Water from Two Rocks: Maximizing the Mutual Information

Water from Two Rocks: Maximizing the Mutual Information

Abstract

We build a natural connection between the learning problem, co-training, and forecast elicitation without verification (related to peer-prediction) and address them simultaneously using the same information theoretic approach.111This work is supported by the National Science Foundation, under grant CAREER#1452915, CCF#1618187 and AitF#1535912.

In co-training/multiview learning [7] the goal is to aggregate two views of data into a prediction for a latent label. We show how to optimally combine two views of data by reducing the problem to an optimization problem. Our work gives a unified and rigorous approach to the general setting.

In forecast elicitation without verification we seek to design a mechanism that elicits high quality forecasts from agents in the setting where the mechanism does not have access to the ground truth. By assuming the agents’ information is independent conditioning on the outcome, we propose mechanisms where truth-telling is a strict equilibrium for both the single-task and multi-task settings. Our multi-task mechanism additionally has the property that the truth-telling equilibrium pays better than any other strategy profile and strictly better than any other “non-permutation" strategy profile when the prior satisfies some mild conditions.

1 Introduction

Co-training/multiview learning is a problem that asks to aggregate two views of data into a prediction for the latent label, and was first proposed by Blum and Mitchell [7]. Although co-training is an important learning problem, it lacks a unified and rigorous approach to the general setting. The current paper will make an innovative connection between the co-training problem and a peer prediction style mechanism design problem: forecast elicitation without verification, and develop a unified theory for both of them via the same information theoretic approach.

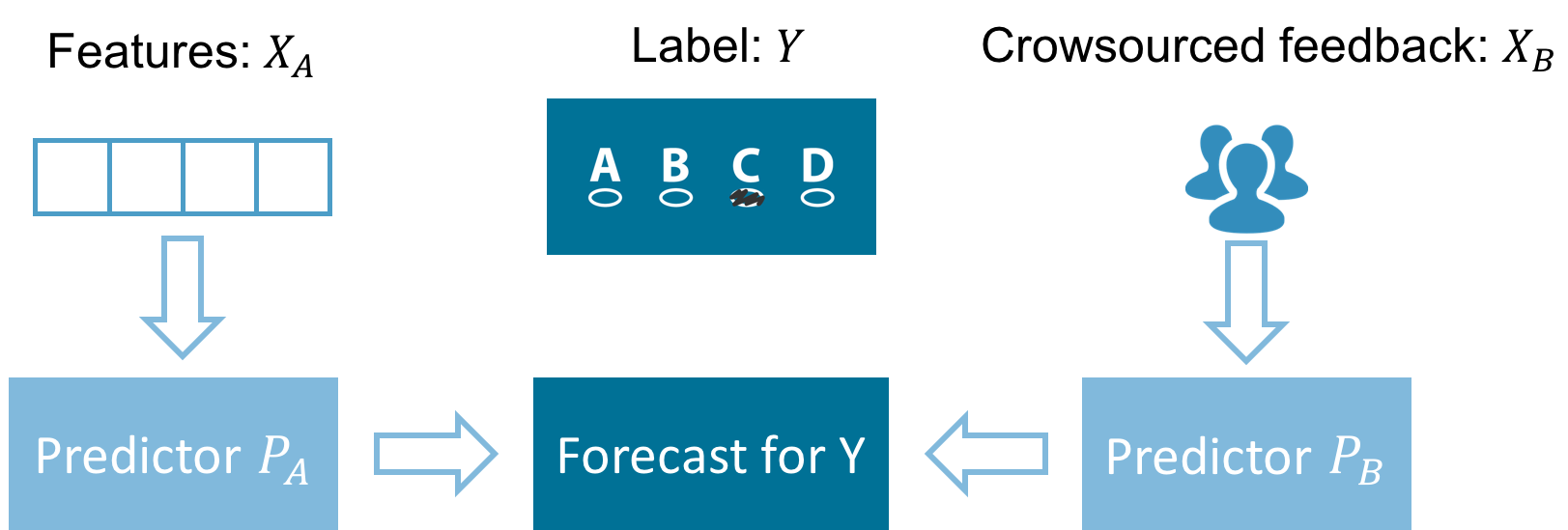

We use “forecasting whether a startup company will succeed” as our running example. We have two possible sources of information for each startup: the features (e.g. products, business idea, target customer) of the startup; and the survey feedback , collected from the crowd (e.g. a survey of amateur investors). Sometimes we have access to both the sources, and sometimes we have access to only one of the sources. We want to learn how to forecast the result (succeed/fail) of a startup company, using both or one of the sources.

We are given a set predictor candidates (e.g. a set of hypotheses) such that each predictor candidate maps the features to a forecast for the result of the startup (e.g. succeed with 73% probability, fail with 27% probability). We are also given a set predictor candidates (e.g. a set of aggregation algorithms like majority vote/weighted average) such that each predictor candidate maps the survey feedback to a forecast for the result . Our goal is to evaluate the performance of a specific pair . The learning problem, learning how to forecast, can be reduced to this goal since if we know how to evaluate the two candidates ’s performance, we can select the two candidates which have the highest performance and use them to forecast.

Given a batch of past startup data each with the features , the crowdsourced feedback , and the result , we can evaluate the performance of the predictors through many existing measurements (e.g. proper scoring rules, loss functions). This evaluation method is related to the supervised learning setting. However, there may be only very few data points about the startups with results .222For example, if we focus on cryptographic or self-driving currencies, there are very few startups labeled with results. When we only use a few labeled data points to train the predictor, the predictor will likely over-fit. Thus, we can boldly ask:

(*Learning) Can we evaluate the performance of the predictor candidates, as well as learn how to forecast the ground truth , without access to any data labeled with ? (See Figure 1)

It is impossible to solve this problem without making an additional assumption on the relationship between and . However, it turns out we can solve this problem with a natural assumption, conditioning on , and are independent. This assumption states that contains all common information between and (see Section 3 for more discussion).

With this assumption, a naive approach is to learn the joint distribution of and using the past data, and then solve the relationship between and by some calculations, using the fact that and are independent conditioning on . However, this naive approach will not work if either or has very high dimension. We will address this issue using learning methods. Before we go further on the learning problem, let’s consider a corresponding mechanism design problem. In the scenario where the forecasts are provided by human beings, we want to ask a mechanism design problem:

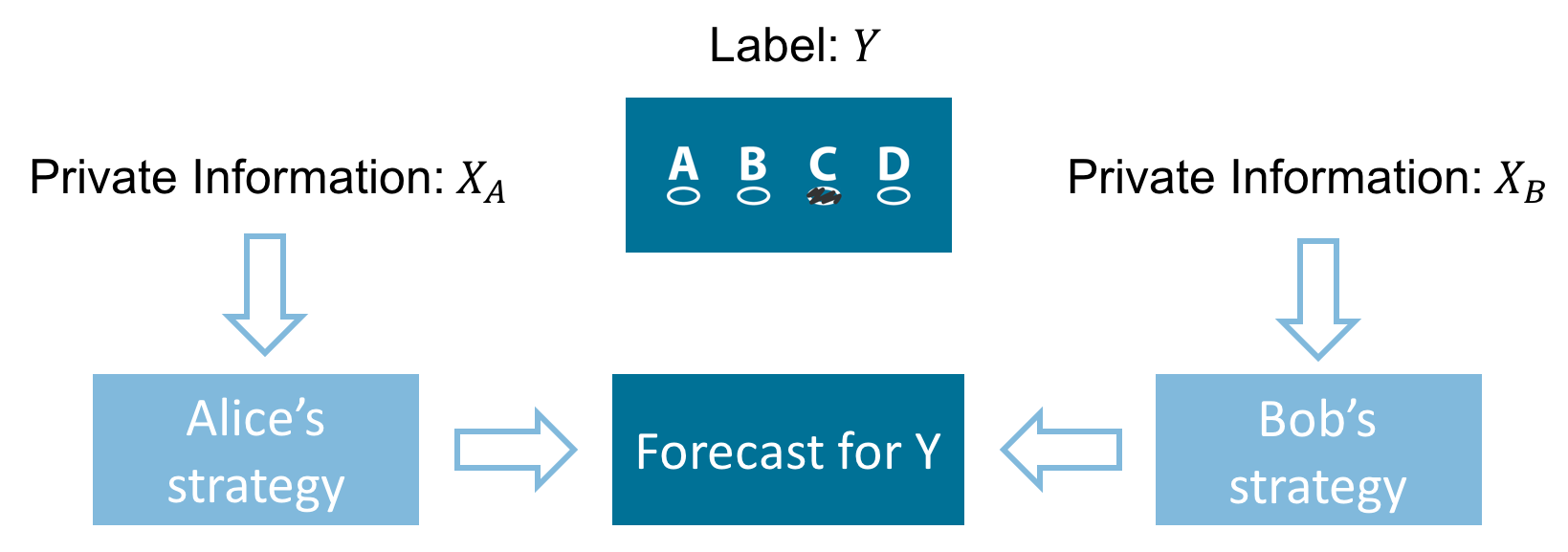

(**Mechanism design) Can we design proper instant reward schemes to incentivize high quality forecast for without instant access to ? (See Figure 2)

People will obtain instant payments from instant reward schemes. If we do not require the reward schemes to be instant, proper scoring rules will work by rewarding people in the future after is revealed. It turns out the above learning problem (*) and mechanism design problem (**) are essentially the same, since there is a natural correspondence between an evaluation of their performance and their rewards. The mechanism design applications still require the conditional independent assumption. To address the two problems, a first try would be rewarding the predictors according to their “agreement”, since high quality predictors should have a lot of agreement with each other. However, if we train the predictors based on this criterion, then the output of the training process will be two meaningless constant predictors which perfectly agree with each other (e.g. always forecast 100% success). We call this problem the “naive agreement” issue.

Note that the mechanism design problem (**) is closely related to the peer prediction literature, incentivizing high quality information reports without verification. It is natural to leverage the techniques and insights from peer prediction to address problems (*) and (**). In fact, the peer prediction literature provides an information theoretic idea to address the “naive agreement” issue, that is, replacing “agreement” by mutual information. In the current paper, we will show that with a natural assumption, conditioning on , , and are independent, we can address problem (*) and (**) simultaneously via rewarding the predictors the mutual information between them and using the predictors’ reward as the evaluation of their performance.

Our contribution

We build a natural connection between mechanism design and machine learning by simultaneously addressing a learning problem and a mechanism design problem in the context where ground truth is unknown, via the same information theoretic approach.

- Learning

-

We focus on the co-training problem [7]: learning how to forecast using two sources of information and , without access to any data labeled with ground truth (Section 3). By making a typical assumption in the co-training literature, conditioning on , and are independent, we reduce the learning problem to an optimization problem such that solving the learning problem is equivalent to picking the that maximize , i.e., the -mutual information gain between and (Section 4). Formally, we define the Bayesian posterior predictor as the predictor that maps any input information to its Bayesian posterior forecast for , i.e., . Then when both are Bayesian posterior predictors, is maximized and the maximal value is the -mutual information between and . With an additional mild restriction on the prior, is maximized if and only if both are permuted versions of the Bayesian posterior predictor.

We also design another family of optimization goals, -gain333 is a proper scoring rule., based on the family of proper scoring rules (Section 6). We can also reduce the learning problem to the -gain optimization problem. We will show a special case of the -gain, picking as the logarithmic scoring rule , corresponds to the maximum likelihood estimator method. The range of applications of -gain is more limited when compared with the range of applications of the -mutual information gain, since the application of -gain requires either one of the information sources to be low dimensional or that we have a simple generative model for the distribution over one of the information sources and ground truth labels, while the -mutual information gain does not have these restrictions.

As is typical in related literature, we do not investigate the computation complexity or data requirement of the learning problem.

To the best of our knowledge, this is the first optimization goal in the co-training literature that guarantees that the maximizer corresponds to the Bayesian posterior predictor, without any additional assumption. Thus, our method optimally aggregates the two sources of information.

- Mechanism design

-

Consider the scenario where we elicit forecasts for ground truth from agents and pay agents immediately. Without access to , given the prior on the distribution of , i.e., , 444This is not a very strong assumption since we do not need the knowledge of the joint distribution over the event and agents’ private information. by assuming agents’ private information are independent conditioning on and the prior satisfies some mild conditions, in the single-task setting (there is only a single forecasting task), we design a strictly truthful mechanism, the common ground mechanism, where truth-telling is a strict equilibrium (Section 5.2); in the multi-task (there are at least two a priori similar forecasting tasks) setting, we design a family of focal mechanisms, the multi-task common ground mechanism s, where the truth-telling equilibrium pays better than any other strategy profile and strictly higher than any non-permutation strategy profile (Section 5.1).

Technical contribution

Our main technical ingredient is a novel performance measurement, the -mutual information gain, which is an unbiased estimator of the -mutual information. To give a flavor of this measurement, we give an informal presentation here: both and are assigned a batch of forecasting tasks, the -mutual information gain between and is

| The agreements between ’s forecast and ’s forecast for the same task | ||

where is the conjugate of the convex function . With this measurement, two agreeing constant predictors have small gain since their outputs have large agreements for both the same task and different tasks. The formal definition will be introduced in Section 4.1 and the agreement measure is introduced in Definition 4.2.

The -mutual information gain is conceptually similar to the correlation payment scheme proposed by Dasgupta and Ghosh [14] (in the binary choice setting), and Shnayder et al. [39] (in the multiple choice setting), which pays agents “the agreement for the same task minus the agreement for the distinct task”. In Dasgupta and Ghosh [14] and Shnayder et al. [39], the payment scheme is designed for discrete signals and the measure of agreements is a simple indicator function. Kong and Schoenebeck [22] show that this correlation payment is related to a special -mutual information. Thus, the -mutual information gain can be seen as an extension of the correlation payment scheme that works for forecast reports.

1.1 Applications

In our startup running example, we consider the situation where one source of information is the features and another source of information is the crowdsourced feedback. In fact, our results apply to all kinds of information sources. For example, we can make both sources features or crowdsourced feedback. Different setups for the information sources and predictor candidates can bring different applications of our results.

Let’s consider the “learning with noisy labels” problem where the labels in the training data are a noisy version of the ground truth labels and the noise is independent. We can map this problem into our framework by letting be the noisy label of features . That is, is a noisy version of . Our framework guarantees that the Bayesian posterior predictor that forecasts using must be part of a maximizer of the optimization problem. However, there are many other maximizers. For example, since and are independent conditioning . The Bayesian posterior predictor that forecasts using is also part of a maximizer, since the scenario also satisfies the conditional independence assumption. If has much higher dimension than , we do not have this issue. But has the same signal space with in the learning with noisy label problem. Thus, it’s impossible to eliminate other maximizers without any side information here. With some side information (e.g. a candidate set , like linear regressions, that only contains our desired maximizer.), it’s possible to obtain the Bayesian posterior predictor that forecasts using . Note that our framework does not require a pre-estimation on the transition probability that transits the ground truth label to the noisy ground truth label , since our framework has this transition probability, which corresponds to the predictor , as parameters as well and learns the correct forecaster and the transition probability simultaneously.

Ratner et al. [35] propose a method to collect massive labels by asking the crowds to write heuristics to label the instances. Each instance is associated with many noisy labels outputted by the heuristics. In their setting, the crowds use a different source of information from the learning algorithm (e.g. the learning algorithm uses the biology description of the genes and the crowds use the scientific papers about the gene). Thus, the conditional independence assumption is natural here and we can map this setting’s training problem into our framework. Ratner et al. [35] preprocess the collected labels to approximate ground truth by assuming a particular information structure model on the crowds. Our framework is model-free and does not need to preprocess the collected labels since we can learn the best forecaster (predictor ) and the best processing/aggregation algorithm (predictor ) simultaneously.

Moreover, since the highest evaluation value of the predictors is the -mutual information between and , our results provide a method to calculate the -mutual information between any two sources of information of any format. Kong and Schoenebeck [22] propose a framework for designing information elicitation mechanisms that reward truth-telling by paying each agent the -mutual information between her report and her peers’ report. Thus, the -mutual information gain method can be combined with this framework to design information elicitation mechanisms when the information has a complicated format.

1.2 Related work

Learning

Co-training/multiview learning was first proposed by Blum and Mitchell [7] and explored by many works (e.g. Dasgupta et al. [15], Collins and Singer [10]). Xu et al. [43], Li et al. [24] give surveys on this literature. Although co-training is an important learning problem, it lacks a unified theory and a solid theoretic guarantee for the general model. Most traditional co-training methods require additional restrictions on the hypothesis space (e.g. weakly good hypotheses) to address the “naive agreement” issue and fail to deal with soft hypotheses. Soft hypotheses output a continuous signal (as opposed to hard hypothesis which output a discrete signal) and are typically required to fully aggregate the information from two sources. Becker [5] deals with a feature learning problem which is very similar to the co-training problem. Becker [5] seeks to maximize the Shannon mutual information between the output of two functions. However, their work only considers hard (not soft) hypotheses and lacks a solid theoretic analysis for the maximizer. Kakade and Foster [19] consider the multi-view regression and maximize the correlation between the two hypotheses. Their method captures the “mutual information” idea (in fact, correlation is a special -mutual information [22]) but their model has a very specific set up and the analysis cannot be extended to other co-training problems.

In contrast, we propose a simple, powerful and general information theoretic framework, -mutual information gain, that has a solid theoretic guarantee, works for soft hypothesis and addresses the “naive agreement” issue without any additional assumption.

Natarajan et al. [29], Sukhbaatar and Fergus [40] and many other works (e.g. Angluin and Laird [4], Khardon and Wachman [21], Scott et al. [38]) consider the learning with noisy labels problem. Natarajan et al. [29] consider binary labels and calibrate the original loss function such that the Bayesian posterior predictor that forecasts ground truth is a maximizer of the calibrated loss. Sukhbaatar and Fergus [40] extend this work to the multiclass setting. These works require additional estimation steps to learn the transition probability that transits the ground truth labels to the noisy labels and fix this transition probability in their calibration step. In contrast, by mapping this problem into our framework (Section 1.1), we do not need the additional estimation steps to make the calibrated forecaster part of a maximizer of our optimization problem, and can incorporate any kind of side information to learn the calibrated forecaster and true transition probability simultaneously.

Moreover, our results can handle more complicated setting where each instance is labeled by multiple labels. Rather than preprocessing the labels by a particular algorithm (e.g. majority vote, weighted average, spectral method) and assuming some information structure model among the crowds [35], our framework is model-free and can learn the best calibrated forecaster (predictor ) and the best processing algorithm (predictor ) simultaneously.

Raykar et al. [36] also jointly learn the calibrated forecaster and the distribution over the crowd-sourced feedback and ground truth labels. Raykar et al. [36] uses the maximum likelihood estimator and assumes a simple generative model for the distribution over the crowdsourced feedback and the ground truth labels, which is conditioning the ground truth label, the crowdsourced feedback is drawn from a binomial distribution, while our framework is model-free. We also extend the maximum likelihood estimator method in Raykar et al. [36] to a general family of estimators, -gain estimators, based on the family of proper scoring rules, which also jointly learn the calibrated forecaster and the distribution. We will show the range of applications of -gain is more limited compared with the range of applications of the -mutual information gain (see Section 6.3 for more details). Cid-Sueiro [9] also uses proper scoring rules to design the loss functions that address the learning with noisy labels problem. However, Cid-Sueiro [9] designs a different family of loss functions from the -gain and cannot jointly learn the calibrated forecaster and the distribution.

Generative Adversarial Networks (GAN) [18] combine game theory and learning theory to make innovative progress. We also combine game theory and learning theory by proposing a peer prediction game between two predictors. The game in GAN is a zero-sum competitive game while the game in the current paper is collaborative.

Several learning problems (e.g. finding the pose of an object in an image [6], blind source separation [8], feature selection [33]) use mutual information maximization (infomax) as their optimization goal. Some of these problems require data labeled with ground truth and some of them have a very different problem set up than our work.

We borrow the techniques about the duality of -divergence from Nguyen et al. [30, 31]. Nguyen et al. [30] show a correspondence between the -divergence and the surrogate loss in the binary supervised learning setting and Nguyen et al. [31] propose a way to estimate the -divergence between two high dimensional random variables. We apply the duality of -divergence to an unsupervised learning problem and not restricted to the binary setting.

We also differ from the crowdsourcing literature that infers ground truth answers from agents’ reports (e.g. [45, 20, 44, 13]) in the sense that their agents’ reports are a simple choice (e.g. A, B, C, D) while in our setting, the report can come from a space larger than the space of ground truth answers, perhaps even a very high dimensional vector.

Mechanism design

Our mechanism design setting differ from the traditional peer prediction literature (e.g.[28, 34, 14, 22, 39]) since we are eliciting forecast rather than a simple signal. We can discretize the forecast report and apply the traditional peer prediction literature results. However, this will only provide approximated truthfulness and fail to design focal mechanisms which pay truth-telling strictly better than any other non-permutation equilibrium since the forecast is discretized, while our mechanisms are focal for 2 tasks setting.

Witkowski et al. [42] consider the forecast elicitation situation and assume that they have an unbiased estimator of the optimal forecast while we assume an additional conditional independence assumption but do not need the unbiased estimator.

Liu and Chen [25, 26] connect mechanism design with learning by using the learning methods to design peer prediction mechanisms. In the setting where several agents are asked to label a batch of instances, Liu and Chen [25] design a peer prediction mechanism where each agent is paid according to her answer and a reference answer generated by a classification algorithm using other agents’ reports. Liu and Chen [26] also use surrogate loss functions as tools to develop a multi-task mechanism that achieves truthful elicitation in dominant strategy when the mechanism designer only has access to agents’ reports. Instead of using learning methods to design the peer prediction mechanisms, our work uses peer prediction mechanism design techniques to address a learning problem. Moreover, our mechanism design problem has a very different set up from Liu and Chen [25, 26]. Agarwal and Agarwal [2] connect learning theory with information elicitation by showing the equivalence between the calibrated surrogate losses in supervised learning and the elicitation of certain properties of the underlying conditional label distribution. Both our learning problem and mechanism design problem have a very different set up from theirs.

Independent work

Like the current paper, McAllester [27] also uses Shannon mutual information to propose an information theoretic training objective that can deal with soft hypotheses/classifiers. However, the optimization functions from these two works are different. We also use a more general information measure, -mutual information, which has Shannon mutual information as a special case, and provide a formal analysis for this general framework. Additionally, we propose an innovative connection between co-training and peer prediction.

2 Preliminaries

Given a finite set , for any function , we use to represent the vector . Given a finite set , is the set of all distributions over .

2.1 -divergence and Fenchel’s duality

-divergence [3, 12]

-divergence is a non-symmetric measure of the difference between distribution and distribution and is defined to be

where is a convex function and .

Here we introduce two -divergences in common use: KL divergence, and Total Variance Distance.

Example 2.1 (KL divergence).

Choosing as the convex function , -divergence becomes KL divergence

Example 2.2 (Total Variance Distance).

Choosing as the convex function , -divergence becomes Total Variance Distance

Definition 2.3 (Fenchel Duality [37]).

Given any function , we define its convex conjugate as a function that also maps to such that

2.2 -mutual information

Given two random variables whose realization space are and , let and be two probability measures where is the joint distribution of and is the product of the marginal distributions of and . Formally, for every pair of ,

If is very different from , the mutual information between and should be high since knowing changes the belief for a lot. If equals to , the mutual information between and should be zero since is independent with . Intuitively, the “distance” between and represents the mutual information between them.

Definition 2.5 (-mutual information [22]).

The -mutual information between and is defined as

where is -divergence. -mutual information is always non-negative [22].

-mutual information is used in the peer prediction literature since if the information is measured by -mutual information, any “data processing” on either of the random variables will decrease the amount of information crossing them. Thus, in peer prediction, if we pay agents according to the -mutual information between her information and her peers’ information, agents will be incentivized to report all information to maximize their payments555In the current paper, we do not directly use the data processing inequality of -mutual information. Thus, we omit the formal introduction here. The interested reader is refer to Kong and Schoenebeck [22]. .

Two examples of -mutual information are Shannon mutual information [11] (Choosing -divergence as KL divergence) and (Choosing -divergence as Total Variation Distance).

We define as the ratio between and , i.e.,

represents the “pointwise mutual information(PMI)” between and . Lemma 2.4 directly implies:

Lemma 2.6 (Dual version of -mutual information).

where is a set of functions that maps to .

The equality holds if and only if .

| -divergence | ) | ||

|---|---|---|---|

| Total Variation Distance | sign() | sign() | |

| KL divergence | |||

| Reverse KL | ) | ||

| Pearson | |||

| Squared Hellinger |

2.3 Proper scoring rules

A scoring rule [41, 17] takes in a signal and a distribution over signals and outputs a real number. A scoring rule is proper if, whenever the first input is drawn from a distribution , then will maximize the expectation of over all possible inputs in to the second coordinate. A scoring rule is called strictly proper if this maximum is unique. We will assume throughout that the scoring rules we use are strictly proper. Slightly abusing notation, we can extend a scoring rule to be by simply taking . We note that this means that any proper scoring rule is linear in the first term.

Example 2.7 (Log Scoring Rule [41, 17]).

Fix an outcome space for a signal . Let be a reported distribution. The Logarithmic Scoring Rule maps a signal and reported distribution to a payoff as follows:

Let the signal be drawn from some random process with distribution .

Then the expected payoff of the Logarithmic Scoring Rule

This value will be maximized if and only if .

2.4 Property of the pointwise mutual information

We will introduce a simple property of the pointwise mutual information that we will use multiple times in the future. In addition to several different formats of the pointwise mutual information (e.g. joint distribution/product of the marginal distributions, posterior/prior), if there exists a latent random variable such that random variable and random variable are independent conditioning on , we can also represent the pointwise mutual information between and by the “agreement” between the “relationship” between and , and the “relationship” between and .

Claim 2.8.

When random variables , are independent conditioning on ,

We defer the proof to the appendix.

3 General Model and Assumptions

Let be three random variables and we define prior as the joint distribution over . We want to forecast the ground truth whose realization is a signal in a finite set . are two sources of information that are related to . ’s realization is a signal in a finite set . ’s realization is a signal in a finite set . We may have access to both of the realizations of and or only one of them. Thus, we need to learn the relationship between and to forecast . It’s impossible to learn by only accessing the samples of without additional assumption. We make the following conditional independence assumption:

Assumption 3.1 (Conditional independence).

We assume that conditioning on , , and are independent.

Intuitively, can be seen as the “intersection” between and . To better understand this assumption and its limitations we return to our running example where the variable is the success of a start-up. In this case, if both and contain the sex of the CEO (which we assume is independent of ), then this assumption will not hold. To make it hold, either would need to be redefined to contain the sex of the CEO, or this information would need to be removed from either or . For the mechanism design application, if the assumption is violated, for example both agents are sexists and forecast using the sex of the CEO, then it is impossible to avoid paying them for this useless/harmful information.

3.1 Well-defined and stable prior

We call a solution if conditioning on , , and are independent. is a solution. However, there are a lot of solutions. For example, conditioning on or , and are independent, which means and are both solutions. Thus, we have an additional restriction on the prior: well-defined prior and stable prior.

We will need restrictions on the prior when we analyze the strictness of our learning algorithm/mechanism. Readers can skip this section without losing the core idea of our results.

To infer the relationship between and with only samples of , we cannot do better than to just solve the system of equations (1), given the joint distribution over : . Our goal is to obtain the Bayesian posterior predictor. Thus, we list a system that the Bayesian posterior predictor satisfies. The system below equations involve variables , and . We insist , and is a solution and we call it the desired solution.

| (1) | ||||

Claim 2.8 shows the above system has the desired solution.

Note that any permutation of a solution is still a valid solution666We may be able to distinguish a solution with its permuted version if we have some side information (e.g. the prior of /a few samples).. Since we cannot do better than to solve the above system, if the above system only has one “unique” solution, in the sense that any two solutions are permuted version of each other, we call the prior a well-defined prior. Formally,

Definition 3.2 (Well-defined).

A prior is well-defined if for any two solutions , and , of the system of equations (1), there exists a permutation such that for any , , .

The well-defined prior exist since intuitively, if and are high and is low, it is likely is the “unique intersection” since the number of constraints of the system will be much greater than the number of variables.

We say a prior is stable if fixing part of the desired solution of the system (1), in order to make it still a solution of the system, other parts of the desired solution should also be fixed.

Definition 3.3 (Stable).

We require stable priors when we design strictly truthful mechanisms.

3.2 Predictors

This section gives the definition of predictors. We have two sets of samples and which are i.i.d samples of and respectively. For , s are i.i.d samples of the joint random variable .

A predictor for maps to a forecast for ground truth . We similarly define the predictors for . We define the Bayesian posterior predictor as the predictor that maps any input information to its Bayesian posterior forecast for , i.e., .

With the conditional independence assumption, we have

| (conditional independence) | ||||

| ( is the pointwise mutual information.) |

When we have access to both the sources where and , given the prior of the ground truth , we can construct an aggregated forecast for using :

In this case, if both and are the Bayesian posterior predictor, the aggregated forecast is the Bayesian posterior predictor as well. Thus, it’s sufficient to only train and . In the rest sections, we will show how to train and (Section 4), given the two sets of samples and , as well as how to incentivize high quality predictors from the crowds (Section 5).

4 Co-training: finding the common ground truth

We have a set of candidates for the predictor for and a set of candidates for the predictor for . We sometimes call each predictor candidate a hypothesis. Given the two sets of samples and , our goal is to figure out the best hypothesis in and the best hypothesis in simultaneously. Thus, we need to design proper “loss function” such that the best hypotheses minimize the loss. In fact, we will show how to design a proper “reward function” such that the best hypotheses maximize the reward.

4.1 -mutual information gain

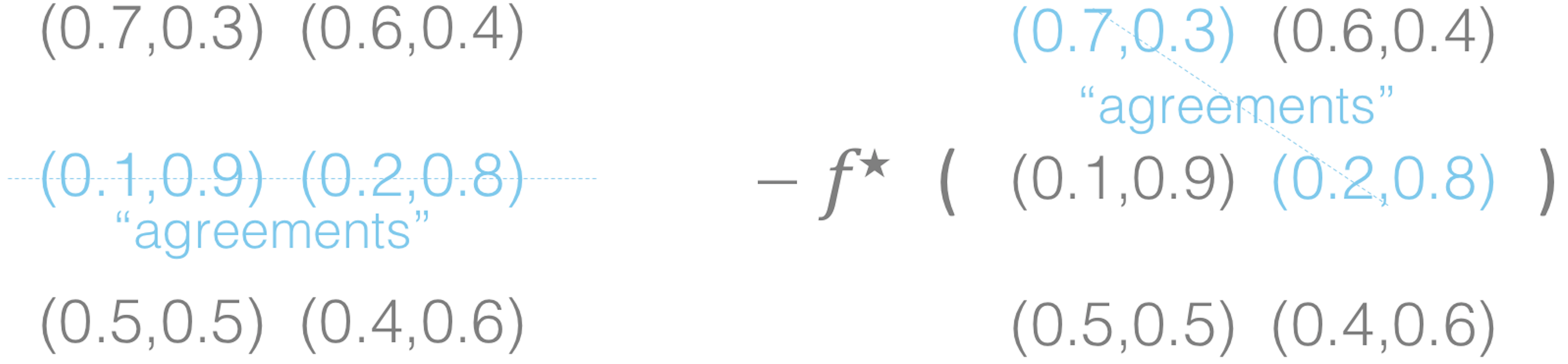

-mutual information gain (Figure 3)

- Hypothesis

-

We are given , : the set of hypotheses/predictor candidates for and , respectively.

- Gain

-

Given reward function ,

for each , reward “the amount of agreement” between the two predictor candidates’ predictions for task , i.e.,for each distinct pair , punish both predictor candidates “the amount of agreement” between their predictions for a pair of distinct tasks , i.e.,

The -mutual information gain that is corresponding to the reward function is

Lemma 4.1.

The expected total -mutual information gain is maximized over all possible , , and if and only if for any ,

The maximum is

Proof.

are i.i.d. realizations of . Therefore, the expected -mutual information gain is The results follow from Lemma 2.6. ∎

Although any reward function corresponds to an -mutual information gain function, we need to properly design the reward function such that, fixing , there exist hypotheses to maximize the corresponding -mutual information gain to the -mutual information between the two sources. We will use the intuition from Lemma 4.1 to design such reward functions in the next section.

4.2 Maximizing the -mutual information gain

In this section, we will construct a special reward function and then show that the maximizers of the corresponding -mutual information gain are the Bayesian posterior predictors.

Definition 4.2 ().

We define reward function as a function that maps the two hypotheses’ outputs and the vector to

where . When is differentiable,

With this definition of the reward function, fixing which can be seen as the prior over , the “amount of agreement” between two predictions are an increasing function of

which is intuitive and reasonable. The increasing function is the derivative of the convex function . By carefully choosing convex function , we can use any increasing function here.

Example 4.3.

Here we present some examples of the -mutual information gain with reward function , associated with different -divergences. We use Table 1 as reference for and .

Total variation distance:

KL divergence:

Pearson:

Theorem 4.4.

With the conditional independent assumption on , given the samples , given a convex function , we define the optimization goal as the expected -mutual information gain with reward function , i.e.,

and optimize over all possible hypotheses , and distribution vectors . We have

- SolutionMaximizer:

-

any solution corresponds to a maximizer of 777Given the prior over , we can fix as the prior over . Without knowing the prior over , becomes a variable of the optimization goal and helps us learn the prior over . : for any solution ,

and the prior over , , is the maximizer of and the maximum is ;

- Maximizer(Permuted) Ground truth

-

when the prior is well-defined, is differentiable, and is invertible, any maximizer of corresponds to the (possibly permuted) ground truth : for any maximizer of , there exists a permutation such that

and .

The above theorem neither investigates computation complexity (which may be affected by the choice of ), data requirements, nor the choice of the hypothesis class for practical implementation (see Section 7 for more discussion).

Proof for Theorem 4.4.

Lemma 4.1 shows that the expected -mutual information gain is maximized if and only if for any ,

(1) SolutionMaximizer: For any solution , we can construct

and . Then

| (Claim 2.8) |

Thus, based on Lemma 4.1, any solution corresponds to a maximizer of the optimization goal.

(2)Maximizer(Permuted) Ground truth: For any maximizer of the optimization goal, when is differentiable, Lemma 4.1 shows that

When is invertible, we have

for all .

Thus, is actually the solution of the system (1). When the prior is well-defined, there exists a permutation such that

and where is the ground truth.

∎

5 Forecast elicitation without verification

This section considers the setting where the forecasts are provided by the crowds and we want to incentivize high quality forecast by providing an instant reward without instant access to the ground truth.

There is a forecasting task. Alice and Bob have private information correspondingly and are asked to forecast the ground truth . We denote , by , correspondingly. Alice and Bob are asked to report their Bayesian forecast , . We denote their actual reports by and . Without access to the realization of , we want to incentivize both Alice and Bob play truth-telling strategies, i.e., honestly reporting their forecast , for .

We define the strategy of Alice as a mapping from (private signal) to a probability distribution over the space of all possible forecast for random variable . Analogously, we define Bob’s strategy . Note that essentially each (possibly mixed) strategy can be seen as a (possibly random) predictor where is a random forecast drawn from distribution . In particular, the truthful strategy corresponds to the Bayesian posterior predictor.

We say agents play a permutation strategy profile if there exists permutation such that each agent always reports given her truthful report is .

Note that without any side information about , we cannot distinguish the scenario where agents are honest and the scenario where agents play a permutation strategy profile. Thus, it is too much to ask truth-telling to be strictly better than any other strategy profile. The focal property defined in the following paragraph is the optimal property we can obtain.

Mechanism Design Goals

- (Strictly) Truthful

-

Mechanism is (strictly) truthful if truth-telling is a (strict) equilibrium.

- Focal

-

Mechanism is focal if it is strictly truthful and each agent’s expected payment is maximized if agents tell the truth; moreover, when agents play a non-permutation strategy profile, each agent’s expected payment is strictly less.

We consider two settings:

- Multi-task

-

Each agent is assigned several independent a priori similar forecasting tasks in a random order and is asked to report her forecast for each task.

- Single-task

-

All agents are asked to report their forecast for the same single task.

In the single-task setting, it’s impossible to design focal mechanisms since agents can collaborate to pick an arbitrary and pretend that they know . However, we will show we can design strictly truthful mechanism in the single-task setting. In the multi-task setting, since agents may be assigned different tasks and the tasks show in random order, they cannot collaborate to pick an arbitrary for each task. In fact, we will show if the number of tasks is greater or equal to 2, we can design a family of focal mechanisms.

Achieving the focal goal in the multi-task setting is very similar to what we did in finding the common ground truth. Note that in the forecast elicitation problem, incentivizing a truthful strategy is equivalent to incentivizing the Bayesian posterior predictor. Thus, we can directly use the -mutual information gain as the reward in the multi-task setting. Achieving the strictly truthful goal in the single-task setting is more tricky and we will return to it later.

5.1 Multi-task: focal forecast elicitation without verification

We assume Alice is assigned tasks set and Bob is assigned tasks set . For each task , Alice’s private information is and Bob’s private information is . The ground truth of this task is .

Multi-task common ground mechanism

Given the prior distribution over , a convex and differentiable function whose convex conjugate is ,

- Report

-

for each task , Alice is asked to report ; for each task , Bob is asked to report . We denote their actual reports by and .

- Payment

-

For each , reward both Alice and Bob “the amount of agreement” between their forecast in task , i.e.,

for each pair of distinct tasks , punish both Alice and Bob “the amount of agreement” between their forecast in distinct tasks , i.e.,

In total, both Alice and Bob are paid

where

We do not want agents to collaborate with each other based on the index of the task or other information in addition to the private information. Thus, we make the following assumption to guarantee the index of the task is meaningless for all agents.

Assumption 5.1 (A priori similar and random order).

For each task , fresh i.i.d. realizations of are generated. All tasks appear in a random order, independently drawn for each agent.

Theorem 5.2.

With the conditional independence assumption, and a priori similar and random order assumption, when the prior is stable and well-defined, given the prior distribution over the , given a differential convex function whose derivative is invertible, if , then is focal.

When both Alice and Bob are honest, each of them’s expected payment in is

The non-negativity of implies that agents are willing to participate in the mechanism. Like Theorem 4.4, in order to show Theorem 5.2, we need to first introduce a lemma which is very similar to Lemma 4.1.

Lemma 5.3.

With the conditional independence assumption, the expected total payment is maximized over Alice and Bob’s strategies if and only if , for any ,

The maximum is

5.2 Single-task: strictly truthful forecast elicitation without verification

This section introduces the strictly truthful mechanism in the single-task setting. If we know the realization of , we can simply apply a proper scoring rule and pay Alice and Bob and respectively. Then according to the property of the proper scoring rule, Alice and Bob will honestly report their truthful forecast to maximize their expected payment. However, we do not know the realization of . In the information elicitation without verification setting where Alice and Bob are required to report their information, Miller et al. [28] propose the “peer prediction” idea, that is, pays Alice the accuracy of the forecast that predicts Bob’s information conditioning Alice’s information, i.e.,

where and are Alice and Bob’s reported information. We note the peer prediction mechanism in Miller et al. [28] is truthful. With a similar “peer prediction” idea, we propose a strictly truthful mechanism in forecast elicitation.

Common ground mechanism

Given the prior distribution over ,

- Report

-

Alice and Bob are required to report , . We denote their actual reports by and .

- Payment

-

Both Alice and Bob are paid

Theorem 5.4.

With the conditional independence assumption (and when the prior is stable), given the prior distribution over the , the common ground mechanism is (strictly) truthful;

moreover, when both Alice and Bob are honest, each of them’s expected payment in the common ground mechanism is the Shannon mutual information between their private information

The non-negativity of the Shannon mutual information implies that agents are willing to participate in the mechanism. The (strictly) truthful property of the common ground mechanism is proved by the fact that log scoring rule is strictly proper.

Proof.

When both Alice and Bob are honest, their payment is according to Claim 2.8. Their expected payment will be

Given that Bob honestly reports , we would like to show that the expected payment of Alice is less than regardless of the strategy Alice plays. The expected payment of Alice is

| ( is a constant that does not depend on Alice’s strategy) | ||||

Moreover, fixing

Thus, can be seen as a forecast for . Since for any , we have

| (2) | ||||

The non-negativity of the Shannon mutual information implies that agents are willing to participate in the mechanism.

It remains to analyze the strictness of the truthfulness. We need to show for any , given that Alice receives , she will obtain strictly less payment via reporting .

Given that Alice receives , her expected payment is

| (see equation (2)) | ||||

| (3) |

Note that when . When the prior is stable, since , then is not the solution of system (1). This implies that there exists such that

Thus, the inequality (3) must be strict. Therefore, when the prior is stable, the common ground mechanism is strictly truthful.

∎

6 -gain

In this section, we will extend the maximum likelihood estimator method in Raykar et al. [36] to a general family of optimization goals—-gain and compare the general family with our -mutual information gain. We will see the application of -gain requires either one of the information sources to be low dimensional or that we have a simple generative model for the distribution over one of the information sources and ground truth label. Thus, the range of applications of -gain is more limited compared with the range of applications of -mutual information gain.

In Raykar et al. [36], is a feature vector which has multiple crowdsourced labels . We have access to which are i.i.d samples of . Raykar et al. [36] also have the conditional independence assumption.

6.1 Maximum likelihood estimator (MLE)

Let be two parameters that control the distribution over and and the distribution over and respectively.

With the conditional independence assumption, we have

The MLE is a pair of parameters that maximizes the expected

Raykar et al. [36] use the MLE to estimate the parameters. In order to compare this MLE method with our -mutual information gain framework, we map this MLE method into our language and provide a theoretical analysis for the condition when MLE is meaningful.

-gain/MLE

- Hypothesis

-

We are given , : the set of hypotheses candidates for and , respectively. Note that maps into a vector in rather than a distribution vector.

- Gain

-

We see

as a forecast for random variable conditioning on and we reward the hypotheses -gain—the accuracy of this forecast via log scoring rule (LSR):

We use to represent the dot product between two vectors.

Note that by picking as the set of mappings—associated with a set of parameters —that map to and picking as the set of mappings—associated with a set of parameters —that map to , maximizing -gain is equivalent to obtaining MLE.

The idea of -gain is very similar with the original peer prediction idea introduced in Section 5.2 as well as our common ground mechanism.

Theorem 6.1.

When for all , the ground truth corresponds to a maximizer of -gain:

The maximum is the conditional Shannon entropy .

Remark 6.2.

Note that without the restriction: for all ,

is not a maximizer and we will have a meaningless maximizer and .

By picking as the set of mappings—associated with a set of parameters —that map to , the restriction for all satisfies naturally. However, it requires the knowledge of the generative distribution model over and with parameter . Raykar et al. [36] assume a simple distribution model between and with parameter —conditioning the ground truth label, the crowdsourced feedback is drawn from a binomial distribution, such that has a simple explicit form.

Proof of Theorem 6.1.

Fixing , since for all , we have

Since for any , we have

| (conditional independence) |

Thus,

is a maximizer and the maximum is the conditional Shannon entropy .

∎

6.2 Extending -gain to -gain

The property for any is also valid for all proper scoring rules. Thus, we can naturally extend the MLE to -gain by replacing the by any given proper scoring rule .

-gain

- Hypothesis

-

We are given , : the set of hypotheses candidates for and , respectively.

- Gain

-

We see

as a forecast for random variable conditioning on and we reward the hypotheses -gain—the accuracy of this forecast via a given proper scoring rule :

Note that the general -gain may involve the calculations of while -gain only requires the value of . Thus, unlike -gain, the general -gain may be only applicable for low dimensional , even if we assume a simple generative distribution model over and .

Theorem 6.3.

Given a proper scoring rule , when for all , the ground truth corresponds to a -gain maximizer:

The proof is the same with Theorem 6.1 except that we replace by for any .

6.3 Comparing -gain with -mutual information gain

Generally, -mutual information gain can be applied to a more general setting.

-gain requires the restriction for all . Thus, -gain requires the full knowledge of for all to check whether it satisfies the restriction, while for the -mutual information gain, it is sufficient to just have the access to the outputs of the hypothesis: . Therefore, in the mechanism design part, we can only use -mutual information gain to design focal mechanisms since we only have the outputs from agents.

Moreover, is also hard to check when is very large. For example, when is a black-and-white image, and checking requires time. Normalizing such that it satisfies the condition also requires time. Thus, when is very large, we need a simple generative distribution model between and with parameter such that we can pick as the set of mappings—associated with a set of parameters —that map to , to make the restriction for all satisfy naturally. When we have the simple generative distribution model, we can use -gain. The general -gain involves the calculations of the dimensional vector——for each . Thus, the general -gain is only applicable to low dimensional .

In the learning with noisy labels problem, the distribution between and can be represented by a simple transition matrix and is low dimensional. Therefore, both -gain and -mutual information gain can be applied to the learning with noisy labels problem.

Therefore, the application of -gain requires either one of the information sources to be low dimensional or that we have a simple generative model for the distribution over one of the information sources and ground truth label, while -mutual information gain does not have the restrictions.

7 Conclusion and discussion

We build a natural connection between mechanism design and machine learning by addressing two related problems: (1) co-training: learning to forecast ground truth using two conditionally independent sources, without access to labeled data; (2) forecast elicitation: eliciting high quality forecasts from the crowds without verification, by the same information theoretic approach.

For the co-training problem, as usual in the related literature, we reduce the problem to an optimization problem and do not investigate the computation complexity or the data requirements. To implement our -mutual information gain framework in practice, we implicitly assume that for high dimensional , there exists a trainable set of hypotheses (e.g. neural networks) that is sufficiently rich to contain the Bayesian posterior predictor but not everything to cause over-fitting. The most apparent empirical direction will be running experiments on real data by training two neural networks to test our algorithms. Interesting theoretic directions include the analysis of the Bayesian risk and the influence of the choice of the convex function on the convergence rate.

For forecast elicitation, the most apparent direction will be performing real-world experiments. To apply our mechanisms, we do not need that every two agents’ information is conditionally independent. In fact, for each agent, we only need to find a single reference agent for her such that the reference agent’s information is conditionally independent of hers. Then we can run our mechanisms on the agent and her reference agent. In practice, we can pair the agents with some side information and make sure each pair of agents’ information is conditionally independent.

Another interesting direction is to ensure fairness, in particular, that agents are not incentivized to coordinate on stereotypes. One solution, is suppressing information from some of the agents and using our framework. However, when this is not possible, the prior peer prediction work on cheap signals [16, 23] may be helpful in addressing this issue.

Acknowledgement

We thank Clayton Scott for useful conversations.

References

- [1]

- Agarwal and Agarwal [2015] Arpit Agarwal and Shivani Agarwal. 2015. On consistent surrogate risk minimization and property elicitation. In Conference on Learning Theory. 4–22.

- Ali and Silvey [1966] Syed Mumtaz Ali and Samuel D Silvey. 1966. A general class of coefficients of divergence of one distribution from another. Journal of the Royal Statistical Society. Series B (Methodological) (1966), 131–142.

- Angluin and Laird [1988] Dana Angluin and Philip Laird. 1988. Learning from noisy examples. Machine Learning 2, 4 (1988), 343–370.

- Becker [1996] Suzanna Becker. 1996. Mutual information maximization: models of cortical self-organization. Network: Computation in neural systems 7, 1 (1996), 7–31.

- Bell and Sejnowski [1995] Anthony J Bell and Terrence J Sejnowski. 1995. An information-maximization approach to blind separation and blind deconvolution. Neural computation 7, 6 (1995), 1129–1159.

- Blum and Mitchell [1998] Avrim Blum and Tom Mitchell. 1998. Combining labeled and unlabeled data with co-training. In Proceedings of the eleventh annual conference on Computational learning theory. ACM, 92–100.

- Cardoso [1997] J-F Cardoso. 1997. Infomax and maximum likelihood for blind source separation. IEEE Signal processing letters 4, 4 (1997), 112–114.

- Cid-Sueiro [2012] Jesús Cid-Sueiro. 2012. Proper losses for learning from partial labels. In Advances in Neural Information Processing Systems. 1565–1573.

- Collins and Singer [1999] Michael Collins and Yoram Singer. 1999. Unsupervised models for named entity classification. In 1999 Joint SIGDAT Conference on Empirical Methods in Natural Language Processing and Very Large Corpora.

- Cover and Thomas [2006] Thomas M Cover and Joy A Thomas. 2006. Elements of information theory 2nd edition. (2006).

- Csiszár et al. [2004] Imre Csiszár, Paul C Shields, et al. 2004. Information theory and statistics: A tutorial. Foundations and Trends® in Communications and Information Theory 1, 4 (2004), 417–528.

- Dalvi et al. [2013] Nilesh Dalvi, Anirban Dasgupta, Ravi Kumar, and Vibhor Rastogi. 2013. Aggregating crowdsourced binary ratings. In Proceedings of the 22nd international conference on World Wide Web. ACM, 285–294.

- Dasgupta and Ghosh [2013] Anirban Dasgupta and Arpita Ghosh. 2013. Crowdsourced judgement elicitation with endogenous proficiency. In Proceedings of the 22nd international conference on World Wide Web. 319–330.

- Dasgupta et al. [2002] Sanjoy Dasgupta, Michael L Littman, and David A McAllester. 2002. PAC generalization bounds for co-training. In Advances in neural information processing systems. 375–382.

- Gao et al. [2016] A. Gao, J. R. Wright, and K. Leyton-Brown. 2016. Incentivizing Evaluation via Limited Access to Ground Truth: Peer-Prediction Makes Things Worse. ArXiv e-prints (June 2016). arXiv:cs.GT/1606.07042

- Gneiting and Raftery [2007] Tilmann Gneiting and Adrian E Raftery. 2007. Strictly proper scoring rules, prediction, and estimation. J. Amer. Statist. Assoc. 102, 477 (2007), 359–378.

- Goodfellow et al. [2014] Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. 2014. Generative adversarial nets. In Advances in neural information processing systems. 2672–2680.

- Kakade and Foster [2007] Sham M Kakade and Dean P Foster. 2007. Multi-view regression via canonical correlation analysis. In International Conference on Computational Learning Theory. Springer, 82–96.

- Karger et al. [2014] David R Karger, Sewoong Oh, and Devavrat Shah. 2014. Budget-optimal task allocation for reliable crowdsourcing systems. Operations Research 62, 1 (2014), 1–24.

- Khardon and Wachman [2007] Roni Khardon and Gabriel Wachman. 2007. Noise tolerant variants of the perceptron algorithm. Journal of Machine Learning Research 8, Feb (2007), 227–248.

- Kong and Schoenebeck [2016] Y. Kong and G. Schoenebeck. 2016. An Information Theoretic Framework For Designing Information Elicitation Mechanisms That Reward Truth-telling. ArXiv e-prints (May 2016). arXiv:cs.GT/1605.01021

- Kong and Schoenebeck [2018] Y. Kong and G. Schoenebeck. 2018. Eliciting Expertise without Verification. ArXiv e-prints (Feb. 2018). arXiv:cs.GT/1802.08312

- Li et al. [2016] Yingming Li, Ming Yang, and Zhongfei Zhang. 2016. Multi-view representation learning: A survey from shallow methods to deep methods. arXiv preprint arXiv:1610.01206 (2016).

- Liu and Chen [2017] Yang Liu and Yiling Chen. 2017. Machine-Learning Aided Peer Prediction. In Proceedings of the 2017 ACM Conference on Economics and Computation (EC ’17). ACM, New York, NY, USA, 63–80. https://doi.org/10.1145/3033274.3085126

- Liu and Chen [2018] Yang Liu and Yiling Chen. 2018. Surrogate Scoring Rules and a Dominant Truth Serum for Information Elicitation. CoRR abs/1802.09158 (2018). arXiv:1802.09158 http://arxiv.org/abs/1802.09158

- McAllester [2018] D. McAllester. 2018. Information Theoretic Co-Training. ArXiv e-prints (Feb. 2018). arXiv:cs.LG/1802.07572

- Miller et al. [2005] N. Miller, P. Resnick, and R. Zeckhauser. 2005. Eliciting informative feedback: The peer-prediction method. Management Science (2005), 1359–1373.

- Natarajan et al. [2013] Nagarajan Natarajan, Inderjit S Dhillon, Pradeep K Ravikumar, and Ambuj Tewari. 2013. Learning with noisy labels. In Advances in neural information processing systems. 1196–1204.

- Nguyen et al. [2009] XuanLong Nguyen, Martin J Wainwright, and Michael I Jordan. 2009. On surrogate loss functions and f-divergences. The Annals of Statistics (2009), 876–904.

- Nguyen et al. [2010] XuanLong Nguyen, Martin J Wainwright, and Michael I Jordan. 2010. Estimating divergence functionals and the likelihood ratio by convex risk minimization. IEEE Transactions on Information Theory 56, 11 (2010), 5847–5861.

- Nowozin et al. [2016] Sebastian Nowozin, Botond Cseke, and Ryota Tomioka. 2016. f-gan: Training generative neural samplers using variational divergence minimization. In Advances in Neural Information Processing Systems. 271–279.

- Peng et al. [2005] Hanchuan Peng, Fuhui Long, and Chris Ding. 2005. Feature selection based on mutual information criteria of max-dependency, max-relevance, and min-redundancy. IEEE Trans. on pattern anal. and machine intel. 27, 8 (2005), 1226–1238.

- Prelec [2004] D. Prelec. 2004. A Bayesian Truth Serum for subjective data. Science 306, 5695 (2004), 462–466.

- Ratner et al. [2016] Alexander J Ratner, Christopher M De Sa, Sen Wu, Daniel Selsam, and Christopher Ré. 2016. Data programming: Creating large training sets, quickly. In Advances in Neural Information Processing Systems. 3567–3575.

- Raykar et al. [2010] Vikas C Raykar, Shipeng Yu, Linda H Zhao, Gerardo Hermosillo Valadez, Charles Florin, Luca Bogoni, and Linda Moy. 2010. Learning from crowds. Journal of Machine Learning Research 11, Apr (2010), 1297–1322.

- Rockafellar et al. [1966] R Tyrrell Rockafellar et al. 1966. Extension of Fenchel’duality theorem for convex functions. Duke mathematical journal 33, 1 (1966), 81–89.

- Scott et al. [2013] Clayton Scott, Gilles Blanchard, and Gregory Handy. 2013. Classification with asymmetric label noise: Consistency and maximal denoising. In Conference On Learning Theory. 489–511.

- Shnayder et al. [2016] Victor Shnayder, Arpit Agarwal, Rafael Frongillo, and David C Parkes. 2016. Informed truthfulness in multi-task peer prediction. In Proceedings of the 2016 ACM Conference on Economics and Computation. ACM, 179–196.

- Sukhbaatar and Fergus [2014] Sainbayar Sukhbaatar and Rob Fergus. 2014. Learning from noisy labels with deep neural networks. arXiv preprint arXiv:1406.2080 2, 3 (2014), 4.

- Winkler [1969] Robert L Winkler. 1969. Scoring rules and the evaluation of probability assessors. J. Amer. Statist. Assoc. 64, 327 (1969), 1073–1078.

- Witkowski et al. [2017] Jens Witkowski, Pavel Atanasov, Lyle H Ungar, and Andreas Krause. 2017. Proper Proxy Scoring Rules.. In AAAI. 743–749.

- Xu et al. [2013] Chang Xu, Dacheng Tao, and Chao Xu. 2013. A survey on multi-view learning. arXiv preprint arXiv:1304.5634 (2013).

- Zhang et al. [2014] Yuchen Zhang, Xi Chen, Denny Zhou, and Michael I Jordan. 2014. Spectral methods meet EM: A provably optimal algorithm for crowdsourcing. In Advances in neural information processing systems. 1260–1268.

- Zhou et al. [2012] Denny Zhou, Sumit Basu, Yi Mao, and John C Platt. 2012. Learning from the wisdom of crowds by minimax entropy. In Advances in neural information processing systems. 2195–2203.

Appendix A Additional proof(s)

Claim 2.8.

When random variables , are independent conditioning on ,

Proof.

| (Conditional independence) | ||||

| (PMI=posterior/prior) | ||||

∎

Theorem 5.2.

Given the prior distribution over the , with the conditional independence assumption, with a priori similar and random order assumption, when and the prior is stable and well-defined, when the convex function is differentiable and is invertible, is focal.

When both Alice and Bob are honest, each of them’s expected payment in is

Proof.

Given that Alice’s strategy is and Bob’s strategy is , with the a priori similar and random order assumption, we represent agents’ report as the output (possibly being random) of their strategy operating on the private information.

We start to show is strictly truthful. Given that Alice is honest, based on Lemma 5.3, Bob will maximize his expected payment if and only if ,

Note that in ,

Since the prior is stable, the above equation is satisfied for all possible if and only if Bob tells the truth, i.e., reporting . Therefore, is strictly truthful.

It remains to show pays truth-telling the most and strictly better than any other non-permutation strategy profile. When agents maximize the expected payment,

Recall that we defined

Thus, when is invertible, we have

for any . This is exactly system (1).

With the conditional independence assumption, when agents tell the truth, the above system will be satisfied. Therefore, agents can maximize their expected payment via truth-telling. The non-negativity of implies that agents are willing to participate in the mechanism.

Moreover, when the prior is well-defined, if the prior is a uniform distribution, then any permutation strategy profile can solve the above system and as well as maximize agents’ expected payment. Even if the prior is not a uniform distribution, although not all permutation strategy profiles solve the above system, still any solution of the above system must correspond to a permutation strategy profile, given the prior is well-defined. Therefore, when agents maximize their expected payment, their strategy profile must be a permutation strategy profile or truth-telling, which implies is focal.

∎

Lemma 5.3.

With the conditional independence assumption, the expected total payment is maximized over Alice and Bob’s strategies if and only if , for any ,

The maximum is

Proof.

Without loss of generality, it is sufficient to analyze Alice’s strategy and report. With the a priori similar and random order assumption, can be represented as since the index of the task is meaningless to Alice when all tasks appear in a random order, independently drawn for each agent. The strategy can be seen as a random predictor. Thus, we can use the same proof of Lemma 4.1 to prove Lemma 5.3. ∎