One family, six distributions – A flexible model for insurance claim severity

Abstract

We propose a new class of claim severity distributions with six parameters, that has the standard two-parameter distributions, the log-normal, the log-Gamma, the Weibull, the Gamma and the Pareto, as special cases. This distribution is much more flexible than its special cases, and therefore more able to to capture important characteristics of claim severity data. Further, we have investigated how increased parameter uncertainty due to a larger number of parameters affects the estimate of the reserve. This is done in a large simulation study, where both the characteristics of the claim size distributions and the sample size are varied. We have also tried our model on a set of motor insurance claims from a Norwegian insurance company. The results from the study show that as long as the amount of data is reasonable, the five- and six-parameter versions of our model provide very good estimates of both the quantiles of the claim severity distribution and the reserves, for claim size distributions ranging from medium to very heavy tailed. However, when the sample size is small, our model appears to struggle with heavy-tailed data, but is still adequate for data with more moderate tails.

keywords:

Automization, extended Pareto, power transformation, reserve estimation, unimodal families1 Introduction

The Burr family of loss distributions goes back to Burr [1942] and is also called extended or generalized Pareto and Beta prime. Its probability density functions are all unimodal (or monotonically decreasing). Further, there are three parameters which capture distributions of widely different shapes that range from heavy-tailed Paretos to light-tailed Gammas. The latter are on the boundary of the parameter space and are only reached as two of the parameters approach infinity. An even more versatile parametric family of distributions is proposed in this paper by applying parametrised power transformations to Burr-distributed random variables. We have used the classical BoxCox approach in Box and Cox [1964] with the modification that there are two free parameters. The resulting PowerBurr family has five parameters. It does again lead to unimodal probability density functions, and includes ten of the most commonly applied and quoted loss models in actuarial science, for example the log-normal and the Weibull in addition to the parent Burr distribution itself. This will be verified in the next section where an even wider class with a sixth parameter also will be introduced.

Constructions such as the preceding one raise the intriguing question of whether loss modelling can be carried out by fitting one of these many-parameter families and simply use the distribution found without any more ado, thus avoiding an additional model selection step. In situations where an underlying heterogeneity of unknown or unquantifiable source that cannot be linked to an observed covariate and expressed into a regression relationship, more complex modelling may be needed. In such cases the natural model is a mixture distribution as in Lee and Lin [2010], Bakar et al. [2015] and Miljkovic and Grün [2016], or even a traditional kernel density estimate based on, say Gaussian mixtures, as in Scott [1992]. Yet, the most common of all types of variations is undoubtedly the unimodal one, and here PowerBurr fitting is an alternative to the traditional approach of trying different two-parameter families and choosing between them by Q-Q plotting, formal selection criteria like AIC or BIC or goodness-of-fit testing.

Our aim is not to decide whether PowerBurr fitting is superior or inferior to such methods in terms of the error in the final solution. However, we will argue that its conceptual simplicity is attractive and offers a useful potential for automating the entire process from historical data to statements of risk in the computer. With a standard Poisson model for claim frequency, or solvency capital may be be evaluated by Monte Carlo, after estimating claim frequency and fitting loss data. The entire process may then be carried out with no or almost no human intervention at all. Such a program is not hard to implement in the computer and would draw on the simple algorithm for simulating PowerBurr variables in Section 2, but it does require a robust numerical procedure for estimating the parameters, which is a challenge. The criterion might be quite flat in some of the parameters, perhaps with multiple optima which are important practical obstacles to be addressed below.

A flat likelihood function means that many alternative distributions are almost equally likely given historical losses. Loss distributions are in reality no more than tools for evaluating risk. Whether they reduce to simple families or not and the interpretation of their parameters may not necessarily be issues of primary importance. However, what is important is that the tail behaviour may be quite different for distributions that are almost equally well-fitting in the central domain containing most of the data. A traditional attempt to deal with this is extreme value mixing, drawing on the result due to Pickands [1975] that over-threshold distributions always become Pareto or exponentially distributed as the threshold becomes infinite; consult Embrechts et al. [1997] for a review of such methods. A more recent contribution to such modelling is Lee et al. [2012]. PowerBurr fitting may be an alternative even here, perhaps by replacing the likelihood by a criterion that emphasizes more strongly the fit in the extreme right tail, for example using a weighted likelihood approach. This will however not be studied here. What will be investigated, is how errors in statements of risk, like the solvency capital, are linked to estimation errors in the PowerBurr family parameters. In particular, estimation uncertainty will increase with the number of parameters, which in the PowerBurr is quite large, as the amount of available data decreases. An extensive numerical experiment will be conducted, where the error in solvency capital will be examined. Litt mer her.

2 The PowerBurr family

2.1 Definition

The most convenient route to the Burr family is to start with Gamma variables and with expectation and shape parameters and . Their standard deviations are sd and sd from which it follows that and as and . The ratio

| (1) |

will be called a standard Burr variable. Two useful observations are immediate. If is , then is ; i.e the same model except for the role of the parameters being switched. Also note that becomes Gamma-distributed as since . The construction below extends in many other directions. The probability density function of is given by

| (2) |

where is the Gamma function. That was how the Burr family was defined originally in Burr [1942]. The proof of (2) is elementary; consult Section 9.7 in Bølviken [2014].

For the Burr model to be workable in practice it must be augmented with a parameter of scale so that it becomes . Our proposal is to replace this relationship with the more general

| (3) |

with , and as additional parameters. The version on the left with parameter vector will be referred to as PowerBurr5, and represents the main thrust of this paper. The other, PowerBurr6, has as a sixth parameter, and now . In either case , and pure Burr reappears when . The construction is inspired by the classical power transformation in Box and Cox [1964], but there and .

2.2 Properties

Unimodality The power transformation in (3) is strictly increasing everywhere. This is however not a guarantee that when one uses it to transform a random variable, the probability density function of the new variable has a shape suitable for modelling. Yet, that is largely the case here, as the following proposition shows.

Proposition 1.

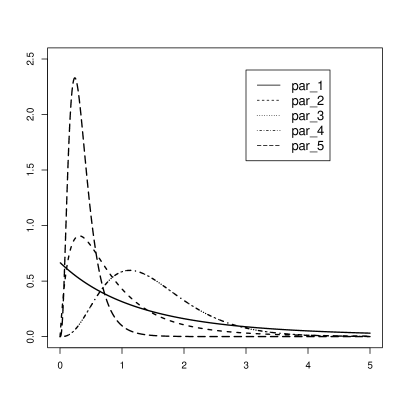

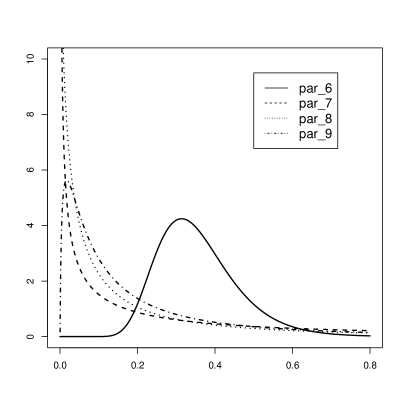

(i) All PowerBurr5 and PowerBurr6 distributions are unimodal if . (ii) The PowerBurr5 distributions are unimodal if .

The calculations when the proposition is proved in Section 2.4 shows that the precise condition for PowerBurr5 distributions being unimodal is

| (4) |

which may be too complicated to be of much practical value. If this fails to

hold, the density function has both a local minimum and a maximum. Examples of

probability density functions and their shapes are offered in Figure

1.

Moments and percentiles

Moments do not always exist. It emerges from expression

(2) that is finite if , and since

is the leading term in (3), the condition

for being finite is . Closed mathematical

expressions for these moments are not available unless , and

numerical methods are needed. Standard one-dimensional quadrature using

(2) is straightforward, and so is Monte Carlo (see

below). Similarly, the percentiles of lack closed formulae unless

, and again numerical methods have to be used.

Sampling It is easy to draw from a PowerBurr distribution when a Gamma

sampler is available. One simply generates Monte Carlo variates of

and , compute their ratio and inserts that into

(3).

Special cases

Most standard loss distributions in property insurance are included as special

cases, which is summarized in the following proposition, verified in Section

2.4.

Proposition 2.

The PowerBurr5 family contains the Burr, Pareto, Gamma, Inverse Gamma, Log-gamma, Logistic, Log-logistic, Weibull, Fréchet, and the Log-normal families when the parameters take the values shown in Table 1.

Nine of the ten families in Table 1 are defined in terms of shape parameters and and a parameter of scale , some of them through stochastic representation, others through the survival function . Only the definition of the Log-normal is different. The table shows how , , , and must be defined for the various special cases to appear. Many of them are located at the boundary of the parameter space and are only reached in the limit. As an example consider the Log-gamma family on row which appears when , and . This means that if PowerBurr5 is fitted Log-gamma losses with enough data, the computer will return large values for all three of , and with the scale parameter approximately the ratio .

| ∗ For the log-normal limit to be true must tend to faster than in the sense that . | |||||||

|---|---|---|---|---|---|---|---|

| Definition | |||||||

| 1 | Burr | ||||||

| 2 | Pareto | ||||||

| 3 | Gamma | ||||||

| 4 | Inverse Gamma | ||||||

| 5 | Log-gamma | ||||||

| 6 | Logistic | ||||||

| 7 | Log-logistic | ||||||

| 8 | Weibull | ||||||

| 9 | Fréchet | 1 | |||||

| 10 | Log-normal∗ | ||||||

Identifiability A stochastic model is identifiable if different parameter vectors always lead to different distributions. That is not the case here. For example, if , (3) shows that and affect through their ratio . It follows that if , the likelihood method in the next section will pick a pair with the right ratio. Which one does not matter since we in applications rarely are interested in the parameters themselves.

2.3 Fitting

Models have in this paper been fitted by maximum likelihood, which requires a mathematical expression for the probability density function of . Using the logarithmic form in (8) below and inserting (2) and (3), straightforward calculations lead to

| (5) | ||||

where

| (6) |

The relationship between and is the inverse of (3). When historical losses are given, must be computed for each observation and added for the log-likelihood function

| (7) |

Optimization was in this paper carried out by the quasi-Newton option in the R-function optim(). This is straightforward for two-parameter models, but more challenging when there are five or even six parameters and a log-likelihood function that may be quite flat, especially when is moderate. This means that widely different parameter values result in rather similar distributions. Consequently, the optimisation of the likelihood is sometimes challenging, but this is not that problematic when the resulting distributions are sensible. Still, we have derived the derivatives of the log-likelihood functions with respect to all parameters, and supply those to optim(). These are given in the Appendix. To ease the optimisation further, it is performed on the log-transformed parameters as all the parameters are positive. Finally, we do the optimisation with several sets of start values for the parameters, and choose the parameter estimates that give the highest likelihood value. More numerical details are given in Appendix 2.

2.4 Proofs of propositions

Proof of Proposition 1.

It is convenient to drop the parameter vector and let be the probability density function for rather than as above. Its relationship to the probability density for is through

and since , it follows that

| (8) |

so that

| (9) |

Recall that where is a constant. Hence

| (10) |

and moreover so that

and

Differentiating this yields

| (11) |

which is with (10)) to be inserted into (9). Then

and after some straightforward manipulations this can be rewritten

where

The sign of the derivative is determined by since the all other factors are positive. A more useful form is

which is established by multiplying out both factors and collecting the terms. A solution of the equation must therefore satisfy

| (12) |

When , the left hand side of (12) is monotonically increasing in whereas the right hand side is monotonically decreasing, and there is at most one solution to the equation. This means that has zero or one root, and is monotonically decreasing everywhere or has a single mode. The latter applies when the maximum of the right hand side of (12) is larger than the minimum on the left, i.e. when . This verifies the first part of Proposition 1.

To address the second part concerning PowerBurr5 let . Now becomes

which is a second order polynomial with negative quadratic term. Such functions have a single maximum, and if so that , there can be no more than one solution of the equation so that unimodality still holds. The condition can be expressed as , as claimed in part (ii) of Proposition 1.

To derive the precise algebraic condition (4) we must examine in detail. Elementary calculations show that its maximum occurs at

with maximizing value

The condition for the equation to have a single, positive root or no positive root at all is that either so that as in (4) left or either of and being true. The latter pair of conditions can be expressed jointly as

as in (4) right. ∎

Proof of Proposition 2.

One immediately sees that the Burr and Pareto distributions themselves are included in the PowerBurr family. The Gamma distribution is obtained by letting so that . By Slutsky’s theorem this implies which defines the Gamma family. The Inverse Gamma is obtained in a similar way. Now as and on row in Table 1.

In order to get the Log-Gamma or row insert and into (3). Then

and it follows that . Since as , and .

The logistic distribution on row emerges when so that by an elementary application of l’Hôpital’s rule

which yields

Let so that follows an ordinary Pareto distribution with parameters . As remarked in in Section 2.1, this is also the distribution of which means that the limit on the right is Er det en for mye i første likhet?

and in conclusion

The logistic model on row follows when . This is the definition used in Beirlant et al. [1996], but one could also contemplate an extended version with as a general parameter.

To obtain the log-logistic, the Weibull and the Frechèt on rows , and one starts with . Then

When , follows an ordinary Pareto distribution, such that

which is the expression on row when .

The Weibull model is defined as , where is the exponential distribution with mean , and emerges when , , and .

The Frechèt is obtained with the same specifications except that now and . Then

as on row .

Finally, to get the Log-normal on row , let and so that

Taylor’s formula with two terms and remainder yields

The bounds for are consequences of and imply as . It now follows after a little reorganization that

| (13) |

Insert so that

As and , and . In the denominator, from which it follows by Slutsky’s theorem that if both and and . Further, as . Since and , the exponent in 13 tends to in distribution, as was to be proved. ∎

3 Total loss model

As mentioned in the introduction, we assume the classic collective model for the total loss , given by (LABEL:eqn:total_loss), where the claim sizes are independent and identically distributed, and also independent of the number of claims. Assuming that s from different policies are identically distributed is obviously a simplification. However, it may be argued that when the main interest is measuring risk in terms of the total loss , and not pricing of individual contracts, differences between policies will be averaged out.

Further, we assume that the number of claims follows a Poisson distribution with fixed intensity for all policies, i.e. , where is the total risk exposure of the portfolio, i.e. the number of policy years in the portfolio during the priod over which the claims are counted. This is also a simplification, but as noted earlier, the main focus of our paper is on the claim size distribution.

Finally, the claims sizes are assumed to follow a distribution with parameters and pdf , more specifically the six-parameter distribution or one of its special cases. The model for the total loss is then such that there is no explicit expression for the reserve for any of the claim severity distributions we consider. Therefore, these have to be estimated with Monte Carlo methods. The first step is then to generate independent samples from the model, as specified in Algorithm 1. Subsequently, the reserve is estimated by

| (14) |

where . In this setting, the total risk exposure is , where is the current number of policies in the portfolio and year. In addition, we are interested in the quantile of the claim size distribution, given by

This will indicate how well our model captures the tail properties of the claim severity distribution and may help us to understand the performance of our model for estimating the reserve. For the extended Pareto distribution, we compute with a numeric search algorithm and for the six-parameter distribution, it is computed by (LABEL:eqn:quantfunc).

Even though the six-parameter distribution is very flexible, it will never be the exact true data generating process . Hence, there will always be some model error in estimates of the reserve from this distribution. If the parameters are estimated by the maximum likelihood, the estimate will converge to the value of that minimises the Kullback-Leibler divergence

from the true to the model . Now, let be the reserve based on , and the corresponding Monte Carlo estimate. Then we have:

where is the Monte Carlo error, is the estimation error and is the model error. The former, , depends on the number of simulations , and will converge to as tends to . Hence, the Monte Carlo error will be quite small as long as one chooses a large enough . Further, the model error depends on the Kullback-Leibler divergence form the true distribution to the assumed distribution. As the six-parameter distribution is very malleable, this error is also likely to be small. We may thus assume that the estimation error , which is a function of the sample size, is the main source of error.

Input: , , , , ,

4 Simulation study

The proposed claim size distribution is more flexible than its two-parameter special cases. The question is how well it estimates the reserve, and how this estimate is affected by the increased parameter uncertainty due to the larger number of parameters. In order to investigate this, we conduct a large simulation study. The parameter settings for the study are presented in Section 4.1, some remarks about parameter estimation are given in Section 4.2 and the results from the study are given in Section 4.3.

4.1 Parameter settings

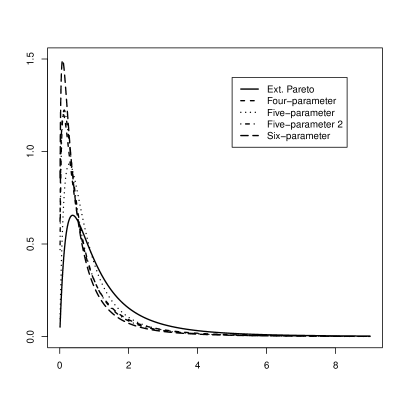

In all, we consider different claim size distributions: the log-normal, the log-Gamma, the Weibull, the Pareto, the Gamma, the extended Pareto, the four-parameter special case with , the two five-parameter special cases with and , respectively, and the full six-parameter distribution. Each experiment is performed as described in Algorithm 2. One of the distributions is the true claim size distribution with pdf . First, a sample of size is drawn from this distribution. Then, the parameters of each of the distributions considered in this study are estimated based on the sample, resulting in the estimates . Finally, one estimates the reserve and the quantile of the claim size distribution using Algorithm 1 with each and corresponding . This procedure is repeated times. Note that the parameter of the claim frequency distribution is not estimated, but set to its true value. This is done in order to isolate the uncertainty in the reserve stemming from the claim size distribution.

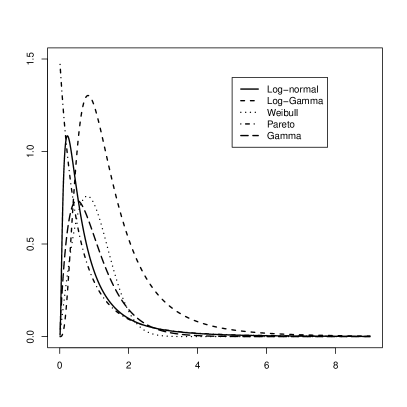

The parameter values used in the study are shown in Table 2. These are chosen so that , except for the log-Gamma distribution, for which this was impossible without making very small. Further, the parameter values are set so that the corresponding distributions range from medium to very heavy-tailed. Figure 2 shows the corresponding pdfs. For the claim frequency distribution (which is Poisson), we let take each of the values to represent variations in portfolio size and claim intensity.

| Distribution | |||

|---|---|---|---|

To assess the effect of the sample size, we have run the experiments for each of , which corresponds to data sets ranging from rather large to rather small, but realistic, depending on the line of business. Further, we used in the Monte Carlo estimation of the reserve. Finally, we let in all experiments.

4.2 Parameter estimation

All the distribution parameters are estimated by maximum likelihood

estimation, using the R function optim() to do

quasi-Newton optimisation. For the two-parameter families, this

optimisation is straightforward. However, especially the five-

and six-parameter distributions appear to have likelihood functions

that are rather flat in some of the parameters. This means that

widely different parameter values result in rather similar

distributions. Consequently, the optimisation of the likelihood

is sometimes challenging, but this is not that problematic when

the resulting distributions are sensible. Still, we have derived

the derivatives of the log-likelihood functions with respect to

all parameters, and supply those to optim(). These are

given in the Appendix. To ease the optimisation further, it is

performed on the log-transformed parameters as all the parameters

are positive. Finally,

we do the optimisation with several sets of start values for the

parameters, and choose the parameter estimates that give the

highest likelihood value. More specifically, we use the moment

estimates ,

as well as and

for the extended Pareto

distribution, where and

are the maximum likelihood

estimates obtained for the Gamma and Pareto distributions, respectively.

For the four-parameter distribution, we employ

and , where

and are the estimates

from the extended Pareto and Weibull distributions. The

start values used for the five-parameter distribution are

and ,

where is the estimate

from the log-Gamma distribution. For the five-parameter 2

distribution, the start values are

,

where

are the estimates from the four-parameter distribution. Finally,

the start values for the six-parameter distribution are

and

,

where

and

are the estimates from the five-parameter and five-parameter 2

distributions.

4.3 Results

The results from the simulations in terms of the bias and root mean squared error (RMSE) of the quantile and reserve estimates are shown in Tables 3 to 14. The relative performance of the models with is rather similar to that with , though with larger biases and RMSEs. Hence, the results from the corresponding simulations are not shown here. Furthermore, our main interest is the performance of the six-parameter distribution and its five- and four-parameter versions when the true distribution is one of the six special cases from Table 1, i.e. whether our model is able to capture the behaviour of these different distributions in practice for finite sample sizes, as it has been shown to do in theory. Hence, we only report the results from the simulations with one of the Table 1 distributions as the true distribution.

Tables 3 and 4 display the bias and RMSE in the estimates of for and , respectively, when the sample size is . Corresponding results for sample size are shown in Tables 5 and 6. We see that when the sample size is large, the quantile estimates from the six-parameter, five-parameter 2 and four-parameter distribution are just as good as the ones from the true distribution, both in terms of bias and RMSE. The performance of the five-parameter distribution is good for the quantile, but inferior to the others for the quantile. As mentioned above, the impression from the simulations with are the same. Hence, our model performs well also for medium sample sizes. When the sample size is reduced to , we see that the estimates of from our model are still rather good in terms of bias, but with comparatively higher RMSE, especially for the most heavy-tailed distributions. As one moves further out in the tail of the claim size distribution, the quality of the estimates is reasonable except when the true distribution is log-normal or log-Gamma. As mentioned in Section 3, the main source of error in the reserve estimates from the six-parameter distribution is likely to be the estimation error, while the Monte Carlo and model error should be small. Hence, the decreased performance is probably due to increased parameter uncertainty for the smaller sample size.

Tables 7 and 8 show the bias and RMSE in the estimates of the reserve for and , respectively, when the parameter of the claim frequency distribution is and . Corresponding results for are displayed in Tables 9 and 10. We see that the reserve estimates from our model are very good, at least for all distributions but the log-normal. The six- and fiv-parameter 2 distributions perform rather well also for the log-normal claims. The four- and five-parameter distributions do not perform that well in this case, especially for the reserve. This may be due to the fact that these two distributions do not have the log-normal as a special case. When increases to , the relative performance of the applied models is similar, though the difference between them is smaller, as one would expect when one sums many independent, identically distributed variables. The results for are somewhere between those for and , and are therefore not shown here.

Results corresponding to the ones in Tables 7 to 10 for are displayed in Tables 11 to 14. The five- and six-parameter versions of our model still produce good estimates of the reserve when . The quality of the reserve estimates is also relatively good, except for the log-normal and log-Gamma distributed claims. The four-parameter distribution does not perform well in this case. When increases to , our model still gives reasonable estimates of the and reserves of the medium-tailed Weibull and Gamma claims. However, it does not perform well for claims from heavy-tailed distributions.

Thus, all in all, our model appears to capture the tail behaviour of claims from widely different distributions, ranging from the moderate-tailed Weibull and Gamma to the very heavy-tailed Pareto and extended Pareto when the amount of data is large or medium. When the sample size is small, however, our model should be used with care. For medium-tailed claim sizes, the performance seems to be reasonable, but not for heavy-tailed ones. Very large RMSEs in such cases indicate that the parameter uncertainty is huge. Further, the performance of the five-parameter 2 and six-parameter distributions is consistently better than that of the four- and five-parameter ones, even for small sample sizes. Also, the five-parameter 2 gives very similar results to the six-parameter. This indicates that the sixth parameter may not be needed, but that the fifth parameter makes a significant contribution to the model.

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.004 | 0.023 | 0.476 | 1.250 | 0.487 | 0.338 |

| L-G | -0.164 | 0.000 | 0.385 | 0.309 | 0.341 | 0.176 |

| We | -0.143 | -0.056 | 0.000 | -0.016 | -0.047 | -0.041 |

| Pa | 0.043 | 0.809 | 1.045 | 0.001 | 0.624 | 0.205 |

| Ga | -0.275 | -0.167 | 0.119 | -0.096 | 0.000 | -0.237 |

| E. Pa. | 0.004 | -0.001 | 0.120 | 0.002 | 0.001 | 0.004 |

| 4-par. | 0.008 | -0.001 | 0.001 | 0.001 | -0.001 | 0.004 |

| 5-par. | 0.007 | -0.001 | 0.039 | 0.001 | 0.000 | 0.003 |

| 5-par. 2 | -0.009 | -0.001 | 0.001 | 0.002 | -0.001 | 0.004 |

| 6-par | -0.004 | -0.001 | 0.001 | 0.000 | -0.001 | 0.003 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.071 | 0.049 | 0.477 | 1.258 | 0.489 | 0.356 |

| L-G | 0.177 | 0.043 | 0.386 | 0.324 | 0.343 | 0.207 |

| We | 0.162 | 0.077 | 0.015 | 0.097 | 0.055 | 0.139 |

| Pa | 0.084 | 0.810 | 1.045 | 0.088 | 0.625 | 0.232 |

| Ga | 0.284 | 0.172 | 0.121 | 0.137 | 0.028 | 0.265 |

| E. Pa. | 0.080 | 0.047 | 0.121 | 0.089 | 0.029 | 0.112 |

| 4-par. | 0.077 | 0.047 | 0.016 | 0.091 | 0.030 | 0.113 |

| 5-par. | 0.080 | 0.047 | 0.057 | 0.090 | 0.029 | 0.112 |

| 5-par. 2 | 0.077 | 0.047 | 0.016 | 0.090 | 0.030 | 0.112 |

| 6-par | 0.077 | 0.047 | 0.016 | 0.091 | 0.029 | 0.112 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.010 | -0.060 | 1.340 | 5.105 | 1.622 | 0.615 |

| L-G | -0.305 | 0.000 | 1.185 | 2.131 | 1.362 | 0.911 |

| We | -1.600 | -0.862 | 0.000 | -1.453 | -0.212 | -2.243 |

| Pa | -0.664 | 1.073 | 2.188 | 0.007 | 1.287 | -0.982 |

| Ga | -1.886 | -0.911 | 0.333 | -1.914 | -0.001 | -2.667 |

| E. Pa. | 0.735 | 0.013 | 0.333 | 0.008 | 0.007 | 0.020 |

| 4-par. | 0.296 | 0.013 | 0.004 | 0.009 | -0.001 | 0.021 |

| 5-par. | 0.668 | 0.008 | 0.105 | 0.018 | 0.005 | 0.014 |

| 5-par. 2 | 0.081 | 0.009 | 0.003 | 0.007 | -0.001 | 0.009 |

| 6-par | 0.028 | 0.005 | 0.003 | 0.006 | 0.000 | 0.006 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.175 | 0.104 | 1.342 | 5.132 | 1.625 | 0.680 |

| L-G | 0.354 | 0.091 | 1.186 | 2.161 | 1.366 | 0.969 |

| We | 1.606 | 0.867 | 0.022 | 1.467 | 0.216 | 2.258 |

| Pa | 0.692 | 1.075 | 2.188 | 0.320 | 1.288 | 1.025 |

| Ga | 1.890 | 0.913 | 0.334 | 1.922 | 0.044 | 2.674 |

| E. Pa. | 0.797 | 0.126 | 0.334 | 0.325 | 0.051 | 0.384 |

| 4-par. | 0.393 | 0.127 | 0.026 | 0.338 | 0.057 | 0.399 |

| 5-par. | 0.744 | 0.123 | 0.154 | 0.336 | 0.052 | 0.392 |

| 5-par. 2 | 0.279 | 0.127 | 0.026 | 0.339 | 0.057 | 0.403 |

| 6-par | 0.268 | 0.126 | 0.026 | 0.342 | 0.055 | 0.406 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.113 | 0.049 | 0.462 | 1.312 | 0.501 | 0.316 |

| L-G | -0.094 | -0.005 | 0.355 | 0.276 | 0.324 | 0.103 |

| We | -0.111 | -0.100 | -0.017 | -0.120 | -0.071 | -0.242 |

| Pa | 0.102 | 0.825 | 1.042 | -0.050 | 0.629 | 0.084 |

| Ga | -0.210 | -0.172 | 0.100 | -0.170 | -0.016 | -0.349 |

| E. Pa. | 0.145 | -0.002 | 0.102 | -0.034 | 0.010 | -0.075 |

| 4-par. | 0.123 | -0.009 | -0.020 | -0.043 | -0.041 | -0.077 |

| 5-par. | 0.079 | -0.029 | -0.003 | -0.035 | -0.031 | -0.099 |

| 5-par. 2 | 0.066 | -0.018 | -0.021 | -0.102 | -0.042 | -0.125 |

| 6-par | 0.059 | -0.016 | -0.018 | -0.078 | -0.038 | -0.131 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.719 | 0.448 | 0.551 | 1.962 | 0.666 | 1.131 |

| L-G | 0.684 | 0.439 | 0.435 | 1.005 | 0.494 | 1.060 |

| We | 0.722 | 0.507 | 0.155 | 0.881 | 0.278 | 1.111 |

| Pa | 0.688 | 0.925 | 1.064 | 0.898 | 0.694 | 0.991 |

| Ga | 0.730 | 0.463 | 0.196 | 0.923 | 0.266 | 1.122 |

| E. Pa. | 0.861 | 0.532 | 0.197 | 0.927 | 0.284 | 1.168 |

| 4-par. | 0.827 | 0.529 | 0.160 | 0.949 | 0.290 | 1.148 |

| 5-par. | 0.785 | 0.497 | 0.160 | 0.933 | 0.285 | 1.111 |

| 5-par. 2 | 0.787 | 0.522 | 0.160 | 0.921 | 0.289 | 1.121 |

| 6-par | 0.779 | 0.515 | 0.161 | 0.933 | 0.289 | 1.112 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.325 | 0.007 | 1.329 | 5.675 | 1.681 | 0.643 |

| L-G | -0.052 | 0.007 | 1.132 | 2.215 | 1.340 | 0.825 |

| We | -1.536 | -0.933 | -0.026 | -1.652 | -0.253 | -2.610 |

| Pa | -0.433 | 1.117 | 2.183 | 0.127 | 1.296 | -1.180 |

| Ga | -1.776 | -0.918 | 0.300 | -2.042 | -0.030 | -2.852 |

| E. Pa. | 1.725 | 0.140 | 0.310 | 0.394 | 0.112 | 0.231 |

| 4-par. | 1.452 | 0.266 | -0.021 | 0.594 | -0.016 | 0.445 |

| 5-par. | 0.691 | -0.006 | 0.030 | 0.280 | -0.014 | -0.187 |

| 5-par. 2 | 0.676 | 0.132 | -0.021 | -0.160 | -0.025 | -0.230 |

| 6-par | 0.318 | 0.094 | -0.013 | -0.124 | -0.023 | -0.421 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 1.841 | 0.893 | 1.491 | 8.173 | 1.993 | 2.947 |

| L-G | 1.891 | 0.939 | 1.261 | 4.298 | 1.620 | 3.392 |

| We | 2.032 | 1.235 | 0.224 | 2.443 | 0.492 | 3.317 |

| Pa | 1.941 | 1.316 | 2.209 | 3.612 | 1.371 | 2.951 |

| Ga | 2.130 | 1.137 | 0.397 | 2.595 | 0.417 | 3.377 |

| E. Pa. | 4.173 | 1.615 | 0.410 | 4.359 | 0.668 | 4.901 |

| 4-par. | 4.042 | 1.752 | 0.274 | 5.033 | 0.660 | 5.019 |

| 5-par. | 2.762 | 1.341 | 0.271 | 3.900 | 0.583 | 3.893 |

| 5-par. 2 | 2.809 | 1.494 | 0.274 | 3.444 | 0.638 | 3.935 |

| 6-par | 2.523 | 1.445 | 0.279 | 3.592 | 0.606 | 3.701 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.025 | -0.054 | 1.344 | 9.265 | 2.012 | 0.976 |

| L-G | -0.399 | 0.001 | 1.073 | 3.835 | 1.568 | 1.496 |

| We | -1.437 | -0.215 | 0.000 | -1.875 | -0.041 | -2.104 |

| Pa | -0.662 | 1.315 | 1.853 | 0.006 | 1.224 | -1.136 |

| Ga | -1.719 | -0.549 | 0.137 | -2.064 | -0.004 | -2.520 |

| E. Pa. | 1.321 | 0.018 | 0.138 | 0.009 | -0.001 | 0.038 |

| 4-par. | 0.523 | 0.018 | 0.000 | 0.024 | -0.006 | 0.046 |

| 5-par. | 1.191 | 0.012 | 0.043 | 0.028 | -0.005 | 0.034 |

| 5-par. 2 | 0.193 | 0.012 | 0.000 | 0.006 | -0.005 | 0.026 |

| 6-par | 0.097 | 0.006 | -0.001 | 0.009 | -0.005 | 0.029 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.419 | 0.250 | 1.353 | 9.329 | 2.027 | 1.181 |

| L-G | 0.587 | 0.253 | 1.082 | 3.917 | 1.585 | 1.672 |

| We | 1.487 | 0.334 | 0.120 | 1.934 | 0.182 | 2.194 |

| Pa | 0.789 | 1.337 | 1.858 | 0.652 | 1.239 | 1.302 |

| Ga | 1.760 | 0.599 | 0.184 | 2.121 | 0.177 | 2.593 |

| E. Pa. | 1.461 | 0.273 | 0.184 | 0.655 | 0.178 | 0.781 |

| 4-par. | 0.748 | 0.269 | 0.123 | 0.676 | 0.179 | 0.798 |

| 5-par. | 1.358 | 0.270 | 0.138 | 0.676 | 0.179 | 0.795 |

| 5-par. 2 | 0.562 | 0.273 | 0.121 | 0.678 | 0.179 | 0.808 |

| 6-par | 0.540 | 0.273 | 0.121 | 0.682 | 0.180 | 0.817 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.054 | -0.199 | 2.112 | 20.726 | 3.478 | 0.423 |

| L-G | -0.079 | 0.006 | 1.760 | 12.505 | 2.967 | 4.066 |

| We | -3.958 | -0.781 | 0.008 | -6.153 | -0.115 | -7.145 |

| Pa | -2.140 | 1.936 | 3.162 | 0.042 | 2.089 | -4.802 |

| Ga | -4.444 | -1.221 | 0.252 | -6.763 | -0.004 | -7.870 |

| E. Pa. | 5.122 | 0.054 | 0.253 | 0.039 | 0.007 | 0.133 |

| 4-par. | 1.809 | 0.057 | 0.009 | 0.095 | -0.005 | 0.169 |

| 5-par. | 4.536 | 0.039 | 0.082 | 0.135 | -0.004 | 0.125 |

| 5-par. 2 | 0.814 | 0.050 | 0.004 | 0.057 | 0.000 | 0.091 |

| 6-par | 0.459 | 0.033 | 0.006 | 0.076 | 0.001 | 0.106 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.663 | 0.380 | 2.122 | 20.867 | 3.496 | 1.166 |

| L-G | 0.764 | 0.346 | 1.771 | 12.669 | 2.988 | 4.335 |

| We | 3.991 | 0.846 | 0.150 | 6.189 | 0.249 | 7.194 |

| Pa | 2.241 | 1.962 | 3.168 | 1.464 | 2.103 | 4.903 |

| Ga | 4.471 | 1.258 | 0.295 | 6.793 | 0.225 | 7.909 |

| E. Pa. | 5.363 | 0.405 | 0.296 | 1.523 | 0.228 | 1.679 |

| 4-par. | 2.142 | 0.404 | 0.150 | 1.736 | 0.225 | 1.867 |

| 5-par. | 4.871 | 0.398 | 0.194 | 1.761 | 0.223 | 1.763 |

| 5-par. 2 | 1.388 | 0.412 | 0.150 | 1.764 | 0.225 | 1.909 |

| 6-par | 1.232 | 0.407 | 0.150 | 1.776 | 0.226 | 1.964 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 1.26 | -0.49 | 46.57 | 319.30 | 66.01 | 29.99 |

| L-G | -9.65 | 0.02 | 34.58 | 161.65 | 47.61 | 53.50 |

| We | -12.18 | 8.62 | 0.03 | -39.49 | 2.79 | -26.221 |

| Pa | -11.98 | 11.10 | 15.36 | 0.99 | 10.32 | -31.01 |

| Ga | -14.39 | -4.37 | 1.10 | -25.48 | 0.14 | -29.39 |

| E. Pa. | 55.84 | 0.47 | 1.02 | 1.17 | 0.08 | 1.76 |

| 4-par. | 19.15 | 0.52 | -0.11 | 1.91 | 0.07 | 2.32 |

| 5-par. | 48.58 | 0.31 | 0.49 | 2.32 | -0.01 | 1.63 |

| 5-par. 2 | 8.61 | 0.39 | -0.13 | 1.66 | 0.07 | 1.58 |

| 6-par | 5.25 | 0.23 | -0.14 | 1.80 | 0.00 | 1.49 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 20.12 | 13.65 | 47.34 | 322.21 | 67.19 | 42.76 |

| L-G | 23.02 | 13.85 | 35.57 | 166.01 | 49.17 | 63.76 |

| We | 23.60 | 16.73 | 7.84 | 45.75 | 11.27 | 40.92 |

| Pa | 23.50 | 17.85 | 17.32 | 27.93 | 15.07 | 43.01 |

| Ga | 25.362 | 14.62 | 7.93 | 36.20 | 10.89 | 44.28 |

| E. Pa. | 62.72 | 14.10 | 7.93 | 28.00 | 10.91 | 34.87 |

| 4-par. | 30.11 | 14.10 | 7.96 | 29.30 | 10.92 | 35.83 |

| 5-par. | 57.06 | 14.05 | 8.13 | 29.40 | 10.92 | 35.25 |

| 5-par. 2 | 24.55 | 14.12 | 7.98 | 29.37 | 10.93 | 36.04 |

| 6-par | 23.68 | 14.11 | 8.00 | 29.54 | 10.96 | 36.09 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 1.29 | -0.90 | 50.14 | 372.22 | 71.81 | 23.28 |

| L-G | -6.77 | -0.07 | 37.54 | 266.02 | 52.73 | 70.31 |

| We | -19.53 | 7.27 | 0.02 | -58.29 | 2.57 | -46.76 |

| Pa | -15.90 | 15.76 | 22.18 | 1.36 | 14.87 | -47.18 |

| Ga | -22.77 | -6.56 | 1.61 | -45.57 | 0.12 | -51.52 |

| E. Pa. | 88.52 | 0.49 | 1.51 | 1.70 | 0.07 | 2.49 |

| 4-par. | 25.86 | 0.51 | -0.09 | 3.53 | 0.06 | 3.70 |

| 5-par. | 75.18 | 0.30 | 0.67 | 4.06 | 0.01 | 2.46 |

| 5-par. 2 | 12.03 | 0.40 | -0.11 | 3.15 | 0.06 | 2.82 |

| 6-par | 7.43 | 0.20 | -0.14 | 3.58 | 0.00 | 2.66 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 21.14 | 14.11 | 50.90 | 375.62 | 72.98 | 39.77 |

| L-G | 23.55 | 14.34 | 38.50 | 271.57 | 54.25 | 80.64 |

| We | 28.66 | 16.48 | 8.03 | 63.08 | 11.49 | 57.03 |

| Pa | 26.54 | 21.35 | 23.68 | 32.74 | 18.69 | 56.60 |

| Ga | 31.38 | 15.77 | 8.19 | 52.80 | 11.21 | 61.88 |

| E. Pa. | 96.18 | 14.64 | 8.20 | 33.14 | 11.19 | 39.86 |

| 4-par. | 36.74 | 14.66 | 8.16 | 36.89 | 11.19 | 42.55 |

| 5-par. | 85.49 | 14.58 | 8.33 | 37.11 | 11.22 | 40.86 |

| 5-par. 2 | 28.17 | 14.65 | 8.17 | 37.06 | 11.21 | 43.02 |

| 6-par | 26.62 | 14.65 | 8.18 | 37.48 | 11.22 | 43.22 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 0.79 | 0.14 | 1.37 | 10.56 | 2.22 | 1.08 |

| L-G | 0.23 | 0.08 | 1.02 | 4.14 | 1.60 | 1.40 |

| We | -1.13 | -0.23 | -0.03 | -2.24 | -0.05 | -2.79 |

| Pa | -0.05 | 1.40 | 1.84 | 0.54 | 1.26 | -1.48 |

| Ga | -1.32 | -0.50 | 0.10 | -2.37 | -0.00 | -2.98 |

| E. Pa. | 3.66 | 0.40 | 0.11 | 1.20 | 0.13 | 0.97 |

| 4-par. | 3.10 | 0.56 | -0.02 | 1.64 | 0.06 | 1.21 |

| 5-par. | 1.59 | 0.15 | -0.02 | 0.88 | 0.04 | -0.02 |

| 5-par. 2 | 1.46 | 0.31 | -0.02 | -0.11 | 0.05 | -0.20 |

| 6-par | 0.90 | 0.26 | -0.01 | 0.06 | 0.05 | -0.52 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 4.31 | 2.51 | 2.03 | 16.10 | 3.24 | 6.59 |

| L-G | 4.44 | 2.56 | 1.72 | 9.17 | 2.71 | 7.52 |

| We | 3.81 | 2.57 | 1.15 | 5.01 | 1.65 | 6.10 |

| Pa | 4.29 | 2.87 | 2.26 | 7.67 | 2.17 | 6.36 |

| Ga | 3.90 | 2.50 | 1.17 | 5.21 | 1.66 | 6.29 |

| E. Pa. | 8.79 | 3.33 | 1.17 | 9.53 | 1.80 | 10.08 |

| 4-par. | 8.71 | 3.51 | 1.15 | 11.56 | 1.72 | 10.66 |

| 5-par. | 5.95 | 2.96 | 1.16 | 8.34 | 1.69 | 8.26 |

| 5-par. 2 | 5.96 | 3.11 | 1.15 | 7.22 | 1.71 | 8.24 |

| 6-par | 5.41 | 3.08 | 1.16 | 7.64 | 1.69 | 7.77 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 1.41 | 0.10 | 2.18 | 25.13 | 3.85 | 0.89 |

| L-G | 1.38 | 0.16 | 1.70 | 14.84 | 3.09 | 4.68 |

| We | -3.56 | -0.83 | -0.04 | -6.63 | -0.14 | -8.07 |

| Pa | -0.66 | 2.07 | 3.14 | 3.86 | 2.13 | -4.64 |

| Ga | -3.94 | -1.17 | 0.20 | -7.16 | -0.01 | -8.46 |

| E. Pa. | 14.70 | 1.25 | 0.21 | 7.89 | 0.32 | 6.33 |

| 4-par. | 12.82 | 2.03 | -0.02 | 11.57 | 0.20 | 8.24 |

| 5-par. | 6.07 | 0.61 | -0.010 | 5.89 | 0.09 | 2.45 |

| 5-par. 2 | 5.53 | 1.09 | -0.02 | 2.37 | 0.16 | 2.05 |

| 6-par | 3.82 | 1.08 | -0.01 | 2.93 | 0.14 | 1.02 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 6.97 | 3.29 | 2.99 | 39.46 | 5.22 | 10.85 |

| L-G | 8.32 | 3.50 | 2.51 | 27.20 | 4.50 | 16.41 |

| We | 5.95 | 3.31 | 1.36 | 9.05 | 2.01 | 10.80 |

| Pa | 7.67 | 3.79 | 3.54 | 24.29 | 3.06 | 11.92 |

| Ga | 6.13 | 3.24 | 1.40 | 9.37 | 2.02 | 11.06 |

| E. Pa. | 30.94 | 6.36 | 1.41 | 42.30 | 2.71 | 32.95 |

| 4-par. | 35.87 | 8.03 | 1.36 | 62.22 | 2.37 | 39.93 |

| 5-par. | 18.65 | 4.92 | 1.37 | 31.50 | 2.13 | 25.01 |

| 5-par. 2 | 17.54 | 5.56 | 1.36 | 23.48 | 2.35 | 23.98 |

| 6-par | 16.97 | 6.25 | 1.37 | 27.72 | 2.28 | 22.07 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 35.95 | 9.37 | 47.76 | 379.00 | 75.69 | 33.02 |

| L-G | 21.65 | 4.37 | 32.34 | 203.38 | 50.69 | 55.15 |

| We | 6.11 | 10.80 | -0.91 | -55.01 | 3.86 | -56.26 |

| Pa | 16.91 | 14.76 | 14.28 | 63.59 | 12.09 | -47.55 |

| Ga | 8.57 | -0.46 | -0.15 | -40.20 | 1.65 | -52.97 |

| E. Pa. | 230.25 | 16.97 | 0.02 | 164.58 | 4.95 | 100.62 |

| 4-par. | 221.97 | 25.83 | -0.47 | 279.04 | 4.26 | 143.03 |

| 5-par. | 107.65 | 7.68 | -1.03 | 113.62 | 2.71 | 82.51 |

| 5-par. 2 | 88.75 | 12.74 | -0.48 | 57.37 | 3.86 | 38.23 |

| 6-par | 97.79 | 18.13 | -0.25 | 112.87 | 3.84 | 31.50 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 205.64 | 142.70 | 97.14 | 632.16 | 142.68 | 304.37 |

| L-G | 217.06 | 143.74 | 88.36 | 489.20 | 127.64 | 360.71 |

| We | 194.86 | 149.82 | 76.73 | 233.29 | 103.96 | 292.84 |

| Pa | 209.12 | 147.00 | 79.63 | 493.96 | 105.37 | 305.72 |

| Ga | 204.40 | 146.70 | 76.95 | 251.56 | 103.61 | 310.20 |

| E. Pa. | 583.73 | 172.87 | 76.95 | 1,255.97 | 106.77 | 671.77 |

| 4-par. | 802.98 | 187.32 | 76.86 | 2,046.01 | 105.02 | 877.81 |

| 5-par. | 445.44 | 159.55 | 77.27 | 719.91 | 104.17 | 994.71 |

| 5-par. 2 | 378.09 | 164.44 | 76.85 | 552.24 | 105.09 | 564.65 |

| 6-par | 611.29 | 202.13 | 77.06 | 1,254.26 | 105.26 | 502.11 |

| Bias | ||||||

|---|---|---|---|---|---|---|

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 38.71 | 9.44 | 51.42 | 464.55 | 82.16 | 27.93 |

| L-G | 32.59 | 4.59 | 35.23 | 401.23 | 56.32 | 91.35 |

| We | -67.00 | 9.34 | -0.99 | -74.62 | 3.56 | -7.84 |

| Pa | 19.52 | 19.65 | 21.08 | 197.96 | 16.69 | -58.51 |

| Ga | 96.10 | -2.60 | 0.23 | -60.93 | 1.61 | -76.01 |

| E. Pa. | 532.12 | 23.82 | 0.44 | 640.07 | 6.21 | 303.66 |

| 4-par. | 603.33 | 44.13 | -0.53 | 1,307.18 | 5.05 | 482.09 |

| 5-par. | 331.77 | 11.94 | -1.06 | 401.44 | 2.86 | 1,632.20 |

| 5-par. 2 | 203.55 | 19.97 | -0.54 | 308.52 | 5.01 | 217.32 |

| 6-par | 831.41 | 68.95 | -0.29 | 1,279.52 | 5.52 | 250.79 |

| RMSE | ||||||

| AT | L-N | L-G | We | Pa | Ga | E. Pa. |

| L-N | 217.17 | 147.23 | 101.21 | 799.52 | 150.22 | 322.07 |

| L-G | 244.53 | 148.72 | 91.57 | 913.80 | 134.35 | 452.60 |

| We | 201.83 | 154.23 | 78.41 | 247.45 | 106.58 | 308.23 |

| Pa | 230.12 | 152.05 | 83.37 | 1,346.81 | 109.04 | 341.41 |

| Ga | 211.16 | 150.92 | 78.65 | 264.53 | 106.25 | 325.22 |

| E. Pa. | 1,523.81 | 203.41 | 78.68 | 6,470.25 | 112.34 | 1,911.60 |

| 4-par. | 3,027.09 | 262.63 | 78.54 | 12,924.03 | 108.72 | 2.84 |

| 5-par. | 2,842.04 | 173.23 | 78.96 | 2,667.00 | 106.85 | 31,310.46 |

| 5-par. 2 | 1,161.21 | 185.25 | 78.52 | 2,268.97 | 111.26 | 2,020.67 |

| 6-par | 16,704.91 | 813.31 | 78.72 | 34,387.69 | 120.78 | 1,767.23 |

5 Real data example

In this section, we will apply our model as a claim severity distribution to a set of motor insurance losses from a Norwegian insurance company. These are discussed in Bølviken [2014], and consist of claims from the years … to … The deductible is subtracted from the claims, which are given in NOK. Further, the average claim intensity is . We have fitted each of the ten distributions considered in the simulation study, and estimated the and reserves for each of them, when we assume an expected number of claims during the next year. We have also estimated the and quantiles of the claim severity distribution for interpretation purposes. Each quantile estimate is accompanied by a confidence interval obtained from bootstrap samples from the given distribution. These are compared to the corresponding empirical estimates from the data. The results are shown in Table 15.

We see that the reserve estimates from the five-parameter 2 and the extended Pareto distribution are the ones that are the closest to the empirical ones. However, the empirical estimate is within the confidence interval from almost all the distributions. The five- and six-parameter distributions all have confidence intervals that cover the empirical estimates, but the five-parameter 2 gives the estimate with the smallest uncertainty. The four-parameter distribution, on the other hand, over-estimates the two reserves. For the quantiles of the claim size distribution, the log-normal and the five-parameter 2 distribution give the estimates that are the closest to the empirical ones. All the versions of our model have confidence intervals that cover the empirical estimate of the quantile, but the four-parameter distributions significantly over-estimates the quantile, which may explain why its estimates of the reserve are too large. Further, the quantiles are over-estimated by the log-Gamma and partly by the Pareto, whereas they are under-estimated by the Weibull, Gamma and extended Pareto distributions. To test the quality of the quantile estimates, we also perform a binomial back-test. The results from the test are shown in Table 16. These confirm the impression that the five- and six-parameter distributions manage to capture the tail behaviour of the data. All in all, the five- and six-parameter distributions therefore seem to be good models for this data set, and particularly the five-parameter 2, which is consistent with our findings from Section 4.

| Quant. of severity distr. | Reserve | |||

|---|---|---|---|---|

| Distr. | ||||

| Emp | 72.5 | 139.9 | 25.9 | 26.7 |

| L-N | 73.9 (71.3, 76.5) | 140.8 (134.7, 146.9) | 26.4 (25.6, 27.2) | 27.3 (26.5, 28.1) |

| L-G | 91.7 (87.7, 96.2) | 231.4 (217.4, 247.2) | 32.8 (31.2, 34.4) | 35.8 (33.8, 38.0) |

| We | 68.5 (66.7, 70.2) | 102.2 (99.1, 105.2) | 25.7 (25.2, 26.3) | 26.5 (25.9, 27.0) |

| Pa | 74.3 (71.9, 76.7) | 122.9 (117.0, 128.9) | 25.7 (25.0, 26.3) | 26.5 (25.8, 27.2) |

| Ga | 65.1 (63.5, 66.6) | 96.3 (93.7, 98.7) | 25.6 (25.0, 26.1) | 26.3 (25.7, 26.8) |

| E. Pa. | 68.5 (65.6, 71.0) | 131.1 (121.8, 139.1) | 25.7 (24.9, 26.5) | 26.6 (25.8, 27.5) |

| 4-par. | 69.1 (65.5, 72.6) | 160.5 (144.5, 179.1) | 28.2 (26.6, 29.9) | 31.3 (28.8, 34.5) |

| 5-par. | 69.4 (65.9, 86.9) | 146.4 (130.9, 192.7) | 26.5 (24.8, 30.3) | 27.8 (25.7, 32.5) |

| 5-par. 2 | 70.3 (67.1, 73.7) | 143.0 (131.4, 154.2) | 26.0 (25.1, 27.0) | 27.0 (26.0, 28.1) |

| 6-par. | 69.6 (65.8, 84.6) | 147.9 (131.0, 185.8) | 26.5 (24.7, 29.6) | 27.8 (25.7, 31.7) |

| No. of exc. | p-value | |||

|---|---|---|---|---|

| Distr. | ||||

| L-N | 314 | 64 | 0.668 | 1.000 |

| L-G | 212 | 11 | 0.000 | 0.000 |

| We | 361 | 162 | 0.030 | 0.000 |

| Pa | 310 | 102 | 0.511 | 0.000 |

| Ga | 393 | 195 | 0.000 | 0.000 |

| E. Pa. | 361 | 85 | 0.030 | 0.012 |

| 4-par. | 355 | 43 | 0.063 | 0.006 |

| 5-par. | 351 | 58 | 0.103 | 0.453 |

| 5-par. 2 | 346 | 61 | 0.179 | 0.754 |

| 6-par. | 348 | 57 | 0.145 | 0.381 |

6 Conclusion

We propose a new class of claim severity distributions with six parameters, and show that this model has the standard two-parameter distributions, the log-normal, the log-Gamma, the Weibull, the Gamma and the Pareto, as special cases. This distribution is much more flexible than its special cases, and therefore more able to to capture important characteristics of claim severity data. On the other hand, an increased number of parameters usually leads to a larger uncertainty in parameter estimates. Therefore, we have investigated how this parameter uncertainty affects the estimate of the reserve, which is one of the nost important risk measures within non-life insurance. This is done in a large simulation study, where we vary both the characteristics of the claim size distributions and the sample size. We have also tried our model on a set of motor insurance claims from a Norwegian insurance company.

In all we simulate claim size data from ten different distributions, including the six special cases and four versions of our model, each time fitting all the ten distributions to the data. Further, we estimate the corresponding and quantiles of the fitted distributions, and also the and reserves, where the total loss distributions follows the collective risk model with Poisson distributed claim numbers. The quality of the resulting estimates is assessed by the bias and the RMSE.

The results from the study show that as long as the amount of data is reasonable, the five- and six-parameter versions of our model provide very good estimates of both the quantiles of the claim severity distribution and the reserves, for claim size distributions ranging from medium to very heavy tailed. When the sample size is small, our model appears to struggle with heavy-tailed data, but is still adequate for data with more moderate tails. The impression from the fit to the real data set is the same. Further, the performance of the five-parameter 2 distribution, obatined when the parameter is set to , is overall just as good as the six-parameter one. This sixth parameter therefore does not seem to provide a flexibility that is needed. On the other hand, the performance of the four-parameter distribution, where the parameter has also been set to , is not as consistently good, not even for smaller sample sizes. Hence, this fifth parameter really seems to improve the distribution.

The poor performance of our model for small data sets following heavy-tailed distributions is worth a closer look. Of course, estimates of quantiles far out in the right tail will inevitably be quite uncertain for such data. Still, one might obtain more reliable parameter estimates in these cases by adapting the estiamtion procedure. One could for instance try to put more emphasis on the right tail by using a weighted maximum likelihood estimator with an adequate weight function. This is a subject for further work.

7 Acknowledgements

Appendix 1

Let be the partial derivatives of with respect to which is straightforward to derive from in (LABEL:loglike1) and (LABEL:loglike2). Adding their values , and so forth over all historical losses yield the gradient vector of the log-likelihood function that can assist optimization. Introduce

and write for the so-called Digamma function. Then,

References

- Bakar et al. [2015] Bakar, S., Hamzah, N., Maghsoudi, M., Nadarajah, S., 2015. Modeling loss data using composite models. Insurance: Mathematics and Economics 61, 146–154.

- Beirlant et al. [1996] Beirlant, J., Teugels, J., Vyncker, P., 1996. Practical Analysis of Extreme Values. Leuven University Press.

- Bølviken [2014] Bølviken, E., 2014. Computation and Modelling in Insurance and Finance. Cambridge University Press.

- Box and Cox [1964] Box, G., Cox, D., 1964. An analysis of transformations (with discussion). Journal of the Royal Statistical Society, Series B 26, 231–252.

- Burr [1942] Burr, I. W., 1942. Cumulative frequency functions. Annals of Mathematical Statistics 13, 215–232.

- Embrechts et al. [1997] Embrechts, P., Klüppelberg, C., Mikosch, T., 1997. Modelling Extremal Events. Stochastic Modelling and Applied Probability. Springer.

- Lee et al. [2012] Lee, D., Li, W., Wong, T., 2012. Modeling insurance claims via a mixture exponential model combined with peaks-over-threshold approach. Insurance: Mathematics and Economics 51, 538–550.

- Lee and Lin [2010] Lee, S., Lin, X., 2010. Modeling and evaluating insurance losses via mixtures of erlang distributions. North-American Actuarial Journal 14, 107–130.

- Miljkovic and Grün [2016] Miljkovic, T., Grün, B., 2016. Modeling loss data using mixtures of distributions. Insurance: Mathematics and Economics 70, 387–396.

- Pickands [1975] Pickands, J., 1975. Statistical inference using extreme order statistics. Annals of Statistics 3, 119–131.

- Scott [1992] Scott, P. W., 1992. Multivariate Density Estimation: Theory, Practice and Visualization. John Wiley sons.