On Time-Varying Amplitude HGARCH Model

Ferdous Mohammadi Basatini and Saeid Rezakhah111email: rezakhah@aut.ac.ir

Amirkabir University of Technology

424 Hafez Avenue, Tehran 15914, Iran.

Abstract

The HGARCH model allows long-memory impact in volatilities. A new HGARCH model with time-varying amplitude is considered in this paper. We show the stability of the model as well. A score test is introduced to check the time-varying behavior in amplitude. Some value-at-risk tests are applied to evaluate the forecastings. Simulations are provided which provide further support to the proposed model. We have also have shown the competative performance of our model in forecasting, by compairing it with HGARH and FIGARCH models for some period of SP500 indices.

Keyword: HGARCH, long-memory, time-varying, amplitude.

JEL: 13, 22, 58

Mathematics Subject Classification: 91B84, 91B30, 62F03

1 Introduction

Determining the volatility structure is the main step in measuring risk in financial time series. The GARCH models (Engle, 1982; Bollerslev,1986) are widely used for modeling volatility. Two kinds of structure are recognized for GARCH models as geometric and hyperbolic decaying that can be described as some kinds of short-memory and long-memory respectively. Long-memory property is present in the volatility of many financial data (Kwan et al., 2011). As a hyperbolic-memory model, HYGARCH (Davidson, 2004) is the most popular one and has shown good performance in modeling long-memory behavior for many financial time series (Davidson, 2004; Tang and Shieh, 2006). The conditional variance of HYGARCH model is a convex combination of the conditional variances of GARCH (Bollerslev, 1986) and FIGARCH (Baillie, 1996). The FIGARCH also shows hyperbolic-memory but has infinite variance. Li et al. (2015) argued that the conditional variance of the HYGARCH model has an unnecessarily complicated form. This motivated them to propose a new hyperbolic GARCH (HGARCH) model which is as simple as FIGARCH but has finite variance.

Financial time series often have time-varying volatilities which in many cases follow long memory in effect of exogenous and endogenous shocks. Thus models with time-varying structure are more appropriate for many financial time series. We consider a HGARCH model with logistic time-varying amplitude to impose a more flexible behavior which we call TV-HGARCH. This time-varying amplitude allows the conditional variance to be more sensitive to the last observation. So when a sudden shock influences the volatilities the TV-HGARCH permits the magnitude of variations in the conditional variance changes and so make more dynamical behavior. We show under some regularity conditions the moments of the model are bounded. Maximum likelihood estimators (MLEs) of the parameters are derived. We develop a score test to check the presence of the time-varying amplitude in the proposed TV-HGARCH structure. The asymptotic behavior of MLEs and score test is verified by simulation. Value-at-risk (VaR) is a useful measure for quantifying the risk which depends directly on the volatility. The forecasts from various volatility models are evaluated and compared on the basis of how well they forecast VaR. Hence, we perform some statistical hypothesis testing to compare the VaR forecasts of competing models. We consider S&P500 indices from 17th February 2009 to 30th January 2015 to show the competitive behavior of TV-HGARCH model in compare to HGARCH and FIGARCH. The paper organized as follows. The TV-HGARCH model and the moment properties are given in section 2. Maximum likelihood estimation is proposed in section 3. A score test is developed in Section 4 for checking time-varying amplitude. Section 5 reports the simulation studies. The VaR forecasting and its statistical testings are provided in Section 6. The performance of the model for the empirical data of S&P500 indices is reported in Section 7. Conclusions are presented in the last section.

2 The model

Let follows a HGARCH() model as

| (2.1) |

where are identically and independently (i.i.d.) random variables with mean 0 and variance 1, , is the back-shift operator, , and are known positive integers; also where in which . Let be the information up to t-1 then is the conditional variance as, . The parameter is called the amplitude parameter that determines the magnitude of variations in the conditional variance (Kwan et al., 2012). For the model will reduce to the FIGARCH. In this model the has fixed form by enriching the HGARCH model with a time-varying amplitude we provide a more dynamical model for describing the volatilities.

2.1 The Time-Varying HGARCH Model

Let follows the TV-HGARCH() model as

| (2.2) |

where , are defined as in (2.1). Here is a logistic time-varying function defined as

| (2.3) |

It is clear that bounded between 0,1. is called the smoothness parameter which determines the speed of transition between high and low volatility. In financial time series several possible choices for the transition variable, are proposed (Dijk et al., 2002; McAleer, 2008). We consider so the amplitude changes with the size of the last observation and hence the magnitude of the last shock cause of the smooth changes of the conditional variance.

2.2 Moment properties

Now we study the moments of the . Let , we can rewrite model (2.2) into the form:

where the ’s for are functions of . Denote , and . Note that , assuming that and using the fact that it holds that

| (2.4) | ||||

| (2.5) | ||||

| (2.6) | ||||

| (2.7) |

By the law of iterated expectations,

Using Holder’s inequality, it holds that

and therefore

| (2.8) |

The right hand side of (2.8) is a recursive relation, so if the are exist the condition is sufficient condition for the existence of the . We find that for the condition (2.8) is the same as the conditions for ARFIMA-HYGARCH model presented by Kwan et al. (2012). As an example, we calculate the second-order moment for the TV-HGARCH(1,d,1) model

After some calculations it holds that

| (2.9) |

Also if and for we have that

and therefore

Thus the is sufficient for the existence of the second-order moment of the ; i.e. .

3 Estimation

Let denotes the parameter vector of the TV-HGARCH model defined in relations (2.2) - (2.3) and refers to the conditional variance of the when the true parameters in TV-HGARCH model are replaced by the corresponding unknown parameters. Suppose the are a sample from the TV-HGARCH model. By assuming the normality on , the conditional log likelihood function is where

The derivatives of with respect to the parameters are given as follows:

where refers to the element of the . The partial derivatives of are obtained as:

Here we need some numerical approaches such as quasi-Newton algorithms to find the maximum likelihood estimator of the (Chong and Zak, 2001).

4 Testing Time-Varying Amplitude

For fitted HGARCH a score test is developed to check the presence of the time-varying amplitude in the model. It is very proper test because only requires the constrained estimator under . The null hypothesis of testing time-varying amplitude corresponds to testing against in the TV-HGARCH model defined by relations (2.2) - (2.3). Under null hypothesis . The null hypothesis implies the absence of the time-varying amplitude and we obtain standard HGARCH model (Amado and Teräsvirta, 2008). Consider the conditional log-likelihood function where

At following the indicates the maximum likelihood estimator under .

Let is the average score test vector and is the population information matrix. Consider as true parameter vector under . The score test statistic is defined as follows:

| (4.1) |

Also, let where and

. So

| (4.2) |

and

Under normality, the population information matrix equals to negative expected value of the average Hessian matrix:

Note (4.1) depend on the unknown parameter value so it is useless. It is common to evaluate the at the to get a usable statistic. Hence

| (4.3) |

where

| (4.4) |

Denote

| (4.5) |

5 Simulation Study

This section conducts two simulation experiments to investigate the consistency of the MLEs (section 3) and the asymptotic behavior of the score test (section 4). We consider three sample sizes, n=300, 500 and 1000 in two experiments, and there are 1000 replications for each sample size. In each generated sequence the first 1000 observations have been discarded to avoid the initialization effects, so there are 1000+n observations generated each time. We simulate the data from a TV-HGARCH(1,d,1) model as follows:

| (5.1) |

where are iid standard normal variables.

In the first experiment the value of the parameter vector is The MLE values in section 3 are calculated, the biases (Bias) and the root mean squared error (RMSE) are summarized in Table 1. It is observed that both Bias and RMSE are generally small and decrease as the sample size increases.

The second experiment is conducted to evaluate the empirical sizes and powers of the score test statistic in section 4. The value of the parameter vector is when corresponds to the size and correspond to the power of the test. We consider three different values =0.4, 1 and 3 and two significance values .05 and .10. The empirical rejection rates are reported in Table 2. It can be seen that the empirical sizes are all close to the nominal values and this closeness increases as the sample size increases also empirical powers are increasing function of the sample size and of the .

| n=300 | n=500 | n=1000 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| parameter | Real value | Bias | RMSE | Bias | RMSE | Bias | RMSE | |||||

| 0.3 | 0.031 | 0.162 | 0.017 | 0.130 | 0.005 | 0.030 | ||||||

| 0.4 | 0.030 | 0.014 | 0.008 | 0.012 | 0.001 | 0.006 | ||||||

| 0.2 | 0.048 | 0.003 | 0.044 | 0.002 | 0.038 | 0.001 | ||||||

| 0.7 | 0.055 | 0.003 | 0.030 | 0.001 | 0.026 | 0.0008 | ||||||

| 1 | 0.084 | 0.019 | 0.057 | 0.019 | 0.025 | 0.018 | ||||||

| n=300 | n=500 | n=1000 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | |||||

| 0.069 | 0.112 | 0.057 | 0.108 | 0.049 | 0.095 | |||||

| 0.247 | 0.421 | 0.547 | 0.731 | 0.838 | 0.913 | |||||

| 0.290 | 0.474 | 0.578 | 0.759 | 0.889 | 0.958 | |||||

| 0.294 | 0.492 | 0.613 | 0.791 | 0.915 | 0.966 | |||||

6 VaR Forecasting

In order to investigate the ability of the TV-HGARCH model in forecasting the future behavior of the volatilities, we study the VaR forecasts. The one-day-ahead VaR with probability , , is calculated by where is the inverse distribution of standardized observation and . Due to the importance of VaR in management risk, the accuracy of the VaR forecasts from different models is evaluated based on some likelihood ratio (LR) tests (Ardia, 2009; Brooks and Persand, 2000).

Unconditional Coverage test

The Kupiec test (Kupiec, 1995), also known as the unconditional coverage (UC) test, is designed to test whether VaR forecasts cover the pre-specified probability. If the actual loss exceeds the VaR forecasts, this is termed an “exception,” which is a Bernoulli random variable with probability . The null hypothesis of the UC test is . Then the LR statistic of the unconditional coverage () is defined as

Where is the number of the forecasting samples, is the number of the exceptions and is the MLE of the under . Then under the is asymptotically distributed as a random variable with one degree of freedom.

Independent Test

If the volatilities are low in some periods and high in others, the forecasts should respond to this clustering event. It means that, the exceptions should be spread over the entire sample period independently and do not appear in clusters (Sarma et al., 2003). Christoffersen (1998) designed an independent (IND) test to check the clustering of the exceptions. The null hypothesis of the IND test assumes that the probability of an exception on a given day t is not influenced by what happened the day before. Formally, , where denotes that the probability of an event on day must be followed by a event on day where . The LR statistic of the IND test () can be obtained as

Where is the number of observations with value followed by value (), and . Under , the is asymptotically distributed as a random variable with one degree of freedom.

Conditional Coverage test

Also Christoffersen (1998) proposed a joint test: the conditional coverage (CC) test, which combines the properties of both the UC and IND tests. The null hypothesis of the CC test checks both the exception cluster and consistency of the exceptions with VaR confidence level. The null hypothesis of the test is . The LR statistic of the CC test ( is obtained as

Under , is asymptotically distributed as a random variable with two degrees of freedom. It is a summation of two separate statistics, and .

7 Empirical Data

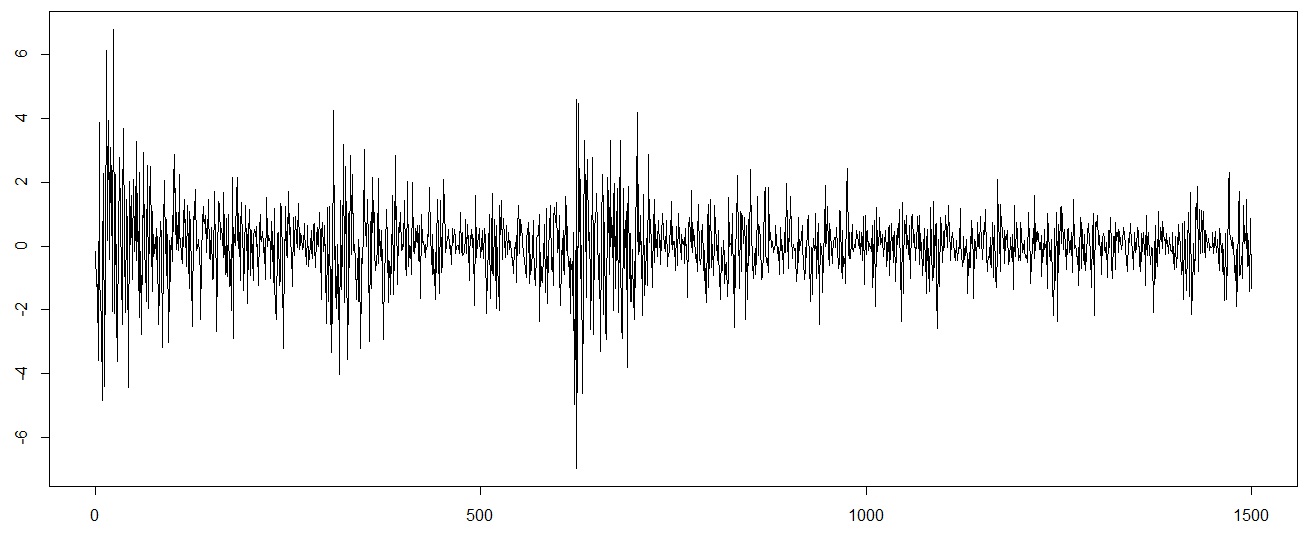

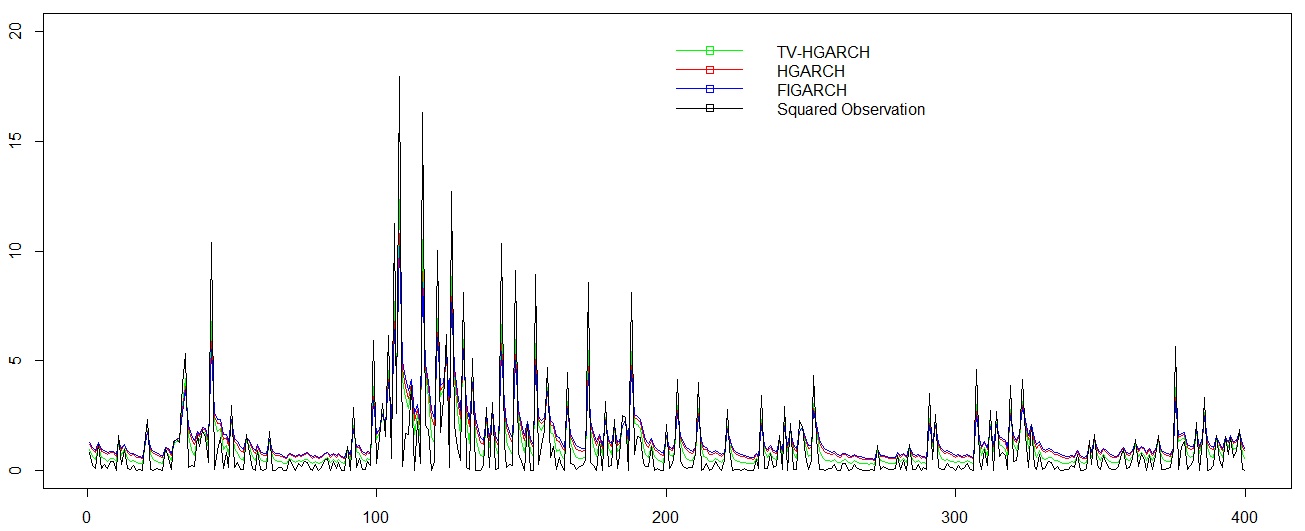

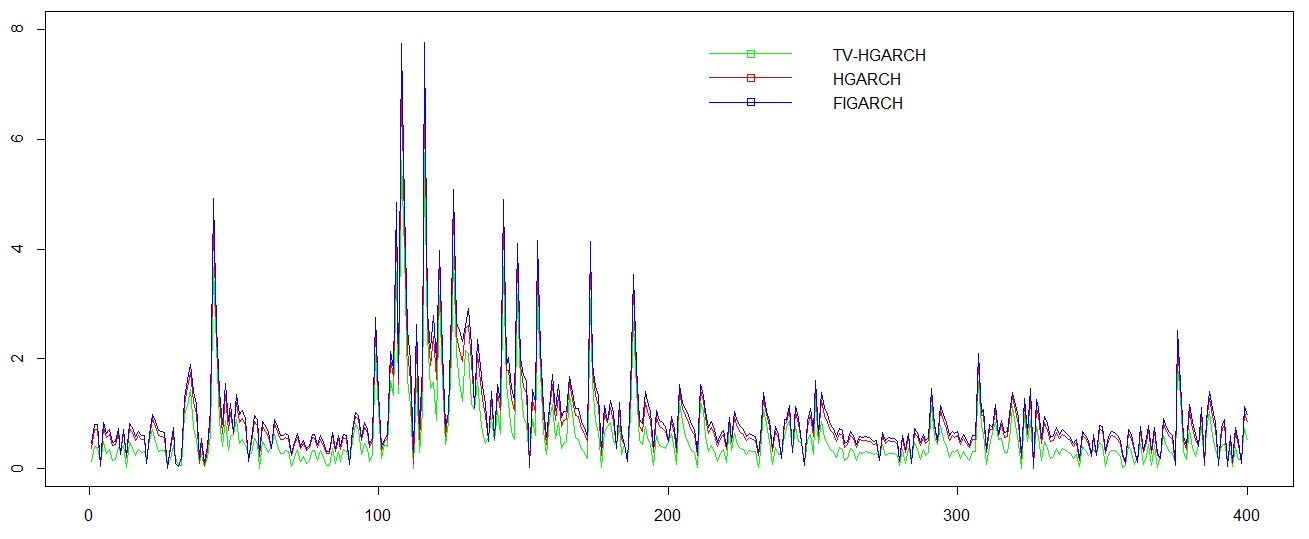

In this section, we apply the TV-HGARCH(1,d,1), HGARCH(1,d,1) and FIGARCH(1,d,1) models on the daily percentage log-returns of the S&P500 indices from February 17, 2009 to January 30, 2015 (1500 observations). Figure 1 presents the time plot of data. Some descriptive statistics of the S&P500 indices are listed in Table 3. We observe the negative skewness and excess kurtosis of these returns. To compare the empirical performance of the models from both fitting and forecasting the whole sample is divided into two parts. The first part contains 1,000 observations and is used as in-sample data to conduct fitting and the second part is used as out-of-sample data to evaluate model forecasting. The models are then applied to the first part of data. The MLE values are reported in Table 4. Also the score test in section 4 is performed and the value is obtained, so the critical value shows that at 5 significance level the data possesses a time-varying amplitude. To evaluate the performance of the models in computing true conditional variances that are measured by squared returns, we considered the root mean squared error (RMSE) and the log likelihood value (LLV) for in-sample and out-of-sample data. As out-of-sample performance, the one-day-ahead forecasts are computed using estimated models. The results are given in Table 5. It is observed that the TV-HGARCH model has the best performance. The HGARCH model outperforms the FIGARCH model, and has a lower RMSE and a higher LLV. To clarify the out-performance of the TV-HGARCH model, we plot the forecasting conditional variances and true conditional variances for some of the data in Figure 2. It can be seen that the TV-HGARCH follows the shocks very well. Figure 3 shows the absolute forecasting errors between different models and the true conditional variances for some of the data, it can be observed that the TV-HGARCH model has the smallest absolute error. Based on the out-of-sample data, one-day-ahead VaR forecasts at a level risk of for the models are calculated and the accuracy tests are performed. The results are reported in Table 6. The first and second rows show the number of expected exceptions (Ex.e) and empirical exceptions (Em.e) respectively. It can be seen that the Em.e for the TV-HGARCH model is closer to the Ex.e than HGARCH and FIGARCH models; in this respect also the HGARCH make better results than the FIGARCH. For VaR(0.05) at 5 significance level, the TV-HGARCH model passes all the tests while the HGARCH model passes IND and CC tests and FIGARCH model passes only IND test. Also for VaR(0.10), all models pass only IND test but the TV-HGARCH model has the smallest and . Hence, the results indicate that the TV-HGARCH model produces the most accurate VaR forecasts. Also the HGARCH model outperforms the FIGARCH model.

| series | Mean | Std.dev | Minimum | Maximum | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| S&P | 0.062 | 1.114 | -6.896 | 6.837 | -0.148 | 4.564 |

| TV-HYGARCH | HGARCH | FIGARCH | ||

|---|---|---|---|---|

| 0.179 | 0.237 | 0.237 | ||

| 0.340 | 0.455 | 0.505 | ||

| 0.315 | 0.315 | 0.315 | ||

| 0.550 | 0.567 | 0.505 | ||

| 2.444 | - | - | ||

| - | 0.972 | - |

| In-Sample | Out-of-Sample | |||||

|---|---|---|---|---|---|---|

| Model | RMSE | LLV | RMSE | LLV | ||

| TV-HGARCH | 1.406 | -1187.4 | 0.431 | -447.9 | ||

| HGARCH | 1.808 | -1294.3 | 0.637 | -514.6 | ||

| FIGARCH | 1.988 | -1325.6 | 0.710 | -530.5 | ||

| TV-HGARCH | HGARCH | FIGARCH | |||||||

| VaR(0.05) | VaR(0.10) | VaR(0.05) | VaR(0.10) | VaR(0.05) | VaR(0.10) | ||||

| Ex.e | 25 | 50 | 25 | 50 | 25 | 50 | |||

| Em.e | 21 | 33 | 16 | 29 | 13 | 28 | |||

| 7.210 | 3.890 | 11.371 | 7.298 | 12.588 | |||||

| 11.852 | 8.047 | 12.967 | |||||||

Notes: 1. At the 5% significance level the critical value of the and is 3.84 and for is 5.99. 2. * indicates that the model passes the test at 5% significance level.

Conclusion:

HGARCH is a hyperbolic-memory process. In this study we have generalized it by introducing TV-HGARCH model to have a better description of the dynamic volatilities. Our proposed model exploits a time-varying amplitude to update the structure of the volatility using logistic function of last observation. We show under some conditions the moments of model are bounded. One of the privilege of this work is implying of score test to check existence of the time-varying structure. Simulation evidences showed that empirical performance of test is competitive. The empirical example of some periods of S&P500 indices showed that the TV-HGARCH model gives better forecasting of volatilities and more accurate VaR than HGARCH and FIGARCH.

References

- [1] Amado C. and Teräsvirta T. (2008). Modelling conditional and unconditional heteroskedasticity with smoothly time-varying structure, CREATES; Research Paper, http://ssrn.com/abstract=1148141.

- [2] Ardia D. (2009). Bayesian estimation of a Markov-switching threshold asymmetric GARCH model with student t innovations, Econometrics Journal, 12(1), 105-126.

- [3] Baillie R. T., Bollerslev T. and Mikkelsen H. O. (1996). Fractionally integrated generalized autoregressive conditional heteroscedasticity, Journal of Econometrics, 74(1), 3-30.

- [4] Bollerslev T. (1986). Generalized autoregressive conditional heteroscedasticity, Journal of Econometrics, 31(3), 307-327.

- [5] Brooks C. and Persand G. (2000). Value at risk and market crashes, Journal of Risk, 2(4), 5–26.

- [6] Christoffersen P. (1998). Evaluating interval forecasts. International Economic Review, 39, 841-862.

- [7] Davidson J. (2004). Moment and memory properties of linear conditional heteroscedasticity models, and a new model, Journal of Business and Economic Statistics, 22(1), 16-19.

- [8] Dijk D., Teräsvirta T. and Franses H. (2002). Smooth transition autoregressive models: A survey of recent developments, Econometric Reviews, 21(1), 1-47.

- [9] Engle R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation, Econometrica, 50(4), 987-1007.

- [10] Gerlach R. and Chen C. (2008). Bayesian inference and model comparison for asymmetrics smooth transition heteroskedastic models, Statistics and Computing, 18(4), 391-408.

- [11] Kupiec P. (1995). Techniques for verifying the accuracy of risk measurement models, Journal of Derivatives, 2, 73-84.

- [12] Kwan W., Li W. K. and Li G. (2011). On the threshold hyperbolic GARCH models, Statistics and its Interface, 4(2), 159-166.

- [13] Kwan W., Li W. K. and Li G. (2012). On the estimation and diagnostic checking of the AFRIMA-HYGARCH model, Computational statistics and data Analysis, 56(11), 3632-3644.

- [14] Li M., Li G. and Li W. K. (2011). Score tests for hyperbolic GARCH models, Journal of Business and Economic Statistics, 29(4), 579-586.

- [15] Li M., Li W. K. and Li G. (2015). A new hyperbolic GARCH model, Journal of Econometrics, 189(2), 428-436.

- [16] McAleer M. and Medeiros M. C. (2008). A multiple regime smooth transition heterogeneous autoregressive model for long memory and asymmetries, Journal of Econometrics, 147(1), 104-119.

- [17] Sarma M., Thomas S. and Shah A.(2003). Selection of value-at-risk models, Journal of Forecasting, 22(4), 337-358.

- [18] Tang T. L. and Shieh S. J. (2006). Long memory in stock index futures markets: A value-at-risk approach, Physica A:Statistical Mechanics and its Applications, 366, 437-448.

- [19] Chong E. K. P. and Zak S. H. (2001). An Introduction to Optimization, New York: John Wiley.