BNSP: an R Package for Fitting Bayesian Semiparametric Regression Models and Variable Selection

Abstract

The R package BNSP provides a unified framework for semiparametric location-scale regression and stochastic search variable selection.

The statistical methodology that the package is built upon utilizes basis function expansions to represent semiparametric covariate

effects in the mean and variance functions, and spike-slab priors to perform selection and regularization of the estimated effects.

In addition to the main function that performs posterior sampling, the package includes functions for assessing convergence of the sampler, summarizing model fits, visualizing covariate effects and obtaining predictions for new responses or their means given feature/covariate vectors.

Keywords: additive models; basis functions; heteroscedastic models; variable selection

1 Introduction

There are many approaches to non- and semi-parametric modeling. From a Bayesian perspective, Müller & Mitra, (2013) provide a review that covers methods for density estimation, modeling of random effects distributions in mixed effects models, clustering and modeling of unknown functions in regression models.

Our interest is on Bayesian methods for modeling unknown functions in regression models. In particular, we are interested in modeling both the mean and variance functions non-parametrically, as general functions of the covariates. There are multiple reasons why allowing the variance function to be a general function of the covariates may be important (Chan et al.,, 2006). Firstly, it can result in more realistic prediction intervals than those obtained by assuming constant error variance, or as Müller & Mitra, (2013) put it, it can result in more honest representation of uncertainties. Secondly, it allows the practitioner to examine and understand which covariates drive the variance. Thirdly, it results in more efficient estimation of the mean function, and lastly, it produces more accurate standard errors of unknown parameters.

In the R (R Core Team,, 2016) package BNSP (Papageorgiou,, 2018) we implemented Bayesian regression models with Gaussian errors and with mean and log-variance functions that can be modeled as general functions of the covariates. Covariate effects may enter the mean and log-variance functions parametrically or non-parametrically, with the nonparametric effects represented as linear combinations of basis functions. The strategy that we follow in representing unknown functions is to utilize a large number of basis functions. This allows for flexible estimation and for capturing true effects that are locally adaptive. Potential problems associated with large numbers of basis functions, such as over-fitting, are avoided in our implementation, and efficient estimation is achieved, by utilizing spike-slab priors for variable selection. A review of variable selection methods is provided by O’Hara & Sillanpää, (2009).

The methods described here belong to the general class of models known as generalized additive models for location, scale and shape (GAMLSS) (Rigby & Stasinopoulos,, 2005; Stasinopoulos & Rigby,, 2007) or the Bayesian analogue termed as BAMLSS (Umlauf et al.,, 2018) and implemented in package bamlss (Umlauf et al.,, 2017). However, due to the nature of the spike-and-slab priors that we have implemented, in addition to flexible modeling of the mean and variance functions, the methods described here can also be utilized for selecting promising subsets of predictor variables in multiple regression models. The implemented methods fall in the general class of methods known as stochastic search variable selection (SSVS). SSVS has received considerable attention in the Bayesian literature and its applications range from investigating factors that affect individual’s happiness (George & McCulloch,, 1993), to constructing financial indexes (George & McCulloch,, 1997) and to gene mapping (O’Hara & Sillanpää,, 2009). These methods associate each regression coefficient, either a main effect or the coefficient of a basis function, with a latent binary variable that indicates whether the corresponding covariate is needed in the model or not. Hence, the joint posterior distribution of the vector of these binary variables can identify the models with the higher posterior probability.

R packages that are related to BNSP include spikeSlabGAM (Scheipl,, 2016) that also utilizes SSVS methods (Scheipl,, 2011). A major difference between the two packages, however, is that whereas spikeSlabGAM utilizes spike-and-slab priors for function selection, BNSP utilizes spike-and-slab priors for variable selection. In addition, Bayesian GAMLSS models, also refer to as distributional regression models, can also be fit with R package brms using normal priors (Bürkner,, 2018). Further, the R package gamboostLSS (Hofner et al.,, 2018) includes frequentist GAMLSS implementation based on boosting that can handle high-dimensional data (Mayr et al.,, 2012). Lastly, the R package mgcv (Wood,, 2018) can also fit generalized additive models with Gaussian errors and integrated smoothness estimation, with implementations that can handle large datasets.

In BNSP we have implemented functions for fitting such semi-parametric models, summarizing model fits, visualizing covariate effects and predicting new responses or their means. The main functions are mvrm, mvrm2mcmc, print.mvrm, summary.mvrm, plot.mvrm and predict.mvrm. A quick description of these functions follows. The first one, mvrm, returns samples from the posterior distributions of the model parameters, and it is based on an efficient Markov chain Monte Carlo (MCMC) algorithm in which we integrate out the coefficients in the mean function, generate the variable selection indicators in blocks (Chan et al.,, 2006) and choose the MCMC tuning parameters adaptively (Roberts & Rosenthal,, 2009). In order to minimize random-access memory utilization, posterior samples are not kept in memory, but instead written in files in a directory supplied by the user. The second function, mvrm2mcmc, reads-in the samples from the posterior of the model parameters and it creates an object of class "mcmc". This enables users to easily utilize functions from package coda (Plummer et al.,, 2006), including functions plot and summary for assessing convergence and for summarizing posterior distributions. Further, functions print.mvrm and summary.mvrm provide summaries of model fits, including models and priors specified, marginal posterior probabilities of term inclusion in the mean and variance models and models with the highest posterior probabilities. Function plot.mvrm creates plots of parametric and nonparametric terms that appear in the mean and variance models. The function can create two-dimensional plots by calling functions from package ggplot2 (Wickham,, 2009). It can also create static or interactive three-dimensional plots by calling functions from packages plot3D (Soetaert,, 2016) and threejs (Lewis,, 2016). Lastly, function predict.mvrm provides predictions either for new responses or their means given feature/covariate vectors.

We next provide a detailed model description followed by illustrations on the usage of the package and the options it provides. Technical details on the implementation of the MCMC algorithm are provided in the Appendix. The paper concludes with a brief summary.

2 Mean-variance nonparametric regression models

Let denote the vector of responses and let and denote design matrices. The models that we consider express the vector of responses utilizing

where is the usual n-dimensional vector of ones, is an intercept term, is a vector of regression coefficients and is an n-dimensional vector of independent random errors. Each is assumed to have a normal distribution, , with variances that are modeled in terms of covariates. Let . We model the vector of variances utilizing

where is an intercept term and is a vector of regression coefficients. Equivalently, the model for the variances can be expressed as

| (1) |

where .

Let denote an n-dimensional, diagonal matrix with elements . Then, the model that we consider may be expressed more economically as

| (2) |

where and .

In the next subsections we describe how, within model (2), both parametric and nonparametric effects of explanatory variables on the mean and variance functions can be captured utilizing regression splines and variable selection methods. We begin by considering the special case where there is a single covariate entering the mean model and a single covariate entering the variance model.

2.1 Locally adaptive models with a single covariate

Suppose that the observed dataset consists of triplets where explanatory variables and enter flexibly the mean and variance models, respectively. To model the nonparametric effects of and we consider the following formulations of the mean and variance models

| (3) | |||

| (4) |

In the preceding and are vectors of basis functions and and are the corresponding coefficients.

In package BNSP we implemented two sets of basis functions. Firstly, radial basis functions

| (5) |

where denotes the Euclidean norm of and are the knots that within package BNSP are chosen as the quantiles of the observed values of explanatory variable , with , and the remaining knots chosen as equally spaced quantiles between and .

Secondly, we implemented thin plate splines

where and the knots are determined as above.

In addition, BNSP supports the smooth constructors from package mgcv e.g. the low-rank thin plate splines, cubic regression splines, P-splines, their cyclic versions and others. Examples on how these smooth terms are used within BNSP are provided later in this paper.

Locally adaptive models for the mean and variance functions are obtained utilizing the methodology developed by Chan et al., (2006). Considering the mean function, local adaptivity is achieved by utilizing a large number of basis functions . Over-fitting, and problems associated with it, is avoided by allowing positive prior probability that the regression coefficients are exactly zero. The latter is achieved by defining binary variables that take value if and if . Hence, vector determines which terms enter the mean model. The vector of indicators for the variance function is defined analogously.

Given vectors and , the heteroscedastic, semiparametric model (2) can be written as

where consisting of all non-zero elements of and consists of the corresponding columns of . Subvector is defined analogously.

We note that, as was suggested by Chan et al., (2006), we work with mean corrected columns in the design matrices and , both in this paper and in the BNSP implementation. We remove the mean from all columns in the design matrices except those that correspond to categorical variables.

2.2 Prior specification for models with a single covariate

Let . The prior for is specified as (Zellner,, 1986)

Further, the prior for is specified as

Independent priors are specified for the indicators variables as , from which the joint prior is obtained as

where .

Similarly, for the indicators we specify independent priors . It follows that the joint prior is

where .

We specify inverse Gamma priors for and and Beta priors for and

| (6) |

Lastly, for we consider inverse Gamma and half-normal priors

| (7) |

2.3 Extension to bivariate covariates

It is straightforward to extend the methodology described earlier to allow fitting of flexible mean and variance surfaces. In fact, the only modification required is in the basis functions and knots. For fitting surfaces, in package BNSP we implemented radial basis functions

We note that the prior specification presented earlier for fitting flexible functions remains unchained for fitting flexible surfaces. Further, for fitting bivariate or higher order functions, BNSP also supports smooth constructors s, te and ti from mgcv.

2.4 Extension to additive models

In the presence of multiple covariates, the effects of which may be modeled parametrically or semiparametrically, the mean model in (3) is extended to the following

where, includes the covariates the effects of which are modeled parametrically, denotes the corresponding effects, and are flexible functions of one or more covariates expressed as

where are the basis functions used in the th component, .

For additive models, local adaptivity is achieved using a similar strategy as in the single covariate case. That is, we utilize a potentially large number of knots or basis functions in the flexible components that appear in the mean model, and in the variance model, . To avoid over-fitting, we allow removal of the unnecessary ones utilizing the usual indicator variables, and Here, vectors and determine which basis functions appear in and respectively.

The model that we implemented in package BNSP specifies independent priors for the indicators variables as . From these, the joint prior follows

where .

Similarly, for the indicators we specify independent priors . It follows that the joint prior is

where .

We specify the following independent priors for the inclusion probabilities.

| (8) |

The rest of the priors are the same as those specified for the single covariate models.

3 Usage

In this section we provide results on simulation studies and real data analyses. The purpose is twofold: firstly we point out that the package works well and provides the expected results (in simulation studies) and secondly we illustrate the options that the users of BNSP have.

3.1 Simulation studies

Here we present results from three simulations studies, involving one, two, and multiple covariates. For the majority of these simulation studies, we utilize the same data-generating mechanisms as those presented by Chan et al., (2006).

3.1.1 Single covariate case

We consider two mechanisms that involve a single covariate that appears in both the mean and variance model. Denoting the covariate by , the data-generating mechanisms are the normal model with the following mean and standard deviation functions

-

1.

,

-

2.

.

We generate a single dataset of size from each mechanism, where variable is obtained from the uniform distribution, . For instance, for obtaining a dataset from the first mechanism we use

> mu <- function(u){2 * u}

> stdev <- function(u){0.1 + u}

> set.seed(1)

> n <- 500

> u <- sort(runif(n))

> y <- rnorm(n,mu(u),stdev(u))

> data <- data.frame(y,u)

Above we specified the seed value to be one, and we do so in what follows, so that our results are replicable.

To the generated dataset we fit a special case of the model that we presented, where the mean and variance functions in (3) and (4) are specified as

| (9) |

with denoting the radial basis functions presented in (2.1). Further, we choose basis functions or, equivalently, knots. Hence, we have which results in identical design matrices for the mean and variance models. In R, the two models are specified using

> model <- y ~ sm(u, k = 20, bs = "rd") | sm(u, k = 20, bs = "rd")

The above formula (Zeileis & Croissant,, 2010) specifies the response, mean and variance models. Smooth terms are specified utilizing function sm, that takes as input the covariate , the selected number of knots and the selected type of basis functions.

Next we specify the hyper-parameter values for the priors in (2.2) and (7). The default prior for is inverse Gamma with (Liang et al.,, 2008). For parameter the default prior is a non-informative but proper inverse Gamma with . Concerning and , the default priors are uniform, obtained by setting and . Lastly, the default prior for the error standard deviation is the half-normal with variance , .

We choose to run the MCMC sampler for iterations and discard the first as burn-in. Of the remaining samples we retain 1 every 2 samples, resulting in posterior samples. Further, as mentioned above, we set the seed of the MCMC sampler equal to one. Obtaining posterior samples is achieved by a function call of the form

> m1 <- mvrm(formula = model, data = data, sweeps = 10000, burn = 5000, + thin = 2, seed = 1, StorageDir = DIR, + c.betaPrior = "IG(0.5,0.5*n)", c.alphaPrior = "IG(1.1,1.1)", + pi.muPrior = "Beta(1,1)", pi.sigmaPrior = "Beta(1,1)", sigmaPrior = "HN(2)")

Samples from the posteriors of the model parameters are written in seven separate files which are stored in the directory specified by argument StorageDir. If a storage directory is not specified, then function mvrm returns an error message, as without these files there will be no output to process. Furthermore, the last two lines of the above function call show the specified priors, which are , , and , respectively. As we mentioned above, these priors are the default ones, and hence the same function call can be achieved without specifying the last two lines. Here we display the priors in order to describe how users can specify their own priors. For parameters and only inverse Gamma priors are available, with parameters that can be specified by the user in the intuitive way. For instance, the prior can be specified in function mvrm by using c.betaPrior = "IG(1.01,1.01)". The second parameter of the prior for can be a function of the sample size (but only symbol would work here), so for instance c.betaPrior = "IG(1,0.4*n)" is another acceptable specification. Further, Beta priors are available for parameters and with parameters that can be specified by the user again in the intuitive way. Lastly, two priors are available for the error variance. These are the default half-normal and the inverse Gamma. For instance, sigmaPrior = "HN(5)" defines as the prior while sigmaPrior = "IG(1.1,1.1)" defines as the prior.

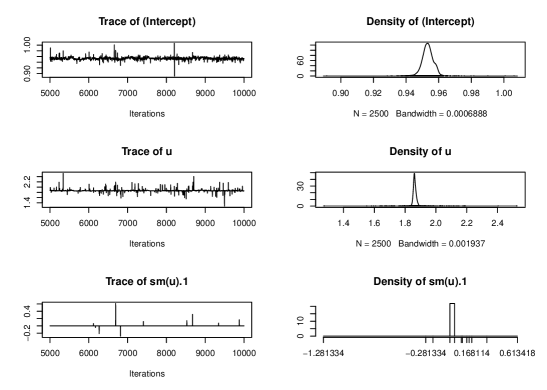

Function mvrm2mcmc reads in posterior samples from the files that the call to function mvrm generated and creates an object of class "mcmc". Hence, for summarizing posterior distributions and for assessing convergence, functions summary and plot from package coda can be used. As an example, here we read in the samples from the posterior of

> beta <- mvrm2mcmc(m1, "beta")

and summarize the posterior using summary. For the sake of economizing space, only the part of the output that describes the posteriors of , and is shown below

> summary(beta)

Iterations = 5001:9999

Thinning interval = 2

Number of chains = 1

Sample size per chain = 2500

1. Empirical mean and standard deviation for each variable,

plus standard error of the mean:

Mean SD Naive SE Time-series SE

(Intercept) 9.534e-01 0.004399 8.799e-05 0.0002534

u 1.864e+00 0.042045 8.409e-04 0.0010356

sm(u).1 3.842e-04 0.016421 3.284e-04 0.0003284

2. Quantiles for each variable:

2.5% 25% 50% 75% 97.5%

(Intercept) 0.946 0.9513 0.9533 0.9554 0.960

u 1.833 1.8565 1.8614 1.8682 1.923

sm(u).1 0.000 0.0000 0.0000 0.0000 0.000

Further, we may obtain a plot using

> plot(beta)

Figure 1 shows the first three of the plots created by function plot. These are the plots of the samples from the posteriors of coefficients and . As we can see from both the summary and Figure 1, only the first two coefficients have posteriors that are not centered around zero.

Returning to function mvrm2mcmc, it requires two inputs. These are an object of class "mvrm" and the name of the file to be read in R. For the parameters in the current model the corresponding file names are ‘beta’, ‘gamma’, ‘alpha’, ‘delta’, ‘cbeta’, ‘calpha’ and ‘sigma2’ respectively.

Summaries of ‘mvrm’ fits may be obtained utilizing functions print.mvrm and summary.mvrm. Function print takes as input an object of class "mvrm". It returns basic information at the model fit as shown below

> print(m1)

Call:

mvrm(formula = model, data = data, sweeps = 10000, burn = 5000,

thin = 2, seed = 1, StorageDir = DIR, c.betaPrior = "IG(0.5,0.5*n)",

c.alphaPrior = "IG(1.1,1.1)", pi.muPrior = "Beta(1,1)",

pi.sigmaPrior = "Beta(1,1)", sigmaPrior = "HN(2)")

2500 posterior samples

Mean model - marginal inclusion probabilities

u sm(u).1 sm(u).2 sm(u).3 sm(u).4 sm(u).5 sm(u).6 sm(u).7

1.0000 0.0040 0.0036 0.0032 0.0084 0.0036 0.0044 0.0028

sm(u).8 sm(u).9 sm(u).10 sm(u).11 sm(u).12 sm(u).13 sm(u).14 sm(u).15

0.0060 0.0020 0.0060 0.0036 0.0056 0.0056 0.0036 0.0052

sm(u).16 sm(u).17 sm(u).18 sm(u).19 sm(u).20

0.0060 0.0044 0.0056 0.0044 0.0052

Variance model - marginal inclusion probabilities

u sm(u).1 sm(u).2 sm(u).3 sm(u).4 sm(u).5 sm(u).6 sm(u).7

1.0000 0.6072 0.5164 0.5808 0.5488 0.6760 0.5320 0.6336

sm(u).8 sm(u).9 sm(u).10 sm(u).11 sm(u).12 sm(u).13 sm(u).14 sm(u).15

0.6936 0.6708 0.5996 0.4816 0.4912 0.3728 0.6268 0.5688

sm(u).16 sm(u).17 sm(u).18 sm(u).19 sm(u).20

0.5872 0.6528 0.4428 0.6900 0.5356

The function returns a matched call, the number of posterior samples obtained and marginal inclusion probabilities of the terms in the mean and variance models.

Whereas the output of function print focuses on marginal inclusion probabilities, the output of function summary focuses on the most frequently visited models. It takes as input an object of class ‘mvrm’ and the number of (most frequently visited) models to be displayed, which by default is set to nModels = 5. Here to economize space we set nModels = 2. The information returned by functions summary is shown below

> summary(m1, nModels = 2) Specified model for the mean and variance: y ~ sm(u, k = 20, bs = "rd") | sm(u, k = 20, bs = "rd") Specified priors: [1] c.beta = IG(0.5,0.5*n) c.alpha = IG(1.1,1.1) pi.mu = Beta(1,1) [4] pi.sigma = Beta(1,1) sigma = HN(2) Total posterior samples: 2500 ; burn-in: 5000 ; thinning: 2 Files stored in /home/papgeo/1/ Null deviance: 1299.292 Mean posterior deviance: -88.691 Joint mean/variance model posterior probabilities: mean.u mean.sm.u..1 mean.sm.u..2 mean.sm.u..3 mean.sm.u..4 mean.sm.u..5 1 1 0 0 0 0 0 2 1 0 0 0 0 0 mean.sm.u..6 mean.sm.u..7 mean.sm.u..8 mean.sm.u..9 mean.sm.u..10 1 0 0 0 0 0 2 0 0 0 0 0 mean.sm.u..11 mean.sm.u..12 mean.sm.u..13 mean.sm.u..14 mean.sm.u..15 1 0 0 0 0 0 2 0 0 0 0 0 mean.sm.u..16 mean.sm.u..17 mean.sm.u..18 mean.sm.u..19 mean.sm.u..20 var.u 1 0 0 0 0 0 1 2 0 0 0 0 0 1 var.sm.u..1 var.sm.u..2 var.sm.u..3 var.sm.u..4 var.sm.u..5 var.sm.u..6 1 1 1 1 1 1 1 2 1 0 1 1 1 1 var.sm.u..7 var.sm.u..8 var.sm.u..9 var.sm.u..10 var.sm.u..11 var.sm.u..12 1 1 1 1 0 1 0 2 1 1 1 1 1 1 var.sm.u..13 var.sm.u..14 var.sm.u..15 var.sm.u..16 var.sm.u..17 var.sm.u..18 1 1 1 1 1 1 1 2 0 1 1 1 1 0 var.sm.u..19 var.sm.u..20 freq prob cumulative 1 1 1 141 5.64 5.64 2 1 0 120 4.80 10.44 Displaying 2 models of the 916 visited 2 models account for 10.44% of the posterior mass

Firstly, the function provides the specified mean and variance models and the specified priors. This is followed by information about the MCMC chain and the directory where files have been stored. In addition, the function provides the null and the mean posterior deviance. Finally, the function provides the specification of the joint mean/variance models that were visited most often during MCMC sampling. This specification is in terms of a vector of indicators, each consisting of zeros and ones that show which terms are in the mean and variance model. To make clear which terms pertain to the mean and which to the variance function, we have preceded the names of the model terms by ‘mean.’ or a ‘var.’. In the above output we see that the most visited model specifies a linear mean model (only the linear term in included in the model) while the variance model includes twelve terms. See also Figure 2.

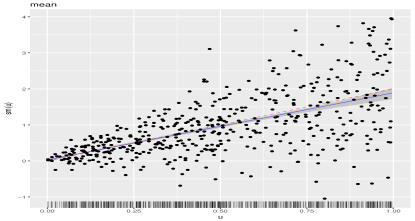

We next describe function plot.mvrm which creates plots of terms in the mean and variance functions. Two calls to function plot can be seen in the code below. Argument x expects an object of class ‘mvrm’, as created by a call to function mvrm. Argument model may take on one of three possible values: ‘mean’, ‘stdev’ or ‘both’, specifying the model to be visualized. Further, argument term determines the term to be plotted. In the current example there is only one term in each of the two models which leaves us with only one choice, term = "sm(u)". Equivalently, term may be specified as an integer, term = 1. If term is left unspecified, then by default the first term in the model is plotted. For creating two-dimensional plots, as in the current example, function plot utilizes package ggplot2. Users of BNSP may add their own options to plots via argument plotOptions. The code below serves as an example.

> x1 <- seq(0, 1, length.out = 30) > plotOptionsM <- list(geom_line(aes_string(x = x1, y = mu(x1)), col = 2, alpha = 0.5, + lty = 2), geom_point(data = data, aes(x = u, y = y))) > plot(x = m1, model = "mean", term = "sm(u)", plotOptions = plotOptionsM, + intercept = TRUE, quantiles = c(0.005, 0.995), grid = 30) > plotOptionsV = list(geom_line(aes_string(x = x1, y = stdev(x1)), col = 2, + alpha = 0.5, lty = 2)) > plot(x = m1, model = "stdev", term = "sm(u)", plotOptions = plotOptionsV, + intercept = TRUE, quantiles = c(0.05, 0.95), grid = 30)

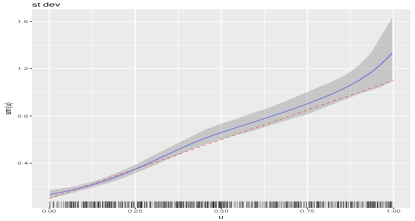

The resulting plots can be seen in Figure 2, panels (a) and (b). Panel (a) displays the simulated dataset, showing the expected increase in both the mean and variance with increasing values of the covariate . Further, we see the posterior mean of evaluated over a grid of values of , as specified by the (default) grid = 30 option in function plot. For each sample from the posterior of , and for each value of over the grid of values, function plot computes . The default option intercept = TRUE specifies that the intercept is included in the computation, but it may be removed by setting intercept = FALSE. The posterior means are computed by the usual and are plotted with solid (blue-color) line. By default, the function displays point-wise credible intervals (CI). In Figure 2 panel (a) we have plotted CIs, as specified by option quantiles = c(0.005, 0.995). This option specifies that for each value on the grid, CIs for are computed by the and quantiles of the samples . Plots without credible intervals may be obtained by setting quantiles = NULL.

Figure 2, panel (b) displays the posterior mean of the standard deviation function, given by . The details are the same as for the plot of the mean function, so here we briefly mention a difference: option intercept = TRUE specifies that is included in the calculation. It may be removed by setting intercept = FALSE, which will result in plots of .

|

|

| (a) | (b) |

|

|

| (c) | (d) |

We use the second simulated dataset to show how the s constructor from package mgcv may be used. In our example, we used s to specify the model as follows

> model <- y ~ s(u, k = 15, bs = "ps", absorb.cons=TRUE) | + s(u, k = 15, bs = "ps", absorb.cons=TRUE)

Function BNSP::s calls in turn mgcv::s and mgcv::smoothCon. All options of the last two functions may be passed to BNSP::s. In the example above we used options k, bs and absorb.cons.

The remaining R code for the second simulated example is precisely the same as the one for the first example, and hence omitted. Results are shown in Figure 2, panels (c) and (d).

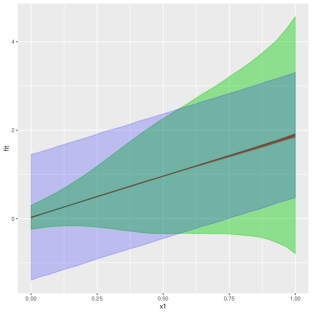

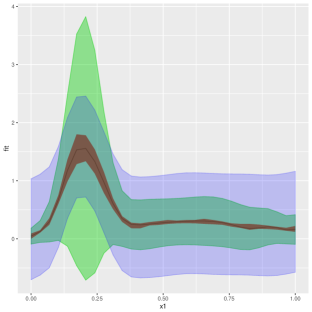

We conclude the current section by describing the function predict.mvrm. The function provides predictions and posterior credible or prediction intervals for given feature vectors. The two types of intervals differ in the associated level of uncertainty: prediction intervals attempt to capture a future response and are usually much wider than credible intervals that attempt to capture a mean response.

The following code shows how credible and prediction intervals can be obtained for a sequence of covariate values stored in x1

> x1 <- seq(0, 1, length.out = 30) > p1 <- predict(m1, newdata = data.frame(u = x1), interval = "credible") > p2 <- predict(m1, newdata = data.frame(u = x1), interval = "prediction")

where the first argument in function predict is a fitted mvrm model, the second one is a data frame containing the feature vectors at which predictions are to be obtained and the last one defines the type of interval to be created. We applied the predict function to the two simulated datasets. To each of those datasets we fitted two models: the first one is the one we saw earlier, where both the mean and variance are modeled in terms of covariates, while the second one ignores the dependence of the variance on the covariate. The latter model is specified in R using

> model <- y ~ sm(u, k = 20, bs = "rd") | 1

Results are displayed in Figure 3. Each of the two figures displays a credible interval and two prediction intervals. The figure emphasizes a point that was discussed in the introductory section, that modeling the variance in terms of covariates can result in more realistic prediction intervals. The same point was recently discussed by Mayr et al., (2012).

|

|

| (a) | (b) |

3.1.2 Bivariate covariate case

Interactions between two predictors can be modeled by appropriate specification of either the built-in sm function or the smooth constructors from mgcv. Function sm can take up to two covariates, both of which may be continuous or one continuous and one discrete. Next we consider an example that involves two continuous covariates. An example involving a continuous and a discrete covariate is shown later on, in the second application to a real dataset.

Let denote a bivariate predictor. The data-generating mechanism that we consider is

As before, and are obtained independently from uniform distributions on the unit interval. Further, the sample size is set to .

In R, we simulate data from the above mechanism using

> mu1 <- matrix(c(0.25, 0.75))

> sigma1 <- matrix(c(0.03, 0.01, 0.01, 0.03), 2, 2)

> mu2 <- matrix(c(0.65, 0.35))

> sigma2 <- matrix(c(0.09, 0.01, 0.01, 0.09), 2, 2)

> mu <- function(x1, x2) {x <- cbind(x1, x2);

+ 0.1 + dmvnorm(x, mu1, sigma1) + dmvnorm(x, mu2, sigma2)}

> Sigma <- function(x1, x2) {x <- cbind(x1, x2);

+ 0.1 + (dmvnorm(x, mu1, sigma1) + dmvnorm(x, mu2, sigma2)) / 2}

> set.seed(1)

> n <- 500

> w1 <- runif(n)

> w2 <- runif(n)

> y <- vector()

> for (i in 1 : n) y[i] <- rnorm(1, mean = mu(w1[i], w2[i]),

+ sd = sqrt(Sigma(w1[i], w2[i])))

> data <- data.frame(y, w1, w2)

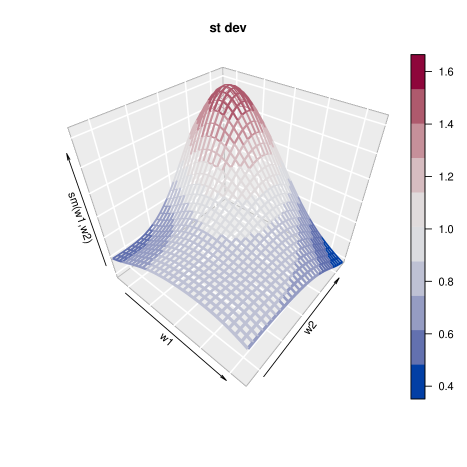

We fit a model with mean and variance functions specified as

The R code that fits the above model is

> Model <- y ~ sm(w1, w2, k = 10, bs = "rd") | sm(w1, w2, k = 10, bs = "rd") > m2 <- mvrm(formula = Model, data = data, sweeps = 10000, burn = 5000, thin = 2, + seed = 1, StorageDir = DIR)

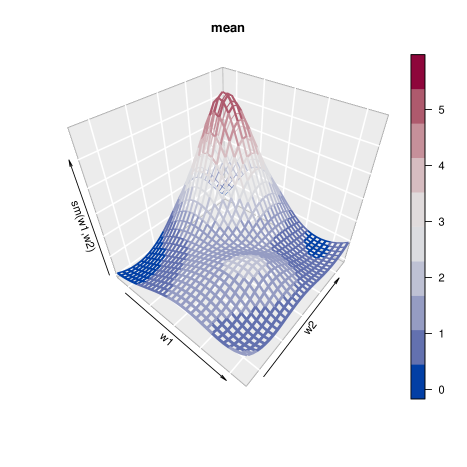

As in the univariate case, convergence assessment and univariate posterior summaries may be obtained by using function mvrm2mcmc in conjunction with functions plot.mcmc and summary.mcmc. Further, summaries of the ‘mvrm’ fits may be obtained using functions print.mvrm and summary.mvrm. Plots of the bivariate effects may be obtained using function plot.mvrm. This is shown below, where argument plotOptions utilizes package colorspace (Zeileis et al.,, 2009).

> plot(x = m2, model = "mean", term = "sm(w1,w2)", static = TRUE, + plotOptions = list(col = diverge_hcl(n = 10))) > plot(x = m2, model = "stdev", term = "sm(w1,w2)", static = TRUE, + plotOptions = list(col = diverge_hcl(n = 10)))

Results are shown in Figure 4. For bivariate predictors, function plot.mvrm calls function ribbon3D from package plot3D. Dynamic plots, viewable in a browser, can be created by replacing the default static = TRUE by static = FALSE. When the latter option is specified, function plot.mvrm calls function scatterplot3js from package threejs. Users may pass their own options to plot.mvrm via the plotOptions argument.

|

|

| (a) | (b) |

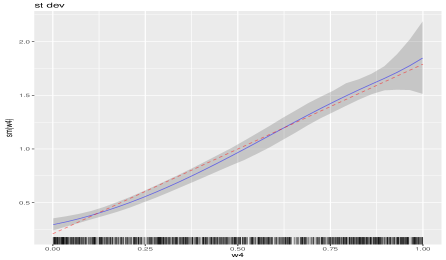

3.1.3 Multiple covariate case

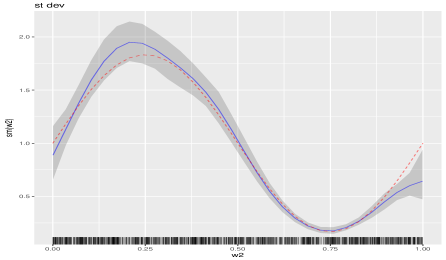

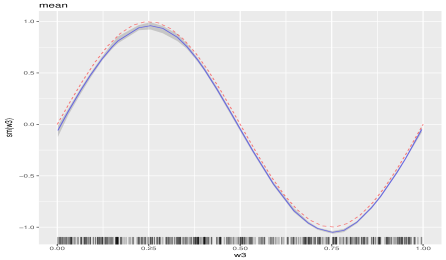

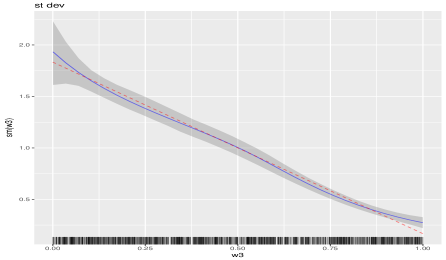

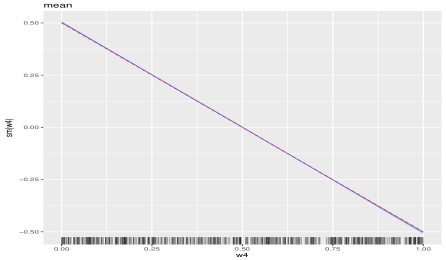

We consider fitting general additive models for the mean and variance functions in a simulated example with four independent continuous covariates. In this scenario, we set . Further the covariates are simulated independently from a uniform distribution on the unit interval. The data-generating mechanism that we consider is

where functions are specified below

-

1.

,

-

2.

, -

3.

,

-

4.

.

To the generated dataset we fit a model with mean and variance functions modeled as

Fitting the above model to the simulated data is achieved by the following R code

> Model <- y ~ sm(w1, k = 15, bs = "rd") + sm(w2, k = 15, bs = "rd") + + sm(w3, k = 15, bs = "rd") + sm(w4, k = 15, bs = "rd") | + sm(w1, k = 15, bs = "rd") + sm(w2, k = 15, bs = "rd") + + sm(w3, k = 15, bs = "rd") + sm(w4, k = 15, bs = "rd") > m3 <- mvrm(formula = Model, data = data, sweeps = 50000, burn = 25000, + thin = 5, seed = 1, StorageDir = DIR)

By default function sm utilizes the radial basis functions, hence there is no need to specify bs = "rd" as we did earlier, if radial basis functions are preferred over thin plate splines. Further, we have selected k = 15 for all smooth functions. However, there is no restriction to the number of knots and certainly one can select a different number of knots for each smooth function.

As discussed previously, for each term that appears in the right-hand side of the mean and variance functions, the model incorporates indicator variables that specify which basis functions are to be included and which are to be excluded from the model. For the current example, the indicator variables are denoted by and . The prior probabilities that variables are included were specified in (8) and they are specific to each term, The default option pi.muPrior = "Beta(1,1)" specifies that Further, by setting, for example, pi.muPrior = "Beta(2,1)" we specify that To specify a different Beta prior for each of the four terms, pi.muPrior will have to be specified as a vector of length four, as an example, pi.muPrior = c("Beta(1,1)","Beta(2,1)","Beta(3,1)","Beta(4,1)"). Specification of the priors for is done in a similar way, via argument pi.sigmaPrior.

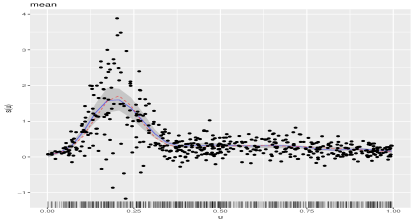

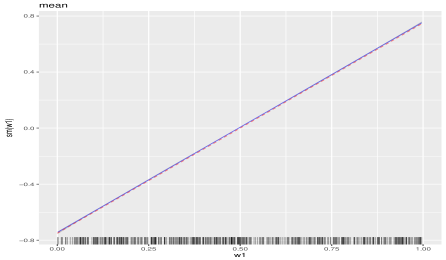

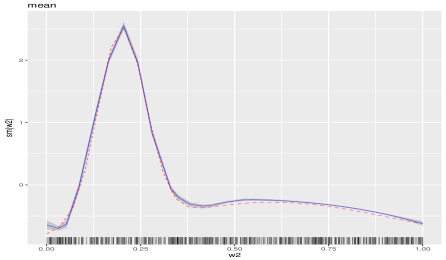

We conclude this section by presenting plots of the four terms in the mean and variance models. The plots are presented in Figure 5. We provide a few details on how function plot works in the presence of multiple terms, and how the comparison between true and estimated effects is made. Starting with the mean function, to create the relevant plots, that appear on the left panels of Figure 5, function plot considers only the part of the mean function that is related to the chosen term while leaving all other terms out. For instance, in the code below we choose term = "sm(u1)" and hence we plot the posterior mean and a posterior credible interval for , where the intercept is left out by option intercept = FALSE. Further, comparison is made with a centered version of the true curve, represented by the dashed (red color) line and obtained by the first three lines of code below.

> x1 <- seq(0, 1, length.out = 30) > y1 <- mu1(x1) > y1 <- y1 - mean(y1) > PlotOptions <- list(geom_line(aes_string(x = x1, y = y1), + col = 2, alpha = 0.5, lty = 2)) > plot(x = m3, model = "mean", term = "sm(w1)", plotOptions = PlotOptions, + intercept = FALSE, centreEffects = FALSE, quantiles = c(0.005, 1 - 0.005))

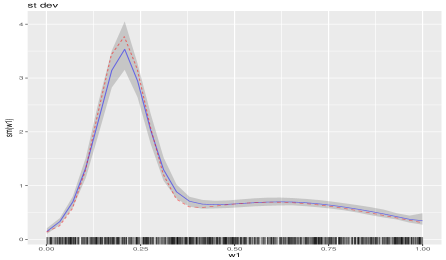

The plots of the four standard deviation terms are shown in the right panels of Figure 5. Again, these are created by considering only the part of the model for that is related to the chosen term. For instance, below we choose term = "sm(u1)". Hence, in this case the plot will present the posterior mean and a posterior credible interval for , where the intercept is left out by option intercept = FALSE. Option centreEffects = TRUE scales the posterior realizations of before plotting them, where the scaling is done in such a way that the realized function has mean one over the range of the predictor. Further, the comparison is made with a scaled version of the true curve, where again the scaling is done to achieve mean one. This is shown below and it is in the spirit of Chan et al., (2006) who discuss the differences between the data generating mechanism and the fitted model.

> y1 <- stdev1(x1) / mean(stdev1(x1)) > PlotOptions <- list(geom_line(aes_string(x = x1, y = y1), + col = 2, alpha = 0.5, lty = 2)) > plot(x = m3, model = "stdev", term = "sm(w1)", plotOptions = PlotOptions, + intercept = FALSE, centreEffects = TRUE, quantiles = c(0.025, 1 - 0.025))

|

|

|

|

|

|

|

|

3.2 Data analyses

In this section we present four empirical applications.

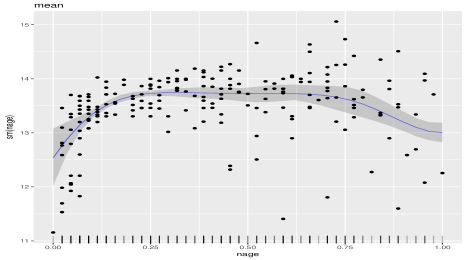

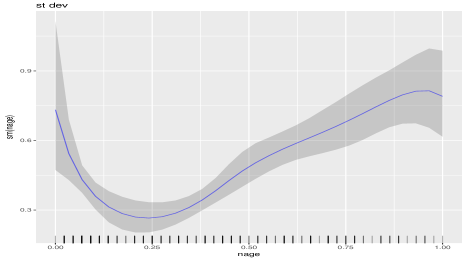

3.2.1 Wage and age

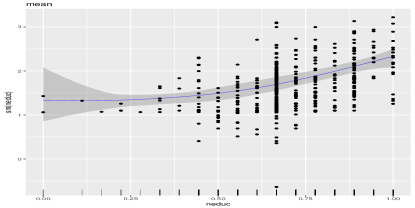

In the first empirical application, we analyse a dataset from Pagan & Ullah, (1999) that is available in the R package np (Hayfield & Racine,, 2008). The dataset consists of observations on dependent variable logwage, the logarithm of the individual’s wage, and covariate age, the individual’s age. The dataset comes from the 1971 Census of Canada Public Use Sample Tapes and the sampling units it involves are males of common education. Hence, the investigation of the relationship between age and the logarithm of wage is carried out controlling for the two potentially important covariates education and gender.

We utilize the following R code to specify flexible models for the mean and variance functions, and to obtain posterior samples, after a burn-in period of samples and a thinning period of .

> data(cps71) > DIR <- getwd() > model <- logwage ~ sm(age, k = 30, bs = "rd") | sm(age, k = 30, bs = "rd") > m4 <- mvrm(formula = model, data = cps71, sweeps = 50000, + burn = 25000, thin = 5, seed = 1, StorageDir = DIR)

After checking convergence, we use the following code to create the plots that appear in Figure 6.

> wagePlotOptions <- list(geom_point(data = cps71, aes(x = age, y = logwage))) > plot(x = m4, model = "mean", term = "sm(age)", plotOptions = wagePlotOptions) > plot(x = m4, model = "stdev", term = "sm(age)")

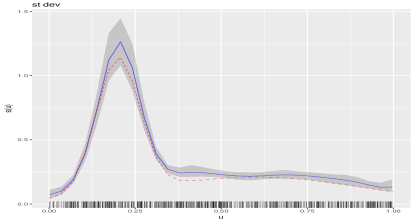

Figure 6 (a) shows the posterior mean and an credible interval for the mean function and it suggests a quadratic relationship between age and logwage. Figure 6 (b) shows the posterior mean and an credible interval for the standard deviation function. It suggest a complex relationship between age and the variability in logwage. The relationship suggested by Figure 6 (b) is also suggested by the spread of the data-points around the estimated mean in Figure 6 (a). At ages around years the variability in logwage is high. It then reduces until about age , to start increasing again until about age . From age to it remains stable but high, while for ages above , Figure 6 (b) suggests further increase in the variability, but the wide credible interval suggests high uncertainty over this age range.

|

|

| (a) | (b) |

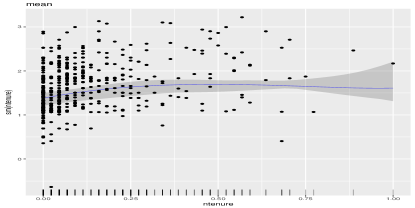

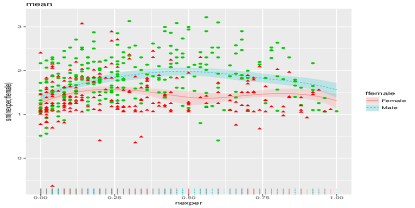

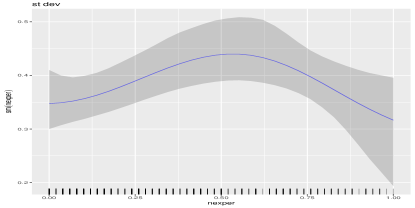

3.2.2 Wage and multiple covariates

In the second empirical application, we analyse a dataset from Wooldridge, (2008) that is also available in R package np. The response variable here is the logarithm of the individual’s hourly wage (lwage) while the covariates include the years of education (educ), the years of experience (exper), the years with the current employer (tenure), the individual’s gender (named as female within the dataset, with levels Female and Male), and marital status (named as married with levels Married and Notmarried). The dataset consists of independent observations. We analyse the first three covariates as continuous and the last two as discrete.

As the variance function is modeled in terms of an exponential, see (1), to avoid potential numerical problems, we transform the three continuous variables to have range in the interval , using

> data(wage1) > wage1$ntenure <- wage1$tenure / max(wage1$tenure) > wage1$nexper <- wage1$exper / max(wage1$exper) > wage1$neduc <- wage1$educ / max(wage1$educ)

We choose to fit the following mean and variance models to the data

We note that, as it turns out, an interaction between variables nexper and female is not necessary for the current data analysis. However, we choose to add this term in the mean model in order to illustrate how interaction terms can be specified. We illustrate further options below.

> knots1 <- seq(min(wage1$nexper), max(wage1$nexper), length.out = 30) > knots2 <- c(0, 1) > knotsD <- expand.grid(knots1, knots2) > model <- lwage ~ fmarried + sm(ntenure) + sm(neduc, knots=data.frame(knots = + seq(min(wage1$neduc), max(wage1$neduc), length.out = 15))) + + sm(nexper, ffemale, knots = knotsD) | sm(nexper, knots=data.frame(knots = + seq(min(wage1$nexper), max(wage1$nexper), length.out=15)))

The first three lines of the R code above specify the matrix of (potential) knots to be used for representing . Knots may be left unspecified, in which case the defaults in function sm will be used. Furthermore, in the specification of the mean model we use sm(ntenure). By this, we chose to represent utilizing the default knots and the radial basis functions. Further, the specification of in the mean model illustrates how users can specify their own knots for univariate functions. In the current example, we select knots uniformly spread over the range of neduc. Fifteen knots are also used to represent within the variance model.

The following code is used to obtain samples from the posteriors of the model parameters.

> DIR <- getwd() > m5 <- mvrm(formula = model, data = wage1, sweeps = 100000, + burn = 25000, thin = 5, seed = 1, StorageDir = DIR))

After summarizing results and checking convergence, we create plots of posterior means, along with credible intervals, for functions . These are displayed in Figure 7. As it turns out, variable married does not have an effect on the mean of lwage. For this reason, we do not provide further results on the posterior of the coefficient of covariate married, . However, in the code below we show how graphical summaries on can be obtained, if needed.

> PlotOptionsT <- list(geom_point(data = wage1, aes(x = ntenure, y = lwage))) > plot(x = m5, model = "mean", term="sm(ntenure)", quantiles = c(0.025, 0.975), + plotOptions = PlotOptionsT) > PlotOptionsEdu <- list(geom_point(data = wage1, aes(x = neduc, y = lwage))) > plot(x = m5, model = "mean", term = "sm(neduc)", quantiles = c(0.025, 0.975), + plotOptions = PlotOptionsEdu) > pchs <- as.numeric(wage1$female) > pchs[pchs == 1] <- 17; pchs[pchs == 2] <- 19 > cols <- as.numeric(wage1$female) > cols[cols == 2] <- 3; cols[cols == 1] <- 2 > PlotOptionsE <- list(geom_point(data = wage1, aes(x = nexper, y = lwage), + col = cols, pch = pchs, group = wage1$female)) > plot(x = m5, model = "mean", term="sm(nexper,female)", quantiles = c(0.025, 0.975), + plotOptions = PlotOptionsE) > plot(x = m5, model = "stdev", term = "sm(nexper)", quantiles = c(0.025, 0.975)) > PlotOptionsF <- list(geom_boxplot(fill = 2, color = 1)) > plot(x = m5, model = "mean", term = "married", quantiles = c(0.025, 0.975), + plotOptions = PlotOptionsF)

|

|

| (a) | (b) |

|

|

| (c) | (d) |

Figure 7, panels (a) and (b) show the posterior means and credible intervals for and . It can be seen that expected wages increase with tenure and education, although there is high uncertainty over a large part of the range of both covariates. Panel (c) displays the posterior mean and a credible interval for . We can see that although the forms of the two functions are similar, i.e. the interaction term is not needed, males have higher expected wages than females. Lastly, panel (d) displays posterior summaries of the standard deviation function, . It can be seen that variability first increases and then decreases as experience increases.

Lastly, we obtain predictions and credible intervals for the levels "Married" and "Notmarried" of variable fmaried and the levels "Female" and "Male" of variable ffemale, with variables ntenure, nedc and nexper fixed at their mid-range.

> p1 <- predict(m5, newdata = data.frame(fmarried = rep(c("Married", "Notmarried"), 2),

+ ntenure = rep(0.5, 4), neduc = rep(0.5, 4), nexper = rep(0.5, 4),

+ ffemale = rep(c("Female", "Male"), each = 2)), interval = "credible")

> p1

fit lwr upr

1 1.321802 1.119508 1.506574

2 1.320400 1.119000 1.505272

3 1.913341 1.794035 2.036255

4 1.911939 1.791578 2.034832

The predictions are suggestive of no ‘marriage’ effect and of ‘gender’ effect.

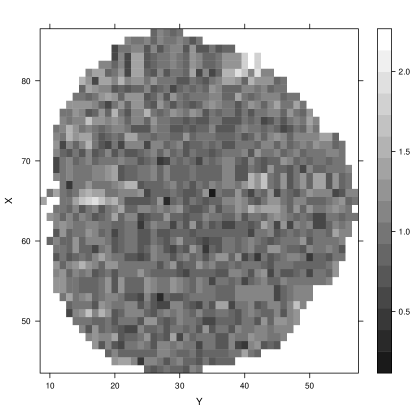

3.2.3 Brain activity

Here we analyse brain activity level data obtained by functional magnetic resonance imaging. The dataset is available in package gamair (Wood,, 2006) and it was previously analysed by Landau et al., (2003). We are interested in three of the columns in the dataset. These are the response variable, medFPQ, which is calculated as the median over three measurements of ‘Fundamental Power Quotient’ and the two covariates, X and Y, which show the location of each voxel.

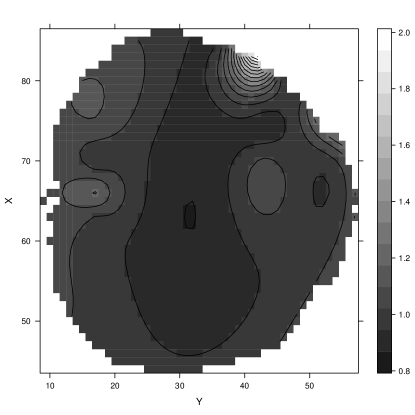

The following R code loads the relevant data frame, removes two outliers and transforms the response variable, as was suggested by Wood, (2006). In addition, it plots the brain activity data using function levelplot from package lattice (Sarkar,, 2008).

> data(brain) > brain <- brain[brain$medFPQ > 5e-5, ] > brain$medFPQ <- (brain$medFPQ) ^ 0.25 > levelplot(medFPQ ~ Y * X, data = brain, xlab = "Y", ylab = "X", + col.regions = gray(10 : 100 / 100))

The plot of the observed data is shown in Figure 8, panel (a). Its distinctive feature is the noise level, which makes difficult to decipher any latent pattern. Hence, the goal of the current data analysis is to obtain a smooth surface of brain activity level from the noisy data. It was argued by Wood, (2006) that for achieving this goal a spatial error term is not needed in the model. Thus, we analyse the brain activity level data using a model of the form

where is the number of voxels.

The R code that fits the above model is

> Model <- medFPQ ~ sm(Y, X, k = 10, bs = "rd") | 1 > m6 <- mvrm(formula = Model, data = brain, sweeps = 50000, burn = 20000, thin = 2, + seed = 1, StorageDir = DIR)

From the fitted model we obtain a smooth brain activity level surface using function predict. The function estimates the average activity at each voxel of the brain. Further, we plot the estimated surface using function levelplot.

> p1 <- predict(m6) > levelplot(p1[, 1] ~ Y * X, data = brain , xlab = "Y", ylab = "X", + col.regions = gray(10 : 100 / 100), contour = TRUE)

Results are shown in Figure 8, panel(b). The smooth surface makes it much easier to see and understand which parts of the brain have higher activity.

|

|

| (a) | (b) |

3.2.4 Cars

In the fourth and final application we use function mvrm to identify the best subset of predictors in a regression setting. Usually stepwise model selection is performed, using functions step and stepAIC in R. Here we show how mvrm can be used as alternative to those two functions. The data frame that we apply mvrm on is mtcars, where the response variable is mpg and the explanatory variables that we consider are disp, hp, wt and qsec. The code below loads the data frame, specifies the model and obtains samples from the posteriors of the model parameters.

> data(mtcars) > Model <- mpg ~ disp + hp + wt + qsec | 1 > m7 <- mvrm(formula = Model, data = mtcars, sweeps = 50000, burn = 25000, thin = 2, + seed = 1, StorageDir = DIR)

The following is an excerpt of the output that function summary produces and it shows the three models with the highest posterior probability.

> summary(m7, nModels = 3) Joint mean/variance model posterior probabilities: mean.disp mean.hp mean.wt mean.qsec freq prob cumulative 1 0 1 1 0 1085 43.40 43.40 2 0 0 1 1 1040 41.60 85.00 3 0 0 1 0 128 5.12 90.12 Displaying 3 models of the 11 visited 3 models account for 90.12% of the posterior mass

The model with the highest posterior probability () is the one that includes explanatory variables hp and wt. The model that includes wt and qsec has almost equal posterior probability, . These two models account of of the posterior mass. The third most promising model is the one that includes only wt as predictor, but its posterior probability is much lower, .

4 Appendix: MCMC algorithm

In this section we present the technical details of how the MCMC algorithm is designed for the case where there is a single covariate in the mean and variance models. We first note that to improve mixing of the sampler, we integrate out vector from the likelihood of , as was done by Chan et al., (2006)

| (10) |

where, with , we have .

The six steps of the MCMC sampler are as follows

-

1.

Similar to Chan et al., (2006), the elements of are updated in blocks of randomly chosen elements. The block size is chosen based on probabilities that can be supplied by the user or be left at their default values. Let be a block of random size of randomly chosen elements from . The proposed value for is obtained from its prior with the remaining elements of , denoted by , kept at their current value. The proposal pmf is obtained from the Bernoulli prior with integrated out

where denotes the length of i.e. the size of the block. For this proposal pmf, the acceptance probability of the Metropolis-Hastings move reduces to the ratio of the likelihoods in (10)

where superscripts and denote proposed and currents values respectively.

-

2.

Vectors and are updated simultaneously. Similarly to the updating of , the elements of are updated in random order in blocks of random size. Let denote a block. Blocks and the whole vector are generated simultaneously. As was mentioned by Chan et al., (2006), generating the whole vector , instead of subvector , is necessary in order to make the proposed value of consistent with the proposed value of .

Generating the proposed value for is done in a similar way as was done for in the previous step. Let denote the proposed value of . Next, we describe how the proposed vale for is obtained. The development is in the spirit of Chan et al., (2006) who built on the work of Gamerman, (1997).

Let denote the current value of the posterior mean of . Define the current squared residuals

. These will have an approximate distribution, where . The latter defines a Gamma generalized linear model (GLM) for the squared residuals with mean , which, utilizing a -link, can be thought of as Gamma GLM with an offset term: . Given the proposed value of , denoted by , the proposal density for is derived utilizing the one step iteratively re-weighted least squares algorithm. This proceeds as follows. First define the transformed observations

where superscript denotes current values. Further, let denote the vector of .

Next we define

where is the design matrix. The proposed value is obtained from a multivariate normal distribution with mean and covariance , denoted as , where is a free parameter that we introduce and select its value adaptively (Roberts & Rosenthal,, 2009) in order to achieve an acceptance probability of (Roberts & Rosenthal,, 2001).

Let denote the proposal density for taking a step in the reverse direction, from model to . Then the acceptance probability of the pair is the minimum between 1 and

We note that the determinants that appear in the above ratio are equal to one when utilizing centred explanatory variables in the variance model and hence can be left out of the calculation of the acceptance probability.

-

3.

We update utilizing the marginal (10) and the two priors in (7). The full conditional corresponding to the IG prior is

which is recognized as another inverse gamma IG distribution.

The full conditional corresponding to the normal prior is

Proposed values are obtained from where denotes the current value. Proposed values are accepted with probability . We treat as a tuning parameter and we select its value adaptively (Roberts & Rosenthal,, 2009) in order to achieve an acceptance probability of (Roberts & Rosenthal,, 2001).

-

4.

Parameter is updated from the marginal (10) and the IG prior

To sample from the above, we utilize a normal approximation to it. Let . We utilize a normal proposal density where is the mode of , found using a Newton-Raphson algorithm, is the second derivative of evaluated at the mode, and is a tuning variance parameter the value of which is chosen adaptively (Roberts & Rosenthal,, 2009). At iteration the acceptance probability is the minimum between one and

-

5.

Parameter is updated from the inverse Gamma density IG.

-

6.

The sampler utilizes the marginal in (10) to improve mixing. However, if samples are required from the posterior of , they can be generated from

where is the non-zero part of .

5 Summary

We have presented a tutorial on several functions from the R package BNSP. These functions are used for specifying, fitting and summarizing results from regression models with Gaussian errors and with mean and variance functions that can be modeled nonparametrically. Function sm is utilized to specify smooth terms in the mean and variance functions of the model. Function mvrm calls an MCMC algorithm that obtains samples from the posteriors of the model parameters. Samples are converted into an object of class ‘mcmc’ by function mvrm2mcmc which facilitates the use of multiple functions from package coda. Functons print.mvrm and summary.mvrm provide summaries of fitted ‘mvrm’ objects. Further, function plot.mvrm provides graphical summaries of parametric and nonparametric terms that enter the mean or variance function. Lastly, function predict.mvrm provides predictions for a future response or a mean response along with the corresponding prediction/credible intervals.

References

- Bürkner, (2018) Bürkner, P.-C. (2018). brms: Bayesian Regression Models using ‘Stan’. R package version 2.3.1.

- Chan et al., (2006) Chan, D., Kohn, R., Nott, D., & Kirby, C. (2006). Locally adaptive semiparametric estimation of the mean and variance functions in regression models. Journal of Computational and Graphical Statistics, 15(4), 915–936.

- Gamerman, (1997) Gamerman, D. (1997). Sampling from the posterior distribution in generalized linear mixed models. Statistics and Computing, 7(1), 57–68.

- George & McCulloch, (1993) George, E. I. & McCulloch, R. E. (1993). Variable selection via Gibbs sampling. Journal of the American Statistical Association, 88(423), 881–889.

- George & McCulloch, (1997) George, E. I. & McCulloch, R. E. (1997). Approaches for Bayesian variable selection. Statistica Sinica, 7(2), 339–373.

- Hayfield & Racine, (2008) Hayfield, T. & Racine, J. S. (2008). Nonparametric econometrics: The np package. Journal of Statistical Software, 27(5).

- Hofner et al., (2018) Hofner, B., Mayr, A., Fenske, N., & Schmid, M. (2018). gamboostLSS: Boosting Methods for GAMLSS Models. R package version 2.0-1.

- Landau et al., (2003) Landau, S., Ellison-Wright, I. C., & Bullmore, E. T. (2003). Tests for a difference in timing of physiological response between two brain regions measured by using functional magnetic resonance imaging. Journal of the Royal Statistical Society: Series C (Applied Statistics), 53(1), 63–82.

- Lewis, (2016) Lewis, B. W. (2016). threejs: Interactive 3D Scatter Plots, Networks and Globes. R package version 0.2.2.

- Liang et al., (2008) Liang, F., Paulo, R., Molina, G., Clyde, M. A., & Berger, J. O. (2008). Mixtures of g Priors for Bayesian variable selection. Journal of the American Statistical Association, 103(481), 410–423.

- Mayr et al., (2012) Mayr, A., Fenske, N., Hofner, B., Kneib, T., & Schmid, M. (2012). Generalized additive models for location, scale and shape for high dimensional data-a flexible approach based on boosting. Journal of the Royal Statistical Society: Series C (Applied Statistics), 61(3), 403–427.

- Müller & Mitra, (2013) Müller, P. & Mitra, R. (2013). Bayesian nonparametric inference - why and how. Bayesian Analysis, 8(2), 269–302.

- O’Hara & Sillanpää, (2009) O’Hara, R. B. & Sillanpää, M. J. (2009). A review of Bayesian variable selection methods: What, how and which. Bayesian Analysis, 4(1), 85–117.

- Pagan & Ullah, (1999) Pagan, A. & Ullah, A. (1999). Nonparametric Econometrics. Cambridge University Press.

- Papageorgiou, (2018) Papageorgiou, G. (2018). BNSP: Bayesian Non- And Semi-Parametric Model Fitting. R package version 2.0.8.

- Plummer et al., (2006) Plummer, M., Best, N., Cowles, K., & Vines, K. (2006). Coda: Convergence diagnosis and output analysis for mcmc. R News, 6(1), 7–11.

- R Core Team, (2016) R Core Team (2016). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Rigby & Stasinopoulos, (2005) Rigby, R. A. & Stasinopoulos, D. M. (2005). Generalized additive models for location, scale and shape, (with discussion). Journal of the Royal Statistical Society: Series C (Applied Statistics), 54(3), 507–554.

- Roberts & Rosenthal, (2001) Roberts, G. O. & Rosenthal, J. S. (2001). Optimal scaling for various Metropolis-Hastings algorithms. Statistical Science, 16(4), 351–367.

- Roberts & Rosenthal, (2009) Roberts, G. O. & Rosenthal, J. S. (2009). Examples of adaptive MCMC. Journal of Computational and Graphical Statistics, 18(2), 349–367.

- Sarkar, (2008) Sarkar, D. (2008). Lattice: Multivariate Data Visualization with R. New York: Springer. ISBN 978-0-387-75968-5.

- Scheipl, (2011) Scheipl, F. (2011). spikeSlabGAM: Bayesian variable selection, model choice and regularization for generalized additive mixed models in R. Journal of Statistical Software, 43(14), 1–24.

- Scheipl, (2016) Scheipl, F. (2016). spikeSlabGAM: Bayesian Variable Selection and Model Choice for Generalized Additive Mixed Models. R package version 1.1-11.

- Soetaert, (2016) Soetaert, K. (2016). plot3D: Plotting Multi-Dimensional Data. R package version 1.1.

- Stasinopoulos & Rigby, (2007) Stasinopoulos, D. M. & Rigby, R. A. (2007). Generalized additive models for location scale and shape (GAMLSS) in R. Journal of Statistical Software, 23(7), 1–46.

- Umlauf et al., (2018) Umlauf, N., Klein, N., & Zeileis, A. (2018). BAMLSS: Bayesian additive models for location, scale and shape (and beyond). Journal of Computational and Graphical Statistics.

- Umlauf et al., (2017) Umlauf, N., Klein, N., Zeileis, A., & Koehler, M. (2017). bamlss: Bayesian Additive Models for Location Scale and Shape (and Beyond). R package version 0.1-2.

- Wickham, (2009) Wickham, H. (2009). ggplot2: Elegant Graphics for Data Analysis. Springer-Verlag New York.

- Wood, (2018) Wood, S. (2018). mgcv: Mixed GAM Computation Vehicle with Automatic Smoothness Estimation. R package version 1.8-23.

- Wood, (2006) Wood, S. N. (2006). Generalized Additive Models: An Introduction with R. Boca Raton, Florida: Chapman and Hall/CRC. ISBN 1-58488-474-6.

- Wooldridge, (2008) Wooldridge, J. (2008). Introductory Econometrics: A Modern Approach. South Western College.

- Zeileis & Croissant, (2010) Zeileis, A. & Croissant, Y. (2010). Extended model formulas in R: Multiple parts and multiple responses. Journal of Statistical Software, 34(1), 1–13.

- Zeileis et al., (2009) Zeileis, A., Hornik, K., & Murrell, P. (2009). Escaping RGBland: Selecting colors for statistical graphics. Computational Statistics & Data Analysis, 53(9), 3259–3270.

- Zellner, (1986) Zellner, A. (1986). On assessing prior distributions and Bayesian regression analysis with g-prior distributions. In P. Goel & Zellner (Eds.), Bayesian Inference and Decision Techniques: Essays in Honor of Bruno de Finetti (pp. 233–243).: Elsevier Science Publishers.