neutral measure by considering symmetry, there seems to be no theoretical support of this selection.

(a)

(b)

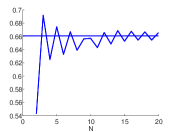

Now, suppose the move set is . Figure 4 plots the upper and lower hedging prices calculated by solving (5) recursively for each . We also calculated the limits of upper and lower hedging prices by solving the Black-Scholes-Barenblatt equation (22) numerically. In the finite difference method, we set the step sizes to and , which satisfy the Crank-Nicolson condition, and restricted the domain of to . The calculated values are

| (30) |

These values are shown in Figure 4 by the horizontal lines.

(a)

(b)

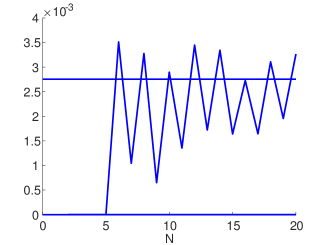

5.2 Option on the minimum of three assets

Here, we calculate the upper hedging price of the option on the minimum of three assets (Johnson, 1987) defined as

| (31) |

In our experiments we take .

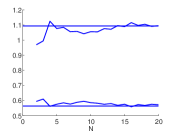

Suppose the move set is . Then, in (20) and are obtained as

| (32) |

| (33) |

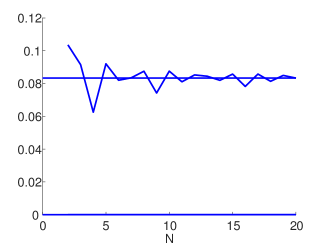

Figure 5 plots the upper hedging price calculated by solving (5) recursively. It almost converges around . On the other hand, from Theorem 4.3,

where . We calculated this expectation by the Monte Carlo method with samples and obtained

| (34) |

This value is shown in Figure 5 by the horizontal line. It agrees well with the convergence value.

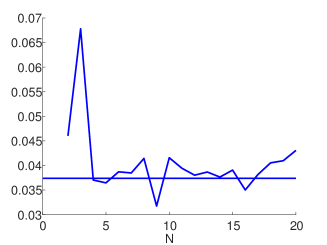

5.3 Butterfly-type options

Finally, we consider European options motivated from Butterfly spread options. Nakajima et al. (2012) calculated the upper and lower hedging prices of the Butterfly spread options when :

Here, we consider the case where and the move set is or . In numerical solution of the Black-Scholes-Barenblatt equation (22) by the finite difference method, we set the step sizes to and , which satisfy the Crank-Nicolson condition, and restricted the domain of to .

5.3.1 Non-separable case

Consider a European option defined as

| (35) |

When is fixed, this payoff function behaves like the Butterfly spread option as a function of .

Figure 6 plots the upper and lower hedging prices calculated by solving (5) recursively for each . On the other hand, the limit values calculated by solving the Black-Scholes-Barenblatt equation (22) numerically are

These values are shown in Figure 6 by the horizontal lines. They agree well with the convergence values.

(a)

(b)

5.3.2 Separable case

Consider a European option defined as

| (36) |

where

| (37) |

is the butterfly spread option used in Nakajima et al. (2012). This option is separable.

Figure 7 plots the upper and lower hedging prices calculated by solving (5) recursively for each . On the other hand, the limit values calculated by solving the Black-Scholes-Barenblatt equation (22) numerically are

These values are shown in Figure 7 by the horizontal lines. They agree well with the convergence values. Note that the upper and lower hedging prices coincide for , which illustrates Proposition 2.4.

(a)

(b)

6 Conclusion

We investigated the upper hedging price of multivariate contingent claims from the viewpoint of the game-theoretic probability. The pricing problem is reduced to a backward induction of an optimization over simplexes. For European options with submodular or supermodular payoff functions such as the options on the maximum or the minimum of several assets, this optimization is solved in closed form by using the Lovász extension. As the number of game rounds goes to infinity, the upper hedging price of European options converges to the solution of the Black-Scholes-Barenblatt equation. For European options with submodular or supermodular payoff functions, the Black-Scholes-Barenblatt equation is reduced to the linear Black-Scholes equation and it is solved in closed form. Numerical experiments showed the validity of the theoretical results.

We mainly restricted our attention to European options. Extension to path-dependent payoff functions, including American options, is an important future problem. For such payoff functions, the definition of submodularity or supermodularity seems not trivial.

Also, we mainly assumed that the move set is a product set (1). In particular, our results on submodular and supermodular payoff functions are based on the lattice binomial model. Extension to general move sets is another interesting future problem.

The Black-Scholes-Barenblatt equation is a special case of time-dependent diffusion equation (Hundsdorfer and Verwer, 2003). Although we used a simple finite difference method for numerical solution, it would be interesting to investigate more effective numerical methods.

Acknowledgment

We thank Naoki Marumo and Kengo Nakamura for helpful comments. This work was supported by JSPS KAKENHI Grant Numbers 16K12399 and 17H06569.

References

- Black and Scholes (1973) Black, F. & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81, 637–654.

- Boyd and Vandenberghe (2004) Boyd, S. & Vandenberghe, L. (2004). Convex Optimization. Cambridge University Press, Cambridge.

- Boyle et al. (1989) Boyle, P. P., Evnine, J. & Gibbs, S. (1989). Numerical evaluation of multivariate contingent claims. The Review of Financial Studies, 2, 241–250.

- Calinescu et al. (2007) Calinescu, G., Chekuri, C., Pal, M. & Vondrak, J. (2007). Maximizing a submodular set function subject to a matroid constraint. In Proceedings of the 12th International Conference on Integer Programming and Combinatorial Optimization, 541–567.

- Cox et al. (1979) Cox, J. C., Ross, S. A. & Rubinstein, M. (1979). Option pricing: a simplified approach. Journal of Financial Economics, 7, 229–263.

- Dughmi (2009) Dughmi, S. (2009). Submodular functions: extensions, distributions, and algorithms. A survey. arXiv 0912:0322.

- El Karoui and Quenez (1995) El Karoui, N. & Quenez, M. C. (1995). Dynamic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization, 33, 29–66.

- Fallat et al. (2017) Fallat, S., Lauritzen, S., Sadeghi, K., Uhler, C., Wermuth, N. & Zwiernik, P. (2017). Total positivity in Markov structures. The Annals of Statistics, 45, 1152–1184.

- Fleming and Soner (2006) Fleming, W. H. & Soner, H. M. (2006). Controlled Markov Processes and Viscosity Solutions. Springer, New York.

- Fujishige (2005) Fujishige, S. (2005). Submodular Functions and Optimization. Elsevier, Amsterdam.

- Hundsdorfer and Verwer (2003) Hundsdorfer, W. & Verwer, J. G. (2003). Numerical Solution of Time-Dependent Advection-Diffusion-Reaction Equations. Springer, Berlin.

- Johnson (1987) Johnson, H. (1987). Options on the maximum or the minimum of several assets. Journal of Financial and Quantitative Analysis, 22, 277–283.

- Karatzas and Shreve (1998) Karatzas, I. & Shreve, S. E. (1998). Methods of Mathematical Finance. Springer, New York.

- Karlin (1968) Karlin, S. (1968). Total Positivity. Stanford University Press, Stanford.

- Lovász (1983) Lovász, L. (1983). Submodular functions and convexity. Mathematical Programming: The States of the Art, 235–257, Springer, Berlin Heidelberg.

- Musiela (1997) Musiela, M. & Rutkowski, M. (1997). Martingale Methods in Financial Modelling. Springer, Berlin.

- Nakajima et al. (2012) Nakajima, R., Kumon, M., Takemura, A. & Takeuchi, K. (2012). Approximations and asymptotics of upper hedging prices in multinomial models. Japan Journal of Industrial and Applied Mathematics, 29, 1–21.

- Peng (2007) Peng, S. (2007). G-expectation, G-Brownian motion and related stochastic calculus of Ito type. In Stochastic Analysis and Applications: Abel Symposium, 2, 541–567, Springer, Berlin.

- Pham (2009) Pham, H. (2009). Continuous-time Stochastic Control and Optimization with Financial Applications. Springer, Berlin.

- Rockafeller (1997) Rockafeller, R. T. (1997). Convex Analysis. Princeton University Press, Princeton.

- Romagnoli and Vargiolu (2000) Romagnoli, S. & Vargiolu, T. (2000). Robustness of the Black-Scholes approach in the case of options on several assets. Finance and Stochastics, 4, 325–341.

- Ruschendorf (2002) Ruschendorf, L. (2002). On upper and lower prices in discrete time models. Proceedings of the Steklov Institute of Mathematics, 237, 134–139.

- Schrijver (2003) Schrijver, A. (2003). Combinatorial Optimization: polyhedra and efficiency. Springer, New York.

- Shafer and Vovk (2001) Shafer, G. & Vovk, V. (2001). Probability and Finance: It’s Only a Game!. Wiley, New York.

- Shreve (2003) Shreve, S. E. (2003). Stochastic Calculus for Finance I: The Binomial Asset Pricing Model. Springer, New York.

- Shreve (2005) Shreve, S. E. (2005). Stochastic Calculus for Finance II: Continuous-Time Models. Springer, New York.

- Smith (1985) Smith, G. D. (1985). Numerical Solutions of Partial Differential Equations. Clarendon Press, Oxford.

- Stapleton (1984) Stapleton, R. C. & Subrahmanyam, M. G. (1984). The valuation of multivariate contingent claims in discrete time models. Journal of Finance, 39, 207–228.

- Stulz (1982) Stulz, R. M. (1982). Options on the minimum or the maximum of two risky assets. Journal of Financial Economics, 10, 161–185.

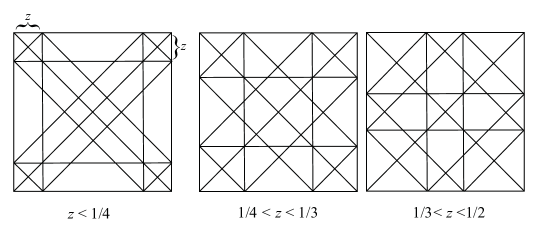

Appendix A Number of candidates in three dimension

Here, we calculate the number of candidates when . Let be the interior of a set and be the complement of .

Lemma A.1.

Let

be the regular tetrahedra in the cube . Consider a point and let be the set of tetrahedra containing .

-

•

If , then .

-

•

If or , then .

-

•

If , then .

Proof.

We only give a sketch of a proof, because we used computer to count the number of tetrahedra containing a point .

The cube is denoted as the left picture of Figure 8. There are 14 planes containing three or four vertices of the cube, which cut into the cube. There are 6 Type 1 planes containing four vertices with the equations

| (38) |

and there are 8 Type 2 planes containing three vertices with the equations

| (39) |

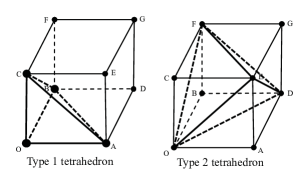

There are 58 tetrahedra (simplexes) in 4 types as in Figure 9. There are 8 Type 1 tetrahedra, which are corner simplexes. There are 2 Type 2 regular tetrahedra denoted as in the lemma. There are 24 Type 3 tetrahedra and there are 24 Type 4 tetrahedra. We keep the list of these 58 tetrahedra in a computer program.

On the other hand, it is easy to visualize the 14 planes in (38) and (39) by fixing and drawing the sections of the cube as in Figure 10. The 14 planes appear as 14 lines inside the unit squares in Figure 10. Note that we only need to consider by symmetry: . For each region of the sections of Figure 10 we count the number of tetrahedra containing the region. Then we obtain the lemma.

∎

Note that Lemma A.1 applies only for generic . For on the boundary of a tetrahedron, the number may be larger. For example is contained in tetrahedra of Types 2-4.

Appendix B Lower bound on the number of candidate

Here, we provide a lower bound on the number of candidates for general .

Lemma B.1.

Assume . Consider a point in the -dimensional hypercube and define . Then,

Proof.

First, we consider the case where is a generic point Without loss of generality, we assume

| (40) |

Let

and be an index attaining the minimum:

| (41) |

Note that since . In the following, we focus on simplexes that have the zero vector as one vertex. Note that such simplex has nonempty interior if and only if the other vertices are linearly independent.

Let , be a 0-1 vector defined by

| (42) |

In particular, is the zero vector. Then, the vector is decomposed as

| (43) |

where we define and . Therefore, from (40),

| (44) |

Now, we construct simplexes containing by changing the vertex in (44). Note that every 0-1 vector is uniquely expressed as

where satisfies

Under this correspondence, there are vectors with and . These vectors are given by

| (45) |

for some and . Thus,

| (46) |

where the sum of coefficients in the left hand side is 1 or 2. By substituting (46) into (43),

where and . Therefore,

Since there are choices of , we have .

Next, we consider the case where is not a generic point. Without loss of generality, we assume

where at least one inequality holds with equality. Then, we can take a sequence of generic points satisfying (40) and having the same that converges to . Let . Then, from the above argument, for each and the simplexes containing are common. In particular . Also, since the simplex is closed, belongs to each simplex in : . Therefore, . ∎