An integrated local depth

Lucas Fernandez-Piana∗ and Marcela Svarc∗∗111Corresponding author: Marcela Svarc, Departamento de Matemática y Ciencias, Universidad de San Andrés, Vito Dumas 248, Victoria, Argentina. Email: msvarc@udesa.edu.ar

∗Instituto de Cálculo, FCEyN, Universidad

de Buenos Aires and CONICET, Argentina.

∗∗Departamento de Matemática y Ciencias,

Universidad de San Andrés and CONICET, Argentina

Abstract

We introduce the Integrated Dual Local Depth which is a local depth measure for data in a Banach space based on the use of one-dimensional projections. The properties of a depth measure are analyzed under this setting and a proper definition of local symmetry is given. Moreover, strong consistency results for the local depth and also for the local depth regions are attained. Finally, applications to descriptive data analysis and classification are analyzed, making the special focus on multivariate functional data, where we obtain very promising results.

Keywords: classification, data depth, multivariate functional data, projection procedures.

1 Introduction

Data depth measures play an important role when analyzing complex data sets, such as functional or high dimensional data. The main goal of depth measures is to provide a center-outer ordering of the data, generalizing the concept of median. Depth measures are also useful for describing different features of the underlying distribution of the data. Moreover, depth measures are powerful tools to deal with several inference problems such as, location and symmetry tests, classification, outlier detection, etc.

Nonetheless, since one of their major characteristics is that the depth values decrease along any half-line ray from the center, they are not suitable for capturing characteristics of the distribution when data is multimodal. Hence, over the last few years, there have been introduced several definitions of local depth, with the aim of revealing the local features of the underlying distribution. The basic idea is to restrict a global depth measure to a neighborhood of each point of the space. In this way, a local depth measure should behave as a global depth measure with respect to the neighborhoods of the different points. It can be considered that the -mode (see Cuevas et al. [9]), which is a depth measure defined for data in an arbitrary normed space, is the first precedent of a formal definition of local depth. This notion of depth has a “local” meaning since it is defined via a kernel function and recalls, in a way, the idea of defining a depth in in terms of the density function. Since in infinite dimensional spaces there is no natural concept of density, this definition can serve as a substitute. The definition strongly depends on the choice of a bandwidth, which remains fixed throughout the data. This definition has attract the attention in the last years, the consistency has been proved by Nagy [16] and the classical properties for depth measures have been deeply studied by Gijbels and Nagy [12]. Agostinelli and Romanazzi [2] gave the first formal definition of local depth for the case of multivariate data. They extended the concepts of simplicial and half-space depth so as to allow recording the local space geometry near a given point. For simplicial depth, they consider only random simplices with sizes no greater than a certain threshold, while for half-space depth, the half-spaces are replaced by infinite slabs with finite width. Both definitions strongly rely on a tuning parameter, which retains a constant size neighborhood of every point of the space, something which plays an analogous role to that of bandwidth in the problem of density estimation. Desirable statistical theoretical properties are attained for the case of univariate absolutely continuous distributions. Paindaveine and Van Bever [17] introduce a general procedure for multivariate data that allows converting any global depth into a local depth. The main idea of their definition is to study local environments. This means regarding the local depth as a global depth restricted to some neighborhood of the point of interest. They obtain strong consistency results of the sample version with its population counterpart. Following the same line as in the case of the -mode Chen et al. [7] and Sguera et al. [18] introduce the kernelized spatial depth for the multivariate and functional cases respectively. More recently, for the case of functional data, Agostinelli [1] gives a definition of local depth extending the ideas introduced by Lopez-Pintado and Romo [14] of a half-region space. This definition is also suitable for finite large dimensional datasets. Asymptotic results are obtained. The proposals given by Agostinelli and Romanazzi [2], Paindaveine and Van Bever [17] and Agostinelli [1] explicitly provide a continuum between definitions of local and global depth. All the authors highlight the usefulness of local depth to well known statistical problems such as: classification (Sguera et al. [18], Paindaveine and Van Bever [17]), outlier detection (Chen et al. [7] and Sguera et al. [19]), clustering (Agostinelli [1]), regression depth (Paindaveine and Van Bever [17]), among others.

Our goal is to give a general definition of local depth for random elements in a Banach space, extending the definition of global depth given by Cuevas and Fraiman [10], where they introduce the Integrated Dual Depth (IDD). The main idea of IDD is based on combining one-dimensional projections and the notion of one-dimensional depth. Let be a probability space and a separable Banach space. Denote by the dual space. Let be a random element in with distribution and a probability measure in independent of The IDD is defined as,

| (1) |

where is an univariate depth (for instance, simplicial or Tukey depth), and is the univariate distribution of

In the present paper, we define the Integrated Dual Local Depth (IDLD). The main idea is to replace the global depth measure in Equation (1) with a local one-dimensional depth measure following the definition given in Paindaveine and Van Bever [17]. We study how the classical properties, introduced by Zuo and Serfling [20], should be analyzed within the framework of local depth. We prove, under mild regularity conditions, that our proposal enjoys those properties. Moreover, uniform strong consistency results are exhibited for the definition of the empirical local depth of the population counterpart, and also for the local depth regions. The main advantages of our proposals are its flexibility in dealing with general data and also its low computational cost, which enables it to work with high-dimensional data. We apply local depth to classification problems, with special emphasis on the application of multivariate functional data.

The remainder of the paper is organized as follows. In Section 2 we define the integrated dual local depth and study its basic properties. Section 3 is devoted to the asymptotic study of the proposed local depth measure. In Section 4 the local depth regions are defined and the consistency results are exhibited. A simulation study and real data examples are given in Section 5. Some concluding remarks are given in Section 6. All the proofs appear in the Appendix.

2 General Framework and Definitions

In this section, we first review the concept of local depth for the univariate case. Then we define the Integrated Dual Local Depth, and we finally show that, under mild regularity assumptions, our proposal has good theoretical properties that correspond to those established in Paindaveine and Van Bever [17]. Let be a probability measure on and Let be a local depth measure of with respect to , for example, the univariate simplicial depth, that is

| (2) |

where is the cumulative distribution function of and is the neighborhood width defined as follows.

Definition 1.

Let be a univariate cumulative distribution function and Then, for we define the neighborhood width by

| (3) |

where is the locality level.

Remark 1.

If is absolutely continuous, the infimum in Equation (3) is attained and hence, Even more, it is clear that if then

The locality level is a tuning parameter that determines the centralness of the point of the space conditional to a given window around If the value is high it approaches the regular value of the point depth whereas if it is low it will only describe the centralness in a small neighborhood of . As tends to one, the local depth measure tends to the global depth measure.

We can also define, in an analogous way, the Tukey univariate local depth,

In what follows, without loss of generality, we restrict our attention to the case of simplicial local depth, .

2.1 Integrated Dual Local Depth

Our aim in this section is to extend the IDD introduced by [10], to the local setting. The IDD is a depth measure defined for random elements in a general Banach space. The idea is to project the data according to random directions and compute the univariate depth measure of the projected unidimensional data. To obtain a global depth measure, these univariate depths measures are integrated. Under mild regularity conditions, the IDD satisfies the basic properties of depth measures described by Zuo and Serfling [20], and it is strongly consistent. In addition, it is important to highlight its low computational cost, even in high dimensions, since it is based on the repeated calculation of one-dimensional projections (the Appendix includes a numerical analysis to support this claim).

Let be a probability space and a separable Banach space, with its dual space. Let be a random element in with distribution a probability measure in independent of , and . We define the Integrated Dual Local Depth (IDLD),

| (4) |

where is the univariate local depth given in Equation (2), and is the univariate distribution of As suggested by [10], in the infinite dimensional setting may be chosen to be a non-degenerate Gaussian measure and in the multivariate setting as a uniform distribution in the unitary sphere. The fact that is independent of allows us to proceed to the univariate case when projecting , where it is feasible and easy to calculate the local depth. With a slight abuse of notation, we write for the cumulative distribution function of Specifically, it reduces to

From now, every time we mention that is a continuous random element we mean that for every non-null functional on is an absolutely continuous random variable. It is clear that the IDLD is well-defined, since it is bounded by and non-negative.

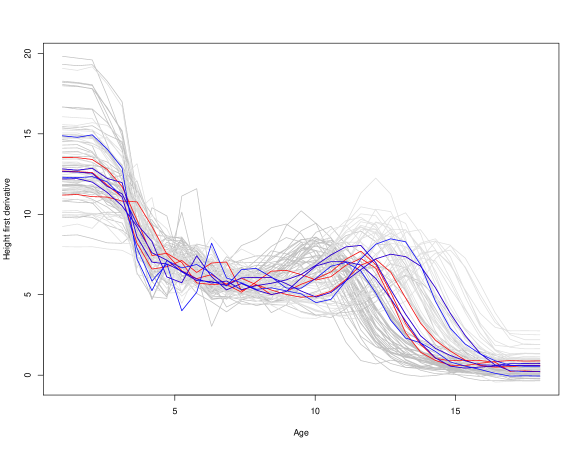

Local depth measure aims to highlight data local features that play an important role in statistical analysis. We consider the well-known growth data set, which is publicly available in the FDA R package. It consists of the height measurements of 54 girls and 39 boys, who were measured 31 times from 1 to 18 years. The original data was smoothed by monotonic cubic regression spline. The growth velocity has different patterns in boys and girls. At puberty, the growth rate has a local maximum. This typically occurs between 12 and 14 years for girls, a couple of years earlier than for boys, see Figure 1.

IDLD is sensitive to the choice of the locality parameter, , its choice will be addressed in detail later in this work. For different locality levels, the features that stand out from each dataset vary. In our example, for locality levels lower than within the locally deepest curves two belong to boys and three to girls, maintaining the proportion in which they appear in the dataset. While for locality levels greater than the deepest curves correspond to boys, as exhibited in Figure 1. For locality levels between and typically only one of the locally deepest curves corresponds to boys. Enlarging the proportion of deepest curves (up to ) this pattern is still observed.

Zuo and Serfling [20] established the general properties that depth measures should satisfy (P. 1 - P. 6). Paindaveine and Van Bever [17] analyze some of those properties for their proposal. In this work we study the properties that a local depth should fulfill, specifically, we show that under certain conditions, our proposal satisfies them.

The first property deals with the invariance of the local depths. For the finite dimensional case, IDLD is independent of the coordinate system. This property is inherited from the IDD. Since IDLD is a generalization of IDD, which is not in general affine invariant (i.e., let be a non-singular linear transformation in and denote the distribution of then is not equal to ), neither is IDLD. It is clear that IDLD is also invariant under translations and changes of scale.

The proofs of properties P. 1 - P. 6 appear in the Appendix.

P. 1. (affine-invariance).

Let with the Euclidean norm and a random vector, let be the uniform measure on the unit sphere of independent of Let be an orthogonal transformation and Then

Remark 2.

It is well known that the spatial median is not affine invariant, hence, transformation and retransformation methods have been designed to construct affine equivariant multivariate medians (Chakraborty and Chauduri [5] and Chakraborty and Chauduri [6]). IDLD can be modified following the ideas of Kotík and Hlubinka [13] to attain this property.

Depth measures are powerful analytical tools, especially in cases where the random element enjoys symmetry properties. Local depths should locally (restricted to certain neighborhoods) inherit these properties. Hence we give an appropriate definition of local symmetry.

Definition 2.

Let be a real random variable and Then is said to be -symmetric about if the cumulative function distribution satisfies

| (5) |

A random element in a Banach space is -symmetric about if for every not null is -symmetric.

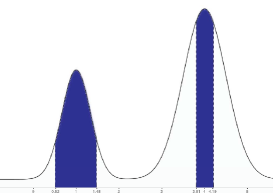

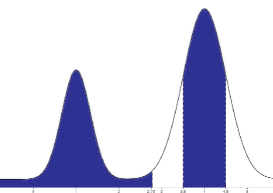

The notion of -symmetry aims to locally capture the behavior of a unimodal random variable on a neighborhood of probability about the locally deepest point. Figure 2 (a) and (b) exhibit a bimodal distribution, with modes at and On the former, both modes are local symmetry points for , while on the latter is a local symmetry point for but is not a local symmetry point for the shaded area around is non-symmetrical.

An important property of depth measures is maximality at the center, meaning that if is symmetric about then attains its maximum value at that point. This property should be inherited by local depths if the distribution of is unimodal and convex. Local depths are relevant for detecting local features, for instance local centers, hence our aim is to extend the property of maximality at the center to each point that is -symmetry.

P. 2. (maximality at the center).

Let be a random continuous element -symmetric about For we have that

| (6) |

Proposition 1 bridges the definition of -symmetry with the usual definition of -symmetry (see [20]). According to Dharmadhikari and Joag-dev [11] a random variable is unimodal on if the cumulative distribution function is convex on and it is concave on In addition, if it is absolutely continuous, then the density function is increasing on and decreasing on It is important to remark that in what follows we consider the continuous representantion of the density function.

Proposition 1.

Let be a random continuous element -symmetric about Then is -symmetric about for each

Proposition 2 describes the -symmetry points of

Proposition 2.

Let be a -symmetric random element in and such that for every Then is a -symmetry point.

P. 3 establishes that the IDLD is monotone relative to the deepest point. Several auxiliary results that appear in the Appendix must be stated before proving this property.

P. 3. (monotonicity relative to the deepest point).

Let be a separable Banach space and the corresponding dual space. Let be a random -symmetric element about with probability measure Let be a probability measure in independent of and assume that for every has unimodal density function symmetric about and fulfills

| (7) |

Then, for every and

Remark 3.

Inequality (3) holds for the standard normal distribution. Hence, the projections of a Gaussian process fulfill P. 3.

P. 4. (vanishing at infinity).

Assume that where is a function such that Then,

We omit the proof of P. 4. since it is analog to the proof of Theorem 1 given by Cuevas and Fraiman [10].

P. 5. (continuous as a function of ).

Let be a random continuous element and Then is continuous.

P. 6. (continuous as a functional of ).

Le be a separable Banach space and defined on such that weakly converges to . Then, for every

3 Empirical Version and Asymptotic Results

In this section we introduce the empirical counterpart of the IDLD and give the main asymptotic results. Let be an absolutely continuous random variable with distribution Suppose given iid random variables, also with distribution denote to the cumulative function distribution of and to the empirical counterpart.

First of all, recall the definition ofPaindaveine and Van Bever [17] of the empirical local unidimensional simplicial depth. Let Then

where and where is the integer part function. Remark 4 entails the well-definedness of the empirical neighborhood width,

Remark 4.

Let and be a random sample of iid variables with distribution Given put, for each and let denote the th order statistics of Let it is clear that almost surely. Hence, and the empirical neighborhood width is

Then the empirical counterpart of IDLD is given as follows.

Definition 3.

Let be a continuous random element and a random sample with the same distribution as Let For each and define

| (8) |

Let The empirical version of IDLD of locality level is

| (9) |

The theorems below establish the uniform strong convergence of the empirical counterpart of the univariate simplicial local depth to the population counterpart. The proofs appear in the Appendix as well as several lemmas needed to establish these results.

Theorem 1.

Let be a separable Banach space with dual space Suppose given a random sample of elements on with probability measure and Then, we have

-

(a)

(10) -

(b)

(11)

Theorem 2.

Let be a random element on a separable Banach space with associated probability measure such that Let be a random sample following the same distribution as and Then,

4 Local Depth Regions

In this section we define the local depth inner region at locality level Ideally, these central regions will be invariant of the coordinate system and nested. We also study, under mild regularity conditions, the asymptotic behavior.

Denote by a local depth measure and its empirical counterpart. In particular, one can consider the integrated dual local depth defined in Section 2.1.

Definition 4.

Let be a separable Banach space, let a random element with associated probability measure Fix a locality level, and The local depth inner region at locality level of level is defined to be

| (12) |

Let be a random sample of elements on Then the empirical counterpart of is

Throughout this section the locality level will remain fixed, hence we write (respectively, ) for (respectively. ) when no ambiguity is possible.

Remark 5.

If is a finite dimensional space, and is invariant under orthogonal transformations, then inherits this property.

Remark 6.

If then

Theorem 3 shows that the empirical local depth inner region at locality level is strongly consistent with its corresponding population counterpart, under regularity conditions. We omit the proof since it is analog to the prove given by Zuo and Serfling [20] in Theorem 4.1.

Theorem 3.

Let be a separable Banach space and let be a random element with associated probability measure Assume that

-

a)

-

b)

a.s.

Then, for every and sequence :

-

(I)

There exists an such that

-

(II)

If then a.s.

5 Numerical considerations

Local depth measures are depths conditional to a neighborhood of each point of the space. These measures are sensitive to the size of the neighborhood, which depends on a parameter that must be chosen. They may be classified into two families. On one hand, there are those depending on a global parameter, which indicates the size of the neighborhood for every point of the space. Within this family we find the proposals made by Cuevas et al. [9], Agostinelli and Romanazzi [2], Chen et al. [7], Sguera et al. [18] and Agostinelli [1]. In most of these papers, heuristic strategies are introduced for choosing this parameter in a data-driven way.

On the other hand, both in the proposal given by Paindaveine and Van Bever [17] as well as ours, the size of the neighborhood is adaptive to each point of the space In these cases the parameter indicates a fixed probability that will be considered surrounding each point then the neighborhood is determined by We give a heuristic strategy for choosing in a data driven way.

Different values reveal different features that are more or less adequate to describe and analyze a dataset.

It is well known that as locality becomes extreme local depth measures lose the nature of centrality, as pointed out by Paindaveine and Van Bever [17]. Therein they present a detailed characterization of the behavior of the extreme localization for the univariate case. Hence, since our proposal is constructed departing from this expression it can neither capture local centrality for close to zero.

For high values (typically greater than 0.5), the correlation between depth and local depth is high, that is, the structure described by these two measures is similar. In the remaining range of values, local depths describe adequately datasets typically with more than one subpopulation.

We suggest that instead of choosing a single value for it is useful to provide clusters of that highlight different features of the dataset.

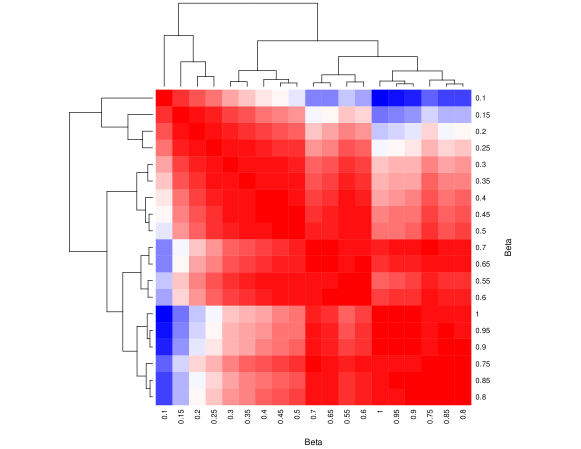

To exemplify, we return the case of the first derivatives of the growth dataset that we showed in the Introduction. Now analyze the correlations between local depths at different locality levels. To do this, we take an equispaced grid for values between and 1 with step To compute IDLD we generate 500 random directions following a standard brownian motion as in Cuevas and Fraiman [10]. We perform the heatmap of the local depth correlations calculated at the different locality levels, see Figure 3. The dendrogram shows that there are four groups. We can order the clusters in ascending order following the locality levels that constitute them. The first one is a singleton conformed by the smallest value. In the second cluster beta ranges between and ; in the third cluster between and and finally, the fourth cluster has the remaining values. On the one hand, IDLD for belonging to the first cluster is not informative. On the other hand, for the last cluster, the neighborhoods contain more than half of the points, hence the information given by the local and global depth is practically the same. The second cluster is the one that best manages to capture the central curves for girls and boys. The third cluster presents an interface between the second and the fourth cluster, where the information of the two subpopulations is present although somewhat blurred.

To stress this point, if we consider the locally deepest of the data, for locality values smaller than the proportion of boys and girls among them is the same that in the entire data set, while for locality levels between and typically, the girl’s rate grow. Finally, for locality levels greater than all the local deepest data correspond to girls. In Figure 1 (which appears in the Introduction) we can notice that the local depth curves () better capture the centers for boys and girls while the ones corresponding to the global depth only identify one center and does not highlight the most salient information of the data set. If instead of retaining the locally deepest curves we increase this proportion, in every case for locality levels in the second cluster the central curves reveal the peaks for boys and for girls, while for locality levels greater than the central curves do not reveal this pattern.

The pattern described in this example is typically observed in all the datasets that we had analyzed. The heatmap aids to analyze the matrix correlation of the local depth at different locally levels. Typically locality levels between and will capture valuable information on the data.

6 Simulations and real data examples

In this section, we analyze the performance of the IDLD for classification and descriptive statistics. Even though we develop the theoretical part in the most general case, for the numerical part we concentrate on functional data, specifically in the multivariate case, where there is no other local depth available.

6.1 Descriptive Statistic. The Gross Domestic Product data set

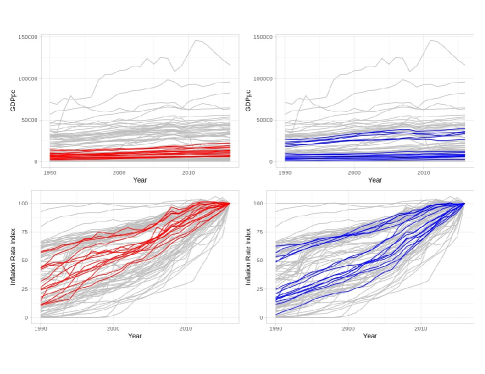

In this example, we consider a two-dimensional functional data set, which is available at the International Monetary Fund website https://www.imf.org/external/datamapper/NGDPD@WEO/OEMDC/ADVEC/WEOWORLD. The database contains the annual series of Growth Domestic Product (GDP) per capita and the inflation rate (interannual variation of the consumer price index with the base year 2016), for 101 countries from 1990 to 2016. The relationship between GDP and inflation has been one of the most widely researched topics in macroeconomics, where not only the marginal behavior of each of these variables provides valuable information, but also the compound analysis between them. Although the database has measurements since 1980, many countries did not report their inflation rates during the 1980s, hence we analyze the series beginning in 1990. The data corresponding to each of the variables are measured in different units (which differ in their order of magnitude, see Figure 4), therefore both series were standardized to have comparable scales by dividing the GDP by 400. The objective of this analysis is to adequately describe the data set that is being analyzed. At first glance, the univariate GDP and inflation charts do not present any clear pattern.

We compute the IDLD at locality level To compute 500 random directions are generated as follows. We assume that each functional coordinate of the data belongs to where is the period of time studied. Then, we consider the product space with the usual inner product. The trajectories are generated following a standard brownian motion distribution.

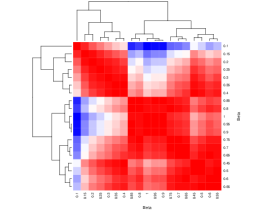

In Figure 5 (a) the heatmap of the correlation between the IDLD at different locality levels show a three-group structure. One group is a singleton, where no structure can be appreciated since the local depths of many points are high and similar. The larger cluster contains the locality levels higher than which present a high correlation with the global depth. Finally, the remaining values constitute a group, which will be analyzed in detail.

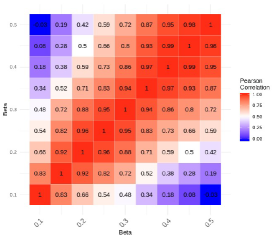

Then we study the IDLD at locality level To carry out a deeper analysis we proceed as follows. Given two locality levels and consider the set of observations that correspond to of the local deepest data for at least one of the locality level, denote to this set. Calculate the correlation matrix of the rankings of the and where is the distribution of the complete data set. These results appear In Figure 5 (b), clearly there are regions of locality level where the correlation is high, the area that stands out the most is The fact that the correlation, in a range of is high and stable suggests that a clear structure is being captured, otherwise, the spurious structures would be described. For this reason we chose

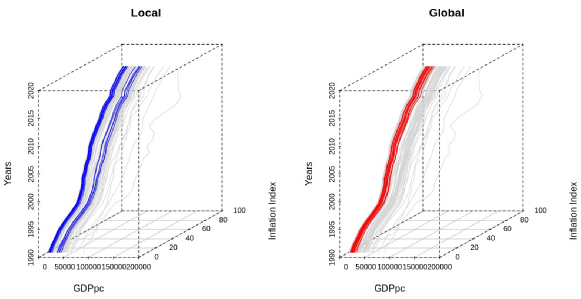

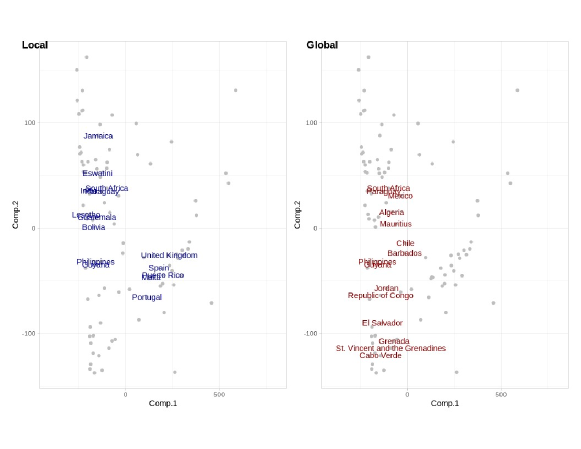

To deepen this exercise we will analyze the of the deepest data, locally and globally. In Figures 4 and 6 it can be appreciated that not only the deepest observations are different but also in the local case a bimodal structure is clearly described, this pattern is described by both variables. Moreover, if we analyze the first two principal components, clearly one mode is dominated by emergent countries (for instance Paraguay and Bolivia) while the other mode is dominated by developed countries (for example UK and Spain). On the other hand, among the deepest curves for the global depth, only emergent countries appear (see Figure 7).

6.2 Classification

In this section we perform a simulation study as well as analyze two well-known data sets and show that the IDLD improves the max-depth classification.

6.2.1 Simulation

Five models are studied for classification purpose. In every case we consider bivariate functional data. In all the cases, each functional curves are obtained from the process where is the mean function of the class and for coordinate and is a gaussian process with zero mean and covariance operator with The functions are generated in the interval on a grid of equidistant points. The models are inspired in those of Cuesta-Albertos et al. [8].

-

•

Model 1: The mean of Population 1 is and for Population 2 Each coordinate of Population 1 has error process by and for Population 2 where The sample size of the training and validation samples for each population is 100.

-

•

Model 2: Population 1 and 2 follow the same distribution as in Model 1, but the sample size of the training and validation sets for Population 1 is 70, while for Population 2 is 100 observations.

-

•

Model 3: The mean of Population 1 is the same as in Model 1, while Population 2 is a mixture of two subgroups one with mean and the other one with mean the mixing proportion is The error process for both coordinates of Population 1 is generated with and both coordinates of Population 2 with The sample sizes for the training and validation samples for each population is 50 observations.

-

•

Model 4: Population 1 is a mixture of two groups with means and Population 2 is a mixture of two groups with means and In both cases the mixing proportions is The error process for both coordinates of Population 1 is generated with and both coordinates of Population 2 with The sample sizes for the training and validation samples for each population is 50 observations.

-

•

Model 5: Has the same distribution as Model 4, but in this case each subgroup is a group.

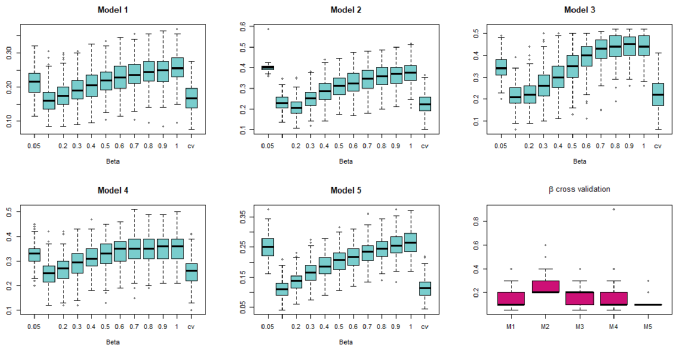

The simulation results are based on 200 independent replicates. The observations are assigned to the Population with highest local depth for fix and also for a 5-fold cross-validated For each of them we analyze missclasification error rate at different locality levels.

| 0.05 | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1 | cv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| M1 | 0.21 | 0.16 | 0.18 | 0.19 | 0.21 | 0.22 | 0.23 | 0.24 | 0.24 | 0.25 | 0.26 | 0.17 |

| M2 | 0.42 | 0.23 | 0.21 | 0.25 | 0.29 | 0.31 | 0.33 | 0.34 | 0.35 | 0.36 | 0.37 | 0.23 |

| M3 | 0.35 | 0.22 | 0.22 | 0.26 | 0.30 | 0.35 | 0.39 | 0.42 | 0.43 | 0.44 | 0.44 | 0.22 |

| M4 | 0.33 | 0.25 | 0.27 | 0.29 | 0.31 | 0.33 | 0.34 | 0.35 | 0.35 | 0.35 | 0.35 | 0.26 |

| M5 | 0.25 | 0.11 | 0.14 | 0.16 | 0.19 | 0.20 | 0.22 | 0.23 | 0.25 | 0.26 | 0.26 | 0.12 |

In Table 1 the mean misclassification error for IDLD at different locality levels is presented. The benchmark is given when which is the IDD, in every case these values are among the highest. The last column presents the misclassification rate for obtained via cross-validation, these results are very close to the best ones. In every case, for the smallest locality level considered the IDLD is not successful, since it cannot identify the central observations of the sample. In all the cases the best performance is attained either for or Typically the misclassification level increases as increases. The misclassification rate for Model 1 is smaller than for Model 2. For Models 3 and 4, where at least one of the groups is a mixture of two distributions, for greater than the results are practically the same because the local features are not captured. In Model 5, for and it correctly identifies the four groups. These features are also captured by the boxplots in Figure 8. The performance for selected by cross-validation is similar to the performance given in the best case for the fixed locality parameter. In almost every case is smaller than and typically is either or these results are consistent with the ones given for fixed locality level.

The R code is available at https://github.com/lfernandezpiana/lidDepth/tree/master/Simulations.

6.2.2 The Growth data set

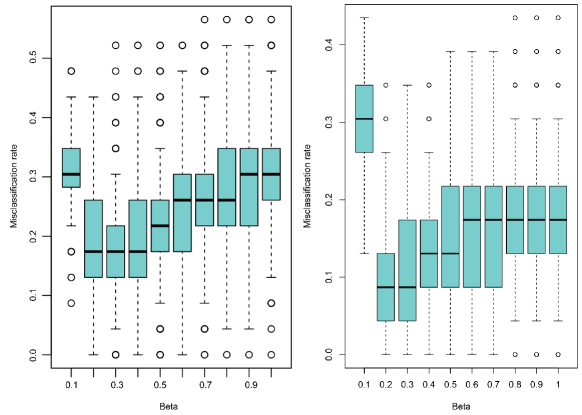

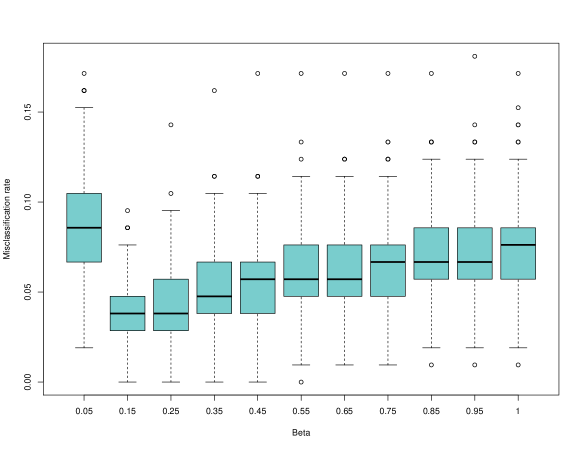

We return to the Growth dataset, now we will analyze it from the classification perspective. To begin with, our aim is to classify the growth curves for a sample of boys and girls, we start working with the trajectories. Since there is no learning and test sample we shall proceed following the ideas from Sguera et al. [18]. A thousand replications are made with the following scheme. On each replicate the training sample is randomly chosen, respecting the proportions of girls and boys in the data set, 40 curves correspond to girls and 30 to boys. The remaining observations are classified, using the criterion of maximum local depth, taking into account different locality levels, where is the global depth. It is important to highlight that we consider the same locality level for boys and girls for the sake of simplicity since the IDLD is stable in certain intervals.

The left-hand side panel in Figure 9 presents the boxplot of the misclassification rate, for each locality parameter Clearly, the misclassification depends on the locality parameter, and in this case, the optimal locality level is where with median (respectively mean) misclassification rate is (respectively ). If instead of the IDLD at locality level we had considered the global depth measure the median (respectively mean) misclassification rate is (respectively ) hence the relative improvement is (respectively ). It is important to highlight that these results are similar to those obtained by Sguera et al. [18].

Finally, we repeat the exercise with the derivatives of the growth curves. The right-hand side in Figure 9 shows the boxplots corresponding to the misclassification rate for the velocity of the growth curves are shown. Once again, we can conclude that the classification is better when considering local depths with locality levels between and Overall, better classification rates are achieved considering the trajectories instead of the derivatives.

6.2.3 The Character Trajectory data set

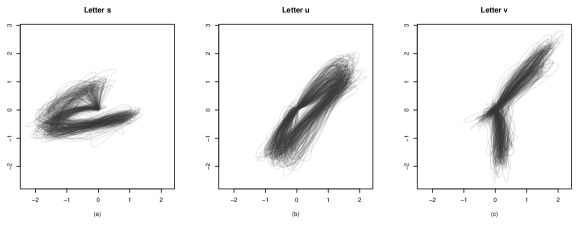

We analyze the bivariate functional writing data which is a part of the Character Trajectory data set that is available at the UCI machine learning repository (Bache and Lichman [3]). The data measure the horizontal and vertical coordinates of a pen tip while a person writes either the letter ‘s’, ‘u’ or ‘v’, there are observations for the letter ‘s’ and observations for the letter ‘u’ and for the letter ‘v’. The observed data were first interpolated to obtain equally spaced time points. The trajectories for the letter ‘s’, ‘u’ and ‘v’ are plot in Figure 10 (a), (b) and (c) respectively.

Our aim is to classify the letter trajectories in the correct category. Since there is no learning and test sample we shall proceed as in the previous example. Five thousand replications are made with the following scheme. On each replicate, the training sample is selected following a probability proportional to the size of each letter sampling scheme. The remaining observations are classified, using the criterion of maximum local depth, taking into account different locality levels, where is the global depth.

For the misclassification rate is much higher than for any other value. The lower misclassification rates are attained for between and which remain moderate for between and Finally, for locality levels above the malclassification rates are higher. The lowest mean misclassification rate is for and the median is (see Figure 11)

7 Concluding Remarks

In this paper, we introduced a local depth measure, IDLD, suitable for data in a general Banach space with low computational burden. It is an exploratory data analysis tool, which can be used in any statistical procedure that seeks to study local phenomena. From the theoretical perspective, local depths are expected to be generalizations of a global depth measure. Our proposal has this property. Additionally, they are expected to inherit good properties from global depths, this point has been deeply analyzed in this work. Strong consistency results for the local depth and local depth regions have been proved.

From a practical point of view, we explored the use of local depth measures as a powerful tool for describing datasets, specifically if current multimodal distributions and also their use in classification problems show better performance than the use of global depths.

A natural extension of this work is to explore classification strategies similar to classifiers based on local depth similar to those proposed in Cuesta-Albertos et al. [8], but it goes beyond the scope of this paper.

8 Appendix

8.1 Proofs of properties P.1-6.

Proof: P.1. affine - invariance.

Let be an orthogonal transformation and denotes the probability measure of

Since is the uniform measure on the unit sphere then which concludes what we wanted to prove.

∎

Proof: P.2. maximality at the center.

It is enough to show that for each and

Since the bound, is attained, we have that has a global maximum at Then, is clear that also is a global maximum. ∎

Proof: Proposition 1.

Let is -symmetric about if for every not null is symmetric about Then, for every

Finally,

which is what we wanted to show. ∎

Proof: Proposition 2.

First note that, given and

From the definition of is clear that,

Let attains a global maximum at hence attains its maximum when If this property is satisfied for every then, is a -symmetry point of

Then, let

For every is bounded by Hence, From the first part of the proof we know that is a -symmetry point of hence is a -symmetry point of ∎

We now focus on the proof of P.3 that establishes that the local depth is monotone relative to the deepest point. We first show that this results holds if the distribution is unimodal. We begin by proving several auxiliary results that we will need to prove P. 3.

Lemma 1 (P.3.).

Let be an absolutely continuous, symmetric and unimodal about random variable with cumulative distribution function Let define the functions,

-

•

-

•

Then, for every we have that:

-

a)

If

-

b)

If

Proof.

a) It is clear that if then by symmetry the equality is attained.

Let and be the density function of There are two possible cases to analyze:

i) If

Since decreases on we have that

By symmetry for every then

On the other hand, since which implies that

Thus,

ii) If,

Observe that if we have that and since the density function is symmetric about we know that Hence,

Since decreasing, we obtain the following inequalities,

Then,

Finally, since y

b) Consider the random variable which is absolutely continuous, symmetric and unimodal about Denote the cumulative distribution function of and the cumulative distribution function of In addition, observe that given

Analogously,

Then, if we have that and since part (a) of the proof holds we have that,

∎

Lemma 2 (P.3.).

Let be an absolutely continuous random variable with cumulative distribution function, and density Let Let such that the density function satisfies or Then, there exists an interval centred at and function such that is on Even more, for each

Proof.

The proof follows straight forward applying the implicit function theorem to the function

Then we have,

∎

Lemma 3 (P.3.).

Let be an absolutely continuous, symmetric and unimodal about random variable, such that the cumulative distribution function is . Let and the density function such that which in addition satisfies that

Then,

-

a)

is non increasing if

-

b)

is non decreasing if

Proof.

Following Lemma 2 and for the sake of simplicity denote

It is clear that,

The derivative of with respect to is:

By Lemma 2 and considering the derivative of respect to we have that:

From Lemma 1 we have that:

-

a)

If

-

b)

if

∎

Lemma 4 (P.3.).

Let be a random variable and Let and Denote and to the corresponding cumulative distribution functions, then,

Proof.

Let we have that Then,

entails the desired equality. ∎

Finally we prove P.3.

Proof: P.3. monotonicity relative to the deepest point.

∎

Before proving P.5. the following result must be stated.

Lemma 5.

Let be an absolutely continuous random variable with cumulative distribution function then Let be a real sequence such that and Then,

Proof.

Since is continuous is enough to show that

Let denote to the symmetrize version of about Recall that,

Then,

Meaning that analogously for Given that is clear that

∎

Proof: P.5. continuous as a function of .

It goes straight forward from Lemma 5 and the Dominated Convergence Theorem. ∎

Proof: P.6. continuous as a functional of .

It goes straight forward from Theorem 2.1, Billingsley [4] and the fact that in uniformly continuous. Since is the cumulative distribution function of which converges pointwise to then is clear that

Then it is consequence of the Dominated Convergence Theorem.

∎

8.2 Uniform Strong Consistency of the IDLD.

In order to establish the uniform strong convergence of the one dimensional simplicial local depth. The following Lemma must be proved in advanced.

First of all, it is important to note the following facts. Assuming that the conditions stated in Remark 4 hold. For the sake of simplicity denote, and Let then,

-

(i)

and

-

(ii)

Moreover,

Then,

-

(iii)

-

(iv)

-

(v)

-

(vi)

and

-

(vii)

Lemma 6.

Let be an absolutely continuous random variable with distribution Suppose given iid random variables, also with distribution . Let be the quantile from and the quantile from which is the empirical cumulative distribution function of Then,

-

(i)

-

(ii)

-

(iii)

Proof: Lemma 1.

-

(i)

It follows straight forward by definition.

-

(ii)

Let

-

(iii)

Let

∎

Lemma 7.

Let be a real random sample with cumulative distribution function Let and Then,

| (1) |

Proof: Lemma 2.

For the sake of simplicity denote and

| (2) | |||

We analyze each term of Equation (2),

-

(a)

-

(b)

-

(c)

-

(d)

Analogue to item (a).

Finally, denote

and

Then,

On one hand, since Proposition 2 holds its clear that each term of is smaller than or equal to . Hence,

| (3) |

On the other hand, we already know that,

| (4) |

Proof:Theorem 1.

(a) Let and Denote to the probability measure associated to where is a random element on with probability measure Analogously, denote to the empirical probability measure of based on and to the empirical cumulative distribution function.

By Proposition 2 we have,

Observe that,

Thus,

| (5) |

Since it does not depend on the inequality hold for the supreme of the left hand side of Inequality (5).

| (6) |

Thus,

| (7) |

From (8.2) it is enough to show that

Let there exists such that

By Dvoretzky-Kiefer-Wolfowitz inequality Massart [15] we have that

| (8) |

It is important to note that the convergence does not depend on the functional which will be useful to prove part (b) of the result.

(b) It follows straight forward from part (a) of the theorem and the fact that it is the integral of a mensurable, positive and bounded function. Hence, given there exists such that for every

Then,

∎

Proof:Theorem 2.

Note that,

It is enough to show that

By Borell-Cantelli lemma it is enough to prove that if the probability of the sets

are summable, then, for all and the prove would be done.

Let

Given that there exists such that

then

By Dvoretzky-Kiefer-Wolfowitz inequality,

Which is bounded by Borell-Cantelli’s lemma,

| (9) |

∎

8.3 Computational Cost

It is well known that one of the main drawback of depth and local depth measures is that they are highly demandant computationally. Therefore, we analyze this problem from this perspective, focusing in the multivariate case where these problems usually arise. In what follows we compare the computational times for the three local depths measures, LDS (Agostinelli and Romanazzi, 2011), LDPV (Paindavaine and Van Bever, 2013) and IDLD, our proposal. We generate data that has a three group structure each is generated according to a multivariate -dimensional normal distribution, for with centers and the covariance matrix is the identity matrix, the first two variables are informative while the remaining, () have normal independent noise variables centered at the origin with unit standard deviation. Also we considered different sample sizes, and For ILDL random directions were generated. Since the computational time increases exponentially as the dimension increases and the benchmark procedures are expesive computationally, we only performed replicates under each scenario.

| LDS | |||||

|---|---|---|---|---|---|

| LDPV | |||||

| IDLD | |||||

| LDS | |||||

| LDPV | |||||

| IDLD | |||||

| LDS | |||||

| LDPV | |||||

| IDLD |

From Table 2 we can see that in every case IDLD is the fastest procedure, moreover it is not affected by the dimension of the dataset, while the computational efforts required by LDS and LDPV grow dramatically as increases. LDPV is overall the slowest procedure. Even though all the procedures demand more time as the sample size grows, IDLD is the one with the least pronounced growth rate. In every case the mean square error between the estimates is smaller than being the three proposals able to detect the multimodal structure.

Acknowledgements

This work was partially supported by the Spanish Agencia Estatal de Investigación (AEI) and Fondo Europeo de Desarrollo Regional (FEDER), Grant CTM2016-79741-R for MICROAIPOLAR project and by Grant pict 2018-00740 from anpcyt (M. Svarc). We appreciate the valuable comments done by Matías Fernandez Piana, in the GDP data set analysis.

References

- [1] Agostinelli, C., 2018. Local half-region depth for functional data. Journal of Multivariate Analysis. 163, 67-79. DOI: 10.1016/j.jmva.2017.10.004.

- [2] Agostinelli, C., Romanazzi, M., 2011. Local Depth. Journal of Statistical Planning and Inference. 141, 817-830. DOI: 10.1016/j.jspi.2010.08.001.

- [3] Bache, K., Lichman, M., 2013. UCI Machine Learning Repository.

- [4] Billingsley, P., 1968. Convergence of probability measures. John Willey and Sons, New York.

- [5] Chakraborty, B., Chaudhuri, P., 1996. On transformation and retransformation technique for constructing an affine equivariant multivariate median. Proceedings of the American Mathematical Society. 124, 2539-2547. DOI: 10.1090/S0002-9939-96-03657-X.

- [6] Chakraborty, B., Chaudhuri, P., 1998. Operating transformation retransformation on spatial median angle test. Statistica Sinica. 8(2), 767-784.

- [7] Chen, Y., Dang, X., Peng,H., Bart, H.L., 2009. Outlier detection with kernelized spatial depth function. IEEE Transactions on Pattern Analysis and Machine Intelligence. 31(2), 288-305. DOI: 10.1109/TPAMI.2008.72.

- [8] Cuesta-Albertos, J.A., Febrero-Bande, M., de la Fuente, M.O., 2017. The -classifier in the functional setting. Test. 26(1), 119-142, DOI: 10.1007/s11749-016-0502-6.

- [9] Cuevas, A., Febrero-Bande, M., Fraiman, R., 2007. Robust estimation and classification for functional data via projection-based depth notions. Computational Statistics. 22, 481-496. DOI: 10.1007/s00180-007-0053-0.

- [10] Cuevas, A., Fraiman, R., 2009. On depth measures and dual statistics. A methodology for dealing with general data. Journal of Multivariate Analysis. 100(4), 753-766. DOI: 10.1016/j.jmva.2008.08.002.

- [11] Dharmadhikari, S., Joag-dev, R. 1988. Unimodality, Convexity and Applications. Academic Press, Nueva York.

- [12] Gijbels, I., Nagy, S., 2017. On a general definition of depth for functional data. Statistical Science. 32, 630–639. DOI: 10.1214/17-STS625.

- [13] Kotík, L., Hlubinka,D., 2017. A weighted localization of halfspace depth and its properties. Journal of Multivariate Analysis. 157, 53–69. DOI: 10.1016/j.jmva.2017.02.008.

- [14] Lopez-Pintado, S., Romo, J., 2011. A half-region depth for functional data. Computational Statistics and Data Analysis. 55(4), 1679–1695. DOI: 10.1016/j.csda.2010.10.024.

- [15] Massart, M., 1990. The Tight Constant in the Dvoretzky-Kiefer-Wolfowitz Inequality. Annals of Probability. 18(3), 1269-1283. DOI:10.1214/aop/1176990746.

- [16] Nagy, S., 2015. Consistency of the mode depth. Journal of Statistical Planning and Inference. 165, 91–103. DOI:10.1016/j.jspi.2015.04.006.

- [17] Paindaveine, D., Van Bever, G., 2013. From depth to local depth: A focus in centrality. Journal of the American Statistical Association. 108(503), 1105–1119. DOI: 10.1080/01621459.2013.813390.

- [18] Sguera, C., Galeano, P., Lillo, R., 2014. Spatial depth-based classification for functional data. Test. 23(4), 725-750. DOI: 10.1007/s11749-014-0379-1.

- [19] Sguera, C., Galeano, P., Lillo, R., 2015. Functional outlier detection by a local depth with application to NOx levels. Stochastic Environmental Research and Risk Assessment. 30(4), 1115-1130. DOI: 10.1007/s00477-015-1096-3.

- [20] Zuo, Y., Serfling, R., 2000. General Notion of Statistical Depth Function. The Annals of Statistics. 28(2), 461-482. DOI: 10.1214/aos/1016218226.