Optimal Bidding, Allocation and Budget Spending for a Demand Side Platform Under Many Auction Types

Abstract.

We develop a novel optimization model to maximize the profit of a Demand-Side Platform (DSP) while ensuring that the budget utilization preferences of the DSP’s advertiser clients are adequately met. Our model is highly flexible and can be applied in a Real-Time Bidding environment (RTB) with arbitrary auction types, e.g., both first and second price auctions. Our proposed formulation leads to a non-convex optimization problem due to the joint optimization over both impression allocation and bid price decisions. Using Fenchel duality theory, we construct a dual problem that is convex and can be solved efficiently to obtain feasible bidding prices and allocation variables that can be deployed in a RTB setting. With a few minimal additional assumptions on the properties of the auctions, we demonstrate theoretically that our computationally efficient procedure based on convex optimization principles is guaranteed to deliver a globally optimal solution. We conduct experiments using data from a real DSP to validate our theoretical findings and to demonstrate that our method successfully trades off between DSP profitability and budget utilization in a simulated online environment.

1. Introduction

In targeted online advertising, the main goal is to figure out the best opportunities by showing an advertisement to an online user, who is most likely to take a desired action, such as ordering a product or signing up for an account. Advertisers usually use the service of companies called demand-side platforms (DSP) to achieve this goal.

In a DSP, each individual advertiser sets up a list of campaigns that can be thought of as plans for delivering advertisements. For each campaign, the advertiser specifies the characteristics of the audience segments that it would like to target (e.g., males, ages 18-35, who view news articles on espn.com) along with the particular media that it would like to display to the target audience (e.g., a video ad for beer). In this work we will call an impression type to a specific collection of those attributes (e.g., male, California, interested in sports). In addition, the advertiser specifies a budget amount, time schedule, pacing details, and performance goals for each campaign. The performance goals typically can be specified by minimizing cost-per-click (CPC) or cost-per-action (CPA).

The DSP manages its active campaigns for many different advertisers simultaneously across multiple ad exchanges where ad impressions can be acquired through a real-time bidding (RTB) process. In the RTB process, the DSP interacts with several ad exchanges where bids are placed for potential impressions on behalf of those advertisers. This interaction happens in real time when an ad request is submitted to an ad exchange (which may happen, for example, when a user views a news story on a webpage). In this scenario, the DSP needs to offer a solution to decide, among the list of all campaigns associated with its advertiser clients, which campaign to bid on behalf of and the bid values.

The advertisers who work with the DSP expect its budget to be spent fully or at least in an adequate amount as their marketing areas count on it. Failure to do so may motivate an advertiser to stop working with the DSP in the future, which is unacceptable for its business. In addition, they would like their budget to be spend smoothly if possible. Then, the DSP faces the problem of maximizing its profit while ensuring an adequate budget spending for its advertisers clients.

DSPs can charge their clients using several pricing schemes, for example in a CPM format advertisers are charged a fixed amount per thousand of impressions showed to users (which is mostly used for branding of products). If the advertisers are interested in some click or action of interest, they may pay in CPM scheme, but requiring that no more than certain amount per click or action of interest is paid (action of interest could be filling a form, purchasing a product, etc.). In this work, we we will assume that the DSP gets paid only when a click or action of interest occurs, but has to pay to the ad exchanges for each impression it acquires. This is a challenging payment setting as the DSP may have a negative operation if the actions or clicks of interest don’t occur at the rates the DSP expects. It is important to mention that DSPs usually receive millions of ad requests opportunities per minute, and their bidding systems needs to respond to each of this ad request in matter of milliseconds making most companies apply simple heuristics to bid in the RTB systems. To simplify notation we will assume in this work that the advertisers are interested in clicks of interest, while this work apply in general to any action of interest.

As a final remark ad exchanges may use different auctions types to sell advertisement opportunities. As an example, several ad exchanges such as OpenX, AppNexus have announced that they use first price auctions, i.e. the highest bidder pays the ad exchange the amount it offered, while others like Google’s AdX have announced that they use second price auctions which is that the highest bidder pays the second highest bid submitted to the ad exchange. This add an extra layer to any general DSP optimization algorithm that may want to bid in different ad exchanges for the same advertisers.

In this paper, we propose a novel approach to maximize the DSP profit while ensuring an adequate budget spending for its advertisers clients. We take into account that the DSP may bid in different ad exchanges who may use different auction rules. Appropriately modeling the impression arrival, auction, and click/action processes our non-convex model gives as an output bidding and allocation vectors that can be used in real time by a DSP to bid in RTB environments. To solve our model we propose a dual formulation using Fenchel conjugates and derive a two-phase primal-dual procedure to solve our non-convex problem. We show that the solutions given by our solution procedure are optimal for several first and second price auctions, results that up to our knowledge are novel in the literature. Experimental results show how our methodology is able to trade off DSP profitability for better budget spending for first and second price auctions in synthetic data, and data based on a real DSP operation.

Due to space limitations we only review works very close to ours, and of those who we take ideas from. In terms of finding biding and allocation schemes different schemes have been suggested in the literature from the ad exchange point of view (Balseiro et al., 2014; Chen et al., 2014; Grigas et al., 2017), and from the DSP side (Perlich et al., 2012; Chen et al., 2011). In terms of spending the advertisers budget adequately (Lee et al., 2013; Xu et al., 2015) set smart pacing strategies. Strategies for bidding using Lagrangian schemes for DSPs have appeared (Zhang et al., 2014a; Ren et al., 2018) and who use the Ipinyou dataset to validate their results (Zhang et al., 2014b) as us. Here we formulate a dual problem using the concept of Fenchel conjugates (Boyd and Vandenberghe, 2004, p. 91), which we solve using standard subgradients methods. Our results are similar in spirit to the recent work (Wang, 2017). The latter studies a non-convex multi-agent optimization problem and also uses Fenchel conjugates to construct a dual problem. Our work differs from the latter as we are able to obtain stronger theoretical results in comparison to (Wang, 2017) using the structure of the online advertising problem studied here (which makes our proofs unique).

The rest of the paper is organized as follows. In Section 2, we describe the notation and problem statement and we set up the model. Section 3 show our proposed optimization problem. In Section 4 we propose a dual for our problem of interest, showing several properties of it and proposing a two-phase primal-dual scheme. In Section 5 we show important optimality results and propose two-phase primal-dual scheme to solve our problem of interest. Experimental results using the Ipinyou data (Zhang et al., 2014b) are presented in Section 6, and we mention some future work directions. Section 7 is the appendix which has the proofs to all propositions and theorems shown in this work.

2. Model Foundations

Let us begin by describing the basic structure and flow of events in the model. Let denote the set of all campaigns associated with advertisers managed by the DSP. The DSP interacts with several ad exchanges, and recall that each auction held by one of these ad exchanges represents an opportunity to show an ad to a particular impression (i.e., a user). Although there may be billions of possible impression opportunities each day, we assume that the DSP uses a procedure for mapping each impression opportunity to an impression type. Let denote the set of all such impression types. Whenever an opportunity for an impression of type arrives to one of the ad exchanges, the DSP has to make two real-time strategic decisions related to the corresponding auction: (i) how to select a campaign to bid on behalf of in the auction, and (ii) how to set the corresponding bid price . If the DSP wins the auction on behalf of campaign , then the DSP pays the corresponding market price (which depends on the auction type) to the ad exchange, and an ad from campaign is displayed to the user. The advertiser corresponding to campaign is charged only if the user clicks on the ad.

Key Parameters for Impression Types and Campaigns

Our model presumes that the DSP has knowledge (or estimates) of the following parameters:

-

•

is the expected number of impressions of type that will arrive during the planning horizon.

-

•

is the (advertiser selected) budget for campaign during the planning horizon.

-

•

denotes the set of impression types that campaign targets. (Note that each advertiser can create multiple campaigns to achieve different targeting goals.)

-

•

is the CPC (cost per click) price for campaign , i.e., the amount charged to the associated advertiser each time a user clicks on an advertisement from campaign .

Auction Modeling

We take a flexible approach to auction modeling. In particular, we simply presume that, for each impression type , the DSP has constructed the following two bid landscape (Cui et al., 2011) functions (which include first and second price auctions):

-

•

– the probability of winning an auction for an impression of type given that the DSP submitted a bid of .

-

•

– the expected amount the DSP pays the ad exchange, conditional on the DSP winning the auction with a submitted bid of .

We will assume and to be non-decreasing functions, and for all and .

Click Events

Whenever an ad of campaign is shown to an impression of type (after the DSP wins the corresponding auction), we presume that a click event happens with probability . In other words, is the expected click-through-rate. In addition, given an impression type and a campaign , let denote the corresponding expected revenue earned by the DSP, which is the same as the expected cost per impression (eCPI) to the advertiser. Namely, it holds that where is the CPC price defined earlier.

Decision Variables and Additional Notation

When the DSP has the opportunity to participate in an auction for an impression of type it needs to decide which campaign to bid on behalf of and the bid value to submit. Let denote the edges of an undirected bipartite graph between and , whereby there is an edge whenever campaign targets impression type , i.e, . Let denote the set of campaigns that target impression type . For each edge , we define two decision variables: (i) the probability that the DSP selects campaign , and (ii) the bid value to submit to the auction. Interpreted differently, represents a proportional allocation, i.e., the fraction of auctions for impression type that are allocated to campaign on average. (The fraction of impression type auctions for which the DSP decides to not bid is .) Note that represents the bid price that the DSP submits to an auction for impression type conditional on the fact that the DSP has selected campaign for the auction. Let denote vectors of these quantities, which will represent decision variables in our model.

Let us also define some additional notation used herein. For a given set and a function , let denote the (possibly empty) set of maximizers of the function over the set . If is a convex function then, for a given , denotes the set of subgradients of at , i.e., the set of vectors such that for all . Finally, let be the function that returns the maximum between the input and 0, and ′ denote a derivative in the right context.

3. Optimization Formulation

Let us begin by recalling the model developed in (Grigas et al., 2017) (proposed only for second price auctions there), which aims to maximize the profit of the DSP under budget constraints:

| (1) | subject to | |||

The first set of constraints above specify that the expected budget spent by each campaign should be less than the total available budget. The second set of constraints bounds the range of the bid prices, and the third and fourth set of constraints ensure that x represents a valid probability vector when restricted to each impression type. The objective function is the expected DSP profit, which we aim to maximize. Indeed, note that for each pair the quantity is the expected profit earned by the DSP whenever an ad of campaign is show to an impression of type , and is the expected number of impression of type that we will acquire on behalf of campaign . Therefore, is the expected profit due to bidding for impressions of type on behalf of campaign , and summing these quantities over all pairs yields the total expected profit for the DSP, which we call .

Notice that the previous formulation does not ensure or even encourage an adequate budget spending for the campaigns, it only ensures that each campaign does not spend in expectation more than its total budget. In reality, advertisers are not satisfied by merely ensuring that their spending on each campaign is below the specified budget level. Rather, most advertisers view the budget value as a “target” and may have complex preferences regarding their spending behaviors. For example, an advertiser may be very dissatisfied with underspending behavior and may in fact prefer slightly overspending above the budget value instead of severely underspending well below .

In order to greatly enhance the flexibility of our model as well as its ability to capture complicated budget spending preferences, we replace the budget constraints in (3) with a more general utility function model as follows. First, note that the expected total spending of campaign , as a function of the decision variables, is given by . Now, let be a concave utility function describing the budget spending preferences of campaign , whereby is the “utility” of campaign when its expected spending level is . Furthermore, define the vector of expected spending levels whose coordinate is , and let be the overall budget spending utility function whereby . Finally, as an extra way to simplify notation let’s define the feasible set of allocation and bidding variables:

We are now ready to state our proposed optimization model:

| (2) |

Note that problem (2) is non-convex, and in Section 4 we propose a computationally efficient procedure based on convex duality. We finish this section by showing three examples of utility functions that illustrate the improved generality and flexibility of model (2).

- Examples of Utility Functions:

- (1)

-

(2)

If we want to maximize the DSP profit but also try to enforce an appropriate target spending for a campaign , we can take to be the concave function such that equals if is strictly greater than , and otherwise. Here is a user defined penalization constant.

-

(3)

If we want to maximize the DSP profit while requiring both a minimum and maximum expected spending for campaign , we can take to be the concave function such that equals if is strictly greater than or strictly less than , and otherwise. Here, the parameter is user defined and represents the minimum percentage of expected budget spending.

Note that the model (2) allows for each campaign to have its own distinct utility function , and therefore the three examples above may be combined together across the different campaigns, for example. Finally, note also that the separable structure of the utility function , whereby , is actually not needed for all of the results that we develop herein. Indeed, the only crucial assumption about is that is a concave function. However, the separable structure is quite natural and all of our examples do have this separable structure as well, so for ease of presentation we present the model in this way.

4. Dual Optimization Problem and Scheme

We begin this section with a high-level description of our approach for solving (2). Our algorithmic approach is based on a two phase procedure. In the first phase, we construct a suitable dual of (2), which turns out to be a convex optimization problem that can be efficiently solved with most subgradient based algorithms. A solution of the dual problem naturally suggests a way to set the bid prices . In the second phase, we set the bid prices using the previously computed dual solution then we solve a convex optimization problem that results when is fixed in order to recover allocation probabilities . A very mild assumption we make for the rest of the paper is that , otherwise there would be no optimization problem to optimize.

As we mentioned before we have assumed that our utility function is concave, therefore is a convex function and we can define its convex conjugate as which is a convex function. The Fenchel Moreau Theorem (Boyd and Vandenberghe, 2004, p. 91) ensures that . Using the latter we can re-write our primal problem as (here we use ):

For a given we will define the dual function as:

And the dual problem as:

Then, the following inequalities hold for our primal and dual formulations (they follow from the max-min inequality (Boyd and Vandenberghe, 2004, p. 238)):

Let’s now define the expected profit the DSP receives from showing an ad of campaign to an impression of type which has an expected revenue of $ when submitting a bid of value $. Then, given a fixed the dual function can re-defined as:

Proposition 4.1 (Efficient computation of ).

Given a dual variable , an optimal solution for the dual function can be found using Algorithm 1.

Theorem 1 shows that the dual problem can be solved in a parallel fashion, and furthermore finding can be a simple operation. For example, in the case of a second price auction it is known that , and some examples for first price auctions have nice close forms as shown in the next section. Being able to solve efficiently is of great importance as it is a core component to find a subgradient of as the following theorem shows:

Proposition 4.2.

Given the output of Algorithm 2 is a vector .

Notice that with STEP 1. in Algorithm 1 we can recover bidding prices from dual variables . The final Theorem of this section shows that for fixed bidding prices is easy to obtain allocation probabilities by solving problem (2).

Proposition 4.3.

For fixed bidding prices , problem (2) is a convex problem.

Proposition 4.3 tell us that we could use a sub-gradient method to find to find an allocation vector given a fixed . Better than the previous, depending on the utility function used (2) can have a nice structure, for example for the utility function examples shown in the previous section, examples 1. and 3. transform problem (2) in a linear program and example 2. in a quadratic problem. Problems that could be solved directly using solvers like Gurobi (Gurobi Optimization, 2016). We finish this section by presenting Algorithm 3 which formalize our approach to solve problem (2).

5. Zero Duality Gap Results

Algorithm 3 can always be used as long as the parameters and functions of problem (2) are well defined. Here we we will go further and show that our dual formulation and dual scheme are the right methods to solve (2). In particular, we have strong duality results which to the best of our knowledge are novel and have important applications to first and second price auctions by showing optimal bidding prices to be used in an RTB environment. These will be derived from the following theorem:

Theorem 5.1.

If for all we have that and are differentiable and:

-

•

for all .

-

•

is strictly increasing for all .

for all , then for any , we have for any .

Notice that Theorem 5.1 ensures that no duality gap exists, but furthermore for an optimal dual variable it gives a form of the variables such that . Also, notice that the second condition of the theorem is a form of diminishing returns.

- Applications of Theorem 5.1:

-

(1)

If for all their auctions are second price and is a strictly increasing function in , then Theorem 5.1 holds. Also, for an optimal dual variable optimal bidding prices are for all .

-

(2)

If for all all auctions are first price auctions or more generally scaled first price auctions in which the winning DSP pays an percentage of the bid it offered, Theorem 5.1 holds when is a strictly increasing twice differentiable concave function. Example of the later are: 1) for some fixed , 2) square roots and logarithms, 3) representing the cumulative distribution function of an exponential or logarithm-exponential random variable.

-

(3)

If for all all auctions are first scaled price auctions with in which for each impression there is a fixed number of other DSPs who bid independently as , then Theorem 5.1 holds. Furthermore, for an optimal dual variable optimal bidding prices are for all .

-

(4)

Any combination of the above, or cases in which each impression type satisfies the conditions of Theorem 5.1.

We finish this section by making three important comments. First, to obtain the form of the optimal bidding prices is only needed to solve . In many cases, like second price auction, this will have a close form, but for many others the DSP can have tables with approximate solutions that can be used instead of solving the problem in real time. Second, many ad-exchanges use what are called hard reserve prices that consider a bid valid only if it is higher than the reserve price. This poses a problem for Theorem 5.1 as the condition of being strictly non-decreasing would not be true. If the impression types had fixed hard reserve prices this is not a major issue as we can change the model to bid between the reserve price and (if the reserve price were higher than wouldn’t bid for that impression type). In the case that hard reserve prices change dynamically, heuristics could be used, e.g. considering bidding in real time only only for those campaigns with bid values higher than the reserve price, putting levels of reserve price as a field in the impression types, and others which we don’t explore here. Third, it can be proven that Theorem 5.1 guarantees that Algorithm 3 would converge to an optimal solution for (2) as we get better solutions of the dual problem. For space reasons we don’t extend on this topic here.

6. Computational Experiments

Here we present computational results using the Ipinyou DSP data (Zhang et al., 2014b) to which we applied our two-phase solution procedure comparing its performance w.r.t. a greedy heuristic. The way we suggest and apply in our experiments an allocation and bidding variables in a practical RTB environment is shown in Policy 4 and the heuristic to which we compare our method is shown in Policy 5.

The Greedy Heuristic is optimal for the case of infinite budgets and second price auctions (is easy to extend it to arbitrary auction types). As an important remark our method should be used in a real DSP operation inside a Model Predictive Control Scheme, which calls Algorithm 3 as budgets get used and different model inputs gets updated as time progresses.

The public available Ipinyou data (Zhang et al., 2014b) contains information about real bidding made by the chinese DSP Ipinyou in 2013. It contains different features including the bidding prices of the impressions for which Ipinyou bid for, and the price paid by Ipinyou to the ad-exchange in case an impression was won and if a click or conversion occurred (we did not use conversion data). Ipinyou assumes that ad-exchanges use second price auctions. The data is already divided in train and test sets and it has been used to test bidding strategies for DSPs (Zhang et al., 2014a; Ren et al., 2018) but we haven’t found a paper that use it for both bidding and allocation strategies, reason why we compare to the Greedy Heuristic 5. Ipinyou data is divided in three different time periods in 2013, of those we decided to use the third as in the first there is no information about the campaigns Ipinyou bid for, and in the second Ipinyou assumed that all impression types could serve all campaigns which make the impression-campaign graph non-interesting. The third season contains 3.15M of and 1.5M logs of impressions won by Ipinyou in the train and test set resp. in behlaf of four advertisers, which have 2716 and 1155 clicks associated to them. Here we use the different advertisers as our campaigns.

To create “impression types” we divided the impressions by the visibility feature which has a strong correlation with CTR, and then by the regions, homepage url, and “width x height” of the ad to be shown (features that appear in all impression logs). The last three features have a high dimensionality, for example homepage url have 54,108 unique urls. For that reason we created mutually exclusive sets of the form all urls that were targeted only by advertiser 1, all that were targeted only by advertisers 1 and 3, etc. With this technique we partition all impressions for which Ipinyou bid for in 160 clusters of impressions which we used to create our final partition of 23 impression types. Of those 19 corresponds to the clusters with a minimum of 30,000 impressions won in the train set and the 4 left are the union of all clusters having different visibility attribute (we grouped together the second, third, fourth and fifth view as if they were the same visibility type). Our final graph is composed of 4 campaigns, 23 impression types, it has 43 edges, and the different CTR were taken as the empirical rates for each combination of (impression type, advertiser). Using only the impressions won in the train set for each impression type we fitted a beta distribution using the python Scipy package (imposing the location parameter to be equal to zero) to obtain parameters to estimate the bid landscape functions (the function is just a function call, but the function was estimated using Monte-Carlo). Finally, we count the times each impression type appears in the test set to create the values, and the budgets correspond to the total amount of money that Ipinyou paid for the impressions assigned to each advertiser in the test set. To simulate a real time environment we used the empirical train CTR to train our models and the greedy heuristic (we took the average CTR per impression for the pairs of (impression type,advertiser) that appear less than 5000). To test our model we use the impressions won by Ipinyou in the actual order saving their impression type. Then, one by one we read each impression log and we assume that the impression was won if the proposed bid for it is higher than the amount Ipinyou paid for it. A click for the proposed advertiser occurs with probability equal to the empirical CTR from the test data for the pair (impression type, advertiser). We tried the utility functions 1. and 2. from Section 3, using for all for second one.

Results

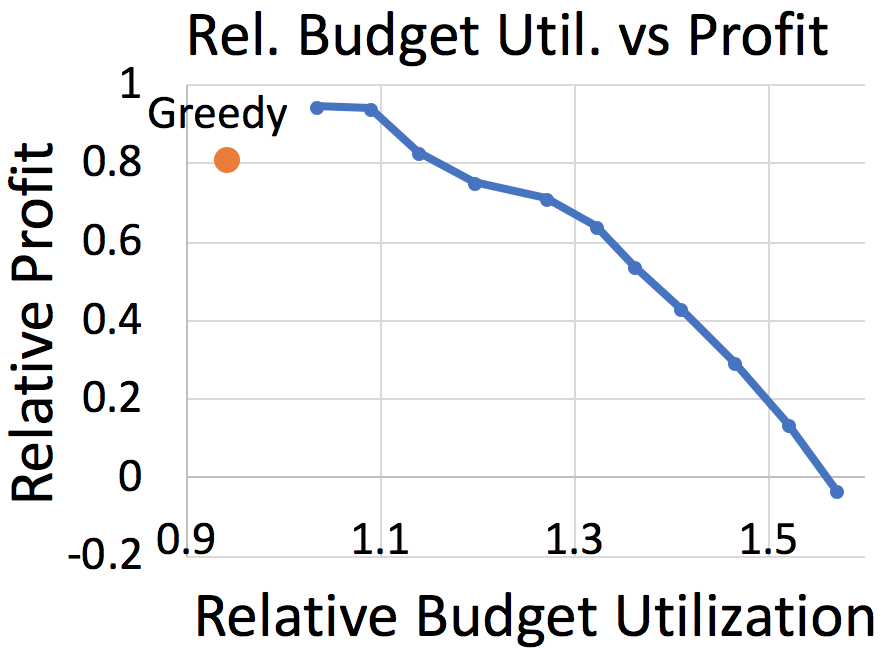

Our results are shown in Figure 1. Here we define budget utilization (b.u.) as the percentage of the total budget that was used at the end of one simulation, and u.f. stands for utility function. We performed two experiments. The first was to see the sensitive of our model w.r.t. to the budget. We tried , , , and of the budgets Ipinyou used for each advertiser in the test data and we run 100 simulations for each setting obtaining average profit and b.u. Our results are all relative to the average profit and b.u. obtained by using the greedy heuristic. What makes one simulation different from the other is that the CTR is a random variable. In the second experiment we multiply the penalization parameters that appear in the u.f. 2 by 0.1, then by 0.3, and so on until 2.1 running 100 simulations in each case obtaining the average profit and b.u. All our results are relative to the average profit and b.u. of the u.f. 1. and we also include the average results from the greedy heuristic for comparison. Our results show that our methodology works very well for cases in which the budget is tight, but when is not the case the greedy heuristic is a good alternative. From our second experiment we can see that a better b.u. utilization can be obtained at the cost of having a worst profit (it can even be negative).

|

||||||||||||||||||||||||

|

||||||||||||||||||||||||

Let us conclude this section by mentioning a few directions for future research. It would be very valuable to perform experiments in which impressions are auctioned in both first and second price auctions and in which the cardinality of the impression types and campaigns are higher. Also, several of the quantities we assume as known in this work are hard to estimate in practice. We will study robust approaches to our model.

7. Proofs of the Propositions and Theorem 5.1

In this appendix we will make use of the following definitions which for space we skip in the main text (we use them in the proofs of Proposition 4.2 and Theorem 5.1):

Definition 7.1.

-

•

The set of feasible bidding and allocation variables for a given impression type is:

-

•

The expected amount campaigns spend in impressions of type is which is a vector whose coordinate takes the value of if and o.w. Then, .

-

•

The contribution of the different impression types in the dual function is separable, and therefore given a fixed dual variable we define for each :

-

•

Let’s define the profit from impressions of type in the objective from impression of type in (3) as , and therefore .

Notice that for any both and depend only in , but we decide to use this notation to not carry the “” everywhere.

7.1. Proof of Proposition 4.1

Proof.

For fixed we have that is a constant, then we need to focus only on the maximization part of . For any fixed we have:

Take arbitrary and assume , then any is an optimal bidding price for the pair independent of the value of which proves STEP 1. of Algorithm 1. Fixing , we can use that for each we have and for all are the only constraints for (w.r.t. to impression type ), therefore is optimal for each impression type to bid only for a campaign that maximizes the profit we can get from it. If for an impression type there is no campaign which gives us a positive profit, then is optimal to not bid for that impression type. That’s exactly what STEP 2. of Algorithm 1 concluding the proof. ∎

7.2. Proof of Proposition 4.2

Proof.

Here we assume fix. Notice that using the definitions from Definition 7.1 we have . We are going that to show that for any and any we have . The previous is enough to finish this proof as and . Let be any dual variable different from (if not the following set of equations are trivial), and let arbitrary, then:

∎

7.3. Proof of Proposition 4.3

Proof.

Assume b fixed. The domain of is a set of linear constraints, then we only need to proof that the objective function is concave. Clearly the summation part of the objective function is linear and therefore concave, then is only left to show that the utility function part is concave. The latter is true as is an affine function in term of the allocation probabilities, therefore is the composition of a concave and affine function and therefore concave. ∎

7.4. Proof of Theorem 5.1

This proof uses the terminology defined in Definition 7.1 and we can assume and to be continuous functions for all parts in this proof as it is a weaker condition than being differentiable which is part of the hypothesis of Theorem 5.1. We will start by showing that if we assume and to be continuous for all , then we can obtain the explicit form of the sub-differential for any fixed (Lemma 7.2). Result that we combine with Lemma 7.3 to prove Lemma 7.4. The later results will help us prove that if there exists an optimal dual variable that satisfies a condition we call “Unique Solution” (Definition 7.5), then there is no duality gap (Lemma 7.6). Finally, we will prove Theorem 5.1 by showing that when the hypothesis of the theorem holds, then the “Unique Solution” condition hold for any feasible lambda (i.e., ), and therefore for any optimal dual variable.

Let’s first define as the set of optimal solutions for given for some , i.e. , and .

Lemma 7.2.

(Equivalent to Lemma 3.3 in (Wang, 2017)) The sub-differential of the dual function is

Proof.

Let’s define for each . Then, , and is differentiable w.r.t. to its first argument, is a continuous function w.r.t. both of its arguments, and is a continuous function w.r.t. to its second argument for all . Then, Danskin’s Theorem says . Finally, using that we obtain the desired conclusion. ∎

Lemma 7.3.

If there exists optimal dual variable, such that , for some , then .

Proof.

Using that , the optimality of and the definition of we have:

We will show that by proving

Let’s define the convex function , then for any . By hypothesis it exists , such that then, using the subgradient inequality:

Which shows that is a minimizer of concluding the proof. ∎

Lemma 7.4.

If there exists optimal dual solution, such that the sets are convex for all , then it exists , such that .

Proof.

Definition 7.5 (Condition: Unique Solution (US)).

We say that the dual variable satisfy the unique solution condition if

is a singleton whenever for all .

Lemma 7.6 (Unique Solution).

Assume for all , then if is an optimal dual solution that satisfies the Unique Solution condition, then there exists such that .

Proof of Theorem 7.6.

Let be an optimal dual solution that satisfies the Unique Solution condition. Our goal here will be to show that sets from Corollary 7.4 w.r.t. to are convex for all which would conclude this proof. Let with the set of impression types such that for all , and if . Notice that we can assume for all as if it weren’t case for some it would be optimal to make in our primal problem (3) and the edge could have been removed from the problem definition. Then, using the latter, the continuity of functions and and that for all and an impression type is in if and only if for all , and is the unique maximizer of for all . For this case we have:

Then, the set from Lemma 7.4 is a convex set for any as it would be equal to the convex hull over a finite amount of points. This is easy to see as the coordinate of any of its vectors is equal to 0 if or if , and if and the general form of the coordinate of its vectors is and with for all . For there is at least one with which implies (the implication follows from the continuity of the bid landscape and for all and ). Let’s define as for all , then for any :

Making a convex set for all . ∎

Proof Theorem 5.1.

First notice that the second condition of Theorem 5.1 implies that for all . Let and denote arbitrary bid landscape functions and the bidding range for an arbitrary impression type. Let arbitrary represent and expected revenue, then for any we have:

Notice that by hypothesis so sign is directly related to the term . Let’s use that is strictly increasing in and define . Then, is equal to:

The previous can be understood in very simple words, given that is strictly increasing in if , then is optimal to bid the maximum possible which is as is always strictly positive in . If for all then for all and therefore is optimal to bid 0 and by definition we would have . Finally, if neither of the previous cases occurs it means that there was a change of sign of in making it optimal to bid the value in which the change of sign occurs which is . Here we need to use in the definition of as is not necessarily continuous. Notice that always exists and is unique by definition. Notice that we have proven that the Unique Solution would hold for any dual variables, and therefore for any optimal dual variable . Then, by Lemma 7.6 holds we conclude this proof. ∎

References

- (1)

- Balseiro et al. (2014) Santiago R Balseiro, Jon Feldman, Vahab Mirrokni, and S Muthukrishnan. 2014. Yield optimization of display advertising with ad exchange. Management Science 60, 12 (2014), 2886–2907.

- Boyd and Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. 2004. Convex optimization. Cambridge university press.

- Chen et al. (2014) Bowei Chen, Shuai Yuan, and Jun Wang. 2014. A dynamic pricing model for unifying programmatic guarantee and real-time bidding in display advertising. In Proceedings of the Eighth International Workshop on Data Mining for Online Advertising. ACM, 1–9.

- Chen et al. (2011) Ye Chen, Pavel Berkhin, Bo Anderson, and Nikhil R Devanur. 2011. Real-time bidding algorithms for performance-based display ad allocation. In Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 1307–1315.

- Cui et al. (2011) Ying Cui, Ruofei Zhang, Wei Li, and Jianchang Mao. 2011. Bid landscape forecasting in online ad exchange marketplace. In Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 265–273.

- Grigas et al. (2017) Paul Grigas, Alfonso Lobos, Zheng Wen, and Kuang-chih Lee. 2017. Profit Maximization for Online Advertising Demand-Side Platforms. In Proceedings of the ADKDD’17 (ADKDD’17). ACM, New York, NY, USA, Article 11, 7 pages. DOI:http://dx.doi.org/10.1145/3124749.3124761

- Gurobi Optimization (2016) Inc. Gurobi Optimization. 2016. Gurobi Optimizer Reference Manual. (2016). http://www.gurobi.com

- Lee et al. (2013) Kuang-Chih Lee, Ali Jalali, and Ali Dasdan. 2013. Real time bid optimization with smooth budget delivery in online advertising. In Proceedings of the Seventh International Workshop on Data Mining for Online Advertising. ACM, 1.

- Perlich et al. (2012) Claudia Perlich, Brian Dalessandro, Rod Hook, Ori Stitelman, Troy Raeder, and Foster Provost. 2012. Bid optimizing and inventory scoring in targeted online advertising. In Proceedings of the 18th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 804–812.

- Ren et al. (2018) Kan Ren, Weinan Zhang, Ke Chang, Yifei Rong, Yong Yu, and Jun Wang. 2018. Bidding Machine: Learning to Bid for Directly Optimizing Profits in Display Advertising. IEEE Transactions on Knowledge and Data Engineering 30, 4 (2018), 645–659.

- Wang (2017) Mengdi Wang. 2017. Vanishing Price of Decentralization in Large Coordinative Nonconvex Optimization. SIAM Journal on Optimization 27, 3 (2017), 1977–2009.

- Xu et al. (2015) Jian Xu, Kuang-chih Lee, Wentong Li, Hang Qi, and Quan Lu. 2015. Smart pacing for effective online ad campaign optimization. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM, 2217–2226.

- Zhang et al. (2014a) Weinan Zhang, Shuai Yuan, and Jun Wang. 2014a. Optimal real-time bidding for display advertising. In Proceedings of the 20th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 1077–1086.

- Zhang et al. (2014b) Weinan Zhang, Shuai Yuan, Jun Wang, and Xuehua Shen. 2014b. Real-Time Bidding Benchmarking with iPinYou Dataset. arXiv preprint arXiv:1407.7073 (2014).