Agents’ beliefs and economic regimes polarization

in interacting markets

Abstract

In the present paper a model of a market consisting of real and financial interacting sectors is studied. Agents populating the stock market are assumed to be not able to observe the true underlying fundamental, and their beliefs are biased by either optimism or pessimism. Depending on the relevance they give to beliefs, they select the best performing strategy in an evolutionary perspective. The real side of the economy is described within a multiplier-accelerator framework with a nonlinear, bounded investment function. We show that strongly polarized beliefs in an evolutionary framework can introduce multiplicity of steady states, which, consisting in enhanced or depressed levels of income, reflect and reproduce the optimistic or pessimistic nature of the agents’ beliefs. The polarization of these steady states, which coexist with an unbiased steady state, positively depends on that of the beliefs and on their relevance. Moreover, with a mixture of analytical and numerical tools, we show that such static characterization is inherited also at the dynamical level, with possibly complex attractors that are characterized by endogenously fluctuating pessimistic and optimistic levels of national income and price. This framework, when stochastic perturbations are included, is able to account for stylized facts commonly observed in real financial markets, such as fat tails and excess volatility in the returns distributions, as well as bubbles and crashes for stock prices.

Keywords: complex dynamics; bifurcations; multistability; market interactions; heterogeneous beliefs.

The 2008-2009 crisis stimulated new reflections on the origins and the

causes of turmoil in the economic environment. Accordingly, it turned

out to be relevant the understanding of how instability can reinforce

and spread among different sectors, and of what are the factors that may

hinder their interaction. As a consequence of such complexity, agents

populating the economic system are often better represented as

boundedly rational actors, mispricing risks and inappropriately evaluating the

economic variables. This is usually at the source of

instabilities, that can make the economic system evolve in

unpredictable ways, especially when non-deterministic components are

acting.

The research goal of the present paper is to improve the

understanding of the effect that a biased evaluation of the economic

variables may have on the resulting economic dynamics and of whether an

increase in the integration between the real and financial sectors is harmful or

beneficial to the economy. Relying on analytical investigations

complemented by numerical simulations, we study how a boundedly

rational agents framework can give rise to multistability phenomena in the

economic system, and how the eventual related instability may spread

between the integrated markets.

1 Introduction

Seeking the explanations of the 2008-2009 crisis only within the real

or the financial side of the economy leads to a dead end way. The

global response to the crisis in the form of fiscal stimulus indeed

awakened the interest in the multiplier-accelerator approach dating

back to [26], from which the modern business

cycle theory originated. According to this scheme, endogenous

fluctuations spring in the economic activity as a consequence of the

mutual interplay between consumption, investments and national income

changes, driven either by a multiplicative component that links

expenditures to national income (the so-called Keynesian multiplier)

or by the principle through which induced investments depend on the

pace of growth in the economic activity (the accelerator

principle). The original model of [26] has been refined

and developed through the decades, emphasizing from time to time

different aspects, ranging from the role of the monetary sector or of the

inventory adjustment to that of expectations in the national income,

or to the effect of bounded investment functions. A burgeoning

literature has been widely disseminating: we just mention

the contributions in [7, 13, 14, 20, 24, 25].

However, the increasing relevance and influence of the financial side

of the economy on the real sector (the so-called phenomenon of

financialization of the real economy) can not be neglected,

with the consequent need to investigate the interactions between the

real and stock subsystems. The related literature can be roughly

divided into two research strands, where the former sustains and

describes the reverberations of the financial sector into the real one

(as in [6, 19, 21, 28]), while the latter, on the

contrary, contains a support for the opposite influence direction (see

e.g. [1, 18, 19, 21]).

In the wake of the aforementioned discussion, the recent financial crisis strengthened the need to understand the causes of turmoil in the economic environment, keeping a focus on the role of the financial system. Among several factors, a systematic mispricing of risk is commonly regarded as one of the underlying sources of instability for the economic environment. The presence of such a bias, indeed, reflects a boundedly rational behavior of the involved economic actors, who may have a rough knowledge of the economic fundamentals. This can lead agents to systematically overestimate or underestimate them, and to possibly stick to or switch among different forecasting rules on the basis of simple heuristics. It is well-known (see [14]) that bounded rationality together with heterogeneity is a potential source of endogenous fluctuations in the dynamics of the relevant economic variables. An interesting consequence of this modeling framework is also the capability to exhibit simulated time series characterized by several qualitative properties, as leptokurtic returns distributions, large and clustered volatility, that are distinctive features of real time series.

The present contribution belongs to the research strand on the

study of interacting markets, and embraces a modelling approach similar

to those adopted in [4, 23, 28]. In particular, in each of

these works, the sources of complex dynamics are always clearly linked

to and explained through particular mathematical phenomena occurring

in the model.

For example, in [28] a Keynesian-type goods real

market is combined with a stock market populated by heterogeneous

fundamentalist and chartist agents. The main result is that the system

is characterized by different coexisting steady states, that can

become unstable and give rise to complex dynamics. From the

mathematical point of view, we have persistent multistability of

stable steady states or of attractors characterized by similar degrees

of complexity.

Conversely, in [23] it was deeply investigated

the effect of coupling either stable and unstable isolated real and

stock markets. In this case, a Keynesian good market interacts with a

stock market characterized by optimistic and pessimistic agents, whose

fractions can change over time according to an evolutionary switching mechanism.

Surprisingly, instabilities

can not only spread from one market to the other, but they can even arise by increasing

the level of interaction between markets that are stable

when isolated. From the mathematical viewpoint, this is explained

investigating the loss of stability and the kinds of consequent

dynamics arising, depending on the degree of interaction or on the

degree of optimism/pessimism. Moreover, the analysis of the resulting

time series of the economic variables shows a significant deviation

from normality.

The work in [4] provides evidence that even a potentially stable

economic system can show endogenously fluctuating dynamics, since a

locally stable steady state can coexist with other complex

attractors, so that the long-run dynamics are strongly path-dependent

and can result in sequences of alternating periods of persisting large or small volatility.

In all the above-mentioned papers, the agents’ heterogeneity and their

boundedly rational nature have no effects on the set of possible

steady states, which always consists of a unique steady state

([23, 4]) or of three coexisting steady states

([28]).

However, it is reasonable to wonder whether the boundedly rational

nature of the agents can also affect the final outcomes of the system

in terms of existing steady states and their position. In other words,

we are interested in inquiring if, as a consequence of a biased

evaluation of economic variables, “biased” steady states can

emerge. For example, may an excess of optimistic/pessimistic bias

foster the emergence of “optimistic” and “pessimistic” steady

states, which, in turn, can evolve into optimistic and

pessimistic complex attractors? Additionally, to which extent the

birth of biased steady states is affected by the markets’

integration?

In order to investigate these aspects, building on the approach pursued in the above mentioned contributions, we analyze an economy made by two, possibly interdependent, subsystems, namely a real and a financial sector. The real sector essentially recalls the economy presented in [4] and [24], in which a multiplier-accelerator model with a bounded investment function is studied, and it is coupled with a stock market populated by optimistic and pessimistic fundamentalists, modeled by following the approach in [23]. In so doing, we shall focus our attention on the degree of interaction between markets, which positively depends on the parameter as well as we shall take into account the role of agents’ beliefs, represented by a symmetric optimistic/pessimistic bias and their willingness to switch toward the best performing strategy while operating in the stock market, described by the so-called intensity of choice (see e.g. [14]) that regulates the evolutionary selection between forecasting rules. The resulting dynamics are described by a three-dimensional nonlinear system of difference equations for which we analyze the existence and the stability of steady states and, through global analysis, we investigate the presence of multistability phenomena.

The results we come up with can be read under different

perspectives. Our most relevant finding concerns the

static analysis of the set of possible steady states. We show that,

independently of the structural features of the sectors under

consideration and of their degree of integration, the steady state final

outcomes depend on the optimistic/pessimistic bias and on the

intensity of choice of the evolutionary process. If both and

are suitably small, a unique steady state exists, whose

position is independent of and Conversely, if either

or increases, two new biased steady states emerge,

whose position depends on such parameters and which coexist with the

previous one. With respect to it, the two new steady states respectively exhibit larger or

smaller values in the level of national income and price. This means that

in some sense, such final outcomes “keep track” of the

optimistic/pessimistic biased belief of the agents, and depart from the unbiased equilibrium.

The intuition for the existence of these biased steady states can be read as follows: when the realizations of the true fundamental value of the traded asset are close to some biased beliefs, if the intensity of choice is high enough, then almost all agents will adopt the optimistic or pessimistic predictor, which is the best performing predictor in terms of forecasting error, leading the dynamics to converge to a biased equilibrium. In the same way, when the intensity of choice is sufficiently large, even small differences in predictors’ performances may lead agents to massively switch among forecasting rules. Such alternating waves of optimism and pessimism can drive the system to periodic cycles.

From the mathematical viewpoint, the emergence of additional steady states

follows a pitchfork bifurcation, whose consequent multistability

is further investigated through global analysis, in order to have a

complete picture of the possible dynamical scenarios. The

independence of the emergence (but not of the position) of the biased steady states from makes possible that the same economic

setting can simultaneously take advantage or be hindered from

isolated or fully integrated markets, with a consequent increase in

the level of national income and prices, or, conversely, a

reduction in the level of national income like, for instance, during a

financial shock within an integrated system. The latter framework can

be read in the wake of the recent financial crisis where, if on the one

hand an integrated economy may facilitate exchange and production

through the intermediation of financial instruments, on the other hand

no real benefits to the society deriving from the activities of

increased financialization may be appraised.

Carrying on the investigation and moving to a dynamical perspective, the analysis we perform allows us to determine the local stability conditions for each steady state, from which we infer a possible ambiguous role for each relevant parameter. Deepening the investigation with the help of numerical simulations, we show that periodic, quasi-periodic and complex dynamics can occur, from a global viewpoint, either when a unique or three steady states exist. Accordingly, oscillations arising in our model are endogenously generated and stoked by the acceleration principle acting in the real subsystem which, in turn, may be triggered by the nonlinearity of the real subsystem, as found in [24] too. In addition, we show the possible coexistence of pairs of complex attractors, arising by the loss of stability of the two new steady states, which give rise to endogenous fluctuations around either the pessimistic or the optimistic steady state. We also find that, even when the fundamental steady state is locally stable, other attractors may coexist with it, making the choice of initial condition crucial for the course of the resulting economic dynamics. Dealing with a purely deterministic version of the model, the convergence toward a particular attractor is determined in advance by the choice of the initial datum. Conversely, when a stochastic version of the model is considered, in which the agents’ demands are buffeted with noise, trajectories can approach different attractors from time to time, so that, for example, periods of persistent optimistic and pessimistic fluctuations can interchange, giving rise to alternating booms and busts. In general, the emergence of stylized facts is mathematically connected with an increasing complexity of the generated dynamics. On the contrary, we show that this is possible in our model even in the presence of stable steady states, when the pitchfork bifurcation occurs. That level of investigation turns out to be relevant to reproduce realistic dynamics observed in the real financial markets together with several stylized facts regarding the return of stock prices (and output as well), such as positive autocorrelation, volatility clustering and non-normal distribution characterized by a high kurtosis and fat tails, with dynamics resulting from the combination of nonlinear forces and random shocks. Therefore, the analytical and numerical results we retrieve from the deterministic framework flow into a better understanding of the stochastic framework.

To summarize, a growing polarization of beliefs gives rise to an increasing richness in the economic regimes that may originate due to the evolutive framework. In such regimes the optimistic and pessimistic hallmark of the belief is not lost but it is mixed up by the complexity of the scenarios, and marks the emerging regimes which are characterized by low, medium or high levels of economic activity.

The remainder of the paper is organized as follows: Section 2 describes the model economy highlighting the features of the two markets; in Section 3 we present the analytical results on the steady states and their local stability; in Section 4 the simulations regarding the deterministic framework as well as the stochastic version of the model are performed and analyzed; in Section 5 we draw some conclusions on our findings; the Appendix gathers all the proofs.

2 The model economy

In the present section we shall introduce the baseline model made up of two interacting sectors, i.e., the real market and the stock market, which are separately outlined in the following subsections. Since the real market we consider essentially consists in the same closed economy taken into account in [4], while the stock market is very close to that depicted in [23], we limit ourselves to report the constitutive and distinctive elements of each market, addressing the interested reader to the above-mentioned works for a more detailed description. In what follows, we are making use of sigmoid functions, namely functions that satisfy the following assumptions:

| (1a) | ||||

| (1b) | ||||

| are bounded above and below. | (1c) | |||

2.1 The real market

As usual, at each time the national income can be expressed through the macroeconomic equilibrium condition

| (2) |

in which we assume constant exogenous government expenditures and aggregate consumption depending on autonomous consumption and on the last period national income, setting where represents the marginal propensity to consume. Private investments are expressed through

| (3) |

where are exogenous investments, while the last two terms

respectively encompass the accelerator principle and the dependence of

the real market on the stock sector, with

representing the degree of interaction between the two markets,

the marginal propensity to invest from the stock market wealth and

the price of the financial asset. As noted in [28], a

better performance of the financial side of the economy, here

encompassed in has a beneficial effect on the patrimonial

situation of the private sector, promoting greater investments.

Concerning the second term, is the accelerator parameter

and is a function that satisfies

assumptions (1). Thanks to assumption (1a), if the

national income raises or decline, after a gestation lag, the

component of investments depending on national income variation

increases or decreases accordingly, by a bounded

quantity, thanks to assumption (1c). Finally, thanks to

assumption (1b), the effect of both positive and negative

national income variations are less and less significant as

attaining its

maximum at where the slope coincides with

accelerator We stress that all the previous aspects are in

line with the classic macroeconomic literature of the 1930s-1950s (see

e.g. [12, 15, 16]).

Taking into account the expressions for the government expenditure, aggregate consumption and private investments, from (2) we obtain

where we defined as the sum of the autonomous components. We stress that if the stock market has no influence on the national income, while if the two markets are fully integrated.

2.2 The stock market

We assume that the stock market is populated by fundamentalists, who buy (sell) the asset if its price is lower (higher) than the value estimated as the fundamental asset price but, due to some form of bounded rationality, do not know the true fundamental value of the asset price, trying to form forecasts about it. On the basis of these beliefs, they operate in the stock market. In particular, we suppose there are two groups of fundamentalists: optimists, who typically overestimate the true fundamental asset price, and pessimists, who underestimate it. This approach has been adopted before in [8] and [14], assuming that optimists (resp. pessimists) expect a constant price above (resp. below) the fundamental price. The asset price is set by a market maker on the basis of the following nonlinear adjustment mechanism

| (4) |

where represents the fraction of optimistic fundamentalists, and denote optimistic and pessimistic demand, respectively, while measures the reactivity of the price variation to aggregate excess demand and is a function fulfilling assumptions (1). We stress that a similar price adjustment mechanism has been deeply investigated in [22], where it was introduced to prevent an overreaction of price variation to a large excess demand with the consequent unrealistic uncontrolled growth or negativity of prices. In the present contribution, an overreaction would also lead the real sector variables to diverge or to become economically meaningless.

The demand of optimistic and pessimistic agents is proportional to the

gap between the estimated fundamental asset price and the realized

price, i.e.,

where represents the agents’ reactivity to such gap. In an

environment in which agents, due to their bounded rationality, roughly

know the fundamental stock price, they can disagree about the correct

value of the fundamental price and can make different estimates on it. In particular, we assume that

and where

is a positive parameter representing the bias on the

fundamental price. On raising agents become more and more

distant in their beliefs, which are increasingly polarized

toward high level of optimism/pessimism. Hence, parameter

also portrays the degree of agents’ heterogeneity555As

it will become evident along the paper, is one of the

most relevant parameters from both the interpretative and the

mathematical point of view. To keep the investigation analytically

tractable and the interpretation more straightforward, we decided

to limit ourselves to

consider the symmetric situation in which and lie at the same distance

from .

As concerns the true, unobserved, fundamental value it is described by a

weighted average between an exogenous fundamental value and an

endogenous component proportional to the national income

resulting in where

captures the strength of the linear dependence between the

fundamental value and the current national income level. In

this way, is linked to the course of the real economy

through i.e., the interaction degree intensity

parameter which has been introduced for the investments’ function in

(3). It is worth noticing that if the true

unobserved fundamental value is completely exogenous, while if

it is endogenously

determined by national income, as in [28].

Therefore, the demand functions for both optimists and pessimists become

and, replacing them into the price equation (4), we obtain the following expression for the price dynamics

In order to discipline the evolution of the agents’ share employing a certain speculative rule, we assume that a fraction of optimistic agents can switch from period to period to the other behavior, and vice versa. In the present model, differently from [23] and similarly to [5], such an evolutionary process is governed by the squared forecasting error evaluated on the last realization of the fundamental value and of the stock price, namely

Following [2], we assume the fractions evolve according to a multinomial logit rule, that is

where the positive parameter also called intensity of choice, measures how fast the mass of optimistic fundamentalists will switch to the optimal prediction strategy. In the limit case , fractions will be constant and equal to 0.5, and traders never switch strategy; in the other extreme case , in each period all traders use the same, optimal strategy. The latter case represents the highest possible degree of rationality with respect to strategy selection based upon past performance in a heterogeneous agents environment (see [14] for further discussion on the topic). Moreover, also encompasses the agents’ perception of the beliefs relevance. Independently of the moderate or strong polarization of the beliefs (small or large value of ), if the agents give a small relevance to them ( is small), they will more likely stick to their current forecasting behavior, while if they give a serious consideration to them ( is large), their tendency to trust and switch to the best performing belief will result strengthened.

In so doing, the equation that describes the dynamics of the asset price reads as

Summarizing, defining in view of the subsequent analysis and taking into account both the real and financial sectors, we can introduce the function which describes the functioning of the whole economy:

| (5a) | |||

| (5b) | |||

| (5c) | |||

where

3 Analytical results on steady states and their stability

In this section we investigate the existence of equilibria for the model in (5), studying the effect on the position and on the stability of the steady states played by the relevant parameters, paying specific attention to the role of the intensity of choice of the bias and of the interaction parameter We start by investigating the number and the expression of possible steady states of the map in (5).

Proposition 1.

System (5) has

-

a)

a unique steady state if

(6) Such steady state is well defined for any interaction degree value provided that

(7) -

b)

three steady states and if In particular, and are symmetric w.r.t. which is still well defined for any provided that (7) is fulfilled. Moreover, it holds that for and

(8) All the components of such new steady states are strictly positive if

(9)

From Proposition 1, it is possible to have either one or three steady states, whose existence is triggered by sufficiently large values of and Steady state in which reduces to the same steady state of the Samuelson model when is in agreement with those found in [4, 21, 23], so that all the comments therein apply to as well.

We stress that the steady state represents an unbiased final outcome of the economic system, since it is affected neither by the bias, nor by the evolutionary pressure. Conversely, suitably strong beliefs (namely a suitably strong joint effect of belief polarization and relevance given to them by the agents) trigger the emergence of the two supplementary biased steady states and Moreover, recalling (8), consists in intermediate steady price and national income levels, while and represent polarized steady states, with respectively small and large steady values. Proposition 1 then shows that sufficiently strong beliefs can drive, independently of the economic setting and its features, the system toward optimistic (like ) or pessimistic (like ) steady states. This result is absent in the related literature, where the only possibilities are given either by a unique steady state ([4, 23]) or by always existing multiple steady states ([28]), which are then independent of the underlying characteristics of the economy and of the agents. In agreement with a Keynesian line of thought, Proposition 1 clearly shows how beliefs, influencing the stock market performance that, in an integrated framework, has in turn a direct influence on the investments, can be the essential cause and driving force that introduces and leads to final outcomes consisting of persistent flourishing or depressed income levels. The optimistic/pessimistic polarization of beliefs, under the evolutionary perspective, reflects on the “sentiment” of the steady states, and can drive the dynamics of the economy toward a more optimistic or pessimistic final output. We stress that also in such situations, the intermediate outcome is still relevant, as it will become evident from the dynamical analysis, while in [28] it attracts just a set with null measure.

We recall that encompasses the boundedly rational nature of the agents, while the presence of the switching mechanism, that is crucial as well, is regulated by the parameter , that is positively connected to the rationality of the agents in the selection of the forecasting rule, as the larger is the intensity of choice, the larger is the fraction of agents that “rationally” turns to the speculative rule that proved to be the most effective in forecasting the actual stock price. In this sense, we can say that the emergence of the pessimistic and optimistic steady states is fostered by the joint action of an irrational component () and of a rational component () in agents’ behavior. The roles of and which we already noted to be very interconnected from the interpretative point of view, can not be completely disentangled also from the mathematical viewpoint, and we will see that both parameters have a similar influence on the results.

From (8), the optimistic or pessimistic divergence of the biased steady states from the unbiased one is potentially more relevant as the polarization of the beliefs increases. Our next level of investigation is then devoted to study the effect of the main parameters on the steady states position. Since and has not its own relevance from the economic point of view, we do not deal with it, recalling, however, that it behaves exactly as

In order to have the steady state well defined for any

interaction degree value in the remainder of the

paper we shall assume that (7) is fulfilled, even when not

explicitly mentioned, as well as we also assume (9) when

dealing with and , to guarantee the economic meaningfulness

of each

steady state value.

In the following comparative static result, we investigate the effects

of and on the steady state values and

Proposition 2.

Under assumption (7), remains

unchanged on increasing or

Let Then, on increasing we have that

and are strictly increasing, while and are

strictly decreasing. Moreover,

and

and

with and representing respectively the lower and upper bounds defined in (8).

On increasing

we have that and are strictly increasing, while

and are strictly decreasing.

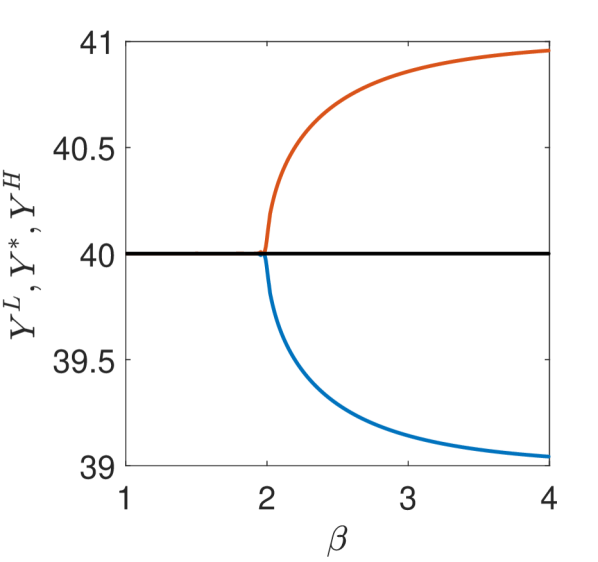

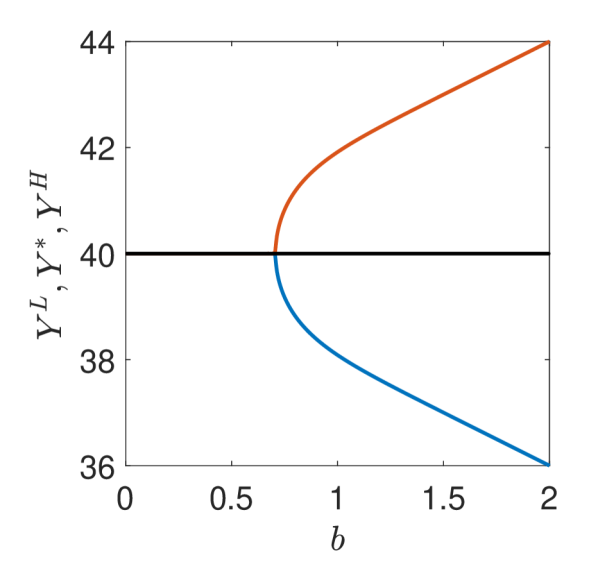

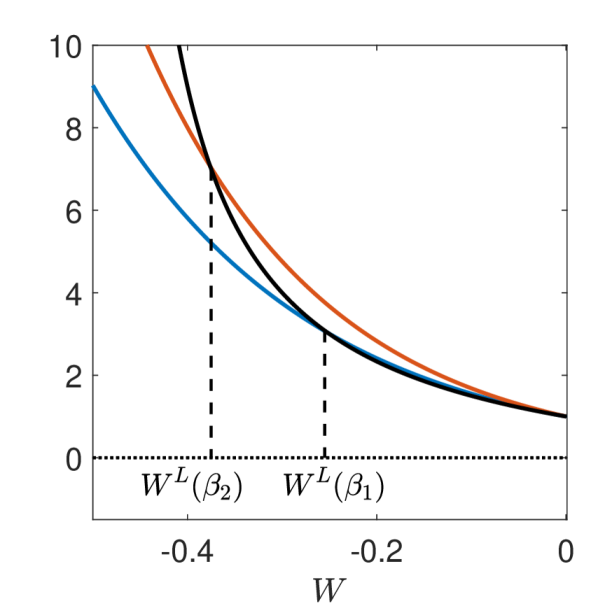

The comparative static results of Proposition 2 deepen the understating of the effect of the beliefs on the steady states. In Figure 1 we report the evolution of and on increasing and setting and (Figure 1 (A)), (Figure 1 (B)). The values of and are obtained numerically solving an implicit equation similar to (17), but in terms of using (16). Indeed, is neither affected by the intensity of choice nor by the bias. Conversely, not only the existence of and is affected by and but also their values, and in particular their departure from the intermediate steady state This means that the stronger are the beliefs (in terms of polarization or intensity of choice), the stronger get the optimistic/pessimistic connotation of the possible final outcomes. In agreement with (8), the maximum possible deviation of and from is proportional to the belief polarization and the bounds for and can actually be approached as , that is agents immediately switch to the best performing behavior as if “perfectly rational”.

(A)

(B)

The next proposition studies the effects of on the steady states.

Proposition 3.

Under assumption (7), on increasing

can be either increasing, decreasing or there exists

such that decreases on

and increases on

On increasing

can be either increasing or there exists

such that increases on

and decreases on

Let and assume that

| (10) |

Then, on increasing we have that, for can be either increasing, decreasing or there exists such that decreases on and increases on On increasing for can be either increasing or there exists such that increases on and decreases on

(A)

(B)

(C)

The previous proposition shows that the effect produced by the degree of interaction between real and stock markets on the steady state values can be quite ambiguous. Since the value of is the same as that resulting in [4] in the case of exogenous government expenditure, the unbiased steady national income is either increasing or concave unimodal, reaching a greater value in the case of completely integrated markets than in that of isolated ones (see [4]). Additionally, both optimistic and pessimistic steady national income can be either increasing or concave unimodal as well.

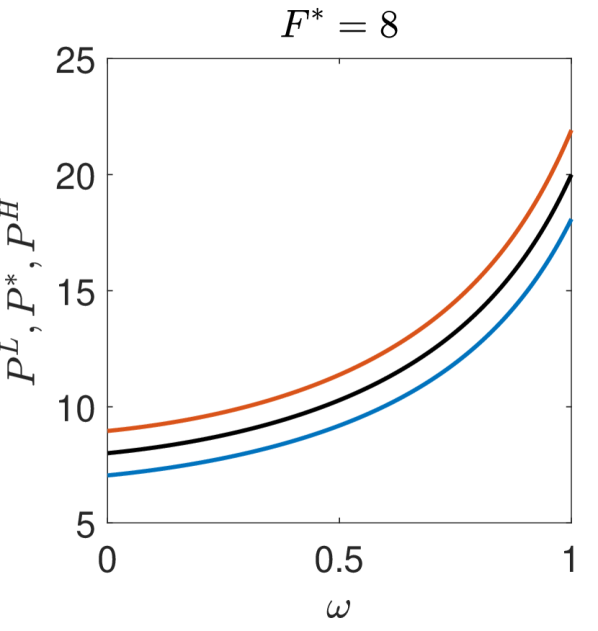

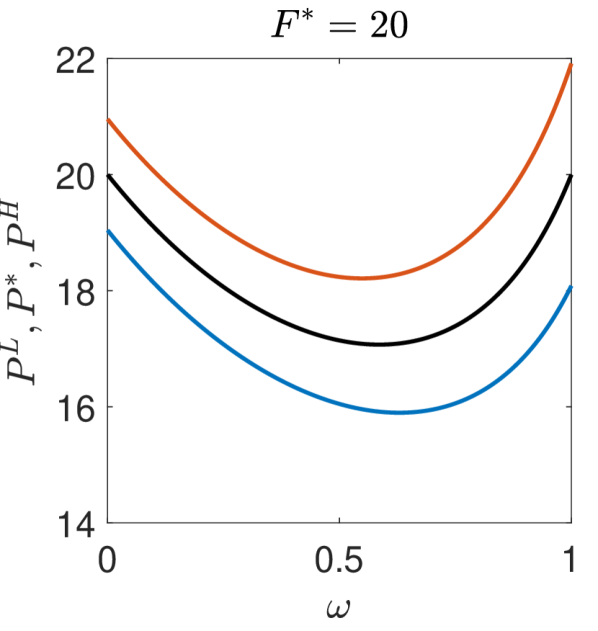

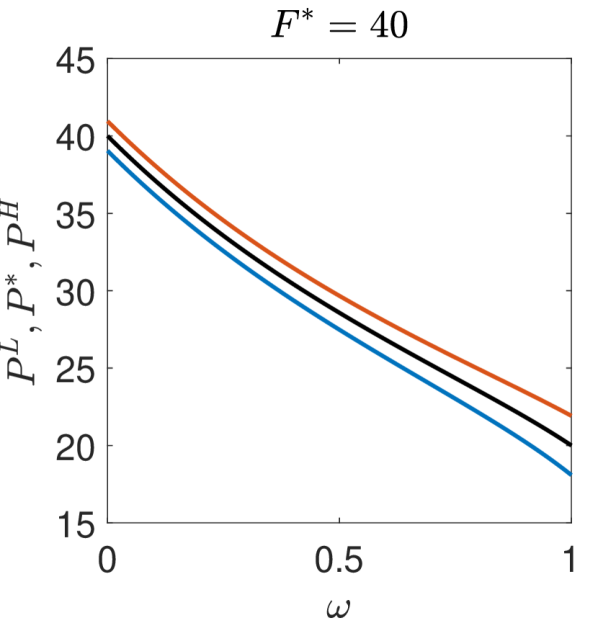

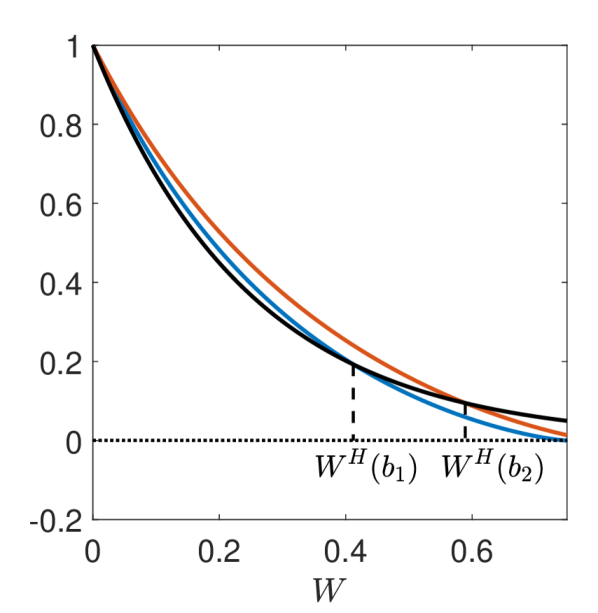

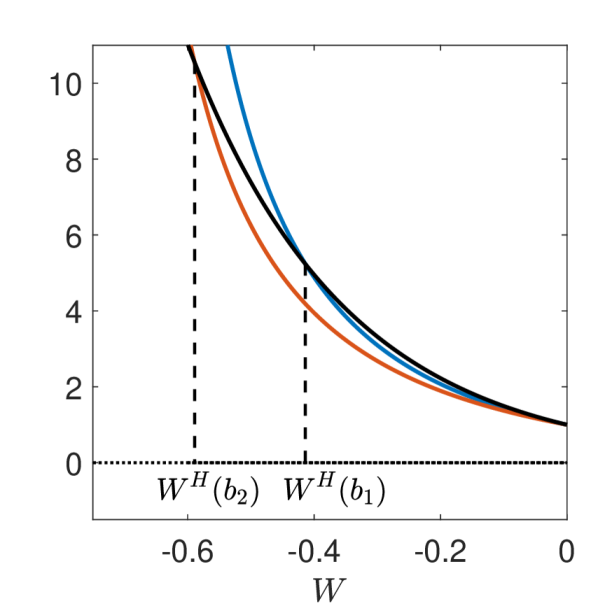

Concerning prices, in Figure 2 we report the evolution with respect to

of the steady state values and setting

and for different values of

We remark that and are computed numerically

solving equation (17) through which they are implicitly defined. On

increasing we may have situations in which the more the

markets are integrated, the more price increases (Figure

2 (A)), as well as opposite situations in which,

increasing the market integration, price is penalized (Figure

2 (C)), with intermediate scenarios in which a partial

integration provides the lowest price (Figure 2 (B)). In

this last case, we stress a further element of ambiguity: if we

compare the steady state values obtained for the same pair of

stock and real markets when independent () and completely

integrated (), it is not possible to conclude which

one has the largest prices. From Figure 2 (B), it

is evident that we can simultaneously have all the possible

orderings between prices, as

and

In the rest of the section, we focus on the local stability of the steady states. The

first group of results (see Propositions 4–6) deals with We start providing

analytical conditions under which is locally asymptotically

stable.

Proposition 4.

Before making explicit from (11) the roles of the interaction

degree, of the intensity of choice and of the bias on the stability of

we note that condition (11a) actually coincides with (6), whose

violation leads to the emergence of two more steady states. As it will become evident

also from the simulations, when loses stability because

of (11a), a pitchfork bifurcation occurs and two stable

steady

states and emerge.

We now turn our attention to the roles of and . We

highlight that a neutral effect on a steady state is realized when it

is locally asymptotically stable/unstable independently of the

parameter values; a stabilizing/destabilizing effect occurs when

the steady state is locally asymptotically stable only above/below

a given threshold value of the considered parameter and unstable

otherwise; a mixed effect arises when the steady state is locally

asymptotically stable only for intermediate parameter values,

between two stability thresholds, and unstable otherwise.

Proposition 5.

Under assumption (7), increasing or can have a mixed, destabilizing or neutral effect on .

The previous result points out that the bias and the intensity of choice have the same qualitative effect on the stability of If the polarization and the relevance of the beliefs is sufficiently increased, necessarily loses stability. Indeed, from the proof of Proposition 5 we find that can be unstable for any values of and but it cannot be always locally asymptotically stable. The unbiased steady state is then weakened when increasing heterogeneity of the beliefs as it becomes surrounded by the new potentially attracting polarized steady states and because it becomes unstable, although from a static viewpoint its position is not affected by and However, as we will see in Section 5, the role of the unbiased steady state, when unstable, may still be significant.

In the following result, we describe the possible stability scenarios arising for when varies.

Proposition 6.

Under assumption (7), increasing on can have a neutral, destabilizing, stabilizing or mixed effect on

The results obtained in Proposition 6 on the role of are in agreement with those reported in [23], namely the possible scenarios are the same, proving once more the ambiguous role of the interaction degree. It is then not possible to conclude that either encouraging or dampening the integration between the two sides of the economy improves the stability of the markets.

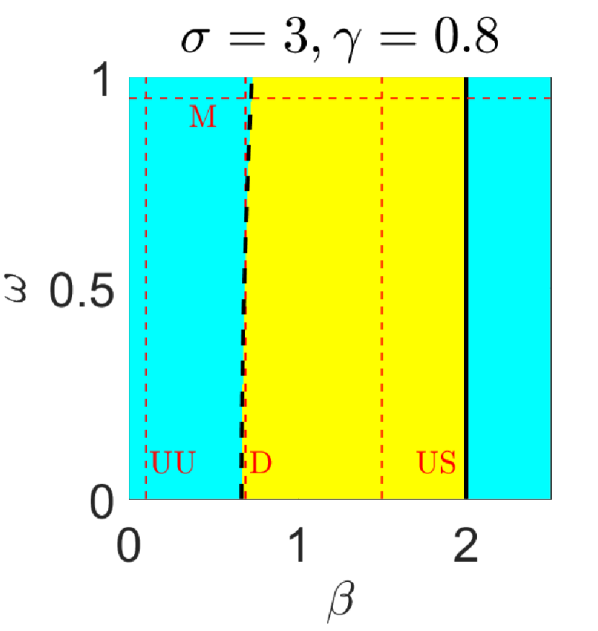

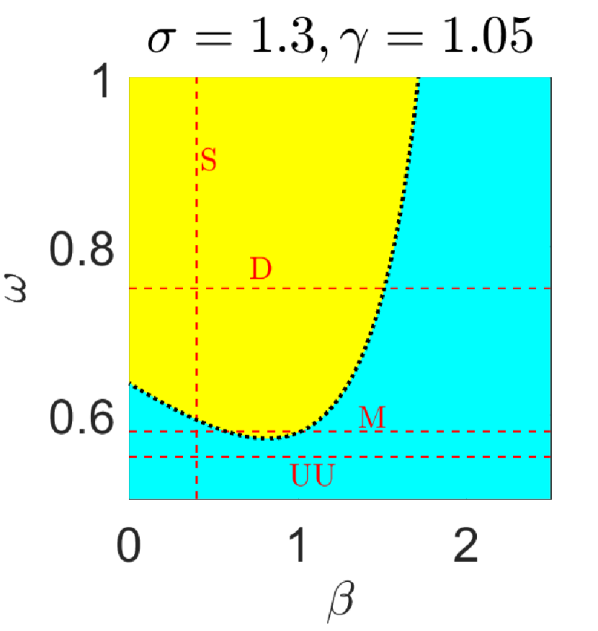

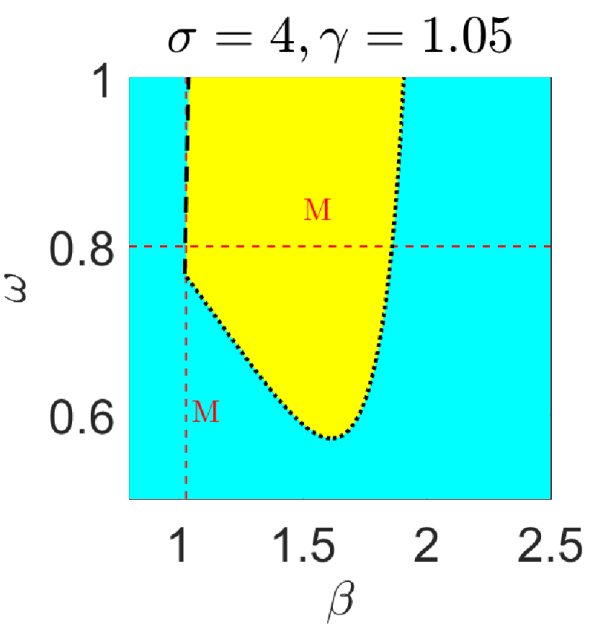

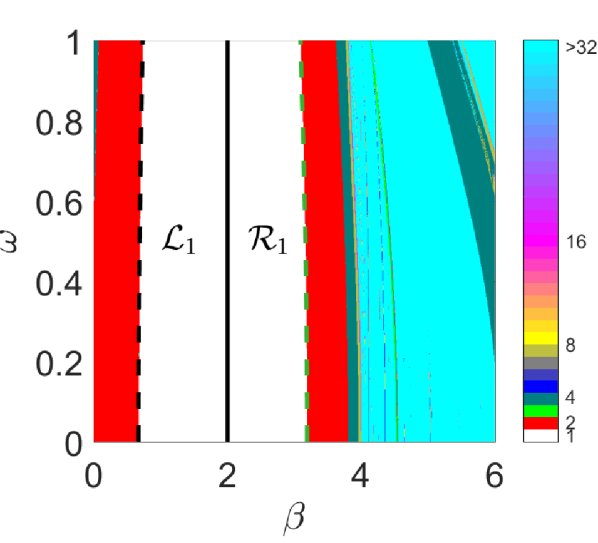

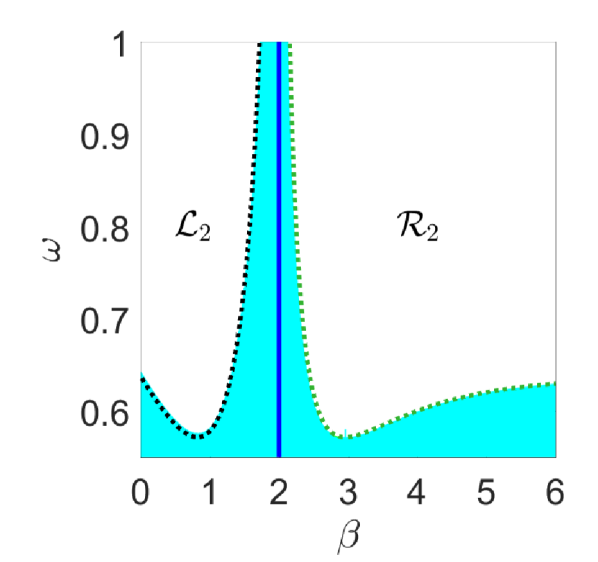

To summarize the findings about the stability of in Figure 3 we report three different stability regions in the -plane, obtained setting and and changing and from time to time in order to highlight different stability configurations. Parameters’ combinations for which is locally asymptotically stable are represented using yellow color, while cyan color is used for the instability region. The stability thresholds corresponding to conditions (11a), (11b) and (11c) are represented by solid, dashed and dotted black lines, respectively.

(A)

(B)

(C)

In particular, the region reported in Figure 3 (A) is obtained setting and shows the occurrence, on varying , of unconditionally unstable, destabilizing and unconditionally stable scenarios for , and respectively (vertical dashed red lines). On varying we always find a mixed scenario (e.g. horizontal dashed red line ). The stabilizing scenario (vertical dashed red line ) on increasing is reported in Figure 3 (B), which is obtained setting and On varying we have unconditionally unstable (e.g. when ), mixed (e.g. when ) and destabilizing (e.g. when ) scenarios. Finally, setting and we obtain the stability region reported in Figure 3 (C), in which we underline the occurrence of mixed scenarios both on varying (e.g. for ) and (e.g. for ). The previous considerations allow concluding that each scenario predicted by Propositions 5 and 6 is actually possible. We stress that the mixed scenarios on varying pointed out in each of Figures 3 (A)–(C) are obtained crossing different couplings of thresholds.

In the next proposition we show the possible effects of and on the local asymptotic stability of and provided that they exist and are positive.

Proposition 7.

Let assumptions (7) and (9) hold

true. If, keeping fixed and

increasing for we have

a destabilizing scenario, then on increasing

we can either have a stabilizing or an

unconditionally stable scenario on

and

a mixed scenario, then on increasing

we can either have a destabilizing or a

mixed scenario on

and

an unconditionally unstable scenario, then

and are unconditionally unstable, too.

Moreover, on increasing there is a one to one

correspondence between the scenarios for for

and those for and for

The previous proposition shows that the stability of and is strongly connected to that of From the mathematical point of view, we actually have that the stability behavior of and is a “specular reflection” of that of with respect to Decreasing has the same effect on the stability of of increasing it on the stability of and Thanks to Proposition 7, we can highlight a substantial difference with the scenarios of the economic setting reported in [23]: in the present case, for increasing values of the intensity of choice, when loses stability (both in the destabilizing and in the mixed scenarios) we can still have convergence toward a steady state. Such framework occurs when undergoes a pitchfork bifurcation and the new steady states and are locally stable. This means that, in such scenario, the final outcome is always a steady state, which, even if it changes, may be locally stable. The most extreme situation is realized when a destabilizing scenario for is followed by an unconditionally stable one for and Accordingly, convergence toward a steady state may occur for any value of

4 Numerical simulations

In this section we present the results of several numerical

investigations, collected pursuing a double aim. Firstly, we wish to

complement the analysis of Section 3. In particular, we

want to understand what kinds of dynamics occur when

becomes unstable, as well as to investigate the possible

scenarios arising with the emergence of and Secondly, we

want to study the qualitative properties of the time series when

exogenous non-deterministic effects are taken into account, that is,

considering a stochastically perturbed version of the model, in

agreement with [4, 11, 23]. In continuity with Section

3, we focus on the effect of the degree of

interaction and of the intensity of choice

In order to perform simulations, we need to specify the analytical expressions of and In what follows, we use the same sigmoid function considered in [3], i.e.,

| (12) |

where and are positive parameters, with

as upper bound when and as lower bound

when . A straightforward check shows that function

belongs to and satisfies assumptions

(1). In all the simulations reported in the present section

we set

, , and

Concerning the upper and lower bounds of

functions and we start by recalling that the steady state

values of and significantly change on varying Since

such bounds represent the maximum possible positive or negative

variation of and it is reasonable to assume that they are

qualitatively connected to the magnitude of prices and national

incomes. In fact, it makes economic sense to think that investments

and prices can not grow indefinitely but that, instead, their

variation is linked to the pace of economic activity, reflected in the

level of prices and national income, which are in turn connected to

the amount of resources existing in a certain country. To encompass

such fact into the simulations, we let proportionally change

depending on the value of the steady state setting

and

In this way, for we have

while they increase/decrease,

on varying proportionally to and (see

Proposition 3). We recall that we checked the robustness of

the simulations by varying all the parameters in suitable ranges,

obtaining results that are qualitatively comparable with those

reported in the next subsections. We also point out that the reported two-dimensional

bifurcation diagrams are obtained setting the same initial datum for

each parameters’ coupling. Conversely, in order to highlight

coexistence, one-dimensional bifurcation diagrams are all obtained

“following the attractor”. This means that, having a strictly

increasing or decreasing sequence of parameters ,

we set the initial datum for the first simulation

equal to while the initial datum for the simulation with

is set suitably close to the solution of the simulation

obtained with .

4.1 Deterministic simulations

(A)

(B)

(A)

(B)

(C)

(D)

(E)

(F)

We shall now explain the functioning of the model by considering

different sets of simulations, which provide a portrait of the

possible dynamics that may occur in our model economy, emphasizing how

the relevant parameters affect the evolution of the economic

variables. In particular, we aim to account for the richness of the

possibly complex dynamical behaviors arising in unstable regimes,

which however keep evident track of the simple distinctive

characterization of the

beliefs, in terms of optimistic/pessimistic bias.

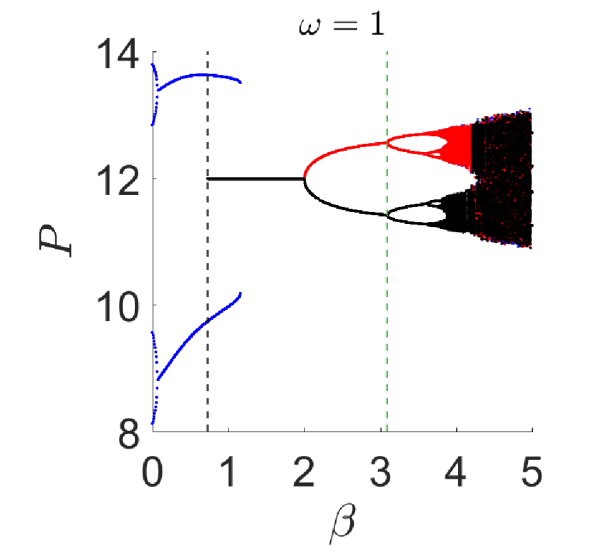

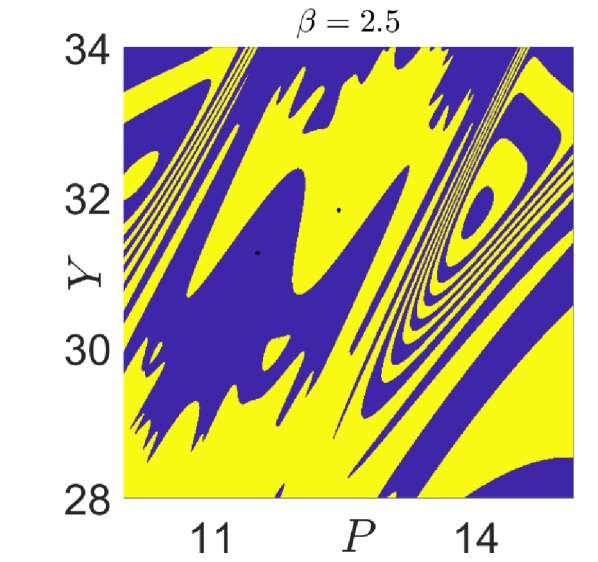

In the first set of simulations we set and

and the resulting stability region for is that reported in

Figure 3 (A). In Figure 4 (A) we show the

two-dimensional bifurcation diagram in the -plane,

where each point is represented using a different color depending on

the number of points of the attractor that was approached starting by

the initial datum

after

iterations. In particular, white color denotes parameter

combinations for which convergence is toward a one-point attractor,

i.e., a steady state, red color is used for period-2 cycles, cyan

color for attractors consisting of more than 32 points (namely, high

period cycles, chaotic attractors or closed invariant curves), and the

remaining colors for cycles with periods between 3 and 32. Black solid

and dashed lines respectively represent the stability thresholds

corresponding to (11a) and (11b), delimiting the

region within which (see also the yellow set in Figure 3

(A)) the steady state is stable and dynamics converge

toward it (white region ). If we start from any

and we increase we exit the

stability region as crosses the black solid

line, but in the white region dynamics again converge

toward a steady state. In fact, according to Propositions 1 and

4, such black line, whose equation is given by

since , represents both the bound for the stability condition

(11a) for and the threshold to the left/right of

which we have a unique/three coexisting steady states. As a

consequence, when the solid line is crossed on increasing

, the steady state becomes unstable by means of a

pitchfork bifurcation and the two stable steady states and

arise. We stress that, with the present choice of the initial datum,

dynamics converge toward for all

Region is the specular of with respect to In particular, the green dashed line is obtained starting from the black dashed threshold line and numerically solving the implicit equations used in the proof of Proposition 7. This, in agreement with Proposition 7, confirms that region is the region of local asymptotic stability for

As remarked in the comments to Figure 3 (A), on increasing

we have mixed scenarios for for any From

Proposition 7, since the right stability threshold for

is described by the “pitchfork” condition (11a),

this is the only situation in which a mixed scenario for

“translates” into a destabilizing scenario for As described

after Proposition 7, this is simply due to the fact

that, crossing from right to left, disappears. In

fact, starting from any for

increasing values of we cross the green stability threshold,

while decreasing we leave entering

To be more precise about the possible dynamics

occurring when steady states lose stability, we can see that when we

leave both and crossing a dashed

stability threshold, we enter one of the red regions, meaning that

dynamics, previously converging to a steady state, now converge to a

period-2 cycle.

In Figure 4 (B) we report three bifurcation diagrams

obtained for 666We checked that for

we obtain bifurcation diagrams that are qualitatively the

same of that reported in Figure 4 (B).. The blue

bifurcation diagram is obtained setting

and on

varying between and while the red and the black

bifurcation diagrams are obtained respectively setting

and

and on

varying between and

We can see that as long as (black dashed line), but close to such value,

dynamics converge toward a period-2 cycle

which attracts almost all the trajectories777More precisely, when

belongs to the dashed lines in Figure

4 (A) a flip bifurcation occurs. In fact, for the

present parameters’ configuration, on such dashed line, condition

(11b) becomes an equality, while the remaining stability

conditions in Proposition 4 are satisfied. Condition

(11b) is violated when being the

characteristic polynomial of the Jacobian matrix

evaluated at Since the largest eigenvalue modulus of

is equal to a flip bifurcation occurs.. Such

period-2 cycle coexists with the stable steady state on an

interval of values of and then the former disappears when its

basin of attraction shrinks and is absorbed by that of the steady

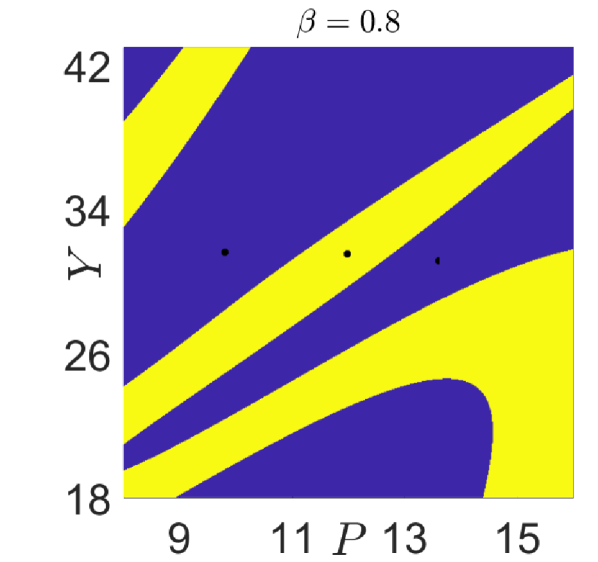

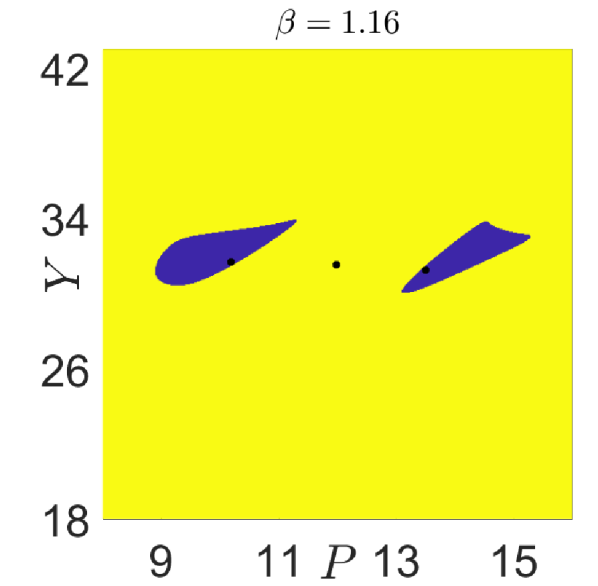

state. This coexistence is also reported in Figures 5

(A)-(B) where the basin of attraction888We remark that Figure

5 reports the slice on plane of the

three-dimensional basins of attraction for some increasing

values of together with the projection on such plane of the attractors toward which the initial data converged. of is represented in yellow while the basin of the 2-cycle is depicted in violet. The two panels show that, as grows, the basin of the 2-cycle reduces in size and for further increases of the intensity of choice parameter there is a contact between the periodic points and their basin boundary leading to the disappearance of the 2-cycle.

From the red and the black bifurcation diagrams of Figure

4 (B), it is evident the pitchfork bifurcation occurring

at with the red and the black lines springing from

that respectively represent and (see Figure

5 (C), which reports the basins of attraction of the

steady states born via the pitchfork bifurcation). These are the

biased steady states, whose birth via pitchfork bifurcation can be

read as the effect of agents’ decision when the intensity of choice is

high enough. In this case almost all agents adopt the optimistic or

pessimistic predictor, which is the best performing predictor in terms

of forecast error, leading the dynamics to converge to an equilibrium

different from We stress that, according to Proposition

2, all components of and are respectively

increasing and decreasing with respect to If is

further increased, they both lose stability through a flip bifurcation

and then a cascade of period-doubling bifurcations leads to chaos. In

fact, from Figure 4 (D) on we observe the basins of

attraction of the couple of 2-cycles born when and lose

stability. It is also worth remarking that Proposition 7

guarantees that the first period-doubling bifurcation occurs for the

same value both for and and Figure 4

(B) suggests that the subsequent period-doubling bifurcations are

simultaneous, too. Still increasing has the effect of making

these 2-cycles unstable, leading to the emergence of chaotic

attractors (see Figures 4 (E)-(F)) associated with

erratic dynamics in the course of price and national income. In this

scenario, on increasing the intermediate unbiased steady

state loses its relevance when becomes unstable, as almost all

trajectories converge toward the optimistic or the pessimistic

attractor.

We now focus on the role of the degree of interaction , considering vertical sections of the bifurcation diagram in Figure 4 (A). The destabilizing scenario for both and only leads to the emergence of a period-2 cycle (e.g. for ). It is worth noticing that the possible effects on of increasing the interaction degree when are again specular with respect to those on when In fact, we can identify neutrally stable (e.g. for ) or unstable (e.g. for ) scenarios, as well as destabilizing scenarios (e.g. for ).

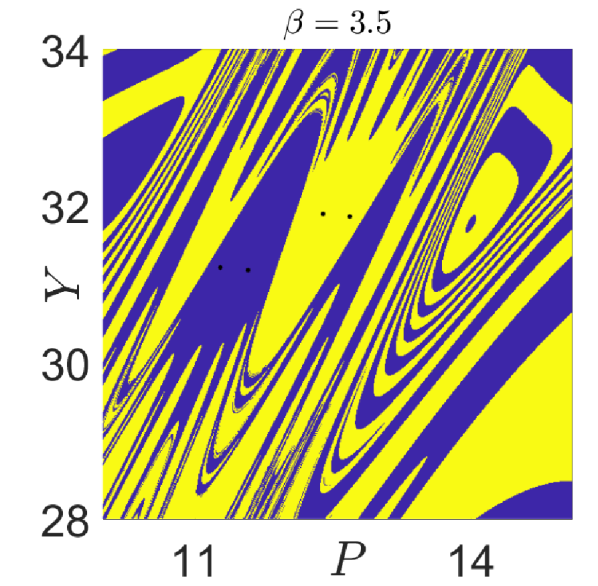

The second family of simulations we consider is obtained setting

and The corresponding stability region for

is depicted in Figure 3 (B) and the

corresponding two-dimensional bifurcation diagram is reported in

Figure 6 (A), in which the dotted black line represents

the stability threshold (11c). Differently from the first set

of simulations, condition (represented using blue color)

acts no more as a stability threshold, but it still shapes regions in

which we have either one or three steady states. The initial datum is

always set equal to

and in

region the convergence is toward while in

region convergence is toward

In this case, we can have either convergence toward a steady state (in

regions denoted by and ) or toward an

attractor consisting of more than points (cyan regions). Both

couple of regions are specular with respect to the vertical blue line

in agreement with Proposition 7, and,

depending on the value of the interaction degree, unconditionally

unstable, mixed and destabilizing scenarios for

respectively correspond to

unconditionally unstable, mixed and stabilizing scenarios for

This means that the emergence of new steady

states makes possible to have convergence toward a stable steady state

as

If we start from and we increase (or, depending on also if we decrease) , the crossing of the black dotted line makes unstable and immediately trajectories converge toward an attractor consisting of more than 32 points (represented by cyan color). The same happens in relation to if we start from and we decrease (or, depending on also if we increase) crossing the green dotted line (which, like in Figure 4 (A), is obtained starting from the black dotted threshold and numerically solving the implicit equations used to prove Proposition 7). This stability loss for and is associated with the occurrence of Neimark-Sacker bifurcations, as it looks evident evident also from Figure 6 (B), where we report three bifurcation diagrams on varying for which highlight the presence of a mixed scenario for both and . We stress that we checked that qualitatively similar results are obtained for all the values of for which a mixed scenario arises.

(A)

(B)

The blue bifurcation diagram, obtained setting

and increasing from to lies below the red one,

obtained setting

and decreasing from to which in turns lies above the

black one, obtained setting

and decreasing again from to .

We numerically checked that the closed invariant curve,

arising from the stability loss of ,

attracts almost any trajectory also for intensity of choice values

suitably close to , when steady states

and already exist but are

unstable (black bifurcation diagram, just to the right of the blue

dotted line). Such closed invariant curve coexists, as

increases, first with another couple of closed invariant curves

(blue, red and black bifurcation diagrams just to the left of the

first green dotted line), then with

and (blue, red and black bifurcation diagrams

between the two green dotted lines) and finally again with another

couple of closed invariant curves (blue, red and black bifurcation

diagrams just to the right of the second green dotted line).

Similar considerations hold also when the destabilizing scenario

for is followed by the stabilizing one

for and

Once more, the common aspect is the coexistence of attractors

encompassing optimistic, pessimistic or unbiased levels in the

economic variables, with the addition of the magenta attractor in

which each piece embodies large or small levels too.

On varying from vertical sections of Figure 6

(A) we infer that we can have either stabilizing scenarios for both

(e.g. for ) and

(e.g. for ) or unconditionally unstable

scenarios for both and

when is sufficiently close

to

(A)

(B)

(B)

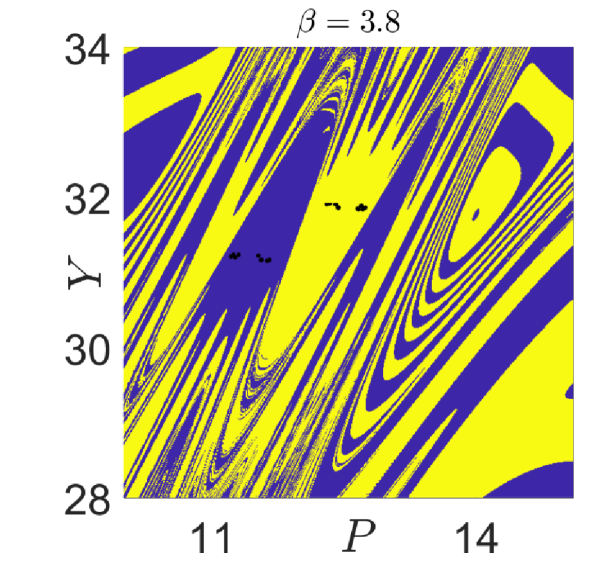

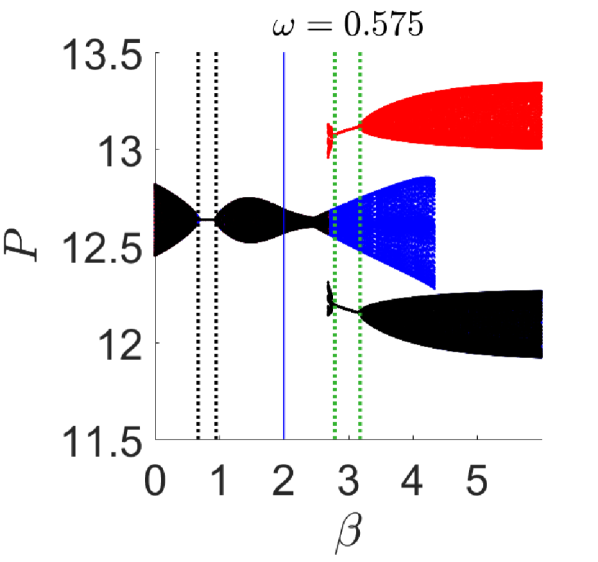

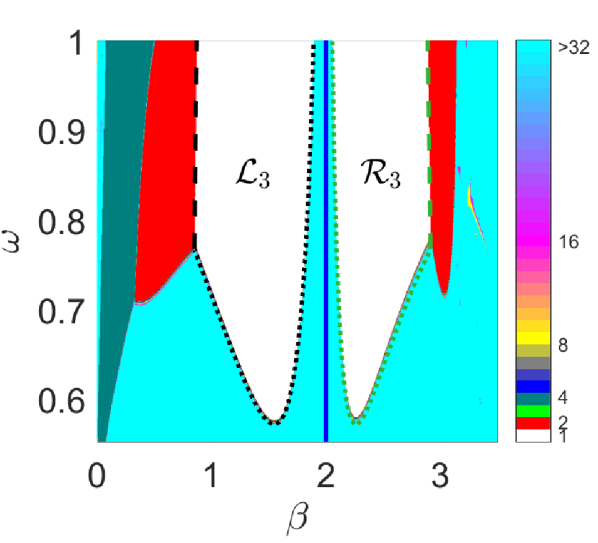

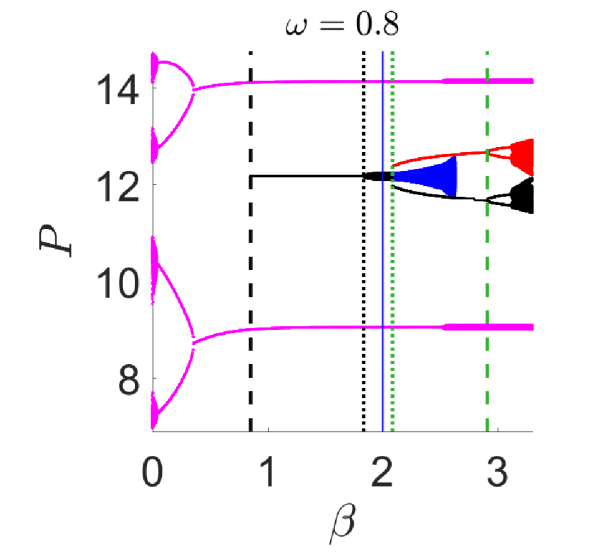

The last family of simulations, whose two-dimensional bifurcation diagram is reported in Figure 7 (A), is obtained setting and and the corresponding stability region is that reported in Figure 3 (C). The initial datum is the same as in the first two sets of simulations and, when dynamics converge for we have convergence toward All the previous considerations about the specular stability/instability regions and stability thresholds for and with respect to still hold. On varying , we can have either unconditionally unstable or mixed scenarios for both and but, differently from the first two families of simulations, the convergence toward the steady states may be replaced, when the aforementioned steady states become unstable, by convergence toward different kinds of attractors for different values of the interaction degree parameter . This is perceivable looking at the stability thresholds for reported in Figure 7 (A). The black dotted curve corresponds to condition (11c), crossing which we enter the cyan region, in which attractors consist of more then 32 points (actually, it is a closed invariant curve and the stability loss of occurs through a Neimark-Sacker bifurcation), while the black dashed line corresponds to condition (11b), crossing which we enter the red region, in which the attractor is a period-2 cycle. The same holds for the green stability thresholds for too, which also in this case are obtained from the black thresholds and numerically solving the implicit equations used in the proof of Proposition 7.

In the four bifurcation diagrams reported in Figures 7

(B)-(C) we study the occurring dynamics when The blue

bifurcation diagram is obtained setting

and

increasing from to the red one is obtained

setting

and decreasing from to the black one is

obtained setting

and

decreasing from to the magenta one is obtained

setting

and increasing from to As turns unstable

on decreasing (when the black dashed line is crossed), the

steady state is replaced by a 2-cycle, similarly to what happens in

the first family of simulations. However, as becomes

unstable on increasing (when there is a crossing of the black

dotted line), the steady state is replaced by a closed-invariant

curve. The attractor arising from the stability loss of

then coexists with the stable steady states and Further increasing when such two steady states

become unstable (green dashed line), a flip bifurcation

occurs999Conversely, if is decreased, we

numerically checked that when and become unstable a closed

invariant curve emerges, which coexists with the blue attractor and

quickly disappears.. The subsequent

period-2 cycles lose stability through a Neimark-Sacker bifurcation.

The magenta attractor exists for the whole range of values of

we consider. If we decrease from to such

attractor firstly evolves toward a period-4 cycle and then a

Neimark-Sacker bifurcation occurs. If we increase starting

from each of the two points composing the attractor is

replaced by a closed invariant curve. As increases, we have

that the attractor originated by the loss of stability of

(blue bifurcation diagram) coexists with steady states and

with a closed invariant curve, and with a period-2 cycle

(magenta bifurcation diagram), giving rise to a quite articulated

multistability situation made by qualitatively different attractors.

Once more, the common aspect is the coexistence of attractors

encompassing optimistic, pessimistic or unbiased levels in the

economic variables, with the addition of the magenta attractor in

which each piece embodies large or small levels, too.

The previous considerations confirm and enrich the analytical results about local stability. From a qualitative point of view, we can not speak about a unique type of mixed scenario, as those arising from the simulations above are significantly different. The first relevant difference can be highlighted in correspondence of the loss of stability of for increasing values of , namely when the rightmost stability threshold is violated. In the example reported in Figure 4, the stable steady state loses stability through a pitchfork bifurcation, and hence the new attractor has the same complexity as the previous one, even if it has a different interpretation from the economic point of view. In the example reported in Figures 6 and 7, dynamics converging to are replaced by quasi-periodic dynamics, that is, by an attractor of different complexity, even if arisen from The second difference can be highlighted in correspondence to the loss of stability of as decreases, when the leftmost stability threshold is violated. In this case, the unique steady state is again but different dynamics are possible, as the stability can be lost through a “simple” period-2 cycle or through more complex quasi-periodic dynamics. We stress that, for the same parameter values describing the stock and the real economy, different dynamics can arise on changing the degree of interaction. However, even in the presence of a very articulated range of complex situations, all the dynamic scenarios can be still traced back to the static setting outlined in Proposition 1, and hence easily read in terms of the effects of beliefs.

4.2 Stochastic simulations

The deterministic analysis has revealed that, starting from a situation in which the fundamental steady state is locally stable, an increase in the parameter generates the onset of endogenous fluctuations as well as the rise of multistability phenomena. The goal of this part is to show that a stochastic version of our model is able to generate varied and realistic dynamics, as observed in real financial markets, such as bubbles and crashes for stock prices and fat tails and excess volatility in the distributions of returns. In the presence of exogenous noise (on investors’ demands) and, accordingly, of fundamental shocks to the price dynamics, periods of high volatility in the price course may alternate with periods in which prices do not depart too much from the fundamental value. Such behavior may arise when the parameter setting is located near the pitchfork bifurcation boundary and exogenous noise can occasionally spark long-lasting endogenous fluctuations around the new steady states.

Therefore the model is modified along the following lines. The demand placed by the two groups of agents is set as

| (13) |

where are sequences of independent, identically

distributed random normal variables, with zero mean and variance

. These random disturbances may reflect errors in investors’

decision making processes, heterogeneity within the same group, or they may

capture the idea that it is quite difficult for investors to determine

the fundamentals (in fact fundamental values may change over time due

to real shocks), as already argued by [17].

Plugging the

perturbed demands into the price equation (4) and acting as in

Section 2, we end up with

| (14) |

where is is a sequence of independent, identically

distributed random normal variables, with zero mean and variance

.

In analyzing the stochastic version of our model, we aim at showing

that several stylized facts of financial markets may be retrieved

that, in turn, can possibly affect the behavior of the real

sector. Thanks to their apparent explanatory power, models that have

been being developed with interacting agents and interconnected

sectors are increasingly used as tools for economic policy

recommendations (see e.g. [9, 11, 27]).

In what follows, we consider the price returns, defined as

focusing, at first, on the deviation from normality of their distribution. In all the simulations reported in this subsection we employ the same parameter setting adopted for Figure 4.

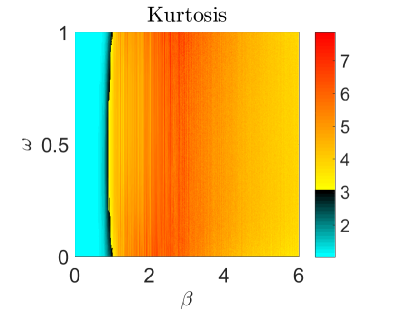

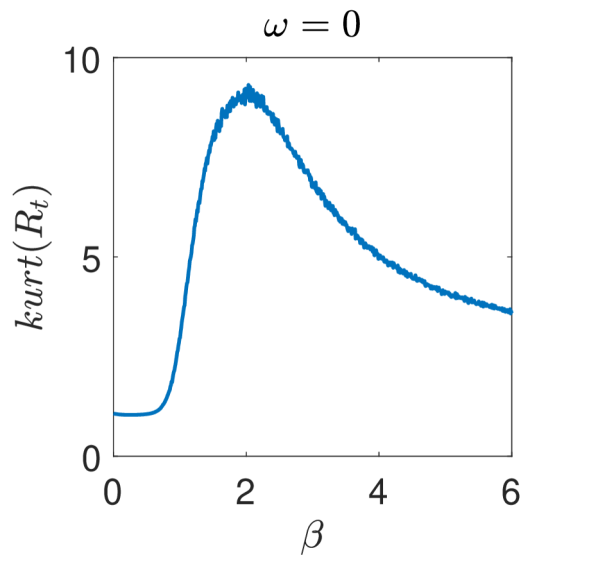

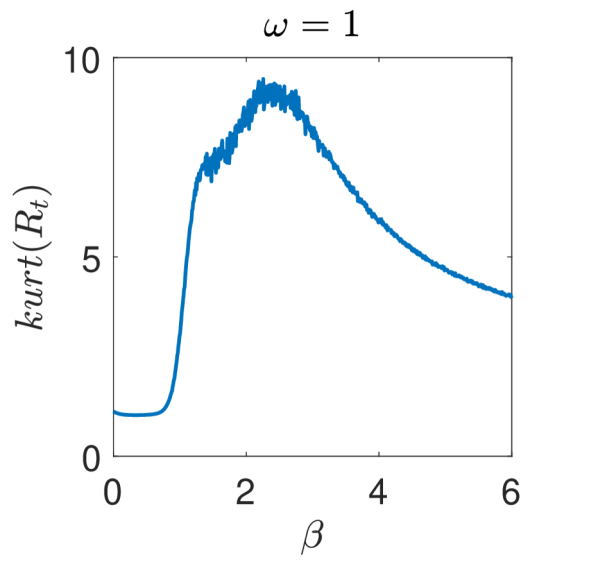

Figure 8 displays the values of the kurtosis in the distributions of the log-returns as the parameters and jointly vary. We observe that, independently of the degree of interaction between the two markets, as the intensity of choice increases from 2 to 4, the kurtosis increases as well, reaching values that reveal a non-normal distribution of the log-returns. In fact, kurtosis measures how fat the tails of the distributions are compared to the ones of a normal distribution. In this respect, to observe fat tails it is essential to have trajectories in which prices move frequently far from their average and, in turn, this is related to the behavior of the intensity of choice . For example, looking at Figure 4, we observe that, as increases, coexisting attractors appear, due to the occurrence of the pitchfork bifurcation, and this reflects into a large kurtosis, e.g. for roughly. As increases further, the bifurcation diagram of Figure 4 shows that the dynamics turn into chaotic and this translates into slightly reduced values for the kurtosis in the log-returns of the stochastic version of the model. Such results are confirmed also by the top and bottom left panels of the Figure 9, obtained for and respectively. As the degree of market interaction grows, the switching between the optimistic and pessimistic strategies towards the best performing rule is able to increase the kurtosis in the distributions of the log-returns.

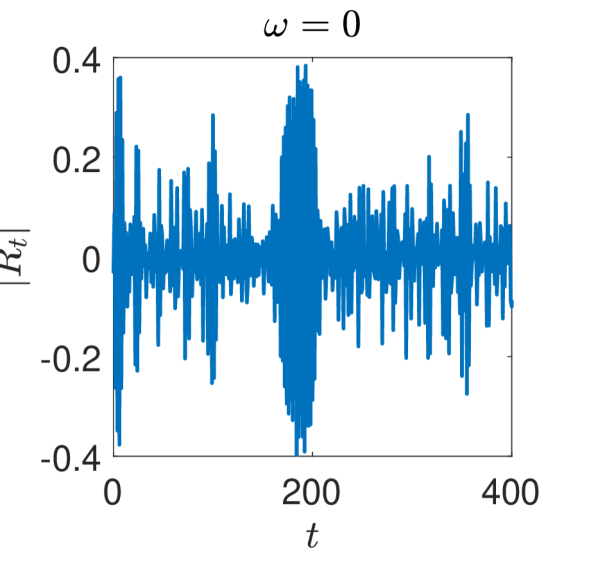

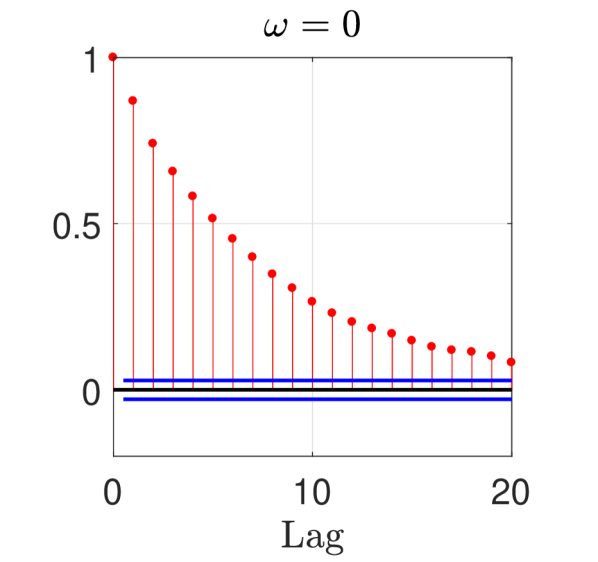

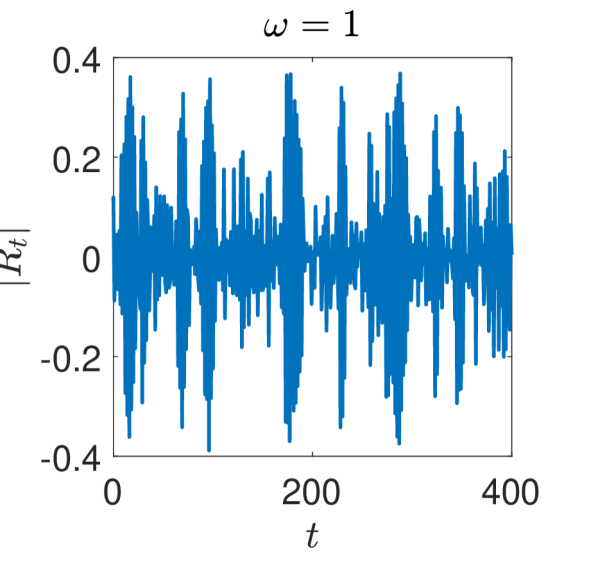

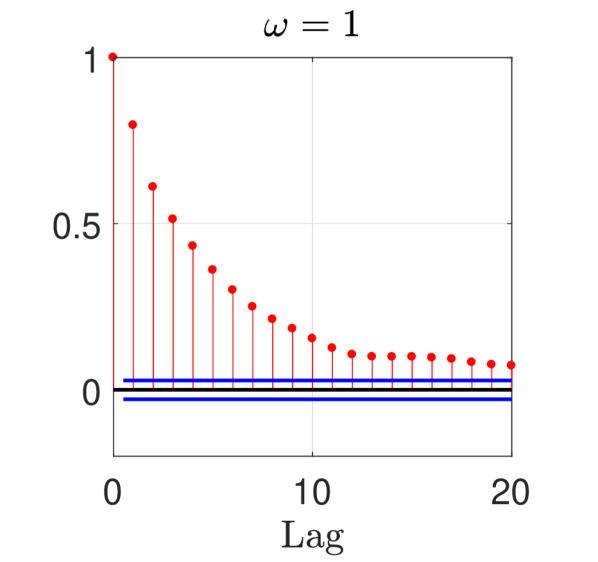

Another peculiar stylized fact of returns’ times series is the volatility clustering, namely, the occurrence of several consecutive periods characterized by high volatility alternated with others characterized by low volatility. This is graphically evident from the central panels of Figure 9, in which a typical example of time series of returns, obtained for the parameter setting used for Figure 4 and , is reported. Finally, volatility clustering is highlighted by the typical strongly positive, slowly decreasing autocorrelation coefficients of absolute returns, reported in the right top and bottom panels of Figure 9.

Overall, we may come up with the conclusion that the stochastic

version of our model with interacting real and financial sectors is

able to replicate key empirical regularities of actual stock markets.

In particular, the functioning of the stochastic version of the model

descends from the functioning of its deterministic counterpart. In the

deterministic setup, endogenous dynamics arise when a model parameter

crosses the Neimark-Sacker bifurcation boundary, as well as coexisting

attractors appear when the pitchfork bifurcation takes place. In the

stochastic version, when the two non-fundamental steady states appear

and are still locally stable, the interplay of nonlinear elements and

random shocks leads to realistic dynamics.

(A)

(B)

(C)

(D)

(E)

(F)

5 Conclusions

The proposed model shows that beliefs can influence the possible final

outcomes of an economy not only in terms of increasing the complexity

in the possible endogenous dynamics of the economic variables, but

also in a more constitutive way. From the static point of view,

strongly heterogeneous expectations can alter the set of steady

states, originating strongly polarized multiple steady states that in

turn reflect the optimism/pessimism of the beliefs. This can then

dynamically evolve into complex attractors still characterized by

optimism/pessimism of the beliefs, provided that such bias is strong

and relevant enough. To sum up, it is certainly evident the role

played by the occurrence of the pitchfork bifurcation, with the

optimistic/pessimistic steady states common to the various sets of

simulations. But this is not the sole effect. From a broader

perspective, the occurrence of such biased steady states coexisting

with the unbiased one is the result of the repeated strategies’

evaluation made by the agents, which may lead the economy to converge

to high, intermediate or low, steady or endogenously fluctuating,

levels of national income (and prices as well), with the consequent

richness of dynamical behaviors related to all equilibria and their

eventual destabilization.

The investigation, performed with a mix of

analytical, numerical and empirical tools, has a twofold aim: besides

understanding the influence of the beliefs on the course of the

economy in terms of possible final outcomes and stability of the

desired equilibrium level of national income and prices, we are

interested in the role of market integration and in its possible

beneficial effect on the overall economy in terms of increasing level

of national income. We showed that an increase of market interaction

may be either beneficial, as it may increase the national income of

the economy, or it may generate a contraction in its level, as no real

benefits to the society deriving from the activities based on an

increased integration may be appraised. The potential beneficial

effect of the degree of interaction seems to emerge also from the

local stability analysis, with the found stabilizing effect of the

interaction degree for suitable values of the intensity of choice

parameter, which measures agents’ reactivity toward the best

performing strategy. This interplay between interaction, imitation and

beliefs is crucial also in view of understanding and interpreting the

stylized facts that our model is able to reproduce when buffeted with

stochastic noise, like the recurrent boom-bust phenomena observed in

the real financial markets together with several stylized facts

regarding stock price returns, such as positive autocorrelation,

volatility clustering and non-normal distribution characterized by a

high kurtosis and fat

tails.

The proposed model belongs to a class of models that, we believe, may

be useful in order to interpret and understand the recent developments

in the increasingly interconnected economy, which constitutes a true

challenge for regulatory measures which seek to appease abrupt market

fluctuations. We hope that our work will stimulate further

investigations in such direction, especially as concerns the deepening

of the understanding of the role of the agents’ beliefs. The financial

crisis at the end of the last decade has not only made evident that

our comprehension of the dynamics of real and financial markets is

still incomplete, but it has also revealed how important is to

intensify the research activity in this field.

Appendix A Proofs of Propositions

Proof of Proposition 1.

In order to find the steady states, we set and in (5). From (5c) we have Inserting it in (5a) and (5b) since, recalling (1a), we have that and that is solved by only, we obtain

| (15a) | |||

| (15b) | |||

The steady state existing independently of and is found setting which immediately provides whose components, by (7), are positive independently of

In order to verify the existence of additional steady states, we notice that, from (15a), national income can be rewritten as a function of the asset price as

| (16) |

Inserting such expression in (15b), we find the following equation in whose solutions are the steady state values of price:

| (17) |

Defining

| (18) |

and

| (19) |

we observe that is a straight line that crosses the horizontal

axis of the Cartesian coordinate plane at the point

and the vertical axis at

We

stress that such points can be either positive or negative and

that the function is increasing in . In fact, thanks to the

positivity condition for the steady state we have

Simple computations allow to conclude that is an increasing

function in and it has an inflection point at , it is convex for and concave for Moreover,

crosses the vertical axis at the point . We always find and, according to the values assumed by the model parameters,

and can also meet at some points and with and where

is the intersection point between the horizontal line

and

Recalling the expression of

it is easy to see that

and

respectively correspond to the left and right bounds for

in (8). In order to determine the bounds on

it is possible to proceed as done for

obtaining an equation like (17) from (15), this

time in terms of

More precisely, since

is an increasing straight line and

is an increasing function in ,

with an inflection point at being convex for and concave for then if we have exactly one solution to (17), that is, while if we have exactly three distinct solutions, and to (17). We notice that corresponds to

To guarantee the economic meaningfulness of and we require their positivity. A sufficient condition to ensure this consists in setting which is verified for each when Since is strictly positive and is strictly increasing, their intersection is realized for

Finally, it is easy to show that and are symmetric w.r.t. i.e., that for every and For that is true because it is a straight line, while for a direct computation shows that

We then have that, when (6) holds, (17) is solved not only by but also by and symmetric values w.r.t. From (16) and since in the steady states we have it follows that national income positively depends on the asset price and thus to and correspond and with as well as and with . Moreover, if and are positive, then, from (16) , and are positive, too. Finally, by the linearity of (16) and by the symmetry of and w.r.t. it follows that and are symmetric w.r.t. and, since in the steady states we have then and are symmetric w.r.t. This concludes the proof. ∎

Proof of Proposition 2.

We start noting that, from (16), positively depends on , so it is sufficient to study the monotonicity for on varying either or . Setting

| (20) |

we may rewrite (17) as

| (21) |

from which it follows that

| (22) |

Moreover, it holds that

| (23) |

For on both sides of equation (22) there are positive, strictly decreasing functions of and the rhs of (22) is also independent of In what follows, we make reference to some explanatory plots reported in Figure 10.

Firstly we consider From (8) we have that defined by (23), belongs to Setting the lhs of (22) is decreasing with respect to , so that if we find An illustrative example is reported in Figure 10 (A), from which it is evident that the last inequality guarantees that the unique solution of (22) on increases with , and hence, recalling (23), increases, too. We proceed in a similar way for . From (8), we have that defined by (23), belongs to Setting , the lhs of (22) is increasing with respect to so that if we find . An illustrative example is reported in Figure 10 (B), from which it is evident that the last inequality guarantees that the unique solution of (22) on decreases with , and hence, recalling (23), decreases, too. The two limits of as can be easily obtained by noting that the lhs of (22) pointwise approaches for each so that tends to and the lhs of (22) pointwise approaches for each so that tends to Using (23) allows concluding. For the limits of it is sufficient to compute the limit as of the rhs of (16), in which we replace with either or and we use the just computed limits.

To study the monotonicity of and with respect to , we rewrite (22) as

| (24) |

which is well defined on and shares the solutions with (23). The lhs is represented by a positive, strictly decreasing function of Let us consider and the corresponding steady states and . From (8) we have that and defined by (23), respectively belong to and For , noting that , we find An illustrative example is reported in Figure 10 (C), from which it is evident that the last inequality allows concluding that if it holds that (indeed, also if since we have ). This implies that increases with , and hence, recalling (23), increases, too.

Now we turn our attention to and still assuming . From (8) we have that and defined by (23), respectively belong to and For , noting that , we find An illustrative example is reported in Figure 10 (D), from which it is evident that the last inequality allows concluding that if it holds that (indeed, also if , since we have ). This implies that decreases with , and hence, recalling (23), decreases, too.

(A)

(B)

(C)

(D)

∎

Proof of Proposition 3.

Let us start focusing on the effects of on A direct computation shows that

Such derivative is non-negative for each when

and in this case increases with

for every When instead the

numerator of may become

negative. More precisely, is

equivalent to

When the discriminant

of

is non-positive, we

have that decreases with for each

When instead the discriminant is positive, it is

easy to show that there are two positive solutions to

such equation, and the larger between them always exceeds Hence,

if the smallest solution

is larger than 1, then decreases with for each If instead lies in then decreases with on and increases with on Setting we obtain the desired result on

As concerns a direct computation shows that

Such derivative is positive for each when and in this case increases with for every When instead the numerator of may become negative. More precisely, when the discriminant of is non-positive, we have that increases with for each When instead the discriminant is positive, it is easy to show that there are two positive solutions to such equation, and the largest between them always exceeds Hence, if the smallest solution is larger than 1, then increases with for each If instead lies in then increases with on and decreases with on Setting we obtain the desired result on

Let us now assume namely (6) is violated and (9) holds true, so that the two additional steady states exist for every In order to analyze their behavior with respect to increasing values of we use the implicit function theorem. Let be defined by the lhs of (17) and let be the function which associates to one of the solutions implicitly defined by for . Recalling the definition of in (20), we then have

and

We can apply the implicit function theorem to investigate how the steady state values for depend on provided that

| (25) |

Setting condition (25) can be rewritten as or equivalently

which holds true if and only if Recalling (23), the last inequality can be rewritten as

| (26) |

By the symmetry of and with respect to (26) is satisfied if (10) holds true for each Under such assumption we have that, since is well-defined for then, by the implicit function theorem, it is continuously differentiable for each and it holds that

| (27) |

From now on, to fix ideas, we focus on analogous

arguments hold for as well.

If , then on and is strictly increasing

for .

Conversely, if , then

if for each , then

is strictly decreasing on , otherwise there

exists such that

| (28) |

If such exists, is decreasing on and . Since

we have