Optimality Conditions in Variational Form for Non-Linear Constrained Stochastic Control Problems

Abstract

Optimality conditions in the form of a variational inequality are proved for a class of constrained optimal control problems of stochastic differential equations. The cost function and the inequality constraints are functions of the probability distribution of the state variable at the final time. The analysis uses in an essential manner a convexity property of the set of reachable probability distributions. An augmented Lagrangian method based on the obtained optimality conditions is proposed and analyzed for solving iteratively the problem. At each iteration of the method, a standard stochastic optimal control problem is solved by dynamic programming. Two academical examples are investigated.

Keywords:

stochastic optimal control, optimality conditions, augmented Lagrangian method, mean-field-type control, relaxation.

AMS classification:

90C15, 93E20, 49J53, 49K99.

1 Introduction

This article is devoted to the derivation of optimality conditions for a class of control problems of stochastic differential equations (SDE). For a given adapted control process , let be the solution to the following SDE:

where the drift , the volatility , and the initial condition are given. For all , we denote by the probability distribution of . Along the article, constrained problems of the following form are considered:

| (1) |

where the mappings and are given and satisfy differentiability assumptions. The set is a set of adapted stochastic processes. A precise description of problem (1) will be given in Section 2. In this paper, we call the mappings and linear if they can be written in the form and , where and . In this specific case, problem (1) is equivalent to the following stochastic optimal control problem with an expectation constraint:

| (2) |

The terminology non-linear used in the title refers to the fact that the functions and for which our result applies are not necessarily linear. In other words, the cost function and the constraints are not necessarily formulated as expectations of functions of . This is the specificity of the present article.

Stochastic optimal control problems with a non-linear cost function are mainly motivated by applications in economy and finance. In many situations, minimizing the expectation of a random cost may be unsatisfactory and one may prefer to take into account the “risk” induced by the dispersion of the cost. In the literature, there exist many different models of risk and some of them can be formulated as functions of the probability distribution of the state variable, as explained for example in [31, Chapter 6]. Some portfolio problems with risk-averse cost functions are studied in [26]. In [3, Section 5], a mean-variance portfolio selection problem is considered as well as in [22]. In [19], a gradient-based method is developed for minimization problems of the conditional value at risk, a popular risk-averse cost function. The risk can also be taken into account by considering a constraint of the form . For example, one can try to keep the probability of bankruptcy under a given threshold with a probability constraint. If models the variance of the outcome of some industrial process, then a constraint on the variance can guarantee some uniformity in the outcome, which can be a desirable property. Final-time constraints have several applications in finance, see for example [33], where probability constraints are used for solving a super-replication problem or [32], where the final probability distribution is fixed for solving a determination problem of no-arbitrage bounds of exotic options. Finally, let us mention that a problem of the form (1) can be seen as a simple model for an optimization problem of a multi-agent system, where a government, that is to say a centralized controller, influences a (very large) population of agents, whose behavior is described by a SDE (see for example [2] and the references therein on this topic). Let us mention however that for general multi-agent models, the coefficients of the SDE at time depend on the current probability distribution .

Let us describe the available results in the literature related to optimality conditions for problems similar to Problem (3). Problem (3), without constraints, is a specific case of an optimal control problem of a McKean-Vlasov process (or mean-field-type control problem). For this more general class of problems, the drift and volatility of the SDE possibly depend at any time on the current distribution . Optimality conditions usually take the form of a stochastic maximum principle: for a solution , minimizes almost surely and for almost every time a Hamiltonian involving a costate which is obtained as a solution to a backward stochastic differential equation (see for example [3], [4], [9], [13]). In a different but related approach, one can consider control processes in a feedback form, that is to say in the form , where the mapping has to be optimized. Under regularity assumptions, the probability distribution has a density, say , which is the solution to the Fokker-Planck equation:

where and where the operators and are defined by

respectively. A derivation of the Fokker-Planck can be found in [12, Lemma 3.3], for example. Note that if and do not depend on , then the Fokker-Planck equation is a linear partial differential equation. In this approach, the problem is an optimal control problem of the Fokker-Planck equation and optimality conditions take the form of a Pontryagin’s maximum principle. The adjoint equation is in this setting an HJB equation. We refer the reader to [1], [2], [4], and [15] for this approach.

In this article, optimal control problems of the following form:

| (3) |

are called standard problems, considering the fact that they have been extensively studied in the last decades. They can be solved by dynamic programming, by computing the solution to the associated Hamilton-Jacobi-Bellman equation (see the textbooks [16], [28], [35] on this field). Since standard problems are of form (2) (without constraints), they fall into the general class of problems investigated in the paper. The optimality conditions provided in the present article can be shortly formulated as follows: if is a solution to (1) and satisfies a qualification condition, then it is also the solution to a standard problem of the form (3), where the involved function is the derivative at (in a specific sense) of the Lagrangian of the problem , for some non-negative Lagrange multiplier satisfying a complementarity condition. Our optimality conditions therefore take the form of a variational inequality. Our analysis relies on the following technical result: the closure (for the Wasserstein distance associated with the -distance) of the set of reachable probability distributions at time is convex. This property is proved by constructing controls imitating the behaviour of relaxed controls. To the best of our knowledge, the optimality conditions for problem () are new, as well as the convexity property satisfied by the reachable set222A proof of the convexity property as well as optimality conditions in variational form for unconstrained problems can be found in the unpublished research report [24].. They differ from the maximum principle mentioned above and are, to a certain extent, related to the optimality conditions obtained for mean-field-type control problems formulated with feedback laws. The presence of non-linear constraints is another novelty of the article; in the literature, most constraints of the form are expectation constraints, see for example [8], [27]. The existence of a Lagrange multiplier, even in a linear setting, is not often considered, see [7, Section 5] or [23, Section 6].

It is well-known that problems of the form (1) are time-inconsistent, i.e. it is (in general) not possible to write a dynamic programming principle by parameterizing problem (1) by its initial time and initial condition, as is customary for standard problems of the form (3). A dynamic programming principle can be written if one considers the whole initial probability distribution as a state variable, see [18], [29], [30]. However, in practice, this approach does not allow, in general, to solve the problem, because the complexity of the method grows exponentially with the dimension of the (discretized) space of probability distributions. The optimality conditions in variational form and the convexity property proved in this article naturally lead to iterative methods for solving problem (1), based on successive resolutions of standard problems and thus overcoming the difficulty related to time-inconsistency. We propose, analyse, and test such a method in the article. The cost function of the standard problem to be solved at each iteration is the derivative, in a certain sense, of an augmented Lagrangian.

We give a precise formulation of the problem under study in Section 2. We also discuss the notion of differentiability which is used. In Section 3, we prove the convexity of the closure of the reachable set of probability distributions. Optimality conditions in variational form are proved in Section 4. The case of convex problems is discussed. Our numerical method for solving the problem is described and analyzed in Section 5. We provide results for two academical examples. Elements on optimal transportation theory are given in the appendix.

2 Formulation of the problem and assumptions

2.1 Notation

-

The set of probability measures on is denoted by . For a function , its integral (if well-defined) with respect to the measure is denoted by

Given two measures and , we denote:

-

For a given random variable with values in , its probability distribution is denoted by . If , then for any continuous and bounded function ,

We also denote by the -algebra generated by .

-

For a given vector , we denote by its Euclidean norm and by its supremum norm.

-

For , we denote by the set of probability measures having a finite -th moment:

We recall that for , the space is included into . We equip with the Wasserstein distance (the definition is given in the appendix). We recall the dual representation of [34, Remark 6.5]: for all , ,

(4) where is the set of real-valued Lipschitz continuous functions of modulus 1.

-

For all , we define

(5) -

The open (resp. closed) ball in of radius and center is denoted by (resp. ), its complement (resp. ), for the Euclidean norm.

-

For a given , we say that a function is dominated by if for all , there exists such that for all ,

(6) -

The convex envelope of a set is denoted . When is a subset of , its closure for the -distance is denoted .

2.2 State equation

We fix a final time and a Brownian motion of dimension . For all , is a standard Brownian motion. For all , we denote by the -algebra generated by .

Let be a compact subset of . Note that we do not make any other assumption on : it can be non-convex, for example, or can be a discrete set. For a given random variable independent of with values in , we define the sets and as the sets of control processes taking values in such that for all , is respectively -measurable and -measurable, respectively.

The drift and the volatility are given. For all , we denote by the solution to the SDE

| (7) |

The well-posedness of this SDE is ensured by Assumption 1 [21, Section 5] below. We also denote by the probability distribution of :

All along the article, we assume that the following assumption holds true. From now on, the initial condition and the real number introduced below are fixed.

Assumption 1.

There exists such that for all , for all ,

There exists such that .

The following lemma is classical, see for example [17, Section 2.5].

Lemma 2.

There exist three constants , , and depending on , , , and such that for all , for all random variables and independent of and taking values in , for all , for all , for all , the following estimates hold:

-

1.

-

2.

-

3.

.

We denote by the set of reachable probability distributions at time , defined by

| (8) |

By Lemma 2, there exists such that

| (9) |

By Lemma 25 (in the appendix), is compact for the -distance, thus it is bounded. It follows that and are bounded. We can therefore consider, for future reference, the diameter of , defined by

| (10) |

2.3 Formulation of the problem and regularity assumptions

Let and be two given mappings. We aim at studying the following problem:

| () |

Throughout the article, we assume that the next two assumptions, dealing with the continuity and the differentiability of and , are satisfied. The constant used in these assumptions is given by (9).

Assumption 3.

The restrictions of and to are continuous for the -distance.

In order to state optimality conditions, we need a notion of derivative for the mappings and . Denoting by the set of finite signed measures on , we define:

Let be a linear mapping. We say that the function is a representative of if for all , the integral is well-defined and equal to :

If is a representative of , then for any constant , is also a representative of , since

Conversely, if the value of a representative is fixed for a given point , then for all , the value of is determined by

where and are the Dirac measures centered at and , respectively. Therefore, the representative, if it exists, is uniquely defined up to a constant.

Assumption 4.

-

1.

For all , , and , there exists a linear form such that for all , there exist and in such that for all and for all ,

where

Moreover, possesses a continuous representative, dominated by , and denoted .

-

2.

For all , , and there exists a linear mapping such that for all , there exists and in such that for all and and for all and ,

(11) where

Moreover, possesses a continuous representative, dominated by , and denoted .

In the article, we make use of the derivative (a linear form from to ) and its representative. The two notions can be distinguished according to the presence (or not) of the variable . Note also that the differentiability assumption on is a strict differentiability assumption. It is a little bit stronger than the assumption on .

2.4 Discussion of the notion of derivative

A general class of cost functions satisfying Assumptions 3 and 4 can be described as follows. Let , let be differentiable, let be a continuous function dominated by . We define then on :

| (12) |

Note that for all control processes ,

For all , the continuity of on follows from Lemma 26 (in the appendix). One can easily check that the mapping is differentiable in the sense of Assumption 4.1. The representative of its derivative is given by

| (13) |

up to a constant. Furthermore, if is continuously differentiable, then is differentiable in the sense of Assumption 4. Note that the function does not need to be differentiable. Further examples are discussed in detail in [25, Section 4]. We finish this subsection with two remarks.

Remark 5.

The fact that should be defined on the whole space discards cost functions whose formulation is based on the density of the probability measure (since a density does not always exists, for probability distributions in ). For example, the following problem does not fit to the proposed framework:

where PDF stands for probability density function and where is a given probability density function.

Remark 6.

The notion of derivative provided in [12, Section 6] and the one introduced in Assumption 4 are of different nature, because they aim at evaluating the variation of functions from to on different kinds of paths. While our derivative is represented by a function from to , the one of [12] is represented by a function from to (see [12, Theorem 6.5]). This difference of nature can be better understood by considering the mapping: . This mapping is a monomial, according to the terminology given in [12, Example, page 43]. Its derivative (in the sense of [12]) is represented by the mapping: (see [12, Example, page 44]). In the current framework, the derivative of is the real-valued mapping , up to a constant.

2.5 Existence of a solution

Observe that problem () can be equivalently formulated as follows:

| () |

where is defined by (8). Indeed, if is a solution to (), then is a solution to () and conversely, if is a solution to (), then any such that is a solution to (). The feasible set of Problem () is defined by

| (14) |

By continuity of for the -distance, the value of the following problem:

| () |

is the same as the one of problems () and (). Indeed, problem () is simply obtained by replacing the feasible set of () by its closure (for the -distance).

Lemma 2 enables us to prove the existence of a solution to problem ().

Proof.

3 Convexity of the reachable set

This section is dedicated to the proof of the convexity of the closure of (the set of reachable probability distributions at time ). This result is an important tool for the proof of the optimality conditions in Section 4 and for the numerical method developed in Section 5. Let us explain the underlying purpose with a simple example. Consider two processes and and the corresponding final probability distributions and . We aim at building a control process such that

| (15) |

A very simple way of building such a control process is to define a random variable independent of and taking two different values with probability . A control realizing (15) can then be constructed in : it suffices that for one value of and that for the other. The obtained controlled process can be seen as a relaxed control, since it is now measurable with respect to a larger filtration. The main idea of Lemma 8 is to construct control processes in imitating the behaviour of the relaxed control process .

Lemma 8.

The closure of the set of reachable probability measures for the -distance, denoted , is convex.

Proof.

Our approach mainly consists in proving that

| (16) |

Let , let in , let in with . To prove (16), it suffices to prove that there exists a sequence in such that

| (17) |

Let , let be processes in such that for all , the processes and can be seen as the same measurable function of respectively

In other words, we simply delay the observation of the variation of the Brownian motion of a time . Let be such that for all ,

and let us denote by the following event:

where is the first coordinate of the Brownian motion. For all , we have . Fixing , we define as follows:

For all ,

| (18) |

where and are given by

Let us first estimate . Using the Lipschitz-continuity of , we obtain that

We deduce from the Cauchy-Schwarz inequality and Lemma 2 that

| (19) |

Let us estimate . Since and are independent of and using the definition of , we obtain that

Therefore,

We obtain with the Lipschitz-continuity of , the Cauchy-Schwarz inequality, and Lemma 2 that

| (20) |

Combining (18), (19), and (20), we obtain that

where is a constant independent of and . Using the dual representation of (given by (4)), we deduce that

This proves (17) and thus justifies (16). We can now conclude the proof. It follows from (16) that

| (21) |

Since , we have , and therefore by (21), . It remains to prove that is convex, which is an easy task. ∎

4 Optimality conditions

We prove in this section the main result: if a control is a solution to () and satisfies a qualification condition, then it is the solution to a standard problem of the form (3). Before proving our result, we recall in Subsection 4.1 some well-known properties of the value function associated with a standard problem.

4.1 Standard problems

Let be a continuous function dominated by . Let us define:

The mapping is linear, in so far as for all and , for all ,

It is also continuous for the -distance, see Lemma 26 (in the appendix). We denote by () the following standard problem:

| () |

Let and let . By continuity of , the control process is a solution to () if and only if

We recall, for future reference, some well-known results concerning the value function associated with the standard problem (). We refer to the textbooks [16], [28], [35] on this topic. The value function associated with () is defined for all and for all by

It can be characterized as the unique viscosity solution to the following Hamilton-Jacobi-Bellman (HJB) equation:

| (22) |

where the Hamiltonian is defined for , , , and by

If is sufficiently smooth, one can prove with a verification argument that any control process is a global solution to () if almost surely,

Finally, note that the value of problem () is given by

where .

4.2 Main result

In this subsection, we give first-order optimality conditions in variational form for problem () (defined in the introduction, page ). Along this subsection, a solution to problem () is fixed. We also set

We first give a metric regularity result (Theorem 10), which is a key tool for the proof of the optimality conditions (Theorem 11).

Let us consider the sets and of active and inactive constraints at , defined by

Let be the cardinality of . We define

We have

The following assumption is a qualification condition.

Assumption 9.

There exists such that .

For all , we denote by the vector defined by for . One can easily check that for all and ,

| (23) |

Theorem 10.

The estimate (24) is basically an estimate of the distance of to . Indeed, by the convexity of , the probability measure lies in . Since is continuous and since , the probability measure lies in . It is at a distance of . The real number is of same order as the quantity , which indicates how much the constraints are violated.

Proof of Theorem 10.

For all , we define

By Assumption 9, . Let be such that

| (25) |

where . The above inequality (as well as all those involving vectors) must be understood coordinatewise.

Claim 1. There exist and such that for all and for all ,

| (26) |

Let us prove this claim. Let , let and in be such that (11) holds. We set and . We reduce the value of , if necessary, so that

| (27) |

For all and for all , we have

| (28) |

therefore, combining (11) and (28),

| (29) |

Moreover, by (27),

| (30) |

Combining (29) and (30), we obtain that

It follows that

Combining the above inequality with (25), we obtain (26). The claim is proved.

Now, let and be sufficiently small, so that for all and for all ,

Let us set

| (31) |

Recall that . Once again, we reduce the value of , if necessary, so that and so that for all ,

| (32) |

Claim 2. There exists such that for all with , for all , there exists such that

Let us prove the claim. We set . For a given and for a given such that , we set . Then, to prove the claim, we just have to check that and that . Using (31), (32), and the definition of , we obtain that

Therefore, . Using the first claim, we obtain that

| (33) |

It directly follows from the definitions of and that

Combined with (33), we obtain that

and finally that , by (23). This proves the second claim.

Conclusion. We can finally prove the theorem. Let and let . We set

Since , there exists such that and such that , by the second claim. By (23),

| (34) |

Since and , we obtain that

The estimate (24) is therefore satisfied. Since and , we deduce from (31) and from (34) that

| (35) |

Let us set . By construction, and thus, , since . Moreover, , since and . Therefore, . The theorem is proved. ∎

In the following theorem, we prove first-order optimality conditions in variational form for problem (). We make use of the Lagrangian , defined by

The Lagrangian is differentiable (with respect to ) in the sense of Assumption 4.1 with

A representative of is given by

up to a constant. Note that the mapping is continuous, by Lemma 26.

In the sequel, we say that a non-negative Lagrange multiplier satisfies the complementarity condition at if for all , .

Theorem 11.

Let be a solution to problem (). Let . If Assumption 9 holds, then there exists a non-negative Lagrange multiplier satisfying the complementarity condition at which is such that is a solution to the standard problem () with

Remark 12.

We say then that the control process satisfies the optimality conditions in variational form. The optimality of for the standard problem with is equivalent to the following variational inequalities:

and

| (36) |

In the sequel, we say that a probability measure such that satisfies the optimality conditions in variational form if there exists a multiplier satisfying the complementarity condition and such that (36) holds.

Proof of Theorem 11.

In view of the complementarity condition, it suffices to prove the existence of such that and such that

where . For all ,

For all , we consider the following optimization problem, denoted ():

| () |

Step 1. We first prove that . For , is feasible (for problem () with ), thus . Now, let be such that . Let and be given by Theorem 10. Let be a convergent sequence with limit 0 taking values in . For all , we set

By Assumption 4, we have

Since and , we have

By Theorem 10, there exists for all a real number such that

and such that , where

Thus,

| (37) |

Since is convex (Lemma 8), . Therefore, for all , by continuity of and , there exists such that and such that . Using the differentiability assumption on (Assumption 4), the feasibility of , the fact that and (37), we obtain that

It follows that and finally proves that .

Step 2. We compute now the Legendre-Fenchel transform (see [6, Relation 2.210] for a definition) of . For all , we have

Using the change of variable , we obtain:

Observing that

we deduce that

| (38) |

Step 3. Using the convexity of (Lemma 8), one can easily show that is a convex function. Let be such that (25) holds. Then, for any with ,

and therefore, problem is feasible and . It follows from [6, Proposition 2.018, Proposition 2.126] that is continuous in the neighbourhood of 0 and has a non-empty subdifferential at 0. Let , by [6, Relation 2.232], we have

Thus, by (38), and

The theorem is proved. ∎

The approach which has been employed to prove Theorem 11 is similar to the one based on relaxation with Young measures for deterministic non-linear optimal control problems. This approach is explained in [5, Section 3] for example, where Pontryagin’s principle is directly deduced from the convexity of the set of reachable linearised states.

The following lemma shows that the value of the standard problem can be used to estimate the loss of optimality of a given probability measure in (defined by (14)), when the mappings , ,…, are convex. We say that is convex if for all , for all and ,

| (39) |

The same definition is used for ,…,. Note that if is convex, then for all and ,

Lemma 13.

Proof.

Let . Since is convex, we have

| (41) |

Denoting by the active set at and setting

we obtain, using the feasibility of and the convexity of ,…, that

Since , we deduce that

| (42) |

By the complementarity condition,

| (43) |

Adding (41), (42), and (43) together, we obtain that

Minimizing successively both sides with respect to , we obtain that

Since , we finally obtain that

which concludes the proof. ∎

As a corollary, we obtain that the optimality conditions in variational form are sufficient optimality conditions, in the convex case.

Corollary 14.

Proof.

In this situation, the right-hand side of inequality (40) is equal to 0, which directly proves the optimality of . ∎

We finish this section with a corollary dealing with stochastic optimal control problems with an expectation constraint.

Corollary 15.

Proof.

Setting and , we obtain that problem (44) falls into the general class of problems studied in the article. The functions and satisfy the required regularity assumptions (see Subsection 2.4). Note that and that (up to a constant). The existence of ensures that the qualification condition is satisfied. The mappings and are clearly convex, therefore, the optimality conditions in variational form are necessary and sufficient, by Theorem 11 and Corollary 14. ∎

5 Numerical method and results

5.1 Augmented Lagrangian Method

We provide in this section a numerical method for solving problem () and give results for two academical problems. The method is an augmented Lagrangian method combined with a projected-gradient-type algorithm.

Let us begin with a rough description of the method, consisting of Algorithms 1 and 2 (page 1). The second algorithm is a building block of the first one. The augmented Lagrangian method is used to solve the following problem:

| (45) |

At the end of the while loop of Algorithm 1 (line 19), the method provides a probability measure satisfying approximately the optimality conditions in variational form for some Lagrange multiplier . At this stage, the method has not computed a control process such that . The ultimate step of the algorithm (line 20) aims at recovering such a control by solving the standard problem () with . One has to check a posteriori that approximately satisfies the optimality conditions in variational form with associated Lagrange multiplier .

Let us go into the details of the method. The augmented Lagrangian associated with (45) is given by

The employed norm in the above definition is the Euclidean norm. Note that the constraints and are not dualized, since they will be ensured by the projected gradient method. The mapping is differentiable (in the sense of Assumption 4.1) with respect to , with

A representative of is therefore given by

| (46) |

up to a constant. The partial gradient of with respect to is given by

Let us first focus on Algorithm 2. It aims at solving the following problem:

| (47) |

for values of the Lagrange multiplier and the penalty parameter given as input variables. The algorithm constructs a sequence of probability distributions in and a sequence of non-negative slack variables in the while loop. At each iteration of the while loop, a kind of line-search (line 10) is performed: the mapping is minimized over the set

| (48) |

where

and where . The operator in the above expression must be understood coordinatewise, it is nothing but a projection of on . The probability distribution is chosen as a solution to

The value of the above problem is non-positive. The measure can therefore be seen as a descent direction for the variable . The next iterate of the algorithm is given by

where minimizes over . Note that Lemma 8 plays here a crucial role: it guarantees that . Let us note that Algorithm 2 is not, strictly speaking, a projected gradient method, since is not obtained as a projection on .

Let us discuss the criterion used in Algorithm 2. It is related to the optimality conditions associated with problem (47): if is a solution to (47), then, by Theorem 11,

| (49) |

moreover, the optimality of implies that

| (50) |

Algorithm 2 stops when the variable (defined line 6 in the algorithm) is smaller than , i.e. when both

| (51) | ||||

| (52) |

The inequality (51) ensures that the optimality condition (49) is approximately satisfied (note that the left-hand side of (51) is always non-negative). The inequality (52) implies that

thus that

and finally that

| (53) |

Moreover, for all , if , then (by (52)) and therefore,

and finally,

| (54) |

Inequalities (53) and (54) therefore ensure that the optimality condition (50) is approximately satisfied.

Let us come back to Algorithm 1. It constructs a sequence of probability distributions in , a sequence of non-negative slack variables and a sequence of Lagrange multipliers . Two sequences of tolerances are also constructed, and , as well as a sequence of penalty parameters . At the iteration , the augmented Lagrangian is minimized by using Algorithm 2 with and the current tolerance . The triplet is the output of Algorithm 2. Three cases are then considered.

-

If , then we consider that the penalty term is large enough. The Lagrange multiplier is updated as follows:

This update rule is motivated by (46).

- –

-

–

Otherwise, the penalty term is unchanged and the tolerances and are tightened (line 12).

-

If , then the penalty term is regarded as too weak, it is therefore increased. The estimate of the Lagrange multiplier is unchanged and the tolerances are re-initialized (line 16).

Remark 16.

In practice, the main difficulty in the method is the resolution of the standard problem. It consists of two phases: in a backward phase, the Hamilton-Jacobi-Bellman equation associated with the standard problem must be solved (see subsection 4.1). It provides an optimal control (for the standard problem) in a feedback form. One must then compute the probability distribution which is associated, in a forward phase.

Remark 17.

5.2 Convergence analysis

We investigate in this subsection the termination of Algorithms 1 and 2. Our analysis follows the main lines of [20, Chapters 3 and 17]. Let us mention that we do not tackle in this subsection the issues related to discretization. In general, termination proofs for line-search methods require that the function to be minimized is differentiable with a Lipschitz-continuous gradient. A similar assumption is therefore considered below.

Assumption 18.

The mappings and are differentiable in the sense of Assumption 4. Moreover, there exist two constants and such that for all , , , and ,

| (55) |

and such that

Remark 19.

Before starting the convergence analysis, we give an example of a mapping satisfying Assumption 18.

Lemma 20.

If and are of the form where is differentiable with a Lipschitz continuous derivative on bounded sets, and where is globally Lipschitz continuous, then Assumption 18 holds.

Proof.

Recall the expression of the derivative, given in this situation by (13). Let be the Lipschitz modulus of . For , by Hölder’s inequality,

Let be the Lipschitz modulus of on the ball of centre 0 and radius . Let be a bound of on the same ball. Using the dual representation of the Wasserstein distance , we obtain that

since is Lipschitz continuous with modulus . Similarly, we also obtain that

since

Thus, Assumption 18 holds with and . ∎

The following lemma provides some useful properties dealing with the Lipschitz-continuity of the derivatives of the augmented Lagrangian.

Lemma 21.

Under Assumption 18, for all , for all , for all bounded sets , there exist three constants , and such that for all and , for all and ,

Proof.

It is clear that is bounded, since is Lipschitz continuous and since and are bounded. The first inequality follows.

We obtain with the Lipschitz-continuity of that

which proves the second inequality.

For proving the third inequality, we focus on the Lipschitz continuity of the mapping (the other terms involved in can be easily treated). Let and be such that for all , for all , and . We have

The third inequality follows. ∎

Proof.

We do a proof by contradiction and therefore assume that the algorithm never terminates. Therefore, it generates a sequence which is such that , for all . One can easily prove that the following set is bounded:

since is bounded on and since for a fixed , is linear-quadratic, with a dominant term independent of . In a similar way, one can prove that is bounded from below. By construction, the sequence is decreasing, therefore, for all , . Let , , and be the three constants given by Lemma 21, for the set .

The proof mainly consists in finding an upper estimate of the decay

at a given iteration . This is achieved with estimate (58) below. Let us introduce some notation, used only in this proof. For , we denote

We also omit the arguments and of the augmented Lagrangian (since they are fixed). Let . Observe first that by Lemma 24,

| (56) |

where is the diameter of (defined by (10)). Let us estimate . By Lemma 21, . Since and since the mapping is Lipschitz-continuous with modulus 1 (it is a projection), we have

| (57) |

Now, we split the decay into two terms as follows:

We split the first term as follows:

Combining Lemma 21 with estimates (56) and (57), we obtain that

Since is the orthogonal projection of on and since , we have

Using , we deduce that

It is proved in [10, Lemma 2.2] that

Combining the last two estimates, we obtain that

Let us estimate . We have

For all , we denote

Combining the three obtained upper estimates of , , and , we obtain that there exists a constant , independent of , such that for all ,

| (58) |

For all , we define

If , then

Otherwise, and . Therefore

Therefore, for all ,

and thus

Recall that the sequence is bounded from below. Let be a lower bound. We deduce from the above estimate that for all ,

The sequence is therefore summable and thus converges to 0. It follows that converges to 0. Since is the sum of two non-negative terms, they both converge to 0, i.e.

It follows that , which is a contradiction. ∎

Proposition 23.

Observe that the two conditions satisfied by are the optimality conditions for the problem

Proof of Proposition 23.

Let us assume that the algorithm does not terminate. Let us first prove that there are infinitely many indices such that . Suppose that it is not the case, then there exists such that for all , . Considering the update formulas for and used in this situation (line 12), we obtain that and and thus for some sufficiently large, and . The algorithm necessarily terminates when these two inequalities hold, which is a contradiction.

When , is unchanged and when (which occurs infinitely many times), . Therefore, . We also have that for all , . It is easy to prove by induction that for all , and that . Therefore, and . For large enough, say for , and . Therefore, for , (otherwise, the algorithm would terminate). It follows that for , the Lagrange multiplier is not updated anymore: . We denote this constant value of the Lagrange multiplier by , for simplicity.

We now prove that the sequence is bounded. Let . The following inequalities hold true:

| (61) | ||||

| (62) |

The value of the augmented Lagrangian is decreasing along the iterations of Algorithm 2. Moreover, the pair is obtained as an output of Algorithm 2, with initial value . Therefore,

Using (61) and denoting , we obtain that

Dividing by and adding on both sides and factorizing, we obtain that

Using the inequality , we obtain

and finally, by induction, for all ,

| (63) |

Since the sequence is a geometric sequence of ratio 10, the sequences and are also geometric with ratios 1/10 and 1/, respectively. These last two sequences are therefore summable and we deduce from (63) that is bounded. Since is bounded, we finally obtain that is bounded.

Since is compact and bounded, the sequence possesses at least one accumulation point. Let be an accumulation point. To simplify, we assume that the whole sequence converges to . The arguments which follow can be easily adapted if only a subsequence converge to . Let . For all , we have

Dividing by and passing to the limit, we obtain that

Minimizing the left-hand side with respect to , we obtain (59). It remains to prove (60). For all , we have

| (64) |

Dividing by and passing to the limit, we obtain that

which proves that . Let be such that . For large enough, and therefore, as a consequence of (64),

meaning that

Dividing by and passing to the limit, we obtain that and therefore, we obtain that , since , which proves that (60) holds. ∎

5.3 Results

We present numerical results for two academical problems. The considered SDE is the following for the two of them:

| (65) |

One can only act on the drift, the volatility is constant and equal to 1. All standard problems are solved by dynamic programming. The corresponding HJB equation is discretized with a semi-Lagrangian scheme (see [11]), which consists in approximating the SDE by a controlled Markov chain, defined at times with and taking values in , with and using reflecting boundary conditions. At any mesh point, the minimization of the Hamiltonian is realized by enumeration, for a discretized set of controls with . As mentioned in Remark 16, the resolution of standard problems (as the one in Algorithm 2, line 4) is done in two phases. Once an optimal control has been found by dynamic programming, the corresponding probability distribution is obtained by solving the Chapman-Kolmogorov equation associated with the discretized Markov chain.

The minimization with respect to involved in the computation of a steplength (line 10, Algorithm 2) is done by enumeration. The considered discretized set is with . Note this step of the method is computationally inexpensive (at least for the considered test cases).

The Algorithm 1 is initialized with (the Dirac distribution centered at 0), , and .

Since the SDE (65) is linear with respect to , the Hamiltonian is itself linear with respect to and one can expect that optimal controls only take the boundary values and when the derivative (w.r.t. ) of the solution to the HJB equation is positive (resp. negative). The optimal controls obtained below indeed take these values for most of the mesh points. This is why we worked with a rather coarse discretization of .

Test case 1: bounded variance

For the first test case, we consider the following cost function and constraint:

| (66) |

where . Observe that : the cost function is the expectation of the final state. The mapping is the variance of . The cost function is linear and is of the form (12). The derivative of at any , obtained with (13), is a linear-quadratic function (with respect to ), given by

Convergence results are shown on Figure 1. The tolerances and are chosen equal, for values ranging from to . For each of these tolerances, the values of and are provided. The column “Var. Ineq.” contains the following value:

which somehow indicates to what extent the variational inequality is satisfied. The column shows the value of the penalty parameter at the last iteration. The last column shows the total number of standard problems which have to be solved.

It can be first observed that for tolerances below , the variational inequality is almost satisfied. The violation of the constraint is small and of the same order as the tolerances. The obtained Lagrange multipliers converge when the tolerance goes to 0. We also observe that the mechanism of Algorithm 1 avoids that the penalty term becomes very high, for small tolerances.

| Tolerance | Var. Ineq. | Iterations | |||

|---|---|---|---|---|---|

| 1e3 | e | e | 29 | ||

| 1e4 | e | e | 100 | 39 | |

| 1e5 | e | e | 1000 | 60 | |

| 1e6 | e | e | 1000 | 60 |

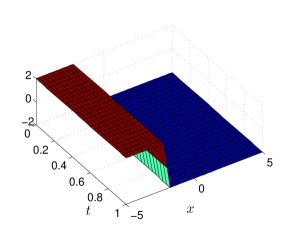

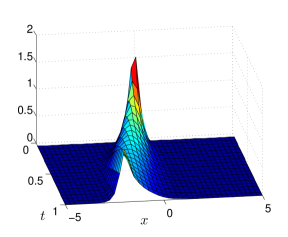

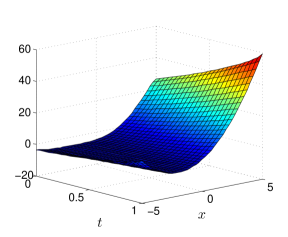

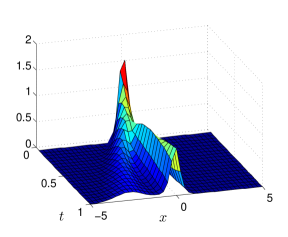

The optimal control generated by the algorithm is shown on Figure 2(a) (page 2(a)), the associated probability measure (at any time ) is shown on Figure 2(b). The value function associated with the standard problem with cost function is represented on Figure 2(c), we recall that it plays the role of an adjoint equation.

As expected, the optimal control has a kind of bang-bang structure. It is constant with respect to time, equal to for and to for . If the same problem was solved without constraint, the optimal control would be equal to , in order to minimize the expectation of the final state. Here, the optimal control must be equal to 2 when is smaller then in order to keep the variance sufficiently small and to satisfy the constraint.

Test case 2: expectation constraint

For this second test case, we consider the following cost function and constraint:

| (67) |

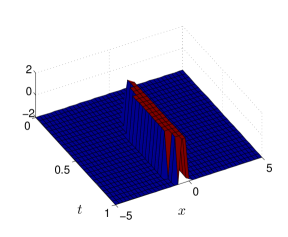

with . Note that both and are linear. Roughly speaking, the constraint ensures that a proportion of the final probability measure remains around 0.

Convergence results are given in Figure 3. The value of converges to 0, suggesting that the constraint is active for the undiscretized problem. Convergence of the Lagrange multiplier is observed. The variational inequality is exactly satisfied, since the derivatives of and do not depend on . The value of the penalty parameter does not increase much.

| Tolerance | Var. Ineq. | Iterations | |||

|---|---|---|---|---|---|

| 1e3 | e | ||||

| 1e4 | e | 0 | 100 | 53 | |

| 1e5 | e | 0 | 100 | 64 | |

| 1e6 | e | 0 | 100 | 64 |

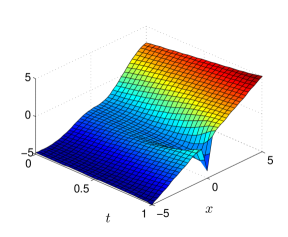

The optimal control, the probability distribution (at any time) and the adjoint are provided in Figures 2(d), 2(e), and 2(f) (page 2(a)). As can be observed, the optimal control only takes the boundary values. The value is taken in a small region around , after , which guarantees that a sufficiently large proportion of the distribution remains located around 0, as can be seen on the graph of the probability distribution.

6 Conclusion

We have proved optimality conditions for a class of constrained non-linear stochastic optimal control problems, using an appropriate concept of differentiability for the cost function and the constraints. The convexity of the closure of the reachable set of probability measures plays an essential role in the proof of these results. An augmented Lagrangian method, based on the convexity property and the optimality conditions has been proposed, demonstrating the relevance of these properties. Good convergence results have been obtained for examples with a one-dimensional state variable. Future work will focus on the extension of these results to more general problems, for example, for cost functions containing an integral cost depending on the current probability distribution.

Acknowledgements

This study was partly supported by the ERC advanced grant 668998 (OCLOC) under the EU’s H2020 research program.

Appendix A Elements on optimal transportation

Wasserstein distance

Let us recall the definition of the Wasserstein distance, denoted by in this article. For all and in ,

| (68) |

the set being the set of transportation mappings from to defined as:

Lemma 24.

For all and , for all ,

| (69) |

A compactness property

Lemma 25.

For all and , the subset of (defined in (5)) is compact for the -distance.

Proof.

We first prove that is compact for the weak topology of . For all and for all ,

| (70) |

and thus, , meaning that is tight. By Prokhorov’s theorem [34, Page 43], is therefore precompact for the weak-topology. Now, let be a sequence in weakly converging to . For all , the function is continuous and bounded, thus:

We obtain, using the monotone convergence theorem:

thus . Therefore, is weakly closed, and thus weakly compact.

A continuity property

We prove in the following lemma the continuity of linear mappings for the -distance on under a growth condition.

Lemma 26.

Let , be dominated by (in the sense of (6)). Then, for all , the following mapping: is continuous for the -distance.

Proof.

Let be a sequence in converging to for the -distance. Let and let be such that (6) holds. We define , where is the orthogonal projection on . For all , if , then and if , then . Thus, for all ,

By [34, Definition 6.8/Theorem 6.9], the convergence for the -distance implies the weak convergence, thus, since is continuous and bounded, we obtain:

The result follows when tends to 0. ∎

References

- [1] Y. Achdou and M. Laurière. On the system of partial differential equations arising in mean field type control. Discrete and Continuous Dynamical Systems, 35(9):3879–3900, 2015.

- [2] G. Albi, Y.-P. Choi, M. Fornasier, and D. Kalise. Mean field control hierarchy. Applied Mathematics & Optimization, 76(1):93–135, 2017.

- [3] D. Andersson and B. Djehiche. A maximum principle for SDEs of mean-field type. Applied Mathematics & Optimization, 63(3):341–356, 2011.

- [4] A. Bensoussan, J. Frehse, and P. Yam. Mean field games and mean field type control theory. Springer Briefs in Mathematics. Springer, New York, 2013.

- [5] J. F. Bonnans, L. Pfeiffer, and O. S. Serea. Sensitivity analysis for relaxed optimal control problems with final-state constraints. Nonlinear Anal., 89:55–80, 2013.

- [6] J. F. Bonnans and A. Shapiro. Perturbation analysis of optimization problems. Springer Series in Operations Research. Springer-Verlag, New York, 2000.

- [7] J. F. Bonnans and F. J. Silva. First and second order necessary conditions for stochastic optimal control problems. Applied Mathematics & Optimization, 65(3):403–439, Jun 2012.

- [8] B. Bouchard, R. Elie, and N. Touzi. Stochastic target problems with controlled loss. SIAM J. Control Optim., 48(5):3123–3150, 2009.

- [9] R. Buckdahn, B. Djehiche, and J. Li. A general stochastic maximum principle for SDEs of mean-field type. Appl. Math. Optim., 64(2):197–216, 2011.

- [10] P. H. Calamai and J. J. Moré. Projected gradient methods for linearly constrained problems. Mathematical Programming, 39(1):93–116, 1987.

- [11] F. Camilli and M. Falcone. An approximation scheme for the optimal control of diffusion processes. RAIRO Modél. Math. Anal. Numér., 29(1):97–122, 1995.

- [12] P. Cardaliaguet. Notes on Mean Field Games, 2012.

- [13] R. Carmona and F. Delarue. Forward-backward stochastic differential equations and controlled McKean-Vlasov dynamics. Ann. Probab., 43(5):2647–2700, 2015.

- [14] A. R. Conn, N. I. M. Gould, and Ph. L. Toint. LANCELOT, volume 17 of Springer Series in Computational Mathematics. Springer-Verlag, Berlin, 1992. A Fortran package for large-scale nonlinear optimization (release A).

- [15] A. Fleig and R. Guglielmi. Optimal control of the Fokker–Planck equation with space-dependent controls. Journal of Optimization Theory and Applications, 174(2):408–427, 2017.

- [16] W. H. Fleming and H. M. Soner. Controlled Markov processes and viscosity solutions, volume 25 of Stochastic Modelling and Applied Probability. Springer, second edition, 2006.

- [17] N. V. Krylov. Controlled diffusion processes, volume 14 of Applications of Mathematics. Springer-Verlag, New York-Berlin, 1980.

- [18] M. Laurière and O. Pironneau. Dynamic programming for mean-field type control. Journal of Optimization Theory and Applications, 169(3):902–924, 2016.

- [19] C. W. Miller and I. Yang. Optimal control of conditional value-at-risk in continuous time. SIAM J. Control Optim., 55(2):856–884, 2017.

- [20] J. Nocedal and S. J. Wright. Numerical optimization. Springer Series in Operations Research and Financial Engineering. Springer, New York, second edition, 2006.

- [21] B. Øksendal. Stochastic Differential Equations: An Introduction with Applications. Hochschultext / Universitext. Springer, 2003.

- [22] J. L. Pedersen and G. Peskir. Optimal mean-variance portfolio selection. Math. Financ. Econ., 11(2):137–160, 2017.

- [23] S. G. Peng. A general stochastic maximum principle for optimal control problems. SIAM J. Control Optim., 28(4):966–979, 1990.

- [24] L. Pfeiffer. Optimality conditions for mean-field type optimal control problems. SFB-report 2015-015, 2015.

- [25] L. Pfeiffer. Numerical methods for mean-field type optimal control problems. Pure and Applied Functional Analysis, 1(4):629–655, 2016.

- [26] L. Pfeiffer. Risk-averse Merton’s portfolio problem. IFAC-PapersOnLine, 49(8):266 – 271, 2016.

- [27] L. Pfeiffer. Two approaches to stochastic optimal control problems with a final time expectation constraint. Applied Mathematics & Optimization, To appear.

- [28] H. Pham. Continuous-time Stochastic Control and Optimization with Financial Applications, volume 61 of Stochastic Modelling and Applied Probability. Springer, 2009.

- [29] H. Pham and X. Wei. Dynamic programming for optimal control of stochastic McKean–Vlasov dynamics. SIAM Journal on Control and Optimization, 55(2):1069–1101, 2017.

- [30] H. Pham and X. Wei. Bellman equation and viscosity solutions for mean-field stochastic control problem. ESAIM-COCV, to appear.

- [31] A. Shapiro, D. Dentcheva, and A. Ruszczyński. Lectures on stochastic programming. MOS-SIAM Series on Optimization. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA; Mathematical Optimization Society, Philadelphia, PA, second edition, 2014.

- [32] X. Tan and N. Touzi. Optimal transportation under controlled stochastic dynamics. Ann. Probab., 41(5):3201–3240, 2013.

- [33] N. Touzi. Direct characterization of the value of super-replication under stochastic volatility and portfolio constraints. Stochastic Process. Appl., 88(2):305–328, 2000.

- [34] C. Villani. Optimal transport. Old and new, volume 338 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer, Berlin, 2009.

- [35] J. Yong and X. Y. Zhou. Stochastic controls: Hamiltonian systems and HJB equations, volume 43 of Applications of Mathematics (New York). Springer-Verlag, New York, 1999.