Lassoing Eigenvalues

Abstract

The properties of penalized sample covariance matrices depend on the choice of the penalty function. In this paper, we introduce a class of non-smooth penalty functions for the sample covariance matrix, and demonstrate how this method results in a grouping of the estimated eigenvalues. We refer to this method as lassoing eigenvalues or as the elasso.

keywords:

Elasso; Marc̆enko-Pasteur distribution; spiked covariance matrices; penalization; principal components; regularized covariance matrices.1 Introduction and Motivation

Principal components play a central role in many multivariate statistical methods. In working with the sample principal component roots, i.e. the eigenvalues of the sample covariance matrix, it has long been recognized that the larger roots tend to be overestimated and the smaller roots tend to be underestimated. Consequently, numerous approaches have been proposed for shrinking eigenvalues together, e.g. bias-correction (Anderson, 1965), decision theoretic (Stein, 1975; Haff, 1991), Bayesian (Haff, 1980; Yang-Berger, 1994), and marginal likelihood (Muirhead, 1982).

The aim of this paper is to study penalization methods for shrinking eigenvalues towards each other, and in particular, penalization methods based on non-smooth penalties. The rationale for using non-smooth penalty functions is that such penalization methods can not only shrink the eigenvalues towards each other, but can also result in partitioning the eigenvalues into sub-groups of equal eigenvalues, i.e. the eigenvalues are lassoed together.

Partitioning the principal component roots into distinct groups can be viewed as a model selection method, with each of the possible partitions representing a different model. Models for which the smallest eigenvalues are taken to be equal are commonly referred to as sub-spherical models, factor models, reduced rank covariance models or spiked covariance models (Anderson, 2003; Baik-Silverstein, 2006; Davis, et al., 2014; Paul, 2007; Johnstone, 2001). The more general case for which different subsets of the eigenvalues are taken to be equal are sometimes referred to as multi-spiked or generalized spiked covariance models (Bai-Yao, 2012; Mestre, 2008). Some such models yield relatively sparse covariance models. An obvious example is the case for which all the eigenvalues are taken to be equal, which corresponds to the covariance being proportional to the identity matrix. For this case, the distinct elements of a covariance matrix of order is reduced to one parameter.

The paper is laid out as follows. In section 2, regularized sample covariance matrices are first reviewed. Some general results on the uniqueness and continuity of the path for penalized sample covariance matrices based on orthogonally invariant penalties, are then given in Theorem 2.1. Also, a relationship between penalized sample covariance matrices and the estimation of covariance matrices under constrains is established in Theorem 2.2. A class of nonsmooth penalties which has the effect of lassoing the eigenvalue together are introduced and treated in section 3. In particular, Theorem 3.1 gives a closed form for the solution path of the corresponding penalized sample covariance matrices. Section 4 discusses selecting a penalty within this class of nonsmooth penalties, as well as selecting the tuning parameter for the penalty term via cross validation. Some asymptotic results are given in section 5, wherein an application of the Marc̆enko-Pasteur law is used to develop a promising choice for a penalty function. An illustrative example with discussion is presented in section 6. Proofs are given in an appendix.

2 Regularized sample covariance matrices

Let represent a -dimensional sample of size , with sample mean and sample covariance matrix . When is nonsingular, which occurs with probability one for when random sampling from a continuous multivariate distribution, uniquely minimizes

| (1) |

over all and , i.e. the class of positive definite symmetric matrices of order . The function corresponds, up to an additive constant, to two times the negative log-likelihood function under random sampling from a multivariate normal distribution. For singular , which always occurs for , the function is not bounded below. Hereafter, unless state otherwise, it is presumed that is nonsingular.

Even when , the sample covariance matrix is not very stable for small or even moderate values of . Consequently, regularized or penalized sample covariance matrices have been introduced (Huang, et al., 2006; Bickel-Levina, 2008; Warton, 2008). Since penalizing the covariance matrix does not effect the estimate for , let

| (2) |

which is uniquely minimized over at . A penalized sample covariance matrix, say , is then defined as a minimizer over of the penalized objective function

| (3) |

Here , defined on , denotes a nonnegative penalty function, with being a tuning constant. Since the function is strictly convex in , so is whenever the penalty function is convex in . In this case the minimizer is uniquely defined, with being a continuous function of .

Penalty functions which are convex in include , which arises in the graphical lasso (Friedman-Hastie, 2008), and , which corresponds to the Kullback-Liebler distance, under the multivariate normal distribution, between and . The Ledoit-Wolf (2004) regularized sample covariance matrix, defined as with being a tuning parameter, can be shown to minimize (3) when and .

The Ledoit-Wolf estimator pulls the sample covariance matrix towards the identity matrix, whereas the goal in this paper is to pull the sample covariance towards proportionality with the identity matrix, i.e. shrink the eigenvalues together. When using the penalized approach, shrinking eigenvalues towards each other without penalizing the scale of the covariance matrix implies the use of a scale invariant penalty, i.e. for and . The only scale invariant penalty which is convex in is a constant penalty. For penalties which are not convex in , the uniqueness of a solution to (3) is not immediate, nor do convex optimization methods necessarily apply.

For shrinking eigenvalues towards each other, aside from scale invariance, one may desire that the penalty attains its minimum at any , and that it be a function of only through its eigenvalues. The last property is equivalent to using an orthogonally invariant penalty function, i.e. for any , the group of orthogonal matrices of order .

Lemma 2.1

The function is orthogonally invariant if and only if for some symmetric, i.e. permutation invariant, function , , where are the ordered eigenvalues of .

Hereafter, the ordered eigenvalues of are denoted by , and the ordered eigenvalues of are denoted by . When using an orthogonally invariant penalty, the optimization problem (3) reduces to an optimization problem on the eigenvalues.

Lemma 2.2

Suppose is orthogonally invariant. Using the spectral value decomposition, express with , and where . Then

where .

Lemma 2.2 implies that the eigenvectors of the penalized sample covariance matrix are the same as those of the sample covariance matrix, with the associated eigenvalues following the same ordering. Hence, given an orthogonally invariant penalty, any solution to minimizing has the form , where with the diagonal terms corresponding to a global minimizer, over , of the function

| (4) |

Since is strictly convex and , it follows that, for any , the function

| (5) |

is strictly convex on whenever is convex, and hence it is strictly convex on the convex set . Furthermore, whenever . These observations, along with Lemmas 2.1 and 2.2, yield the following result.

Theorem 2.1

Suppose is orthogonally invariant, and , as defined in Lemma 2.1, is convex. Then the function has a unique global minimum over , specifically where is defined as in Lemma 2.2 and with the diagonal terms corresponding to the unique minimizer of (4) over . Furthermore, and are continuous functions of .

Examples of penalty functions which satisfies the conditions of Theorem 2.1 include the Kullback-Liebler penalty, since its corresponding function is symmetric and convex. A scale invariant example is the eccentricity penalty , which corresponds to the log of the ratio of the arithmetic mean to the geometric mean of the eigenvalues of . Its corresponding function is again symmetric and convex.

A problem related to the penalized covariance problem is the estimation of the covariance matrix under constrains. In particular, the next theorem establishes the following duality between the penalized problem and a constrained estimation problem.

Theorem 2.2

Assume the conditions of Theorem 2.1, and define and . For , there exists a unique solution to the problem , with the solution being a continuous function of . Furthermore, for each there exists a , and vice versa, such that . The relationship between and is given by .

3 Nonsmooth penalty functions

The choice of the penalty term and the tuning constant determines the nature and the extent to which the eigenvalues are shrunk towards each other. In this section, we study the following class of nonsmooth penalty functions which not only shrink the roots together, but generates equality for various subsets of eigenvalues for a large enough tuning constant.

| (6) |

These penalty functions are scale and orthogonally invariant and, as the following lemma shows, satisfy the conditions of Lemma 2.1. They are not differentiable in general since, although continuous, ordered eigenvalues are not differentiable functions at points of multiple roots.

Lemma 3.1

For , the function is convex and symmetric, where denotes the ordered values of .

Note that . If we had simply defined , then although it is convex, in particular linear, it is not symmetric and so does not satisfy the conditions of Lemma 2.1.

The motivation for considering the class (6) arose from first considering the special case , which corresponds to choosing . The absolute values signs in the penalty term is not, of course, necessary since for , but are included to helps relate the penalty to the penalty used in the regression lasso method. Other member of this class of penalty functions are discussed in the next section.

Using Theorem 2.1, finding the unique minimizer of over when using the penalty reduces to finding the unique minimizer of

| (7) |

subject to . To solve this optimization problems, first suppose the solution satisfies , i.e. the minimum occurs at a point where all the eigenvalues are distinct. In this case, the solution is simply the unique critical point , . If this solution does not satisfy , which will eventually occur with increasing , then the true minimizer must contain at least one multiple root.

More generally, suppose the minimum of (7) is achieved at a point where there are different eigenvalues of , say with respective multiplicities , and hence . Let denote the corresponding partition of , i.e. , with . Given the presumed multiplicities, the objective function (7) becomes

| (8) |

where and . If is the correct partition, then the minimum of (7) is obtained at the unique critical point of , which is given by

| (9) |

Again, if this solution does not satisfy , then the true minimizer does not correspond to the multiplicities implies by the partition . This implies the following condition on .

Lemma 3.2

For , the solution (9), satisfies the constrain if and only if , where

provided , and otherwise. For , the solution holds for any .

The condition is necessary but not a sufficient condition for to be the correct partition. It is possible for more than one partition to satisfy . In particular, it is always satisfied when . It remains then to find the correct partition . For a given , the minimizer of must correspond to the minimizer of for some for which , i.e.

It is not necessary to check all partitions of to find the unique minimizer of . Rather, the unique minimizer can be found by considering only the following hierarchical partitions. Let . For , it readily follows that is the minimizing partition. Next, define to be the partition formed by joining the two eigenvalues which become equal at . Continue in this fashion to produce the sequence of partitions , with . Specifically, given , define

| (10) |

where . Using this notation, we characterize the solution to minimizing in the following theorem.

Theorem 3.1

Suppose and , defined in (10), is unique for each . Then . Furthermore, for , with , , where for . Consequently, the unique minimizer to , when , is given by , where .

The conditions in the preceding theorem hold with probability one when sampling from a continuous distribution. The conditions that and be unique, though, are not necessary. They are included so that the values of are all distinct. An extension of this theorem, which is needed in later sections, is discussed in the appendix.

When using , the penalized method for estimating the covariance matrix is to be referred to as an elasso. The elasso has a number of properties similar to the lasso for regression. The estimated precision matrix is a piecewise linear function of , with the knots or kinks in the function occurring at . Hence, only the knots and the values of at the knots, together with , need to be known to reconstruct the value of for all values of . The value of the knots are easy to compute, and unlike the regression lasso, the value of at a knot has a simple closed form, namely it is a linear function of the sample eigenvalues. The knots of the elasso yield a hierarchical set of models, namely , where implies the sets in can be formed by unions of sets in . In general, for , the grouping of the eigenvalues of consists of the groups indicated by the partition .

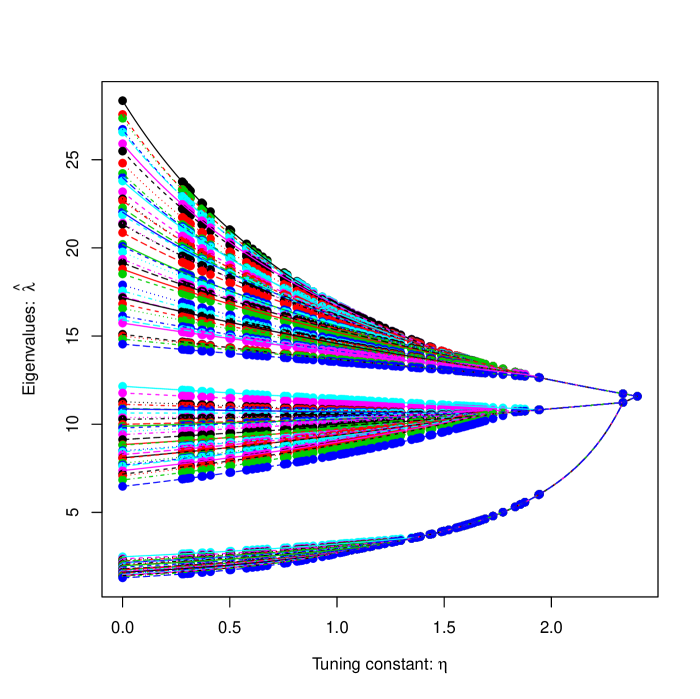

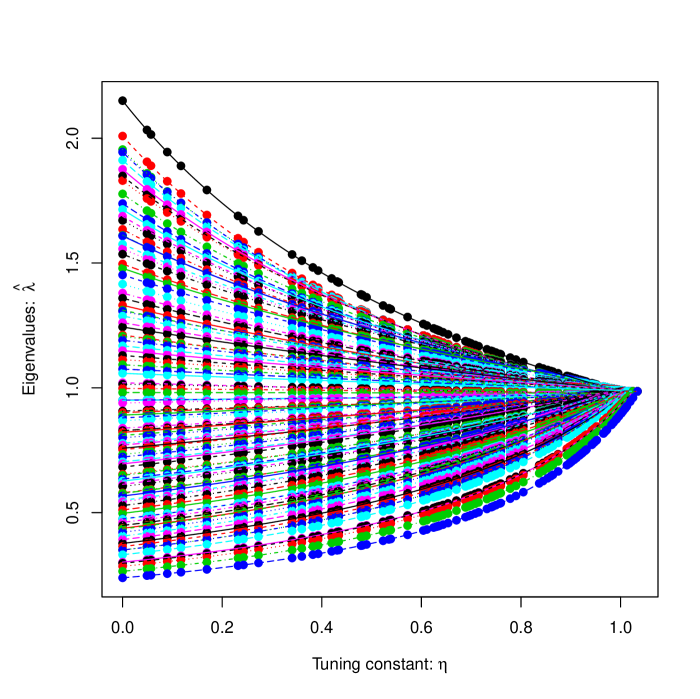

To illustrate the elasso, a pedagogical example is given in Figure 1, which shows the results from a simulated sample of size from a

dimensional multivariate normal distributions, for which the covariance matrix has eigenvalues equal to , equal to and equal to .

The choice of the weights used in the example are based upon the Marc̆enko-Pastur law. These weights are discussed in the next section,

see (11). The points displays in Figure 1

correspond to the knots where two eigenvalue groups are joined. Any eigenvalues that are joined at a given knot, remained joined for all greater

than that knot, hence producing the eigenvalue tree and paths seen in the figure. The eigenvalue tree gives possible models or grouping of the eigenvalues,

and includes the true model at the third from the last knot, i.e. the model for which the multiplicities of the eigenvalues are and respectively.

4 Tuning the elasso

4.1 Choice of weights

In using the elasso, choices for the weights and the tuning constant are needed. The choice of weights partially depends upon the particular application of interest. Consider the condition number penalty , which corresponds to , and . This penalty lassoes only a group of the largest eigenvalues together and/or a group of the smallest eigenvalues together for any fixed . This follows by noting that for , one obtains until is joined to the largest or to the smallest eigenvalue group. As the value of increases, one eventually obtains a solution with only two distinct roots. Such a solution may be of interest if one is interested in producing a double spiked covariance model with one spike representing the signal space and the other representing the noise space. The condition number has been considered by others for constraint likelihood problems (Won-etal, 2013; Wiesel, 2012) but has not been previous studied as a penalty term.

Another possible penalty term is , for which and . This penalty lassoes only a group of the smallest eigenvalues together, i.e. any fixed yields a solution for which the smallest root having multiplicity , with being an increasing function of , and for which the larger roots having multiplicity one. This follows by noting that since the weights are all equal to one, and so and cannot become equal at least until . Lassoing only the smallest roots together can be used to obtain estimates, as well as the rank of the signal space, in the single spiked covariance model or factor model.

For detecting general multi-spike models, the weights should all be different. In this case, as increase, the solutions behave in a manner similar to that displayed in Figure 1, i.e. two groups of roots come together at each knot until all roots are taken to be equal. Based on some simulation studies, the penalty , previously discussed, tends to keep the largest root separate, except for very large values of , even when the largest population root is a multiple root. A more promising penalty is the one used in Figure 1. Here, the weights are obtained by centering decreasing quantiles from the Marc̆enko-Pastur (1967) law, i.e.

| (11) |

with being the Marc̆enko-Pastur cumulative distribution function with parameter . Properties of the elasso based on this choice of weights are studied in section 5.2.

4.2 Using cross validation for choosing and for model selection

There are a number of possible strategies for choosing the tuning parameter . Here, we consider K-fold cross validation. For penalized approaches, cross validation can be applied to the unpenalized objective function, i.e. to (1) in this setting, which gives

| (12) |

calculated for a range of values (Stone, 1974; Huang, et al., 2006). Here denotes a subset of the data, with and representing, respectively, the sample mean vector and the penalized estimate of based on the data not in . K-fold cross validation then seeks to minimize over , where represents a random partition of the data into subsets of equal size, plus or minus one.

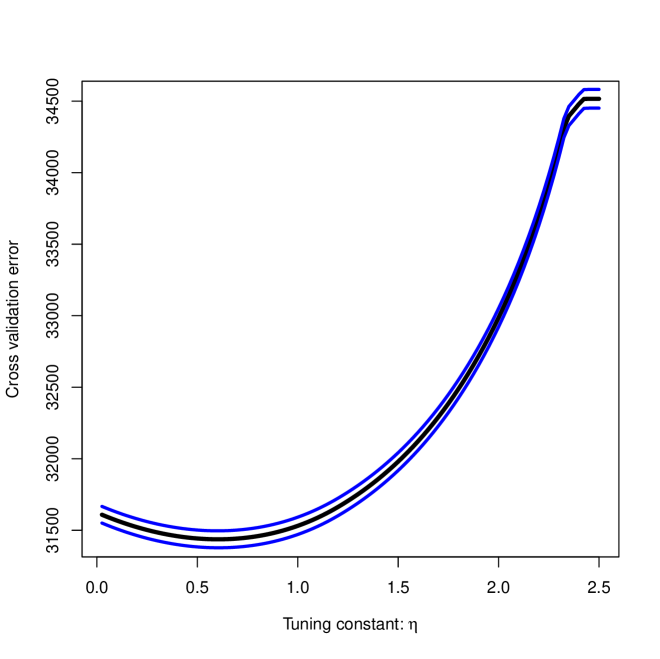

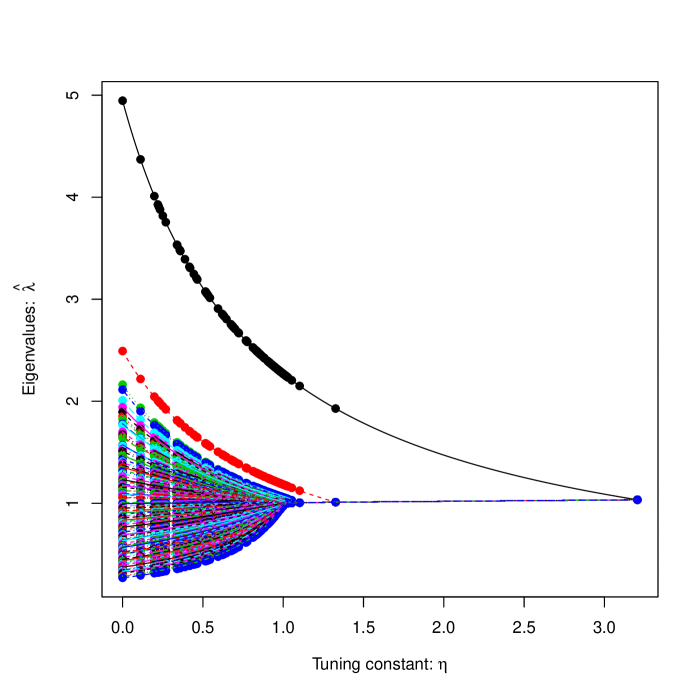

The graph on the left in Figure 2 shows the results of a ten-fold cross validation for the data and weights used in Figure 1. The middle black curve corresponds to the mean of the values of , with the blue lines corresponding to one standard error of the mean of these values. One hundred evenly spaced values between and are used for . The minimum value in the plot is , which is obtained at . Given the model used in the simulations, it can be noted that the grouping of the eigenvalues in Figure 1 at is too coarse.

In regression lasso, a “relaxed” lasso is often recommended (Meinshausen, 2007) in order to obtain a simpler model. The analogy for the elasso would be to choose a larger value of having a cross validation mean equal to the cross validation one standard error at , which in this case corresponds to . Again, this does not yield a refined enough model.

The reason why cross validation does not do well at selecting the correct model, which in this example corresponds to three distinct roots with multiplicities and respectively, is that the correct model does not arise until . At this point, although the model is correct, the roots are overly shrunk together and so the estimates of the parameters for this model result in a poor fit.

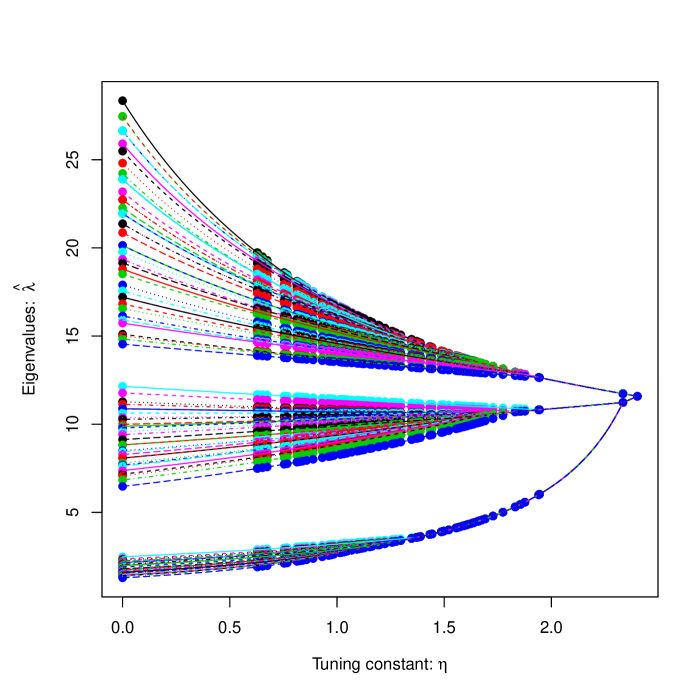

A proposed modification of the relaxed lasso is demonstrated in the right graph of Figure 2. Here, ten-fold cross validation is performed at each of the models in the elasso path, with the minimum value of the cross validation for the model being plotted versus the corresponding model knot. It can be seen, in this case, that the model with the smallest cross validation error is the correct multi-spiked covariance model.

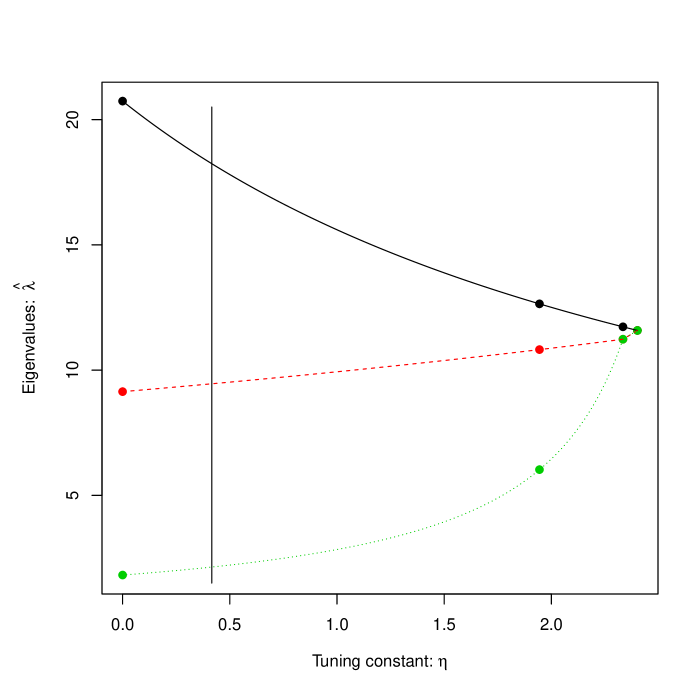

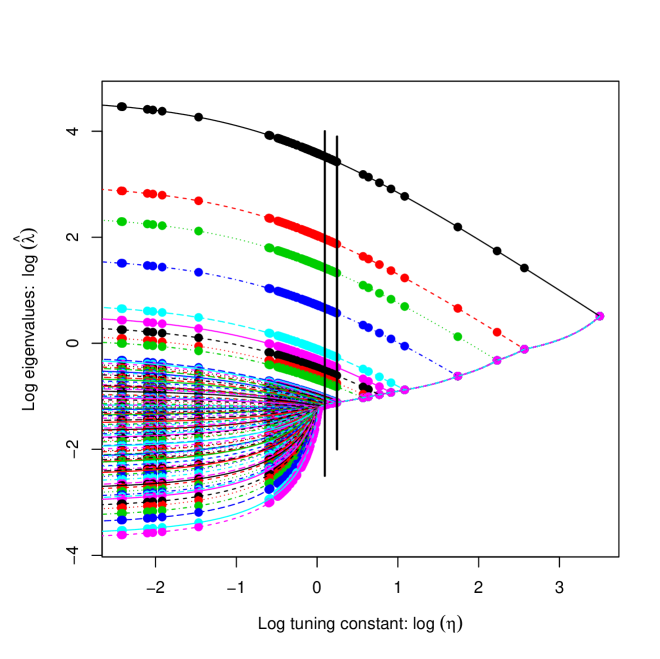

The elasso for a multi-spiked covariance model corresponding to the partition , as defined in (10), is obtained by minimizing (8) over . Theorem 3.1 readily extends to this case. The details are given in the appendix. For this case, the elasso path starts at with the value of the estimated eigenvalues corresponding to their maximum likelihood estimate at the model, namely , the average of the sample eigenvalues for each group of roots in the multi-spiked model. The elasso path is again linear in the inverse of the roots up to the knot for which the model arises, and then follows the original elasso path after the knot. Hence, the model elasso path has distinct knots. This is demonstrated in Figure 3. The left hand graph shows the elasso path corresponding to the multi-spike model given at . The right hand graph shows the multi-spike model selected via the model cross validation method, which in this case is the true model. The vertical line in the right hand graph is at , which is the value of producing the minimal cross validation error for this model. For this model, the cross validation means do not vary greatly for values of near , with the cross validation means for lying within one standard error of the minimal cross validation mean.

The computational effort for model cross validation can be greatly reduced by only considering cross validation on the more parsimonious models, i.e. on models such that , where corresponds to the value of producing the minimum for the original cross validation, which in our example is . Also, for such , we recommend that cross validation be performed only over the range . For the model and , the inverse of the roots are linear in , namely , for . So, for and over the range , rather than perform an exhaustive cross validation on the model , we recommend performing cross validation on , where is a diagonal matrix consisting of repeated times for . This will yield the same result except in the unlikely case that one of the cross validation subsets yield an elasso for which the first knot after zero occurs before . In our example, performing this approximate cross validation only for models associated with knots greater than and only over the range gives the same results as doing a complete model cross validation.

5 Some Asymptotics

5.1 Fixed dimension

Although the focus of this paper is on introducing new methodology, some basic asymptotic justification can be given for the elasso. The asymptotics as , with fixed, is relatively straightforward. If the tuning parameter as , then the penalized estimator gives a consistent estimate. In particular, when is chosen by K-fold cross-validation for the elasso, then one obtains a consistent estimate of . These assertions are stated formally in the following lemmas.

Lemma 5.1

Suppose represents a random sample from having a -dimensional distribution with mean and covariance matrix .

Let be defined as in Theorem 2.1, with the conditions of the theorem holding. Then,

a) If as , then almost surely.

b) Let be the value of chosen via K-fold cross validation, i.e.

where is a random partition of into subsets of equal size, plus or minus one. For fixed , as , almost surely.

The above lemma applies to any penalty function satisfying the conditions of Theorem 2.1, while the second lemma is stated only for the elasso. An important feature of an elasso penalty, i.e. is that it generates knots. These knots are finite for any given data set, and are random variables under random sampling. In particular, the last knot has the expression , where , , and . Under the conditions of Lemma 5.1, if follows from the consistency of the sample eigenvalues that almost surely whenever . Hence, if the tuning parameter is chosen so that under spherical multivariate normal sampling, then . Such a choice for implies, not only is consistent for any , but under multivariate normal sampling, the probability whenever is . Even under spherical normality, the distribution of is complicated. However, the distribution does not depend on the parameter , and so can be simulated using the standard normal distribution.

The problem of identifying the correct multi-spike model needs further study. As with cross validation, simulation studies imply choosing the tuning parameter in the above manner tends to yield values of which are too small to identify the correct model whenever . Using cross-validation over the models, as described previously, though, appears to have a high probability of selecting the correct multi-spike model for large . Further work is needed to formally establish this assertion. However, as stated in the following lemma, the elasso path is strongly consistent, i.e. the probability the path eventually contains the correct model as is one.

Lemma 5.2

Hence, of the possible multi-spike models, for large there is a high probability that the correct model is one of the models in the path. Note that Lemma 5.2 does not apply to the condition number penalty since in this case .

5.2 Increasing dimensions

When the sample size is small relative to the dimension, asymptotic approximations under the setting with are of interest. A classical example is the Marc̆enko-Pastur (1967) law, which states the following. Suppose represents a random sample from , with itself having identical and independent components with unit variances and finite fourth moments. Let denote the empirical distribution of the eigenvalues of the sample covariance matrix , i.e. . Under this setting, almost surely, with being the Marc̆enko-Pastur distribution with parameter and having density for , where .

A motivation for choosing the “Marc̆enko-Pastur” weights, as described previously, in the elasso is the following. The two roots joined at the first knot in the elasso are and , where corresponds to the index for which the value of is minimized, but not negative, over . Under spherical normal sampling, it would be desirable for to be purely random, i.e. uniform. Establishing such a result for given weights appears to be rather formidable. Alternatively, an approximate approach would be to choose weights so that the values of the random are nearly equal. If one could choose , then it readily follows that for . However, is random rather than constant. Under the asymptotic setting used to derived the Marc̆enko-Pastur law, it follows that if for some , then almost surely. Due to scale invariance of , this limiting result also holds whenever the assumption of unit variance is replace by any variance . For finite and , the limiting value can be approximated by , which has the same limiting value as .

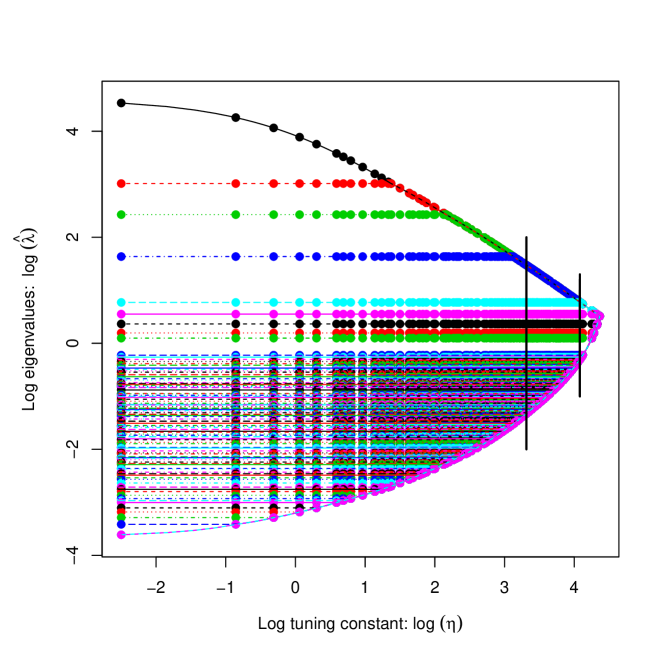

A formal study of the asymptotics in the large large setting is beyond the scope of the present paper. However, some heuristic arguments, backed by simulation studies, suggests if and as , then the largest knot almost surely when using the Marc̆enko-Pastur weights in the elasso, with the convergence to one tending to be from above. Also, for other knots almost surely for any fixed . This is demonstrated in the plot on the left in Figure 4 for the case , and . Consequently, if this conjecture holds and we choose , then the probability that the elasso solution goes to one. Choosing a fixed does not imply inconsistency for the case , which includes fixed as a special case. For the fixed case, the weights depends on , with as . So, if we standardized and express , then for a fixed , .

Results on the behavior of the knots when the true covariance matrix is not proportional to the identity can also be conjectured. An extension of the Marc̆enko Pastur law (Baik-Silverstein, 2006; Paul, 2007) states the following. Suppose represents a random sample from , and , with having identical and independent components with unit variances and finite fourth moments. Also, suppose has eigenvalues . For , if as , with held fixed, then almost surely for . Furthermore, the Marc̆enko-Pastur law applies to the distribution of the standardized smallest roots, i.e. . This suggest that if , then almost surely for , whereas for any fixed . This is demonstrated in the plot on the right in Figure 4 for the case , , , , and . If the last conjecture is true, then it implies the probability the smallest samples roots are grouped together in the elasso at , but also remain separated from the largest sample roots, goes to one provided . The last inequality holds if , where as . Consequently, under these conditions, the probability the elasso would correctly estimate , the dimension of the signal space, goes to one.

The extension of Marc̆enko Pastur law also states that if , for some , then , the maximum of the support of the Marc̆enko-Pastur law. If is the smallest for which this condition on holds, then the Marc̆enko-Pastur law holds for the distribution of the standardized smallest roots. Under these conditions, it is not possible to consistently estimate , but only . The probability the elasso based upon the Marc̆enko-Pastur weights estimates the dimension of the signal space to be then goes to one.

6 An example and concluding remarks

6.1 Telephone call centre data

As an example, we consider the call centre data previously analyzed by Huang, et al. (2006) and Fan, et al. (2009). For each weekday in 2002, except for holidays and six days when the data collecting equipment was out, phone calls were recorded from 7:00 am until midnight, resulting in a sample size of . For each of these days, the responses correspond to the number of calls received in consecutive 10 minute periods, resulting in a dimensional response vector . Since the number of calls tend not to be normally distribution, each data point is then transform to , where the operation refers to each of the elements of and . The sample are presume to be independent observations. A more complete description of the data can be found in Huang, et al. (2006).

Both Huang, et al. (2006) and Fan, et al. (2009) give penalized covariance estimates based on a training set consisting of the first data points, using different types of penalties and tuning via five fold cross validation. We refer the reader to those papers for a discussion of the penalties used within. To make our analysis comparable to these earlier estimates, we also consider only the first data points and use five fold cross validation. Note that an individual observation can be viewed as a nonstationary univariate time series of length 102. Rather than attempt to model this univariate time series, we use the elasso to try to achieve a parsimonious model for its covariance matrix. Figure 5 show the results of the elasso when using the Marc̆enko-Pastur weights and when using the weights associated with the log condition number.

For the Marc̆enko Pastur weights, the minimum 5-fold cross validation mean is , with a standard error of , obtained at (). By comparison, the cross validation mean for the sample covariance matrix is , and for the penalized estimate studied in Huang, et al. (2006) it is reported to be . For the elasso, the model at corresponds to a single spiked covariance model with the largest eigenvalues having multiplicity one, and the smallest eigenvalue having multiplicity . The minimum of the 5-fold model cross validation is , which corresponds to partitioning of the eigenvalues into groups with the largest nine eigenvalues having multiplicity one, and the smallest eigenvalue having multiplicity . If we use a relaxed lasso for this example, i.e. the largest values of for which the resulting cross validation mean is within one standard error of the value at , then one obtains a value of . This then corresponds to partitioning of the eigenvalues into groups with the largest even eigenvalues having multiplicity one, and the smallest eigenvalue having multiplicity .

For the log condition number penalty, the minimum 5-fold cross validation mean is , with a standard error of obtained at (). This result gives a partitioning of the eigenvalues into groups, with the largest eigenvalue having multiplicity , the smallest eigenvalue having multiplicity , and the other eigenvalues having multiplicity one. The minimum of the 5-fold model cross validation is , which corresponds to the partitioning of the eigenvalues into groups, with the largest eigenvalue having multiplicity , the smallest eigenvalue having multiplicity , and the other eigenvalues having multiplicity one. The results based on the log condition number give less refined results and a worse fit than the results when using the Marc̆enko Pastur weights. In general, the log condition number penalty does not allow for generating all possible partitions of the eigenvalues, only partitions of the form , and so as noted previously does not give consistent model paths in general. We recommend using the Marc̆enko-Pastur penalty over the log condition number for both the penalization problem and the dual constrained estimation problem.

By using the training set to fit the model, the remaining observation can serve as a test set. Consider partitioning the dimensional response vector into a -dimensional vector consisting of the first variables and consisting of the other variables. For , both Huang, et al. (2006) and Fan, et al. (2009) use to predict for the test set via the multivariate linear regression . The values of and are estimated from the training set using its sample mean and a penalized sample covariance respectively.

For , define the average absolute forecast error at component to be

For the sample covariance matrix, the average AAFE is . For various penalized covariance estimators, namely a LASSO, an adaptive LASSO, and SCAD, Fan, et al. (2009) reports values of , and respectively. The average AAFE for the elasso using the Marc̆enko-Pastur weights at is . Curiously, however, as increases in the elasso, the average AAFE monotonically decreases from to . The last value corresponds to using , i.e. predicting simply by its mean in the training set. This may not be unreasonable given that the 5-fold cross validation of is , which is only standard errors larger than the smallest cross validation error obtained at . Overall, the average AAFE may not be the best measure of the overall performance of a covariance estimator, since it does not take into account all of the elements of .

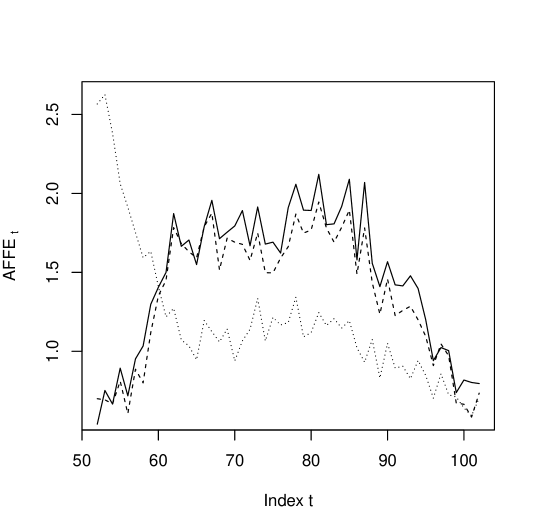

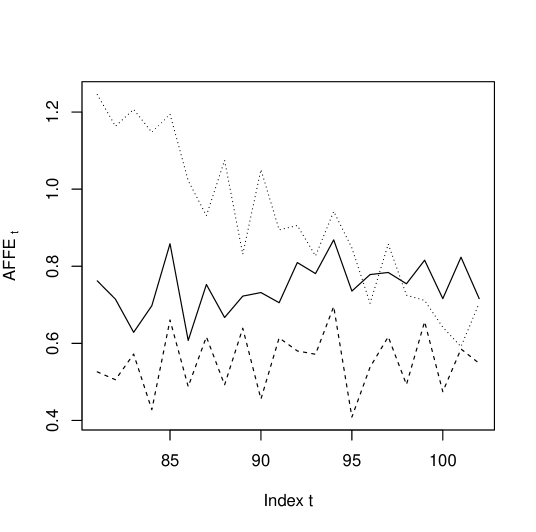

To obtain a more detailed perspective, consider the plots in figure 6. The left plot shows graphs of based on the following three estimates of : the sample covariance matrix, the elasso estimate at , and . The plot based on the elasso estimate is similar to the plot given in Huang, et al. (2006) for their penalized estimator. It can be noted from the plot that simply using the mean of the training set as the predictor gives worse predictions for but better predictions for . The right plot show the same graphs, but when using the first components to predict the last components. Note that more elements of are involved in prediction when as oppose to when . For , it can be seen that using the penalized covariance gives uniformly lower compared to the other two methods.

6.2 Discussion

The intent of this paper is to introduce the elasso method, as well as to give general results on penalized covariance matrices when using orthogonally invariant penalties. Many open problems regarding the elasso still exist. Further study as to the choice of weights for the elasso method may be fruitful, although we are fairly confident that the Marc̆enko-Pastur weights is one of the best choices. Other methods for choosing the tuning constant in the elasso is worth exploring. In particular, one could use cross validation over a different criterion. For example, for the call centre data, a cross validation method which measures the predictive ability of a subset of the variables for the other variables may be more appropriate.

Another possibility for tuning is to use an oracle method for minimizing the mean square error (Bickel-Levina, 2008) or some other measure of the deviation between and its unknown target (Chen, et al., 2011; Ollila-Tyler, 2014). Under some models, the mean square error may be greatly reduced when using an elasso estimator in comparison to the sample covariance matrix. For example, when , a properly tuned elasso will give the estimate with high probability. Under multivariate normality, and using the Frobenius norm, when one obtains , whereas . This reduction in mean square error can be attributed to using a model with only one parameter for as opposed to parameters. In general, the number of parameters for the covariance model associated with a partitioning of the eigenvalues into groups can be shown to be , where represent the cardinality of the largest group. Under the high-dimensional scenario as , the proportional reduction in parameters converges to .

An important property of the elasso is that it generates a set of hierarchical models for the eigenvalue multiplicities. Rather than use model cross validation to choose one of these models, another possibility would be to use sequential testing. That is, first consider the model , and perform a test for sphericity (Anderson, 2003; Muirhead, 1982). The classical test for sphericity is against the general alternative. Given the set of hierachical models , though, one could instead use the sequence of likelihood ratio tests for versus , versus , and so on. One drawback to such a testing approach is that the null distributions tend only to be known asymptotically, for fixed . Furthermore, as is the case for tests of subsphericity, i.e. testing if a subset of the roots are equal (Anderson, 2003; Muirhead, 1982), the sample sizes needed for the asymptotic results to provide good approximations are inversely related to the separation of the eigenvalues in the models for . There has been some recent activity in developing asymptotic result for the test for sphericity in the large , large setting (Li-Yao, 2014), but as far as we are aware these results have not been extended to the more challenging case of testing for subsphericity. From a pragmatic perspective, population eigenvalues may seldom be exactly equal. However, if the theoretical roots are distinct but not well separated enough to detect that they are distinct, then rather than focus on the individual eigenvectors, attention should be given to the joint eigenspaces associated with groups of eigenvalues which are not well separated.

Finally, we note that can be replaced by any estimator of the covariance matrix, say . For example, may be a more robust estimate of covariance matrix. In such cases, rather than associating with the negative log-likelihood function under multivariate normal sampling, one can view simply as a discrepancy measure between and , and then minimize its penalized version.

Acknowledgement

We thank Jianhua Huang and Haipeng Shen for providing us with the edited version of the call centre data used in our paper. The orginal data set was data set was made available to them by Avi Mandelbaum. An R-package to implement the elasso is currently being developed together with Klaus Nordhausen.

Appendix: Proofs and some technical details

Proofs for section 2

Proof of Lemma 2.1: Let , and denote the spectral value decomposition of by

. By orthogonal invariance, it follows

that , with being a permutation matrix. Hence, the function ,

with , is symmetric with .

Proof of Lemma 2.2: Again, express . Also, let , and define and . Since , the extremal properties of eigenvalues gives

with equality when . The lemma follows since

and .

Proof of Theorem 2.1: As previously noted, the first part of the lemma follows from Lemmas 2.1 and 2.2 and the strict convexity of . To prove continuity, we first state the following general lemma.

Lemma .1

Let be a closed subset of . Suppose the real-valued functions and are continuous on , with . Furthermore, suppose has a unique minimum in for any . If the set is compact for any , then the function is continuous for .

To prove this lemma, first note that is increasing in , and so the set is contained in the compact set . So, if , then has a convergent subsequence, say . By definition, . By continuity, the left hand side converges to and the right hand side converges to . By uniqueness, this implies . Hence, , which establishes Lemma .1.

This lemma applies to (5), for which and .

By convexity, both and are continuous. Also, the level sets of are compact since as .

Hence is continuous for , which implies the continuity of

and as functions of .

Proof of Theorem 2.2: Under the conditions of Theorem 2.1, is continuous and non-increasing with . Continuity follows since both and are continuous. To prove that is non-increasing, suppose and define, for , , and . By definition of , it follows that and , which together implies . Hence . Furthermore if , then and , which, by uniqueness, implies .

Next, for , define , and note that . It readily follows from the previous paragraph that is strictly decreasing and continuous from above. By definition, for any , and so . Hence, if , then , which implies . Since is continuous, it follows that is continuous at points of continuity of . It is also continuous at points of discontinuity of since is constant on the sets .

Proofs for section 3

Proof of Lemma 3.1: The functions are convex for , with

being linear. The function is symmetric and can be expressed as

where for and . Each of the summands

is convex, and hence is convex.

Proof of Lemma 3.2:

The inequality holds if and only if

,

which holds if and only if . Hence, the inequality holds for all

if and only if .

Proof of Theorem 3.1: By definition (10), for and for . Also, it can be shown that , for some . Specifically, , with and being defined with respect to the partition . This implies that if then . By Lemma 3.2, the former holds if and only if and the latter holds if and only if . Thus, , with strict inequality holding since it is assumed that is well defined.

As already noted, if it ready follows that . We use finite induction to complete the proof. Suppose for , we have for . It then follows from the continuity of the solution in , see Theorem 2.1, that for the solution corresponds to for . This solution also holds for any , since otherwise if was not the optimizing partition for some in the interval, then there would be a discontinuity of the solution at that value of .

Technical details for sections 4.2 and 6

Although the conditions in Theorem 3.1 that the eigenvalues of be distinct and that be unique hold with probability one when random sampling from a continuous multivariate distribution, they are not necessary. For the penalty , consider the general problem of minimizing over , where is some given matrix, e.g. the population covariance matrix. For this general case, the above conditions on may not hold. Theorem 3.1 then requires a slight modification, namely . That is, the knots of the elasso are not necessarily unique. With this modification, the statement of 3.1 holds.

If the eigenvalues of lie in distinct groups, then . For example, if , then . In general, if is not unique, but rather the infimum in its definition (10) is obtain at points, then knots occur at the same point, namely .

The above results can be applied to generating the elasso for a given multi-spike model. Consider minimizing over all for which the multiplicities of the ordered eigenvalues are respectively, with and . Let denote the corresponding grouping of the eigenvalues, and let denote the average of the eigenvalues of in the group , for . It can be shown that the solution to this problem is then the same as the solution to the problem of minimizing over where is the maximum likelihood estimate of under the model. That is, , with being a diagonal matrix with elements repeated times, for . When random sampling from a continuous multivariate distribution, is unique with probability one for and hence there are distinct knots .

Proofs for section 5.1

Proof of Lemma 5.1: Let be the unique minimum of over , or in other words, is the population or functional version of . Also, without loss of generality, assume there exists a such that .

Part (a): Consider a point in the sample space such that . If or , with possibly depending on , then it follows that . This implies , which is a contradiction since . Hence,

| (13) |

Suppose as , then by (13) it follows there exist a convergent sub-sequence, say . By definition , and . Since is continuous in all three arguments, taking limits give , and . So, . By uniqueness, this implies . Hence, since this holds for any sub-sequence and almost surely, we have

| (14) |

Part (a) then follows as a special case of (14) after noting

Part (b): For , let , and denote the sample mean vector, the sample covariance matrix and the penalized estimate respectively computed from the data not in . Observe that . Also, for , let , and note that .

Consider a point in the sample space so that and for , which by the strong law of large numbers occurs almost surely. This also implies for , and . By compactness, i.e. by applying (13) to , there exist convergent sub-sequences, say for . By definition, , which by taking the limits on both sides gives . However, since , this implies , which only holds if for . Since this holds for any convergent sub-sequences, we have for

It still needs to be shown that . To do so, two cases are considered. The first case is when is bounded. For this case, consider a sub-sequence such that . From (14), it follows that and . However, it has already been shown that and hence . Consequently, .

The second case is when is not bounded above. For this case, by (14), there exist a sub-sequence,

say , and such that .

By definition, ,

where . For this sub-sequence, , otherwise we have a contradiction, and so

. An analogous argument also gives , and since

, we have .

Finally, by definition, .

Passing to the limit gives . The reverse inequality also holds, and so .

Since this holds for any convergent sub-sequence, we have .

Proof of Lemma 5.2: Suppose has order eigenvalues with multiplicities respectively, where . Let denote the corresponding partition. So, if then . It is then to be shown that . The last statement implies convergence in probability. A stronger statement which is shown in this proof is convergence almost surely, i.e. .

Consider a point in the sample space such that . Let denote the first non-zero knot of the population elasso path , as defined in the proof of Lemma 5.1, and consider . The grouping of the eigenvalues of are still given by . Let denote the grouping of the eigenvalues of . By strong consistency (14), for large enough , , with none the subsets within containing both an element from and an element from for . That is, the groupings in correspond to unions of the groupings in . The proof can be completed then by showing the knot for large enough . From its definition in Lemma 3.2, though, it readily follows that since by assumption. So, for large enough , the grouping occurs before .

References

- Anderson (1965) Anderson, G. A. (1965). An asymptotic expansion for the distribution of the latent roots of the estimated covariance matrix. Ann. Math. Statist., 1153 - 1173.

- Anderson (2003) Anderson, T. W. (2003). An introduction to multivariate statistical analysis. New York: Wiley

- Bai-Yao (2012) Bai, Z. & Yao, J. (2012). On sample eigenvalues in a generalized spiked population model. J. Mult. Anal. 106, 167 - 177.

- Baik-Silverstein (2006) Baik, J. & Silverstein, J. W. (2006). Eigenvalues of large sample covariance matrices of spiked population models. J. Mult. Anal. 97, 1382 - 1408.

- Bickel-Levina (2008) Bickel, P. J. & Levina, E. (2008). Regularized estimation of large covariance matrices. Ann. Statist., 199 - 227.

- Chen, et al. (2011) Chen, Y.,Wiesel, A. & Hero, A. O. (2011). Robust shrinkage estimation of high-dimensional covariance matrices. IEEE Transactions on Signal Processing 59, 4097 – 4107.

- Davis, et al. (2014) Davis, R. A., Zang, P. & Zheng, T. (2014). Reduced-rank covariance estimation in vector autoregressive modeling. arXiv preprint arXiv:, 1412.2183.

- Fan, et al. (2009) Fan, J., Feng, Y. & Wu,Y. (2009). Network exploration via the adaptive lasso and scad penalties. Ann. Appl. Stat., 3, 521 – 541.

- Friedman-Hastie (2008) Friedman, J., Hastie, T. & Tibshirani, R. (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9, 432 - 441.

- Haff (1980) Haff, L. R. (1980). Empirical Bayes estimation of the multivariate normal covariance matrix. Ann. Statist., 586 - 597.

- Haff (1991) Haff, L. R. (1991). The variational form of certain Bayes estimators. Ann. Statist., 1163 - 1190.

- Huang, et al. (2006) Huang, J. Z., Liu, N., Pourahmadi, M. & Liu, L. (2006). Covariance matrix selection and estimation via penalised normal likelihood. Biometrika 93, 85 - 98.

- Johnstone (2001) Johnstone, I. M. (2001). On the distribution of the largest eigenvalue in principal components analysis. Ann. Statist., 295 - 327.

- Ledoit-Wolf (2004) Ledoit, O. & Wolf, M. (2004). A well-conditioned estimator for large-dimensional covariance matrices. J. Mult. Anal. 88, 365 - 411.

- Li-Yao (2014) Li, Z. & Yao, J. (2016). Testing the sphericity of a covariance matrix when the dimension is much larger than the sample size. arXiv preprint arXiv: 1508.02498.

- Marc̆enko-Pastur (1967) Marc̆henko, V. A. & Pastur, L. A. (1967). Distribution of eigenvalues for some sets of random matrices. Sbornik: Mathematics 1, 457 - 483.

- Meinshausen (2007) Meinshausen, N. (2007). Relaxed lasso. Computational Statistics & Data Analysis 52, 374 - 393.

- Mestre (2008) Mestre, X. (2008). Improved estimation of eigenvalues and eigenvectors of covariance matrices using their sample estimates. IEEE Transactions on Information Theory 54, 5113 - 5129.

- Muirhead (1982) Muirhead, R. J. (1982). Aspects of multivariate statistical theory. John Wiley & Sons

- Ollila-Tyler (2014) Ollila, E. & Tyler, D. E. (2014). Regularized M-estimators of scatter. IEEE Transactions on Signal Processing 62, 6059 - 6070.

- Paul (2007) Paul, D. (2007). Asymptotics of sample eigenstructure for a large dimensional spiked covariance matrix. Statistica Sinica 17, 1617 - 1642.

- Schott (2006) Schott, J. R. (2006). A high-dimensional test for the equality of the smallest eigenvalues of a covariance matrix. J. Mult. Anal. 97, 827 - 843.

- Stein (1975) Stein, C. (1975). Estimation of a covariance matrix, Rietz Lecture. 39th Annual Meeting IMS, Atlanta, GA

- Stone (1974) Stone, M. (1974). Cross-validatory choice and assessment of statistical predictions. J. Roy. Statist. Soc. Ser. B. 36, 111 - 147.

- Warton (2008) Warton, D. I. (2008). Penalized normal likelihood and ridge regularization of correlation and covariance matrices. J. Amer. Statist. Assoc. 103, 340 - 349.

- Wiesel (2012) Wiesel, A. (2012). Unified framework to regularized covariance estimation in scaled Gaussian models. IEEE Transactions on Signal Processing 60, 29 - 38.

- Won-etal (2013) Won, J., Lim, J., Kim, S. & Rajaratnam, B. (2013). Condition number regularized covariance estimation. J. Roy. Statist. Soc. Ser. B. 75, 427 - 450.

- Yang-Berger (1994) Yang, R. & Berger, J. O. (1994). Estimation of a covariance matrix using the reference prior. Ann. Statist., 1195 - 1211.